Abstract

Equity investment in agricultural cooperatives (co-ops) is typically limited to farmer-members; yet farmers are usually cash-constrained. In addition to the common stock that is held by farmer-members, many co-ops are changing their financial structure by raising equity from external investors. This helps co-ops to collect capital, but also brings to the fore the conflicting benefits of farmers and external investors. In this paper, we develop a two-stage game-theoretic model to examine a start-up co-op’s farm-gate pricing and financing strategies, considering two types of external fund: preferred stock that bears a fixed return rate and outside stock that shares the net profit (in proportion to equity) with common stock. We characterize the co-op’s strategies in different scenarios and generate the following insights. First, while both types of external equity outperform the case with common stock only, the preferred stock generally outperforms outside stock due to its lower financial cost, higher tolerance for fund size limits, and flexibility in setting farm-gate prices. However, outside stock can outperform preferred stock if it allows a higher fund size limit. Second, the co-op’s financial strategy exhibits a similar structure in equilibrium regardless of whether it is preferred stock or outside stock, despite their distinct financial terms. Finally, farm-gate pricing has a unique role in co-ops affecting the returns to farmers and external investors, which also highlights the conflicting roles of farmers as both patrons and investors when external equity is used.

Introduction

Sustainable agriculture is widely recognized as a key challenge for the world, where sustainability is broadly defined both in terms of land and resource use and also in the financial sense for the farmer (Glover, 2020). Agriculture is moving from being an exploitative and extractive industry to a more collaborative and sophisticated undertaking. This is particularly the case for agricultural marketing cooperatives (co-ops), where farmer-owners see financial and resource-use sustainability as critical to their long-term success. This requires the co-op to not only operate efficiently, but also to design effective financial strategies to ensure sufficient funds for its operations and development. However, this is not easily achieved due to the unique features of agricultural co-ops, especially for co-ops with smallholder farmers, who are often trapped in a vicious cycle of insufficient capital, low-intensity farming, low yields, and limited market access (Meemken and Bellemare, 2020).

As a member-owned organization, a co-op differs from other business structures and needs to follow user-owned, user-controlled, and user-benefit 1 principles. These member-focused principles of co-ops do not lend themselves to raising capital from non-member investors (Royerk and Karantininis, 2007). Thus, a co-op’s capital typically comes from its farmer-members, whose equity contribution is tied to the patronage 2 they provide. This causes shortages in funds when co-ops increasingly require more capital investment for sustainable development, such as novel marketing initiatives and processing technologies, especially when farmer members are small-scale and cash-constrained. As a result, many co-ops are looking to diverge from traditional financial structures (Chaddad and Cook, 2004) and seek external, non-member investment while still keeping the key principles of a co-op. For example, U.S. Premium Beef (USPB) restructured in 2004 by introducing external equity, allowing both beef producers and non-producer investors to own USPB units. Similarly, the Fonterra Co-operative Group restructured in 2009 to raise capital from outside investors by selling investment units (Qian and Olsen, 2021).

A co-op is like other businesses in some but not all aspects of its operations. As with a typical agricultural business, a co-op pool harvests from farmers and pays farmers at the farm gate. Furthermore, when selling processed products, a co-op faces an uncertain market. However, unlike other businesses, the relationship between the co-op and farmers is not simply that of customer and supplier. Since a co-op is owned and primarily financed by its farmer members, farmers bear the mixed roles of owners, patrons, and investors. The co-op therefore needs to work for the farmers’ interests, in both its operations and financing. As such, the farm-gate price a co-op pays to farmers is not simply a payment to suppliers, but can be used as a tool to adjust the profit distribution and thus the return to farmers and investors, which in turn influences their decisions regarding participation and investment. Therefore, the co-op’s operations, particularly the farm-gate pricing strategy in this case, are naturally intertwined with its strategy in terms of financing sources and capital structure, especially when external financing is involved. To aid the reader’s understanding, we explain co-op financing in the following subsection.

The Financing of a Co-op

Like other businesses, co-ops require capital to buy equipment and plant, pay staff, and cover other operating expenses. To start up a co-op business, the co-op can raise capital through both equity and debt. In this paper, we focus on equity financing because we are interested in how the emerging shift to non-member equity impacts farmers’ participation behavior and the co-op’s financial strategies. Considering both equity and debt financing is left for future research. Equity provides a key channel to raise capital to cover business costs. When co-ops diverge from traditional member-equity-only financing, more than one type of equity may be issued, to both members and non-members. Though they may appear in different forms, three types of equity are commonly observed in practice: (a) the common stock that farmers are required to purchase to join the co-op, which entitles them to membership and ownership rights; (b) preferred stock, which provides a fixed return to equity holders; and (c) outside stock, which entitles the equity holder to share the net profit (in proportion to equity) with common stock. However, for co-ops, any change in equity financing is often accompanied by a change in ownership structure, residual claim rights, and/or profit distribution. Next, we explain the specific features of each equity type.

Common Stock is tied to patronage, and individual farmers are generally expected to provide common stock in proportion to their patronage (the proportionality principle). Although some co-ops allow variations, most still subscribe to the proportionality principle. For example, each Class A unit in the USPB co-op requires each farmer to deliver one finished animal per year, and each share in Fonterra corresponds to one kilogram of milk solids.

Preferred Stock provides a way for co-ops to raise additional capital from investors while raising only modest concerns over their co-op status. The terms of preferred stock are flexible and dividend provisions vary. In this paper, we specifically consider a preferred stock that provides an expected fixed rate of return but does not confer control rights. For example, CHS co-op in the United States announced an offering of $50 million in preferred stock in 2001 with an 8% effective net annual yield. Furthermore, in 2003, Friesland Foods in the Netherlands issued subordinate notes with a total value of 125 million EUR, which generated a fixed interest of 7.125%. However, due to the limited liability of the co-op (Fee, 1984), the return on preferred stock is not guaranteed in the sense that investors can get a return lower than the committed rate if the co-op ends up with a low profit.

Outside Stock is another way for co-ops to acquire additional equity. The main distinction between preferred stock and outside stock lies in the rights to residual claim (van Bekkum and Bijman, 2006). Outside stock is on a par with, rather than senior to common stock for dividend payments. To provide financial incentives to outside investors, co-ops may switch to distributing net profit in proportion to equity. Therefore, outside stock will rarely have a fixed return rate, and the actual return on investment will depend on profitability. However, wary of turning into investor-owned firms (IOFs), many co-ops limit control rights to farmer-members when introducing outside stock. For example, Fonterra claims that it is still a 100% farmer-owned organization and outside investors only enjoy the economic rights of shareholders. Saskatchewan Wheat Pool (SWP), a Canadian grain marketing co-op, converted members’ equity stock to nonvoting stock (B shares) for outside investors (Chaddad and Cook, 2004). Therefore, although outside stock shares the benefits of common stock, it conveys no or very limited control rights. In this paper, we will focus on the case with no control rights.

In contrast to common stock that is tied to patronage and control rights, both preferred stock and outside stock bear no patronage obligation nor control rights and thus can be issued to any investors for additional capital investment. These are therefore referred to as “external” equity. Note that such external equity stock is also open to farmer-members: those who wish to contribute more than their compulsory common stock share may purchase preferred stock and outside stock; this allows them to earn interest or dividends, but with no additional voting privileges.

As farmer-owned organizations, co-ops are subject to some restrictions when raising capital from external funds. This is because issuing external equity is a diversion from the traditional user-owned, user-controlled, and user-benefit principles of co-ops. In response to this problem, many co-ops, in practice, take measures to control the size of external equity. For example, Fonterra specifies that the equity from external investors shall be no more than 12% of the total equity (Qian and Olsen, 2021). In some countries, co-ops also have to comply with federal and state securities law in connection with the external equity offering. For example, the Law of Agricultural Co-ops in China stipulates that non-farmer members should be no more than 20% of all farmer-members. 3

Research Questions and Contribution

We consider a co-op initiator planning to set up a co-op business with multiple farmers who are cash-constrained. To cover the capital needed, the co-op first raises member equity through common stock and then chooses to raise additional funds through preferred stock or outside stock, both of which are subject to certain fund size limits. In particular, we examine three scenarios for the capital structure, based on (a) pure common stock; (b) common stock and preferred stock; and (c) common stock and outside stock.

This paper seeks to answer the following questions. Considering different sources of funds for equity: (a) What are the equilibrium financial strategies in each scenario? (b) How is the farm-gate pricing linked to the co-op’s financial decisions? (c) Which type of funds should the co-op choose and under what conditions? To answer these questions, it is necessary to explore the interaction between the co-op’s financing and its operations, which are naturally intertwined. In particular, we study the financing decisions regarding the capital structure associated with each fund type, and the tactical decision on farm-gate pricing under an uncertain market. As discussed, co-ops need to follow certain key principles to maintain their co-operative status. These requirements and restrictions create a regulatory friction, which is identified as one primary category of capital market frictions (DeGennaro and Robotti, 2007).

In essence, co-ops are owned by and should be mainly invested in by farmer-members. Our model captures the essence and most salient features unique to agricultural co-ops that introduce regulatory market frictions. First, following co-op principles, the co-op typically aims to maximize the farmer-members’ profit. This is at odds with the objective of maximizing business value as expected by external investors and also provides an opportunity to manipulate the farm-gate price to adjust the profit distribution between farmers and investors. Second, co-ops usually limit the capital obtained from external funds. In the model, this is captured through fund-size constraints, where the external funds cannot exceed certain limits based on the size of common stock raised from farmer-members. This creates liquidity constraints; that is, co-ops’ financing activities are constrained by members’ equity, and thus co-ops are prevented from fully optimizing the capital from external funds.

We find that both preferred stock and outside stock, compared to the scenario with common stock only, contribute to the formation of a co-op and improve the total profit. This provides support for using external equity and is consistent with co-ops’ practice of seeking to issue external equity when possible in order to capture a higher value. Furthermore, the pooling effect, a key driver for co-op formation, enables the co-op to accommodate a higher proportion of external funds, though this positive effect is only present when the fixed cost is not too high.

Comparing the two types of external equity, we demonstrate that preferred stock is likely to (weakly) dominate outside stock in certain practical situations. This is consistent with financial theory (e.g., Houston and Houston, 1990), which emphasizes the lower financial costs of preferred stock. However, our research complements the theory by highlighting additional advantages of preferred stock in its higher flexibility for setting the farm-gate price and/or higher tolerance on the fund size limit, which are unique to co-ops. This provides corroboration for our observation that in practice many co-ops prefer to issue preferred stock when seeking external equity. Furthermore, it is important to note that outside stock could still become the favored option if it allows a larger size limit than preferred stock.

Despite the distinct features of preferred stock and outside stock, we find that the co-op’s equilibrium financial strategy exhibits a similar structure regardless of the type of external equity being raised. This similarity arises from the comparable financial requirements faced by the co-op when raising external equity. Specifically, the co-op utilizes preferred stock or outside stock solely to address capital shortfalls beyond common stock and makes the expected return to external investors at their anticipated premium rate so that external funds are fairly priced.

Furthermore, our results uncover the unique role of farm-gate pricing in co-ops and show that the co-op’s farm-gate pricing with preferred stock can exhibit greater flexibility compared to outside stock. This flexibility stems from the concurrent determination of the farm-gate price and the face value of preferred stock. Essentially, the co-op can offer a higher face value, incorporating a risk premium, to offset the influence if a higher farm-gate price increases the default risk. In contrast, the farm-gate price under outside stock is uniquely set in equilibrium as it directly determines the return to external investors. Meanwhile, the farm-gate price influences the co-op’s financial decisions only when external funds are involved, but not when equity is restricted to farmers. This arises from the conflicting interests of farmers and investors: while farmers as patrons prefer a higher farm-gate price, investors typically favor a lower farm-gate price. As such, our analysis sheds light on the conflicting roles of farmers as both patrons and investors when external equity is used.

The remainder of this paper is organized as follows. In Section 2, we review the relevant literature. Section 3 develops the model and Section 4 characterizes the equilibria in the three scenarios. In Section 5, we discuss managerial insights under our specific financing types, and Section 6 compares the performance of the three types of equity. Finally, Section 7 summarizes the results and discusses future research. Sensitivity analysis, numerical experiments, and the extension considering farmers’ opportunity cost and all proofs are available in the E-Companion.

Literature Review

Our work contributes to quantitative research analyzing both the financial and operational decisions of agricultural co-ops, as there is a general lack of such studies. Existing quantitative analysis of co-ops tends to focus on just one aspect, either financing or operations, and most of the relevant studies are qualitative or empirical (e.g., Rebelo et al., 2017; Russell et al., 2017). Among quantitative studies that limit their analysis to co-ops’ financial decisions, VanSickle and George (1983) present a theoretical model for co-op capital structure optimization, calculating the optimal cash patronage refund rate and the members’ after-tax total profit. In another example, Wang (2016) constructs a maximization model for a co-op adopting an equity management program of revolving funds, and derives the optimal decisions of the dividend rate, the cash patronage refund rate, and the length of the revolving fund cycle. There is also a rich set of quantitative studies on co-ops’ operational decisions, including with regard to co-op formation, contractual coordination, and quality management (e.g., An et al., 2015; Ayvaz-Çavdaroğlu et al., 2021; Bontems and Fulton, 2009; Mu et al., 2019; Qian and Olsen, 2022). However, in these studies, the financial aspect receives only minimal if any consideration.

Only a few studies consider both financing and operations in agricultural co-ops. Qian and Olsen (2020) examine the coordination of operational and financial decisions by co-ops. In their paper, the co-op limits its equity to farmers and does not allow investment from external investors. Removing this restriction, we study financing strategies that allow external investment through preferred stock and outside stock, as already adopted by many current co-ops. Similar capital structure innovations for co-ops have been modeled by Qian and Olsen (2021). Through a case study, they numerically demonstrated that a higher tolerance on the external fund size limit can enhance equity holders’ returns and that raising capital from outside investors could alleviate financial constraints. We find similar results using an analytical approach, and further derive the equilibrium decisions, providing additional insights such as the unique role of the farm-gate price in co-op financing. Moreover, we model two types of external equity and compare their performance, while Qian and Olsen (2021) considered only one type of external equity resembling the outside stock in our paper.

Our work also contributes to the growing literature on supply chain finance that connects operational and financial decisions (e.g., Alan and Gaur, 2018; Boyabatlı and Toktay, 2011; Kouvelis and Dong, 2023; Li et al., 2013). This research stream has derived a rich set of results on how a firm’s financial constraints affect its operational decisions. For example, in an agricultural setting, Yi et al. (2021) consider a supply chain with a capital-constrained smallholder farmer and an intermediary platform that can help solve the bottleneck of capital through debt financing and guarantor financing. However, no studies in this literature consider agricultural co-ops, which have unique operational and financial features.

Our work also relates to the literature on agricultural operations. Dong (2021) and Gupta et al. (2023) review agricultural research from the operations management perspective, and identify challenges and trends in agricultural supply chains. Studies have examined the incentives and interventions to adopt innovations in farm practices such as organic and sustainable farming (e.g., Akkaya et al., 2021; Acs et al., 2009), and the interaction of procurement, processing, and distribution decisions (e.g., Azoury and Miyaoka, 2013; Boyabatlı et al., 2011; Kazaz and Webster, 2011). While these studies mainly focus on agricultural operations, we also take financial decisions into consideration and look at how agricultural co-ops’ operations influence innovation in their financing.

Model Description

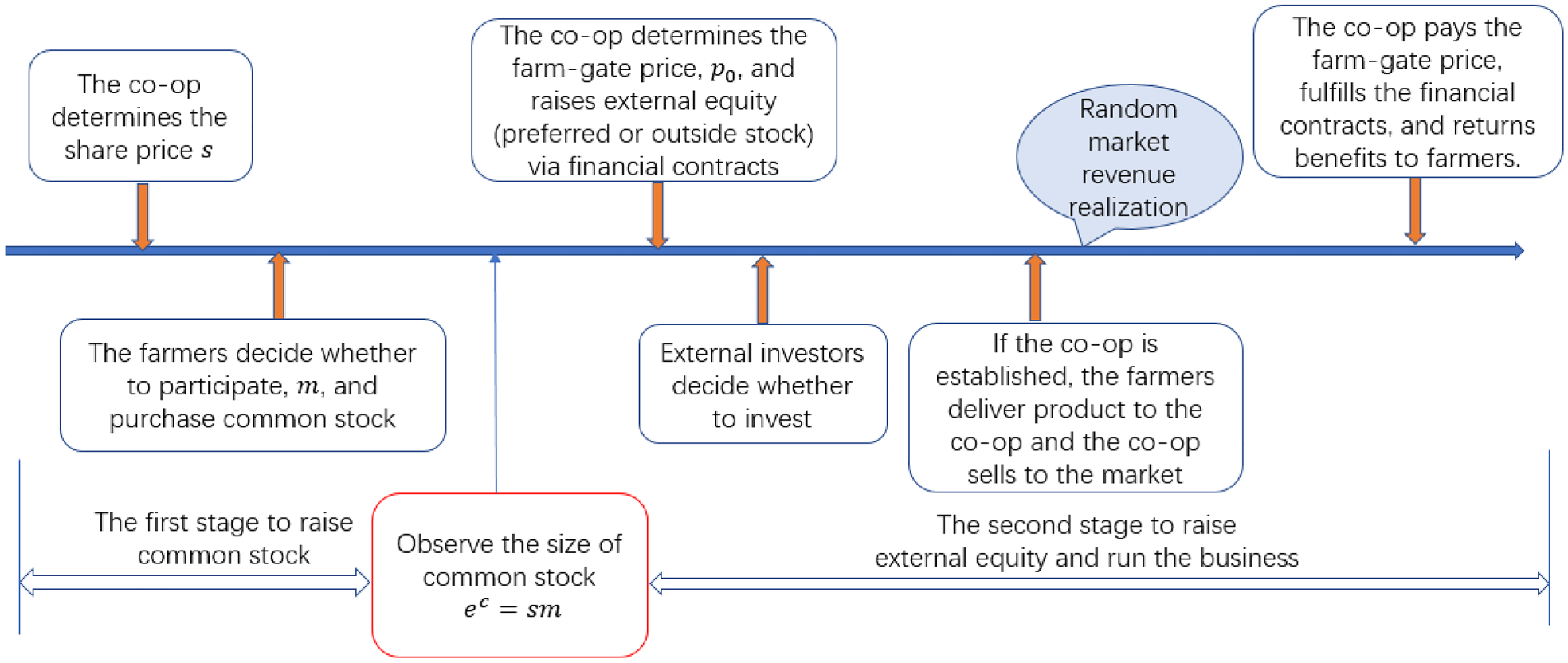

We propose a two-stage game theoretic model to study the financing and farm-gate pricing problem for a start-up co-op seeking to raise equity from both farmers and external investors. As illustrated in Figure 1, the first stage is to raise common stock through interaction between the co-op initiator and the farmers, and the second stage is to raise external equity from investors. The equity raised from both stages is used to fund the co-op’s establishment and operations if feasible. We model both stages as a Stackelberg game in which the co-op takes the leader position. Specifically, the co-op proposes terms for common stock share to farmers in the first stage and then offers financial contracts to competitive external investors, as is standard in the finance literature. This is in line with the observation that a co-op is usually initiated by several leading members who determine a common need and develop an idea of how to fulfill it (Rapp and Ely, 2010). These leading members, who we group together as the co-op initiator, propose co-op terms, such as common stock share, to other farmers who then decide whether to participate accordingly. Most smallholder farmers (as assumed in this paper) just make their individual decisions on whether to participate, rather than operational and financial decisions at the organizational level. Thus, we do not differentiate between the roles of the co-op initiator and the start-up co-op, and simply use the term the co-op to refer to the entity that makes organizational decisions for the co-op in the rest of the paper. A summary of all notation and parameters can be found in Table 1.

The timing of events.

Summary of notation.

As in other businesses, establishing a co-op requires a large amount of capital upfront. As described in a report of United States Department of Agriculture (Rapp and Ely, 2010), the co-op needs to cover both the cost of facilities and operating costs. Required facilities may include land, buildings, and equipment, whose cost is largely dependent on the expected business volume. Operating costs may include raw material costs, employee salaries, office and utilities, transportation, etc., with the per-unit operating costs tending to decline as the volume increases. In line with this, we assume that the total cost for the co-op to get established and operate is

Once established, the co-op can start its operations and process the products collected from farmers. When selling the processed product, the co-op is subject to an uncertain market price. Let

As explained in Section 1.1, we consider three types of equity: common stock, preferred stock, and outside stock. To separate the effects, we assume the co-op can only combine common stock with one other financing source, and accordingly examine three scenarios as described below. Recall that both farmer-members and non-members can purchase preferred stock or outside stock. This does not challenge the rule of profit distribution because in each scenario the profit is distributed based on how the co-op raises the capital, rather than on who finances the co-op.

Scenario 1 (Pure Common Stock): The co-op limits its equity to common stock and distributes the profit by patronage. Scenario 2 (Common Stock + Preferred Stock): In addition to common stock, the co-op determines the size of preferred stock and the financial return to preferred stockholders. After the realization of market revenue, the co-op first pays farmers at the farm-gate price, then meets its obligation to the preferred stockholders, and finally distributes the remaining value by patronage. Scenario 3 (Common Stock + Outside Stock): In addition to common stock, the co-op determines the size of outside stock, which enjoys the same economic benefit as common stock. In this case, the co-op distributes the profit by equity after making the product payment to farmers.

We use

In addition to the size of preferred stock,

To motivate external investors to invest in a co-op, the expected return should at least meet their expectations. In the current supply chain finance literature (see de Véricourt and Gromb, 2018), the investors, on expectation, usually earn a rate equal to the risk-free interest rate (generally assumed to be zero). However, considering the fact that external investors in a co-op rarely enjoy control rights or voting rights, we assume external investors expect a premium rate

As discussed, one critical decision that influences the expected return to external investors is the farm-gate price

Farmers need to decide whether to participate in the co-op based upon the co-op’s decision on the common stock price (the first stage as shown in Figure 1). We consider

There are two conditions for farmer participation. First, a farmer will expect an adequate profit to be willing to join and stay with the co-op. This involves comparing a farmer’s expected profit from the co-op with a reservation profit that can be earned without joining the co-op. When participating in the co-op, the individual farmer’s profit is the co-op’s average profit, that is,

Thus, the participation constraint depends on whether a farmer can afford the individual processing cost. Denote the wealth of farmer

Second, a farmer needs to have sufficient wealth to cover the required common stock for membership. This requires

The decisions of other farmers (regarding whether they will join or not) affect the benefits of all participating members. We assume that co-op membership is observable to the co-op and to all the other farmers. Potential farmer-members must form beliefs about their equilibrium values when deciding whether to join the co-op. In turn, these beliefs must be confirmed in equilibrium; that is, farmers should act rationally with respect to information and correctly predict the equilibrium values as a result. As in all definitions of equilibrium, farmers’ choices and beliefs are simultaneously determined. Taking these into consideration, together with the fact that any farmer will only join the co-op if the common stock share is affordable and if he/she expects to receive a high expected payoff, we can write the following recursive relationships:

As described in Figure 1, the co-op’s problem is a two-stage problem when external equity is used: deciding the share price for common stock in the first stage and considering variables related to raising capital from external funds in the second stage. Note that the second stage is only relevant for Scenarios 2 and 3, since external funds are not considered in Scenario 1. To capture the user-benefit principle, we assume that the co-op aims to maximize the total farmer-members’ profit in all scenarios, as is standard in the co-op literature (Soboh et al., 2009). This objective combined with the fund-size constraint applied in the model ensures the co-op can protect the control rights of farmers in Scenario 3, where outside stockholders share the net profit with farmers.

For all scenarios, the construction of the co-op’s problem follows a similar structure, though the formulated expressions could differ, as will be analyzed in Section 4. In the first stage, the co-op makes a decision on the share price of common stock

With the objective of maximizing total farmer-members’ payoff, the second-stage objective is written as in equation (2). After the market revenue is realized and financial returns are paid to external investors, the payoff for all farmers includes several elements: any leftover funds after setting up the co-op (

Stage 1: Maximizing the expected total profit of all farmers:

Stage 2: Given

We start our analysis with Scenario 1 in Subsection 4.1, where the co-op limits its equity to common stock. We continue in Subsection 4.2 with Scenario 2, where the co-op issues preferred stock and common stock, and in Subsection 4.3 we consider Scenario 3, where the co-op issues outside stock and common stock.

Scenario 1: Pure Common Stock

We first present Scenario 1 where no external funds are raised. This serves as a benchmark to compare with the other scenarios. Recall that the co-op’s problem is a one-stage problem in Scenario 1, with no external equity. Setting

(Scenario 1) Suppose

The profit distribution with preferred stock after the realization of market revenue.

The existence of equilibrium as in Proposition 1 requires that the number of farmers shall be larger than a certain value. This is because a small farm base may mean insufficient farmers to participate and hence make it not profitable to establish a co-op business. The establishment of a co-op also requires farmers to have enough money to pay the share price required to cover the cost, that is,

Note that the farm-gate price is muted when the equity is limited to farmers. This is because both the farm-gate price and the profit after the product payment belong to the farmers. In other words, the farm-gate price does not change farmers’ payoff and thus does not influence their participation behavior. This is consistent with our observations for start-up co-ops. In particular, the co-op would not guarantee a farm-gate price when raising equity from farmer-members due to the uncertain market price (Co-op Farming, 2023). Nevertheless, benefits such as economies of scale, democratic control, or ownership rights continue to serve as incentives for farmers to participate in the co-op.

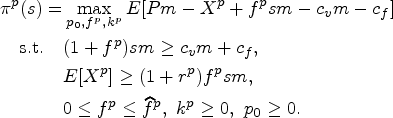

In this scenario, the co-op can issue preferred stock in addition to common stock. Recall that

From Table 2, we can get the expected return to investors from the preferred stock

In the second stage, with given

Lemma 1 shows that the co-op will never issue more preferred stock than needed, so all equity raised is used to cover the required cost; this is because of the financial cost implied by

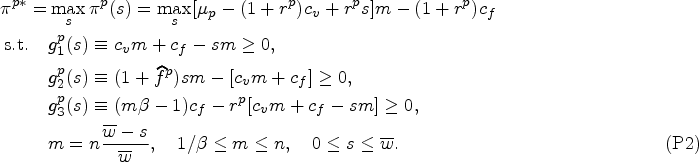

Put the second-stage decisions into the co-op’s first-stage problem and it can be written as:

Regarding the constraints, we can show

(Scenario 2) Assume No business is established if Not include preferred stock, that is, Include the preferred stock but not to the limit, Issue preferred stock up to the limit; that is,

With the share price

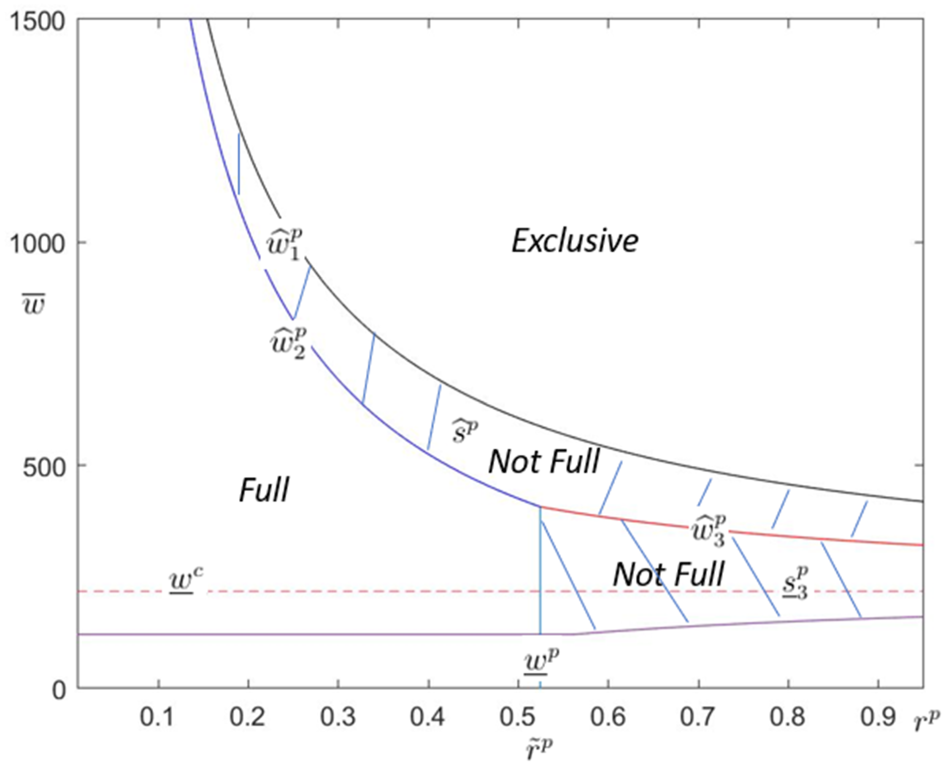

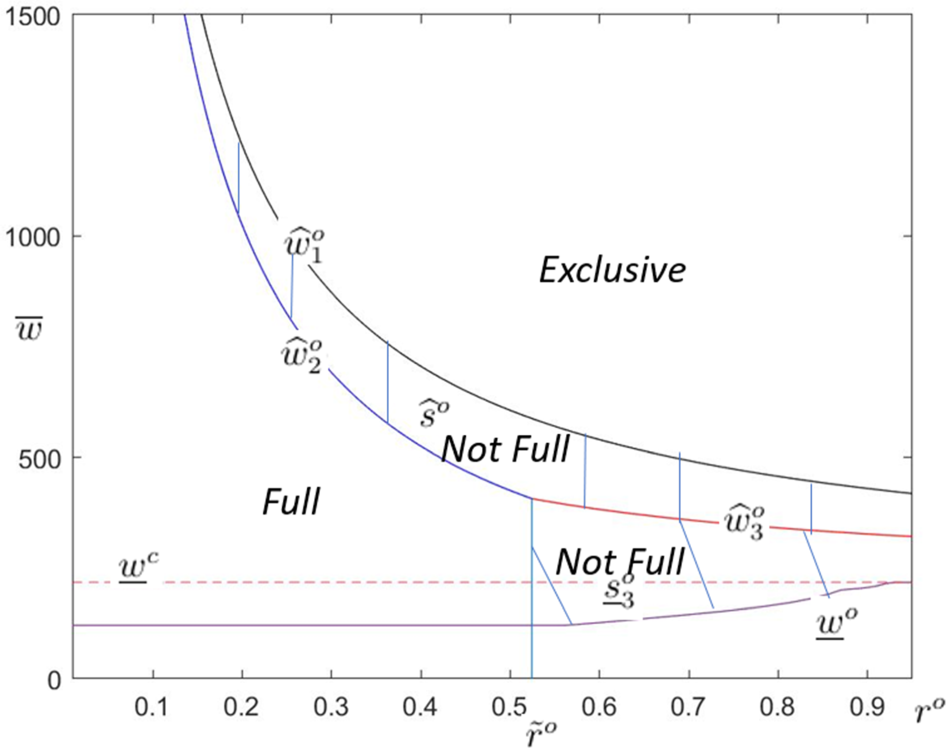

Theorem 1 provides insights into the three key decisions regarding the co-op’s capital structure. The first decision is whether to establish a co-op business; the second is whether to completely exclude external funds (exclusive system) or access external funds (inclusive system); and the third is whether the existing limit on external funds should be fully used (full) or intentionally kept underused (not full) at the profit-maximizing co-op size. To follow the discussion, the reader may find it helpful to refer to Figure 2.

Structure of the financing policy in equilibrium with preferred stock. Notes:

Theorem 1 Part (1) answers the first question, stating that if the wealth of farmers is sufficiently low, that is, lower than a certain threshold (

Part (2) answers the second question by characterizing whether to issue preferred stock. In particular, there exists a threshold between an inclusive and an exclusive system,

Parts (3) and (4) answer the third question by characterizing the financial structure when the system is inclusive. If

Note that when issuing preferred stock, both the farm-gate price and the face value of preferred stock

In this scenario, the co-op raises equity from both common stock and outside stock. Recall that

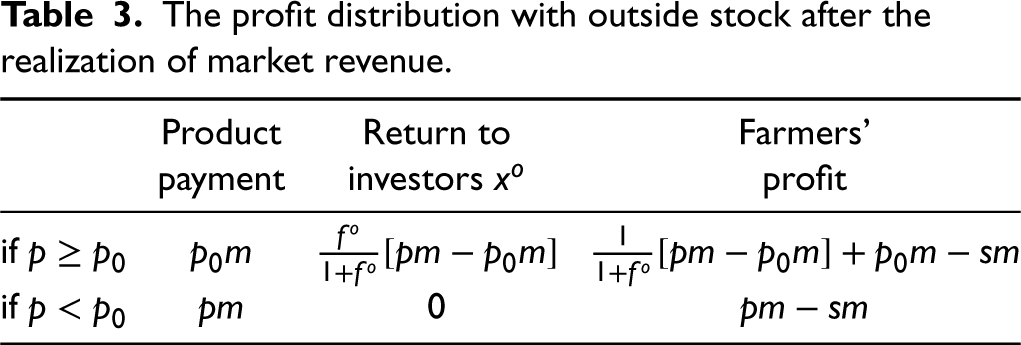

The profit distribution with outside stock after the realization of market revenue.

The profit distribution with outside stock after the realization of market revenue.

Following Table 3, the expected return to investors is

In the second stage, with given

As equation (7) sets the optimal farm-gate price given a certain co-op size, it also highlights the conflicting interests of farmers as patrons and investors. The left-hand side of equation (7) is the expected product payment, while the right-hand side is the expected market revenue minus the financial return. Since the co-op’s total cost

Furthermore, ensuring a non-negative product payment requires

With Lemma 2, the first-stage problem is:

Structure of the financing policy with outside stock in equilibrium. Note: We use the same parameters as in Figure 2.

Similarly, define

(Scenario 3) Suppose No business is established if Not to include outside stock, that is, Include the outside stock but not to the limit, Issue outside stock up to the limit, that is,

With the co-op’s decision on

Each statement in Theorem 2 corresponds to an analogous statement in Theorem 1, with the statements also providing insights into the three key decisions (see Figure 3). As explained above, there exists a watershed in terms of

While preferred stock and outside stock may exhibit similar structures in the co-op’s equilibrium financial decisions, they are priced differently through the farm-gate price

In this section, we provide managerial insights under our specific financing types. Recommendations regarding financing types will be investigated in the following section.

The Role of Farm-Gate Pricing in Agricultural Co-ops

The first insight from our analysis is the unique role of the farm-gate price in agricultural co-ops. To start with, our model indicates that the influence of the farm-gate price in a co-op supply chain is not as significant as in a typical buyer–supplier chain. Typically, the purchasing price set by a buying company will play a critical role in motivating suppliers’ behavior (Ayvaz-Çavdaroğlu et al., 2021). However, this role of farm-gate price is muted in a co-op, particularly when the equity is limited to farmers only. As discussed in the Introduction, one feature that distinguishes the co-op is that it is owned by farmers and thus obliged to return all profit to its farmer-members. This feature makes the farm-gate price in a co-op less critical in motivating farmers’ participation. As such, a co-op does not need to commit to a farm-gate price when farmers make participation decisions.

However, the farm-gate price influences the investors’ returns and hence the co-op’s financial decisions when the equity is extended to external investors. As discussed with Lemmas 1 and 2, the farm-gate price reflects the conflicting benefits between farmers and external investors for both preferred stock and outside stock. This is consistent with the literature (Chaddad and Cook, 2004) that non-common stock can create conflicts with the interests of patron members.

Interestingly, our analysis also highlights the conflicting roles of farmers as patrons who care about product payments and as investors (or owners) who enjoy the residual claim. When the equity is limited to farmers, this conflict is not apparent because both product payments and the after-product payments residual claim belong to the farmers. However, when the equity is open to external investors, this conflict becomes apparent. Naturally, farmers as patrons expect a high farm-gate price while they as investors would prefer a low farm-gate price so the residual claim can be high. In this sense, the farm-gate price serves as a tool for reconciling the conflict in farmers’ dual roles through different approaches for preferred stock and outside stock.

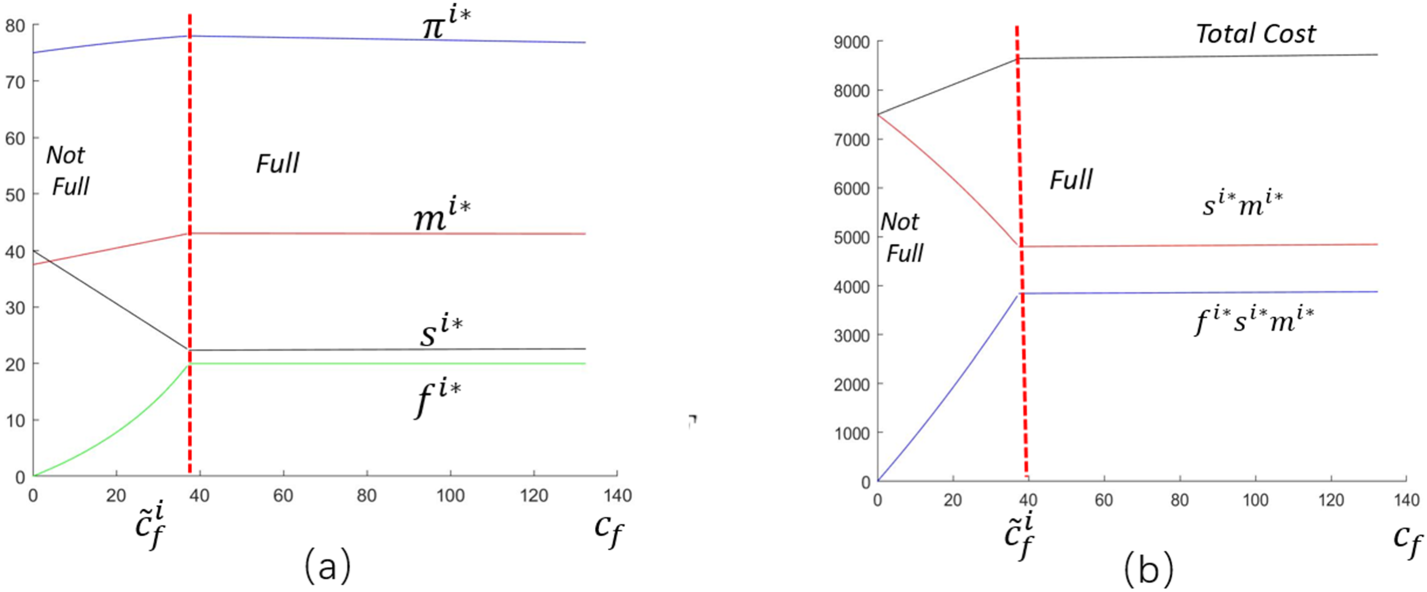

Fixed Cost and the Value of Pooling

As per our analysis, the average cost of the co-op decreases as the co-op size increases, which demonstrates a pooling benefit and forms a motivation for farmers to participate. In our model, the pooling benefit is associated with the fixed cost

Before visualizing the impact, we first characterize the financial strategies in equilibrium in terms of the farmers’ wealth and the fixed cost

The influence of the fixed cost and the pooling benefit. Note: We set

Figures 4(a) and 4 (b) illustrate how the co-op size

The results confirm that pooling benefit is a key driver for farmers to participate and so increases the co-op size and the total profit. Yet these benefits can only be enjoyed until the fixed cost reaches a certain level. The pooling effect does not always help expand the co-op size or increase the profit, and a high fixed cost could lead to side effects, where the co-op size and the total profit start decreasing with the fixed cost.

In this section, we focus on another important aspect of the co-op’s decision, that is, which type of funding is better. We first compare external equity with the benchmark case and then compare performance between the two types of external equity. As preferred stock and outside stock have a similar policy structure and thus lead to the same performance in several cases, the term “dominate” is used to indicate “weakly dominate” throughout this section.

Proposition 2 presents the comparison between common stock and external equity in terms of co-op size, farmers’ total profit, and the individual farmer’s profit. In the earlier analysis, we have shown that the equilibrium share price with preferred stock or outside stock is less than that in the benchmark case, that is,

In comparison with the financial structure limited to common stock,

The financial structure with either preferred stock or outside stock increases the co-op size and the total farmers’ profit, i.e., If

An interesting observation from Proposition 2 is that issuing external equity does not guarantee an improvement in the individual farmer’s profit, which equals the average profit. This is because of the two opposing effects of external equity. On the one hand, introducing external equity increases the co-op size and can lead to a cost reduction through the pooling effect. On the other hand, issuing external equity increases the financial cost of the co-op. So, the individual farmer’s profit is increased only if the cost-saving is larger than the financial cost of raising external equity (as expressed in the inequity condition in Proposition 2), and not otherwise. A specific example of the individual farmer’s profit being reduced compared to the benchmark case is when

This also suggests maximizing the total profit of all farmer-members is not always consistent with maximizing the individual farmer’s profit. With the objective of maximizing the total profit, the co-op may expand the co-op size at the cost of a decreased average profit. As such, the equilibrium co-op size can differ when the co-op applies different objectives. Specifically, when maximizing the total profit, the co-op will choose a co-op size where the marginal utility of

With this result, we are also interested in how the co-op and its external financial strategies impact the profit of the whole farmer population. To explore this, we first examine the profit of farmers before a co-op is established. In the absence of a co-op, only farmers who can afford to process independently, that is, those with

Next, we compare the performance of preferred stock versus outside stock. The comparison between the two is more complicated because each scenario could lead to a different financial structure in equilibrium. To produce meaningful comparisons, we make assumptions about whether external equity-related parameters, such as the size limits of external funds

For both the co-op size and the farmers’ total profit,

Suppose Suppose

When both preferred stock and outside stock have the same size limit and investors’ premium rate, that is,

In practice, investors can demand different premium rates for preferred stock and outside stock. In particular, investors are likely to demand a return higher from outside stock than from preferred stock, that is,

The above results are derived when the size limits of preferred stock and outside stock are the same, which may not always be the case. Recall that outside stock raises concerns over the co-op status of the business, because it shares the net surplus with common stock. In some co-ops, outside stock may even bear limited control and voting rights, which further increases concerns about demutualization. Therefore, it is likely that the size limit of outside stock is less than that of preferred stock, that is,

When

Theorem 4 shows that preferred stock dominates in terms of the total profit if it has a larger size limit (

In summary, preferred stock can be attractive for the co-op due to its relatively low financial cost, higher tolerance on the fund size limit, as well as greater flexibility in the farm-gate price. In this regard, our analysis provides corroboration for our observation that many co-ops prefer to issue preferred stock when seeking external equity (Pitman, 2020). However, from the perspective of investors, preferred stock with a fixed return rate may not provide sufficient return, depending on the interest rate environment and the perceived risk of the co-op. While preferred stock can be attractive to external investors when interest rates are low, investors will quickly switch to alternative investment choices, particularly those that provide a higher rate of return and that are considered to be of a lower risk, when the interest rate rises. Therefore, when preferred stock is unattractive, outside stock could be a good option.

This work is motivated by the increasing number of co-ops restructuring their financial structures and the growing number of co-ops being established with cash-constrained farmers in developing countries. In addition to members’ equity, co-ops have options for seeking external funds, including preferred stock and outside stock. To control the risk and maintain the control rights of farmers, co-ops usually constrain the size of external funds based on how much they can raise from farmers through common stock. Despite the prevalence of such strategies in practice, they have received limited attention in the literature. Thus, one of the important contributions of this paper is developing a stylized framework that helps when building new models to investigate various research questions on related financing and operations problems in co-ops.

Key results from analyzing the model are briefly summarized as follows. First, we have characterized the equilibrium financial strategies when raising external funds and answered questions concerning whether and how much to issue, and under what conditions. Furthermore, our analysis finds that financial strategies in relation to the farm-gate pricing differ when issuing preferred stock compared to outside stock. Second, we have investigated the effect of the pooling benefit on the farmers’ participation decision and show that the pooling benefit is able to motivate farmers to participate while also allowing the co-op to raise more external equity. Third, by comparing the performance of the two types of external funds, we have provided important insights into the co-op’s choice of financing options.

Several limitations arise due to our specific modeling assumptions, and further research is needed to validate the relevance of our insights when these assumptions are relaxed. First, we only consider uncertain market price and assume deterministic yields in this paper. However, there are other uncertainties in agricultural operations that can bring financial risks to investors, such as uncertain yield or uncertain demand. Therefore, considering multiple uncertainties including uncertain and/or heterogeneous yield is worthwhile for future research. Second, we assume that outside stock does not convey any control or voting rights. However, in some co-ops, outside stock may bear limited control and voting rights. In this case, the external investors could challenge the co-op’s objective of maximizing the farmers’ profit and more trade-offs will be considered. Third, we assume that the market price is exogenous. However, it would be interesting to examine a situation in which the market price is determined by the total supply of all farmers and each farmer determines an equilibrium output. Fourth, our model assumes that all farmers are risk-neutral. However, in reality, farmers could be risk-averse, especially toward equity investment. This is interesting but left for future research. Fifth, we consider pure equity financing; but it could be worthwhile considering both equity and debt financing. Last, it would be helpful to examine our model’s predictions regarding priorities for financing strategies using empirical data.

Supplemental Material

sj-pdf-1-pao-10.1177_10591478241262279 - Supplemental material for Financing and Farm-Gate Pricing Strategies for Agricultural Cooperatives With Cash-Constrained Farmers

Supplemental material, sj-pdf-1-pao-10.1177_10591478241262279 for Financing and Farm-Gate Pricing Strategies for Agricultural Cooperatives With Cash-Constrained Farmers by Xiaoyan Qian, Quan Zhou and Tava Lennon Olsen in Production and Operations Management

Footnotes

Acknowledgments

We are grateful to the departmental editor (Professor Sridhar Seshadri), an anonymous senior editor, and two anonymous referees for very inspiring and helpful comments and suggestions.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (grant nos. 71901054, 72371060, 72293563). Xiaoyan Qian received support from the China Scholarship Council (202008210048), and Quan Zhou received support from the University of Wollongong Early Mid-Career Researcher Enabling Grant (no. R5910).

Notes

How to cite this article

Qian X, Zhou Q and Olsen TL (2024) Financing and Farm-Gate Pricing Strategies for Agricultural Cooperatives With Cash-constrained Farmers. Production and Operations Management 33(8): 1641–1658.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.