Abstract

In this paper, using data from indirect auto lending and a structural model of external sales representative (ESR) behaviour, we investigate (1) the role of commissions as a potential tool to influence ESRs’ pricing decisions under limited authority, (2) the impact of optimized commissions on firm profitability, and (3) the implications for customer welfare. The results provide strong evidence for ESRs being strategic (vs. myopic) in their pricing and effort decisions; and in both cases, strategic behaviour is inversely proportional to customer risk. Moreover, once optimized, commissions are an effective tool for firms to bridge the profitability gap between centralized pricing and pricing delegation. Our analyses on social justice and fairness reveal that customer groups along the dimensions of customer risk, income class, and gender, which have been traditionally marginalized in society, suffer from inequities in the indirect-lending ecosystem. While, the optimization of commissions does not intensify these biases, we found females to be the exception, and that the inequities due to gender bias not only persist in the optimized regime, but also deepen. Through counterfactual simulations, we propose two policies for firms to minimize social inequity, which helps them balance immediate profit-maximizing goals with responsible AI initiatives.

Keywords

Introduction

The sales force plays a pivotal role in most organizations and is responsible for key marketing decisions. Specifically, the sales force handles personal selling and, because of its close proximity to customers and superior ability to assess their willingness to pay (Frenzen et al., 2010), is often delegated pricing authority to some extent (Hansen et al., 2008). Sales forces are important for firm success in several ways. Personal selling has an elasticity of 0.31 on immediate sales (Albers et al., 2010), is crucial for maintaining customer lifetime value through repeated sales (Shi et al., 2017), and has a larger impact on ROI than advertising (Narayanan et al., 2004). Industry statistics also support the significance of sales forces for the economy. U.S. employment statistics indicate that 14 million people are employed in sales-related positions, which accounts for 10% of the U.S. workforce (Bureau of Labor Statistics, 2019). U.S. firms also invest more than $800 billion in personal selling, equating to 10% of sales and surpassing the funds allocated to advertising by a factor of three, on average (Zoltners et al., 2008).

Although salespeople are often employed internally within an organization, external sales representatives (ESRs) are also common in various customer markets such as real estate, insurance, lending, and travel, where organizations use brokers or representative firms that act as intermediaries between themselves and customers. Outsourcing the sales function to intermediary firms is common in many service industries, especially when providers are far removed from customers and when customers prefer one-stop shops where they can purchase services from different providers (Gallego and Talebian, 2014). For example, auto lenders issue loans through ESRs employed by auto dealerships that control demand via their proximity to customers who want to finance vehicle purchases.

Even though ESRs are widely used in practice (Coughlan et al., 2006), across an estimated 67% of organizations (Caldieraro and Coughlan, 2007), research about ESRs is scant as academics have focused on internal sales representatives. The context involving ESRs is interesting for three main reasons. First, firms are able to utilize a combination of salary and incentives to compensate internal sales forces (Coughlan and Joseph, 2012). On the other hand, compensation for ESRs is only possible through incentives 1 (Caldieraro and Coughlan, 2007; Kouvelis and Shi, 2020). One compensation structure commonly employed in ESR settings involves spiffs, which are commissions firms directly pay to ESRs (Caldieraro and Coughlan, 2007). Alternatively, firms pay commissions to the intermediary, which then passes part or the entire commission to the ESR. Second, ESRs cannot be easily monitored/controlled by the firm due to their external position (Caldieraro and Coughlan, 2007; Kouvelis and Shi, 2020). This lack of control causes firms’ greater concerns that ESRs will engage in myopic behaviour, resulting in the pursuit of short-term results without considering future consequences or investing in process-oriented decision-making (Locander et al., 2023; Stathakopoulos, 1996). For example, ESRs that are granted pricing authority may ‘shoot for the stars’, electing to sell products to customers at higher prices to earn higher commissions rather than meticulously assessing customer willingness to pay when selecting a price. Third, in contrast to full-price discretion, which organizations with internal sales forces use more commonly, pricing discretion conceded to ESRs is often limited and structured to allow providers to retain some pricing control when outsourcing selling efforts. For example, ESRs often choose prices from a pricing sheet containing a discrete number of price–commission combinations. Firms use this form of limited pricing discretion to enable profitable selling since it compensates salespeople based on margin while limiting the extent of pricing flexibility and sharing of cost-related information (Stiving, 2022; Zoltners et al., 2015).

The profitability of pricing delegation relative to centralized pricing is a topic examined in the academic literature. Although centralized pricing outperforms pricing delegation (Phillips et al., 2015), pricing delegation remains prominent in the field, with an estimated 72% of organizations giving full or limited pricing authority to sales forces (Hansen et al., 2008). In the context of ESRs, this apparent contradiction can be explained by the fact that ESRs are the gatekeepers of demand that firms can lose if they decide to remove pricing power from the sales force through centralized pricing. We propose optimized commissions as an effective tool to bridge the profit gap between centralized pricing and price delegation, allowing firms to influence ESR behaviour while maintaining the relationship with ESRs and, thus, maintaining access to demand. Whether or not commissions can be used to narrow the performance difference between these two pricing strategies is an empirical question with managerial importance. Even still, empirical academic research on the topic is limited.

In summary, while ESRs are critical for sales, they are difficult to control. This highlights the importance of incentive mechanisms, specifically commissions, to influence pricing and effort decisions of ESRs to better align ESR behaviour with firm objectives. In this paper, we investigate how firms can leverage commissions as a tool to influence ESRs’ effort allocation and pricing decisions in an indirect retail channel. We consider the decisions of all important stakeholders in the channel, namely the firm, ESR, and customer, as well as the interdependencies between these, to be able to understand under what conditions ESRs act myopic (i.e. focusing on the commission dollars only) vs. strategic (i.e. focusing on the expected commission dollars) in their pricing decisions. This sophisticated ecosystem framework allows for these three stakeholders to make different decisions motivated by different utility structures, all impacting each other, providing a challenging, yet interesting, setting for research.

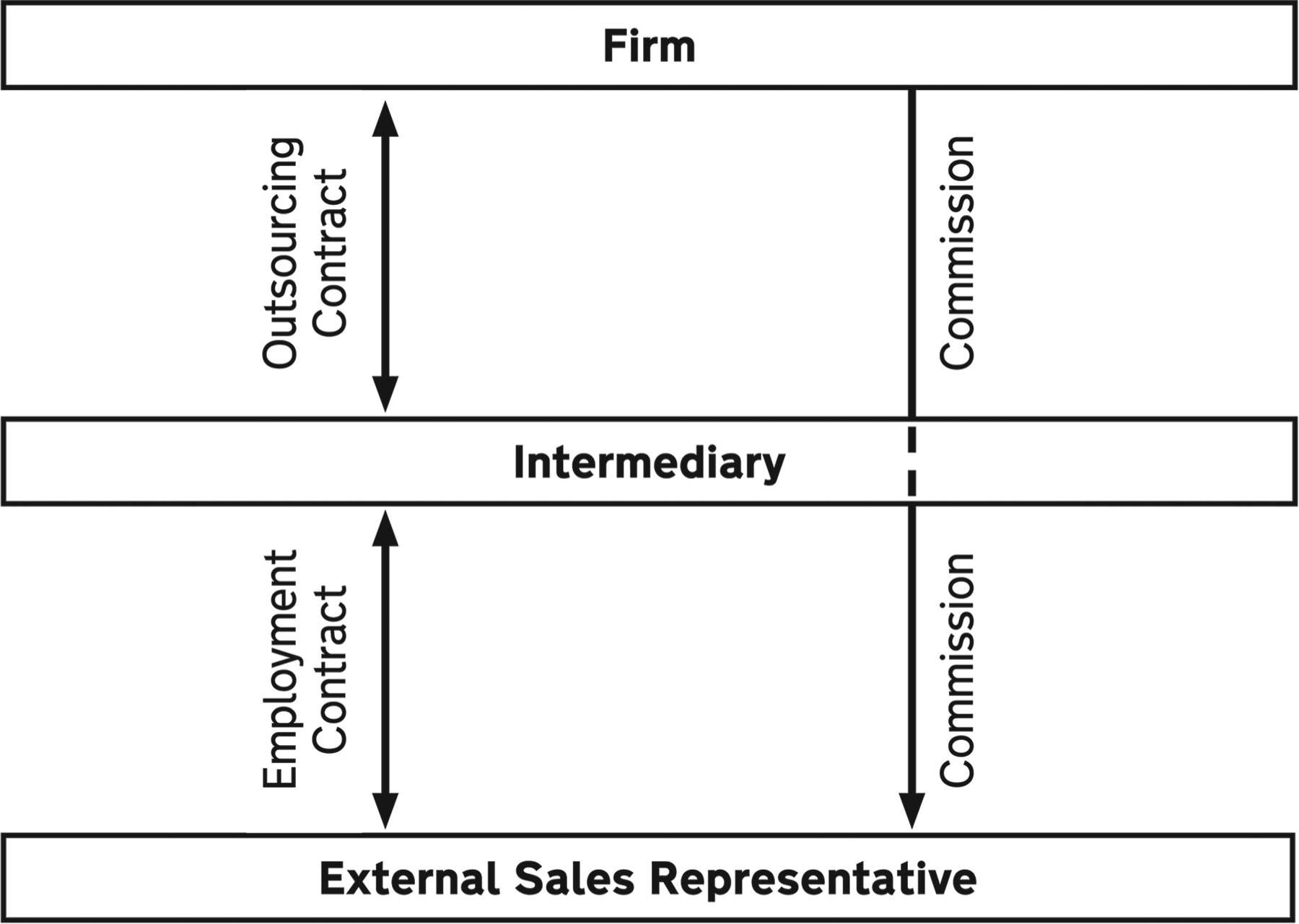

As depicted in Figure 1, the firm uses an outsourcing contract to authorize the selling and pricing of its products to the intermediary, which delegates these activities to its sales force using an employment contract. In exchange, the firm pays the intermediary a commission, which is passed on by the intermediary to its sales force, either partially or entirely. We use indirect auto lending as our context, whereby the firm is a lender, the intermediary is an auto dealership, and the ESRs are the sales representatives employed by the dealer. Typically, auto dealerships segregate sales responsibilities for vehicles and financing, such that salespeople responsible for these tasks are different. The current paper focuses on the latter (i.e. the ESRs).

Visual representation of the ESR setting.

To put it briefly, in our context, the ‘product’ is the auto-loan, and its ‘price’ is the interest rate, which the ESR has partial authority to set. The lender grants partial authority by enabling the ESR to select a pricing option from the lender-provided pricing sheet, whereby price–commission rate combinations are ordered from the highest to the lowest. The commissions pertain to the dealer reserve paid by the lender to the auto dealership. They play a pivotal role in the indirect lending ecosystem because reserves make up a substantial portion of dealerships’ revenues (Davis, 2012; Grunewald et al., 2020) and influence ESRs’ pricing decisions (Financial Consumer Agency of Canada, 2016); thus having implications for lenders and customers. Recent reports regarding a major lender ceasing operations in Canada (Financial Post, 2023; Willis, 2023) and concerns regarding consumer welfare (Consumer Financial Protection Bureau, 2016; Reynolds and Cox, 2020; Sullivan et al., 2020) highlight the importance of understanding the impact of optimized commissions on ESR pricing decisions in the indirect lending context.

Using a dataset from a large financial institution that engages in indirect lending within the North American auto-loan market, we seek to answer the following research questions: (1) Are ESRs myopic or strategic in their pricing decisions, and how do commissions influence this? (2) Are ESRs strategic in their effort allocation decisions and if so, can firms leverage commissions to influence effort? (3) Are commissions, once optimized, useful to align firm and ESR goals? (4) What are the fairness implications of the indirect lending ecosystem and optimal commissions; how can firms use AI and analytics-based tools to implement fairness into their data-driven decision-making processes?

Our intended contribution to the literature is fourfold. First, we show that ESRs are strategic in their pricing behaviour and do take into account the expected likelihood of the deal being booked, rather than merely focusing on the commission dollars in the pricing sheet. While rare, myopic behaviour happens when the deal is of low value to the ESR, and the cognitive effort of strategic pricing is not justified. In such cases, we find that ESRs adopt simple heuristics, such as picking the highest commission option on the pricing sheet. Second, we provide evidence for the dual effect of ESR effort on the indirect-lending ecosystem: a direct quadratic negative effect on ESR utility and an indirect positive effect through its impact on customer utility. We find that through strategic management of effort, ESRs manage this trade-off and mitigate risk for the firm while counteracting customers’ price sensitivity. Third, we show that once optimized, commissions effectively bridge the profitability gap between centralized pricing and price delegation and successfully align ESRs’ behaviour with the lender's objectives. Lastly, welfare analyses suggest that high-risk, low-income, and female customers are marginalized within the indirect lending ecosystem. These inequities are not intensified further by optimizing commissions, except for females. The results suggest the bias against females persist and deepen in the profit maximizing regime. Using counterfactual analysis, we develop two policies to help firms mitigate these inequities experienced by the vulnerable groups, demonstrating that firms can balance profit objectives with responsible AI practices to increase customer welfare.

Relation to the Literature

This article contributes to two main streams of literature, sales force compensation and sales force price delegation. The majority of early research in the sales force compensation literature has been theoretical, focusing on the directionality of the effects and higher-level insights (Misra and Nair, 2011), due to the lack of detailed data regarding salesperson commissions and sales. Over the last few years, empirical research in this domain has been increasing, most of which focuses on internal sales representatives (e.g. Allcott and Sweeney, 2017; Bommaraju and Hohenberg, 2018; Brahm and Poblete, 2018; Chung et al., 2014, 2019; Kim et al., 2019; Kishore et al., 2013; Larkin, 2014; Misra and Nair, 2011; Oyer, 1998; Rouziès et al., 2009; Steenburgh, 2008; Yang et al., 2019). Sales force effort has been a consistent component of work on the topic. However, research on effort has been limited to settings with no pricing authority (e.g. Gopalakrishna et al., 2016) and in a quota-based environment (e.g. Larkin, 2014; Oyer, 1998) rather than within a commission-based environment.

In practice, sales force compensation is closely linked to pricing; the importance of this interaction is acknowledged in the academic literature. Specifically, Oyer (1998) and Larkin (2014) find that quota bonuses result in timing games, where salespeople decrease pricing at the end of the year to pull sales in from future periods to bridge the gap between current performance and their annual quota. Additionally, Yang et al. (2019) find that jointly discounting prices and increasing commissions is more profitable than using either approach alone when a sales representative's sensitivity to commission is moderate (for a summary table of our contribution to the literature, see the E-Companion (EC.1)).

The second stream of literature that we contribute to is sales force pricing delegation, which has largely been theoretical (Chen et al., 2021; Mishra and Prasad, 2004) with few exceptions (e.g. Frenzen et al., 2010; Homburg et al., 2012; Phillips et al., 2015; Stephenson et al., 1979). Both theoretical and empirical research has focused on uncovering the factors that increase the likelihood of delegating pricing to sales forces and examining the effect of pricing delegation on profitability. Concerning these questions, extant research indicates that both the likelihood and benefits of pricing delegation are highest when sales commission is based on gross margin rather than sales revenue. However, previous studies generally assume that the commission rate applied to gross margin is constant (Homburg et al., 2012; Stephenson et al., 1979; Weinberg, 1975). Research also examines the profit implications of pricing delegation compared to centralized pricing, finding the latter to be superior (e.g. Phillips et al., 2015). However, these studies take the compensation structure as given, even though changes in compensation have implications for the pricing decisions that salespeople make. Indeed, academics have called for more research that examines how firms can use sales force incentives to improve the effectiveness of pricing delegation (Kadiyala et al., 2023), bridging the profit gap relative to centralized pricing.

We extend the aforementioned work by examining (1) how commissions affect ESRs’ pricing decisions, (2) given this effect, how commissions should vary as a function of price to maximize firm profits, and (3) how salespeople strategically exert effort, given commissions, when making pricing decisions. In doing so, we aim to provide insights regarding the decision-making of ESRs, which are not only widely used in the industry but also introduce several challenges for the firm's compensation decisions, and we determine whether optimized commissions can narrow the performance gap between centralized pricing and pricing delegation.

Institutional Details and Empirical Setting

Our empirical setting involves a Canadian financial institution that sells automobile loans through auto dealerships that act as intermediaries (Financial Consumer Agency of Canada, 2016). Although first discussions of financing may occur over negotiations concerning the automobile purchase with a sales representative, these discussions will typically be high-level and, at most, determine the maximum monthly amount that the customer is comfortable paying. The final loan arrangements are then performed by the ESRs (i.e. a different sales representative than the one handling the automobile sale), who are employed by dealerships and are given partial pricing authority over loan prices by the financial institution. Using indirect auto lending as a context, we focus only on the ‘prime’ customer segment of relatively high-credit quality customers.

Another characteristic of the indirect auto lending setting is the limited price negotiation between the customer and the dealership staff regarding loan prices. Two factors drive this. First, auto loans are aftermarket goods purchased after the vehicle, the core product, which has a higher price sensitivity (Gil and Hartmann, 2009). Therefore, customers exert most of their negotiation effort finalizing the price of the automobile and are less motivated to negotiate the loan price. Second, pricing in the Canadian auto loan market is opaque. Since lenders do not provide auto loans directly to customers, the complete list of auto loan prices that are available from each competing lender is only visible to auto dealerships. This puts ESRs at an advantage when making pricing decisions since they can select one of the competing lenders and a pricing option from the lender's pricing list without customers having visibility to the pricing options available in the market. Indeed, previous research indicates that, although there are differences in sensitivity to loan pricing across customer segments, individuals are substantially less responsive to loan prices than vehicle prices in general due to customers not fully understanding that loan terms are negotiable and their lack of ability to assess loan prices correctly (Grunewald et al., 2020; Reynolds and Cox, 2020; Sullivan et al., 2020).

Next, we discuss the steps in the loan application process. The process is activated by a vehicle sale that needs financing at one of the partner dealerships. The salesperson obtains customer consent for a credit score inquiry and gathers relevant customer information (e.g. income and employment status) on the lender's behalf. The ESR is also privy to additional information not available to the lender, such as information revealed during the automobile choice process and sales negotiation or the level of anxiety that a customer experiences during the loan application process, leading to some information asymmetry between the ESR and lender.

The ESR submits the loan application on behalf of the customer. The system is consistent across auto dealerships and lenders and is structured in a particular way. The first screen within the system prompts the ESR to select a lender. Once the salesperson selects a lender, the ESR is shown a second screen that requires the salesperson to input information related to the vehicle (e.g. manufacturer, model, year), customer (e.g. income, employment status, credit score), and loan (e.g. term, amortization, loan amount, down payment). After inputting these details, the portal displays a third screen with the loan price/commission rate combinations (i.e. this is also known as the ‘pricing sheet’). The ESR must select one of these discrete options on the pricing sheet for the application. Finally, the system prompts the ESR to submit the loan application and await the lender's response. Because the market shares of the big five banks in Canada have been relatively constant in the observation period, we focus on the ESR's pricing decision and not the demand allocation decision.

Next, the lender starts adjudication for approval. The approval process is relatively consistent in the industry, with strict regulations to ensure consistency across risk management processes in Canada. The approval decision takes an average of 20 minutes and is sent back to the ESR through the online portal. If the loan is approved, the ESR provides the offer to the customer, who can either accept the loan offer at the quoted price or walk away, thus forfeiting the purchase of the vehicle altogether (Phillips, 2005, 2012). If the customer accepts the loan offer, the dealer receives the commission dollars for closing the loan sale at the selected price point with a part, or even the whole commission, passed on as an incentive to the ESR.

Details of ESR Behaviour and Illustration

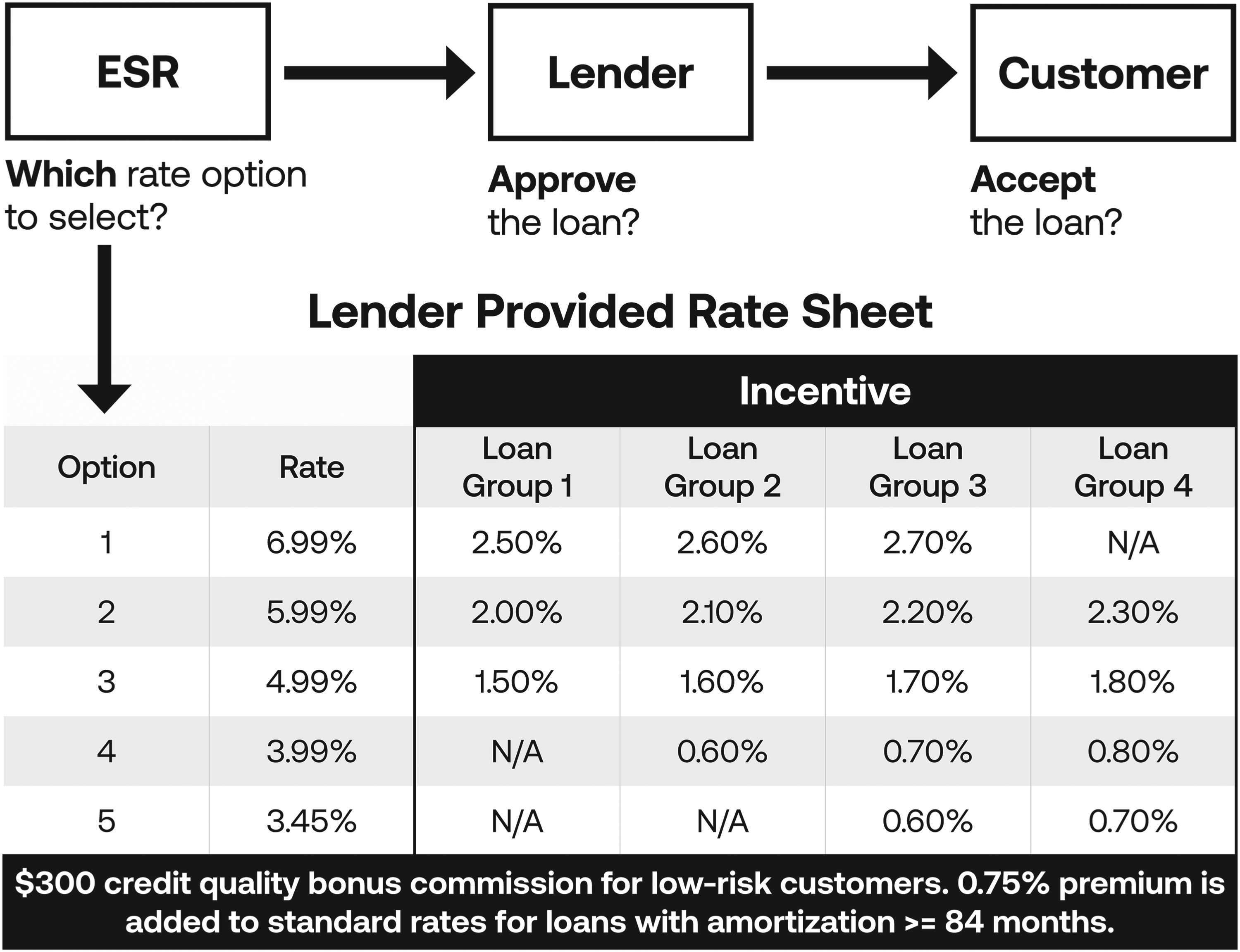

We now detail and illustrate the ESR's behaviour. Figure 2 is a visual representation of the indirect lending framework, including an illustrative example of the lender's pricing sheet, whereby available prices for offer to a customer are based on the loan group (ranging from <$20 K in group 1 to >$40 K in group 4) and amortization duration. The ESR's pricing decision is considered customized pricing with limited discretion (Phillips et al., 2015) since, given the customized pricing menu set by the lender, which is based on the loan amount and amortization requested by the customer, the ESR uses their discretion to select one of the available discrete pricing options from the lender's pricing menu.

Three-stage indirect lending framework. Note: Availability of pricing options depends on loan size. Group 1: <$20,000. Group 2: ≥$20,000 & <$30,000. Group 3: ≥$30,000 & <$40,000. Group 4 ≥ $40,000.

During the process, ESRs consider whether to take a myopic (i.e. default to a higher commission option without considering the impact that this has on the lender's loan approval or the customer's loan offer acceptance probabilities) or a strategic approach (i.e. factor in the likelihood of the loan being booked based on lender and customer decisions) to their pricing decision. In the latter case, the ESR's decision is based on the expected commission, where the ESR accounts for, among other things, differences in willingness to pay across customer segments, as evidenced by prior research in the context of loan prices (Grunewald et al., 2020). ESRs also consider how much effort they are willing to allocate toward the customer to book the loan. We describe and formalize these behavioural aspects of the ESR's decision-making process endogenously under the ‘Model Development’ section.

Using Figure 2 for illustration, let's assume a customer requests financing of $30,000 for 84 months. The ESR, then, selects one of the five options (i.e. price–incentive rate combinations) available on the lender-provided pricing menu under the column labelled ‘Loan Group 3’, at price points 6.99%, 5.99%, 4.99%, 3.99%, or 3.45%. Suppose the ESR selects the option with a loan price of 5.99%, which has a corresponding commission rate of 2.2%, and the lender books the loan. In this case, the customer pays an interest rate of 5.99% (price without amortization premium) + 0.75% (amortization premium) = 6.74% (final price), and the dealership earns 2.2% × $30,000 = $660 in commission dollars (i.e. dealer reserve), part, and sometimes all of which is passed on by the dealership to the ESR. There are also bonus structures set in place by lenders to incentivize booking higher quality customers (Sohoni et al., 2011). For instance, if the customer is low risk, the dealer also receives an additional $300 credit quality bonus. We would like to note that, because duties are segregated in auto dealerships (i.e. certain sales agents sell vehicles and others sell loans), our framework does not account for the commission from the vehicle sale itself.

While we are primarily interested in the ESR's pricing decision, our model framework captures a complete picture of the empirical setting, encompassing the decisions of the three key stakeholders in the indirect lending ecosystem, including the ESR, lender, and customer, as well as the interdependencies between these. We develop a structural model of ESR decision-making allowing for both myopic and strategic pricing behaviour, where the ESR considers commission dollars only (i.e. myopic) or the expected commission dollars by taking into account the probabilities of the lender approval of the application and customer acceptance of the offer (i.e. strategic). Below, we describe the 3-stage model framework in detail.

ESR Decision

The indirect lending process begins with the ESR, who selects one of the J price/commission rate options from the lender's pricing sheet. As illustrated in Institutional Details and Empirical Setting, the commission rates on the pricing sheet are used to calculate the commission dollars for each pricing option. We identify the ESR-related equations with the superscript A and represent their choice between the J pricing sheet options for loan application n by

We model

ESRs maximize their expected utility,

When using myopic pricing, ESR behaviour is akin to heuristics. They default to the option with the highest commission rate and/or are influenced by the commission dollars. In Equation (2), the first term on the RHS is a binary indicator that equals 1 when the pricing sheet option offers the highest commission rate and 0 otherwise. This is followed by the impact of commission dollars,

We model ESR effort endogenously as a function of commission dollars, predicted probability of lender approval, and a dummy variable for Sunday (see Equation (3)). Most dealers are closed on Sunday, which might lead ESRs to strategically adjust their effort. This could be in the form of an increase if the ESR pushes hard to close a deal when the likelihood is high due to the absence of competition or a decrease if the lack of other options serves as a confidence boost.

After ESRs select a commission rate/loan price option, they submit the loan application to the lender for adjudication. We identify the lender-related equations with the superscript L and represent the lender's approval decision regarding each of the N loan applications by

When making the loan approval decision, the lender runs a proprietary deterministic credit approval engine that generates a decision based on several risk models. Following our discussions with the executive team at the financial institution, we approximate this behaviour and model the lender's utility,

If the loan application is approved by the lender, the ESR offers the loan to the customer, who then chooses whether to accept or reject the offer. Similar to the lender model, the accept decision for customer i,

Customer utility follows Equation (8), where

It is likely that the marketing decision variables, specifically commission dollars and price premium, in the ESR (Equations (1) and (2)) and customer utility (Equation (8)) equations are correlated with the corresponding error terms. To control for these potential endogeneity cases, we use a non-instrumental variable approach. Specifically, we use Gaussian copulas to explicitly model these potential correlations (Park and Gupta, 2012). As such, we add the additional regressors,

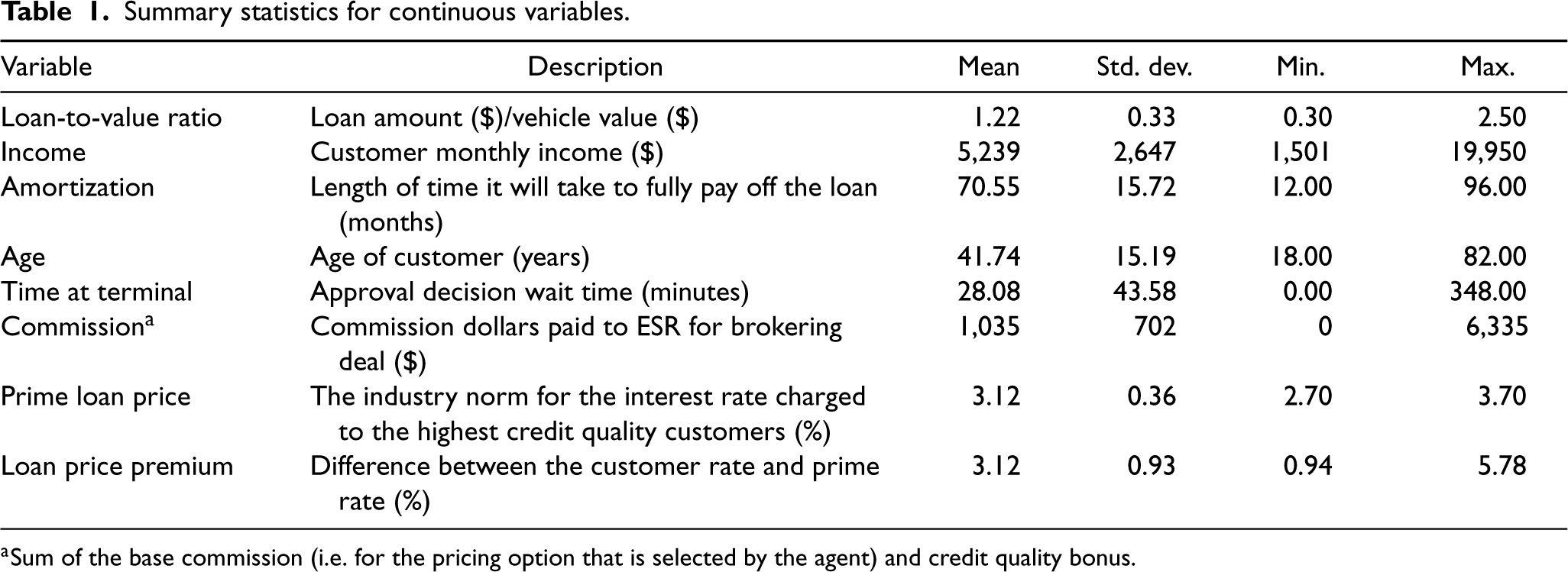

Summary statistics for continuous variables.

Sum of the base commission (i.e. for the pricing option that is selected by the agent) and credit quality bonus.

A requirement of the Gaussian copula approach is for the endogenous regressors, commission dollars, and customer loan price premium, to be non-normally distributed (Park and Gupta, 2012), which we test using a Shapiro–Wilk test. We find that both endogenous regressors are non-normally distributed (customer loan price premium: W = .975, p-value < .001; commission dollars: W = .884, p-value < .001), validating the use of Gaussian copulas for endogeneity correction.

After estimating the three-stage model outlined above while correcting for endogeneity, we optimize the agent commission rates,

We run the optimization in AMPL (A Mathematical Programming Language) and use the Ipopt (Interior Point OPTimizer) solver. Ipopt requires a nonlinear optimization problem, including an objective function and constraints, and finds a local solution to the problem using a primal-dual interior-point algorithm with a filter line-search method (Wächter and Biegler, 2006). The details of the optimization including the mathematical equations are presented in the E-Companion (EC.2).

Empirical Analysis

Data

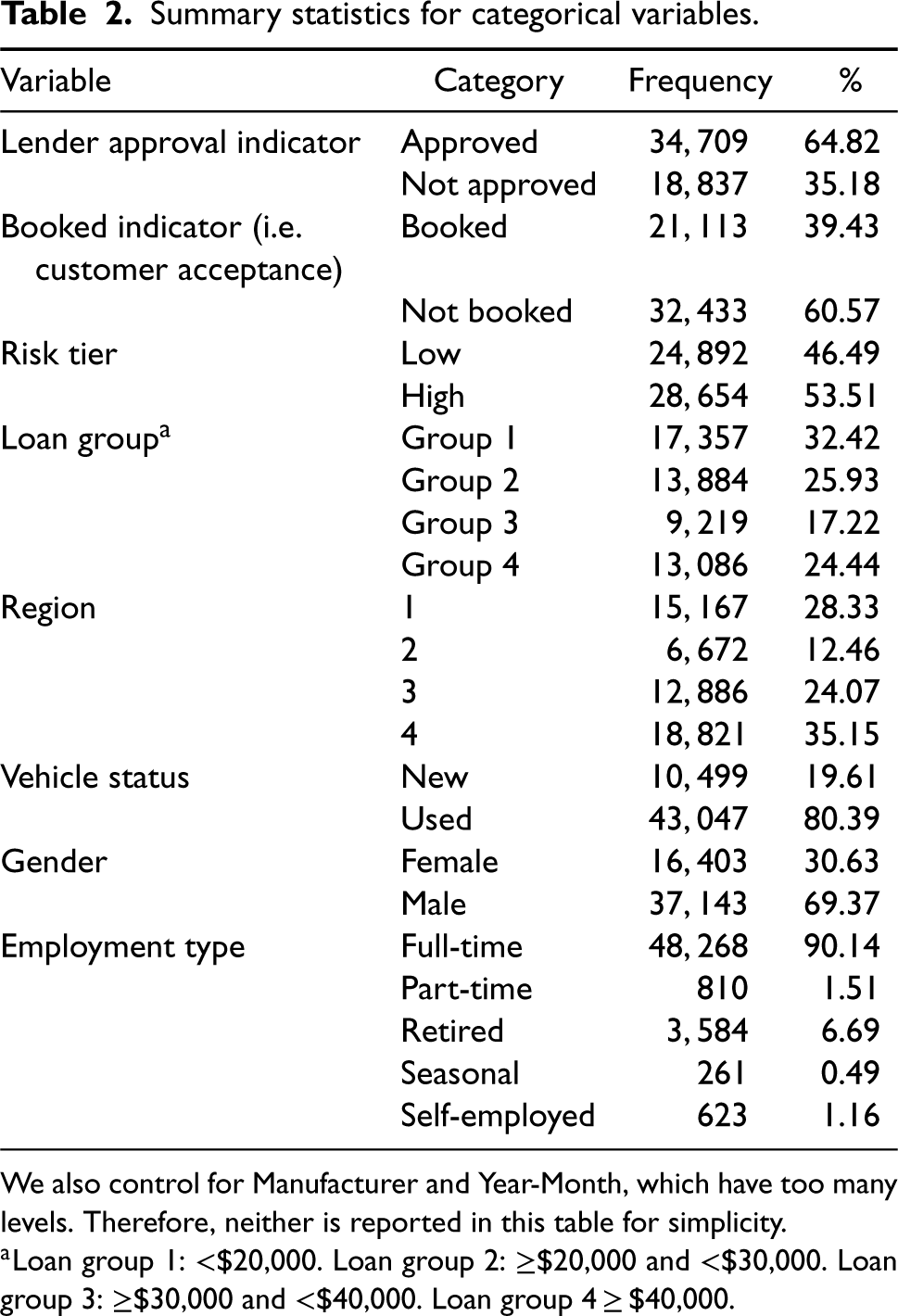

We use a data set from a large North American financial institution that offers indirect auto loans to customers through ESRs. The data include 53,546 loan applications, which were submitted to the lender between December 2016 and August 2018. Of these loan applications, the lender approved 34,709 (64.8%) and booked 21,113 (39.4%). The summary statistics and definitions of the key variables are provided in Tables 1 and 2.

Summary statistics for categorical variables.

Summary statistics for categorical variables.

We also control for Manufacturer and Year-Month, which have too many levels. Therefore, neither is reported in this table for simplicity.

Loan group 1: <$20,000. Loan group 2: ≥$20,000 and <$30,000. Loan group 3: ≥$30,000 and <$40,000. Loan group 4 ≥ $40,000.

Model-free evidence suggests that the relationship between commission dollars and ESR price selection is non-monotonic with the first peak at the option with the highest commission, followed by a bell-shaped choice probability curve. This provides initial support for the complexity of ESRs’ pricing decisions, potentially pointing out both myopic and strategic behaviour. We test this in our estimation and quantify the drivers leading to the use of heuristic (i.e. myopic) and analytical (i.e. strategic) approaches by the ESR.

We provide further discussion of model-free evidence in the E-Companion (EC.3) including evidence for higher volatility in customer acceptance at higher loan prices, suggesting potential differences in price elasticity across customers. As such, we allow for heterogeneity in price sensitivity due to risk tier, region, and vehicle newness through interaction terms in the customer acceptance model (see Equation (8)).

Considering the insights from the model-free evidence, we discuss the estimation results, starting with the ESR model. Although not our focus, we will continue with the lender and customer decisions since these influence ESRs’ pricing decisions through expected commission dollars (see Equation (1)) in cases where ESRs are strategic.

ESR Price Choice

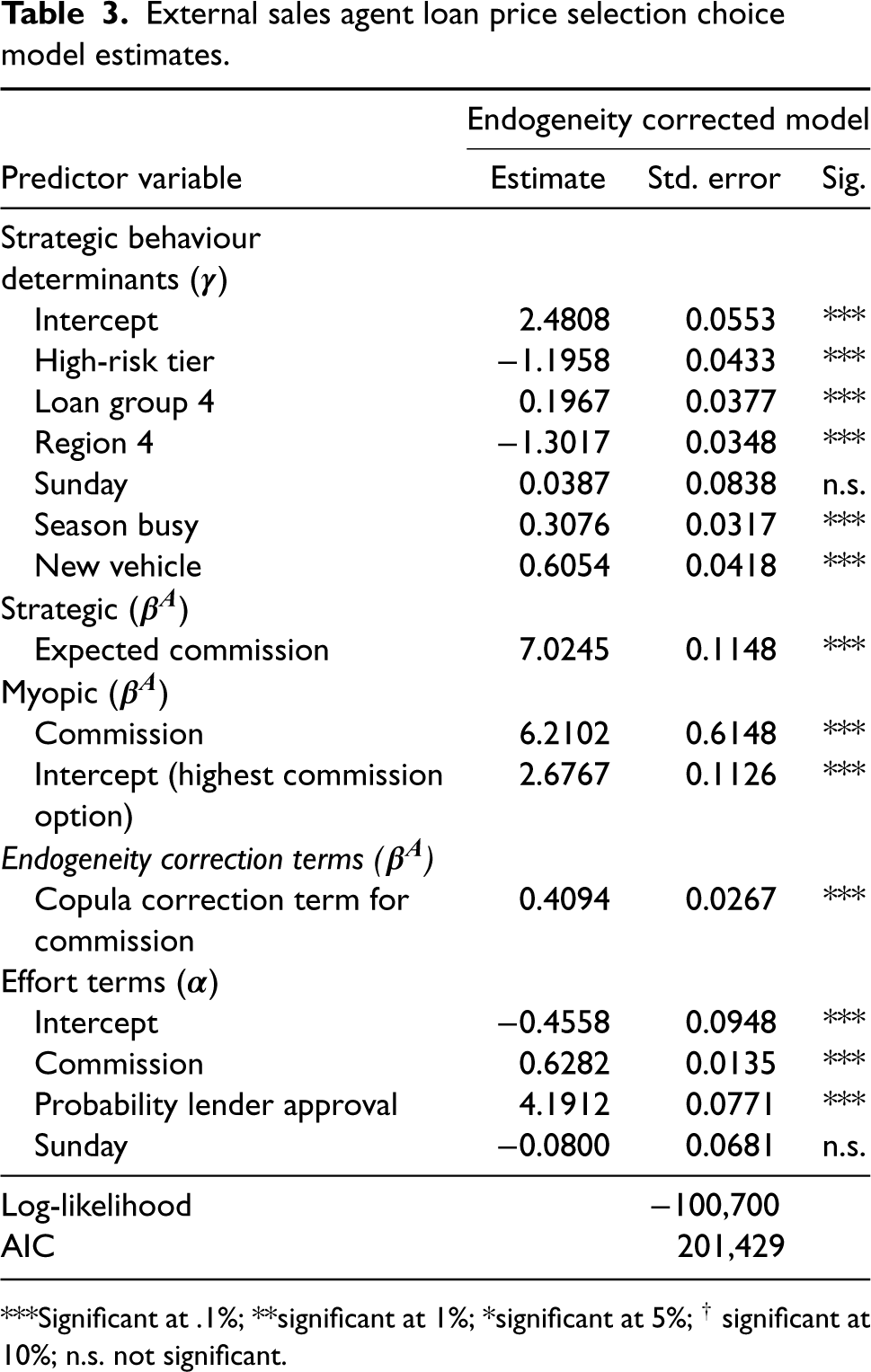

Before examining the factors that drive ESRs’ pricing sheet option selection, we begin with an assessment concerning endogeneity. The results in Table 3 indicate that commission is endogenous, as indicated by the positive and significant copula correction term for commission dollars (

External sales agent loan price selection choice model estimates.

External sales agent loan price selection choice model estimates.

***Significant at .1%; **significant at 1%; *significant at 5%; † significant at 10%; n.s. not significant.

The results suggest that ESRs are four times more likely to be strategic (80.88%) than myopic (19.12%) with respect to their pricing behaviour. Since we normalize the parameters for the myopic latent class (s = 2) to zero for identification of the model, the coefficients (

When ESRs are strategic, their choice is driven by the expected commission dollars. Specifically, the odds of selecting a pricing sheet option increase by 101.87% (

Lastly, as discussed in the ‘Model Development’ section, effort has a dual effect on ESR utility: a direct quadratic negative effect due to the increasing cost of effort and an indirect positive effect due to the impact of effort on the probability of the customer accepting loan offers. Hence, strategic management of effort becomes important in managing this trade-off. ESRs would, therefore, only be willing to take on the additional costs of exerting effort if they anticipate it to increase the probability of booking a loan; thus, when the payoff is large. The results confirm this. We find that ESRs exert more effort when the commission dollars (

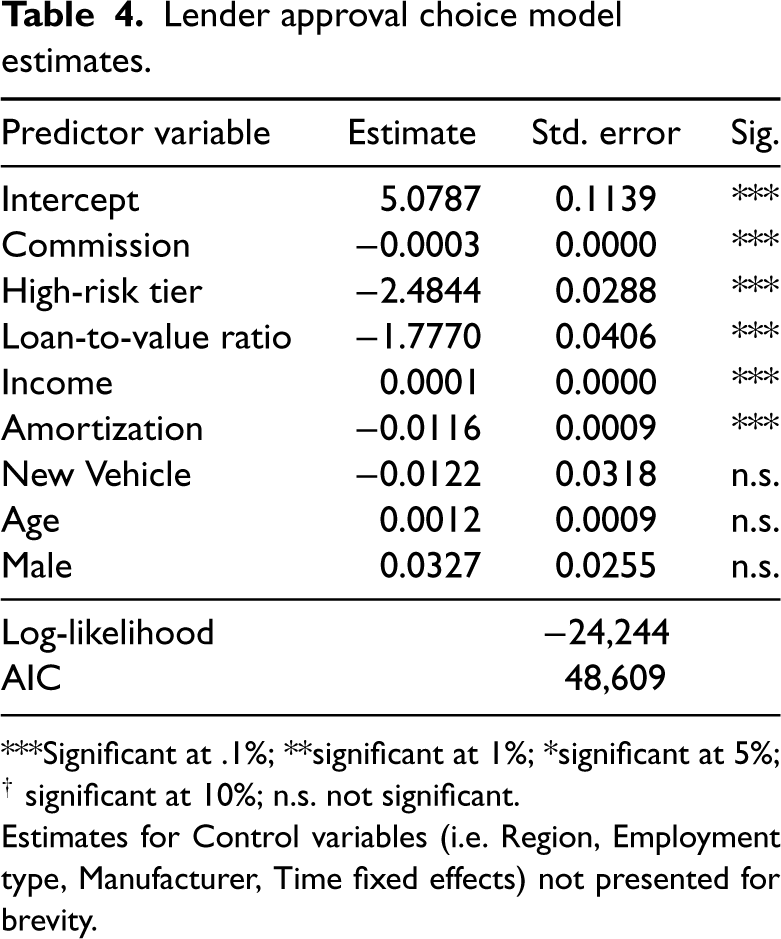

Lender approval choice model estimates.

***Significant at .1%; **significant at 1%; *significant at 5%; † significant at 10%; n.s. not significant.

Estimates for Control variables (i.e. Region, Employment type, Manufacturer, Time fixed effects) not presented for brevity.

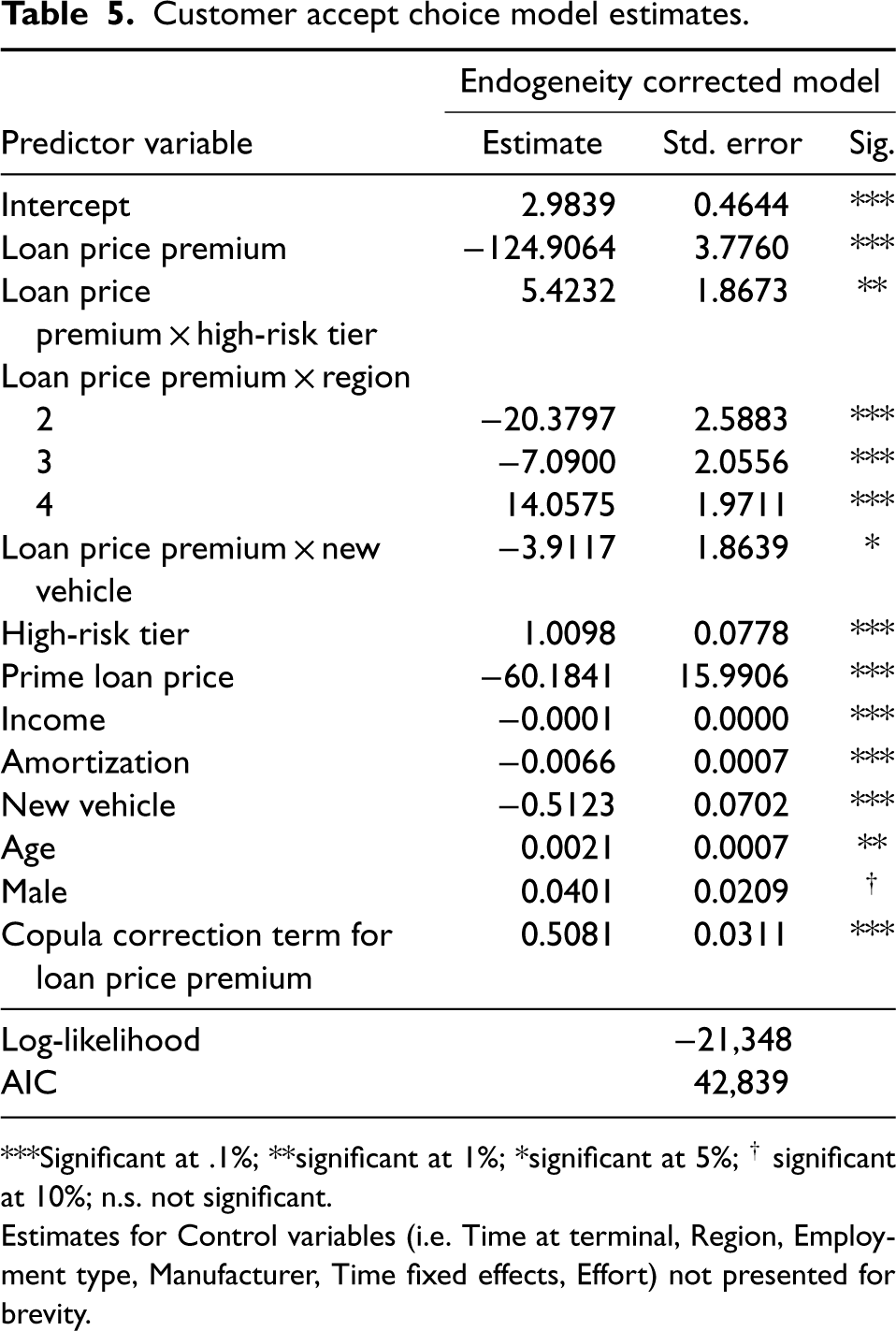

Customer accept choice model estimates.

***Significant at .1%; **significant at 1%; *significant at 5%; † significant at 10%; n.s. not significant.

Estimates for Control variables (i.e. Time at terminal, Region, Employment type, Manufacturer, Time fixed effects, Effort) not presented for brevity.

Moreover, since ESRs exert more effort towards customers that are more likely to be approved and given that lenders are more likely to approve low-risk customers that are also more price sensitive, as confirmed by the estimation results discussed in subsection 4.2.2 and 4.2.3 below, ESRs effort allocation serves to mitigate risk for the lender while also counteracting customers’ price sensitivity. Indeed, comparing the average effort exerted towards low-risk customers with that allocated towards high-risk customers confirms this idea: effort allocated to low-risk customers is 2.13x larger than that allocated towards high-risk customers.

Table 4 presents the estimates for the lender approval decision. The results highlight the important role of risk in several ways. First, the lender is more likely to approve loan applications for less risky customers. Specifically, the odds of approval for high (vs. low) risk customers are 91.66% (

In addition to these risk-related variables, the lender's approval decision is impacted by commission dollars paid to ESRs – a $100 increase decreases approval odds by 2.52% (

Customer Acceptance

In Table 5, we present the results for the customer choice model with endogeneity correction for price as it fits the data better than the no endogeneity model (AICs 42,839 vs. 43,033). Moreover, the copula correction term is positive and significant (

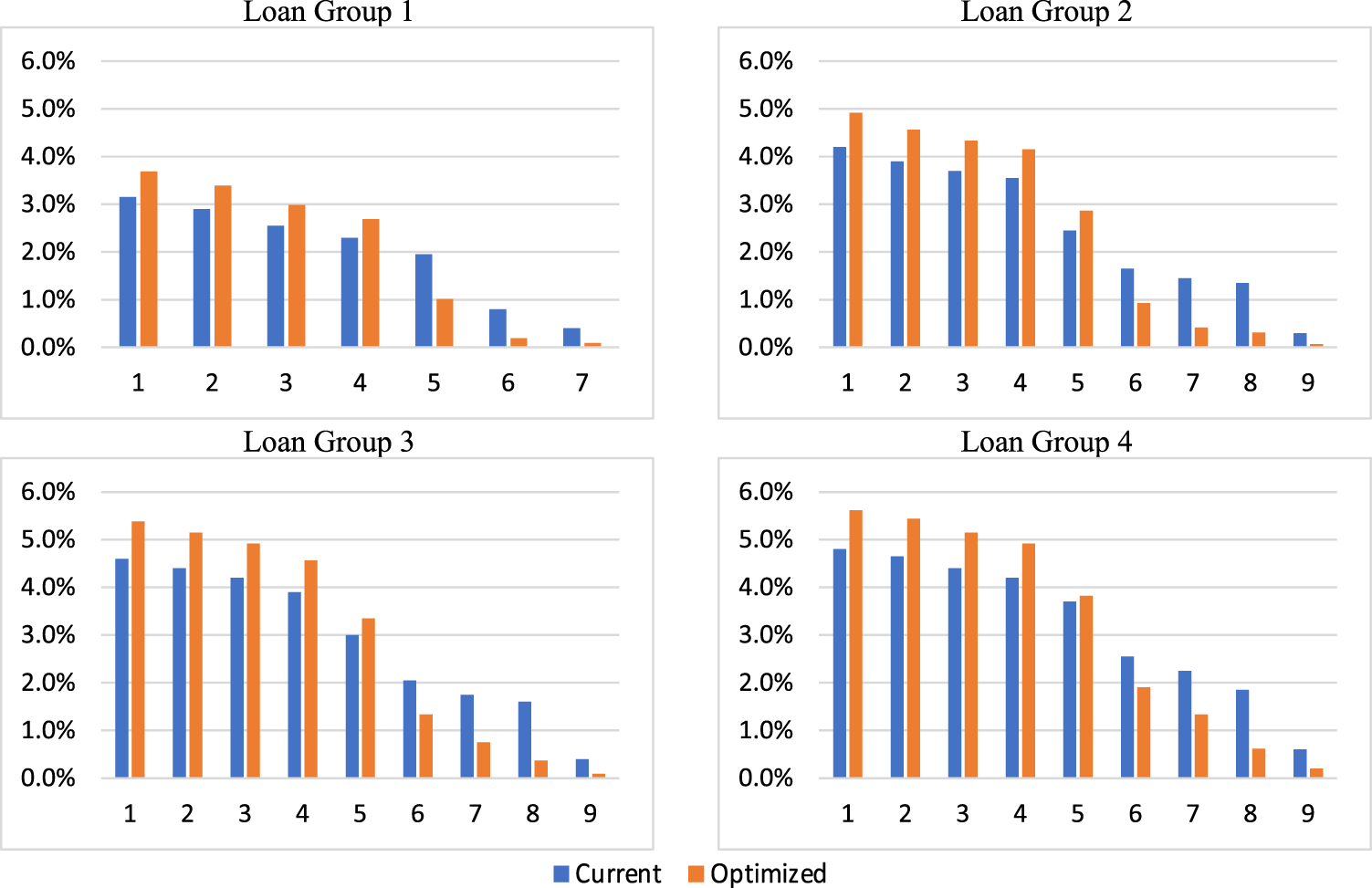

Optimized vs current commission rates by loan group. Note. Options are ordered from highest loan price/commission rate combination (option 1) to lowest (option 7 for loan group 1 and option 9 for loan groups 2–4).

Price, indeed, significantly decreases customer acceptance but this relationship exhibits a large degree of heterogeneity. At the reference level (i.e. low-risk customers, in region 1, and purchasing a used vehicle), a 1% increase in loan price premium decreases the odds of customer acceptance by 71.32% (

Several other factors that we control for are highly significant and play a role in customer acceptance. These controls include economic indicators (i.e. prime loan price), demographics, loan-specific characteristics, as well as region, risk tier, vehicle manufacturer, and month.

Given the estimation results, we optimize the commission rates on the lender's pricing sheet separately for each loan group. The results indicate that the optimal commission strategy is to exponentially increase the commission rate with each price increase (see Figure 3), and this is consistent across all loan groups. In other words, relative to the current commission strategy, the optimal strategy is to reduce the commission rates on pricing sheet options with lower customer loan prices and increase the commission rates on pricing sheet options with higher loan prices. In doing so, the lender can increase the expected net income after tax by 13.51%, 11.46%, 8.80%, and 5.14% for loan groups 1–4, respectively. This commission strategy increases the overall expected net income after tax by 7.95%. Thus, the optimization results confirm that, indeed, commissions can be used as a strategic tool by firms to increase the profitability of sales forces with pricing delegation. In other words, we provide evidence that commissions can be used to bridge the profitability gap between centralized pricing and pricing delegation.

Model Validation

To test the validity of the three-stage model, we assess the predictive performance for the customer, lender, and ESR decisions, both in sample and out of sample (see EC.5 in the E-Companion for further details). Beginning with the in-sample results, we find that the overall hit rate for the customer's decision to accept or reject a loan offer and the lender's decision to approve or reject a loan application is 68% and 77%, respectively, indicating strong performance. Moreover, the predicted ESR choice probabilities track the actual ESR choice probabilities well, predicting higher choice probabilities for the options selected most often (e.g. option 1 and option 6) and predicting lower choice probabilities for the options selected least often (e.g. options 2, 8, and 10). These in-sample results are consistent with the out-of-sample results from the hold-out analysis, thus providing further validation of the model.

Implications and Discussion

Implications for Customer Welfare

We have demonstrated that commissions are effective tools for firms to influence ESR behaviour and align ESR incentives with those of their own. Next, we investigate the implications of the previously analysed indirect-lending framework on the other key stakeholder, consumers, focusing on welfare implications. While extensive application of analytics and AI has been shown to increase efficiencies in firms’ competitiveness and overall business performance, questions regarding the legal and ethical issues relating to the broad application of these tools, particularly as it relates to fairness implications, have surfaced (De-Arteaga et al., 2022; Nkonde, 2019). How analytics and AI can damage fairness and open the gate to systemic discrimination has been documented across business areas, including pricing (Cohen, 2012; The Wall Street Journal, 2012), supply chain (Rea et al., 2021), organizational selection settings (Xu and Zhang, 2024), and healthcare operations (Obermeyer et al., 2019).

We set out to understand if customer segments along social axes such as gender, risk, and income are disproportionately affected and whether optimized commissions exacerbate any pre-existing inequities experienced by these traditionally marginalized groups in the context of our application (see Ozturk et al., 2024 for an example of gender bias within the auto loan sector). While race is an important variable to consider for algorithmic bias, it is not available in our data. Instead, we focus on gender, income, and risk profile to define segments, and we analyse the expected utility for these different customer segments in the current regime and compare it with those in the regime with the optimized pricing menu.

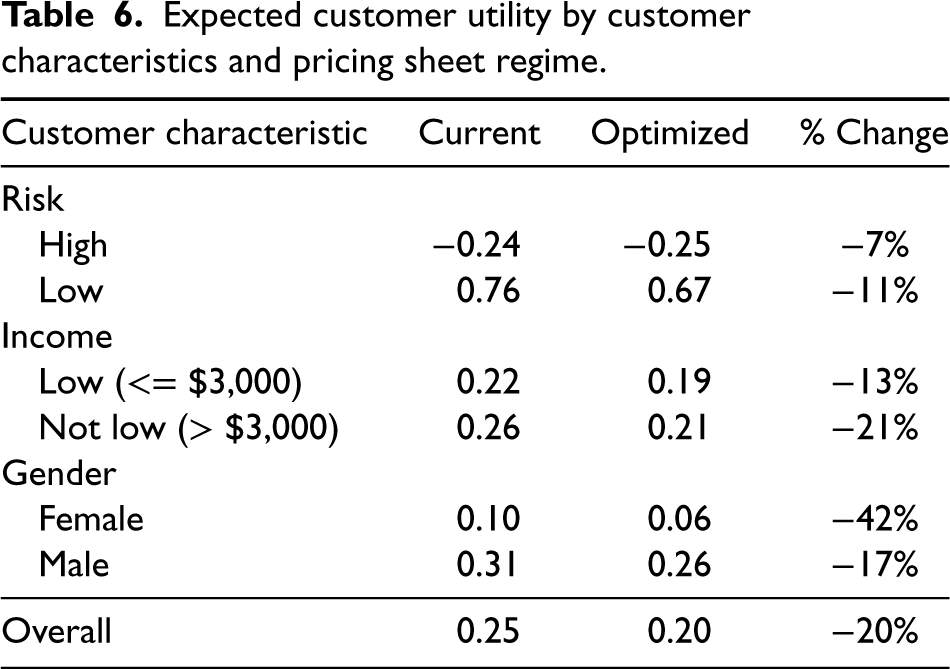

We present the results in Table 6. In the current regime, the average expected customer utility is lower for high-risk customers than low-risk customers (−0.24 vs. 0.76), for low-income customers than higher-income customers (0.22 vs. 0.26), and for females than males (0.10 vs. 0.31). In other words, the traditionally vulnerable groups are indeed at a disadvantage compared to the non-vulnerable.

Expected customer utility by customer characteristics and pricing sheet regime.

Expected customer utility by customer characteristics and pricing sheet regime.

How does optimizing the commissions in the pricing menus impact these inequities? The results suggest that inequities in the risk- and income-based groups are not intensified in the optimized regime. On the contrary, the non-marginalized groups take a more than proportional hit in their utility. Specifically, we find that expected customer utility decreases by 11% for low-risk customers compared to 7% for high-risk customers, and by 21% for higher-income customers compared to 13% for low-income customers. In other words, the extra profits obtained by the lender through optimization are largely extracted from the higher-income, lower-risk groups.

While this is encouraging, the results are the opposite for gender discrimination, where females incur a further negative bias in the optimal regime, with the decrease in their expected utility being roughly 3x more than that for males (−42% vs. −17%). This finding is important as it points out systemic unfairness being more deep-seated in the case of gender. This could be due to decision makers (ESRs in this case) making assumptions based on immediate visual cues, such as assuming that females are less able to judge whether a quoted price is fair as a result of having less knowledge about specific categories (such as car loans) than males (see for example, Ozturk et al., 2024), but also due to the intrinsic behavioural traits that females embody on average (e.g. not being overtly assertive) (Busse et al., 2017).

Addressing the injustices proactively and mitigating bias is as important as identifying the unfairness in the system, if not more. To this end, we use the estimates from our three-stage structural model and run counterfactual simulations to help financial institutions, regulators, and policymakers understand the equity-related outcomes of different policy choices. We use a range of different regimes with profit maximization at one end of the spectrum and minimizing social inequity concerns at the other. We accomplish the latter by introducing fairness-related constraints within the optimization algorithm for the firm. We consider fairness from an income, risk, and gender perspective, as race information is unavailable in the data.

We propose two distinct approaches for firms to enforce fairness within their optimization algorithm. In the first policy, firms, during optimization, set the minimum average utility for females and low-income segments equal to or greater than those for the same groups under the current regime. In the second policy, firms introduce a constraint that sets the negative percentage change in utility equal across comparative segments (i.e. males and females, low and high income). These constraints ensure that any decrease in utility experienced by the customer base due to optimization is entirely from the non-vulnerable group (first policy) or shared equally across vulnerable and non-vulnerable groups (second policy).

These two policy approaches prevent further utility degradation for the traditionally marginalized groups in the population, and help firms balance profit maximization goals with equity concerns. The results suggest that, even after accounting for fairness, the lender increases profits by 3.7% for policy 1 and 1.2% for policy 2. These profit lifts, albeit modest compared to the 7.9% from pure profit maximization without mitigating biases, signal to firms that they can be socially responsible and still accomplish a positive immediate impact on the bottom line and to the world that AI and analytics can serve to facilitate societal welfare as well as business efficiencies.

Conclusions

Sales forces are a critical element of firms’ marketing arsenal, with a roughly three times larger budget than advertising (Zoltners et al., 2008) and a higher ROI (Narayanan et al., 2004). What makes the sales force unique is its close proximity to customers, resulting in salespeople serving as the face of the product and providing them with a superior ability to assess customer-specific characteristics related to purchase, such as willingness to pay (Frenzen et al., 2010). It is probably due to these features that even though centralized pricing is the optimal strategy in terms of firm profitability (Phillips et al., 2015), salespeople are frequently given limited or, in some cases, full pricing authority (Hansen et al., 2008).

For firms, managing sales force price authority is particularly challenging in indirect channels, where they outsource the personal selling activities to brokers or representative firms to act as intermediaries between themselves and the customer. ESRs are common in industries where customers prefer a one-stop shop with access to multiple providers, such as financial lending, real estate, insurance, and travel. Because ESRs are not directly employed by the focal firm, they are more difficult to control. This highlights the importance of carefully designed incentive mechanisms to align an ESR's utility with that of the firm and bridge the profitability gap between price delegation and centralized pricing.

In this paper, this is precisely what we are interested in studying. Specifically, we investigate (1) the role of commissions as a potential tool to influence ESRs’ pricing decisions in the context of limited price authority and (2) the impact of optimized commissions on firm profitability in this context. We use indirect auto lending as our empirical setting and a dataset provided by a large North American financial institution to model the full indirect lending channel, accounting for the decisions of the three key stakeholders, including the ESR, firm (i.e. lender), and customer. While our focus is on the ESR's pricing decision, considering the intricacies within the entire ecosystem is crucial as the utilities of the ESR, firm, and customer are likely to have strong interdependencies.

We develop a structural model of ESRs’ price selection focusing on the impact of commissions. Using a latent class structure, we allow ESRs to be myopic (i.e. ESRs consider the commission dollars) or strategic (i.e. ESRs consider the – probabilistic – expected commission dollars accounting for potential actions by the firm and the customer) in their behaviour. We model ESR effort endogenously as a function of commission dollars, probability of lender approval, and day of the week. This enables us to understand whether ESRs strategically exert effort and whether firms can use commissions to influence ESRs’ effort. Finally, we allow for heterogeneity in customer price sensitivity, particularly with respect to risk tier, vehicle characteristics, and region.

The results contribute to the extant literature in five ways. First, we show that ESRs are four times more likely to be strategic in their pricing behaviour than myopic and that the likelihood of strategic behaviour is inversely proportional to customer risk. In other words, the riskier the customer, the more likely ESRs resort to heuristic decision-making, avoiding strategic calculations and effort. When ESRs use the myopic (i.e. heuristic) approach, they largely default to the pricing option with the highest commission rate, the odds of which are roughly 14 times higher than all other options combined. Second, ESRs strategically exert more effort when the commission dollars are high and for low-risk customers that are more likely to be approved but are also more price-sensitive. This means that ESRs help mitigate risk for the lenders and counteract customers’ price sensitivity with additional effort and that lenders can, indeed, use commissions as a critical lever to influence ESR effort allocation and increase loan bookings.

Third, from a strictly profit-seeking perspective, we show that the optimal strategy is to exponentially increase the commission rate with each price increase. This optimal commission strategy undoubtedly benefits the firm, akin to optimization research applied in other domains (e.g. Besanko et al., 2003; Luo et al., 2007), and the ESR in our context of indirect lending. With this finding, an interesting and important question emerges concerning the impact of the optimized commissions on the welfare of the customer.

Fourth, we investigate the customer welfare implications from a social justice lens and provide firms with AI and analytics-based tools to implement fairness in their data-driven decision-making. We analyse whether customer groups along the dimensions of gender, risk, and income class, which have been traditionally marginalized in society, suffer from inequities in the indirect-lending ecosystem, and whether optimized commissions further exacerbate any pre-existing injustices. We show that, while the vulnerable groups are disadvantaged in the current commission regime, the optimization does not intensify these biases.

We find females to be the exception, and that the inequities due to gender bias not only persist in the optimized regime, but also deepen. In fact, recent research in the auto loan market presents similar findings where females are charged significantly higher interest rate markups compared to males (Ozturk et al., 2024). These results collectively highlight the deep-rooted inequities that women face in their day-to-day lives and draw attention to the importance of finding ways to mitigate them. To this end, we propose two policies for firms to minimize social inequity, which helps them balance immediate profit-maximizing goals with responsible AI initiatives. These counterfactual policy simulations are valuable as they underscore the positive impact AI can have on social welfare while at the same time benefiting firms both with immediate bottom-line lifts and long-term reputational benefits due to equitable, socially responsible behaviour (see Yi et al., 2018 for an example illustrating how fairness seeking customers penalize firms due to perceived unfairness).

Finally, we provide empirical evidence that once optimized, commissions are effective tools for firms to bridge the profitability gap between centralized pricing and pricing delegation. This finding is crucial for firms that rely on intermediaries to access demand. Rather than taking away pricing authority from ESRs, which could result in ESRs offering customers products and services from competitors that give ESRs pricing authority, firms can influence ESRs’ pricing behaviour and effort through commissions to improve profitability without centralizing pricing.

We also note that, while we derive our results from the indirect auto lending context, the underlying approach and corresponding findings have broader application to other markets that involve customized pricing with discretion through external sales forces, such as real estate, consumer mortgages, insurance, travel, and tourism.

This paper has several limitations, most relating to data availability. The reality of the indirect lending industry is that the competitor data is only available at the aggregate level for each month, which forces lenders to make their pricing and commission decisions under this constraint. In our context, this is not a problem because the market shares of the top five banks are relatively stable during the observation period. However, we would like to encourage future empirical research to investigate the role of commissions on ESRs’ demand allocation decisions. Similarly, due to the lack of ESR identifiers in the data set, we do not investigate any salesperson-specific factors that might influence behaviour. This would be another interesting dimension that future research can focus on, as it would shed more light on strategic ESR behaviour, explicitly identifying how individual salesperson characteristics drive such behaviour. Finally, while we demonstrate that academics and practitioners can use AI and analytics-based approaches to minimize fairness-related biases and concerns, our data regarding customer characteristics is not all-encompassing. As such, we advise future research to examine the impact of algorithms on other segments that have been traditionally marginalized, for example, segments based on race, ethnicity, education, family size, occupation, and marital status.

Supplemental Material

sj-docx-1-pao-10.1177_10591478241259791 - Supplemental material for Optimizing Pricing Delegation to External Sales Forces via Commissions: An Empirical Investigation

Supplemental material, sj-docx-1-pao-10.1177_10591478241259791 for Optimizing Pricing Delegation to External Sales Forces via Commissions: An Empirical Investigation by Christopher Amaral, Ceren Kolsarici and Mikhail Nediak in Production and Operations Management

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

How to cite this article

Amaral C, Kolsarici C and Nediak M (2024) Optimizing Pricing Delegation to External Sales Forces via Commissions: An Empirical Investigation. Production and Operations Management 33(9): 1839–1854.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.