Abstract

If a firm afflicted by a disaster chooses to donate to disaster relief, how will this decision affect the firm's market value? From a self-protection perspective, diverting resources to support the public may jeopardize a firm's continuity and thereby reduce its value. Yet from a reputation-building perspective, supporting the public in need may enhance corporate reputation and thus increase firm value. In this study, we contrasted the two perspectives to develop a conceptual framework consisting of various competing hypotheses. We tested these hypotheses using data on Chinese firms’ donations to disaster relief during the first coronavirus disease 2019 outbreak. Our analysis shows that firms’ donations generally led to an increase in firm value. This was especially true for firms that were smaller or less profitable, firms that donated goods in addition to cash, and firms that donated before an increasing number of industry peers had done so. These results support the reputation-building perspective, suggesting that even when firms are afflicted by disaster exposure, their donations are still recognized as a value-adding investment. In contrast, donating a larger amount of cash and donating on an earlier day after the onset of the outbreak resulted in a lower firm value. These results align with the self-protection perspective, pointing to the need to consider resource preservation.

Keywords

Introduction

During times of a major disaster, corporate support for the public can ideally increase social welfare. However, if a firm is afflicted by a disaster but still chooses to donate to disaster relief, how will investors react? The organizational consequences of disaster exposure are attracting growing research attention as disasters such as fires, floods, hurricanes, earthquakes, and pandemics become more frequent due to growing population density, climate change, and cross-border mobility (Palliyaguru et al., 2014). This line of research mainly focuses on the loss of firm resources and negative financial consequences (Gregg et al., 2022; Williams et al., 2017). Firms’ disaster exposure is shown to cause volatile earnings, drains of cash reserves, and diminished flows of information and human resources (Gittell et al., 2006; Rao & Greve, 2018). This depletion of resources can cause investors (individuals, financial institutions, corporations, or public funds) to lower their valuation of an afflicted firm. The resulting loss in firm value further weakens the afflicted firm's financial position, putting pressure on managers to hold more resources in reserve as a means of self-protection (Huang et al., 2018; Oh & Oetzel, 2011; Pek et al., 2018).

In addition to being pressured to protect themselves, firms are also expected to support the public through donations to disaster relief, especially when a disaster has caused widespread and prolonged damage (Gautier & Pache, 2015). Although some disasters are isolated in space and time (e.g., fires or earthquakes), many others, such as the COVID-19 pandemic, have caused extensive disruptions (Craighead et al., 2020). When a major disaster strikes, people are in dire need of support and often expect firms to contribute. This poses a dilemma for afflicted firms: they must protect themselves while also meeting the social expectation of being philanthropic. As firms consider how to deal with this dilemma, they may seek to enhance their reputation through donating to disaster relief. A good reputation for being socially conscious helps build trusting relationships with stakeholders (Hillman & Keim, 2001; Wang et al., 2008), thereby reducing a firm's operating risk and improving its access to financial capital (Beninger & Francis, 2022). To the extent that investors recognize these reputational gains and react positively, donors can recover some of the value loss resulting from disaster exposure, easing their financial pressure (Madsen & Rodgers, 2015; Muller & Kraussl, 2011).

The above discussion reflects two distinct perspectives in the literature. In research on the organizational consequences of disaster exposure, the emphasis is placed on self-protection (Gregg et al., 2022). Some studies estimate that 4 out of 10 firms afflicted by a major disaster could not survive, and even survivors endured financial hardships (Duncan et al., 2011; Williams & Shepherd, 2016). To mitigate the risk of failure, afflicted firms should preserve their resources to buffer against liquidation risk (Dessaint & Matray, 2017; Kemper & Martin, 2010). On the other hand, corporate philanthropy literature highlights that firms’ donations can enhance their images (Gardberg & Fombrun, 2006; Jin & He, 2018) and elicit a favorable attitude from stakeholders (Koschate-Fischer et al., 2016). Most of these studies are based on philanthropy programs in ordinary times (Cha & Rajadhyaksha, 2021; Gautier & Pache, 2015). Although a few studies have examined donations to disaster relief (e.g., Hildebrand et al., 2017; Madsen & Rodgers, 2015; Patten, 2008), most donors in these studies are remote from the impact of a disaster, such as U.S. firms donating amid the 2004 Indian Ocean tsunami. In the scenario where donors are afflicted by a disaster, while they may reap reputational gains from donating, giving resources away also weakens their capacity to self-protect. It is unclear how investors would react to corporate donations in such a scenario.

The present study examines this under-researched scenario. We aim to answer the following research questions: (a) How do investors react when firms afflicted by a disaster announce their donations to disaster relief? (b) To what extent can the underlying mechanisms be characterized by the self-protection versus reputation-building perspectives? Investors’ reactions are captured by the change in a firm's market value attributable to the firm's announcement of its donation. This change in firm value, typically measured as the abnormal stock return attributable to an announcement event, has been widely applied in prior research to evaluate investors’ reactions to reputation-building programs (Sorescu et al., 2017). Following prior research such as Patten (2008), Muller and Kraussl (2011), and Madsen and Rodgers (2015), we use abnormal returns to capture investors’ reactions to corporate donations.

Our conceptual framework consists of two parts. As a baseline, we first examine the overall influence of corporate donations on firm value. While the self-protection perspective suggests that investors may see corporate donations as a risky resource diversion and react negatively, the reputation-building perspective suggests that investors may see donations as a value-adding investment and react positively. Therefore, the change in firm value following a donation announcement can reveal which perspective better describes investors’ reactions in general. Next, we identify an array of situational factors and examine their influence on the change in firm value attributable to a donation announcement. These factors, which delineate firm and donation characteristics, donation timing, and industry conditions, lead to competing hypotheses under the self-protection versus reputation-building perspectives. Testing such hypotheses allows us to assess the relative strength of the two perspectives under varying situations.

Our hypotheses were tested using data on Chinese firms’ donations to disaster relief during the first COVID-19 outbreak in early 2020. We first conducted an event study to assess the overall change in firm value resulting from corporate donations. Next, constructing a two-stage model that controlled for firms’ decisions to donate or not, we examined how the change in firm value resulting from corporate donations is influenced by different situational factors. Our analysis reveals that firms’ donations led to an increase in firm value in general, particularly for smaller and less profitable firms, for firms that donated goods in addition to cash, and for firms that donated before an increasing number of industry peers had done so. These results support the reputation-building perspective. In contrast, donating a larger amount of cash and donating on an earlier day after the onset of the outbreak resulted in a lower firm value. These results are in line with the self-protection perspective.

Our study contributes to research on the organizational consequences of disaster exposure. This body of work focuses on the negative financial consequences caused by disaster exposure and emphasizes resource preservation (Gregg et al., 2022; Williams et al., 2017). We show that corporate donations in times of disaster can be recognized as a value-adding investment, contributing to the recovery of firm value and the relief from financial pressure. This is especially true when donations send a clear signal of a firm's philanthropic nature at an expense that investors find reasonable. Our study also adds to the corporate philanthropy literature, which highlights reputational benefits but has been limited by a focus on philanthropic programs in ordinary times (Cha & Rajadhyaksha, 2021; Gautier & Pache, 2015). Our finding suggests that even in our challenging setting where donors are themselves afflicted by a major disaster, investors still recognize the reputational gains of donations to disaster relief. Such a finding extends the reputation-building perspective to a wider range of contexts.

Our findings provide managers with practical guidance on how investors react when firms donate to disaster relief. For instance, facing tighter resource constraints, managers of smaller or less profitable firms may feel tempted to focus on resource preservation in times of disaster. However, our findings suggest that donations from these firms may elicit more positive reactions from investors, perhaps because investors expect these firms to reap more reputational gains from contributing to disaster relief. Hence, managers of smaller or less profitable firms should strive for a balance between preservation and giving, instead of concentrating only on the former. At a broader level, our findings reject the restricted view that donations to disaster relief represent an unwelcome resource diversion and provide evidence for the potential gains from such donations. Consideration of potential gains encourages managers to be more open to supporting relief operations and funding humanitarian organizations during times of a major disaster.

Conceptual Framework and Hypotheses Development

Literature Background and the General Effect of Donation

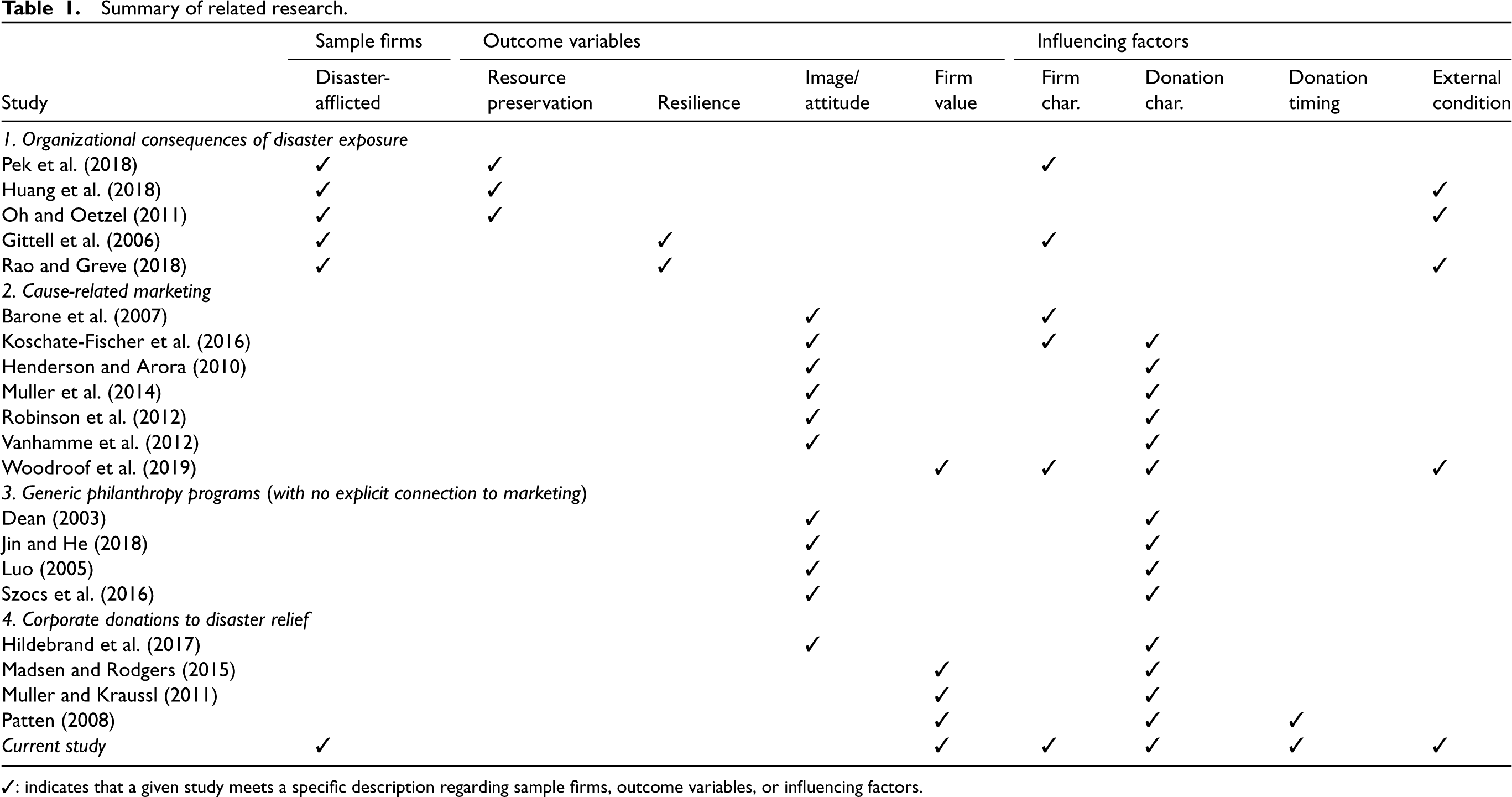

In this section, we first draw from the literature to investigate how a firm's donation to disaster relief will affect its market value in general. Table 1 provides an overview of the four streams of research that we draw from. By leveraging existing research, we develop two distinct theoretical perspectives with opposite implications. Then, the following sections explore a range of situational factors that can help reveal the relative strength of these two perspectives.

Summary of related research.

Summary of related research.

✓: indicates that a given study meets a specific description regarding sample firms, outcome variables, or influencing factors.

First, in the disaster management literature, there is a growing body of research that examines the organizational consequences of disaster exposure. Most studies in this research stream emphasize the depletion of financial, informational, and human resources caused by disaster exposure, which disrupts firm operations and may even result in organizational failure (Gregg et al., 2022; Williams et al., 2017). These studies focus on resource preservation and organizational resilience as the outcome variables. To mitigate the risk of failure, firms are found to keep more resources in reserve and reduce investments (Huang et al., 2018; Oh & Oetzel, 2011), especially when their capabilities are weaker (Pek et al., 2018). Keeping adequate reserves is shown to reduce failure risk and facilitate subsequent investments in recovery, contributing to firms’ resilience (Gittell et al., 2006; Rao & Greve, 2018).

Extending this first research stream, we present a self-protection perspective to theorize about the negative consequences of disaster-afflicted firms donating to disaster relief. This perspective highlights resource preservation. When exposed to a disaster, firms are expected to prioritize resource preservation to ensure their own continuity. By preserving resources, firms can better adapt to the strains imposed by adversities and uncertainties (Corbacioglu & Kapucu, 2006; Dessaint & Matray, 2017). In contrast, donating resources to the public appears questionable, because such behavior can damage a firm's ability to survive and recover (Kemper & Martin, 2010). Investors may even interpret corporate donations as a bad signal that managers pursue their own social and political agendas at the expense of shareholders’ interest in firm continuity (Kruger, 2015). Such a bad signal would prompt investors to sell and bid stock prices down. This line of reasoning predicts that investors will respond negatively when a disaster-afflicted firm donates to disaster relief, leading to a decline in firm value.

H1a: (self-protection perspective): A firm's donation to disaster relief results in a decrease in its market value.

The second and third streams of research concern corporate philanthropy in ordinary times. Both streams of research examine the idea that corporate philanthropy can enhance a firm's reputation and thereby increase its value (Cha & Rajadhyaksha, 2021; Gautier & Pache, 2015). However, they differ in the types of philanthropic programs under study. The second stream focuses on cause-related marketing, where companies leverage specific social causes to promote products or services and generate short-term economic benefits (Barone et al., 2007). In contrast, the third stream examines generic philanthropy programs with no explicit connection to marketing. These generic programs often involve a long-term commitment to broader social concerns. Therefore, the two types of philanthropy programs may elicit different reactions from customers, investors, and other stakeholders. Empirical evidence supports the idea that corporate philanthropy can contribute to reputation-building, showing that cause-related and generic philanthropy programs improve a company's perceived image (Dean, 2003; Henderson & Arora, 2010; Jin & He, 2018; Luo, 2005; Muller et al., 2014) and increase customers’ willingness to support the company (Barone et al., 2007; Koschate-Fischer et al., 2016; Robinson et al., 2012; Szocs et al., 2016). As most studies use perceived corporate image or customers’ attitude as the outcome variable, there has been limited research on the impact of corporate philanthropy on firm value. One exception is Woodroof et al. (2019), which found that investors respond negatively to cause-related marketing in ordinary times, leading to a decrease in firm value.

The fourth stream of research, which examines firms’ donations to disaster relief, is also a part of the broader literature on corporate philanthropy. Unlike the second and third streams, which focus on customers’ perception, the fourth stream mainly focuses on the change in firm value as the outcome variable. In contrast to Woodroof et al. (2019), studies in the fourth stream report a positive effect of donations to disaster relief on firm value, suggesting that investors appreciate this specific type of philanthropy programs (Madsen & Rodgers, 2015; Muller & Kraussl, 2011; Patten, 2008). However, since most donors in these studies are remote from the impact of a disaster, such as firms donating to foreign or distant disasters, it is unclear how investors will react in settings where donors have been afflicted by a disaster.

Extending the second to fourth streams of research, we develop a reputation-building perspective to theorize about the positive consequences of disaster-afflicted firms donating to disaster relief. This perspective highlights the reputational gains from donating to the public in need. A good reputation of being socially conscious helps build trusting relationships with buyers, suppliers, employees, and government agencies (Hillman & Keim, 2001; Wang et al., 2008). The support of these stakeholders provides important social, human, and political capitals that a firm can leverage to sustain itself during times of crisis (Beninger & Francis, 2022). Having a stronger ability to sustain oneself reduces a firm's operating risk and further improves its access to financial capital. If investors recognize these benefits, they may see corporate donations as a value-adding investment. Moreover, in accordance with the signaling theory (Connelly et al., 2011), corporate donations may reveal that a firm's decision makers perceive the company's future to be good enough to spend discretionary resources on unrelated third parties (Shapira, 2012). Accordingly, investors are expected to react positively when a disaster-afflicted firm donates to disaster relief, leading to an increase in firm value.

H1b: (reputation-building perspective): A firm's donation to disaster relief results in an increase in its market value.

Beyond the general argument discussed above, we next investigate how the change in firm value resulting from donations may vary based on different situational factors. Figure A1 in the E-Companion provides an overview of the factors being examined in this paper. These factors have opposite implications under the self-protection versus reputation-building perspectives, resulting in competing hypotheses. Through testing such hypotheses, we can assess the relative strength of the two perspectives under varying situations.

Firm Size

Firms that donate to crisis relief differ in their size. From a self-protection perspective, firm size affects a firm's risk of failure and its need for resource preservation. Smaller firms are more constrained in the resources at their disposal and are therefore less able to withstand the shocks caused by disaster exposure. Therefore, these firms have a greater need for resource preservation (Huang et al., 2018; Pek et al., 2018). If smaller firms donate their limited resources to the public regardless, investors may view the donation decision as a bad signal that managers prioritize their own social and political agendas over securing the firm's continuity (Kruger, 2015). In contrast, because larger firms are more resourceful, they are less likely to fail despite ongoing disaster, and they have a lower need to preserve resources. Thus, larger firms’ donations to disaster relief may be less questioned by investors. This perspective predicts a positive effect of firm size on the change in firm value resulting from a firm's donation.

H2a: (self-protection perspective): Firm size has a positive effect on the change in firm value resulting from a firm's donation to disaster relief.

From a reputation-building perspective, firm size can influence how people perceive a donor's intention. Research has shown that a donor can only develop a good reputation when its giving is interpreted as motivated by social considerations (Barasch et al., 2014). The interpretation of a giver's intention often exerts a greater influence on the appreciation granted to the giver than the actual benefit of the giving (Gershon & Cryder, 2018; Newman & Cain, 2014). Intention interpretation is determined by the perceived level of effort. Relative to larger firms, smaller firms have more limited resources, and thus donating to the public may be perceived as more demanding. Because giving that is perceived as more demanding is associated with more favorable attribution of intention (Heyman & Ariely, 2004; Morales, 2005), when smaller firms donate, the public may view their contributions as more salient and commendable, enhancing reputation-building. When investors recognize such reputational gains, they may also view smaller firms’ donations as a good signal that the firms can still afford giving to the public despite being afflicted by the disaster (Muller & Kraussl, 2011). In contrast, because larger firms are more resourceful, their donations to disaster relief may be perceived as less demanding and, therefore, less appreciated. This perspective predicts a negative effect of firm size.

H2b: (reputation-building perspective): Firm size has a negative effect on the change in firm value resulting from a firm's donation to disaster relief.

Firm Profitability

The profitability of a donating firm is expected to have a similar influence as firm size. More profitable firms can accumulate more resource reserves, which allows them to better protect themselves. Even if they are afflicted by a disaster, they face a smaller risk of failure and have a lower need for resource preservation. When they donate to disaster relief, their decisions may be less questioned by investors since their continuity is less of a concern. On the other hand, less profitable firms face a greater risk of failure and a greater need for resource preservation (Huang et al., 2018; Pek et al., 2018). If they donate regardless, investors may view their donations as a bad signal that managers act against shareholders’ interest in firm continuity (Kruger, 2015). This perspective predicts a positive effect of firm profitability on the change in firm value resulting from a firm's donation.

H3a: (self-protection perspective): Firm profitability has a positive effect on the change in firm value resulting from a firm's donation to disaster relief.

From a reputation-building perspective, donating to disaster relief may be seen as less demanding for more profitable firms. As a result, their donations may be taken for granted and receive limited appreciation. In contrast, firms with a lower profitability are more resource-constrained. If these firms donate, the public may find their donations more commendable (Heyman & Ariely, 2004; Morales, 2005) and investors may view their donations as a good signal that they can still afford to give to the public (Muller & Kraussl, 2011). This perspective predicts a negative effect on firm profitability.

H3b: (reputation-building perspective): Firm profitability has a negative effect on the change in firm value resulting from a firm's donation to disaster relief.

Donation Characteristics

Amount of Cash Donation

In our empirical setting of the COVID-19 pandemic, cash donations were the primary way that corporate donors contributed to emergency response, while some firms also donated goods such as food, medicine, and equipment. Cash donations are typically preferred due to their flexibility (Goldschmidt & Kumar, 2016). In contrast, goods donations are often unsolicited and redundant, complicating relief operations (Kovacs & Spens, 2007).

When firms donate cash, the amount of cash they donate may vary. From a self-protection perspective, donating a larger amount of cash implies giving more financial resources to the public, which may leave donors vulnerable to liquidation risk (Dessaint & Matray, 2017) and hinder investment in their own recovery (Kemper & Martin, 2010). This is expected to elicit negative reactions from investors. In contrast, donating a smaller amount of cash is less likely to be questioned by investors. This perspective predicts a negative effect of the amount of cash donation on the change in firm value resulting from a firm's donation.

H4a: (self-protection perspective): Amount of cash donation has a negative effect on the change in firm value resulting from a firm's donation to disaster relief.

From a reputation-building perspective, the amount of cash donation can influence how donors’ motivations are interpreted. Previous research has shown that people are more likely to view a donor's intention positively when the donation amount is larger, but tend to perceive the donor as self-oriented when the donation amount is smaller (Folse et al., 2010; Muller et al., 2014). The belief that a larger amount of cash donation reflects a donor's benevolent nature can contribute to reputation-building. Accordingly, investors may interpret such a donation as a good signal that the donor is resilient enough to invest in reputation-building (Muller & Kraussl, 2011). In contrast, a smaller amount of cash donation may be seen as perfunctory, hindering the development of a good reputation. This perspective predicts a positive effect on the amount of cash donation.

H4b: (reputation-building perspective): Amount of cash donation has a positive effect on the change in firm value resulting from a firm's donation to disaster relief.

Goods Donation

Although cash is often the primary and preferred type of donation, some firms may donate goods in addition to cash. From a self-protection perspective, donating goods consumes extra firm resources since sourcing and distributing goods can become particularly difficult and costly when a disaster has disrupted the supply chain (Craighead et al., 2020; Kleindorfer & Saad, 2005). Investors may view extra resource expenses on donating goods as a bad signal that managers prioritize their own social and political agenda over securing firm continuity (Bhagwat et al., 2020). In contrast, if a firm focuses on donating cash to avoid extra expenses on sourcing and distributing goods, investors may question the firm's donation less. This perspective predicts a negative effect of goods donation on the change in firm value resulting from a firm's donation.

H5a: (self-protection perspective): Goods donation has a negative effect on the change in firm value resulting from a firm's donation to disaster relief.

In theory, donating goods in addition to cash may affect a firm's reputation in two possible ways. Donating both goods and cash is likely to attract more public attention than donating cash alone, leading to higher visibility. On the one hand, higher visibility can facilitate reputation-building if people recognize the difficulties of sourcing and distributing goods in times of disaster, and interpret a firm's involvement in such challenges as demonstrating the donor's genuine social consideration (Barasch et al., 2014; Heyman & Ariely, 2004; Morales, 2005). On the other hand, however, goods donations may be unhelpful, while handling and disposing of unused goods can disrupt relief operations (Kovacs & Spens, 2007; Perry, 2007). If people are concerned about the troubles caused by unused goods donations, they may blame a donor for being thoughtless, causing reputation damage (Turrini et al., 2020).

In the settings that this study focuses on, reputation-damage is less likely to occur. In times of a major disaster, uncertainties on what constitutes helpful donations are substantial, but people are also eager to secure any help they can get. Prior research has found that when facing uncertainties caused by uncontrollable events, people tend to evaluate the donors of goods more favorably (Hildebrand et al., 2017). For example, the first COVID-19 outbreak in China caused substantial uncertainties regarding public health. As a result, many medical supplies donated during the outbreak eventually expired and had to be disposed of. Nevertheless, donors of medical supplies were still appreciated instead of being blamed for making a poor forecast, since unused medical supplies still served as insurance against uncertainties. As discussed before, a giver may be appreciated regardless of the actual benefits of their giving if the giver is thought to be motivated by social considerations (Barasch et al., 2014; Newman & Cain, 2014). Firms that make extra effort to donate goods in addition to cash can demonstrate their social considerations more strongly and are more likely to win public appreciation (Heyman & Ariely, 2004; Morales, 2005). When recognizing the reputational gains, investors may interpret donating goods as a good signal that a donating firm is resilient enough to engage in the extra resource expenses required (Muller & Kraussl, 2011). This line of reasoning predicts a positive effect of goods donation.

H5b: (reputation-building perspective): Goods donation has a positive effect on the change in firm value resulting from a firm's donation to disaster relief.

Donation Timing

Donation Day

When firms donate to disaster relief, some may donate quickly after the onset of a disaster, while others may donate later. From a self-protection perspective, firms are at a higher risk of failure and have a greater need to preserve resources when disruptions and uncertainties are most substantial in the earlier days after the onset (Craighead et al., 2020; Gregg et al., 2022). If a firm chooses to donate earlier, investors may view such behavior as a bad signal that managers consider their firm's self-protection as secondary (Kruger, 2015). As uncertainties gradually decrease over time, disruptions are increasingly contained by disaster control, and the risk of failure subsides. Hence, donating later is less risky and may appear more acceptable to investors. We refer to the number of days that have passed from the start of a disaster until a firm donates as “donation day.” A larger number indicates that a firm donates at a later date after the onset. Accordingly, the self-protection perspective predicts a positive effect of donation day on the change in firm value resulting from the firm's donation.

H6a: (self-protection perspective): Donation day has a positive effect on the change in firm value resulting from a firm's donation to disaster relief.

From a reputation-building perspective, people are most in need of support shortly after the onset of a disaster. If firms donate earlier, their contributions are more likely to be viewed as a sincere display of care for social well-being (Patten, 2008). This benevolent interpretation facilitates the development of a good reputation (Barasch et al., 2014). Investors may also interpret earlier donations as a good signal that a donor is resilient enough to invest quickly in reputation-building (Muller & Kraussl, 2011). On the contrary, if firms donate only after disruptions have been increasingly contained, their donations may be less appreciated. Later donations may even be viewed as a perfunctory act designed to ingratiate with the public (Gershon & Cryder, 2018). This perspective predicts a negative effect of donation day.

H6b: (reputation-building perspective): Donation day has a negative effect on the change in firm value resulting from a firm's donation to disaster relief.

Industry Condition

Number of Prior Donors

When firms donate to disaster relief, some may donate only after an increasing number of industry peers have done so. From a self-protection perspective, the number of prior donors in the same industry can affect investors’ concern that a firm's donation may be a signal of agency problem. When relatively fewer industry peers have donated, a firm's donation may appear illegitimate for being at odds with what is common (Brower & Dacin, 2020). In this situation, investors are more inclined to view a firm's donation as a bad signal that managers act against shareholders’ interest in firm continuity. In contrast, the more industry peers have donated, the higher the legitimacy of a firm's decision to follow and donate. Additionally, since prior donors can create peer pressure, if a firm chooses to follow suit, its donation is less likely to be viewed by investors as a signal of agency problem (Hsieh et al., 2015). This perspective predicts a positive effect of the number of prior donors on the change in firm value resulting from a firm's donation.

H7a: (self-protection perspective): Number of prior donors has a positive effect on the change in firm value resulting from a firm's donation to disaster relief.

From a reputation-building perspective, the number of prior donors in the same industry can affect how stakeholders interpret a donor's intention. If a firm donates when relatively fewer industry peers have done so, its pioneering contribution is more likely to be identified and appreciated. The perceived prominence of such a contribution encourages stakeholders to view the donation as a reflection of the donor's social considerations (Heyman & Ariely, 2004; Morales, 2005). This favorable view facilitates the development of a good reputation (Barasch et al., 2014), and investors may react more positively with an expectation of reputational gains. In contrast, if a firm donates after an increasing number of industry peers have already done so, its donation may appear redundant and insignificant (Patten, 2008). Such a donation may even be interpreted as a reluctant act driven by peer pressure rather than a genuine consideration of the public (Brower & Dacin, 2020; Gershon & Cryder, 2018), hampering reputation-building. This perspective predicts a negative effect on the number of prior donors.

H7b: (reputation-building perspective): Number of prior donors has a negative effect on the change in firm value resulting from a firm's donation to disaster relief.

Empirical Analysis

Data

We tested our hypotheses in the empirical setting of COVID-19 pandemic in China. Our focus was on the first COVID-19 outbreak in early 2020, starting from January 20, the day when the National Health Commission publicly announced that the new coronavirus could be transmitted from person-to-person. A few days later, on January 23, the Chinese government locked down the city of Wuhan, the epicenter of the first outbreak. We traced the development up until April 7. By then, the Chinese government had lifted the quarantine in all cities throughout China. When the first COVID-19 outbreak occurred in China, it was unprecedented. Firms were under pressure to protect themselves, while people were also in dire need of help and would greatly appreciate corporate donations. Due to this tension between self-protection and reputation-building, our empirical setting represents a suitable context to examine the differing implications of the two perspectives. We sampled the 3875 firms listed on either the Shanghai Exchange or the Shenzhen Exchange by the end of 2019. In China's stock market, the majority of investors are local. Foreign investors hold only 3% of the market, even though the legal maximum for foreign ownership of a publicly traded company stands at 30% (Carpenter et al., 2021). Our sample firms vary in the number of employees, ranging from fewer than 100 to nearly 470,000.

Since the beginning of the pandemic, the China Securities Regulatory Commission (CSRC) has regularly posted information on corporate donations for disaster relief on its website. The CSRC collected data through corporate self-reports, announcements, and press releases. We used the data recorded by the CSRC as our primary data source. To double-check, we further searched corporate websites and online news, through which we identified five additional donation events not recorded by the CSRC. Because the CSRC's census date was March 24, a few firms that donated after the census date were not recorded. Since such a discrepancy was minimal, we concluded that information from the CSRC is reliable. We included the five additional donation events in our data, but their inclusion or exclusion had nearly no impact on the results. According to the data, 1190 (30.7%) listed companies in China had donated to support relief operations. Records of most donations were accompanied by text descriptions about how much cash a firm donated and whether the firm also donated goods. On average, firms donated CNY 188,000 (USD 26,320) in cash, with a median of CNY 389,000 (USD 54,460) and a maximum of CNY 200 million (USD 28 million). In early 2020, 1 CNY was approximately equal to 0.14 USD. Of these donors, about 32% donated goods in addition to cash. Donated goods typically included medical supplies, such as masks, protective gloves and clothes, disinfectants, and ambulatory supplies. Some firms also donated food and hygiene items. We could not find systematic and reliable data on the monetary value of donated goods.

We identified an event day as the day on which a firm announced its donation. An announcement informed investors about a firm's decision to donate. Investors included all parties trading on the Shanghai Exchange or the Shenzhen Exchange, such as individuals, financial institutions, corporations, or public funds. We observed that most donations were announced shortly before or after a donation was actually made. A donation's announcement and implementation typically occurred on the same day or just a few days apart. In less than 1% of cases where a firm made multiple donations, we focused on the announcement of its earliest donation. We were able to identify the exact donation day for 1119 donating firms (94.0%). Among them, 472 (45.2%) donated in late January, 446 (42.7%) donated in the first 2 weeks of February, 105 (10.1%) donated in the last two weeks of February, and the remaining firms donated even later. Although we traced the development up until April 7, we concluded our observation period on April 1 since no donations were reported after that day. On average, firms announced their donations on Day 16 from the onset of the outbreak, with the minimum being Day 1 and the maximum being Day 64.

We collected data on the characteristics and industry classification of firms from the Shanghai Exchange, the Shenzhen Exchange, and a corporate database administered by Phonix New Media. Using information on the donation day and each firm's industry classification, we calculated the number of industry peers who donated before a focal firm. On average, by the time a focal firm announced its donation, 3.52 industry peers had already donated. We also identified the recipients of donations. Federated charities were the recipients of 19.6% of the donations, followed by the Red Cross at 16.7%, hospitals at 13.0%, and government agencies at 4.7%. 24.8% of donations were made to multiple types of recipients. The remaining donations did not specify recipients. Finally, we also collected data on the number of daily COVID-19 fatalities from China's National Health Commission, Google trend metrics of the keyword search for “coronavirus,” and the media coverage of each firm's donation as identified by major search engines in China (Baidu, Bing). We excluded observations with missing values from further analysis, reducing our sample size from 3875 to 3441 firms.

Empirical Strategy

We aimed to address two research questions: (a) How do investors react when firms afflicted by a disaster announce their donations to disaster relief? (b) To what extent can the underlying mechanisms be characterized by the self-protection versus reputation-building perspectives? We captured investors’ reactions by observing the change in a firm's market value following its donation. Our empirical strategy was based on the assumption that if investors expected firms to prioritize self-protection, they should respond negatively since a firm's donation reduces its resource reserve. Conversely, if investors expected firms to prioritize reputation-building, they should respond positively since a firm's donation enhances its reputation. Furthermore, depending on whether a situational factor caused investors to focus more on self-protection or reputation-building, that factor should exert either a negative or positive effect on the change in firm value resulting from a firm's donation.

Our empirical analysis comprised two parts. First, we evaluated the overall relationship between a firm's donation and the corresponding change in firm value using the event study method. We measured the change in firm value using the cumulative abnormal return (CAR) following a donation announcement. Second, we used a two-stage regression model to investigate how factors such as firm and donation characteristics, donation timing, and industry conditions influenced the CAR attributable to a donation announcement. Since these factors were expected to have opposite effects under the two theoretical perspectives, examining their impact on CAR could shed further light on the dominant perspective. Figure A2 in the E-Companion provides a visual illustration of our procedures.

Event Study: Relationship Between a Firm's Donation and Change in Firm Value in General

We used the event study method to evaluate the impact of a firm's donation on its market value. This method calculates the abnormal stock return that investors could obtain from an event that provides new publicly available information. According to the efficient market hypothesis, stock prices incorporate all publicly available information. Therefore, an abnormal stock return reflects the effect of newly available public information (Sorescu et al., 2017). To calculate the abnormal return, we subtracted the expected normal return in the absence of an event from the actual return. We utilized the benchmark asset pricing model to forecast the expected normal return.

In this study, events that delivered new information were firms’ announcements of their donations. Let tie be firm i's donation event day, which is the day when firm i's donation was publicly announced. We defined dpre and dpost as the number of trading days before and after tie, respectively. The event window was then defined as [tie - dpre, tie + dpost], during which we calculated the CAR of firm i's stock, denoted as CARi. We computed CARi through the following steps.

Step 1: Computing the actual returns. The actual return of the firm i's stock on day t is:

Step 2: Computing the expected normal return. Following MacKinlay (1997), we estimated the expected normal return using the following model:

When estimating parameters in equation (3), we had to decide when the estimation period should end and how long the period should be. Sorescu et al. (2017) suggest a minimum length of 100 days to avoid being overly influenced by outliers. Beyond this threshold, the length of the estimation period has minimal impact. Therefore, we followed Woodroof et al. (2019) and chose an estimation period ranging from 255 to 46 trading days before the event day, covering 210 trading days. We used ordinary least squares regression to estimate equation (3) for each firm i. From the regression, we obtained the estimates of

After assessing the overall impact of donation events on the average CAR, we next investigated how a set of situational factors would influence CAR i resulting from a donation announcement. This analysis is only applicable to firms that have donated to disaster relief, raising concern about selection bias. To address this concern, we utilized a two-stage regression model. In the first stage, we modeled a firm's decision to donate on day t as a binary choice. In the second stage, we examined how situational factors would influence CAR i . Below, we will first illustrate the second stage, where CAR i conditional on firm i having chosen to donate was modeled as:

where di is a binary indicator that takes the value of 1 if firm i announced its donation on a day τi, and takes the value of 0 otherwise. εi denotes the error term. Conditional on di = 1, CAR i is determined by an array of explanatory variables as well as control variables denoted by Ci.

The six explanatory variables in the above equation were operationalized as follows. Firm size was measured in terms of a firm's assets (in CNY ten billion). Firm profitability was measured as a firm's net income after taxes divided by its assets. Amount of cash donation was measured as the total amount of cash donated by a firm (in CNY thousand). To reduce skewness, we applied logarithmic transformation to this variable [log (variable + 1)]. Goods donation is a binary variable that takes the value of 1 if a firm donated goods in addition to cash, and takes the value of 0 otherwise. Donation day was measured as the number of days that had passed from the onset of the COVID-19 outbreak in Wuhan (January 20, 2020) until a firm announced its donation. A larger number indicates that a firm announced its donation at a later date after the onset. The number of prior donors indicates how many industry peers (other firms being categorized into the same industry) had announced their donations by the time a focal firm announced its donation. To reduce skewness, we applied logarithmic transformation to this variable [log (variable + 1)].

We specified a set of control variables, which are summarized in Table A1 in the E-Companion. As investors might react differently to donations made to different recipients, we constructed recipient dummies to indicate whether a firm donated to federated charities, the Red Cross, hospitals, government agencies, multiple entities, or unspecified recipients. Additionally, we controlled for three financial ratios to account for the varying operating conditions of firms. Operating margin represents a firm's operating income divided by its revenue. Main business growth reflects the rate of increase or decrease in a firm's revenue from its primary business. Quick ratio was calculated as the sum of a firm's near-cash assets (cash and equivalents, current receivables, and short-term investments) divided by its current liabilities.

We included exchange-industry dummies in our analysis to account for the combined potential influence of industry and exchange heterogeneities. Firms listed on the Shanghai and Shenzhen exchanges differ in their characteristics and are not directly comparable. The Shanghai Exchange primarily serves large and state-owned enterprises, and its listing standards are relatively strict. Typically, firms listed on the Shanghai Exchange are older and larger, have a more diversified business portfolio, and originated from traditional sectors. On the other hand, the Shenzhen Exchange mainly serves small and medium-sized enterprises, and its listing standards are relatively relaxed. Firms listed on the Shenzhen Exchange are younger and smaller, have a clearer business focus, and originated from emerging sectors. (For more information, please refer to www.sse.com.cn and www.szse.cn, the official websites of the two exchanges.) As such, investors’ reactions to a donation event might differ depending on where the donating firm was listed. Additionally, industry affiliation could also affect investors’ response to a firm's donation for two reasons. First, some industries faced more severe disruptions than others. Second, firms in different industries varied in their levels of preparation and resilience due to differences in the market environment, supply chain structure, and business model. By specifying exchange-industry dummies, we could control for any potential influence resulting from the interaction of industry affiliation and listed exchange. Table A2 in the E-Companion provides a list of these dummies.

Location-specific conditions could influence a firm's disaster exposure and investor's reactions to its donation. We specified location dummies, which indicate the province or municipality where the headquarters of a firm was located. Chinese firms typically placed their headquarters in the area where they originated and had the largest operations. Since the pandemic spread unevenly, some locations were more disrupted than others, and firms headquartered in different locations were affected differently. Furthermore, we also constructed a time-varying location variable cumulative fatalities, which measures the number of COVID-19 fatalities in a firm's headquarter location by the day the firm announced its donation. To reduce skewness, we applied logarithmic transformation to this variable [log (variable + 1)].

As the COVID-19 pandemic is a global phenomenon, we monitored the evolving situations outside of China using variable sentiment. This variable was constructed using Google Trends metric for the keyword search “coronavirus.” Lastly, since investors’ reactions to a donation event could be influenced by media coverage, we constructed variable visibility to capture the number of times a donating firm was mentioned in the media in relation to its donation.

To estimate the conditional influence of the above variables on CARi, we modeled a firm's donation decision in the first stage of regression. Specifically, whether or not firm i announced its donation on day t (a binary choice) was modeled as:

We assumed that uit in the donation decision equation (8) (first stage) and

Probit regression was used to estimate equation (8) for the donation decision. This estimation included all firm-day observations associated with firms that did not donate, as well as firm-day observations of donating firms until the day they announced their donations. To avoid selection bias, the inverse Mills ratio derived from equation (8) was included in the CAR equation (7). Including the inverse Mills ratio also helps to mitigate the potential endogeneity issue of donation day, which could occur if an unobserved factor, such as a firm's responsiveness to unexpected social need, influenced both donation day and CARi. This is because the inverse Mills ratio reflects the unobservable factors that could influence a firm's decision to announce its donation on a given day.

Despite our efforts to account for a wide range of variables, the amount of cash donation and goods donation might still be associated with endogeneity issues. Specifically, firms differed in their culture of philanthropy, which mirrored employees’ value orientation, generosity, and care for the wider society. Unobserved philanthropic culture could affect both the amount of cash a firm donated and CARi. Firms also differed in their ability to source and distribute goods during the pandemic, and this unobserved ability could affect both a firm's decision to donate goods and CARi. To address potential endogeneity, we used the control function method introduced in Wooldridge (2015). This method involves two procedures. First, we obtained residuals from an instrumental regression of an endogenous variable on a set of exogenous variables and instruments. Second, we included these residuals as an additional control when estimating the CAR equation. These residuals serve as proxies for unobserved factors. Let xi† denote an endogenous variable that represents either the amount of cash donation or goods donation. The instrumental regression can be expressed as:

Tables A3 and A4 in the E-Companion summarize the variables used in this study and their corresponding information sources. Standard errors were estimated using bootstrapping.

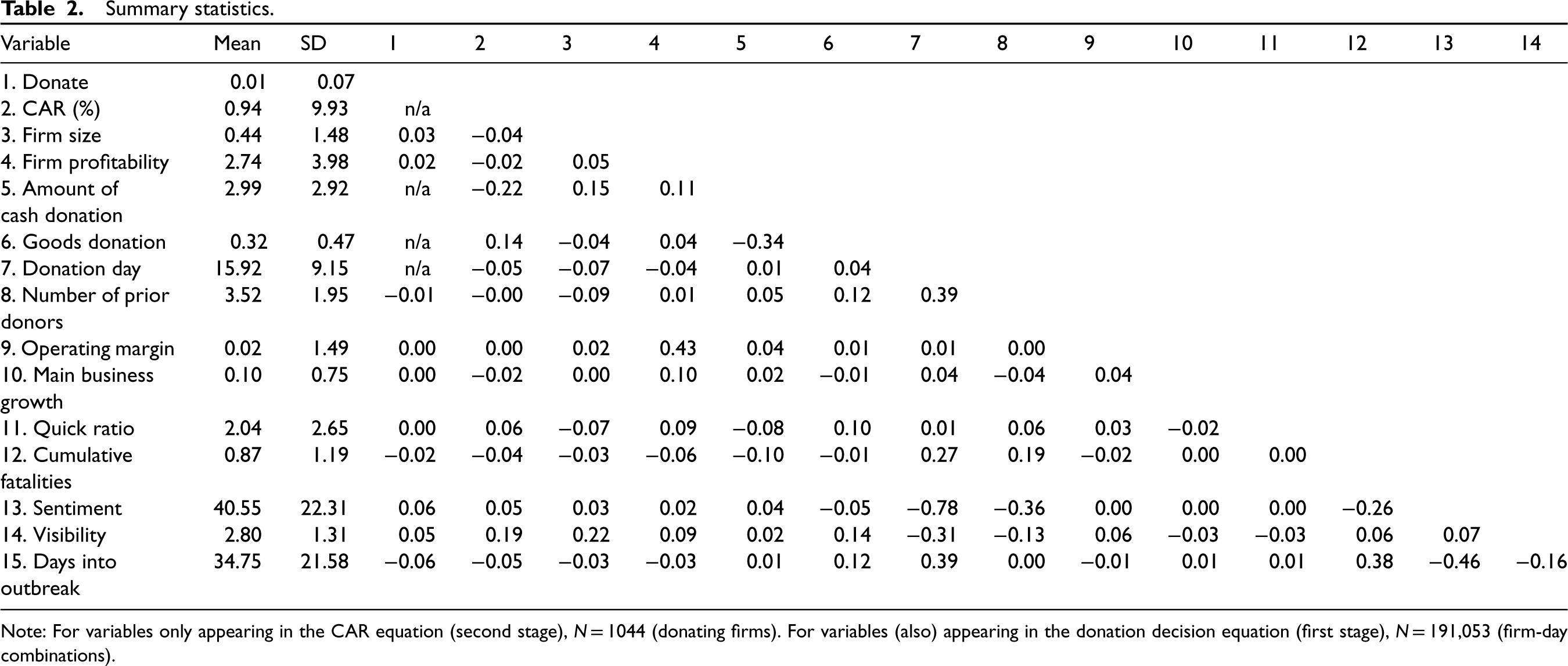

Table 2 presents summary statistics and correlation coefficients for the variables used in this study. None of the correlation coefficients show a high value. We also calculated variance inflation factors (VIFs), most of which were below 1.5, except for donation day (2.75) and sentiment (2.60). According to Hair et al. (2018), a VIF threshold of 4.0 indicates the presence of multicollinearity. Therefore, multicollinearity is not a major concern in this study.

Summary statistics.

Summary statistics.

Note: For variables only appearing in the CAR equation (second stage), N = 1044 (donating firms). For variables (also) appearing in the donation decision equation (first stage), N = 191,053 (firm-day combinations).

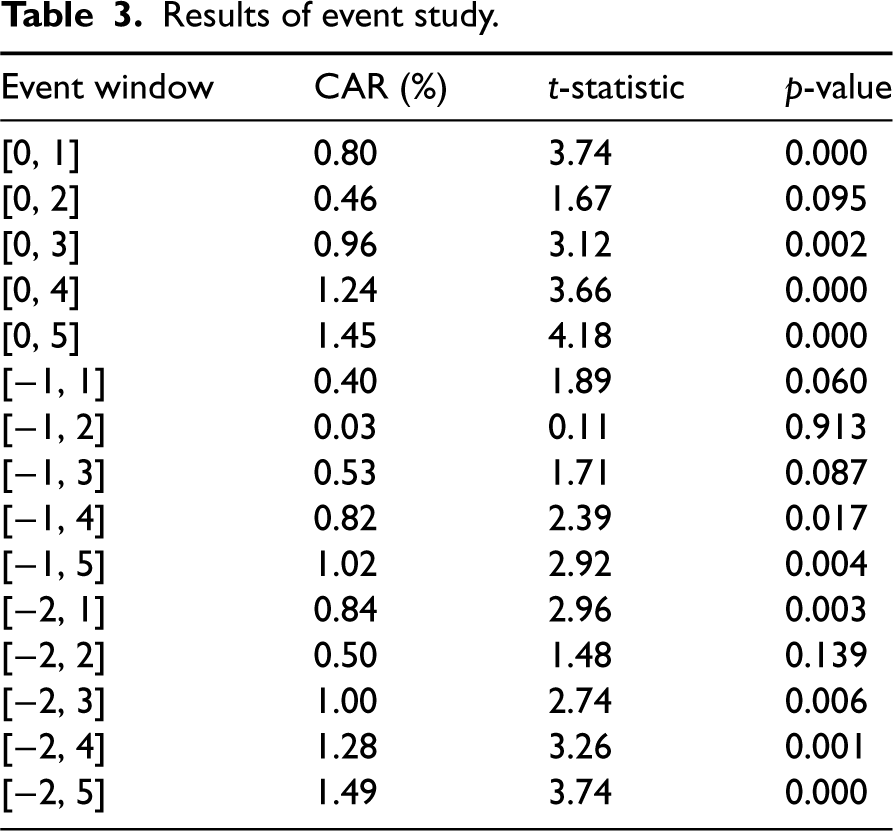

Table 3 presents the results of our event study. Our main analysis was based on the event window [0, 1], while we also examined numerous alternative windows. Table 3 shows that the average CAR estimates during these windows are consistently positive. Among these 15 windows, 13 are associated with a significance level of at least 10%. Overall, these findings support H1b, suggesting that firms’ disaster relief donations generally led to an increase in their market value. However, the presence of several windows with lower levels of statistical significance implies that this positive effect might not be deterministic and could depend on other factors, such as those being explored below.

Results of event study.

Results of event study.

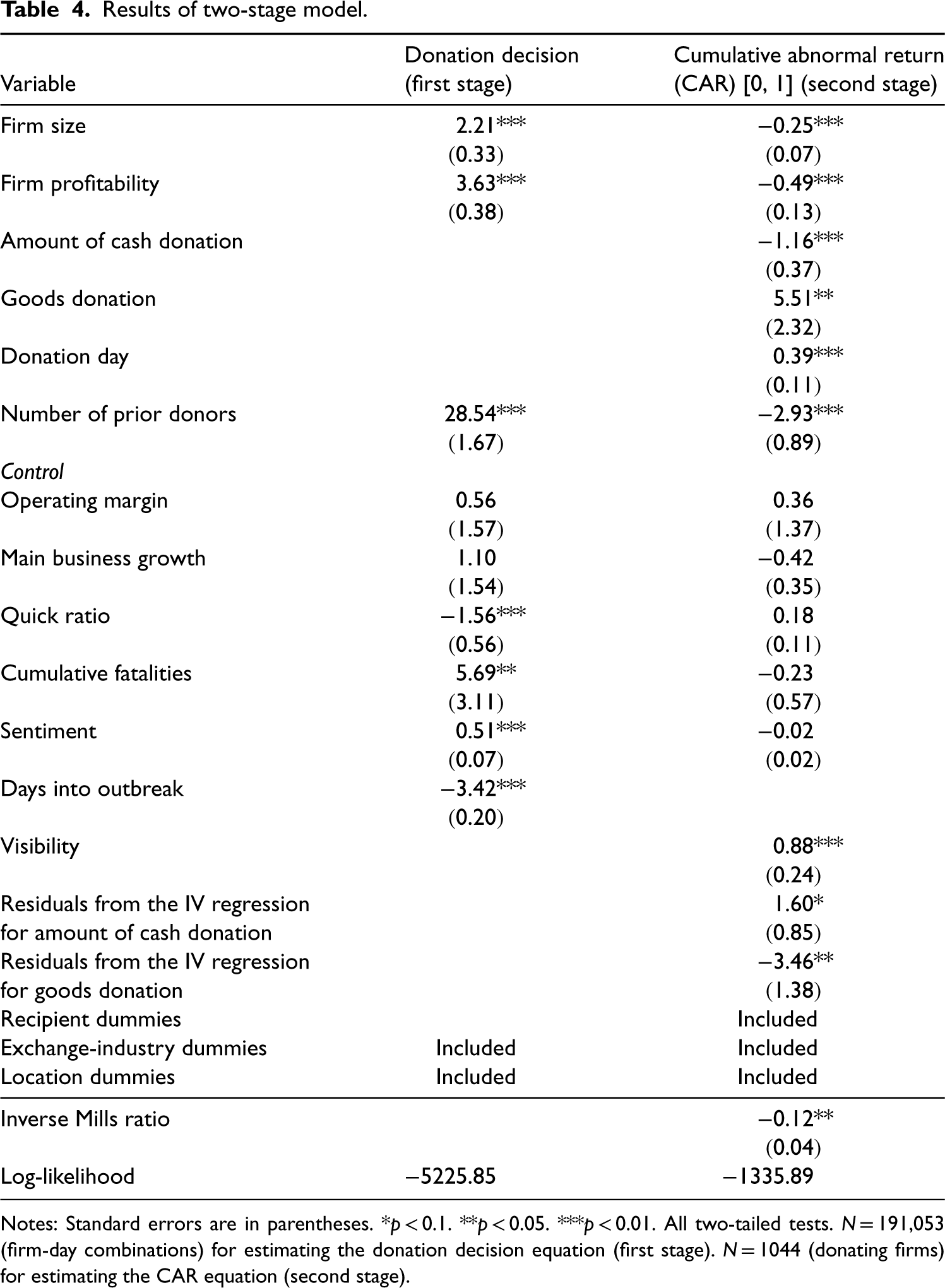

Table 4 reports the results of our two-stage model. Concerning firm characteristics, the coefficient of firm size in the CAR equation is negative and statistically significant (β = −0.25, p = 0.001), suggesting that investors reacted more positively when a smaller firm donated. This finding supports H2b, which derives from the reputation-building perspective. Similarly, the coefficient of firm profitability in the CAR equation is negative and statistically significant (β = −0.49, p = 0.000), indicating that investors reacted more positively when a less profitable firm donated. This result is consistent with H3b, which also stems from the reputation-building perspective.

Results of two-stage model.

Results of two-stage model.

Notes: Standard errors are in parentheses. *p < 0.1. **p < 0.05. ***p < 0.01. All two-tailed tests. N = 191,053 (firm-day combinations) for estimating the donation decision equation (first stage). N = 1044 (donating firms) for estimating the CAR equation (second stage).

Regarding donation characteristics, the coefficient of the amount of cash donation in the CAR equation is negative and statistically significant (β = −1.16, p = 0.002), indicating that investors preferred a firm to limit its cash donation. This result supports H4a, which is based on the self-protection perspective. In contrast, the coefficient of goods donation in the CAR equation is positive and statistically significant (β = 5.51, p = 0.018), suggesting that investors responded more positively when a firm donated goods in addition to cash. This finding supports H5b, which derives from the reputation-building perspective.

In terms of donation timing, the coefficient of donation day in the CAR equation is positive and statistically significant (β = 0.39, p = 0.001), indicating that investors reacted more positively when a firm donated on a later day after the onset of the COVID-19 outbreak. This result supports H6a, which stems from the self-protection perspective.

Finally, in relation to industry condition, the coefficient of the number of prior donors in the CAR equation is negative and statistically significant (β = −2.93, p = 0.001), suggesting that investors preferred a firm to donate before an increasing number of industry peers had done so. This result supports H7b, which is based on the reputation-building perspective.

Out of the six observed effects, four support the reputation-building perspective, indicating that investors’ reactions were often driven by expected reputational gains. Moreover, although donating more cash reduces the CAR following a donation event, donating goods in addition to cash increases the CAR. This contrast suggests that while investors expected firms to preserve more cash, they also recognized the reputational benefit of donating goods in addition to cash. On the other hand, although donating on an earlier day reduces the CAR following a donation event, donating before a larger number of industry peers increases the CAR. This contrast suggests that while investors recognized the reputational benefit of donating before more industry peers, they also expected firms to prioritize self-protection through resource preservation when uncertainties were most profound immediately after the onset of the outbreak.

We used the control function method to address the potential endogeneity of the amount of cash donation and goods donation. The residuals obtained from the instrumental regression show a significant effect on CAR, indicating the need to account for endogeneity. The F statistic for the instrumental regression is 17.69 for the amount of cash donation and 17.27 for goods donation. These values exceed the threshold of 10, suggesting that the instrument used is reasonably strong (Stock & Yogo, 2005). Additional details about the instrumental regression can be found in Table A5 of the E-Companion.

The estimates in the donation decision equation (first stage) reveal some interesting contrasts. Firm size, firm profitability, and the number of prior donors have a positive effect on the donation decision equation, but a negative effect on the CAR equation. Therefore, some factors that increase a firm's inclination to donate result in more negative reactions from investors. Control variables including quick ratio, cumulative fatalities, and sentiment have a significant effect on the donation decision equation, but not on the CAR equation. These contrasts highlight the need to account for a firm's donation decision. The coefficient of the inverse Mills ratio is negative and significant, indicating a negative correlation (ρ) between the error terms of the first- and second-stage equations.

We performed several additional checks to evaluate the robustness of our findings. First, we re-estimated the model using different event windows. Second, we used an alternative period of 225 to 46 trading days prior to the event day (spanning 180 trading days) to estimate the market model in equation (3). Third, we excluded firms headquartered in Hubei, the center of the first COVID-19 outbreak in China, from our sample because these firms may represent unique cases. Lastly, we implemented an alternative method discussed in Xu (2021) to address potential endogeneity. Tables A6 to A8 in the E-Companion present the results of these robustness checks, which are consistent with the results of our main analysis.

We also explored potential interaction effects. First, we tested the interactions between our explanatory variables and industry dummies. Since industry dummies reflect varying industry environment, these interactions can reveal the potential impact of industry environment on our findings. Although most of these interactions do not display a significant effect, we found that the interaction between the number of prior donors and a binary indicator of industries more adversely affected by the COVID-19 pandemic has a negative effect. This finding suggests that the negative effect of the number of prior donors on CAR is more pronounced in industries that suffered more from the pandemic. Second, we also added the interaction between the amount of cash donation and goods donation in our model. This interaction can provide insights into whether the two types of donations might complement or substitute each other. Here, we did not observe a significant interaction effect. The results of these examinations are presented in Table A9 in the E-Companion.

Additionally, we examined whether donation day and the number of prior donors could have a curvilinear relationship with CAR, using quadratic specifications. A curvilinear relationship would imply that “quicker followers” outperformed those who moved ahead or behind them. This additional analysis did not reveal any significant effect in the squared term of either variable, perhaps because our setting differs from the typical contexts where the advantages of quicker followers have been identified. In typical contexts such as product innovations and new market entries, quicker followers are advantageous when they can leverage the technical and market infrastructure developed by earlier movers, while also deterring later movers through accumulated output, buyers’ switching costs, or resource preemption (Lieberman & Montgomery, 1998). These advantages were not present in our setting.

Discussion

Implications for Research

Our study contributes to the growing research on the organizational consequences of disaster exposure. This literature has focused on the risk of failure resulting from resource depletion. The prevailing view is that afflicted firms should keep resource reserves to protect themselves from adversaries (Gregg et al., 2022; Williams et al., 2017). Supporting this self-protection perspective, our analysis suggests that if afflicted firms decide to donate to disaster relief, they should donate a smaller amount of cash and avoid donating in the earlier period after the onset of a disaster. Furthermore, this study injects an investment consideration to complement the prevailing emphasis on resource depletion and preservation. We found that investors generally react positively to donation announcements, perhaps because donations to disaster relief are viewed as a value-adding investment, not simply an unwelcome diversion of resources.

This study extends the corporate philanthropy literature, which has long highlighted the potential benefits of philanthropic programs in enhancing corporate image, strengthening stakeholder relationships, and increasing firm value (Cha & Rajadhyaksha, 2021; Gautier & Pache, 2015). While the reputation-building role of corporate donations has received empirical support, most existing studies have focused on philanthropic programs in ordinary times. A few studies have examined donations to disaster relief and found a positive effect on firm value (Madsen & Rodgers, 2015; Muller & Kraussl, 2011; Patten, 2008), but in these studies, most donors were remote from the adverse impact of the disaster. This study extends the literature to an under-researched setting, showing that even when donors are directly afflicted by a major disaster, investors still recognize the reputational gains from donating to disaster relief.

As philanthropic donations represent a prevalent form of ESG (environmental, social, and corporate governance), our study adds to the ESG literature (Malik, 2015). Prior research has shown that firms engage in ESG primarily for instrumental reasons, such as expected financial benefits (Aguinis & Glavas, 2012). However, the financial outcome of ESG remains a contentious debate in the literature, with inconsistent empirical findings highlighting the importance of identifying contingent factors. We contribute to this line of research by demonstrating how the financial benefits of corporate donations (increased firm value) may vary by firm and donation characteristics, timing of donations, and industry conditions.

This study also contributes to the disaster management literature, where coordination between humanitarian organizations has been identified as a critical determinant of effective response and successful post-disaster rehabilitation (Moshtari, 2016; Toyasaki et al., 2017). However, such coordination is often lacking because humanitarian organizations often need to compete for limited funding and donors, resulting in failures in relief operations (Chakravarty, 2021; Eftekhar et al., 2017; Goldschmidt & Kumar, 2016). Extending prior research including Patten (2008), Muller and Kraussl (2011), and Madsen and Rodgers (2015), our study shows that even for firms who are afflicted by disaster exposure, donating to disaster relief may still benefit themselves. Hence, firms should consider both the need for resource preservation and the potential gains from giving to the public. Consideration of potential gains encourages managers to be more open to supporting relief operations and funding humanitarian organizations in times of a major disaster. Increased funding availability can reduce competition between humanitarian organizations and facilitate coordination, thereby contributing to social welfare.

Implications for Practice

Our findings provide practical guidance on how firms can receive more favorable response from investors when donating to disaster relief. For instance, facing tighter resource constraints, managers of smaller or less profitable firms may be tempted to prioritize resource preservation during disasters. However, our findings suggest that, especially for these firms, contributing to disaster relief can elicit a more positive response from investors, perhaps because investors expect smaller or less profitable firms to reap more reputational gains from contributing to disaster relief. While preserving resources is important, a higher stock price can also help firms withstand the challenges posed by a disaster. Therefore, managers should strive for a balance between preservation and giving.

We found that investors react more negatively when firms donate more cash but react more positively when firms donate goods in addition to cash. Hence, it may be advisable for firms to combine cash and goods donations within a given budget. Additionally, we found that investors react more negatively when firms donate sooner after the onset of a disaster but react more positively when firms donate before an increasing number of industry peers have donated. Therefore, it may be better for average firms to wait for a while, but as they wait, they need to monitor their industry peers. Some industry peers may donate sooner, possibly because they can better withstand uncertainties or because they can seize more reputational benefits from earlier donations. When industry peers begin to donate, managers need to consider whether to follow suit quickly despite ongoing uncertainties. Falling behind may cause a firm to be perceived as a reluctant donor who acts only under peer pressure, rather than out of genuine concern for the public, thereby missing the opportunity to enhance corporate reputation.

At a more general level, our study implies that firms should donate in a way that sends a clear signal of their philanthropic nature and at an expense that investors find reasonable. For managers, acting upon this implication may be difficult because the interests of investors and the public are not fully aligned. While the public expects firms to donate more, investors expect firms to donate less cash. While the public expects firms to donate earlier, investors expect firms to wait unless an increasing number of industry peers have donated. Managers need to identify the mutual interest between the two parties. This task becomes challenging when the zone of mutual interest is limited. Nonetheless, if managers can overcome the challenge, their donations shall benefit society, be appreciated by investors, and in turn, help sustain their company. Such a mutually beneficial outcome is particularly valuable in times of a major disaster.

Generalizability

We tested our conceptual framework using data on donations made by Chinese firms to support disaster relief during the first COVID-19 outbreak in China. As these firms were faced with a tension between self-protection and reputation-building, our empirical setting is appropriate for assessing the relative strength of these two perspectives. Our empirical focus was on firms in one country (China) experiencing one common disaster (the immediate aftermath of the first COVID-19 outbreak), which is consistent with prior research such as Patten (2008) and Muller and Kraussl (2011).

Despite this empirical focus, our conceptual framework can be extended and generalized to other settings where a tension between self-protection and reputation-building exists. Based on the literature reviewed in the earlier section, we anticipate observing such tension in a wide range of contexts. On the one hand, research on the organizational consequences of disaster exposure has identified the need for self-protection in various disaster scenarios (Huang et al., 2018; Oh & Oetzel, 2011; Pek et al., 2018). On the other hand, ESG and marketing researchers have shown that philanthropic donations can enhance firm reputation in ordinary times (Dean, 2003; Koschate-Fischer et al., 2016; Szocs et al., 2016) as well as in times of crisis (Hildebrand et al., 2017). These existing findings suggest that self-protection and reputation-building perspectives are not unique but common, although the literature has yet to bring the two perspectives together.

Future Directions

The current study can be extended in various ways. Below, we will discuss several potential areas for future research. Further opportunities are presented in Exhibit A3 in the E-Companion. First, the COVID-19 pandemic suddenly inflicted massive damage, catching most firms off guard. Firms were unprepared because the emphasis on lean operations has limited the buffers they kept in ordinary times. Because firms are generally unprepared, their resilience was largely determined by factors such as their size and profitability before the disaster hit. The effects we found related to firm size and profitability might reflect this situation. In other settings where a disaster is more foreseeable, future research can examine whether the role of firm size or profitability changes if firms are better prepared before a disaster.

Second, our investigation period covered the first COVID-19 outbreak. When the pandemic returned later, the level of uncertainty had decreased, which might weaken both the self-protection and reputation-building considerations. Nevertheless, we speculate that the reputation-building perspective will still prevail because when uncertainties decrease, the need for firms to self-protect would also decrease, whereas the public's need for corporate support would change but not necessarily decrease. With fewer disruptions over time, the public's need would change from emergency response to rehabilitation, and eventually to general social programs. If firms can adapt their donations to the evolving needs of the public, their donations may still contribute to reputation-building. Future research can test our speculation and further explore the relative strength of the two theoretical perspectives.

Relatedly, our results show that investors react more positively when a firm donates goods in addition to cash. This effect may become more complicated over time. In times of a major disaster, uncertainties caused by uncontrollable events are substantial, and hence donors of goods may be evaluated more favorably (Hildebrand et al., 2017). Even if a firm donates unhelpful goods, it is less likely to elicit negative sentiment. Over time, however, uncertainties regarding what is needed are increasingly resolved, and the level of emergency decreases. Consequently, people have higher expectations for the true value of goods donations. If a firm donates unhelpful goods, people may interpret the firm's intention negatively, such as being motivated by a self-serving interest in increasing its own visibility (Barasch et al., 2014; Newman & Cain, 2014). This development implies that reaping reputational gains from donating goods would become more difficult. Future research can investigate how a firm can enhance its reputation by donating goods that benefit society even when uncertainties decrease.

To better inform future research, we conducted some post-hoc interviews two years after the first COVID-19 outbreak. (Table A10 in the E-Companion summarizes the background information of interviewees.) Through these interviews, we learned about an emerging consideration among managers after uncertainties gradually reduced overtime: accelerating post-disaster rehabilitation. For example, a manager from a leading electronics manufacturer expressed hope that his company's cash donation to support vaccination programs would help “speed up” the lifting of lockdown restrictions, which had caused labor shortage across the supply chain. Similarly, a retail business manager expressed her desire to quickly “bring customers back to the main street; back in our stores” by funding pandemic control programs. Future research conducted over a longer time span can explore how firms can contribute to post-disaster rehabilitation, thereby increasing social welfare while also aiding in donors’ own recovery.

Prior research has shown that prices for goods and services often increase in the aftermath of a disaster (Snyder, 2009). This study does not investigate price gouging because such a phenomenon did not occur in our setting. Shocked by the widespread disruptions caused by the first COVID-19 outbreak, the public and the government closely monitored and quickly punished firms who raised their prices and worsened the chaos. According to the National Bureau of Statistics of China (www.stats.gov.cn), the consumer price index for March 2020 decreased by 1.2% compared to the previous month, and the producer price index decreased by 1.0% compared to the previous month. For future studies in different disaster scenarios, exploring the effects of increased prices on firms, customers, and other stakeholders would be a valuable area of research.

Lastly, disaster relief projects carried out by donation recipients may differ in their effectiveness. During the first COVID-19 outbreak, information on project effectiveness was largely unavailable when investors reacted to donation events. Due to the lack of standards in an unprecedented situation, judging the effectiveness of each project was rather difficult. Future research in other settings where information on project effectiveness is present can investigate the implications of such information for investors’ reactions to donation events.

Supplemental Material

sj-pdf-1-pao-10.1177_10591478231224939 - Supplemental material for Donations by Disaster-Afflicted Firms and Changes in Firm Value: Self-Protection and Reputation-Building Perspectives

Supplemental material, sj-pdf-1-pao-10.1177_10591478231224939 for Donations by Disaster-Afflicted Firms and Changes in Firm Value: Self-Protection and Reputation-Building Perspectives by Ping Xiao, Kai-Yu Hsieh and Weining Bao in Production and Operations Management

Footnotes

Acknowledgments

The authors would like to express their gratitude to the senior editor and three anonymous reviewers for their constructive feedback. Financial support from Taiwan's Ministry of Science and Technology is gratefully acknowledged. The authors contributed equally and are listed in reverse alphabetical order.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Taiwan's Ministry of Science and Technology (grant number 110-2410-H-004-097).

How to cite this article

Xiao P, Hsieh K-Y, Bao W (2023) Donations by Disaster-Afflicted Firms and Changes in Firm Value: Self-Protection and Reputation-Building Perspectives. Production and Operations Management 33(1): 323–341.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.