Abstract

The uncertainty in the supplier’s material flows has become a norm rather than an exception in supply chains. The supply uncertainty can result in unexpected inventory shortfall, amplifying lost sales. However, the design of inventory replenishment and product pricing policy to mitigate both supply uncertainty and demand loss remains unexplored. This is because the resulting dynamic planning problem is highly nonconcave and thus intractable. To address this challenge, we propose an approach that focuses on a class of intuitively appealing and practically plausible policies. Specifically, as the level of on-hand inventory increases, we expect an increased amount of demand fulfillment and a decreased product price. Applying the notions of stochastic functions, we show that, under general conditions of the stochastic supply and demand functions, the dynamic planning problem becomes a concave optimization problem over the restricted policy class. We further reduce the set of candidate policies to a refined class by excluding the dominated policies. A refined policy can be easily computed, and appropriately selected refined policies produce close-to-optimal profits. These developments allow us to evaluate the consequences of demand loss. In particular, demand retention through backordering can be beneficial when overstocking is costly in relation to understocking, but the benefit is insensitive to supply and demand uncertainties. Moreover, inventory-based dynamic pricing is more valuable in mitigating supply risk under lost sales than under backordering.

1 Introduction

The impact of supply uncertainty, amplifying the mismatch between the demand and supply, has gained increasing attention recently. Firms are realizing that effective management of supply chains requires careful coordination between inventory control and demand shaping. On the one hand, inventory replenishment through procurement should aim at meeting the demand, avoiding excessive shortage and surplus. On the other hand, the price adjustment should account for the product availability, ensuring the appropriate profit margin and sales. Amihud and Mendelson (1983) discover the price-smoothing effect, suggesting that a carefully designed procurement policy can reduce the sensitivity of the material flow to the price. Feng (2010) demonstrates the complementarity between replenishment and pricing—When the procured amount is not guaranteed for delivery due to high supply uncertainties, frequent price adjustments can generate a significant benefit.

The combined inventory-pricing strategies have been extensively studied in the existing literature, while almost exclusively for the situation where the unmet demand can be backordered. In many situations, customers may not be willing to postpone the consumption and wait for product availability (Chen and Wu, 2019). Lost sales often happen in the event of stockouts. This is the situation frequently observed in retail, where either there are alternative options for the customers or there is a certain time frame for consumption (e.g., Christmas decorations or snow throwers).

During the COVID-19 pandemic, supply issues due to factory closures and clogged ports aggravated unmet consumer demands in many industries. Gap reported an estimated $300 million in lost sales in a quarter of 2021 (Scott, 2021). Bed Bath and Beyond posted a 7% sales decline because of empty shelves in a quarter of 2021 including a holiday season (Kapner and Grossman, 2022). Under Armour, a sports apparel brand, and Chemours, a chemical company, canceled a large number of orders in 2022 because of supply issues (Williams-Alvarez, 2022). The significant amounts of lost sales due to supply uncertainties have induced retailers to adjust prices to maintain profitability. For example, apparel sellers including Abercrombie and Fitch, Guess, and Gap significantly reduced price discounts to boost profit margins, while closely monitoring stock levels (Maurer and Trentmann, 2021).

In other situations, supply uncertainties can lead to excess inventories. As reported by Smith and O’Neal (2021), many companies, worried about instability in upstream material flows, ordered in large volumes for the end-of-year holidays in 2021 and ended up with stock pileups. For example, Target and Big Lots complained that they had to offer deep discounts to clear excess inventories at the beginning of 2022 (Broughton and Maurer, 2022).

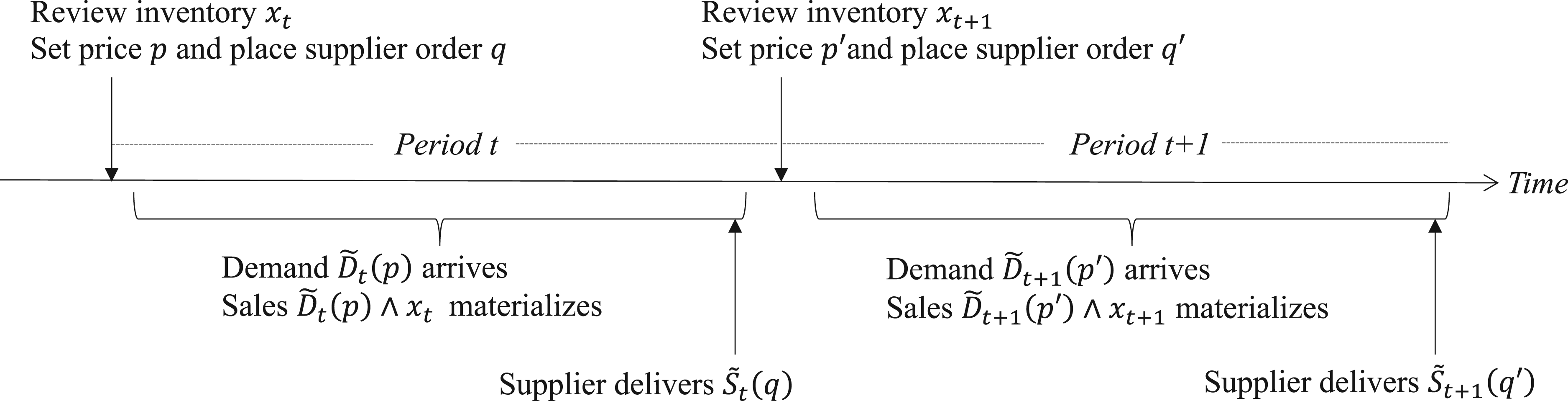

The analysis of a dynamic planning system facing lost sales and supply uncertainty is nontrivial. Performance evaluation and policy design for the general system are unknown. We attempt to address these in this study. Specifically, we consider a periodic-review system involving both supply and demand uncertainties. The amount of supply is a stochastic function of the supply decision and the amount of demand is a stochastic function of the pricing decision. The decision maker determines the order and price for the current period, fulfills the demand with the available inventory, and receives the delivery from the supplier.

The profit function is neither concave nor convex in the decisions even in the special case where the supply is deterministic and the inventory cannot be stored (i.e., the planning horizon is one period). The optimal policy is complex and cannot have a characterization in general. Instead of looking for approximations of the profit function or asymptotic behaviors of the system, we examine potential solutions that are intuitive for implementation.

In the special case of a single-period setting, we show that, if the optimal supply decision is decreasing in the price, the profit function is concave in the pricing decision. This observation suggests we restrict the solution space to decreasing supply paths. Such solutions are practically plausible because firms often cut down the prices in the event of overstock, and firms often order bulk amounts in preparation for price discounts. The policy can be analyzed by adapting a similar approach developed by Feng et al. (2020). This approach applies to general supply functions (that are stochastically linear in midpoint) and to general demand functions (that are stochastically linear in midpoint and stochastically decreasing in the increasing concave order).

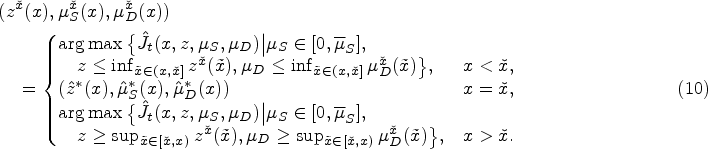

When the planning involves multiple periods, the evolution of the material flow is triggered by the dynamics of the supply and demand uncertainties. In this case, the argument used for the single-period setting does not apply anymore. Instead, we need to examine how the decisions are related to the on-hand inventory level. In view of the potential shortage of future supply, a portion of the on-hand inventory is allocated to meet the current demand, and the rest is reserved for future sales. Such inventory rationing provides decision flexibility to mitigate supply uncertainties. We show that, under general conditions of the stochastic supply and demand functions, the profit function is concave for a given inventory rationing decision. The optimal profit function, however, is generally not concave in the on-hand inventory level, making the analysis of the dynamic program intractable.

In practice, firms often allocate more inventories to meet the incoming demand and lower the product price when a larger amount of stock is available (Gimpl-Heersin et al., 2008). Theoretically, however, such a monotone policy may not be optimal. We prove that, if an optimal policy is indeed monotone, then the value function of the dynamic program is concave. This result entices us to construct a set of candidate policies that reveal the intuitive monotone behaviors. We show that the profit function is concave when any candidate policy is implemented. We further refine the candidate policy set by requiring the policy to be close enough to the truly optimal policy, and show that any refined policy can be computed efficiently. Certainly, the policy refinement reduces the feasible set of the decision space, which could result in a suboptimal profit. An extensive numerical experiment, however, suggests that the profit loss from implementing the refined policies is negligible.

To understand the impact of lost sales on system performance, we use a backorder system as a benchmark, under which the unmet demand can be fulfilled in the future at a cost. Our analysis suggests that the profit difference between a backorder system and a lost-sales system is larger when the inventory carrying cost gets higher and the shortfall penalty gets lower. In other words, retaining unsatisfied customers through backordering can be beneficial when overage is costly in relation to underage. Interestingly, the profit difference between the two models is not sensitive to either supply or demand uncertainty. Furthermore, inventory-based dynamic pricing, as opposed to static pricing, is more beneficial in the lost-sales system than in the backorder system.

The remainder of the article is organized as follows. In Section 2, we review the related literature and discuss the contribution of our study. Section 3 lays out the model formulation. The single-period version of the problem is treated in Section 4. In Section 5, we analyze the multi-period problem by discussing the properties of the profit function, constructing the potential policies, and evaluating the performance of the proposed policies. Section 6 concludes the study. The preliminary results of stochastic functions are relegated to the appendix, and the proof of formal results can be found in Online Appendix EC.1. The computational algorithm is described in Online Appendix EC.2 and supplemental numerical experiments are provided in Online Appendix EC.3. Throughout this article, we name monotonicity (i.e., increasing or decreasing) in the weak sense.

2 Literature Review

Coordinating inventory and pricing decisions is one of the most researched problems in the operations management literature. Whitin (1955) first formulates the price-setting newsvendor model, in which the demand distribution depends on the product price. Since then, many authors have analyzed this problem by assuming either an additive demand, in which the price affects only the location of the distribution (e.g., Whitin, 1955; Mills, 1959), or a multiplicative demand, in which the price affects only the scale of the distribution (e.g., Karlin and Carr, 1962; Monahan et al., 2004). Early developments on this problem are summarized by Petruzzi and Dada (1999).

The major difficulty in the single-period price-setting newsvendor problem lies in the fact that the profit function is, in general, not jointly concave in the ordering and pricing decisions. The focus is given to identifying the properties of the demand–price relationship that lead to the desired structure of the profit function so that an optimal solution can be computed efficiently. Kocabıyıkoǧlu and Popescu (2011) propose a measure, called the lost sales elasticity, which is essentially the price elasticity of the cumulative hazard rate of the demand distribution. They show that the profit function is jointly concave if this measure is above a certain threshold. Lu and Simchi-Levi (2013) derive a general set of conditions for the family of location-scale demands (i.e., the price affects only the location and the scale of the demand distribution), under which the profit function is log-concave and thus the optimal solution can be easily computed. Feng et al. (2020) demonstrate that the conditions obtained by Kocabıyıkoǧlu and Popescu (2011) are restrictive, as they fail under multiplicative demands. Feng et al. (2020) also generalize the results obtained by Lu and Simchi-Levi (2013) for the case of general stochastic demand functions beyond the location-scale family.

Most of the studies on the multi-period extensions of this problem assume that the unmet demand can be fully backordered and a penalty is charged for unfilled demand at the end of the planning horizon (e.g., Federgruen and Heching, 1999; Feng et al., 2014). The advantage of the backorder model lies in the fact that the amount of backorder can be represented as the negative of the inventory level. As a result, the profit function is concave in the realized inventory level under general supply and demand functions (Feng and Shanthikumar, 2018). The shortcoming of the backorder models comes from the assumption that the customers pay the current price, though the demands are filled in the future when the price may be revised. Such an assumption may not be realistic.

When the unmet demand is lost, a situation observed in many practices, the problem becomes analytically challenging because the single-period profit is not jointly concave and neither is the profit-to-go function due to the potential shortage. Zabel (1972) analyzes a two-period version of the model with a deterministic supply and an additive demand that involves a uniformly or exponentially distributed noise. While he is able to identify conditions that involve the mean demand function, holding cost and feasible prices, to ensure a unique solution for additive demands, his analysis does not go too far for multiplicative demands. Thowsen (1975) focuses on additive demands in a nonstationary system. The conditions characterized contain the profit-to-go function, which makes them difficult to verify. Pang (2011) attempts to extend the analysis by Kocabıyıkoǧlu and Popescu (2011) for multi-period settings with additive demands. In summary, the analysis of the optimal solution for the multi-period model is mostly limited to the additive demands.

In view of the difficulty of the multi-period problem, several authors restrict the attention to asymptotes of the model. For example, Polatoglu and Sahin (2000), Chen et al. (2006), Huh and Janakiraman (2008) analyze long-term stationary settings of the problem under a given class of policies. Bu et al. (2020) analyze the performance of the constant-ordering policies and establish the asymptotic optimality of such a policy when the procurement lead time becomes long.

Instead of looking for likely restrictive optimality conditions or focusing on limiting behaviors, Feng et al. (2020) propose to restrict the solution space within a class of intuitively appealing policies in order to address the analytical difficulty of the problem. By restricting to decreasing price paths, they show that the dynamic optimization problem is tractable for a wide class of stochastic demand functions. However, the constructed policy, relying heavily on monotonicity along a single dimension, cannot be applied to our problem with stochastic supply. To deal with supply uncertainty, we need to develop an appropriate approximation of the expected profit and construct policies along three dimensions.

In an essential contrast to the aforementioned studies, the consideration of supply uncertainty leads to a random post-order inventory position. Consequently, the usual trick of dimension reduction by transforming the ordering decision to the order-up-to level does not work any longer. The matching of supply and demand becomes subtle due to the uncertainties from both. As our analysis suggests, we need to modify the development made by Feng et al. (2020) to deal with the single-period version of our model. But such modification would not work for the multi-period setting. Instead, we need a new approach of profit approximation and policy construction.

There is an extensive study on the effect of supply uncertainty in inventory–pricing systems (e.g., Li and Zheng, 2006; Federgruen and Yang, 2008; Feng, 2010; Chen et al., 2013). All of the existing studies assume backordering. The reader is referred to a recent survey by Feng and Shanthikumar (2022) for references therein. Feng and Shanthikumar (2018) show that the problem with backordering is tractable under general supply and demand functions that are stochastically linear in midpoint. It is generally optimal to follow an almost threshold policy (Feng and Shi, 2012; Federgruen et al., 2022). To our knowledge, this study is the first to consider supply uncertainty in a dynamic planning problem facing lost sales.

In terms of methodology, we adopt the notions of stochastic functions (Feng and Shanthikumar, 2022). These notions have been applied to study inventory-based pricing strategies (Feng and Shanthikumar, 2018; Feng et al., 2020) and sourcing strategies under uncertain supplies (Feng and Shanthikumar, 2018; Feng et al., 2019, 2021; Federgruen et al., 2022). In these studies with demand backorder or deterministic supply, the properties of stochastic linearity and concavity are sufficient to ensure a well-behaved profit function and the almost threshold structure of the optimal policy. For our problem involving both supply uncertainty and lost sales, the profit function does not have a concave transformation and the optimal policy reveals a complex structure. In addition to utilizing the properties of the stochastic functions, we need to examine the interaction between supply uncertainty and inventory shortfall in order to design an efficient policy, leading to new developments of the solution approach.

3 Problem Description

We consider a dynamic planning problem over a planning horizon of

The dynamics of the system.

We assume that the stochastic functions

The unmet demand is lost and the leftover inventory is carried over to the next period. Thus, the dynamics of the inventory follows:

For each unit of product delivered by the supplier, the firm pays

The above problem formulation can be seen as an extension of the price-inventory model studied by many (e.g., Federgruen and Heching, 1999; Feng et al., 2014). Two features of this formulation, namely, lost sales and supply uncertainties, impose new challenges to this problem that are not addressed in the previous studies.

We make the following assumptions of the demand and supply functions:

These are the minimal conditions required in all studies involving random supplies and/or random demands, and they do not imply stochastic monotonicity of the supply and demand functions. With these assumptions, we can define the inverses of the mean supply and mean demand, respectively, as

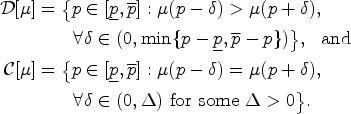

The analysis of the problem relies heavily on the notions of stochastic orders and stochastic functions. We introduce the concepts needed for our analysis below in Definition 1, while discussing their properties in the appendix. Throughout the article, we use the capital letter, say,

A stochastic function

Some basic properties of stochastic functions are discussed in the appendix, which are essential for our subsequent derivations.

4 The Single-Period Problem

In this section, we examine the single-period version of the model. This version is interesting in its own right as a vast literature is devoted to analyzing the price-setting newsvendor problem, a special case of our model with unlimited deterministic supply. To deal with the analytical challenge of the single-period problem, we focus our attention on the class of monotone policies, under which the supply decision and the pricing decision move in opposite directions. Indeed, it is a common practice that firms reduce product prices when inventories are piling up (e.g., Byrnes, 2003; Gimpl-Heersin et al., 2008). In the analysis below, we first prove that the single-period profit function is well-behaved if the optimal policy is indeed monotone. When it is not, we construct a set of candidate monotone policies, with which the resulting profit function is well-behaved. Later in Section 5.3, we will demonstrate that, though the optimal policy may not always be monotone, the restriction to the constructed policies does not lead to a significant profit loss.

When there is only one random demand to be met, the objective is to choose a supply decision, represented by the mean supply

Specifically, under a supply decision

The profit function

Suppose that

the demand satisfies one of the following conditions:

the supply satisfies

If

Feng et al. (2020) proved that condition (C1-b) implies condition (C1-a). Each condition is satisfied by a wide class of demand functions. Feng and Shanthikumar (2018, 2022) showed that condition (C2) covers almost all the supply functions analyzed so far in the existing literature. Thus, the result in Theorem 1 is established for general demand and supply functions, when it is optimal to set a high mean supply for a low price.

The condition of a decreasing

However, the set

The set For any If Suppose

According to Theorem 2(i), the profit as a function of the price is concave along any candidate supply path in set

The result in Theorem 2 is in the similar spirit to that developed by Feng et al. (2020) for the special case of our model with a deterministic supply. This result, however, does not extend to the multi-period setting. As our discussion unfolds in the next section, it becomes clear that the presence of supply uncertainty prevents the dimension reduction used by Feng et al. (2020). Thus, a new development is needed to treat the multi-dimensional decision space for the multi-period model. To facilitate the understanding of our later development, we take an alternative view of the candidate supply path in

The advantage of the policy

5 The Multi-Period Problem

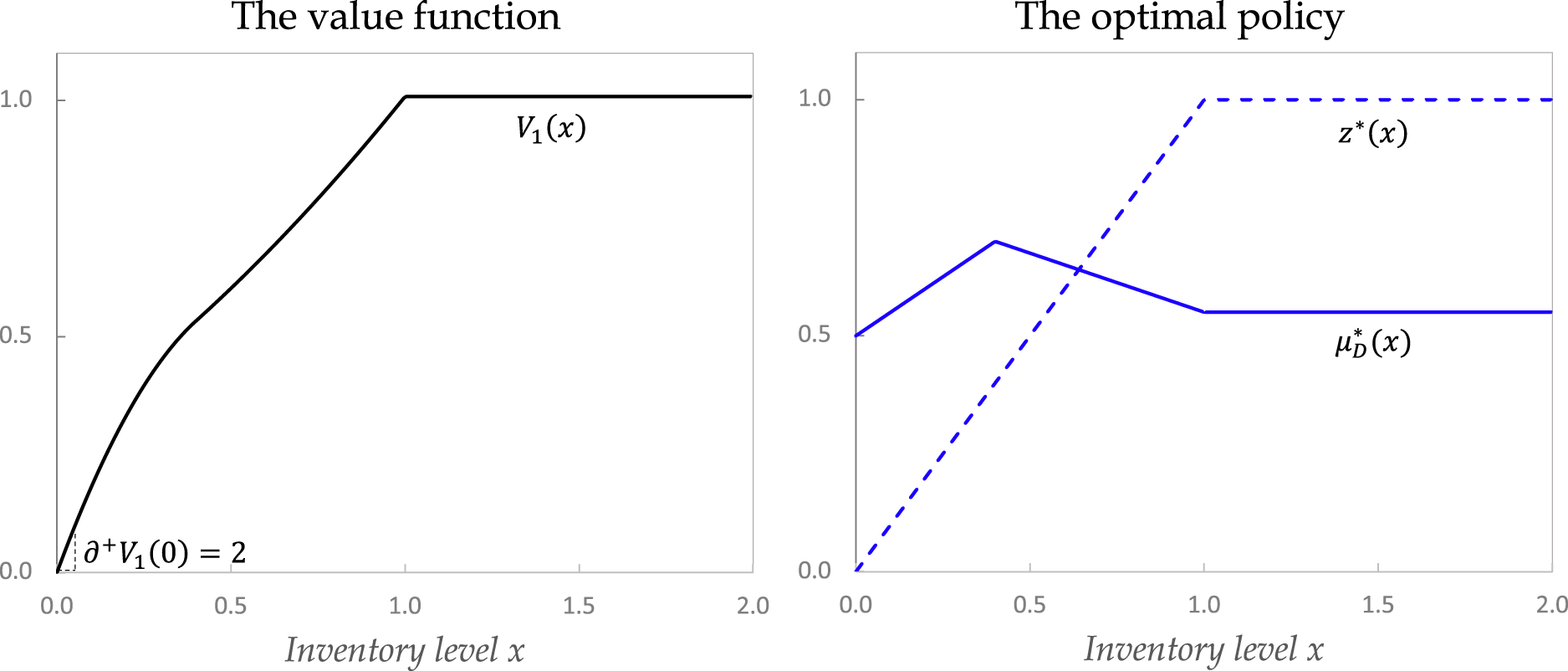

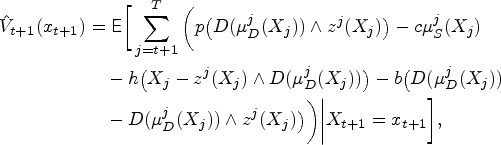

In the context of multi-period planning, the problem formulated in equations (2) and (3) is known to be challenging because neither the instantaneous profit nor the profit-to-go function is well behaved. For the special case of our model with unlimited and deterministic supply, Feng et al. (2020) address the second challenge by deriving an upper bound of the marginal profit. Specifically, the saving of carrying inventory to the next period is capped by the discounted purchase cost and thus by any feasible price. With this property, the profit-to-go function can be transformed into a jointly concave function by applying the notions of stochastic functions. This approach, however, does not work in general with random supply. To see that, we take a one-period example and plot the value function

An example with non-concave value function and non-monotone optimal policy. Notes.

5.1 A Generalized Formulation

When there is no guarantee of receiving the ordered amount from the supplier, the decision maker would face the risk of potential shortage and revenue loss if the inventory level becomes low. It thus makes sense to think of rationing the available stock between meeting the immediate demand and hedging for future shortage. Such a ration would allow the decision maker to best leverage the dynamics of the inventory and pricing strategy to cope with the supply uncertainty. Therefore, we introduce a lever,

Suppose that

For given Suppose for every fixed

If

Lemma 2(i) underscores the complexity of the problem due to the interaction between the pricing decision

5.2 Policy Design

Given that we are facing a dynamic decision-making process, the needed structure of the value function (i.e., the concavity of

Suppose that

If the optimal inventory decision

According to Theorem 3, the value function of the dynamic programing equation is concave for general stochastic demand and supply functions if the optimal inventory decision and the optimal demand decision are monotone in the on-hand inventory level. This monotone property, however, is difficult to verify as it is endogenous, and may not hold in general. Any easy-to-check sufficient condition for the optimal solution to exhibit the monotone property appears restrictive even in the special case when the supply is deterministic (see the discussions by Feng et al., 2020). Thus, we needs to develop an approach to verify whether or not the optimal solution is indeed monotone to apply Theorem 3. In general, the optimal policy may not be monotone (evident from the example in Figure 2). In such a situation, we need to derive an easy-to-implement solution that produces good performance. Our analysis below devices a solution approach that verifies the optimality of a monotone policy, and generates an efficient solution when the optimal policy fails to be monotone.

To enable the analysis of the dynamic program, the value function needs to be concave in the on-hand inventory level so that decisions can be computed efficiently and the desired property of the objective function is retained across periods. Theorem 3 suggests that when a candidate policy exhibits a certain monotone structure, the resulting profit function can preserve concavity to enable tractability.

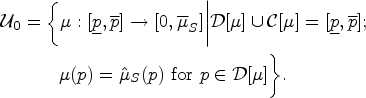

Specifically, we would like to focus on a class of policies, say

Unfortunately, not every element

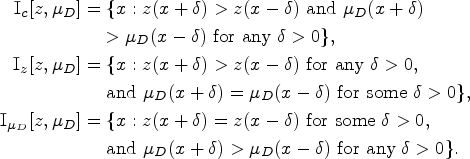

Now define the class of candidate policies For For For For

Thus, a candidate policy in

Suppose that

For any

According to Theorem 4, implementing any policy within the constructed set

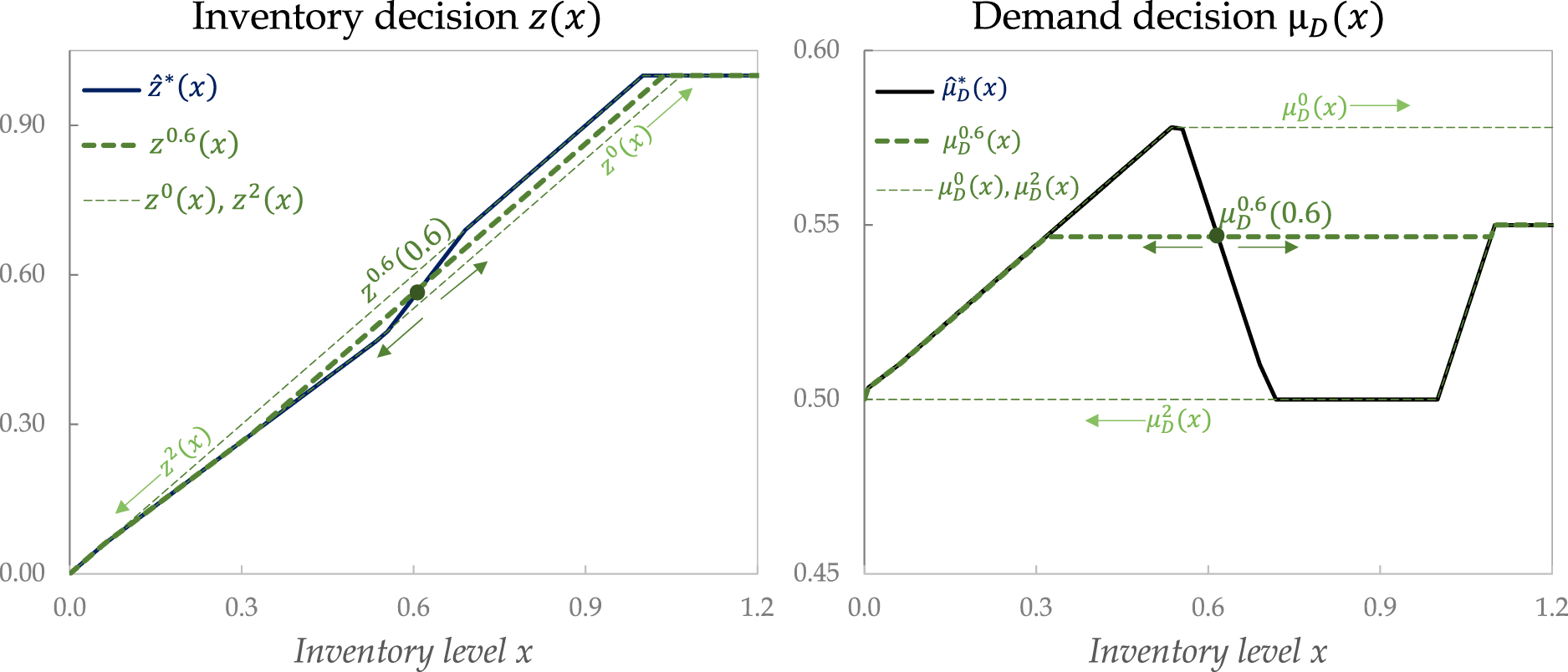

Demonstration of the constructed

Figure 3 also demonstrates two other

A refined policy is a candidate policy, that is,

Theorem 5 confirms that, indeed, the set

It is well-known that even in the special case of deterministic supply, the profit function may not be concave and the optimal policy may not be monotone; see the counterexample given by Feng et al. (2020). Several authors have derived conditions for an optimal monotone policy in this setting. The most recent development is given by Pang (2011), who shows the result by assuming that the demand is additive (i.e.,

In view of this, the result in Theorem 5 provides theoretical justification of our policy construction. Given any problem instance, our approach identifies the optimal policy when it is indeed monotone. In this case, the refined policy becomes independent of

5.3 Policy Performance

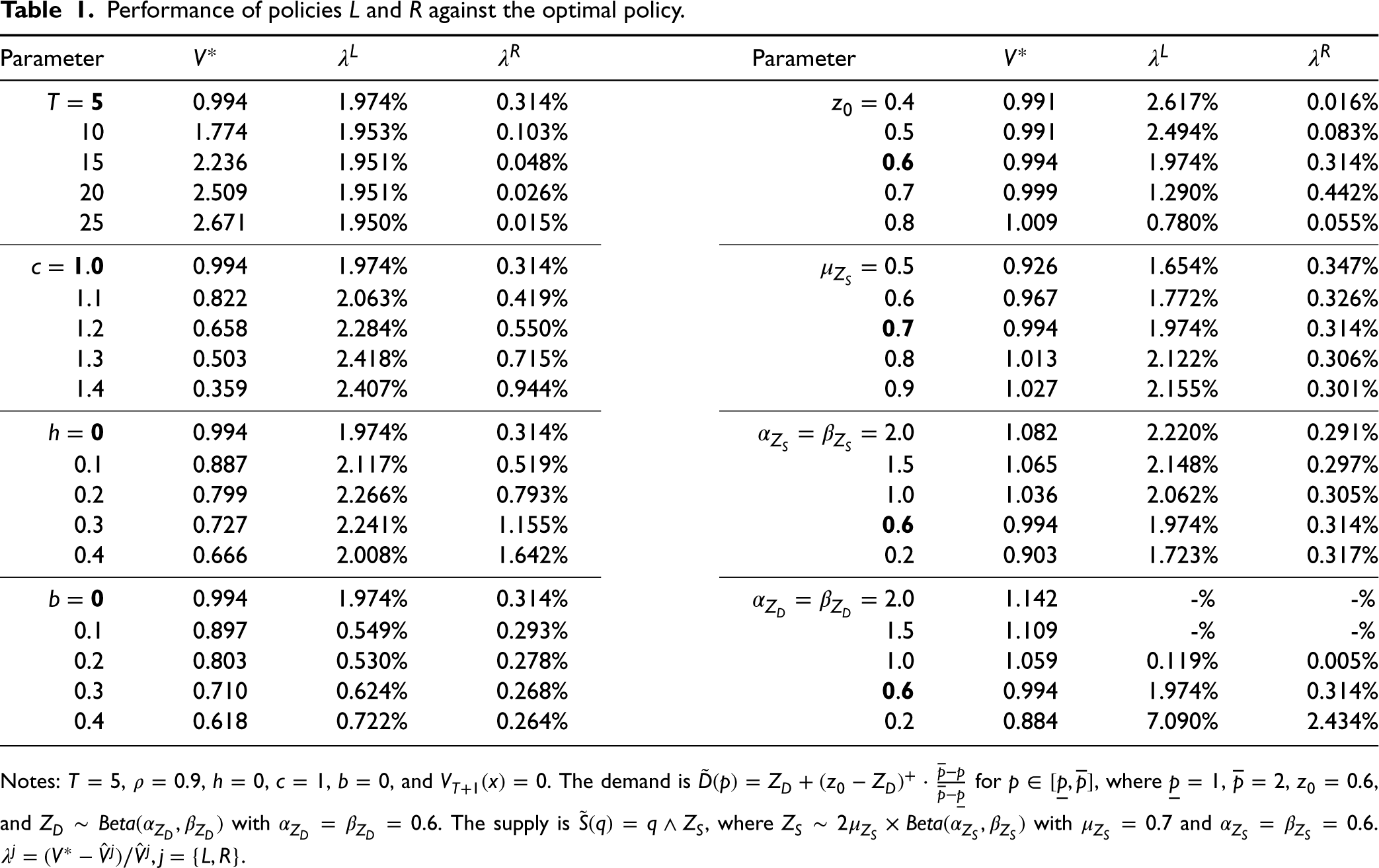

We first evaluate the performance of the policy in the refined set

We use Beta distribution to capture the random noises in the supply and demand functions. This distribution is flexible enough to capture various concentrations of the realizations. In particular, we test Beta distributions with shape parameters

We randomly generate problem instances over a wide range of parameters (see the details described in Remark 1 in Online Appendix EC.2). For each instance, we compute the optimal profit under the truly optimal solution,

To understand how the performance of policies

Performance of policies

Notes:

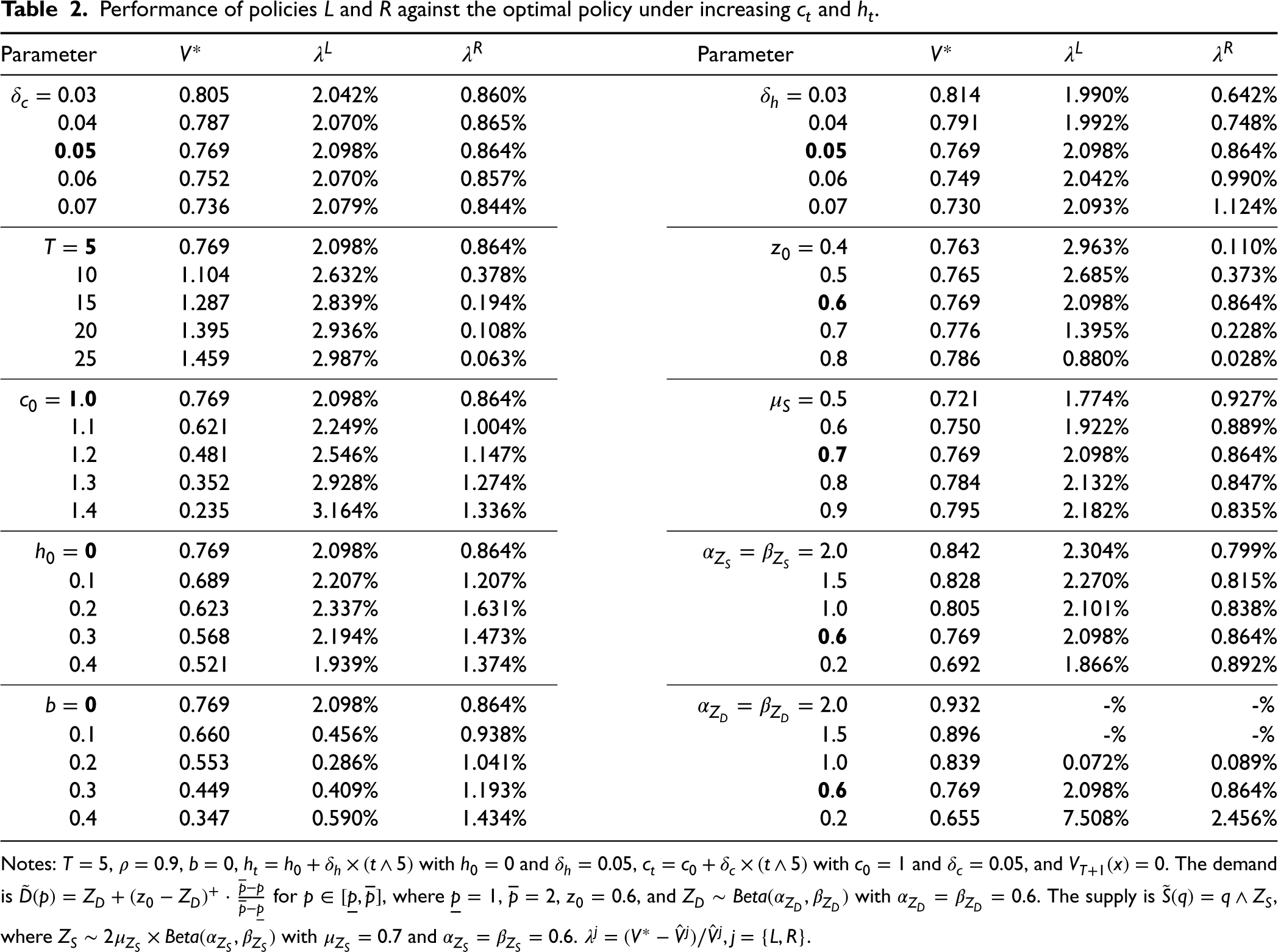

In Table 2, we demonstrate the result for non-stationary cost parameters. In particular, the procurement cost

Performance of policies

Notes:

5.4 The Effect of Lost Sales

A natural question in managing lost demand is: Whether strategies to retain customers through backordering can improve profitability? Our analysis, enabling tractability of the lost-sales model, can be applied to explore the answer. Specifically, we compare the profit under our model and that under demand backorder (Feng and Shanthikumar, 2018). A common assumption imposed in the backorder models, is that a large penalty is charged for any ending backorder. That is,

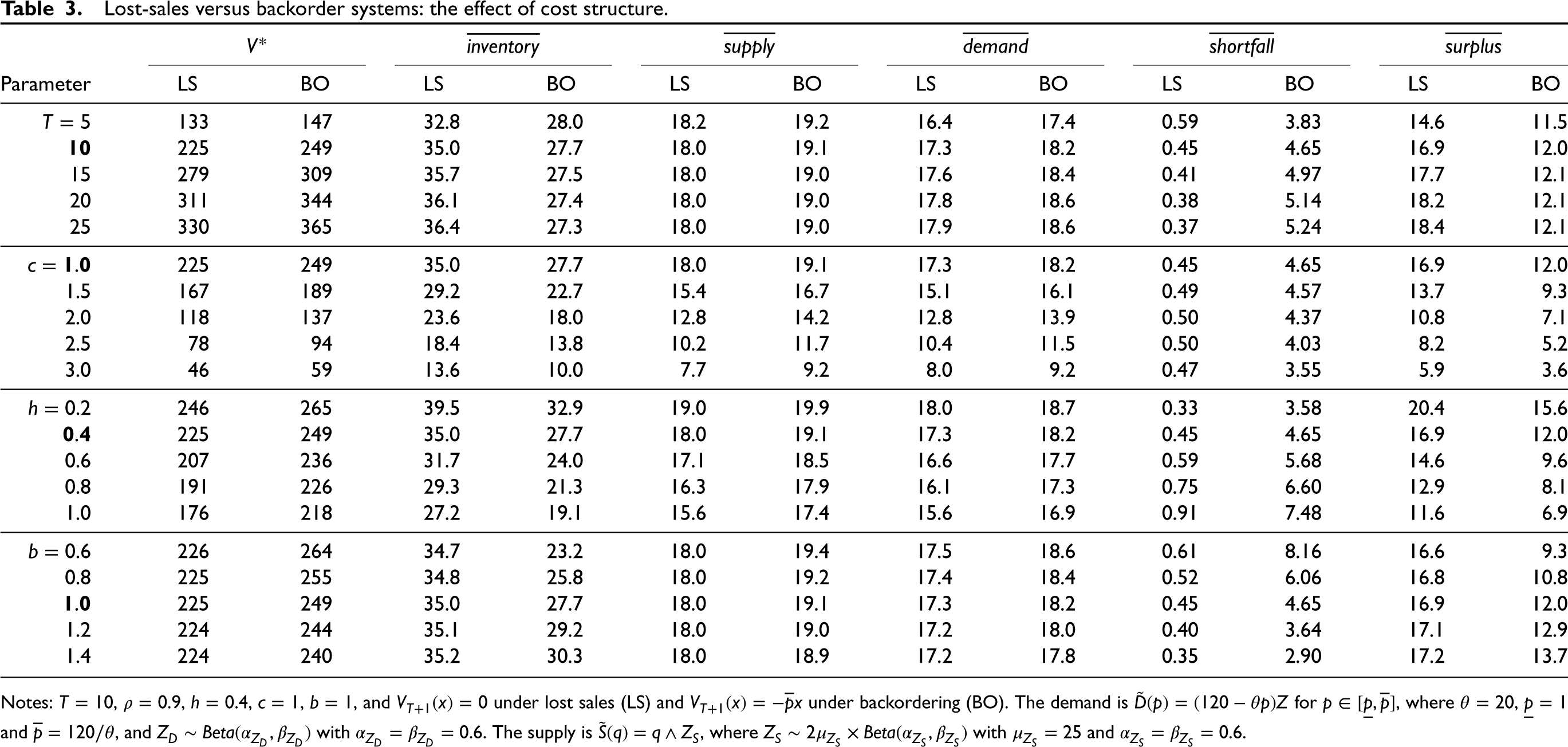

Lost-sales versus backorder systems: the effect of cost structure.

Notes:

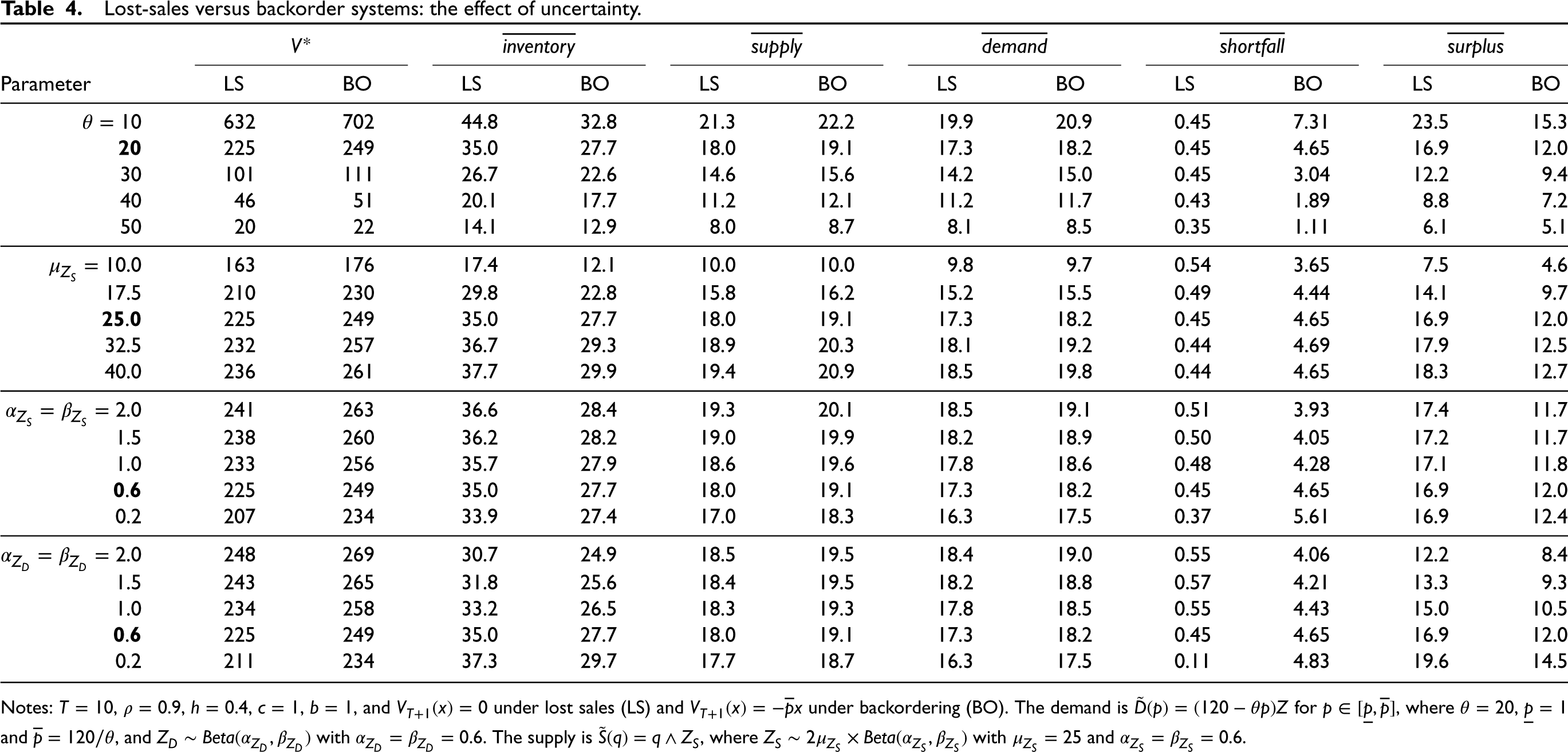

Lost-sales versus backorder systems: the effect of uncertainty.

Notes:

5.4.1 Effect of Cost Structure.

Certainly, the comparison between the lost-sales model and the backorder model depends on the costs of shortfall. To facilitate the comparison, we set the backorder cost to be the same as the lost-sales penalty, though one may expect the former to be smaller than the latter as the goodwill loss would be less if the demand is eventually met.

When it becomes costlier to operate the system (due to an increased procurement cost, holding cost, or shortfall penalty), the optimal policy calls for increased prices or reduced demands under both models. The reduced demands are accompanied with decreased demand uncertainties (as the demand function is decreasing in the dispersive order in the price). These reductions, however, do not necessarily lead to improved supply and demand matching by decreasing the amounts of shortfall or surplus because of supply uncertainties, leading to subtle differences among various cost parameters.

We observe from Table 3 that, when the procurement cost

A higher holding cost

Intuitively, when the cost of shortfall (i.e., the lost-sales penalty or the backorder cost) is the same across the two models, the ability to fulfill the demand with future inventories allows the decision maker to reduce the inventory level, leading to an increased shortfall and a decreased surplus. This intuition is confirmed in all the experiments conducted. Moreover, the average supplies and demands under the lost-sales model are less sensitive to the shortfall penalty than those under the backorder model, while they are more sensitive to the holding cost under the lost-sales model than under the backorder model.

5.4.2 Effect of Uncertainties.

The results in Table 4 suggest that both the lost-sales model and the backorder model exhibit similar responses to the changes of the mean supply (via

Interestingly, the profit difference between the lost-sales model and the backorder model is insensitive to the level of supply or demand uncertainty (the lower panels of Table 4). This suggests that customer retention through backordering generates a certain magnitude of benefit from smoothing the demand and supply matching.

5.5 The Value of Inventory-Based Pricing

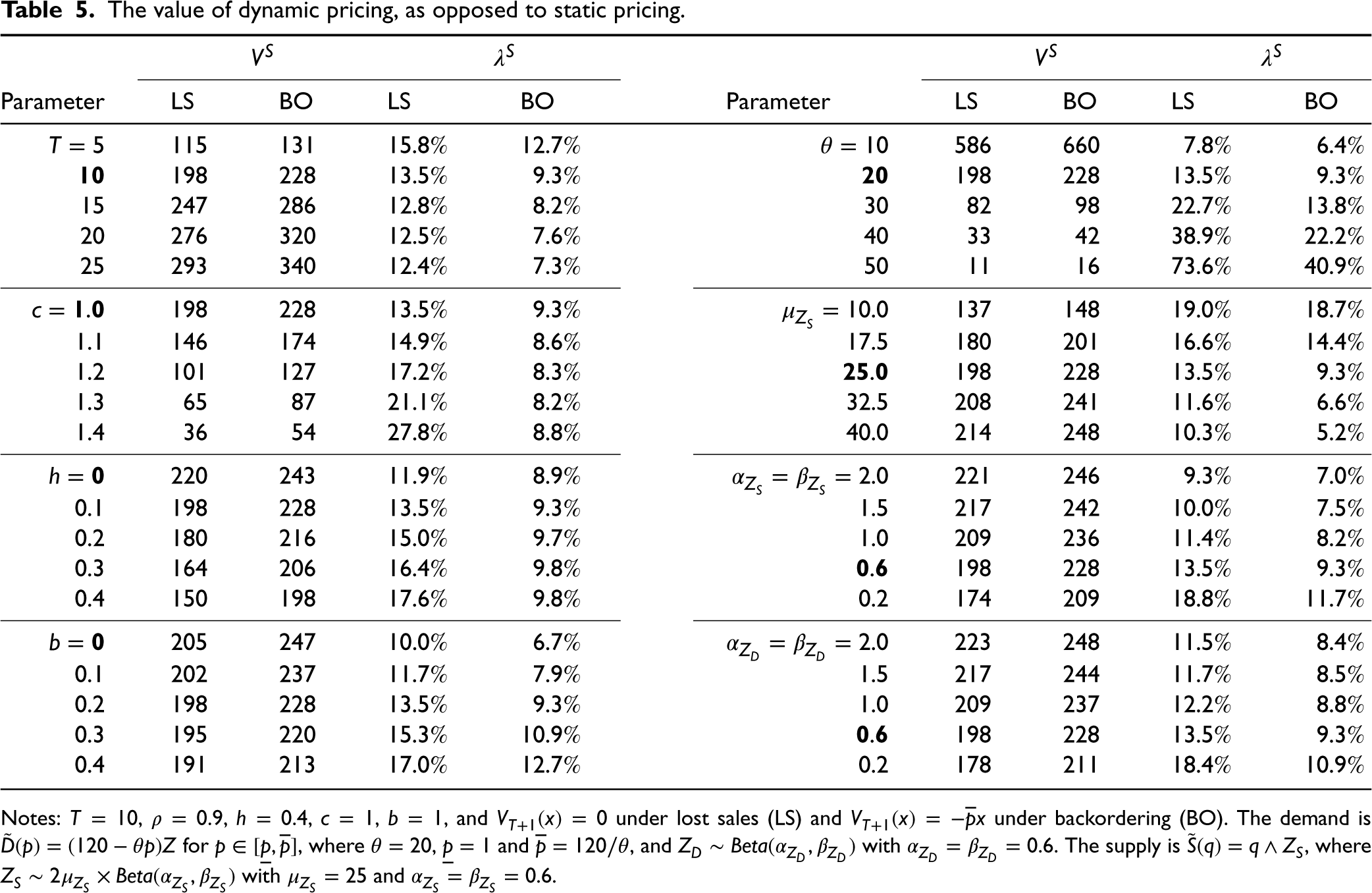

In a stochastic inventory planning system, price adjustments can improve supply–demand matching. When the unmet demand is backordered, Feng (2010) demonstrates that the benefit of dynamic pricing, as opposed to static pricing, can be significant when the supplies are restricted. One would expect a similar behavior in the lost-sales system. To confirm this, we evaluate the value of dynamic pricing as the percentage profit improvement from the optimal profit

From Table 5, we find that the benefit of dynamic pricing becomes larger when the holding cost or the shortfall penalty increases. This suggests that dynamic pricing is more useful when the supply–demand mismatch is costlier. We also observe that the limited supply (induced by a low

The value of dynamic pricing, as opposed to static pricing.

Notes:

Interestingly, the effect of procurement cost

6 Concluding Remarks

We study the inventory and price planning problem involving lost sales and supply uncertainties, a realistic situation that is underresearched. The challenge of the problem lies in the highly non-concave profit function, and the existing approaches developed for the variations of this problem (i.e., under a deterministic supply or under backordering) do not apply to this problem. We propose to restrict the solution space to a class of monotone policies. This policy class is intuitively appealing in practice, as one would expect to allocate more inventory to fulfill the demand and price lower when the on-hand inventory level is higher. We further refine the policy class by defining a subclass of easy-to-compute policies and demonstrate its close-to-optimal profit performance. These developments allow us to examine the effect of lost sales on profit generation and material flow dynamics, as well as the value of inventory-based dynamic pricing.

To our knowledge, this study is the first to examine the coordinated inventory and pricing decisions under both lost sales and supply uncertainties. Our analysis provides a new approach to overcome the technical difficulties in such problems and opens up several avenues for future research. For example, though our extensive numerical experiment suggests efficient performance of the proposed policy and, like in the case of most stochastic dynamic problems, evaluating theoretical performance bounds for the general model is challenging, it is worth exploring the worst-case performance for subclasses of supply and demand functions that are relevant to specific application contexts. Diversifying supplier base through multi-sourcing to mitigate supply risks has been underscored in practice in view of the recent challenges in supply chains. Though an almost threshold policy is known to be optimal in backorder systems (see, e.g., Federgruen et al., 2022), the policy structure for lost-sales systems remains unknown. In many procurement processes, there may be a significant fixed ordering cost. The policy design that accounts for economies of scale under uncertain supplies remains an open problem. Consideration of procurement lead time under a lost-sales system (Chen et al., 2018) is yet another challenging but important issue to be addressed.

Supplemental Material

sj-pdf-1-pao-10.1177_10591478231224916 - Supplemental material for The Effect of Supply Uncertainty on Dynamic Procurement and Pricing Strategies Under Lost Sales

Supplemental material, sj-pdf-1-pao-10.1177_10591478231224916 for The Effect of Supply Uncertainty on Dynamic Procurement and Pricing Strategies Under Lost Sales by Qi Annabelle Feng, Lei Li and J George Shanthikumar in Production and Operations Management

Footnotes

Appendix: Preliminaries on Stochastic Functions

For a monotone function

Because the stochastic comparisons are partial orders, many of the intuitive relations for deterministic values do not necessarily hold. For example, for any two values on the real line, the weighted sum is larger if a larger weight is assigned to the larger value. That is, for

By the construction in Lemma 3, it is easy to see that random variable

The observations from Lemmas 3 and 4 are basic properties that allow us to obtain the needed structures of the decisions to establish the concavity of the profit function for our model. To be able to identify the desired structures of the decisions, we also need to examine how the uncertain demand and supply would respond to the decisions, which requires the notions of stochastic functions. The reader is referred to ![]() for properties and examples of the stochastic functions described in Definition 1. The notions of stochastic linearity and stochastic concavity are much more general than their deterministic counterparts. Many of the almost surely nonlinear functions are linear in the stochastic sense, and many of the almost surely nonconcave functions are concave in the stochastic sense. The notion of

for properties and examples of the stochastic functions described in Definition 1. The notions of stochastic linearity and stochastic concavity are much more general than their deterministic counterparts. Many of the almost surely nonlinear functions are linear in the stochastic sense, and many of the almost surely nonconcave functions are concave in the stochastic sense. The notion of

It is immediate from Lemma 4 that for ![]() , is used in our analysis for the multi-period model.

, is used in our analysis for the multi-period model.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

How to cite this article

QA Feng, Li L, Shanthikumar JG (2024) The Effect of Supply Uncertainty on Dynamic Procurement and Pricing Strategies under Lost Sales. Production and Operations Management 33(1): 108–127.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.