Abstract

Although existing research has extensively explored corporate disclosure, a very little is known about why corporate organisations may remain silent while communicating with their external audiences. This study offers a definition of corporate silence and develops a conceptual framework for the study of silence in the narrative communication of corporate organisations. We develop a typology based on the forms and motivations for corporate silence in written corporate documents. Data was gathered from 26 interviews with senior managers from regulatory bodies, audit firms and listed companies in Pakistan and a grounded theory approach was used for data analysis. We postulate that self-protection from fear and discomfort, cooperation, managerial opportunism, apathy, and resistance are the prime motivators of corporate silence. The analysis also leads to the development of five different forms of silence: (1) defensive; (2) prosocial; (3) opportunistic; (4) authoritative; and (5) counteractive.

Introduction

Silence is a multidimensional concept that can be strategic and meaningful. It may be exercised to achieve a variety of objectives: to resist (Maclure et al., 2010), to maintain the status quo (Shields, 2004), to communicate the existence of power relationships (Pinder & Harlos, 2001) and to protest (Jungkunz, 2012). Silence is also used to reveal and communicating; for example, by not providing required information, a subordinate may reveal their objection to unjust managerial practices, or by not speaking when asked to stay quiet in classroom settings, a student may communicate their respect for teacher. It may also be used to hide information or manipulate through the deliberate concealment of expected or relevant information to the reader/listener (Huckin, 2002). In certain instances, empty speech is utilised, wherein words are communicated without providing any real information (Ephratt, 2011). The concept of silence has received little attention, however, as it is considered the absence of speech, and the study of what is absent remains largely unexamined (Van Dyne et al., 2003). While an emerging body of literature on management and organisational research has focused on silence as a powerful mode of meaningful communication (Donaghey et al., 2011), the study of silence has failed to receive due attention within the corporate communication research, where the analysis of what organisations disclose remains the general focus of the study (Rescher, 1998, p. 91) and little attention is paid to why and how organisations may remain silent on various issues.

Although a number of scholars have explored the concept of silence within organisations (Grey & Costas, 2016), only a few studies explored silence in external corporate communication. This lack of emphasis on silence in the external corporate communication research has resulted in a deficiency in the development of any relevant conceptual or theoretical frameworks and the subsequent shortage of relevant empirical research within the field. We argue that the study of corporate communication research has limited itself to the use of reductionist approaches (such as content analysis) for the study of corporate disclosure. Under the influence of such research, regulators focus on the disclosure of more information, thus entirely ignoring the idea that the absence of information in itself can be a source of information. Since there is a lack of research on the study of silence in corporate communication, the motivations for silence within corporate discourses remain unexplored. In addition, the studies exploring the concept of silence in corporate communication were carried out in developed countries and there is a lack of research in the context of developing countries. This context is particularly important for the study of corporate silence as developing countries exhibit a high level of interference of politically powerful elite in corporate sector whereas power is one of the prime motivators for silence (Buhr, 2001). Furthermore, many developing countries have highly concentrated capital markets (Rwegasira, 2000) characterised with high level of family ownership (Siddiqui, 2010) where protection of collective interests and community spirit are considered supreme. Study of corporate silence is considered appropriate in such contexts as literature suggests silence facilitates protection of collective interests, helps in maintaining the status quo and prevents harm to the group and community cohesiveness (Morrison & Mikkilin, 2000). Therefore, we considered it appropriate to carry out this research in a developing country setting, namely Pakistan. In this regard, through a grounded theory analysis (Strauss & Corbin, 1997, 1998) of data collected from 26 semi-structured interviews, this study investigates what the forms and motivations for silence are within corporate communication in the context of a developing country – Pakistan.

Given the nature of the research question, we conducted field research to theorise about corporate silence. We conducted 26 interviews with experts in the field of corporate communication/disclosure to identify the factors driving corporate silence in Pakistan. Our study makes a contribution by advancing the existing conceptualisation of corporate silence through identification of various motivations for corporate silence. Furthermore, based on these motivations, it develops various forms of corporate silence and presents a theoretical framework for the study of silence within corporate communication. Finally, it provides empirical evidence on how various factors contribute towards corporate silence in the context of a developing country with a high level of political connectedness. Thus, this study proposes a framework that can be used as a guide by both academics and practitioners to study and analyse corporate organisations’ motivations when making non-disclosure decisions.

We begin our discussion by reviewing the existing literature before elaborating on our research methodology. Finally, we develop a framework for silence in corporate communication and then present our conclusions.

Literature Review

Silence in Accounting Communication

Research on why and how organisations choose to remain silent in their external communication is somewhat limited (Merkl-Davies & Brennan, 2017). The existing literature contends that corporate organisations use such techniques as selectivity (Merkl-Davies & Brennan, 2007) or selective disclosure (Marquis et al., 2016), whereby the disclosure of only selected information is made while ignoring/omitting pertinent unfavourable information. This strand of literature explains how managers conceal bad news while emphasising positive information (e.g., Kothari et al., 2009; Milgrom, 1981; Verrecchia, 1983), and attributes the concealment of information to managerial opportunism and managers’ career concerns (Nagar, 1999; Nagar et al., 2003) as owners may replace managers based on information pertaining to their poor performance (Hermalin, 2014).

It is pertinent to note that these studies have investigated ‘selectivity in the presentation of information’ rather than ‘selectivity in the non-disclosure of information’ (Leung et al., 2015, p. 276) and so focus on the level of and motivations for disclosure rather than on non-disclosure. The assumption that what is known about disclosure fully applies to intentional silence is problematic (Van Dyne et al., 2003). What fuels and motivates disclosure does not necessarily motivate intentional silence. The disclosure behaviour of an organisation that provides extensive corporate disclosure within their annual report may be explained using various perspectives on disclosure, such as legitimacy or signalling. The same organisation may simultaneously choose to remain silent on various other material issues owing to a variety of other reasons and the nature and extent of the silence of that organisation cannot be understood by assessing its disclosure behaviour (Brinsfield, 2013). While some of the motivations for disclosure and non-disclosure might intersect (such as managerial opportunism), other motivations might differ significantly.

Therefore, we further reviewed the literature on non-disclosure/silence rather than disclosure. Of the studies that attempted to investigate the motivations for silence and non-disclosure, Leung et al. (2015) is particularly noteworthy, as it defines textual non-disclosure as an attempt to conceal discretionary narrative information and so prevent it from entering the readers’ minds. Leung et al. (2015) studied narrative disclosure in listed Hong Kong companies and found that they used the minimal narrative disclosure of pertinent information about poor performance as a technique for both concealing opportunistic and self-serving managerial behaviour and managing external impressions. In another study, Chwastiak and Young (2003) investigated how corporations use silence as a tool to hide the negative impact of their environmental practices within annual reports and found that corporations focus on defining success within terms of corporate profitability while remaining silent on such issues as humans’ dependency on the earth and nature, overpopulation, and animal cruelty. In another pertinent study on silence in corporate communication, Hollander et al. (2010) examined the silence of managers during conference calls and found that they provide inadequate information to investors. Similarly, Belal and Cooper (2011) investigated the motives behind the absence of corporate social reporting in Bangladesh and found that bad publicity, poor performance, a lack of regulation, the profit imperative and a lack of awareness are the reasons for the absence of such information.

As we analysed the literature, we noticed that the existing research focused on opportunism/impression management and power and adopted a very narrow perspective of the silence of corporate organisations. Our review of the literature highlighted that none of the studies echoed alternative theoretical or conceptual aspects that might be uniquely relevant in motivating silence within corporate narratives; for example, the silence of powerlessness, signifying resistance to authority and control, the apathy and arrogance of the powerful, altruistic motivations to benefit affiliates, confrontation avoidance, threat and protection against perceived dangers. We suggest that a lack of emphasis on the theoretical foundations of corporate silence is a major reason why it is so poorly understood within the existing literature (Leung et al., 2015).

In sum, the review of literature highlighted that existing research focuses on the examination of disclosure practices in corporate communication while there remains a lack of emphasis on the study of corporate silence which consequently results in a very few studies incorporating relevant theoretical and conceptual models. Within this context, and in order to contribute to this gap, the aim of the present study is to advance the conceptual understanding of corporate silence. We develop a conceptual framework in the form of a typology based on motivations and forms of silence in corporate communication. The research question can be formulated as: what the forms and motivations for silence are within corporate communication in the context of a developing country – Pakistan.

Conceptualising Silence in Corporate Communication

In this study, we explore the meaning, motivations and forms of corporate silence. We acknowledge the existing conceptualisations of silence within a variety of disciplines such as management and organisational research and expand upon the existing literature through the development of a new framework. In line with Van Dyne et al. (2003), we focus on the forms of purposeful silence that result from corporations’ deliberate decision to withhold relevant and expected corporate information, only when they hold such information. Furthermore, we focus on corporate silence within their communication with external parties. We also clarify that this research focuses on discretionary and soft law disclosure, where a corporation's decision to stay silent is either completely discretionary or will be met by little regulatory oversight. We specifically focus on corporate silence in communication with external parties because (i) there exists an emerging body of literature that investigates silence in the communication among internal stakeholders within organisations and (ii) despite an increased call for disclosure and transparency by the regulatory bodies as well as investors and society, the non-disclosure of corporate information is not uncommon while the motivations behind it are poorly understood in the existing literature. Silence in corporate communication is worth exploring as deliberate silence on material information can potentially mislead investors, regulators, and society and result in economic, social and environmental losses (Leung et al., 2015).

We also consider it important to clarify that, while we identify the motives for silence based on the existing literature and empirical data analysis, we also realise that silence can be based on other, additional motives. Therefore, while we develop a framework for silence in external corporate communication, we do not suggest that it is a comprehensive model. Rather, we present it as a first step towards the development of a more refined conceptualisation of corporate silence in future studies. We also clarify that the contexts within which silence takes place are critical for interpreting its prevalence, meaning and significance (Pinder & Harlos, 2001). Thus, the various forms of and motives for silence presented in this framework may be more or less relevant in differing contexts. Thus, while this study is a first attempt to present a framework for corporate silence based on different forms of and motives for silence, it also calls for further research to develop and refine the framework.

Definition of Silence

According to the existing literature on the field of management science, silence arises when the receivers of information are not provided with either sufficient information or any signal appropriate for them to comprehend the meaning of information that is known by the withholder (Paulston et al., 2012). Pinder and Harlos (2001) conceptualise silence at an individual level and define it as the withholding of a genuine expression about an individual's behavioural, cognitive and/or affective evaluations regarding the organisational circumstances. On the other hand, Morrison and Milliken (2000) conceptualise silence as a collective rather than individual phenomenon, whereby employees collectively withhold their expressions about potential organisational problems. Knoll and Dick (2013) defined organisational silence as employees refraining from drawing managerial attention towards illegal or immoral practices that may violate the personal, legal or moral standards. Although all of these approaches differ with regard to their level of analysis, the withholding of information remains the vital factor.

We suggest that corporate silence (or disclosure) results from a deliberate decision-making process, as corporate narratives are drafted by corporate experts and approved with the consent of the members of the board, with the aim of constructing a picture of an organisation for the external stakeholders (Stanton & Stanton, 2002). Corporate managers make assessments about the corporation's relationships with various stakeholder groups and the power held by those groups. The managers strategically determine their level of accountability to those stakeholder groups, which ultimately informs their disclosure/non-disclosure decisions (Shocker & Sethi, 1974). Thus, corporate reporting not only reflects the corporation's own moral construction but also the moral standing and choices of its managers (Schweiker, 1993). Since the voice of an organisation cannot simply be attributed to the voice of any single manager, it is more plausible to approach the voice/silence of a corporation by observing its social construction and studying its relationships with various stakeholder groups (Buhr, 2001).

Therefore, we define corporate silence in external communication as the purposeful withholding of information by corporate organisations about the circumstances of the firm from those stakeholders who may be expecting to receive such information, may be interested in such information or may be affected by the concealment of such information. Based on the prior literature, corporate silence entails the withholding of the information that is expected to be disclosed by corporate organisations and includes all of the information that is required to be disclosed according to the regulations, as well as any information that might be material for the corporate stakeholders, the disclosure of which they would expect (Talesnick, 1972; Buhr, 2001; Hollander et al., 2010). The non-disclosure of all such information is regarded as silence.

Motivations for Silence

The existing literature has identified various motivations for silence. Silence can be a response to social injustice, signifying resistance and objection (Cohen, 1990; Parker & August, 1997; Pinder & Harlos, 2001; Stephens & Gwinner, 1998). Pinder and Harlos (2001) presented the idea that silence is multi-faceted and multidimensional and can be caused by a number of factors. They contended that in the contexts of injustice, silence can be classified in to two forms, that is, quiescence and acquiescence. They defined quiescence as deliberate act of omission where one is dissatisfied with the circumstances, and can voice their opinion to change status quo, however they have not voiced their opinions yet. This is the state where they are suffering in silence. Acquiescent silence, in contrast, represents a complete acceptance of injustices, whereby no assessment is made of any alternatives and breaking silence is never considered an option for changing the status quo (Pinder & Harlos, 2001). This occurs when voicing an opinion is perceived as futile, unwelcome or even dangerous (Morrison & Milliken, 2000). Alternatively, Van Dyne et al. (2003) developed a model that postulated resignation, fear and cooperation as the prime motivators for acquiescent defensive and prosocial silence forms of silence respectively.

We also found that the existing research on accounting communication has identified two prime motivators for silence: power (or the lack thereof), and managerial opportunism. Perceptions of the unequal distribution of power influence the decision whether to voice an opinion or remain silent (Morrison & Milliken, 2000). One strand of literature, on power and discourse presents silence as both the production (Lingard, 2013) and a sign of ‘power as well as of the lack of it’ (Benthien, 2006, p. 158). Brown (1996) argued that power is not a precondition for silence, and that it might be exercised by either the powerful or the powerless. As explained by Foucault (1978), discourse not only reinforces power but also undermines and exposes it while making it fragile. Silence has the capacity to engage the powerful and the powerless by serving either as a ‘shelter for power’ or a ‘shelter from power’.

Buhr (2001) elaborates on the dynamics of power and silence and presents arguments derived from social contract theory (Shocker & Sethi, 1974), wherein the social contract signifies the relationship between an organisation and various social stakeholder groups. Some of these groups offer economic, social and political benefits that are essential for an organisation's survival and growth. The organisations make an assessment about the potential of various social groups to harm or benefit them and will ignore the information needs of groups that are assumed to be harmless or powerless (DiMaggio & Powell, 1983). The avoidance of disseminating information to powerless groups thus becomes a ‘viable strategic alternative’ for corporations (Oliver, 1991). Buhr (2001) presents power as a key determinant of accountability and contends that there is a lack of accountability between corporations (being advantaged and powerful) and the public (being disadvantaged and powerless), resulting in the absence of social and environmental disclosure.

Scott (1990) presented the concepts of public transcripts (voice) and hidden transcripts (silence) while conceptualising silence. If an individual maintains a happy face as their public transcript, while their hidden transcript reflects contempt and resentment against the organisation, the level of disparity between their transcripts is very high. The larger this transcript gap, the higher the level of perceived powerlessness. Thus, high levels of silence indicate lower levels of power.

Chwastiak and Young (2003) discuss how language is used to promote beliefs that legitimise the interests and actions of powerful social groups. They contend that the dominant discourse enables the promotion of such values that support the supremacy of the powerful elite, while justifications are provided for the injustice arising from the unequal distribution of wealth and power. Since social injustice is normalised through the dominant discourse, it becomes increasingly difficult to question the underlying systems of power (Giroux & McLaren, 1992; Hall, 2005). The dominant discourses make people believe that social injustice is either beneficial or not injustice at all, and that silence on such injustice enables people to accept and live with the more objectionable aspects of society.

A number of other studies have adopted an impression management perspective and explain managerial opportunism and self-interest as the prime motivators for silence. This strand of literature suggests that corporate managers present selective information within their corporate disclosures to distort the receivers’ perceptions of their firms’ performance and future prospects (Aerts, 2005; Brennan et al., 2009; Courtis, 2002, 2004; Merkl-Davies & Brennan, 2007). Leung et al. (2015) contend that firms use the selectivity of information to conceal poor financial performance. Thus, firms facing high levels of financial distress and poor performance disclose lower levels of information.

Hollander et al. (2010) explain that agency conflicts, proprietary information and litigation risk are the main drivers of incomplete corporate disclosure. From an agency theory perspective, managers are the holders of superior information and will avoid the public disclosure of such information if such an action would not suit their interests. A lack of inside information makes it difficult for outsiders to discipline managers for their opportunism (Shleifer & Vishny, 1989). Similarly, managers are also reluctant to share proprietary information, as the disclosure of such information to competitors may potentially harm the firm, so managers make a close assessment of the costs and benefits attached to the disclosure of such information. Hollander et al. (2010) also note that a fear of litigation can either encourage managers to provide timely, complete information to avoid legal action or discourage disclosure, as managers may fear penalties if they disclose misleading, conflicting or controversial forward-looking information (Healy & Palepu, 2001).

Forms of Silence

Various researchers have argued that conceptualising silence as a unidimensional concept could result in critical differences being ignored regarding various motivations for withholding information and, consequently, the existing literature has conceptualised various forms of silence on the basis of the different types of motives for silence (Knoll & Dick, 2013; Pinder & Harlos, 2001; Van Dyne et al., 2003). According to this approach, it is the underlying motives that guide organisations to engage in silence and lead to phenomenological differences existing between the various forms of silence (Brinsfield, 2013). Here, we will draw upon the conceptualisations offered by Pinder and Harlos (2001), Van Dyne et al. (2003), and Brinsfield (2013) to provide description of various forms of silence.

In the forms of silence introduced by Pinder and Harlos (2001) quiescence is driven by fear, anger, despair, depression and cynicism, while acquiescence silence is motivated by resignation (Pinder & Harlos, 2001, p. 350). Van Dyne et al. (2003) developed a model that postulated that resignation, fear and cooperation are the main motivators for silence. Based on these three motivators of silence Van Dyne et al. (2003) outlined different forms of silence (acquiescent silence, defensive silence, and prosocial silence). They postulated that acquiescent silence is a product of neglect and inaction (Farrell, 1983) while defensive silence is caused by self-protective behaviour. This form of silence is consistent with quiescent silence, entailing the deliberate omission of information in order to protect oneself from any negative consequences of disclosure. Prosocial silence entails withholding relevant, significant information for altruistic motives; that is, to benefit others – whereby one makes an assessment of the situation and the decision to remain silent is deliberate and conscious in nature. ‘For example, an employee may not file a complaint against a colleague who is involved in misconduct at workplace.’ Although both defensive as well as prosocial silence aim at withholding information to prevent undesired outcomes arising due to speaking up, the former is motivated by self-protection while the latter by other-oriented behaviour.

Brinsfield (2013) proposed that the process of silence is initiated by various factors that motivate one to speak, such as injustice, a desire for change or witnessing misconduct. The motivations to stay silent, such as fear, an individual's propensity to speak/stay silent, self-esteem and cultural factors, however, co-exist with and even counteract the motives to speak.

To conclude, the existing literature on the forms and motivations of silence has focused on how and why silence is practiced by individuals, within organisational settings. There is a limited literature on corporate silence in communication with external stakeholders and this literature uses theoretical lenses of power and opportunism for exploring the motivations for corporate silence. This paper expands on this literature by presenting alternative motivations for corporate silence in their communication with external stakeholders. These motivations include resistance to power, display of power and a concern for peer organisations.

Methodology and Data

The Context of the Research

As discussed in ‘Literature Review’ section, power is one of the prime motivators for silence (Buhr, 2001). The powerful elite makes use of language to promote beliefs that legitimise the interests and actions of powerful social groups (Chwastiak & Young, 2003). In order to analyse how the powerful elite may use silence in external communication to their benefit, we considered it appropriate to conduct this research in a country that displayed a significant proportion of corporate political connectedness. There is a close linkage between politics and business in Pakistan. Political families in Pakistan actively participate in corporate sector by owing and controlling corporate organisations (Saeed, 2013) and are directly involved in making decisions about corporate (non)disclosure. The existing literature indicates that politically connected companies conceal bad news (Piotroski et al., 2015), provide more opaque, less informative accounting information (Fan et al., 2014), disclose poor quality information about their earnings (Harymawan & Nowland, 2016), manipulate accounting disclosures without being effectively penalised for this (Yusuf & Yousaf, 2019), and make it difficult to forecast a firm's earnings accurately (Chen et al., 2010). This strand of literature examines the disclosure practices of companies based on the level and quality of the information provided, however, and there is a lack of research on what remains undisclosed.

Pakistan makes a particularly interesting case for the study of corporate silence, for several reasons. First, political connections are a dominant feature of Pakistan's capital market, while politicians are known to exert a significant influence on the corporate sector (Khwaja & Mian, 2005; Saeed et al., 2016; Yusuf & Yousaf, 2019). Second, owing to the underdeveloped capital market, the absence of strong legal institutions and inadequate institutional support, businesses in Pakistan tend to develop political connections as a strategy for overcoming market failure (Saeed, 2013). The majority of the companies in the Pakistani capital market are family-owned and -controlled, with a very small proportion of minority shareholders. These companies did not enlist on the stock exchange to raise equity; rather, to develop a strong stock market with a large number of listed companies the Government of Pakistan offered certain tax benefits to those companies that were listed on the stock exchange. Therefore, the owner-managers of family-owned, unlisted companies decided to float the company's shares on the stock market in order to obtain tax relief (Yusuf et al., 2018). Since these companies still rely on bank financing to raise capital, their controlling owners wield enormous power while the minority shareholders’ rights can easily be exploited. Family relationships also heavily influence the political environment in the country, and many of the politically connected families hold majority ownership in these listed companies. Politicians, when connected to corporate sector often involve in shirking, sharking and rent seeking (Riahi-Belkaoui, 2004), and extend favours to their acquaintances through nepotism, bribery and political support (Bushman et al., 2004) which leads to aggressive managerial opportunism in politically connected firms.

Similar to many other developing countries, Pakistan initiated economic and governance reforms under the influence of international donor agencies such as the International Monetary Fund (IMF) and World Bank (Gordon, 1996; Reed, 2002; Siddiqui, 2010). Companies in Pakistan are also required to adhere to the International Financial Reporting Standards (IFRS) to ensure the transparency and consistency of their corporate reporting, while Pakistan introduced its Code of Corporate Governance in 2002. Non-financial listed companies are regulated by the Securities and Exchange Commission of Pakistan (SECP), and the stock exchange, and listed companies in Pakistan must comply with the various statutory corporate laws and codes, including the Companies Act (2017), the listing regulations and the Code of Corporate Governance, while the Pakistani code of corporate governance closely resembles the UK's corporate governance guidelines (Khan, 2016). Initially, the SECP introduced the Code of Corporate Governance as a soft law, compliance with which was not mandatory. However, the SECP has been introducing amendments in the Code over the years and expectations regarding the extent and quality of disclosure are now gradually increasing. The business sector in Pakistan avoids transparency due to the large number of undocumented transactions (Tahir et al., 2012), while the high level of political corruption enables politicians to extract rents from the corporate sector and avoid making disclosures (Saeed, 2013; Yusuf & Yousaf, 2019).

Data Collection

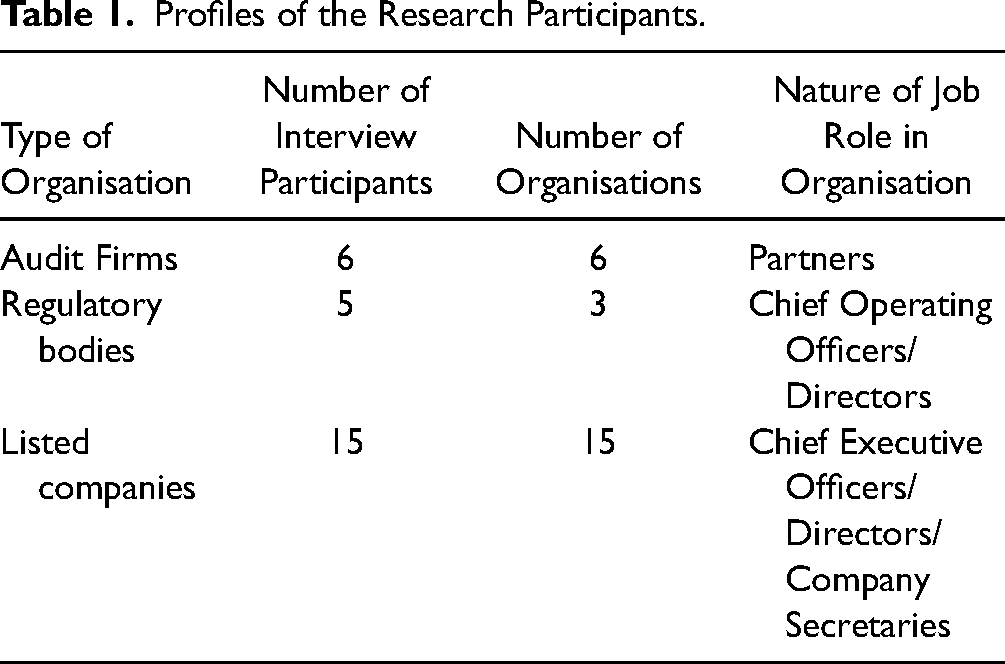

The study involved the collection of primary data through conducting semi-structured interviews with 26 participants from the capital market in Pakistan. The informants were chosen purposefully in order to capture different perspectives on the practices related to corporate silence. The initial interviews were conducted using the existing professional contacts of one of the researchers. Later, further suitable participants were identified using the snowball sampling technique, whereby the initial interviewees were asked to recommend one or more additional potential research participants. We collected data from each of the participant groups that were directly involved in the corporate decision-making or regulatory processes concerning corporate communication and so were in a position to provide theoretically relevant information. All of the participants had at least five years of experience of working in their respective organisation. All held key positions in listed companies, audit firms or regulatory bodies and were closely involved in either the formation of the annual report (i.e., 15 representatives from 15 listed companies) or the auditing/analysis of the annual report disclosures (six partners from six audit firms and five members from three regulatory bodies) and so were in a position to provide context-rich perspectives concerning the phenomenon under study. The pseudonyms developed for our interviewees incorporate a reference to each of these participant groups. Each participant is given a ‘C’ for corporate sector, ‘P’ for partner in audit firm or ‘R’ for a representative from regulatory body, followed by the number of interview being conducted from each participant group. We stopped collecting data from additional participants in each group once the point of theoretical saturation had been reached regarding all theoretical categories.

Table 1 summarises the positions held by the participants and the types of organisations.

Profiles of the Research Participants.

On average, each interview lasted approximately an hour. All of the interviews were recorded with the permission of the interviewees and conducted in English. The interview questions were designed to promote lengthy, open-ended conversations that would allow the emergence of new categories (Farooq & de Villers, 2019). The representatives from listed companies were asked how they made decisions concerning what to disclose (or not) while preparing written corporate communication documents, who made such decisions, whether there were any particular types of information that they might be reluctant to disclose, and the reasons and motivations for such reluctance. The partners of the audit firms were asked to state their own observations and experiences relating to corporate (non)disclosure while auditing the accounts of listed companies, who (in their opinion) were the most important powerful people within the companies in regard to the corporate communication decision-making, and the nature and type of the motivations for the decisions concerning non-disclosure. Finally, the representatives from the regulatory bodies were questioned about their satisfaction with the existing level of corporate disclosure in the country, the response of the listed companies towards the changes in what was expected to be disclosed, the need to introduce more stringent disclosure regulations, and the reasons and motivations for the potential reluctance to disclose. The interviews were conducted by one of the researchers who is from Pakistan and familiar with the context of the country, a familiarity that enabled the researcher to ask follow-up questions and gain an in-depth understanding of the topics discussed.

Data Analysis

We utilised a grounded theory methodology to analyse the data (Perera et al., 2018; Strauss & Corbin, 1997, 1998). Instead of using a traditional grounded theory approach, as suggested by Glaser (1978), which focuses on discovering the underlying theory exclusively from the data analysis, we used the grounded theory analysis proposed by Strauss and Corbin (1997, 1998). As suggested by Corbin and Strauss (2015) this approach allows researchers to read the prior literature with the aim of enhancing their ability to understand pertinent nuances within data. According to Corbin and Strauss (2015), drawing on the literature for comparisons and sensemaking can be particularly useful if researchers find themselves stuck while analysing data. The literature is not to be used as data, however, but merely to derive comparative dimensions for examining the data. Following this approach, we studied all of the relevant literature on silence (section ‘Literature Review’), which literature review provided us with initial insights, a sense of direction and a useful list of the existing concepts within the field. As we embarked on the data analysis, however, we remained open to the new ideas and concepts that emerged from the data. In the words of Corbin and Strauss (2015), during the data analysis process, we drew upon what we knew to help us to understand what we did not know.

We embarked on the process of data analysis immediately after conducting our first interview. The researchers iteratively read the interview transcripts line-by-line, which helped us to gain a basic understanding of the key issues. Later, during the open coding process, we analytically developed the categories and subcategories while reflecting on the similarities/differences between the various open codes. The process of the open coding was divided into five coding sessions, where data from five to six interviews were independently coded by each researcher. We identified the open codes and then compared our results to resolve any discrepancies.

In the following step, we developed detailed dimensions of various categories and subcategories while identifying the relationships between them. During this process, we continuously compared and contrasted the open codes that each researcher had identified and also drew upon the theoretical frameworks described in prior studies for the purpose of making theoretical comparisons (Corbin & Strauss, 2015; Strauss & Corbin, 1997, 1998). During this process, we also reformed and refined some of the categories provided in those frameworks and integrated them into our own, in addition to creating new categories. We analysed the relationships between the categories and subcategories through axial coding and developed new categories or further refined the existing ones. Finally, during the selective coding process, we developed the building blocks for our conceptual framework (Perera et al., 2018; Strauss & Corbin, 1998).

Findings

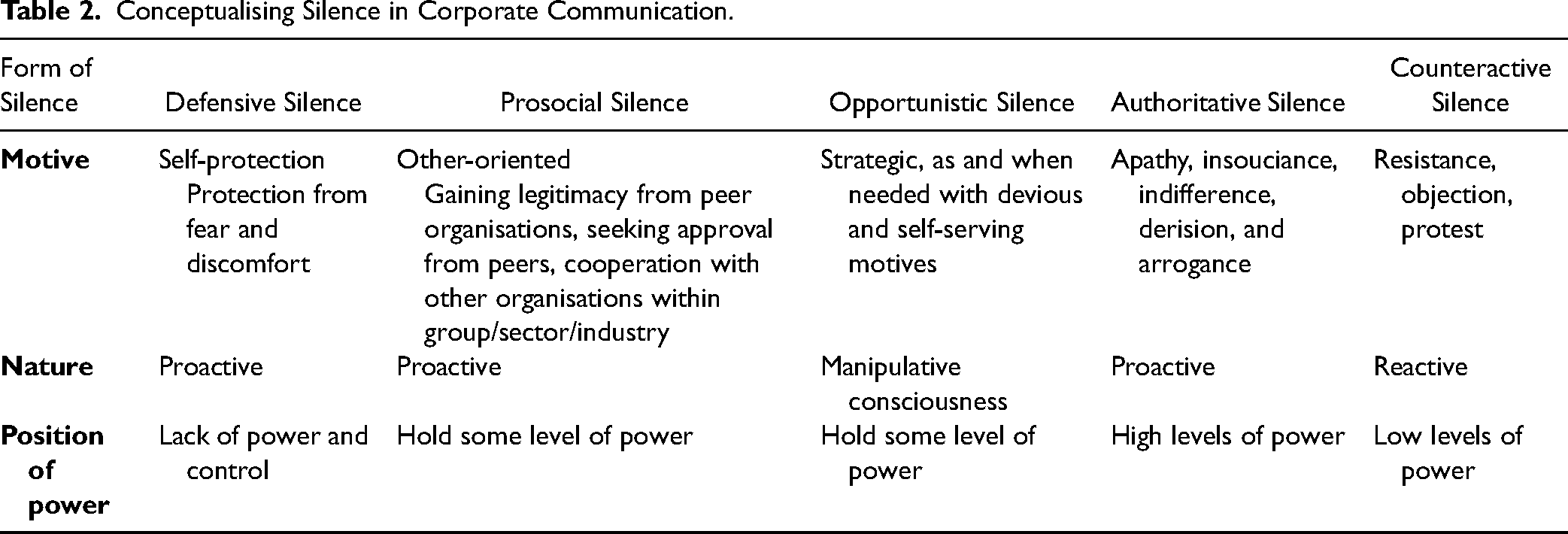

Table 2 presents the theoretical framework developed from an analysis of the research data. The table indicates that silence is a function of various corporate motives. Depending on these motives, corporate firms decide either to remain completely silent on certain issues or to engage in empty speech. The table depicts five distinct motives for corporate silence, namely: self-protection, altruism and cooperation, managerial opportunism rooted in self-serving behaviour, apathy and arrogance, and resistance. The table also shows that these distinct forms of silence lead to the development of five different forms of silence, namely: defensive, prosocial, manipulative, authoritative and counteractive. Table 2 also expands on the position of power held by corporate organisations while they engage in each form of silence. The table further indicates whether corporate managers engage in a particular form of silence with a proactive, manipulative or reactive intent.

Conceptualising Silence in Corporate Communication.

We also clarify that we have purposefully simplified the forms of silence in our framework to allow for and amplify the comparisons. Therefore, although our framework represents five sets of motives (drawn from both the existing literature and our research data), we realise that silence can be based on other, alternative motives. We also contend that silence often represents a complex combination of motives, and various motives for silence might not be mutually exclusive regarding the silence of a particular organisation. Below we provide a detailed account of our analysis while we elaborate on the forms of and motives for silence presented in Table 2.

Defensive Silence

Our data suggest that corporate organisations sometimes anticipate undesirable outcomes in response to the provision of information so the corporate management may strategically display self-protective behaviour while taking the safe, secure decision of assuming less responsibility, eventually resulting in silence. More specifically, corporate firms feel threatened by unwanted interference by the regulatory bodies, as the disclosure of information could potentially result in increased scrutiny by various regulatory departments. A representative from a listed company stated that: Businessmen are unwilling to provide information as…they have some fear in their minds. […] the main problem is [the] powers held by the authorities over here. Because of those powers, businessmen are afraid to disclose information […]. There are around 71 organisations in Pakistan who are pressurising the industrialist directly or indirectly; for example, the income tax department, the sales tax department, social security, the labour department, the electricity department, the mining department, and the local Thana [Police Station], to name a few. So… if they (the companies) disclose […], one institution will approach them every day and press the business owners to…bribe them (C10 – CFO, Listed Company).

We found that, in Pakistan, there exist ambiguities regarding the legal authority held by the various regulatory bodies and government departments. Since the level of corruption in the country is very high, the employees of various regulatory and governmental organisations have the power to harass corporations in order to extract monetary benefits from them. The respondents explained that they did not see any value in providing information to the regulatory bodies, as these regulators had only been a hurdle rather than being helpful [C2, Company Secretary, Listed Company], were solely interested in taking revenue from the corporate sector [C8, Company Secretary, Listed Company], and were interfering without benefiting [C7, Director, Listed Company] the corporate sector. Meanwhile, the representatives from the corporate organisations were found to complain about unnecessary interference, obstacles, and a lack of support from the regulatory bodies, and the partners from the audit firms echoed this sentiment. There are strong fears [in the minds] of the directors…that the disclosure of information will harm them, will negatively influence their (company's) financial standing, or will lead to negative social outcomes (P2, Partner – Audit firm).

As evidence suggests, organisations are fearful to disclose information while the managers are not involved in any wrongdoing, rather they are fearful of undue demands for bribery and corruption from regulatory bodies. They honestly want to protect organisational interests. Thus, prime motivation for defensive silence is self-protection.

We suggest that soft law disclosures – compliance with which is not mandatory, result in creating a fear of scrutiny by both the public and the regulatory bodies. We found that, while the corporate managers feel threatened by excessive, unwarranted regulatory oversight, they engage in the self-protective behaviour of withholding any information if they consider that doing so is their best option at that particular time. This form of silence highlights the power dynamics between the regulators and the corporate sector, whereby the regulators hold the power to harass corporate organisations and corporate organisations resort to silent behaviour owing to their lack of power to confront the undue regulatory practices or harassment. The higher the power held by the regulatory bodies, the more likely it will be that the less powerful will be exploited and eventually resort to silence as a defence strategy. Defensive silence helps listed companies to prevent unwanted interruptions, confrontations and embarrassment during their encounters with the regulatory bodies and other external stakeholders. There are so many problems…caused by various departments like, social securities, old age benefit, taxation department…the management will hide material items that they (regulatory institutions) will not be able locate from the financial statements…in case if a company discloses all the material items while there is no discrepancy in the report…unfortunately these regulatory institutions will not accept it. They already assess the income of company at a higher rate, old age benefit at a higher rate and so on… that's why the management will take the better option of not disclosing information (C11, Director, Listed Company).

We also suggest that defensive silence in corporate communication is intentional and proactive in nature, as it characterises careful assessment of potential threats before dissemination of information, the decision to withhold information is conscious, and involves an assessment of various alternatives before making eventual decision of staying silent. The literature in organisational science recognises that in certain situations employee's defensive silence can be reactive in nature. For example, an employee starts speaking up, notices unfavourable manager reaction, feels threatened, and immediately decides to stop giving further information (Kish-Gephart et al., 2009). In this case, the silence of the employee is reactive in nature- as it is a reaction to a negative response from the manager. However, since in corporate organisations, the process of information disclosure is deliberate and strategic, we did not find any evidence in our data to support the presence of a reactive form of defensive silence. Rather most of the respondents stressed on the presence of unknown fears or strong threats in the minds of corporate management which prevent them from information disclosure right in the beginning while they make proactive decisions about information non-disclosure.

We also found that politically connected companies display high levels of defensive silence as the fear of regulatory as well as public scrutiny increases manifold for politically connected firms. Our respondents explained that the general public also becomes an important stakeholder in politically connected companies, as the politicians associated with these companies are concerned about votes. One of the respondents from a listed company acknowledged this as follows: For political figures, the most important concern is to save their political career so, if you share more information, more questions will arise. Even if you disclose it honestly, everyone reading this information will find some gaps in it. Even if it's a small gap, sometimes this small gap can create huge hurdles for you politically…like they can abuse it in the media or somewhere like that (C4 – CFO, Listed Company).

We conclude that defensive silence will be prevalent within the corporate communication of organisations, where the management is particularly fearful of public and regulatory scrutiny and where the disclosure of information could result in undesirable consequences.

Prosocial Silence

We observed that a common pattern emerged in the responses of the research participants, where they justified the prevalence of corporate silence in relation to supporting peer organisations, community expectations, and culture. The narrative during an interview of the Chief Operating Officer of a Stock Exchange exemplifies this pattern. The corporate community as a whole has not accepted (the disclosure regulations). They have not accepted them as a community and want to maintain the status quo (R1 – COO, Stock Exchange).

We postulate that the companies in the Pakistani context demonstrate group cohesion and cooperation through adopting prosocial silence with an aim of maintaining the status quo, where information is not disclosed when this benefits other members of the corporate community. We postulate that a propensity to remain silent about information that might negatively affect peer organisations is amplified when there exists an interdependence between the companies and when they are close affiliates: If the companies are closely linked, then they will definitely not provide additional information. If they provided additional information, they would fear that their (peer companies’) competitors might start entering the business (C9 – CEO/Chairman, Listed Company).

We conclude that organisations display cooperation and other-oriented behaviour by failing to disclose confidential or sensitive information, which enables peer corporate organisations to protect their proprietary information from being distributed for general discussion or knowledge. This reluctance to disclose information is guided by the community expectations and extends to the corporate management supporting affiliated companies, subsidiaries, and other related parties: Firms hesitate to show their turnover, and especially the transactions concerning related parties. I have seen on many occasions that they hesitate to disclose properly. They’re reluctant…they say, ‘No, this's our parent company, this's our subsidiary, this's our holding, and this and that’. They do not disclose the transactions properly (P6 – Partner, Audit Firm).

This desire to protect peer organisations might be amplified when there are interdependencies among business organisations in the way they are structured and designed, for example, when the companies are related. It is important to note, however, that the act of staying silent or speaking up does not bring any direct material damage to the company itself. The companies can disseminate that information without facing any negative consequences themselves, and disclosure of that information will directly harm the company whose interests are protected by staying silent. Therefore, the key motive for staying silent is to protect the interests of an affiliate with an intent to save them from harm. The intent to cooperate, support, and protect serves as the prime motivator of prosocial silence.

The quotes from the participants illustrate the pragmatic and instrumental approach of the corporate managers, where corporate silence is a deliberate decision with an intent to protect the collective interests of allied companies. Since Pakistani society places great value on group identity, group consciousness, and group benefits, it demonstrates high levels of cultural collectivism (Bashir & Nasir, 2013). We found that, since Pakistan is a culturally tight society (Chua et al., 2015), secrecy is practiced as a strong social norm in the country, and our respondents frequently expressed that ‘no one wants to disclose information in Pakistan’ [R2 – Director, the SECP] and ‘we do not have a culture of providing information in the corporate sector’ [C11, Director, Listed Company]. Similarly, partner of an audit firm explained I think boards are not interested in giving information or sharing information in true sense because disclosure culture does not exist in the country (P3 – Partner, Audit Firm).

We noted that silence in this context serves to celebrate collective values of non-disclosure and promotes unity, harmony, and solidarity among corporate organisations (Morrison & Milliken, 2000). Despite this other-oriented behaviour towards peer organisations, however, we also observed a negative aspect of prosocial silence, namely that: in order to protect their peers, companies choose to engage in the unethical practice of hiding relevant information from those stakeholders who have a right to access that information (specifically, minority shareholders). We found that, in the Pakistani context, the importance of minority shareholders is undermined by the fact that most of the companies depend on bank financing to raise finance and do not issue shares on the capital market, which further intensifies the information asymmetry, ultimately resulting in non-disclosure. Our respondents explained that the majority of companies issued shares solely for the purpose of being listed on the stock market. Since they do not intend to issue equity capital in the future, their minority shareholders do not matter at all: Most of these businesses are family-owned […]. Although they are listed, they remain private companies, and only a small portion is held by outsiders, so it's hard to disclose…the minority shareholders do not matter as much because a single shareholder will only have a 100 rupee investment (C1 – CEO, Listed Company).

This context has resulted in fostering an environment where silence has become a part of corporate culture. Therefore, the companies in Pakistani context, maintain community norms and preserve the culture for silence, regardless of how it overrides information needs of minority shareholders.

Here we also emphasise upon the differences in the underlying motivations of prosocial silence in contrast to defensive silence. In defensive silence the focus is on self-protection from harm against the consequences of disclosure. Defensive silence often takes place where power dynamics are at play. For example, corporate organisations are becoming silent as a response to the fear of scrutiny from powerful regulatory bodies. Prosocial silence, on the other hand, is motivated by a desire to help others and to adhere to social norms and culture. It focuses on promoting cooperation and collaboration among community and aims for group cohesion. It is motivated by altruism as it aims to benefit other peer organisations and affiliates, is founded on a concern for others, and protects peer organisations from facing unexpected troubles. It intends to maximise benefit for all concerned parties (although it can have negative consequences for the parties from whom the information is concealed). It is pertinent to mention that in contrast to defensive silence, prosocial silence is not motivated by purely material self-interest as the organisations engaging in prosocial silence are not exposed to any direct threats or fears as a result of speaking up. Rather, the purpose is to support peer organisations, and maintain community spirit.

Opportunistic Silence

An interesting perspective emerged when the representatives from the regulatory bodies explained that unjust institutional pressure from the regulatory bodies is not the only reason for the non-disclosure of corporate information. Rather, the fear of scrutiny influences the non-disclosure decisions when the management is actually involved in organisational malpractices with the aim of cheating the system and extracting private benefits. The partner from an audit firm stated: In some companies, the management is less willing to provide certain information; for example, the number of employees […]. They’re unwilling to give details about their number of employees because they might be more employees than are registered with the social security, and differences in the information will attract the attention of various [government] departments […], so they’ll have to pay for social security (P1 – Partner, Audit Firm).

We found that managerial opportunism is one of the prime motivators for the silence of the corporate organisations. Managerial opportunism refers to a situation whereby the managers seek to enhance their own future welfare at the cost of the welfare of other claim holders. In contrast to defensive silence, whereby corporate managers attempt to safeguard the organisational interests with an honest intent to protect organisational interests, or prosocial silence, whereby corporate managers engage in silence with altruistic motives, opportunistic silence is characterised by a manipulative intent and entails the maximisation of self-interest and managerial opportunism. Since the majority shareholders/owner-managers consider the company theirs, they may extract rents and never disclose information. The Director of a listed company stated: They [the corporate management] are uninterested [in] properly disclosing the information. They withdraw money by engaging in overpricing and other similar practices [and] can’t disclose such information. There's no transparency (C7 – Director, Listed Company).

The CFO of another listed company expressed a similar view: If you’re involved in wrongdoing of any kind, then it means you have corrupt intentions…if you’re involved in any financial or non-financial illegal activity. As I’ve shared with you…if you’re producing more than you‘re allowed to produce (under the license) or, I mean…[if you’re involved in] any illegal activity…then you’ll definitely try to distort the information provided by your company, because you are going to do this for your own interest (C10 – CFO, Listed Company).

While, in certain instances the motive for this type of silence is to hide managerial misdoings, in other instances, the motive for manipulative silence may be to control and/or retain the organisational resources for the use and benefit of the owner-managers through impeding their distribution to other stakeholders: They force their management to rejig the figures, so that the figures will not disclose any huge profits…or they will have to distribute dividends. They will have to pay taxes. They avoid dividends and taxes; that's the ultimate objective for them…so they disclose minimum information (P2, Partner – Audit Firm).

We propose that the corporate management sometimes demonstrates self-serving behaviour by withholding information to gain undue advantages for themselves. Consequently, we introduce the concept of opportunistic silence as a form of corporate silence. Opportunistic silence is deliberate, strategic, proactive, as well as manipulative at the same time. Since the organisations involved in opportunistic silence engage in silence with a devious intention, we suggest that they do it while being manipulatively conscious of their environment. Manipulative silence is not reactive in nature rather it occurs in situations where managers are aware of their manipulation and make a deliberate and strategic decision of staying silent for protection of their personal self-interest and opportunism. Since they are proactively conscious of the organisational context, while being manipulative at the same time, we argue that this type of silence in is manipulatively conscious in nature.

Authoritative Silence: Silence as a Symbol of Power

Since power is an important motivator of silence, we enquired our research participants about (non)disclosure practices of those companies that were managed and controlled by members of the board having political affiliation. It is important to note that most of the leading politicians in Pakistan are connected to corporate sector. While we enquired participants about the (non)disclosure behaviour of politically connected companies, they referred to the practices of politicians (involved in the management of these companies). Our data suggest that, in the Pakistani corporate context, silence is used by these powerful elite as a weapon and a means to assert power and exploit the information rights of minority shareholders. Silence, in this context demonstrates the power and control held by these politically powerful elite. So, politicians…they make policies and regulations which they later break themselves. No one can do anything against them. Honestly, there are no rights enjoyed by minority shareholders. If I have a share in a company, then I have a right to information…people (the minority shareholders) raise their voices, but nothing happens. They do ask [the] board of directors for information, they do raise their voices at the annual general meetings. Nothing happens. These politicians are too powerful (C7 – Director, Listed Company).

These politically connected companies ignore the information needs of the other stakeholders, especially the minority shareholders, and ostracise and annihilate them metaphorically by excluding them from all communication. If we reflect on the power dynamics, silence conveys a message to the shareholders and regulators that, despite their need for information, they will not be provided with it and no one can do anything about this. Even the representatives from the regulatory bodies recognised this power and control and explained that the powerful elite does not comply with the regulations when this does not suit their interests. Obviously, the powerful people in Pakistan…make the laws. They can twist the [disclosure] regulation, and give the [disclosure] regulation their own meaning, and they can implement it according to their own terms. Things aren’t very simple in Pakistan (R2 – Director, the SECP).

Another representative from a regulatory body explained the role of power in the silence of the political elite as follows:

Different people analyse it (the silence of the powerful elite) in different ways. Some people say “a lack of education”, some say “feudalism”, some say “the improper distribution of wealth or money”…but I think…, in Pakistan, every man thinks he is the owner of a woman, every upper division clerk wants dominance over a lower division clerk, and a lower division clerk wants dominance on peon…Even supervisors want dominance over the workers…this is how they want to keep dominating others…it's all about power (R3, Director, the SECP)

Since the level of political corruption in the country is high and politicians often participate in the corporate sector with the intention of extracting benefits for themselves, they also prefer a degree of secrecy to be maintained regarding corporate affairs (Fan & Wong, 2002; Wu, 2005). Thus, the avoidance of disseminating information to those groups that are perceived as powerless also becomes a ‘viable strategic alternative’ in their view (Oliver, 1991, p. 164).

A representative from a listed company explained: They [the politically connected companies] conceal information. If they want to, they can (C9 – CEO/Chairman, Listed Company).

We argue that authoritative silence is motivated by apathy and arrogance. This silence on the part of the political elite is cold and has a perlocutionary effect on the addressees. Our respondents described the indifference and arrogance of the politically connected elite and they elaborated on how this elite does not care about the demand for disclosure by minority shareholders or regulators, and is apparently unaware of the regulations: These members of the national assembly (MNAs) or members of the provincial assembly (MPAs) belong to a very high class, so I don’t think…they don’t bother about information disclosure. These things are such small issues for them…mostly, they don’t even know about it. Like if you ask Fahmida Mirza (a renowned Pakistani politician), “What's corporate governance?”, I don’t think she knows about it…so individuals will comply with the [disclosure] regulations only if they are aware of them. They are working at a high level so they don’t know about such things (C1 – CEO, Listed Company).

We argue that organisations make an assessment of the power that they possess in relation to their stakeholders and hold themselves accountable only to those stakeholders whom they perceive to be powerful, while ignoring the information needs of the powerless. More specifically, we found that politically connected companies in Pakistan enjoy discretion concerning matters of corporate disclosure and may remain silent in order to symbolise their authority and power. In this regard, silence pushes the minority shareholders and regulators to accept the lack of accountability and transparency in politically connected companies as the norm. They’re free to do anything…I mean, for example, if I were a politician, nobody’d dare ask me for any information. As I’m not a politician, therefore, every single piece of information has to be provided to the regulators. Then, we have to answer and justify it. You see, in Pakistan and in developing countries, politicians have huge influence (C5 – CEO/Chairman, Listed Company).

Although political connections are beneficial in facilitating access to bank finance, lower taxation and market power for corporations, these companies do not outperform their peers in the long run so, in order to hide their poor performance, the quality of the information disclosed is compromised (Faccio, 2006; Fan et al., 2014; Riahi-Belkaoui, 2004). Thus, value maximisation is not the aim of the politically connected companies, as politicians have diverging political interests (Piotroski et al., 2015). Usually, these companies perform poorly in both financial and social terms. In such a situation, silence helps to normalise the lack of accountability of this political elite, and it becomes increasingly difficult to question the underlying systems of power (Giroux & McLaren, 1992; Hall, 2005). We conclude that organisations that are managed and controlled by the politically powerful elite may not always act in the best interests of various stakeholders and may demonstrate as well as maintain their own power through silence. We propose that corporate organisations may decide to remain silent when they are controlled by the powerful elite.

Counteractive Silence: Resistance to Power and Authority

The SECP, as the primary regulator of Pakistan's corporate sector, introduced the Code of Corporate Governance in Pakistan in 2002. The purpose of this Code was to improve the information disclosure and transparency within the corporate sector. Although the regulators adopted a flexible approach and disclosure regulations were implemented as soft laws, the business sector in Pakistan resisted the implementation of the Code, due to a lack of sufficient incentives or benefits for providing information, the costs associated with compliance, and an unwillingness to disclose sensitive information to their competitors (Areneke et al., 2019). We found strong evidence for this resistance to the disclosure regulation in the responses of all participant groups, and the representatives from the regulatory bodies also recognised the presence of this resistance: The government has imposed it [the disclosure regulation] without asking about their [the listed companies’] concerns, without considering their stake, and without seeking their opinion. […]. It's been imposed upon them. They’re resisting it (R1 – COO, Stock Exchange).

The partners from an audit firm also recognised that the listed companies are resisting disclosure regulations by staying silent: There's a general concern that [the corporate governance regulation] isn’t a good document. They [the listed companies] are resisting it, so that's the reason why the disclosure of information is lacking in the corporate documentation (P1 – Partner, Audit Firm).

A careful evaluation of the context indicates that many companies were delisted from the stock exchanges in Pakistan following the introduction of the Code of Corporate Governance, due to their unwillingness to provide corporate information. Thus, we suggest that the silence of listed companies may also be an expression of their resistance and protest concerning this demand for disclosure by the regulatory bodies. The expression of silence in such a case is blatant, wherein their unwillingness to provide information can be readily noticed.

A respondent from a listed company stated: If, as according to the Code of Corporate Governance, you want us to provide all of the information, it won’t make any difference. The companies will definitely not provide any additional information because they don’t want to provide [it] (C9 – CEO/Chairman, Listed Company).

Although the representatives from the listed companies recognised the resistance of the corporate sector to corporate disclosure through making generic statements, we observed that they did not explicitly state that their respective company was failing to comply with the Code, which we concluded was owing to a fear of scrutiny by the regulators; for example, the representative from a listed company stated that: In Pakistan, no one wants to disclose information…financial or non-financial; in Pakistan, no one likes to disclose any information…you know, even personally, we don’t want to share any information with anyone (C10 – CFO, Listed Company).

This form of silence aims to accomplish some social or political objective through resistance. In particular, organisations operating in capital markets that are dominated by family-owned businesses may adopt this form of protest towards disclosure regulation. Thus, we propose that corporate organisations may decide to remain silent as a form of resistance against disclosure regulation, especially when the institutional environment supports non-disclosure.

Discussion

Our research investigated the forms and motivations for silence in corporate communication within the context of a developing country; namely, Pakistan. This question is pertinent and vital, considering that the majority of the existing literature has traditionally focused on corporate disclosure and very little is known about corporate silence. We found it useful to conceptualise corporate silence on the basis of various motivations.

Our study identified self-protection from fear and discomfort as the primary motivation for defensive silence, whereby the corporate managers take an ‘active, selective and proactive’ decision to safeguard the organisation against potential threats in their environment with an honest intent (Morrison & Milliken, 2000). As suggested by Pinder and Harlos (2001), this form of silence allows organisations to avoid engaging with the regulatory discourse, and possibly partake in certain practices that they would be unable to maintain if they were to engage with the regulatory discourse. Since the disclosure regulations are soft laws in Pakistan, non-compliance is easy, despite the presence of established regulatory structures (Jungkunz, 2012, p. 134). In the context of Pakistan, defensive silence helps organisations to protect themselves from unjust organisational practices, although this might not be a valid motivation in a different context, where the regulatory institutions are not corrupt. Moreover, there may exist other, unique factors driving organisational fear in varying contexts.

We emphasise the role of culture while we expand further on prosocial silence. Cultures demonstrating high levels of collectivism (such as that of Pakistan) prefer to maintain silence when a voice is perceived as having the potential to damage the collective interests, spark disruptive consequences, challenge the status quo or harm the group and community cohesiveness (Morrison & Mikkilin, 2000). We propose that prosocial silence involves a process of conscious decision-making and results in harbouring collegiality and affiliation, and preserves social identity (Ashforth & Mael, 1989). The companies operating in the Pakistani context have formed a strong community that supports the non-disclosure of information, whereby the desire to maintain the status quo reduces their propensity to speak (Hollander et al., 2010; Young et al., 2008). Prosocial silence helps them to earn the approval of the community and supports all of the family-owned and -controlled peer organisations that are reluctant to disclose information, promotes proprietary information retention and serves to maintain the status quo. On the negative side, however, as non-disclosure breaches the information rights of the minority shareholders, prosocial silence perpetuates the unethical organisational practice of non-disclosure that violates the societal, legal or organisational standards of acceptable conduct and may potentially harm various stakeholders (Knoll & Dick, 2013).

We also introduce the concept of opportunistic silence and postulate that this form of silence is manipulative in nature. In line with Knoll and Dick (2013), we propose that manipulative silence occurs when the corporate management either withholds useful, material information or provides distorted information with an intent to conceal, mislead or confuse the users of corporate communication. Thus, this type of silence is characterised by a deceitful intent to maximise self-interest while harming other stakeholders’ interests. This type of opportunistic behaviour has been widely studied, and researchers argue that it encourages the management to employ various strategies for the purpose of concealment and impression management; for example, earnings management, obfuscation or the concealing of bad news, using complex language to reduce the information's readability, persuasion and attribution (Brennan et al., 2009). The existing literature also suggests that corporate narratives are drafted by opportunistic managers with the intention of maximising the managerial benefits at the cost of the other stakeholders’ interests (Brennan et al., 2009; Merkl-Davies & Koller, 2012; Moerman & van der Laan, 2007). We propose that the corporate management sometimes withholds information to obtain undue advantages for themselves.

This research presents silence as ‘a vehicle for the exercise of power’ as it leads its addressees to believe that what is not said will not be revealed and that it is completely impossible for them to access that information (Achino-Loeb, 2005, p. 3). The expression of such silence is blatant. The authoritative form of silence ignores the information needs of the stakeholders, blocks all communication with them, and annihilates them symbolically (Kurzon, 2007). Silence in this situation demonstrates the power held by the powerful elite. According to Akman (1994, p. 211), this sends the message: ‘You need me to give you the information you want. I am not cooperating with you, and you cannot make me’. It is a demonstration of the power held by the political elite, who refuse to acknowledge the presence or rights to information of the powerless minority shareholders. It is motivated by indifference, apathy, and arrogance. As DeVito (1989) notes, silence can demonstrate a refusal to treat others as persons and renders them as inanimate objects, which can consequently cause harm. Withholding information might also be useful if individuals are unwilling to give away their power and status (Knoll & Dick, 2013) and it serves as a necessary precondition for maintaining the ‘sacred’ domain of influence, a domain that serves to intimidate others in order to preserve the current systems of power and control (Bateson & Bateson, 1987).

We expand upon the existing literature on silence in general, and silence within external corporate communication in particular, by introducing resistance and objection as motivators for counteractive silence. In the literature relating to research methods (Stanton, 2014) and education (Fordham, 1993; Jin, 2017), several researchers have conceptualised silence as a form of resistance to domination, whereby the research participants and students were found to use silence to resist information disclosure and fight teacher control, respectively. Similarly, research in the field of clinical psychology also highlights the use of silence by patients to resist treatment plans until an alternative, more acceptable plan is presented (Koenig, 2011). From an organisational perspective, employees use silence as a tool for conveying anti-subordination, objection, and dissent (Cohen, 1990; Ward & Winstanley, 2003). Thus, drawing on our analysis of the research data and review of literature drawn from various domains, we postulate that corporate silence may indicate resistance to oppression and signify confrontation or protest, thus challenging the authority of the regulators and other stakeholders. Thus, silence within corporate communication might also be used as a form of resistance against certain regulations. This form of silence may prove disruptive as, by concealing information on the desired aspects, the firm is failing to meet its social and regulatory obligations regarding information disclosure (Jungkunz, 2012).

Conclusion

While we conclude, we clarify that we have purposefully simplified the forms of silence in our framework to allow for and amplify the comparisons. Therefore, although our framework represents five basic motives (drawn from both the existing literature and our research data), we realise that silence can be based on other motives. We also propose that silence often represents a complex combination of motives, and thus the various motives for silence may not be mutually exclusive. For example, a politically connected company might stay silent on various issues owing to a fear of scrutiny from public or regulatory bodies while simultaneously displaying the power they hold for non-disclosure, and thus engage in defensive as well as authoritative silence at the same time. However, a study of these combinations does not fall under the purview of this research while we focus on the development of a simplified conceptual framework.

This paper opens up several interesting lines for future research. We suggest that the theoretical work in the area of corporate silence is currently nascent, particularly in the accounting literature. Thus, we present this framework as a first step towards the development of a more refined conceptualisation of corporate silence. We call for further field-based studies to refine and consolidate the theoretical categories and concepts related to this area.

Here, we also consider it appropriate to explicate that, although it does not seem reasonable to generalise from the study of one country to all countries, it is pertinent to note that generalisation is not the purpose of grounded theory analysis. Qualitative case study research aims at analytical generalisation, as opposed to the statistical generalisation which is typically associated with quantitative research. To achieve analytical generalisation, we specify the context of Pakistan, and elaborate on the specific conditions in which corporate silence is located within this study. We postulate that this framework will be useful for providing insights into the phenomenon of corporate silence in those contexts where similar conditions exist. For example, many African countries display the characteristics of close ethnic and community affiliation having closely held highly concentrated capital markets (Rwegasira, 2000). Many other developing countries (such as India, Bangladesh, South Korea and South Africa) also characterise markets with high level of family ownership (Siddiqui, 2010) and share remarkable similarities with the institutional settings of Pakistan. These countries might present rich contexts for study of this framework.