Abstract

Empirical research documents persistent socioeconomic and race gaps in parental investments in children. This article presents a formal model that describes the process through which parents’ beliefs about the returns on investments in children evolve over time in light of new information that they receive regarding the outcomes of past investments. The model, which is based on Bayesian learning, accounts for how parents of low socioeconomic status may come to underinvest in their children because they have false low beliefs about the returns on investments. Moreover, the model describes how beliefs are transmitted across generations, thus creating dynasties of underinvesting parents who reproduce inequalities in children’s socioeconomic outcomes. Finally, this article uses National Longitudinal Survey of Youth data to provide illustrative empirical evidence on key aspects of the proposed model. The main contribution of this article is to integrate parents’ beliefs about returns on investments into existing models of intergenerational transmissions.

Keywords

Introduction

Practitioners of empirical analyses based on Rational Choice Theory have long been aware that when individuals face various choices, they are rarely fully informed about what options they have and the returns on their choices, but rather base their decisions on personal beliefs and attitudes (Breen, 1999; Morgan, 2005; Piketty, 1995). The concept of beliefs has been subject to a large body of research in various contexts. For example, Calargo (2014), Lareau (2003), and Weininger and Lareau (2009) document how parents of high and low socioeconomic status (SES) differ in their beliefs about parenting practices and desired school behaviors. Similarly, Morgan (2005) addresses how young people form beliefs about their educational opportunities and how these beliefs vary across racial groups. On a theoretical level, Breen (1999) presents a formal model which assumes that students hold beliefs about the relative returns on effort versus ability with respect to school outcomes and shows how students in theory can have stable, but false beliefs about these returns. Furthermore, recent research shows that parental resources and their investments in children have substantial impacts on educational, labor market, and health outcomes regardless of gender, race, and SES (Alwin and Thornton, 1984; Björklund and Salvanes, 2011; Cunha and Heckman, 2007; Englund et al., 2004; Smyth et al., 2010; Yeung et al., 2002; Zhan and Sherraden, 2003). To date, however, no study has presented a comprehensive formal model analyzing how parents’ investments in their child are shaped by the beliefs they (the parents) have about the returns on those investments.

Parents’ monetary investments in buying toys and employing high-quality day care, as well as their time investments in reading and taking their child to museums, have been shown to generate large returns with respect to the child’s educational attainment, earnings, and behavioral problems (Björklund and Salvanes, 2011; Cunha and Heckman, 2007; Deslandes et al., 1997; Smyth et al., 2010; Todd and Wolpin, 2007). For example, Yeung et al. (2002) find that access to cognitively stimulating materials, such as newspapers and books, improves a child’s cognitive skills and reduces behavioral problems. Jæger and Breen (2016) argue that parents actively use activities, such as museum visits, to transfer cultural knowledge to their children, thereby increasing academic performance and long-term success. Similarly, Englund et al. (2004) show significant returns on parental involvement in schools as well as the instructional skills of the parents, a finding which Deslandes et al. (1997) and Smyth et al. (2010) corroborate. Englund et al. (2004) also show that parents’ involvement and educational expectations for their children increase when the child performs well in school. Some research also points to mixed evidence of the uniformly positive returns to parental involvement in the home and suggests that certain parent behaviors can adversely affect the child (Pomeranz et al., 2007). The overall picture, though, is that parental investments in children under most circumstances increase cognitive skills, improve educational attainment, and reduce behavioral problems (Björklund and Salvanes, 2011; Cunha and Heckman, 2007; Englund et al., 2004; Smyth et al., 2010).

However, mounting empirical evidence also indicates that low SES and non-White parents tend to invest less in their children, not only in terms of monetary investments but also in terms of engaging their children in stimulating activities (Mayer, 1997; Pomeranz et al., 2007; Todd and Wolpin, 2007; Yeung et al., 2002). Consequently, differences in parental investments by SES and race, for example, may be key factors in explaining the persisting inequalities in children’s outcomes. A wide range of theoretical models exist that account for SES and race gaps in parental investments in children. These models can, broadly speaking, be classified into socio-cultural reproduction models and rational choice models (Smyth et al., 2010).

Socio-cultural reproduction models attribute SES and/or race differences in parental investments and children’s achievements to differences in norms, values, and behavior and often emphasize the role of cultural resources or cultural capital (e.g. Bourdieu and Passeron, 1990; Fordham and Ogbu, 1986; Kohn, 1977; Lareau, 2003). Intergenerational transmission of SES, in these models, happens when parents (in some cases, unwittingly) imbue their children with norms, values, and/or behaviors that the educational system rewards. Rational choice models such as those presented by Becker and Tomes (1979, 1986), Cunha and Heckman (2007), Boudon (1974), Breen and Goldthorpe (1997), and Morgan (2005) instead conceptualize children and their parents as forward-looking rational agents who attempt to maximize their utility in light of their available information and preferences. In these models, intergenerational transmission of human capital happens through parents’ investments, which in turn depend on the child’s endowments and the parents’ resources.

Although socio-cultural reproduction models differ from rational choice models in their behavioral assumptions as well as their implied mechanisms, they also share several aspects. Pertinent to this article, both types of models have parents behaving in certain ways with respect to their children dependent on their SES. While this article presents a new rational choice model, it also acknowledges findings from research based on socio-cultural reproduction models, which document differences in beliefs and values concerning parental behavior across SES groups and races (Fordham and Ogbu, 1986; Lareau, 2003; Morgan, 2005).

Models such as the ones mentioned above have greatly expanded our understanding of why SES and race differences in parental investment and child outcomes exist and how they persist over time. However, each class of models also has it shortcomings, which the model presented in this article attempts to amend. Socio-cultural reproduction models are rarely formalized, and their assumptions and mechanisms often remain implicit and difficult to test (for a notable exception, see Jæger and Breen (2016)). This article formalizes the role of SES and race for parental investments and makes explicit how these factors interact with parents’ beliefs about the returns on their investments in their children. Rational choice models typically operate on the assumption that parents are fully informed about the returns on their investments (e.g. Becker and Tomes, 1986; Cunha and Heckman, 2007). While such assumptions reduce the complexity of the model, they can be relaxed by explicitly incorporating parents’ beliefs about the returns on investments into the theoretical model. This provides a richer and more realistic account of the causes and consequences of parental investments as parents are unlikely to possess full information about the actual returns on their investments in their children. However, they do have beliefs about these returns that may or may not be consistent with the truth. It then follows that utility-maximizing parents invest in their children to the extent that they believe their investments will have a positive effect on child outcomes. Regardless of whether investments actually yield a return, parents who do not believe that investments matter, or who do not derive utility from their child’s outcomes, would not be expected to invest time and money in their children but rather to increase their personal consumption (Becker and Tomes, 1986).

Finally, Morgan (2005) indicates that there is little reason to believe that beliefs are static but rather that they change as individuals receive new information, echoing the theoretical notion of beliefs presented in Breen (1999). In the case of returns on parental investments, if parents believe that their investments yield low returns with respect to their child’s school performance, they may invest little time and/or money in their child. However, if they experience that their child performs poorly in school, this may cause them to shift their beliefs toward higher returns on investments when they see that they did not invest much and their child performed poorly (Quadlin, 2014). This article models this process using Bayesian learning, which allows parents to gradually change their beliefs in light of new information while still taking into account prior beliefs (Anwar and Loughran, 2011; Breen, 1999; Breen and García-Peñalosa, 2002; Morgan, 2005; Piketty, 1995).

This article extends existing theoretical models of intergenerational transmissions in three respects. First, it proposes a formal model that uses Bayesian learning to explicitly incorporate parents’ beliefs about the returns on investments into the modeling framework. This model argues that parents are rational actors who, while having their children’s best interests at heart, may come to systematically underinvest in their children if they believe that the returns on their investments are lower than what they actually are. Second, the article models how beliefs about returns on investments depend on SES and race, and it provides a theoretical explanation of the persistent SES and racial gaps in parental investments that previous research has documented. Third, the model incorporates an account of how beliefs about the returns on investments are transmitted across generations. If beliefs help to explain investment gaps, the intergenerational persistence of these gaps is conditional on children who, to some degree, inherit their parents’ beliefs. The literature that addresses the intergenerational transmission of beliefs normally assumes that children inherit their parents’ exact beliefs (Breen, 1999; Piketty, 1995). While this assumption is both convenient and useful, the process through which beliefs are transmitted across generations may be modeled more completely by relaxing it.

Furthermore, this article uses data from the National Longitudinal Survey of Youth 1979–Children and Young Adults (NLSY79-CYA) to test key features of the model. In particular, the empirical results illustrate that parents modify their investments over time based on prior investments and on their children’s academic performance. Many of the theoretical models presented in this article greatly owe their formulations and conceptualizations to Breen (1999), who presented similar models. While part of this article’s contribution comes from applying the framework of Breen (1999) to a new field—that of parental investments—the article also contributes beyond mere re-application of existing models. Apart from including an empirical test of some of the assumptions of the model, the article also offers a formalized mechanism for intergenerational transmission of beliefs and shows how systematic underinvestment due to low, stable beliefs may itself differ by SES and race.

The following section presents the formal model of how parents’ beliefs about the returns on investments evolve during their children’s childhoods and how beliefs partly determine parents’ level of investments. The subsequent section addresses intergenerational transmission of beliefs and demonstrates that even when relaxing the assumption that children inherit their parents’ exact beliefs, they still tend toward doing so. The third section presents an empirical illustration of a set of the model’s predictions. The final section discusses the article’s findings and reflects on the limitations of the research as well as the prospects of future research.

A formal model of beliefs in returns on parental investments

This section proposes a formal model of the formation and evolution of beliefs regarding returns on parental investments. The section first outlines the processes leading to child academic performance and argues that this performance serves as a signal to parents about the returns on their investments. Second, the section addresses parents’ decision-making when determining how much to invest in their child by jointly considering the utility derived from both their child’s academic success and their personal consumption. Third, the section argues that the evolution of parents’ beliefs about the returns on their investments can be modeled using Bayesian learning models, and moreover, it shows how parents update beliefs in different ways depending on their prior beliefs. Fourth, the section shows that the model predicts the existence of two different sets of stable beliefs: one which leads to optimal parental investments in their child and one which, due to false beliefs, leads to underinvestment.

Child academic outcome as an imperfect signal

Following Burton et al. (2002), Cunha and Heckman (2007), and Jæger and Breen (2016), this article conceptualizes childhood as consisting of a series of time periods denoted as

The probability that a child experiences academic success at time

Thus, at any given time

And conversely, the probability that the child experiences success in state

The world exists in one and only one of these states. That is, either parental investments are more important than other factors, or conversely, the opposite holds. Parents are unaware of the true state of the world but have subjective beliefs about the relative importance of their investments.

3

These beliefs are denoted by

and

As

Combining the notation above, parents’ belief in the probability that their child succeeds in school is written as

Thus, while parents’ beliefs in the probability of their child succeeding academically,

In summary, the model proposes that the probability that a child is academically successful depends on both parental investments,

Parental utility and level of investment

Models of intergenerational transmission and human capital accumulation often argue that parents face a trade-off between investments in children and personal consumption (i.e. Ayalew, 2005; Becker and Tomes, 1986; Behrmann, 1997). It is demonstrated herein how parents, all of whom possess a limited stock of resources, make decisions about this trade-off based on their beliefs about the probability that their child will succeed academically. If all parents were perfectly informed about this probability, differences in investments would be the sole product of differences in resources and altruism, as in Becker and Tomes (1986). However, the utility function presented herein incorporates the role of parental beliefs not previously included in economic models of intergenerational transmissions. Moreover, the model illustrates how parents determine the level of investment that will maximize their utility.

The utility function includes two components: child academic success and personal consumption. These are interdependent as resources can be used either for parental investment, thereby increasing the probability that the child is academically successful, or for personal consumption, but not for both. The model assumes that while all parents have a preference for their child’s academic success, they also have some preference for personal consumption. Parents weigh these two preferences against each other by maximizing their joint utility,

where

The utility function also assumes that both expected utilities,

The utility function above describes how parents derive utility from both child academic success and their personal consumption, and that they do not know exactly how much their child benefits from their investments. This lack of full information constrains parents to invest according to their beliefs about the returns on their investments,

Appendix 1 shows the derivation of equation (2).

Bayesian learning in the evolution of beliefs

This article has argued that beliefs play a crucial part in shaping parental investments. Moreover, beliefs may change over time. It is now proposed that parents are Bayesian learners who update their beliefs in light of new information. Bayesian learning allows parents to change their beliefs based on the signaling value of their child’s academic success or failure while acknowledging that new beliefs do not emerge in a vacuum. Rather, parents have a prior belief before receiving a signal from their child. They then update their prior belief in accordance with the new information provided by the signal as they form their posterior belief. This subsequent belief then becomes their new prior as parents receive even more signals over time. In this way, both prior beliefs and new signals contribute to the evolution of parents’ beliefs about returns on investments in their child.

At time 0, parents have a belief,

This is a standard application of Bayesian learning (Breen, 1999; Breen and García-Peñalosa, 2002; Piketty, 1995). Note that this method of updating requires that parents consider the signal, whether it comes in the shape of grades, test scores, or comments from teachers, to be valid information, to which they should react. For simplicity, this article assumes that parents accept the signal at face value, although a more realistic elaboration of the model could incorporate different levels of parents’ trust in the signal. Ultimately, though, as long as parents trust the information somewhat (and do not act counter to it), the model’s properties and predictions hold.

A vital property of this learning model is that because parents are conditioned on their prior beliefs, different parents may react in different ways to the same new information. For example, a child’s academic success can cause parents to either increase or decrease their belief in state

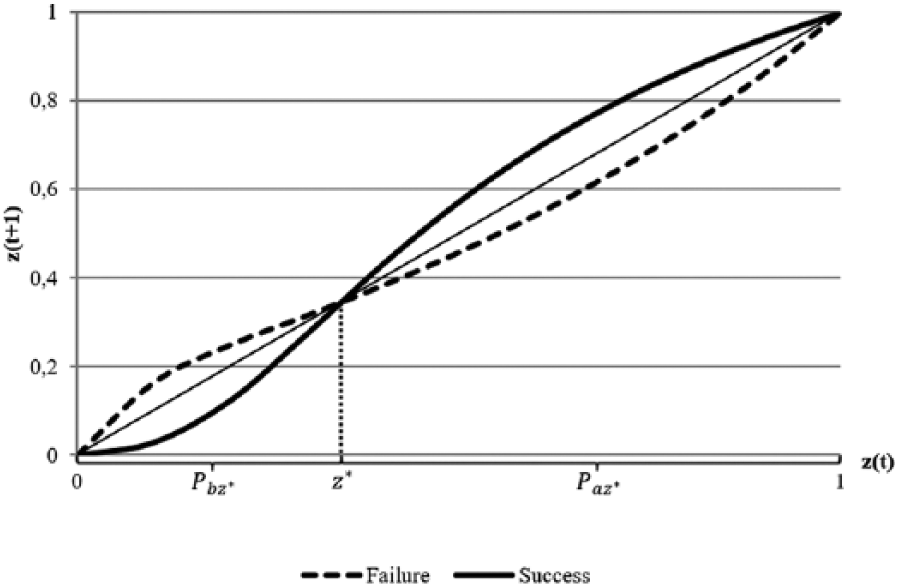

The evolution of belief.

Figure 1 shows parental belief,

Steady state beliefs

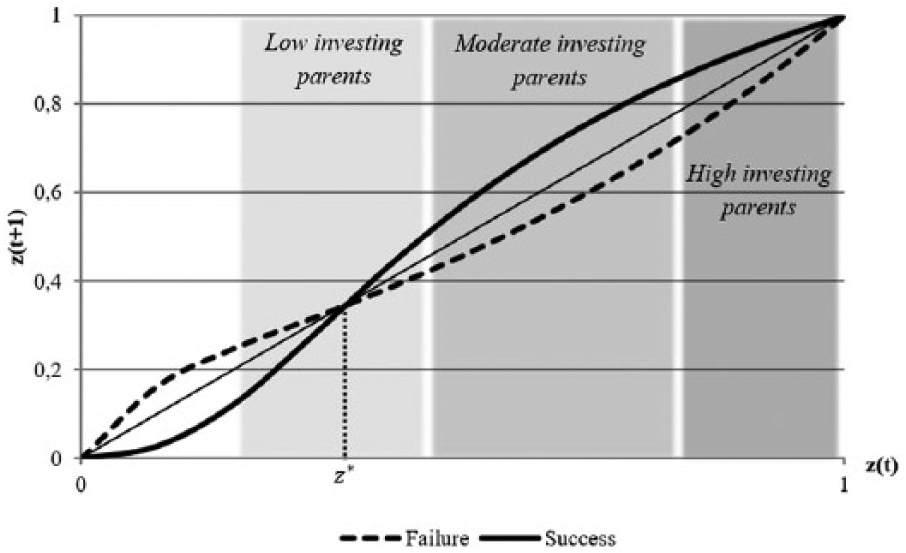

As presented in the previous section, this model does not treat beliefs as static. Parents continuously receive signals from their child and use these signals to make inferences about the returns on their investments in their child. Accordingly, the proposed model leads to two steady-state beliefs (or equilibria) in which new signals about academic success or failure do not change parents’ beliefs. These beliefs lead to underinvestment in the child, which then causes investment gaps that are conditioned on prior beliefs and on other factors, such as SES and race.

In a system of Bayesian learning, steady-state beliefs are possible at two different values (Piketty, 1995; Smith and Sørensen, 2000). One such value is at the true belief,

Figure 1 also shows that there exists a certain value of

However, before making the above claim, the mechanism of the model that generates

that is, the level of parental investment that makes child academic success equally likely, regardless of whether the world is in state

where

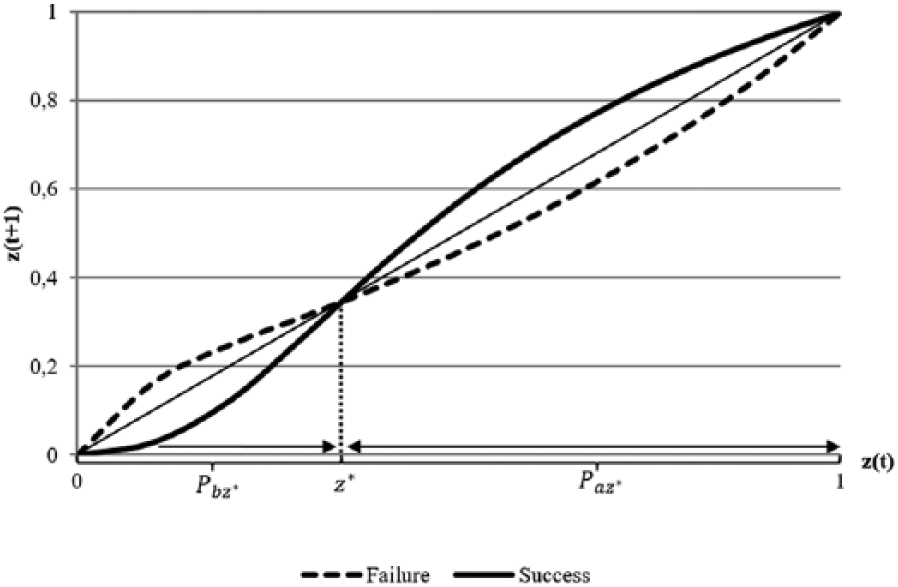

Before considering the role of other factors,

The arrows parallel to the x-axis in Figure 2 indicate the possible patterns of convergence. Converging with

The evolution of beliefs and pattern of convergence.

Thus, it follows that movement upward to

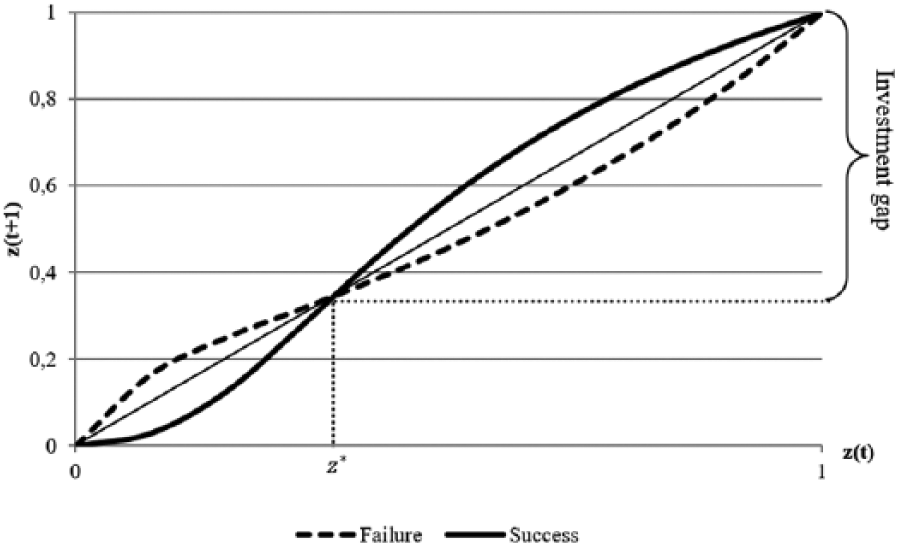

The evolution of beliefs and the investment gap.

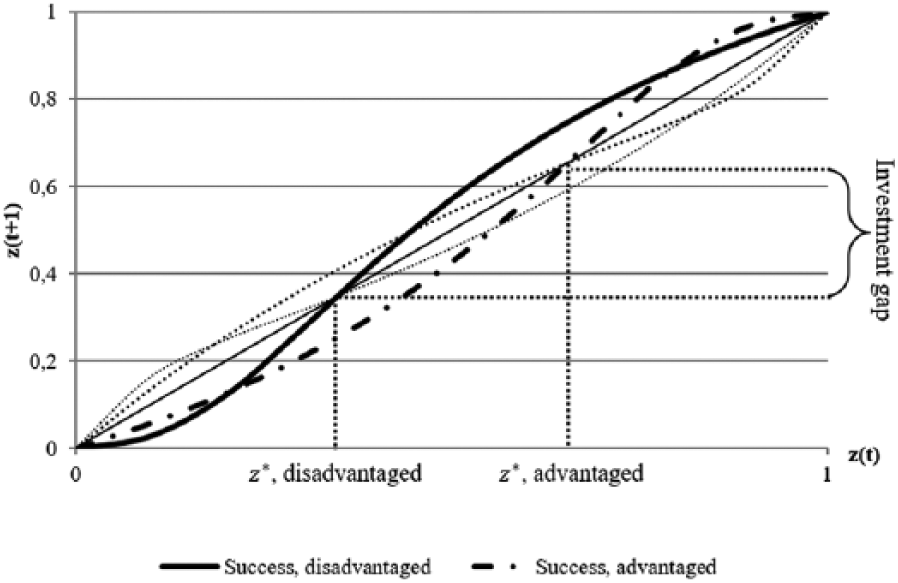

In addition to the investment gap illustrated in Figure 3, another gap is possible if the CLE varies systematically between advantaged and disadvantaged social groups. From equation (4), it is possible that

See Appendix 3 for full proof and the conditions under which this holds true. Thus, the CLE assumes a higher value for parents with favorable other factors,

The evolution of beliefs and investment gap with false belief.

Figure 4 presents two sets of success and failure trajectories, one each for advantaged and disadvantaged parents (the failure trajectories are dimmed for ease of understanding). As with previous figures, the CLE occurs where the success and failure trajectories simultaneously cross the diagonal, thus indicating no change in belief. The figure further indicates that investment gaps between advantaged and disadvantaged groups are present even when both groups are at their CLE.

A final aspect of the relationship between other factors and the CLE to consider is that, for

Finally, a remark upon the CLE, which discusses its status as an equilibrium. Unlike previous research employing this concept (Breen, 1999; Breen and García-Peñalosa, 2002; Piketty, 1995), this article recognizes that the CLE is not “trembling hand perfect” (Carbonell-Nicolau, 2011; Selten, 1975). That is, the CLE is only an equilibrium as long as parents update their beliefs and choose their level of investments without any error or confusion. Should a pair of parents at the CLE invest above their expected level for stochastic reasons, they might escape the CLE and converge to the true belief. 14 However, as proposed by Breen (1999), though never formalized, updating beliefs might also impose a cost on the parents, making them less likely to update their beliefs. As such, the equilibrium property of the CLE might be compromised in opposing directions: If parents are prone to stochastic variation in their level of investments, the CLE is not necessarily stable. On the contrary, if there is a high enough cost to updating beliefs, every belief between 0 and 1 is a potential equilibrium (though not a CLE) as parents weigh the cost of updating against the benefits of having an updated belief. Concurrently, as long as both (or none) of these forces are in play, the CLE has the possibility to exist as a stable equilibrium to the degree that they cancel each other out. In the interest of space, this article does not formalize the circumstances under which this balance occurs, but implicitly assumes that it does. Future research, both theoretical and empirical, should address these potential limitations of the CLE.

In conclusion, this article has now proposed a formal model that conceptualizes parental investment gaps as arising from systematic differences in stable beliefs about the returns on investments and has identified two types of possible gaps. First, a possible gap exists between parents holding the true belief and parents at their CLE, as illustrated in Figure 3. Second, a possible gap exists between advantaged and disadvantaged parents both at their CLE. This gap between false beliefs is a product of disadvantaged parents’ CLE being systematically lower than that of advantaged parents, as presented in Figure 4.

Intergenerational transmission of beliefs

It has been argued herein that parents continuously receive imperfect signals from their child and use these signals to make inferences about the returns on their investments and that over time parents shift toward one of two stable beliefs: the CLE or the true belief. Which belief parents adopt is determined by an interplay between parents’ initial beliefs and other factors, such as SES and race. The model argues that unfavorable factors outside of the parent’s immediate control, for example, low SES, increase the detrimental effect of having low initial beliefs in the returns on parental investments by lowering the parents’ CLE, which in turn results in underinvestment. This section expands the model to consider how beliefs are transmitted from one generation to the next and, moreover, to examine the long-run consequences of parents’ beliefs in the reproduction of SES. In doing so, the model explains how parents form their initial beliefs.

There is strong evidence that children inherit values and beliefs from their parents (Bisin et al., 2011; Dahl et al., 2014; Hitlin, 2006; Kohn, 1977; Weininger and Lareau, 2009). Research that has used Bayesian learning models argues that children inherit beliefs from their parents in a direct way, which suggests that their initial beliefs are identical to the steady-state beliefs of their parents (Breen, 1999; Piketty, 1995). Introducing a generation subscript

and

This simple model of belief transmission means that a child’s initial beliefs can only be either the true belief or his or her parents’ CLE, assuming that parents have had sufficient time to adopt a steady state at time

However, relaxing the assumption of perfect transmission of beliefs breaks this deterministic pattern by introducing a stochastic error term,

and

Considering equation (5), the probability that a child converges with the CLE if his or her parents held the true belief at time

Conversely, a child whose parents had adopted the CLE will, when he or she enters adulthood, also adopt the CLE with probability

as long as

The model suggests that intergenerational transmission of beliefs has clear implications for the persistence of parental investment gaps as underinvesting parents at the CLE are likely to pass on this false belief to their child. Accordingly, the intra- and intergenerational dynamics in the evolution of beliefs reveal that the level of investments is established in one generation and then passed on to the next. Thus, the model leads to two types of dynasties: one in which parents underinvest due to false beliefs and one in which parents invest in accordance with the true state of the world. In addition, as previously shown, the CLE of disadvantaged groups occurs at a lower value than it does for advantaged groups, thus placing low SES families at a double disadvantage. First, they tend to transmit their false beliefs in the low returns on investments to their children. Second, this false belief has a more detrimental effect on their investments even when compared to the false beliefs of high SES families, as the latter have a higher value of CLE. In this manner, the model helps to understand how investment gaps persist across generations, which then leads to gaps in education, income, and health (Ayalew, 2005; Burton et al., 2002; Card, 1999; Reynolds and Ross, 1998).

Empirical illustration

An empirical illustration of key aspects of the proposed formal model is necessary. As previously stated by Breen (1999), it is challenging to test Bayesian learning models such as these, as doing so in this case requires longitudinal and reliable measures of beliefs, parental investments, and child academic success or failure. Absent such a data source, this article uses an empirical measure of parents’ investments as a proxy for parents’ beliefs about the returns on investments. While not ideal, such a framework may provide provisional evidence on the usefulness of the model. Following Breen (1999), the model’s predictions are analyzed by evaluating “testable propositions about how [parents’ beliefs] should change conditional on its previous value and on the outcome of the event in question” (p. 475). Specifically, the hypothesis that parents with either an initial low or high level of investment are likely to adopt a stable belief, the CLE or the true belief, respectively, is tested. Thus, these groups should not make adjustments to their investments in light of new information about child academic success. On the contrary, parents with an initial level of investment in the middle of the distribution of investments should change their level of investment when observing child academic success or failure (cf. Figure 5).

Illustration of the empirical hypothesis.

Data and variables

The empirical illustration uses data from NLSY-CYA. These data are the best-suited available data for this purpose as they are longitudinal, measured every second year, and have detailed information on parental investment, child academic achievement, and a multitude of parent and child background factors. The data include observations only if they have valid information for all variables for two consecutive periods between 1988 and 2010, which is the span of the data that include parental investment measures. This sampling frame leads to an analysis sample of 5434 children aged 6–14 years with 75% of children aged 6–10 years.

The model uses changes in parental investments over time as the dependent variable. While ideally the analysis would instead focus on changes in parents’ beliefs, to my knowledge, no such longitudinal data exist. Using actual investments as a proxy is not perfect, but the assumption that actual investments are linked to beliefs about their importance is supported by the theoretical model and also tentatively by the data. When the mothers in the data are first surveyed about their child, they report whether they believe children learn best on their own or whether their parents should teach them. 15 Mothers who believe that parents should teach their children also tend to exhibit higher levels of investments, lending some credence to this assumption.

This article measures parental investments using a series of variables from the HOME-SF battery of questions pertaining to both money spent on and time spent with the child, providing a single variable that captures overall parental investments (Cunha and Heckman, 2007; US Bureau of Labor Statistics, 2015). The battery includes the number of books the child has, whether the child has a musical instrument, whether he or she is enrolled in extra lessons or extracurricular activities, how often the child is taken to a museum or a performance, how often parents assist with homework, and how often parents discuss television programs with the child. 16 Appendix 4 describes the wording and distributions of all items.

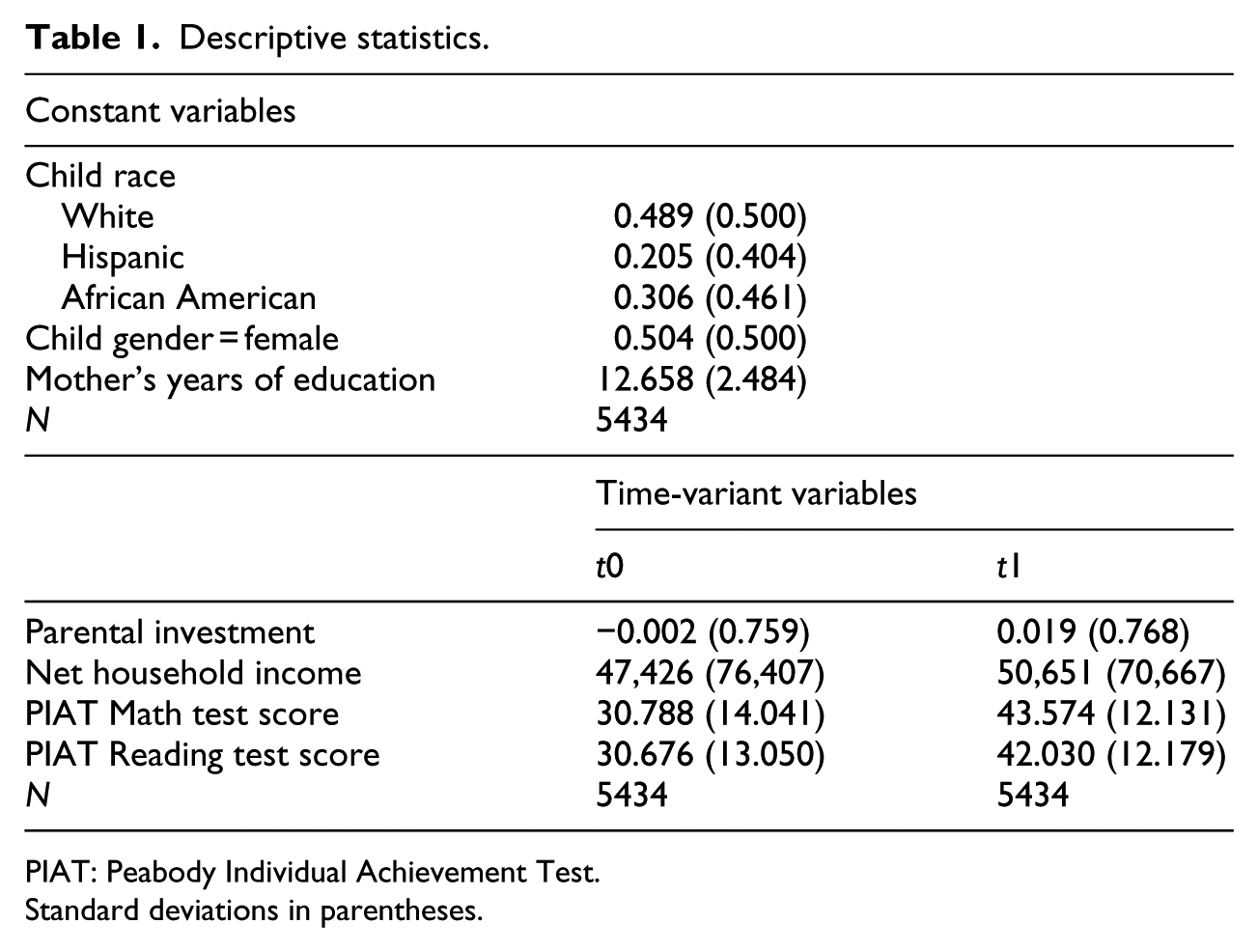

The main explanatory variable in the analysis is the child’s academic success or failure as measured by changes in the Peabody Individual Achievement Test (PIAT) of mathematics and reading. This test is considered a highly reliable and valid assessment of academic ability, its results correlate strongly with other cognitive measures (US Bureau of Labor Statistics, 2015), and it is often used as a measure of academic ability (Fryer and Levitt, 2004; Rosenzweig and Wolpin, 1994; Todd and Wolpin, 2007; Waldfogel et al., 2002). However, it is important to note that this test score is not viewed directly by the parents and only serves as a signal insofar as it correlates with other measures that parents observe, such as grades, SAT scores, or passing classes. Thus, the variable is inherently a weak signal and is likely to underestimate the changes in investments that would occur from stronger signals. In light of this circumstance, the analysis code for test scores is divided into three groups: success, failure, or no signal. Parents whose child’s changes in test scores fall in the upper or lower quartile of the distribution of test score changes receive a signal of child academic success or failure, respectively. 17 The empirical model assumes that test score changes in the middle part of the distribution are too weak a signal for parents to respond in a meaningful way. All models also control for race and sex of the child, mother’s education, and changes over time in household disposable income. The models do not control for child age as the sample has little variation in child age, and performing the analysis separately for age groups does not alter the results substantially (results not shown). Table 1 summarizes these variables.

Descriptive statistics.

PIAT: Peabody Individual Achievement Test.

Standard deviations in parentheses.

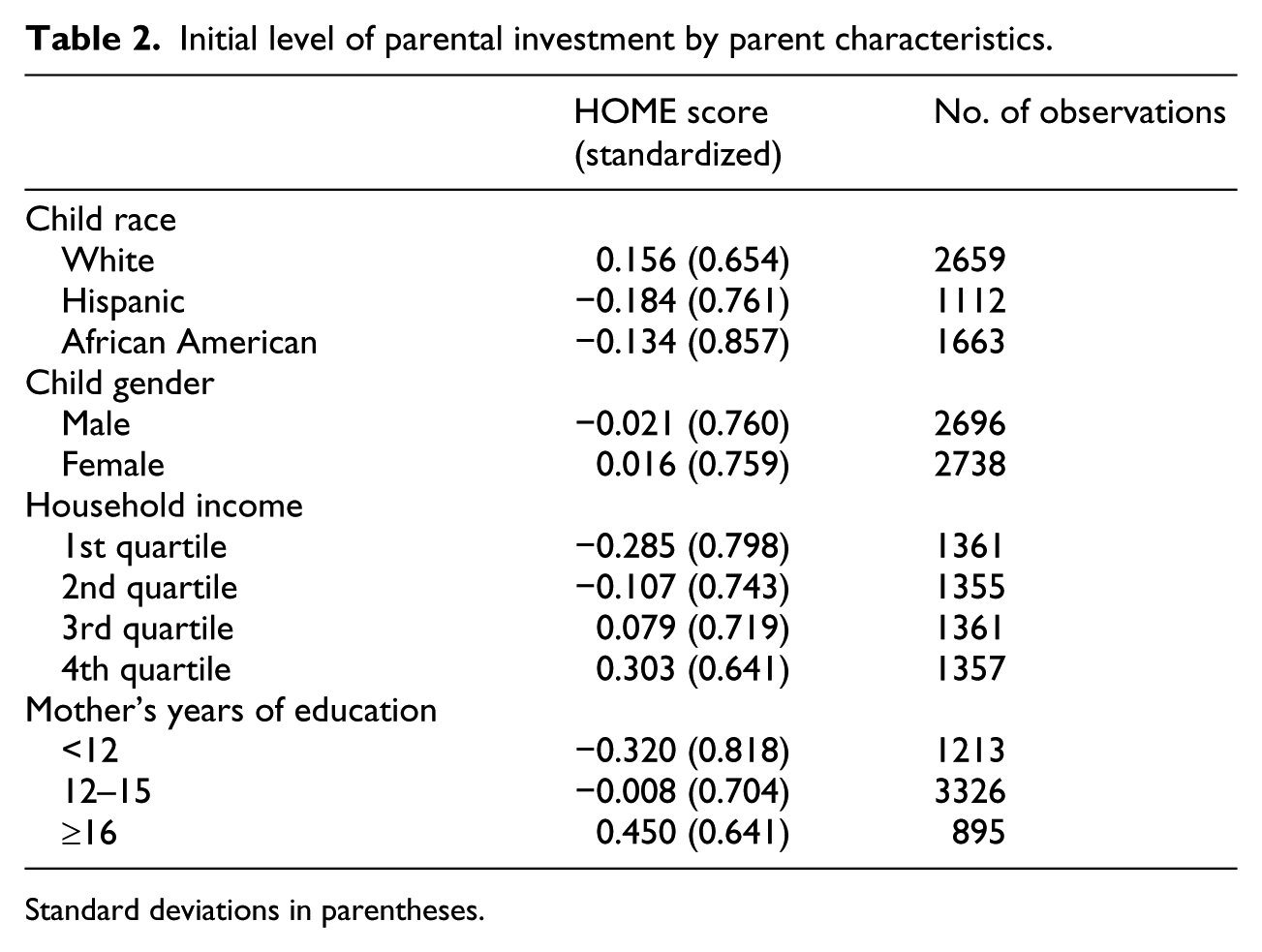

Furthermore, Table 2 shows how parents’ initial level of investment varies by their observable characteristics. Higher income and higher maternal education are both associated with substantially increased parental investment. White parents invest more on average than both Hispanic and Black parents do, and girls tend to benefit from a slightly higher level of investments than boys do. These differences follow the expected patterns considering both the formal model and previous findings and suggests that they should be included as control variables in the analysis.

Initial level of parental investment by parent characteristics.

Standard deviations in parentheses.

Model illustration: heterogeneous responses to signals from the child

To test the hypothesis presented herein, this section proposes a model that exploits variations over time in parental investments and child test scores. The model regresses the change in parental investments on changes in the child’s reading and math test scores, representing success, failure, or no signal, as described above, net of a vector of controls. By estimating a total of three regression models for parents with a low, intermediate, or high level of prior investments, the model evaluates whether these three groups react differently to their child’s signals of academic success or failure. As changes in both test scores and parental investments occur simultaneously over a period of 2 years, causality does not only flow from changes in test scores to changes in investments but also from changes in investments to changes in test scores. Accordingly, over the course of the 2 years, multiple updates may occur. The model is descriptive and seeks to describe heterogeneity in responses conditioned on initial levels of investments rather than to evaluate the causal link between test scores and parental investments. The model uses ordinary least squares for estimation and takes the following form

where the dependent variable, ∆

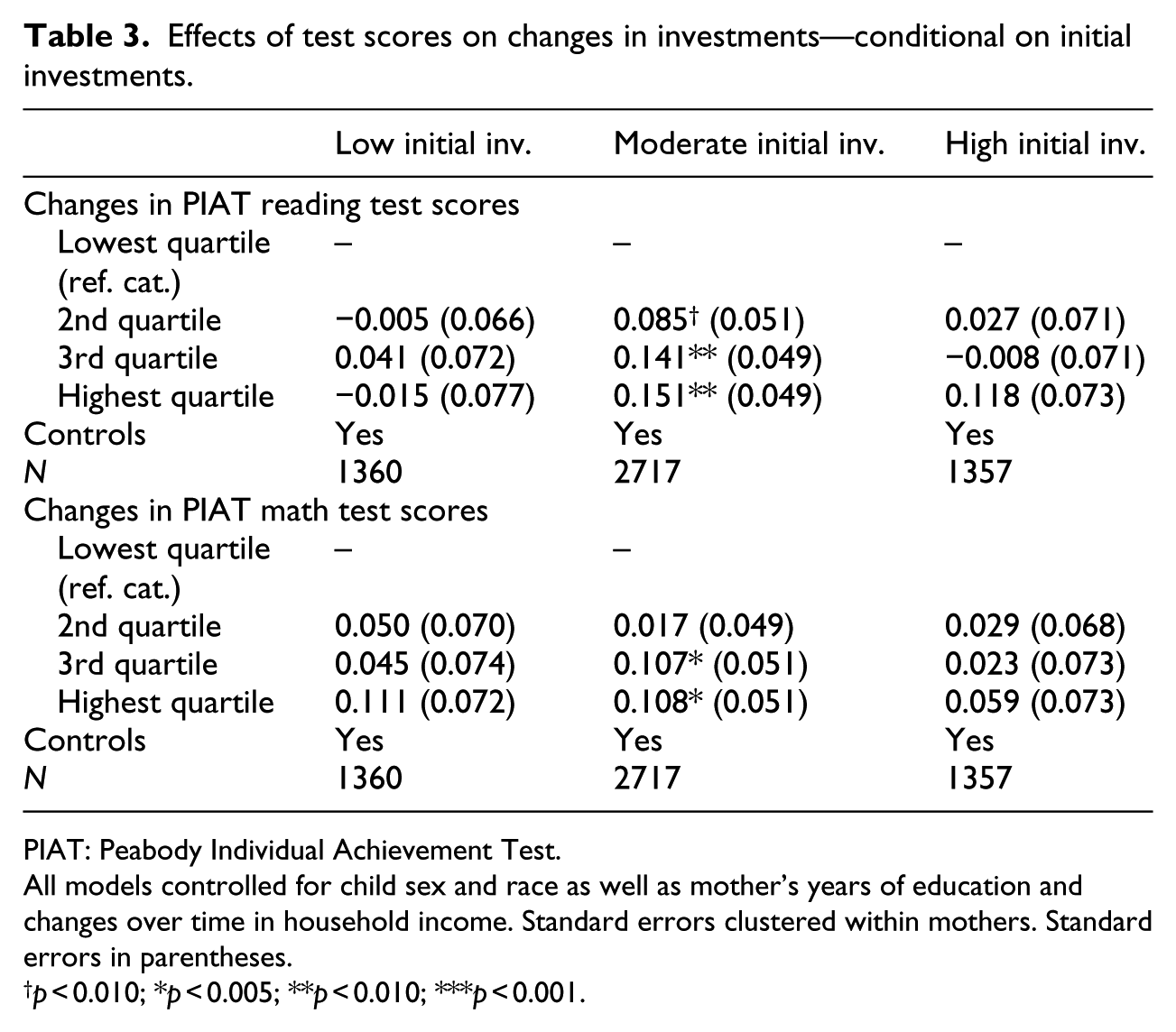

Effects of test scores on changes in investments—conditional on initial investments.

PIAT: Peabody Individual Achievement Test.

All models controlled for child sex and race as well as mother’s years of education and changes over time in household income. Standard errors clustered within mothers. Standard errors in parentheses.

p < 0.010; *p < 0.005; **p < 0.010; ***p < 0.001.

Overall, the empirical results follow expectations as parents in the top and the bottom quartiles of the initial investment distribution do not adjust their investments due to changes in child test scores. By contrast, parents whose initial investments are in the two intermediate quartiles increase their investments significantly in light of positive changes in test scores, and vice versa. These results support the hypothesis that investments only change for parents who have not yet adopted one of the two stable beliefs. Compared to using math test scores, effect sizes are larger and p-values are smaller when using reading test scores, perhaps because the ability to read and write is a larger component of the everyday interactions that parents have with their child. In conclusion, the empirical results are consistent with a central assumption in the proposed formal model. That is, parents respond differently to the same signals of child academic performance when they have different prior levels of investments. This finding cautiously points to the feasibility of conceptualizing parents as Bayesian learners and supports the notion that multiple stable beliefs exist. At the very least, any conceptualization of parents learning the returns on their investments should include the possibility of holding a stable, but false belief. Despite the returns on parental investments presented in previous literature works (Cunha and Heckman, 2007; Todd and Wolpin, 2007; Yeung et al., 2002), these parents maintain a low level of investments regardless of their child’s academic failure or success. Thus, these parents represent the prototype of parents who believe that they do not have a substantial influence on their child’s academic success when compared to other factors, such as race, luck, teacher bias, school quality, or child ability. Conversely, parents with high levels of investment do not respond to the signals they receive from their child because they are already convinced (rightly) that they know the actual returns on their investments.

Discussion

The positive effects of parental investments in children, such as reading to them or providing high-quality day care, are well documented in recent research, as are the socioeconomic gradients in these investments (Cunha and Heckman, 2007; Todd and Wolpin, 2007; Yeung et al., 2002). Highly educated, financially stable, and/or White parents systematically invest more in their children, which offers an explanation for the empirically observed gaps in academic success between SES and race groups (e.g. Fryer and Levitt, 2004). This article proposes a formal model to explain the mechanisms through which these gaps in parental investments come to be and how they persist across generations. The main contribution of the article is to propose a formal model that clarifies the role of parental beliefs in the returns on their investments, a concept traditionally missing from models of intergenerational transmission of resources and human capital accumulation (e.g. Becker and Tomes, 1986; Cunha et al., 2006)). Rather than assuming that all parents know the actual returns on their investments, this article presents a model in which parents have a belief about the returns on their investments, and this belief may or may not be consistent with the truth. Conceptually, the model argues that if parents do not believe that their investments are an important factor contributing to their child’s outcomes, they will spend more of their resources on personal consumption compared to those parents who believe their investments contribute significantly to the success of their child.

Consistent with previous research, this article models the process of belief formation and evolution by using Bayesian learning (Breen, 1999; Morgan, 2005; Piketty, 1995). The model indicates that parents can have two different stable beliefs about the returns on their investments. They can either hold the true belief knowing the actual returns on their investments or hold a false belief, known as the CLE (Breen, 1999; Breen and García-Peñalosa, 2002; Piketty, 1995), which causes them to underinvest. While the true belief is the same for all parents, the CLE varies due to other factors, such as race and SES. Thus, comparing, for example, high SES and low SES parents both at the CLE, the disadvantaged parents will underinvest even more so than their advantaged counterparts. This provides two explanations for the parental investment gaps that arise from the systematic differences in holding true or false beliefs as well as from disadvantaged parents who suffer even more severe consequences due to false beliefs than do advantaged parents. The model also formalizes the mechanism through which parents transmit beliefs to their child and concludes that children are more likely to inherit their parents’ stable beliefs, thus reproducing intergenerational gaps in parental investments.

The empirical section of the article uses American data on parental investments to test key features of the model. The results offer tentative support for the existence of two stable beliefs, one true and one false, by showing that parents adjust their investments differently depending on their prior investments. Parents with either a high or a low level of prior investments do not change their investments in light of their children’s academic success or failure, a finding that the model interprets as them having already committed to the true belief or the CLE, respectively. On the contrary, parents with an intermediate level of prior investments react to child academic outcomes by changing their subsequent level of investments.

Suggestions for future research

Models such as the one presented in this article need not be restricted to explaining educational outcomes. Previous empirical research has shown differentials in parental investment behavior whether the outcome is child health or child education (Ayalew, 2005). Just as the model presented in this article draws on Breen’s (1999) work on student beliefs in effort versus ability, future models could utilize this framework with different outcomes or different inputs. This type of formal modeling presents a flexible way to conceptualize and explain a wide range of processes regarding the adjustment of beliefs in light of new information and the transmission of these beliefs across generations.

In addition, this article holds several prospects for future empirical research pertaining to the role of beliefs in parental investments. In particular, an analysis of longitudinal data sets with direct measures of beliefs would be useful with respect to the further investigation of the usefulness of the model. Similarly, studies of the links between, on one hand, beliefs in the returns on parental investments and, on the other, parents’ actual investment levels would be valuable.

Limitations and assumptions

The model presented in this article assumes that parent learning is completely endogenous, that is, that parents only update their beliefs according to the signals they receive from their child. This assumption is strong, and research on identity formation finds that although parents are the primary source of values and beliefs, peer groups and neighborhoods also play an important role (Bisin et al., 2011; Fordham and Ogbu, 1986). Furthermore, research on the importance of information and beliefs about college costs reveals that external sources of learning, such as instruction, can change not only the beliefs but also the behaviors of students (Barone et al., 2017; Bettinger et al., 2010; Loyalka et al., 2013). However, as observed by Breen (1999), there are several challenges associated with learning from others as, for example, it is difficult for parents to obtain precise information on many aspects of other parents, such as SES, child’s ability, and level of investments. Considering this, it seems unlikely that parents will change beliefs based on information that they may deem unreliable. However, if parents are able to observe a case about which they have information regarding most of the variables, such as family or close friends, they may then be able to learn from this information. For policy purposes, an example of such a case would be to provide parents with prolonged exposure to strong role models, a strategy that has previously proven effective (Evans, 1992; Ssewalama et al., 2012; Whiting, 2006). In regard to this approach, future research should seek to formalize learning from others as a component in the model.

Another limitation of the formal model in its current form is the assumption of one-child families. While this simplification substantially eases the derivation and interpretation of the model, it is unlikely to hold for obvious reasons. Parents more often than not have more than one child, and it is highly plausible that they use lessons learned from their first child to inform their investments in the second child. The possibilities to theorize about these learning processes are many. For example, do parents hold separate beliefs about returns on investment for each child, or do they update a single belief for all children? If so, what implications does this have for the first-born child as parents receive new information? Questions such as these should be considered as contributions in themselves and as promising avenues for future research.

Policy implications

Although the formal presented in this article is theoretical and the empirical illustration not a strict causal analysis, this article may cautiously inspire a new supplementary focus for policy intervention. For example, research on college education indicates that it is possible to change people’s beliefs about costs and opportunities by providing them with high quality information (Barone et al., 2017; Bettinger et al., 2010; Loyalka et al., 2013). On the contrary, though, interventions targeted at increasing parental involvement show mixed results when it comes to changing parents’ behavior (Pomeranz et al., 2007). If, however, persistent parental investment gaps are indeed partially rooted in false beliefs about low returns, policy-makers could provide disadvantaged groups with reliable information and attempt to change their beliefs rather than directly affect their behavior. Through campaigning and the use of role models, it may be possible to shift low investing parents’ beliefs toward the optimal stable belief, thus prompting them to invest more in their child. Such policy interventions are relatively inexpensive compared to targeted monetary transfers. Thus, they may serve to activate untapped parent resources already present in disadvantaged racial or social groups, thereby narrowing or closing parental investment gaps. It bears repeating, however, that this article in itself does not provide sufficient evidence to base any policy intervention on; rather the article presents a theoretical framework for further empirical analyses that may bolster or test these recommendations.

Footnotes

Appendix 1

Appendix 2

Appendix 3

Appendix 4

Acknowledgements

I thank Mads Jæger, Richard Breen, Anders Holm, Robin Kaarsgaard, Kristian Karlson, Peter Skov, Peter Fallesen, Jens-Peter Thomsen, Per Engzell, Asta Breinholt Lund, Benjamin Jarvis, and the participants of UNITRAN’s summer workshop 2015, the RC28 Spring Meeting 2015, and the ASA 126th Annual Meeting for valuable comments and feedback.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research leading to the results presented in this paper has received funding from the European Research Council under the European Union’s Seventh Framework Programme (FP/2007-2013)/ERC Grant No. 312906 and No. 324233, Riksbankens Jubileumsfond (DNR M12-0301:1), and the Swedish Research Council (DNR 445-2013-7681 and DNR 340-2013-5460).