Abstract

This study revisits the assumption that moderate growth offers the most reliable path to new venture survival. Adopting a lifetime growth perspective, we distinguish genuine failure from strategic or neutral exits to better understand the growth–survival relationship. Using 246,831 venture-year observations from 52,277 Dutch startups (2007–2019), we replicate and extend prior research. While moderate annualized growth enhances short-term survival, our extension reveals a contrasting long-term pattern: ventures with either low or high lifetime growth exhibit the greatest survival likelihood. These findings reconcile competing perspectives and highlight how ventures need to navigate short- and long-term pressures to survive.

Introduction

The long-standing assumption that moderate growth offers the most sustainable path to new venture survival has profoundly shaped entrepreneurship theory. This view holds that growing at a moderate pace allows ventures to accumulate resources and develop operational routines without overextending managerial, financial, or organizational capacity (Coad et al., 2020; Delmar et al., 2013; Pierce & Aguinis, 2013). By balancing ambition and control, moderate growth has been portrayed as a strategically cautious response to the uncertainties of venturing. However, this logic has increasingly been questioned, as alternative perspectives suggest that survival may also emerge at opposite ends of the growth continuum, when ventures either deliberately consolidate or scale rapidly.

Retrenchment theory, for instance, proposes that negative or very low growth associated with downsizing, restructuring, or strategic refocusing can improve long-term viability (Barker & Duhaime, 1997; Pearce & Robbins, 2008) by shedding unprofitable activities, reducing excess capacity, and reallocating resources to core functions (Flammer & Ioannou, 2021; Tangpong et al., 2015). Conversely, theories of competitive dynamics and first-mover advantages emphasize that rapid growth can enhance survival by enabling ventures to capture market share and preempt rivals (Cirik & Makadok, 2023; Paeleman et al., 2024). Together, these perspectives suggest that ventures may survive through either disciplined retrenchment or aggressive expansion, thereby challenging the assumption that moderate growth is universally optimal and raising a central question: under what conditions do low, moderate, and high growth trajectories differentially shape venture survival?

To reconcile these seemingly competing views, we argue that it is essential to examine ventures’ lifetime growth trajectories and to distinguish failure from other exit routes. Prior research has typically operationalized growth using annualized employment changes in the 1 to 3 years preceding survival or failure events (Soto-Simeone et al., 2020). Although this approach captures short-term variation, it may conflate temporary fluctuations with the cumulative processes that shape long-term outcomes (Denrell et al., 2015; Lundmark et al., 2020). Prior studies suggest that survival depends on cumulative dynamics through which ventures build capabilities, financial slack, reputational standing, and competitive positions across successive growth episodes (Kor & Mesko, 2013; Symeonidou et al., 2022). Accordingly, the effects of growth are path-dependent rather than immediate and accumulate as ventures develop routines, resources, and legitimacy over time (Levie & Lichtenstein, 2010). Failures, in turn, rarely arise from a single year of contraction or stagnation but instead reflect prolonged patterns of underinvestment, eroding legitimacy, or persistent resource constraints (Coad, Daunfeldt, et al., 2018; Lukason & Laitinen, 2019). Beyond these dynamics, a fuller understanding of the growth–survival relationship also requires distinguishing failure from other types of exit. Some discontinuations, such as acquisitions or mergers, may reflect successful entrepreneurial outcomes rather than failure (DeTienne et al., 2015). These exits often mark the achievement of entrepreneurial goals and the continuation of products, services, or capabilities under new ownership (Coad & Kato, 2021; Rauch & Rijsdijk, 2013; Wennberg et al., 2010). Acknowledging these distinctions clarifies the boundary between genuine failure and positive or neutral exits and provides a more nuanced understanding of how ventures grow, adapt, and survive over time.

In this study, we re-examine how venture growth influences survival by replicating and extending prior research on the growth–survival relationship. Building on the influential work of Pe’er et al. (2016; hereafter PVK), we analyze a longitudinal dataset of 246,831 firm-year observations from 52,277 Dutch new ventures founded between 2007 and 2017 and followed until 2019. Because growth effects on survival are cumulative and not all exits represent failure, our approach introduces two-key refinements to the measurement of growth and survival. First, we move beyond annualized growth rates that capture short-term variation and instead measure each venture’s average growth rate from its first substantive expansion up to each year of observation. This approach mitigates short-term fluctuations and captures the cumulative nature of growth processes (Denrell et al., 2015). Second, we refine the measurement of failure by excluding alternative exit modes, such as mergers, acquisitions, and restructurings, from the failure category (Coad & Kato, 2021; Dobrev & Gotsopoulos, 2010; Wennberg et al., 2010). Our exact replication of PVK confirms that moderate annualized growth enhances short-term survival. However, our extension reveals a contrasting long-term pattern: ventures with either low or high lifetime growth exhibit the greatest survival likelihood. This finding challenges the long-standing assumption that moderate growth is universally optimal and suggests that both disciplined retrenchment and sustained aggressive expansion can serve as viable long-term survival strategies for new ventures.

In doing so, our study advances the literature on new venture growth, high-growth firms, and entrepreneurial survival in two important ways. First, we show that the relationship between growth and survival is contingent on the temporal horizon considered. Grounded in the growth theory of the firm (Penrose, 1959), traditional models that adopt a relatively narrow time horizon portray moderate growth as optimal because it balances expansion and control while limiting the short-term risks of under- or overextension (Pe’er et al., 2016). Taking a lifetime perspective, however, our study shows that these short-term benefits can translate into long-term liabilities. While moderate growth sustains new ventures in the short run, it may position them between two distinct long-term survival logics. On the one hand, low-growth ventures preserve viability through focus, cost discipline, and reliability (Pearce & Robbins, 2008; Trahms et al., 2013). On the other hand, high-growth ventures may endure by prioritizing speed over efficiency to build capabilities and capture markets through first-mover advantages (Hoffman & Yeh, 2018; Jansen & Tippmann, 2026; Tidhar et al., 2025; Varga et al., 2023). In this way, our study bridges short-term logics of control and risk reduction with long-term logics of conservation and adaptation, thereby advancing a more dynamic understanding of how ventures transform growth into resilience over time (Levie & Lichtenstein, 2010; Van de Ven & Engleman, 2004).

Second, our results help explain why prior studies have reported inconsistent findings on the growth–survival relationship. We show that these inconsistencies arise not only from differences in the temporal horizon used to measure growth but also from how survival has been defined and operationalized. Many studies conflate genuine failure with positive discontinuation events such as acquisitions or mergers, thereby blurring theoretically distinct outcomes and biasing estimates against high-growth firms, which often exit through acquisition precisely because of their success (Coad & Kato, 2021; Wennberg et al., 2010). By restricting failure to the discontinuation of productive activity and excluding exits that reflect continuity under new ownership or strategic control, our study clarifies the conceptual boundaries of survival and provides a more accurate account of how growth trajectories shape ventures’ long-term endurance.

Re-Examining the Venture Growth–Survival Relationship

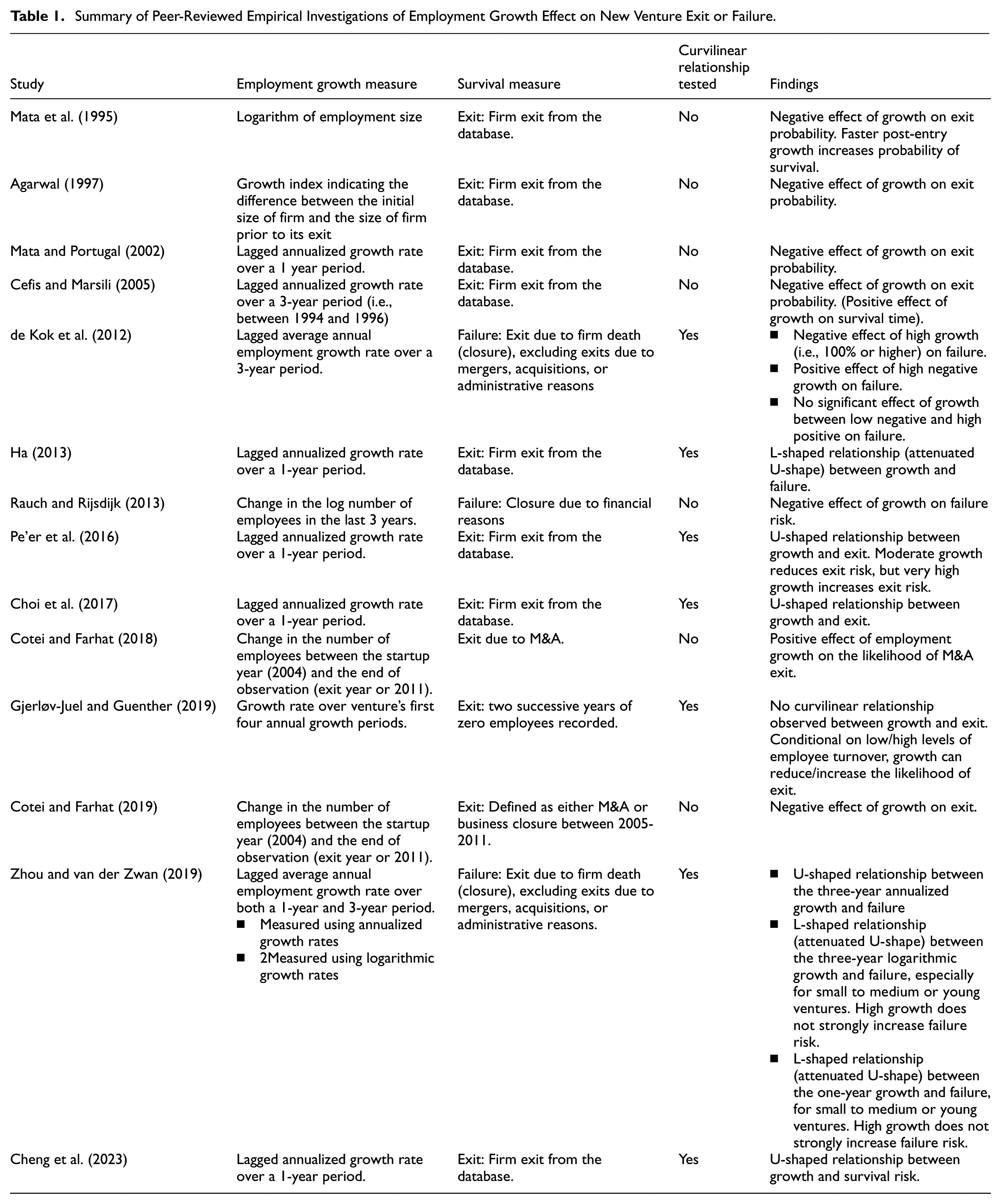

The relationship between new venture growth and survival has been a central theme in entrepreneurship and strategy research. 1 A long tradition of studies has explored how and when growth enhances a venture’s capacity to endure beyond its formative years (Gjerløv-Juel & Guenther, 2019; Pe’er et al., 2016; Zhou & Van der Zwan, 2019). Research has established growth as a key determinant of long-term viability and emphasized mechanisms such as economies of scale, learning, and improved access to resources (Delmar et al., 2013; Mata & Portugal, 2002). A major insight from this literature is that the growth–survival relationship is not strictly linear but shaped by tensions between the benefits of expansion and the strains it imposes. Despite these advances, two theoretical limitations remain. First, prior studies have relied on short-term measures of growth, which limits understanding of how growth trajectories unfold and shape survival over time. Second, survival is often treated as the mere continuation of operations, overlooking the different meanings and outcomes of exit. As summarized in Table 1, we argue that the variation in the conceptualization and measurement of growth and survival may explain inconsistencies in findings and the resulting interpretations of the venture growth–survival relationship.

Summary of Peer-Reviewed Empirical Investigations of Employment Growth Effect on New Venture Exit or Failure.

Most studies on the growth–survival relationship estimate survival models using growth rates observed 1 to 3 years before exit or failure (Muzi et al., 2023; Rannikko, Tornikoski et al., 2019). While this approach captures how ventures respond to immediate pressures such as market shifts or competitive shocks, it risks overemphasizing short-term fluctuations and conflating temporary adjustments with the cumulative processes that shape long-term survival (Denrell et al., 2015). In essence, it captures isolated episodes rather than broader growth trajectories. Theories of the “shadow of death” illustrate this limitation. Negative growth in the years preceding exit often reflects anticipation of failure rather than its underlying cause, as firms nearing closure deliberately downsize or liquidate assets to limit losses (Coad, 2018; Coad et al., 2021). Conversely, late-stage growth spurts may signal reactive attempts to stave off decline (Paeleman et al., 2024). As a result, studies relying on annualized growth rates may capture symptoms of impending failure rather than the deeper mechanisms through which ventures develop endurance and resilience.

What remains theoretically underdeveloped is how lifetime growth trajectories shape why some ventures endure while others fail. The liability of newness perspective suggests that survival depends on the gradual accumulation of routines, relationships, and legitimacy (Brüderl & Schüssler, 1990; Stinchcombe & March, 1965). Ongoing growth decisions in hiring, retrenchment, or scaling become embedded in these structures and shape stakeholders’ perceptions of competence and reliability (DeSantola & Gulati, 2017). Legitimacy rarely hinges on a single growth episode but instead emerges from enduring patterns that signal stability and long-term potential (Nason et al., 2015; Zimmerman & Zeitz, 2002). From a resource-based perspective, survival likewise depends on how ventures build and reconfigure financial, human, and reputational capital over time (Kor & Mahoney, 2005; Kor & Mesko, 2013; Symeonidou et al., 2022). Each hiring wave, market entry, or retrenchment adjusts these resources and shapes the firm’s capacity to absorb shocks and adapt to change. Ventures that align cumulative growth investments can transform expansion into resilience and adaptive capability (Levie & Lichtenstein, 2010), whereas erratic or reactive growth may yield short-term gains but leave firms structurally fragile.

A long-term perspective helps explain how different growth trajectories, ranging from low to moderate to aggressive expansion, shape the gradual development of capabilities and legitimacy over time, thereby influencing survival (Penrose, 1959; Teece et al., 1997; Trahms et al., 2013). Rather than assuming that any single level of growth is universally optimal, this view emphasizes that outcomes depend on how ventures translate cumulative expansion into enduring organizational strength. This reasoning underpins our extension approach, which focuses on lifetime growth rather than short-term adjustments to capture how ventures convert growth into survival potential.

A refined understanding of survival is also essential. Prior research typically models survival by tracking firms until an exit event such as bankruptcy, acquisition, or restructuring occurs (Cefis et al., 2022; Wennberg et al., 2010). While this approach captures firm longevity, it often conflates outcomes that differ fundamentally in meaning and consequence. Many studies operationalize survival as the absence of exit, treating bankruptcy, liquidation, acquisition, and merger as equivalent outcomes. Although this perspective has been instrumental in demonstrating the fragility of new ventures and the difficulty of sustaining operations in competitive markets (Cefis et al., 2022; Pe’er et al., 2016), it obscures important distinctions between failure and positive discontinuation. Failure marks the cessation of productive and organizational activity, whereas positive discontinuation occurs when ventures continue under new ownership or strategic control. Some exits arise from internal restructuring that preserves key routines, resources, or capabilities in a different organizational form (Coad, 2014; Decker & Mellewigt, 2007). Others, such as acquisitions, reflect the successful realization of entrepreneurial intent, where founders deliberately build ventures for sale or integration into larger entities (Dobrev & Gotsopoulos, 2010; Wennberg et al., 2010). Overlooking these differences risks distorting survival models, particularly for high-growth firms that attract acquirers precisely because their expansion has created market value and legitimacy. Defining survival as the likelihood of avoiding genuine failure, understood as the definitive end of productive and organizational continuity, provides a more accurate and theoretically grounded account of venture endurance.

Our replication and extension build directly on these theoretical refinements and translate them into an empirical framework that captures how ventures evolve, adapt, and persist over time. By adopting a longitudinal perspective on growth trajectories together with a refined conceptualization of survival, we address both the temporal and definitional foundations of the venture growth–survival relationship. Specifically, we redefine survival to exclude positive discontinuation events such as acquisitions and mergers, and measure growth using lifetime averages rather than short-term fluctuations. These extensions allow us to revisit established assumptions and show how survival depends on the cumulative processes that shape long-term growth trajectories.

Sample and Data Collection

To anchor our analysis in an established empirical framework, we replicated and extended the study by Pe’er et al. (2016; hereafter PVK), which examined how new venture growth relates to survival using a large panel of Canadian startups. Their work provides a rigorous foundation for modeling the link between firm-level growth patterns and exit probabilities and has become a key reference in the literature. By adopting a comparable sampling strategy and empirical design, we both validate and refine their findings in a different national and institutional context. At the same time, we incorporate conceptual and methodological extensions that address the measurement of growth trajectories and the distinction between failure and other forms of exit.

Sample

Our sample consists of Dutch ventures identified using a procedure similar to that of PVK. We constructed the dataset from census data provided by Statistics Netherlands (CBS), which contains complete records of all registered firms in the Netherlands. Specifically, we relied on three longitudinal sources. The General Business Registry (ABR) provided data on registration and deregistration dates as well as restructuring events such as mergers, acquisitions, and dissolutions. The Business Demographics (BDK) database offered annual information on employment, industry classification, and metropolitan area. The Finances of Non-financial Corporations (NFO) database supplied financial indicators including revenues, sales, and expenses. Our observation window spans 13 years, from 2007 to 2019.

Consistent with PVK, we excluded ventures that were subsidiaries or otherwise dependent on existing firms at the time of founding. We also excluded ventures with multiple establishments and began tracking ventures only after they started hiring, meaning they reported positive employment growth and had at least two workers at the start of observation (including founders). Firms with only one observation were removed to avoid bias from ventures that, by construction, showed both an exit and a positive growth rate. We also excluded observations with fewer than two workers in years t–2 and t–1. As a result, our final sample reflected genuine new ventures excluding subsidiaries of larger corporations and self-employed entrepreneurs, while minimizing extreme growth rates derived from worker counts below two (e.g., growth from 0.5 to 1.5 employees would produce an inflated 300% rate). Finally, we trimmed the upper and lower 0.5% of the growth distribution to reduce the influence of outliers that could distort the estimated growth effects and to align the growth range with PVK.

Following the recommendations of Ethiraj et al. (2016) and Eden (2002), we enhanced the quality of our replication by expanding the scope of our sample. Specifically, we moved beyond PVK’s single-industry focus and included ventures from all non-governmental industries. A broader industry base allowed us to test whether the theoretical logic underlying the growth–survival relationship generalizes across industries (Ethiraj et al., 2016). We also addressed one of PVK’s acknowledged trade-offs between the richness of variable measurement and the comprehensiveness of the sample (Pe’er et al., 2016, p. 564). Our data allowed us to expand coverage without compromising variable inclusion. However, finance-related control variables could not be measured for all observation years because the NFO dataset contained fewer records than the BDK and ABR sources used to estimate employment and exit-related variables (i.e., growth, failure, relative employment, and employment-rate failure). To address this, we followed Benton et al. (2022) and Wasserman (2017) by applying multiple imputation to missing financial data. 2 Specifically, we applied Predictive Mean Matching to ensure robustness against nonlinearities, heteroscedasticity, and non-normality in our large sample (Kleinke, 2018).

Our resulting manufacturing sample comprised 15,047 yearly observations from 3,178 ventures, including 813 exits. The multi-industry sample contained 246,831 yearly observations from 52,277 ventures, with 15,424 exits. This corresponded to exit rates of 25.58% in manufacturing and 29.5% in the multi-industry sample. For comparison, PVK reported 46,879 ventures, 250,524 yearly observations, 11,052 exits, and a total exit rate of 23.57%. Overall, our sample closely mirrors PVK’s dataset, and the comparable exit rates provide support for the robustness of our replication.

At the same time, it is important to acknowledge several contextual and temporal differences between our setting and that of PVK that may shape the observed relationships. PVK analyze Canadian manufacturing ventures between 1984 and 1998, whereas our study examines a more recent cohort of Dutch ventures between 2007 and 2019 and extends beyond manufacturing to a broader set of industries. These differences are also reflected in the composition and institutional setting of the samples. Moreover, the Netherlands represents a densely populated and highly interconnected economy characterized by strong agglomeration, localized competition, and knowledge spillovers (Boschma, 2017; Frenken et al., 2007; Steijn et al., 2022), whereas Canada’s economic geography is more spatially dispersed and regionally heterogeneous (Beaudry & Schiffauerova, 2009). These structural differences may influence how growth translates into survival, particularly with respect to the role of local competition, knowledge spillovers, and geographic dynamics. In addition, the more recent observation window of our study captures an economic context marked by increasing globalization and a shift toward service-oriented and knowledge-intensive activities in advanced economies (Bosma et al., 2008). Taken together, these contextual and temporal differences suggest that some of the environmental mechanisms identified by PVK may not fully generalize across settings, while at the same time reinforcing the value of replication and extension for identifying boundary conditions of the growth–survival relationship (Ethiraj et al., 2016).

Exact Replication: Measurement Approach

We adopted the exact measurement approach for the dependent and independent variables as in PVK. The dependent variable, new venture exit, was coded as 1 when the firm was no longer observed in our dataset. The independent variable is the annualized growth defined as the lagged relative change in employment from t–2 to t–1. Employment is expressed in full-time equivalents (FTEs), which convert part-time and flexible contracts into standardized units of full-time labor. This approach ensured that our estimates capture substantive growth dynamics rather than institutional artifacts, which is particularly important in the Dutch context where permanent employees are costly to dismiss (Anyadike-Danes et al., 2015; Haltiwanger et al., 2013). As detailed in Appendix A, we also included a similar set of control variables to those used by PVK. These comprised venture assets, human capital quality, and size (each relative to the venture’s sector) as well as the venture’s Economic Region (ER) failure rate, ER average wage, industry sales growth, ER industry sales growth, industry competition, and metropolitan area, industry, and time fixed effects.

Extension: Measurement Approach

To measure the dependent variable (i.e., failure) in our extension, we used event data from the ABR, which records nine distinct events that may change a firm’s identifier: (a) birth, (b) change of characteristic or link, (c) birth–death combination, (d) demerger, (e) breakup, (f) acquisition, (g) merger, (h) restructuring, and (i) death. We identified venture failure as those events classified as death (9), since they represent the termination of business operations without the intent to continue under a new legal entity or structure. All other exit events (e.g., acquisition, merger, restructuring) were treated as right-censored observations at the time of occurrence. These death events represent 83% of all exits in our sample.

The independent variable is the compound annual growth rate (CAGR), a time-varying measure that captures cumulative employment growth over the venture’s lifetime. It is calculated using Equation (1), where

Observed annualized growth and CAGR prior to exit for a growing firm (a) and a declining firm (b).

Yet, if their size prior to exit remains above founding levels, CAGR remains positive and captures the broader lifetime growth path.

We extended the baseline specification with several additional controls. First, we included firm age at t–1 as a time-varying covariate, since age is a key determinant of survival due to the liabilities of newness and adolescence, and because CAGR is mechanically correlated with venture age (Brüderl & Schüssler, 1990; Nason et al., 2015). Second, we added an interaction term between lagged CAGR and firm age at t–1 to account for potential variation in the effect of growth across the venture’s lifetime (DeSantola & Gulati, 2017; Hannan & Freeman, 1984). Third, we controlled for initial venture size at the beginning of each observation period, as the starting scale of a venture shapes the meaning of subsequent growth trajectories and influences early survival odds (Coad, Holm, et al., 2018; Mata & Portugal, 2002). Finally, we included a measure of lagged profitability at t–1 (operating profit margin), and a corresponding interaction term with CAGR, to ensure that observed growth effects do not simply proxy underlying financial strength (Altman et al., 2010; Geroski et al., 2010).

Model Specifications

Prior research on new venture survival typically employs either a maximum likelihood (ML) model with a Weibull distribution (as in PVK) or a Cox proportional hazards model, which generally yield similar marginal effects (Boehmke et al., 2006). The ML model is useful for benchmarking results against a Full-Information Maximum Likelihood (FIML) specification that can reduce bias in non-random samples or when self-selection is present (Boehmke et al., 2006). However, because our census-based dataset minimizes selection concerns, we used the Cox regression model. Its semi-parametric nature avoids assumptions about the underlying distribution of failure times and is widely considered robust since results closely approximate those of the correct parametric model (Kleinbaum & Klein, 2011). We replicated the main-effect models using both the linear and squared terms of annualized growth and CAGR, and omitted year dummies since the Cox model regresses failure over time (i.e., years) by design.

The Cox model accommodates both right-censored data and time-varying covariates, which allows us to include ventures with different lifespans without biasing results toward those surviving shorter or longer periods (Klein & Moeschberger, 2003; Therneau & Grambsch, 2000). This mitigates concerns that CAGR measures might otherwise capture growth over unequal observation periods across firms. The Cox model has become the standard in longitudinal survival analysis because it estimates hazard rates without requiring strict assumptions about the baseline hazard function (Box-Steffensmeier & Jones, 2004; DeTienne et al., 2015). In medical research, for example, it is commonly used to assess patient survival after treatments that begin at different times and vary in duration (Altman & Bland, 1994; Bradburn et al., 2003). By incorporating time-varying predictors, the model captures evolving firm characteristics and yields consistent survival estimates across observation periods. Across all specifications, we report robust standard errors clustered at the firm level. In our robustness checks, we also explore whether the functional form of the growth–survival relationship is more complex than typically modeled.

Findings

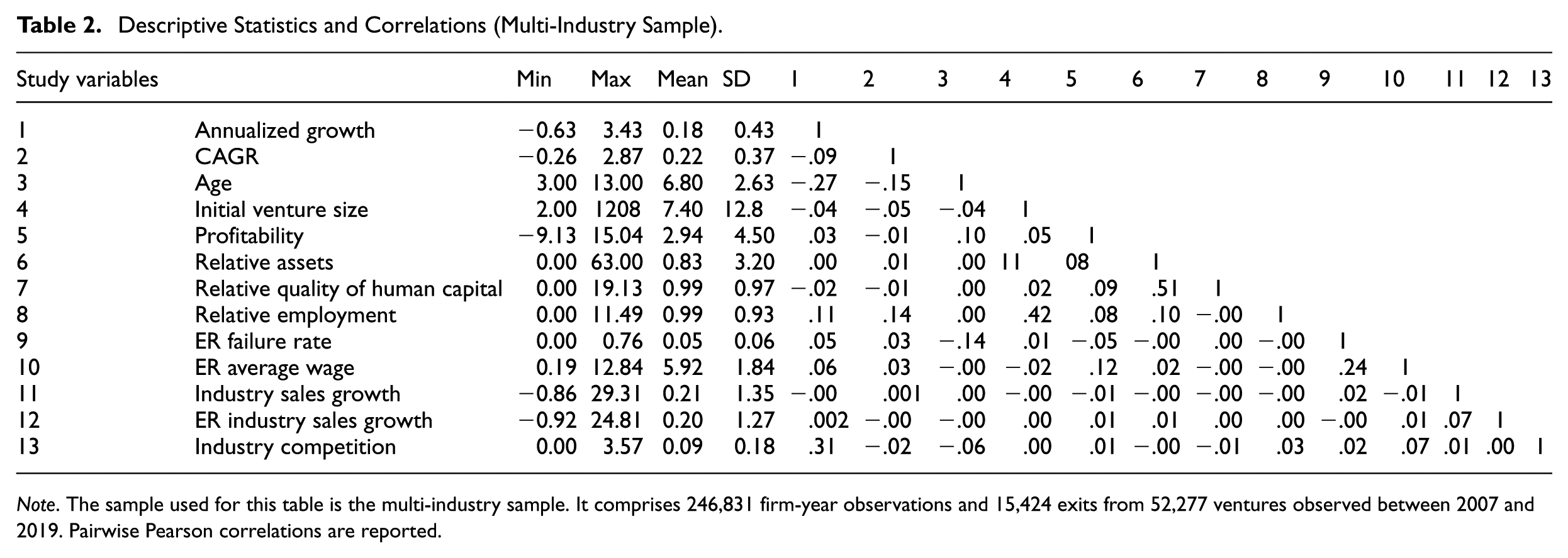

Table 2 presents the descriptive statistics and correlation matrices for all variables used in the replication and extension analyses for the multi-industry sample. The descriptive statistics indicate substantial variation in growth measures and industry characteristics. The correlation matrix reveals several notable patterns. First, annualized growth and CAGR are negatively correlated (r = −.09), suggesting that short-term growth fluctuations do not align with cumulative growth trajectories over time. Second, firm age is negatively correlated with both annualized growth and CAGR, reflecting that ventures tend to grow more slowly as they mature. Finally, the relative low to moderate correlations among the remaining variables indicate limited multicollinearity and provide support for the validity of the analyses presented below. For additional context, Appendix B provides a comparison of summary statistics across the PVK sample, our manufacturing replication sample, and the multi-industry extension sample.

Descriptive Statistics and Correlations (Multi-Industry Sample).

Note. The sample used for this table is the multi-industry sample. It comprises 246,831 firm-year observations and 15,424 exits from 52,277 ventures observed between 2007 and 2019. Pairwise Pearson correlations are reported.

Exact Replication: Effect of Annualized Growth on Exit in the Manufacturing Sample

In Table 3, models A1 and A2 present the results from our Cox regression model about the new ventures in the manufacturing sector. To maintain comparability with PVK, we further computed the Cox model’s average effects “E,” which are approximately equivalent in scale to Weibull log-hazard coefficients for standardized or relative variables (Cleves et al., 2016; Hosmer et al., 2008). These effects are computed as the expected change in log-hazard between the 25th and 75th percentiles of each covariate (Harrell, 2015). Based on Table 3, all coefficients of growth are statistically significant (p < .01) for both the linear and quadratic terms. The average effects are also similar to the coefficients reported in PVK. PVK reported (

Replication of PVK Model on the Effect of Annualized Growth on New Ventures’ Exit and Failure.

Note. The dependent variable is venture exit in Models A and B (1 = exit, 0 = censored) and venture failure in Model C (1 = failure, 0 = censored). Venture failure is defined as firm “death” with all other exits (e.g., acquisitions, mergers, restructuring) treated as right-censored. Failure events account for 83% of exits. Annualized growth is measured as employment growth between t−2 and t−1.

Coefficients from Cox proportional hazards models are reported. Robust (Huber–White sandwich) standard errors clustered at the firm level are reported in parentheses.

ER = Economic Region; PVK = Pe’er, Vertinsky, & Keil.

Significance levels: **p < .05. ***p < .01.

Effect of annualized growth on new venture exit for manufacturing sample (a), and the multi-sector sample (b).

Exact Replication: Effect of Annualized Growth on Exit in Cross-Industry Sample

Next, we broadened our sample to include all other non-government industries. Both the linear and quadratic models B1 and B2 in Table 3 resulted in similar coefficients as in the manufacturing sample. As illustrated in Figure 2b, the annualized growth-exit relationship remains distinctly U-shaped even in the cross-industry sample. These findings indicate that moderate growth in the short term is most likely helping ventures to avoid exit.

Extension: Effect of Annualized Growth on Failure in Cross-Industry Sample

We began our extension analysis by using our refined measure of failure. The results are presented in Table 3, Models C1 and C2. While the coefficient of the linear term remains similar to that in model B, the quadratic term becomes smaller. This indicates that high growth exerts a weaker negative influence on the probability of survival under this specification. Figure 3 illustrates these effects. The downward slope at negative to low growth levels remains consistent with PVK, but the decline in survival probability at high growth rates appears more attenuated. These results indicate that while high annualized growth may be associated with high exit rates, it is less likely to lead to distress-driven exits.

Effect of annualized growth on new venture failure.

Extension: Effect of CAGR on Failure in Cross-Industry Sample

In Table 4, we present the results of our full extension analysis, which includes additional control variables, the refined measure of failure, as well as measuring growth as the CAGR up to each year of observation. As reported in model D2, the linear growth term is positively associated with failure

Extension analysis: CAGR and new venture failure.

Note. The dependent variable is venture failure (1 = failure, 0 = censored), defined as firm “death” with all other exits (e.g., acquisitions, mergers, restructuring) treated as right-censored. Growth is measured as the CAGR from founding to t−2 (robustness checks use growth measured up to t−1). We extend the replication model by controlling for firm age, initial venture size, and lagged profitability (all at t−1), and by interacting CAGR with age and profitability to allow growth effects to vary with lifecycle stage and financial performance. Coefficients from Cox proportional hazards models are reported. Robust (Huber–White sandwich) standard errors clustered at the firm level are reported in parentheses. Significance levels: *p < .10. **p < .05. ***p < .01.

CAGR=compound annual growth rate.

Effect of CAGR on new venture failure.

Extension: Functional Form Analysis Using a LASSO Cox Model

To assess whether the observed inverted-U relationship does not depend on the imposed quadratic specification, we conducted an additional functional-form analysis using a LASSO Cox model that allows the data to select the relevant polynomial terms of growth. Specifically, we estimated a model including polynomial terms of CAGR up to the fifth order together with all control variables, and selected the regularization parameter through cross-validation. The LASSO Cox model retained the linear growth term (β = .71) and a cubic term (β = −.04). We report the full estimation results in Appendix C and plot the growth–failure relationship obtained from a Cox model estimated using only the variables selected by the LASSO procedure in Figure 5. The resulting pattern closely mirrors the main specification and confirms that a quadratic approximation adequately captures the underlying relationship between growth and venture failure.

Effect of CAGR on new venture failure using variables selected by the LASSO Cox model.

Robustness Checks

To ensure the reliability of our findings, we conducted several robustness checks to address potential concerns about outliers, measurement window, exit heterogeneity, venture age, founding size, and model specification.

First, we examined whether our results were driven by extreme high-growth outliers. Figure D1 in Appendix D plots the empirical distribution of CAGR values across the sample. The inflection point at which growth begins to increase failure risk occurs near 100% annual growth. Ventures exceeding this rate represent 7,517 observations, or 3% of the sample, which is consistent with prior evidence on the rarity of persistent high-growth young firms or “gazelles” (Coad et al., 2018; Henrekson & Johansson, 2010). Following PVK, we retained these observations because recent research emphasizes that such exceptional cases are integral to understanding entrepreneurial dynamics rather than mere anomalies (Clark et al., 2023). They represent the extreme but aspirational outcomes of entrepreneurship, or the “exceptional of the exceptional” (Ruef & Birkhead, 2024), that can reveal mechanisms and boundary conditions often hidden in average cases (Ruef et al., 2023).

Second, we re-estimated all models using an alternative specification of growth that extends CAGR up to t−1 instead of t−2, to test whether ending the growth measure earlier biased the results. Because ventures that anticipate closure often downsize to contain costs, consistent with the “shadow of death” effect (Coad, 2018), we treated these cases in two ways. First, we censored exits preceded by annualized negative growth at t−1. Second, we calculated CAGR only up to t−2 rather than up to t−1 for such cases to exclude potential downsizing associated with imminent failure while preserving earlier growth dynamics. As reported in Appendix E, both approaches yield consistent inverted U-shaped relationships between lifetime growth and failure, and confirm that negative growth can serve as a deliberate retrenchment strategy that reduces likelihood of failure.

Third, we refined the definition of failure to isolate financially distressed exits. Restricting the outcome variable to failures preceded by negative profitability distinguishes economic failure from voluntary discontinuation. Prior studies show that distress-driven failures are often preceded by sustained losses or liquidity constraints, whereas voluntary exits may occur under stable financial conditions (Coad & Kato, 2021; Wennberg et al., 2010). As shown in Appendix F, this narrower definition produces results that are virtually identical to those in our main analysis. As such, this robustness check reinforces that the observed pattern is not likely an artifact of how failure is coded.

Fourth, to explore potential heterogeneity in the growth–survival relationship, we examined whether the effect of growth varies with venture age. High growth may be critical in early years for overcoming liabilities of newness but may generate coordination costs as firms mature (Brüderl & Schüssler, 1990; Hannan & Freeman, 1984). We therefore divided the sample by new venture age of three categories, 3 to 6 years, 7 to 9 years, and 10 to 13 years, and re-estimated our extension model within each group. Although uncertainty increases at very high growth levels, the inverted U-shaped pattern persists across all cohorts (see Appendix G). We also tested whether the relationship depends on venture size at founding. For very small ventures, particularly those with two to four employees, negative CAGR values typically indicate near-closure rather than strategic retrenchment. Larger ventures can substantially reduce employment while still reporting positive lifetime growth. To address this, we stratified the analysis by founding size, and distinguished between micro ventures with two to four employees, small ventures with five to nine employees, medium ventures with 10 to 19 employees, and large ventures with 20 or more employees (Mata & Portugal, 2002; Nason et al., 2015). We re-estimated the Cox models within each stratum and plotted the results in Appendix H1. We also unpacked the distribution of initial venture size in the sample in Appendix H2. Even though most ventures in our sample are micro, and larger sizes are progressively less represented, the inverted U-shaped relationship remains apparent across all size categories. Overall, these robustness checks indicate that our findings are not driven by mechanical features of the growth measure or size distribution.

Finally, we further assessed the proportional hazards assumption using Schoenfeld residual diagnostics. As we report in Appendix I, the tests indicate no systematic time dependence for the focal growth variables (CAGR and CAGR2) or their interactions with age. Additional robustness analyses reported in Appendix J confirm the consistency of these findings across alternative specifications.

Discussion

This study re-examines how venture growth affects survival by refining two central aspects of prior research in entrepreneurship: treating growth as a cumulative lifetime process and distinguishing genuine failure from strategic or neutral exits. Using a large longitudinal dataset of Dutch ventures, we show that ventures that grow very slowly or scale aggressively over their lifespan are more likely to survive than those that grow at moderate rates. While earlier studies argued that moderate growth balances opportunity and control (Coad et al., 2020; Pe’er et al., 2016; Penrose, 1959), our findings indicate that moderate growth appears to represent a comparatively fragile trajectory in the long run. Through this replication and extension, our study advances a more comprehensive understanding of how growth trajectories shape the long-term endurance of ventures.

First, our study offers important implications for research on new venture growth, survival, and organizational adaptation. We show that the relationship between growth and survival depends critically on the temporal horizon used to examine it. Grounded in theories emphasizing control, adjustment costs, and managerial constraints (Coad, 2007; Greiner, 1998; Kazanjian & Drazin, 1990; Penrose, 1959), earlier studies have typically modeled survival as a short-term response to growth fluctuations. Within this perspective, moderate growth appears optimal because it balances the immediate costs of expansion against short-term gains in scale and efficiency (de Kok et al., 2012; Pe’er et al., 2016). Our findings reveal that this balance shifts when growth is examined over a venture’s lifetime. Over longer horizons, the benefits of expansion compound as ventures build legitimacy, deepen resource bases, and develop adaptive capabilities (DeSantola & Gulati, 2017; Kor & Mahoney, 2005; Levie & Lichtenstein, 2010), while the marginal costs of growth may decline as ventures learn to manage complexity more effectively. Growth and survival are thus linked by cumulative processes that transform growth into endurance through gradual consolidation or rapid scaling (Bingham & Eisenhardt, 2011; Jansen & Tippmann, 2026; Ott & Eisenhardt, 2020; Shepherd et al., 2021). Our replication and extension help reconcile seemingly competing perspectives in the literature and call for more integrated and longitudinal frameworks that embrace both short-term and long-term perspectives when exploring and examining the consequences of entrepreneurial action and growth.

Second, we clarify one potential reason why prior studies report divergent shapes in the growth–survival relationship by emphasizing that much of this variation arises from how failure is defined and measured. The literature has produced mixed empirical patterns ranging from inverted U-shaped to L-shaped, linear, and null effects (de Kok et al., 2012; Gjerløv-Juel & Guenther, 2019; Pe’er et al., 2016; Zhou & Van der Zwan, 2019). A central reason for these inconsistencies may lie in the conflation of genuine organizational failure with other exit routes. Many studies are unable to empirically differentiate different types of exit even though such events often represent positive or neutral discontinuations rather than organizational demise (Coad & Kato, 2021; Wennberg et al., 2010). This distinction is not trivial since high-growth ventures are systematically more likely to experience these positive exits due to their attractiveness to investors, acquirers, and partners (Cotei & Farhat, 2018; Dobrev & Gotsopoulos, 2010). Treating such transitions as failures biases estimates against high-growth ventures and can create the false impression that moderation is the safest growth path. By adopting a stricter definition of failure that captures true organizational discontinuation, our study isolates the mechanisms that threaten survival and reveals that the empirical relationship between growth and failure is more consistent than previously assumed. By defining failure separately from positive or neutral exits, our study calls for refining the conceptual boundaries of venture growth–survival research and better aligning measurement with the mechanisms it seeks to explain.

Third, the results of our replication and extension together reveal an important paradox that entrepreneurs face when growing their venture: the very strategies that protect their ventures from failure in the short term undermine their endurance in the long term. Ventures generally face strong pressures to contain risks, control costs, and avoid overextension. Such caution helps prevent premature failure but often leads to incremental, loosely coordinated growth that lacks strategic direction (Cullen et al., 1986; Kim & Kim, 2022). However, our findings suggest that such a moderate growth trajectory traps ventures in suboptimal equilibria because they are large enough to face the coordination costs of expansion but too small to capture the reinforcing benefits of scaling. As such, ventures require entrepreneurial action to escape this trap. For instance, founders and managers may need to recognize when short-term prudence turns into long-term inertia and actively create the conditions that allow their venture to move beyond moderation. By fostering a shared ambition and strategic clarity, leaders can help their ventures avoid moderation and sustain endurance over time (Beckman et al., 2023). In this respect, future research could examine how leadership cognition, temporal framing, and strategic reorientation or pivoting enable ventures to escape moderate-growth traps and reorient toward more resilient strategies.

Fourth, our findings suggest that ventures’ long-term survival hinges on their ability to develop and sustain a temporally aligned growth trajectory. Endurance emerges not just from the rate of expansion but also from the capability to continuously synchronize growth decisions with evolving structures, resources, and strategic intent (Kor & Mahoney, 2005; Jansen et al., 2023; DeSantola & Gulati, 2017; Levie & Lichtenstein, 2010). Ventures that maintain such alignment, either through disciplined consolidation or rapid scaling, transform the inherent pressures of growth into organizational resilience and adaptive strength. In contrast, those trapped in incoherent or moderate growth patterns often lose strategic focus and accumulate structural strain over time. By linking coherence and temporal alignment to scaling outcomes, our study advances the literature on organizational growth and scaling (Ott & Eisenhardt, 2020; Tidhar et al., 2025; Varga et al., 2023). In particular, scaling is not simply a function of growth intensity, but of whether ventures sustain alignment between growth, structure, and strategic intent over time. Lifetime high growth can strengthen, rather than threaten, survival when it evolves into a recursive process of capability accumulation and renewal (Jansen & Tippmann, 2026). Sustained expansion allows ventures to build legitimacy, consolidate market positions, and embed adaptive learning routines that transform rapid growth into a durable scaling capability. Conversely, ventures that deliberately pursue a slow and stable growth path may also endure when they preserve focus, reliability, and efficiency through disciplined retrenchment and strategic consolidation. Future research could examine how ventures maintain alignment and coherence between their growth trajectories, evolving organizational configurations, and shifting strategic priorities over time. Studies may explore how ventures adaptively recalibrate growth decisions to preserve consistency between ambition and capacity, thereby transforming expansion into a sustained source of endurance. Further work could also investigate whether distinct configurations of growth trajectories, such as punctuated, episodic, or oscillating patterns, differentially influence survival outcomes. In this regard, examining how environmental conditions, including industry dynamics, technological change, and institutional contexts, shape the effectiveness of these trajectories represents a promising avenue for future research.

Limitations

While our study advances our understanding of the growth–survival relationship, it also has limitations that highlight several promising directions for future research. First, future studies could broaden the conceptualization of growth beyond employment to include dimensions such as sales, profitability, market share, or innovation outcomes. Examining how these forms of expansion jointly or differentially affect survival could provide a more comprehensive account of how ventures may survive. Second, our use of compounded annual growth rates provides a comparable indicator of firm expansion, yet it does not capture fluctuations or irregularities in growth trajectories. Future research could apply alternative modeling techniques to account for the nonlinear and episodic nature of entrepreneurial growth and assess whether ventures that experience volatile or punctuated growth patterns exhibit distinct survival dynamics compared with those that grow more uniformly.

Third, our data does not distinguish bankruptcies from voluntary closures. This matters because bankruptcies reflect acute financial distress, whereas closures may occur even when ventures remain solvent. Combining both may obscure differences in failure mechanisms. Future research could disentangle these outcomes to assess whether growth trajectories have distinct effects on bankruptcy versus closure. Fourth, the effects of employment growth may vary across industries. Although we control for two-digit industry codes, growth trajectories may operate differently across competitive contexts. For instance, rapid scaling may be critical in winner-take-all markets, while gradual growth may suffice in fragmented industries. Future work could examine whether the observed pattern depends on industry-specific dynamics.

Finally, our Dutch setting may limit generalizability. Labor market institutions in the Netherlands are characterized by relatively strict employment protection regulations, which may constrain firms’ ability to adjust employment and amplify the consequences of growth trajectories for survival outcomes (Bassanini & Venn, 2007). Although we use FTEs to capture employment dynamics, future research should examine whether the results hold in more flexible labor markets where firms can adjust employment more easily. In addition, economic geography differs substantially across contexts. The Netherlands features dense urban networks and strong agglomeration economies, whereas economic activity in larger countries (such in PVK’s Canadian sample) tends to be more spatially dispersed (van Oort & Bosma, 2013). These structural differences may influence how growth translates into survival. In dense regions, stronger competition and knowledge spillovers may amplify both the benefits and the risks associated with growth, enabling some ventures to learn faster and capture market opportunities while exposing others to greater competitive pressure from nearby rivals (Boschma, 2017; Stam & van de Ven, 2021). In more dispersed environments, weaker spillovers and lower competitive frictions may allow ventures to survive with steadier, incremental growth trajectories (Fritsch & Mueller, 2007). Future research could therefore examine how different geographic contexts moderate the relationship between venture lifetime growth and survival.

Conclusion

By moving beyond the notion of a single optimal growth rate toward a broader understanding of how different growth trajectories can support survival, our study reframes the growth–survival relationship as a dynamic, cumulative process rather than a static trade-off. In doing so, we encourage future research to examine how ventures navigate between focus and expansion, and how the timing, intensity, and persistence of growth interact to shape long-term resilience in complex and evolving environments.

Supplemental Material

sj-pdf-1-etp-10.1177_10422587261441597 – Supplemental material for Is the Venture Growth-Survival Relationship Inverted U-Shaped or Not? A Replication and Extension

Supplemental material, sj-pdf-1-etp-10.1177_10422587261441597 for Is the Venture Growth-Survival Relationship Inverted U-Shaped or Not? A Replication and Extension by Yassine Lamrani Abou Elassad, Giuseppe Criaco, Justin J.P. Jansen and Tom J.M. Mom in Entrepreneurship Theory and Practice

Footnotes

Acknowledgements

The authors would like to thank participants of seminars at the European Scaleup Institute, Harvard Business School, Luiss Business School, NOVA Business School and Vlerick Business School for their valuable feedback about earlier versions of this paper.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.