Abstract

This study develops a temporal socioemotional wealth (SEW) perspective to examine how family firms’ strategic decisions shift as intergenerational succession approaches. Integrating SEW perspective with temporal construal theory, we argue that perceived proximity to succession triggers a shift from aspiration-based to temporal-needs-based SEW, reducing the salience of long-term benefits such as innovation while increasing the appeal of short-term concrete actions such as asset investment. Using data on pre-succession Chinese family firms, we find that firms approaching succession reduce R&D investment while increasing asset investment over time. Successor preparation weakens, while sibling competition strengthens, these effects. Our findings highlight the importance of temporal distance to succession in shaping SEW priorities and offer new insights into heterogeneity among family firms.

Keywords

Introduction

The overlap of family and business in family firms means that family-centric priorities and business goals are intertwined, resulting in behaviors distinct from nonfamily firms (Debicki et al., 2016; Gomez-Mejia et al., 2011). These differences are often attributed to the preservation of socioemotional wealth (SEW), the noneconomic benefits families derive from the firm, such as family control and influence, identity, social status, emotional attachment, and dynastic continuity (Berrone et al., 2012; Miller & Le Breton-Miller, 2014). Strong loss aversion to SEW, combined with heterogeneous family goals, leads to variation in strategic behavior (Chrisman & Patel, 2012; Daspit et al., 2021; Fang et al., 2018; Li et al., 2022). While SEW research has identified what families value, including the structure and prioritization of SEW goals (Dou et al., 2020; Miller & Le Breton-Miller, 2021), less attention has been paid to when these values exert the greatest influence and how certain goals take precedence at specific points in time, highlighting the need to incorporate temporal dynamics (Ahlstrom et al., 2025; Kellermanns et al., 2012; Jiang et al., 2018; Kotlar & De Massis, 2013). Moreover, scholars have increasingly recognized that SEW is not static but requires ongoing replenishment (Chua et al., 2015; Le Breton-Miller et al., 2004), calling for incorporating temporality into family firm research (Sharma et al., 2014).

Recent work on family firm heterogeneity increasingly highlights the temporal nature of strategic decisions (Daspit et al., 2021). Chrisman and Patel (2012) suggested that variation in R&D investment arises from whether firms emphasize short-term SEW preservation or long-term legacy. De Massis et al. (2014) reported an S-curve in investment proactiveness as family firms age. Scholars examining heterogeneity in internationalization have called for greater attention to chrono-contextual factors (De Massis et al., 2018), such as the family’s life course (e.g., succession, family stage) and the firm’s business stage. Drawing on construal level theory, Tumasjan et al. (2013) examined how perceived temporal distance to a business opportunity influences entrepreneurial evaluation of the opportunity. Despite these insights, temporality is largely treated implicitly. For example, research on family succession frequently treats succession as a singular event, focusing on its antecedents and consequences (Dorsch et al., 2023; Hauck & Prugl, 2015; Waldkirch et al., 2025), rather than looking into the temporal process leading up to it. As a result, this approach may overlook important dynamics in the pre-succession period (Zhu & Kang, 2022).

In this study, we use intrafamily succession as a context to examine how temporality influences strategic decision-making in family firms. We focus specifically on the pre-succession phase, as it provides a clearer view of temporal effects for two reasons. First, succession represents a major temporal milestone that reshapes family and business priorities, particularly intensifying SEW-related needs in decision-making (De Massis et al., 2016; Hauck & Prugl, 2015; Zellweger et al., 2012). As incumbents approach exit, the decision-making horizon compresses and family-centered considerations, such as maintaining family control and addressing emotional needs, become more salient (Sharma et al., 2003; Daspit et al., 2016). For example, Kotlar and De Massis (2013) showed that as intrafamily succession approaches, goal diversity intensifies, prompting organizational members to navigate goal setting processes toward collective commitment to family-centered goals. Second, family behavior during imminent succession tends to be shaped by dominant temporal SEW needs aimed at ensuring a smooth transition (Hauck & Prugl, 2015; Waldkirch et al., 2025; Zhao et al., 2020), with comparably less influence from external market conditions.

Drawing on temporal construal theory (TCT), we develop a temporal SEW perspective to explain how temporal proximity to succession shapes two strategic behaviors: R&D investment and asset investment. TCT posits that distant events are construed abstractly and outcome-focused, while near-term events are viewed concretely and feasibility-focused (Liberman & Trope, 1998; Trope & Liberman, 2003). Integrating TCT with the SEW perspective, we distinguish between temporal-needs-based SEW and aspiration-based SEW. As succession approaches (a near, concrete event), family firms shift attention distant aspirations to short-term feasibility and security. They may increase asset investment, or even engage in aggressive empire-building, to signal strength and wealth, instilling confidence among stakeholders and facilitating a smoother leadership transition. R&D investment, being more abstract and long-term oriented, tends to decline as succession approaches.

By theorizing temporality in this way, we make three main contributions. First, we respond to recent calls to integrate time and process into family business theory by developing a temporal SEW perspective. This adds a temporal dimension to the SEW paradigm (Chua et al., 2025; Daspit et al., 2021; Kellermanns et al., 2012), extending it to account for how SEW priorities evolve over time, especially around sensitive periods. Second, we enrich the succession literature by highlighting the distinctive patterns of investment behaviors as family firms approach succession, calling for greater attention to resource allocation decisions. Third, we show how internal family dynamics, such as successor preparation and sibling rivalry, moderate firms’ responses to temporal-needs-based SEW, contributing to research on heterogeneity among family firms (Chrisman & Patel, 2012; Daspit et al., 2021).

A Temporal SEW Perspective

Temporal Construal Theory

TCT is a foundational psychological framework that explains how psychological distance, particularly temporal distance, shapes individuals’ mental representations of events and decisions (Liberman & Trope, 1998; Trope & Liberman, 2003, 2010). According to TCT, individuals construe distant-future events at a high level, abstractly, focusing on central, goal-relevant features that emphasize the “why” and big-picture outcomes. In contrast, near-future events are represented at a low level, highlighting concrete, detailed, and context-specific attributes that pertain to the “how” and immediate details (Trope & Liberman, 2003, 2010). This distinction has implications for decision-making processes. Desirability-related considerations, aligned with high-level construals, are more salient when evaluating distant outcomes, whereas feasibility-related aspects, associated with low-level construals, dominate evaluations of imminent actions (Liberman & Trope, 1998; Tumasjan et al., 2013). These dynamics illuminate how changing temporal distance shapes managerial cognition and provide a theoretical foundation for examining decision-making in time-sensitive organizational contexts, such as intrafamily succession in family firms.

In the entrepreneurship field, TCT has been adopted to explain how entrepreneurial judgments are shaped by perceived time horizons (Hallam et al., 2016). For instance, Tumasjan et al. (2013) showed that temporal distance moderates the influence of desirability and feasibility in opportunity evaluation. Drawing on a similar construal mechanism, Chen et al. (2018) linked four types of psychological distance, including temporal, spatial, social, and hypotheticality, to the abstractness of entrepreneurial action. Along this line of inquiry, Chen and Nadkarni (2017) showed that CEO temporal dispositions, such as time urgency or future orientation, significantly influence corporate entrepreneurship. Long-term leadership horizons tend to encourage exploratory creativity, whereas extreme urgency can narrow focus and yield short-termism. Highlighting the subjective nature of time at construal level, Branzei and Fathallah (2023) argued that entrepreneurial resilience involves active recalibration of both objective time (e.g., adjusting timelines) and subjective temporal experience (e.g., shifting one’s perception of urgency or future possibility).

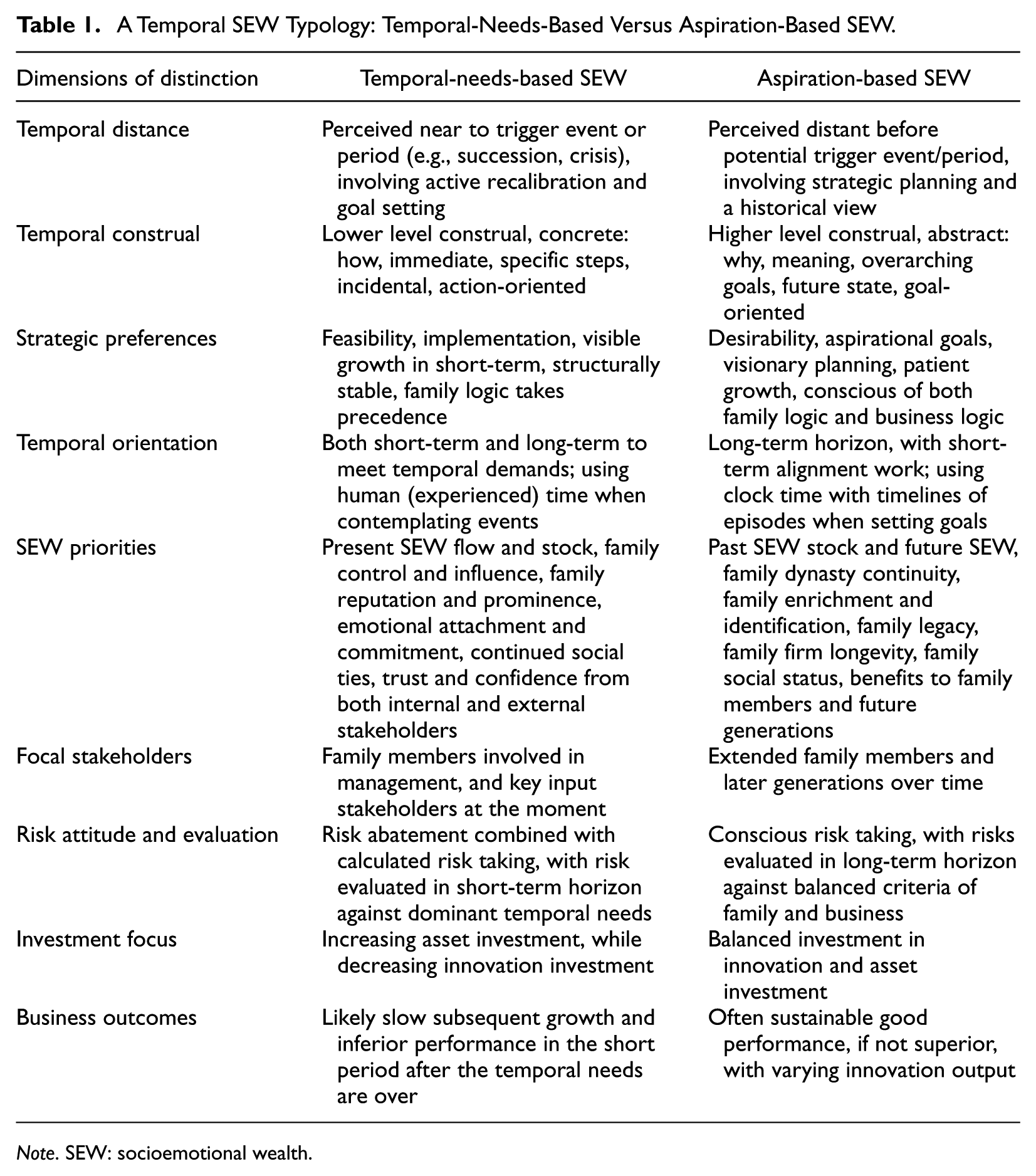

A Temporal SEW Typology: Temporal-Needs-Based SEW Versus Aspiration-Based SEW

Scholars have long recognized that SEW priorities not only vary among firms and even family members (Kotlar & De Massis, 2013) but also shift across different stages of the family firm life cycle (Miller & Le Breton-Miller, 2014). Approaching SEW explicitly from a temporal perspective, we propose a temporal SEW typology that draws on TCT principles while integrating insights from prior research that disentangles SEW dimensions. Specifically, we propose that SEW composes two dimensions: temporal-needs-based SEW and aspiration-based SEW. This distinction builds on the premise that SEW priorities may be temporarily shaped by key events such as succession. As perceived temporal distance to a focal event time decreases, long-term SEW benefits become less salient, while immediate temporal needs become more pressing (Hallam et al., 2016; Trope & Liberman, 2003), triggering concrete actions aimed at fulfilling temporal-needs-based SEW.

An early effort to deconstruct SEW by Miller and Le Breton-Miller (2014) distinguishes between restricted and extended SEW based on the scope of stakeholders targeted for benefit (the immediate family versus broader constituencies). Similarly, Gu et al. (2019) distinguished between focused SEW and broad SEW in examining family business groups’ entry into new industry. The focused SEW is primarily driven by family control and influence, mainly benefiting current generation, while the broad SEW emphasizes perpetuation of family dynasty, benefiting both current and future generations. Adopting a more technical approach, Debicki et al. (2016) identified three dimensions, including family prominence, family continuity, and family enrichment, based on the convergence structure of SEW measurement items. In addition, scholars have highlighted goal diversity, goal hierarchy (e.g., family control before considering succession), and sequential logic (e.g., profitability goals before control goals) related to SEW (Dou et al., 2020; Kotlar & De Massis, 2013).

While drawing on prior work, the temporal SEW framework that we develop is distinct in its focus on temporal demands, departing from existing approaches anchored in considerations such as the range of benefiting stakeholders, intergenerational focus, or dominant time horizon. None of these criteria is sufficient to distinguish the temporal-needs-based SEW from the aspiration-based SEW, as shown in Table 1. Moreover, the temporal SEW framework uniquely grounds the prioritization of SEW goals in cognitive shifts associated with changing temporal distance. TCT provides foundational cognitive mechanism that directs the direction of priority (e.g., concrete, feasible, visible), while SEW offers specific goals and options that family firms select and prioritize. This synergy makes the two theories inseparable within the framework; one provides the “how” of cognitive processing, while the other provides the “what” of familial motivation.

A Temporal SEW Typology: Temporal-Needs-Based Versus Aspiration-Based SEW.

Note. SEW: socioemotional wealth.

The temporal-needs-based SEW focuses on resource allocation to meet dominant temporal demands. As temporal proximity increases and pressure intensifies, the dominant coalition in family firms prioritizes SEW preservation and inflow to address immediate needs, such as ensuring a smooth and timely succession. Construal during this period operates at a relatively low level, emphasizing concrete actions and feasibility considerations (Trope & Liberman, 2010), and favoring visible, tangible outcomes that can be achieved quickly to minimize the risk of SEW loss. Several SEW dimensions, such as family control, social ties, and family reputation, are classified under this category due to their salience during critical events and their capacity to enable immediate action, particularly for risk prevention. The employed time horizons may vary across investment decisions. Major investments, such as acquisitions or entry into related industries, may not yield long-term benefits but may still be pursued if they serve temporal needs (e.g., signaling financial strength and future prospects). For example, Dou et al. (2020) showed that family firms with strong transgenerational intention are more likely to invest in diversifications, despite its risk and uncertain returns. Under temporal-needs-based SEW, focal stakeholders extend beyond the immediate family to include key input stakeholders (e.g., creditors and suppliers) to reduce the risk of SEW loss and facilitate navigation through demanding periods, while the underlying logic remains family-centered.

In contrast, the aspiration-based SEW is less responsive and instead reflects enduring aspirations to preserve family legacy and perpetuate the family dynasty, making it a defining characteristic of family firms. In the absence of temporally dominant demands, these SEW goals prioritize family enrichment through maintaining a well-performing and well-respected family business. In this context, cognitive construals of firm activities and planning are more abstract and higher-level, focusing on long-term visions and desirable end states grounded in past and current conditions. The meaning attached to goal pursuit, along with future-oriented goals themselves, is more important than immediate, incremental actions. Despite ongoing adjustments and responses to both internal and external dynamics, such as increases in suppliers’ bargaining power (Kotlar et al., 2014), the overall time horizon remains long term, with an emphasis on chronological aspects of time such as planning timing, pace and the sequencing of goal attainment (Aguinis & Bakker, 2021). Firms are more willing to take risk, evaluated against a long-term time window, seeking a balance between family logic and business logic. They consciously accumulate and invest resources for survival and persistence in the long run (Chua et al., 2025). Similarly, the focal stakeholders extend beyond the immediate family, but they cover a much bigger range than when firms are driven by the temporal-needs-based SEW, now including future generations and larger community.

In the following section, we apply this temporal SEW framework to theorize on how temporal distance to intrafamily succession, a particular temporal need, influences family firm strategic preferences with respect to R&D and asset investment. This demonstrates how research questions previously inaccessible without a temporal lens can now be examined using a temporal SEW perspective. For the purpose of this study, we define temporal distance to succession as the time gap between the present year, when the successor has already assumed a management role in the firm, and the year in which the succession is anticipated to occur.

Hypothesis Development

Intrafamily succession has increasingly been understood as a temporal process rather than a single leadership transition event (Daspit et al., 2016; Sharma et al., 2014). It typically unfolds across several stages: pre-succession planning (or establishing ground rules), successor nurturing and development, joint management, transition and power transfer, and post-succession integration (Daspit et al., 2016; Hauck & Prugl, 2015). Each stage is influenced by the interplay of individual, family, and firm-level factors, as well as broader contextual conditions (Hauck & Prugl, 2015; Kotlar & De Massis, 2013). Prior research has shown that key processes, such as successor early socialization and training (Cabrera-Suarez, 2005) and intergenerational solidarity (Gimenez-Jimenez et al., 2021), unfold over time. However, despite recognizing intrafamily succession as a temporal process, existing research rarely treat time as a central concept in theorizing. Studies linking transgenerational succession to innovation, for example, often invoke cognitive mechanisms such as time horizon and risk preference without explicitly modeling temporal cognition. As a result, failing to incorporate temporality and evolving priorities limits our ability to demonstrate theorized effects and capture their temporal dynamics.

In this study, we theorize the impact of temporal distance to succession on strategic behavior by examining two types of investment activities prior to intrafamily succession, R&D investment and asset investment. Such a contrast approach in theorizing can be very useful in comparing strategic choices. For instance, Fang et al. (2021) pulled together internationalization and R&D investment to investigate whether family business owners apply narrow-framing or group them together in deciding on the two types of investments that share similar risk profile but differ enough to be isolated in minds. We choose R&D investment because R&D is vital for long-term survival and has been a central topic in family business research, including family succession literature, yet scholars have noted the lack of a temporal perspective on how family firms invest in innovation over time (Calabro et al., 2019; Sharma et al., 2014). Meanwhile, R&D investment offers strategic flexibility and future growth options but entails highly uncertain outcomes. As such, it is highly sensitive to a family’s transgenerational vision and willingness to bear uncertainty for long-term payoffs that may materialize beyond the current leadership.

We select asset investment (e.g., non-R&D capital expenditures and acquisitions) as a contrasting strategic choice because it reflects the unique focus of the temporal-needs-based SEW (see Table 1). While there is extensive literature on R&D investment in family firms, far less is known about asset investment, particularly in the context of succession. We argue that strategic resource allocation decisions, such as R&D and asset investment (e.g., capacity expansion), are especially relevant during succession, as the need for family control and influence intensifies and is directly reflected in investment choices. Furthermore, asset investment emphasizes strategic commitment and operational capacity, generating tangible (and some intangible) assets that enable firms to execute its current strategy at scale. As such, it signals commitment to and confidence in the current strategic trajectory, an important message to stakeholders during succession. In weak institutional environments, such as parts of Southeast Asia, family firms often pursue rapid asset expansion to signal financial strength during challenging periods or preempt doubts about their future prospects. Notably, both Shanxi Highsee Iron & Steel Group and Evergrande Group, two highly prominent Chinese family business groups, pursued aggressive asset investment strategies prior to sudden bankruptcy.

After theorizing the main relationships, we will also propose how two of chrono-context factors closely associated with succession, successor preparation and successor sibling competition, moderate the impact of temporal distance to succession on R&D investment and asset investment. Successor preparation refers to the extent to which the successor is groomed, educated, and experienced in the business before taking charge, thus representing a critical phase of intrafamily succession process (Daspit et al., 2016; Le Breton-Miller et al., 2004). Sibling competition, which denotes rivalry among potential family successors, is also important to understand the investment decisions as the siblings are often involved in decisions to some extent. Prior studies already show that sibling competition impacts SEW perceptions and adds costs to succession (Atılgan & Kellermanns, 2025; Jayantilal et al., 2016; Xu, Song, et al., 2024).

There are important theoretical reasons to examine these two moderating effects. From a temporal perspective, successor preparation can extend the family’s temporal horizon by stabilizing expectations about intergenerational continuity and clarifying the future custodianship of family identity and control (Erdogan et al., 2020; Le Breton-Miller et al., 2004). In other words, successor training and co-management with the incumbent are likely to reshape perceptions of temporal distance to succession, thereby influencing the family firms’ investment decisions. In contrast, sibling competition operates as a temporal compression mechanism that shortens the family’s effective time horizon 1 . Specifically, sibling status conflicts and the associated political dynamics among family members prior to succession add temporal urgency into succession process (Atılgan & Kellermanns, 2025; Zhu & Kang, 2022), potentially altering the temporal pattern of resource allocation, including R&D and asset investment.

Temporal Distance to Succession and R&D Investment

Prior studies report mixed results regarding the influence of intrafamily succession on R&D investment (Baltazar et al., 2023). Research focusing on transgenerational intent or the initiation of succession tends to find positive effects (e.g., Dorsch et al., 2023; Zhu & Kang, 2022), consistent with the long-term orientation commonly attributed to family firms. In contrast, studies examining the post-succession period often report declines in R&D investment during or following succession (e.g., Li et al., 2022; Yang et al., 2022), often linking such effects to managerial myopia, risk aversion and short-term focus on SEW preservation. These inconsistencies likely stem from a lack of temporal clarity in distinguishing phases of the succession process. For example, does the effect arise before, during, or after succession? Is it driven by transgenerational intent, the successor preparation process, or the succession event itself? In this study, we focus on the pre-succession period, defined as the stage when the successor has already entered the management team.

We propose that R&D investment declines as the succession approaches for two main reasons. First, drawing on the temporal SEW framework, when succession is temporally distant and construed as an abstract and long-term aspiration, owners focus on long-term desirability, such as building innovation capacity and future family benefits. These investments align with high-level goals like transgenerational dynasty and technological leadership (Chrisman & Patel, 2012; Lumpkin & Brigham, 2011). As succession nears, mental construal becomes increasingly concrete and immediate, shifting priorities toward temporal-needs-based SEW, such as preserving current wealth, maintaining control, and ensuring a smooth transition. This shift in SEW leads family firms to deprioritize R&D, which is slow to yield visible outcomes and offers limited contributions to immediate SEW needs, such as strengthening social ties or enhancing family reputation, factors that matter to key input stakeholders and make succession more attractive to successors (Sharma et al., 2003; Venter et al., 2005). R&D thus diverts resources from initiatives that offer quicker, more tangible support for succession, such as visible assets building. Consequently, as temporal distance to succession decreases, therefore, firms reduce R&D intensity.

Second, as the succession timeline shortens during this sensitive period, maintaining prior levels of R&D investment may undermine the current stock and flow of SEW. Arrangements such as external financing or hiring external experts for R&D are now perceived as threats to current SEW (Kotlar et al., 2014). At the same time, incumbents’ shortening personal time horizons increase sensitivity to legacy protection, making succession less likely to be viewed as an opportunity for innovation (Hauck & Prugl, 2015). The desire to avoid uncertainty or negative signals intensifies, and explorative R&D during this period may raise concerns among key stakeholders (e.g., suppliers and creditors). Imminent succession further amplifies the perceived risks of R&D. DesJardine and Bansal (2019) showed that negative external evaluations shorten decision-making horizons and narrow the search for solutions, reinforcing a focus on short-term outcomes to preserve external confidence. Consequently, strong social ties, though beneficial for succession, become constraints on innovation. Meanwhile, successors tend to act cautiously prior to succession to avoid conflict with incumbents and to demonstrate competence to stakeholders. Consistent with this, scholars find that even after succession, new family CEOs reduce R&D spending under close scrutiny from outgoing leaders and external stakeholders (Li et al., 2022; Yang et al., 2022).

Temporal Distance to Succession and Asset Investment

Asset investments represent cash-intensive strategic initiatives that expand a firm’s asset base, including acquisitions, joint ventures, new headquarters, capacity expansion, and entry into new markets or regions. From a temporal SEW perspective, their appeal increases as family firms approach intrafamily succession. When succession is relatively distant, incumbents have the temporal latitude to pursue patient growth strategies aligned with aspiration-based SEW, such as building family legacy and ensuring long-term prosperity (Chrisman & Patel, 2012; Lumpkin & Brigham, 2011). As succession becomes imminent, abstract, future-oriented aspirations give way to more immediate and concrete objectives, such as transferring a financially robust and visibly successful firm under continued family control. Temporal proximity also makes the action-outcome pathways clearer (Wood et al., 2021), prompting attention shift toward implementation and “how” considerations (Chen et al., 2018; Trope & Liberman, 2010; Tumasjan et al., 2013). Consequently, asset investments become more attractive due to their near-term, observable outcomes, including increased sales, the pride of overseeing a larger business empire, greater assets under control, visibly expanded operations, or symbolic achievements tied to family reputation. These outcomes align closely with temporal-needs-based SEW goals by preserving family control and influence, reinforcing family prominence, and signaling strength to key stakeholders, thereby facilitating a smoother leadership transition (Kotlar & De Massis, 2013).

As succession nears, the incumbent’s diminishing time horizon may further encourage accelerated asset investment. Outgoing leaders may engage in empire building to “go out on a high note,” rapidly expanding the firm’s footprint to cement their legacy (Venter et al., 2005). Controlling families may also reinvest substantial earnings into capital expenditures, such as expansions and acquisitions, that enhance family prestige and entrench control, even when such investments offer limited prospects for profitability or sustained advantage (Kellermanns et al., 2012). Family firms may also undertake symbolic asset investments to signal endorsement of the successor. Because relational capital tied to incumbents is not fully transferable (Fan et al., 2012), outgoing leaders may mobilize family assets and social networks to help successors overcome potential obstacles (Bennedsen et al., 2015). At the same time, asset investments provide valuable opportunities for successors to build legitimacy, authority, and experience within core operations (Sardeshmukh & Corbett, 2011). Together, these responses to temporally dominant SEW needs reflect family-centric behavior and can lead to extreme resource allocation patterns (Miller & Le Breton-Miller, 2021). Although asset investments involve uncertainty, their risks are often perceived as more manageable than those of exploratory activities such as R&D, as they typically leverage existing strengths and remain closely tied to the core business.

The Moderating Role of Successor Preparation

We argue that a high level of successor preparation weakens the effect of temporal distance to succession on strategic decisions, making both R&D cuts and asset growth less pronounced as family firms approach succession. First, multi-year successor preparation serves as a psychological and organizational buffer that attenuates temporal needs, which would otherwise shift SEW priorities toward rapid action. As successors accumulate managerial experience across functions and levels, this process signals family commitment and incumbent support while reinforcing expectations of a well-paced transition (Umans et al., 2021). Such preparation enhances successor legitimacy internally and externally, reducing the need for asset investments as symbolic support or credibility signaling. It also reframes the succession timeline construal from a looming threat requiring urgent responses to a manageable process in which family identity and control remain intact. In this sense, perceived temporal distance remains relatively high even as chronological distance shortens, due to early successor involvement and sustained interaction with incumbents over time. As a result, successor preparation tempers the urgency that drives increased asset investment and reduced innovation as succession approaches. For example, Li et al. (2022) showed that longer successor tenure reduces susceptibility to myopic loss aversion, making new leaders less likely to cut R&D.

Second, the deliberate planning embedded in successor preparation can attenuate extreme shifts in investment behavior as succession approaches. Through mentoring, role modeling, and incremental responsibility, successors accumulate firm-specific knowledge and develop judgment aligned with family priorities. These structured engagements build stakeholder credibility for successors (Cabrera-Suarez, 2005; Gagne et al., 2021) and foster shared mental models that support continuity in strategic vision (Zhu & Kang, 2022), which reduce tendencies toward division-centric expansion or opportunistic asset overinvestment. Repeated exposure to decision-making and interactions with incumbents also facilitates the transfer of tacit knowledge (Fang et al., 2025). This process of “family imprinting” (Erdogan et al., 2020) strengthens emotional commitment and helps successors manage the innovation–tradition paradox, encouraging continuity rather than deviation from the firm’s strategic trajectory. Zhao et al. (2020) found that firms are more likely to sustain strategic investment momentum during transition when successors are appointed after internal grooming.

The Moderating Role of Successor Sibling Competition

We argue that sibling competition strengthens the effect of temporal distance to succession on both R&D and asset investment decisions in family firms. As succession nears, firms tend to deprioritize R&D investment due to compressed time horizons and heightened risk. When multiple siblings are involved in management, this temporal urgency is further intensified. Sibling rivalry often manifests as struggles for influence and recognition, particularly under opaque or contested succession (Avloniti et al., 2014), and exacerbates intrafamily conflict and strategic divergence (Lee et al., 2023; Xu, Chan, et al., 2024). In such contexts, siblings may withhold cooperation or pursue individual agendas, making consensus on long-term investments such as R&D more difficult (Alderson, 2015; De Massis et al., 2008). R&D allocations may become politicized, as family members avoid backing initiatives that could advantage one sibling over others (Zhu & Kang, 2022). Sibling competition also weakens the temporal salience of SEW, reinforcing short-termism and defensive behavior (Atılgan & Kellermanns, 2025). Consequently, resources are redirected toward more immediate and visible returns, amplifying the negative effect of temporal proximity on R&D investment. The threat of internal competition thus intensifies myopic loss aversion (Chrisman & Patel, 2012), leading to steeper declines in R&D investment as succession approaches.

In contrast, asset investments, such as expansion into adjacent businesses, infrastructure, or international markets, become more prominent when sibling competition is intense and succession is imminent. With multiple heirs, both incumbents and successors may engage in strategic asset accumulation to influence succession outcomes or strengthen future bargaining positions (Fang et al., 2018). Investments in tangible assets (e.g., acquisitions, physical expansion, or new ventures) serve as visible signals of capability and commitment to the family legacy, which are particularly salient in competitive intrafamily environments (Avloniti et al., 2014). Siblings may also demand differentiated roles or resources to assert their positions, creating pressure for resource partitioning or individualized projects (Alderson, 2015). This dynamic shifts capital allocation away from unified long-term strategy toward accommodating multiple internal stakeholders (Atılgan & Kellermanns, 2025). To mitigate conflict, families may pursue diversification or allocate new ventures across heirs (Blanzo-Mazagatos et al., 2024; Gu et al., 2019), or structure expansions that distribute influence without ceding full control over core assets (De Massis et al., 2008). By reinforcing the urgency to demonstrate performance and secure future influence, sibling competition thus amplifies the positive relationship between temporal proximity to succession and asset investment.

Methods

Data and Sample

We compiled a sample of Chinese family firms listed in Shanghai and Shenzhen Stock Markets from 2007 to 2019 from the China Stock Market Accounting Research (CSMAR) database and Chinese Research Data Services (CNRDS) database. The CSMAR database provides comprehensive information on family firms, such as firm characteristics (e.g., founding date, ownership structure) and financial data (e.g., R&D spending, total sales). Importantly, it also identifies family relationships among shareholders, directors, and executives. These relationships are established through systematic cross-verification of publicly disclosed sources, including annual reports, IPO prospectuses, and equity change reports, where companies must disclose kinship ties (e.g., spouse, parent, child, sibling) among board members and major shareholders. CSMAR constructs predefined variables that indicate these familial links using a combination of manual verification and automated name-matching procedures based on official disclosures and company filings. The CNRDS database provides detailed information on successors’ official positions within the firm, including what leadership roles they have taken and when, as well as when a succession takes place. We choose 2007 as the starting year because few family firms experienced generational succession before then, and the adoption of new financial reporting standards in 2007 reduced the comparability of financial data across periods. We chose 2019 as the ending year because firm investment strategy may have been seriously interrupted by the COVID-19 pandemic, which began in January 2020 and lasted for over 3 years.

China offers a particularly suitable context for testing our theory for two main reasons. First, compared with family firms in Western countries, Chinese family firms tend to exhibit a centralized governance model, with major decisions controlled by the founding family, particularly the founder (Zhu & Kang, 2022). Such governance structure makes family factors, transgenerational succession in this case, more salient, introducing less interference of outside shareholders. Second, shaped by Confucian traditions and deep-rooted family values, Chinese family firms view intergenerational succession as both an economic necessity and a symbolic legacy (Chen et al., 2021; Li et al., 2022). These firms treat successor preparation seriously and may even engage in certain investments such as internationalization for the purpose of successor development (Shi et al., 2019). Because of sensitivity of intrafamily succession to business partners and external stakeholders (Bennedsen et al., 2015; Xu et al., 2015), timing of succession is important to Chinese family firms.

Following Xu et al. (2011), we define family firm as one in which a family owns at least 10% of the shares and at least one family member (a person related by blood or by marriage to the owning family) serves in the top management team. The 10% ownership threshold also confers substantial shareholder rights in Chinese corporate governance. During the sampling process, we excluded firms without a clearly identified succession year or with missing information on successor positions, as these cases prevent us from measuring the temporal distance to succession and successor preparation with these firms. Firms with succession events occurring before 2009 were also excluded because our analysis focuses on the pre-succession preparation phase and requires at least 2 years of data prior to the succession year for valid analysis. It is important to note that the analytical sample consists exclusively of firm-year observations prior to, and including, the year of intrafamily succession. We do not include any post-succession observations, as this study focuses on firms’ strategic and organizational behaviors during the pre-succession period. After removing further observations with missing values, our final sample consists of 774 firm-year observations. This sample covers 111 transgenerational leadership transitions, of which 84 cases were from father to son, 20 were from father to daughter, 3 was from mother to son, 1 was from mother-in-law to son-in-law, and 3 were from uncle to nephew. All transitions are first-to-second generation successions.

Measures

Dependent Variable: R&D Investment and Asset Investment

R&D investment was measured as the ratio of R&D expenditure to total sales, consistent with prior studies on R&D investment (Chrisman & Patel, 2012; Li et al., 2022). Following Williams and Lee (2009), we measured asset investment as the sum of investment-related expenditures reported in the cash flow statement, divided by total sales. Investment-related expenditures include cash payments for the construction of fixed assets, intangible assets, and other long-term assets, as well as net cash payments for acquiring subsidiaries and other business units. To ensure our measure captures only non-R&D investment, we excluded capitalized R&D expenditures in the calculation of the asset investment measure. To mitigate concerns of reverse causality and account for the time-lagged effect of the investment decisions, we used R&D investment and asset investment measures in year t+1 in regression tests.

Independent Variable: Temporal Distance to Succession

We measured temporal distance to succession as the number of years between the observation year and the year of the transgenerational succession event, defined as the year in which the founding generation officially steps down while the next-generation successor takes over the position of either board chair or CEO, consistent with prior studies on intrafamily succession (Li et al., 2022). The succession year is identified from the “Successor Information” dataset of the China Family Firms Research Database within the CNRDS database. Temporal distance to succession ranges from −14 to 0 in our sample. A value of 0 indicates the year of succession, while negative values (e.g., −1, −2, …, −14) indicate the years before the succession. As such, the higher the absolute value of this measure, the further away the firm is from the succession year. For example, in Hengtong Optic-Electric Co., Ltd., the second-generation successor, Cui Wei, officially took over as board chair in 2021. When observing Hengtong in 2018, the temporal distance to succession would be −3. The observation year in 2007 would generate a temporal distance of −14.

Moderating Variables: Successor Preparation and Sibling Competition

We took two steps to obtain the measure of successor preparation. First, we calculated the cumulative number of positions each year held by successors before they took over the business. The greater the total number of positions held prior to succession, the better prepared the successors are in obtaining important knowledge and skills for a successful succession. Second, to reduce the skewness of the distribution and facilitate interpretation, we took the natural logarithm of this cumulative count plus one. This continuous measure of successor preparation was used in both main and moderation analyses. In our sample, the number of positions held by successors before succession ranges from 0 to 11, indicating variation in the extent of successor preparation across firms.

Sibling competition was measured as the number of the actual controller’s children involved in the firm in a given year. For firms with multiple actual controllers, we identify the one with the highest generational rank and count the number of their children participating in the firm. In our sample, 28.55% of actual controllers have no children in the firm, while the majority (70%) have 1 to 3 children.

Controls Variables

To mitigate potential bias from omitted variables, we include a set of control variables at three levels: firm, individual, and macro environment. Firm level controls include age, size, organizational slack, founding type, CEO duality, family ownership, sales growth, and strategic change. Age was measured as the natural logarithm of the number of years the firm has been operating. The age of firms in our sample ranges from 6 to 34 years, with an average of 15 years. Size was captured by the natural log of total sales, a common indicator of firm strategic capacity (Fang et al., 2025). We included organizational slack, measured as the ratio of current assets to current liabilities (Li et al., 2022) because available slack is key to investment activities. Founding type equals 1 if the firm was directly found; and 2, if the firm was found as a result of equity transfer, restructuring, etc. CEO duality was measured as a dummy variable, where it equals 1 if the CEO also serves as the chair of the board, and 0 otherwise (Chen & Hsu, 2009). Family ownership was measured as the number of shares held by family group divided by the total shares outstanding (Chen & Hsu, 2009). We also controlled for family involvement, measured as the percentage of top executives who are family members (Oh et al., 2019). Sales growth was calculated as the difference in sales between year t and year t−1 divided by sales in year t−1 (Chen & Hsu, 2009).

To account for major shifts in firm strategy unrelated to succession, we included a measure of strategic change. Following prior studies (Datta et al., 2003), we calculated the 5-year variance (from t−1 to t+3) of six key financial indicators related to resource allocation and cost structure, including the ratio of advertising expenses to revenue, the ratio of R&D expenditures to revenue, the ratio of net fixed assets to gross fixed assets, the ratio of non-production expenditure to revenue, the ratio of inventory to revenue, and the financial leverage ratio. These variance values are then aggregated to construct the strategic change index for each firm-year, with higher values indicating a greater degree of strategic transformation.

At the individual level, we included founder age, founder education, successor age, and successor education. Both founder age and successor age were measured as the natural logarithm of their actual age plus one. Both founder education and successor education were measured as a 7-point scale capturing the highest level of education obtained (1 = technical secondary school or below, 2 = junior college, 3 = bachelor’s degree, 4 = master’s degree, 5 = doctoral degree, 6 = other types of education [e.g., honorary doctorates, correspondence courses], and 7 = MBA/EMBA) (Oh et al., 2019).

We also controlled two macro conditions, including market competition and regional development because these environmental factors may drive investment activities. Market Competition was measured as 1 minus the Herfindahl–Hirschman index, reflecting the competitive intensity in the firm’s industry (Li et al., 2017). Regional development was measured as the GDP per capita of the region where the firm is located, capturing the local economy context (Jiang et al., 2020). Moreover, firm and year fixed effects, as well as prior-year investment in R&D and asset were included to control for unobserved heterogeneity across firms and over time.

Results

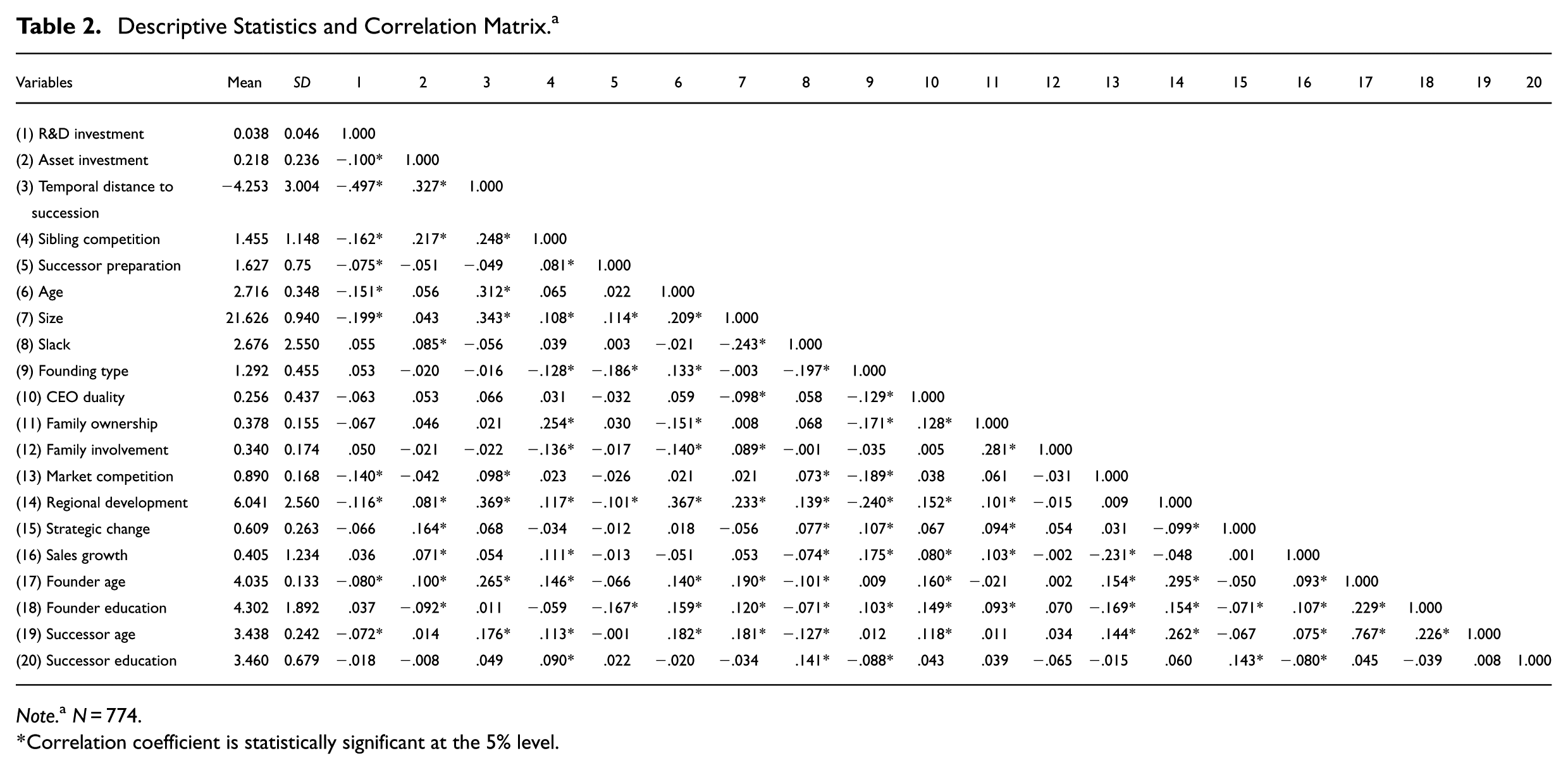

Table 2 reports the descriptive statistics and correlation matrix for all the variables included in the models. Temporal distance to succession is negatively correlated with R&D investment (r = −.497*, p < .05) but positively correlated with asset investment (r = .327*, p < .05). Sibling competition is negatively correlated with R&D investment (r = −.162*, p > .05), but positively correlated with asset investment (r = .217*, p < .05). Successor preparation is negatively correlated with R&D investment (r = −.075*, p < .05). The correlation between R&D investment and asset investment is negative and significant (r = −.100*, p < .05), suggesting opposite direction in resource allocation. The variance inflation factors are well below the threshold of 10, indicating no serious multicollinearity concerns.

Descriptive Statistics and Correlation Matrix. a

Note. aN = 774.

Correlation coefficient is statistically significant at the 5% level.

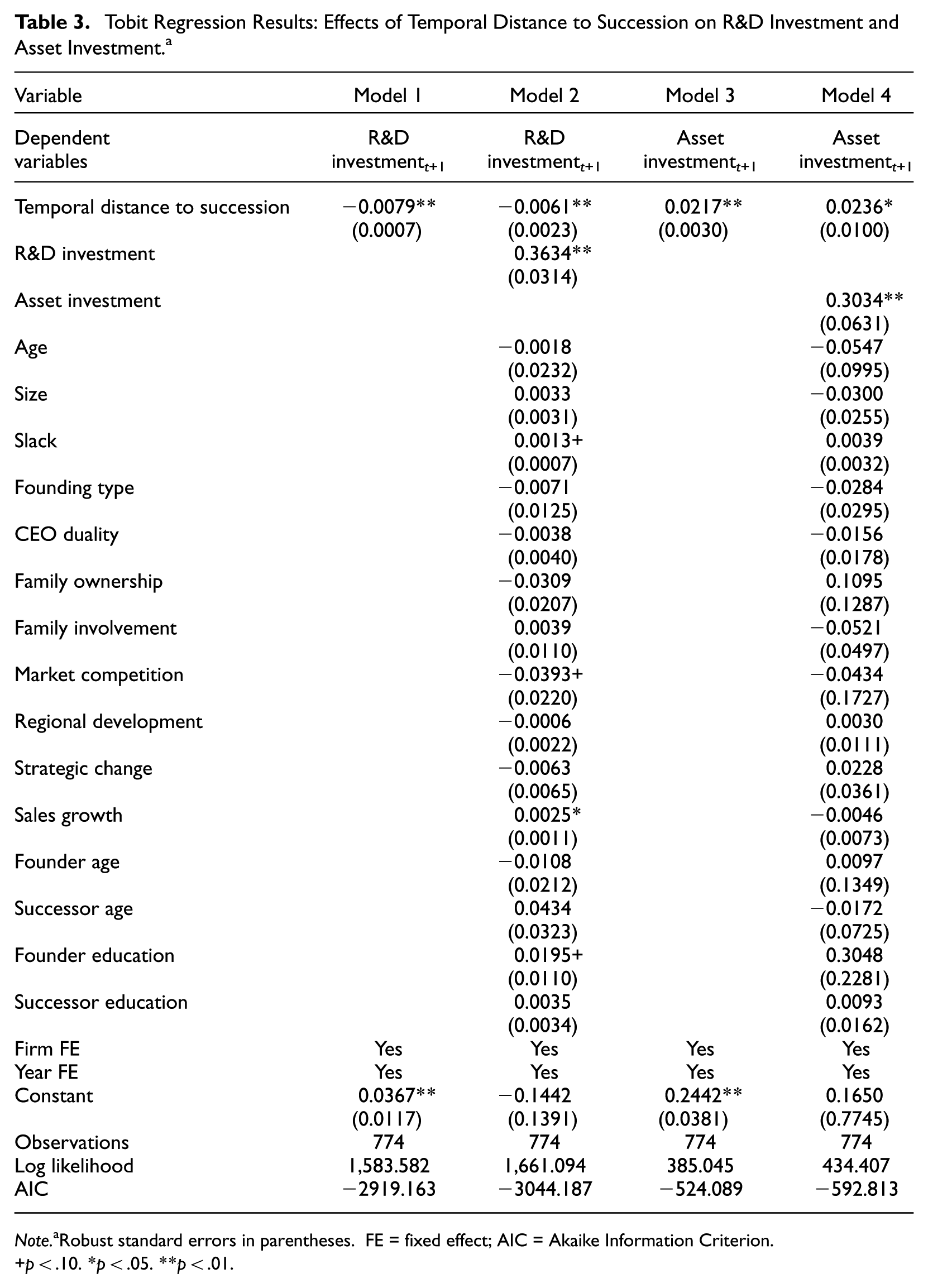

Table 3 presents the results of the Tobit regression analyses, estimated using xttobit procedure in Stata, on the relationship between temporal distance to succession and both R&D investment and asset investment. Xttobit can efficiently handle censored panel data, allowing for consistent estimation in the presence of censored dependent variables. Models 1 and 3 show the direct relationships without including control variables. The observed relationships are consistent with our hypothesized main effects. H1 predicts that family firms decrease R&D investment over time as they approach closer to succession. In Model 2, where R&D investment at t+1 serves as the dependent variable, the coefficient of temporal distance to succession is negative and significant (β = −.0061**, p < .01). In terms of economic magnitude, each year closer to succession is associated with a 0.61% decline in R&D investment. Thus, H1 is supported.

Tobit Regression Results: Effects of Temporal Distance to Succession on R&D Investment and Asset Investment. a

Note. aRobust standard errors in parentheses. FE = fixed effect; AIC = Akaike Information Criterion.

p < .10. *p < .05. **p < .01.

H2 predicts that family firms increase asset investment over time as they approach closer to succession. In Model 4 of Table 3, where asset investment at t+1 serves as the dependent variable, the coefficient of temporal distance is positive and significant (β = .0236*, p < .05). In terms of economic magnitude, each year closer to succession is associated with a 2.36% increase in asset investment. Thus, H2 is supported. Taking together, we found that family firms in proximity to transgenerational succession event tend to engage in significantly lower level of R&D investment, but higher level of asset investment, than those relatively far from the succession.

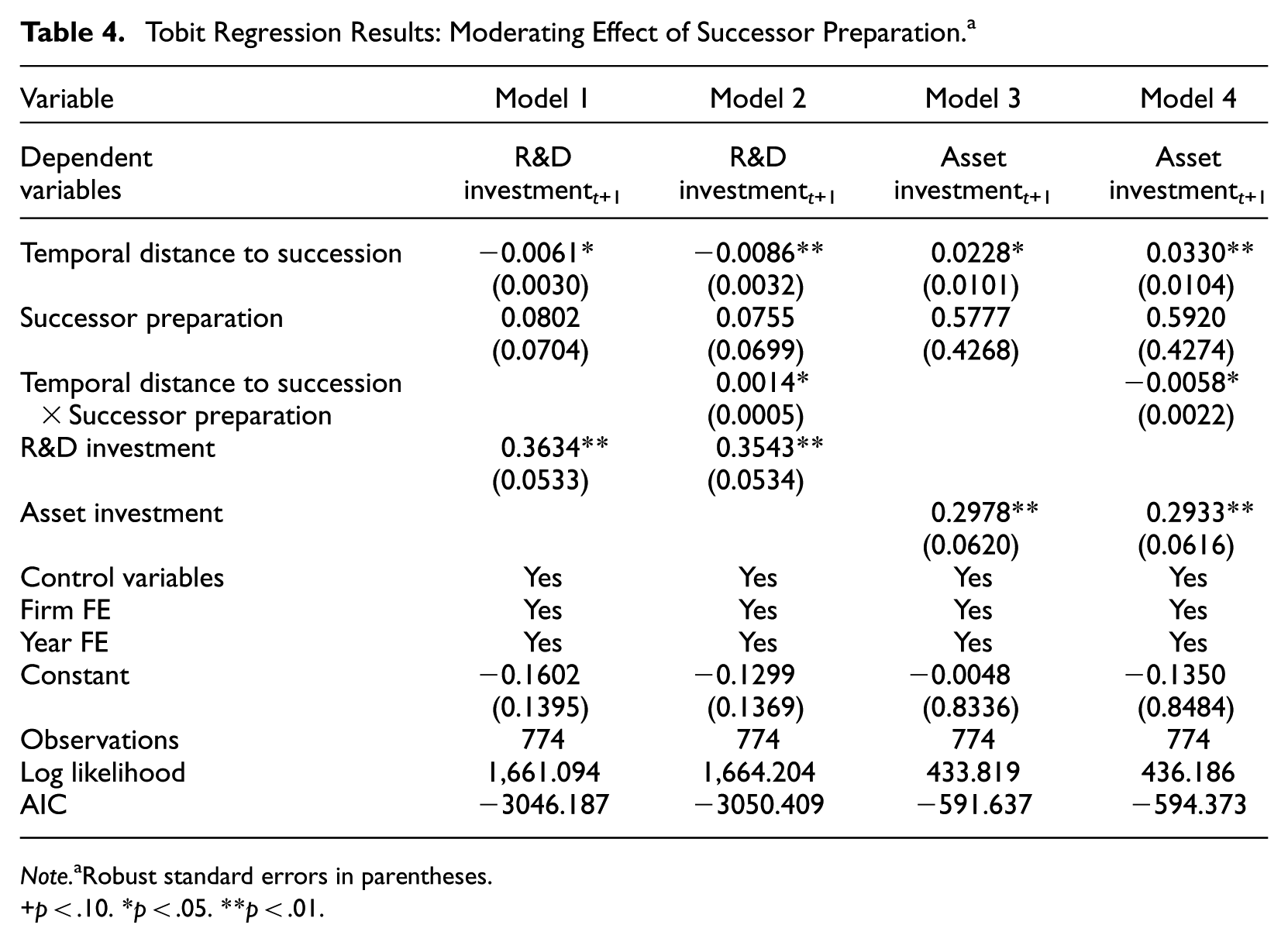

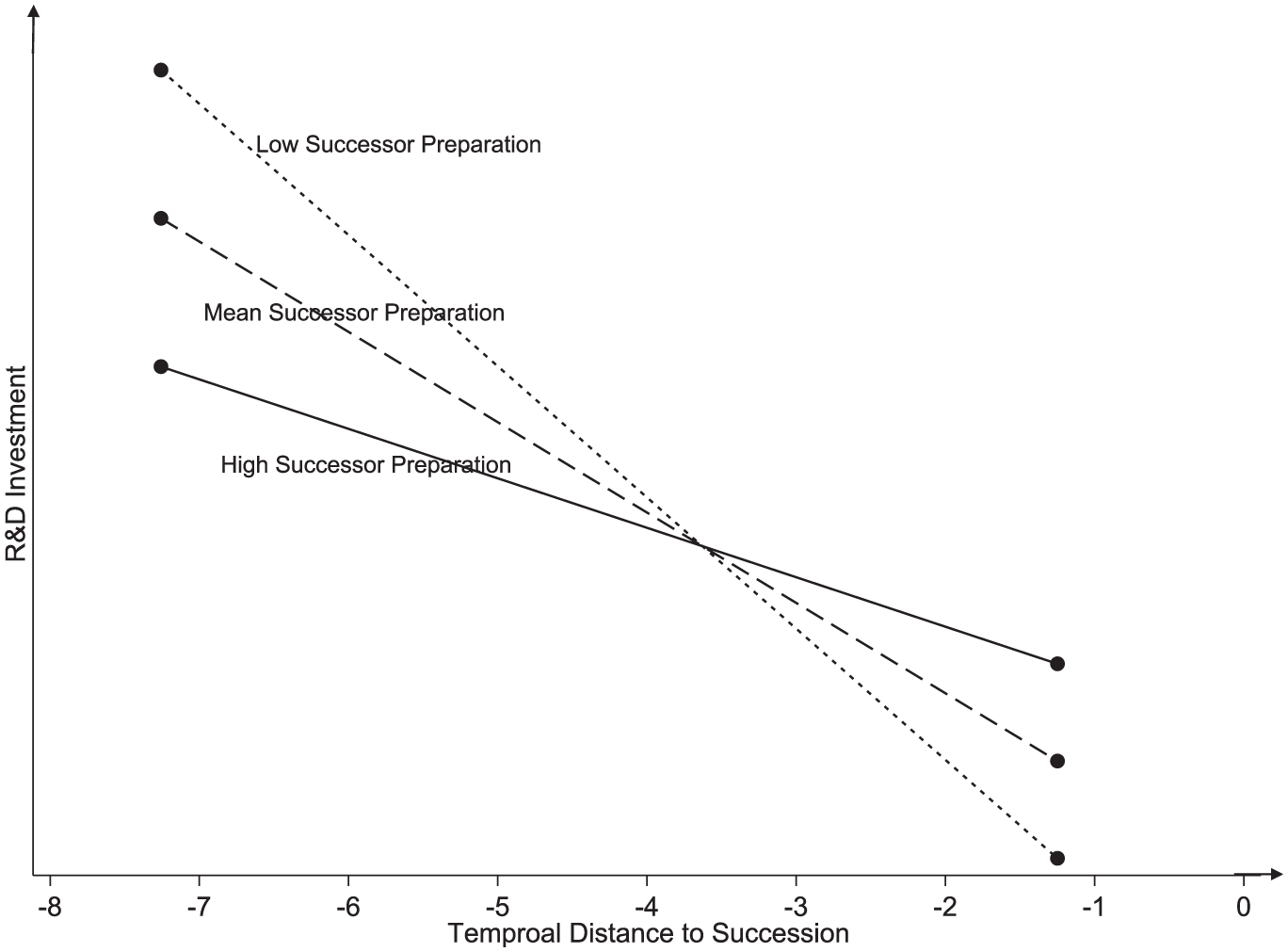

H3 predicts that the level of successor preparation weakens the impact of temporal distance to succession on strategic decisions regarding R&D investment and asset investment before succession. Table 4 reports the results with successor preparation as the moderator. As shown in Model 2, the coefficient estimate of the interaction between temporal distance to succession and successor preparation is positive and significant (β = .0014*, p < .05), supporting H3a. As illustrated in Figure 1, family firms with a high level of successor preparation tend to exhibit a less abrupt decline in R&D investment as succession approaches.

Tobit Regression Results: Moderating Effect of Successor Preparation. a

Note. aRobust standard errors in parentheses.

p < .10. *p < .05. **p < .01.

The moderating effect of successor preparation (Dependent Variable (DV): R&D Investment).

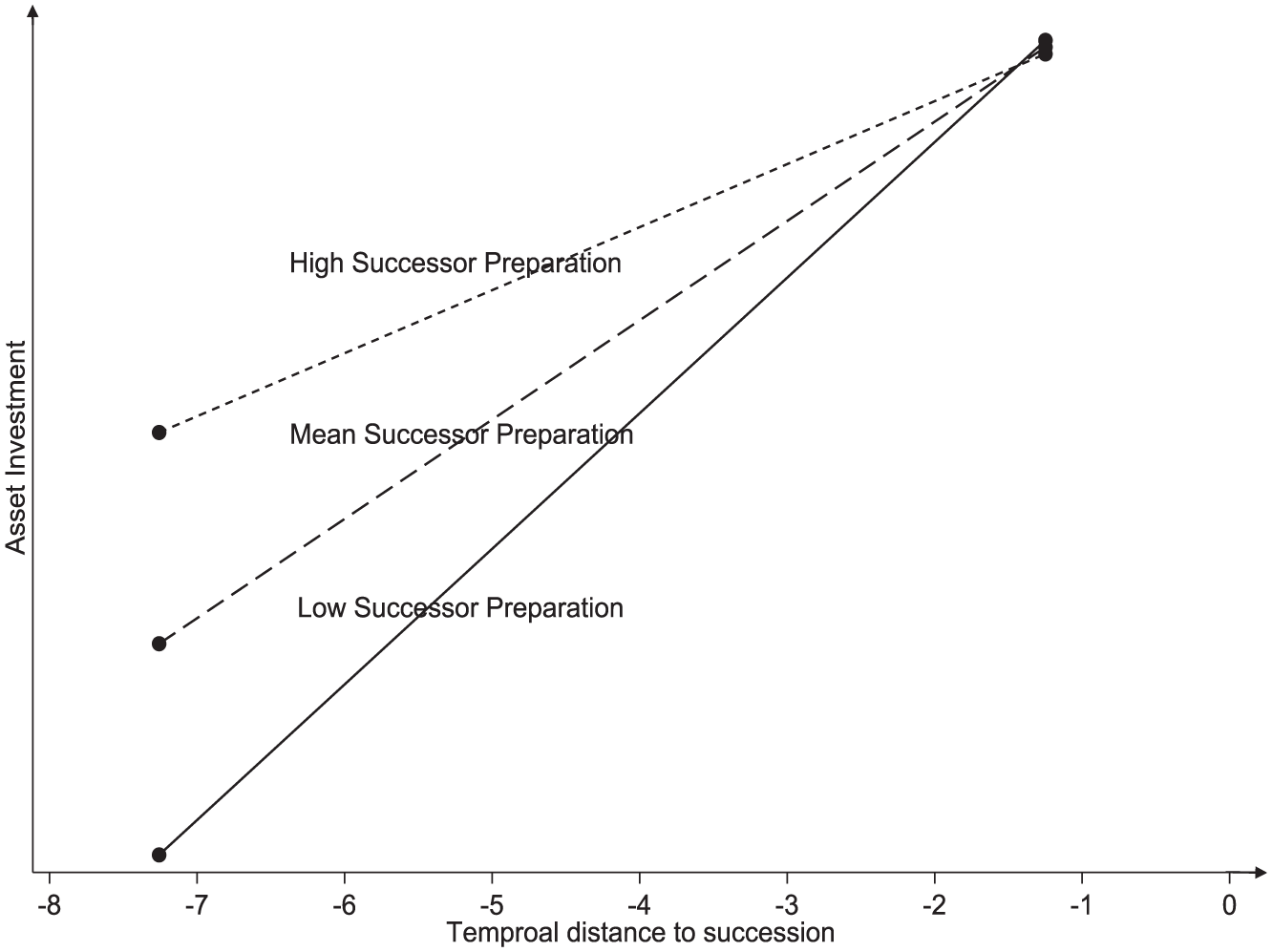

As shown in Model 4 of Table 4, when asset investment at t+1 serves as the dependent variable, the coefficient of the interaction term of temporal distance to succession and successor preparation is negative and significant (β = −.0058*, p < .05), supporting H3b. As illustrated in Figure 2, family firms with a high level of successor preparation are more likely to avoid over-investing in assets before succession.

The moderating effect of successor preparation (DV: asset investment).

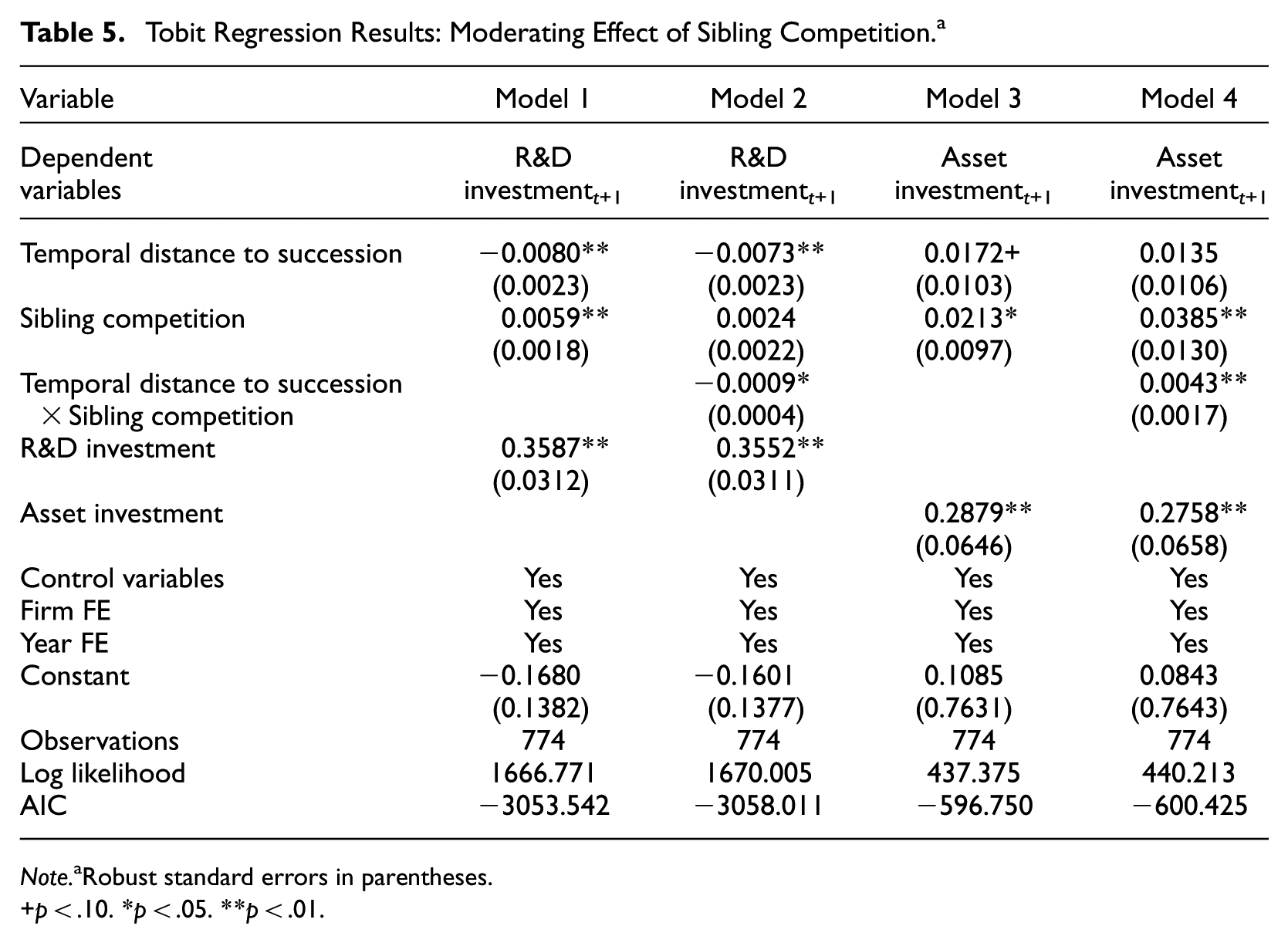

H4 predicts that sibling competition in succession strengthens the relationship between temporal distance to succession and both R&D investment and asset investment before succession. Table 5 presents the test results of these moderating effects. As shown in Model 2 where the dependent variable is R&D investment at t+1, the coefficient of the interaction term of temporal distance and sibling competition is negative and significant (β = −.0009*, p < .05), supporting H4a. As illustrated in Figure 3, greater sibling competition clearly amplifies the negative effect of the temporal distance to succession on R&D investment.

Tobit Regression Results: Moderating Effect of Sibling Competition. a

Note.aRobust standard errors in parentheses.

p < .10. *p < .05. **p < .01.

The moderating effect of sibling competition (DV: R&D Investment).

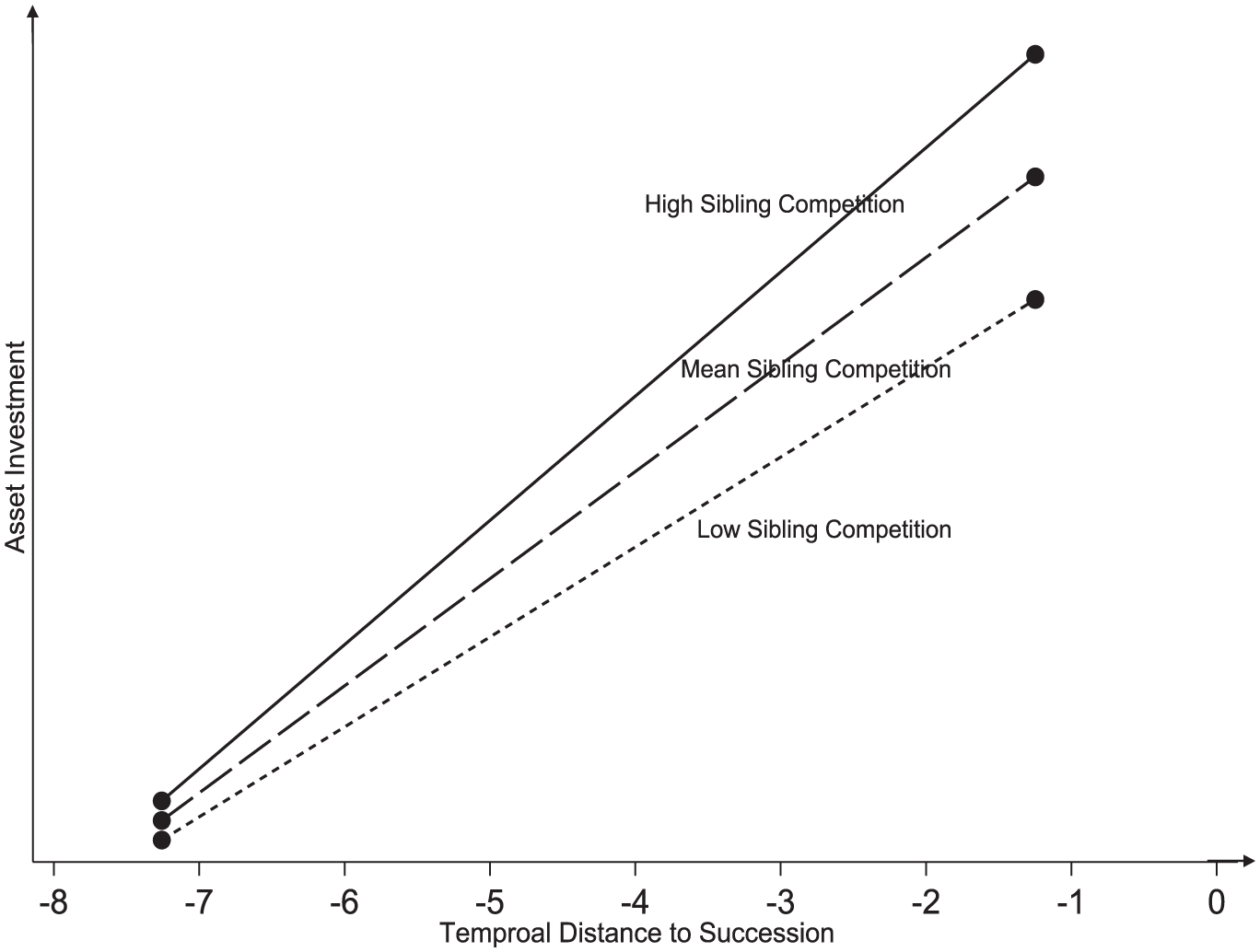

Model 4 of Table 5 presents the moderation effect of sibling competition with respect to asset investment. The coefficient of the interaction term of distance to succession and sibling competition is positive and significant (β = .0043**, p < .01), thus supporting H4b. As illustrated in Figure 4, sibling competition amplifies the positive effect of temporal distance to succession on asset investment, such that firms with higher sibling competition increase asset investment more rapidly as succession approaches.

The moderating effect of sibling competition (DV: asset investment).

Supplemental Analysis

Robustness Tests

To verify the independence of the two moderating effects, we re-estimated a comprehensive model including both interaction terms: temporal distance to succession × successor preparation and temporal distance to succession × sibling competition. As reported in Table S1 of the Supplemental Analysis, both interaction terms remained statistically significant, with their signs and magnitudes consistent with those obtained from the separate models.

We also conducted several sensitivity tests to assess the robustness of our findings, as reported in Table S2 of the Supplemental Analysis. First, we re-estimated the models using alternative measures of the dependent variables, replacing total sales with total assets as the denominator in calculating R&D and asset investment. The regression results remained consistent with those reported in Tables 3 to 5. Second, to address the potential concern that Tobit regression results might be driven by omitted time-invariant firm heterogeneity, we re-estimated the models using a fixed effect specification. The regression results of fixed effect models are consistent with the main findings. Third, we tested alternative sample specifications based on different pre-succession time windows, given that our baseline analysis included only firms with at least 2 years of data before succession. To assess sensitivity, we restricted the sample to firms with a minimum of 1 year and, separately, 3 years before succession. The main findings are robust across these alternative samples, reinforcing the validity of our conclusions. Fourth, we further assessed the robustness of our findings by varying the family ownership threshold used to define family firms. Specifically, we re-estimated all models using more stringent criteria: 15% and 20% family ownership, compared to the 10% cutoff applied in the baseline analysis. Again, the empirical results remain qualitatively unchanged, confirming the robustness of our findings to alternative definitions of family firms. Fifth, we replaced the measure of sibling competition with the number of sons of the actual controller involved in the firm, instead of using the number of children, as sons are typically the primary heirs in the succession context. The regression results remain qualitatively unchanged. Lastly, to account for potential distortions caused by the global financial crisis in 2008, we re-estimated all models after excluding observations from the year 2008; the key results remain unchanged.

Endogenous Tests

Although our explanatory variable, temporal distance to succession, represents a time frame rather than a substantive succession-related action, we adopted three strategies to address potential endogeneity concerns. This is important given that, in some cases, succession planning may influence both the timing of succession and strategic investment decisions. First, we used R&D investment and asset growth at time t+1 as dependent variables, while measuring all independent and control variables at time t. This temporal structure helps mitigate simultaneity and reverse causality concerns, consistent with prior studies (Chrisman & Patel, 2012; Fang et al., 2021). We further included a 1-year lag of the dependent variables in all regressions to construct a dynamic panel model, which captures path dependence and investment inertia while accounting for unobserved firm-level heterogeneity and omitted variables that may correlate with both succession timing and investment decisions. Second, we employed Heckman two-stage modelling to address potential sample selection bias that may arise from focusing on firms that had undergone transgenerational succession. Third, we applied the system Generalized Method of Moment (GMM) estimation to address potential correlation between the explanatory variables and the error term, while also accounting for lag effects, autocorrelation, and individual fixed effects in dynamic panel data. Details of the Heckman and system GMM approaches are provided in the Supplemental Analysis, with results consistent with the main findings, further supporting the robustness of our conclusions.

Discussion

Despite broad recognition of the importance of time in family behavior research (Kellermanns et al., 2012; Kotlar & De Massis, 2013; Sharma et al., 2014), particularly in SEW-based studies that acknowledge the evolving nature of social relations, cognitive perceptions, and affective needs over time (Jiang et al., 2018; Kellermanns et al., 2012), the literature continues to fall short in developing theories with an explicit temporal frame (Berrone et al., 2012). In this study, we bring temporality to the forefront by examining how temporal distance to succession influences strategic decisions in family firms, using the pre-succession context as a naturally occurring setting of changing temporal demands. Rather than treating succession as a static event, the temporal SEW framework that we developed conceptualizes it as a time period that unfolds with shifting reference points (Kotlar & De Massis, 2013; Kotlar et al., 2014): as the prospect of succession becomes more concrete, families recalibrate the type of “wealth” they value most, increasingly emphasizing the temporal-needs-based SEW. We find that this shift in SEW priorities influences strategic decisions before succession, leading firms to allocate more resources toward tangible asset investments while reducing commitment to R&D. Moreover, we find that this shift in strategic behavior is moderated by two chrono-context variables: successor preparation, which weakens the impact of temporal distance to succession, and sibling competition, which strengthens it. In doing so, we make several contributions.

First, we enrich SEW theory by developing a temporal SEW perspective that integrates SEW research with construal level theory. Such integration with psychological theory is overdue for advancing SEW research, considering that social-psychological mechanisms underlie the SEW construct and its behavioral implications (Gomez-Mejia et al., 2011; Jiang et al.., 2018). Emphasizing the temporal construal of dominant events, the proposed SEW typology (temporal-needs-based vs. aspiration-based) presents great potential for application beyond succession, such as family crises (e.g., leader death, founder divorce), certain stages of merger and acquisition (e.g., deal evaluation), and key phases of corporate entrepreneurship (e.g., new venture creation). Across the family firm life cycle, critical temporal junctures heighten the salience of family-centered goals and associated social interactions (Daspit et al., 2016; Kotlar & De Massis, 2013; Miller & Le Breton-Miller, 2021), introducing complexity into strategic behavior during these periods. In this sense, a temporal SEW perspective offers a novel theoretical lens for capturing both the dynamic and deeply contextual nature of strategic investment decisions in family firms. Adopting this perspective enables researchers to pose and examine questions that would otherwise remain difficult to address, such as evolving family dynamics and their outcomes (Ahlstrom et al., 2025) and shifting generational differences in responses to firm age and events across life stages (De Massis et al., 2018; De Pontet et al., 2007).

Second, with respect to R&D investment in family firms, our results help reconcile the inconsistent effects of succession on innovation documented in prior research. Existing studies report significant variation in R&D investment among family firms, often attributing it to families’ conservative, loss-averse tendencies (e.g., Chrisman & Patel, 2012; Li et al., 2022). However, succession has largely been treated succession as a static event, either by comparing firms with and without transgenerational intent or by examining R&D investment before and/or after succession. As a result, understanding of how and when loss aversion manifests remain limited. Kotlar and De Massis (2013) highlighted the “triggering role” of imminent intrafamily succession in goal setting, while Miller and Le Breton-Miller (2021) emphasized how “temporally and socially” embedded priorities shape how family discretion and emotional bonds lead to extreme strategic outcomes. We extend this existing knowledge by showing that impending succession shifts investment priorities, leading to a gradual decline in R&D investment during the years leading up to succession. This finding suggests that broad claims about the effects of succession on innovation may be misleading without specifying the temporal frame of analysis. Likewise, portraying family firms as uniformly long-term or short-term oriented overlooks the more pertinent question of which orientation dominates at a given moment and under what conditions (Kotlar et al., 2014). Future research may find it valuable to examine whether the long-studied effects of transgenerational succession are primarily concentrated in the pre-succession period.

Third, the distinctive pattern of asset investment in temporal proximity to succession, in contrast to R&D investment, highlights an important yet overlooked area of family business research. Prior studies have primarily examined standard business outcomes, such as internationalization, performance, innovation, finance costs, and succession intension and satisfaction (Daspit et al., 2021; Fang et al., 2018). While inquiries using these outcomes facilitate comparisons between family and non-family firms, shifting resource allocation preferences unique in family firms have received much less attention. Yet, observed outcomes may be temporally shaped by various unidentified factors arising between resource allocation and final outcomes. As a result, we continue to lack understanding of where the observed performance comes from and how family firms prioritize resource allocations across different life-cycle stages or around critical events. The tendency toward rapid asset growth, for instance, would remain undetected without examining the period leading up to succession. Our findings suggest that family firms approaching succession prioritize empire building over innovation investment, using asset investment strategically to facilitate succession. Future research, thus, may find it fruitful to examine specific resource allocation decisions beyond R&D investment. From a theoretical development perspective, asset investment is particularly aligned with temporal construal, as spending decisions directly reflect social-psychologically embedded priorities that evolve over time in family firms. Psychological responses to perceived temporal proximity, conceptualized as temporal-needs-based SEW, appear stronger in asset investment than in R&D investment, driving marked asset growth rather than curtailing innovation spending.

Fourth, our finding on successor preparation offers new insights into intrafamily succession. Prior studies highlights various benefits of succession planning, often positioning successor preparation as a factor influencing the success or effectiveness of succession (Cabrera-Suarez, 2005; Venter et al., 2005), but provides limited evidence on its concrete strategic benefits. We show that the commitment to nurturing and developing a successor yields strategic advantages by mitigating the adverse effects of temporal proximity to succession, specifically, by moderating the decline in R&D investment and tempering excessive growth in asset investment. This finding is particularly important for family firm owners, many of whom do not engage in systematic succession planning or invest in strategically preparing a successor. Future research could further examine whether the benefits of successor preparation stem from increased involvement in decision-making or from the enhanced social relationships developed through sustained, purposeful interactions between the successor, the incumbent, and internal and external stakeholders.

Finally, the role of sibling competition in moderating the impact of temporal distance to succession on strategic decisions warrants attention. While prior literature has noted the potential negative implications of sibling rivalry (Avloniti et al., 2014; Jayantilal et al., 2016; Lee et al., 2023), relatively little research has examined how these dynamics unfold in practice, particularly lacking empirical evidence. Our results show that sibling competition can amplify the adverse effects of approaching succession, leading to a sharper decline in R&D investment and a more aggressive increase in asset investment as the succession nears. This finding cautions family firms that involve multiple children in the management team, especially when using competition as a deliberate strategy for successor selection. Such firms should critically assess whether this approach is optimal, and if it is preferred, consider implementing corrective mechanisms to mitigate its negative strategic consequences.

Limitations and Future Research

We acknowledge several limitations in this study. First, although our conceptualization of temporal distance to succession encompasses both objective clock time and perceived event time (Aguinis & Bakker, 2021; Branzei & Fathallah, 2023), our empirical measure primarily captures objective temporal distance, specifically, the number of years between the observation and the succession event. We adopt this approach because anecdotal and experiential evidence suggests that clock time before an anticipated deadline (e.g., manuscript revisions) does induce time pressure and heighten the perception of temporal proximity and urgency. In this sense, clock time serves as a reasonable proxy for an ideal measure that would also capture the subjective temporal perceptions. Moreover, because succession is a past event in our sample, retrospective recovery of time perceptions is not feasible. Nonetheless, this study marks an important first step toward bringing temporality to the center of theorizing, rather than leaving both time and SEW implicit or limited within arguments (Calabro et al., 2019; Miller & Le Breton-Miller, 2014; Debicki et al., 2016). Given that incumbents often retain certain discretion over the actual succession timing, future research may explore how divergence, actual or perceived, from the intended succession timeline constitutes an additional chrono-contextual factor shaping strategic decisions before, during, and after succession.

Second, the generalizability of the findings should be approached with caution, as the results are based on a sample of publicly listed Chinese family firms, where both family business practices and succession processes exhibit unique behavioral patterns compared to family firms in other parts of the world (Bennedsen et al., 2015; Cao et al., 2015; Li et al., 2022). For instance, there is a strong preference for appointing a son as successor rather than passing the baton to a daughter (Xu, Chan, et al., 2024), partly due to the influence of the one-child policy. Chinese family firms also tend not to rely on competitive processes for successor selection (Cao et al., 2015), in part because of age gaps among siblings, although competition still arises when multiple children are involved in the management. It would therefore be valuable to investigate the investment behaviors of family firms in countries with different cultural and familial context. For example, in Western contexts, multiple siblings are often involved and successor selection tends to be more competitive than in China.

Finally, due to data constraints, we are unable to directly capture the firms’ temporal SEW needs in proximity to succession, the underlying mechanism in our theorized relationships. The nature of succession further complicates direct assessment of SEW, as SEW shifts over time and post hoc measurement is difficult. While this limitation is common in SEW research, it points to valuable opportunities for future research to directly examine dynamic shifts in SEW priorities and link them to important outcomes. For example, future studies could employ longitudinal survey designs to capture changes in SEW priorities or construal levels, experimental approaches, as well as qualitative process tracing during real-time succession. Mechanism-focused research of this kind will substantially advance our understanding of SEW and its evolutions in family businesses. Nevertheless, incorporating an explicit temporal frame, as we do here, represents one step further to capture SEW more accurately. Levesque and Stephen (2020) highlighted promising methodologies for advancing entrepreneurship research from a temporal lens, including historical approaches, experimental designs, diary studies, and experience sampling methods.

Conclusion

The interplay of family, business, and individual family members makes strategic decision-making in family firms both unique and complex. Temporality adds an additional layer of complexity by highlighting how key factors vary across different stages of the family firm life cycle. Yet theorizing with explicit attention to temporal conceptions and time frames is essential for generating knowledge that more accurately captures the idiosyncrasies of strategic processes in family firms. Advancing a temporal SEW perspective, we demonstrate how temporality in relation to intrafamily succession shapes strategic behavior through the temporal construal of distance to that event. Our findings suggest that family firms approaching succession face the risk of underinvesting in R&D while overcommitting to asset expansion. Such behavior may cause firms to miss critical windows for innovation and build empires that may require costly retrenchment later, ultimately squandering valuable family resources. We call for further research to examine dynamics surrounding the time of succession more closely and explore how such strategic pitfalls might be anticipated and mitigated.

Supplemental Material

sj-pdf-1-etp-10.1177_10422587261435911 – Supplemental material for Would Family Firms Approaching Succession Prioritize Innovation Investment or Empire Building? A Temporal SEW Perspective

Supplemental material, sj-pdf-1-etp-10.1177_10422587261435911 for Would Family Firms Approaching Succession Prioritize Innovation Investment or Empire Building? A Temporal SEW Perspective by Zhongjuan Sun, Jialin Feng and Jijun Gao in Entrepreneurship Theory and Practice

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is funded by the National Natural Science Foundation of China (No. 72172097), the Project for the Cultivation of Young Top-Notch Talents of Beijing Municipal Institutions (No. BPHR 202203174), and the Scientific Research Project-Young Academic Innovation Team of Capital University of Economics and Business (No. QNTD 202203).

Ethics Approval and consent to participate

There are no human participants in this article and informed consent is not required.

Supplemental Material

Supplemental material for this article is available online.