Abstract

Institutional alignment comprises the integration of sanctioned organizational models and standardized managerial roles, thus reconstructing traditional organizations as contemporary actors with homogenous global identities. We adopt this perspective to illuminate the processes by which a business family homogenizes to conform to the global world order, through extensive use of advisors and management consultants. To do so, we narrate the experience of a third-generation Israeli-based multinational enterprise. We find that the cumulative adoption of standardized corporate organizational models periodically shifts the family’s decision-making reference points, enabling it to expand its product and geographic scope and act as a global player.

Keywords

Introduction

Understanding how traditional organizations adopt standardized forms of corporate organization is a growing focus of management and organization theory (Bromley & Meyer, 2015, 2021; Drori et al., 2006; Marquis et al., 2017). Conforming to World Society (WS; Meyer, 2010) norms and values represents the transformation of traditional organizations, such as charities (Hwang & Powell, 2009), health care (Scott, 2000), libraries (Ignatow, 2011), mental health (Meyer, 1985), museums (DiMaggio, 1991), public education (Meyer et al., 1988), and universities (Ramirez & Meyer, 2012), by incorporating professional management models and control systems (Bromley & Meyer, 2015; Drori et al., 2006). The WS perspective (Meyer et al., 1997) is a branch of Institutional Theory concerned with attaining organizational legitimacy across multiple jurisdictions (Bromley & Meyer, 2015; Meyer, 2010; Meyer et al., 1997). The enabling process comprises the homogenization of unique and traditional organizations to function in globalized environments, such that “the legitimacy of older national and local cultures’ capacity to sustain more traditional organizational forms is weakened” (Drori et al., 2006, p. 13).

Much literature documents the prevalence and inefficiency of traditional family firms (Chandler, 1990; Gordon & Nicholson, 2010; Morck & Yeung, 2003). A contemporary contribution to this theme views family firms as characterized by emotional ties to the firm (Berrone et al., 2012; Gómez-Mejía et al., 2011). This tendency postulates that family firms differ from non-family firms because the family derives utility from their affective endowments at the expense of efficiency and better financial performance (Gómez-Mejía et al., 2011). Cognitive processes function as decision-makers reference points that shape their goals and aspirations (Shinkle, 2012). Cognitive processes are relevant in the family business field, as scholars contend that family business owners have unique “psychological, behavioral, social, and cognitive” attributes (Gómez-Mejía et al., 2011, p. 655) that lead to the utilization of socioemotional reference points in reaching strategic decisions (Gómez-Mejía et al., 2007). Theorizing how owners’ reference points change over time (Jaskiewicz et al., 2019; Mazzelli et al., 2019; Nason et al., 2019) and how they influence economic decision-making (Stommel et al., 2024) is a growing concern. Family firms may prefer to retain their autonomy, insulating themselves from professional management (Stewart & Hitt, 2012), thereby influencing their reference points and making them unwilling to adopt contemporary organizational models.

However, alternative accounts of family firm efficiency challenge this view due to its reification (Schulze & Kellermanns, 2015), arising from its reductive, essentializing view of family firms as homogeneous entities sharing common dysfunctional attributes (Hsueh et al., 2023). Researchers find mixed evidence about the relative financial performance of family firms, suggesting differences in organizational and managerial practices (O’Boyle et al., 2012; Van Essen et al., 2015). Recent accounts of family firm heterogeneity (Daspit et al., 2021) suggest that many family firms escape the penalties of emotionally laden decision-making. Thus, how business families loosen their cognitive constraints represents a significant gap in our understanding of organizational change processes in long-lived family firms.

To address the tension between family firms’ emotional disposition and their potential to conform to a global world order, we employ inductive theory building based on an in-depth historical case study of a family-owned and controlled Israeli multinational, the Marcus Group, the country’s largest publicly listed and internationally diversified food group. Marcus is the archetype of a traditional family firm. Founded in 1937, Marcus operated in survival mode for some 25 years. However, a decisive event in the firm’s growth and development occurred with the appearance of external advisors who recommended adopting simple strategic planning and accounting practices. Subsequently, successive generations adopted contemporary corporate organization practices introduced by management consultants and family advisors. We show that the cumulative adoption of standardized corporate organizational models and family-management practices enabled this business family to improve its performance by expanding its product and geographic scope. Accordingly, we framed our research question: How do external advisors and consultants mediate reference point shifts that lead the business family to homogenize and conform to the global world order?

To interpret our findings, we apply two management theories: First, to explain the direction of the organizational change process, we draw upon the reference point literature (Jaskiewicz et al., 2019; Nason et al., 2019; Shinkle, 2012; Stommel et al., 2024; Ye et al., 2021) concerning the malleable reference points families develop to orient their decision-making (Sinha et al., 2020). Reference points are “integrated representations of goals, data, and inferences that act as filters by influencing what aspects of the environment receive attention” (Nason et al., 2019, p. 851). They guide the selection, categorization, and organization of information, shaping decision-making processes and interpretations of the environment. Second, based on the WS perspective, which suggests standardized “best practice” models circulate through several channels, including business schools, business media (Sahlin-Andersson & Engwall, 2002), professional advisors, and management consultants (Ruef, 2002), we explain the origins of standardized corporate models in family firms. Our findings depict the catalytic impact of advisors and management consultants on a traditional mom-and-pop family firm, standardizing and aligning organizational structures and decision-making processes to conform to global WS norms and values.

Our longitudinal case study of the advisors’ role in mediating reference points by introducing standardized models in traditional family firms situated in a field-specific context makes three related contributions to organization theories of family firm evolution beyond the traditional conception of the family firm. Our first finding contributes to the rising interest in reference point shifts in family firms by identifying specific actors and their roles in articulating and mediating an expansive global identity. We build on Nason et al.’s (2019, p. 862) call for qualitative research “to explore the process of reference point selection, as well as how external opinions coming from social class peers, evaluators, and professionals affect the spatial focus.” We extend their suggestion that reference points shift from inward to outward and from backward to forward, empirically demonstrate these shifts, and formalize them. The business family in our study changes from an emotional, particularistic survival to a homogeneous global identity over three generations. Second, we contribute to the growing literature of advisors in family firms, showing in detail the family’s as well as the advisors’ processes and mechanisms, thereby building on Strike et al.’s (2018, p. 26) call to “teasing out the specific attributes of the advice, advisor, or environment of the advising process,” and not to treat advice “as a blanket concept.” Our longitudinal data show how advisory engagements and processes correspondingly evolve as family firms standardize, which augments the mostly cross-sectionally based literature on family firm advisors.

Furthermore, we extend Magrelli, Rovelli, et al.’s (2022, p. 23) study on advisors’ mediating role on relational succession issues between generations, by focusing on how they mediate reference point shifts and demonstrating in detail “both generations’ temporal orientations,” where the next generation shows enthusiasm for “turning the page.” We also contribute to a better understanding of how family generations differ in their focus (Magrelli, Rondi, et al., 2022; Magrelli, Rovelli, et al., 2022), showing that the older generation prefers to protect the traditional past. In contrast, the new generation focuses on adopting global norms and values. Third, we contribute to the WS literature, which has primarily focused on formalizing non-profit organizations and, until recently, has overlooked business organizations (Bromley & Meyer, 2021). Our focus is on the diffusion and adoption of standardized corporate models, tracing their global origins within a family-firm advisory ecology. Our depiction of the unfolding organizational change process captures how the family firm cumulatively acquires capabilities to compete in international markets.

Relevant Theory

Scholars often depict tradition in long-lived family firms as an accumulated legacy that enables the preservation of the family’s identity (Sasaki et al., 2020), reflects past achievements, and accumulates knowledge stocks and competencies (Lattuch, 2019). Scholars also construe the traditional family firm as inflexible, resistant to change, and an inward-looking culture that breeds conformity (Miller et al., 2013; Nordqvist & Melin, 2010). In this view, preserving tradition can exert path dependency forces and limit managerial agency (Suddaby & Jaskiewicz, 2020). Furthermore, family firm tradition can be imbued with national cultural qualities and values, reflecting and reinforcing traditional hierarchical role relationships (Lu et al., 2021). Recent research suggests that family firms can retain tradition while, paradoxically, achieving innovation (Erdogan et al., 2020). Indeed, a mounting argument suggests that managing tradition can be a strategic imperative for a family firm (Suddaby & Jaskiewicz, 2020).

Marcus’ development from a precarious mom-and-pop dairy to a diversified multinational enterprise represents significant cognitive and organizational change. Our first relevant theory concerns cognitive processes, which are shaped by decision-makers’ reference points and thereby influence their goals and aspirations (Shinkle, 2012). Family firms concerned with preserving their emotional attachments may prefer insularity and may mistrust non-family executives (Gómez-Mejía et al., 2011). This conservative viewpoint is inconsistent with radical organizational change. Some family firms are described as more effective at implementing adaptive change strategies than others (Pieper et al., 2025); therefore, how business families overcome cognitive constraints represents a significant gap in our understanding of organizational change processes in long-lived family firms. Describing how advisors mediate reference point shifts builds on Strike and Rerup’s (2016, p. 881) assertion that it reflects “the ambiguous role played by mediators, who work with and influence the individuals who are sensemaking, yet are also ‘outsiders’ who pay ‘attention to the larger context in which sensemaking occurs and introduce new cues and perspectives into a local setting’.”

The neglect of understanding how business families overcome cognitive constraints is especially characteristic of founder CEOs (Wasserman, 2003), who often concentrate strategic decision-making in their own hands, failing to build structures that delegate decision-making authority to other managers (Gedajlovic et al., 2004). Family CEOs are known to have long tenures and can become “stale in the saddle” (Miller, 1991), relying on dated practices (Bloom & Van Reenen, 2007) and being closed to market feedback (Quigley & Hambrick, 2012). However, Nason et al. (2019) argued that long-lived family firms can reduce the constraints of tradition and insular reference points by renewing their knowledge structures and shifting family mental models toward external and future-oriented reference points, thereby serving as antecedents of organizational change. Nason et al. (2019) suggested that socialization drives these shifts through three actors: next-generation family members, peers from social class, and non-family professional advisors. Jaskiewicz et al. (2019) claimed that only a subset of highly functional, adaptive-to-change families is receptive to new knowledge and, thus, may be willing to shift their reference points. While Mazzelli et al. (2019) agreed that families with limited socialization are unlikely to shift their reference points, the emerging conversation about when and how reference points shift in family firms has so far been theoretical. As adaptive organizational change is central to a firm’s prosperity, understanding the mechanisms and processes that enable these cognitive shifts can help firms align their strategy, resources, and capabilities with changing conditions in their external environments. Addressing this gap should help scholars, advisors, and business owners better understand strategic processes that promote family firms’ performance.

Our second relevant theory draws on the institutional theory of WS, which posits that nations are embedded in a global culture rather than disconnected from the international context (Drori et al., 2009). WS scholars argue that to achieve legitimacy and social approval, organizations must seek alignment with global cultural norms and values circulating in transnational discourse (Meyer, 2010). These include discourses on the value of economic development, good governance, human rights, sustainability, and inequality, which broadly impact contemporary civil society, including government, healthcare, education, and the professions (Meyer et al., 1997). From this perspective, organizations are no longer exclusively constrained by specific regional or national contexts. Firms become homogenized when they adopt standardized corporate organizational models, reflected in “highly similar mission and vision statements, organizational logos, executive board structures, compensation schemes, annual meetings, sustainability reports, and standardized job titles” (Pope & Meyer, 2015, p. 174).

However, discourse in WS is dynamic and subject to change in response to scientific discoveries, cultural changes, and political events. Moreover, best practice management models are also malleable in response to cultural and social change (Bromley & Meyer, 2015) and subject to trends or fads (Abrahamson, 1991). Recent WS theorizing conceives organizations as pursuing an extended purpose beyond efficiency toward projecting a social vision of managerial charisma, innovation, and entrepreneurship (Bromley & Meyer, 2015, 2021). Such behavior provides a measure of legitimacy and transparency to organizations operating across multiple domains. Unlike much of institutional theory, with its emphasis on structural constraints and isomorphism (Powell & DiMaggio, 2023), WS portrays professional managers as endowed with “empowered actorhood” who, compared to persons, “are much more agentic- more bounded, autonomous, coherent, purposive and hardwired” (Meyer, 2010, p. 3). More generally, “Actorhood models” are cultural and cognitive understandings that bestow roles, responsibilities, and behavioral scripts on individual and collective actors (Bitektine et al., 2020).

Actors embrace WS values and norms to generate legitimate models of proper human actors. This embrace calls for leadership qualities beyond formal authority or technical expertise, including soft skills, communication, collaboration, and inspiration. Actors carrying WS models rationalize and formalize corporate organization and management positions, such as Human Resource Managers, accountants, lawyers, and other professional service firms (Sahlin-Andersson & Engwall, 2002). Commensurate with mass education in modern society, sources of formality are “highly-schooled” carriers of scientific, abstract, and universalistic management principles (Sahlin-Andersson & Engwall, 2002; Schofer & Meyer, 2005). The epitome of such carriers is elite management consulting (Kipping et al., 2019), and this study focuses on the family firm context. These transnational professionals “combine abstract knowledge global mobility across national and organizational settings … and distributed agency to shape global practices” (Harrington & Seabrooke, 2020, p. 399). Thus, the focal actors in this study are business advisors and management consultants, who have expanded exponentially over the past 50 years (David et al., 2013; Ernst & Kieser, 2002).

Method

Research Context

We decided to study Marcus during a discussion among two authors, one of whom was a family member of the firm. The firm presented an ostensible paradox compared to much of the family firm literature on wealth preservation and stable reference points across generations (Patel & Chrisman, 2014). Over three generations, the family firm moved from survival mode and wealth preservation toward periodically adjusting its goals toward more ambitious aspirations. Marcus offered a rare opportunity to access historical and real-time inside data on long-term ownership and strategic decision-making, enabling a study of how family decision-makers realized aspirational objectives assisted by multiple consultants and advisors. While scholars criticize single cases for their limited generalizability to larger populations, they offer depth and richness for tracing and understanding concepts that would otherwise be unobservable in multi-organization studies (Sinha et al., 2020).

Family firms and their advisors provide a valuable context for discovering how organizations standardize and shift reference points over time for three reasons. First, family firms have more readily observable complexities than their non-family counterparts. The overlap of family, business, and ownership increases the tendency for and visibility of conflict and opposing goals. Second, the dominant coalition (DC) in family firms has a longer tenure than decision-making coalitions in widely held firms (Strike et al., 2015). The tenure of CEOs in non-family firms is 6.43 years, whereas the average tenure of family CEOs in family firms is 17.6 years (McConaughy, 2000).

Moreover, long after family CEOs leave their positions, they often remain members of the DC, frequently at arm’s length, and continue to reach out and influence the firm’s decision-making. As scholars have underlined the need to focus on temporality in strategy process research (Kouame & Langley, 2018), this continuity allows us to study how reference points shift over time. Third, an emergent research stream has shown that family firm advisors are uniquely positioned to serve family firms and play influential roles, shaping the firm’s and family’s DC (Harrington, 2016; Nason et al., 2019; Strike & Rerup, 2016). Strike et al. (2018) suggested examining advice-giving and advice-taking in family firms to understand this process better. In our case, one advisor—a German executive—developed a lifelong relationship with the Marcus family and was an active DC member for over 30 years. These family firm advisors are pivotal actors in strategic theorizing, linking multiple levels of analysis. Through micro-level processes and practices, they drive macro-level outcomes (Harrington & Strike, 2018), providing a topical research context for examining the mediating processes that enable reference point shifts.

Data Collection: Sources of Data

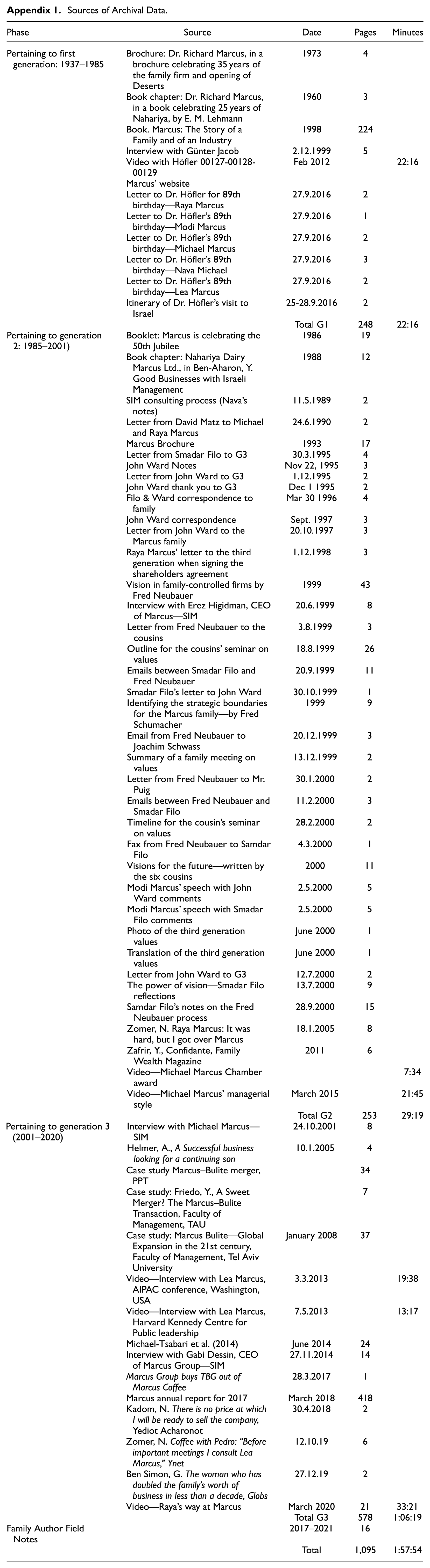

In line with our research question, we conducted an inductive single-case study of Marcus spanning three generations. Inductive approaches focus on answering “how questions,” which are helpful when aiming to open new areas of inquiry (Golden-Biddle & Locke, 2007). Following a case study approach, we collected data from multiple sources (Yin, 1994). Collecting data from various sources enables triangulation, thereby increasing the reliability and integrity of the data (Hartley, 2004; Yin, 1994). We collected and analyzed data sources covering almost 90 years, from 1936 to 2025. We kept a detailed record of the data collection process, including email exchanges and personal conversations with family members, current and prior family firm employees, board members, and advisors.

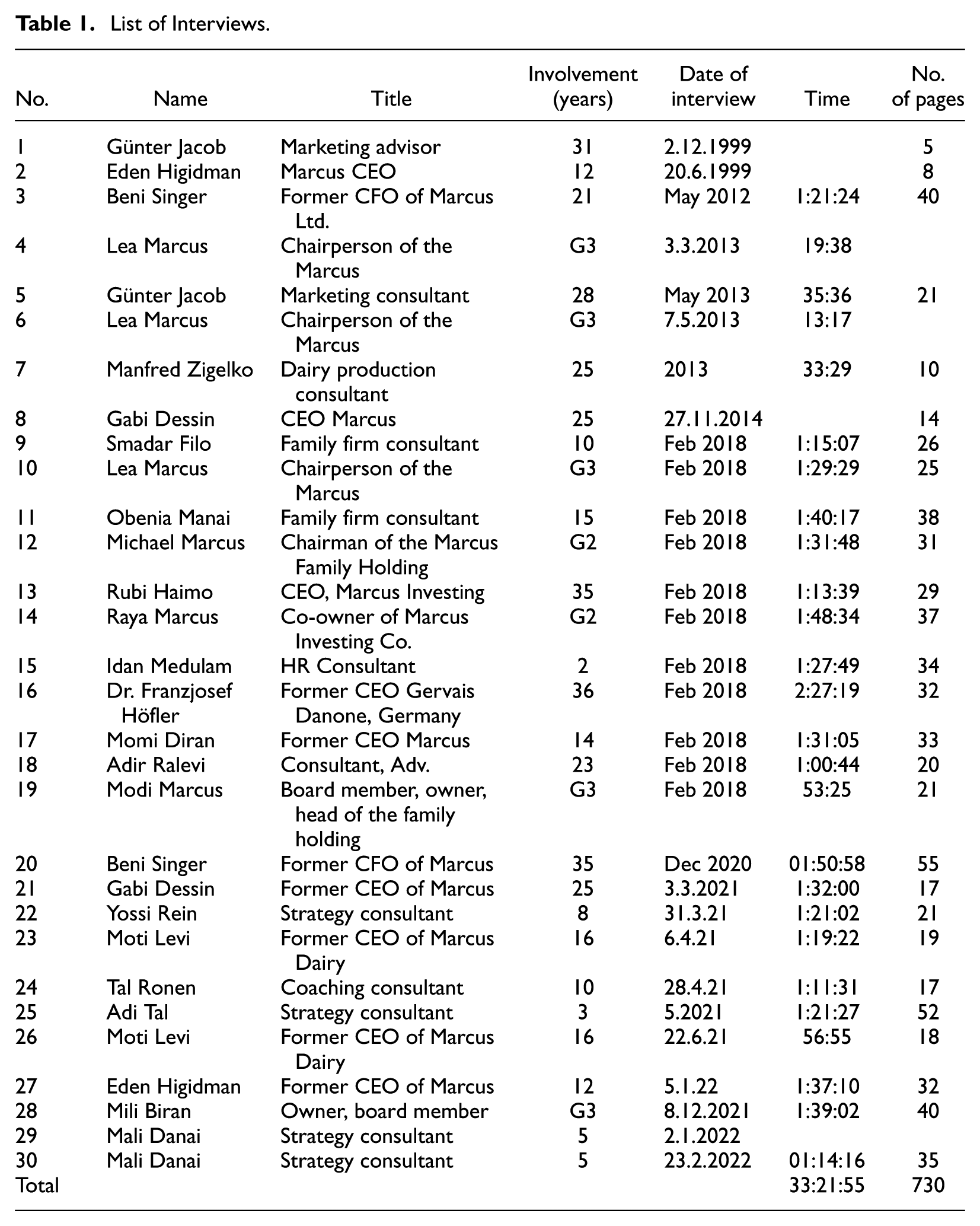

Our primary data sources, which enabled us to examine how advisors mediate the family firm’s reference points and resulting global identity over time, were open-ended, in-depth 30 interviews with 22 individuals (6 were interviewed twice, 1 was interviewed 3 times) plus 6 additional interviews from the archival data. We collected longitudinal data on microprocesses and organizational outcomes to understand how the family’s scope and focus changed across generations. We define micro-processes as “individual or collective processes and activities taking place at a lower level than organizational level” and macro-level outcomes as “organization-level characteristics, processes, and behaviors” (Kouame & Langley, 2018, p. 561). In studying the processes, we explicitly consider temporal linkages between events, providing insights into how micro-processes recursively affect organization-level outcomes.

Interviews

Our interviews included historical accounts and real-time data on the current family coalition, goals, and the role of advisors. In February 2018, three authors conducted semi-structured interviews with 10 informants. Based on our open coding of the narratives, using purposeful sampling (Lincoln & Guba, 1985), we interviewed five advisors and four family members, including the current and past family member chairpersons, the former CEO, and the CEO of the family office. Our initial questions were to establish the nature of the relationships between past and current family firm members and advisors. For example, we asked how the advisors first met the family, how long they had been engaged with the family as advisors, how frequently they met, the nature of the meetings, and how they established the goals and objectives for working together. These interviews shed light on the differences between relational and transactional advisors (Schein, 1987). The former is deeply embedded within the business-owning family, while transactional advisors are consultants hired for specific mandates (Nason et al., 2019). They helped us understand the presence of a DC—the primary point of contact for the advisors—who governed the firm and its strategic decisions.

The interviews shed light on the family firm’s need for guidance in defining and establishing reference points. We probed for examples and stories of relationships, goals, and reference points to unearth the rich data underlying the relationships. We conducted another interview in 2018 with one of the family firm’s past advisors. As is integral to inductive studies, we refined our questions further following several rounds of data analysis and as our theory emerged.

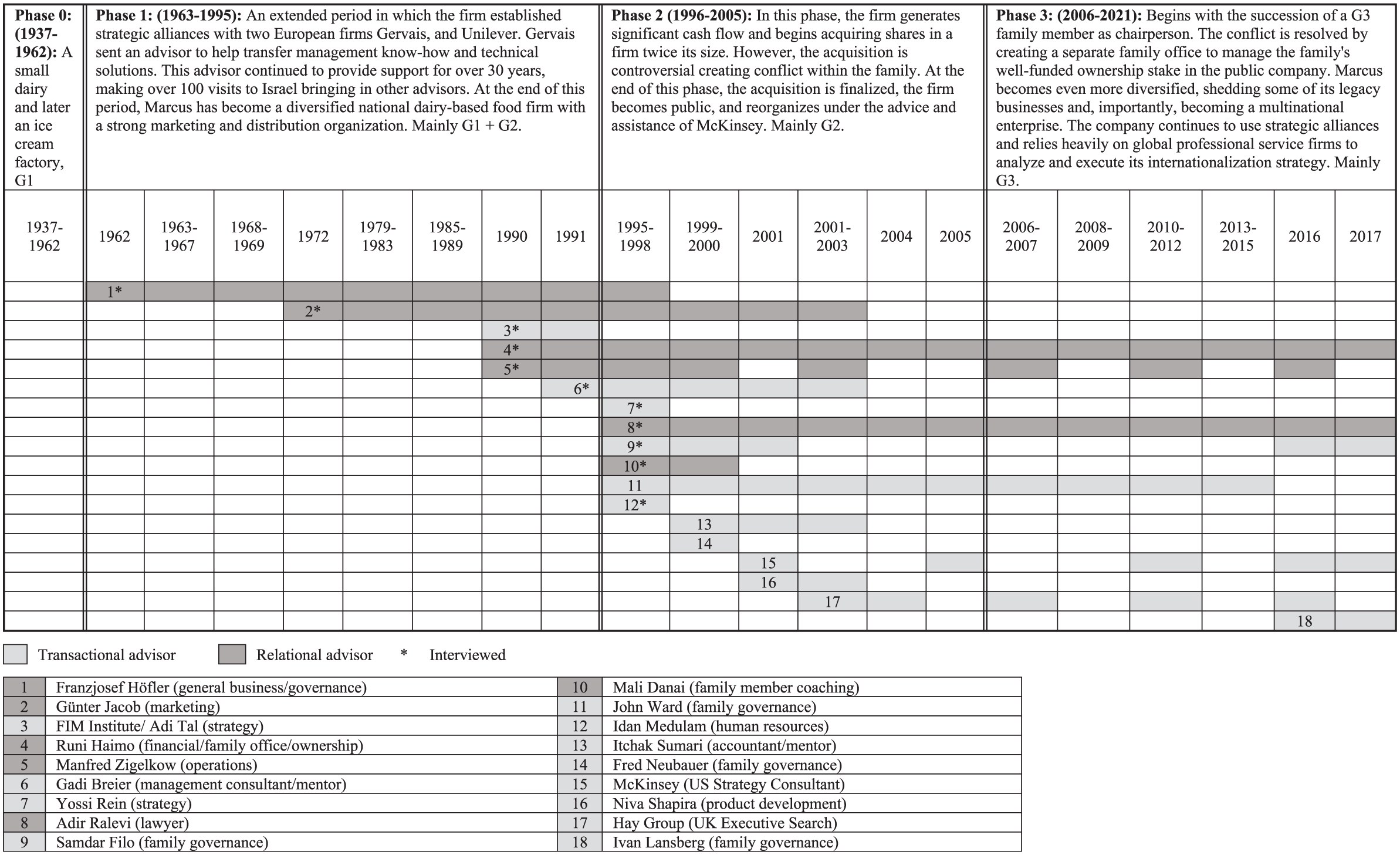

In 2020 to 2022, we interviewed 11 additional family firm members and advisors whose names snowballed from the initial interviews, for a total of 30 interviews with 22 individuals. Interviews lasted 73 to 147 min. We supplemented the interviews with six taped interviews with other advisors, employees, and family members from the archival data (see Table 1 for a list of interviews; see Figure 1 for a description of consultants over time and a summary of business phases). We recorded 33 hr of interviews and transcribed them, producing 730 pages of data.

List of Interviews.

Advisor’s involvement over time.

Archives

Our archival data included, but was not limited to, private correspondence between advisors, family members, and family firm members; reports and private notes; meeting minutes; advisor and company presentations; and family and firm governance documents (e.g., value statement, shareholders’ agreement). The family member author’s involvement within the firm and family granted us access to data, such as email exchanges and personal conversations, which are not part of public records. Furthermore, her intimate understanding of the firm’s and family’s historical and real-time activities provided us with invaluable insights that would not have been possible from interviews and data sources alone. An insider’s participatory ethos “also draws in diverse voices, often surfacing power-laden conflicts that are embodied, affective and historically silenced … [which] holds the potential to generate both locally useful insights … and theoretically generative knowledge (understanding latent tensions and dynamics through their impact on organizational decisions and actions)” (Greco & Berti, 2025, pp. 2–3). However, all analyses were conducted in collaboration with other team members to ensure objectivity.

We also accessed company and partner websites, press articles, media coverage, video interviews, presentations, itineraries, case studies, book chapters, marketing materials, and other external and internal family and business documents. The archives helped identify advisors and their roles within the firm and the family, how/whether these roles changed over time, reference points, and how they shifted over time. We traced reference point shifts, standardization and the involvement of advisors over time to create a detailed timeline (see Appendix 1 for data sources).

Site Visits and Observational Data

Three authors visited the firm’s corporate headquarters, met with the current chairperson, and toured the facilities. These same authors also visited the family’s original homestead and dairy. The homestead now stands as a private museum, featuring documentary videos of the family’s and firm’s journey, artifacts, personal journals/diaries, and other archives for the authors to study and review. Archival data were integral to understanding and reconstructing how reference points unfolded over three generations, as well as to the role of advisors in defining and mediating these shifts. The archival data also helped us develop our initial list of informants to interview and our interview protocol. 1

Data Analysis and Coding

Our analytical approach combines two methods that Kouame and Langley (2018) labelled as “progression” and “instantiation.” This approach (termed hybrid 3 in Kouame and Langley [2018]), which typically utilizes single case studies, is used to consider how recursive micro-processes constitute (or instantiate) macro-processes over time. Hybrid 3 brings together the complementary strengths of progression and instantiation: progression recognizes temporality; instantiation includes both real-time and retrospective data, provides in-depth, detailed data to reveal the significance of micro-level activities, and assumes that micro and macro are recursively interconnected (see Kouame & Langley [2018] for a detailed explanation of the two methods and hybrid 3). This integrated approach allowed us to conduct a fine-grained analysis of each period under study to propose a recursive model of how dynamic family coalitions interact with advisors to define and realize their reference points, and to develop norms summarized in the current organizational culture, layer by layer throughout the periods.

As is typical with rich inductive qualitative research, to answer the question, how do external advisors and consultants mediate reference point shifts through which the business family homogenizes to conform to the global world order? We analyzed our data inductively by continually comparing them with the literature and emerging data structures (Langley, 1999; Miles & Huberman, 1994). We did not enter the field with a perspective of reference points and standardization, nor that of WS. These ideas emerged only after several rounds of data collection and iterations between the data and various literatures on goal setting, decision-making, DCs, family business, and, eventually, reference points, standardization, and WS. We were interested in the role of advisors within Marcus and their influence on the firm’s and family’s entrepreneurial endeavors. We first developed a rich, detailed, chronologically ordered narrative and timeline of Marcus’ historical account—both the family and the firm—spanning almost 90 years. Our narrative included Israel’s external environment (political, cultural, economic, and social) that shaped Marcus’ activities.

Once the constructs of reference points and standardization began to emerge and gain traction, we identified four periods organized through “periodization” (Rowlinson et al., 2014) of reference points and macro outcomes. We wrote the narratives to reflect these four periods, and the evidence of redefining, mediating, and realizing that reference points and standardization were recursively interconnected emerged. We studied the political and industrial environments during these periods as they greatly influenced the firm’s definition and realization of reference points.

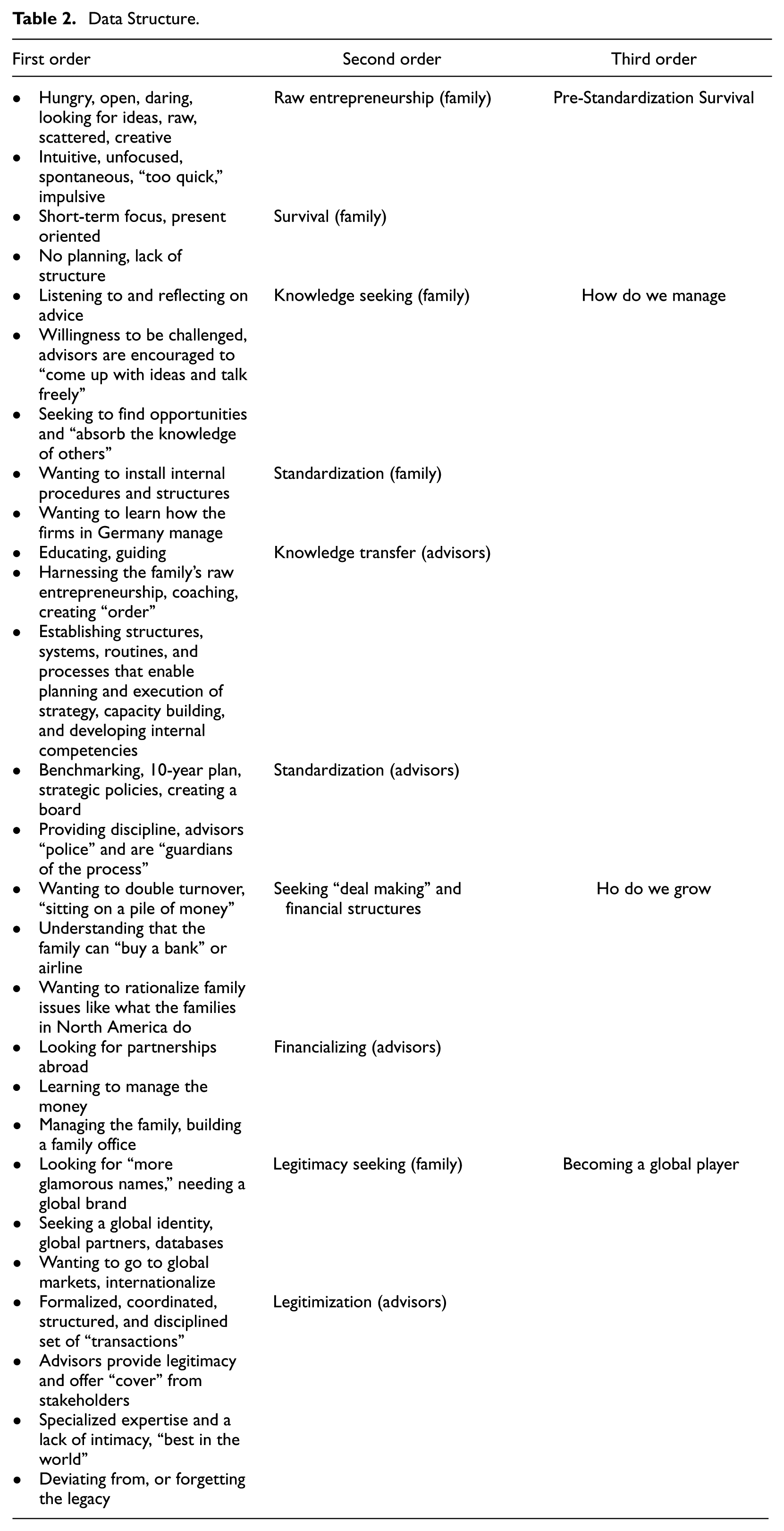

Two authors independently coded the data, including the interviews and historical and current data on the firm and family. Using an inductive approach allowed the constructs to emerge and gave voice to the perspectives of the advisors, family members, and family firm employees (Gioia et al., 2013). We identified constructs and grouped them into categories, developing our first-order codes. We sought evidence of triangulation (Jick, 1979) across current and historical interviews, observations, and historical family and firm data. We continued to collect additional data, going back and forth between analysis, data collection, and the literature, refining codes, constructs, and the ensuing. Here, the family member author was able to impart insights that would not have been otherwise available. By coding the data distinctly across time, we could map the origins of reference point redefinition, the process of realizing the reference point, and the rich yet complex interactions between the advisors, family coalition, and key employees. We identified relationships among recurring themes and grouped them into higher-order themes. These themes were aggregated into overarching dimensions, forming the foundation of our emerging framework. We describe the data structure and themes in Table 2. We completed data collection in 2021, when analyses no longer yielded additional first-order concepts and there was “nothing new to add in the databank” (i.e., theoretical saturation; see Alam, 2021, p. 18; Glaser & Strauss, 1967; Mathias & Fisher, 2022).

Data Structure.

We adopt a post-positivist epistemology (Lê & Schmid, 2019) combined with a critical realism ontology, as this approach allows us to recognize an objective reality while acknowledging that these phenomena can only be partially accessed through interpretation (a core tenet of critical realism). By combining post-positivist rigor (e.g., triangulation of sources) with critical realism’s focus on deep structures, we provide both empirical insights and theoretical advancement in a family firm’s adoption of a global identity over time (Hlady-Rispal & Jouison-Laffitte, 2014).

A Process Model of Mediating Reference Point Shifts in a Business Family

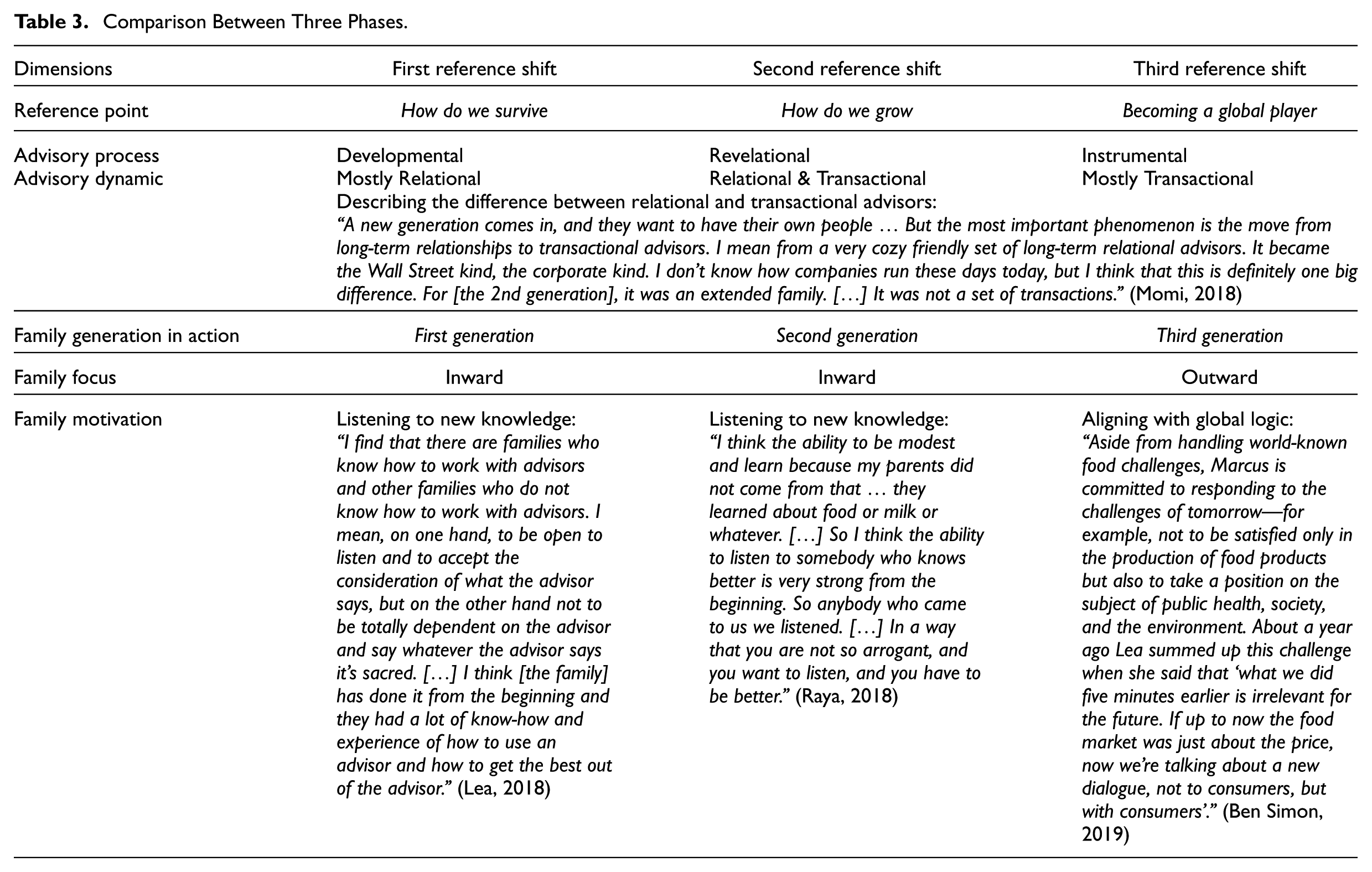

Our narratives revealed three phases of standardization at Marcus. We define standardization as the process of establishing formal policies, procedures, and globally accepted organizational models to control, standardize, and ensure consistency within the organization. Each phase, influenced by advisors, led to strategic reforms and the eventual establishment of new norms of standardization. Relatedly, we also identified the heterogeneity of advisors and the specialized roles they play, often working in concert, in the standardization process. We differentiate between the first two shifts and the last third shift: from two inward-focused reference points mediated by relational advisors to an outward reference point mediated by transactional advisors, as summarized in Table 3. It describes the data as “temporally ordered tables” which are “particularly useful, if not indispensable, to understand processes” (Cloutier & Ravasi, 2021, p. 123).

Comparison Between Three Phases.

The following section outlines the processes we observed across the three generations of Marcus’ history, with the first two generations similar in their focus on relational advisors and reference points. In contrast, the third generation introduced a shift toward transactional advisors and alignment with the global order. We begin by considering the family’s entrepreneurial style at the outset of its engagement with advisors, which we term pre-standardization. While we present our findings as linear, the process itself is recursive. The repeated application of each process leads to successive executions and results, layering and building upon the previous process.

The family initiated the engagement with advisors, who are both drivers of cognitive change and instruments of shifts already underway. However, our data revealed that this is interdependent on the type of advisor (relational vs. transactional), the generation (first, second, or third), and where along the reference point shift continuum the decision-makers are (prior to the reference point shift, moving toward the realization of the reference point). The relational advisors were primarily in the first and second generations. They were active drivers of cognitive change as they injected new information that shifted the reference point, thereby prompting sensemaking, and then enabled that shift to happen through the installation of standardized models. The transactional advisors, in turn, who were present with the third generation, acted more as instruments of the shifts underway as they brought legitimacy to them.

Pre-Standardization: Survival

We define the pre-standardization period as the integration of raw entrepreneurship and the family’s will to survive. We saw their raw entrepreneurship in their spontaneous, undisciplined approach to seizing opportunities and pursuing new ventures. In 1936, Dr. Richard and Hilde Marcus immigrated to Palestine from Germany with their 2-year-old son, Michael. Their daughter, Raya, was born soon after. The couple’s focus was to survive in this new land. In 1937, Richard gave up his academic career, and the couple bought a small farm and two dairy cows. As they knew little about dairy production, they sought advice on how to survive and sustain their livelihoods from other dairy owners and cheese producers. Hilde began making simple cheeses in her kitchen for the local area, thus founding Marcus. Richard and Hilde continued to work hard in a context where they defined success as firm continuity for the next generation.

In 1956, their son Michael, then 22, returned home from university in Switzerland. Only then did he recognize how his parents struggled to survive: I saw the pitiable state of the dairy and witnessed the daily struggle for existence … I could not leave my parents alone with their troubles (Michael Marcus, 2012)

In 1962, Michael brought home a white cheese from Europe, which they then copied and marketed. Unrecognized by the family, it was the famous Gervais cheese. A lawsuit from Gervais soon followed as they did not have permission to make the cheese. Richard, keen to explore opportunities to connect with external expertise and advice, turned the lawsuit into a know-how agreement with Gervais’s French branch. Michael began spending a month each year at the Gervais factories in France to continue to learn from them. Seeking external expertise and advice marked the beginning of the first phase of adopting a global identity.

Phase 1—Developmental: How Do We Manage?

During this phase, we recognize family and advisor mechanisms as knowledge-seeking and knowledge and standardization transfer. We define knowledge-seeking as the family’s willingness to seek knowledge and information from external sources. We define knowledge transfer as the process by which the advisor(s) educate and guide the family firm while allowing for local variations, to develop the family firm’s internal competencies. Standardization in the above processes refers to the search for and establishment of standardized organizational models. The Marcus family was open to outside experts on various production issues from the beginning of the young dairy. However, the influence of advisors on the family’s standardization began to emerge through the story of the First generation (G1) reaching out to Dr. Franzjosef Höfler, the CEO of the German branch of the French–German company Gervais.

In 1963, almost 30 years after founding the small family firm, Hilde traveled to the German branch of Gervais to try to switch the Gervais connection from France to Germany. Hilde had strong German roots—she felt she understood the people and culture better than those in France. Marcus’ financial position improved with the receipt of the German State’s reparations for the confiscation of Jewish property in Europe between 1933 and 1945. With the additional funding, Hilde first approached Höfler with a plea for help with know-how and to aid in buying new machines: On the first day Hilde asked me “I want you to help me … how can I do it? I want to buy machines for ice cream, and for the dairy, like packaging machines and so on”. (Höfler, 2018)

Hilde not only persuaded Höfler to help purchase machinery for the dairy, but he also offered further aid with technical know-how, production, and the products. Höfler described the G1 approach to management as exuberant and unfocused. The description of a raw and scattered way of G1 entrepreneurship influenced the way the firm introduced ideas: [The family] were hungry! They wanted to achieve something! They wanted to build something! They were creative! They had ideas! … At the beginning I had problems with him [Richard], because he was too … too spontaneous, too … how should I say that, too focused on what could be done at present, and quickly. (Höfler, 2018)

Höfler began visiting Israel and mentoring the family. His willingness to help the small family firm and the personal relationship he established with the G1 owners marked a new era for the Marcus family firm. Guided by Höfler, the collective knowledge structure of Marcus’ dominant coalition (DC; Richard, Hilde, and Michael) began changing how they interpreted and filtered their family business practices. Michael referred to this shift as: The stage of going big … Marcus learned two things from Gervais Danone [Höfler]: to manufacture sophisticated milk products and to think like a large concern. (1988, book chapter)

Firm survival had been a fundamental anchor around which the DC constructed meaning, understood their experiences, and made decisions. When Höfler began his visits to the family firm, he conducted an in-depth analysis of the firm and its environment. He found no strategic plan or focus: Everything they thought they could earn money with, they pursued. It did not always fit together … Richard said “I know so many dairies in Germany that produce processed cheese so we should do it too … there was never any planning, no management committees … how they would distribute their instructions to the employees, this had no structure” (Höfler, 2018)

In a country that lived under the constant threat of war, the prospect of environmental shocks kept the family focused on the short term. The family engaged in impulsive risk-taking with little foresight of the potential consequences. Höfler understood the present focus and the consequential lack of planning: They had never planned! They did not know whether tomorrow the next missile would come from Lebanon. Why should one think about the next five years in Israel? They were happy if they were still alive next year! (Höfler, 2018)

Höfler’s understanding of the DC’s current focus and analysis kindled compassion for the family’s plight. He became attuned to the family, helped define the firm’s future, and accelerated the standardization reconstruction process. In educating and guiding the family, Höfler encouraged learning, capacity-building, and the development of internal competencies. He shared context-specific expertise and skills to help the family firm improve efficiency, decision-making, and localized innovation.

Höfler promoted the adoption of standardized procedures and structures to reduce variability and enhance predictability within and across organizations. Transferring knowledge to the family firm includes establishing structures, planning, installing systems, providing discipline, and creating physical infrastructure. Höfler established structures and boundaries absent from the DC’s vocabulary. Standardized structures included defining family roles, developing cross-functional teams, and establishing a board of directors. Importantly, in establishing the board, Höfler noted the importance of instituting an environment of strategic planning: A board made sense because we were shareholders … [the family] had never had a board (laughs). For me it was clear, I said “now please, we have to strategize, we have to prepare plans” […] It was a different style of managing a company … one is not responsible only to oneself, but also for the whole company.

Höfler introduced advisors who aided the DC by installing systems: he brought with him other professionals from Gervais, including a production manager and his marketing manager [Günter Jacob]. Both advisors brought predefined best practices. Günter helped establish multi-year marketing plans, transforming Marcus’ thinking about new products. A former CEO described Günter’s influence on Marcus Group’s undisciplined entrepreneurial spirit. Günter complained about the Marcus people “jumping all over the place,” so he saw himself as a “policeman of ideas,” demanding structure and a religious execution: His [Günter’s] job is basically to be a policeman and make sure that we have a proper structure and a religious execution of decisions. His view was that we are not structured and that we are not consistent, or not persistent in our execution. So we go this way, and next week somebody comes and says I have a better idea and you move that way and that way and that way. (Gabi Dessin, 2021)

Günter subjected any new product development proposals to a rigorous empirical, market-based environmental scanning, believing that subjecting Marcus Group’s undisciplined entrepreneurship to structured management processes was a necessary and valuable step.

Höfler soon realized that providing Marcus with the know-how was insufficient. They also required additional physical facilities to house their assets, such as machinery, and to provide space for the know-how to function. Due to the long-term relationship with Gervais, Höfler partnered with Gervais to finance the necessary physical infrastructure. In 1974, Höfler helped build a new factory for milk desserts, with two primary outcomes: one, Gervais became a strategic partner with a role on the board of directors. Two, the strategic venture into the new category of milk desserts enabled Marcus to attain market leadership, a new market identity, and financial success, which generated the revenues to finance future endeavors.

Advisors leveraged the family’s openness to establish processes that directly enhanced the firm’s capabilities and resources, such as strategic planning, knowledge creation, and the formation of strategic alliance networks. Through these management structures, additional advisors were used to develop strategies for both the family and the firm’s development. In the early 1970s, there were very few advisors located in Israel. Consequently, the skills Höfler introduced were unheard of in their context, and Marcus built the organization to leverage them. The joint venture with Gervais, and later with Unilever, and the timely implementation of these technical management practices enabled Marcus to become a dominant national organization in its sector. In planning, Höfler shifted the DC toward a future focus. This moved the DC from a present to a future-focused reference point. He introduced the idea of short-term, mid-term, and 10-year plans. The practice of planning for the future became fully assimilated as the right way to manage, without managers even remembering how it started. CEO Gabi Dessin described how Marcus institutionalized the elaborate corporate planning process: Every 8–10 years, the management convenes a series of meetings over a year, usually at a location out in the countryside, isolated from the outside world. They take advisors from a global strategy consulting company to help them imagine how the world will look in ten years and how we want the company to look ten years later. At the end of the process, we produce a film of it to be viewed only by the management team, with the board of directors’ approval. Eighty percent of what we thought would occur in ten years happened. We have already gone through this process three times. It is obligatory, stretches the organization, and takes us forward. (SIM, Gabi Dessin, 2014).

These types of questions guided the DC in determining where to invest its funds. The structure and processes, budgeting, and product planning established during the strategic alliances with Gervais and later with Unilever improved Marcus’ management, production, and marketing capabilities. Höfler’s involvement with the firm occurred when Marcus was on the threshold of growth beyond the family’s capacity.

Phase 2—Revelational: How Do We Grow?

During this phase, we recognize family and advisors’ mechanisms, focusing on seeking to“make deals” and financialization, which we define as seeking financial opportunities and establishing financial structures. Michael (G2) extended the range of advisors and consultants. In the late 1980s, SIM, an Israeli consulting firm with ties to Harvard Business School professors, was brought in to work with Marcus, with this financial focus, seeking to increase firm value: SIM made a plan with the management team to reach sales of $100 million. One of the key strategies was to bring in new, young, talented managers. Michael and Raya (G2) wanted to find a way to ensure that the company would last a long time and become a leading company in the market. At that time to say in Israel that a company will become $100 million was something … we were operating at $50 million, and the goal was to double the business. (Moti, 2021)

These external advisors financialized Marcus’ corporate governance, emphasizing financial revenue and profit objectives and targets; Marcus’ managers institutionalized these changes as organizational norms. In the mid-1990s, Michael approached a local strategic consulting company, led by Yossi Rein, to evaluate Marcus. From the outset of the relationship, advisor Yossi described how, after careful analysis, he had to confront Michael as he was reluctant to disclose financial information: The family was blind regarding financial understanding, their real assets. Michael went away and said “no, we can’t expose that, it is a secret,” so I said, “fair enough, just find somebody else.” Three months later he returned. I had to sign a nondisclosure agreement, … but Michael came and said “OK we surrender; you can look into the business.” (Yossi Rein, 2021)

Yossi felt that the confrontational encounters had the most significant impact on the relationship. If the client’s understanding of an issue shifted due to the confrontations, this was their best contribution to the client. Yossi noted that the results of their analysis often differed from the family’s perceived reality. During an explosive meeting with the family, Yossi explained that they had $100 million in cash. The family insisted that Yossi was incorrect; however, when they tried to verify this with their CFO, they quickly realized Yossi was correct. Unlike the slow, gradual changes in thinking implanted by Höfler, the cognitive reference points pivoted toward financial objectives and deal-making, such as acquisitions and strategic partnerships. As Raya described: Yossi suddenly said “you have too much money.” We were shocked. When Bulite came on the map I understood that we needed to buy it, not because I understood so much in numbers but because I listened to Yossi. It changed the history of Marcus. (Raya, 2018)

While Yossi confronted the family early in the relationship, his continued role as a long-term relational advisor permitted him to engage in an ongoing confrontation with the family. Yossi imported standardized methods for financial management, which he said were missing from the firm: Michael doesn’t have a clue about running the money, but he knows very well how to run the factory operationally. But the family business is money. (Yossi Rein, 2021)

The insights into the balance sheet and the financial tools Yossi brought to the firm changed their self-perception and mediated a new reference point. The family no longer saw itself as a small family firm in survival mode but instead realized they were a resource-rich and powerful entity with many options: Raya said “you suddenly showed me the stars.” It was a moment … suddenly they discovered that they were sitting on a pile of money and now had options. We said “you can buy Bulite, you can buy a bank, the banks were for sale, you can buy anything! You are the biggest holding cash in Israel because nobody has 100 million dollars.” (Yossi Rein, 2021)

Motivated to secure the family firm’s survival beyond the next generation, Michael worked with Yossi to develop a portfolio of strategic partners. Yossi and Michael went shopping in London (United Kingdom) for strategic partners. Yet, Michael did not trust the next generation and wanted strategic partners aligned with each operating business to ensure the firm’s success. Under Yossi’s guidance, the family began to engage advisors on family issues beyond the firm’s boundaries. The extended family also needed managing. Long-term engagement with local and international family relational consultants and renowned North American leaders in the field ensued. As Yossi explained, he confronted the family to recognize the next generation(s): You can’t treat the next generation as kids anymore and give them 10,000 shekel every Chanukah, as a sort of family acknowledgement … this is a disgrace! They have kids, you have grandkids. I don’t know anything about family psychology, but it looks sick. And this is when they brought in Smadar [family advisor] to assist with the psychological issues. (Yossi Rein, 2021)

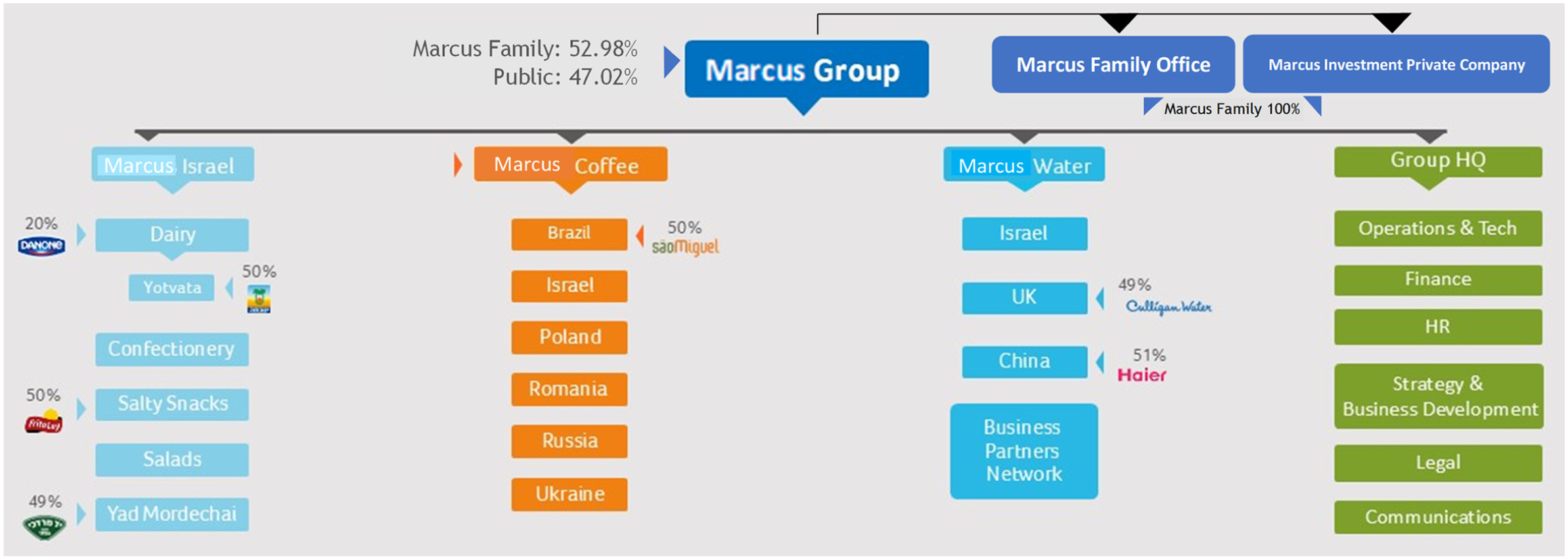

The family’s seeking to maximize value and advisors’financializing mechanisms helped to establish holding and investment companies along with a family office (see Figure 2). The structure was overseen by the family office advisor, Rubi, whose discretion, according to Raya, was “mute as a sphinx.” Based upon cash flow from the core operating business, the investment company permitted the two G2 owners to cooperate on a variety of personal projects that reflected their preferences. The establishment of the family office enabled Marcus to become a business family, with a range of business interests beyond the firm and a more detached relationship with the operating company. The family office’s coordination of these diversified interests marked a clear distinction between family and firm and led to a distancing of family members from the operating company.

Marcus group corporate structure.

Phase 3—Instrumental: Becoming a Global Player

During the third phase, we recognize a shift in focus from inward to outward, aligning with a WS identity, as family and advisor mechanisms focus on seeking and providing legitimacy. With legitimization, advisors aligned organizational practices with international norms, thereby gaining legitimacy in the global arena. At the end of 1999, as G3 began to take a leadership role within the firm, the types of advisors engaged by the family began to change. Whereas previously, the family had relied on long-term relational advisors, such as Höfler (36 years) and Günter (30 years), they began instead to engage advisors for shorter-term interactions. As Yossi noted: When Lea (G3) came into the picture, she needed more glamorous names and more than an Israeli brand. We are just an Israeli low consulting firm. Lea needed a brand. (Yossi Rein, 2021)

Marcus had matured into a national brand, generating substantial free cash flow; as Yossi suggested, “we have enough money to buy EL AL” (the national airline). However, Marcus’ growth options remained limited. The strategic alliances with Gervais and Unilever in the dairy and ice-cream industries were exclusive and authorized only for the Israeli market.

Bulite, an international public firm with product lines focused on chocolate and coffee, had twice Marcus’ revenue yet was in poor financial condition. The firm approached Marcus seeking a bailout. However, Michael and Raya, the two majority shareholders, reached an impasse with different visions for Marcus’ future. Michael was pragmatic and saw the potential for growth, while Raya’s ethos was producing high-quality, nutritious food. She perceived Bulite as a manufacturer of non-nutritious confections. Wishing to retain Marcus’ dairy legacy, Raya was adamantly opposed to the potential merger and threatened to withdraw her shareholding, which would severely erode the firm’s capital structure by reducing its equity base by 50%. As described by Raya: I started to be aware of health. Many years before anybody even talked about it, when we bought Bulite we had this—I was begging, let us do these cookies with butter and whole wheat. Nobody listened, and I didn’t have the strength, and my brother only hears about health, he said it’s all phony. (Raya, 2018)

Michael and Raya also differed about whether Marcus should remain a private family firm to retain its traditional familial culture. The impasse reached a peak when several consultants advocated for the Bulite acquisition, which succeeded, heralding a new era in Marcus’ growth. McKinsey, a prominent Boston-based management consultancy, was mandated to structure the merger. Subsequently, McKinsey recommended a multi-divisional organization structure for Marcus. Other advisors assisted in establishing a corporate structure for a business family. The decision engendered the “birth” of the G3 business family. A business magazine reported: The Marcus company, unlike other family businesses, was able—with the help of a battalion of family consultants—to peacefully pass the management wand to its third generation, led today by Michael’s daughter … The family’s openness regarding the need for a rational arrangement of the family relationships was well integrated with their reliance on Rubi Haimo as an executor who had brought her personal capabilities to the process. (Family Wealth, 2011)

Engaging McKinsey, a prestigious global management consultancy, shifted the rationale for engaging advisors from local to global. McKinsey offered status and legitimacy. Momi, the CEO at the time, described how the new advisors differed from the previous advisors, who mediated the first two reference point shifts: From a cozy friendly set of long-term relational advisors, it became “Wall Street” advisors. For Michael, the other advisors were an extended family who came to family birthdays. It was not a set of transactions. (Momi, 2018)

While the transactional advisors began with an analysis of the firm, they were no longer attuned to the family as the relational advisors had been. Michael referred to the transactional advisors as his daughter’s type: My daughter is using advisors all the time. Some I like. I never liked McKinsey. I have a word for that. It’s mother-xxxxxxx. They take a lot of money, but their basic knowledge—they know to look in the computers worldwide and find other places similar and make their analysis. But they are 25-year-old guys [who] never worked, and they come to tell you what to do, and when you look like this because it’s five million dollars, it’s crazy.” (Michael, 2018)

The confrontation with the McKinsey advisors divided the family itself, as Michael and Lea sided with their advice to merge the private historical Marcus with the publicly traded Bulite, while Raya was against this advice: I really didn’t understand it. Young people, the young people from university but they don’t know life … I said things that I knew were the truth but I’m not a professor, I couldn’t bring numbers for it but I knew this is what it needs to be. I tell you, because I didn’t understand and I was fighting with them because they were analytically better … I said it’s totally different and they were no, no, like I’m stupid … and nobody listened to me because I was the only one in the management. (Raya, 2018)

This confrontation led Raya to sell her shares in Marcus and exit the family firm after the merger’s announcement. She blamed the advice from McKinsey, demonstrating the possible negative influence outside advisors might also have: I tell you, the first time in my life that I understood the advisor is not always the best is with McKinsey, when they did the big work and I was very disappointed. (Raya, 2018)

The transactional advisors’ role shifted to become a tool for the DC, and several interviewees criticized McKinsey for echoing the DC’s wishes. McKinsey would orient their recommendations to the goals of the DC; as they were so prestigious and so costly to engage, it was “hard not to agree with whatever the management wanted” (Mili, 2021, interview). McKinsey’s role conferred legitimacy on the DC’s goals and decisions, strengthening managerial identification with the capitalist class.

The relational advisors had educated the family on harnessing their raw entrepreneurial energies to establish and manage a thriving enterprise with an inward focus on the family. In turn, the transactional advisors provided benchmark data on international companies, aligning with an outward focus. As an international company, Marcus required more data on the world around it. Marcus learned to use this benchmark data to evaluate its own operations. Lea (G3) valued this global data as a managerial tool, which led to her positive opinion on the transactional advisors, opposing that of her father’s: I love to work with the McKinseys of the world. They have so much experience from other companies. It’s much less expensive to learn from other people’s mistakes, no matter how much we need to pay, as long as they bring those benchmarks into our companies: data and benchmarking. The Günter’s were about their skill, thinking, and marketing. The McKinsey’s of the world work with the best-in-class companies. They have databases on everything. They can hire the best in class. We are an international company now, and competing in the world requires more and more data. (Lea, 2018)

The decision to go to international markets and “to take on partners” was implanted by Yossi, but Lea (G3) admitted that Bulite’s potential to become international is what attracted her support of the merger: The real thing that made us want this company Bulite is that we suddenly saw the opportunity to be international. So our company is … the people were—I call them local, not entrepreneurial. They didn’t have even the spirit. (Lea, 2018)

The role of advisors shifted. The first task was external checks and balances on the firm’s decisions in the eyes of the outside world to enhance legitimacy: But it’s just sometimes we use it as a structure to minimize the risk of those what might be bold moves. So it comes with a lot of responsibility, but advisors are part of our way of life … I’d prefer someone to work with the big and the best in the world. And then I will bring entrepreneurship or a different way of thinking, and someone will do the check and balances. (Lea, 2018)

The second task was to provide an alternative objective opinion. For example, using the Hay Consulting Group for the merger: Hay Group, we employed them on the merger because we needed due diligence on the two companies’ culture because most mergers fail due to cultural differences. We wanted to check what’s the best way and for us, it was big money for the family, the biggest ever, and it’s more than just the money to buy a larger company than ours. So we brought Hay Group to do a due diligence on culture because the Marcus people said we are very different from the Bulite people. No way. The due diligence showed that we had the same culture. (Lea, 2018)

In her 2021 presentation of the new corporate vision “Nourishing for a better tomorrow,” Lea recounted the firm’s corporate assets. It consisted of layers applied by previous mechanisms and advisors. These layers included being open to outsiders (brought in by G1), good manufacturing standards and procedures (brought in by Höfler during the first reference point shift), and having outside partners (introduced by Yossi during the second reference shift): Our method: looking inside-out and outside-in to look ahead. We have important assets: Global alliance, Good manufacturing—sound and agile supply chain, Trusted brands, Trusted people and partners, Care for people, Inclusivity, Partnerships with all stakeholders and communities. (26.7.21, new vision)

The vision itself, “nourishing for a better tomorrow,” was a global vision for the whole of humankind, adopting a global reference point, making global issues like public health, society, and the environment part of its purpose: There is so much we can do with food and with the spirit of nourishing, help people become healthier and live longer together, help people live up to their potential and feel fulfilled and happier, make families closer and relationships grow, make communities thrive and be proud of their beliefs and traditions—nourishing for a better tomorrow. (26.7.21, new vision)

Following a lengthy succession process, Lea was appointed Marcus’ Chairperson in 2001. With the shift toward transactional advisors, followed by an acceleration in the firm’s international activities, Lea sought assistance from the new advisors to shift Marcus’ public image toward a more global, outward-looking profile. Human Resources and executive search firm Hay Group was mandated to perform an organizational culture audit. A United Kingdom marketing agency, Brand Engineers, was mandated to evaluate Marcus’ brand portfolio. A partnership was established with a Texas-based private equity firm to assist Marcus with acquisitions in new overseas markets. When asked about the difference between how advisors were used early on compared to today, Momi described that Lea brought in a new style of dealing with advisors, explaining the shift in hiring prominent global consulting groups: This was very unusual in Israel at that time in the 20th century to hire McKinsey if you were not the Ministry of Defense or the Prime Minister, and the same with the Hay Group and later we also used a company called the Brand Engineers, a British company.

Under Lea, management completed the Marcus–Bulite merger, making Marcus an international publicly traded group and Israel’s second-largest food company. McKinsey accompanied the merger. Marcus entered the North American food market in 2005 by acquiring a 51% stake in the American Mediterranean salads and dips company, Tomato, as yet another step in realizing the Group’s international expansion strategy. Acquisitions of several coffee companies in Poland, Brazil, Russia, and the Balkan states contributed to Marcus Coffee’s international growth. In 2008, Marcus signed a collaboration agreement with TPG Capital, one of the largest private equity investment firms, for investment by TPG in Marcus Coffee (25.1%). In the United States, Marcus Group signed a 50/50 partnership agreement with PepsiCo for Tomato, to develop, manufacture and market refrigerated dips and spreads in the United States and Canada. In 2011, Marcus Group signed a deal with the Haier Group, the Chinese home appliance and consumer electronics giant, to establish a joint venture in China for the home water solutions market. The new company, Haier Marcus Water, launched its first products in the Chinese market the same year. As a coda to our case findings, Marcus’ stock price has declined consistently since 2021 and, at the time of writing, has reached an all-time low. The third-generation chairperson, Lea Marcus, states that the solution to the problem was “to erase the family DNA from the firm.” This sentiment seals the complete transformation from the familial to the global-formal. Figure 2 depicts the current Marcus business family structure and the Marcus Group corporate structure.

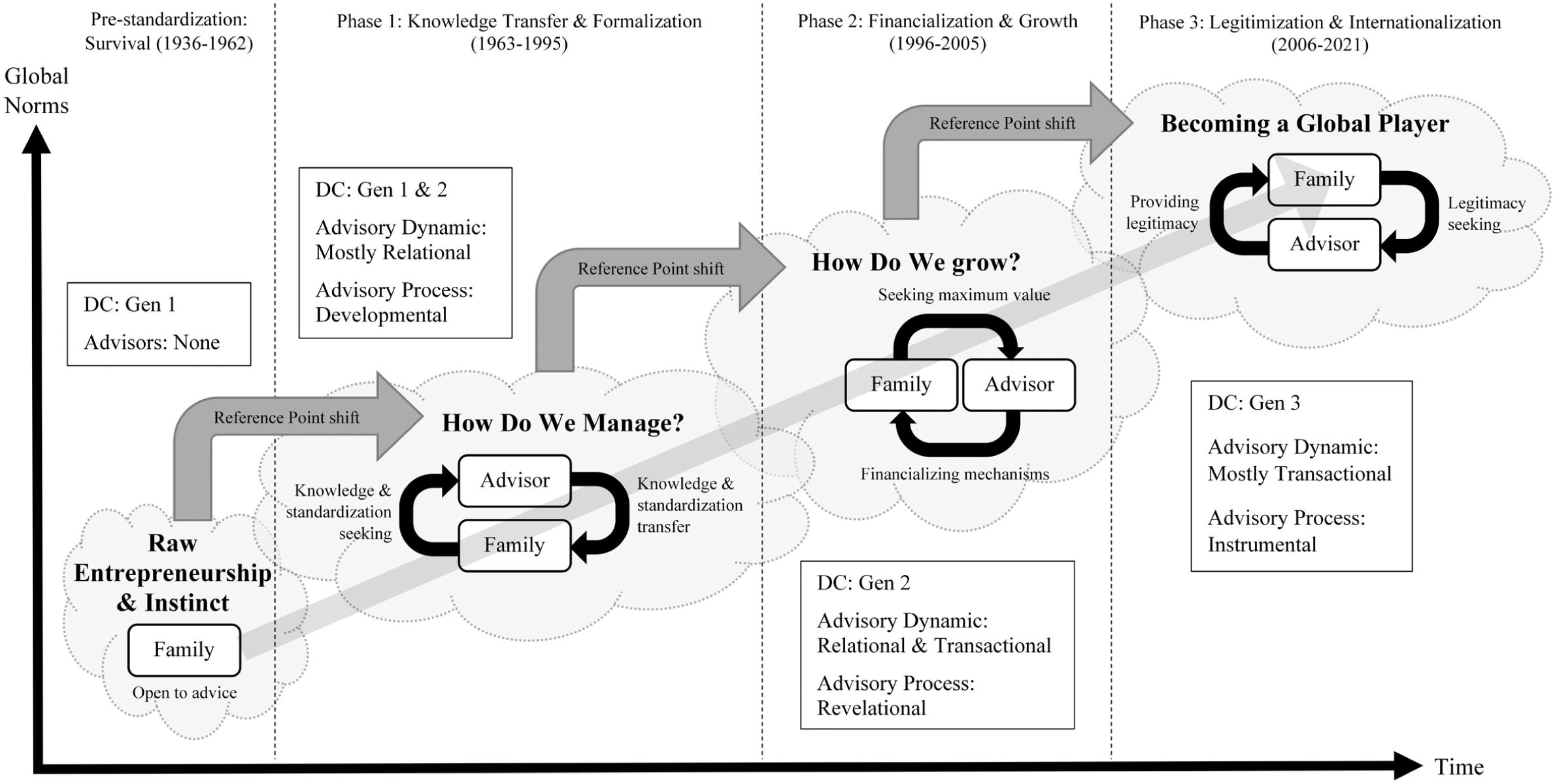

Given the preceding discussion, Figure 3 illustrates the process through which advisors progressively standardize the family firm to align with global norms and values. The figure captures our three distinct phases of advisor-family engagement, each contained in a cloud denoting the family’s prevailing reference point. Underlying each reference point shift is an evolving advisor engagement dynamic, wherein reciprocal arrows indicate the bidirectional influence between advisors and the family. Notably, the actors’ positional configuration changes across phases (with advisors leading in Phase 1, more collaboration in Phase 2, and the family leading in Phase 3), signifying a gradual transition toward increased organizational sophistication and family autonomy. This developmental trajectory is reinforced by a light gray upward-sloping arrow spanning the figure, symbolizing both the family’s deepening engagement with advisory processes and its broader movement away from emotionality and toward institutionalized, globally recognized practices. Figure 3 further delineates the dominant coalition (in terms of generational power), the advisory dynamic (relational vs. transactional), and the advisory process (progressing from developmental to revelational to instrumental) in each phase. Taken together, these elements illustrate how the family’s growing capabilities and the advisors’ evolving roles jointly shaped the trajectory of the advisory relationship over time, leading to corresponding shifts in reference points and culminating in a pattern of increasing firm-level standardization and alignment with global business norms.

Standardization and reference point shifts over time.

Discussion

Our findings depict the role of advisors and management consultants who mediate shifts in a business family’s reference points through the adoption of standardized corporate and organizational models. Theoretically, we examine how the WS perspective addresses emergent critiques that characterize family firms as emotionally tied, with our primary focus on advisors and management consultants mediating business families’ reference point shifts through standardization. We then consider our process findings, illuminating the cultural origins of corporate models and the actors who drive business-family standardization. Furthermore, we outline the boundary conditions encompassing WS insights and how exploring these boundaries may provide opportunities for future research concerning business families’ acquiescence and resistance to the diffusion of WS management models. We demonstrate in detail Strike and Rerup’s (2016, p. 881) suggestion that an outside advisor can help family sense-makers to “slow down and doubt their knowledge,” enabling them to generate new understandings. We add to the theorizing on reference point shifts in business families, showing that a small, first-generation firm can be open to outside knowledge and transform. The standardization and cognitive shifts of Marcus begin with the initial advice to Marcus’ mom-and-pop dairy firm. We find that Marcus’ advisors and consultants increasingly standardize the firm with successive sanctioned corporate organizational models, through three phases, which we label (i) Developmental: How can we manage? (ii) Revelational: How can we grow? and (iii) Instrumental: Becoming a global player. Outside advisors with models originating in the evolution of Western management models over the last several decades influenced Marcus’ operational repertoire, extending the family’s knowledge structure (Nason et al., 2019) and culminating in the current Marcus family’s global vision for the firm, with a mission of “nourishing for a better tomorrow.” In this view, we focus on content mediated through three principal advisors across three generations of family leadership. In this regard, we contribute to Nason et al.’s (2019) call for qualitative research on reference point shifts and the processes that enhance them, carried out by families on one side and advisors on the other. The family invites the advisors in, while advisors bring along the best practices of their time, serving as “instruments of valorization … like handrails on already existing ladders” (Magrelli, Rovelli, et al., 2022, p. 19). While Magrelli, Rovelli, et al. (2022) examine the mediating role of advisors in relational succession issues across generations, we show how they mediate reference point shifts through standardization. We show in detail how business families “might eagerly embrace external advisors and capitalist class membership,” as suggested by Jaskiewicz et al. (2019, p. 917), advancing a generalizable theory of business-owning families’ reference point shifts.

We contribute to a better understanding of how family generations differ in their focus (Magrelli, Rondi, et al., 2022; Magrelli, Rovelli, et al., 2022). We show the conflict between Raya, the second generation who was against merging to become a publicly traded firm, and so choosing the traditional past, whereas Lea, the third-generation new leader who was “trying to create its own idea of future by detaching itself from the senior generations’ past” (Magrelli, Rovelli, et al., 2022, p. 19), and preferred a global-publicly traded firm. Answering Jaskiewicz et al. (2019, p. 917), who wonder “what happens when these families fail to reconcile their competing reference points?”, we show that competing reference points can lead to a split within the family firm and a break from family DNA.

We show how WS models filter into the business family and the firm’s knowledge structure, thereby shifting the family members’ reference points for the goals pursued in the subsequent phase of corporate standardization. Thus, in contrast to the emotional perspective emphasizing the unique, traditional character of the family firm, we contribute to WS theory, which provides an overarching sociological account of the transition of older social forms toward a model of corporate organization comparable to a broad range of contemporary “managed” organizations (Bromley & Meyer, 2015, 2021). We theorize advisors and management consultants as carriers of WS logic in establishing standardized corporate organizational models. Viewed over 6 decades of Marcus using management consultants, we can depict the layering of often contradictory organizing models.

Developmental: How Do We Manage

In the first phase, through the agency of a board member advisor, Höfler initiated the standardization process. Höfler had a distinguished career as an executive in a family-owned European multinational enterprise. Höfler and his colleagues implemented a strategic planning system and a disciplined approach to marketing, accounting, and recruiting key executives. As an executive of a European family business, Höfler is an essential carrier of (then) current models of best-practice corporate organization, such as top management planning (Steiner, 1969), corporate strategy (Ansoff, 1965), and planning systems (Ansoff, 1977). These strategic planning models enable the rational allocation of financial and managerial resources and are subject to individual business units’ systematic accountability (Fligstein & Freeland, 1995). Höfler and his associates transplant the prevailing strategic planning model of corporate organization into receptive Marcus, whose pre-standardization reference point shifts toward a strategic planner focused on better management, thereby setting the stage for the firm’s flourishing in the domestic Israeli context.

However, consistent with fads and fashions in management consulting (Abrahamson, 1991), strategic planning models fell from favor due to their internal focus, characterized by a rigid logic of the separation of planning and doing, where detached upper management passes down a set of objectives and plans to a disempowered middle management (Mintzberg, 1994). Moreover, under the influence of strategic planning, executives perceived themselves as a corporate elite (Useem, 1980) and were inattentive to shareholder interests (Useem, 1993).

Revelational: How Can We Grow?

Given the myopia of strategic planning models that privileged top management, a rival dominant corporate organization model emerged in the form of the finance conception of the firm (Fligstein & Freeland, 1995). This model encouraged the emergence of investor power by large institutional shareholders such as insurance companies, pension funds, and money managers (Useem, 1993), and emphasized maximizing shareholder value through hostile takeovers, restructuring, and leveraged buyouts. Once again, business families resisted these corporate models in the United States (Palmer & Barber, 2001) and Europe (Franks et al., 2012), but eventually families began leveraging their concentrated ownership to improve their financial performance (Anderson & Reeb, 2003; Villalonga & Amit, 2006). In contrast, the finance conception of the firm was uncommon in Israel. Yet Marcus adopted the model under Israeli consultant Yossi Rein’s guidance, who had worked for the Dutch multinational Philips before becoming a consultant, and shifted from strategic to financial management. This shift in reference point prompted the acquisition of Bulite, a company twice Marcus’ size. This shift prompted a period of searching for strategic partners in Europe, establishing a family office, and setting up a private holding company.

Instrumental: Becoming a Global Player

The decision to acquire Bulite also ushered in an era of internationalization in which Marcus became a geographically dispersed enterprise expressing an expanded vision of its mission. In this regard, we contribute to the growing body of literature on family firm internationalization (Arregle et al., 2021) by uncovering, in significant detail, the antecedent organizational learning required for international operations. A third reference point shift occurs with the rise of G3 Lea Marcus as the Marcus Chairperson, who emphasizes the role of management consultants in legitimizing high-risk strategic alliances in pursuit of a global vision.

The internationalization process unfolded during an apotheosis of economic globalization, which Marcus followed under the guidance of the elite U.S. consultancy firm McKinsey. In this phase, Lea adopts a model of a global visionary player linked to corporate social responsibility. Specifically, Marcus commits to a global vision beyond food production. Lea engages with global issues such as public health, clean water, nutrition, and sustainability, under the expressed mission of “nourishing for a better tomorrow.” This vision precisely demonstrates what Bromley and Meyer (2015) described as “expanded purpose.” It is insufficient for Marcus to be efficient and profitable. Consistent with the WS’s perspective, an institutionally standardized Marcus must have a cultural and moral purpose to be an appropriate corporate actor across multiple countries.

The reference point shifts also align with the transition between three generations of the Marcus family. The pre-standardization and the first shift to “How do we manage?” are mainly executed while the first generation holds the shares; the second shift to “How do we grow?” occurs with the second generation; and the third generation initiates the last shift to “Global player.” While the first generation mainly invites relational advisors (see Figure 1), the second generation mixes relational with transactional, and the third generation primarily works with transactional advisors, aligning with the growing standardization over time. The shift of WS perspective changes the survival-chaotic-emotional founding era reference point to a global-standardized reference point in the third generation. When Marcus’ stock price reached an all-time low during the writing of this study, Lea Marcus issued her “erase the family DNA” assessment, which sealed the transformation from the familial to the global firm. Implanting corporate planning, financialization, and corporate social responsibility necessitates organizational elaboration and complexity. Apart from diminishing traditional goals of the family firm, such as intrafamily succession and emotional attachments, the introduction of professional management and management consultants incorporates externally socialized identities into the organizational structure.

Contribution

Leveraging our confidential access to an Israeli multinational enterprise, we contribute to calls for qualitative research on the process of reference point change (Nason et al., 2019). Through a three-generation case study, we identify dramatic shifts in reference points—from survival to becoming a global player with a mission to nourish the world. The shift is from an inward focus to an outward one, and from an emotional, particularistic start to a formal, global identity. Second, we contribute to the advisory literature on family firms (Strike et al., 2018) by showing the multifaceted processes and mechanisms that families and advisors use and how they change over time. Our longitudinal data show how advisory engagements and processes correspondingly evolve as family firms standardize, which augments the mostly cross-sectionally based literature on family firm advisors. We also show how different generations of the family use advisors differently: from knowledge-seeking and mediated sense-making to legitimacy-seeking. Third, we draw upon the WS perspective, depicting a business family that is upward striving (Shinkle, 2012), adapting standardized business best practices while simultaneously aiming to sustain a profitable, high-growth enterprise and pursue a virtuous global identity across multiple geographies.

Limitations