Abstract

We examine how entrepreneurs’ use of cognitively complex language—language that involves nuance, differentiation, and comparison—influences funding decisions of early-stage investors. Our theorizing builds on the notion that individuals interpret language as a social signal and attribute another person’s language use to that person’s general dispositions. On this basis, we surmise that investors perceive an entrepreneur as more cognitively complex—that is, engaging in more nuanced and differentiated thinking—the more the entrepreneur uses cognitively complex language. Arguing that perceived cognitive complexity matches investors’ prototypical construals of entrepreneurial competence, we hypothesize a positive relationship between an entrepreneur’s use of cognitively complex language and the investment amount they receive. Drawing on our theoretical framework, we also argue that signaling cognitive complexity has a decreasing marginal effect, and that elite education functions as a credibility signal, amplifying the association between cognitively complex language and investment amount. A field study of 547 actual investment pitches and a randomized experiment with 240 professionals support our ideas. Our study introduces a more nuanced portrayal of complexity in entrepreneurial communication, accentuates the role of entrepreneurs’ signals of cognitive dispositions, and introduces the concept of cognitive complexity, and linguistic displays thereof, to entrepreneurship theory.

Introduction

A key question in the entrepreneurship literature is how early-stage investors pick the ventures they support and how entrepreneurs’ communication influences investors’ funding decisions (Chen et al., 2009; Kalvapalle et al., 2024; Petty et al., 2023; Zacharakis & Shepherd, 2001). Consensus in this literature—and a canonic stance in entrepreneurship education—is a general warning against complexity in entrepreneurial communication. In fact, a substantial body of literature cautions entrepreneurs to avoid language that may be difficult to grasp when pitching their ideas (e.g., Daly & Davy, 2016a, 2016b; De Villiers Scheepers et al., 2021; Spinuzzi et al., 2014). Complexity creates ambiguity and cognitive load, making messages less accessible, memorable, and impactful (W. Guo et al., 2021; Heath & Heath, 2007). As Kahneman (2011, pp. 62–63) suggests, “anything you can do to reduce cognitive strain will help […]. If you care about being thought credible and intelligent, do not use complex language where simpler language will do.” Ultimately, complexity seems poised to make it harder for investors to see a new venture’s value and invest in it (e.g., Clark, 2008, p. 269; Clarke et al., 2019, p. 339).

And yet, is complexity in communication indeed always dysfunctional in entrepreneurial pitches? We believe that it is pivotal for entrepreneurship research to critically examine this assumption. In particular, professional investors are cognizant that entrepreneurship is essentially dynamic, uncertain, and complex (Sarasvathy, 2001), as new ventures typically emerge in dynamic and evolving environments (Aldrich & Fiol, 1994; Tushman & Anderson, 1986), inherently characterized by multifaceted challenges, intricate interdependencies, and an “unstructured technological dialogue” (Monteverde, 1995, p. 1624) where dominant categories and vocabularies are only emerging (Kaplan & Tripsas, 2008). Thus, investors may well respond unfavorably to communication that overlooks or oversimplifies these complexities. Indeed, ample qualitative evidence—including from interviews conducted in preparation of this study—indicates that investors seek entrepreneurs who demonstrate a sophisticated understanding of and an ability to manage complexities (Baron, 2006). In other words, by showcasing complex thinking through their communication, entrepreneurs could enhance their and their ventures’ appeal to investors.

In this article, we develop a more nuanced perspective on complexity in entrepreneurial communication. We focus on how investors process elements of entrepreneurs’ communication in a funding pitch as signals when evaluating a new venture (Bafera & Kleinert, 2023; Malmström et al., 2017). We study how investors make dispositional attributions about entrepreneurs based on the entrepreneurs’ use of what we label cognitively complex language, and how these attributions ultimately affect investors’ early-stage investment decisions. Drawing from research on cognitive complexity—that is, an individual’s degree of nuanced and differentiated thinking (e.g., Scott, 1962)—we define cognitively complex language as words that reflect nuance, differentiation, and comparison (Graf-Vlachy et al., 2020), and we propose that investors perceive an entrepreneur’s use of cognitively complex language as a signal of cognitive complexity (Malmström et al., 2017; Trope, 1986). Arguing that perceptions of cognitive complexity align with investors’ construals of the “prototypical entrepreneur” (Davis et al., 2017, p. 96), we then hypothesize a positive relationship between entrepreneurs’ use of cognitively complex language and the investment amount they receive. Based on signaling theory in entrepreneurship research (Bafera & Kleinert, 2023; Kalvapalle et al., 2024), we also argue that signaling cognitive complexity has a decreasing marginal effect. Finally, we surmise that an entrepreneur’s elite education signals credibility (Ko & McKelvie, 2018) so that it amplifies the association between the entrepreneur’s use of cognitively complex language and investment amount. We find support for our ideas in a field study of 547 actual investment pitches, and provide causal evidence for our central premises using a randomized experiment with 240 professionals.

This article is the first in entrepreneurship theory to study linguistic signals of cognitive complexity—a central concept in psychology and increasingly also in management research (e.g., Graf-Vlachy et al., 2020; Malhotra & Harrison, 2022). Particularly, we take the “investor vantage point” (Kalvapalle et al., 2024, p. 571) and make three important contributions to the literature on a cognitive view of signaling theory in entrepreneurship research (Bafera & Kleinert, 2023; Drover et al., 2018). First, we challenge the overwhelmingly negative portrayal of complexity in entrepreneurial communication. Established theory in this regard—echoing the broader literature on the dysfunctionality of language complexity (e.g., Adler, 2012; W. Guo et al., 2020)—conceptualizes investors primarily as individuals who seek to minimize cognitive effort and, in turn, focuses on the negative implications of cognitive load introduced by language complexity (Bushee et al., 2018; W. Guo et al., 2021; König et al., 2018). We, in contrast, build on recent contextualized understandings of communication complexity in management (Crilly et al., 2016) and audiences’ processing of entrepreneurial pitches (Falchetti et al., 2022). In particular, we consider investors as knowledgeable audiences who expect that entrepreneurs acknowledge complexity and who, in turn, respond favorably to signals of nuanced and differentiated thinking in entrepreneurial pitches. More specifically, our article develops and empirically corroborates a conceptual framework of how investors compare an entrepreneur’s linguistic signaling of cognitive complexity to their prototypical expectations. Second, we argue and show in our field study that using such language has decreasing marginal effects: approaching investors’ prototypical expectations is more beneficial than surpassing those expectations. As such, we contribute to the discussion of “optimal quantities” of signals in entrepreneurship research (Bafera & Kleinert, 2023, p. 2440). Third, we examine how cognitive complexity interacts with the entrepreneur’s educational background. Signaling theory has only recently begun to acknowledge the role of language-based signals (Steigenberger & Wilhelm, 2018). Specifically, recent studies have highlighted that language includes rhetorical signals that can be effective, especially in combination with other signals (Chandler et al., 2024; Steigenberger & Wilhelm, 2018). We add to this emerging conversation by demonstrating that, in addition to rhetorical signals (i.e., characteristics of language that appeal to modes of persuasion), linguistic signals (i.e., structural characteristics of language) also influence investors. In addition, we show how these linguistic signals interact with more traditional signals, specifically “elite” education. Finally, we make two noteworthy methodological contributions. We introduce Graf-Vlachy et al.’s (2020) measure of cognitively complex language to the entrepreneurship literature, and we demonstrate that investors develop perceptions of cognitive complexity from linguistic signals in a randomized experiment. Therefore, our study responds to recent calls for experimentally grounded theorizing on signaling, especially in entrepreneurship research (Bafera & Kleinert, 2023; Drover et al., 2018).

Entrepreneurial Behavior and Investors’ Funding Decisions

A vibrant scholarly conversation revolves around the question of how early-stage investors (we use “investors” as shorthand) deal with notorious information asymmetries when processing the signals that entrepreneurs send as part of their funding pitch (Huang & Knight, 2017; Kalvapalle et al., 2024). Funding pitches constitute a particularly important opportunity for investors to learn about and assess investment opportunities (Clark, 2008; Zott & Huy, 2007). Investors listen to entrepreneurs present their business idea, their team, and themselves (Brooks et al., 2014; Mason & Harrison, 1996). In the questions-and-answers section (Q&A), investors can ask questions and potentially start investment negotiations (Kalvapalle et al., 2024). Overall, entrepreneurs’ pitches significantly impact investors’ funding decisions (Ciuchta et al., 2018; Kalvapalle et al., 2024).

Beyond the substantive information provided in a pitch, investors receive signals about the ventures’ and entrepreneurs’ less manifest, difficult-to-observe characteristics that they consider vital for the success of a new venture (Bafera & Kleinert, 2023). Investors face systematic challenges since information known to the entrepreneur may be hidden to them (Colombo, 2021), and because information regarding future developments is inherently incomplete and historical data are essentially useless to predict dynamic outcomes in new markets (Aldrich & Fiol, 1994; Huang & Pearce, 2015). Therefore, investors rely on social cues or signals (Colombo, 2021; Huang & Knight, 2017). Notably, scholars of entrepreneurial pitches use the term “signal” to denote any observable behavior by entrepreneurs that investors may use as a mental “shortcut” (Fiske & Taylor, 2017, p. 188) to alleviate interpretive uncertainty and overcome the inherent lack of information (Bafera & Kleinert, 2023; Connelly et al., 2011). Thus, “signals” can include costly signals, such as affiliating with high-status individuals, spending money on advertising, and acquiring academic degrees (e.g., Jin et al., 2017; Nagy et al., 2012; Vanacker & Forbes, 2016) as well as more “social-symbolic” and less costly signals such as entrepreneurs’ language and the pitches’ choreography (Garud et al., 2023; Kalvapalle et al., 2024; Zott & Huy, 2007).

Investors rely strongly on signals that relate to entrepreneurs’ dispositions—their general personality, experience, and knowledge (Pollack et al., 2012)—and consider these dispositions as fundamental for all entrepreneurial activities, including designing, establishing, and developing the venture (e.g., Ciuchta et al., 2018). In fact, as substantive information about a new venture is scarce, investors may even consider entrepreneurs’ dispositions as the most important investment criterion (Block et al., 2019; Ko & McKelvie, 2018; Muzyka et al., 1996; Shepherd, 1999). Arthur Rock, for example, a storied Silicon Valley venture capitalist, stated:

I invest in people, not ideas. If you can find good people, if they’re wrong about the product, they’ll make a switch, so what good is it to understand the product that they’re talking about in the first place? (quoted in Sahlman, 1997, p. 101)

Research on entrepreneurial pitching shows that investors respond positively to behaviors signaling the dispositions that make up investors’ perceptions of “prototypical,” successful entrepreneurs (Davis et al., 2017, p. 96). Prototypicality-based social judgments refer to the process by which signal-receivers assess signal-senders based on how closely a receiver perceives the sender to align with the “prototype” they have in mind, given the signal sender’s behaviors such as the language they use (Cantor & Mischel, 1979; Fiske & Taylor, 2017). In that process, the receiver of a signal “chooses how to interpret the information […] while making social judgments about the signaler” (Chandler et al., 2024, p. 1012). The underlying idea is that people develop implicit theories about how types of behaviors correlate with underlying dispositions and attribute a certain behavior shown by a person to a more general disposition of that person (Trope, 1986; Trope & Higgins, 1993). Those judgments rest on the comparisons of observed behaviors to specific sets of idealized expectations that jointly form so-called prototypes (Jacquart & Antonakis, 2015; Tversky & Kahneman, 1974). The more a person’s behavior is prototypical—that is, signals a correspondence of the person’s dispositions with the expectations associated with the person’s social position or function—the more favorably observers will judge that person (e.g., Cornelissen, 2012; Farmer et al., 2011; Malmström et al., 2017). Signal receivers will mostly rely on such prototypicality-based social judgments in situations when clear performance signals are unavailable (Jacquart & Antonakis, 2015). Research on entrepreneurial pitching has highlighted that investors share views of the prototypical entrepreneur and are more willing to fund a new venture the more that they perceive signals that match that prototype (e.g., Antonakis et al., 2011; Huang & Knight, 2017).

Entrepreneurship research has shown how pitching behavior can effectively signal prototypical dispositions such as passion (Chen et al., 2009), commitment (Busenitz et al., 2005), and “coachability” (Ciuchta et al., 2018). However, scholars have devoted almost no attention to what is likely another important facet of the prototypical entrepreneur—namely, their cognitive dispositions or thinking style (e.g., Harrison et al., 2020). A thinking style denotes generalized ways in which a person perceives, structures, and interprets their environment (e.g., Epstein, 1994). Rather than referring to the content of a person’s mind, it refers to a person’s “cognitive processes, or how [their] mind works” (Graf-Vlachy et al., 2020, p. 938). Thinking styles such as Jungian thinking styles (Nutt, 1993) and paradoxical thinking (W. K. Smith & Lewis, 2011) have long been shown to affect how people behave in dynamic and uncertain environments and how others view communication senders (Zhang et al., 2022). Thinking styles profoundly impact the ability to implement entrepreneurial ideas (K. G. Smith et al., 2001). In other words, there is good reason to believe that investors’ perceptions of an entrepreneur’s thinking style may play a pivotal role in shaping investment behavior. We seek to provide a foundation for research in this area by focusing on linguistic signals of one particularly well-studied thinking style: cognitive complexity (Scott, 1962).

Signals of Cognitive Complexity and Venture Funding

Language-Based Attributions of Cognitive Complexity

Psychologists define cognitive complexity as a person’s degree of “differentiated and nuanced thinking” (Graf-Vlachy et al., 2020, p. 938). The more cognitively complex an individual, the more they think in differentiated and nuanced categories and compare those categories (Scott, 1962; Tetlock et al., 1993). In other words, a person of higher cognitive complexity thinks more in “shades of grey” than in “black and white.” A more cognitively complex entrepreneur might, for instance, think about customers, technologies, and market niches in numerous varieties and gradations. In contrast, a less cognitively complex entrepreneur might consider customers, technologies, and markets as rather homogenous. Importantly, cognitive complexity is conceptually distinct from cognitive flexibility (Martin & Rubin, 1995; Scott, 1962), and not correlated with cognitive ability (Bieri, 1955; Ceci & Liker, 1986; Woznyj et al., 2020).

A substantial amount of research in psychology leads us to argue that observers interpret a person’s use of a certain type of language as a signal of that person’s cognitive complexity. First, people generally make language-based attributions, taking aspects of language as signals regarding the communicator’s generalized dispositions (e.g., König et al., 2024; Reeder & Brewer, 1979). Second, research suggests that cognitive complexity exists as a category of social inference in people’s minds. In fact, notions regarding whether a person thinks in “shades of grey” rather than in “black and white” exist in everyday language in many languages (Lakoff & Johnson, 1980). Although observers—including investors—may use other terms to describe another person’s degree of differentiated and nuanced thinking, they will likely make such attributions. Third, recent research indicates that language includes elements that reflect and thus could serve as signals of cognitive complexity. In particular, Graf-Vlachy et al. (2020) have developed and extensively validated dictionaries of words whose use significantly corresponds to a person’s level of cognitive complexity.

Denoting the words included in Graf-Vlachy et al.’s (2020) dictionaries as cognitively complex language, we argue that investors interpret an entrepreneur’s use of cognitively complex language as a signal of differentiated and nuanced thinking. We also argue that cognitive complexity forms part of the entrepreneurial prototype. Exposure to information that is consistent with the prototype leads to the judgment that the sender is more similar to the prototype, also evoking the assessment that other (non-signaled) aspects of the prototype are present (Fiske & Taylor, 2017, pp. 113–114). Investors will therefore judge entrepreneurs who signal cognitive complexity more favorably, which will ultimately lead to higher investment amounts.

Entrepreneurs’ Use of Cognitively Complex Language and Investment Amount

We deduce this argument by combining research showing that investors respond positively when entrepreneurs’ signals match construals of the prototypical entrepreneur, and the idea that cognitive complexity is a constituent element of that entrepreneurial prototype. As outlined above, notions of prototypicality play a central part in investors’ responses to funding pitches (Kalvapalle et al., 2024). Indeed, there is ample evidence that social and economic evaluations of entrepreneurs and their ventures benefit from the congruence between entrepreneurs’ signals and the generally shared views of the prototypical entrepreneur (Brooks et al., 2014; N. Guo & Leung, 2021). In this regard, the entrepreneurship literature has largely focused on signals of entrepreneurial passion and spiritedness as elements of prototypical entrepreneurship, as well as on expectations associated with the entrepreneur’s more general role of a “leader,” including, for example, the expectation that an entrepreneur radiates optimism and a certain level of aggressiveness (Brooks et al., 2014; Kanze et al., 2018; Malmström et al., 2017).

We argue that cognitive complexity is another key component of the entrepreneurial prototype. The greater the entrepreneur’s use of cognitively complex language, the more will investors perceive that entrepreneur as competent and, ultimately, their venture as fundable. First, entrepreneurship scholars have noted that investors generally, apart from more motivation-related expectations, also look for signals of entrepreneurs’ cognitive dispositions (Chen et al., 2009; Ciuchta et al., 2018; Harrison et al., 2020; Huang & Knight, 2017). These cognitive dispositions do not only include general notions of intelligence or cognitive content, but also thinking styles. For instance, Huang et al. (2021) found that investors reward entrepreneurs’ long-term growth orientation, which can be considered a thinking style.

Second, and more specifically, abundant qualitative evidence underscores the notion that cognitive complexity—described in synonyms of nuanced and differentiated thinking—is widely expected and associated with the prototypical entrepreneur. In particular, cognitive complexity is often mentioned in statements of investors and advisors about what it means to be an entrepreneur. For instance, the Business Development Bank of Canada (2024) compiled a list of “key entrepreneurial traits,” including being “comfortable living in a world where answers come in shades of gray” at the top of the list. The media also praise prototypical entrepreneurs such as Steve Jobs for “showcasing the remarkable power of understanding complex patterns of causality in business and human behavior” (Romero, 2023), and the entrepreneurship community discusses that “entrepreneurs possess […] the ability to work in shades of grey, rather than in […] plain black and white” (Newton, 2016). In line with these ideas, a highly experienced investor, whom we interviewed as part of this study,

1

described what he was looking for in an entrepreneur:

It’s the person and their awareness and their ability to linguistically articulate the relative benefits and costs of the thing that they’re going about. […] They’ve got to communicate that they’ve thought [it] through. [When an entrepreneur “speaks in black-and-white,” they] come across ignorant of the market and the potential competition [and as] not thinking through the problem in a way that there’s always alternatives. […] Entrepreneurs who are “speaking in black and white” [are] a little insensitive, and insensitivity gives me a sense that they’re not aware.

Third, there is solid empirical evidence showing that it is rational for investors to associate cognitive complexity with entrepreneurial competence and venture success (Huang & Knight, 2017; Zacharakis & Shepherd, 2007). In fact, cognitively complex managers have long been shown to have a greater understanding of the nuances of competitive landscapes (McNamara et al., 2002). Furthermore, more cognitively complex managers exhibit more effective leadership, as they can tolerate ambiguity more easily and consider more alternative perspectives (Nadkarni & Narayanan, 2007; Wong et al., 2011). Cognitive complexity will likely enable an entrepreneur to process more and different stimuli and effectively make sense of dynamic, ambiguous, and multifaceted—that is, entrepreneurial—environments (Bogner & Barr, 2000; Calori et al., 1994).

Importantly, we have no reason to expect that investors’ positive response to linguistic signals of cognitive complexity will be overcompensated by potential drawbacks of such language. In this regard, investors might assume that sensitivity to nuance and thorough differentiation of multiple perspectives might render an entrepreneur indecisive, cognitively overloaded, and distracted from “getting the job done” (Downey & Slocum, 1982). However, our qualitative inquiry and the evidence on prototypicality-based judgements make us confident that investors look for signals of cognitive complexity despite these potential drawbacks (Moore & Tenbrunsel, 2014). One could also object that cognitively complex language almost inherently adds linguistic complexity, which increases the cognitive processing load (Pallotti, 2015) and, in turn, potentially reduces investor favorability. Yet, given our grounded evidence suggesting that nuanced and differentiated thinking is indeed central to the entrepreneurial prototype, we expect this countervailing effect to be relatively small.

In sum, we argue that investors perceive an entrepreneur’s use of cognitively complex language as a signal of that entrepreneur’s cognitive complexity. We surmise that cognitive complexity is consistent with construals of prototypical entrepreneurs. Investors have been found to incorporate their perceptions of entrepreneurial prototypicality into their investment decisions, viewing the entrepreneur as central to achieving returns on their investments. Formally stated:

Hypothesis 1 (H1): An entrepreneur’s use of cognitively complex language is positively related to the amount of funding the entrepreneur’s venture receives.

Decreasing Marginal Effect of Cognitively Complex Language

A common finding in the literature on prototypicality signals is that such signals have decreasing marginal effects (e.g., van Knippenberg & Lee, 2023). Once observers sense that there is a sufficient basis for them to infer that an individual matches the prototype, further signals of prototypicality are less influential. For example, Steffens et al. (2021) found diminishing marginal effects for leader group prototypicality, and Sherlock et al. (2017) showed that facial masculinity exhibits decreasing marginal signaling effects regarding perceived social dominance. These findings reflect more general neuropsychological mechanisms, particularly Fechner’s law (Fechner, 1860; Gescheider, 2013), which suggests that subjective sensation is proportional to the logarithm of stimulus intensity. This means that increases in the objective strength of a signal result in positive but increasingly smaller changes in the subjective perception of that signal.

Building on these foundations, we predict a decreasing marginal effect of entrepreneurs’ use of cognitively complex language. If an entrepreneur uses only little cognitively complex language, it is likely that investors lack a sufficient basis to infer that the focal entrepreneur matches the entrepreneurial prototype. In particular, investors will perceive the entrepreneur to lack a necessary degree of cognitive complexity. In turn, using more cognitively complex language will have a comparatively large effect at lower levels of cognitively complex language use. In fact, it is relatively easy to picture investors being particularly skeptical if an entrepreneur uses little or no cognitively complex language. Consequently, at low degrees of cognitively complex language, even a small increase will strongly increase investors’ willingness—or decrease their unwillingness—to fund the venture. Conversely, at higher levels of cognitively complex language use—that is, when the entrepreneur’s use of such language reaches or exceeds prototype-congruent levels—investors are less likely to note and value further increases as they will have already judged the entrepreneur to be sufficiently cognitively complex and prototypical. Thus, marginal increases of cognitively complex language will strengthen investors’ perceptions of prototypicality and, ultimately, their funding intentions to an increasingly smaller extent.

In addition, at higher levels of cognitively complex language, two countervailing effects, which we have mentioned above in the development of H1, may increasingly come into play. First, despite its prototypicality, investors may also expect higher levels of cognitive complexity to get in the way of entrepreneurial success, for instance, as differentiated and nuanced thinking may distract an entrepreneur from “getting the job done” (for a review, see Graf-Vlachy et al., 2020). Second, nuances, differentiations, and comparisons inherently involve a greater number of interrelated linguistic elements (Pallotti, 2015). Thus, at higher levels, cognitively complex language may require greater cognitive effort to process, which would subconsciously diminish investors’ favorability to some extent (Crilly et al., 2016; DuBay, 2004). 2 Formally put:

Hypothesis 2 (H2): There is a decreasing marginal effect of an entrepreneur’s use of cognitively complex language on the amount of funding the entrepreneur’s venture receives.

Elite Education as an Amplifier of the Influence of Cognitive Complexity

A standard premise in signaling theory is that a signal’s strength and effectiveness is a function of its credibility and that of its signaler (Bafera & Kleinert, 2023; Certo et al., 2001; Cialdini, 2007). This notion resonates with the concept of “ethos” in classical Greco-Roman rhetoric (Corbett & Connors, 1998) as well as modern concepts of source credibility and legitimacy (Garud et al., 2023; Rhee & Fiss, 2014). Generally, the more that receivers of a signal perceive the signaler and the signal as credible, the lower their uncertainty regarding the signal and their perceived need to scrutinize it. Research shows that this is especially true for signals that are relatively costless for the sender (Anglin et al., 2018), as is the case for the use of cognitively complex language. In this regard, Chandler et al. (2024, p. 1011) emphasized that “the influence of a costless signal is often dependent upon its interaction with […] costly signals being simultaneously sent.”

In line with this reasoning, we focus on the moderating role of one of the most extensively studied costly credibility signals: elite education. Elite education denotes cases in which an entrepreneur holds a degree from particularly prestigious universities such as Harvard or Oxford (Salas-Díaz & Young, 2025). It generally functions as a credibility signal because the widely recognized status of an elite institution confers externally legitimized credibility upon the sender of the signal—a credibility that may surpass that provided by other signals, particularly those emanating from the individual sender (Colombo, 2021). Furthermore, as Connelly et al. (2011) discussed, a signal’s effectiveness depends on its availability and correspondence. Elite education is a particularly available signal in the specific context of our study because entrepreneurs typically provide investors with their curriculum vitae and often refer to their education during pitches. In addition, elite education strongly corresponds with investors’ specific credibility criteria as it is often associated with productivity and access to elite networks (Ko & McKelvie, 2018). Also, entrepreneurs with elite education forgo greater compensation from alternative employment, thereby incurring higher opportunity costs for starting a business (Gimeno et al., 1997). As such, elite education is not only a particularly effective credibility signal per se, but it will likely also add credibility to, and amplify the impact of, other signals, including the use of cognitively complex language.

Signaling theory in entrepreneurship research offers two lines of argumentation to support the hypothesis that elite education amplifies the effect of cognitively complex language on funding. First, elite education is highly congruent with cognitively complex language, complementing its effect as a signal of actual cognitive complexity. Indeed, elite educational institutions advertise their focus on students’ abilities to “present and defend […] opinions, accept constructive criticism and listen to others [in] rigorous academic discussion” (University of Oxford, 2024), and their ability to “think critically about their own views” (Stanford University, 2024). To this end, they make use of “nuanced assessments” to allow for a full appreciation of the “complexities […] explored in class” (Harvard University, 2024). This focus likely contributes to the perception that elite universities select and nurture individuals with differentiated and nuanced thinking styles and that their graduates are equipped to think productively with greater nuance than graduates of other institutions. As a result, when an entrepreneur with an elite education uses cognitively complex language, investors are particularly inclined to notice this and interpret it as evidence of cognitive complexity.

Second, elite education will render investors more likely to rely on their perceptions of cognitive complexity to proxy future entrepreneurial success. As we have argued above, despite its prototypicality, investors may anticipate cognitive complexity to have certain negative effects (for an overview, see Graf-Vlachy et al., 2020), such as slowing down decision making. However, the entrepreneur’s elite education will likely alleviate these concerns, as investors will tend to assume that it is hard to obtain such a degree without the ability to “get things done” and that people with an elite education are generally more effective (Ko & McKelvie, 2018; Salas-Díaz & Young, 2025). In other words, an elite education will reinforce investors’ perception that the entrepreneur can leverage their cognitive complexity for the benefit of the new venture.

Altogether, the signal that is elite education is likely to enhance both investors’ attribution of cognitively complex language to entrepreneurs’ actual cognitive complexity and the impact of attributed cognitive complexity on perceptions of entrepreneurial competence. We therefore conclude that an entrepreneur’s use of cognitively complex language will positively affect venture funding especially when the entrepreneur has an elite education. We thus posit:

Hypothesis 3 (H3): The positive relationship between an entrepreneur’s use of cognitively complex language and the amount of funding the entrepreneur’s venture receives is stronger for entrepreneurs with an elite education than for entrepreneurs without an elite education.

Methods of the Field Study

We conducted two studies: a field study on 547 actual investment pitches and an experiment with 240 professionals. In sections “Methods of the Field Study” and “Results of the Field Study,” we describe the methods and results of the field study. Section “Randomized Vignette Experiment” describes the experiment’s design and results.

Setting and Sample

We used a sample of early-stage startups that pitched to investors during the TechCrunch Disrupt Startup Battlefield (Kanze et al., 2018). Since its inception in 2009, over 763 ventures, including high-profile startups like Dropbox, Yammer, and N26, have participated and subsequently raised USD 8.8 billion (TechCrunch, 2023). The competition takes place annually across several locations in the United States, Europe, Latin America, Africa, and Asia. This is a compelling setting to investigate our research question for several reasons. First, the pitches are made in a standardized format with real-life interactions between startups and investors. Each pitch comprises a 6 min presentation and a 6-min Q&A session in which entrepreneurs spontaneously respond to judges. The format is thus similar to other interactions between entrepreneurs and investors (Clarke et al., 2019; Kanze et al., 2018). Second, the setting allows us to collect data as the pitches are video-recorded. We supplement this data with information from established sources such as Crunchbase or VentureSource. Third, the sample includes a comparable and relevant set of ventures: all are early-stage and actively seeking funding. We compiled the videos of pitches made by 547 ventures during 26 competitions between 2009 and 2018. 3

Measures

Dependent Variable

Our goal is to understand how investors’ decisions are influenced by the cognitive complexity of entrepreneurs. Therefore, we take the funding amount raised by a focal venture as our dependent variable. We measure this continuous outcome variable as the amount of capital raised in the year following the pitch in USD. One year is the lower time limit for early-stage startups to launch a funding round (Ewens et al., 2016). In addition, cognitive complexity will likely be somewhat stable for (at least) a year. In line with previous research, we mitigate the effect of the dependent variable’s skewed distribution by using the natural logarithm in our analyses (Kanze et al., 2018; van Balen et al., 2019). 4 We used VentureSource, which is generally considered one of the most reliable and comprehensive datasets on financing activity (Ewens et al., 2018; Gompers et al., 2009). We augmented the data via Crunchbase, which contains community-supplied information, especially for angel investments and early seed investments (Clingingsmith & Shane, 2018; Kanze et al., 2018). We manually researched all investment rounds where the amounts were not in either database. 5

Independent Variable

To measure the use of cognitively complex language, we follow previous studies (e.g., Graf-Vlachy et al., 2020; Harrison et al., 2020) and use the Q&A session after the pitch since it can be expected to reflect cognitive processes as it entails unscripted, spontaneous answers to investors’ questions. It is less influenced by impression management than the prepared, rehearsed, and collaboratively developed pitch presentation (Clingingsmith & Shane, 2018; Graf-Vlachy et al., 2020; Harrison et al., 2020). We employ computer-aided text analysis since it does not require the entrepreneurs’ cooperation and allows us to analyze large amounts of text. This also offers substantial benefits compared to human coding. For instance, it does not suffer from biases like coder fatigue or drift (Neuendorf, 2017), and is transparent and replicable (Tetlock et al., 2014). It has been used extensively to measure psychological and cognitive attributes (Pan et al., 2018; Parhankangas & Renko, 2017; Pollack et al., 2012).

Our measurement captures the three underlying facets of the construct: differentiation, nuance, and comparison. We rely on the extensively validated method developed by Graf-Vlachy et al. (2020) to measure each facet using dictionaries. First, differentiation is measured using a dictionary that includes words like “but,” “except,” and “however,” which refer to instances in which individuals simultaneously consider multiple dimensions and aspects (Crilly et al., 2016). The measure is calculated as the number of differentiation words divided by the number of words spoken by the individual. Second, nuanced thinking is gauged via weak modal words (e.g., “could,” “might”) and tentative words (e.g., “apparently,” “seems”) as indicators of a more nuanced thinking style, as well as strong modal words (e.g., “always,” “will”) and certainty words (e.g., “completely,” “purely”), which indicate a greater tendency towards a black and white thinking style (Loughran & McDonald, 2011). The measure is calculated by dividing the number of weak/tentative words by the sum of strong/certainty and weak/tentative words. Third, comparative language is captured through words such as “better,” “later,” or “harder,” as they demonstrate an individual’s tendency to consider and discriminate between multiple distinct concepts. The measure is calculated as the ratio of comparison to total words. Finally, we standardize and average the three components to arrive at an index. To ensure the reliability of our measure, we require each entrepreneur to speak at least 250 words (Graf-Vlachy et al., 2020).

Moderator

To measure elite education, we coded a dummy variable for all entrepreneurs indicating whether they received a degree from an elite university. In our main specification, we considered the top 20 universities in the 2018 vintage of the Academic Ranking of World Universities, colloquially known as the Shanghai Ranking, as elite universities.

Control Variables

We included industry fixed effects based on the VentureSource industry classification and year fixed effects since the funding environment can differ (Busenitz et al., 2005). 6 We control for company age in years (Kanze et al., 2018) and the location of the venture with indicators for the United States, Europe, Asia-Pacific, and “other,” as they affect the availability of funding. We also controlled for prior funding, measured as the number of previous funding rounds (van Balen et al., 2019), and the number of patent applications as additional quality signals (Hsu & Ziedonis, 2013). We focus our analysis on the main entrepreneur, but control for the use of cognitively complex language by other team members, measured using the same procedure. We substitute missing values for missing second or third entrepreneurs with the sample means (Block et al., 2014). We also calculated the use of cognitively complex language by jury members to account for the possibility that entrepreneurs mirror investors (Graf-Vlachy et al., 2020). We controlled for the ease of understanding using the Flesch Reading Ease measure, calculated based on sentence and word length on a scale from 0 to 100 (Parhankangas & Renko, 2017), and language concreteness based on a dictionary (Brysbaert et al., 2014; Huang et al., 2021). In addition, we controlled for language tone with the standardized Janis–Fadner coefficient of imbalance (Blevins et al., 2019) based on LIWC dictionaries for positive emotion and negative emotion (Pennebaker et al., 2015). We used dummy variables to indicate if the entrepreneur held an MBA or PhD degree or had previously founded ventures (serial entrepreneur; Gompers et al., 2010; Ko & McKelvie, 2018). We gathered this data from LinkedIn, company websites, and BoardEx. We controlled for team size as the number of entrepreneurs representing the venture during the pitch. Finally, we included a dummy for female entrepreneurs, as prior research shows that women tend to get less funding (Kanze et al., 2018).

Results of the Field Study

Hypotheses Tests

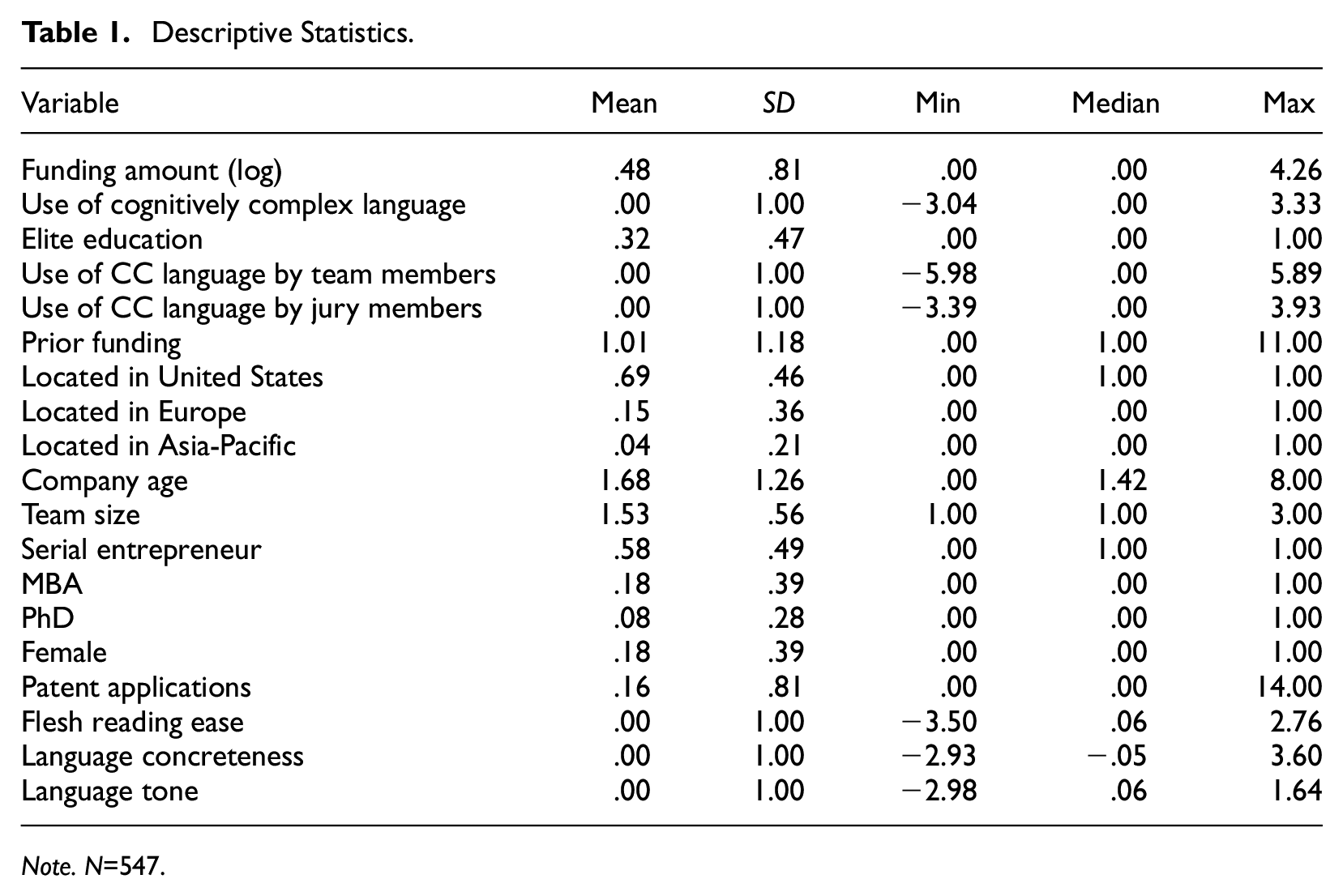

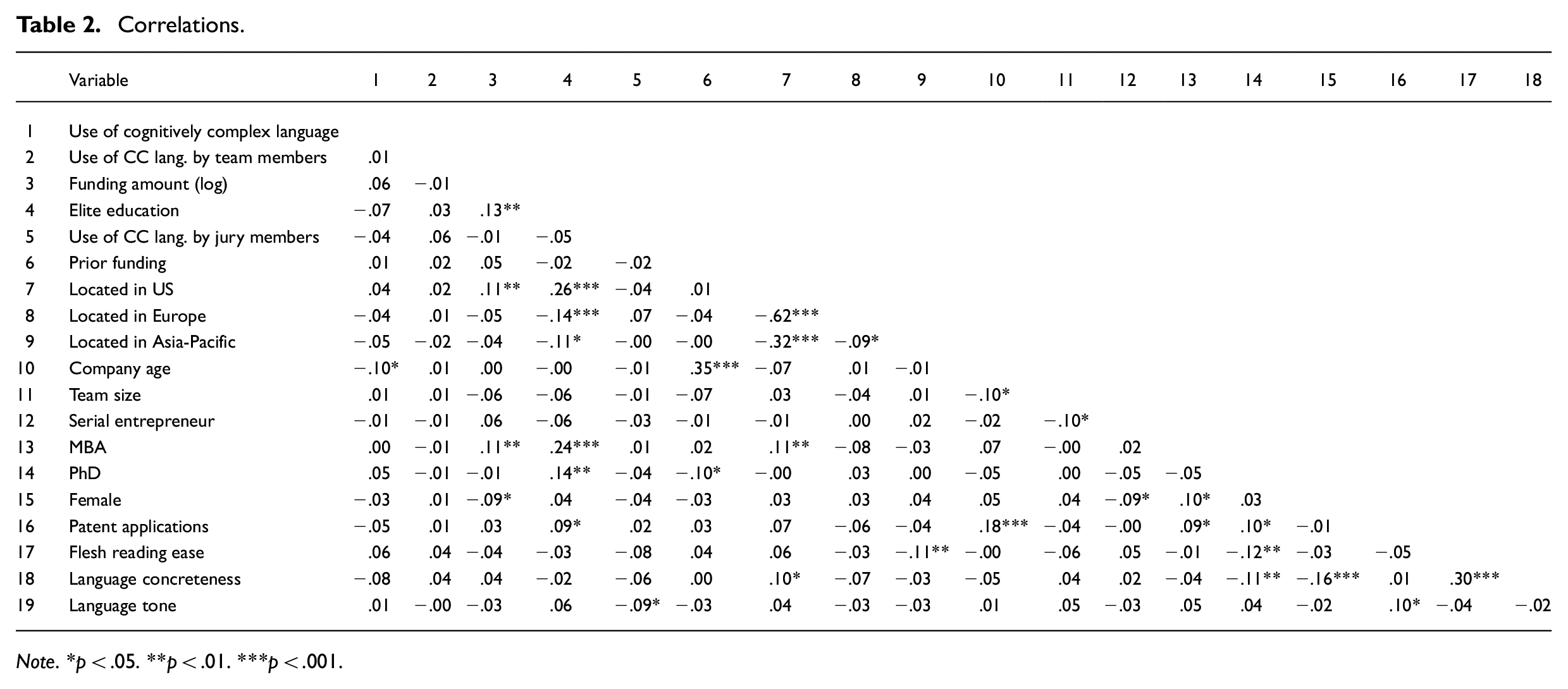

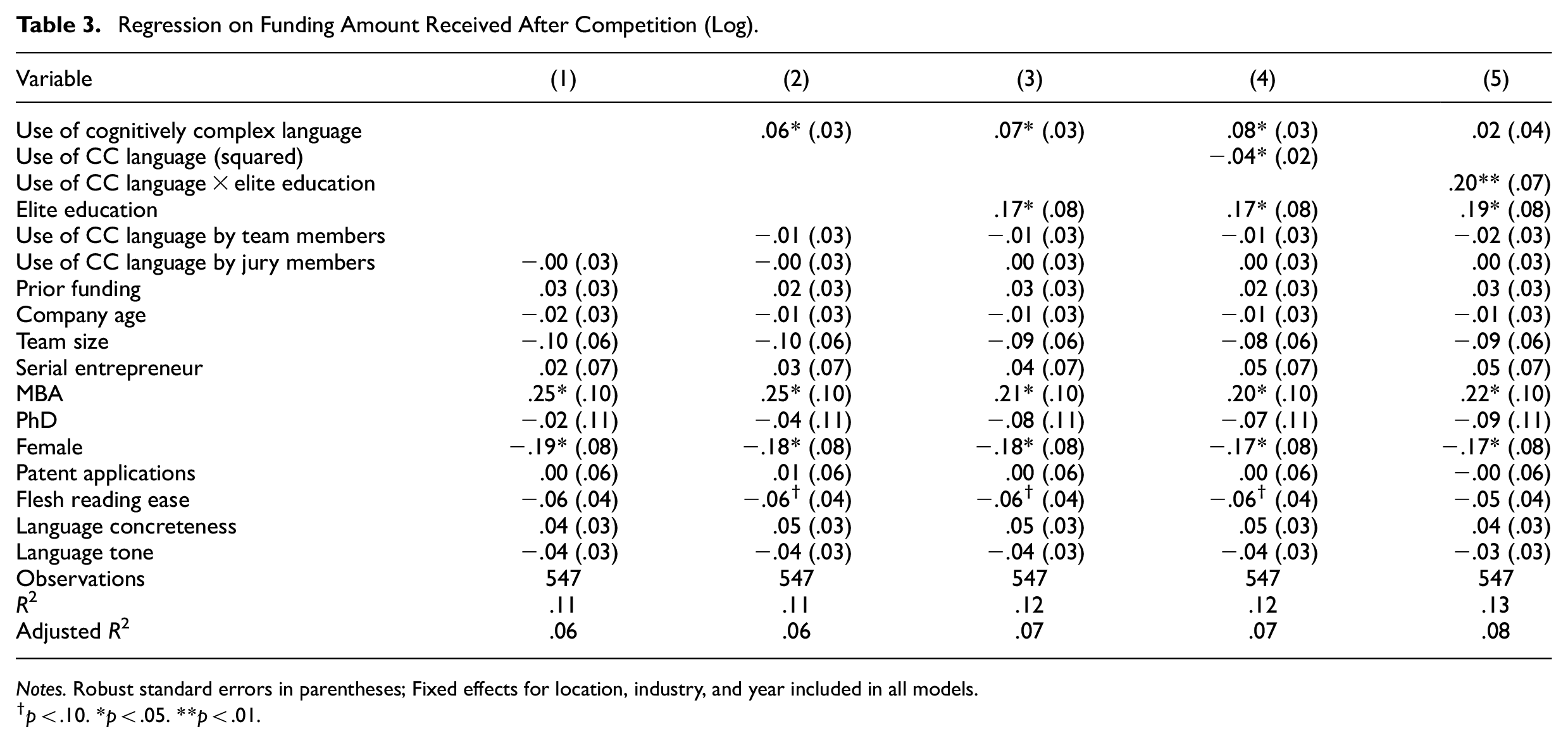

Table 1 shows the descriptive statistics, Table 2 the correlations between the variables in our study, and Tables 3 the results we use to test our hypotheses. We used OLS regressions with robust standard errors to analyze the funding amount received after the competition.

Descriptive Statistics.

Note. N=547.

Correlations.

Note. *p < .05. **p < .01. ***p < .001.

Regression on Funding Amount Received After Competition (Log).

Notes. Robust standard errors in parentheses; Fixed effects for location, industry, and year included in all models.

p < .10. *p < .05. **p < .01.

In Table 3, Model 1 includes the control variables. Model 2 adds the use of cognitively complex language by the main entrepreneur and the other team members. Model 3 adds elite education. Model 4 also includes the use of cognitively complex language as a squared term, and Model 5 the interaction term for the use of cognitively complex language and elite education. H1 states that entrepreneurs’ use of cognitively complex language increases the amount of funding received. In Model 3, we find support for this hypothesis, as the coefficient for the use of cognitively complex language is positive and statistically significant (p = .029). The effect is also economically relevant. The dependent variable—funding amount—ranges from USD 0 (i.e., no funding) to USD 70 million, with an average value of USD 1.73 million. The coefficient for the use of cognitively complex language is .07. Since the dependent variable is log-transformed, a one-unit change in the use of cognitively complex language corresponds to an effect size of 7.25%. The measure for the use of cognitively complex language is standardized, so a one-unit change is equal to a change by one standard deviation. Therefore, a one standard deviation higher value for the use of cognitively complex language translates to 7.25% more funding, or about USD 125,000 from the average value of USD 1.73 million.

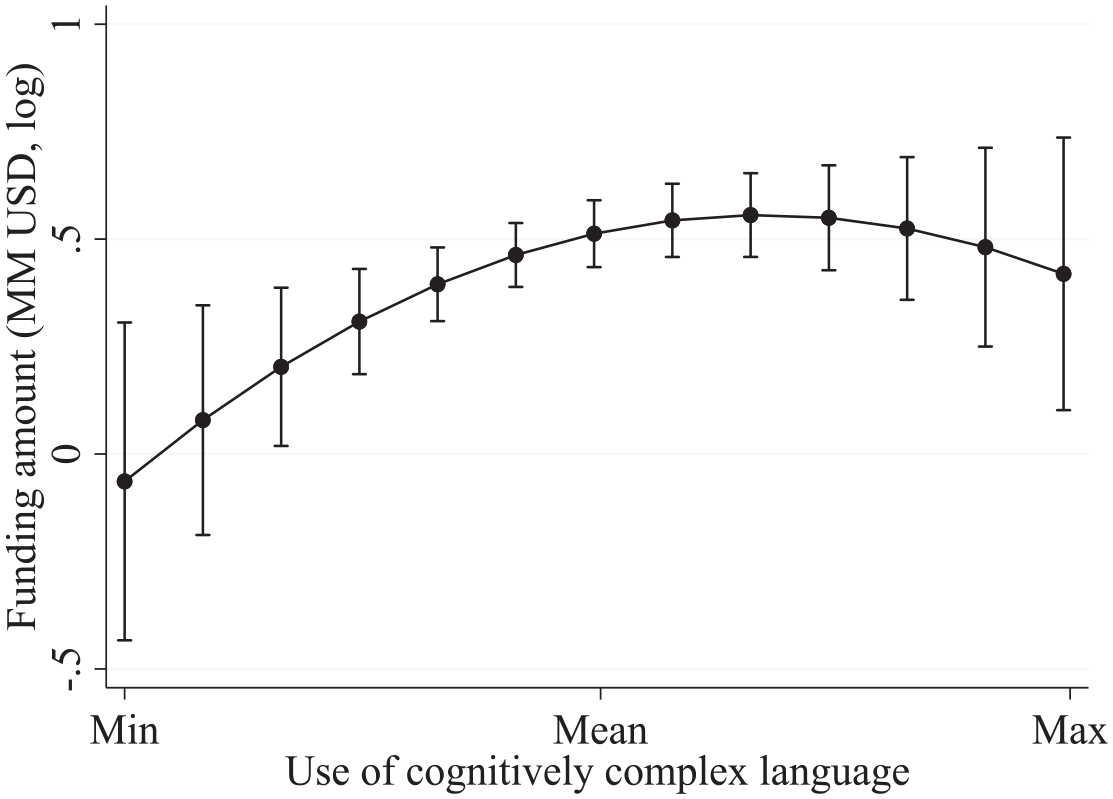

In support of H2, Model 4 shows that the squared term of use of cognitively complex language has a negative and significant coefficient (p = .041). Figure 1 displays the decreasing positive marginal effect graphically. Across the range of values, the use of cognitively complex language is positively associated with funding amount (with the exception of a few very low values where the effect is not statistically significant). The marginal effect increases markedly below the mean and slightly above it. The increase flattens out and turns negative for high values of cognitively complex language. To further probe this result, we split the score for the use of cognitively complex language into five categories and used the generated categorical variable to analyze the impact of the quintiles of the use of cognitively complex language on funding amount. The analysis is reported in Online Appendix 1. Although not all obtained coefficients are statistically significant, we find that the funding amount increases for subsequent quintiles, peaking at the fourth quintile before declining again in the last quintile. The decline thus occurs only at a relatively high level. We further split the use of cognitively complex language into its positive and negative spline. The negative spline is equal to the variable for values below the mean (i.e., contains its negative values) and zero otherwise. The positive spline contains all positive values and is zero otherwise. Online Appendix 2 shows the analysis. It indicates that the observed effect stems primarily from the negative spline, that is, using more cognitively complex language is more beneficial at lower values of cognitively complex language. We also tested formally for the presence of an inverted U-shape relationship with the method described by Lind and Mehlum (2010) using the Stata command utest. Note that we hypothesized a decreasing positive marginal effect, and not that the marginal effect would turn negative and then increase in magnitude (i.e., not an inverted U-shape relationship). The test indicated a marginal significance level (p = .079), which hints at the potential presence of a slight inverted U-shape relationship. This suggests that investors who observe very high levels of cognitively complex language possibly deem this as reflecting characteristics of the entrepreneur that may hinder venture success, which would resonate with the previously acknowledged theoretical arguments that high levels of cognitive complexity can have a negative impact, for instance due to decision paralysis.

Decreasing positive marginal effect of cognitively complex language.

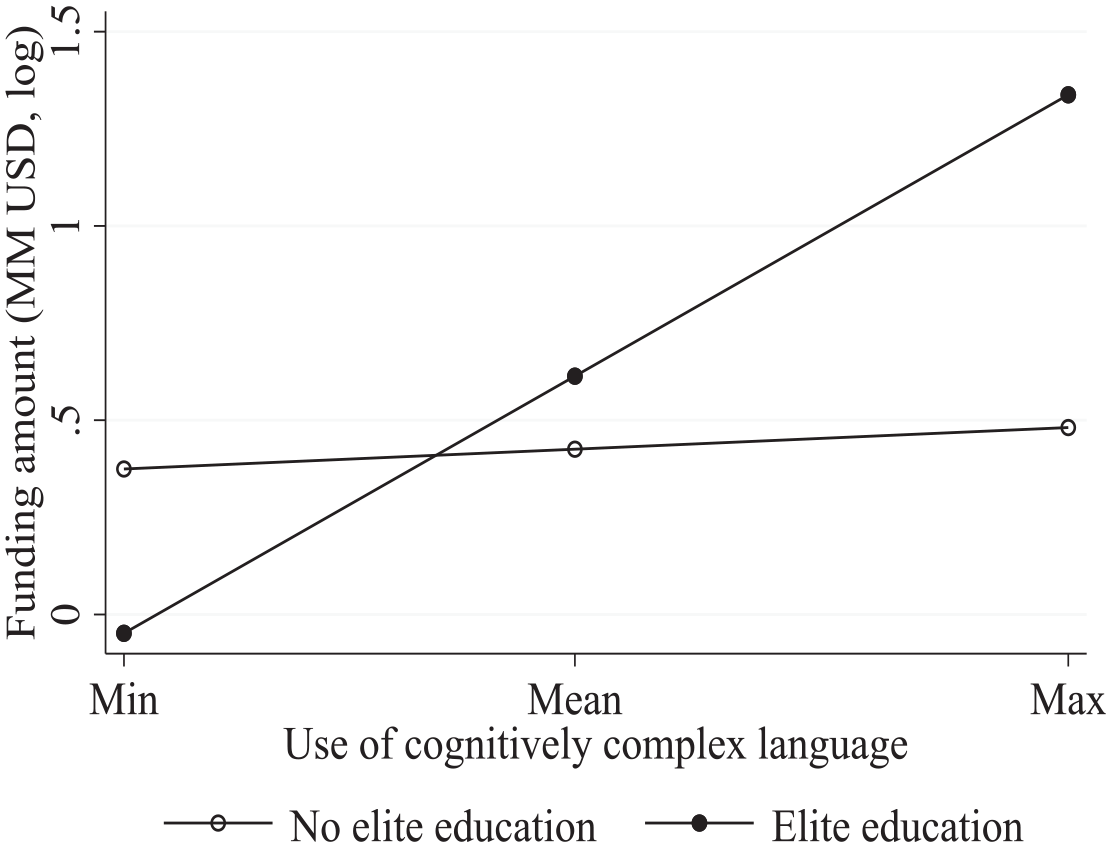

In H3, we argue that the impact of the use of cognitively complex language on funding is amplified by elite education. The interaction between the use of cognitively complex language and elite education in Table 3, Model 5 is significant (p = .008), supporting this idea. Figure 2 displays the interaction effect for the observed spectrum of values for the use of cognitively complex language. As the figure illustrates, increasing values for the use of cognitively complex language are associated with greater funding amount for entrepreneurs with an elite education. For entrepreneurs without an elite education, funding amount increases much less (slope not significant). As we argued above, investors may be more inclined to take cognitively complex language as evidence of the entrepreneur’s thinking style if the entrepreneur has an elite education. One explanation for the apparent strength of the moderation effect could be that investors even fail to detect the signal of cognitively complex language entirely for entrepreneurs without an elite education. Similarly, we argued that investors may not appreciate the signal of cognitively complex language unless it is accompanied by elite education as a credibility signal. If perceived, investors may interpret such language as strategically sent and not authentic when it is not backed up by an elite education. This echoes the idea of reputational penalties, that is, that linguistic signals are perceived to be more authentic if the sender is also sending a costly signal because they would incur higher reputational costs if caught sending the linguistic signal disingenuously (Anglin et al., 2018; Chandler et al., 2024).

Interaction effect between cognitively complex language and elite education.

Robustness Checks

We performed various robustness checks. First, we re-ran our models using various alternative operationalizations of elite education. All results are robust (see Online Appendix 3). Second, analyses in which we control for the Big Five personality traits and venture quality further support the results’ robustness (see Online Appendix 4). Third, even though we control for a host of possible confounding variables, we calculate the impact threshold of confounding variables to assess how concerned we should be about omitted variables. Following Busenbark et al. (2022), we evaluate the impact of an omitted variable that would invalidate a certain significance level of our inferences (e.g., p < .05); this is best evaluated against the observed variables since the omitted variable is unknown by definition. The impact value is .011 for H1 and .034 for H3. An omitted variable would have to be about three (H1) or six (H3) times as highly correlated with our independent and dependent variable than the control variable with the highest impact value to invalidate our inferences (i.e., p > .05). This suggests that our results are robust against bias from potentially omitted variables.

Randomized Vignette Experiment

Although the field study has high external validity given the real-world, high-stakes empirical setting, it is limited in that it assumes that investors form perceptions on an entrepreneur’s thinking style based on characteristics of the entrepreneur’s language. Also, by design, it does not allow us to randomly assign linguistic manifestations of cognitive complexity to Q&A sessions. We address both limitations by performing a randomized experiment. It allows us to obtain evidence for the assumption that investors recognize linguistic cues and attribute them to entrepreneurs’ cognitive complexity. By randomly assigning participants to experimental conditions, we can also substantiate causality claims for the main relationship of the field study.

Design

We recruited our main sample 7 of professionals with at least 5 years of management experience on Prolific. We required management experience because we sought participants with experience in risk assessment and decision making under uncertainty comparable to investors. Based on a power analysis, we decided to recruit 240 participants. We conducted a randomization check using participants’ demographic information and found no significant differences across conditions, indicating successful randomization.

We used a randomized between-subject design, in which we manipulated the independent variable, that is, the use of cognitively complex language in the answers of the entrepreneur to the questions in the Q&A sessions. We created two experimental conditions—that is, low and high degrees of cognitively complex language—with a short text vignette that simulated a pitch-situation similar to the one in the field study. We worded the vignettes so that the content of the entrepreneur’s answers was the same, but the entrepreneur’s language varied along Graf-Vlachy et al.’s (2020) conceptualization and validated measure, that is, the same we had used in the field study. See Online Appendix 5 for further details on the experimental procedures and participants.

Measures

Investment Likelihood

Respondents answered the question “How likely are you going to invest?” on an 11-point Likert scale from 0% to 100% immediately after the vignette. Note that this dependent variable differs from the one in the field study (invested amount in USD) to avoid various methodological issues of asking for an indication of the amount participants would invest. 8 At the same time, it adds further robustness to our results since it allows us to compare whether our results are consistent across different operationalizations of investment decisions, potentially showing that our results do not depend on a specific measurement.

Perceived Cognitive Complexity

We measured the perception of the entrepreneur’s cognitive complexity, which participants might form based on the linguistic characteristics in the vignette, on a 5-point Likert scale, with the endpoints anchored by “1 = low complexity” and “5 = high complexity.” We assessed these perceptions on a separate page after measuring investment likelihood, and the participants were not able to return to change their answer. The rating of their perception can thus, by design, not influence the indicated investment likelihood.

Results

Effect of the Use of Cognitively Complex Language on Perceived Cognitive Complexity

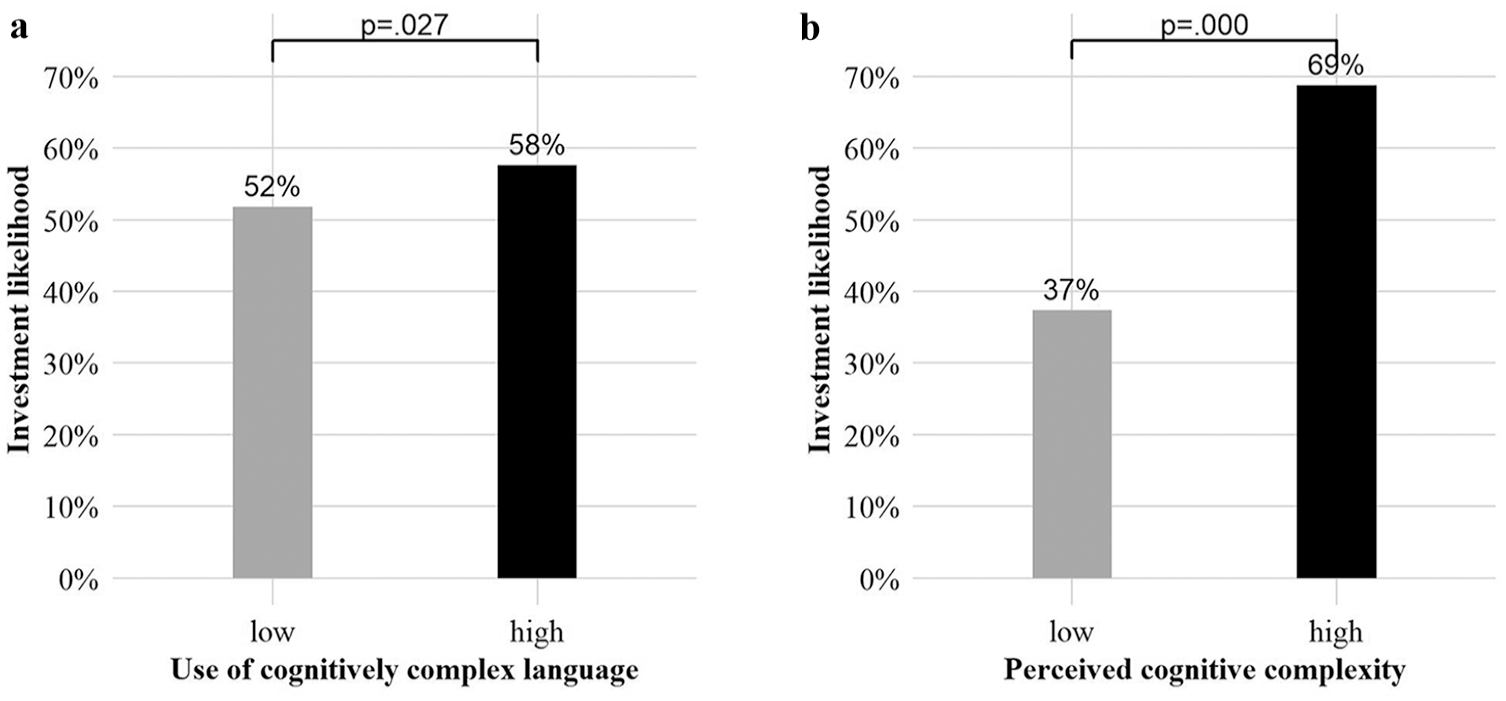

In the field study we assume that investors form perceptions of entrepreneurs’ thinking styles based on language use. The experiment provides evidence for this assumption. Participants who read the answers of the entrepreneur in the “high” use of cognitively complex language condition perceived the thinking style of the entrepreneur as significantly more complex (M = 3.26, SD = .91) than those who read the version where such language was “low” (M = 2.61, SD = 1.12), t(238) = −.65, p = .000). This also suggests that our manipulation was effective.

Effect of the Use of Cognitively Complex Language on Investment Likelihood

The results (see Figure 3a) corroborate H1. As predicted, participants in the “high” use of cognitively complex language condition were more likely to invest (M = .58, SD = .20) than in the “low” condition (M = .52, SD = .26). This difference was significant (t[238] = −.06, p = .027). The effect size—a 6% higher investment likelihood—is economically meaningful, especially considering that our manipulation only changed the wording of two short answers. In practice, investors would spend much more time with an entrepreneur, gather much more information about them, and therefore be in a position to form more pronounced perceptions.

Effects of the use of cognitively complex language and perceived cognitive complexity.

Relationship Between Perceived Cognitive Complexity and Investment Likelihood

Figure 3b shows that there is a positive and significant relationship between respondents’ perception of cognitive complexity and investment likelihood. We compared the 83 respondents that perceived the entrepreneur to be low in cognitive complexity (response options 1 and 2 on the Likert scale) with the 74 that perceived them as high (response options 4 and 5). 9 Participants who perceived high cognitive complexity were 32% more likely to invest (M = .69, SD = .15) than participants who perceived low cognitive complexity (M = .37, SD = .22)—a significant difference (t[155] = −.32, p = .000). These results provide further support for H1.

We replicated the experiment with a second, independent sample of university students, finding consistent results (see Online Appendix 6). We also tested a mediation model, showing that the relationship between cognitively complex language and investment likelihood is fully mediated by perceived cognitive complexity (see Online Appendix 7).

Discussion

We adopted the “investor vantage point” (Kalvapalle et al., 2024, p. 571) and contribute to a cognitive view of signaling theory in entrepreneurship research (Bafera & Kleinert, 2023; Drover et al., 2018). We explore an entrepreneur’s use of cognitively complex language as a meaningful signal for investors and, in turn, an influence on their funding decisions. Our field study of 547 high-stakes pitches by entrepreneurs, and the funding acquired by their new ventures, corroborates our key ideas: investors invest more in a new venture when the entrepreneur uses more cognitively complex language; the entrepreneur’s use of cognitively complex language has a decreasing marginal effect; and the association between entrepreneurs’ use of cognitively complex language and funding is more pronounced for entrepreneurs with an elite education. Our randomized experiment with 240 professionals—and its replication in a student sample—offer preliminary evidence for a causal effect of the entrepreneur’s use of cognitively complex language and substantiate our theoretical premise that investors process cognitively complex language as a linguistic signal and attribute its use to the entrepreneur’s cognitive complexity.

Theoretical Contributions

Our study is the first in entrepreneurship research to conceptually and empirically investigate investors’ responses to linguistic signals of cognitive complexity—a foundational concept from psychology gaining prominence in management research (e.g., Graf-Vlachy et al., 2020; Malhotra & Harrison, 2022). In this way, we make three key contributions, primarily to signaling theory in entrepreneurship research (Bafera & Kleinert, 2023; Kalvapalle et al., 2024).

First, our research challenges the generally negative portrayal of complexity in (entrepreneurial) communication (e.g., W. Guo et al., 2020; Kahneman, 2011). Established theory in this regard tends to assume that audience members because they are boundedly rational and seek to minimize cognitive effort, generally respond unfavorably to the cognitive load imposed by language complexity (Bushee et al., 2018; König et al., 2018). In contrast, our study is motivated by recent entrepreneurship and management research, which argues that knowledgeable audiences may cognitively process communication—and specifically language-based signals—differently than general audiences (Crilly et al., 2016; Falchetti et al., 2022). From the vantage point of investors (Kalvapalle et al., 2024), linguistic displays of cognitive complexity are processed as a signal of an entrepreneur’s thinking style that matches with the entrepreneurial prototype. In particular, while we adhere to the view of investors as boundedly rational—as we envision them to draw on prototypes to deal with uncertainty and to limit cognitive load (e.g., Tsay, 2021)—we consider investors as knowledgeable audiences who are aware of the advantages of thinking in “shades of grey” rather than “black and white,” and who expect such cognitive complexity from entrepreneurs.

More specifically, we present and empirically corroborate a conceptual framework of how entrepreneurs’ linguistic displays of cognitive complexity—rather than of other, previously studied prototypical dispositions—constitute entrepreneurial signals that influence investors’ decision making (Kalvapalle et al., 2024). Researchers have long understood investors’ funding decisions to be driven by entrepreneurial signals and their power to induce perceptions of the focal entrepreneur’s prototypicality (Bafera & Kleinert, 2023). However, scholars have focused primarily on entrepreneurs’ signals of passion (Chen et al., 2009) or gender stereotypes (Kanze et al., 2018). They have largely neglected the notion that entrepreneurs’ cognitive dispositions—that is, how entrepreneurs think and process the world around them—are also essential to social constructions of the prototypical entrepreneur (Ciuchta et al., 2018; Clarke et al., 2019; Mitchell et al., 2002). Our field study of 547 entrepreneurial pitches corroborates our framework, showing that an entrepreneur’s use of cognitively complex language is significantly related to the amount of funding their venture receives (H1). In the randomized experiment, we substantiated causality for this direct effect and provide evidence for the underlying assumption that investors infer entrepreneurs’ cognitive complexity from their language use.

Second, we contribute to signaling theory in entrepreneurship research by answering calls for inquiries into “optimal quantities” of signals (Bafera & Kleinert, 2023, p. 2440). In this regard, we argue that the perspective shift to the investors’ vantage point and their cognitive processing of linguistic signals does not preclude the possibility that linguistic complexity—at a certain level and certain types thereof—may also be dysfunctional. Indeed, we observe a decreasing marginal effect of cognitively complex language (H2). Our research is the first to argue and demonstrate that audiences, particularly investors, share expectations or prototypes regarding actors’ cognitive complexity and are, in turn, affected by corresponding linguistic signals. The decreasing marginal effect indicates that approaching investors’ expectations of a prototypical entrepreneur is more beneficial than surpassing them. Thus, our study promotes not only a more fine-grained understanding of complexity and simplicity, emphasizing the importance of identifying and exploiting the functional aspects of both, but also that the “optimal quantity” of a signal may be a function of the signal receivers’ expectations or prototypes.

Third, we also advance signaling theory in entrepreneurship research by examining how multiple signals are cognitively processed by investors and affect their decision-making (Bafera & Kleinert, 2023; Drover et al., 2018). Particularly, we explore the interaction between a relatively costless language-based signal and another, more costly signal: cognitively complex language and elite education, respectively (Chandler et al., 2024; Steigenberger & Wilhelm, 2018). Interestingly, although language is one of the most relevant means to convey information, signaling theory has traditionally underemphasized its significance, particularly because language-based signals lack the (substantial) costs traditionally associated with signals (Steigenberger & Wilhelm, 2018). Recent accounts, however, highlight that language-based signals can indeed be effective, especially when they interact with other signals (Steigenberger & Wilhelm, 2018). We theorize (H3), and empirically demonstrate in our field study, that investors appreciate linguistic signals of cognitive complexity: they assess entrepreneurs who use more cognitively complex language more favorably, particularly when they have an elite education. Our explanation is that investors perceive cognitive complexity and elite education as congruent, so that (a) investors perceive elite education to add credibility to and amplify the impact of cognitively complex language; (b) investors are particularly inclined to interpret cognitively complex language as signaling cognitive complexity; and (c) investors are more likely to rely on their perceptions of cognitive complexity as a proxy for entrepreneurial success. Our research differs from earlier accounts of language-based signals in two ways. First, we demonstrate that, in addition to rhetorical signals (i.e., characteristics of language that appeal to modes of persuasion), linguistic signals (i.e., structural characteristics of language) also influence investors (König et al., 2018). Second, we show how linguistic signals—specifically cognitively complex language—interact with more traditional signals—specifically elite education (Spence, 1973). While most studies on entrepreneurial signaling have focused on investors’ perceptions of isolated signals, we recognize and empirically underscore the idea that, in reality, investors process signals simultaneously (Chandler et al., 2024). Altogether, our research adds to recent scholarship within signaling theory that attempts to provide a more holistic understanding of signal portfolios (Bettinazzi et al., 2024; e.g., Steigenberger & Wilhelm, 2018; Trzebiatowski et al., 2025).

Finally, we make broader methodological and empirical contributions. We introduce Graf-Vlachy et al.’s (2020) measure of cognitively complex language to the entrepreneurship literature. We also present the first randomized experiment—including in social psychology—that demonstrates how cognitively complex language causes attributions of cognitive complexity. Overall, our article responds to recent calls for experimentally grounded theorizing on signaling, especially in entrepreneurship research (Bafera & Kleinert, 2023; Drover et al., 2018).

Practical Implications

Our study’s most important practical implications are for entrepreneurs and investors. First, we urge entrepreneurs to reconsider the ubiquitous advice to keep pitches simple. Specifically, our theorizing and data suggest that entrepreneurs should exude a complex—that is, nuanced and differentiated—thinking style when communicating with investors. Perhaps most importantly, they should be aware that heeding the canonic advice to strive for clear communication might result in overly simple communication that involves too little cognitively complex language, as failing to meet prototypical expectations in this regard can significantly reduce the funding opportunities for the new venture. Second, entrepreneurs with a degree from an elite educational institution should be particularly aware of using the power of cognitively complex language. Third, investors should be aware of the subtle, mostly unconscious, and potentially biasing influence of cognitively complex language when evaluating entrepreneurs and their ventures.

Limitations and Future Research

We acknowledge our study’s limitations, which may also present new research opportunities. First, because we test the decreasing marginal effects of cognitively complex language and the moderation by elite education only in our field study, we call for further experimental investigations of these effects. Second, while we are able to relate linguistic signals of cognitive complexity to actual funding amounts, future research could measure intermediate mechanisms of how investors cognitively process such linguistic signals and perceptions of cognitive complexity. Third, we treat early-stage investors as a homogenous group. However, early-stage investors encompass both venture capitalists and business angels, who may respond differently (Colombo, 2021; Huang & Pearce, 2015). Future research could also consider how other audience types—say, customers or potential business partners—cognitively process linguistic signals of cognitive complexity, given that their expectations might differ (Fisher et al., 2017). We also encourage research on heterogeneity in signal receivers’ cognition, as their own cognitive complexity might influence how they process a signal sender’s use of cognitively complex language. Fourth, it would be interesting to see whether cognitive complexity loses or gains importance in later investment stages (Bafera & Kleinert, 2023). Prior research suggests that the role of linguistic signals typically diminishes over time, as actors get to know each other (Fiske & Taylor, 2017). Intriguingly, though, investors may also perceive cognitive complexity as more important the more a company grows and the more complex its relationships and business practices become. Finally, we see promise in analyzing whether the entrepreneur’s use of cognitively complex language matches their actual cognitive complexity. Future studies could investigate if signal receivers sense and respond to discrepancies between linguistic signaling and other reflections of cognitive complexity.

Supplemental Material

sj-pdf-1-etp-10.1177_10422587251347042 – Supplemental material for Shades of Grey or Black and White? How Entrepreneurs’ Use of Cognitively Complex Language Affects Investor Funding

Supplemental material, sj-pdf-1-etp-10.1177_10422587251347042 for Shades of Grey or Black and White? How Entrepreneurs’ Use of Cognitively Complex Language Affects Investor Funding by Patrick Figge, Lorenz Graf-Vlachy, Andreas König, Florian Demann and Martin Diessner in Entrepreneurship Theory and Practice

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Parts of this research were funded by the Dr. Theo and Friedl Schoeller Research Center for Business and Society.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.