Abstract

We examine the physical health consequences to entrepreneurs of firm growth and decline. Using register-based panel data (2000–2021), we find that entrepreneurs and hired CEOs are, on average, healthier and live longer than individuals from a socio-economically similar random sample from the general population. However, our findings also reveal that entrepreneurs are more likely to fall ill during their tenure and die younger than hired CEOs. Importantly, our findings demonstrate that both cumulative exposure to growth and episodic, rapid declines in sales and in the number of employees are equally taxing for entrepreneurs and hired CEOs.

Introduction

“No stop signs, speed limit; Nobody’s gonna slow me down!”

Highway to Hell lyrics, AC/DC, written by Bon Scott, Angus Young, and Malcolm Young

The World Health Organization (WHO) declared the association between work-related stress and employee health as one of the biggest challenges of the 21st century (Houtman & Jettinghoff, 2007). Roles of responsibility, such as that of a CEO, can be highly stressful. A recent article in the Wall Street Journal stated: “Maybe the job of CEO should come with a warning label” (Borchers, 2024). This topic has also received increasing attention in entrepreneurship research. Health and well-being are studied both as important outcomes of entrepreneurial activity and as crucial prerequisites for entrepreneurs to run their ventures successfully (Boudreaux et al., 2022; Patel et al., 2019; Stephan, 2018; Wiklund et al., 2019). In addition, prior research demonstrates that stress is an important predictor of entrepreneurs’ well-being. However, the primary focus of prior work has been on psychological well-being (Baron et al., 2016; Gish et al., 2022; Kibler et al., 2019; Obschonka et al., 2023; Stephan et al., 2023; Wach et al., 2021), with few studies addressing the consequences of stress on physical health (Cardon & Patel, 2015; Patel et al., 2019).

Prior empirical evidence on the relationship between stress and health in entrepreneurial contexts is equivocal. While several studies suggest that entrepreneurs, on average, are healthier and report lower levels of stress than salaried employees (Hessels et al., 2017; Obschonka et al., 2023; Rietveld et al., 2015; Stephan & Roesler, 2010), others point to entrepreneurs having high levels of occupational stress, with adverse health consequences (Cardon & Patel, 2015; Lerman et al., 2021; Patel et al., 2019). We argue that the inconsistent findings are likely due to the heterogeneity of entrepreneurship (Wolfe & Patel, 2019) and the empirical samples used in prior studies. For example, a self-employed individual without employees who mainly leverages their human capital for the business (e.g., a self-employed carpenter or an independent consultant) faces different levels and types of stress (Hessels et al., 2017), as well as a different scope for coping with the stress, compared to an entrepreneur who runs a technology venture with 50 employees (Nikolaev et al., 2020).

Our study sheds additional light on the relationship between stress and health by focusing on the specific context of venture growth. High-growth firms receive special attention in research and public policy because of their importance in creating new jobs, sustaining economic development, and advancing the overall welfare of society (e.g., Crawford et al., 2015; Storey, 1994). However, leading a high-growth venture may take a toll on the leader’s health. While the health effects of firm growth on entrepreneurs have been raised in the popular press (e.g., Bruder, 2013), systematic scholarly inquiries into the topic are lacking (Shepherd & Patzelt, 2015). Managing a growing firm, while an exciting challenge that involves substantial responsibility, may also expose entrepreneurs to particularly intense and/or severe stressors over longer periods of time that can subsequently lead to adverse health consequences.

Drawing on the Challenge-Hindrance Stressor Framework (CHSF; Cavanaugh et al., 2000; LePine et al., 2005; for a review, see Podsakoff et al., 2023) and the allostatic load (AL) model (McEwen & Stellar, 1993), we propose that managing a growth-oriented firm comes with high levels of a variety of stressors that can subsequently lead to adverse physical health outcomes. Some of the stressors are hindrances that are difficult to control (e.g., uncertainty of market demand, resource constraints, regulatory adjustments), while others are challenges that entrepreneurs can manage (e.g., complex projects, high workload, tight deadlines). Even if the challenges of growth are stressors that entrepreneurs are motivated to tackle, they can be intense in a growing venture, and prolonged exposure to such stressors can cause significant strain that leads to reduced health and culminates in serious, potentially life-threatening health events. This may particularly be the case if the growth is rapid and episodic (i.e., happens only sometimes and not regularly) or occurs over a long period of time as these processes would involve intense and sustained efforts that may expose entrepreneurs to demanding periods of challenge and strain. Furthermore, entrepreneurs may experience even more severe physical consequences when their business is declining, especially if the decline is intense or occurs over a long period of time. Previous literature suggests that exposure to these conditions may be even more stressful than managing growth (e.g., Pearsall et al., 2009; Podsakoff et al., 2023).

The aim of our study is to generate a rigorous and systematic understanding of the effects of managing a growing or declining venture on entrepreneurs’ health through an exploratory quantitative study (Wennberg & Anderson, 2020). Instead of formulating specific hypotheses, we present research questions and use multiple statistical techniques to create a multifaceted overview of the relationship between venture growth or decline and entrepreneurs’ health. Our principal research question is: How does exposure to intense or sustained periods of venture growth or decline affect entrepreneurs’ risk of serious, stress-related health events and premature mortality?

We utilize a variety of Finnish official registers to assemble a bespoke longitudinal dataset spanning two decades. The data sources include: (a) financial statement data from 2000 to 2021 to model firm growth and decline; (b) several data sources to identify CEOs and their status as entrepreneurs or hired executives over the same period; (c) a sample of the general Finnish population matched based on gender, age, educational attainment, and income level; and (d) comprehensive individual health data for 2000 to 2021 including heart attacks, strokes, cancer, type-2 diabetes, and deaths. The health data allow us to both control for past health conditions and examine the stress-related, serious health consequences of firm growth and decline.

Our study contributes to the burgeoning stream of research on entrepreneurial health (for reviews, see Lerman et al., 2021; Stephan, 2018), which yields limited and fragmented findings on how severe health consequences of entrepreneurial stress fueled by venture growth or decline unfold over time (Rauch et al., 2018; Shepherd & Patzelt, 2017). By using unique and robust longitudinal data, we demonstrate that (a) episodic, rapid decline and cumulative exposure to growth in sales and the number of employees is equally taxing for entrepreneurs and hired CEOs and (b) while entrepreneurs and hired CEOs are healthier and live longer than the matched sample from the general population, entrepreneurs are more likely to fall ill during their tenure 1 than hired CEOs. In doing so, we not only add to our understanding of entrepreneurial health (Shepherd, 2019) but also respond to the general calls in the management literature for more inquiries into the physiological effects of work stress (Gonzalez-Mulé & Cockburn, 2021; Keloharju et al., 2023), especially using hard medical outcomes (Bliese et al., 2017).

Theoretical Background and Research Questions

Stressors, Strains, and Health Outcomes

The principal idea of the CHSF is that the type of stressor (the condition that causes stress) is more important than the level of stress (Cavanaugh et al., 2000; LePine et al., 2005). CHSF further posits that it is possible to predict well-being outcomes based on the type of stressor without measuring perceived stress because people react to stressors in consistent ways. The predictions of CHSF have gained support in prior research across different organizational outcomes (see e.g., LePine et al., 2005; Lerman et al., 2021, for meta-analytic evidence).

CHSF distinguishes between two types of stressors (LePine et al., 2005). Challenge stressors comprise obstacles that can be tackled with the prospect of positive outcomes, such as learning, achievement, job satisfaction, and personal growth. Examples of challenge stressors include high workload, tight deadlines, complex projects, and a high level of responsibility. Hindrance stressors, on the other hand, refer to obstacles that thwart goal attainment and personal growth, such as organizational politics, time pressure, bureaucracy, lack of resources, and interpersonal conflicts. Challenge stressors can increase motivation because individuals expect the effort expended to cope with the demand to generate positive results, whereas hindrance stressors diminish motivation because people think that no reasonable effort will be enough to meet the demands (Lazarus & Folkman, 1984). While challenge stressors can be positive and constructive for performance, both challenge and hindrance stressors are related to strains, including burnout, fatigue, and psychological and physical symptoms (LePine et al., 2005; Lerman et al., 2021; Mazzola & Disselhorst, 2019).

CHSF applies the stressors–strains perspective in which stressors are environmental stimuli that cause strains, which, in turn, are individual’s psychological and physiological responses to those stimuli, including exhaustion, depression, headaches, and chest pains (LePine et al., 2005; Lerman et al., 2021). Such strains can lead to adverse health outcomes, especially if the individual is exposed to heavy stressors either repeatedly or over long periods of time (Gonzalez-Mulé & Cockburn, 2017; Juster et al., 2010). Thus, physiologically, stress is a highly complex combination of the body’s responses to stressors (Juster et al., 2010).

Prior studies have examined the long-term physiological consequences of stress by drawing on the AL model (McEwen & Stellar, 1993). The AL model proposes that an individual’s body maintains stability by adjusting its internal processes—cardiovascular, metabolic, and neuroendocrine—to accommodate the burden caused by stressors such as by elevating blood pressure, changing appetite, and releasing stress hormones (Gonzalez-Mulé & Cockburn, 2021). While temporary adjustments are not problematic, episodic, or prolonged exposure to stress can make these physiological changes the “new normal” (Selye, 1955). This can lead to chronic over-activity of physiological systems, which shows in an elevated AL, or “wear and tear” on the body and brain (Juster et al., 2010). Thus, the AL model predicts that unresolved stress leads to declining physical health as a proximal outcome and to severe, potentially life-threatening health conditions and ultimately death as distal outcomes (Gonzalez-Mulé & Cockburn, 2021).

Stress, Entrepreneurs’ Health, and Venture Growth

Typical stressors that entrepreneurs are exposed to include high levels of uncertainty, cash flow concerns, high workload, substantial responsibility over the venture, and serious resource constraints (Boyd & Gumpert, 1983; Obschonka et al., 2023; Rauch et al., 2018; Stephan, 2018). In addition, entrepreneurs usually have significant personal, financial, and emotional stakes in the business, which give rise to the threat of substantial losses should the venture not succeed (Cardon et al., 2005; Cardon & Patel, 2015; Douglas & Shepherd, 2002; Ucbasaran et al., 2013). Furthermore, entrepreneurship erodes boundaries between work, leisure, and family life, which makes it intensely demanding and leaves little scope for entrepreneurs to detach from work (Williamson et al., 2021). Long work hours typical of entrepreneurs can be psychologically and physiologically taxing (Lerman et al., 2021). These features make entrepreneurs generally susceptible to high levels of stress and strain, which causes high levels of AL and can lead to adverse health outcomes (Lerman et al., 2021; Patel et al., 2019). For example, Patel et al. (2019) found that particularly over longer periods of time, entrepreneurs experience higher levels of AL than employees, leading to reduced physical health.

However, research evidence on the relationship between entrepreneurship and stress is equivocal. While some studies find entrepreneurs to have higher stress levels than comparison groups (Cardon & Patel, 2015; Lee et al., 2023), others point to the opposite conclusion of entrepreneurs experiencing lower levels of stress (Baron et al., 2016; Hessels et al., 2017; Obschonka et al., 2023). An explanation for the finding of low stress levels is that entrepreneurs are in a better position to cope with stressors than employees because of greater degrees of autonomy and control over their work, which allows more agency in stress regulation (Demerouti et al., 2001; Hessels et al., 2017; Obschonka et al., 2023; Ryff, 2019). Studies have also found entrepreneurs to have higher levels of locus of control, psychological capital, and tolerance for ambiguity than non-entrepreneurs, which increase entrepreneurs’ stress resistance (Baron et al., 2016; Cardon & Patel, 2015; Lerman et al., 2021).

Inconsistent research findings may be due to the heterogeneity of entrepreneurs: a random sample of self-employed individuals will mostly contain people operating small and very small businesses, who experience different levels and types of stressors than entrepreneurs running larger or growing ventures. The health differences may also depend on the timing of the health assessment: healthier individuals may be more likely to become entrepreneurs initially (selection effect), but their health may not develop more favorably over time while being an entrepreneur (health effect). Another factor influencing research findings is that self-appraisals are commonly used to measure stress. For example, entrepreneurs who mainly cope with challenge stressors can feel highly motivated and may thus not find their work particularly stressful and, as a result, do not feel adverse well-being effects (Lerman et al., 2021; Patel et al., 2019). Thus, the mix of entrepreneurs and the measurement approach (self-reported strain versus actual physical health) will affect the results.

While there are multiple ways to model the effects of exposure to stressors, most of the epidemiological literature uses a measure of cumulative exposure, with interest in incorporating intensity and duration in assessing the risk of physical diseases and mortality (de Vocht et al., 2015). Even though prior research on the health consequences of managing a growth venture is virtually nonexistent, research from other contexts provides indirect support for the argument about the potentially adverse health consequences of growing organizations and related responsibilities. Nicholas (2023) found that top-level managers at General Electric died 3 to 5 years earlier than their counterparts in lower-ranking positions. Furthermore, Borgschulte et al. (2019) found that CEOs who exclusively served under strict governance were more likely to pass away while in office or within the first 5 years of stepping down as CEO. Also serving as a CEO during an industry-wide downturn decreased life expectancy by 1.5 years (Borgschulte et al., 2021), indicating that intense managerial responsibilities cause stress that has an impact on life expectancy. Similar to entrepreneurial and managerial responsibilities, Olenski et al. (2015) found that political leadership is also related to higher odds of premature mortality. They investigated elected and unelected “runner-up” candidates in parliamentary and presidential elections in 18 countries from 1722 to 2015 and found that candidates who served as a head of government lived 2.7 fewer life-expectancy-adjusted years after their last election than runners-up.

Nevertheless, we acknowledge that there is the possibility of a null or even the opposite result. For example, Stephan et al. (2020, 2023) did not find a significant relationship between self-employment and physical health, whereas Lerman et al. (2021) found a weak relationship between physical health and hindrance (but not challenge) stressors. Gonzalez-Mulé and Cockburn (2017, 2021) found job demands to be negatively related to the risk of death in high-control jobs. Finally, Keloharju et al. (2023) found that the CEO job did not take a substantial toll on the sampled Swedish executives because people selected to these positions were healthier than the comparison groups to begin with. Hence, we put forward the following exploratory research questions:

RQ1: Do the health histories of entrepreneurs and hired CEOs differ from a socio-economically similar random sample at the time of assuming their role?

RQ2: Do entrepreneurs and hired CEOs differ from a socio-economically similar random sample in their risks of disease onset or mortality during their tenure?

We also propose that exposure to firm growth, such as increases in sales (Davidsson & Wiklund, 2017; Weinzimmer et al., 1998) and in the number of employees (Penrose, 1959; Shepherd & Wiklund, 2009), comes with a particularly wide array of intense stressors. Some of them may be hindrances (e.g., administrative hassles, conflicts among the board members), while the majority are arguably challenges with high workload, tight deadlines, managing team members, and a high level of responsibility. More specifically, high growth in sales is a potential challenge stressor, as sales growth frequently requires establishing and expanding marketing and distribution networks (Lechner & Dowling, 2003), scaling up manufacturing processes (Arend & Wisner, 2005), and developing new organizational capabilities to expand in international markets (Knight & Cavusgil, 2004). These arguments are in line with White and Gupta (2020, p. 86), who state that, “Building market demand or capturing it from rivals […] could be […] a significant stressor for practicing entrepreneurs.”

Relatedly, high growth in the number of employees may intensify challenge stressors for the entrepreneur (Hessels et al., 2017). While the seminal work of Greiner (1998) highlights the general coordination challenges of a growing organization, recent studies advance the discussion by stating that “identifying, hiring, and retaining quality employees” can be a major stressor for entrepreneurs (e.g., White & Gupta, 2020, p. 86). Further studies identify concern for employees as a key obstacle for pursuing growth (McKelvie et al., 2021; Wiklund et al., 2003). Simultaneously, one of the major implications of growing firms is the time spent on issues related to human resources, including recruiting, training, and managing core employees (Chandler et al., 2009; Fischer et al., 1998; Sims & O’Regan, 2006). In line with the strong sense of personal responsibility over the firm, a growing organization may give rise to additional stressors, as entrepreneurs are argued to “bear the cost of their mistakes and those of their employees” (Cardon & Patel, 2015, p. 383).

Thus, although venture growth can be predominantly perceived as a challenge stressor, intensive or prolonged exposure to the stressor may lead to AL and thus exposure to physical strain, resulting in higher odds for serious, stress-related physiological events or even mortality. To scale and reconfigure the required resources and capabilities for growth, such an intense or prolonged increase in managerial tasks and responsibilities can force entrepreneurs to extend (beyond) the limits of their existing knowledge and skills (Baum et al., 2001; Wiklund & Shepherd, 2003). As a result, they experience multiple stressors that are of greater magnitude than those faced by entrepreneurs who are not growing their businesses. Exposure to the conditions required to achieve growth may cause strain and physical exhaustion (Boyd & Gumpert, 1983; Lerman et al., 2021), which can lead to serious health issues in the long run (Bakker et al., 2003; Gonzalez-Mulé & Cockburn, 2017, 2021).

While our argumentation above draws on the entrepreneurship literature, we acknowledge that such exposure to growth in sales and/or number of employees may be straining and hazardous also for hired CEOs. Even though hired CEOs may not have a similar personal stake in the company as entrepreneurs, they face many of the same stressors associated with managing a growing venture, such as high workload and a high level of responsibility. With this in mind, we put forward the following exploratory research question:

RQ3: Does high growth in sales/employees influence the health and mortality risks of entrepreneurs and hired CEOs?

Moreover, we suspect that managers who experience declining businesses may face severe hindrance stressors, especially when exposed to a prolonged and/or intense decline. More specifically, the concern about employees during declining business may be an extremely significant stressor. Lefebvre (2024), for instance, found that the strong interpersonal ties between employees and managers make it hard for small- and medium-sized enterprise owners and managers to dismiss employees. Or as Torres (2011) put it, “laying off someone is the most difficult as well as the hardest to live with.”

Furthermore, while the above might hold true both for entrepreneurs and hired CEOs, we also suspect that the intensity or cumulative load of responsibilities in declining business is going to be higher for entrepreneurial leaders than hired managers. This is based on two reasons. To begin with, entrepreneurs face acute personal risks as they typically have to put their own skin in the game by, for example, signing personal collateral to fund the venture, which increases entrepreneurs’ financial exposure and strain (Cope, 2011). Thus, entrepreneurs who experience declining businesses with high personal debt “that takes years to clear” (Ucbasaran et al., 2013, p. 175) are likely to face serious stress, as it is known that “poverty is toxic for one’s psychological health” (Santiago et al., 2011, p. 218). Previous studies support this by suggesting that experienced financial problems (Gorgievski et al., 2010) and uncertainty about income (Schonfeld & Mazzola, 2015) increase entrepreneurs’ stress and that declining economic conditions decrease their well-being (Annink et al., 2016). Relatedly, often seeing their enterprises as their babies (Cardon et al., 2005), and even bonding at neural level (Lahti et al., 2019), entrepreneurs are at a relatively greater risk of putting the “health” of their business before their own health—possibly even more so than hired managers. We put forward our fourth exploratory research question:

RQ4: Does a substantial decline in sales/the number of employees influence the health and mortality risk of entrepreneurs and hired CEOs?

Methods

Sample: Inclusion and Exclusion Criteria

We pursue our inquiry using data sourced from several firm- and person-level registers in Finland (for a summary of the data sources, see Supplemental Appendix 1). The dataset includes the entire population of Finnish companies with revenues of 500,000 euros or higher in 2017. As such, our sample includes companies that a few years earlier were just getting started and had no revenues, but that become established firms with revenues of note during our study timeframe. The 500,000 euro mid-panel threshold thereby excludes microfirms or hobby companies (e.g., solo, part-time, and nascent-stage entrepreneurs toward the end of the panel). We track each firm’s performance and growth from 2000 to 2021 by using audited financial statement data.

Furthermore, for each firm, we have access to the identities and operative periods of the CEOs. The CEOs were identified using information from the Finnish Patent and Registration Office and subsequently identified (their personal IDs were retrieved) with the help of the Digital and Population Data Services Agency. We also have data to identify whether these individuals were entrepreneurs or salaried managers at any given time. We exclude CEOs with very short tenures (e.g., <1 year), as they are not likely subject to the challenges that we otherwise attempt to study. Finally, we have personal data on their gender, age, education level, and income as well as a variety of health-related information. We combine the data from various official sources into a single panel using the Finnish social security ID numbers for individuals and firm ID numbers from the Business Register for the companies. The processing of sensitive data was done using the secure servers of Statistics Finland to preserve the anonymity of the individuals included in the analysis. Supplemental Appendix 2 presents further details on the ethical considerations of using such personal data.

To complement the focal sample of entrepreneurs and hired managers and their firms, we also have a socio-economically similar random sample (a matched control sample or matched controls for short) of the general Finnish adult population who were matched with the CEOs based on gender, age, education level, and income bracket. Similar to previous studies (e.g., Dahl et al., 2010; Keloharju et al., 2023; Lerner et al., 2021), we use the matched sample to compare and contrast the health of entrepreneurs and hired managers with that of the matched population before and after the entrepreneurs and salaried managers assumed their role. The matched control sample is approximately twice the size of the focal sample. The number of observations varies considerably across analyses, especially when pre-health variables are included. The number of observations is denoted in the tables for each analysis.

Dependent Variables

Our dependent variables comprise disease outcomes and causes of death that have previously been associated with high work stress. Epidemiological studies have associated work-related stressors (e.g., job strain, effort-reward imbalance, long working hours), especially with a higher risk of stroke and coronary heart disease (CHD) (Kivimäki, Jokela, et al., 2015; Kivimäki & Steptoe, 2018) and type-2 diabetes (Ervasti et al., 2021; Kivimäki, Virtanen, et al., 2015; Nyberg et al., 2014). Evidence for cancer risk has been equivocal: one multi-cohort analysis found no association between work stress and cancer risk (Heikkilä et al., 2016), whereas a meta-analysis found work stress to be associated with a higher risk of cancer (Yang et al., 2019). We obtained this data for each individual in our focal sample (and the matched control sample) for 2000 to 2021.

Ischemic Heart Disease

We build upon Kivimäki et al. (2006), who conducted a meta-analysis on estimating the relative risk of CHD and work stress and found that there is an average 50% excess risk for CHD among employees with work stress. For capturing severe diagnosed heart diseases, we rely on two registries, both collected by the Social Insurance Institution of Finland. The first registry keeps records of diagnostics data regarding rights to apply medical reimbursements from the government. These reimbursement rights (diagnosis, start month + end month) are recorded with International Classification of Diseases (ICD-10) codes. We focus on ischemic heart diseases (I20–I25 as an aggregate variable), including CHD (angina pectoris, I20) and heart attack (acute myocardial infarction, I21). The second registry keeps records on an individual’s prescribed and reimbursed medicine purchases (date of purchase, number of packages). This registry categorizes medicines with the Anatomical Therapeutic Chemical (ATC) classification. We focus on medicines in the category of cardiac therapy (C01). However, category C01 also includes some medicines for non-severe heart problems, such as arrhythmia. Hence, we use both of these measures to capture severe heart diseases.

Cerebrovascular Diseases

We build on Kivimäki, Jokela et al. (2015), who found that long working hours were associated with an increased risk of death due to cerebrovascular disease in a multi-cohort analysis of ~600,000 participants. Fransson et al. (2015) also found high job strain to predict higher stroke risk. For capturing such diseases, we rely on the two registries collected by the Social Insurance Institution of Finland. We use the ICD-10 codes for cerebrovascular diseases (I60–I69) as separate variables including stroke (I63) and cerebrovascular accident (I61) to retrieve the diagnoses from the registry of medical reimbursement rights. Again, we also rely on the registry of prescribed and reimbursed medicine purchases (date of purchase, number of packages). Aligned with the ATC classification, we focus on medicines in the category of antithrombotic medicines (B01), which are widely used for stroke survivors to prevent recurrence (Del Brutto et al., 2019).

Type-2 Diabetes

Studies of long working hours (Kivimäki, Virtanen et al., 2015) and job strain (Nyberg et al., 2014) have shown that the incident rate of type-2 diabetes (i.e., adult-onset diabetes) is higher among individuals with higher levels of work stress. We use ICD-10 code E11 to identify cases of type-2 diabetes. Medicine purchases of glucose-lowering medications (A10) are included as additional indicators of type-2 diabetes.

Cancer

Although the evidence regarding the association between job stress and cancer is inconclusive, the most recent meta-analysis suggests an association, especially for esophageal, colorectal, and lung cancers (Yang et al., 2019). Therefore, we included it as one of the health outcomes. In doing so, we rely on the diagnostics data regarding the rights to apply medical reimbursements from the government (ATC classification L01). We focus on ICD-10 codes C00 to C97 (all malignant cancers) and D00 to D09 (carcinoma in situ, cancer in stage 0) as an aggregate variable to capture individuals who have been diagnosed with cancer.

Date and Cause of Death

Statistics Finland (2020) records the dates and underlying causes of death according to the ICD-10 compiled by the WHO. We follow Kivimäki et al. (2003) and analyze all-cause mortality and in a supplemental analysis, also cause-specific mortality within seven major categories. 2

Independent Variables

Tenure of Entrepreneurs Versus Hired CEOs

Following established literature, we define an entrepreneur as a person who performs work for personal profit rather than for wages paid by others (Shane, 2003) and holds a leading managerial position with ownership (Gartner, 1990). In contrast, a hired CEO is hired to manage a firm owned by someone else. We identify entrepreneur-CEOs using data from The Finnish Centre for Pensions. 3 The tenure of entrepreneurs (and hired CEOs respectively) starts the year they start working in their roles and ends when they either end working in that role for their respective firm, or our follow-up ends.

Growth/Decline in Sales and Number of Employees

We operationalize growth using three distinct measurement approaches to reflect its heterogeneous nature. First, as our main measure, we focus on relative (AmountTime1 − AmountTime0)/AmountTime0) growth rates over a 3-year period (Delmar et al., 2003; Shepherd & Wiklund, 2009). This allows us to understand the more nuanced implications of growth, where adding 10 new employees may be extremely significant (for a 10-person firm) or relatively modest (for a 500-person firm) and thereby lead to differential health outcomes. More specifically, we use the OECD (2007) definition that describes high-growth firms as those with at least 10 employees and with annualized positive growth (and analogously, negative for a rapid decline) in revenues exceeding 20% during a 3-year period. Thus, for each 3-year period, we explore if the company was a high-growth or a declining firm (0 = stable, 1 = growth, 2 = decline). In the regression models, high-growth firms and firms with declining sales are compared to the reference group of stable firms. We use the same analogy to also capture high growth and substantial decline in terms of employees, recognizing that the efforts and outcomes to achieve growth in each of these metrics may be varied.

Second, we capture the prolonged (cumulative) exposure to growth/decline (de Vocht et al., 2015) over the years using the same OECD (2007) 20% cutoff. Thus, in our second operationalization, we study the impact of cumulative exposure over the years (instead of 3-year periods). Here, the measure indicates the number of consecutive years of growth/decline that the firm (the CEO) has experienced up to that year. Third, we look at the intensity of short-term growth/decline during each 1-year period (growth rate within 1 year). This allows us to tap into the episodic rapid growth/decline of companies and investigate whether it is the fast but intensive episodes (e.g., hockey stick growth) rather than the long-term cumulative exposure that is harmful to health (Daunfeldt & Halvarsson, 2015; Delmar et al., 2013). We winsorize the short-term growth/decline data at the 1% level.

Combined, our approach to capturing growth takes into account important measurement and temporal components (3- and 1-year periods, prolonged exposure to growth/decline and episodic rapid growth/decline) that reflect the current methodological practice in the growth literature (Coad & Srhoj, 2020; McKelvie & Wiklund, 2010; Nason et al., 2019; Shepherd & Wiklund, 2009) as well as allows us to empirically examine delays between growth/decline episodes and health impacts.

Control Variables

We control for the individual’s age and gender, in line with research in epidemiology (e.g., Kivimäki et al., 2003) and on CEO health (Keloharju et al., 2023). When studying our research questions 2, 3, and 4, we also provide analyses where we control for the individuals’ baseline health by including their health history (pre-health) in the analysis, operationalized as the prevalence of any previous diseases of the four disease categories (heart attacks, strokes, type-2 diabetes, and cancer) in the preceding year before baseline. Additionally, we include industry- and year-fixed effects to adjust the models for macro-level influences in our analyses related to research questions 3 and 4.

Analysis Approach

In our analysis of research question 1, the dependent variable is the prevalence of any of the four disease categories (e.g., ischemic heart disease, cerebrovascular diseases, type-2 diabetes, and cancer) up to 10 years before the study baseline. We define the study baseline for each CEO as the year when the CEO tenure begins (year 0). The analysis is done by comparing the annual disease prevalence in 0, −1, −2, …, and up to −10 years before baseline, analyzed with logistic regression in which the years are nested within the participants. Cluster-robust standard errors are estimated to account for the non-independence of the repeated person-observations from the same participants. The main comparisons are between CEOs and a socio-economically similar random sample (matched controls), and entrepreneurs versus hired CEOs, adjusted for age and gender. This is tested as the interaction between the CEO indicator and year (coded as a categorical and continuous variable in different models).

For research question 2, in the main analysis, the dependent variables are (a) the prevalence of any of the four diseases after the individual started as CEO (hired or entrepreneur) and (b) death. We predict this outcome in the same way as in RQ1, predicting disease or mortality risk annually from year 0, +1, +2, …, up to +10 years after baseline, analyzed with logistic regression in which the years are nested within the participants. The main comparison is between entrepreneurs versus hired CEOs, and CEOs (hired and entrepreneurs) compared to the matched controls, adjusted for age and gender. This is tested as the interaction between the CEO indicator (entrepreneur/hired) and year (coded as a categorical and continuous variable in different models). In addition to the analysis of CEOs during their tenure, we include a group of CEOs whose tenure ends during the follow-up (i.e., if their tenure is less than 10 years), which gives us information on the health status of CEOs whose poor health may have influenced their exit from the CEO position.

To examine whether the changes in health during tenure reflect any differences in health before tenure, we also examine the disease-risk associations in a sub-sample of participants who do not have any of the diseases before baseline. The difference in the mortality risk in years between entrepreneurs and hired CEOs was assessed with discrete-time survival analysis, that is, participants were followed until their death or the end of the follow-up period, whichever came first. After this, the participant was censored from the mortality-risk analysis.

The analysis of research questions 3 and 4 exclusively focuses on the CEOs, comparing the entrepreneurs and the hired CEOs. The dependent variable is the annual incidence of any of the four disease categories or death. The main exposure variable is the average growth or decline of sales and number of employees in the three preceding years in which the disease/death incidence is assessed. The analysis is fitted with logistic regression in which years are nested within the participants, adjusted for gender and birth year. In addition, the models are adjusted for industry and year fixed effects to account for macro-economic influences. Finally, we rerun the models restricted to participants who did not have diseases in the year before the baseline up to the assessment year. As a supplemental analysis, we examine each disease category (heart disease, cerebrovascular disease, type-2 diabetes, and cancer), as separate dependent variables. 4

Results

Main Findings

The mean CEO age was 47 years. The CEOs were predominantly (81%) male with a level of education on average equivalent to a Bachelor’s degree. We first assessed the matching quality relying on the basic information about matching demographics across gender, age, education, and income bracket (for descriptives, see Supplemental Appendix 3). Using t-tests, we compared our focal CEO sample with the matched controls. Matched controls were not substantially different from the CEOs in terms of their age, gender, or education at the time of matching. The CEO income was somewhat (statistically significantly) higher than that of the matched controls, however, especially if they were active in CEO roles at the time of matching. When comparing the entrepreneurial and hired CEOs during their tenure, we can see that the entrepreneurs were somewhat more likely to be male, older, less educated and with higher incomes than the hired CEOs. These figures need to be interpreted with the average tenure of the two groups in mind, as the average tenure of the entrepreneurs during our panel (2000–2021) was 12.9 years (SD 9.6), which was substantially longer than that of hired CEOs (5.2 years, SD 8.2). 5 While the companies led by entrepreneurs were smaller than that of hired CEOs, there were no large differences in their median growth rates.

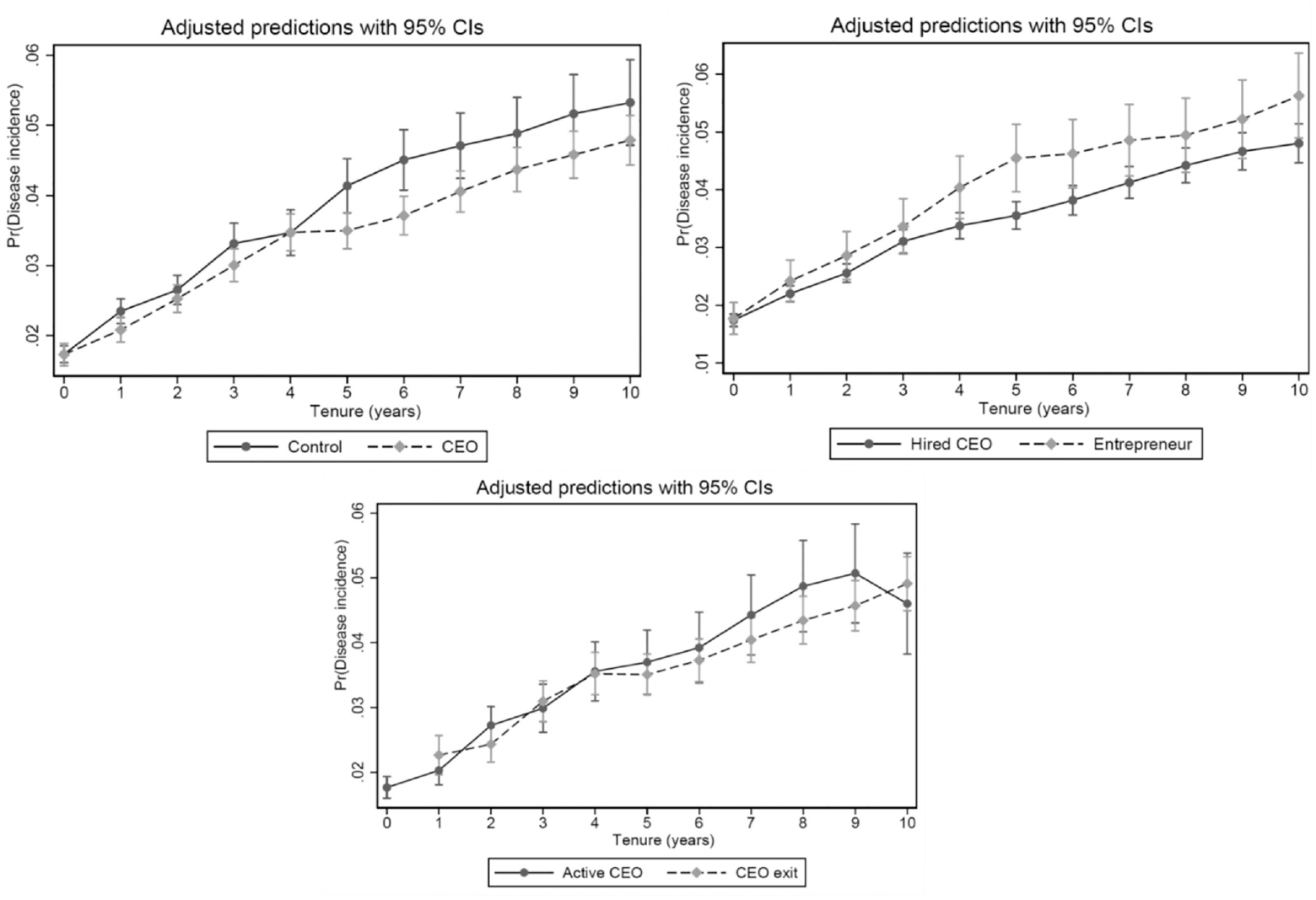

In our first research question, we asked if the health histories of entrepreneurs and hired CEOs differed from each other and from a socio-economically similar random sample at the time of assuming their role. Table 1 shows that the average health of entrepreneurs does not differ from that of the hired CEOs before tenure (OR = 1.00, SE = 0.08), and this difference does not change over the 10-year pre-tenure period (OR = 1.00, SE = 0.00; see also Figure 1). The average health of CEOs (including both hired and entrepreneurs) is slightly better compared to matched controls (OR = 0.95, SE = 0.03, p < .10). This association does not change over the 10-year period before tenure (OR = 1.00, SE = 0.00 for the interaction between continuously coded time and CEO versus control comparison; see Figure 1).

Incidence of Diseases and Mortality: Differences Between CEOs (Hired, Entrepreneur, Exiting) and Matched Controls.

*Note. In this table, we predict the incidence of diseases and mortality of entrepreneurs and hired CEOs during their tenure to exited CEOs and matched controls. Change over time is estimated as an interaction effect with time. Mortality risk was assessed in the whole sample, following CEOs after their exit. Values are odds ratios intervals. SE in parentheses. Estimates and sample sizes from an analysis adjusted for pre-tenure health conditions are reported in square brackets. na = not applicable. Statistically significant findings bolded.

#p < .10. *p < .05. **p < .01. ***p < .001.

Probability of disease incidence before entrepreneurs and hired CEOs before start of tenure, compared to matched controls.

In our second research question, we asked if entrepreneurs and hired CEOs differ from a socio-economically similar random sample in the risks of disease onset or mortality during their tenure. Our results displayed in Table 1 indicate that entrepreneurs have a higher disease risk compared to hired CEOs during their tenure (OR = 1.13, SE = 0.07, p < .05). Our supplemental analysis suggests that this association is somewhat stronger when the analysis is restricted to those individuals who did not have any diseases before tenure (OR = 1.23, SE = 0.10, p < .05), suggesting that these health differences emerge during tenure (see Figures 2 and 3). The difference between entrepreneurs and hired CEOs remains stable over the tenure period (OR = 1.00, SE = 0.00 for interaction with continuously coded time).

Probability of disease incidence after entrepreneurs and hired CEOs start their tenures, compared to matched controls and exiting CEOs.

Probability of disease incidence after entrepreneurs and hired CEOs start their tenures, compared to matched controls and exiting CEOs: the analysis is adjusted for pre-tenure health conditions.

The mortality risk of entrepreneurs is slightly higher compared to hired CEOs (OR = 1.27, SE = 0.17; p < .10), and this association is stronger, but not statistically significant, when examined only among those without any disease at baseline (OR = 1.40, SE = 0.31). The more conservative (OR = 1.27) estimate would translate into a 1.8-year difference in life expectancy after the age of 50 years (based on absolute age-specific mortality risks derived from the Finnish population life tables compiled by Statistics Finland, stat.fi). The cause-specific estimates are imprecise with wide confidence intervals, but the entrepreneurs’ higher mortality risk is somewhat more prominent for smoking-related deaths (OR = 1.72, SE = 0.54, p < .10).

Compared to the matched control group, CEOs (including both hired CEOs and entrepreneurs) have a lower risk of disease (OR = 0.92, SE = 0.03, p < .01) during their tenure, and this is observed even when including only those without disease before tenure (OR = 0.90, SE = 0.03, p < .01). This difference remains stable throughout the tenure follow-up period (OR = 1.00, SE = 0.00 for continuously coded interaction with time). CEOs who exit their position during the 10-year follow-up period have on average poorer health than those who remain in their position (OR = 1.18, SE = 0.05, p < .001). This association is not different for entrepreneurs compared to hired CEOs (OR = 0.94, SE = 0.08) and does not vary over time (OR = 1.01, SE = 0.01). CEOs have a lower mortality risk compared to the matched control group (OR = 0.23, SE = 0.01, p < .001), and this holds for all cause-specific associations as well. The estimate is the same when controlling for previous health conditions (OR = 0.23, SE = 0.02, p < .001). However, the mortality difference is amplified by the fact that the CEOs were very unlikely to die within the first 5 years of their tenure (mortality rate 1.2 per 10,000 person-years), whereas individuals in the matched control group did not have a similar selection effect (mortality rate 149.1 per 10,000 person-years). In other words, compared to the general population, CEOs initially face very low mortality rates. More broadly however, while the dataset covers two decades of medical records, given the limited mortality observations by the end of the panel, the estimate cannot be taken as the overall mortality risk difference between CEOs and individuals in the control group (but only as the difference between starting CEOs and the control group).

In our research questions 3 and 4, we asked if high growth (RQ3) and substantial decline (RQ4) in sales/the number of employees influence the health and mortality risks of entrepreneurs and hired CEOs. Our results in Table 2 show that the average 3-year growth in personnel (OR = 1.18, SE = 0.11, p < .05) is associated with a higher disease risk, whereas growth in sales is not statistically significant (OR = 1.06, SE = 0.07). Similarly, the cumulative growth is related to higher risk. This is particularly true for growth in employees, for which the odds of disease risk increase 1.24-, 1.34-, and 1.40-fold with 1, 2, and 3 growth years, respectively. Thus, the disease risk of cumulative growth is heightened over time (OR = 1.17, SE = 0.05 for linear trend, p < .001). The health risks of episodic decline are observed when 1-year changes in revenues and employees are estimated as continuous variables and driven by decline in both sales (OR = 1.49, SE = 0.13, p < .05) and employees (OR = 1.72, SE = 0.13, p < .05). The health risk of a 1-year decline does not differ for entrepreneurs and hired CEOs. When including only participants who did not have any diseases at baseline, the associations between sales and employees decline/growth and disease onset are attenuated, but the attenuated estimates are within the confidence intervals of the initial estimates. The overlap between point estimates and confidence intervals indicates that the differences are not statistically significant.

Incidence of Diseases Associated With Growth/Decline in Sales and Personnel.

Note. Values are odds ratios. See Supplemental Appendix 5 with a more detailed analysis on the incidence of stroke, heart attack, type-2 diabetes, and cancer. Statistically significant findings bolded.

*p < .05. **p < .01. ***p < .001.

We also fitted the corresponding logistic regression models for mortality risk (research questions 3 and 4), but there were too few deaths to estimate these associations with changes in sales and employees; many of the covariates-value cells (e.g., industry categories) included no deaths. Therefore, results related to mortality risk related to growth/decline are not reported here.

Supplemental Analysis

We conducted a supplemental analysis on each disease onset separately, after we first examined whether each firm growth/decline measure predicts the onset of any of the four diseases considered together (see Supplemental Appendix 5). In total, we performed 48 tests to explore how the six growth/decline measures (1-year short term, average, cumulative growth, and decline) in sales and employees are associated with the onset of the four diseases (type-2 diabetes, CHD, cerebrovascular diseases, and/or cancer). Out of the 48 tests, seven were statistically significant. Using the Benjamini and Hochberg (1995) false discovery rate correction (see Supplemental Appendix 6), all the statistically significant associations with specific diseases were below the critical values of the test, suggesting that they were unlikely to be false positives. This supplemental analysis suggests that the disease risks observed were mainly driven by type-2 diabetes, and to some extent cerebrovascular diseases and ischemic heart disease, but not cancer.

Discussion

This study yields significant contributions to the quickly advancing body of work on health and entrepreneurship. First, our findings demonstrate that although entrepreneurs start their tenure with similar health conditions as hired CEOs, entrepreneurs are more likely to develop serious illness during their tenure compared to hired CEOs. Relatedly, we found that on average, entrepreneurs die 1.8 years earlier than hired CEOs. We also found that entrepreneurs’ tenures are substantially longer than those of hired CEOs. Hence, the findings support the notion that entrepreneurs’ personal, emotional, and financial commitments and responsibilities (Cardon et al., 2012) can be so overwhelming that they override the rational decision to take care of oneself.

Prior literature suggests that entrepreneurship affords opportunities for self-realization and high levels of job control, which not only facilitate a passion for and perseverance in running the business, but they also help in coping with stress (Baron et al., 2016; Cardon & Patel, 2015; Shepherd & Patzelt, 2015). Our results point to an underlying complexity beneath the seemingly positive outlook. They suggest that the demanding nature of entrepreneurial work can be, over time, hazardous to one’s health and even reduce the entrepreneur’s expected lifespan. Thus, our findings shed new light on the “dark, downside, and destructive side” of entrepreneurship (Shepherd, 2019). However, it is important to note that in our analysis, entrepreneurs’ health risks are higher only in comparison to hired CEOs, rather than a socio-economically similar general population (matched sample). This is aligned with previous research (Keloharju et al., 2023; Rietveld et al. 2015) that found CEOs to be healthier compared to their socio-economic peers both at the beginning and during their tenure.

Second, our study adds to the literature by examining the health consequences of firm growth and decline. Our findings demonstrate that cumulative exposure to prolonged growth in sales and particularly in the number employees takes its toll and leads to adverse health outcomes. Hence, the concerns related to human resources, such as recruiting, training, and managing employees, seem to be major stressors (Hessels et al., 2017; McKelvie et al., 2021; White & Gupta, 2020) when the firm is going through an expansion phase. With this finding, we answer the call of Shepherd and Patzelt (2017, p. 222) who point to numerous opportunities to “learn more about how stress links to […] venture growth” by demonstrating that, for example, managing growth in human resources has consequences on entrepreneurs’ health.

Similarly, our findings suggest that a rapid, episodic decline in sales or in the number of employees is taxing for entrepreneurs’ (and hired CEOs) physical health. Interestingly, a longer decline may not yield similar health hazards to a sudden and perhaps shocking 1-year drop as managers may have time to incrementally adjust the firm’s operations to the deteriorating situation. This is in line with prior studies that have found adverse health effects of a sudden, industry-wide downturn (Borgschulte et al., 2021), as well as those suggesting that a sudden need to lay off employees can be a major stressor (Lefebvre, 2024; Torres, 2011). Hence, while a business failure is a major source of “severe stress reactions” (Rauch et al., 2018, p. 348), even a rapid decline seems to be a stressful experience with adverse health consequences.

Even though our registry-based data does not capture challenge and hindrance stressors per se, it is intuitive to expect that prolonged cumulative growth is associated with motivating challenge stressors whereas a rapid decline yields hindrance stressors that are demotivating and difficult to manage. Furthermore, we need to bear in mind that according to the AL model the mechanisms through which strain leads to physical consequences are the same for both types of stressors (Juster et al., 2010). Our findings reveal that a prolonged exposure to cumulative, higher than 20% year-over-year growth has health consequences and that a 1-year long episodic decline (drop in sales and in the number of employees) can create health risks. Interestingly, the findings regarding growth and decline apply to both entrepreneurs and hired CEOs. While there may be some variation among the causes of stress between entrepreneurs (e.g., personal financial risks, emotional bonds) and hired CEOs (e.g., pressure from the board), our findings suggest that leading a steadily growing or a suddenly declining firm is equally taxing for entrepreneurs and hired CEOs.

Our study offers implications for practitioners and policymakers. Interested stakeholders beyond academia include existing entrepreneurs and their families, the entrepreneurs of the future (e.g., students), entrepreneurial hubs and accelerators, and policymakers. Start-up hubs and accelerators could support their resident entrepreneurs by offering health-related services (e.g., bi-annual check-ups, nutrition coaching), facilities for exercise or meditation, HR-related support for entrepreneurs who are hiring employees, and peer-support sessions to share best practices on how to tackle the managerial challenges of venture growth and how to cope with stress. Finally, we also encourage entrepreneurs’ board of directors, advisors, co-founders, and families to observe and ask how entrepreneurs are doing and provide help if needed.

Limitations and Suggestions for Future Research

Despite its significant strengths, this study must also be evaluated given its limitations. First, a distinctive strength of our study is that our health data come from the population registries of the Finnish healthcare system. Thus, selective attrition in terms of health-related drop-out from the sample (e.g., non-response to survey questionnaires due to poor health) is not a problem, as follow-up health data are available for all participants regardless of their health status. That said, the access to healthcare services may differ somewhat between entrepreneurs and hired CEOs. The Finnish tripartite healthcare system includes three schemes: public healthcare for all residents, occupational healthcare for those employed, and private healthcare for those who are willing to pay. This means hired managers belong to the occupational health scheme and can go to private clinics at their employers’ expense. Such convenient and free access to private clinics may lead to better health monitoring, prompt diagnosis, and a lower probability of life-threatening events. However, the three schemes are not exclusive, and entrepreneurs do not have to rely only on public healthcare. On the contrary, it is very common that people use different kinds of combinations of healthcare services (e.g., public and occupational, and private). For example, Blomgren and Virta (2020) analyzed the socioeconomic differences in the use of public, occupational, and private healthcare within 1 year. Their evidence suggests that entrepreneurs use private clinics and have rather equal opportunities for monitoring their health conditions.

Second, the threshold of 500,000 euros revenue partway through our dataset excludes some types of entrepreneurs (e.g., solo, part-time, nascent-stage, and bankrupt entrepreneurs). Hence, these types of entrepreneurs may also face severe health risks due to extremely scarce financial resources and long working hours, among other things. Unfortunately, our dataset does not allow us to capture such health risks, even if entrepreneurs grew their companies in sales volume (e.g., from 100,000 to 200,000 euros) or in terms of the number of employees (e.g., from one person to two persons). Hence, we encourage future research to investigate the health-related consequences of growth and decline among solo and small-scale entrepreneurs. These entrepreneurs typically engage in the accommodations and restaurant sector; the real estate sector; the health and social work sector; and in the arts, entertainment, and recreation sector (Statistics Finland, 2021). Similarly, the entrepreneurial journey to bankruptcy is known to be an extremely stressful experience (Rauch et al., 2018; Shepherd & Patzelt, 2015). Hence, future research could examine the specific health-related outcomes of such stressful journeys and follow the entrepreneurs throughout their lifespan to better understand how health risks relate to mortality.

Supplemental Material

sj-pdf-1-etp-10.1177_10422587241280079 – Supplemental material for Knocking on Heaven’s Door? Entrepreneurship, Firm Growth, and Health Risks

Supplemental material, sj-pdf-1-etp-10.1177_10422587241280079 for Knocking on Heaven’s Door? Entrepreneurship, Firm Growth, and Health Risks by Jukka Partanen, Aino Tenhiälä, Teemu Kautonen, Markus Jokela, Daniel A. Lerner and Alexander McKelvie in Entrepreneurship Theory and Practice

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: First and foremost, we thank Ari Rajala and Alma Media for their help with the initial sample selection. This dataset was a vital baseline for all subsequent datasets. We also thank the Statistics of Finland (TK/1120/07.03.00/2021), Findata (THL/1988/14.02.00/2021), Finnish Tax Authorities (VH/1338/07.01.03/2019), Finnish Patent and Registration Office, the Finnish Population Register Centre (VRK/1433/2019-3), the Social Insurance Institution of Finland (THL/1988/14.02.00/2021), the Finnish Centre for Pensions (THL/1988/14.02.00/2021), and Suomen Asiakastieto for granting us the additional data permits to conduct this project. We are also grateful for the help and support from Marion Carson, MD, Leena Saastamoinen, PhD, Hannu Silvennoinen, MD, and Professor Marko Elovainio who helped in developing our model and selecting the health variables. Similarly, we thank Ismael Ahrazem (PhD) for his help with data curation from the Virre database of the Finnish Patent and Registration Office. Finally, we are grateful for the financial support from the Foundation for Economic Education (Grant Nos. 16-8539 and 20-11304), the Wallenberg foundation, the Kaute foundation, the Foundation of Private Entrepreneurs, and Zayed University. Research reported in this paper was also partially funded by MCIU/AEI/10.13039/501100011033/FEDER, UE Grant No. PID2023-148726OB-I00. The funders supporting the work had no involvement in study design, in the collection, analysis, and interpretation of data, in the writing of the report, or in the decision to submit the article for publication.

ORCID iDs

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.