Abstract

Intermittent exporting (repeatedly exiting and reentering foreign markets) is often associated with the initial stages of internationalization. However, some small and medium-sized enterprises (SMEs), including family firms, pursue an intermittent exporting strategy beyond the initial stages. Drawing on a refinement of the behavioral agency model (BAM) and real options reasoning, we theorize that a high level of family involvement in SMEs is positively associated with intermittent exporting. We also argue that this relationship is moderated by Chief Executive Officers (CEOs) and board members with a foreign background. We test our hypotheses using a unique longitudinal dataset of Swedish SMEs in the manufacturing and retail industries.

Keywords

Introduction

With the advent of globalization, small- and medium-sized enterprises (SMEs), including family firms, are increasingly pursuing internationalization, mainly through exporting (Hennart et al., 2019; Lahiri et al., 2020). However, research on the internationalization of family firms has yielded mixed results on the relationship between family involvement and SMEs’ exporting behavior (Debellis et al., 2021). Some studies show that family firms are more likely to engage in internationalization (Carr & Bateman, 2009; Zahra, 2003), others find that family firms are less likely to internationalize (Gallo & Pont, 1996; Gomez-Mejia et al., 2010; Ray et al., 2018), exporting at a lower (Eddleston et al., 2019; Fernández & Nieto, 2005) or the same level (Hennart et al., 2019) as nonfamily firms. One reason for these inconsistent findings is that these studies are based on the implicit or explicit assumption that once family SMEs have entered the export market, they will remain there and continue to expand. Similarly, research focused on the export development of family firms over time suggests that family SMEs follow a gradual process or a born-again global path (Kontinen & Ojala, 2010; Pukall & Calabrò, 2014). However, in practice, the export development path is not necessarily linear and continuous, and exporting SMEs often do not permanently commit to export markets. Instead, some SMEs adopt an intermittent export strategy (Crick, 2004; Katsikeas, 1996; Samiee & Walters, 1991), meaning they switch between exporting and non-exporting over time (Blum et al., 2013; Vissak, 2010). For example, Bonaccorsi (1992) shows that only one-third of Italian exporters committed to exporting continuously over a period of 5 years. In their sample of Chilean firms, Blum et al. (2013) found that one-third of exporters can be classified as intermittent exporters. Similarly, approximately half of the population of French manufacturing firms switch between exporting and non-exporting over time (Bernini et al., 2016). Therefore, to shed light on these mixed findings and gain greater insights into the internationalization path of family SMEs (Arregle et al., 2021; Debellis et al., 2021), we address the following research questions: Does family involvement (i.e., the degree to which the family is involved) in the firm’s ownership and management (Banalieva et al., 2022) influence intermittent exporting in SMEs, and if so, under what conditions?

We do so by combining a refinement of the BAM with real options reasoning. According to the BAM mixed-gamble logic, managers make decisions based on a trade-off between the potential losses and gains to their current and their prospective wealth (Martin et al., 2016). While nonfamily firms mainly consider current and prospective financial wealth, firms with family involvement also consider gains and losses in current and prospective socioemotional wealth (SEW) (Gomez-Mejia et al., 2007; Martin et al., 2016), which makes the decision to commit to export markets particularly challenging and shrouded in uncertainty. However, with intermittent exporting, SMEs do not commit fully to one strategy or another. Therefore, real options reasoning is an appropriate lens to complement the BAM mixed-gamble logic.

Real options reasoning suggests that firms do not always have to fully commit to a strategy but can exercise a flexibility option whereby the firm invests in an activity that leads to a right, but not an obligation, to take certain actions in the future (Myers, 1977). This flexibility option allows the firm to switch between two strategies (Bowman & Hurry, 1993; Kulatilaka, 1995), namely, to export or to exclusively serve the home market. The firm can continue to exercise this flexibility option until it commits to exporting or decides to focus on the home market only. The decision to persistently commit to foreign markets or keep the options open (intermittent exporting) is related to the perceived uncertainty in the market (Bowman & Hurry, 1993; Folta, 1998).

Our central argument is that family involvement is positively associated with intermittent exporting because family members can manage the perceived uncertainty associated with the mixed-gamble decision of whether or not to commit to exporting by choosing a flexibility option, namely intermittent exporting. Furthermore, based on international business research and real options reasoning, family firms can reduce the perceived uncertainty associated with the mixed-gamble decision of committing or not to exporting if they have information and knowledge of foreign markets. The literature suggests that CEOs and board members with a foreign background are embedded in, and have information and experience of, other country contexts that can facilitate collecting and interpreting information about export markets (Barroso et al., 2011; Greve et al., 2009). In other words, CEOs or board members with a foreign background can influence the understanding and perceived uncertainty of exporting (Athanassiou & Nigh, 2002; Muzychenko, 2008). Therefore, we predict that the relationship between family involvement and intermittent exporting is moderated by the presence of a CEO and board members with a foreign background. With supporting empirical evidence based on a unique dataset of 48,407 Swedish SMEs in the manufacturing and retail industries for the years 2004 to 2017, we contribute to research on family business and intermittent exporting in a number of ways.

First, we offer a novel approach to the study internationalization of family firms by theorizing and showing that SMEs with high family involvement might not necessarily be less likely to export—as previous family business literature suggests (Graves & Thomas, 2004; Liang et al., 2014)—but that they are less likely to be persistent exporters. Second, and related to the previous point, since intermittent exporting is associated with lower export intensity (e.g., Samiee & Walters, 1991), we offer an additional mechanism—that is, the preference for keeping their options open—to understand why SMEs with high family involvement tend to export less (Gomez-Mejia et al., 2010). Third, we further show that the relationship between family involvement and intermittent exporting is contingent on the presence of CEOs with a foreign background. This contributes to the contemporary debate regarding the local versus global focus of family firms, suggesting that a CEO with a foreign background can act as a bridge between the local focus of SMEs with high family involvement and the global environment (Baù et al., 2019). Finally, by showing that family involvement is a key internal factor influencing intermittent exporting., we extend Bernini et al.’s (2016) work that has emphasized the importance of considering not only external drivers of intermittent exporting, but also internal drivers.

Theoretical Background

Intermittent Exporting

Since the 1970s, several scholars have attempted to explain the export development process (e.g., Bilkey & Tesar, 1977; Cavusgil, 1980; Leonidou & Katsikeas, 1996; Reid, 1981). In early studies, intermittent exporting is associated with the initial stage when managers explore the feasibility of continuous exporting (Leonidou & Katsikeas, 1996). However, other studies (Katsikeas, 1996; Samiee & Walters, 1991) note that intermittent exporting is not always limited to the trial stage, and that SMEs may pursue discrete episodes of exporting (entry and exit) as a stable and viable ongoing strategy (Katsikeas, 1996). Most of these studies tend to dichotomize exporters into one of two groups. The terms sporadic, temporary, or occasional exporters are used interchangeably (i.e., Katsikeas, 1996) to refer to the group of SMEs that are not continuously committed to their export markets and experience periods without exporting. As summarized in the study by Welch and Welch (2009, p. 568), these firms engage in intermittent exports for extended periods and “would not be regarded as firms that have exited given that they are fully prepared to respond to the international orders as and when they arise.” On the contrary, the group of SMEs that, over time, follow export development models and remain in the export market are termed regular, persistent, or perennial exporters. To avoid a static and ex ante dichotomization of exporters into one of these two groups, some scholars refer to intermittent exporting to capture the process of entering, exiting, and reentering the export market, sometimes frequently (Bernini et al., 2016).

We follow this latter approach to gain insights of the dynamics of export development. In particular, we focus on intermittent exporting to indicate the likelihood that a firm enters, exits, and reenters exporting, and the reoccurrence of this process over time. Research on intermittent exporting is limited, but in the last decade there has been renewed interest in these dynamics to explain SMEs’ exit from exporting and their subsequent reentry. In a recent review, Sousa et al. (2021) identify the following main explanations for intermittent exporting: uncertainty and stochastic demand in the home market and learning and performance in international markets. Some studies show that uncertainty and stochastic demand for products and services in the home market are important external factors that can help explain intermittent exporting (Blum et al., 2013). Others propose a learning explanation, whereby SMEs enter exporting to “test the water” or respond to unsolicited orders, which might help them gain relevant knowledge about international markets (Albornoz et al., 2012). Relatedly, some studies consider prior performance in international markets and the role of the firm’s internal resources in helping SMEs cope with the challenges they face in international markets and learn from these experiences, thereby reducing uncertainty (Bernini et al., 2016). Thus, while prior studies have largely focused on external factors that influence intermittent exporting, Bernini et al. (2016) emphasize the importance of internal factors as well. In this study, we consider one additional explanation that integrates the aforementioned accounts. SMEs exercise intermittent exporting to keep their options open over time instead of committing fully to international or domestic markets. This explanation is hinted at in Blum et al.’s (2013) study, “[i]t may also be that firms export occasionally to maintain foreign market relationships, thus providing these occasional exporters the option of becoming perennial exporters subsequently.”

Family Firm Export Development and the BAM Mixed-Gamble Logic

Since the 1990s, increasing attention has been paid to how family involvement influences export development (Kontinen & Ojala, 2010; Pukall & Calabrò, 2014), identifying a number of factors that influence the internationalization of family SMEs and potentially exporting persistence. Beyond the degree of family involvement, the presence of an external CEO and board members’ (Banalieva & Eddleston, 2011; Pukall & Calabrò, 2014) generational succession can be an important internal reason for family SMEs to venture into foreign markets to gain new skills, capabilities, and a renewed international orientation (Calabrò et al., 2016). An external factor that can influence the export behavior of SMEs with high family involvement is the presence in a global niche industry, which allows selling standardized products and therefore requires lower investments to adapt to different target markets (Hennart et al., 2019). Although a niche market strategy can facilitate internationalization, it may not work for all country contexts, for example, country-of-origin effects can result in barriers to exporting, even in a niche industry (Eddleston et al., 2019). Another external factor that can influence export behavior is industry peers (Mazzelli et al., 2022), whereby SMEs with family involvement are more likely to enter foreign markets when their industry peers do so. Other scholars have complemented this body of knowledge on the relationship between family involvement and exports with the concept of SEW (Metsola et al., 2021; Santulli et al., 2019; Scholes et al., 2016). As family firms are generally controlled and managed by multiple family members (Carney, 2005; Fernández & Nieto, 2005), the overlap between the family and the business influences perceptions about uncertainty, and thus the export decision (Pukall & Calabrò, 2014). Grounded in BAM, SEW refers to the “non-financial aspects of the firm that meet the family’s affective needs, such as identity, the ability to exercise family influence, and the perpetuation of the family dynasty” (Gomez-Mejia et al., 2007, p. 106). SEW derives from a variety of sources, such as family members’ identification with the firm, control and influence over the firm, the firm’s social ties, and the relating feeling of belonging, emotional attachment, and dynastic control (Berrone et al., 2012).

According to BAM, managers are not risk-averse and their risk preferences are not constant but depend on framing the problem. Thus, choices are viewed from the perspective of gains and losses in relation to current wealth (Wiseman & Gomez-Mejia, 1998). Choices are positively framed when anticipated outcomes are acceptable in relation to current wealth. A negative framing means that there is a perception that the anticipated outcomes would result in a loss (Wiseman & Gomez-Mejia, 1998, p. 135). A negative framing might, for example, mean that managers perceive that continuing with the current strategy would result in a certain loss. To avoid the loss, managers will opt for a riskier option, even if the expected outcomes of that option may be comparatively low (Chrisman & Patel, 2012). Building on BAM, Gomez-Mejia et al. (2007) suggest that whereas nonfamily firms will base their decisions on potential financial gains or losses, family firms will also consider their potential SEW gains and losses. Thus, family firms may be willing to pursue riskier options than nonfamily firms when the firm’s survival is at stake and SEW could be lost, but they may be risk-averse in regard to pursuing new strategies, including committing to the export market (Gomez-Mejia et al., 2007, 2010). For example, research suggests that the higher the family involvement, the more reluctant SMEs are to commit to exporting because of the threat it poses to their SEW in terms of decreasing family control and influence, and changes in organizational structures and relationship networks (Alessandri et al., 2018).

A refinement of the SEW framework has integrated the mixed-gamble concept to improve its prediction. As Gomez–Mejia et al. (2014, p. 1353) explain, the mixed-gamble logic goes beyond the idea that family owners are only cognizant of the potential SEW losses when making decisions under risk. Rather, family owners “will attempt to estimate possible socioemotional gains when making such decisions in order to consider whether it is worth risking the prospective socioemotional losses.” This may result in businesses choosing to opt for a more exploratory strategy that results in variable sales, but which reduces current losses in SEW (Patel & Chrisman, 2014).

In the mixed-gamble logic, SME export-related decisions can be viewed as a mixed gamble in which managers are aware of possible gains and losses to their current and prospective wealth (Gomez–Mejia et al., 2014; Martin et al., 2013). For family firms, these decisions are particularly challenging and shrouded in uncertainty. First, they involve weighting the anticipated losses and gains along two dimensions: financial and socioemotional wealth (Alessandri et al., 2018; Banalieva et al., 2022). Second, these decisions involve weighting the losses and gains that have an intertemporal dimension (as outcomes occur at different moments in time): current and future wealth. Research on intertemporal decisions shows that individuals tend to discount losses in the future relative to losses in the present (Thaler et al., 1997), suggesting that when financial and SEW are at risk, family members will push the potential loss into the future. As Martin et al. (2016) note, one way to achieve this is by extending the time horizon of their decisions.

We suggest that real options reasoning can yield new insights on how family firms address such uncertain and intertemporal decisions, including exporting. As we discuss next, SMEs with a high degree of family involvement may choose the flexibility of keeping their options open rather than taking the gamble of committing or not to exporting.

Real Options Reasoning

Real options reasoning holds that a firm’s investment in real assets gives it the right, but not the obligation, to take certain actions in the future (Bowman & Hurry, 1993; Myers, 1977). A real option reduces the downside risk in an uncertain world while providing access to upside opportunities (Myers, 1977; Tong & Reuer, 2007). Real options reasoning emphasizes three key aspects that influence the decision-making process.

First, for an option to exist, firms must make an investment that cannot be fully recouped (Folta & O’Brien, 2004). The investment costs associated with exporting include, among others, conducting market research, procuring export licenses, developing a foreign sales network, training employees, and adapting products to local tastes and regulations (Lee & Makhija, 2009). These initial investments create options for the firm by providing a foothold in the foreign market, options that can be exercised over time, like the option to grow, to learn, or to abandon at a later point in time (Li, 2007), resulting in an incremental option or a series of actions based on call and put options (Bowman & Hurry, 1993).

Second, it can result in a flexibility option where the initial investments allow the firm to switch between different strategies depending on the development of the environment (Folta & O’Brien, 2004). Intermittent exporting is an example of a flexibility option where firms do not fully commit to exporting due to limited investment, but at the same time cannot be considered as having completely exited from exporting when they do not sell abroad, as they are prepared to reenter exporting as soon as the external environment justifies it (Welch & Welch, 2009). 1 As such, it allows the firm to keep its options open rather than fully committing to a single strategy. By creating these options, firms can increase the strategic flexibility of their internationalization strategy (Christofi et al., 2021). Although exporting requires relatively low investments in real physical assets, real options can be created by using the firm’s personnel in the home market to travel abroad to meet customers and build a network through which knowledge can be acquired (Ipsmiller et al., 2021). This enhances the upside potential of exports, and SMEs can respond more flexibly to changes in the external environment by adjusting sales and production while maintaining control over the timing and magnitude of changes.

Third, perceived uncertainty is a key determinant of whether firms keep their options open or commit to a strategy (Bowman & Hurry, 1993; Folta, 1998). Firms perceive higher uncertainty when they lack information about the relevant environmental factors and/or the expected outcome of a strategic decision (Duncan, 1972; Kulatilaka, 1995). When firms perceive high uncertainty, real options are valued more highly (Bowman & Hurry, 1993). The extent to which firms perceive uncertainty in the environment depends on their characteristics, meaning that different firms can perceive the same external environment differently (Bourgeois, 1985). SMEs with higher family involvement that prioritize SEW may therefore perceive the external environment differently to nonfamily SMEs, and thus place a different emphasis on the value of a flexibility option. In the following, we build on SEW and real options reasoning to develop our hypotheses on the relationship between family involvement and degree of intermittent exporting, and then identify the boundary conditions.

Hypotheses Development

Family Involvement and Intermittent Exporting

The mixed-gamble logic of SEW suggests that the greater the family involvement in an SME’s ownership and management, the more the export decision is perceived as a mixed gamble shrouded in uncertainty (Banalieva et al., 2022), because it involves the weighting of current and future losses and gains of not only financial wealth, but also SEW (Gomez–Mejia et al., 2014).

Current SEW losses can be substantial when family SMEs fully commit to exporting, ranging from the need to rely more on newer and less trusted network relations (Kontinen & Ojala, 2011), the reduction of family control due to hiring professional managers or the need to monitor foreign activities at arm’s length (D’Angelo et al., 2016), to the need for external funding to support export activities (Gallo & Sveen, 1991). In addition, the integration of export activities may require changes to the firm’s historical foundations, altering the business model based on emotional ties (Alessandri et al., 2018). Prospective SEW gains may also derive from additional financial gains from exporting that contribute to the firm’s longevity, and thus the potential for succession to the next generation. However, these prospective gains are speculative and highly uncertain (Alessandri et al., 2018; Gomez–Mejia et al., 2014).

Building on real options reasoning, we argue that SMEs with a higher degree of family involvement approach the mixed-gamble decision of whether or not to commit to exporting by choosing the flexibility option that also allows postponing the decision into the future, namely intermittent exporting. First, intermittent exporting entails relatively low investments in exporting, which may take the form of responding to unsolicited orders or piggybacking on the efforts of a network partner (Katsikeas, 1996; Samiee & Walters, 1991). For family owners of SMEs, intermittent exporting does not pose a serious threat to the family’s current SEW because it does not divert resources from traditional activities or require changes in relationship networks and the organizational structure. In addition, intermittent exporting does not entail dependence on external sources of finance and specialized human capital not available within the family.

Second, intermittent exporting will result in a foothold in the foreign market and allow the SME to explore the market and gain more knowledge and information, reducing uncertainty regarding prospective financial wealth and SEW (Trigeorgis, 1993). In the context of exporting, this information can lead to a more accurate assessment of foreign demand for the firm’s products, partners to work with, and potential institutional challenges to overcome (Li, 2007). This is particularly valuable for family owners and managers who need to gain knowledge not only to better estimate future financial gains, but also potential SEW gains (and losses).

From the above discussion, we can conclude that the higher the family involvement in the SMEs, the more the SME will prefer to maintain the flexibility of switching between exporting and not exporting, rather than fully committing to exporting or only the home market. Therefore, we hypothesize:

H1: Family involvement is positively associated with intermittent exporting.

Boundary Conditions: Foreign Background

We have argued that SMEs with family involvement are more likely to choose the flexibility option (intermittent exporting) because family members perceive the decision to commit or not to export markets as a mixed gamble shrouded in uncertainty. A key notion underlying international business research and real options reasoning is that perceived uncertainty is closely related to a lack of information about the export market and can therefore be reduced when decision-makers have knowledge about foreign markets (Eriksson et al., 1997; Zucchella et al., 2007). An important source of such knowledge is the individuals in the upper echelons of the organization with a foreign background, namely those born in a country other than the firm’s home country (Drori et al., 2009; Pisani et al., 2018). While individuals with foreign backgrounds in the upper echelons of the firm are potentially valuable for all SMEs, knowledge of foreign markets is especially critical for SMEs with family involvement, which need to weigh not only current and potential losses of financial wealth but also current and potential losses of SEW when making decisions concerning exporting. In more detail, equipped with this knowledge, SMEs with family involvement are likely to perceive less uncertainty in decisions concerning exporting, as they can better predict the potential SEW gains and losses, reducing the need to resort to intermittent exporting as a flexibility option. Accordingly, in this study, we propose two factors that may attenuate the relationship between family involvement and intermittent exporting: (1) having a CEO with a foreign background and (2) having an international board of directors.

CEO Foreign Background and Intermittent Exporting

We argue that a CEO with a foreign background attenuates the positive relationship between family involvement and intermittent exporting, since she/he will have knowledge and experience of other country contexts and can detach from thinking in terms of a single culture or country, thus facilitating the interpretation of information about foreign markets and the international business environment (Greve et al., 2009; Muzychenko, 2008). While this can lead to a more accurate assessment of potential financial outcomes of exporting for any SME, it may be particularly beneficial for SMEs with higher family involvement that also need to balance current and future gains and losses in SEW. For example, a CEO with a foreign background can help family SMEs better assess current and prospective SEW losses resulting from the need to rely on nonlocal relationship networks when committing to export markets. Family SMEs tend to be highly embedded in their local communities, more so than nonfamily SMEs (Graves & Thomas, 2004). Local and community embeddedness is an important dimension of SEW preservation and includes an interest in maintaining a strong reputation and positive relationships with community actors, such as other local firms (Lumpkin & Bacq, 2022). CEOs with a foreign background can bridge the gap between the local and global environment, as they are embedded in two different countries and cultures (Baù et al., 2021; Light, 2021), reducing the uncertainty of the decision to engage with international networks. In other words, CEOs with a foreign background are better able to assess the extent to which engaging in foreign networking might affect their local image and reputation, reducing the need to resort to intermittent exporting as a flexibility option. Moreover, CEOs with a foreign background are embedded in trustworthy networks in two countries, which can support export activities and reduce the need to manage foreign market activities at arm’s length (Miller & Le Breton-Miller, 2021; Mustafa & Chen, 2010). In addition, these CEOs can use their networks to first assess the extent to which they will need to rely on arm’s length monitoring when fully committing to export activities, and thus the degree of control that might be lost. Their networks can also be used to identify potential trustworthy ties to rely on for these export activities (Mustafa & Chen, 2010; Terjesen & Elam, 2009), reducing the need to build new relationships.

Overall, family firms will place less emphasis on keeping their options open when the CEO has a foreign background, and will instead be more likely to commit to either the home market or the foreign market. Hence, following hypothesis:

H2: A CEO’s foreign background moderates the relationship between family involvement and intermittent exporting, such that the positive association between family involvement and intermittent exporting weakens when the CEO has a foreign background.

Board Members’ Foreign Background and Intermittent Exporting

As a second boundary condition, we argue that the presence of board members with a foreign background moderates the relationship between family involvement and intermittent exporting. While boards of directors are mainly tasked with monitoring and controlling management to ensure a balance among the goals, boards in SMEs tend to be more active compared to those of larger firms, providing expertise and resources to make strategic decisions (Baysinger & Hoskisson, 1990; Bennett & Robson, 2004). Board members with a foreign background can be an important source of knowledge and information about foreign markets (Shin et al., 2016). While this knowledge can be valuable for all SMEs, it may be particularly beneficial for SMEs with a higher level of family involvement that need to consider SEW losses (and gains). For example, board members with a foreign background can help SMEs better assess the current and potential SEW losses associated with maintaining family control when new managers or owners are brought into the business to support internationalization. First, board members with a foreign background provide access to information to properly assess the need to recruit nonfamily managers with international experience to commit to export markets (Lohe et al., 2021). Second, they can help assess whether the firm needs external funding to support export activities (Gallo & Pont, 1996). Commitment to exporting requires a relatively large investment of resources for SMEs. This may entail greater reliance on external funding and the potential loss of control to external investors, such as venture capitalists and banks (Bauweraerts et al., 2019; Tosi & Gomez-Mejia, 1989), and hence a loss of SEW (Berrone et al., 2012). Board members with a foreign background can facilitate the gathering, analysis, and interpretation of information about foreign markets, such that family members can make a better assessment of the costs associated with commitment to foreign markets and the related external funding needs (Barroso et al., 2011; Tihanyi et al., 2003).

In sum, board members with a foreign background will support family members in assessing whether or not committing to exporting will affect the preservation of SEW, thereby reducing the need to resort to intermittent exporting as a flexibility option. Therefore, we propose:

H3: Board members with a foreign background moderate the relationship between family involvement and intermittent exporting, such that the positive association between family involvement and intermittent exporting weakens as the share of board members with a foreign background increases.

Methodology

Sample and Data

We tested our hypotheses on micro-data from Swedish SMEs (10–250 employees) in the manufacturing and retail industries from 2004 to 2017. We selected the manufacturing (NACE 10–33) and retail (NACE 45–47) industries as they have the highest shares of exports as identified by customs data. We collected the data from seven registers administered by Statistics Sweden (the official census bureau), covering all residents aged 16 and older and all firms in Sweden. First, we used the multi-generation register (Flergenerationsregistret) that links all individuals in Sweden to their biological parents, siblings, offspring, and partners, which enabled us to identify families and family relationships. 2 Second, we used the LSUM (Kontrolluppgiftsbaserad lönesummestatistik) panel data on jobs to identify owners of firms registered in Sweden (legal ownership). Third, we used the OPF-Funktion (Operativaledarefunktion) panel data to identify managers in all firms in Sweden. Fourth, we used the OPF (Operativaledare) panel data to identify the CEO of each firm. Merging these data enabled us to identify firms owned and managed by members of the same family. Fifth, we used the migration (Inv och Utvandring) and birthplace (Fodelseuppg) datasets to identify the foreign backgrounds of inhabitants in Sweden. Sixth, we used the RAMS (Registerbaserad arbetsmarknadsstatistik) panel data to create all firm-level variables (e.g., firm age, performance, etc.) and identify SMEs. 3 Lastly, we used the exporting (Utrikeshandel) panel data to identify exporting SMEs and their exporting activities over the years. We merged all the data using individual, family, and firm identifiers. Our final sample includes 46,729 SMEs with 353,884 firm-year observations from 2004 to 2017 to test H1 and H2, and 38,658 SMEs with 308,210 observations to test H3.

As we study export development over the 2004 to 2017 period, the global financial crisis is included as an important change in the external environment. The uncertainty related to the global economic crisis increased the importance of real options as a source of strategic flexibility, whereas in periods of relative stability, investment in real options has less value (Lee & Makhija, 2009). Thus, it is a relevant period to study the development of exporting from the perspective of real options reasoning.

Model Specification and Estimation

To test our hypotheses, we used a conditional risk set model that estimates the likelihood of an event (i.e., exporting) taking place at a certain point in time (Jenkins, 2005; Singer & Willet, 2003). The conditional risk set model is useful when a firm experiences multiple (re-)occurrences of a given event (exporting in our study) (for a detailed discussion on conditional risk set models, see Prentice et al., 1981). The model follows a stratified Cox proportional hazard, where the analysis is stratified by the event occurrence order (i.e., exporting orders). The assumption is that a firm is not exposed to a second export occurrence (precisely, an export reoccurrence) until the first export occurrence, and so forth. Accordingly, each export occurrence (given the order of occurrences) has a different baseline hazard function (Cleves et al., 2016). In addition to the likelihood of an event taking place, Cox proportional hazard models consider the timing of the event (Jenkins, 2005). In this study, the time to each event is measured as the number of years since the previous event occurred. Thus, time is not measured continuously from entry into the study, but rather the clock is set to 0 after each event.

Furthermore, in our survival settings condition, we account for 8 years of historical exporting behavior (i.e., from 1997 to 2003). Including these years partly addresses the left-truncated cases. Left truncation occurs when firms exhibit historical intermittent exporting behavior prior to the years we analyze (i.e., before 2004). We account for these left-truncated cases because our exporting data starts from 1997, but our analysis begins in 2004 due to data availability (see the sample and data section).

Finally, in our conditional risk set model, we also stratify by industry type (i.e., manufacturing vs. retail), meaning that for different industries, a different baseline hazard is taken into account (Cleves et al., 2016).

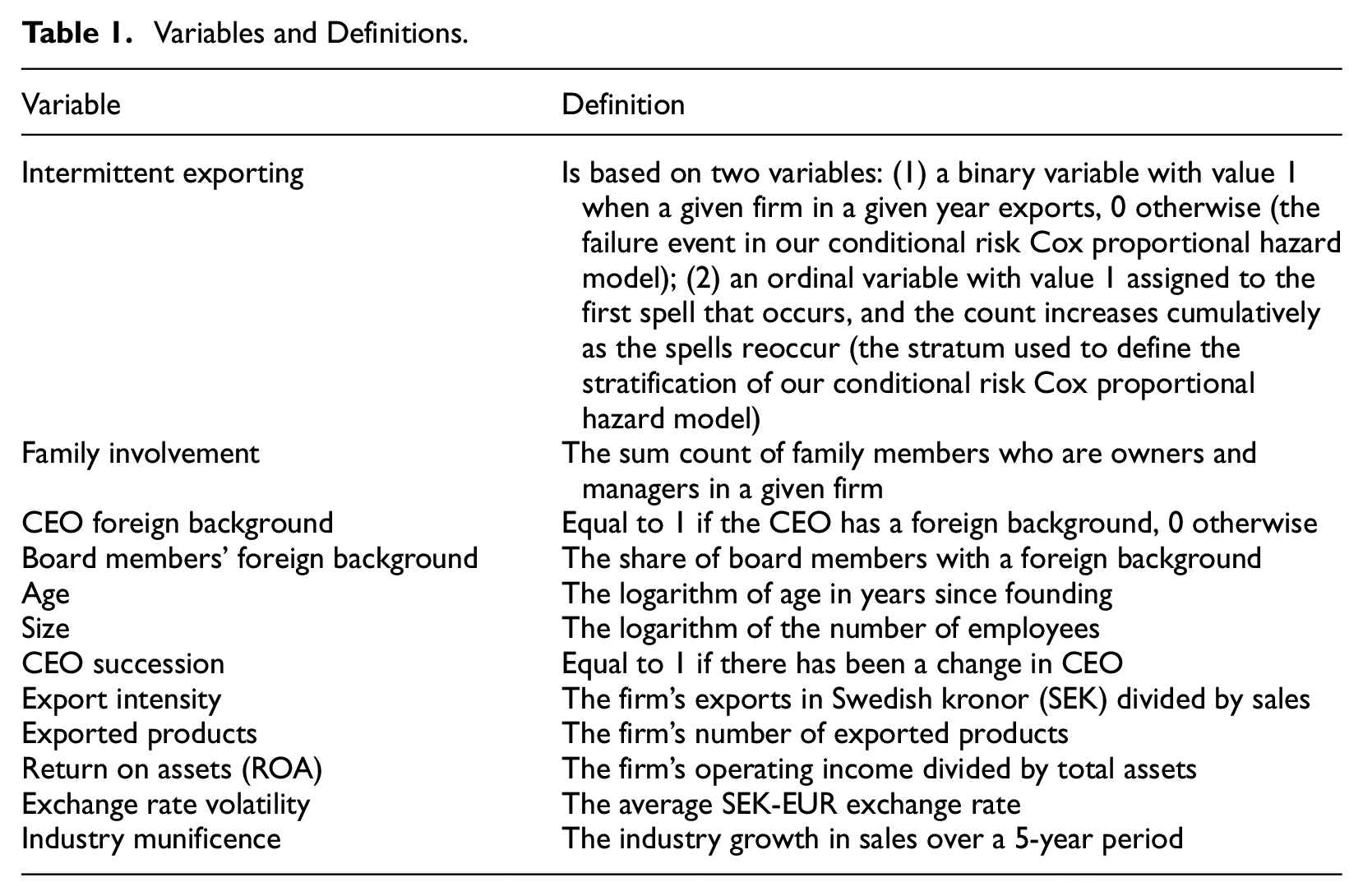

Variables

Dependent Variable

In this study, we are interested in SMEs’ degree of intermittent exporting. The conditional risk set model estimates the likelihood of an event taking place at a certain point in time (Jenkins, 2005; Singer & Willet, 2003). In this model, intermittent exporting is captured by a higher likelihood of events taking place, and thus a shorter time between different events. Specifically, intermittent exporting is based on two variables: (1) a binary variable with value 1 when a given firm in a given year exports, and 0 otherwise (the failure event in our conditional risk Cox proportional hazard model); (2) an ordinal variable, which captures the number of spells. The spells variable is the cumulative count of the number of exporting spells (i.e., entering, exiting, and reentering the export market), where value 1 is assigned to the first spell that occurs, and the count increases cumulatively as the spells reoccur. This is the stratum (i.e., group) used to define the stratification of our conditional risk model.

Table 1 summarizes the definitions of the independent variable and all controls used in the main analysis.

Variables and Definitions.

Independent Variable

Following Baù et al. (2019), we measure family involvement in terms of (a) the total number of family members declaring partial ownership in their tax declaration and (b) the total number of family managers (e.g., Le Breton-Miller et al., 2011). In our study, family members are identified as individuals in a biologically linked family (which includes not only partners and their children but also grandparents, nieces, nephews, aunts, uncles, and cousins on the father’s and the mother’s side).

Moderating Variables

We included two moderating variables: foreign background of the CEO and foreign background of board members. Country of birth is a common measure to capture international experience and knowledge of foreign markets (Nielsen, 2010). Hence, CEO foreign background is a binary variable that takes a value of 1 if the CEO was born outside Sweden, and 0 if born in Sweden. To capture the international representation on the board of directors (board members’ foreign background), the number of board members born outside Sweden is divided by the total number of board members.

Control Variables

We also included a number of control variables. First, firm age, which has an important influence on export development as young firms may experience the liability of newness that is a barrier to exporting (Freeman et al., 1983). However, younger firms can also have the learning advantage of newness because they do not yet have established structures and are therefore more flexible (Sapienza et al., 2006). Firm age is measured as the natural logarithm of the number of years since the firm was founded. Second, we include firm size, as larger firms have more available resources, in turn influencing the likelihood of committing to exports in the long run (Miesenbock, 1988; Sui & Baum, 2014). Firm size is measured as the average of the natural log of the number of employees for each spell. Third, given its relevance to the firm’s strategy in general, and exporting decisions in particular, we control for firm CEO succession measured as a binary variable equal to 1 if the CEO of a given firm in a given year has been changed and 0 otherwise.

Furthermore, to control for past international activities, we included two control variables related to internationalization. Past international activities can reduce intermittent exporting as it reduces the likelihood to exit (Love & Máñez, 2019), but also increase the likelihood of reentry when SMEs with more past export activity exit, as these firms are likely to be more productive (Bernini et al., 2016). The first is export intensity, measured as the value of exports over the value of total sales. We use the latest available lagged value of export intensity since the last exporting activity to examine the effect of export intensity on the event (i.e., reentry). The second internationalization variable is the firm’s number of exported products. It is measured by the number of products a given firm exported in the last exporting activity.

We also control for overall firm performance, namely return on assets (ROA), measured by scaling the firm’s operating income by its total assets. We use 1-year lagged ROA to avoid potential reverse causality (Anderson & Reeb, 2003).

Then, we control for exchange rate volatility as an important macroeconomic factor that influences export decisions because it reflects the potential level of risk of operating abroad (Sui & Baum, 2014). As the Eurozone is the main export region, the exchange rate between the Swedish krona and euro (but not other currencies) is taken into account. We also control for industry munificence as another important macroeconomic factor, which measures the industry’s growth in sales over a period of 5 years (Dess & Beard, 1984). This also captures environmental capacity and indicates the availability of environmental resources that support growth. Following Keats and Hitt (1988), industry munificence is the coefficient of a time series model that regresses the natural logarithm of industry sales on time (i.e., years).

Results

Main Results

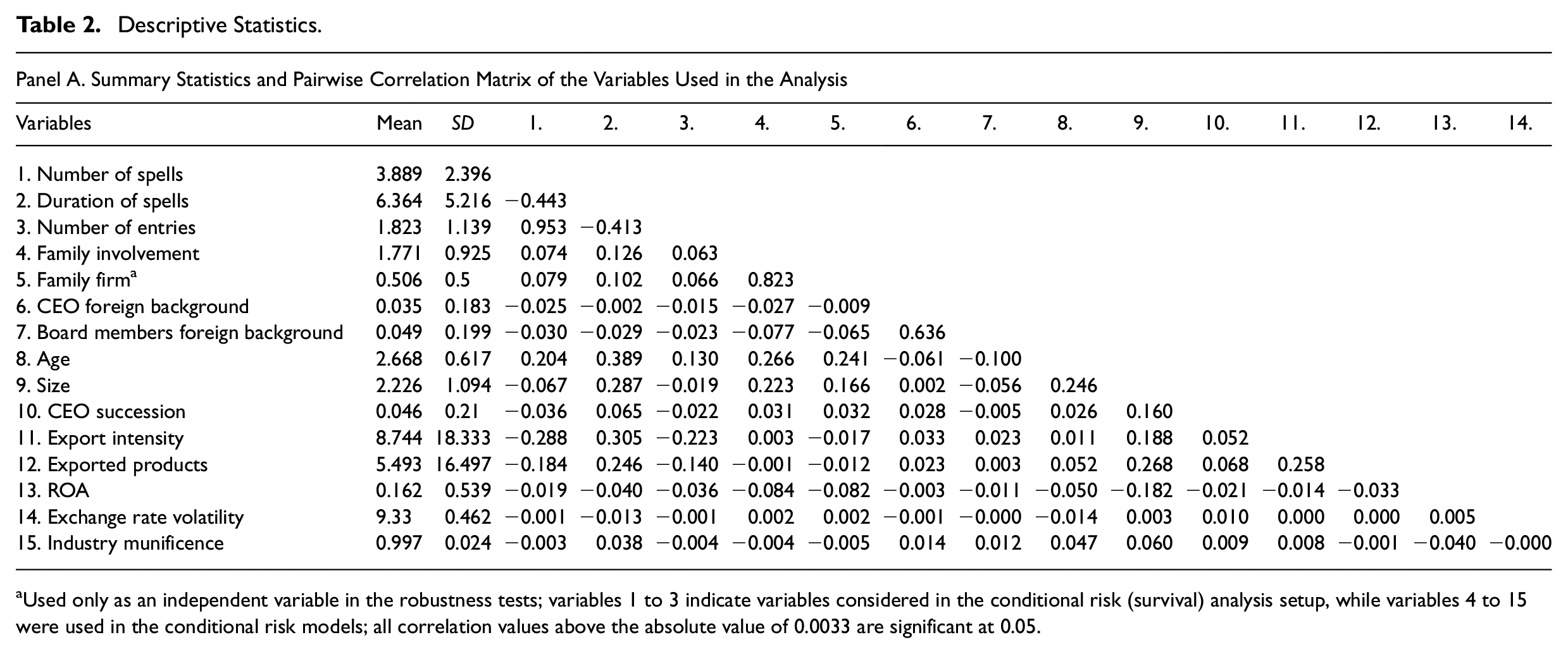

Panel A in Table 2 presents the descriptive statistics and correlations, showing an average of 1.8 reentries and 3.9 spells (i.e., entry, exit, and reentry). The average duration of a spell is 6.5 years. In general, 60% of the observed firms experienced a degree of intermittent exporting, 64% of the family firms experienced a degree of intermittent exporting, and 57% of the nonfamily firms (see Panel B in Table 2). Approximately half of the firms are family firms with an average of 1.8 family members involved. In general, the correlations are low, suggesting low likelihood of multicollinearity. Based on our main model, and as an additional step, we observe no value above 0.3 in the variance–covariance matrix of estimators. 4 Moreover, the highest variance inflation factor value is 1.66 and 1.64 for board members’ foreign background and CEO foreign background, respectively. As these values are still well below the maximum acceptable tolerance value of 10 (Hair et al., 2010), we find no multicollinearity concerns.

Descriptive Statistics.

Used only as an independent variable in the robustness tests; variables 1 to 3 indicate variables considered in the conditional risk (survival) analysis setup, while variables 4 to 15 were used in the conditional risk models; all correlation values above the absolute value of 0.0033 are significant at 0.05.

(continued)

The remaining percentage columns indicate total number of remaining firms in the respective spell.

This value is calculated with respect to the total number of firms.

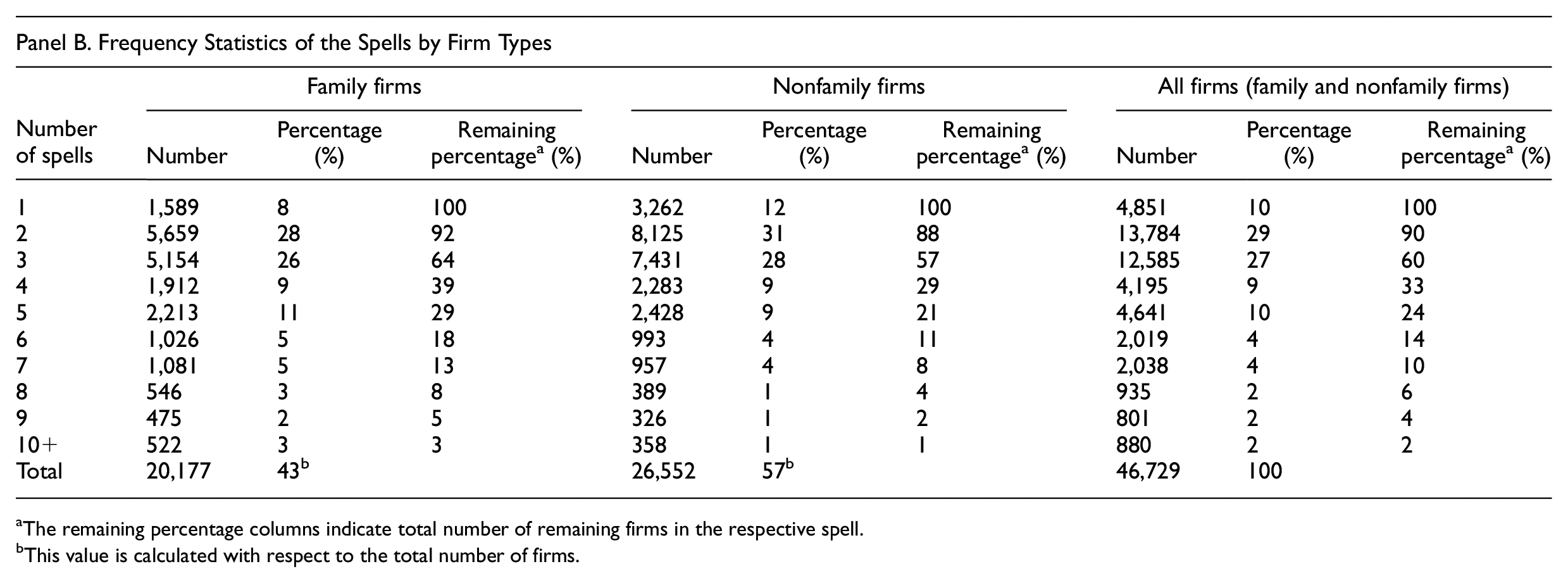

Table 3 reports the results of the hypothesis tests using the conditional risk set model. In general, our models are statistically significant (e.g., Model 1: Chi2 = 8859.1, p < .01). Model 1 is the baseline model with controls only, showing that older and larger SMEs are more likely to experience an event, thus likely to be more intermittent for older and larger firms. Overall historical performance (i.e., 1-year lagged ROA) impacts the intermittent process, whereby firms with higher levels of ROA are less likely to experience an event (hr = 0.891, p < .01), indicating that high historical ROA ensures the firm’s export continuity. Meanwhile, prior export intensity and number of exported products have small effects on the likelihood of an event occurring. The results of the control variables remain similar for the subsequent models.

Estimating the Family Involvement Effect on Intermittent Exporting: Conditional Risk Model.

Notes. Hazard ratios (exponentiated coefficients) reported; robust standard errors clustered on firm level in parentheses; all models stratified by exporting spells and manufacturing versus retailing industries dummy.

p < .05, ***p < .01.

Model 2 shows that family involvement has a positive and significant association with intermittent exporting (hr = 1.048, p < .01), thus supporting H1. In particular, having an additional family member involved in the SME is associated with a 5% increase in the hazard of intermittent exporting. In statistical terms, the mean increase in family involvement is associated with an 8% increase in the hazard of intermittent exporting. To obtain more insights on reentry time and spell duration, we used the confidence intervals for the survival time mean, finding that involving one additional family member (i.e., two family members in total—becoming a family firm) reduces average spell duration from 2.6 to 2.2 years (i.e., approximately 5 months), two additional family members reduce average spell duration from 2.6 to 2 years (i.e., approximately 7 months and 6 days), and three additional family members reduce average spell duration from 2.6 to 1.8 years (i.e., approximately 9 months and 18 days). Altogether, these findings suggest that involving more family members not only increases the likelihood of intermittent exporting but also shortens spell duration.

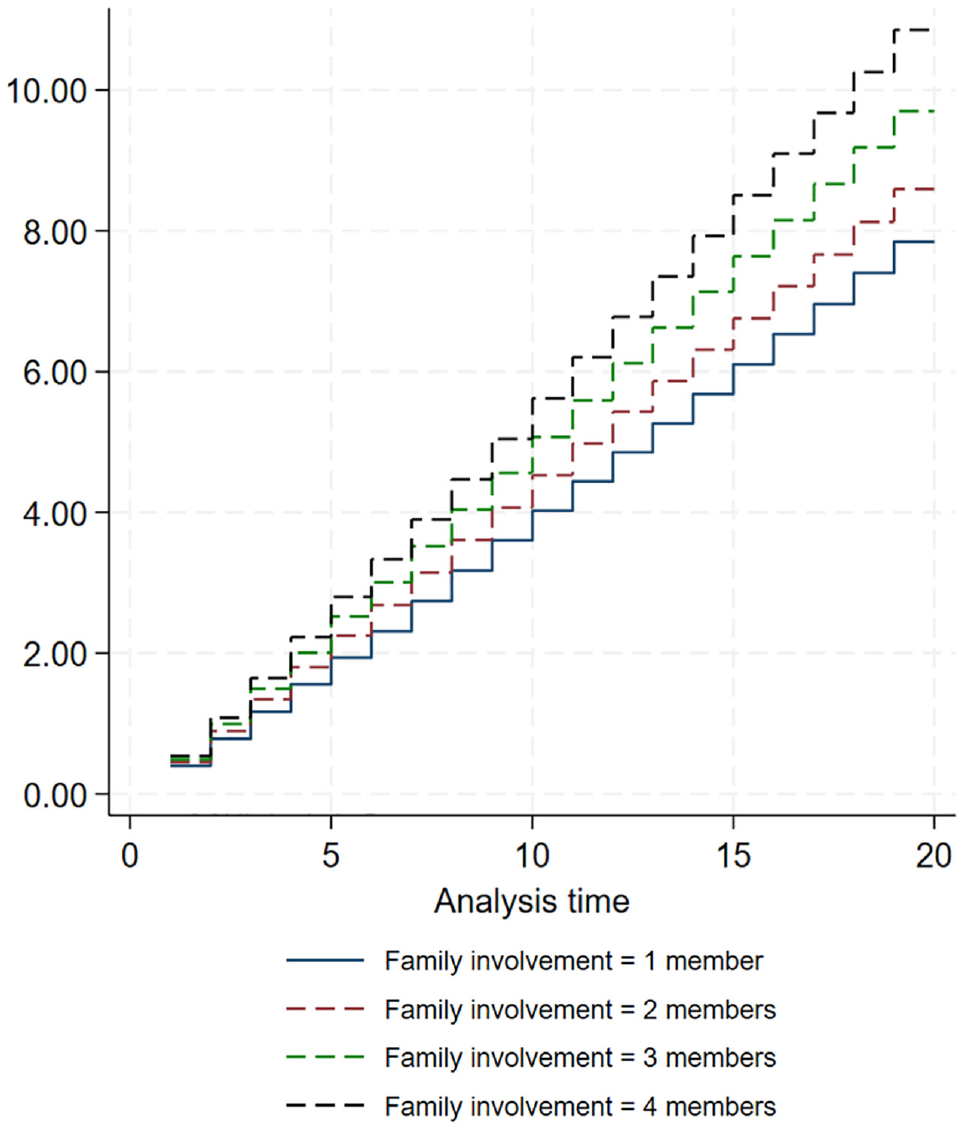

We also tested for equality of survivor function across levels of family involvement. This function (log-rank test) tests whether the survivor functions of each level of family involvement is the same, contrasting the observed events against the expected events over the stratifications of spells defined in our model. The results show that with one, two, or three additional family member(s) involved in the SME, the number of observed events exceeds the number of expected events. We reject the null hypothesis of the log-rank test that the survivor functions of different types of family involvement in the SME are the same (log-rank Chi2 = 1780.31, p < .01). Interestingly, this difference in events even increases as more members are involved, indicating that the more family members are involved, the more observed events than expected vis-à-vis more intermittent exporting. 5 This is also confirmed in Figure 1, which shows the cumulative hazard of intermittent exporting at different levels of family involvement (see the dashed lines compared to the solid line). Importantly, our results support H1, namely, the greater the level of family involvement in the SME, the more intermittent the exporting.

Nelson–Aalen cumulative hazard curves by family involvement level.

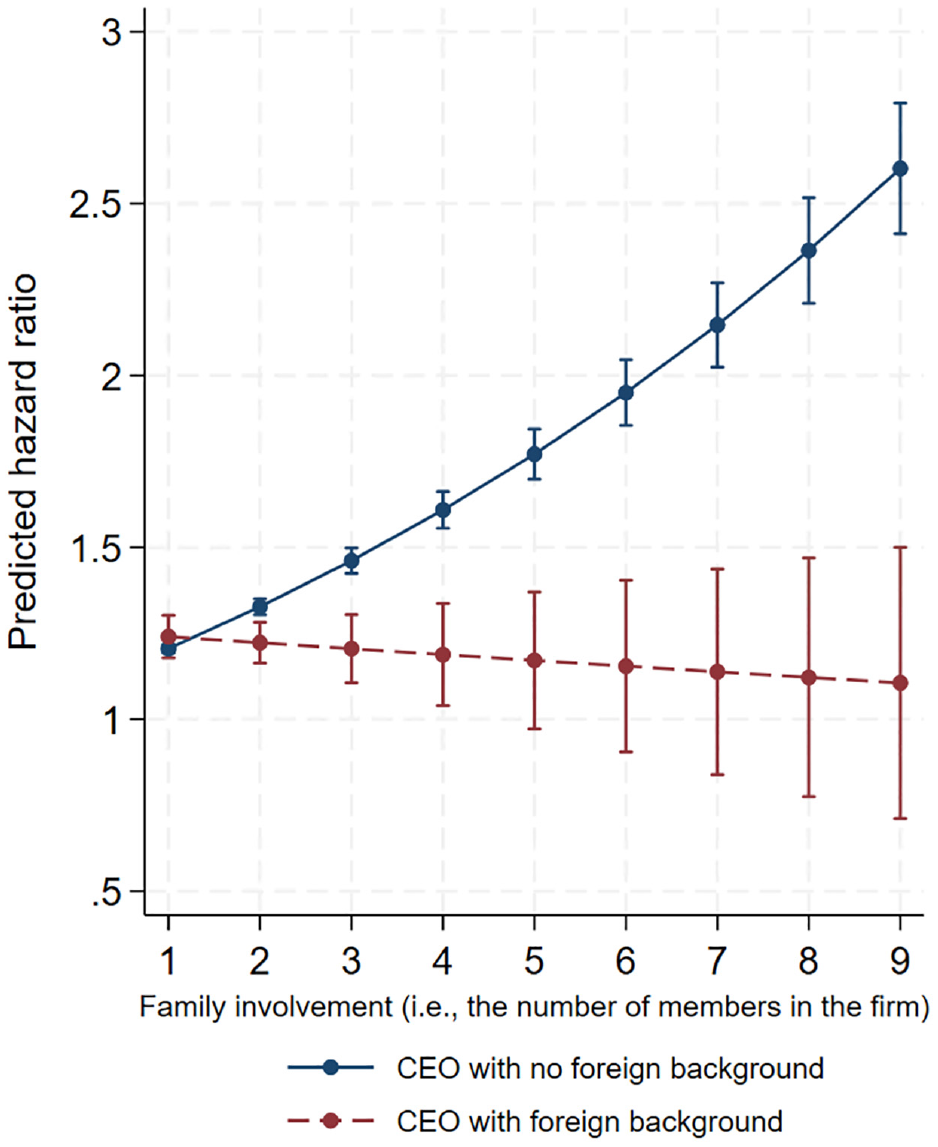

Model 4 in Table 3 provides the results for H2, testing whether CEO foreign background moderates the relationship between family involvement and intermittent exporting. Also in this case, Model 4 is statistically significant (Chi2 = 8721.01, p < .01), showing that a CEO with a foreign background in charge of the SME alleviates the family involvement effect on intermittent exporting (see the downward trend of the dashed line in Figure 2), hence a lower likelihood of intermittent exporting. In particular, having an additional family member involved in the SME managed by a CEO with a foreign background reduces the likelihood of intermittent exporting by 6% (hr = 0.945, p < .05). Thus, the results support H2, and the interaction plot in Figure 2 confirms these findings.

Interaction plot: Family involvement and CEO foreign background.

Model 5 in Table 3 presents the results for H3 stating that board members with a foreign background can moderate the relationship between family involvement and intermittent exporting. While this model is statistically significant (Chi2 = 6432.3, p < .01), we find no statistically significant moderation effect of board members’ foreign background (hr = 1.015, p > .1), hence not supporting H3.

Robustness Tests

We conducted extensive robustness tests to support our main findings.

Endogeneity of Family Firms

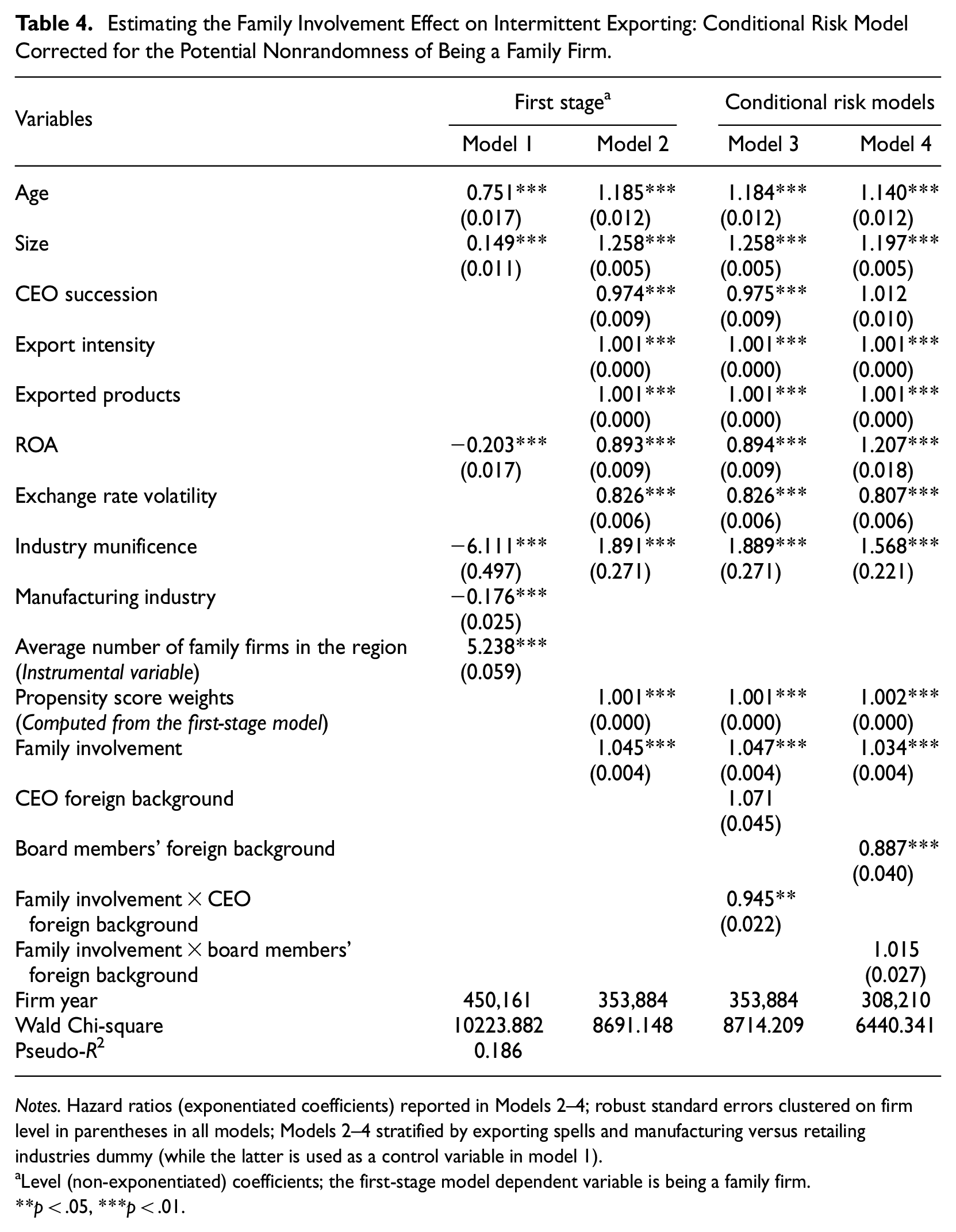

Family firms may be subject to nonrandomness, creating potential endogeneity problems in our main models. In other words, the factors that induce intermittent exporting could be the same as those that maintain a firm as a family business. 6 Accordingly, we first identify an exogenous instrumental variable related to maintaining a firm under family control but not to intermittent exporting. In particular, our instrumental variable is the average number of family firms located in the same geographic region in a given year. To account for the nonrandomness of firms controlled by a given family, we first use a logit model, including the instrumental variable and a vector of controls to estimate the propensity score of being a family-controlled firm. 7 In Table 4, our first-stage model shows that the average number of family firms located in the firm’s geographic region is positively associated with being a family firm (β = 5.238, p < 0.01). We computed the propensity scores and control for them in our conditional risk models. As shown in Models 2–4 in Table 4, our results are virtually identical to our main analysis in Table 3.

Estimating the Family Involvement Effect on Intermittent Exporting: Conditional Risk Model Corrected for the Potential Nonrandomness of Being a Family Firm.

Notes. Hazard ratios (exponentiated coefficients) reported in Models 2–4; robust standard errors clustered on firm level in parentheses in all models; Models 2–4 stratified by exporting spells and manufacturing versus retailing industries dummy (while the latter is used as a control variable in model 1).

Level (non-exponentiated) coefficients; the first-stage model dependent variable is being a family firm.

p < .05, ***p < .01.

Right-Censored Cases

Common in intermittent exporting studies is the right-censoring issue, namely the absence of reentries for some firms in our sample. 8 Hence, we reran our main analyses including only firms with at least two entries (i.e., excluding the right-censored cases). 9 The findings are reported in the online Appendix.. The results are virtually identical to our main analysis in Table 3.

Binary Family Firm Variable

In our main analysis, we used a continuous variable to measure the degree of family involvement. However, as a robustness check, we also consider a binary variable to measure family firms. Following prior research, the family firm variable takes value 1 when there are at least two family members with partial ownership and managers in a given firm, and 0 otherwise (Chirico et al., 2019; Daily & Dollinger, 1993; Fernandez & Nieto, 2006). The findings are reported in the online Appendix. The results are identical to our main analysis in Table 3.

Nelson–Aalen Cumulative Hazard

A binary variable enables us to show the cumulative hazard of intermittent exporting of family versus nonfamily firms. The Nelson–Aalen cumulative hazard curves in the online Appendix show that family firms have a higher hazard rate for intermittent exporting than nonfamily firms, which is in line with Figure 2 when considering different levels of family involvement.

In addition, we account for potential endogeneity when using family firm as the independent variable. The results are identical (see the online Appendix).

Proportional Hazard Assumption (Schoenfeld Test)

The binary independent variable enables running further (diagnostic) tests for additional insights. Specifically, we tested for the proportional hazards’ assumption using the Schoenfeld residuals (or Schoenfeld test) of our Cox proportional model. We reject the null hypothesis of the family firm variable of the Schoenfeld test (Chi2 = 0.05, p = .82), meaning that our independent family firm variable fulfills the proportional hazards assumption in our Cox proportional model.

Log–Log Plot (Kaplan–Meier) Survival Function

Similarly, we checked the proportional hazards assumption using the log–log survival plot, which is a Kaplan–Meier estimate of the survival function (reported in the online Appendix). The plot shows that the family and nonfamily firm lines are parallel, and our independent family firm variable therefore fulfills the proportional hazards assumption (for details on such tests, see Cleves et al., 2016).

Family-Related CEO Succession

In our main model in Table 3, we include a control variable labeled CEO succession to account for a recent change of the CEO. As an additional robustness test, we also control for whether the new CEO belongs to the firm’s owning family (i.e., a family-related CEO succession) or not. The results obtained when accounting for family-related CEO succession closely mirror the results displayed in Table 3, suggesting that recent changes in the firm leadership do not drive our findings.

Survived Firms

In general, SMEs are more prone to failure. SMEs that successfully survive over the years may have different characteristics related to intermittent exporting. Therefore, as an additional check, we consider only firms that survived to the last year of observation, finding that even among these firms, family involvement is positively associated with intermittent exporting. In sum, the results are virtually identical.

Reverse Causality With Moderators

There may be reverse causality between CEO and board members’ foreign background and exporting. Following Pisani et al. (2018), we therefore regressed export intensity at time (t-1) on CEO foreign background and board members’ foreign background. The results show that the coefficients are not significant, providing further evidence that foreign background precedes internationalization and not the other way around.

Left-Truncated Cases

Last, our conditional risk set models mostly cover left-truncated cases, as we observe the exporting behavior for eight historical years prior to 2004. In a robustness check, we altered our survival analysis setting to ignore the exporting information of these historical years (i.e., 1997–2004), finding similar results to our main analysis. In fact, our results also hold when considering the binary view of family firms and the nuclear family view, 10 suggesting our results are stable whether we partially treat or ignore the left-truncated cases.

Post Hoc Analysis: Heterogeneity Among Family Firms

A critical tenet in family business research is that not all family firms are the same, and thus not all will pursue the same or similar internationalization paths (De Massis et al., 2018). Therefore, it is important to explore whether and how heterogeneity among family firms affects intermittent exporting. In our main analysis, we consider one dimension of heterogeneity: the degree of family involvement. To complement this analysis, we conducted post hoc analyses to assess whether our main findings hold across different types of family structures and different types of family involvement.

Types of Family Structure: Nuclear and Biologically Linked Families

We conceptualize and measure family firms as owned and managed by individuals in a biologically linked family, including not only partners and their children, but also grandparents, uncles, aunts, and cousins. However, as De Massis et al. (2018) suggest, extended and nuclear families are different types of family structures that may affect the managerial discretion of individuals, their capabilities, and their motivations for internationalization. Therefore, we reran our analysis considering only members of the nuclear family, including partners, their children, and siblings. The results are identical to our main models and thus stable regardless of the family view. We also considered the right-censored concerns with identical results. All results of nuclear family view are reported in the online Appendix.

Types of Family Involvement: Family Involvement in Ownership and Family Involvement in Management

Our conceptualization and measure of family involvement combines two main dimensions of family control over the firm: (1) family involvement in ownership and (2) family involvement in management (e.g., Baù et al., 2019; Le Breton-Miller et al., 2011). However, some studies argue that these two dimensions of family control may independently and differently affect firms’ internationalization strategies (Lahiri et al., 2020; Liang et al., 2014; Ray et al., 2018). Therefore, we created two variables: (1) family involvement in ownership (the number of family members who are owners of the firm) and (2) family involvement in management (the number of family members who are managers in the firm), and reran the analyses using these as our independent variables. The similar results suggest the robustness of our findings across different dimensions of family involvement.

Discussion and Conclusion

Past research has yielded contradictory findings on the relationship between family involvement and internationalization (Arregle et al., 2017; Graves & Thomas, 2008; Zahra, 2003). However, these studies rely on the assumption that family SMEs choose between persistently committing or not to exporting (Gallo & Sveen, 1991; Lumpkin et al., 2010). We depart from this assumption and propose a theoretical framework that allows for intermittent exporting, thereby providing more insights into the exporting path of SMEs. Specifically, we theorize and provide empirical evidence that family involvement results in more intermittent exporting. Our findings also show that the impact of family involvement on intermittent exporting is reduced by the presence of a CEO with a foreign background, but not by the presence of board members with a foreign background. Our study contributes to the current body of knowledge in several ways.

Our first contribution lies in providing a novel approach to the study of family business internationalization by theorizing that family involvement does not necessarily reduce or increase the likelihood of entering exporting in general but that it reduces the likelihood of persistent exporting. While past research has provided mixed results, suggesting that family involvement can reduce or increase the likelihood of entering exporting, we propose a complementary approach, suggesting that SMEs with family involvement are less likely to commit to the export market permanently but are ready to respond to any export opportunities when these arise to reap short-term financial gains while limiting any potential losses in current and prospective SEW. A second related contribution made by this article is to the BAM and “mixed-gamble” perspective on family firm internationalization. According to this research, family firms generally decide to export less than nonfamily firms because exporting is a mixed-gamble decision where current SEW is at risk and potential SEW gains are uncertain (Alessandri et al., 2018; Gomez-Mejia et al., 2010). By adding a real options reasoning to the mixed-gamble logic of BAM, we conceptualize commitment to exporting not as an isolated decision but as a decision in a sequence of decisions where firms also have the possibility of keeping their options open without having to permanently commit to the export market or only to the home market. Since intermittent exporting is associated with lower export intensity (e.g., Katsikeas, 1996; Samiee & Walters, 1991), we offer an additional mechanism—that is, the preference for keeping their options open—to understand why SMEs with high family involvement tend to export less (Gomez-Mejia et al., 2010).

Our third contribution is in theorizing the contingent role of CEO and board members’ foreign background, responding to the call of Debellis et al. (2021) to focus on the role of individuals and their background in the internationalization of family firms. Specifically, our findings indicate that having a CEO with a foreign background is key for SMEs with high family involvement to move away from intermittent exporting and fully commit to either the export or the domestic market. This is consistent with the argument that CEOs with a foreign background can act as a bridge between the local focus of SMEs with high family involvement and the global environment (Baù et al., 2019) through complementary foreign market knowledge and international networks that adjust the framing of the export decision so that perceived uncertainty about the impact of exporting or not on current and future SEW is reduced, and with that the value of exercising the flexibility option.

Contrary to our expectations, board members with a foreign background do not alleviate the relationship between family involvement and intermittent exporting. There are two possible explanations that warrant further research. First, especially in family SMEs, board members are often recruited on the basis of existing long-term relationships (Calabrò et al., 2009), and may therefore not provide advice and insights that affect perceived uncertainty. Second, board members with different cultural backgrounds are likely to interpret information differently (Elron, 1997), and thus provide different advice on export decisions. As a result of this diversity of advice, uncertainty about potential losses and gains in current and future SEW may persist, increasing the value of a flexibility option.

This study also contributes to the literature on intermittent exporting. Our findings complement Blum et al.’s (2013) suggestion that SMEs export occasionally to create the option of delaying the decision to commit to exporting or not, showing that more than 50% of SMEs in our sample experience some level of intermittent exporting. Specifically, we argue that family involvement results in different perceived uncertainty about export markets, as SMEs with high family involvement consider not only the impact of exporting on current and future financial wealth, but also on current and future SEW. Our findings confirm the importance of family involvement in intermittent exporting, showing that family involvement has a significant and positive impact on intermittent exporting. Hence, we extend the work by Bernini et al. (2016), which emphasized the importance of considering not only external but also internal drivers of intermittent exporting.

Our post hoc analyses provide some insights with regard to family firm heterogeneity. We find that, at least in the context of SMEs, the effect of the degree of family involvement on intermittent exporting is consistent across different types of family involvement (in ownership and management) and different types of family structures (extended and nuclear families). While these findings appear to run counter to research arguing that different types of family involvement may lead to different internationalization strategies (De Massis et al., 2018), the answer may lie in the SME context where these types of family involvement are highly intertwined. SMEs lack the slack resources and formalized decision-making systems of larger firms. Thus, in these firms, all family members—whether owners or managers—are likely to play both strategic and operational roles, therefore equally involved in strategic decisions, such as whether to commit or not to exporting.

Our findings have implications for family owners and policymakers. For family owners and managers, our study suggests that SMEs are less likely to engage in intermittent exporting if appointing a CEO with foreign background. A CEO with a foreign background can provide family firms with knowledge and networks in foreign markets, which can help the firm better weigh the SEW gains and losses associated with committing to exporting. Indeed, a CEO with a foreign background can help family firms reduce export, exit, and reentry and instead make a more permanent decision about whether to commit to the export market or the home market.

Our findings also suggest that policymakers should carefully consider the characteristics of SMEs when designing trade promotion programs. For example, while some SMEs are willing to commit to export markets, those with greater family involvement in ownership and management may be more reluctant to commit fully. Therefore, trade promotion programs could support these firms by providing targeted initiatives that allow them to enter export markets at their own pace, and the tools and knowledge to reduce perceived uncertainty.

Limitations and Future Research

As with most research, our study has some limitations that can be addressed in future research. First, the appointment of a CEO and board members with foreign backgrounds might be correlated with the firm’s export strategy. Following Pisani et al. (2018), we have tried to empirically address this issue by regressing a 1-year lagged export intensity (t-1) on our moderators, namely the CEO’s foreign background and board members’ foreign background. While we found statistically insignificant results (for details, see the robustness tests section), we acknowledge that endogeneity can still be an issue, not least because of the dynamic relationships between a firm's internationalization strategy and the international background of the CEO and board members. Second, although we capture the practice of entering, exiting, and reentering the exporting market in line with the literature using a conditional risk model and controlling for export intensity, in the estimation of intermittent exporting, we do not predict the degree to which firms commit in terms of export intensity. Future research could capture this dimension of intermittent exporting. Third, we were unable to directly measure SEW. Therefore, following the extant literature (e.g., Moreno-Menéndez & Casillas, 2021; Patel & Chrisman, 2014), we proxied SEW with the degree of family involvement and ownership in the firm. Future studies can adopt a survey methodology to capture SEW more accurately (Berrone et al., 2012). Similarly, exchange rate volatility and industry munificence (e.g., Dess & Beard, 1984; Sui & Baum, 2014) reflect uncertainty in the external environment. However, our data do not fully capture how uncertainty is perceived by decision-makers. Future research can capture this in more detail, for example, by utilizing survey data or adopting a case study methodology.

Fourth, we observe the first time a firm exports in our dataset only for the subset of firms founded since 1997. Although we conducted further robustness checks to account for this potential left truncation of our dataset, we acknowledge this as a limitation of our study. Similarly, because our observation window is finite, our data are right censored. In other words, our data include firms that exported, but did not exit, and firms that exited the market once, but had not yet reentered the exporting market during the years observed. While it is important to account for “censored” exit and reentry in our conditional risk models to avoid potential bias and while we conducted a number of robustness tests that account for these right-censored cases, we acknowledge this as a limitation of our study.

Fifth, our theorizing assumes that export commitment is a mixed gamble for firms with family involvement, as they need to consider and weigh potential financial gains and losses against potential SEW gains and losses (Alessandri et al., 2018). However, our data do not allow us to empirically observe these processes in detail. Therefore, future research could consider extending our study using other methodologies, such as longitudinal case studies, and follow financial and SEW considerations over the SMEs’ exporting history for a better understanding of how the combination of BAM and real options reasoning can explain the intermittent exporting of SMEs with higher levels of family involvement.

Sixth, a potential limitation is that our data capture firms in only one market (Sweden). The results obtained from Swedish data are likely replicable with data from other countries, but it cannot be assumed that Swedish exporting behavior is without particularities. Therefore, future research could address this question by conducting studies on intermittent exporting in other countries and comparing export behavior in different national settings. Seventh, while we show that our findings hold across different types of family involvement and family structure, future research could consider whether and how the heterogeneity that originates from the evolution of a family firm—for example, distinguishing between the lone founder, family post-founder, and family founder firms (Miller & Le Breton–Miller, 2011)—influences the internationalization patterns of family firms. Finally, our observation window ended in 2017. However, in recent years and even more since the outbreak of the pandemic, the retail industry has experienced an increase in e-commerce, which might have decreased the commitment required to export and the value of a flexibility option. More research is needed to explore this possibility.

Supplemental Material

sj-docx-1-etp-10.1177_10422587231226113 – Supplemental material for Keeping One’s Options Open: Intermittent Exporting, Family Control, and Foreign Background

Supplemental material, sj-docx-1-etp-10.1177_10422587231226113 for Keeping One’s Options Open: Intermittent Exporting, Family Control, and Foreign Background by Andrea Kuiken, Lucia Naldi and Mohamed Genedy in Entrepreneurship Theory and Practice

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.