Abstract

Our study challenges the notion that intuition is used to explain away gender biases in access to finance, arguing instead that women's success in crowdfunding is rooted in the use of intuition. We measured investors' intuition using self-reports and fast investment decision-making related to crowdfunding campaigns in three randomized controlled experiments involving 2,911 subjects from Europe and the United States. Our Bayesian analysis provides evidence for a gender equality effect, suggesting that intuition cannot be cited as the reason for gender biases in investment decisions. Our research highlights the importance of reassessing the scientific reputation of intuition.

Introduction

Bringing new ideas to life often requires support and financial resources, and crowdfunding has emerged as a novel financial market that can serve as a springboard for startups. Crowdfunding enables founders to access financing for their ideas through an online platform from a large, diverse group of individuals with varying levels of venture-related financial experience, or no experience at all (Mollick, 2014; Short et al., 2017).

Reward-based crowdfunding is a type of crowdfunding where entrepreneurs seek funding for their projects by offering incentives, or “rewards,” to backers who contribute money. These rewards can range from a simple thank you note or a small gift, to pre-orders of the product or service being offered, or exclusive experiences related to the project. The funding process usually takes place on an online platform where the entrepreneur shares a video pitch to showcase their idea and attract backers (Allison et al., 2015).

While there is a widely documented and substantial gender gap in traditional funding markets (Malmström et al., 2017), women are at least as likely as men to successfully secure support through reward-based crowdfunding (Greenberg & Mollick, 2017; Johnson et al., 2018) across a wide range of sectors, geography, and cultures (Leland, 2022).

This marked discrepancy in gender equality regarding the same fundamental objective of obtaining financial support motivates us to examine decision-making in the reward-based crowdfunding context. We aim to understand the mechanisms that promote gender equality and investigate why women are more successful in reward-based crowdfunding compared to traditional funding markets.

Despite progress in gender equality, women still face challenges in accessing financial resources in traditional funding markets (Geiger, 2020). Studies have identified several factors such as stereotypical behavior (Balachandra et al., 2019; Brooks et al., 2014) and unconscious biases (Carter et al., 2007; Verheul & Thurik, 2001) that affect how women are evaluated when applying for venture capital (Alsos & Ljunggren, 2017; Alsos et al., 2006; Boden & Nucci, 2000; Huang & Pearce, 2015). However, in contrast to the evaluation process in venture capital, research has found that women are evaluated as more trustworthy in the crowdfunding market (Johnson et al., 2018), which is characterized by more diversity among investors (Bapna, 2019), including many novices with limited investment education (Li et al., 2017; Mollick, 2014). Prior research has also shown that crowdfunding investors tend to use more intuitive than analytical decision-making (Huang, 2018), particularly in situations with limited access to information (Courtney et al., 2017; Gigerenzer & Gaissmaier, 2011; Huang & Pearce, 2015; Mousavi & Gigerenzer, 2014). While analytical-rational decision-making is intentional and reflective, an intuitive decision-making approach is automatic and effortless (Denes-Raj et al., 1996). These findings suggest that crowdfunding may offer a more equitable funding option for women entrepreneurs, highlighting the potential benefits of this novel financial market.

The use of intuition has long been a topic of debate among scholars, with some arguing that it can lead to errors or biases (Evans & Over, 2010; Kahneman, 2003; Tversky & Kahneman, 1973, 1974) while others suggest it leads to superior results (Dane et al., 2011; Gigerenzer & Gaissmaier, 2011; Julmi, 2019; Mousavi & Gigerenzer, 2014; Waroquier et al., 2010). This has led to a plethora of research aimed at understanding intuition’s many characteristics, including mental shortcuts or heuristics (Gigerenzer, 2008; Hodgkinson & Sadler-Smith, 2018; Ma-Kellams & Lerner, 2016; Rouder et al., 2013).

Fast, intuitive decisions tend to be influenced by stereotyping (Geiger, 2020). However, research suggests that gender-based heuristics could be a key factor in gender preferences in crowdfunding and why women perform as well as men in this domain (Johnson et al., 2018). To expand on this topic, our study investigates whether experienced or inexperienced investors’ use of intuition affects their gender preferences regarding their willingness to invest. We also aim to determine if different types of intuition, such as lay or expert intuition, can promote gender equality.

The previous studies were limited in their methodology, making it difficult to differentiate between expert and lay intuition. Additionally, they had other limitations (Sinclair, 2020; Sinclair & Ashkanasy, 2005), such as small sample sizes, lack of cross-cultural scope (Allinson & Hayes, 2000; Hayes et al., 2004; Norenzayan et al., 2002), and a focus on artificial laboratory tasks rather than real-world situations (Kahneman & Frederick, 2007, 2002; Kruglanski & Gigerenzer, 2011; Lufityanto et al., 2016; Sinclair, 2020). Researchers have previously measured investors’ intuition through self-reports (Fenton-O’Creevy et al., 2011) or bias scales (Johnson et al., 2018), which are subject to biases such as recall or retrospective bias (Podsakoff & Organ, 1986), and do not necessarily reflect their actual behavior. Therefore, it is important to overcome these limitations in order to gain a clearer understanding of how expert and lay intuition operate in investment decision-making.

Our design choices allowed us to overcome methodological limitations by (1) merging self-reports to avoid retrospective biases with (2) real-world scope using actual crowdfunding scenarios (3) to apply a behavioral intuition measurement and (4) target a cross-cultural scope that would also (5) control for possible confounding variables in our (6) between- and within-subject designs. We used emotion-driven, real-world crowdfunding investment decisions across diverse projects because a person’s tendency to use either an intuitive or a deliberative decision-making style is not stable across decision domains (Pachur & Spaar, 2015). As we invited both lay and professional investors to participate, we ensured that all potential confounds were controlled through random and blind assignments and that participants’ willingness to invest was attributable to our controlled manipulations: gendered pitches across three studies. Thus, our work provides an advanced contribution to research examining the underpinnings of crowdfunding decisions and relevant biases, which are areas that have remained largely opaque (Drover et al., 2017).

Overview of the Studies

To overcome the limitations of previous research, to consider critiques of traditional intuition measurements (Krajbich et al., 2015), and to capitalize on the growing interest among policymakers to provide better conditions for women to access financing, we used three fully web-based, large-scale randomized controlled experiments with both between- and within-subject designs to test whether investor intuition and pitcher gender affect investors’ willingness to invest. We measured intuition in two complementary ways: a traditional self-report using the well-established Rational Experiential Inventory (REI) (Pacini & Epstein, 1999) across all three studies (see Supplemental Text 3), and a behavioral approach using fast decision-making tasks for investing in past real-world crowdfunding campaigns only in Study 3. While our dependent variable is willingness to invest, investor intuition and pitcher gender serve as independent variables. We used Prolific, a leading supplier of research participants, to recruit stratified samples across studies.

Across three studies involving 2,911 subjects, we explored how investor intuition influences willingness to invest across gender and tested both a theoretically and practically relevant intervention designed to investigate gender equality in access to finance. We predicted that intuition in general, whether generated by experience or heuristics, will predict willingness to invest in crowdfunding, regardless of gender. In other words, irrespective of whether (heuristic or expert) intuition leads to errors and biases or to better outcomes, it facilitates gender equality in accessing finance. As such, it cannot be identified with stereotyping.

Study 1

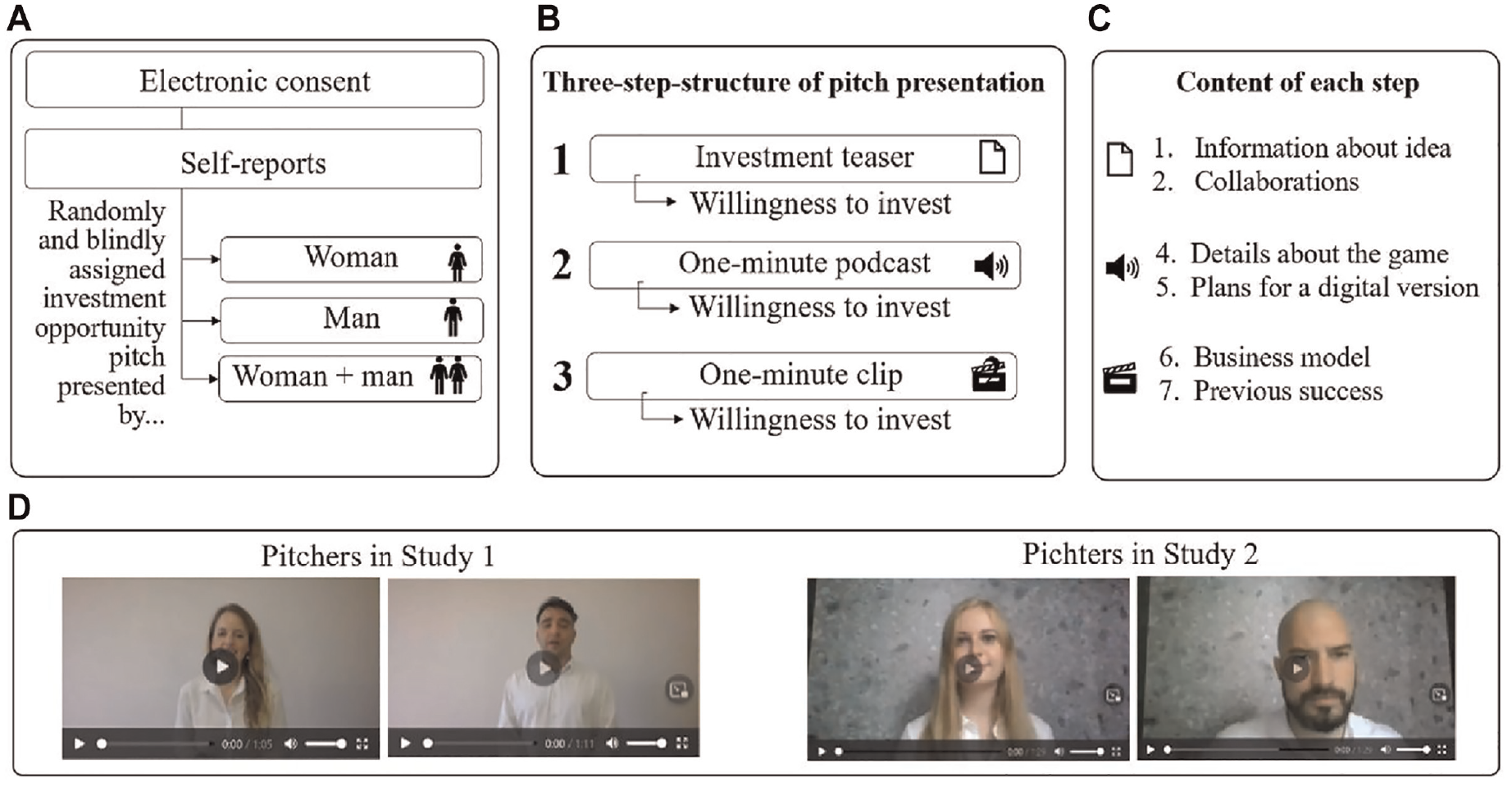

In Study 1 (n = 1,364), we used a randomized, between-subject experimental design in which we manipulated the gender of pitchers (male vs. female vs. both genders) who all presented the same idea. Subjects were randomly and blindly assigned to one of three conditions: treatment group 1 (pitch presented by female), treatment group 2 (pitch presented by male), or control group 3 (pitch presented by both). Participants were asked to assess their willingness to invest in the idea based on a seven-item scale adapted from prior work (Welpe et al., 2012) immediately after each of three steps: (1) a written teaser without pitcher name, (2) a podcast, and (3) a 1-min video clip. We recruited equal proportions by gender (women vs. men), nationality (Europe vs. the United States), and professional categories (Bapna & Ganco, 2021) of entrepreneurs, investors, and non-entrepreneurs; for vignettes, see Supplemental Text 2.

Study 2

In Study 2 (n = 657), we repeated Study 1 to test whether our initial findings were replicated with different pitchers. In addition, we introduced the gender of the pitcher at the written teaser stage to replicate a field experiment (Bapna & Ganco, 2021) that did not detect any gender bias when using only written investment teasers. We included this intervention to clarify at which stage (teaser, podcast, or video clip) intuition might create biases in willingness to invest. As in Study 1, we recruited in a stratified way.

Study 3

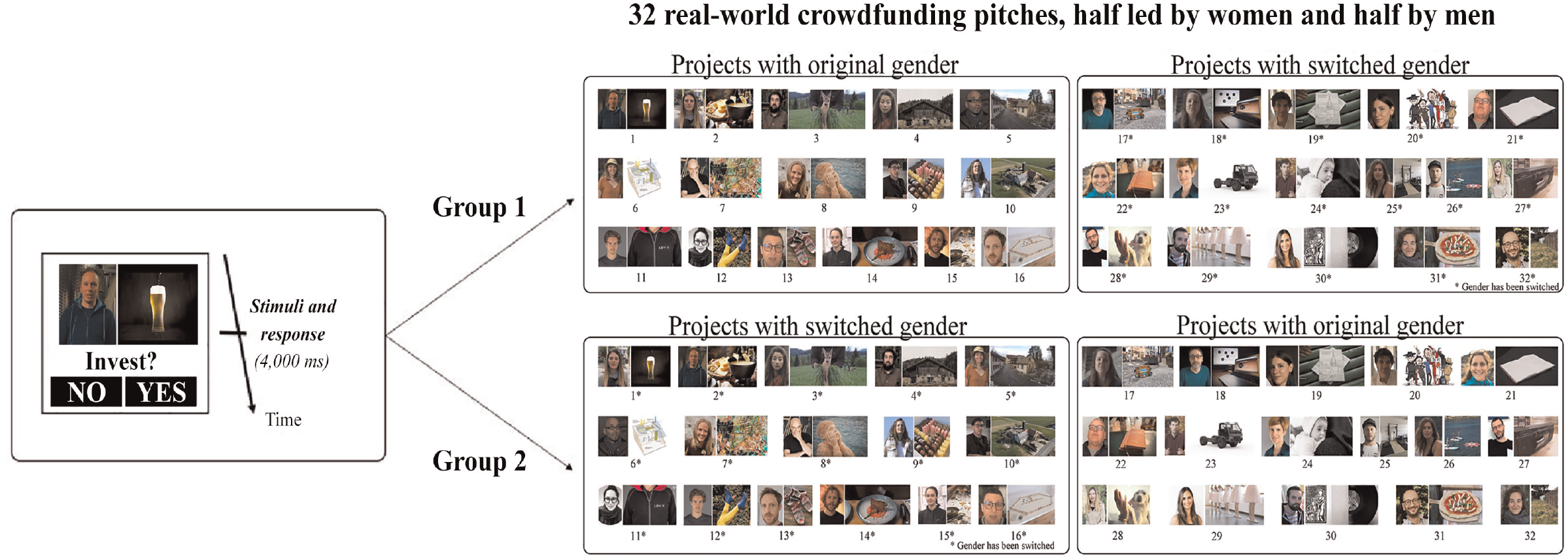

In Study 3 (n = 899), we measured intuition behaviorally using 32 real-world crowdfunding pitches with between- and within-subject designs. We used the most common and traditional intuition measurement, which is decision speed (Kahneman, 2011; Rand et al., 2012). Subjects had to decide whether to invest within 4 s of being exposed to each of the 32 real-world crowdfunding campaigns; half the “founders” were female and half male, but only half represented the actual founders. Subjects were randomly and blindly assigned to both conditions: (1) 16 images with the real founder (control) and (2) 16 images with a “founder” of the opposite gender (treatment); we switched the 16 images of real versus “fake” founders between groups 1 and 2. Each subject was thus randomly and blindly assigned to 32 investment opportunities (16 female and 16 male founders; only eight of each gender were real). We thus controlled for any potential confounding variables (e.g., domain-specific preferences or sectors with clear gender preferences) and for gender-related biases. Reaction speed to distinguish intuition from reflection has been used in prior research (Kahneman, 2011; Rand et al., 2012). Thus, we have chosen 4 s as the decision deadline because previous studies suggest that time limits below 5 s are short enough to induce spontaneous responses, effectively resulting in low-deliberation conditions that are appropriate for assessing a decision as intuitive (Myrseth & Wollbrant, 2017). In Study 3 we stratified for gender (women vs. men), nationality (Europe vs. the United States), and investment experience (none vs. some).

In summary, via three studies, we tested investors’ use of intuition during investment decisions with different self-reported and behavioral interventions in different ways. Together, these studies address whether, when, and how intuition affects investors’ willingness to invest, with a particular focus on gender equality. Materials, data, and code for all studies are available at https://osf.io/zp7kb.

While most research focuses on how to decrease biases (Huang & Pearce, 2015) or provides recommendations for women to change or adapt to the financial markets to overcome barriers (Balachandra et al., 2019), we shed light on investors’ use of intuition to clarify its fundamental role in creating a gender balance in rationally driven financial decision-making. Investigating this phenomenon can help us explain why women tend to be at least as successful as men in new financial markets like crowdfunding. It is important to understand whether intuition facilitates willingness to invest, regardless of gender, to significantly advance our knowledge of gender equality and help policymakers craft novel methods to promote gender-equal access to financing across regions and sectors. We expect that investigating financial decision-making for idea pitching in particular will reveal ideas for new policies for gender equality, because pitching ideas to convince others represents a common experience, whether in seeking capital, at workplaces of all kinds, or even in people’s private lives. Thus, our work significantly advances gender gap research by explaining intuition’s positive role in facilitating our willingness to support others, regardless of gender.

Theoretical Framework

In the crowdfunding literature, prior work has explored the role of heuristic-based biases among amateur investors (Kahneman & Klein, 2009) and expert intuition among experienced investors (Dane & Pratt, 2007; Kahneman & Klein, 2009) in investment decisions. To advance this discussion to make theoretical advancements (Anderson et al., 2019; Fisher & Aguinis, 2017), we propose adding signal detection theory (Macmillan & Creelman, 2004; Stanislaw & Todorov, 1999) as a framework for understanding how gender-based stereotypes can impact investment decisions in the reward-based crowdfunding ecosystem. We provide an explanation of why and how gender-based stereotypes—which can be always at place implicitly—may not necessarily disadvantage any gender during investment decisions in the reward-based crowdfunding ecosystem, as long as either expert or lay intuition comes into play.

Signal detection theory explains how individuals make decisions in situations where a signal of interest is mixed with noise (Macmillan & Creelman, 2004; Stanislaw & Todorov, 1999). This theory suggests that decision-making is influenced by both sensitivity to the signal and the response criterion. We use this theory to explain how both heuristic-based biases and implicit gender-based stereotypes among amateur and experienced investors can affect their ability to accurately identify promising investment opportunities in crowdfunding. By considering the role of both lay and expert intuition in the context of signal detection theory (Macmillan & Creelman, 2004; Stanislaw & Todorov, 1999), our study provides a nuanced understanding of how different types of intuition by different experienced investors can impact gender balance in access to finance in crowdfunding.

Heuristics are mental shortcuts that simplify decision-making processes during fast and effortless judgments (Gigerenzer, 2008; Horvath & Wiegmann, 2016). Lay intuition, often referred to as heuristics, can lead to correct decisions, but it is also prone to errors (Tosi & Einbender, 1985). However, heuristics can be particularly effective in risky and complex situations such as crowdfunding (Gigerenzer, 2007). In this environment, gender-based heuristics and stereotypes may not necessarily disadvantage any gender during investment decisions. For instance, amateur investors may use gender-based heuristics to evaluate female entrepreneurs more positively, based on stereotypes such as the perception that women are more trustworthy and collaborative (Johnson et al., 2018).

Inexperienced investors are more likely to rely on lay intuition (Johnson et al., 2018), which is more likely to be less influenced by typical gender stereotypes in financing and more open to evaluating entrepreneurs based on their project’s potential for future success. Referring to signal detection theory (Macmillan & Creelman, 2004; Stanislaw & Todorov, 1999), inexperienced investors may have a lower sensitivity to signals of typical gender stereotypes but higher sensitivity to signals of potential success due to their open mind. Therefore, we argue that in the context of reward-based crowdfunding, gender-based heuristics can promote gender equality in access to finance, depending on the specific biases and heuristics used by inexperienced investors.

Expert intuition, in contrast to lay intuition, is developed through extensive domain-specific experience (Huang, 2018) and involves a pattern recognition process that can lead to more accurate judgments (Dane & Pratt, 2012; Kahneman & Klein, 2009; Lufityanto et al., 2016). However, experienced investors may still hold implicit biases and gender stereotypes that can impact their decision-making process (Bapna & Ganco, 2021). For example, a gender stereotype may lead an investor to believe that women are less competent in financial matters or high-tech industries, which could affect their investment decisions. Based on signal detection theory (Macmillan & Creelman, 2004; Stanislaw & Todorov, 1999), experienced investors are expected to have a higher sensitivity to detect signals of potential success through their expert intuition, even when implicit biases or gender stereotypes are at play. Therefore, we argue that more experienced investors in the crowdfunding ecosystem are not less likely to be influenced by gender stereotypes and biases in their investment decisions, but their expert intuition can help promote gender equality in access to finance by creating signals for potential success.

To summarize, in the context of reward-based crowdfunding, both lay and expert intuition can promote gender equality in access to finance. Inexperienced amateur investors who rely on heuristics and experienced professional investors who deploy expert intuition can react to subject-driven signals for potential future success, regardless of gender. To conclude, we address the main hypothesis as follows: Investor use of intuition facilitates willingness to invest, regardless of presenter’gender.

Materials and Methods

Ethics Information

This research complies with all relevant ethical regulations. It was approved by the ethics committees of both the Swiss Federal Institute of Technology Zurich (German: Eidgenössische Technische Hochschule Zürich, ETH Zürich) with number 2020-N-01 and Harvard’s Committee on the Use of Human Subjects, which serves as the university-wide institutional review board (IRB), with number IRB21-0021. Electronic informed consent was obtained from all participants. In our metadata, we have excluded the subjects’ Prolific IDs, as recommended by the IRB, to make our data more than merely pseudo-anonymous. In line with ethical standards for fair online labour pay, subjects received incentives of at least £6.00 (~US$8.00) per hour for their participation, which took an average 30 min per subject. Details on participants’ demographic characteristics and all data, materials, and code are at https://osf.io/zp7kb/.

Preregistered Hypotheses

When using Bayesian inference, preregistration is not as important as with null hypothesis significance testing (Gronau et al., 2020). We reported all inclusions and exclusions and every measure given. To examine our key hypothesis of interest, the lead author preregistered the main hypothesis in her Marie Curie proposal, setting the starting and leading points for this project. In addition, for Study 3 we preregistered our main hypothesis through aspredicted.org (https://aspredicted.org/blind.php?x=GRD_ZKS piloting for the Bayes Factor (BF) design analysis and https://aspredicted.org/KZ3_H22 for the main study) and the Open Science Framework (OSF; https://osf.io/zp7kb) as follows: Investor use of intuition facilitates willingness to invest, regardless of presenter’ gender. In other words, intuition promotes gender equality.

Experimental Design

We apply Bayesian inferences for the following key advantages: (1) collecting data for interim analysis, (2) generating estimates and credible intervals for any derived parameter or predicted variable computed directly from the posterior distribution, and (3) the provision of methods to calculate support in favor of and not only against the null hypothesis (Dienes, 2014). To be more precise, we are able to explain our results in such a way that we accept our null hypothesis—that intuition facilitates willingness to invest, regardless of pitcher’s gender. Intuition thus promotes gender equality, and the use of intuition cannot be explained as a central reason for any bias observed in financial decision-making.

For our Bayesian analyses, we used R 4.1.2 and R Studio version 1.4.1106 (R Development Core Team, 2003), along with popular packages. We report results according to best practices and guidelines (Kruschke, 2021). Although Studies 1 and 2 were not preregistered via aspredicted.org, we followed the Marie Curie time stamp of August 23, 2019. Study 2 was a replication of Study 1. Study 3 was preregistered (https://aspredicted.org/blind.php?x=GRD_ZKS) for piloting data for our BF design analysis and main study (https://aspredicted.org/KZ3_H22). Table 1 provides an overview of our analyses. All detailed analyses and code are available in Supplemental Material S2 at https://osf.io/zp7kb.

Figure 1 presents an overview of the designs chosen for Studies 1 and 2, and Figure 2 does the same for Study 3. Across all studies, after providing their consent, subjects supplied their nationality, age in years, gender, years spent in education, experience in years (general work, entrepreneurial, and investment), risk perception (Byrnes et al., 1999), and the well-established 10-item REI (Pacini & Epstein, 1999). In Studies 1 and 2, we also had participants complete the short 15-item Big Five Inventory of personality dimensions (Lang et al., 2011). Because we used randomized, between-participant experimental designs across studies and manipulated the gender of the pitcher (male vs. female vs. gender-mixed pitcher in Studies 1 and 2, and male vs. female in Study 3), all potential confounds were controlled in our stimuli. Thus, participants received identical pitches in each experimental condition, indicating that any differences in willingness to invest were attributable to our controlled manipulations. Because crowdfunding platforms are characterized by information asymmetries (Courtney et al., 2017), research indicates that funding campaigns predict funding success (Ciuchta et al., 2016), depending on idea category (Greenberg & Mollick, 2017), including emotional aspects (Li et al., 2017; Mollick, 2014). Thus, we used only headshots and the same idea for Studies 1, 2, and 3. In Studies 1 and 2, four different actors were chosen to test whether our assumptions would hold true across several known or unknown biases. In addition, we used a gender-mixed team pitch as a control. In Study 3, subjects’ intuition was also measured behaviorally using fast investment decision-making in 32 real-world crowdfunding campaign images; half were led by men and half by women. In addition, we switched genders for half the campaigns to control for gender-related products.

Studies 1 and 2: Mixed between- and within-subject designs to assess investors’ willingness to invest. (a) The between-subjects design is characterized as follows. After signing the electronic consent and providing self-reports in Studies 1 and 2, subjects were randomly and blindly assigned to one of three pitch presentations of the same investment opportunity, presented by a woman, a man, or a man-woman team. (b) The within-subject design is characterized as follows. In Studies 1 and 2, each pitch was structured in the same way, regardless of presenter gender, in three steps: first, an investment teaser was shown, then an audio file providing further details was played, and finally a video presentation was shown. The differences between Studies 1 and 2 were as follows. Presenters were changed, and the investment teaser indicated presenter gender by the use of “Mr.” or “Ms.” in step 1. The within-subject design was used for secondary analysis and robustness checks (see Supplemental Material). (c) With each step, additional information was added to the pitch. To simulate real-world crowdfunding in the laboratory, the experiment included key elements of a crowdfunding campaign. For instance, while general information was provided in the teaser, the presenter’s previous success was presented in the final step. (d) Pitchers in each study. For vignettes, please refer to Supplemental Materials. Audio and video files are available at https://osf.io/zp7kb/.

Study 3: Behavioral measurements of subjects’ use of intuition and willingness to invest. (a) Intuition and willingness to invest were measured behaviorally using fast investment decisions of real-world crowdfunding investment opportunities obtained from www.wemakeit.com and representing diverse project categories. Subjects were shown a headshot of the founder and a picture of the product and had 4 s to decide whether to invest. (b) Subjects were randomly and blindly assigned to two groups; each group was shown 32 images of real-world crowdfunding pitch images. The difference between the two groups is that the gender of the founder was switched in half the campaign images. Thus, only 16 pitches presented the real founder, which enabled us to control for any potential confounding variables and for gender-related biases embedded in the projects themselves.

We intentionally excluded any information related to expected rewards across all of our studies. Our main objective was to evaluate participants’ investment behavior and decision-making while minimizing the influence of any rewards. In both Study 1 and Study 2, we deliberately omitted any details about rewards during the three different pitch stages. Instead, participants were provided with the opportunity to invest virtual money exclusively. Similarly, in Study 3, we utilized images of entrepreneurs and their products from reward-based crowdfunding campaigns. However, participants were again restricted to making investment choices, reinforcing the investment context. By framing the pitches as investment opportunities, we aimed to ensure that participants’ decisions and responses were solely based on their perception of investment potential. This deliberate approach allowed us to investigate investment behavior in a more focused and relevant manner. By removing the influence of expected rewards, we gained insights into participants’ investment-related perceptions and actions.

Self-Reported Variables, Composite Measures, Independent Variables

Self-Selected Categories of Study Participants

In Studies 1 and 2, we have three main professional categorizations of investor type to investigate whether our effects were bound to specific professions, with entrepreneurs and non-entrepreneurs as control groups. Subjects self-selected their category based on the following definitions. “Entrepreneur: you are self-employed, meaning you run some kind of business (including non-profit organizations, freelancing)”; “Financier: you have ever invested your own or others’ money in any business: e.g., crowdsourcing, friend’s business idea, shares of stock”; and “Professional investor: your job is related to investment decisions: for example, angel investor, organizational investor, venture capitalist, crowdfunding investor.” Groups 2 and 3 were merged due to the scarcity of professional investors in our dataset. To verify professional investors in Studies 1 and 2, we asked the following question: “Do you agree with the following statement: According to the risk-return relationship, risk and return are connected. Thus, higher risk guarantees higher returns.” In Study 3, we also asked subjects the following question: “What percentage of your wealth do you have invested at the moment (e.g., projects or companies on crowdfunding platforms, stock market)?” These two questions also served as a control for investment experience and risk awareness.

Self-Reported Use of Intuition

Across all three studies, we applied the five-item REI (Pacini & Epstein, 1999). Participants were asked to indicate their level of agreement from one (Strongly disagree) to seven (Strongly agree) with the following statements to measure their intuitive decision-making style: (1) when making a decision, I rely on my instincts; (2) when I make decisions, I tend to rely on my intuition; (3) I generally make decisions that feel right to me; (4) when I make a decision, I trust my inner feelings and reactions; and (5) when I make a decision, it is more important for me to feel the decision is right than to have a rational reason for it. A composite measure of self-reported decision-making style was created by averaging each participant’s responses to the five items on the scale.

Behavioral Use of Intuition

In Study 3 we additionally investigated people’s use of intuition behaviorally. Participants were given a maximum of 4 s to make an investment decision after being presented with two images: the founder’s headshot and the product. Traditionally, reaction speed represents a well-established method to measure intuitive decision-making (Kahneman, 2011; Rand et al., 2012). Subjects were exposed to 32 successful real-world crowdfunding campaign images; half were led by females and half by males. We chose the images from a leading crowdfunding platform, www.wemakeit.com, which has than €67.2 million in total backings, more than 5,900 successful projects, and more than 524,000 community members, as of October 2022. To control for gender-related products, we switched the founder’s gender in half the campaigns and randomly and blindly assigned subjects to one group or the other.

Risk Perception

Across all studies, we measured risk perception based on a well-established scale (Byrnes et al., 1999), incorporating a meta-analysis of 150 studies comparing risk-taking behaviors of men and women in a variety of domains such as financial risks and tasks like hypothetical choices or self-reported behaviors. Our subjects were asked to indicate how risky they perceived each of the following six situations to be on a scale from one (Not at all risky) to seven (Extremely risky): (1) betting a day’s income at the casino; (2) investing 10% of your annual net income in a moderate growth mutual fund; (3) investing 5% of your net annual income in a highly speculative stock; (4) betting a day’s income on the outcome of a sporting event; (5) betting a day’s income in a high-stakes poker game; and (6) investing 10% of your net annual income in a new business venture. The composite measure of self-reported risk perception was created by averaging each participant’s responses to the six items.

Big Five Inventory

In Studies 1 and 2, we also asked Big Five Inventory items (Lang et al., 2011) to explore personality-related connections. We used the short 15-item version of personality dimensions, which is well suited to applications in large-scale multidisciplinary surveys (Lang et al., 2011). Seven-point Likert-type rating scales ranging from one (Strongly disagree) to seven (Strongly agree) were used with the following conclusions to the preamble “I see myself as someone who…”: (1) worries a lot, (2) gets nervous easily, (3) remains calm in tense situations, (4) is talkative, (5) is outgoing and sociable, (6) is reserved, (7) is original and comes up with new ideas, (8) values artistic and aesthetic experiences, (9) has an active imagination, (10) is sometimes rude to others, (11) has a forgiving nature, (12) is considerate and kind to almost everyone, (13) does a thorough job, (14) tends to be lazy, and (15) does things efficiently. A composite measure of self-reported Big Five inventory items was created by averaging each participant’s responses to three items for each of five traits.

Control Variables and Demographics

Subjects self-reported their gender (women vs. men) and age in years. In Studies 1 and 2, we also controlled for highest educational level achieved: high school diploma or equivalent, associate degree or equivalent, bachelor’s degree or equivalent, master’s degree or equivalent, and doctorate or equivalent. In Study 3, we asked subjects to report their years spent in formal education. Because experience has been discussed as a powerful factor in people’s use of intuition (Kahneman & Klein, 2009), we controlled for diverse variables related to experience such as investment experience in years, overall work experience in years, and entrepreneurial experience in years. This is particularly important in the crowdfunding domain, where both experienced and inexperienced investors are active. We also asked subjects to report the average percentage of monthly net income they had left after paying all personal expenses.

Behavioral Measure, Dependent Variable

Studies 1 and 2. Willingness to Invest at Scale

In Studies 1 and 2 across all three treatment conditions (idea pitch presented by woman, man, or both) immediately after each (written, audio, and video) pitch, the subject had to assess his or her willingness to invest on a seven-item scale adapted from prior work (Welpe et al., 2012). (1) What percentage of your real savings would you be willing to invest in this firm? (2) What percentage of 100,000 units in virtual money would you be willing to invest? (3) What percentage of others’ real savings would you be willing to invest? (4) How likely (as a percentage) would you be to recommend a due diligence (analyzing the enterprise in more detail) to proceed with your investment decision? (5) How likely (as a percentage) is it that this business would be an overall future success in terms of profits and growth? (6) As a percentage, how much do you think the entrepreneur of this business will outperform in terms of financial success, compared to the industry profit benchmark? (7) To what extent would you be willing to devote your personal resources (as a percentage of your available time) to support the enterprise? A composite measure of willingness to invest was created by averaging each participant’s responses to these sevens items.

Study 3. Willingness to Invest via Dichotomy

In Study 3, subjects had to decide within 4 s whether they were willing to invest in a pitch illustrated by the founder and product image. We chose 4 s for the investment decision because fast decision-making represents the traditional measurement of intuition (Kahneman, 2011; Rand et al., 2012); in this way, we guaranteed that the investment decision was intuitive. Subjects were randomly and blindly assigned to two groups; each group was shown 32 images of real-world crowdfunding pitches. The difference between groups was that in half the campaign images, the founder’s gender was switched, meaning that we showed a “fake” founder of the opposite sex from the original founder. In this way, we controlled for any potential confounding variables and for any gender-related biases that a given project might arouse. All images reflect successful real-world projects across diverse categories from www.wemakeit.com. Willingness to invest was calculated as the cumulative percentage of all decisions to invest in those 32 campaigns, with 1 indicating a positive investment decision and 0 a negative investment decision. Due to our within-subject design, a composite measure of willingness to invest was created by averaging each participant’s responses to the female- and male-led campaigns items. For robustness checks, we also created a composite measure of willingness to invest for switched female and male pitches. This enabled us to measure whether one gender was more successful with the same products; in other words, we could determine whether there were stereotypes related to products.

Data Collection and Procedures per Study

Study 1. Self-Reported Use of Intuition and Willingness to Invest

After our exclusion, Study 1 comprised 1,364 individuals (n = 1,498, collected from July 3, 2021 to August 16, 2021; 134 participants were excluded). Through Prolific, we collected a stratified random sample characterized by equal proportions of gender (women vs. men), participant type (entrepreneurs, investors, and non-entrepreneurs), and nationality (American vs. European). To simulate real-world crowdfunding in our laboratory setting, the experiment included key elements of a crowdfunding campaign: information about the market and the idea, which was a digital board game for promoting children’s health, existing collaborations, details of the game, plans for a digital version, the business model, and the previous success of the pitcher or pitch team. We conducted a fully web-based laboratory experiment that manipulated presenter gender and featuring three randomized treatments in a between-subject design: treatment group 1 (female-presented audio and video pitches), treatment group 2 (male-presented audio and video pitches), and control group 3 (audio and video pitches presented by a man and a woman). The pitch was presented in three stages: (1) a written abstract investment teaser with no names (as induction for neutral emotional status), (2) a podcast, and (3) a 1-min video clip. Immediately after each stage, the subject had to assess his or her willingness to invest based on a modified version of a seven-item scale (Welpe et al., 2012). Using three investment stages enabled our analysis because all subjects across conditions received the same bias-free idea teaser in the first stage. This served as a baseline for willingness to invest within each subject. As such, our design combines between- and within-subject factors (see Supplemental Material S2, secondary analysis, and robustness checks).

Study 2. Self-Reported Use of Intuition and Willingness to Invest

Study 2 includes 657 individuals (n = 728, collected between September 21, 2021, and September 23, 2021; 71 subjects were excluded). A stratified sample similar to Study 1 was also recruited online via Prolific. The recruitment criteria were equal proportions of gender (women vs. men), nationality (American vs. European), and participant type (entrepreneurs, financiers, and non-entrepreneurs). Study 2 served as a replication of Study 1 but had two design changes. We used different female and male actors than those in Study 1 and a name in the teaser. Subjects were randomly assigned to the same conditions as in Study 1: treatment group 1 (female-presented audio and video pitches), treatment group 2 (male-presented audio and video pitches), and control group 3 (audio and video pitches presented by a man and a woman). In the written teaser in stage 1, participants were informed of the pitcher’s gender by the use of “Ms.” or “Mr.” or both (see vignettes in Supplemental Text 2, Supplemental Material). Unlike the no-name investment teaser in Study 1, this study was built on a field experiment (Bapna & Ganco, 2021) that found no preferences among investors as to firm founder gender at the written investment teaser stage if the teaser is gendered.

Study 3. Behaviorally Measured Use of Intuition and Willingness to Invest

The aim of Study 3 was to measure intuition behaviorally using the traditional method that assessed its speed of operation and ease of application (Kahneman, 2011). We tested whether fast intuitive decision-making facilitated willing to invest, regardless of pitcher gender. Based on our BF design analysis of pilot data (n = 60, collected on July 28, 2022; see Supplemental Material S2, sections 6.1.2 and 6.1.3), we recruited 1,089 individuals for this study (n = 899, collected on August 20, 2022 and August 21, 2022; 190 subjects were excluded). A person’s tendency to use an intuitive or a deliberative decision-making style is not stable across decision domains (Pachur & Spaar, 2015). Thus, we used an emotion-driven, real-world crowdfunding investment decision task across disciplines, as crowdfunding decisions are both emotionally and rationally driven. Subjects were exposed to two images, one of the founder and one of the product, from each of 32 successful crowdfunding campaigns. They were randomly and blindly assigned to one of two groups to control for gender-related products. Subjects had a maximum of 4 s in each case to decide whether to invest.

For subject recruitment across studies, we used Prolific, the leading online platform in terms of data quality, transparency, ethical standards regarding participant incentives, attrition rates, and study features (Peer et al., 2017). Sample size was determined based on a cost-benefit analysis given the available resources outlined in our funding proposal and expected effect sizes that would be theoretically informative. Because Bayesian inference obeys the likelihood principle, we stopped collecting participants in line with our plans in the funding proposal while maintaining the validity of our results (Rouder, 2014). Our decision to recruit approximately 1,000 subjects for Study 3 was guided by a BF design analysis for compelling evidence (Schönbrodt & Wagenmakers, 2018). We chose sequential BF with a fixed maximal n design (Schönbrodt et al., 2017) to calculate the sample size for Study 3 based on Monte Carlo simulation and preliminary data, achieving a BF10 > 10 under H0 with a probability of 70% (Schönbrodt & Wagenmakers, 2018). For further details on why and how we selected the n we did, please refer to Supplemental Material S2, section 6.1.3. For the vignettes used in Studies 1 and 2, please refer to Supplemental Material, Supplemental Text 2, and for self-reports across all studies, please refer to Supplemental Material, Supplemental Text 3.

Bayesian Analysis as Basis for Statistical Analysis: Prior and Decision Rule

Bayesian analysis allow us to provide evidence for the absence of evidence, meaning we can make a case for the absence of an effect or relationship (Ly et al., 2016; Schönbrodt & Wagenmakers, 2018). This is particularly useful for the aim of our study as we want to show that a gender effect is truly absent interacting with intuition. We also report Bayes Factor (BF) which provides a direct measure of evidence in favor of a hypothesis relative to an alternative hypothesis. This can be easier to interpret than p-values, which can be difficult to understand and are often misinterpreted. BF is a also flexible tool that can be used with a wide range of statistical models, making it suitable for many research questions and settings (Schönbrodt et al., 2017). Finally, BF is often more robust to violations of assumptions compared to traditional statistical methods, such as normality assumptions or homogeneity of variance. Overall, the use of BF can provide us with a more informative and nuanced approach to statistical inference, particularly in situations where traditional methods may fall short (Rouder, 2014).

For all our analyses of the interaction effect, we used default, non-informative priors to reflect the absence of prior knowledge of these parameters’ distributions. Our decisions to accept or reject our null hypotheses are based on the decision rules using 95% highest density interval (HDI) with the region of practical equivalence (ROPE) (Kruschke, 2018). The HDI limits were computed from an MCMC chain using Kruschke’s method (Kruschke, 2014) and exceeding an effective sample size of 10,000. Using HDI with the ROPE decision rule for hypothesis testing has been advocated to increase the predictive precision of theories in the organizational sciences. The ROPE represents a decision threshold, and its limits are always chosen in the context of current theory and measurement precision (Serlin & Lapsley, 1985). As recommended (Kruschke, 2018), we used conventional parameters and the limits typically observed in social and behavioral research, such as Cohen’s d, to measure small effect sizes (Cohen, 2013). Thus, in line with Cohen’s d for small effects at 0.2., the effect size of a mean as δ = (μ−µ0)/σ is practically equivalent to zero. This choice of ROPE states that any value of effect size that is less than half as small is practically equivalent to zero. As recommended (Etz & Wagenmakers, 2017; Kruschke, 2021; Ly et al., 2016), we determined the size of the effect by plotting the posterior distributions marked with their modal and mean values and their 95% HDIs and decided to accept or reject the null hypotheses by the HDI+ROPE decision rule (Kruschke, 2018). That is, the null value is declared to be rejected if the 95% HDI falls completely outside the ROPE, and the null value is declared to be accepted for practical purposes if the 95% HDI falls completely inside the ROPE. We use figures and tables to visually and numerically present posterior modes, medians and means, standard deviations, posterior distributions, 95% HDI, ROPE, and percentage within ROPE to allow readers to decide on their own. The detailed analyses, R code, and additional figures are provided in Supplemental Material.

Results

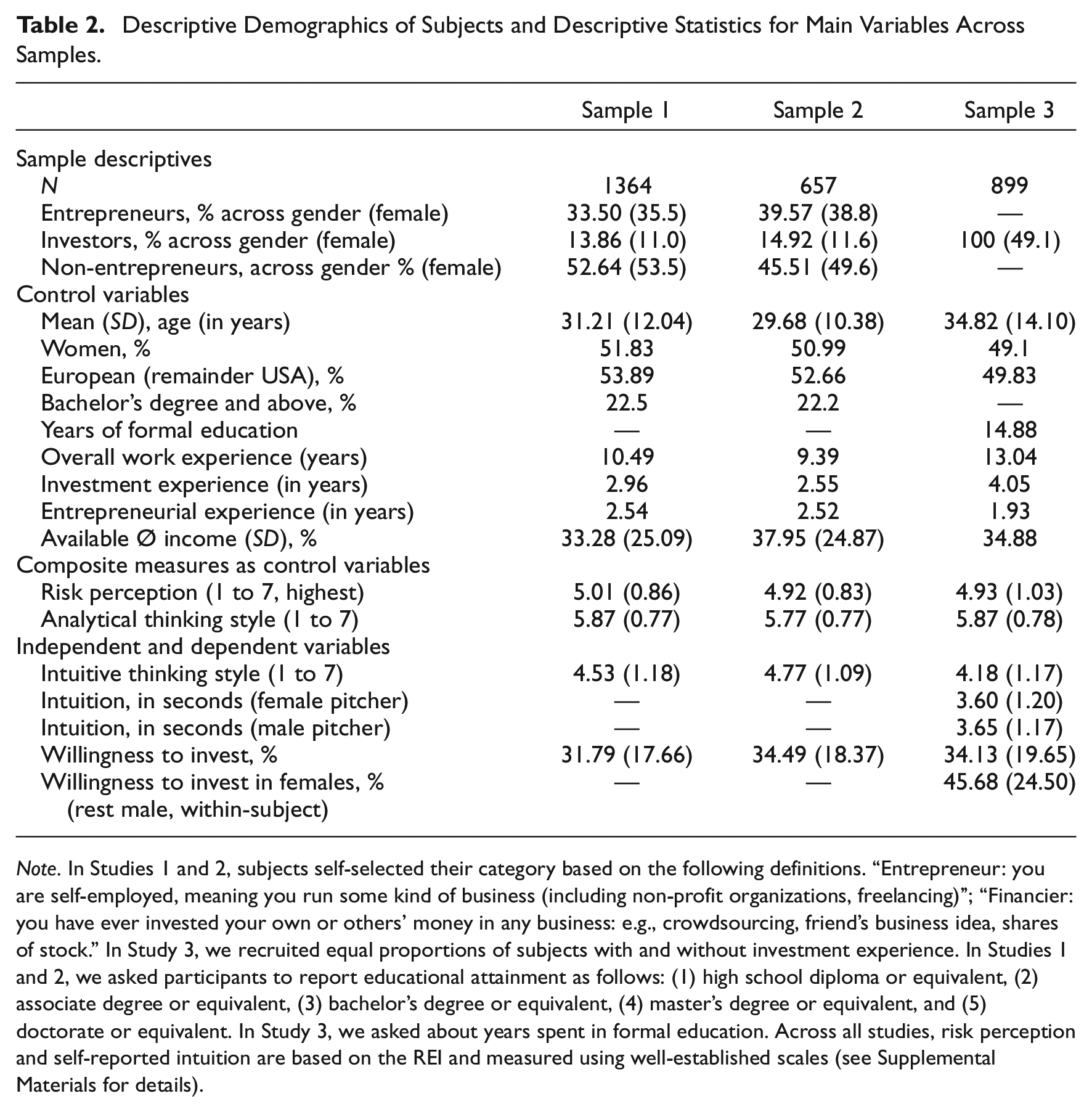

Table 1 presents an overview of subject demographics in all three studies. We recruited equal proportions by gender and nationality (Europe vs. the United States) across studies. While in Studies 1 and 2, we also recruited equal proportions for participant type for control group purposes (entrepreneurs, investors, non-entrepreneurs), in Study 3 we recruited equal proportions regarding investor experience (none vs. some). Across studies, our subjects were on average 31.90 years old. On average, our subjects had 3.19 years of investment experience. See Supplemental Material (Supplemental Text 1) and Supplemental Material S2 (section 4.1, 5.1 and 6.1) for data preparation such as testing key assumptions for our models, exclusion and inclusion criteria applied to the data, robustness checks, and randomization checks. All key assumptions for the models were met, randomization checks were successful, and robustness checks of all data confirmed the results.

Study Overview.

Note. N indicates the number of subjects analyzed after exclusion criteria were applied. Robustness analyses including excluded subjects that do not change our results or conclusions are provided in the Supplemental Material S2.

Investor Willingness to Invest Across Pitcher Gender

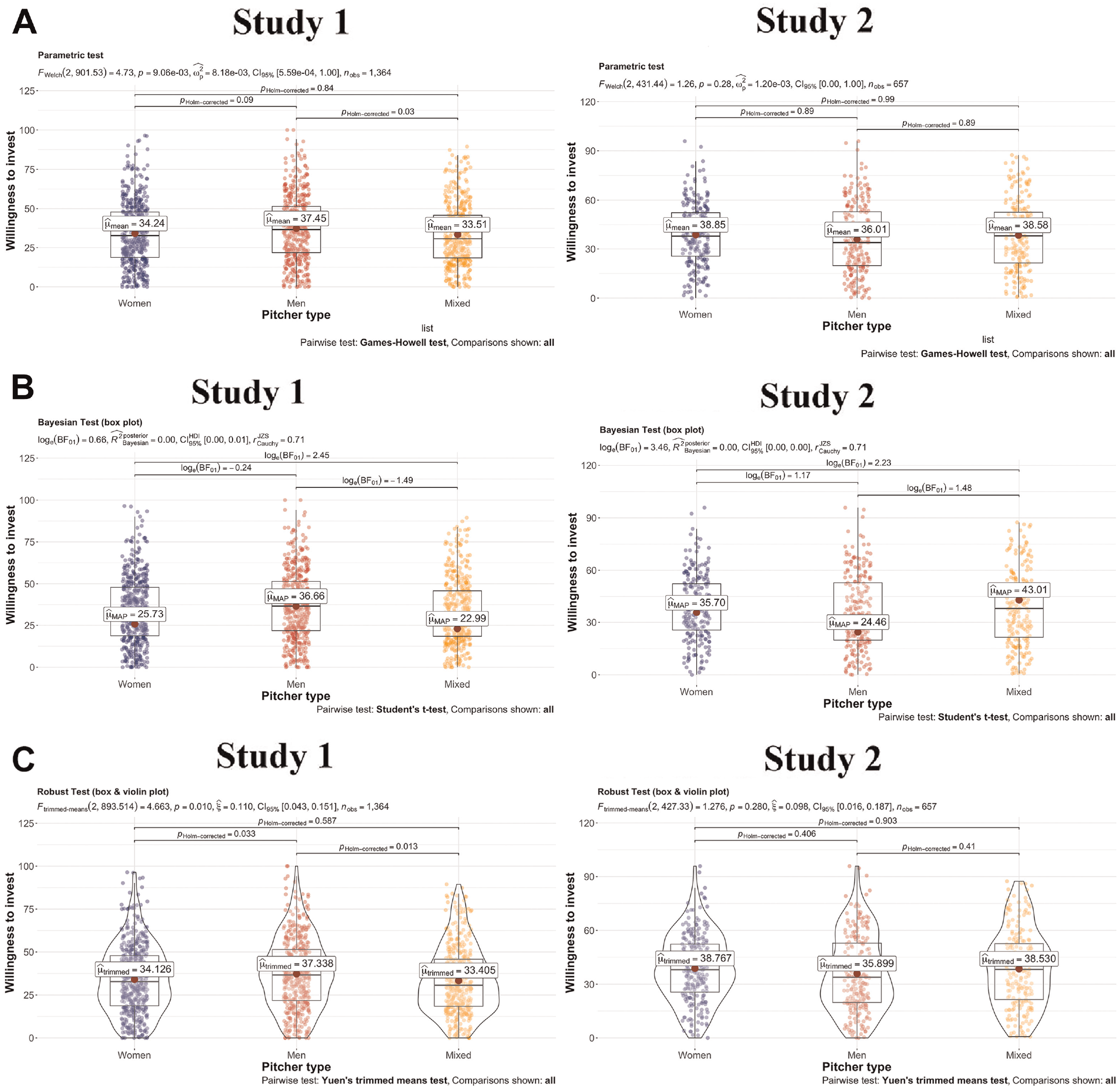

As we are primarily interested in the two-way interaction between intuition and treatment in pitches with different gender profiles, we first inspect the data regarding differences between the conditions across studies. We thus begin by exploring whether investor willingness to invest is significantly different between the three conditions (female pitch vs. male pitch vs. mixed-gendered pitch) between subjects in Studies 1 and 2 and between female and male pitches within subjects in Study 3. Figures 3 and 4 outline the following violin plots and tests across studies: (A) parametric Welch t-tests or Student t-tests for Study 3, (b) BF tests, and (c) robust t-tests. Violin plots with 95% confidence intervals (CIs) were chosen; by default, natural logarithms for BF values are shown (loge(BF01) = −loge(BF10)). To calculate BFs and posterior estimates, we used default priors that are described by a JZS/Cauchy distribution centered around zero and with a width parameter of rJZS/Cauchy = 0.71.

Violin plots of test results for willingness to invest in between-subject Studies 1 and 2. (a) Welch’s t-tests. (b) Bayesian tests. (c) Robust t-tests. The robustness test involves Yuen’s t-test for trimmed means and p-values based on Hochberg’s method. The trim level for the mean was set to 0.005.

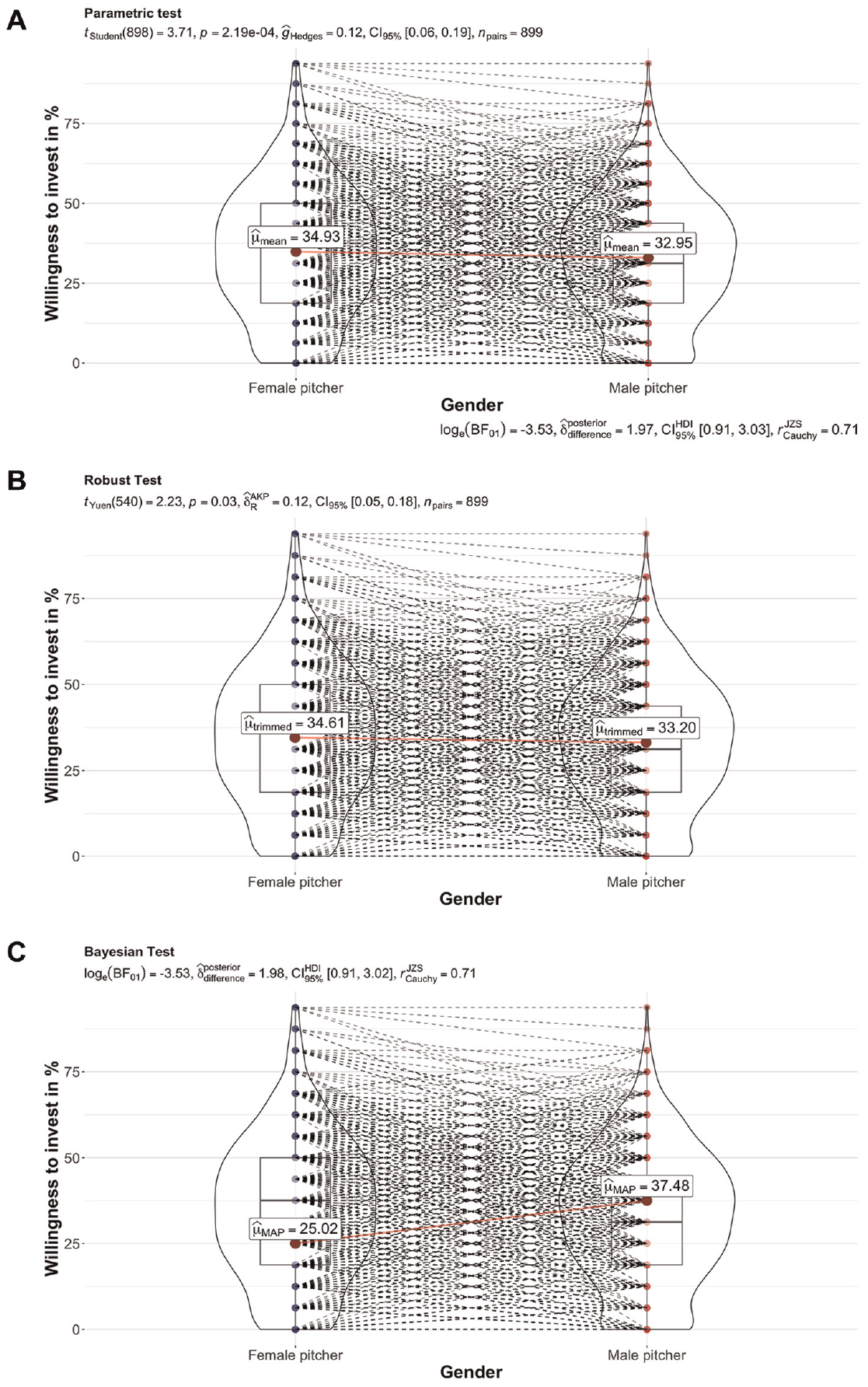

Violin plots for test results for willingness to invest for within-subject Study 3. (a) Student’s t-tests. (b) Robust t-tests. The robustness test involves Yuen’s t-test for trimmed means and p-values based on Hochberg’s method. The trim level for the mean was set to 0.005. (c) Bayesian tests.

Study 1

Figure 3a illustrates the Study 1 (n = 1,364) results, which reveal that female and male pitchers performed significantly differently in terms of investors’ willingness to invest. For that willingness, the parametric Welch’s t-test shows a tWelch(2,901.53) = 4.73, P = 9.06e−03 (two-sided), with 95% CI [5.59e−04, 1.00] and effect size Omega squared w&2; = 8.18e−3, indicating a significant difference between investors’ willingness to invest with women, men, and both. On average, investor’s willingness to invest in women was 34.24%, whereas in men it was 37.45%; the gender-mixed pitch control was 33.51%. The Bayesian statistics shown in Figure 3b reveal loge(BF01) = 0.66, δ = 0.00, and 95% HDI [0.00, 0.01], indicating strong evidence for the alternative hypothesis (BF10) over the null hypothesis (BF01) and highlighting a significant gender difference between women (µMAP = 25.73%) and men (µMAP = 36.66%); the gender-mixed pitch used as control had a µMAP of 22.99%. The Yuen robustness t-test in Figure 3c with trimmed means (set to 0.005) and P-values based on Hochberg’s method supports those results: tYuen (2,893.51) = 4.663, P = 0.010, and δ = 0.103, with 95% CI [0.058, 0.163], and µtrimmed = 34.13% for women and µtrimmed = 37.34% for men. To conclude, in Study 1 the male pitcher performed significantly better, on average, with regard to investor willingness to invest than the female pitcher.

Study 2

In contrast to Study 1, Figure 3a illustrates the Study 2 (n = 657) results, which reveal that female and male pitchers performed equally successfully in terms of investors’ willingness to invest. For that willingness, the parametric Welch’s t-test shows a tWelch(2,431.44) = 1.26, P = 0.28 (two-sided), with 95% CI [0.00, 1.00] and effect size Omega squared w&2; = 1.20e−3, highlighting that there is not enough evidence for a significant difference between investors’ willingness to invest in women and men. On average, that willingness was 38.85% for women, whereas for men it was 36.01%; the gender-mixed pitch used as control was 38.58%. The Bayesian statistics shown in Figure 3b reveal loge(BF01) = 3.46, δ = 0.00, with 95% HDI [0.00, 0.00], which represents substantial evidence for the null (BF01) over the alternative hypothesis (BF10), meaning that there is no significant gender gap: (µMAP = 35.70% for women and µMAP = 24.46% for men; µMAP = 43.01% for gender-mixed pitch as control. Yuen’s robustness t-test (see Figure 3c) with trimmed means (set to 0.005) and P-values based on Hochberg’s method confirms those results: tYuen (2,427.33) = 1.276, P = 0.280, and δ = 0.104, with 95% CI [0.023, 0.172] and µtrimmed = 38.77% for women and µtrimmed = 35.90% for men (µtrimmed = 38.53% for gender-mixed pitch as control). To conclude, on average, in Study 2 female and male pitchers performed equally successfully in terms of investors’ willingness to invest. Through the use of Bayesian statistics, we were able to provide substantial evidence in support of the gender equality effect.

Study 3

Figure 4a illustrates the results for Study 3 (n = 899), which used a within-subject design. The analysis shows that female pitchers had a higher rate of success in terms of investors’ willingness to invest compared to male pitchers. For that willingness, the paired samples t-test shows t (898) = 3.71, P = 2.19-4 (two-sided), with 95% CI [0.06, 0.19] and effect size ĝHedges = 0.12, highlighting that there is enough evidence to identify significant difference between investor’s willingness to invest in women and men. On average, investors’ willingness to invest in men was 32.95%, whereas in women it was 34.93%. The Bayesian statistics shown in Figure 4c reveal loge(BF01) = −3.53, δ = 1.97, which indicates substantial evidence for the alternative (BF10) over the null hypothesis (BF01) and highlights a significant gender difference, with 95% HDI [0.90, 3.03] and µMAP = 25.02% for women and µMAP = 37.48% for men. Yuen’s robustness test (Figure 4b) with trimmed means (set to 0.005) and P-values (two-sided) based on Hochberg’s method support these results: tYuen (540) = 2.23, P = 0.03, and δ = 0.12, with 95% CI [0.06, 0.19], and µtrimmed = 34.61% for women and µtrimmed = 33.20% for men. The parametric and robust tests measure means and trimmed means, respectively, whereas the Bayesian test measures the maximum a posteriori (MAP) probability, which can be regarded as the mode of the posterior distribution. The female distribution has a larger average (mean) but a relatively low peak (mode), whereas the male distribution has a smaller average (mean) but a relatively high peak (mode). To conclude, Study 3 indicates investors, on average, tend to invest more in women than in men. As our samples included both experienced and non-experienced investors, we performed a robustness analysis to assess whether experience influences willingness to invest significantly. Our results reveal that investor experience does not change our results (see Supplemental Material S2, section 6.6.2).

Investors’ Use of Intuition Drives Willingness to Invest, Regardless of Pitcher Gender

In our preregistrations, we hypothesized that use of intuition drives willingness to invest in a pitcher of different gender (HA). From a Bayesian perspective, we also test the null hypothesis (H0): investors’ use of intuition drives willingness to invest, regardless of gender. To test this hypothesis, we use a linear regression model of the effect of intuition measured via REI in Studies 1 and 2 and the between-subject condition that used differently gendered pitches, including two-way interactions. In Study 3, we used decision time to measure intuition and included the random slopes for each participants because we used trial-level data. Due to our between-subject design in Studies 1 and 2, we do not have to control for potential confounding variables, while the design in Study 3 allowed us to control for products and changes in gender.

Our regression equations for Studies 1 to 3, where for i = n observations, yi = willingness to invest (%), β0 = intercept, REIi = self-reported intuition, PGi = pitcher’s gender, β1 to β3 = slope coefficients for each variable and the interaction, and ϵi = error term are as follows ((1 + PG | ID) is only added in Study 3 in which we use trial-level data):

Our regression equations for Study 3, where for i = n observations, yi = willingness to invest (%), β0 = intercept, FIi = behavioral intuition via fast decisions (decision time in seconds), PGi = pitcher’s gender, β1 to β3 = slope coefficients for each variable and the interaction, and ϵi = error term are as follows ((1 + PG | ID) is only added in Study 3 in which we use trial-level data):

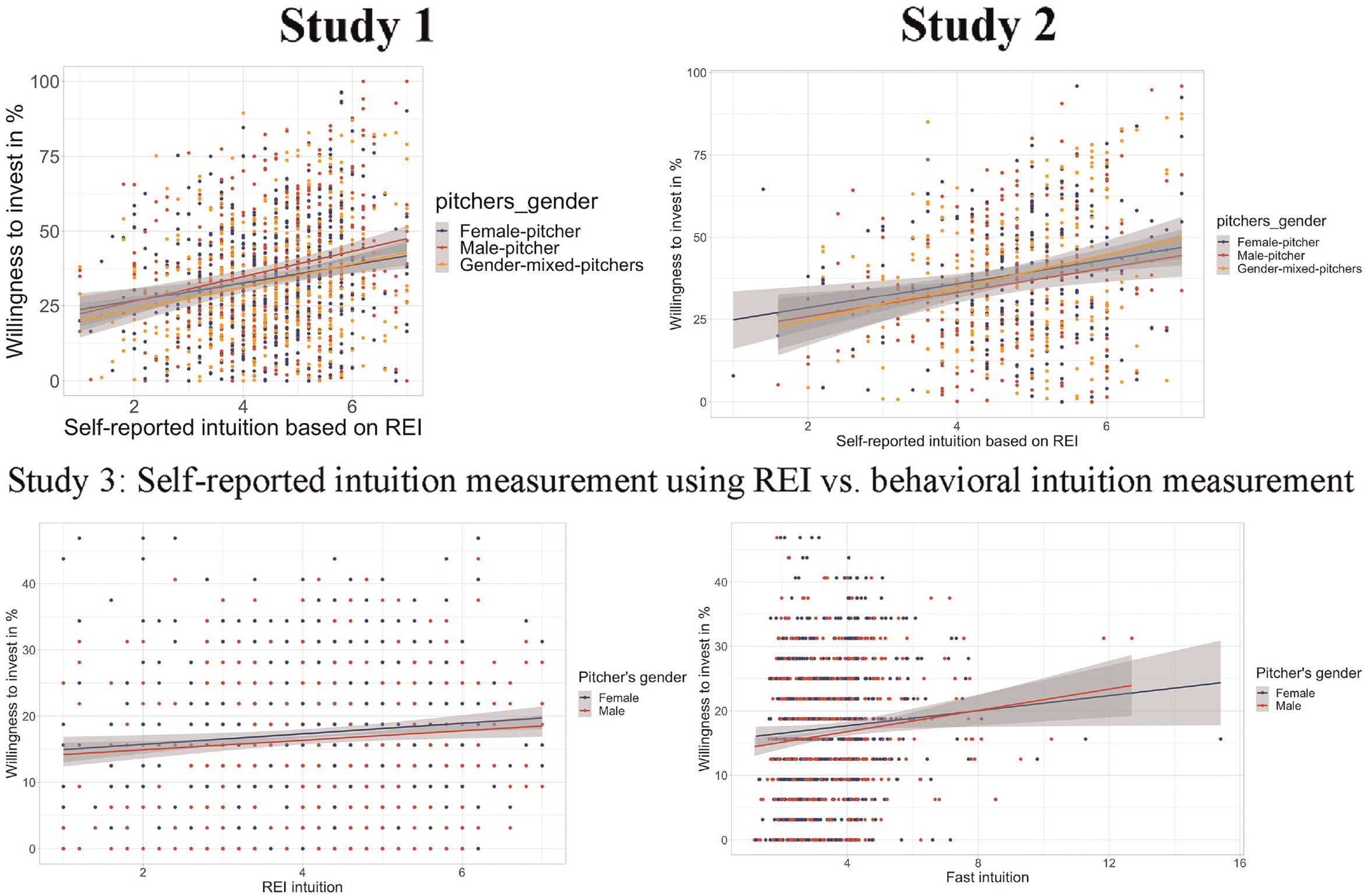

Figure 5 visualizes the regression slopes of willingness to invest and self-reported intuition across the studies.

Regression slopes for investors’ willingness to invest for different genders by intuition.

Bayesian Inferences: Investors’ Use of Intuition Drives Willingness to Invest, Regardless of Pitcher Gender

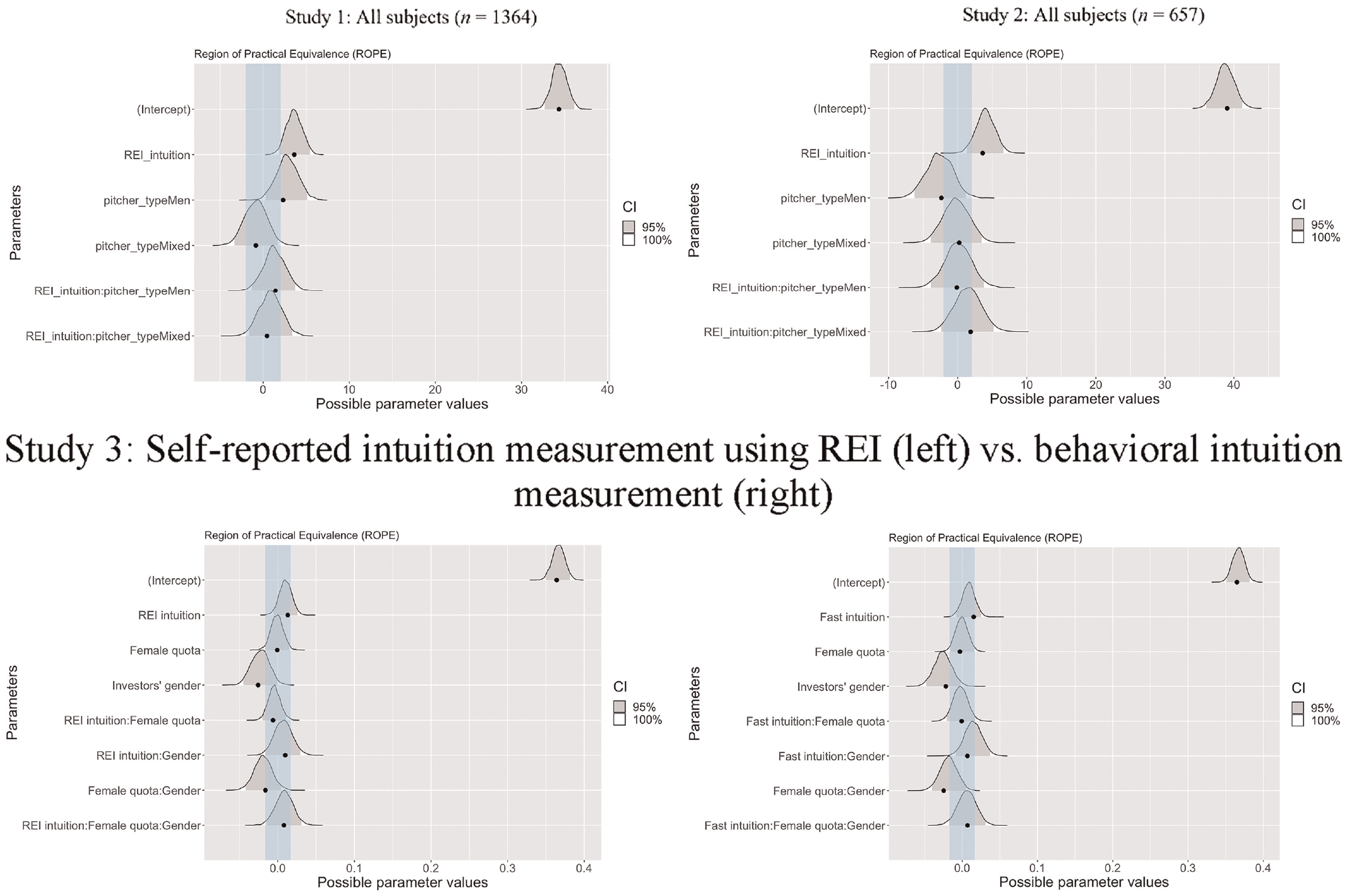

For all three studies, Figure 6 illustrates investors’ mean willingness to invest via a point, possible parameter values of all variables under investigation, predictive band intervals of the HDI alongside the data via its posterior predictions (levels 95%, gray curves), and the conventional region of practical equivalence (ROPE), using Cohen’s d to indicate small effect sizes (marked in blue).

Bayesian posteriors distributions, HDI, and ROPE across studies.

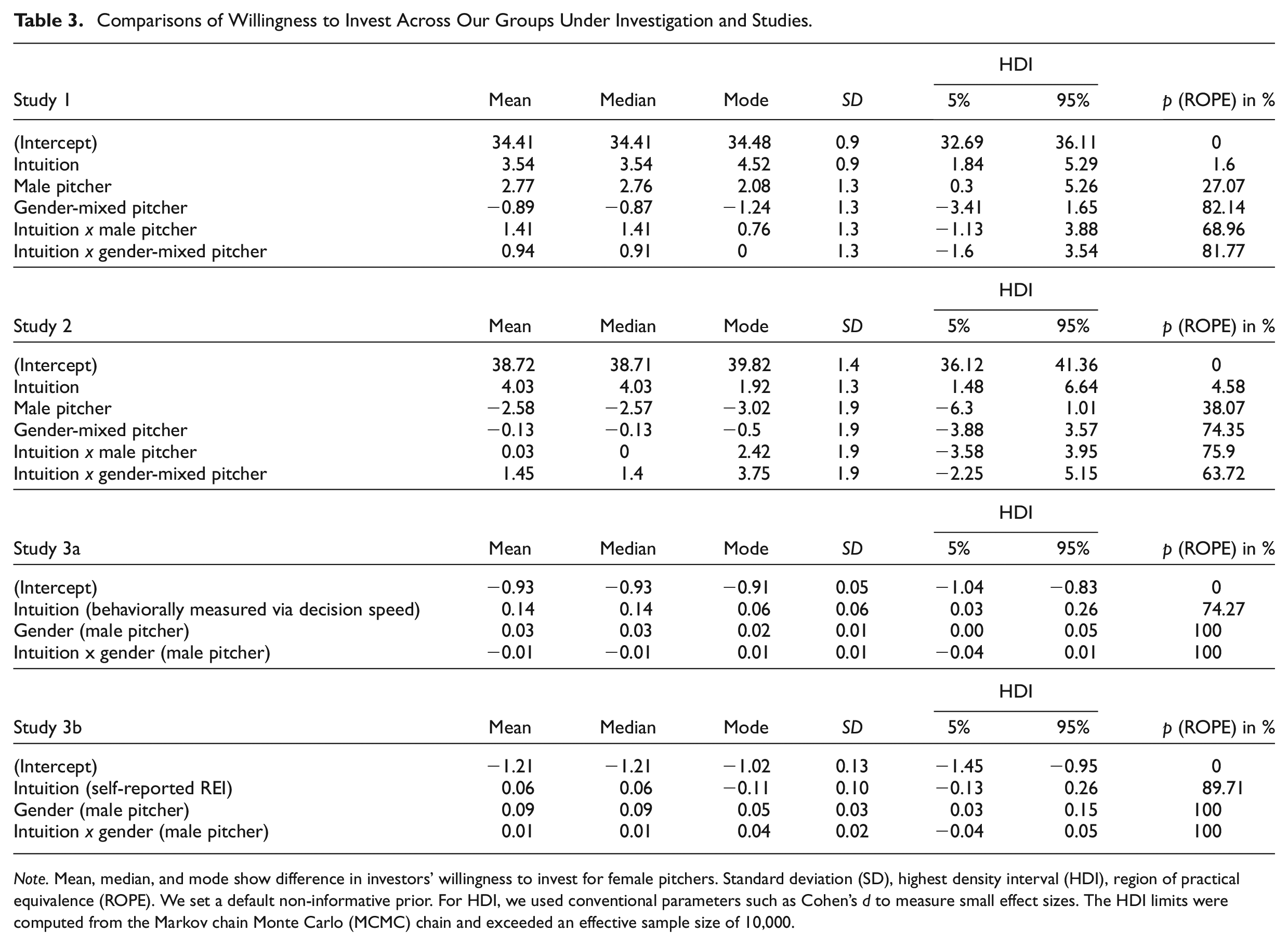

Table 2 presents the mean, median, mode, standard deviations (SD), HDI, and percentage within ROPE to allow readers to decide whether to accept or reject the null hypothesis. Our Bayesian analysis reveals that in the between-subject design in Study 1 examining self-reported intuition, only 1.6% of the HDI falls within the ROPE, which provides strong evidence in favor of the alternative hypotheses that investors’ self-reported intuition shows significant effect on their willingness to invest (β = 3.54, SD = 0.9, 95% HDI [1.84, 5.29]). This significant effect was also detected in the replication Study 2 (with a between-subject design), in which only 4.58% of the HDI falls within the conventional ROPE (β = 4.3, SD = 1.3, 95% HDI [1.48, 6.64]). However, these findings that intuition facilitates willingness to invest were not confirmed in Study 3, which used a different design (a within-subject design) with both self-reported REI (89.71% in ROPE, β = 0.06, SD = 0.10, 95% HDI [−0.13, 0.26]) and intuition measured behaviorally using fast decision-making (74.27% in ROPE, β = 0.14, SD = 0.06, 95% HDI [0.03, 0.26]). These conflicting results regarding whether intuition facilitates willingness to invest and the results regarding whether one gender is preferred over the other allow us to investigate the interaction effects of the results in the context of real-world biases.

Descriptive Demographics of Subjects and Descriptive Statistics for Main Variables Across Samples.

Note. In Studies 1 and 2, subjects self-selected their category based on the following definitions. “Entrepreneur: you are self-employed, meaning you run some kind of business (including non-profit organizations, freelancing)”; “Financier: you have ever invested your own or others’ money in any business: e.g., crowdsourcing, friend’s business idea, shares of stock.” In Study 3, we recruited equal proportions of subjects with and without investment experience. In Studies 1 and 2, we asked participants to report educational attainment as follows: (1) high school diploma or equivalent, (2) associate degree or equivalent, (3) bachelor’s degree or equivalent, (4) master’s degree or equivalent, and (5) doctorate or equivalent. In Study 3, we asked about years spent in formal education. Across all studies, risk perception and self-reported intuition are based on the REI and measured using well-established scales (see Supplemental Materials for details).

We found strong support for the null over the alternative hypothesis for the interaction effect of (self-reported or behaviorally measured) intuition and gender across all studies. In other words, intuition and gender do not affect willingness to invest. Although the gender of the pitcher (in our analysis, the male) did show a positive impact on investors’ willingness to invest in Study 1 (27.07% in ROPE, β = 2.77, SD = 1.3, 95% HDI [0.3, 5.26]) and a negative impact in Study 2 (38.07% in ROPE, β = −2.58, SD = 1.9, 95% HDI [−6.3, 1.01]), Bayesian analysis provides strong evidence supporting the absence of a reliable interaction effect between gender and self-reported intuition in both Study 1 (68.96% in ROPE, β = 1.41, SD = 1.3, 95% CI [−1.13, 3.88]) and Study 2 (75.9% in ROPE, β = 0.03, SD = 1.9, 95% CI [−3.58, 3.95]). This suggests that there is strong evidence for the lack of a significant interaction effect between gender and self-reported intuition. Likewise, Bayesian analysis provides strong evidence for the absence of a reliable interaction effect between a gender-mixed pitch and intuition in both Study 1 (81.77% in ROPE, β = 0.94, SD = 1.3, 95% HDI [−1.6, 3.54]) and Study 2 (63.72% in ROPE, β = 1.45, SD = 1.9, 95% HDI [−2.25, 5.15]). This suggests that there is strong evidence supporting the lack of a significant interaction effect between a gender-mixed pitch and self-reported intuition based on the Bayesian analysis. Study 3 provided similar results for both self-reported intuition and intuition measured behaviorally through fast decision-making. In line with the findings from Studies 1 and 2, the Bayesian analysis provides strong evidence for the absence of a reliable interaction effect between gender and intuition, both for self-reported intuition (100.00% in ROPE, β = 0.01, SD = 0.02, 95% CI [−0.04, 0.05]) and behaviorally measured intuition (100.00% in ROPE, β = −0.01, SD = 0.01, 95% CI [−0.04, 0.01]). These robust results offer substantial support for the absence of a significant interaction effect between gender and both self-reported and behaviorally measured intuition. Thus, we can conclude that—whether intuition does facilitate willingness to invest (as in Studies 1 or 2) or does not (as in Study 3)—intuition cannot be cited as the reason for any gender biases in investment decisions, whether there is a bias in place (as in Studies 1 and 2) or not (as in Study 3).

For each study, we run a BF design analysis to determine how many subjects would be needed to receive a significant interaction of gender and intuition (see Supplemental Material S2). For Study 1, we would need approximately 40,000 subjects to obtain a BF larger than 10 with a 5% probability. For Study 2, we would need a sample size of ~37,500–40,000 to ensure a BF larger than 10 with a 95% probability. Finally, using Study 3 data, we would need approximately 20,000 to ensure a BF larger than 10 with a 95% probability to receive a significant within-subject gender–intuition interaction. Our BF design analysis and these high sample sizes highlight how challenging it is to obtain a significant interaction result of gender and intuition and thus provide enough evidence to confirm that investor intuition (whether self-reported or behaviorally measured) is not responsible for gender bias. This analysis supports our conclusion that intuition facilitates gender equality rather than the opposite, which has previously been used to explain human errors and stereotyping (Balachandra et al., 2019).

Secondary Analyses

We performed a series of secondary analyses to check several assumptions: (1) the higher one’s risk awareness, the lower one’s willingness to invest; (2) the greater an investor’s investment experience, the lower the willingness to invest; (3) investor gender affects willingness to invest; and (4) the higher the average decision time, the greater one’s willingness to invest. All of these assumptions were non-significant except for assumption (3). All code and results can be found in Supplemental Material S2.

Bayesian Sensitivity Analysis and Robustness Checks

To assess the robustness of our results, we performed several reliability and validity checks across the three studies. (1) We tested how results changed across different actors in Studies 1 and 2 and across different products and founders in Study 3. Although we observed different biases in Studies 1 and 2, our results are robust and did not change. Likewise, in Study 3 we tested gender-oriented industry types by switching the gender seen with a product pitch. This gender-switching did not change our results. (2) We used a real-world investment task. Because we used images including founder and product to invest as naturally occurring stimuli, our results are both ecologically valid and thus generalizable to a specific context or population and externally valid and thus generalizable across different contexts and populations (Campbell, 1957; Highhouse, 2009). (3) We performed checks to ensure that our randomization worked (see Supplemental Text 1). Overall, randomization and active subject participation boosted our internal validity (Kenny, 2019). Furthermore, we performed ex ante and post hoc manipulation checks related to understanding the material, manipulation awareness, and the effectiveness of the material. (4) Variables are taken from both subjective sources like self-reports and objective sources like behavioral responses. For the self-reports, we assessed interrater reliability using Cronbach’s α (see Supplemental Text 1). (5) We performed analyses both with and without the outliers and both applying and ignoring the exclusion criteria. None of the resulting analyses affected our results; see Supplemental Material S2 for more details.

Discussion

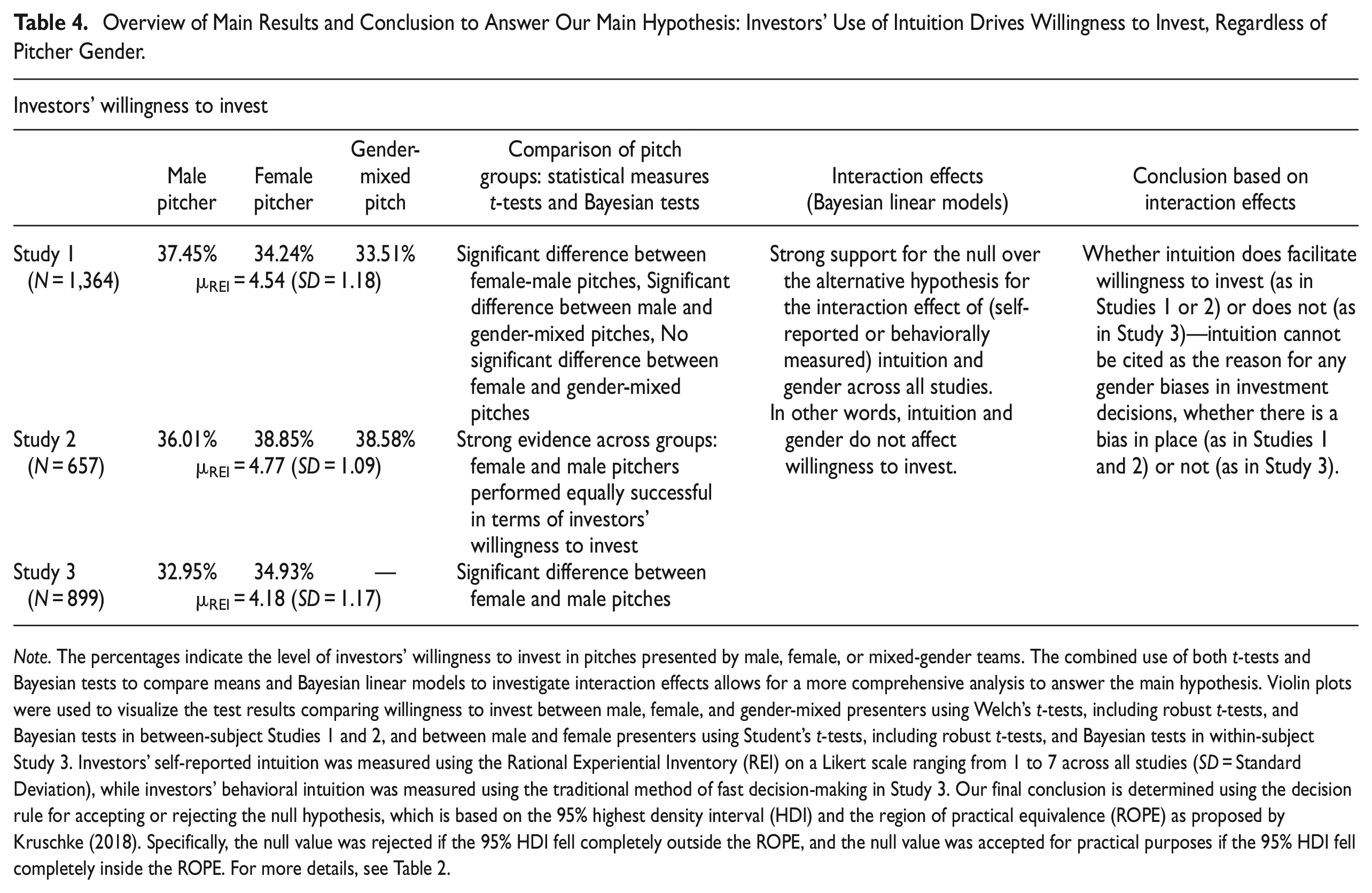

Because women tend to be at least as successful as men in the reward-based crowdfunding context, the aim of our research was to assess whether intuition promotes gender equality in this novel financial market. Our approach, building on previous studies (e.g., Johnson et al., 2018), enabled us to investigate whether intuition could explain gender biases. We investigate whether investors’ intuition was a significant driver for gender preferences in their willingness to invest. In particular, based on signal detection theory (Macmillan & Creelman, 2004; Stanislaw & Todorov, 1999) we argued that both experience and inexperienced investors’ self-reported intuition and/or actual behavioral use of intuition tend to be equal as to founder’s gender in terms of their willingness to invest. Table 3 summarizes the main findings for our central hypothesis if investors’ use of intuition drives willingness to invest, regardless of pitcher gender.

Comparisons of Willingness to Invest Across Our Groups Under Investigation and Studies.

Note. Mean, median, and mode show difference in investors’ willingness to invest for female pitchers. Standard deviation (SD), highest density interval (HDI), region of practical equivalence (ROPE). We set a default non-informative prior. For HDI, we used conventional parameters such as Cohen’s d to measure small effect sizes. The HDI limits were computed from the Markov chain Monte Carlo (MCMC) chain and exceeded an effective sample size of 10,000.

Overview of Main Results and Conclusion to Answer Our Main Hypothesis: Investors’ Use of Intuition Drives Willingness to Invest, Regardless of Pitcher Gender.

Note. The percentages indicate the level of investors’ willingness to invest in pitches presented by male, female, or mixed-gender teams. The combined use of both t-tests and Bayesian tests to compare means and Bayesian linear models to investigate interaction effects allows for a more comprehensive analysis to answer the main hypothesis. Violin plots were used to visualize the test results comparing willingness to invest between male, female, and gender-mixed presenters using Welch’s t-tests, including robust t-tests, and Bayesian tests in between-subject Studies 1 and 2, and between male and female presenters using Student’s t-tests, including robust t-tests, and Bayesian tests in within-subject Study 3. Investors’ self-reported intuition was measured using the Rational Experiential Inventory (REI) on a Likert scale ranging from 1 to 7 across all studies (SD = Standard Deviation), while investors’ behavioral intuition was measured using the traditional method of fast decision-making in Study 3. Our final conclusion is determined using the decision rule for accepting or rejecting the null hypothesis, which is based on the 95% highest density interval (HDI) and the region of practical equivalence (ROPE) as proposed by Kruschke (2018). Specifically, the null value was rejected if the 95% HDI fell completely outside the ROPE, and the null value was accepted for practical purposes if the 95% HDI fell completely inside the ROPE. For more details, see Table 2.

Regarding the gender-mixed pitch control in Study 1, it is not surprising that the willingness to invest was lower in this condition compared to the all-male or all-female pitches. However, the difference between the female pitch and the gender-mixed pitch in Study 1 is minimal and lacks statistical significance. It is important to note that this finding is consistent with previous research which has shown that individuals may experience bias or uncertainty when evaluating mixed-gender groups (e.g., Eagly & Karau, 2002; Heilman & Haynes, 2005). This may be due to several factors, such as investors perceiving mixed-gender teams as less cohesive or having more communication problems. Additionally, investors may find it more difficult to evaluate mixed-gender teams, particularly if there are, gender dynamics at play that could impact decision-making. For instance, there has been a considerable amount of research exploring the potential impact of various factors on crowdfunding success, including aspects of entrepreneurial pitches such as linguistic content (Balachandra et al., 2019; Ren et al., 2021), vocal expressions (Allison et al., 2022), facial expressions (Jiang et al., 2019; Stroe et al., 2020; Warnick et al., 2021), and more general bodily gestures (Clarke et al., 2019). It is important to note that our results are based on two studies, and further research is needed to confirm and expand on these findings. Additionally, it is important to interpret the results to our gender-mixed pitch control, which represents not the center of our research interest in this work, with caution and not jump to conclusions about individual preferences or biases towards specific gender groups.

Our statistical analysis of pitch groups using t-tests and Bayesian tests produced contrasting results across our three studies. In Study 1, we observed a significant difference between male and gender-mixed pitches with men performing better, a significant difference between female and male pitches, and no significant difference between female and gender-mixed pitches. In Study 2, we found strong evidence indicating that female and male pitchers performed equally well in terms of investors’ willingness to invest. In Study 3, we observed a significant difference between female and male pitches, with women performing better. While our research focuses on the interaction effect of gender and investors’ intuition, these contradictory results in gender preferences warrant further discussion.

One possible explanation for the difference between Studies 1 and 2 could be the context or the quality of the videos in which the pitches were presented. However, as we have used three pitching stages (written teaser, audio teaser, and video teaser), we were able to test whether investors’ willingness to invest changed significantly from the written teaser stage to the audio teaser stage in Study 1. Our findings revealed that there was no significant change in willingness to invest, suggesting that the timing of gender disclosure did not affect gender preferences. Another potential explanation could be the particular characteristics of the investors in each study, such as a greater receptiveness to pitches from female entrepreneurs in Studies 2 and 3. However, it is important to note that the focus of our research is on the interaction effects between gender and investors’ intuition, and studies with and without gender preferences have helped us to highlight that, regardless of biases toward a specific gender, the interaction effect of intuition and presenter gender promotes gender equality. Through our Bayesian approach, we were able to provide evidence for this effect.

Prior research has highlighted the empirical challenges involved in explaining causal relationships between gender and investment decisions (Bapna & Ganco, 2021; Brooks et al., 2014). While it is feasible to measure actual investment decisions in a controlled setting with a gender manipulation (Bernstein et al., 2017; Døskeland & Pedersen, 2016; Hornuf & Siemroth, 2023), manipulating gender to investigate intuition in investment decisions in real-world contexts poses considerable challenges. Therefore, conducting a field experiment would not have been a suitable method to explore causal relationships in this context. Moreover, colleagues have addressed additional methodological challenges in measuring the actual use of intuition (e.g., Allinson & Hayes, 2000; Hayes et al., 2004; Norenzayan et al., 2002; Sinclair, 2020; Sinclair & Ashkanasy, 2005). Methodologically, we therefore designed laboratory experiments (Studies 1 and 2) as a first step to test our hypothesis and replicated them with actual founders and products from successful real projects (Study 3).

As a consequence, the following reasons underline our study’s ecologically validity. (1) As we focus on one pitching idea and four founders in the between-subject Studies 1 and 2 rather than any observed or unobserved characteristics of the founder or unobserved quality differences across ventures in the sample, we do not face any endogeneity problem in the estimates in Studies 1 and 2. The pitches between subjects, manipulated only by gender, were held constant across Studies 1 and 2, with one exception in Study 2—the first stage of the written investment teaser mentioned the name of either a male or female founder. In Study 3, our randomization across 16 switched gender pitches and 16 real gender pitches helped us rule out gender-related founder characteristics of projects that could affect funding decisions. (2) As we used pitching examples with equal proportions of female and male pitchers, we do not face issues arising from the existence of more male- than female-founded ventures. Moreover, due to our gender-switched pitches, we also investigated whether female-founded ventures tend to be active in specific domains that could affect investors’ willingness to invest. (3) Due to inconsistent findings in the literature across different types of investors, we recruited both professional and lay investors who were both active in reward-based crowdfunding.

Our results are externally valid for the following reasons. (1) On one hand, we included different investor types; on the other, we also controlled for differences in investment experience in years by using both between- and within-subject designs. Our secondary analyses and robustness checks show that the non-significant intuition–gender interaction on willingness holds true regardless of investor experience or investor type. The use of Bayesian analysis enabled us to provide evidence for the absence of effects. (2) Intuition has usually been measured by speed of operation and ease of application (Krajbich et al., 2015). While across studies we used self-reported intuition by employing the well-established REI, we tested the behavioral use of intuition through fast investment decisions in Study 3. Even if there is a gender bias making investors more willing to invest in one gender than the other (a male presenter in Study 1 or a female presenter in Study 3), the non-significant relationship of the intuition–gender interaction on willingness to invest holds true for both complementary self-reported and behaviorally measured intuition. The use of Bayesian analysis enabled us to provide evidence for the absence of effects. Thus, we can conclude that our results remain unchanged regardless of which measurement (between- or within-study design and self-reported vs. behavioral intuition measurement) is used. (3) We used four actors (two females and two male) to pitch the same idea in Studies 1 and 2; in Study 3, we used many real-world pitchers and products from successful real-world reward-based crowdfunding campaigns. As our robustness analysis reveals, even switching the gender of the founder did not change investors’ willingness to invest depending on their intuition. Moreover, our secondary analyses reveal that whether a gender difference or bias exists, intuition is not responsible for that difference or bias. Therefore, we can conclude that our results are applicable to pitchers of all genders, which calls for a reevaluation of intuition’s scientific credibility in financial decision-making.

Theoretical Implications

According to Fisher and Neubert (2023) financing involves ambiguity and equivocality, making it difficult to rely solely on a rational evaluative process. Therefore, intuition can play an important role that should not be overlooked. We enhanced the reward-based crowdfunding literature which investigated the role of heuristic-based biases among amateur investors (Kahneman & Klein, 2009) and expert intuition among experienced investors (Dane & Pratt, 2007; Kahneman & Klein, 2009) via adding signal detection theory (Macmillan & Creelman, 2004; Stanislaw & Todorov, 1999) as a theoretical framework for understanding how gender-based stereotypes can impact investment decisions in the reward-based crowdfunding ecosystem. We argue that gender-based stereotypes, which are often present implicitly, may not necessarily harm any particular gender during investment decisions in the reward-based crowdfunding ecosystem, as long as investors rely on either expert or lay intuition. The subjective-driven signal used to identify investment opportunities plays a crucial role in this regard.

Our results also extend prior intuition theory and the gender literature more broadly by showing that investor intuition is a driver of gender equality in reward-based crowdfunding. Dane and Pratt’s (2007) theory of intuition argues that task characteristics influence the effectiveness of intuition. More specifically, intuition becomes more effective relative to rational analysis if an environment is unstructured. While traditional financial markets that are characterized by gender differences are highly structured, such as venture capital markets, crowdfunding’s emotional aspects (Li et al., 2017; Mollick, 2014) show characteristics of an unstructured market with judgement tasks for which both experienced and inexperienced investors are more likely to use intuition which is beneficial for gender equality in the crowdfunding ecosystems.

Much of the research to date views bias as something that must be reduced or eliminated to reduce inequalities (Brands & Kilduff, 2014), or assumes that one gender must adapt to the conditions of bias; for example, women might be more successful if they were more masculine (Balachandra et al., 2019). Using Bayesian inferences across three studies, we have provided strong evidence that—whether there is a gender bias or preference at play or whether intuition boosts willingness to invest—the interaction of gender and intuition does not have a significant influence on that willingness. Thus, intuition cannot serve as an explanation or meaningful factor for gender biases that should be eliminated, and we can conclude that intuition does not create biases that could harm the central outcome. As such, the present study highlights how important intuition is for financing tomorrow’s innovation, regardless of gender, because it shows potential to promote gender equality.

Limitations and Further Research