Abstract

People well known to the general public are increasingly acting as business angels (BAs) for young and innovative ventures worldwide. These BAs are less known for their venture evaluation skills and often do not have a professional reputation as investors. The signaling function of these well-known investors could therefore be less relevant for founders because of a limited quality assurance function. Nonetheless, a venture’s affiliation with a well-known BA may still positively alter the quality perceptions of various stakeholders because the BAs can put their reputation in other areas of life at risk, provide an easy-to-interpret and fluent cue to the general public, and improve the observability of the signal. Using a sample of more than 2,900 early-stage ventures that made a venture pitch during the Canadian, German, U.K., and U.S. versions of the reality TV show Dragons’ Den, we find that BAs’ degree of being known has a positive impact on target firm survival, web traffic, and sales. The impact of BAs’ general degree of being known is particularly strong if the congruency between the investors and the target ventures is high. These effects exist over and above potential selection effects, the professional reputation of the BA, and the greater financial resources of a funded venture. The empirical findings indicate that well-known BAs can have a positive effect on venture performance and that founders should consider not only the professional reputation of BAs but also the degree to which they are known to a general audience.

JEL classifications: G24, M13

Investors as startup promotors is underrated, @chrija has indirectly generated us 10s of thousands of $ in MRR over the year. Picking investors with the largest (targeted) audience is a very winning strategy.

—Nick Franklin (CEO and Founder of ChartMogul) on Twitter about the seed investor Christoph Janz (June 3, 2021) This Ashton-Kutcher Backed Startup Is Helping the Self-Employed Get Organized.—Forbes Magazine (June 30, 2021)

Early-stage investors often strive to improve the operating performance of their portfolio ventures (Rosenbusch et al., 2013). Their active support occurs through multiple channels, such as providing strategic and operational guidance, introducing the founders to customers and other investors, helping with sourcing, and hiring key employees (Gompers et al., 2020). However, investor support also has a passive component. By being affiliated with ventures that suffer from information asymmetry (Cohen & Dean, 2005) and performance uncertainty (Loch et al., 2008), business angels (BAs) and venture capitalists (VCs) certify the quality of a venture to external parties, such as customers, suppliers, and other investors (e.g., Megginson & Weiss, 1991). Thus, BA and VC investments passively serve as a signal of quality for ventures (Ozmel et al., 2013).

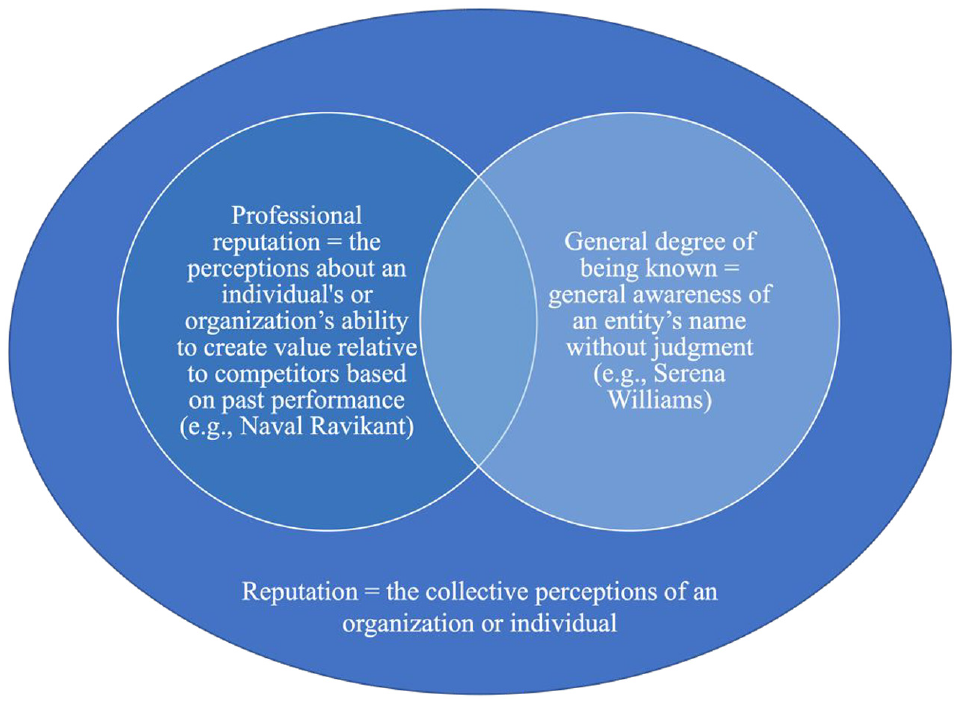

Certification of venture quality mainly occurs from the reputation of the BA or VC affiliate (Stuart et al., 1999), which is at risk when the endorsed venture does not deliver on its promises (Pollock et al., 2010). In general, reputation refers to the collective perception of an audience of an individual or organization (Lange et al., 2011; Wei et al., 2017). However, reputation is multidimensional and audience-specific (Rindova et al., 2005; Vanacker & Forbes, 2016). Most research differentiates between two distinct but related dimensions of reputation (Lange et al., 2011): (1) an individual’s or organization’s general degree of being known, which captures the general awareness of an entity’s name without judgment (Wei et al., 2017), and (2) the degree of professional reputation, 1 or the perception of an individual’s or organization’s ability to create value based on proven past performance (Rindova et al., 2005). The difference between professional reputation and the general degree of being known with regard to early-stage investor becomes clearer when considering the cases of Serena Williams and Naval Ravikant: with more than 200 investments and over 70 successful exits, including Uber, Twitter, and Clubhouse, Naval Ravikant is one of the most active and successful BAs and enjoys a high level of professional reputation among other investors and strategic partners. Nevertheless, he is far less known to the general public than Serena Williams, who enjoys less professional reputation based on her track record in angel investing.

As Figure 1 shows, the general degree of being known and the degree of professional reputation are both dimensions of an individual’s or organization’s reputation. The two dimensions of reputation may overlap, for example, when a BA or VC is generally known by a large audience and known for making value-enhancing investments. However, in practice, the two dimensions of reputation often do not overlap. Individuals or organizations are usually well known as investors because of their track record or generally well known as a result of their professional career, for example, in sports or media. Therefore, we follow Wei et al. (2017) and argue that professional reputation and the degree of being known are orthogonal constructs. Abundant evidence suggests that being affiliated with a BA with a high level of professional reputation improves venture performance and functions as a signal of quality, due to expectations that the new venture will benefit from the investors’ skills, expertise, and networks and their known evaluation skills (Gomulya et al., 2019). This perception of professional quality assurance, however, is not caused by the degree to which an investor is known to the general public. Whether the degree to which an investor is known to the general public can positively affect venture performance is still unclear.

Dimensions of reputation.

Given the growing relevance of investors who are well known to the general public but often have low levels of professional reputation, the reputational dimension of being known requires further attention. As Tide (2019) reports using data from Crunchbase, venture investments by generally well-known people are rising and becoming economically significant, with more than US$12.8 billion of capital provided over the last 10 years. Little is known about whether such affiliations benefit the venture beyond providing financial resources, as evidenced by contradicting views in social media and the business press on the advantages (e.g., Abecassis, 2017) and disadvantages (e.g., Carson, 2015) of taking money from generally well-known people.

In this study, we draw on the sociocognitive perspective in signaling theory (Rindova et al., 2012; Spence, 1973; Vanacker et al., 2020) to theoretically develop and empirically test the role of a BA’s degree of being known in early-stage financing. Specifically, we examine whether a BA’s general degree of being known affects venture performance and assess the economic relevance of this reputational dimension. We hypothesize that a BA’s general degree of being known positively affects venture performance. Moreover, we expect the positive impact of the degree of being known to be stronger if the BA is known for something that is congruent with the activities of the venture. For a general audience, congruency may serve as an easy-to-process heuristic, suggesting that stakeholders can put trust in the BA’s perceived knowledge about the venture’s quality (Hallen & Pahnke, 2016).

To empirically test our research question, we use a unique hand-collected dataset based on entrepreneurial television pitches from four different TV shows and countries (Shark Tank, United States; Dragons’ Den, Canada; Dragons’ Den, United Kingdom; and Höhle der Löwen, Germany) with 657 episodes over 15 years and covering 3,260 pitches. Our dataset allows us to capture the effect of investments by well-known BAs by tracking the ventures’ performance up to 2 years after the show. Moreover, the set of investors in these shows varies in the two dimensions of reputation because the dataset includes generally well-known people such as Charles Barkley, publicly less-known but professionally reputable BAs such as Christopher Sacca, and people falling high (e.g., Ashton Kutcher) or low (e.g., Rachel Elnaugh) on both dimensions. Our findings lend support to the prediction that an investor’s general degree of being known has a positive impact on venture performance in terms of target venture survival, web traffic, and sales. The impact of a BA’s degree of being known is particularly strong if the congruency between this BA and the target venture is high. This effect exists over and above potential selection effects, the professional reputation of the BA, and the greater financial resources of a funded venture.

We contribute to the literature on new ventures’ and affiliates’ reputations in several important ways. Our analysis of well-known BAs extends research on the role of affiliates’ reputations by examining the nonevaluative dimension of being known, which has received little empirical testing in the entrepreneurial finance literature. In doing so, we build on available research on celebrity endorsements (e.g., Zamudio, 2016) and introduce a new measure of the degree of being known to this research stream. By examining the impact of BAs’ congruency with the venture, we shed additional light on the underlying mechanisms that render the effect of being known more or less effective. To the best of our knowledge, our study is one of the first to investigate the capacity of generally well-known people acting as BAs to promote venture performance. We further contribute to the literature on the impact of BAs on new ventures. While extant research suggests that BAs significantly enhance the outcomes and performance of the selected ventures (e.g., Bruton et al., 2010; Chahine et al., 2007; Croce et al., 2021; Kerr et al., 2014), little is known about the relative importance of BAs’ different value-adding activities. In addition to assessing the role of BAs’ degree of being known, we investigate the relevance of several factors known to affect the performance of funded ventures, including the financial resources provided to the venture and the professional reputation of the BA (Bonini et al., 2019; Ratinho et al., 2020). We find that the funds a venture receives are most important for reducing the probability of venture failure while the degree of being known ranks second.

Background and Hypotheses

BAs and Reality TV Shows

BAs are investors who use their personal funds to support promising new ventures with which they have no personal connection (Avdeitchikova et al., 2008; Macht, 2011). Reality TV shows featuring BAs originated in Japan with The Tigers of Money and subsequently aired in more than 40 countries 2 under titles such as Dragons’ Den, Shark Tank, and Lion’s Den. In the past decade, these shows have become a worldwide success story in the prime-time TV spot of major broadcasters and are seen by millions of consumers every week. Entrepreneurs who apply for a slot in the shows are pre-screened and selected by the producing company. In case of a successful application, they present their products or services during the show under the belief that they have a viable venture idea but lack funding and potential guidance through a BA. Up to six high-net-worth people who are often celebrities, founders of successful ventures, or, in some cases, active early-stage investors assess the venture ideas and decide whether to support the entrepreneurs in their endeavors. Some of these people are also known outside the reality TV show, which is likely why they have been asked by broadcasters to join the show. Thus, in a sense, these people are playing the angel with their own money. Entrepreneurs usually present their ideas or prototypes and make a first offer to the investors, including the amount of money they wish to obtain and the percentage of the venture they are willing to sell. The rules of the show often stipulate an all-or-nothing mechanism, which means that if entrepreneurs do not raise at least the amount suggested to the investors, they go home with nothing. Because the amount the entrepreneurs seek to raise is often budgeted for specific enhancements or development of the product or service, negotiations often center more on the percentage of the venture’s stock than on the overall amount entrepreneurs want to raise.

After the entrepreneur’s pitch, the investors can scrutinize the product or service and ask questions. If the investors believe that, for example, the venture will not be profitable or caters only to a niche market or that they cannot add value to the venture, they might quickly withhold from making an offer. If investors are interested in funding the venture, they can either accept the entrepreneur’s offer as is or articulate a counteroffer. Counter offers frequently include changes in the share of the venture requested and sometimes proposals of joint investments of two or more investors and/or changes in the amount offered by the investor. Thereafter, entrepreneurs can either accept the offer or make a counteroffer, which the investors then ultimately accept or reject. While in some cases, investors compete against each other with different offers, entrepreneurs most often receive no or only one offer and do not know ex ante which investors, if any, will make an offer.

Because bargaining can take time and each episode features multiple entrepreneurial pitches, these reality TV shows do not present the entire pitch and bargaining process but only the most relevant scenes, which are often broadcast in a different order than recorded. However, viewers see the same information that we have collected in our dataset so that hidden information during the show does not affect our outcome variables, web traffic, or sales figures. Furthermore, the structure and mechanisms of the shows and investment environments are comparable across the four countries (Groh et al., 2021). Moreover, not all deals that are agreed to are actually executed after the show because investors conduct due diligence and might uncover hidden facts. This is the empirical variation we subsequently use to statistically separate the signaling effect of a deal during the show from the effect of simply receiving more money and the screening outcome by the BA.

As reality TV shows have grown in popularity, academic research has capitalized on the transparency of these shows to examine BA behavior more generally. At least six academic studies have recently investigated reality TV shows featuring BAs, most of them examining which attributes and characteristics of entrepreneurs affect the propensity to receive funding from the BAs during the show (Maxwell & Lévesque, 2014; Pollack et al., 2012; Sanchez-Ruiz et al., 2021) or the decision-making process of the BAs (Jeffrey et al., 2016; Maxwell et al., 2011). Closely related to our research question is the study of Smith and Viceisza (2017), which investigates the propensity of a venture to receive follow-on funding. Their study evidences that funding during the reality TV show mainly reduces internal financial constraints rather than providing a quality signal to outside investors. Building on this finding and the signaling literature, we develop a novel theoretical framework with the intent to clarify why investments by generally well-known BAs may be relevant to improve venture performance.

Well-Known BAs

In this section, we aim to bring theoretical clarity to the concept of being known as a specific dimension of BAs’ reputation. The degree of being known captures stakeholders’ generalized awareness of the BA without judgment (Wei et al., 2017) and thus is a social construct based on the general visibility of and public attention to an individual or organization (Lange et al., 2011). 3 As a distinctive perceptual but nonevaluative representation (Rindova et al., 2006), a BA’s degree of being known may involve positive and negative aspects (Gardberg & Fombrun, 2002), but allows a general audience to rank a BA relative to others. We consequently refer to little-known and well-known BAs in this study and examine whether a BA’s general degree of being known affects venture performance.

This definition also allows us to distinguish a BA’s degree of being known from other terms, such as being famous, notorious, or celebrity. While fame is often deemed a mark of quality, being notorious often has negative connotations (Inglis, 2010). By definition, celebrities are people who attract large-scale public attention but also elicit positive emotional responses (Rindova et al., 2006). Thus, all three terms include a judgment of people and capture a different perception than the general degree of being known. The judgment component of reputation is also a key aspect that separates the degree of being known from professional reputation, which is the perception of a BA’s demonstrated ability to create value relative to competitors and is based on past performance (Rindova et al., 2005). While research suggests that a higher degree of being known enables organizations to charge higher prices (Rindova et al., 2005) and increases their sales (Kotha et al., 2001), application of the concept is missing in an entrepreneurial finance context.

Signaling Effectiveness of Well-Known BAs

Economic transactions often involve situations in which a better-informed party wants to transact with a less-informed party. To prove its quality, the better-informed party deliberately sends quality signals to the less-informed party to mitigate information asymmetry and uncertainty (Connelly et al., 2011). For these signals to be effective and to generate a separating equilibrium, three conditions must be met: signals need to be observable to the receiver, the expectations evoked by the signal must be confirmed through experience, and the signals need to be costly because otherwise low-quality senders would easily be able to imitate these signals (Bergh et al., 2014; Spence, 1973).

Signals can come in multiple forms, such as the revelation of proprietary information or third-party endorsements. Third-party endorsements traditionally come from the signaler’s affiliation with other parties (e.g., Dineen & Allen, 2015), such as through strategic alliances, verbal endorsements by supporters, or investments by BAs or VCs (e.g., Plummer et al., 2016). If ventures possess and send such signals to the market, the signal receivers may infer superior quality of the endorsed venture or product, as the endorser puts his or her own reputation at risk (Gulati & Higgins, 2003; Stuart et al., 1999) and the endorsement triggers expectations that the new venture will benefit from the endorser’s skills, expertise, and networks (e.g., Gomulya et al., 2019). Investments by BAs and especially by those with a high level of professional reputation constitute a quality signal (Kerr et al., 2014) because (1) these investments are observable by others, (2) BA presence typically improves venture performance, and (3) BA investments are difficult to obtain by low-quality ventures as BAs put their own money at risk to openly convey the quality of a product or venture to the market. As such, the effectiveness of an investment signal is mainly driven by the degree of professional reputation of the endorsing party. The higher the professional reputation, the higher the expectations on performance, but also the greater the potential damage to the BA in case of poor performance (Stuart et al., 1999).

Research in the field of entrepreneurial finance generally confirms that investments by early-stage investors affect the venture’s propensity to receive subsequent funding or to form strategic alliances (e.g., Kerr et al., 2014; Ozmel et al., 2013). Such third-party signals might, however, affect not only the future fundraising capacity of a venture but also the propensity to sell its services and products to consumers. Reality TV shows provide a neat setting to investigate this link because, unlike in traditionally private negotiations between entrepreneurs and investors, they make the settlement of a deal between the BA and the entrepreneur salient to consumers as well. During a reality TV show, potential consumers have little personal connections with the entrepreneur and most likely no previous experience with the respective product or service. Therefore, their decisions of whether to further engage with and ultimately buy the product or service are more likely affected by third-party signals.

The effectiveness of third-party endorsements from early-stage investors is due to the key assumption that third parties infer a higher venture quality due to the known and superior evaluative abilities of the endorser. In the case of well-known but potentially nonprofessional BAs, this mechanism is questionable. While some of the BAs participating in the show are known to most TV viewers, most are not known for their ability to select the best ventures, thus questioning the quality assurance function of the investment. However, signaling theory does not rule out the possibility that a well-known BA can send an effective signal by making an investment, especially considering that other areas of the BA’s life might be negatively affected if the investment fails. Moreover, organizational research shows that quality signals influence the decisions of stakeholders not only on the basis of the information content conveyed but also depending on whether and how stakeholders pay attention to certain signals when forming impressions of ventures and products (Pollock & Rindova, 2003; Vanacker et al., 2020). Building on this sociocognitive perspective, we argue that well-known BAs are likely to promote venture performance by rendering the signal of their investment credible for at least three reasons.

First, well-known BAs’ actions can be seen by a wide audience, mainly on the reality TV shows themselves but also on other media such as print media and the internet. Investments by well-known BAs might constitute an effective signal because, if the investment target goes insolvent, failure will be associated not only with the investment project and the professional reputation of the BA but also possibly with other areas of the BAs’ lives. Applying the concept of illusory correlation (Hamilton & Rose, 1980) to our setting implies that the audience will perceive a connection between venture failure and BA failure in other areas of life, such as Serena Williams’s tennis skills and successes, even if no such relationship exists. This false association forms because rare or novel events such as an insolvency are also more noticeable and therefore tend to catch people’s attention. The horn effect (Nisbett & Wilson, 1977) is closely related to illusory correlation and causes a person’s perception of a BA to be overly affected by a single negative event, such as the insolvency of the venture in which the BA invested. For example, the actor Matt Damon received considerable negative press and harsh criticism on social media for his endorsement of Crypto.com as an investor as soon as the market went down and the venture began laying off employees (Tedder, 2022). For well-known BAs, the cost of such a negative association is higher than that for little-known BAs, which makes the endorsement through a well-known BA an effective signal.

Second, the support of a well-known BA can simply lead to increased coverage in the general press, not only drawing consumers’ attention to the venture but also helping the venture gain legitimacy (Zimmerman & Zeitz, 2002) and transform consumer perception (Pease & Brewer, 2008). In the 4 weeks after receiving an investment from Leonardo DiCaprio in September 2021, press coverage of the meat ventures Mosa Meat and Aleph Farm increased almost tenfold compared with any other 4-week period before the investment, according to data from Factiva. 4 Ventures might benefit if the BA had the chance to make statements about the venture during an interview, such as in the Forbes Magazine article cited at the beginning of this article. 5 Awareness of the existence of a product or service is an important prerequisite to a person’s decision to search for and consume it. In addition to increased observability, potential consumers may rate a product or service more favorably if it receives more media coverage due to the mere exposure effect described by the psychologists Albert Harrison (1977) and Robert Zajonc (1968) half a century ago. This effect can also be transferred to the organizational context (Pollock & Rindova, 2003; Vanacker & Forbes, 2016). Even if the endorsement does not necessarily evoke quality expectations, an investment from a well-known BA is a way of introducing entrepreneurs and their ventures to potential consumers and possibly being perceived more favorably, thereby improving the venture’s performance. Investments by well-known investors are more like to receive greater attention from general media outlets that are relevant to a general audience.

Third, an endorsement from a generally well-known BA is likely to be an easier-to-interpret and more fluent cue to the general public than an endorsement from a lesser-known but professionally successful BA. The processing fluency of a stimulus describes the metacognitive experience of the ease with which individuals can process information (Oppenheimer, 2008). Easy processing is usually more pleasant than difficult processing and triggers positive affective reactions (Monahan et al., 2000). A key aspect of processing fluency is the familiarity of the receiver with the stimuli (Schwarz et al., 2021), which, in our case, is the endorsement by a well-known BA. Because a higher degree of being known is easier to process, people judge familiar cues as more likable, trustworthy, and believable, even if the exposure was shallow and several weeks ago (Brown et al., 2002). Social standing and general perceptions of endorsers influence the public evaluation of stakeholders (Petkova, 2012; Stuart, 2000). A study of the perceived sympathy of investors, which was carried out in the German version of the reality TV show Höhle der Löwen in 2017 by the market research institute Mafo, supports the view that the degree of being known is actually associated with higher perceived sympathy. For example, Judith Williams, known to the general public as the face of the shopping channel QVC, ranks first in the study, while Georg Koffler, former CEO in the media industry and less known to the public, ranks last. Therefore, we expect the endorsement of a well-known BA to make a positive contribution to the venture’s performance due to the easier processing fluency, which can positively affect the effectiveness of the investment signal and perceptions involved.

Overall, our arguments center on the notion that a BA’s general degree of being known has a positive influence on whether and how recipients perceive his or her investment signal. Well-known BAs can risk their reputation not as professional investors but in other relevant areas of their lives, increase public awareness of the venture, and increase the ease of information processing fluency. Thus, we hypothesize:

Congruency Between BA and the Venture

While the degree of being known captures the superficial knowledge and general awareness of a BA, knowledge about the BA’s activities may also affect consumers’ perceptions. We therefore turn to the question whether BAs and target ventures need to be congruent in their business orientation for the BA’s general degree of being known to work as an effective signal. Various research fields refer to congruency as fit, similarity, and relevance (Bergkvist & Zhou, 2016), but in our context, we refer to it as the degree of similarity or consistency between the public’s image of the BA and the venture’s product or service (Albert et al., 2017). As such, the concept captures what the BA is known for—which is presumably not related to investment activities—but it remains a nonevaluative perception that may involve positive and negative aspects.

For a general audience, congruency may serve as an easy-to-process heuristic. According to source credibility theory (Hovland & Weiss, 1951) and the so-called match-up hypothesis, persuasion of consumers is particularly high when an investor’s perceived expertise is high in the domain of the endorsed product or service. Consumers rely on endorsements as informative cues to the extent of their level of adaptive significance (Knoll & Matthes, 2016). If a high level of congruency exists between an endorser’s public image of expertise and a product or service on some relevant attribute, the endorsement becomes an information source of adaptive significance for consumers, rendering it a more salient cue for their decision-making process (Kamins, 1990). Thus, being known for something that is well in line with the activities of the venture may evoke the expectation that the investor has better evaluation skills, insights, or abilities to add value to the venture. However, this link is less substantiated for a well-known BA than for a BA with a professional reputation, which is formed from proven past performance. In other words, congruency is not necessarily built on past success, but it influences the audience’s expectations as a sufficiently satisfactory indicator of quality (Hallen & Pahnke, 2016).

In our context, we would therefore expect a BA such as Carsten Maschmeyer, who is well known for his background in financial services, to be a better match for FinTech ventures than Judith Williams, who is known for her expertise in the beauty industry. This phenomenon is empirically well-documented in the marketing literature, which indicates that a high degree of being known, and brand congruency is the primary condition for successful endorsement marketing communications. Indeed, empirical studies show that congruency improves brand evaluations; that is, a better fit between an endorser and a brand improves brand evaluations (Choi & Rifon, 2012; Kamins & Gupta, 1994; Kirmani & Shiv, 1998). Albert et al. (2017) recently found that brand-consumer congruency affects brand attitude, brand commitment, brand identification, and behavioral intentions. Finally, empirical evidence also shows that a higher degree of being known is more effective under conditions of high rather than low congruency (Bergkvist & Zhou, 2016), with a positive effect on brand purchase intention (Lee & Thorson, 2008). For these reasons, we expect that congruency strengthens the positive effect of the degree of being known on venture performance.

Data and Methods

Data

We constructed a unique and large dataset based on entrepreneurial television pitches from four different TV shows and countries (Shark Tank, United States; Dragons’ Den, Canada; Dragons’ Den, United Kingdom; Höhle der Löwen, Germany) since their respective inception over a period of 15 years. In 43 seasons and 657 episodes, the pitching entrepreneurs asked for more than US$1 billion and received offers of more than US$318 million from 62 different BAs, rendering this an important channel for entrepreneurial finance.

We first downloaded all episode videos directly from the web page of each broadcaster or acquired them through iTunes if not available. As each episode contains several pitches of different entrepreneurs, we manually cut each video into parts of different lengths so that it only contained a distinctive pitch. In doing so, we obtained 3,260 pitch videos with a total length of more than 500 hours. To extract key information from these videos, we employed different machine-learning algorithms using Amazon Web Services. First, we used the Rekognition application programming interface (API) to automatically extract the textual information from the pitch. During each pitch, overlays are shown to viewers that include the name and location of the venture and the entrepreneurs, details of the request made by the entrepreneurs, and details on the outcome, such as the investment amount in case of a deal. Second, we used the Transcribe API to recognize speech in the videos and to transcribe it into text. By leveraging the speaker diarization feature of the API, we can differentiate between speeches by entrepreneurs and investors. With the resulting text files, we then created linguistic variables using the Linguistic Inquiry and Word Count (LIWC) tool.

To verify the accuracy of the obtained information and processing techniques, we randomly selected 800 pitches. We first set a seed and put all 3,260 observations in random order by generating rectangularly distributed random numbers between 0 and 1 using the random number generator Mersenne Twister (Matsumoto & Nishimura, 1998). We then sorted the observations along these numbers and kept the first 800 observations. Next, we trained two human coders to manually extract the same information we obtained using the approach described above, including the names of the ventures and entrepreneurs, locations of ventures’ headquarters, details of the offer, and deal (Requested Amount, Offered Stake, Deal in Show, and Deal After Show). In 727 cases (91%), the results were identical to our automatic approach. The differences between the human and automatic approaches were due to incorrect transcriptions of character combinations (e.g., “cl” instead of “d” or “rn” instead of “m”). We then manually checked all observations with these letter combinations and corrected them if necessary.

Finally, we used the information obtained to manually create several of our variables directly or to retrieve additional data from available databases (Crunchbase, CB Insights, Dealroom, and Pitchbook). For 358 of the 3,260 ventures appearing in the shows, we were not able to retrieve some basic information. The missing variables include the date of venture registration, the organizational form of the venture, the websites, and the location of headquarters. These pitches were mostly undertakings that were not incorporated in any form, such as philanthropic endeavors or specific innovations that were offered for sale to the investors instead of acquiring shares in a venture. However, many of these ventures were not comparable to the mainstream pitches during the show and should have been removed as outliers anyway. We discuss the operationalization and the measurement of each variable in the next section. Table A1 in the Appendix summarizes the definitions of all variables.

Dependent Variables

To test our hypotheses regarding the impact of an investor’s degree of being known on venture performance, we differentiate between three different dependent variables for our second-stage regression models. First, Venture Failure measures whether the venture filed for insolvency or discontinued operations or the website became unavailable within 24 months after the show. This variable constitutes a crude but often-used measure of venture performance (e.g., Blaseg et al., 2021). Using the names of the ventures and entrepreneurs, we leveraged the databases from Crunchbase, CB Insights, Dealroom, and Pitchbook to retrieve the status of the venture. As a robustness check and for ventures not available in these databases, we used the URL of the website of each venture if available and checked whether the website was available 24 months after the show using Wayback Machine. 6 Finally, we randomly selected 10% of the sample and asked two human coders to assess the operating status of the ventures 2 years after the show to ensure that our classification is capturing failure and discontinuation of a venture and not, for example, other corporate transactions, such as mergers and acquisitions. The two human coders manually searched for each venture’s name on the internet and in the Eikon and Orbis databases to check whether any further information was available. The results of the robustness check indicate 100% accuracy for the coding of 10% of the sample for the variable Venture Failure. Second, following Kerr et al. (2014), we use Increase in Web Traffic as an alternative venture performance measure. Using Similarweb and, if available, the website of each venture, we retrieve the number of total website visits in the month before the television pitch and measure the relative increase of website visits over a 12-month period after the show. Because not all ventures had a web page and Similarweb provides a maximum of 3 years of historical data, this measure is only available for a subsample of 570 ventures. Third, we use different aggregator websites that collect and present information on the ventures and their products appearing in the shows (e.g., sharkalytics.com) to retrieve URLs of their products as listed on Amazon.com. Using these links, we retrieved the average sales rank on Amazon via AMZshark and CamelCamelCamel at the time of the show and measured Increase in Sales Ranks as the relative change over a 12-month period after the show. 7 As not all ventures have products sold on Amazon, this measure is only available for a subsample of 272 ventures.

Explanatory Variables

Our main variable of interest is Degree of Being Known. To operationalize the theoretical concept of being known, we follow Zamudio (2016) and use Google Trends, which provides information on which BA names users entered in Google and how often. As entering a name in a search engine requires at least superficial knowledge of the name, Google Trends, which has become a well-established tool across disciplines, provides a valid measure of the degree of being known. For example, studies on investor attention to VC-backed initial public offerings (Ragozzino & Blevins, 2021) and on economic indicators such as automobile sales and consumer confidence (Choi & Varian, 2012) have also used this tool. However, indices of different terms from Google trends cannot be compared directly, as the tool provides an index of relative search interest for a given term based on the term’s frequency in all searches during the same time frame. While the tool allows retrieving comparable data on up to five terms within the same request, the obtained data points change as a function of which set of terms is used.

To obtain comparable and meaningful data across different search terms (62 unique investors in our case), a common solution is to include a comparable benchmark term across all requests (e.g., Fowle, 2020). As Zamudio (2016) suggests, this benchmark should be ranked similarly to but, on average, lower than the search term of interest on Google Trends. As the Google Trend index incorporates location effects, using the same benchmark search term across different countries is likely to yield inconsistent comparison sets. To account for these challenges, we used the name of the respective president of a country’s central bank at the time the BA appeared during the broadcast as a control search term for two reasons. First, the index for the name of the central bank president is comparable across countries when specified alone over the years (averages between 24.17 [Canada] and 26.08 [United Kingdom]), and second, the index is quite stable over the period of 15 years (average standard deviation across countries of 2.76). Thus, we add this search term as a benchmark to each of the 62 names of investors. We retrieve the indices for all pairs over time, create the average for both search terms, respectively, over a period of 12 months before show appearance, and take the difference between these averages. The resulting difference serves as our measure of the degree of being known and can be negative or positive, depending on how the investor ranks relative to the benchmark search term.

We follow best practices for using Google Trends as a measure of the degree of being known (e.g., Zamudio, 2016) and add a constant (i.e., the lowest negative value in the sample, which is −12 in our case) to each individual score so that the minimum value of the degree of being known is 0. All results remain quantitatively and qualitatively robust when using alternative time frames (e.g., day of show appearance) or benchmark search terms (e.g., name of the national representative at the Miss World contest in the year after participation).

Hypothesis 2 posits that the impact of the degree of being known depends on the level of congruency between the investor and the venture. In line with the literature, we use the definition of congruency as a structural correspondence between two entities (Mandler, 1982). To construct our measure of congruency, we leverage textual descriptions of the ventures and the investors that capture their core activities and perceptions in public. For the ventures, we use descriptions of the venture as provided on the websites of the broadcaster at the time of episode appearance. For the investors, we retrieve the text from their Wikipedia page on the date of each episode’s appearance (Knoll & Matthes, 2016). We calculate the Congruency variable by assessing the semantic distance between these descriptions using cosine similarity, a well-established method for calculating the similarity between two text documents by comparing their relative word frequencies (Hoberg & Phillips, 2010). To define the vectors, we take the text in each venture’s and investor’s description and construct binary vectors summarizing the usage of words. These vectors have a length equal to the number of unique words used in the set of all descriptions. For a focal description, a given element of this vector takes the value of 1 if the associated word is included in the focal description and 0 otherwise. Following Hoberg and Phillips (2016), we focus on known words to allow a meaningful assessment of the thematic similarity between subjects, such as industry, products, and activities. Thus, we restrict the words in the vectors to nouns that appear in fewer than 25% of all descriptions. For the different combinations of ventures and investors, we then normalize the frequency vectors to unit length and take the dot product of their normalized vectors to retrieve the cosine similarity score. We repeat the procedure with all words and then all words except a list of common stop words using the list from the Natural Language Toolkit library; we find quantitatively and qualitatively robust results. The Congruency variable obtained is scaled between 0 and 1, with higher values indicating a higher degree of similarity.

Control Variables

To account for potential selection effects of the ventures that received a deal, we specify the dichotomous variable Deal in Show in the first stage, which captures whether or not the entrepreneur received an offer from at least one BA during a reality TV show and subsequently agreed to a deal. To disentangle the effect of a BA’s degree of being known on venture performance, we need to control for other, well-established value-adding activities and selection effects that may affect venture performance (e.g., Botelho et al., 2021; Da Rin et al., 2013). For this reason, we control for a BA’s professional reputation (Nahata, 2008). Our measure of professional reputation is Connectedness of Investor, or the percentage of the investor’s co-investments with other professional investors in other deals at the time of each episode. According to Hochberg et al. (2007), this measure reflects a BA’s professional reputation because it is highly correlated with the extent to which he or she has access to syndicate deal flows and investment opportunities. We also add the variable Board Seat (Amornsiripanitch et al., 2019) as a measure of the strategic resources, active monitoring, and involvement of the investor. The binary variable Board Seat measures whether at least one of the investors joined the supervisory board of the venture or not. Selection effects might also stem from the fact that entrepreneurs who received a deal are financially less constrained and receive more support from the BA than ventures that did not secure a deal. The variable Deal After Show, therefore, captures two theoretical concepts. On the one hand, receiving a deal implies that the venture is no longer financially constrained and likely benefits from other value-adding activities of the investor. On the other hand, not all ventures receive a deal subsequent to accepting an offer during the show. This is because BAs conduct due diligence after the show and might, for example, discover that the entrepreneur misstated the value of the venture during the show or that patents are owned by another party. Statistically, we cannot disentangle financial constraints from negative selection; thus, we capture them simultaneously. However, the variable Funding Amount provides a finer-grained measure of the absence of financial constraints and quantifies the financial resources, which have been provided by the BA, unified, and converted to U.S. dollars at the exchange rate on the day of the show as provided by the International Monetary Fund.

Next, we control for several investor traits known to affect the extent and quality of contribution by investors to their portfolio ventures. Number of Investors captures how many sharks, dragons, and lions joined the venture as an investor after the show, implying a higher amount of available intangible and tangible resources. Portfolio Similarity captures the level of similarity between the focal venture and the BA’s portfolio using the cosine similarity of venture descriptions retrieved from Pitchbook and Crunchbase. Both variables serve as measures of general and industry-specific experience of the investor (e.g., Zarutskie, 2010). We include the Geographic Distance between the venture and the location of the investor or its firm because it can affect the involvement of the investor (e.g., Bernstein et al., 2016). The median Portfolio Size reflects the number of investments the investor made in other early-stage ventures until the date of the respective episode. 8 We also control for whether the investor was a major shareholder or CEO of a venture with at least 100 employees (Corporation of Investor) that could be leveraged to support the growth of the portfolio venture, either as a customer or by providing a platform for sales or other resources (e.g., Jim Treliving and Boston Pizza), and add a measure of whether the investor had a Professional Investment firm with employees managing the portfolio (e.g., Ashton Kutcher investing through A-Grade Investments). Using the names of the ventures and investors, we retrieved these variables from Crunchbase, CB Insights, Dealroom, Pitchbook, and Wikipedia.

In addition, we control for an array of traits of the entrepreneurs and the ventures themselves that can affect the likelihood of obtaining external financing from early-stage investors and the venture’s performance. We take the organizational form of the venture as a measure of its size and level of professionalization (Blaseg et al., 2021) and measure it with the binary variable Limited Liability, which is coded as 1 for ventures with a limited liability organizational form and 0 otherwise. Next, we control for whether the venture presented a functioning Prototype during the pitch and Venture Age as indicators of the stage of development of the venture (Tumasjan et al., 2021). We add binary variables of the availability of a Patent as a signal of valuable intellectual property rights and Venture Experience among the pitching entrepreneurs as a signal of human capital, which is a binary variable with the value 1 if at least one team member started a venture in the past and 0 otherwise (Hoenig & Henkel, 2015). To acknowledge the effect of the communication cues of the entrepreneur during the pitch, we also include Authenticity by employing the LIWC tool 9 on the speech parts of the entrepreneur (Cardon et al., 2017). We also add the Requested Amount and the percentage of equity as Offered Stake by the entrepreneurs in the first-stage regression, as these proxies help capture the level of confidence of the entrepreneur (e.g., Adomdza et al., 2016).

Similarly, we add Relative Tonality of Investor to the first-stage regression, which also serves as our exclusion restriction. This covariate should help discriminate between ventures receiving and not receiving a deal during the show but should also be sufficiently weakly correlated with the performance measures in the second stage. To meet these requirements, we use LIWC to measure the sentiment of an investor as average tonality across all his or her speeches made on the same day of the focal pitch and then divide it by the average tonality across all of his or her other speeches during the entire show. As such, this variable captures the general mood of an investor on a specific day relative to his or her mood during all other shows. It is well known that moods and feelings influence investment decisions (see Lucey & Dowling, 2005, for an overview). For example, people in a good mood make more optimistic judgments than those in a bad mood (Johnson & Tversky, 1983). Angel investors, who are particularly known for being affected by their feelings in the decision-making process, tend to rely heavily on gut feeling when making decisions (Blohm et al., 2022; Huang & Pearce, 2015; Murnieks et al., 2016). Thus, the relative mood of an investor on the day of the focal pitch is likely to affect his or her funding decision but not the venture’s performance directly. In other words, we expect that if an investor is in a comparatively better mood on a specific day, he or she is more likely to make an offer to the pitching entrepreneur.

Exposure to a large audience on a prime-time TV show will have positive effects on all ventures, regardless of whether the venture receives a deal during the show. To ensure that our results are not driven by exposure of the venture to a large audience, we include Pitch Length, the number of minutes a focal pitch aired on TV, and Show Audience, the number of people watching an episode in millions, as control variables.

Methods

While an abundance of research suggests that VCs improve the performance of a venture by providing resources and support following their investment (Rosenbusch et al., 2013), little is known about the value-adding activities of BAs (Ratinho et al., 2020). However, for BAs and VCs, value-adding activities are conditional on receiving an offer and deal in the first place, which will depend on an array of observable and unobservable characteristics of the venture, the entrepreneur, and the investor (e.g., Bertoni et al., 2011). Thus, considering whether positive effects on portfolio ventures occur over and above selection is necessary (Knockaert & Vanacker, 2013).

We account for selection on observables by controlling for established factors that affect the funding decision of early-stage investors as outlined previously and apply corrective methods for sample selectivity, as Heckman (1979) and Van de Ven and Van Pragg (1981) suggest. We specify a two-stage model with sample selection for the different dependent variables. In the first stage, we predict the likelihood that a venture receives an offer conditional on a set of established venture-, entrepreneur-, and investor-specific control variables and an exclusion restriction to ensure that the model is not only identified by the nonlinearities of the probit model (Wolfolds & Siegel, 2019). Second, conditional on selection, we estimate the latent outcome, which is only observable for selected subjects in the first stage. We specify an ordinary least squares (OLS) model for the continuous variables and a probit model for the binary dependent variables and include the relevant control variables. To correct for selection bias, we specified the resulting inverse Mills ratio based on the first-stage regressions and included it as a regressor in our second-stage models (Certo et al., 2016).

To further assess the economic importance of Degree of Being Known and other variables on venture performance, we decompose the total variance predicted in the second-stage models by employing a relative weight analysis using RWA Web, which Tonidandel and LeBreton (2015) provide. This approach decomposes the total predicted variance given by the R2 of the OLS and probit models into weights that reflect the relative contribution of each explanatory variable. We transform the explanatory variables into a set of orthogonal representations to solve the problem of correlated predictors. Regressing the dependent variable on these orthogonal factors, the model provides a set of standardized regression coefficients. To rescale these coefficients back to the original variables, we then combine the standardized coefficients with the standardized coefficients obtained by regressing the original variables on their orthogonal counterparts (Tonidandel et al., 2009). The relative weight analysis produces estimates of relative effect sizes for each predictor variable and allows us to identify which predictors explain nontrivial variance in an outcome, even in the presence of correlated predictors (Johnson, 2000; Kulik et al., 2016; Tonidandel & LeBreton, 2011).

Results

Descriptive Statistics

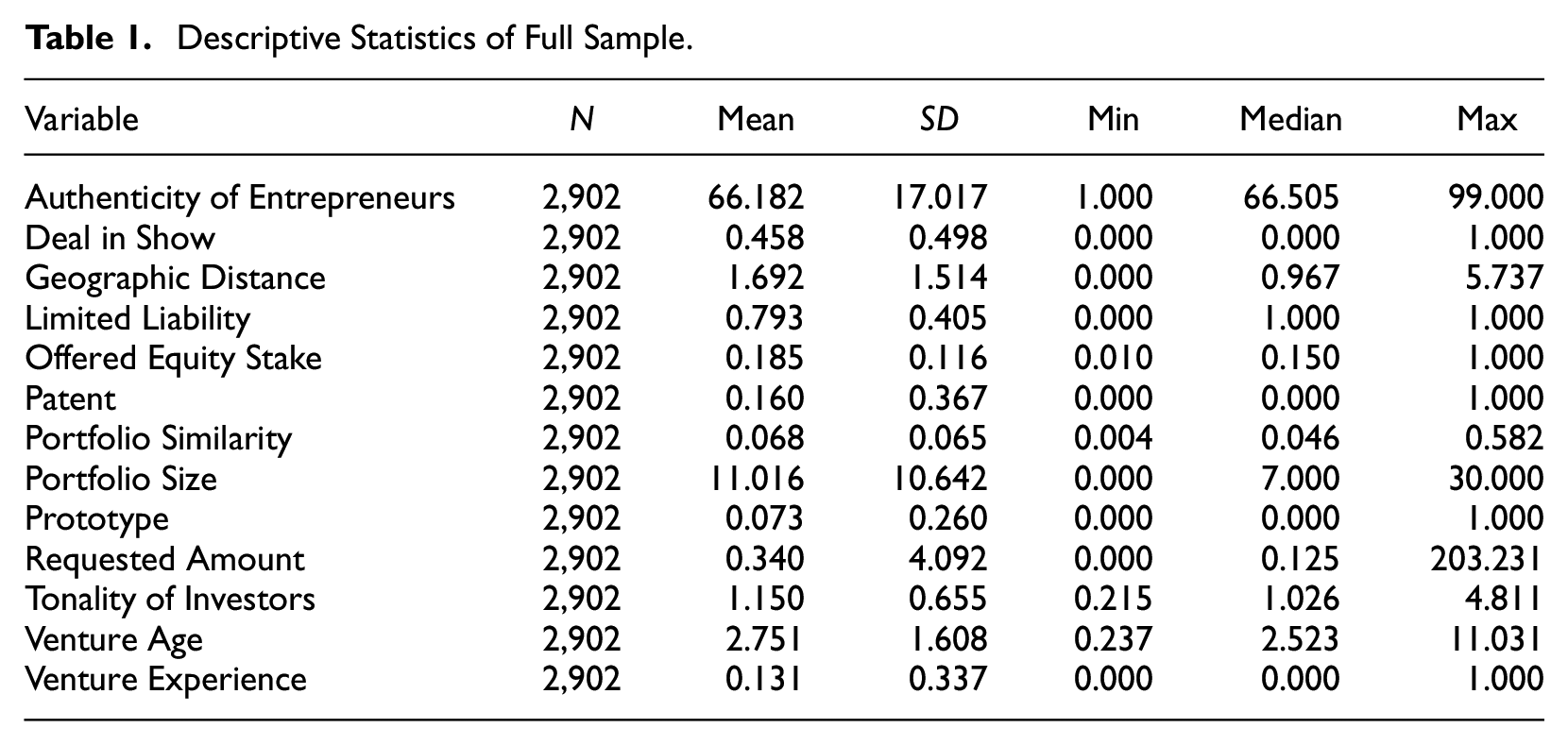

Tables 1 and 2 show the descriptive statistics for our samples, which we, respectively, use in the first- and second-stage regressions. Table 1 reveals that for 2,902 of the 3,260 ventures appearing in the show, complete information was available. The ventures were 2.75 years old on average and had a limited liability status in almost 80% of the cases. Approximately 16% of the ventures held a patent, 13.1% had at least one team member with venture experience, and 7.3% presented a working prototype during the show. The BAs appearing in the respective episode were located 1,692 miles away on average from the focal venture and had made 11 other venture investments before. These investments were quite dissimilar in terms of industry from the focal ventures, as indicated by the average cosine similarity of 0.068. On a scale between 0 and 100, the average authenticity of the pitching entrepreneurs was 66.18, with considerable variation, as indicated by a standard deviation of 17.02. The average entrepreneur asked for US$340,000 and offered an equity stake of 18.5%, which implies a venture valuation of around US$1.8 million. Overall, 1,329 of the 2,902 (45.8%) ventures agreed to a deal during the show.

Descriptive Statistics of Full Sample.

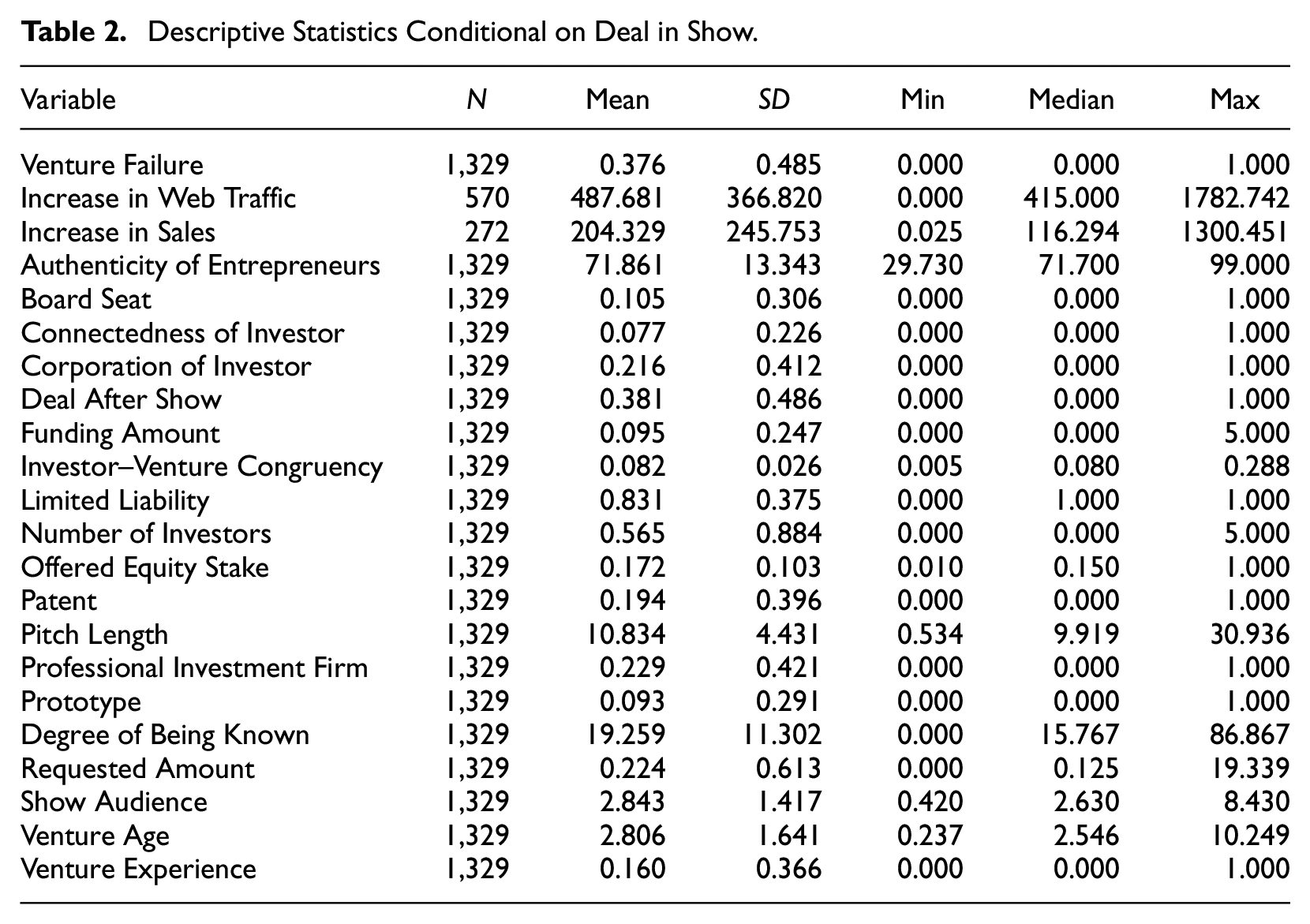

Descriptive Statistics Conditional on Deal in Show.

In total, 45.8% of the ventures appearing during the show agreed to a deal and entered our second-stage regression. Table 2 presents the descriptive statistics. Overall, 37.6% of the ventures receiving an offer failed within 24 months after the show. The web traffic of the average venture increased by 487.68 percentage points within 12 months after the show, while the Amazon sales rank of the average venture increased by 204.33 percentage points. The average pitch length was slightly above 10 minutes, and more than 2.8 million TV viewers watched the respective episode on average.

We find that 38.1% of the ventures that agreed to a deal during the show also realized the deal after the show. 10 Although we cannot precisely identify why a deal was not upheld, we control for the fact that a deal did not materialize after the show in the multivariate regressions. The ventures finalizing the deal after the show actually received around US$248,000 on average. The BA’s degree of being known in realized deals was 18.89, with a standard deviation of 12.07, while the medium congruency between the BA and the venture description was 0.08, indicating a relatively low fit between the professional activities of the BA and the focal venture. Overall, 1.48 BAs actually invested in the venture after the TV show. Unconditional on finalizing the deal after the show, 7.7% of BAs’ investments were syndicated. In roughly one of three cases, the BAs invested through a professional investment firm or were a major shareholder or CEO of a venture with more than 100 employees at that time of the episode. If a deal came about, in 10.5% of the cases, the BA became a board member of the venture.

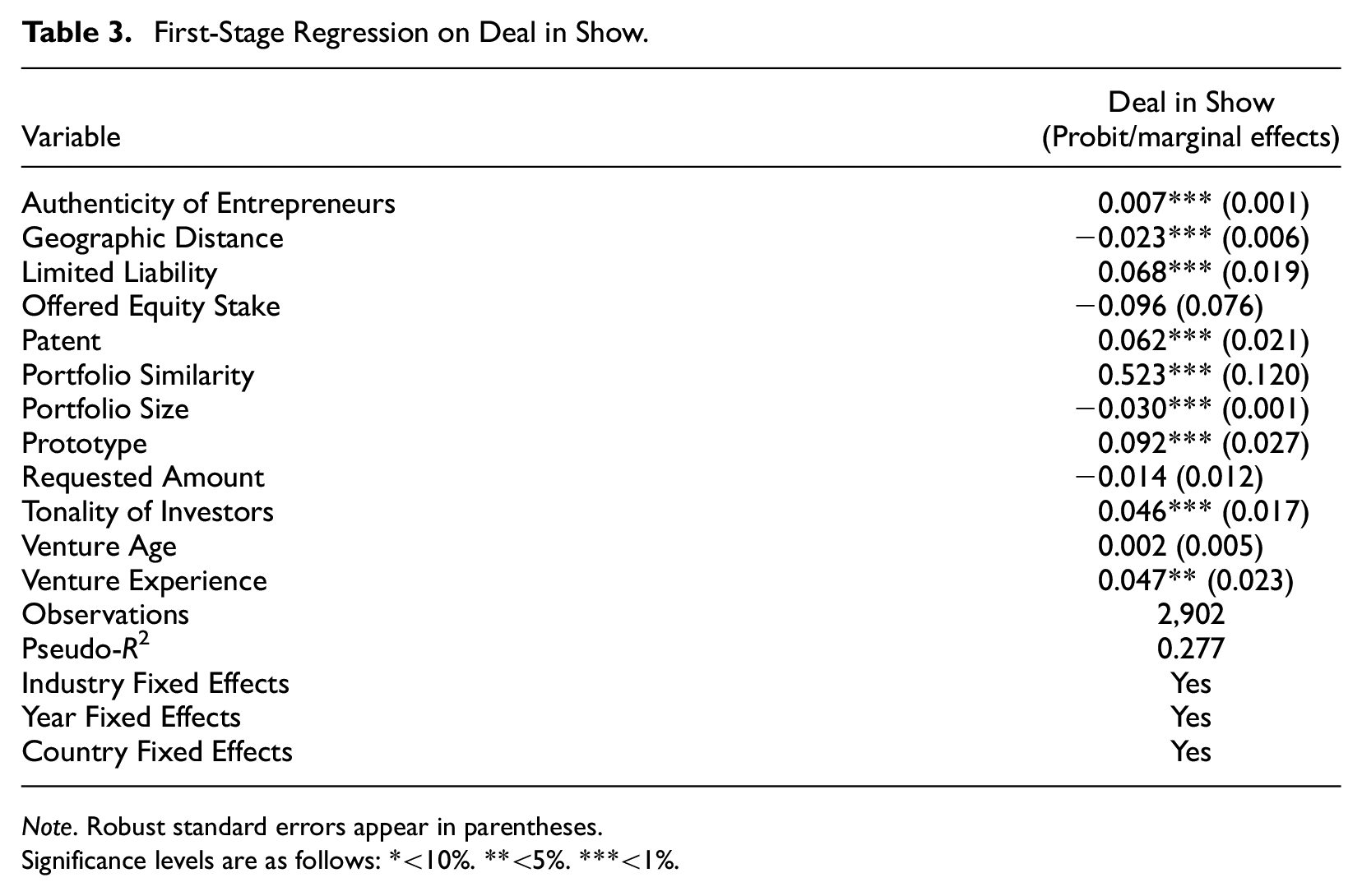

First Stage: Determinants of Receiving a Deal in Show

Table 3 provides the results for the first-stage regression, which determines whether an entrepreneur received a deal during the show. We report average marginal effects, which are suitable for a “more linear” interpretation (i.e., a change in the variable of interest is associated with a change in the dependent variable; Hoetker, 2007). We include industry, year, and country fixed effects to account for unobserved time-variant and time-invariant heterogeneity. The first-stage regression is the same for all second-stage regressions reported in Table 4.

First-Stage Regression on Deal in Show.

Note. Robust standard errors appear in parentheses.

Significance levels are as follows: *<10%. **<5%. ***<1%.

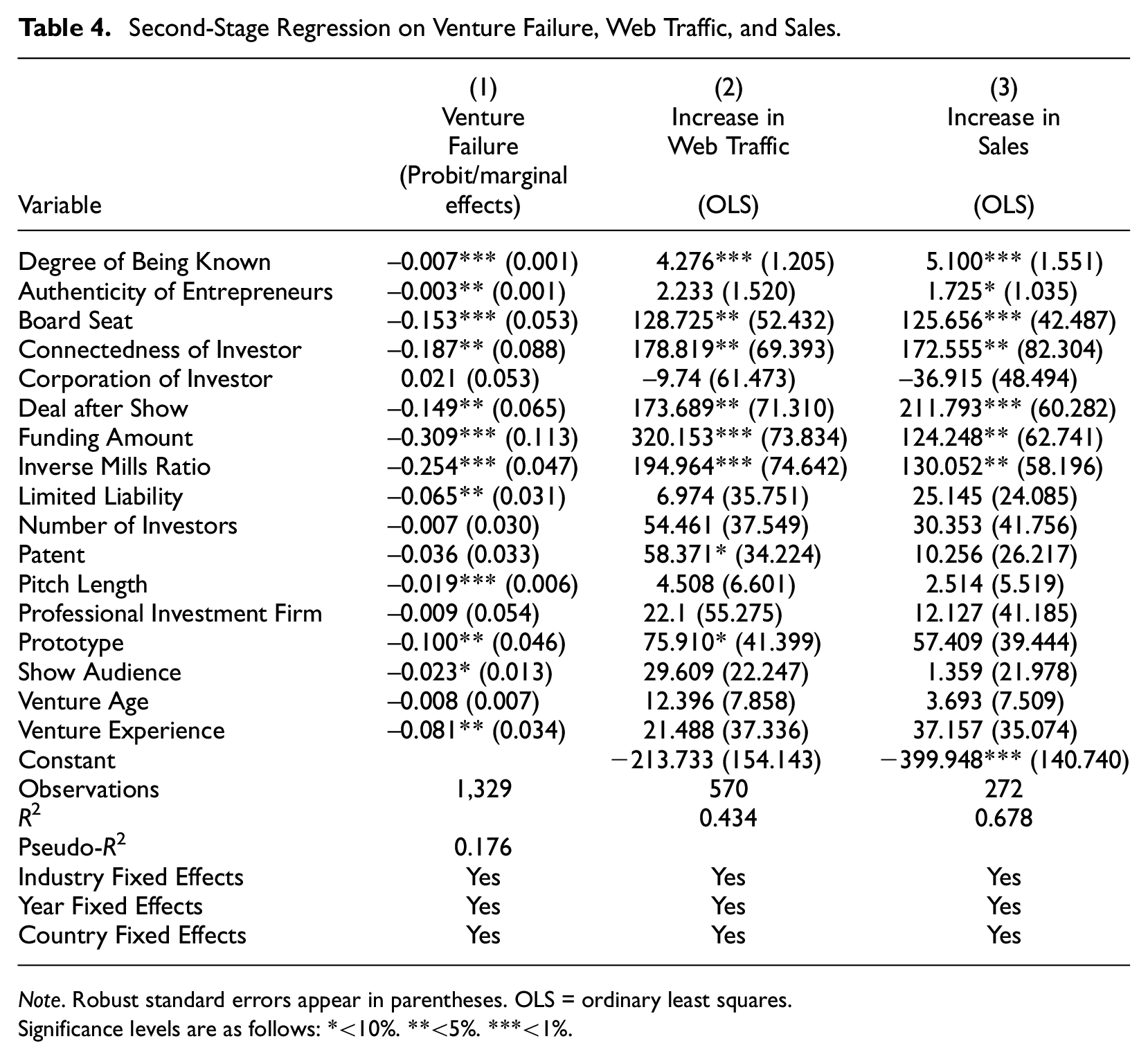

Second-Stage Regression on Venture Failure, Web Traffic, and Sales.

Note. Robust standard errors appear in parentheses. OLS = ordinary least squares.

Significance levels are as follows: *<10%. **<5%. ***<1%.

We find that investor portfolio size and the geographic distance between the investor and the entrepreneur have a negative impact on the propensity to secure a deal during the show, which is in line with the theoretical conjectures that investors have limited recourses and geographic distance constitutes a transaction cost (Hornuf et al., 2022). Venture age, the requested amount, and the offered stake have no significant impact on the probability of receiving a deal during the show. This is most likely because the ventures are all in an early stage and generally young. The requested amount and offered stake are often subject to negotiations and, as such, are not binding constraints. The portfolio similarity between the BA and the venture and the fact that the entrepreneur established a limited liability venture, presented a prototype, and filed or held a patent all have a positive and significant impact on the dependent variable Deal in Show. Moreover, venture experience, the authenticity of the pitching entrepreneur, and the relative tonality of the BA also positively and significantly affect the chances of reaching a deal. Overall, the pseudo-R2 indicates that we can explain 27.7% of the variance in the dependent variable, which is quite high given the observational nature of our data.

Second Stage: Determinants of Venture Performance

Table 4 provides the results for the second-stage regression, which determines how successful a venture has become after the show, as measured by the three dependent variables Venture Failure, Increase in Web Traffic, and Increase in Sales. Hypotheses 1a–1c propose that finalizing a deal with a well-known BA is negatively associated with the likelihood of venture failure but positively associated with the venture’s web traffic and sales. We find that the explanatory variable of interest, Degree of Being Known, has the expected sign and is significant in all specifications. The coefficient of −0.007 in Column 1 indicates that a one standard deviation increase in the BA’s degree of being known decreases the probability of venture failure by 7.9%. Likewise, a one standard deviation increase in the BA’s degree of being known increases web traffic by 48.3 percentage points and sales by 57.6 percentage points. In line with previous research on professional reputation and standing (Kerr et al., 2014; Ozmel et al., 2013), we find that the connectedness of investors and a BA having a board seat both have the expected sign and are statistically significant in all three models. A one standard deviation increase in connectedness results in a 4.2% reduction in the probability of venture failure, a 40.4 percentage point increase in web traffic, and a 39.0 percentage point increase in sales. A board seat reduces the probability of venture failure by 15.3%, increases web traffic by 128.7 percentage points, and increases the sales rank by 125.7 percentage points.

The Inverse Mills Ratio is negative and significant in Model (1) in Table 4, which indicates that ventures receiving a deal during the show are indeed different and that BAs are capable of selecting better ventures during the show. This result holds in Models (2) and (3), which show that the selection of BAs has a positive and significant impact on web traffic and sales. We also consider the screening of the BA after the show, when BAs have more time and resources to conduct due diligence and potentially decide to no longer transfer funds to the venture. We find that Deal After Show has the expected sign and is statistically significant in all specifications. Not receiving a deal after the show—even if the BA offered a deal during the show—results in a 14.9% higher likelihood of venture failure. In addition to these selection effects, we find that money matters. That is, our variable Funding Amount indicates that US$1 million more in funds reduces the probability of venture failure by 30.9%, increases web traffic by 320.2 percentage points, and increases sales by 124.3 percentage points. Thus, unlike many previous studies, our empirical setting allows us to disentangle the effect of signaling and merely receiving funds. The empirical identification results from the fact that some ventures receive a deal during a show (signaling), which is generally known by TV audiences and should have an impact on web traffic and sales, but do not necessarily receive funding after the BA conducted due diligence, which is generally not communicated to the broader audience.

In line with recent discussions on weak versus substantive signals (e.g., Steigenberger & Wilhelm, 2018), we further examine whether a soft promise versus a hard commitment might be sufficient for the venture to benefit from the reputation of a well-known BA. In unreported regressions, 11 we test whether the actual investment by a well-known BA is required for the signal to work or whether the mere promise of an investment is sufficient to leverage the “star dust” of a well-known BA. Because not all deals agreed to on the show are executed after the show, we can statistically identify this question by running the regressions in Table 4 on a subsample of ventures that did not close the deal after the show. We find a robust effect for the Degree of Being Known on Venture Failure. The coefficients remain positive for the other two specifications as well but are only statistically significant at the 10% level (p = .052 and p = .075, respectively). In this sense, evidence implies that the investment itself is not required for the signal to work but that the mere promise is sufficient to leverage the “star dust” of a well-known BA.

With regard to the control variables, we find that longer pitches; the presentation of a working prototype; and whether the entrepreneur has venture experience, is more authentic, and has incorporated the venture with limited liability all reduce the likelihood of venture failure. Moreover, the R-square indicates high explanatory power of the selected explanatory variables, given that 17.6% (Failure), 43.4% (Web Traffic), and 67.8% (Sales) of the variance in the dependent variable are, respectively, explained by the explanatory variables.

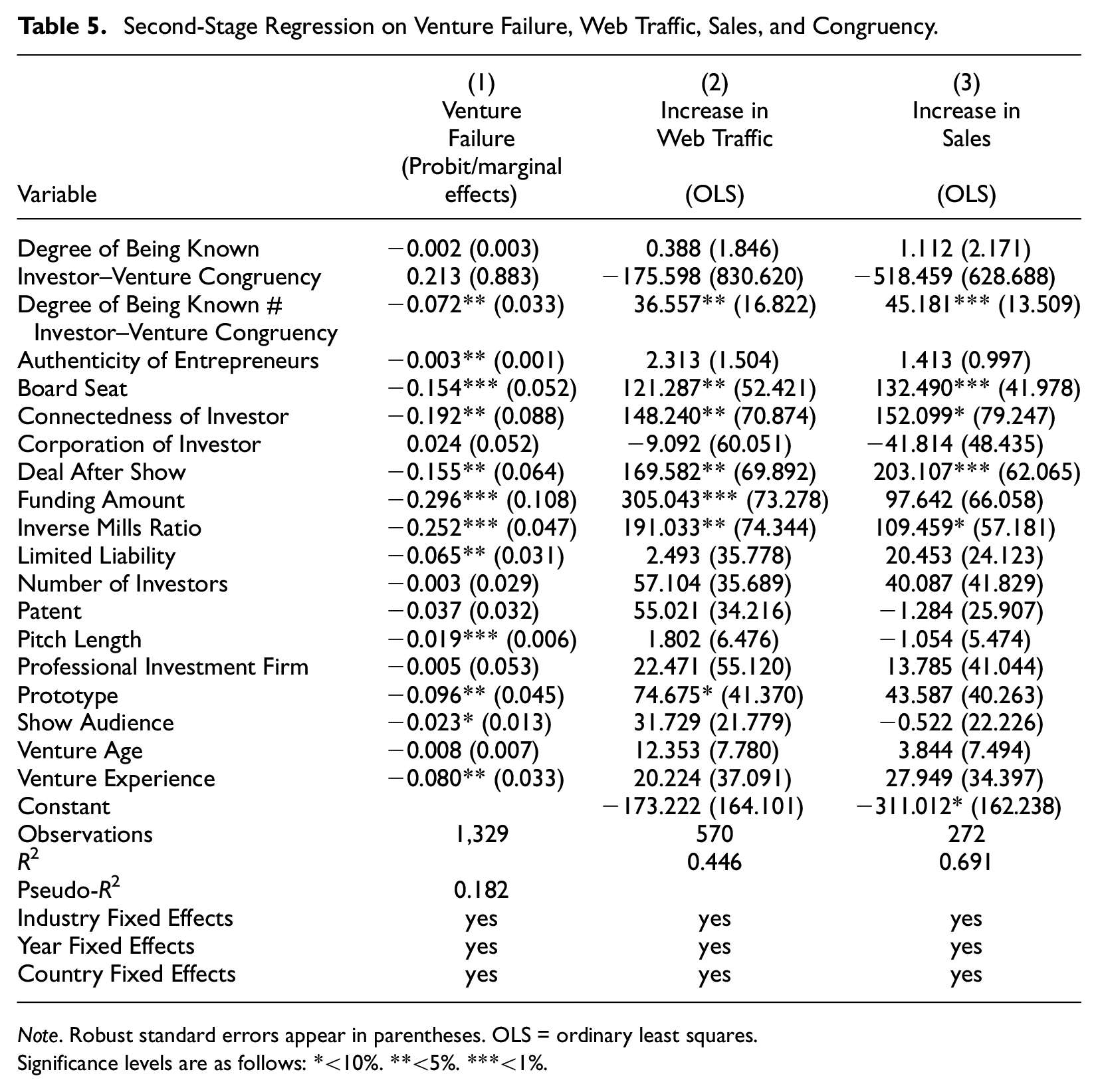

Hypothesis 2 proposes that receiving an offer from a well-known BA is even more negatively associated with the likelihood of failure but more positively associated with web traffic and sales if the professional activities of the BA and investment target are congruent. Table 5 provides the results for the second-stage regression, which determines how successful a venture has become after the show, and includes the additional variable Investor–Venture Congruency and the interaction term Degree of Being Known × Investor–Venture Congruency. The results show that the interaction term Degree of Being Known × Investor–Venture Congruency has the expected sign and is statistically significant in all three models. Because Degree of Being Known and Degree of Being Known × Investor–Venture Congruency are linearly related, the multicollinearity between the variables might undermine statistical significance. Therefore, we next conduct a test of joint significance and find that Degree of Being Known and Degree of Being Known × Congruency interaction are jointly significant, indicating that Degree of Being Known is indeed a signaling channel and Congruency amplifies the investment signal (the respective F-tests/χ2 tests for our three dependent variables show p = .028 for Failure, p = .030 for Increase in Web Traffic, and p = .001 for Increase in Sales). Finally, we use the Jaccard coefficient as an alternative operationalization for Congruency and find that our results hold.

Second-Stage Regression on Venture Failure, Web Traffic, Sales, and Congruency.

Note. Robust standard errors appear in parentheses. OLS = ordinary least squares.

Significance levels are as follows: *<10%. **<5%. ***<1%.

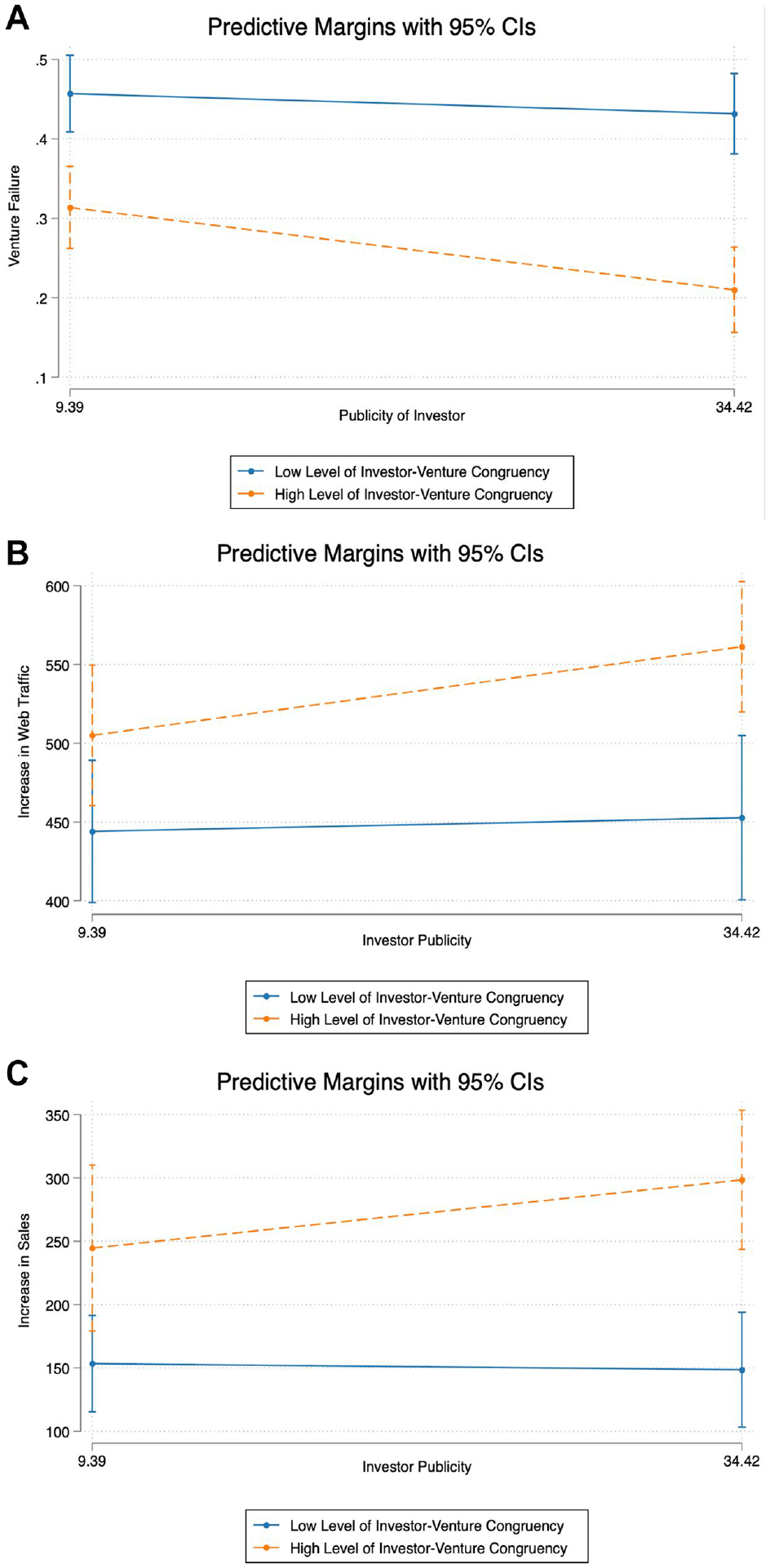

To further illustrate the magnitude of the interaction terms, we conducted slope tests comparing the effects of Degree of Being Known at low (p10) and high (p90) levels of Investor–Venture Congruency on our three dependent variables (see Panels A–C in Figure 2). When Investor–Venture Congruency is low, the effect of Degree of Being Known on Venture Failure (β = −0.006, p = .000 < .01), Increase in Web Traffic (β = 2.435, p = .047), and Increase in Sales (β = 3.642, p = .036) is smaller than the effect of Degree of Being Known when Investor–Venture Congruency is high (Failure: β = −0.009, p = .000; Web Traffic: β = 4.336, p = .000; Sales: β = 5.991, p = .000). The significant differences between these effects (−0.003 for Failure [p = .048], 1.901 for Web Traffic [p = .030], and 2.349 for Sales [p = .001]) highlight the importance of congruency to fully unleash the potential of an investor’s degree of being known.

Slope analysis of the effects of the degree of being known. Panel (A): Venture Failure; Panel (B): Increase in Traffic; and Panel (C): Increase in Sales.

In summary, we find that the effect of a BA’s degree of being known exists over and above potential selection effects, a BA’s professional reputation and standing, and the greater financial resources of a funded venture. However, the congruency between the investor and the entrepreneur amplifies the effect of a BA’s degree of being known on venture performance. We next turn to the question of how important the degree of being known is relative to other factors.

Relative Weight Analysis

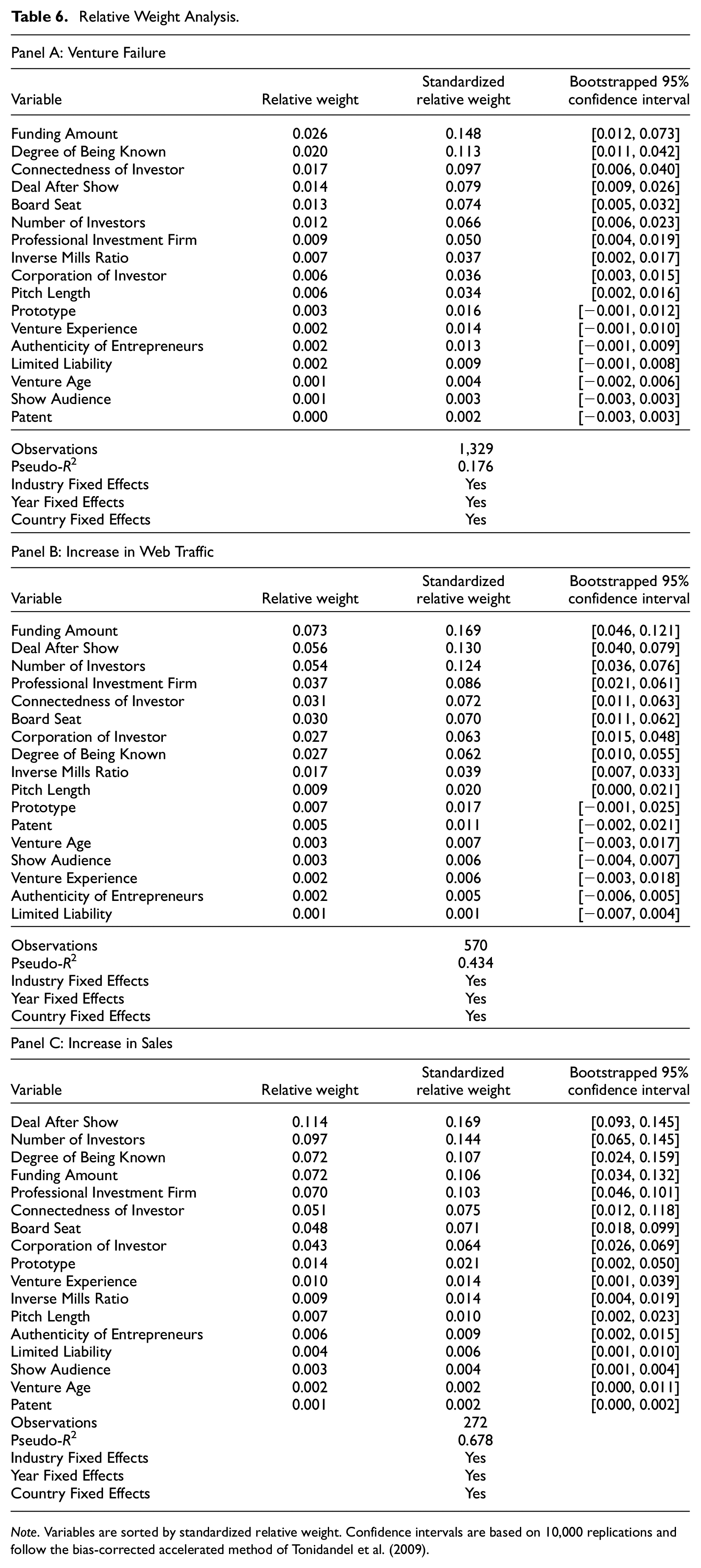

Table 6 provides the results of the relative weight analysis. In Panel A, we investigate the importance of our explanatory variables for venture failure. We find that the funds a venture receives are most important in reducing the probability of venture failure, explaining 14.8% of the variation. However, our variable of interest, Degree of Being Known, ranks second, with an 11.3% contribution in explaining venture failure. Also of importance are three measures capturing the professional standing of the BA: The connectedness of the investor, having a BA as a board member, and the BA operating through a professional investment firm. Next in terms of importance are the signal of receiving a deal during the show and the knowledge and resource transfer as a result of having more than one BA invest in the venture. With regard to web traffic, the most important factors are the amount of funds transferred, receiving a deal after the show, and the number of BA investors. The BA’s degree of being known still contributes 6.2% in explaining the variance of the model with the dependent variable Increase in Web Traffic. However, the BA’s professional standing is more important than the mere degree of being known. Finally, with regard to sales, the three most important explanatory variables are Deal After Show, Number of Investors, and Degree of Being Known. Jointly, these three variables explain more than 40% of the increase in the Amazon sales rank resulting from a pitch during a reality TV show. In all analyses, the number of viewers appears to be significantly less important in quantitative terms than our variable of interest Degree of Being Known, indicating that plain outreach is less relevant for a venture’s performance than having well-known investors on board. In summary, we find that the relative importance of having a well-known BA supporting a venture is particularly high in reducing venture failure and increasing sales.

Relative Weight Analysis.

Note. Variables are sorted by standardized relative weight. Confidence intervals are based on 10,000 replications and follow the bias-corrected accelerated method of Tonidandel et al. (2009).

Discussion

Extant research rests mainly on the notion that the effectiveness of an investment signal is driven by the degree of professional reputation of the endorsing party. In this article, we investigated whether an investor’s general degree of being known, another and distinct dimension of reputation, has an impact on venture performance. We developed a theoretical answer to this question by arguing that the degree of being known can have an effect on venture performance for the following reasons. First, a higher degree of being known constitutes an effective signal because, if the investment fails, the BAs might also suffer a cost in other relevant areas of their lives. Second, a well-known BA can have a positive effect on venture performance by drawing consumers’ attention to the venture, such as through increased coverage in the general media and press, thus increasing signal observability. Third, the endorsement by a well-known BA is likely an easier-to-interpret and fluent signal to the general public than the endorsement by a BA recognized for professional reasons, again improving signal observability. Thus, the effectiveness of investment signals is driven not only by the level of professional reputation but also by the degree to which the BA is known to a general audience. By examining the impact of BAs’ congruency with the venture, we shed additional light on the underlying mechanisms that render the effect of being known more or less effective. These theoretical insights extend the literature on signaling and reputation. They are also of relevance to entrepreneurs, given the growing market for people well known to the general public to act as BAs (Tide, 2019) and investors in terms of how to attract the best investment targets and support them.

We tested our theoretical conjectures using novel data and innovative methods. We gathered a large dataset of more than 2,900 pitch videos of entrepreneurs that have been featured on reality TV shows in four different countries over a period of 15 years. To extract the relevant information, we employed machine-learning algorithms and tested their validity. For the explanatory variable of interest, Degree of Being Known, we used data from Google Trends and adapted previously used benchmarks to an entrepreneurial context. We find strong evidence that a well-known BA reduces the probability of venture failure but increases web traffic and sales and show that the congruency between the BA and the respective venture is an important driver of the relationship between venture performance and the BA’s degree of being known. By using a relative weight analysis, we also assess the economic relevance of the degree of being known. For the likelihood of venture failure and sales performance, the BA’s degree of being known is among the most important determinants, which is trumped only by the funding the venture receives and the quality of the BA’s due diligence. Finally, the impact of the degree of being known is important over and above potential selection effects that result from receiving funding, the professional standing of the BA, signaling effects resulting from third-party certification, and the funded venture’s greater financial resources. To the best of our knowledge, our study is one of the first to provide systematic evidence for the relative importance of BAs’ different value-adding activities.

While our results show a positive effect of the BA’s degree of being known on venture performance, such awareness might also backfire in other contexts. An example is the American actor Kevin Spacey, who supported ventures and start-up events such as the Munich-based start-up conference Bits & Pretzels. Spacey’s speech during the event was widely received in the press; however, in the wake of the Harvey Weinstein scandal, Spacey was charged with sexual harassment in more than 30 cases in October 2017, the same year he joined Bits & Pretzels as a partner. Thus, a BA’s degree of being known might also have a dark side, which has not yet been researched. Moreover, the positive effect of a BA’s degree of being known on venture performance depends on the observability of the affiliation itself. In other words, if a venture does not disclose the affiliation with a BA, and thus nobody knows that a well-known BA is supporting a venture, the affiliation will have no effect on venture performance. While our study provides an apt setting to investigate the effect of BAs’ general degree of being known on venture performance because, unlike in traditionally private negotiations between entrepreneurs and investors, the deal between the BA and the entrepreneur is made salient to consumers, the disclosure of an affiliation with a BA might vary in degree in other settings outside the show. How investors can efficiently achieve observability of the investment (e.g., through public relations, through disclosure on the venture’s website) to leverage their reputation of being known provides an avenue for further research. Moreover, our analysis focuses primarily on ventures offering business-to-consumer products and services. Whether the degree of being known is equally relevant for business-to-business products and services should be subject to future research as well.

Our results also have practical implications for entrepreneurs, BAs, and the platforms that host entrepreneurs and BAs. The early-stage funding market is rapidly developing, not only because of digitalization—enabling new virtual funding channels—but also as a result of new market players, which include well-known and celebrity investors. Entrepreneurs have traditionally considered the professional capacities of a BA, the network offered, and the amount of money the BA is willing to offer per share. Our results show that entrepreneurs may also consider how well known a BA is and whether the public orientation of the BA matches the orientation of the venture. The evidence further indicates that a BA’s degree of being known is among the most important factors determining venture failure and sales performance, which can be actively steered by the entrepreneur, unlike, for example, the quality of the due diligence of the BA. BAs, by contrast, can work on becoming better known, which might be particularly relevant if new ventures are scarce and money chases new deals (Gompers & Lerner, 2000).

Footnotes

Appendix

Descriptive Statistics Conditional on Deal After Show.

| Variable | N | Mean | SD | Min | Median | Max |

|---|---|---|---|---|---|---|

| Venture Failure | 507 | 0.199 | 0.400 | 0.000 | 0.000 | 1.000 |

| Increase in Web Traffic | 248 | 691.834 | 393.789 | 0.000 | 711.641 | 1782.742 |

| Increase in Sales | 128 | 378.105 | 264.597 | 123.770 | 278.823 | 1300.451 |

| Authenticity of Entrepreneurs | 507 | 73.642 | 14.496 | 33.000 | 72.550 | 99.000 |

| Board Seat | 507 | 0.274 | 0.447 | 0.000 | 0.000 | 1.000 |

| Connectedness of Investor | 507 | 0.186 | 0.315 | 0.000 | 0.000 | 1.000 |

| Corporation of Investor | 507 | 0.566 | 0.496 | 0.000 | 1.000 | 1.000 |

| Funding Amount | 507 | 0.248 | 0.349 | 0.010 | 0.150 | 5.000 |

| Investor–Venture Congruency | 507 | 0.082 | 0.030 | 0.005 | 0.079 | 0.288 |

| Limited Liability | 507 | 0.862 | 0.345 | 0.000 | 1.000 | 1.000 |

| Number of Investors | 507 | 1.481 | 0.832 | 1.000 | 1.000 | 5.000 |

| Offered Equity Stake | 507 | 0.180 | 0.103 | 0.010 | 0.150 | 1.000 |

| Patent | 507 | 0.229 | 0.420 | 0.000 | 0.000 | 1.000 |

| Pitch Length | 507 | 10.969 | 5.089 | 0.534 | 9.399 | 30.936 |

| Professional Investment Firm | 507 | 0.594 | 0.492 | 0.000 | 1.000 | 1.000 |

| Prototype | 507 | 0.097 | 0.296 | 0.000 | 0.000 | 1.000 |

| Degree of Being Known | 507 | 18.892 | 12.074 | 3.911 | 14.851 | 82.777 |

| Requested Amount | 507 | 0.242 | 0.879 | 0.005 | 0.144 | 19.339 |

| Show Audience | 507 | 2.839 | 1.413 | 0.540 | 2.640 | 8.290 |

| Venture Age | 507 | 2.932 | 1.696 | 0.237 | 2.619 | 10.009 |

| Venture Experience | 507 | 0.191 | 0.394 | 0.000 | 0.000 | 1.000 |

Acknowledgements

We thank the participants in the Economics Research Colloquium (University of Regensburg), the ESADE Strategy Seminar, the Finance Research Seminar (TU Munich), the BSE Summer Forum on Entrepreneurship, and DRUID22 for their thoughtful comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: Daniel Blaseg acknowledges the financial support of the Joachim Herz Stiftung.