Abstract

Entrepreneurial orientation (EO) can generate substantial gains and losses, exhausting firm resources and straining a firm’s ability to sustain its activities. We develop and test a resource exhaustion theory of firm failure, conceptualizing conditions under which EO increases the risk of firm failure by generating unsustainable amounts of entrepreneurial entropy. Using panel data on 804 large U.S. high-technology firms over 18 years, we find that EO increases the risk of firm failure, which is mediated by the lack of organizational resource slack. An abrupt change in EO increases the risk of firm failure, especially among underperforming firms.

Keywords

Introduction

Entrepreneurship scholars rightly laud the benefits of entrepreneurial orientation (EO) and assert that, in general, EO positively affects firms’ financial performance (Gupta & Dutta, 2016). This consensus has led scholars to understand how these positive financial returns are realized (Gupta et al., 2020; Lee et al., 2019). However, empirical studies examining EO’s positive contributions rely on three crucial pillars. First, studies rely on samples of active firms, creating a survival bias against failed firms (Rauch et al., 2009; Schweiger et al., 2019). But risk-taking, innovative, and proactive behaviors can strain organizational resources, affecting the firm’s ability to serve its markets and address opportunities and threats. Second, studies over rely on cross-sectional designs, omitting the temporal and longitudinal effects of EO on firm performance (Lomberg et al., 2017). As a predominantly explorative orientation, EO can give rise to questionable, tenuous, and unproductive entrepreneurial initiatives that are often not promptly terminated (Covin & Wales, 2019; Hughes et al., 2021), wasting scarce resources. Third, scholars accept that EO is capable of substantial gains and losses (Patel et al., 2015; Wales, 2016). The explorative functions of EO prioritize opportunity-seeking behavior, potentially generating unexpected, unanticipated, and undesirable outcomes (Wiklund & Shepherd, 2011). Sometimes, the losses outpace the gains. In the event of asset specificity, the straightforward reallocation of finite resources to cope with a series of undesirable outcomes is more difficult. Yet, the literature is virtually silent about when EO might jeopardize firm survival and increase the risk of firm failure (Kindermann et al., 2022). Despite evidence that finds favor with EO, we reflect on the underlying resource dynamics and address: when and under what circumstances might EO intensify the risk of firm failure?

Entropy and the entropic nature of entrepreneurial firms hold the potential to answer this question. Entropy is a measure of disorder in any system (including firms). Entrepreneurial firms are drawn relentlessly toward a state of disorder (Vogel, 1989) as forward-looking, novel, and ambitious initiatives go awry or as the firm pursues several additional opportunities at once. It takes significant resources to restore order. This effort represents entropy-combating “work” needed to reduce disorder before it becomes irrecoverable (Kümmel, 2011). “Work” is a process of coordinating and transforming scarce resources into outputs and has one of the two outcomes: it combats entropy and keeps the firm in a low, manageable entropic state (“entropy-combating work”), or it accelerates entropy to arrive at a more acute, disordered, less controllable state (“entropy-accelerating work”). In one of the few applications of entrepreneurial entropy, Slevin and Covin (1998) argue that an entrepreneurial firm is in a constant battle against disorder, beset by time pressures, strains on available resources, and high rates of internal and external change. A firm in a state of high entropy is under unrelenting pressure to survive because of frequent and irrecoverable resource commitments. That is, a highly entrepreneurially oriented firm, over time, is in a far greater position to exhaust resources in ways that it cannot easily recover. Regrettably, the existing literature has yet to provide a predictive theory addressing how entrepreneurial entropy from EO can increase the risk of firm failure.

EO exemplifies a “strategic” posture toward entrepreneurship, emphasizing innovativeness, proactiveness, and risk-taking behavior (Covin & Slevin, 1989). A firm low in EO is conservative, stable, and inert, but a firm high in EO is forward-looking, changeable, and transformational. This volatile cocktail means that EO is entropy-accelerating work. Where “suck[ing] orderliness from its environment” (Schrodinger, 1947, p.75) is needed to return the firm to a stable state (Slevin & Covin, 1998), EO prompts high entrepreneurial entropy by persistently, intensively, and boldly deploying large amounts of resources to exploit identified entrepreneurial opportunities as they arise. As a variance-creating mechanism, EO pushes the firm in several different directions and leans against many frontiers. These pioneering efforts can impoverish resources whereby the entropic firm becomes resource exhausted: EO loses its strategic focus at high levels, a tipping point after which EO becomes too explorative, and its behaviors fuel a surge in entropy that is potentially organizationally unsustainable. While the entrepreneurship literature assumes that EO (conveniently) creates new resources to offset such a problem (Eshima & Anderson, 2017), asset specificity and resource irrecoverability suggest that at best only part of the liquid resources invested in EO activities can be recovered. Because of a trajectory toward resource exhaustion, we foresee that EO can increase the risk of firm failure substantially.

Change is a “given” to an entrepreneurially oriented firm, either because the novelty of risky, forward-looking endeavors erodes the effectiveness of existing organizational arrangements or misjudgments about environmental changes result in misalignments that cause substantial resource and financial losses (Slevin & Covin, 1998). EO is an intensely resource-consuming process needed to transform novel exploration into commercial outcomes (Covin & Wales, 2019). Since firms realizing the positive impact of EO are overrepresented among existing studies (Schweiger et al., 2019), any risk that EO and entropy might pose for firm survival is understated. Second, the potential for firm failure stems from the propensity of EO to generate unencumbered experimentation (Patel et al., 2015) that exhausts resources. Its outcomes take time to bear fruit, which masks or misses “total losses” from EO (Wales, 2016), the effects of which have been typically modeled as financial (Kindermann et al., 2022), not resource based. Moreover, overlooking the manifestation and effects of EO across time (Lomberg et al., 2017) omits analyses of a change in EO. While EO should represent temporally stable recurring patterns of risk-taking, innovativeness, and proactiveness (Wales, 2016), underperforming firms may change their EO to escape their predicament. This further strains the firm’s resources because they commonly both lack the organizational routines and capabilities to reallocate resources effectively and are constrained by asset specificity (Slevin & Covin, 1998).

We develop a resource exhaustion theory of firm failure to address these theoretical and empirical deficits to better understand the risk of firm failure, and the role of EO, and the bearableness of the entrepreneurial entropy it gives rise to, in that risk. We test our theoretical model with a panel dataset of 804 large U.S. firms across nine high-technology industries from 2000 to 2018. We provide three contributions to EO theory and practice. First, we contribute a resource exhaustion theory of the risk of firm failure. In doing so, we reconceptualize EO as entropy-accelerating work in which the sum of entrepreneurial entropy represents a state of resource exhaustion. EO generates substantial gains and losses. Sometimes, the losses outpace the gains. We discuss when this happens and conceptualize a series of effects representing different mechanisms explaining how EO increases entropy and resources exhaustion to a state that is irrecoverable and fatal to firm survival. Our resource exhaustion theory provides the first comprehensive explanation for why EO poses a significant risk of firm failure and under what circumstances this association occurs.

Second, we provide a theoretical treatment and empirical test of changes in EO longitudinally over time and unveil two new boundary conditions of its role in a resource exhaustion theory of firm failure. We discuss how pacing, stability, and changes in EO vary the entropy that makes reaping its gains more challenging. Because a firm is extended in too many initiatives either simultaneously or sequentially, the costs (resources committed) eventually outstrip the gains so substantially that at an extreme firm discontinuation occurs. We reveal how large abrupt changes in EO made in a short time escalate the risk of firm failure by destabilizing existing organizational arrangements and exhausting resources faster. Asset specificity and illiquidity prevent the seamless capacity to manage the disorder accompanying such a shift. We reveal how relative underperformance intensifies this effect.

Third, we advance our understanding of entropy in entrepreneurship research. Prior studies loosely use “entropy” to describe diversification, including product (Jacquemin & Berry, 1979; Palepu, 1985) and international diversification (Hitt et al., 1997), and social diversity (Audretsch & Keilbach, 2007), measured by the scope of product strategy, international strategy, and voting behavior, respectively. However, these characterizations are inconsistent with entropy’s original meaning in physics, where entropy represents a state of disorder that all systems tend to maximize (Von Neumann, 1955). Characterizing this as a state of resource exhaustion, our theory equips entrepreneurship scholars with a foundation to accurately conceptualize entropy and an opportunity to revitalize entropy treatments of entrepreneurial phenomena. Collectively, our resource exhaustion theory and test answer the call of Wales et al. (2021) to enrich theory underlying EO.

A Resource Exhaustion Theory of Firm Failure

We begin by casting the concept of entropy in the context of entrepreneurial firms. Our objective is to expose a theoretical framework of resource exhaustion with which scholars can generate new predictions about EO that appreciate its entrepreneurial entropy.

For entrepreneurial firms, Slevin and Covin (1998) theorize that entropy occurs in reversible and irreversible organizational processes. Entropy represents disorder, turmoil, and instability in a firm. In physics, and the second law of thermodynamics, any process or behavior converting “energy” or resources produces entropy (Kümmel, 2011), and resource conversion is often irreversible because an output that has occurred cannot be converted back. In entrepreneurship terms, available organizational resources represent the energy available to pursue EO behaviors and manage its outcomes. An entrepreneurial firm uses and converts resources to produce innovative, forward-looking products and services (Slevin & Covin, 1998), raising its entropy—a state of resource exhaustion because the resources used are unrecoverable, irreversible, and specific to the purpose deployed.

We position EO as resource-intensive behavior which embodies entropy-accelerating work. We conceive of “resources” in terms of liquidity. Cash is the most fungible resource; however, cash must be committed and transformed into a more specific state when the firm explores new product–market entry opportunities through its EO. Because EO is pioneering, EO consumes large amounts of resources in its innovative, risky, and proactive behaviors and exhausts finite liquid resources while producing outputs whose returns and odds of success are uncertain, distant, and prone to setbacks and sunk costs. This is our first assumption.

Converting resources through EO reduces organizational resource slack as the liquid resources consumed by EO are not easily replenished or substituted by any new resource that EO might generate. As resources committed cannot be converted readily into cash (due to asset specificity), a loss occurs equivalent to the amount of resources depleted and exhausted (e.g., the amount of resources now unavailable and which cannot be moved to assist in the exploration and exploitation of new promising paths). Some expenditures may be recovered, but there will be a loss of cash resources after a “failed” exploratory path is abandoned. As entrepreneurial firms are beset by time, competitive, and external environment pressures, their entrepreneurial acts induce more entropy as slack (liquid) resources are exhausted. Because a state of high entropy is a state of high resource exhaustion, the firm must avoid the point at which the entrepreneurial entropy resulting from EO becomes unsustainable, risking firm failure: failure may not be due to “bad performance” but because entropy is no longer manageable, and the firm is severely distressed due to resource exhaustion. 1

At high levels of EO, entrepreneurship is unencumbered: free-flowing ideas are routinely acted on and bets on uncertain future markets become commonplace. Overzealous pursuits of EO lead to more tenuous and unproductive entrepreneurial initiatives, where intense resource use and resource exhaustion become unsustainable. We conceptualize the tendency for EO to generate variance-inducing activities capable of substantial gains and losses as EO’s “exploration liability effect.” We see the magnitude of the exploration liability effect as the root cause of entrepreneurial entropy and resource exhaustion culminating in the heightened risk of firm failure. Under this effect, firms with high EO over-explore and under-exploit, where high EO firms no longer balance exploration and exploitation effectively. Entropy and the exploration liability effect mechanism predict that a firm’s cash resources become overcommitted in too many directions and frontiers when EO is kept at a high level for too long.

EO heightens the risk of failure because its entropy-accelerating work leads the firm into a less liquid state where costly exploration exhausts resources. As entrepreneurial entropy increases, entropy-combating work through effective and efficient management of organizational structures, processes, and properties are needed to combat this disorder (Slevin & Covin, 1998). This is our second assumption. Orderliness suggests the need for systems, processes, and approaches which manage resources expended toward uncertain endeavors. Entrepreneurial entropy introduced through many (often sizable) resources gambles with variously specific, irrecoverable resource commitments and describes how resource exhaustion occurs in the new growth avenues pursued by entrepreneurially oriented firms.

Thus, if a firm exhibits some stability with its EO, entropy-combating routines should form. These routines should improve the efficiency of exploration and increase the effectiveness of its exploitation, mitigating the rate at which resources are exhausted. For instance, in a study of post-IPO firms, Kindermann et al. (2022) observe that EO may reduce firm failure contingent on its configuration and organizational factors. The ascent toward high entrepreneurial entropy is then slowed, but not stopped. Moreover, maintaining higher levels of EO over time develops additional routines that channel more acts of exploration and risk more unencumbered exploration (raising the prospect of outlandish projects), prompting more resource use. This is a consequence of the path dependence that occurs as exploration repeats its (favored) activities, procedures, and structures at a cost to those favoring exploitation (March, 1991). This is our third assumption.

We conceptualize this as a “repetition effect.”Hambrick (1983) alluded to this when discussing Miles and Snow’s strategic types, commenting that organizations following certain strategies develop internal consistencies that tend to perpetuate those strategies. While this repetition can develop tested, mature processes, an organization can co-develop a difficulty to accept or implement change as resources are geared for the established strategy. A firm that perpetuates its EO will see its organizational properties intensify path dependently. While the momentum toward high entropy is slower, it continues nonetheless because liquid resources are still used, and asset specificity consolidates further. Although the system will potentially generate some cash flow from its new initiatives, the firm’s aggregate risk continues to grow. This growing aggregate risk increases the probability that more incidents of exploration liability effects occur, multiplying the resource and financial costs and losses to the firm when explorations fail. The repetition effect is consistent with how a system tends to maximize entropy over time, increasing the danger that the entropy outpaces the cash flow and revenue generated.

Time and change in EO are vital considerations. These are regularly absent in treatments of entrepreneurial phenomena (Lévesque & Stephan, 2020) but matter greatly for entrepreneurial entropy (Slevin & Covin, 1998). EO is a variance-generating mechanism reshaping a firm’s product–market portfolio and rewriting its performance frontier (Wiklund & Shepherd, 2011). Prolonged high EO generates exploration liability and repetition effects that puts a firm dangerously out of balance between exploration and exploitation. Managers might respond to this by “cycling” EO, reducing its magnitude to exploit and mine productive opportunities to replenish resources. This could represent entropy-combating work that attempts to reduce entrepreneurial entropy and maintain manageable order—one defined by averting a state of resource exhaustion. However, the extent to which managers turn up or turn down the EO dial gradually or suddenly changes whether entropy accelerates quickly or slowly and whether resources generated through opportunity pursuit sufficiently prevent resource exhaustion. A firm with low EO moving to a state of high EO has not been able to do the work needed to combat the entrepreneurial entropy that comes with this disturbance.

When a firm exhibits low EO but substantially increases it over a short time (a large abrupt change in EO), it moves rapidly from a state of modest entropy to a state of much higher entropy. Few if any routines or capabilities will be in place to manage this profoundly different strategic posture (and manage the intense resource use accompanying it). In this state, total resource exhaustion from entrepreneurial entropy is far greater. Fewer slack resources are available to manage the new behaviors applied by this posture, and failure is more likely. Similarly, rapidly halting EO by shifting suddenly toward a more conservative, exploitation-focused posture reduces product–market variation and diminishes some of the entrepreneurial entropy, but entropy does not suddenly disappear. When EO is rapidly halted and a very different strategic posture is taken, the large abrupt change in EO can increase the total entropy because of the absence of organizational routines, practices, and properties associated with it and asset specificity preventing resources from switching easily to fund the new strategic posture. We conceptualize this as a “punctuated effect,” an effect generated when a large abrupt change in EO destabilizes the firm’s organizational arrangements and moves the firm far from its status quo. The resource implications of this shift coupled with irrecoverable investments and asset specificity suggests an inability to offset a higher state of resource exhaustion (entropy) from occurring. This heightened entropic state endangers firm survival. More gradual cycling should lessen this effect. This is our fourth assumption.

A leap from a low entropy state to a high entropy state characterized by large abrupt changes in EO might have been a rational choice, suggesting that managers can undertake the entropy-combating work needed to prevent the firm from descending into disorder. But when the firm underperforms greatly against its industry average, managers reacting by making a large abrupt change in EO are unlikely to benefit from prior work because underperforming firms lack the advantages of current success. Relative underperformance suggests inadequate prior entropy-combating work on organizational arrangements and resourcing. Responding to underperformance with a large abrupt change in EO suggests that prior entropy-combating efforts must have failed, and prior routines were unproductive for the firm to have fallen into this state. Therefore, the firm was already in an entropic condition: underperformance may then intensify the impact of large swings in EO, increasing the punctuated effect that shifts the firm closer to an unrecoverable state of resource exhaustion. This is our fifth assumption.

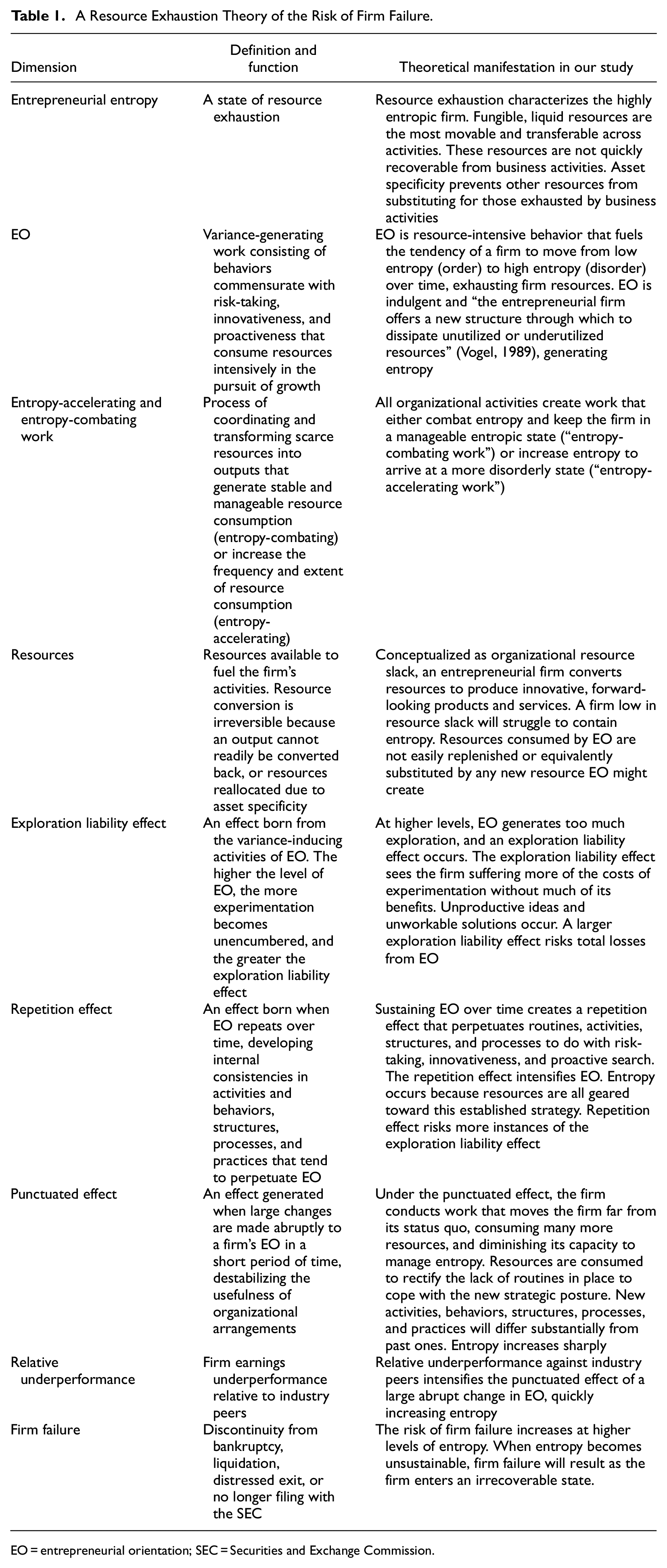

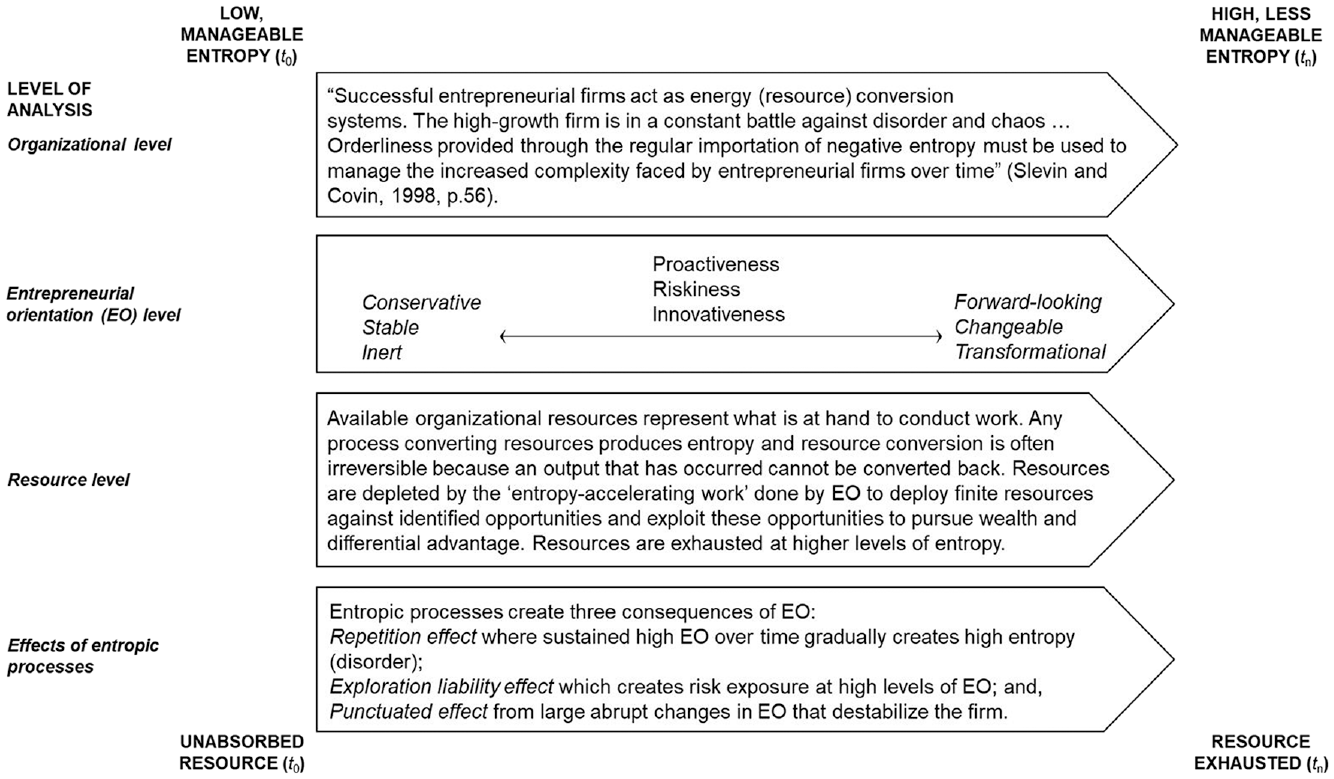

Table 1 summarizes each of these dimensions and reports their treatment in our resource exhaustion theory of the risk of firm failure. Figure 1 depicts our reasoning.

A Resource Exhaustion Theory of the Risk of Firm Failure.

EO = entrepreneurial orientation; SEC = Securities and Exchange Commission.

An entropy perspective on resource exhaustion from EO.

Hypotheses

EO and Resources Exhaustion

Entrepreneurial behaviors produce a great deal of variance in performance outcomes as EO intensifies, because not all experiments will succeed (Wales, 2016). Failed experiments prompt a broader search for more productive ones consistent with risk-taking, innovativeness, and proactiveness (Levinthal & March, 1993). This type of entrepreneurial strategy leads to profound change involving costly estimation errors (Wiklund & Shepherd, 2011) where sunk costs are probable. Both act as agents of entrepreneurial entropy because large amounts of resources are consumed but not easily replenished.

EO prioritizes taking long-term gambles and investing earnings to pursue future markets for which anticipating future demand is at most imprecise (Patel et al., 2015). Extreme financial losses from some of these forward-looking actions are possible because the probability of “winning” is difficult to predict in advance (Coad & Rao, 2008). A firm is then at a greater risk of EO’s exploration liability effect intensified over time by a repetition effect. The firm’s available organizational resource slack will fall as entrepreneurial failures reduce the liquid resources available for new entrepreneurial activities. When entrepreneurial efforts fail, asset specificity prevents cash locked into present activities from being diverted to mitigate resource exhaustion, further heightening entrepreneurial entropy.

Sustaining higher levels of exploration over time deprioritizes exploitation and can limit the ability of the firm to realize the commercial value of its discoveries. Entrepreneurial behaviors can serve as jolting events that spur new but imprecise ways of thinking and doing (Barnett & Pratt, 2000). These actions contain higher degrees of uncertainty and accelerate resource consumption and entrepreneurial entropy. EO may generate some new resources from the new initiatives, but they are not necessarily equivalent to the liquid resources used, exhausted, or lost, and perhaps more importantly, the entropy or loss of resources may outpace the resources generated. The path dependence associated with exploration causes firms to continue to pursue exploration beyond an optimal level, putting any prior financial gain at risk (Wang & Li, 2008). Exploitation might be cut short if the high EO firm is pulled in too many directions either at once, or over time (seeking the next big thing). We do not disregard that EO intends to break inertial forces, but as EO increases, the initial positive breaking of inertial forces is counterbalanced by reductions in unabsorbed organizational resource slack and cumulative increases in entrepreneurial entropy.

Over time, EO performs more work that increases variance and entropy inside the firm: the greater probability for failed experiments coupled with the conditions for unencumbered experimentation carries the potential to exhaust resource beyond a sustainable point, increasing the risk of firm failure. Business survival is jeopardized by a commensurate reduction of organizational resource slack, where liquid resources are absorbed and exhausted by EO activities, where discretion is low without drawing resources from activities elsewhere in the firm, and the ability to reallocate resources is constrained by asset specificity. Thus:

Hypothesis 1. The lack of organizational resource slack mediates the relationship between EO and the risk of firm failure over time. As the level of EO increases, unabsorbed organizational resource slack will fall, heralding an increased risk of firm failure.

Large Abrupt Changes in EO

Abrupt changes in EO have entropic consequences increasing the risk of firm failure. Existing research associates EO with a sustained pattern of entrepreneurial behavior—one that is not spontaneous, infrequent, or occurring by chance (Wales, 2016). Although a sustained pattern does not mean a firm will not change the magnitude of its EO (Anderson et al., 2015), rather than being rigidly fixed, we should expect at least some fluctuation in EO over time in line with a firm’s strategic decisions and circumstances.

Firms go through periods of relative stability interrupted by abrupt and intense change (Romanelli & Tushman, 1994). During periods of stability, firms generally benefit from exploitation. In time, over-exploiting generates rigidities that compel a temporal transition (Mudambi & Swift, 2014) from efficiency to exploration (and a different level of EO). This represents a “discontinuous jump” between two very different sets of behaviors (Kang & Kim, 2020). The larger this abrupt change in EO, the greater the intensity of the punctuated effect the firm encounters. Large abrupt changes in EO represent substantial resource-consuming work that moves the firm far away from its status quo, creating disruption and instability that culminate in a potentially dysfunctional entropic state. This abrupt change can be from low EO to high EO or high EO to low EO, but the impact is the same: substantial resources are consumed, and entropy-combating work is needed to coordinate this shift.

Firms are prone to change their EO to stay ahead of their competitors (Patel et al., 2015). A large abrupt change in EO increases the probability that outcomes are more variable, with the firm subjecting itself to more possibilities of total losses (e.g., Kang & Kim, 2020), financially and in its resources. The difficulty in managing the entropy that accompanies this change results from preexisting organizational systems, processes, and routines associated with a previous strategic orientation becoming less useful or obsolete (Slevin & Covin, 1998). The resources needed to rectify this situation are substantial at a time when resources are especially limited. When a change in EO is large and intense over a small timeframe, the entropy associated with this abrupt change is harder to relieve as the firm will not have had time to generate processes that best capture value. In turn, the firm must expend more resources to utilize the new strategic posture.

When a change in EO is large and abrupt then, the punctuated effect of this change should intensify EO’s exploration liability effects on organizational resources. Large abrupt changes in EO trigger acute changes in searching and experimenting. When an abrupt shift is made to a state of high EO, experiments are more likely to fail and initiate further (increasingly desperate) exploratory efforts commensurate with the exploration liability effect. When the shift is from high EO to low EO, the punctuated effect destabilizes the usefulness of organizational arrangements. Abruptly altering existing strategies is more likely to generate poor outcomes, increasing the risk of firm failure. Therefore:

Hypothesis 2. A large abrupt change in EO increases the risk of firm failure over time. 2

The Moderating Effect of Firm Earnings Underperformance

Underperforming firms face two entropy-related challenges. First, legacy resources and organizational arrangements are inadequate or badly degraded. Firms experiencing a high deficit sometimes “go for broke” (Singh, 1986) to rectify their past failings. But the literature on firm underperformance and managerial risk-taking is mixed. For example, while greater levels of underperformance tend to increase risk-taking (Park, 2007), overperformance has a stronger effect on reducing risk-taking than underperformance has on increasing it (Greve, 1998). Other studies show that inferior performance changes aspiration levels whereby the only desire is to survive (March & Shapira, 1987). We expect those managers making large abrupt changes in EO when experiencing worsening underperformance to substantially increase the risk of firm failure because their firms lack the resource advantages of current success needed to combat entropy. Troubled, underperforming firms abruptly changing their risk-taking intensity, novelty, and proactive search should experience a more pronounced punctuated effect and a more powerful and rapid jump toward high entropy made more unsustainable by their inability to draw on productive legacy resources and organizational arrangements or a reservoir of fungible resources. Their absence coupled with the disruption accompanying an intense rapid change in strategic posture acts as entropic accelerants that are otherwise absent among more successful firms.

Second, when a firm underperforms relative to its industry average, managers characteristically interpret this situation as a loss relative to their benchmark. Managers may respond with riskier organizational changes (Wiseman & Bromiley, 1996), gamble to regain market position (Miller & Chen, 2004), and consider substantial changes in their EO in the hope of a better future (Huang et al., 2019). Such actions further exhaust resources, hastening the risk of firm failure as the firm chases a “home run” while even more vulnerable to total losses and their resource implications. At higher levels of underperformance, responding with large abrupt changes in EO is expected to reduce firms’ life expectancy further. Therefore:

Hypothesis 3. Firm underperformance relative to its industry average positively moderates the relationship between a large abrupt change in EO and the risk of firm failure.

Research Methods

Sample and Dataset

We tested our theory and hypotheses with panel data of publicly traded U.S. firms operating in high-technology sectors during 2000–2018. 3 We selected these years because before the fiscal year 2000, the “dotcom” crash caused several firms to fail and may bias our results. We used longitudinal secondary datasets from Compustat and CRSP to compile data for our study. 4 Our sampling frame consisted of 804 large firms belonging to nine high-technology sectors. 5 High-technology firms emphasize innovation in their competitive strategies and spend substantially on R&D (averaging US$850 million annually in our sample). These firms face high rates of technological change and uncertainty surrounding what technologies, features, and products will be successful in the medium to long term. These are ingredients for entropic pressure (Slevin & Covin, 1998).

The final sample exceeded the minimum sample size required to ensure statistical power when testing our hypotheses (Murphy et al., 2014). A statistical power analysis using effect size and significance level α determined the minimum amount needed for regression analysis. The significance level was set to .05 to guard against type I error (Murphy et al., 2014). We use β to guard against type II error. Cohen (1992) recommends that β be equal to α and is set to .05. Statistical power was then calculated as 1 − β = 0.95, the probability of avoiding a type II error because of sampling error. The effect size was set to a medium level (F-test for regression or f2 ratio = 0.15) to ensure the difference between the population mean and sample mean was large enough to be detectable (Kim et al., 2004). We then calculated sample size requirement as the effect size (f2 = 0.15), α = .05, power = 0.95, and the number of predictor variables (including controls) (19), culminating in a recommended sample size of 218. Our sample of 804 firms ensures valid conclusions when testing our hypotheses.

Across the 18 years, there were 6,018 observations. After removing missing values and mergers and acquisitions (M&As) among successful businesses from the analysis (where the Altman Z-score is greater than 3; see Section “Measures”), the final sample consisted of 4,971 observations. As sample selection criteria, only large firms with more than 500 employees were selected because smaller firms exhibit a generally higher risk of firm failure due to factors beyond EO (e.g., liabilities of newness and smallness). Firms with zero R&D expenditure were excluded. The sample consisted of high-technology firms because firms in high-technology industries tend to have strategies favoring proactive search and risk-taking and are subject to frequent technological changes encouraging innovativeness.

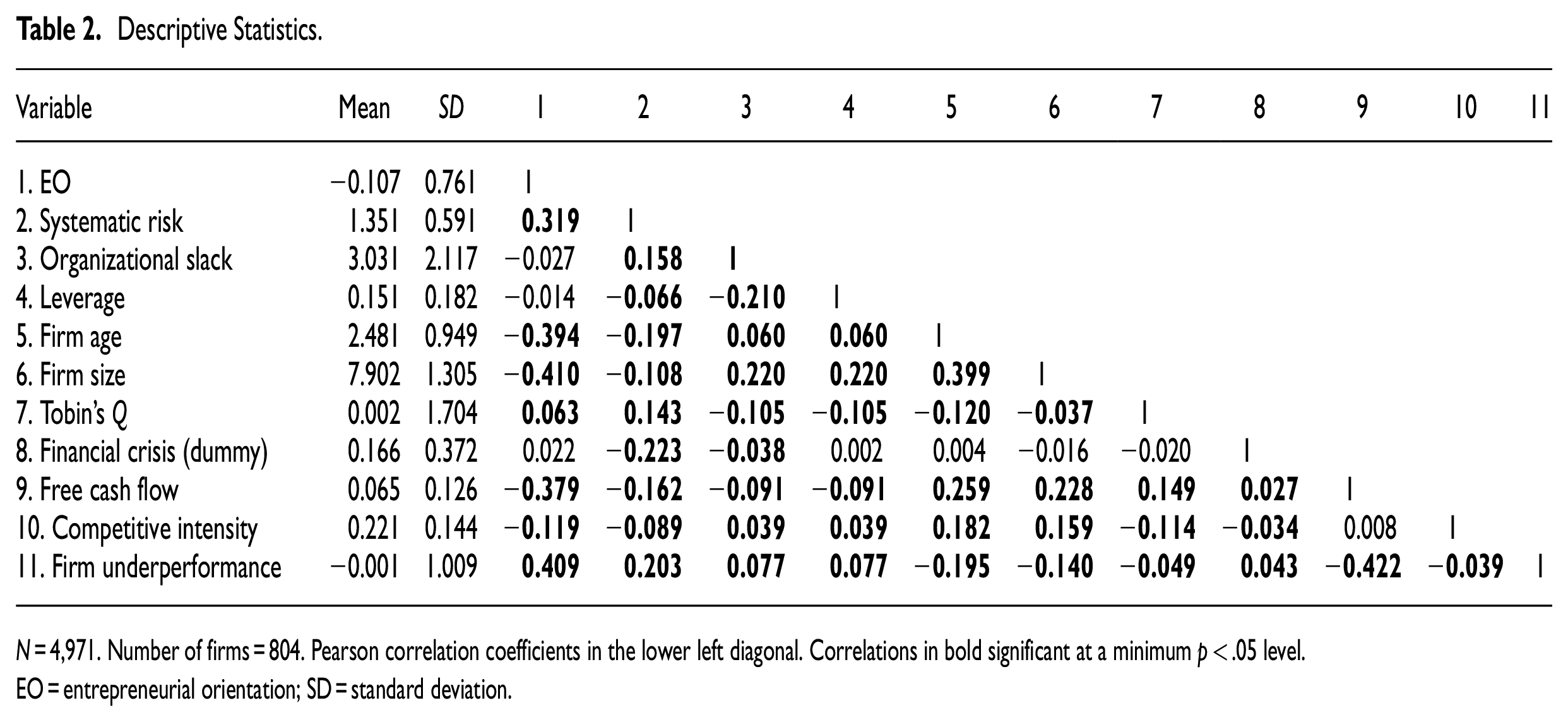

High-technology firms might exhibit a higher baseline EO and show little variance in their EO. We evaluated our sample of high-technology firms against a second sample of non-technology-focused firms to test both assumptions. Both assumptions are incorrect. First, the mean value of EO among our sample is −0.107 with a standard deviation of 0.761; the mean value of EO in our comparative sample is −0.48 with a standard deviation of 0.722. While the mean is relatively higher among our sample of high-technology firms compared to the comparative sample, the assumption that high-technology firms exhibit little variance in EO is false given the high standard deviation. Second, the mean of −0.107 suggests that the baseline value of EO in the high-technology sample is not abnormally high.

Measures

Dependent Variable

For the risk of firm failure, the log of the hazard function in the Cox proportional hazard was used, measured as the interaction between the length of time in the sample and the status of the firm (surviving or failed). The length of time for surviving firms was calculated from the start of the time included (fiscal year 2000) until the year of the last observation (fiscal year 2018). Furthermore, firms can enter the Compustat dataset at different time points. We account for this in the Cox regression by including start time and end time for each firm in our dataset. We determined the length of time to event for failed firms using the delisting date “DLDTE” in Compustat. Firm failure is not limited to business liquidation or bankruptcy. It can also arise from an unsuccessful merger and acquisition or a cessation of filing with the Securities and Exchange Commission (SEC).

Firms are delisted in Compustat for several reasons. Delisting is classified by a “reason for deletion” variable specified as a two-digit delisting code. Firm failure encompassed discontinuity of ownership (M&A), bankruptcy or liquidity, and no longer filing with the SEC (Josefy et al., 2017). Concerning “discontinuity of ownership,” those firms exiting successfully were separated from unsuccessful exits using Altman’s (1968)Z-score of financial distress. This method determines whether a firm that exited due to a merger or acquisition would have gone bankrupt had it not been for the merger or acquisition. Several studies have used the Altman Z-score to classify firm failure (Baù et al., 2017; Chakrabarti, 2015; Gómez-Mejia et al., 2022; Swift, 2016; Wiklund & Shepherd, 2011). Altman’s Z-score has several firm-level indicators including firm size, leverage, liquidity, and performance to characterize firms in financial distress. Like Wiklund and Shepherd (2011), a Z-score of less than 3 signals a distressed, failing firm. Consequently, 285 firms remained among those that had undergone M&A and were considered as failed (sample size was 4,971 observations, 804 firms, and 966 failure events).

Independent Variables

EO represents the joint exhibition of innovativeness, proactiveness, and risk-taking behaviors. We use financial indicators to measure EO following Miller and Le Breton-Miller (2011) and Kreiser et al. (2020). EO is traditionally measured using survey-based data (see Supplemental Material), but it is practically impossible to survey failed firms or track EO longitudinally with surveys. Financial indicators illustrate what a firm did with its resources, capturing tangible behaviors and outcomes each year (Kreiser et al., 2020), and reflect each firm’s financial condition as mandated by law and verified by auditors, reducing the risk of measurement error (Miller & Le Breton-Miller, 2011). Agreeing with Kreiser et al. (2020), we argue that financial ratios best capture a behavioral, firm-level perspective on EO.

We measured innovativeness as R&D intensity because firms that invest more in R&D tend toward innovative investments and producing innovation outputs (Hall et al., 2005). We calculated R&D intensity as R&D expenditure divided by total assets (Kreiser et al., 2020). R&D intensity reflects the extent a firm invests in new technologies and facilitates exploration by incorporating new knowledge.

Proactiveness was measured as the percentage of annual earnings reinvested in the company, calculated as retained earnings divided by total assets (Miller & Le Breton-Miller, 2011). Consistent with Miller and Le Breton-Miller (2011), we computed proactiveness by subtracting the industry average from each of the firms’ percentage of reinvested profits. This measure is an overall proxy for the firm’s pursuit of opportunities adjusted for industry-level factors that affect the reinvestment of profits over time. This measure of proactiveness is consistent with its definition (i.e., anticipating future demand and retaining resources to ensure the firm’s market positioning), symbolizing a firm’s overall proactiveness in building up its business for the long term.

Risk-taking represents the unsystematic risk of the firm (the portion of risk unattributed or unexplained by the industry). Unsystematic risk reflects management’s tendency to pursue risky endeavors. We used the daily stock return file from CRSP when computing unsystematic risk. We measured unsystematic risk as the standard deviation of residuals from the regression of running the daily stock returns (raw returns minus the risk-free rate) on the value-weighted market returns (value-weighted returns minus the risk-free rate) (Miller & Le Breton-Miller, 2011). The unsystematic risk value was readjusted based on fiscal year. This measure of risk-taking is consistent with the idea that firms embarking on risky projects are subjected to more volatility in their stock price.

The standardized values of these dimensions were added to compute an EO index.

Large abrupt changes in EO were calculated as the largest values in changes in EO among the sample of firms based on the top 25% in our sample over the 18-year period. We used a GARCH (Generalized Autoregressive Conditional Heteroskedastic) model to estimate the time trend of EO. This measure represented the largest changes from the absolute value for studentized residuals for the sample of firms from a GARCH time trend of EO and identifies the extreme or unexpected changes in EO from our sample of firms during the study’s period (Mudambi & Swift, 2014). Previous research has used GARCH to estimate the trend of R&D or technological changes over time (e.g., Mudambi & Swift, 2014). By conducting a GARCH model, we obtained the residuals from the regression, which represent the extent or frequency within which the firm’s EO diverges from a forecast that one would have reasonably predicted based on the historical trend of the firm’s EO. Thus, the residuals in comparison with this historical trend indicate meaningful changes in EO over time. Small residuals indicate that a firm had a balanced EO trend over time; large residuals indicate an abrupt change in EO over time. To test for large residuals, we took the top 25% values per firm per year from the absolute studentized residual values.

Moderating Variable

We computed Firm Earnings Underperformance Relative to Industry Average by using a lower partial moment of the firm’s earnings underperformance relative to the target (Mudambi & Swift, 2014). The earning benchmark was calculated as the average return on assets for the industry where the firm competed from the previous year (Miller & Reuer, 1996).

Mediating Variable

To determine the lack of organizational resource slack, first, unabsorbed organizational resource slack was computed as current assets divided by current liabilities. Unabsorbed slack represents available resources (a liquid form of internal slack) (Singh, 1986). To represent the lack of organizational resource slack for our causal mediation analysis, we reverse-coded unabsorbed organizational resource slack by multiplying it with −1. A lack of organizational resource slack indicates few resources are available for new entrepreneurial activities, where present product/service market activities absorb most resources, and discretion is low without having to draw resources from existing activities.

Control Variables

We controlled for the firm, environmental conditions, and market risk. We controlled for systematic risk, the market-driven volatility that has a known significant positive effect on firm failure (Acharya et al., 2017). Systematic risk represents the value-weighted market returns (Miller & Le Breton-Miller, 2011). We controlled for firm age (the log of the years since listing on CRSP). Listing age has more economic meaning than founding year since the listing year is a significant time in a firm’s life, affects ownership and governance structures, and improves a firm’s growth opportunities (Bebchuk et al., 2011). Firm size was computed as the logged value of the number of employees. Larger firms tend to have better access to resources. We controlled for organizational slack except when it served as a mediating variable. Leverage was computed as the ratio of total debt to total assets. More debt increases the risk of firm failure (Altman, 1968).

Tobin’s Q can influence the risk of firm failure (Opler & Titman, 1994). We calculated an industry-adjusted Tobin’s Q for each firm by subtracting the value of Tobin’s Q for each firm in each fiscal year from the industry average during that fiscal year. Free cash flow was measured as the earnings before depreciation after interest, taxes, and dividends divided by net assets; net assets were calculated by subtracting cash and marketable securities from total assets (Bates et al., 2009). Competitive intensity, represented by the Herfindahl–Hirschman index (HHI), was calculated as the sum of the squared market shares of firms in a high-technology industry. Increases in the HHI index indicate a decrease in competition. The financial crisis was accounted for through time dummies coded as 1 for fiscal years 2007, 2008, and 2009. The separate high-technology industries were included in the analysis to control for unobserved industry-related factors.

Data Analysis Method

We used the Cox proportional hazard model to test our hypotheses because this approach can better handle unobserved heterogeneity. The Cox proportional hazard regression model estimates the probability that a surviving firm at time t will experience the event of a failure in the next few periods included in the study’s timeframe. The effect of the independent variables is interpreted as coefficients greater than 0 (or hazard ratios [HRs] greater than 1) indicating that the variable increases the risk of firm failure (or reduces the chances of survival). The percentage of failure reduction was computed as 1-HR. Using a Cox proportional hazard regression is advantageous because no assumptions are needed on how the baseline hazard depends on time (Keele, 2010). However, Cox regression relies on the assumption of proportional hazards. We ran several tests to confirm that the proportionality assumption was not violated (see Supplemental Material of this manuscript). We included the surviving firms in the analysis using the censoring of their observations.

Results

Table 2 presents the descriptive statistics and correlation matrix, Table 3 presents the main results of the Cox proportional hazard regression analyses, and Table 4 presents the causal mediation analysis.

Descriptive Statistics.

N = 4,971. Number of firms = 804. Pearson correlation coefficients in the lower left diagonal. Correlations in bold significant at a minimum p < .05 level.

EO = entrepreneurial orientation; SD = standard deviation.

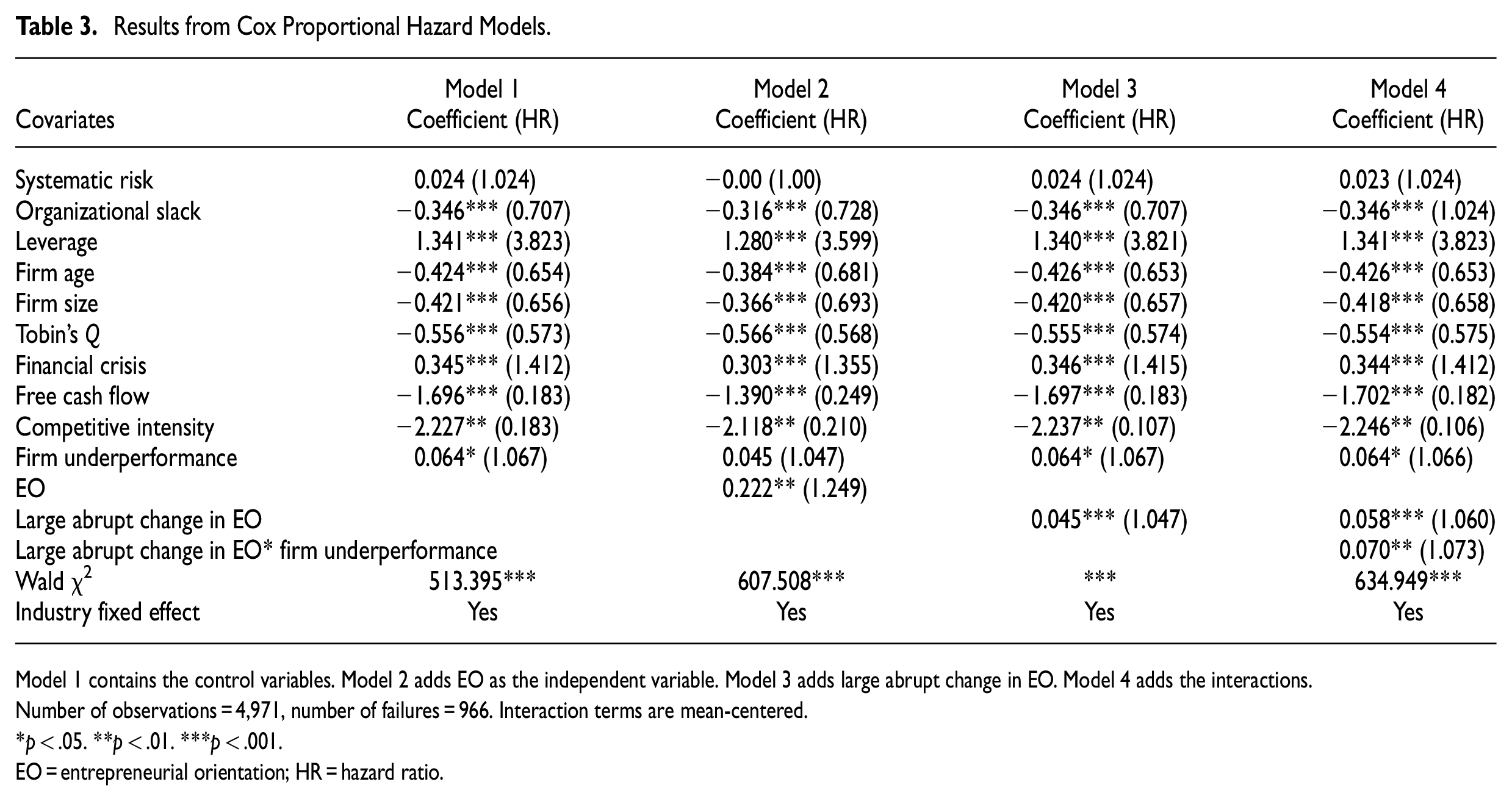

Results from Cox Proportional Hazard Models.

Model 1 contains the control variables. Model 2 adds EO as the independent variable. Model 3 adds large abrupt change in EO. Model 4 adds the interactions.

Number of observations = 4,971, number of failures = 966. Interaction terms are mean-centered.

p < .05. **p < .01. ***p < .001.

EO = entrepreneurial orientation; HR = hazard ratio.

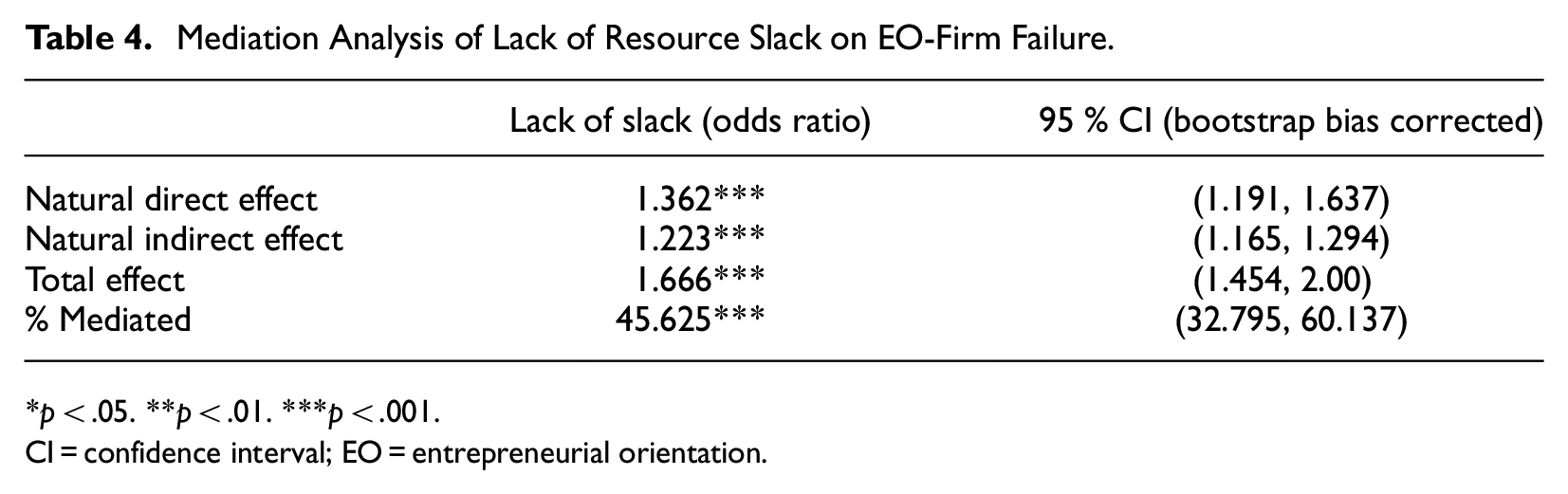

Mediation Analysis of Lack of Resource Slack on EO-Firm Failure.

p < .05. **p < .01. ***p < .001.

CI = confidence interval; EO = entrepreneurial orientation.

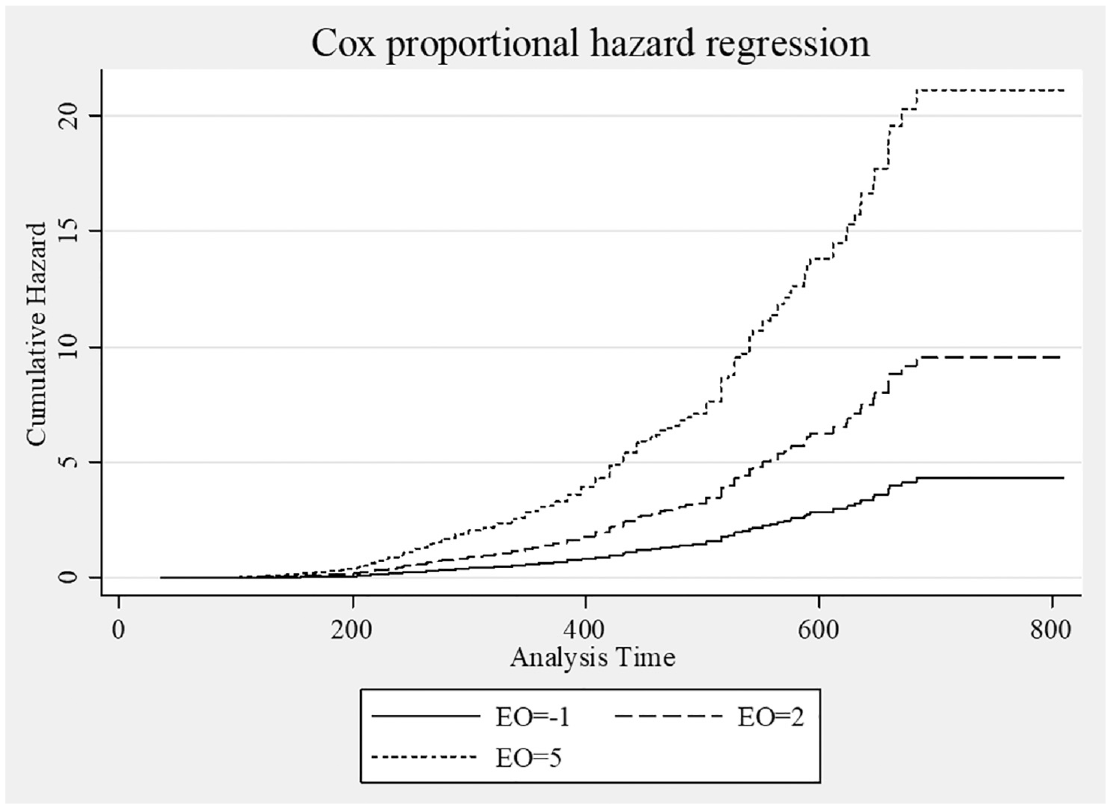

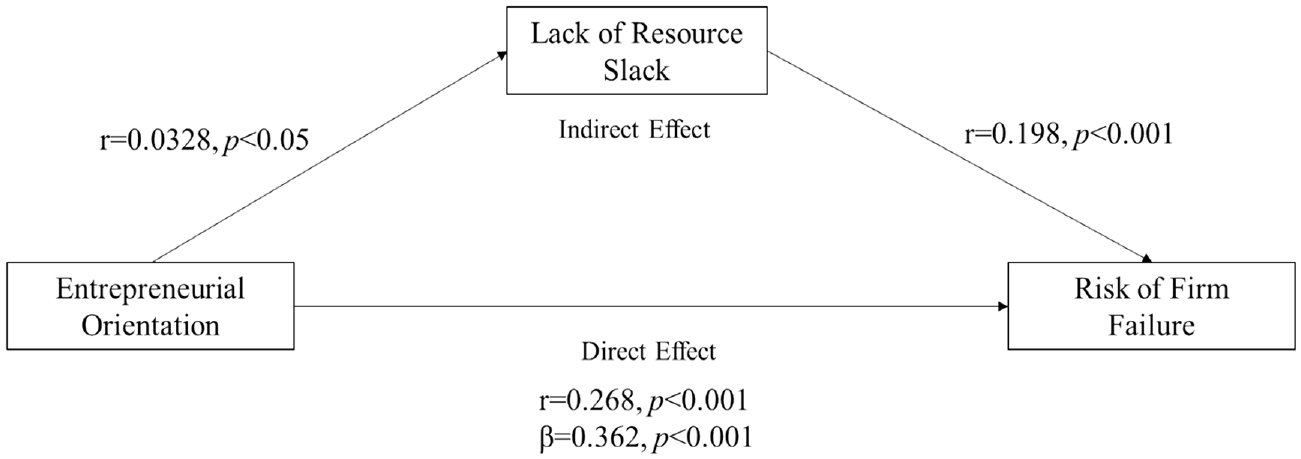

We find strong evidence supporting Hypothesis 1: the lack of organizational resource slack mediates the relationship between EO and the risk of firm failure over time. First, in Model 2 of Table 3, EO exhibits a significant positive effect on the risk of firm failure, increasing this risk by 24.9% (0.222, p = .002) with every one-point increase in EO. Given the multiplicative nature of the HR, if we were to compare two firms whose levels of EO were 10 points apart, the risk of failure of the less entrepreneurial firm would be 90.77% of the more entrepreneurial one (or 9.23% lower, since 1.24910 = 9.23). Figure 2 illustrates the cumulative risk of firm failure at various levels of EO. Second, as shown in Table 4, the lack of organizational resource slack significantly and positively mediates the relationship between EO and risk of firm failure. Based on the causal mediation analysis, more EO depletes resources, increasing the risk of firm failure. Specifically, the odds ratio of the natural direct effect of EO on the risk of firm failure not mediated by lack of organizational resource slack is 1.363 (p < .001), and the odds ratio of the natural indirect effect of lack of organizational resource slack on EO risk of firm failure is 1.223 (p < .001). The results of the mediation analysis are shown in Figure 3. The percentage of the total effect mediated is 45.625% (p < .001).

The effect of EO values on the risk of firm failure.

Mediation analysis of lack of slack on the EO risk of failure relationship.

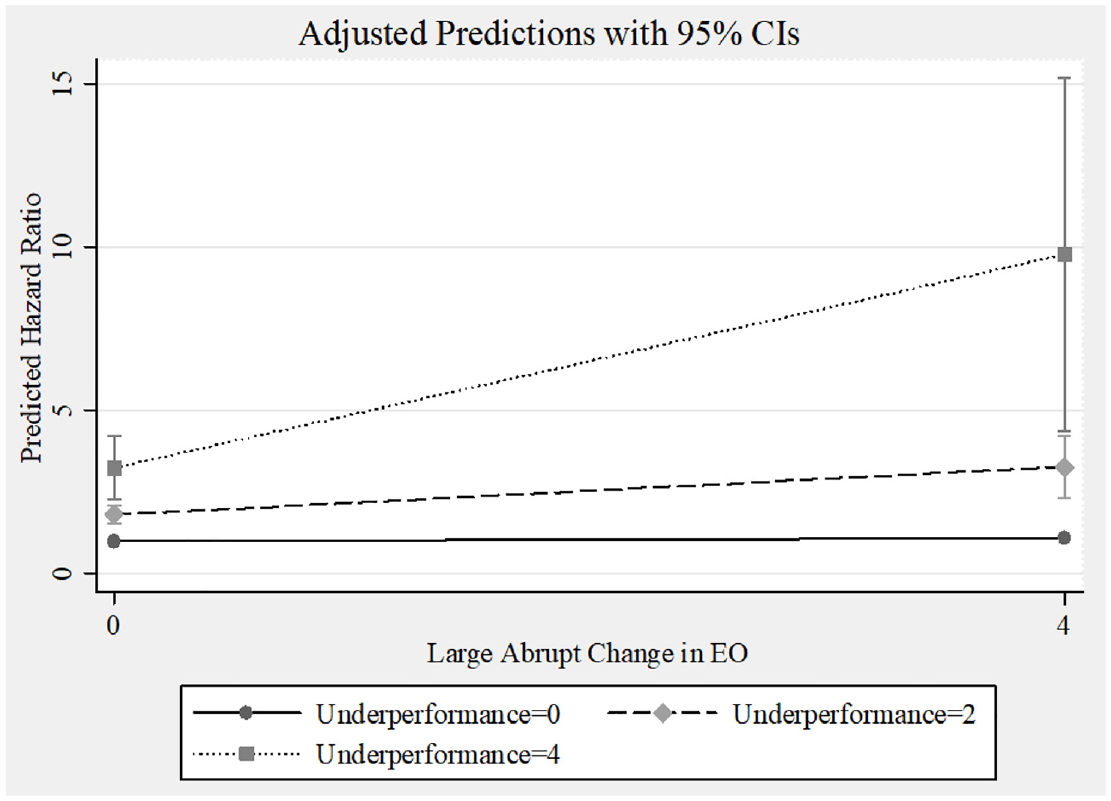

We find strong evidence for Hypothesis 2: a large abrupt change in EO over time increases the risk of firm failure. In Model 3, large abrupt changes in EO positively and significantly affect the risk of firm failure, increasing their risk of firm failure by 4.7% (p < .001). Moreover, we found that the interaction between firm underperformance and large abrupt changes in EO is significant at p < .05 (Table 3, Model; Figure 4). Hypothesis 3 is supported: firm underperformance positively moderates the relationship between large abrupt changes in EO and the risk of firm failure.

The moderating effect of firm underperformance.

Robustness Tests

We tested against several changes in model specification. First, we ran a logistic regression and found that EO significantly affects the risk of firm failure (odds ratio = 1.362, p < .001). Second, the lagged value of EO had a significant positive effect on the risk of firm failure (p < .001), increasing the risk by 32.5%. Third, we applied alternative measures for proactiveness and innovativeness following Miller and Le Breton Miller (2011). We adjusted the innovativeness dimension to R&D/total sales. EO continued to positively affect the risk of firm failure (HR = 1.207, p < .05). We then applied research quotient (variation in revenue from a 1% increase in R&D, sourced from WRDS), as a measure of innovative ability (Santi, 2019). Here, EO increased the risk of firm failure by 23% (p = .006). Our measure for proactiveness does not reveal the details about investments (e.g., whether it is just updating equipment, making bold forays into the territory of its competitors, or pioneering a greenfield strategy) (Miller & Le Breton Miller, 2011). We used an alternative measure of proactiveness by subtracting investments in long-term assets (property, plant, and equipment) from retained earnings. EO continued to significantly affect the risk of firm failure by 25% at p = .002.

Fourth, we tested the effects of each EO dimension separately on the risk of firm failure. Proactiveness (HR = 1.061, p < .001) and risk-taking increased the risk of firm failure (HR = 1.249, p < .01), but innovativeness (HR = 1.33, p > .05) had no significant individual effect. Innovativeness is an integral element of EO, and without proactiveness and risk-taking, innovativeness neither increases nor reduces the risk of firm failure. The mediating effect of a lack of organizational resource slack on the relationships between innovativeness, proactiveness, and risk-taking and the risk of failure shows that each dimension is positively and significantly mediated (results available on request from the authors). Large abrupt changes in proactiveness (HR = 1.107, p < .05) and risk-taking (HR = 1.168, p < .001) increase the risk of firm failure. A large abrupt change in innovativeness is not significant. We conclude that although the effects of individual indicators sometimes vary in significance, their interdependence as EO makes the difference to the risk of firm failure, as predicted.

Fifth, the continuous regressors were winsorized to their respective 1st and 99th percentiles for robustness (Maula & Stam, 2020). The results remained the same. Finally, we considered the possibility of a nonlinear relationship between EO and firm failure. We find no significant nonlinear effect (p > .05).

Discussion

Theory on the failure of entrepreneurial firms remains surprisingly scarce. EO can contribute positively to firm performance, but there is considerable doubt over how that positive contribution is realized (Gupta et al., 2020; Lee et al., 2019) in ways that mitigate severe losses precipitating a risk of firm failure (Kindermann et al., 2022; Patel et al., 2015; Wales, 2016). The performance-enhancing ability of EO represents a story truncated by survival bias (Rauch et al., 2009; Schweiger et al., 2019), cross-sectional bias (Lomberg et al., 2017), and assumptions about its temporal stability (Wales, 2016). Much of the EO literature also relies on theory borrowing (Whetten et al., 2009) and scaffolding (Wales et al., 2021). However, inattention to a theory that predicts when EO jeopardizes firm survival has led us to miss when, why, and under what circumstances EO can heighten the risk of firm failure. We contribute toward closing this critical gap.

We developed a resource exhaustion theory of firm failure explaining how the tendency of EO to generate variance-inducing activities and unencumbered experimentation gives rise to unsustainable amounts of entrepreneurial entropy as root cause of the higher risk of firm failure. EO prompts exploratory behaviors epitomizing experimentation, broad search, discovery, risk-taking, and innovation that seek out and produce variance in pursuit of a richer and more exciting future (Covin & Wales, 2019). We characterize the state of high entropy as one of severe resource exhaustion where the explorative nature of EO gives rise to an exploration liability effect that accelerates resource depletion. Our theory helps us understand how the “work” of EO centers around a repertoire of exploratory acts that are capable of substantial gains and losses (Wales, 2016). Imbalance of exploration against exploitation depletes resources and exhausts them rapidly at its extreme.

Our findings draw attention to time and to when the exploration liability effect is at its most severe. The exploration liability effect sees the firm suffering too many underdeveloped and unproductive new ideas as entrepreneurship becomes unencumbered. As EO increases, the firm experiences more acutely the battle against time and an unrelenting forward pressure for continuous adaptation beset by EO (Slevin & Covin, 1998). However, while EO increases the risk of failure (by 24.9% in our data), we show that entrepreneurship dissipates underutilized (unabsorbed slack) resources through new activities to mediate the relationship between EO and the risk of firm failure. These insights shed new light on the link between EO and firm failure. For instance, while Kindermann et al. (2022) remark that EO might reduce firm failure contingent on its configuration and organizational factors—the effects of which are typically modeled as financial, not resource-based—their study of post-IPO firms risked omitting firms that are resource strained. Kindermann et al. (2022) partly anticipate this possibility by reflecting on working capital efficiency. However, our work is first to provide the theoretical logic and mechanisms to more fully explain the EO–resource–failure thesis. As resource slack falls, EO’s exploration liability effect takes hold. In excess, the outcome is firm failure, with the reason being rooted in the entropy generated and the failure to manage this process. These findings add nuance to Kreiser et al. (2020) who associate recoverable slack (surplus resources in a firm’s cost structure) with more EO behavior when environments are hostile where otherwise there is no change. We extend Rosenbusch et al.’s (2013) observation that firms operating in threatening environments struggle to acquire the resources needed to benefit from high EO. We reveal that an increase in EO will induce greater resource consumption that exacerbates the firm’s cumulative entropy and resource exhaustion, heightening the danger posed by any inability to replenish resources.

This discussion crystallizes our first theoretical contribution. We provide scholars with a resource exhaustion theory of firm failure that resolves the inattention given to explaining when EO endangers firm survival. The risk of firm failure posed by EO is not an anomaly and our resource exhaustion theory provides the missing theoretical logic (entrepreneurial entropy) and theoretical mechanisms (asset specificity and exploration liability effect) needed to predict when and why EO jeopardizes firm survival. We conceptualize the exploration liability effect as an outcome of the work of EO, explaining how EO increases entropy to a state of resource exhaustion that can become irrecoverable and fatal. Our resource exhaustion theory provides a first comprehensive explanation for why, despite its positive financial performance returns, EO can still cause firm failure. We have long appreciated that EO generates substantial gains and losses. Sometimes, the losses outpace the gains, and we reveal when this happens. We acknowledge the potential upside of EO and by considering the pacing and magnitude of EO, we demonstrate that entropy often makes reaping the gains more challenging such that the costs (resources committed) eventually outstrip the gains so substantially that firm failure occurs. Our new theory provides scholars with the means to predict the conditions under which failure may occur and directs the spotlight onto entropy-combating initiatives and thwarting those that accelerate entropy without impediment.

Time-based analyses of EO are rare (Lomberg et al., 2017) and the assumption among studies is that EO should be stable over time (Lee et al., 2019; Wales, 2016). When firms maintain a temporally stable EO, managers have time to develop necessary capabilities. Managers also have opportunities to set the structure, processes, and routines that order and stabilize entrepreneurial activities (Slevin & Covin, 1998), which should improve resource use and reduce resource misallocations. However, manifesting EO in a temporally stable way does not stop entropy; it merely slows it down. We theorize how temporal stability gives rise to a repetition effect. EO breeds exploratory, proactive behaviors and propels acts of trial and error that generate large changes to current strategies (Patel et al., 2015). Over time, entrepreneurial firms tend to want to continue prospecting and experimenting (Hambrick, 1983). Thus, the repetition effect is equally capable of fueling entropy, but at a relatively slower rate. The range of outcomes from engaging in EO in a temporally stable manner remains relatively unpredictable and stochastic. However, managers benefit from at least some opportunity to create semi-stable structures that replenish organizational resources. To date, EO scholars are non-comital on whether the temporal stability of EO is economically beneficial or not. For instance, temporal stability is needed to override the notion that a firm behaving entrepreneurially is not doing so randomly (Wales, 2016). However, other studies indicate that EO should change based on circumstances in the firm’s task environment (Kreiser et al., 2020; Rosenbusch et al., 2013). Coupling the repetition effect with the exploration liability effect in our theory provides a novel theoretical rationale for why the temporal stability assumption in EO research does not satisfactorily distinguish a high-performing entrepreneurial firm from one that ultimately fails.

We show how the temporal form of EO matters when considering its contribution to the risk of firm failure. Specifically, the entrepreneurial firm is under relentless forward pressure and competitive strain that stretches its resources (Slevin & Covin, 1998). While scholars accept that EO is an intensely resource-consuming strategic posture (Covin & Wales, 2019), we have too readily accepted that EO creates or garners resources to substitute what it depletes. Our theory corrects for this and emphasizes asset specificity. Liquid resources are important to entrepreneurially oriented firms. Resources used up by EO cannot always be recovered because their transformation from cash (e.g.) into outputs cannot be readily converted back into a liquid state that combats entropy. Moreover, resources applied in the pursuit of entrepreneurial endeavors and new product–market initiatives cannot be easily uncommitted and transferred, worsening the problem posed by asset specificity in recovering from entrepreneurial entropy and mounting resource exhaustion.

Firms encounter periods of relative stability that are interrupted by abrupt and intense change (Mudambi & Swift, 2014; Romanelli & Tushman, 1994). Over time, the temporal stability of EO must give way to punctuated changes in strategic posture that gear up or gear down the firm’s EO. Abrupt changes in EO are likely when growth erodes the effectiveness of existing organizational arrangements or environmental changes cause misalignments with existing structures, processes, or routines (Slevin & Covin, 1998), At times then, an EO might be ill-suited to a firm, despite its intuitive appeal (cf. Schweiger et al., 2019). We theorize how large changes in EO occurring abruptly in a short period of time give rise to a punctuated effect, rapidly increasing entropy in a way that is far less sustainable than under temporal stability and its repetition effect. Our empirical results validate this effect as we demonstrate how these large abrupt changes increase the risk of firm failure above the time trend of EO alone. Our punctuated effect extends recent studies on temporal transition and discontinuous jumps (Kang & Kim, 2020; Mudambi & Swift, 2014) by focusing on the resource-based, and entropic, consequences of large changes in strategic behaviors.

Some firms might still be better (or worse) placed to manage the entropy that comes with large abrupt changes in the firm’s EO. A large abrupt change in EO requires a fundamental reshaping of the organization, its resource mix, and its processes all while its current resources are geared for the established strategic orientation (e.g., Hambrick, 1983). We believe that EO scholars have been indirectly addressing the entropic nature of EO for many years. Specifically, scholars have identified a range of EO–performance relationship moderators. Reconsidering some of these studies through resource exhaustion theory draws attention to their entropy-combating work. Examples include absorptive capacity (Engelen et al., 2014) and resource orchestration (Wales et al., 2013; Yang et al., 2019) supporting the positive performance consequences of EO. We unveil firm underperformance as a key contingency. Historically, overperforming firms will have better organizational arrangements and more resources to cope with fluctuations and changes in course. For underperforming firms, their existing organizational arrangements, past activities, and extant resources are inadequate. A common response to relative underperformance is risky problematic search (Titus et al., 2019), riskier organizational changes (Wiseman & Bromiley, 1996), and gambling to regain market position (Miller & Chen, 2004). A large shift in strategic posture is likely (Huang et al., 2019). Our findings show that firm underperformance intensifies the risk of firm failure posed by large abrupt changes in EO because managers will have little time to perform the entropy-combating work needed to alleviate the resource exhaustion accompanying a large shift. Entropy is already high because underperformers lack the advantages (or resources) of prior success. For these firms, the punctuated effect of a large abrupt change in EO will be even greater, significantly increasing the risk of firm failure. Therefore, we reveal an additional boundary condition in that underperforming firms are more negatively impacted by a large abrupt change in EO. Expecting that a compact change in EO will reverse their fortunes is misguided.

This discussion yields our second theoretical contribution. By bringing time into the EO conversation (Lévesque & Stephan, 2020), we advance the resource exhaustion theory of firm failure with a set of boundary conditions that enable more accurate prediction of the risk of firm failure over time and the role of EO within that risk. Moreover, our entropy theory and boundary conditions contribute to advancing knowledge on managerial risk-taking. Studies on managerial risk-taking rely on the behavioral theory of the firm, prospect theory, the behavioral agency model, and upper echelons theory (Hoskisson et al., 2017), through which the debate has often centered on entrepreneurial actions taken (or not) because of over- or under-performance. Our conceptualized effects originate from managerial decisions about sustaining and changing EO. Our work contributes to a resource exhaustion lens on managerial risk-taking to address the relative lack of research on moderators of relationships between managerial risk-taking and firm-level outcomes (see Hoskisson et al., 2017).

Finally, we advance theoretical and conceptual understanding of entropy in entrepreneurship research. Prior studies tend to use entropy loosely to describe instances of diversification. These include product (Jacquemin & Berry, 1979; Palepu, 1985) and international diversification (Hitt et al., 1997) and social diversity (Audretsch & Keilbach, 2007), measured by the scope of product strategy, international strategy, and voting behavior, respectively. However, these characterizations overlook its most important component: that entropy represents disorder in a system. Any system will gravitate toward high entropy (Kümmel, 2011; Schrodinger, 1947; Vogel, 1989), and high entropy is unsustainable because it represents a state of acute resource exhaustion where asset specificity prevents resource recovery and straightforward resource reallocation. Our theory provides entrepreneurship scholars with a basis to accurately conceptualize entrepreneurial entropy, its functioning, and likely effects, and an opportunity to revitalize entropy treatments of entrepreneurial phenomena. Relatedly, we believe these efforts offer a small advancement to learning theory. The entropy-accelerating work of EO leads to aggressive resource consumption that precipitates failure, made worse by large abrupt changes and firm underperformance. But firm failure occurs as heightened entropy gives rise to exploration liability, repetition, and punctuated effects that resemble ideas in learning theory about failure and competence traps and the path dependence of activities, routines, and structures associated with exploration (Levinthal & March, 1993). Entropy, and resource exhaustion theory, holds promise to (re)conceptualize tensions between exploration and exploitation.

Managerial Implications

Extant research highlights the importance of EO for firm growth and developing new sources of competitive advantage. We reveal managers must realize that pursuing entrepreneurial strategies might enhance the risk of firm failure over time. Even though firms in high-technology industries may be subject to more pressures to change their EO, a large abrupt change in EO increases their risk of firm failure over time. A manager of a high-technology firm needs to assess relative firm performance. If it is underperforming, then a large abrupt change in EO may further harm the firm’s standing. EO must be applied strategically. The key issue here is not in avoiding EO, but in successfully managing EO over time to reduce the cost of failure and in limiting the exposure to the downside of EO while preserving its access to growth opportunities made possible by an EO. Managers should carefully evaluate the asset specificity of their resources and manage carefully and strategically its resource stock and holdings to reduce its vulnerability to rapid resource exhaustion when entrepreneurial efforts (inevitably) fail.

Limitations and Future Research

Our study bears some limitations. First, we conceptualize EO as a unidimensional construct (Covin & Slevin, 1989), adopting the firm level in which an index is correct (Wales et al., 2020). However, our robustness tests suggest that innovativeness (individually) has no beneficial or worsening effect on the risk of firm failure. Their effects among alternative types of firms warrant further scrutiny. Second, our results are potentially context dependent, being empirically relevant to large U.S. high-technology firms. Future research can extend our theory and analysis to firms of different sizes, industries, variations in technology intensity, and country settings.

Third, we use proxies grounded in well-established financial metrics to measure EO objectively, but on the assumption that these indicators are comparable with well-validated survey measures. Objective measurement is not inherently ideal because of concern over construct validity when using archival proxies (Ketchen et al., 2013). We mitigated these concerns by ensuring consistency between our measures and construct definitions (Maula & Stam, 2020). For our study, these objective measures are robust, enable fair comparison among the firms in our sample, are not subject to perceptual biases possible when using subjective measures, and enable us to overcome survival bias. We also use alternative measures of the EO dimensions in our robustness tests. Financial indicators are not inherently superior to other EO measurement systems (Kreiser et al., 2020), but neither are traditional survey measures (Covin & Wales, 2019). Archival financial measures are best suited to capture EO as a behavioral construct, as intended in our study.

Scholars have long been critical of the lack of a distinct theory of EO (Wales et al., 2021). We provide a resource exhaustion theory capable of accurately predicting when and how EO may disrupt firms irretrievably, concluding in firm failure. Studies should now grapple with resource exhaustion and entrepreneurial entropy. For example, while EO may cause a firm to innovate disruptively, it requires stability and structure within the firm to keep it productively entrepreneurial over time and combat the entropy that will otherwise accumulate. Where managers can create stability by organizing effective structures and processes, entrepreneurial behaviors are likely to be more productive and tenuous projects more swiftly terminated (Covin & Wales, 2019), keeping entropy under control. We recommend this as a fruitful avenue for future research. Also, from an entropy-combating perspective, asset specificity represents at least one boundary condition to our theory as firms which explore new product–market entry opportunities (increase EO) with less asset specificity can combat entropy by allowing for less resources to be lost (e.g., resource use is more reversible at least to an extent). The entropy metaphor drawn from physics, while useful to understand entrepreneurship, is not a perfect one-to-one match.

Finally, we believe the time is ripe for time-based theories of EO. By omitting time, the EO literature suffers from an experiential regress problem in which past experiences leading to EO are not well understood. A hierarchal problem also forms, in which the origins of EO as a collective construct at the firm level may have emerged from conditions at other levels of analysis. Developing time-based theories of EO holds considerable promise to understand how EO forms, when and why it evolves, evaluate its temporal stability, and further understand the actions managers must take to combat resource exhaustion and entropy.

Conclusion

As our understanding of EO has matured, the scholarly community has embraced EO as being capable of substantial gains and losses. It is puzzling then that we know little about why and under what circumstances EO might intensify the risk of firm failure. We develop a resource exhaustion theory of the risk of firm failure and address survival bias, cross-sectional bias, and assumptions of time indifference and temporal stability present in EO research that have led to the underreporting of potential failure. We provide the first theory, hypotheses, and evidence forming a resource exhaustion theory of firm failure to explain how, when, and under what circumstances EO increases the risk of firm failure over time.

Supplemental Material

sj-pdf-1-etp-10.1177_10422587231151957 – Supplemental material for Entrepreneurial Entropy: A Resource Exhaustion Theory of Firm Failure From Entrepreneurial Orientation

Supplemental material, sj-pdf-1-etp-10.1177_10422587231151957 for Entrepreneurial Entropy: A Resource Exhaustion Theory of Firm Failure From Entrepreneurial Orientation by Nazha Gali, Mathew (Mat) Hughes, Robert E. Morgan and Catherine L. Wang in Entrepreneurship Theory and Practice

Footnotes

Acknowledgements

We are incredibly thankful to ETP Editor Bill Wales for his constructive editorial handling of our work and his efforts to help bring out and shape our ideas to their fullest. We extend our gratitude to our three anonymous reviewers for their invaluable insights and comments as we refined the ideas in this manuscript. We are also grateful to Brian Anderson and Lou Marino for their valuable feedback on earlier versions of work that ultimately became this manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.