Abstract

Larger firms are increasingly acquiring innovative new ventures at an early stage. Despite significant integration challenges with these acquisitions, the elongated pre-acquisition process of aligning buyers’ and sellers’ different objectives is rarely studied. By studying nine academic spin-off acquisitions, we develop a three-phase model outlining the temporal dynamics of the pre-acquisition process. In each phase—namely, strategic fit, synergy confidence, and deal structure—a specific buyer-seller tension emerges. By showing how each of these tensions needs to be overcome prior to an acquisition event, our dialectical model complements the dominant focus on post-integration activities in the acquisition literature.

Keywords

Introduction

Being acquired is among the most viable options for new ventures to grow and scale their activity and for founders and investors to harvest value. However, research on the process leading to the acquisition of an entrepreneurial firm is nearly absent (Welch et al., 2020). This paper seeks to untangle the dynamics of this critical pre-acquisition process. To do so, we study academic spin-offs (ASOs), a unique category of new ventures, which are increasingly being acquired by existing organizations (Woolley, 2017; Renko et al., 2020).

By commercializing scientific knowledge developed at universities, ASOs are acclaimed for their role in developing innovations (Shane, 2004), contributing to industrial research and development (Motohashi, 2005; Bonardo et al., 2011), and translating scientific research into societal impacts (Fini et al., 2018). However, like new ventures in general, ASOs suffer from the liabilities of newness and smallness and often struggle to reach markets successfully (Knockaert et al., 2011; Stinchcombe, 1965; Vanacker et al., 2014). Indeed, for early stage ASOs, both technological and market uncertainty are typically high (Renko et al., 2020), and these firms’ lack of track records and assets makes financial valuation difficult (Shane & Cable, 2002). Hence, acquisition by a larger firm is a means to survive and access customers, funding, and other resources and competencies (Rasmussen et al., 2011), and being acquired is a preferred exit option for many ASO owners (Clarysse et al., 2013; Cumming & MacIntosh, 2003).

In contrast, potential buyers have other rationales for entering an acquisition, such as seeking to extend (substitute) or deepen (complement) their existing resources and capabilities (Sears, 2017). Specifically, larger incumbent organizations often struggle to develop radical innovations in-house (Christensen, 2013), so they often acquire ASOs and other new technology-based ventures (Graebner et al., 2010; Andersson & Xiao 2016) with the aim of diversifying into new markets (Vermeulen & Barkema, 2001), gaining access to complementary resources or new capabilities (Cefis & Marsili, 2015), increasing their market power (Santos & Eisenhardt, 2009), and/or achieving strategic renewal (Sears, 2017).

An acquisition of an entrepreneurial firm is not purely an economic transaction or takeover by a dominant buyer but involves strategic consideration for both the buyer and seller that resembles an elongated courtship process (Graebner & Eisenhardt, 2004). Hence, the likelihood of an acquisition depends on the strategic and interpersonal fit between the partners (Graebner & Eisenhardt, 2004) and the trust developed between them (Graebner, 2009) before a deal is made. A successful acquisition represents potential benefits for both parties, but this potential often goes unrealized due to post-merger integration problems (Choi & McNamara, 2018). Indeed, prior research has looked at acquisition challenges related to strategic and sociocultural factors (Graebner et al., 2017), such as integrating complex tacit and social knowledge (Ranft & Lord, 2002), justifying the acquisition (Ellis et al., 2009), and managing employee emotions (Vuori et al., 2018). An implicit assumption of these studies is that integration challenges are dealt with only after an acquisition is completed. This assumption is reflected in the relatively sparse pre-acquisitions literature (Welch et al., 2020). We extend this line of research by highlighting that the pre-acquisition process, or the courtship period, is foundational for overcoming a number of tensions and uncertainties between the buyer and seller, which can subsequently ease post-merger integration.

While the literature is clear on the importance of overcoming tensions and uncertainties through an elongated courtship process (Graebner & Eisenhardt, 2004; Schweizer, 2005), a strong understanding of how the pre-acquisition process unfolds is lacking. In other words, the literature on pre-acquisition dynamics lacks theoretical conceptualization of the process leading to a deal (Welch et al., 2019) and therefore remains abstract for practitioners seeking guidance on how to proceed in this process. Considering the limited use of financial valuation techniques and formal due diligence processes in acquisitions of ASOs and other early stage privately held entrepreneurial ventures (Coff, 1999), there is a need to understand how tensions and uncertainties between buyers and sellers are overcome before a deal is made (Graebner et al., 2010; Welch et al., 2020). Thus, as recommended by Welch et al. (2020), we build on dialectical theorizing to better understand ASOs’ pre-acquisition process, asking the following research question: During the process preceding the acquisition of ASOs, how do tensions between buyers and sellers emerge, and how are these tensions overcome?

Answering this research question presents a methodological challenge because the pre-acquisition process often unfolds over a long time period and is not easily identifiable. Moreover, this acquisition process is typically conducted under a high degree of confidentiality (Harwood, 2006), making access to data difficult. We resolve this issue by relying on a hand-collected dataset following the development of a population of 374 ASOs in Norway. Among 32 identified acquisitions, we gained access to nine cases for in-depth qualitative enquiry, incorporating both the buyer and seller sides. Based on inductive data coding and an abductive analysis incorporating dialectical process theory, we develop a process model of how the pre-acquisition process evolves and thereby contribute to the literature in three distinct ways.

First, our dialectical process model unpacks the extended courtship period and builds theory on the processual dynamics throughout the pre-acquisition process (Graebner & Eisenhardt, 2004). We identify three phases in the pre-acquisition process of early stage privately held ASO acquisitions—strategic fit, synergy confidence, and deal structure. Each phase involves a functional opposition (e.g., technology vis-à-vis scalability) between buyers and sellers and an interactive unity (e.g., strategic fit), thereby resulting in a tension (e.g., technology fit vs. fit for scalability) that needs to be overcome. Buyers and sellers engage in an interactive process to unify the distinctive tensions that arise in each phase, providing an explanation for why these negotiations are elongated and time consuming (Shen & Reuer, 2005; Welch et al., 2020). Though there is no complete resolution, overcoming each tension is essential to progress in the pre-acquisition process (Graebner et al., 2010).

Second, our process model of pre-acquisition dynamics extends the theoretical foundations of the acquisition literature, which is predominantly variance driven (Welch et al., 2020) and explores acquisition outcomes (Ahuja & Katila, 2001) and challenges related to post-acquisition integration (Graebner et al., 2017; Trichterborn et al., 2016). By unpacking the elongated pre-acquisition process (Graebner & Eisenhardt, 2004; Welch et al., 2020), we add to the current emphasis in the literature on post-integration activities as the basis for acquisition success (Graebner et al., 2010; Ranft & Lord, 2002). Our findings indicate that many of the challenges arising during post-acquisition integration can be addressed and managed, at least partly, prior to an acquisition event.

Third, considering the increased volume of acquisitions of early stage privately held entrepreneurial firms (Capron & Shen, 2007; Renko et al., 2020), particularly ASOs (Woolley, 2017), our study sheds light on a relatively neglected pathway for commercializing scientific research and new technologies. The academic entrepreneurship literature predominantly looks at the conditions necessary to establish and grow independent ASOs, which may entail distinct processes and competencies compared with reaching the market through industrial acquisition. Hence, our findings provide several insights for entrepreneurs and owners of ASOs regarding how to manage the complex pre-acquisition process and the associated tensions preceding an acquisition event (Bonardo et al., 2010; Mathisen & Rasmussen, 2019).

Theoretical Background

Acquisition as Courtship

Following Graebner and Eisenhardt (2004, p. 395), we conceptualize acquisition as a form of courtship involving a “social exchange between buyers and sellers that is shaped by considerations of long-term fit as well as price.” Hence, an acquisition is rarely a quick market-based transaction or takeover but an elongated process by which the buyer and seller overcome a number of tensions before entering a deal (Welch et al., 2020).

The literature on technology venture acquisitions points to several potential sources of tensions in the acquisition process (Schweizer, 2005). While strategic hurdles in entrepreneurial firms and founders’ personal motivations could trigger the need to sell, the combination potential and the organizational rapport of the buyer and seller influence who entrepreneurial firms are willing to sell to (Graebner & Eisenhardt, 2004). Buyers of technology firms typically seek to obtain specific product-related technologies or product innovation and engineering capabilities as their primary motive (Ranft & Lord, 2000). Here, a moderate degree of knowledge overlap in the buyer’s and seller’s technological knowledge leads to higher acquisition success (Ahuja & Katila, 2001; Sears & Hoetker, 2014). Hence, strategic fit between the buyer and seller is often seen as important for acquisition success.

Several factors can potentially influence the acquisition process and outcome. For example, firms that are active corporate venture capital investors tend to earn greater returns when acquiring start-ups compared to firms that make only sporadic venture capital investments in start-ups (Benson & Ziedonis, 2009), and previous alliance activity is associated with higher valuations of acquisitions (Ozmel et al., 2013). Additionally, buyers’ pre-acquisition innovation experience can influence post-acquisition innovation actions (Choi & McNamara, 2018). Managers from acquired technology firms can also play an important role in realizing the value of and potential opportunities from acquisitions (Graebner 2004). Furthermore, the buyer’s and seller’s behaviors and activities during an acquisition influence its outcome. For instance, building and exploiting common ground in the knowledge shared between the buyer and seller can reduce the need for structural integration, which comes with the risk of destroying the innovative capabilities that made the focal technology firm attractive to buy in the first place (Puranam et al., 2009). Finally, Graebner (2009) shows how trust asymmetries between buyers and sellers emerge and persist in acquisitions, indicating that building trustworthiness is an elongated and dialectical process with inherent tensions.

Despite considerable research on buyers’ and sellers’ motivations, characteristics, and behaviors (Graebner et al., 2010; Haleblian et al., 2009), Welch et al. (2020) highlight four fundamental challenges stalling the development of our understanding of the pre-acquisition process: (1) the use of a relatively limited set of high-level variables, (2) simplistic understanding of the multiple actors involved and their interactions, (3) limited attention to the temporal dynamics of activities and decisions, and (4) the predominant theoretical focus on variance over process theorizing. These challenges underscore the need for a more processual understanding of how the pre-acquisition process unfolds. Given the many tensions that need to be overcome before and during an acquisition, we propose that a dialectical process view can provide a more detailed understanding of the pre-acquisition interactions and behaviors of ASOs and their buyers.

Dialectical Process Theory

Dialectical theory focuses on how contradictions are transformed over time (Hargrave & Van de Ven, 2017). In contrast to other process theories, such as evolutionary and teleological theories, the dialectical perspective can be characterized as a relational process philosophy (Farjoun, 2019). The idea of dialectics is not new to organization scholars (Benson, 1977), with several process studies building on the dialectical approach (Langley et al., 2013). Indeed, dialectical process models have been developed to describe different types of organizational change, such as competency acquisition (Marcus & Geffen, 1998), competitive dynamics (Chen & Miller, 2015), serendipity (Cunha et al., 2015), strategic alliances (De Rond & Bouchikhi, 2004), and sensemaking in post-merger integration (Monin et al., 2013).

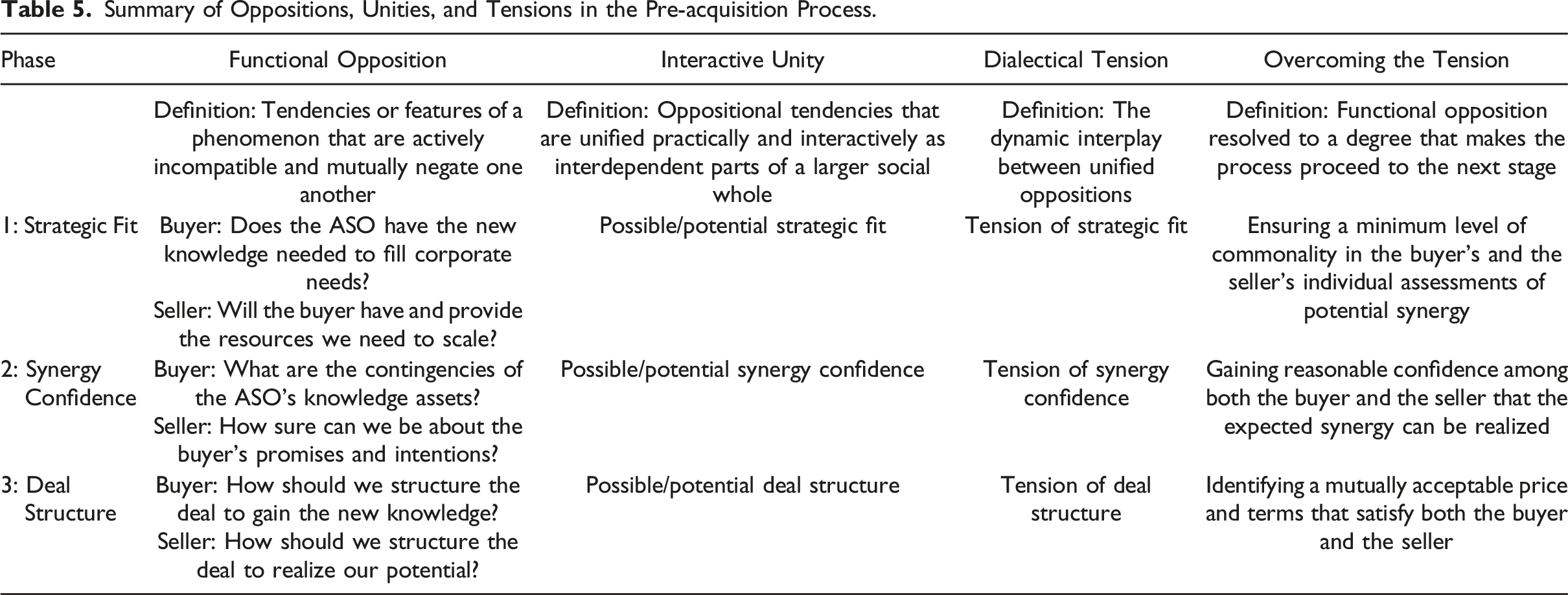

We build on the relational dialectics tradition, which is based on the Bakhtinian process of tension-based dialectics (Bakhtin, 1981; Werner & Baxter, 1994). This view proposes that a dialectical process plays out in a series of tensions between actors (e.g., buyer and seller), with each actor depending on the other side to ensure constant interplay. Change is shaped by how the sides deal with the tensions. Within the relational dialectics tradition, tensions rest on the presence of oppositions (logical or functional), the unity of oppositions (identity or interactive), and the dynamic interplay between the individual oppositions and the unity of these oppositions (Baxter & Montgomery, 1996). While logical oppositions are binary in nature (e.g., rich/poor; good/evil), functional oppositions are bipolar (e.g., autonomy/integration). Oppositions are necessary but not sufficient for dialectical tensions. For a dialectical tension to occur, oppositions need to be simultaneously unified or interdependent. This unity of opposition can manifest in two ways—unity of identity or interactive unity. Unity of identity presupposes the existence of a logical opposite (e.g., night requires day), while interactive unity is developed practically and interactively as interdependent parts of a larger social whole (e.g., individual autonomy and relational connection in a marriage). Dialectical tensions refer to the ongoing dynamic interactions between unified oppositions (e.g., technology fit vis-à-vis fit for scalability), which serve as the driving force for ongoing change (e.g., acquisition deal) in any social system (Baxter & Montgomery, 1996).

An acquisition represents a significant organizational change for both the buyer and the seller, who must engage in a dyadic exchange of information and access to each other (i.e., functional oppositions and interactive unities at play) involving several dialectical tensions that must be overcome to progress toward a new (changed) state (Baxter & Norwood, 2015). Hence, established organizations’ acquisitions of entrepreneurial firms are full of what Zeitz (1980) summarizes as dialectics—namely, reliance on external resources, inequality in resource exchange, contradictions to be overcome, and reactive effects on interorganizational relationships. Hence, dialectical theory appears promising to help explain ASOs’ pre-acquisition process, including why and how the pre-acquisition process proceeds.

Acquisitions of Academic Spin-Offss

Academic Spin-Offs acquisitions are well suited for studying the dialectical nature of the pre-acquisition process because several challenges are particularly prevalent in this context (Fini et al., 2019). ASOs possess scientific knowledge that can complement buyers’ knowledge and contribute to higher-quality and more novel inventions (Makri et al., 2010). Hence, ASOs are attractive acquisition targets (Bonardo et al., 2010). However, assessing the potential value of ASOs and being able to efficiently convert their knowledge and technologies into value-creating innovations is challenging for several reasons.

First, the scientific discoveries within ASOs predominantly come in the form of “proofs and prototypes” (Shane, 2004, p.103), which are associated with both technological uncertainty (Lubik & Garnsey, 2016) and market uncertainty (Gruber et al., 2013). To commercialize such scientific knowledge, explicit knowledge alone might not suffice (Knockaert et al., 2011), and tacit knowledge from the original inventors is often required. Appraising such tacit knowledge is difficult, especially by potential buyers during acquisition (Coff, 1999; Cumming & MacIntosh, 2003).

Second and related, the early stage and innovative nature of ASOs mean that they have no financial track record and few assets and that there is a lack of comparable firms that can be used to assess their value (Bonardo et al., 2011). Hence, agreeing on a price is not straightforward because it incorporates the strategic value for the buyer, the buyer’s capability of exploiting this value, and the seller’s objectives.

Third, ASOs are typically embedded in an academic context, which encompasses different motives and goals compared to a purely commercial context in terms of, for example, the economic system (non-profit/profit), nature of work (scientific novelty/knowledge use), and output (publishing/appropriation) (Perkmann et al., 2019). Academics are involved in ASOs for a variety of reasons, including science and technology dissemination, technology development, financial gain, public service, and peer motivation (Fini et al., 2019). Thus, integrating the technologies and knowledge of an acquired ASO into the buyer’s organization poses particular challenges related to aligning the motives and goals of both parties.

These characteristics call for a better understanding of the tensions that emerge between buyers and sellers of ASOs during the pre-acquisition process.

Method

Considering the limited understanding of how ASOs’ pre-acquisition process unfolds, we use a multiple case design (Wadham & Warren, 2014) to build a process model of pre-acquisition dynamics.

Context and Case Selection

To identify acquisitions, we drew on a dataset of new ASOs established in Norway between 1999 and 2011. During this period, 374 ASOs established at Norwegian universities and public research organizations were identified through the Research Council of Norway’s FORNY program, the key governmental policy initiative in Norway supporting infrastructure for research commercialization (Rasmussen & Mathisen, 2017). All new ASOs are reported to the program annually, which limits the survivorship bias typically associated with retrospective studies in entrepreneurship (Davidsson & Honig, 2003). Because the dataset represents the full population of ASOs in Norway during the study period (Rasmussen & Mathisen, 2017), it enabled us to systematically select cases from a relevant national population.

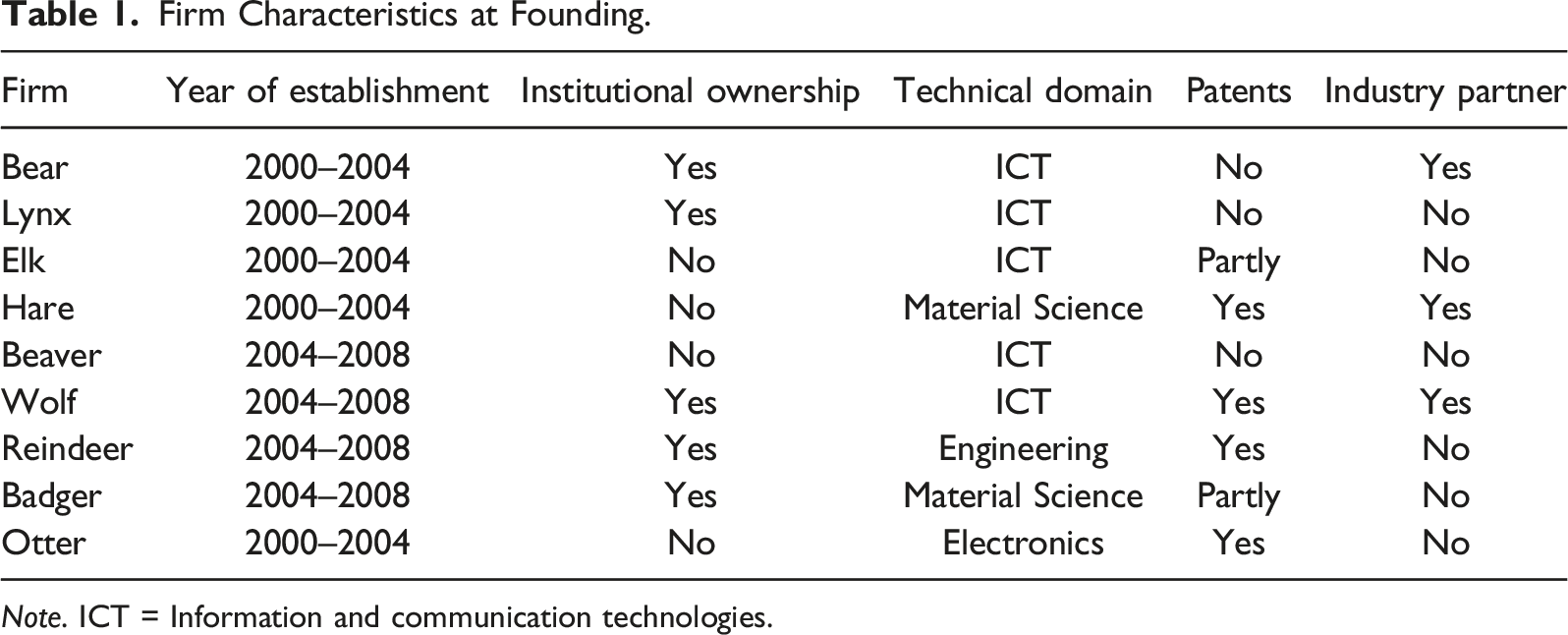

Firm Characteristics at Founding.

Note. ICT = Information and communication technologies.

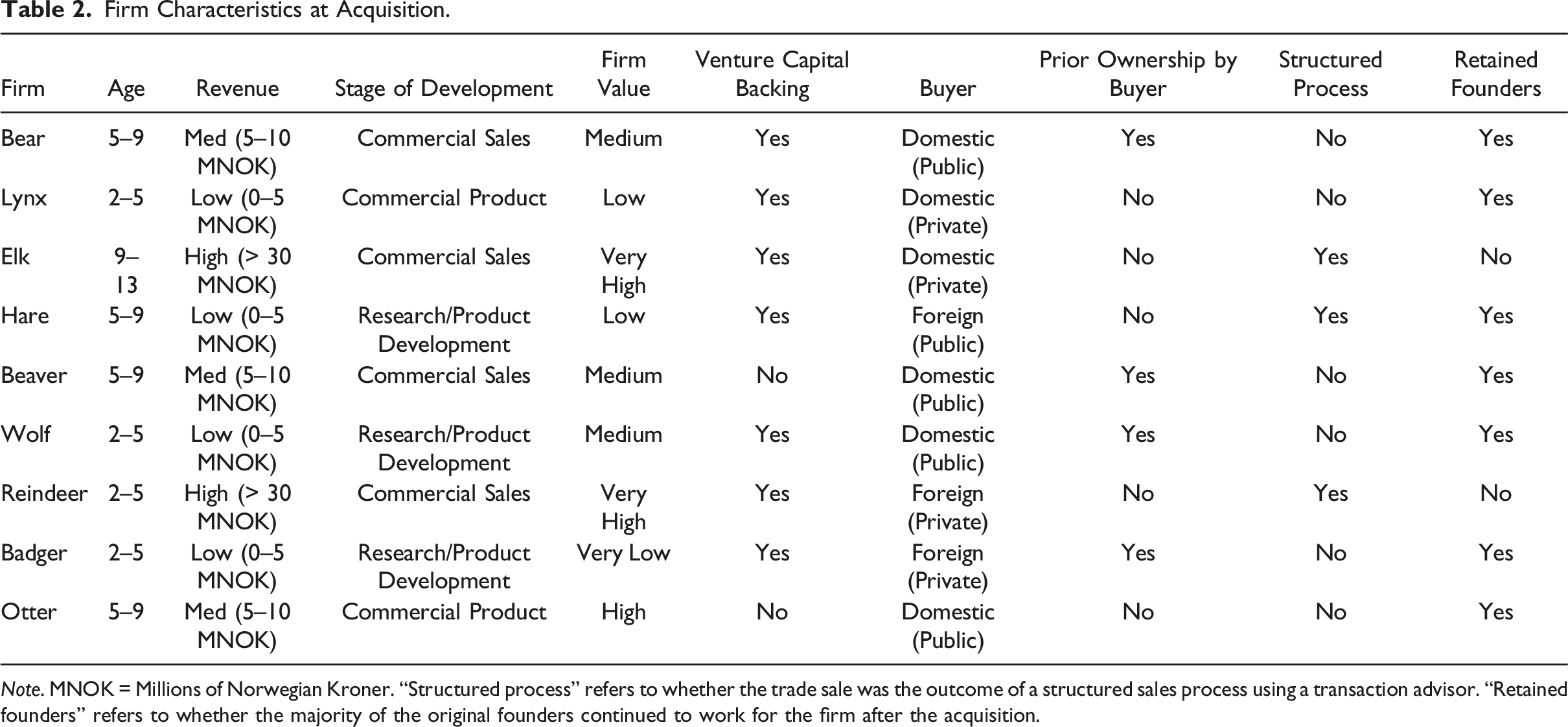

Firm Characteristics at Acquisition.

Note. MNOK = Millions of Norwegian Kroner. “Structured process” refers to whether the trade sale was the outcome of a structured sales process using a transaction advisor. “Retained founders” refers to whether the majority of the original founders continued to work for the firm after the acquisition.

Data Collection

Interviews

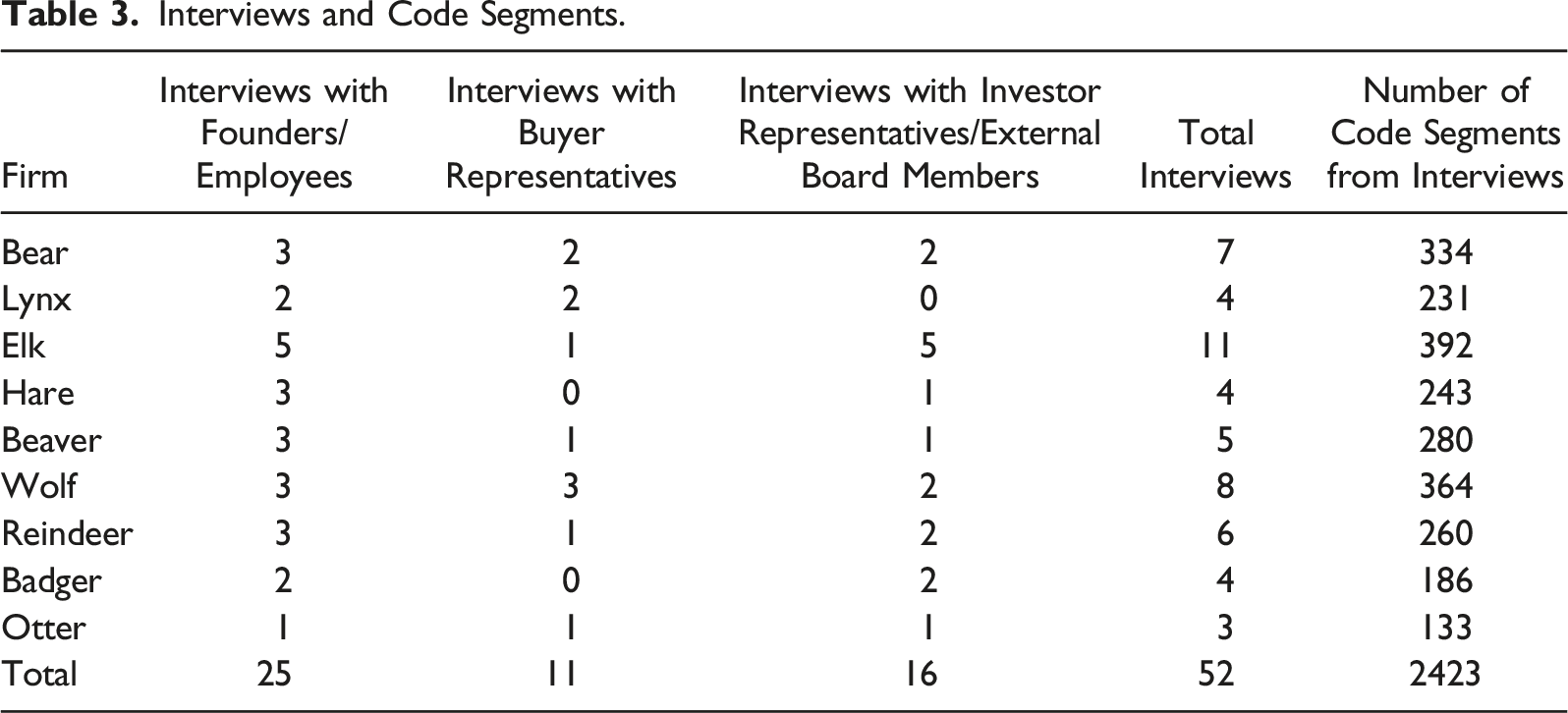

Semi-structured interviews were the main source of primary data, providing rich descriptions of the acquisition process (King et al., 2018). To minimize retrospective sensemaking, we interviewed three groups of stakeholders: founders/employees, buyer representatives, and external stakeholders. We approached relevant informants using documentary sources, always starting with the founder(s), then moving chronologically through the development process of the firm, and concluding with representatives from the buyer. Through interactions with informants, we identified new individuals to approach for interviews. We aimed to interview at least one informant from each of the three stakeholder groups, which we did, except for buyer representatives in two cases and external stakeholders in one case. The confidential nature of acquisition processes meant that relatively few individuals were involved. Therefore, in some cases, we had to rely on a few key informants, while in other cases, we stopped interviewing new informants when the last interview only added marginal new information compared to the previous one (Corbin & Strauss, 2015).

The prior literature on ASOs and technology acquisitions helped us in preparing three interview guides for the buyers, sellers, and third parties. As the interviews progressed, we continuously altered the interview guides, consistent with the constant comparative method (Corbin & Strauss, 2015). The interviews generally proceeded through three phases while also providing opportunities for informants to take detours (Suddaby, 2006). First, we covered the focal firm’s development process from founding to acquisition. For this part, we leaned heavily on our documented history of the firm (see “Secondary data” below) and focused on corroborating facts and adding richer insights. Second, we focused on the intricate details of the pre-acquisition process. Third, we covered post-acquisition events, such as integration activities.

Interviews and Code Segments.

Secondary Data

The dataset contains a range of secondary data sources, including (1) the firms’ annual reports (including board statements, detailed financial statements, and notes), (2) a comprehensive news archive with the firms’ press releases and relevant print and online news articles, and (3) all corporate announcements registered by the National Register of Business Enterprises in Norway. Corporate announcements are mandatory notices on significant events, such as legal mergers, divestments, equity changes, and CEO/board member changes. From these sources, we constructed a timeline documenting the historical development of each ASO, including a short narrative of the firm’s development and a structured overview of key events, such as commercial breakthroughs, venture capital investments, ownership changes, new subsidiaries, internationalization, and team member entry/exit. We also identified all individuals involved in each firm since its founding (i.e., board members, CEOs, employees, and owners).

Data Analysis

We build on the existing acquisition literature and extend it to the context of ASOs (Wadham & Warren, 2014). Our coding strategies are based on Gioia et al. (2013) and Grodal et al. (2020). Our inductive-abductive approach to analysis is inspired by recent editorials (Pratt et al., 2020; Van Burg et al., 2020) and papers (Erdogan et al., 2020; Farny et al., 2019; Gur & Mathias, 2021). Although we proceeded through the analysis recursively, moving back and forth between our data and the literature on acquisitions and ASOs (Locke et al., 2008), the analysis moved through three distinct phases.

Identifying First-Order Categories

The first step involved identifying informant-centric themes using “open coding” (Corbin & Strauss, 2015). We imported all the interview transcripts (preserving annotations and comments) into NVivo (version 10) and then assigned sections of informant statements to emerging themes along with relevant secondary data and notes. Unlike purely inductive approaches, we stepped back from the data and used our knowledge of the literature on ASOs and acquisitions to ask questions and search for puzzles that challenged our present understanding of the phenomenon (Grodal et al., 2020). This stepping back was important for two reasons: (1) there is an existing literature on acquisitions we could build on (although there are few studies on the pre-acquisition process) and (2) engaging in purely inductive coding of raw data removes both the processual nature and multi-level dimension from the data. Hence, we used a modified approach, which helped us not only confirm several aspects of prior knowledge (especially acquisitions) but also clearly identify those parts of the data that were unique and challenging with regard to unresolved aspects of the literature (Grodal et al., 2020; Wadham & Warren, 2014). This comparison between existing literature and data helped us divide, delete, merge, and alter first-order codes to form a manageable number of first-order categories (Grodal et al., 2020). It is important to note that the resulting first-order categories are abstracted (Grodal et al., 2020). Further, this straddling between our data and prior literature strengthened our growing recognition of the presence of tensions, which led us to separate the buyer and seller categories. The process concluded when the code structure was stable, at which point we had identified 32 first-order categories.

Developing Second-Order Themes

In the second step, we clustered our first-order categories into second-order themes to segregate and relate the categories (inspired by Gioia et al., 2013). We eventually ended up with 12 second-order themes.

Theoretical Dimensions and Data Structure

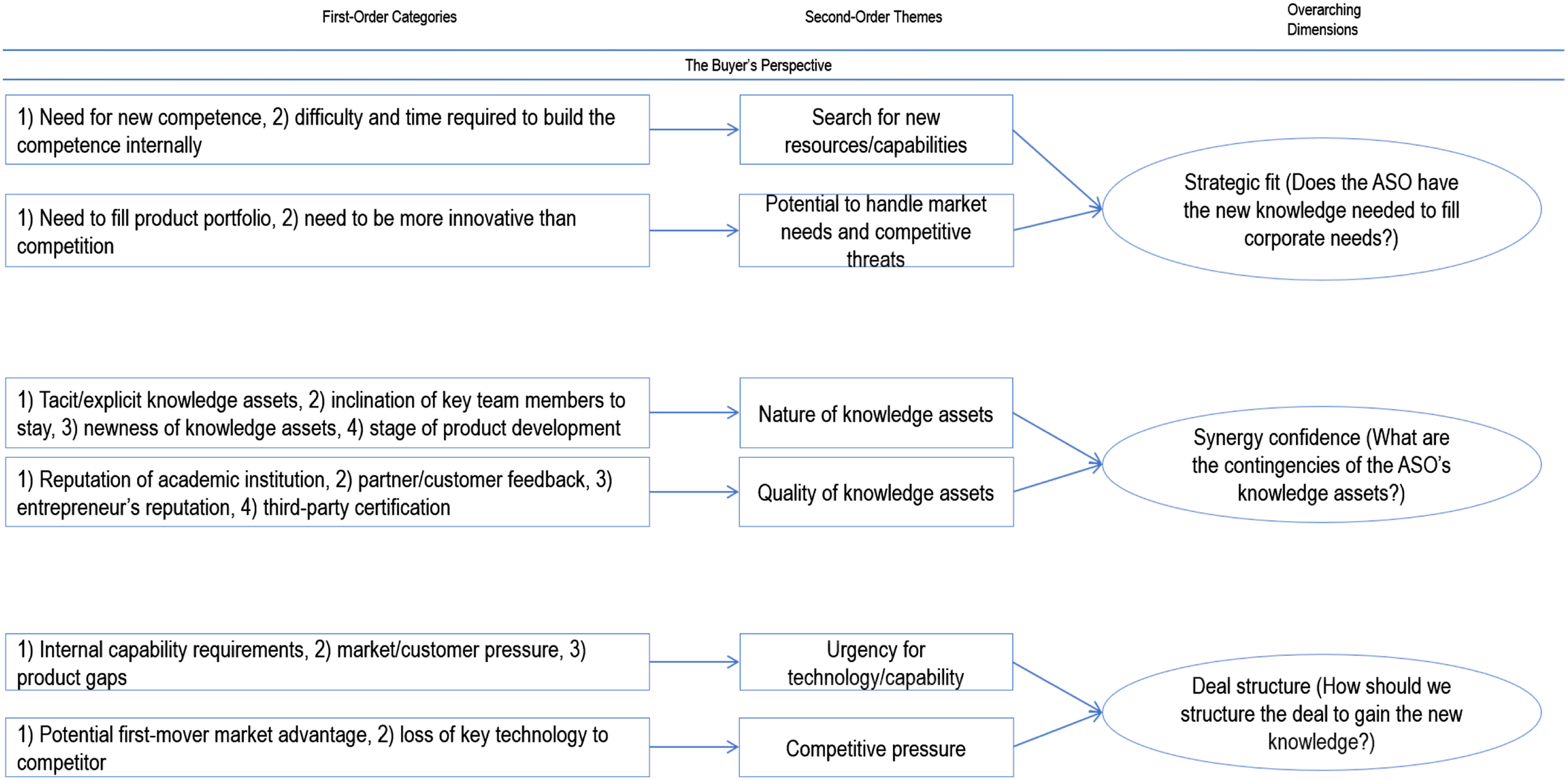

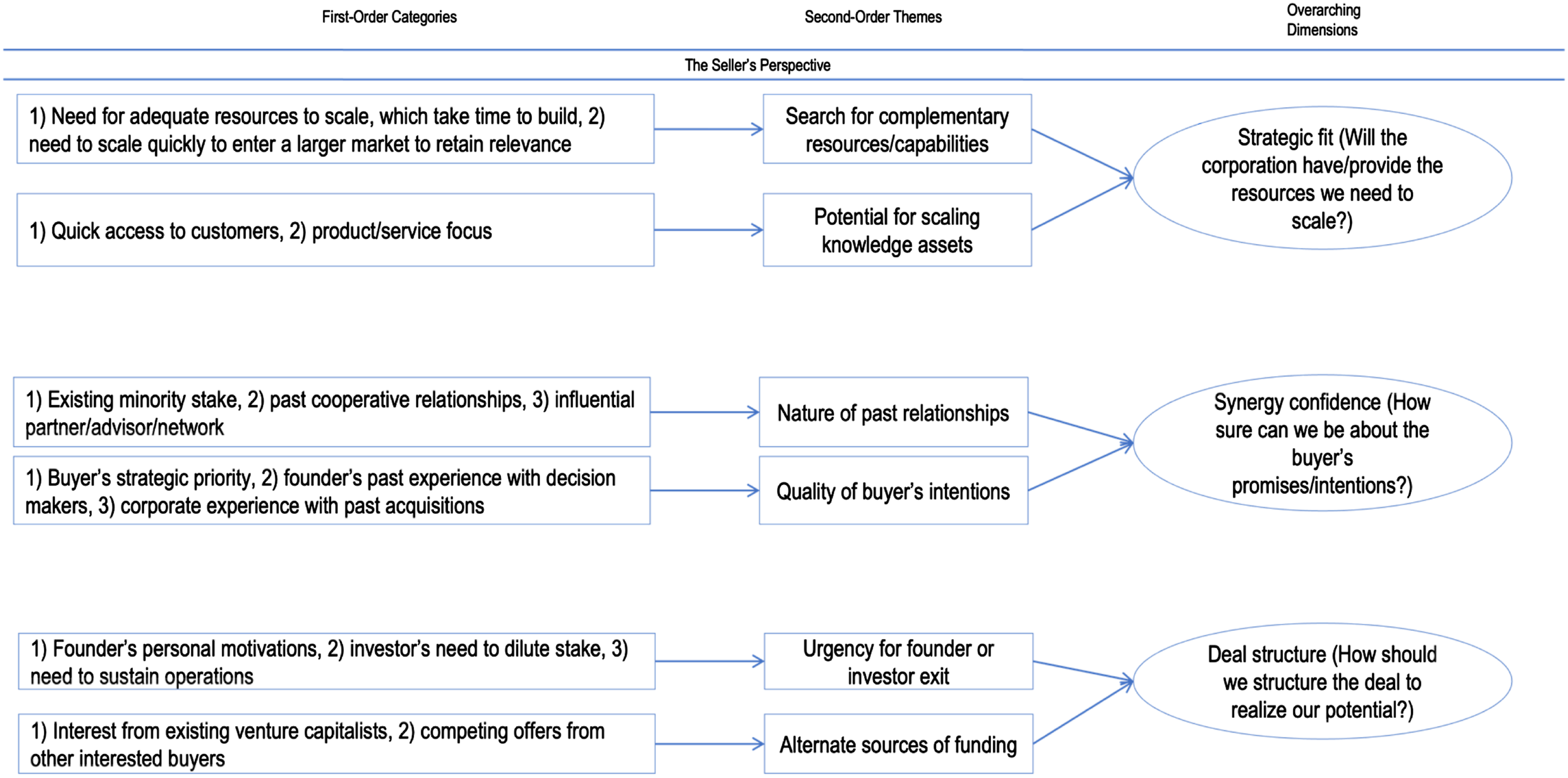

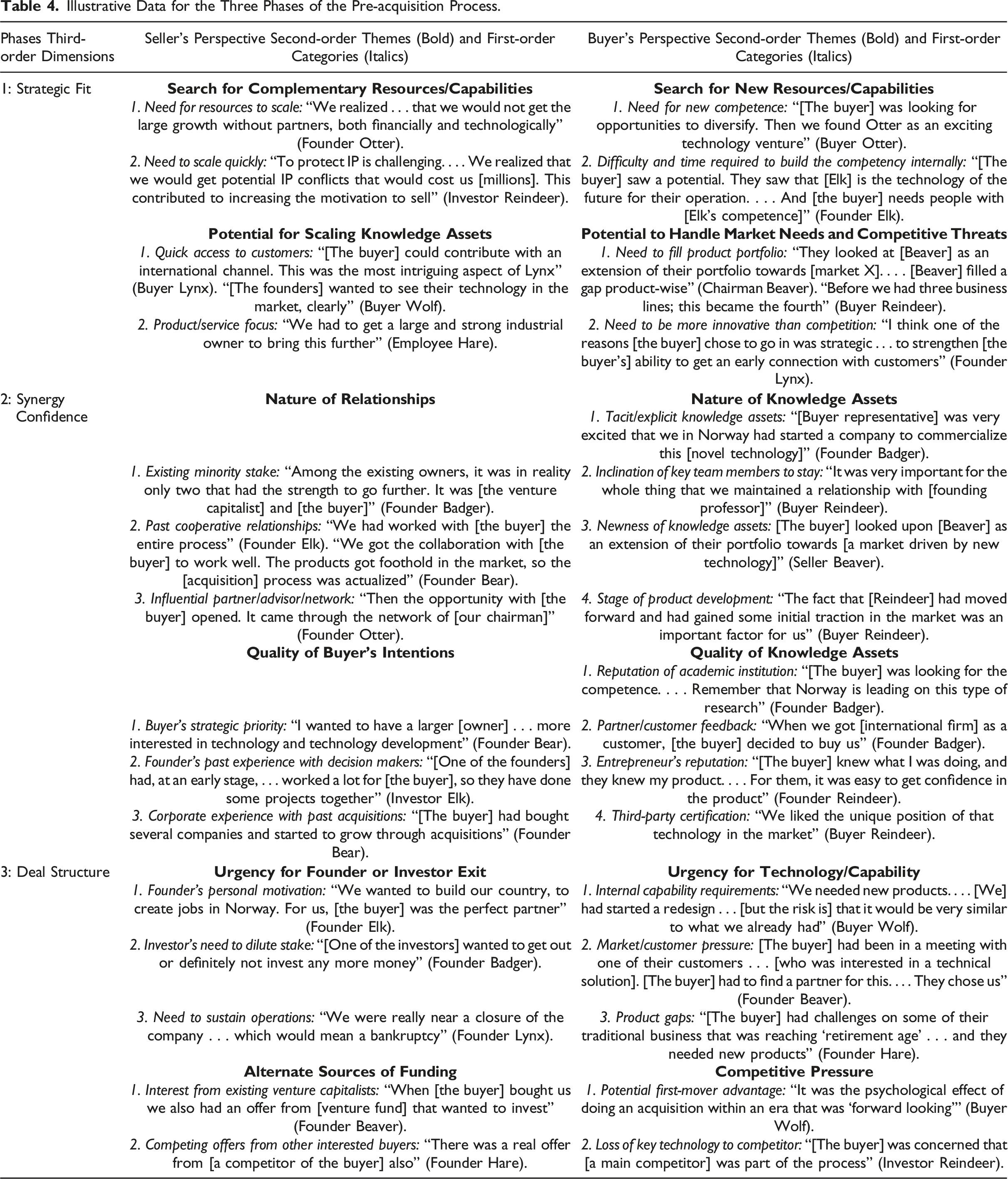

The final step involved merging the second-order themes into higher-order dimensions. Using the principles of constant comparison (Corbin & Strauss, 2015), we drew boundary conditions that helped us group the second-order themes into overarching conceptual dimensions. Our analysis pointed to three distinct dimensions in the pre-acquisition process related to strategic fit, synergy confidence, and deal structure. We present the data structure, an artifact of the inductive coding, in Figures 1 and 2 along with example quotes for each coded category from both the buyers and sellers in Table 4. Data structure—The Buyer’s perspective. Data structure—The Seller’s perspective. Illustrative Data for the Three Phases of the Pre-acquisition Process.

From Data Structure to a Process Model

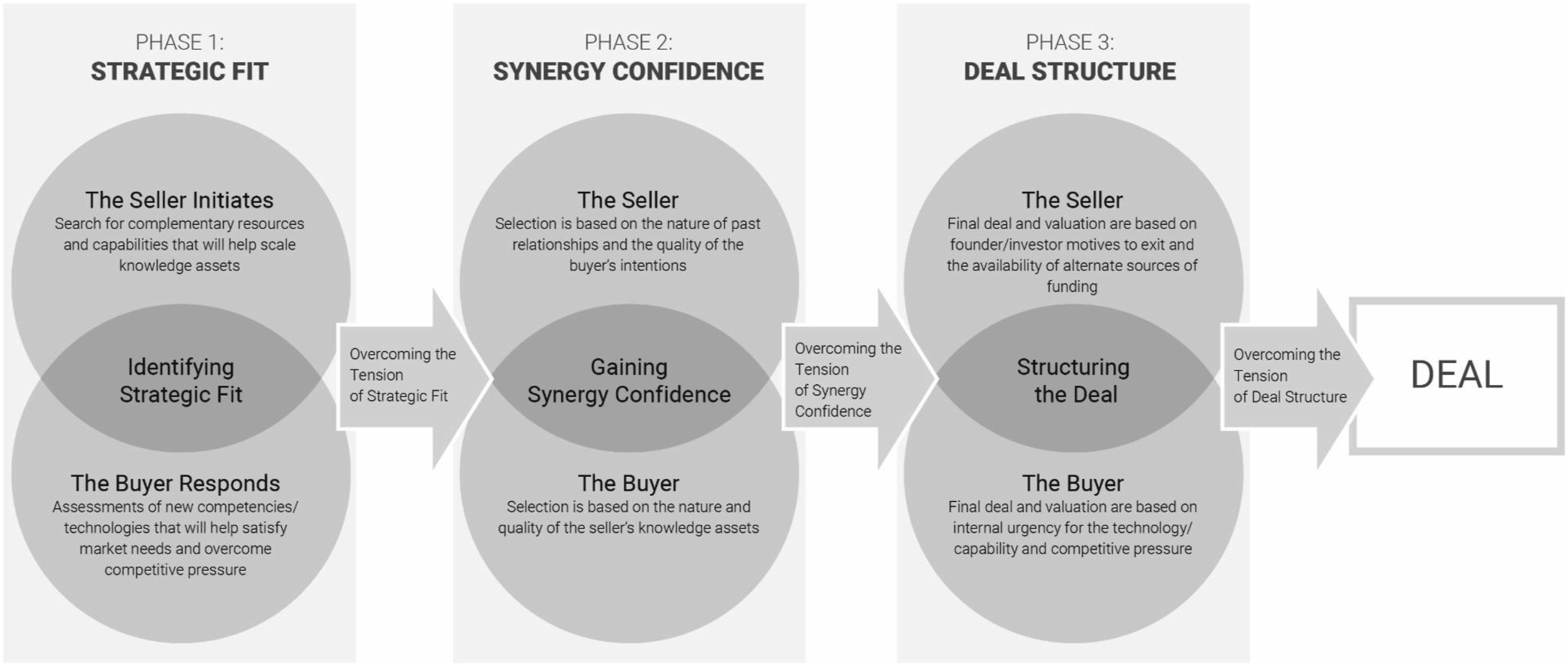

Since the data structure (see Figures 1 and 2) is not a causal model but the outcome of an analytical process (inspired by Gioia et al., 2013), it does not depict the dynamism of the phenomenon. We used “relating,” a common move used by qualitative researchers, to identify relationships among emerging conceptual categories, themes, and dimensions (Grodal et al., 2020). Hence, harnessing our proximity to the data and the analysis, we arranged the various themes and dimensions from the data structure to form a process model with boxes and arrows (Corbin & Strauss, 2015). We noticed that both the buyers and sellers were concerned with specific issues throughout the process related to strategic fit, synergy confidence, and deal structure but with partly opposing perspectives. It was during this relating process that we realized the dialectical nature of the pre-acquisition process. In subsequent iterations of the analysis, we used the dialectics literature to build the process model. Doing so enabled us to gain deeper insights into the underlying tensions the buyers and sellers experienced. We saw that both the buyers and sellers were able to overcome these tensions in a step-wise process until the deal was closed. We revisited the data and explored how these tensions were overcome in each phase. The resulting process model, presented in Figure 3, provides a more dynamic representation of the pre-acquisition process as it unfolds. Three-phase process model of the pre-acquisition process.

Findings

Summary of Oppositions, Unities, and Tensions in the Pre-acquisition Process.

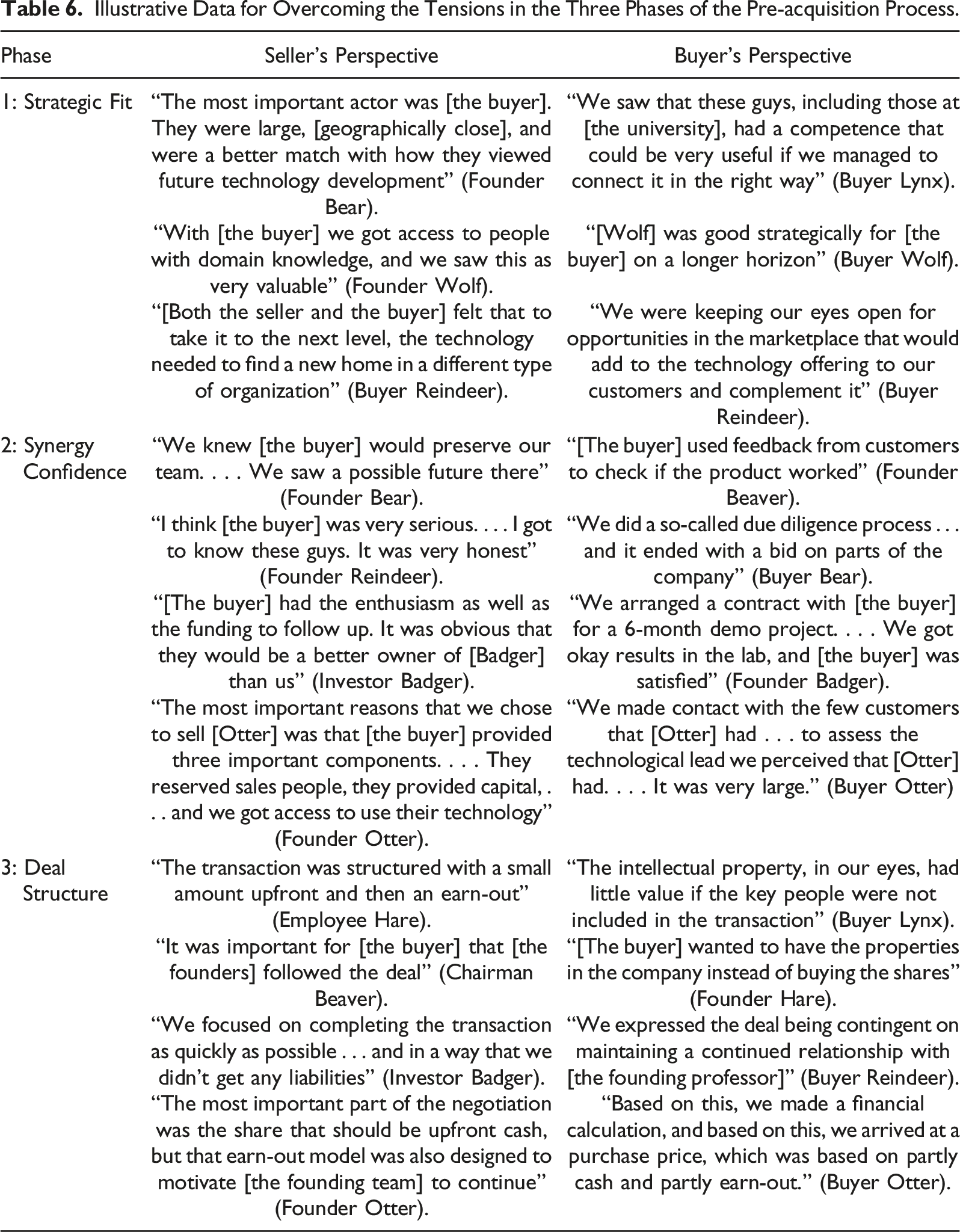

Phase 1: Strategic Fit

Strategic fit is the first phase of the pre-acquisition process. In our context, the sellers typically initiated the process by considering potential buyers, and the buyers responded with differing and, at times, conflicting expectations, resulting in an underlying dyadic tension.

The Seller’s Perspective

The ASOs in our study started to consider potential buyers for two main reasons. First, their lack of adequate resources and capabilities for scaling drove the ASOs to search for complementary resources. In most cases, these resources and capabilities were related to manufacturing, marketing, sales, and distribution—functions that most incumbents have. The ASOs acknowledged the lengthy amount of time it would take to build these resources and capabilities themselves. For example, one of the founders of Badger captured this need: “If we succeed, and when our technology is mature, [the buyer] would be the manufacturer of these [end products]. And then we are talking about scaling to enormous volumes.” This requirement also resonated in the views of an investor in Badger, who, when referring to the buyer’s manufacturing capabilities, explained, “[The buyer] had ‘the key’ that could make the technology work commercially. [Badger] could not do this alone.”

Second, the ASOs started to explore potential buyers because they needed to scale their knowledge assets. The ASOs’ principal asset was scientific knowledge, and the founders wished to realize the full potential of their unique knowledge base. This realization would require becoming part of larger product offerings and gaining early access to key customers and markets—all of which large organizations could easily enable. As stated by an employee in Hare, “We knew it had enormous potential. . . . Our product would increase efficiency very early in the value chain, so it would have a ‘multiplier’ effect. We were just not there yet, far from it.”

The Buyer’s Perspective

In response to the ASOs’ initiation of the process, the buyers became engaged for two main reasons. First, their need for new resources and capabilities made it interesting for the buyers to assess the ASOs. These internal needs arose from the buyers’ lack of competence to fulfill new requirements or address new trends. While some of the buyers could build the needed resources or capabilities themselves, they concluded that developing them would be slower and costlier than buying them. They also feared that building resources and capabilities in-house could delay their market entry and eventually cause them to lose out to competition. At times, the ASOs’ competence was also difficult to develop internally or gain from the market, as highlighted by a key employee in Elk: “They acquired the opportunity to fill a competence gap they had. Even with [a large number of] employees, they still have a gap when it comes to [Elk’s expertise].”

Second, the market and competitors also prompted the buyer organizations to assess potential ASOs. Customer feedback revealed gaps in the buyers’ product portfolios and led to both the need for new products and/or technologies and an increasing urgency to procure them. This customer aspect was captured in the following quote: The basic strategy of our business is . . . that customers can buy several products from us and preferably that these products are reasonably well integrated functionally. . . . We wanted to obtain more products for our larger product offering and leverage that for our customer base. (Buyer Representative, Bear)

This practice of buyers purchasing ASOs to fill gaps in their product portfolios was made explicit by the founder of Wolf: “We filled a gap in [the buyer’s] product portfolio.”

Overcoming the tension of strategic fit

During the strategic fit phase, buyers and sellers undertake their own, possibly functionally opposing, assessments of potential synergy. While sellers are interested in the possibility of scaling their knowledge assets through access to complementary resources, buyers explore if the knowledge resources up for sale are the right fit to either fill holes in their portfolios or, in the case of cutting-edge knowledge, gain an advantage in the marketplace. Assessing strategic fit requires both parties to acknowledge their own needs and assess if the other is the right partner to realize these needs, which leads to an inherent tension for both buyers and sellers. Despite the functional opposition (i.e., scale and technology), both parties attempt to identify the interactive unity in opposition (i.e., potential strategic fit), which results in a dialectical tension that needs to be overcome to move to the next phase.

Illustrative Data for Overcoming the Tensions in the Three Phases of the Pre-acquisition Process.

Phase 2: Synergy Confidence

In the second phase the buyers and sellers assessed each other’s intentions and capabilities regarding potential synergy differently, which led to tensions regarding synergy confidence.

The Seller’s Perspective

The ASOs gained confidence in potential buyers based on two main factors. First, past relationships or partnerships, either in the form of minority stakes or past collaborations, heavily influenced the ASOs’ confidence. Although the ASOs clearly benefitted from having industrial partners that provided resources, these relationships also limited their ability to attract other potential buyers. In three of the cases, the firm that later became the buyer had a minority equity position in the ASO. This situation appeared to be both a blessing and a curse—each of these ASOs got support from a large organization but was cut off from other potentially more valuable buyers. As the chairman of Beaver noted, “Although we tried to keep [industrial partner] at arm’s length, they eventually maneuvered themselves to take over the company in the end.”

Second, the quality of potential buyers and their intentions were carefully assessed by the ASOs. A potential buyer’s strategic priorities provided an indication of how the ASOs would be treated after the acquisition. When the ASOs noticed a specific and strong fit with a potential buyer’s intentions, it increased their confidence, as expressed by the CEO of Hare: We fit hand in glove into the product portfolio that [the buyer] had at their factory in [a European country]. They needed a new business to grow on. [Hare] fit right with their production and market. They were already into the [specific] industry and wanted to get a product based on [our technology].

In addition, the ASO founders’ past relationships with potential buyers helped them assess these buyers’ intentions. For example, the relationship between Lynx’s buyer and one of its founders went back many years, as a buyer representative explained: “It goes back to when [the founder] worked for us back in the ‘90s. We knew him as a very skilled person who was involved with building our [critical technical] system.” Information about potential buyers’ past acquisition experience also influenced the ASOs’ synergy confidence. For example, the CEO of Beaver said, “[The buyer] wanted to be on [our technology platform]. They also bought [another company].”

The Buyer’s Perspective

The buyers evaluated potential ASOs based on both the nature and the quality of their knowledge assets. First, ASOs are based on new knowledge, which may have both tacit and explicit components. The nature of ASOs’ knowledge assets was a key criterion for the buyers in pursuing a potential acquisition, as reported by a buyer representative of Lynx: You can have patents and software, but early on, they have limited value without the people who developed them and understand the complexity of them. This is always the situation in knowledge-based businesses, where knowledge generally is tacit in my experience. . . . You might be able to document 20%, while the rest remains tacit.

If an ASO’s activity relied on a high degree of tacit knowledge, the buyers had to be confident that the ASO’s key technical personnel would commit to staying with the firm after the acquisition. This criterion was remarkably consistent, and the buyers generally stated that the transactions would not proceed without meeting this condition. For example, a buyer representative of Wolf explained, “The people had to stay; the company would be worthless to us without them.”

Second, when considering an ASO, it was important for the buyers to assess the quality of the new knowledge and technology being developed by the ASO. One indicator of quality the buyers paid close attention to was the reputation of an ASO’s entrepreneur(s). As an investor representative of Badger explained, “It was the link between [the buyer representative] and [the inventor] which was key here. . . . He was himself a technology guy and was very impressed with [the inventor] being an authority on this subject area internationally.” Another indicator of quality was an ASO’s technical certifications. For instance, a buyer representative of Wolf commented, “We found out they had received a [technical] certification from [an important industry player], and that carried a lot of weight. That provided significant value.” Moreover, an ASO’s ability to obtain market acceptance through early customer sales was also important for increasing the buyers’ confidence, as reflected by a buyer representative in Bear: “The technology was already in good shape . . . products are already in the market. The customers have accepted the product, and it only needs modifications for particular conditions.”

Overcoming the Tension of Synergy Confidence

During the synergy confidence phase, buyers and sellers individually assess their confidence in realizing the potential synergy they identified in the first strategic fit phase. Buyers are wary of the nature and quality of sellers’ knowledge assets, and sellers are wary of past relationships with buyers’ and their intentions. The presence of a functional opposition between buyers and sellers and an interactive unity leads to the underlying dialectical tension of synergy confidence, which the two parties attempt to overcome in different ways. On the one hand, buyers assess the nature and quality of ASOs’ knowledge assets often with the help of a formal “due diligence” process. The confidence buyers derive from these assessments drives their decisions to enter further negotiations with ASOs, as explained by Wolf’s Buyer: “[The CTO] and a couple from his team were [visiting Wolf]. Spent a day with the founders and gained ‘comfort.’” On the other hand, ASOs are influenced by their past relationships with incumbents and their beliefs about buyers’ intentions, reputation, and trustworthiness. ASOs engage with potential buyers based on how much confidence they have that the relationship will help them realize their potential, as exemplified by the chairman of Elk: “We perceived [the buyer] as a ‘good home’ for [Elk] . . . that could create the basis for further development and growth of the concept.” This confidence assessment requires both parties to acknowledge similarities and differences in their motives and priorities and leads to an inherent tension for both buying organizations and selling ASOs.

In contrast to Phase 1, Phase 2 was longer and involved numerous interactions whereby the buyers and sellers relied on both formal and informal approaches to overcome the underlying tension of synergy confidence. Example approaches include due diligence, certification, past relationships, and trusting networks. Progress to Phase 3 happened only when both the buyers and sellers were reasonably confident that the expected synergy could be realized.

Phase 3: Deal Structure

The third and final phase is deal structure. As the buyers and sellers attempted to achieve their main objectives, an underlying tension of how to structure the deal emerged.

The Seller’s Perspective

The ASOs’ acceptable deal structure was driven by two very different factors than those of the buyers. First, the decision to accept deal terms was related to the urgency to exit of the founder(s) and/or investor(s). ASO owners, particularly venture capitalists, can be eager to exit their investments. In several cases, there were conflicts between the founders and investors in the ASOs related to when and how a sales transaction should be initiated. In one case, the venture capital investor initiated a structured sale process just after the ASO had finalized a commercial product but before any commercial sales had taken place. Potential buyers did not meet the investor’s value expectations, and the process was eventually stopped. Acting in a rushed manner was counterproductive when attempting to maximize value. As the transaction advisor for Elk commented, “12 months is not atypical when dealing with a technology-based firm. . . . It takes time to get all potential buyers in line.” Further, the sellers’ financial situations sometimes created urgency. Three of the ASOs in our study needed funding quickly to sustain their future development.

The second factor influencing what deal terms the ASOs accepted was the availability of alternate sources of funding, such as venture capitalists and competing buyers. Seven of our cases had raised institutional venture capital at some point. In two cases, the ASOs had negotiated term sheets from new venture capitalists as an alternative to acquisition. A buyer representative of Wolf elaborated, “[The seller] thought we were too conservative in pricing. The message that was communicated to us was that they had another option with [a venture capital firm].”

The Buyer’s Perspective

The buyers arrived at an acceptable price and deal structure based on two main factors. First, the most important factor influencing price was the buyers’ perceived urgency to obtain a technology or capability. We found that urgency arose from both internal and external sources. The buyers sometimes found it too risky to develop the relevant knowledge assets internally because the competencies were new, unique, and unavailable in the market. As the chairman of Beaver commented, “[The ASO] represented a brand-new set of competencies for [the buyer].” Even when the buyers considered purchasing the new technical competencies, the ASOs often had specialist knowledge that was difficult to obtain in the market. As a buyer representative of Wolf explained, This knowledge is very difficult to obtain. I am hiring people with a similar profile at the moment. . . . We found nobody in Norway. I had to search across Europe, and we found one in Belgium and one in Poland. And they were not even on the same level as [the founders], but they could be trained. We are talking about unique competence.

Second, the price the buyers offered for an ASO was influenced by competitive pressure. Specifically, the buyers needed to ensure they were ahead of their competitors. Except for one case, the buyers publicized their acquisitions through press releases and promotional materials. They used the opportunity to signal to the market that new products would soon be available. As a buyer representative of Wolf explained, “It was actually external pressure from our customers. . . . I also think it was extra influential that we acquired the firm. It would have been a weaker signal to the market if the team had been employed and done the development internally with us.” Some of the buyers were also concerned that the ASOs’ technologies would end up with competitors. This concern translated into a willingness to increase the valuation and close the deal. For example, a key employee in Elk reasoned, “Despite robust strategic rationale for doing the acquisition, the threat of a competitor getting control over us surfaced as a driver in the process.”

Overcoming the tension of deal structure

During the deal structure phase, buyers and sellers must identify a price range within which they will enter a transaction and a deal structure that satisfies the interests of both parties. Buyers seek to close a deal at the lowest price and with deal terms securing their interests (e.g., retain founders’ competencies, reduce liabilities and risks), which may contrast with sellers’ expectations to receive the highest price and favorable deal terms (e.g., buy out investors, secure future operations and employees). On the one hand, buyers consider how urgently they need the focal technology/capability and how much competitive pressure they face. On the other hand, ASOs consider their own urgency to exit (founder and/or investor exit) and the availability of alternate funding sources (especially venture capital) to negotiate attractive offers. ASOs also have other dilemmas to handle, particularly founder-investor conflicts.

In our cases, overcoming the tension of deal structure was central for successfully closing a deal. In contrast to Phases 1 and 2, in Phase 3, both the buyers and sellers relied on more formal approaches to overcome the underlying tension. The buyers often used various forms of earn-out models (e.g., investors were bought out; founders were retained with the option to sell their equity after a set period of time) to share risk and incentivize the founders to continue. As explained by the buyer of Wolf, “[We] created incentives for the key personnel in Wolf. . . . We had stay-on bonuses that made it possible to secure the competence.” Therefore, to finally conclude the pre-acquisition process and complete a deal, the buyers and sellers needed to identify a mutually acceptable price and terms that satisfied both parties.

Discussion and Implications

By examining ASOs’ pre-acquisition process and focusing on how the tensions between buyers and sellers are overcome, we extend theory on the elongated courtship period prior to an acquisition event (Welch et al., 2020). We show that the pre-acquisition process progresses through three distinct phases: strategic fit, synergy confidence, and deal structure. We also uncover one dialectical tension between the buyer and seller that has to be overcome in each phase. The ability to overcome one tension appears to be a necessary condition for progressing from one phase to the next and ultimately to a completed acquisition event. As such, we propose a novel dialectical process model (Hargrave & Van de Ven, 2017; Rasmussen, 2011) explicating the scarcely studied pre-acquisition process (see Figure 3 and Table 5).

The first dialectical tension revolves around how buyers and sellers identify mutual strategic fit. In our study, the ASOs were looking for a buyer that could help commercialize their technologies and knowledge. This meant they sought only a few potential industrial buyers. The buyers responded when they were seeking to add to or extend their capabilities with those the ASOs potentially had. Therefore, strategic fit with their current operations was essential for the buyers’ interest in considering an acquisition. Structured search, informal networks, and past relationships were the primary approaches used to overcome the tension of strategic fit.

The second tension revolves around how buyers and sellers gain confidence to realize the potential synergy. This was important because the potential value of the acquisitions depended on successful integration of the buyers’ and ASOs’ technologies and competence. Therefore, the technical and business-related pre-conditions needed to be assessed and the intentions of both sides revealed so that the tension related to integrating two different firms could be overcome. This phase of the pre-acquisition process was relatively time consuming. Due diligence, certifications, scientist reputation, and customer validation were used to overcome the tension of synergy confidence.

The third and final tension revolves around how buyers and sellers arrive at a mutually acceptable deal structure. The diverging interests of the sellers (e.g., funding needs, founders’ and investors’ exit needs, employee retention) and buyers (e.g., financing, corporate strategy, technical operations) made it necessary to negotiate a deal that would satisfy multiple interests. A variety of deal structures were used to satisfy both sides; however, this phase was relatively short and formal. We particularly noticed the use of the “earn-out model” to overcome the tension of deal structure.

Our dialectical process model extends the literature on acquisitions of entrepreneurial ventures in several ways. First, building on the courtship view of acquisitions (Graebner & Eisenhardt, 2004) and taking a dialectical perspective, we unpack the elongated courtship period—specifically, the phases of the pre-acquisition process in the context of early stage privately held ASOs—and highlight the key tension between the buyer and seller in each phase (Graebner, 2004; Shen & Reuer, 2005; Welch et al., 2020). We add to prior research focusing on one side of the relationship (e.g., buyers [Coff, 2003] or sellers [Graebner & Eisenhardt, 2004]) or on one dimension of the relationship (e.g., trust [Graebner, 2009]) by providing a theoretical explanation of the pre-acquisition dynamics over time that unites both the seller’s and the buyer’s perspectives. Our model also addresses the call to synthesize multiple findings over time to provide a more holistic picture of the pre-acquisition process (Haleblian et al., 2009). For instance, our study confirms that factors like engaging investment advisors, developing trust, and designing retention/earn-out models are used to overcome the tensions in the pre-acquisition process. However, these factors do not come into play at the same time but arise at different phases of the pre-acquisition process and help overcome specific tensions between the two parties. Hence, we believe our process model contributes to the present understanding of why acquisitions take time, how different factors influence different phases of the process (Welch et al., 2020), and what leads to agreement between buyers and sellers.

Second, our process model deepens the theoretical foundations of the relatively sparse pre-acquisition literature, which is predominantly variance driven (Welch et al., 2020) and explores acquisition outcomes (Ahuja & Katila, 2001). Our findings show that pre-acquisition tensions are related to common challenges experienced during post-acquisition integration (Graebner et al., 2017; Trichterborn et al., 2016). By unpacking the elongated pre-acquisition process (Graebner & Eisenhardt, 2004), we add to the current emphasis on post-integration activities as the basis for acquisition success (Ranft & Lord, 2002), arguing that the process preceding a deal needs more attention. Hence, many of the challenges typically arising during post-acquisition integration can be better addressed and overcome, at least partly, prior to an acquisition event.

Third, considering the increased volume of acquisitions of early stage privately held entrepreneurial firms (Capron & Shen, 2007; Renko et al., 2020), particularly ASOs (Woolley, 2017), our study sheds light on an important but relatively neglected pathway (i.e., acquisition) for commercializing scientific research (Fini et al., 2018). ASOs typically have long development paths before becoming commercially viable firms, and they often encounter difficulties in building capabilities in manufacturing, distribution, and marketing. Hence, acquisition has become a feasible path for ASOs to overcome these difficulties and realize their potential (Renko et al., 2020). However, the academic entrepreneurship literature predominantly looks at the conditions necessary to establish and grow independent ASOs (Mathisen & Rasmussen, 2019), which may entail distinct processes and competencies compared with reaching the market through industrial acquisition. Hence, our findings provide several insights for entrepreneurs and owners of ASOs on how to manage the complex process and associated tensions preceding an acquisition event (Bonardo et al., 2010). For instance, we find that the knowledge intensity of ASOs makes it important for buyers to encourage key employees to stay after an acquisition. While the reliance on tacit knowledge may be particularly strong for ASOs, this finding has implications for other knowledge-intensive entrepreneurial firms, other negotiation processes, and post-merger integration in general (Graebner et al., 2017; Welch et al., 2020). Moreover, the literature on science commercialization and academic entrepreneurship predominantly focuses on acquisitions of ASOs that are publicly listed (Bonardo et al., 2010; 2011; Meoli et al., 2013; Woolley, 2017). Since acquiring public firms is very different from acquiring private firms (Capron & Shen, 2007), our study adds novel insights into the rarely studied process of early stage privately held ASO acquisitions (Mathisen & Rasmussen, 2019).

Limitations and Implications for Research

Several limitations and future research implications should be noted. First, we investigated a process for which empirical data is hard to access. As emphasized by our model, it takes time for a buyer and seller to build trust, and the process involves confidential information that both parties are reluctant to share. Thanks to the availability of population-level data on ASOs in Norway and the strong network of one of the authors, we were able to identify and access an adequate number of cases to shed light on the pre-acquisition process. However, the use of retrospective interviews may have led to recall biases, and the findings may be partly context specific. Hence, future research is needed to validate our findings. Moreover, we did not study unsuccessful instances of the pre-acquisition process. Empirical investigations of failed pre-acquisition processes would help clarify how and why firms are able to or fail to overcome the specific tensions arising between buyers and sellers. Finding opportunities to engage in longitudinal studies or an ethnography (e.g., following the process from pre-acquisition to post-acquisition integration) could yield important insights.

Next, the context of our study—namely, ASOs spun out of universities and public research institutes and acquired at an early stage—may limit the generalizability of our findings to other contexts. Moreover, all our ASO cases were from Norway, a country with a limited public market for small and new technology-based firms, making initial public offerings less attractive. However, the majority of ASOs in our sample were operating in an international market, and several of the buyers were from other countries, indicating that the pre-acquisition process is relatively universal and common across contexts (Renko et al., 2020; Woolley, 2017).

Theoretically, using a dialectical perspective puts the key actors—in our case, buyers and sellers—in focus. While this theory provides a parsimonious description of the pre-acquisition process, it may exaggerate the role of buyers and sellers compared to external factors. Hence, we see tremendous potential to study the influence of contextual factors in the acquisition process. Acquisitions are influenced by several external factors, so studying these factors is critical to advance contingent models of acquisitions.

Furthermore, we did not systematically follow the post-merger integration process or overall performance of the acquisitions. However, our findings point to strong links between the pre-acquisition tensions and issues that arise after a deal is complete, as discussed in the literature on post-integration. Future research could extend our process model to explore how the post-integration process is influenced by pre-acquisition and whether it proceeds in similar dialectical phases. Such research could lead to a more holistic understanding of the entire acquisition process that incorporates the activities both before and after a deal is closed. For instance, researchers can study how different strategies implemented to overcome pre-acquisition tensions influence post-merger integration success.

From a practice perspective, we believe future research can help ASOs learn how to find the most suitable partners for growth through acquisition and when is the best time to get acquired, and it can help buying organizations overcome difficulties in retaining team members after an acquisition. As such, future research can perhaps explore whether buyers’ early involvement with ASOs helps with post-acquisition integration or affects the courtship period and negotiation time, how buyers can engage with ASOs during their early stages without hindering their autonomy, and whether there are alternate ways to preserve tacit knowledge other than retaining ASO founders or other key team members. Future research can also explore how these factors play out across the various phases of the pre-acquisition and post-acquisition integration processes, how founders/managers handle the associated tensions, and how their decisions to overcome these tensions affect their choice of acquisition target and eventual performance.

Implications for Practice

Managers of acquiring organizations and founders of entrepreneurial firms wishing to be acquired can use our three-phase pre-acquisition process model as a basis for identifying, engaging with, and negotiating with potential partners. Going against the popular belief that negotiation happens primarily on price after other factors have been objectively evaluated (Coff, 2003), we find that developing mutually valuable acquisition deals requires sustaining an elongated process by overcoming specific tensions that arise across the three phases (related to identifying strategic fit, gaining synergy confidence, and structuring the deal). Being aware of the functional oppositions, interactive unities, and dialectical tensions in the three phases will hopefully enable managers and founders to handle the socially complex pre-acquisition process more effectively.

Our findings also help explain why sellers do not always seek to maximize price when engaging with potential buyers. Indeed, financial valuation methods and peer valuation approaches are less relevant for agreeing on a transaction price for these early-stage firms. Therefore, managers overseeing acquisitions are left with subjective evaluation approaches to assess firms’ potential rather than relying on their historical track records and assets. Our process model emphasizes the need to engage in an elongated process to assess strategic fit and how the potential synergy can be realized before entering a discussion on deal structure.

Finally, we believe our findings have implications for the post-integration process, which often fails to realize the expected returns (Graebner et al., 2017). Our cases clearly show that pre-acquisition dynamics are not separate from the subsequent integration process but can instead be seen as an important part of the post-integration process. If a buyer and seller successfully overcome the distinct tensions of strategic fit, synergy confidence, and deal structure during the pre-acquisition process, this may decrease post-integration challenges and potentially lead to a more successful acquisition.

Footnotes

Acknowledgments

Earlier versions of this paper were presented at the University of Bologna in May 2019, at the 2019 BCERC Conference and the Academy of Management Annual Meeting 2019. We are grateful to the editor and reviewers for comments and advice that greatly benefited this paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.