Abstract

All-or-nothing necessary conditions are critical for the unfolding of subsequent entrepreneurial outcomes. A condition is necessary when an entrepreneurial outcome emerges only in the presence or absence of that condition. While a necessary condition does not guarantee the outcome, it makes the outcome possible by virtue of its theoretical necessity. We discuss the philosophical roots and importance of necessary conditions in entrepreneurship. We offer an empirical illustration of necessary condition analysis using founder’s experience, a critical concept in entrepreneurship. We argue that theory-method compatibility in entrepreneurship research can be enhanced by explicitly accounting for necessary conditions.

Keywords

Recent studies point to a critical problem in quantitative entrepreneurship research—a recurrent mismatch between the principles that undergird our popular analytical tools and the phenomena we study (Yang & Aldrich, 2012; Crawford et al., 2015; Douglas et al., 2020; Maula & Stam, 2020). For example, according to the resource-based view, performance is a function of continuous quality differentials in a firm’s value-creating resources (Barney, 1991), including in entrepreneurial settings (Alvarez & Busenitz, 2001). Thus, adopting a resource-based view, we would investigate “how many” or “to what degree” firms and startups possess these beneficial resources. By doing so, we would invoke a probabilistic perspective—where more of a predictor X (resources) leads to more of an outcome Y (performance)—that we will then test using the popular and powerful linear regression-based methodologies. 1 Linear regression-based techniques assume that effects operate in isolation, are additive (Douglas et al., 2020), and follow “Hempelian general law” like relation (Ron, 2002, p. 120). In fact, such fundamental assumptions, concepts, and metaphors undergird all our analytical tools. Therefore, when applying any methodology, we implicitly assume that its underlying notion of cause and effect also applies to the phenomenon we are studying (Gigerenzer, 1991). Disharmony between our methodology’s and our phenomenon’s cause and effect assumptions is at the root of the theory-method incompatibility problem in entrepreneurship. Our goal is to highlight necessary condition analysis and showcase how it can be leveraged as one solution to this problem.

The entrepreneurial journey is full of important milestones and crucial thresholds (Davila et al., 2003; Shepherd & Gruber, 2020). In this context, necessary conditions are all-or-nothing relationships between our explanans and explanandum—critical for the unfolding of subsequent entrepreneurial outcomes. For example, we know that success in the first venture capital (VC) financing round gives a startup the requisite resources to manufacture its product and, thus, enables the startup to go to market as a pre-condition for commercial success. In fact, the entrepreneurial journey has been described as a sequence of conditions where one leads to another (Shepherd & Gruber, 2020). As such, venture capitalists financing decisions are inherently binary because VCs either back a startup or not. Thus, success in the first VC round or the explanans becomes a necessary condition for a startup’s future success or the explanandum. Other examples of necessary conditions are—satisfying legal requirements to operate in a market, legitimacy to sell, and market disequilibrium for entrepreneurial behavior to flourish.

Necessary condition analysis offers entrepreneurship research a valuable analytical tool to identify necessary conditions that allow firms to, say, enter a market. Necessary conditions are theoretically different from what enables firms to, say, outperform peers. In other words, an entrepreneurial outcome Y cannot occur unless a necessary condition X is met. However, fulfilling the necessary condition X does not guarantee the outcome Y because necessary conditions do not imply sufficiency. Instead, condition X makes outcome Y possible by virtue of its theoretical necessity. Necessary condition analysis gives us the minimum or maximum thresholds at the periphery of the observed distribution, whereas linear regression-based methods give us the average effects. Furthermore, we offer an empirical illustration of necessary condition analysis with the Panel Study of Entrepreneurial Dynamics (PSED) II data. For our illustration, we use founder’s experience, a widespread concept in entrepreneurship. We show that necessary condition analysis can tease out the different and incommensurable effects of a founder’s experience on opportunity recognition and resource mobilization.

We make several contributions. First, we answer calls for a clear distinction between linearity and necessity (Goertz & Starr, 2003; Braumoeller & Goertz, 2000; Dul, 2016; Ragin, 2000). Second, we introduce the concept of license-to-play, defined as a theoretical argument of a necessary condition, to help researchers spot opportunities for implementing necessary condition analysis. 2 Third, we add to ongoing methodological discussions on improving the theory-method compatibility in quantitative entrepreneurship research (Douglas et al., 2020; McKenny et al., 2018). Fourth, we highlight the non-neutrality of theory and construct development during methodological applications (Abbott, 1988; Gigerenzer, 1991). When choosing any analytical tool, we make implicit assumptions about cause and effect. Inattention to those underlying assumptions can make our theory-method pairing incompatible and diminish the overall quality of our knowledge of entrepreneurship (Powell et al., 2006). Finally, we shed light on a set of important “conditions” in entrepreneurial contexts. We see a fruitful path forward for thinking more about how conditions are created and how they enable, constrain, or accelerate various outcomes in management writ large. 3

Discovery and Justification

According to the dominant realist paradigm, we create scientific knowledge by combining two distinct elements of the scientific inquiry process (Avgerou, 2013). First, we fit general observations into theories and discover new explanations; second, we justify the underlying causal mechanism we proposed (Mantere & Ketokivi, 2013). The first element is the creative part of the scientific discovery process because it consists of the genesis and invention of scientific theories and hypotheses (Albert, 1972). The second element, justification, is the analytical component of the scientific discovery process, during which we validate our speculative discoveries (Reichenbach, 1938). We make scientific progress by aligning our discovery process with our justification process (Avgerou, 2013; Mantere & Ketokivi, 2013; Reichenbach, 1938). But methodological tensions arise as we try to reconcile the subjective discovery process with the justification process rigorously (Gigerenzer, 1991).

In this regard, quantitative entrepreneurship research has commonly focused on testing and presenting empirical evidence to determine if two variables are causally related to explain entrepreneurial phenomena. But establishing whether “two variables or events are causally related” is not the same as “developing good or acceptable explanations” (Hedström & Wennberg, 2017, p. 91–92). This is an important distinction for our purpose because acceptable explanations are about causal mechanisms. 4 Let us say we have identified two distinct events—a cause X and an effect Y or the phenomenon—and we have established that X and Y are causally related. But how does X bring about Y? We may not know because establishing whether “two variables or events are causally related” is not the same as “developing good or acceptable explanations” (Hedström & Wennberg, 2017, p. 91–92). It is an important distinction for our purpose because acceptable explanations relate to causal mechanisms. 4 The causal mechanism identifies the kind of effect X has on Y (Hedström & Ylikoski, 2010) and how Y was brought about (Hedström & Wennberg, 2017). 5 Why do some individuals sense opportunities while others do not? Why do some startups scale? How do successful founders exploit opportunities? These are examples of some core questions in entrepreneurship. Such why or how questions determine what an appropriate representation of a causal mechanism (e.g., constructs or concepts) should be for it to be considered “explanatory” (Hedström & Ylikoski, 2010). While explaining entrepreneurial phenomena, quantitative entrepreneurship research commonly emphasizes testing and presenting empirical evidence to determine if X and Y are causally related. Yet many causal mechanisms can connect X and Y. Therefore, establishing X and Y are causally related is a useful but incomplete step toward opening the black box of “mechanisms linking the causes to the effects” and developing acceptable explanations (Hedström & Wennberg, 2017, p. 92). Despite an interest in causal mechanisms, popular methodologies in quantitative entrepreneurship research often fall short of uncovering the specific nature of causal mechanisms linking X and Y.

For example, we know that investors care about the geographic proximity (Fritsch & Schilder, 2008) and social proximity (Hegde & Tumlinson, 2014) of their investment targets. But there are two possibilities for the precise causal mechanisms that connect investor support and geographic/social proximity. Either higher proximity increases investors’ willingness to provide financial support (probabilistic). Or once an investment object is classified as close enough (necessity) by investors, it ends up on their shortlist of potential investment targets. The causal mechanism in this example is inherently unspecified, even when we confirm that the X and Y here are causally related. Many examples exist across quantitative entrepreneurship research, where the precise nature of the interaction between X and Y through which a phenomenon emerges is vague despite the overall methodological rigor of a study. Baron and Ensley (2006), for instance, explicitly relate pattern recognition to sensing opportunities. But readers have to infer the underlying causal mechanism. Next, Clarysse et al. (2011) highlight the influential role of the social environment on academic entrepreneurship. But the causal complexity associated with the influence of the social environment is underspecified. Another example is Mishkin’s (2021) insightful study on family firms and succession. The study notes that when there are sons available for potential ownership succession, parental investments of “money, businesses, and human capital” in the daughters in the family decreases (Mishkin, 2021, p. 6116). Consequently, in the presence of sons, the likelihood of “intergenerational transmission of entrepreneurship” from fathers to daughters also decreases (Mishkin, 2021, p. 6116). Arguably, the causal mechanism underlying such intergenerational transfers is complex and unclear.

Causal realists contend that the causal mechanism is a structural feature of entrepreneurial reality. From this vantage point, the world produces effects independent of the researcher’s mind (Gibran, 2014). The researcher’s task, then, is to develop empirically justifiable theories and hypotheses on the causal mechanisms of their interest. 6 Thus, when we generate empirical evidence, we turn a “possible mechanism to a plausible mechanism” and may eventually identify “the actual mechanism” (Hedström & Ylikoski, 2010, p. 53). Specifically, we adopt a probabilistic perspective when we argue that an event X is the cause of an event Y (or the causal mechanism driving the outcome) if—and only if—X makes Y more likely. Such likelihood-increasing properties are often called probability raisers (Gerring, 2005). But we also regularly encounter events that we regard as the cause of another had the first event not occurred, neither would the subsequent event (Bennett, 1987; Durand & Vaara, 2009). In this second scenario, event X is necessary for outcome Y. Why does this distinction between the dominant probabilistic and the lesser known necessity-based arguments matter? It matters because statistical methods are never value-free. All our methodologies are tied implicitly to our substantive assumptions about cause and effect. These implicit assumptions are critical because they inform how we investigate our observed variables and express our ideas logically or mathematically. 7

The Regression Paradigm

We take a probabilistic perspective of the entrepreneurial “reality” when using regression-based analytical techniques. Before moving to complex examples from entrepreneurship, let us look at a simple example of Formula One racing to unpack our ideas. Several conditions of a car—weight (X1), power (X2), aerodynamics (X3), and acceleration (X4)—explain the success in Formula One racing and, thus, constitute the causal mechanism. Generally, more of each condition (X

n

) raises the probability of observing the outcome of a race win (Y). Therefore, racing teams constantly strive to optimize these conditions to outperform the competition. Based on this mechanism, a Formula One race can be modeled as equation Equation (1)

Taking a probabilistic perspective, we would usually theorize how each condition (Xn) relates to Y during the discovery process. Such theorizing would result in testable hypotheses statements, like “an increase of X leads to an increase of Y.” We then test such a hypothesis with simple linear regression and associated techniques. A simple linear regression model can be formally stated as

License-to-win conditions X n are probability raisers because they can increase the likelihood of observing an outcome Y. In other words, if a firm possesses more of such decisive resources than its competitors, it will likely outperform its rivals. Thus, uncovering such conditions can give firms and startups a competitive advantage and become part of their winning strategy. Besides our introductory example of resource-based arguments, proximity for organizational learning (Mattes, 2012), network size for discovering opportunities (Arenius & Clercq, 2005), and absorptive capacity for technology sourcing (Cohen & Levinthal, 1990) are some classic examples of probability raisers in entrepreneurship and management.

License-to-Play

We know that Formula One drivers must comply with the FIA’s (Fédération Internationale de l’Automobile) safety regulations. Without adhering to the FIA safety compliance threshold, the outcome Y takes the value zero, or drivers cannot compete to win a race. Specifically, the safety compliance condition must be met before arriving at our outcome of interest Y. 9 Let us look at another example relevant to entrepreneurship. State subsidies are available for “innovative” startups in European nations such as Italy. To be considered innovative, a startup must (i) offer a market innovation and (ii) its founder(s) must hold a PhD (Fiorentino et al., 2021). Let us assume that a startup has introduced a market innovation and turn to the second criteria. Regarding the second criteria, more than one PhD in the founding team will not increase the chances of state subsidy. If it did, it would be a license-to-win condition. Instead, having no PhDs in the founding team prevents the startup from meeting the innovation condition or criteria altogether. Therefore, we argue that the requirement of a PhD in the founding team is a license-to-play, as is meeting the FIA safety regulation for Formula One aspirants.

Once a critical threshold or license-to-play is achieved, more X does not result in more Y—making these conditions fundamentally different from licenses-to-win. Also, more of a license-to-play X1 cannot compensate for the lack of another license-to-play X2. Thus, it violates the assumption of additivity embedded within linear regression-based techniques. For instance, exceeding safety regulations cannot substitute for a car’s excessive weight for an Formula One win. Similarly, startups usually lack a “necessary” level of legitimacy that established firms often enjoy, preventing startups from accessing essential resources. For such licenses-to-play, a causally symmetric relationship among the conditions of interest is neither theoretically claimed nor observable in reality. Instead, we encounter necessary conditions.

Necessary Conditions

Necessary conditions can be hypothesized as “Y only if X” (Braumoeller & Goertz, 2000). In other words, X is a necessary condition for Y if X is always present when Y occurs. Alternatively, if X is necessary for Y, then the absence of X is also sufficient for the absence of Y. The defining element of a necessary condition is the impossibility of the combination of X (0) and Y (1) (Mackie, 1965). Logically, X (0) cannot produce the outcome Y (1) because that implies a nonexistent cause generates an effect. So the combination of X (0) and Y (1) is a logical contradiction. Thus, X (0) is a sufficient condition for Y (0) (Mackie, 1965). But the presence of a necessary condition X (1) does not guarantee the outcome Y (1). Instead, it merely suggests that the outcome is possible (Braumoeller & Goertz, 2000; Goertz & Starr, 2003). A “theoretical possibility” is not logically interchangeable with probability. In the probabilistic universe, the presence of X could increase the likelihood of Y. If a condition, say adequate fuel, takes the value of zero or X (0) in our Formula One example, the outcome Y (1) or a win would be impossible. But adequate fuel in a race car does not guarantee Formula One victory. So the outcome can be either Y (1) or Y (0)—implying that adequate fuel is a necessary but not sufficient condition for racing success. Necessary conditions can be formally represented by a multiplicative rather than an additive expression (Goertz, 2003), as follows

If just one of the right-hand side conditions in equation (iii) takes the value of zero (say, X1(0) and

There are many examples of necessary conditions. If we broaden our Formula One example, we can see this apply to all types of drivers and cars. Only a few among us become elite Formula One racers, while some become lower-tier elite drivers. But most of us use a compact car for grocery runs or work commute. Different necessary conditions apply regarding fuel requirements and safety regulations based on car or driver type. 10 Specifically, while it may be evident that cars need fuel, we do not know how much fuel is necessary for each car type—presenting us with an empirical puzzle. Next, interpersonal trust for teamwork is an example of a necessary condition in management and entrepreneurship. Individuals are reluctant to cooperate without a minimum level of trust. Again, government assistance for small firms to compete in international markets, possession of an internet domain before starting an e-commerce business, legitimacy to operate in a market, and obtaining a banking license to start a bank are some other examples of necessary conditions.

Necessary conditions—or “Y only if X”—based arguments may be represented in multiple ways in our theories. For example, “X is needed for Y,” “X is critical for Y,” “X is crucial for Y,” “X is essential for Y,” “X is indispensable for Y,” “X is a prerequisite for Y,” “X is a requirement for Y,” “X is a pre-condition for Y,” “X allows Y,” “Y requires X,” “Y exists only if X is present,” “Y is only possible if X is present,” or “Y becomes possible with X” (Dul et al., 2010). These are amenable to necessary condition analysis that we will illustrate next.

Founder’s Experience: An Illustration of Necessary Condition Analysis

In entrepreneurship research, the founder’s experience is a driving force behind various important entrepreneurial outcomes (Martin et al., 2013; Marvel et al., 2016; Unger et al., 2011). Founder’s experience constitutes managerial experience, industry experience, education, and prior involvement in startup activities—all of which can equip founders with valuable knowledge, skills, and capabilities. Founder’s experience is known to help startups and entrepreneurs discover and create entrepreneurial opportunities (Alvarez et al., 2013) and exploit opportunities by enabling the acquisition of financial resources and launching new ventures (Dimov, 2010). Human capital theory (Becker, 1964) suggests that higher levels of experience lead to higher performance (Unger et al., 2011). Unsurprisingly, experience is an important evaluation criterion when applying for financing, such as loans (Zacharakis & Meyer, 2000). Consequently, we can expect that founder’s experience is a license-to-win, whereby more experience will lead to more loans. 11 Next, we turn to two critical outcomes in entrepreneurship that are contingent upon funder experience.

First, exploitation versus exploration. Exploration entails search, variation, and experimentation to generate novel knowledge recombination (Andriopoulos & Lewis, 2009). By contrast, exploitation requires efficiency and convergent thinking that can improve existing products and services. While exploration is commonly linked to developing new creative ideas that may not be contingent upon prior experience, exploitation depends on understanding solutions currently available and the existing scope for improvement. An entrepreneur’s decision to exploit an opportunity depends on her knowledge about consumer demand, the availability of necessary technologies, managerial capabilities, and stakeholder support (Choi & Shepherd, 2016). It is difficult to exploit opportunities without sound insights into existing products and how they fail to satisfy current consumer needs (Alvarez et al., 2013; Mueller & Shepherd, 2016). With more experience (e.g., industry experience or startup experience), a founder will have more knowledge to exploit opportunities. With less experience, she will be more likely to explore to accrue knowledge. Therefore, we can expect a probabilistic relationship between the founder’s experience and opportunity exploitation. So here founder’s experience is a license-to-win. More (less) experience will increase (decrease) exploitation compared to exploration of entrepreneurial opportunities.

Second, past research tells us that experience can also help founders access financial resources, such as loans (Zhang, 2011). Specifically, past research offers us reasons to speculate that the relationship between a founder’s experience and startup financing may not just be probabilistic. Banks, for example, expect a certain level of prior industry or work experience from founders to reduce risks. Experiences serve as a cue that the applicant can operate in a particular industry or market, as well as lead and manage relevant tasks and people (Beckman et al., 2007). Below this necessary threshold, financiers will be reluctant to provide loans to entrepreneurs. Industry experience, then, can also operate as a license-to-play. Without satisfying a minimum level of experience, founders will not qualify for loans. Therefore, while human capital theory in entrepreneurial contexts would suggest a probabilistic causal agency writ large (Marvel et al., 2016), past research suggests a potentially necessary condition based relationship between founders’ experience and loans for their ventures.

In sum, founder’s experience may be a license-to-play (for loans) in one context and a license-to-win (for exploitation vs. exploration) in another. With this motivation in place, we next turn to our methodology.

Methodology

We use the PSED II data for our empirical illustration. 12 Instead of new theory development, our goal is to illustrate necessary condition analysis. In this regard, the PSED II data serves several important purposes for our study. First, PSED II has been extensively used to develop and test entrepreneurship theories. Second, by using standard concepts with a long tradition in entrepreneurship research, such as the ones provided by PSED II versus a more recent or novel dataset, we can reflect on the accepted practices in our field. Third, to substantiate our claim of theory-method incompatibility in quantitative entrepreneurship, our data must mirror the field’s state of the art. Finally, PSED II contains the “modest majority” of new businesses (Davidsson, 2016). These startups have a low level of complexity and can operate from home—like daycare, real estate, and small mom-and-pop enterprises. For such businesses, venture capital is not an option. Instead, they are financed primarily with savings and loans. Also, we only consider solo founders in our study because they offer the primary source of experience for a new venture (Kor et al., 2007). To ensure our sample is homogeneous, we exclude founding teams and focus on 609 solo founders in PSED II.

Exploitation vs. Exploration (EXvEX)

We measure EXvEX using two items. The first asks whether or not “many, few, or no other businesses offer the same products or services to your potential customers?” The second item assesses if “all, some, or none of your potential customers consider this product or service new and unfamiliar?” With this operationalization, we hope to circumvent resource biases, such as the technological foundations that already exist and are commonly known to all actors. So firms do not need to explore new resource combinations and can focus on exploitation. The same rationale applies if customers are familiar with the product/service. Startups can also have a mixed strategy (Raisch et al., 2009). Thus, we also considered scenarios where a founder’s strategy might fall somewhere between exploration and exploitation. We perform post hoc analyses to ensure that our measures accurately capture differences in founders’ behavior. PSED II provides several measures that allow us to cross-check the reliability of our classifications. We find a high degree of consistency, which gives us confidence in the accuracy and reliability of our measures.

Loans Received (LOAN)

Our next outcome of interest is startup financing. To capture an entrepreneur’s ability to attract loans, we look at the U.S. dollar value of loans received by founders in our sample. With loan financing, an entrepreneur generally has complete control of her firm and has sufficient incentive to exert effort (Bettignies & Brander, 2007). So a loan provider can recognize the founder’s capability to manage the business effectively and repay the loan.

Founder’s Experience

We look at four types of experience relevant to entrepreneurship: managerial and industry experience, education, and startup experience (for an overview, see Unger et al., 2011). Our measure of managerial experience (MGNT) is based on the assumption that greater managerial experience is associated with greater human capital. This measurement is built on the number of years spent in a managerial, supervisory, or administrative role by PSED II respondents. We measure industry experience (INDU) by the number of years an individual has worked in the industry in which the new venture competes (Cassar, 2014). We include a discrete indicator for previous entrepreneurial activities or prior startup involvement (START) as a proxy for learning and knowledge acquisition through prior experience.

Education

We also consider education as an additional condition that can influence our research context. 13 Studies show that formal education is an important antecedent of successful self-employment (Robinson & Sexton, 1994). We know that education—in terms of specialization (e.g., business), level (e.g., MBA), or quality (e.g., program reputation)—may serve as a signal for the strength of an applicant and, thus, enable better access to financing (Walter & Block, 2016). Loan providers might require some formal education among the recipients to reduce default risk. If the startup fails, education may signal a loan recipient’s ability to repay a loan with income from paid employment. When applicants without a formal education are not considered for loans, a particular educational level becomes a necessary (condition) for financing. Therefore, education is potentially a license-to-play, where a minimum level must be satisfied before an outcome can manifest. We measure the highest level of education (EDU) attained by an entrepreneur.

Analysis and Findings

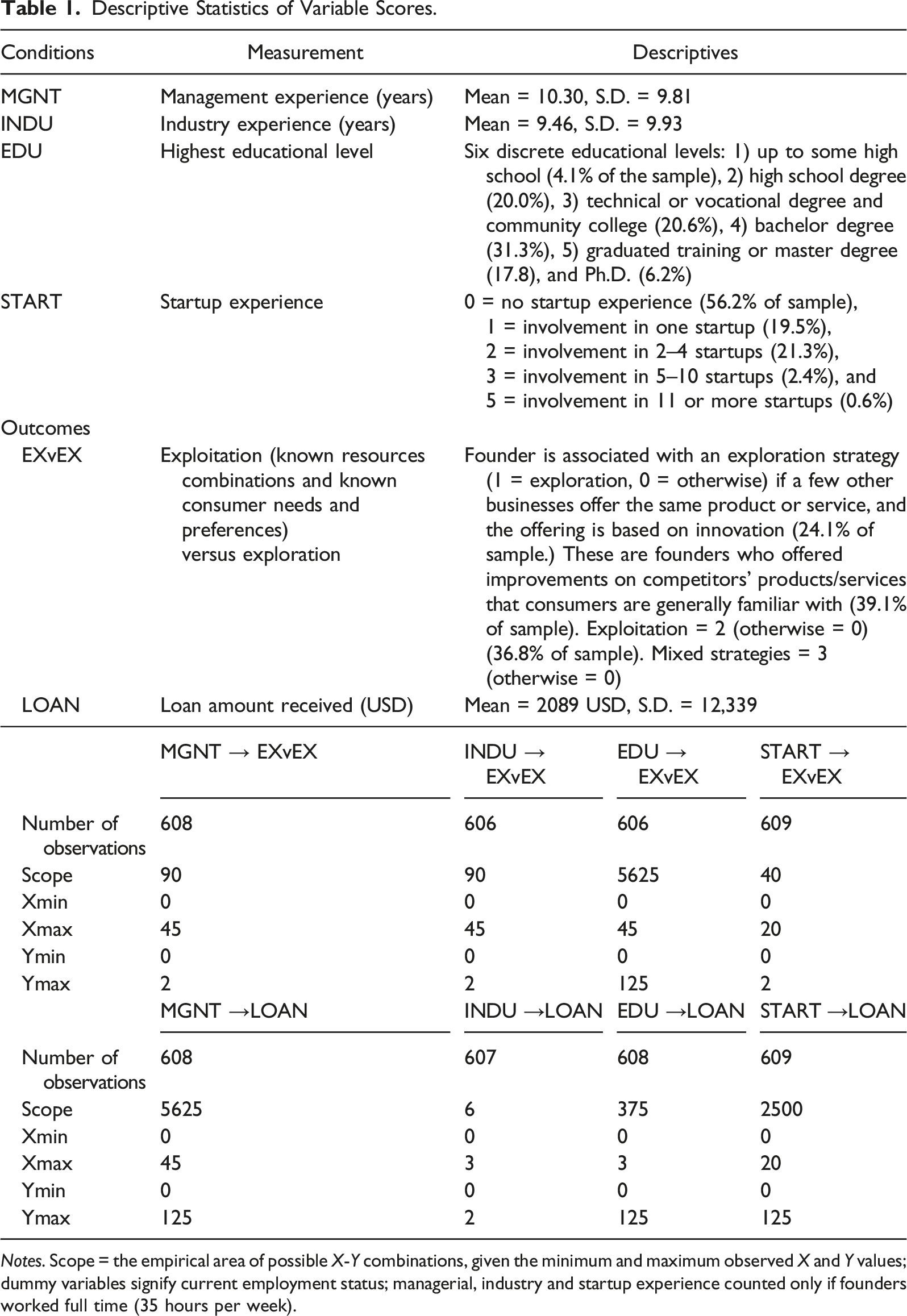

Descriptive Statistics of Variable Scores.

Notes. Scope = the empirical area of possible X-Y combinations, given the minimum and maximum observed X and Y values; dummy variables signify current employment status; managerial, industry and startup experience counted only if founders worked full time (35 hours per week).

Our goal is to demonstrate that founder’s experience can be both a license-to-play and license-to-win depending on the outcome of interest in entrepreneurship theories. Therefore, we must detect both a linear relationship and a necessary condition in our analyses.

Necessary Condition Analysis

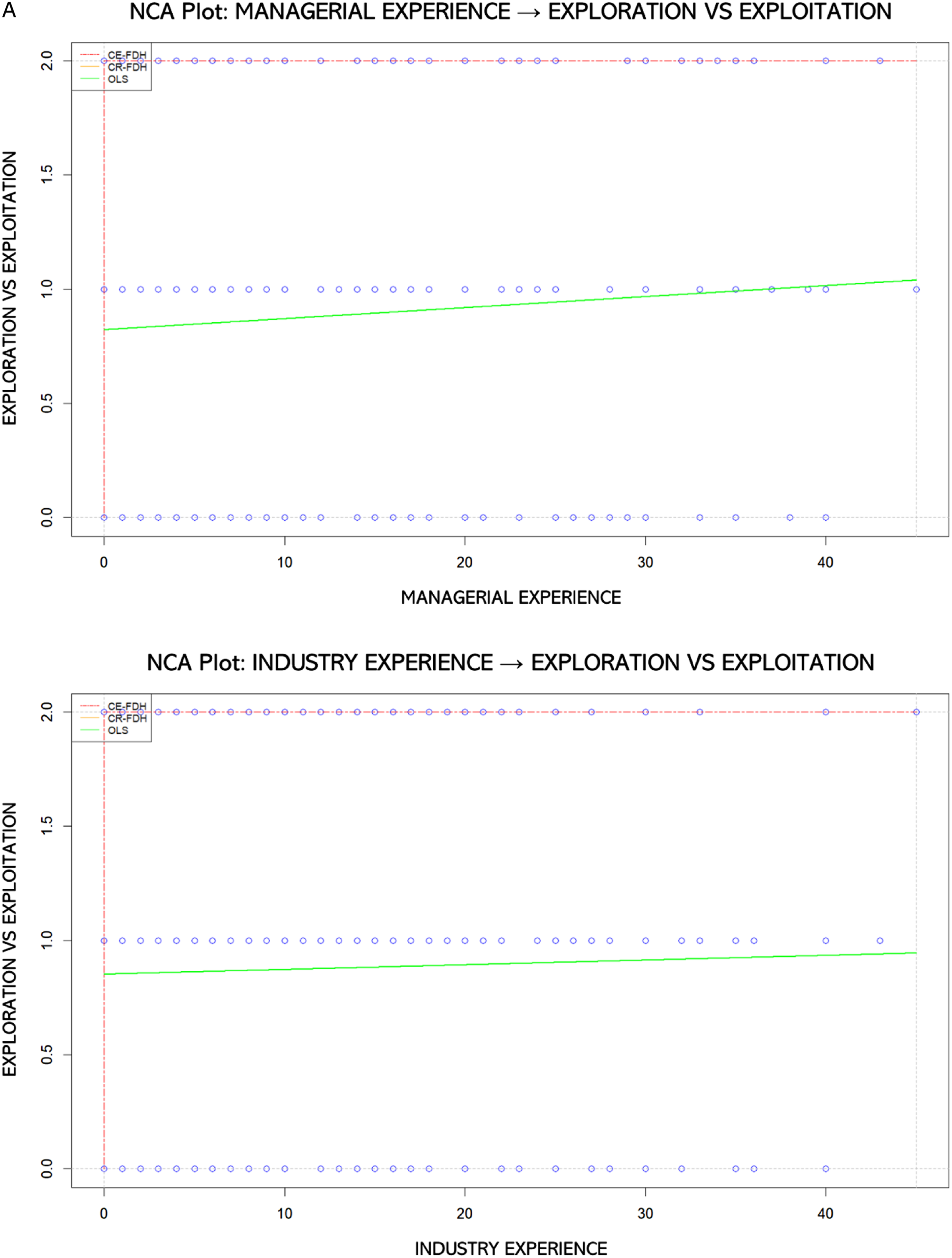

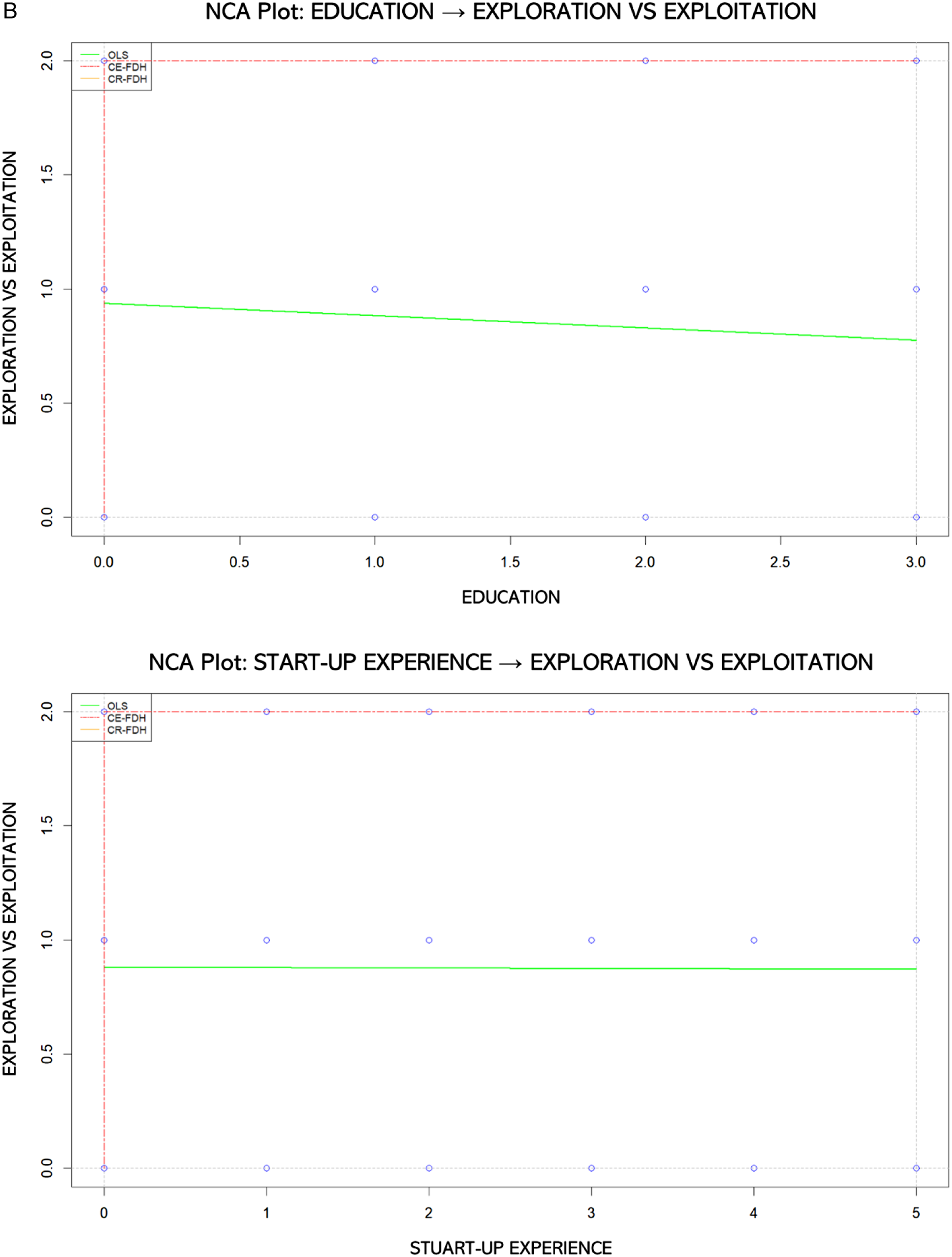

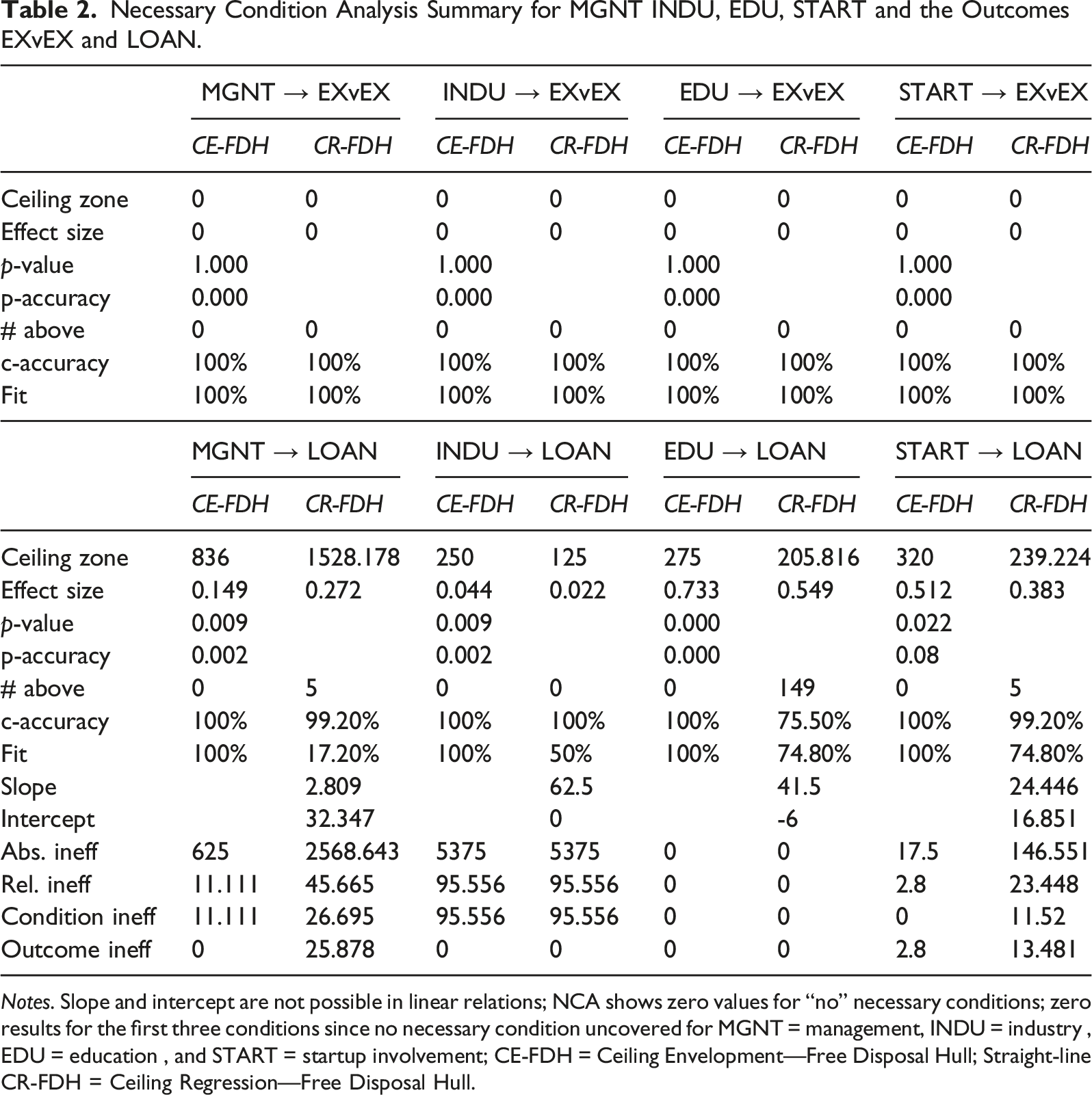

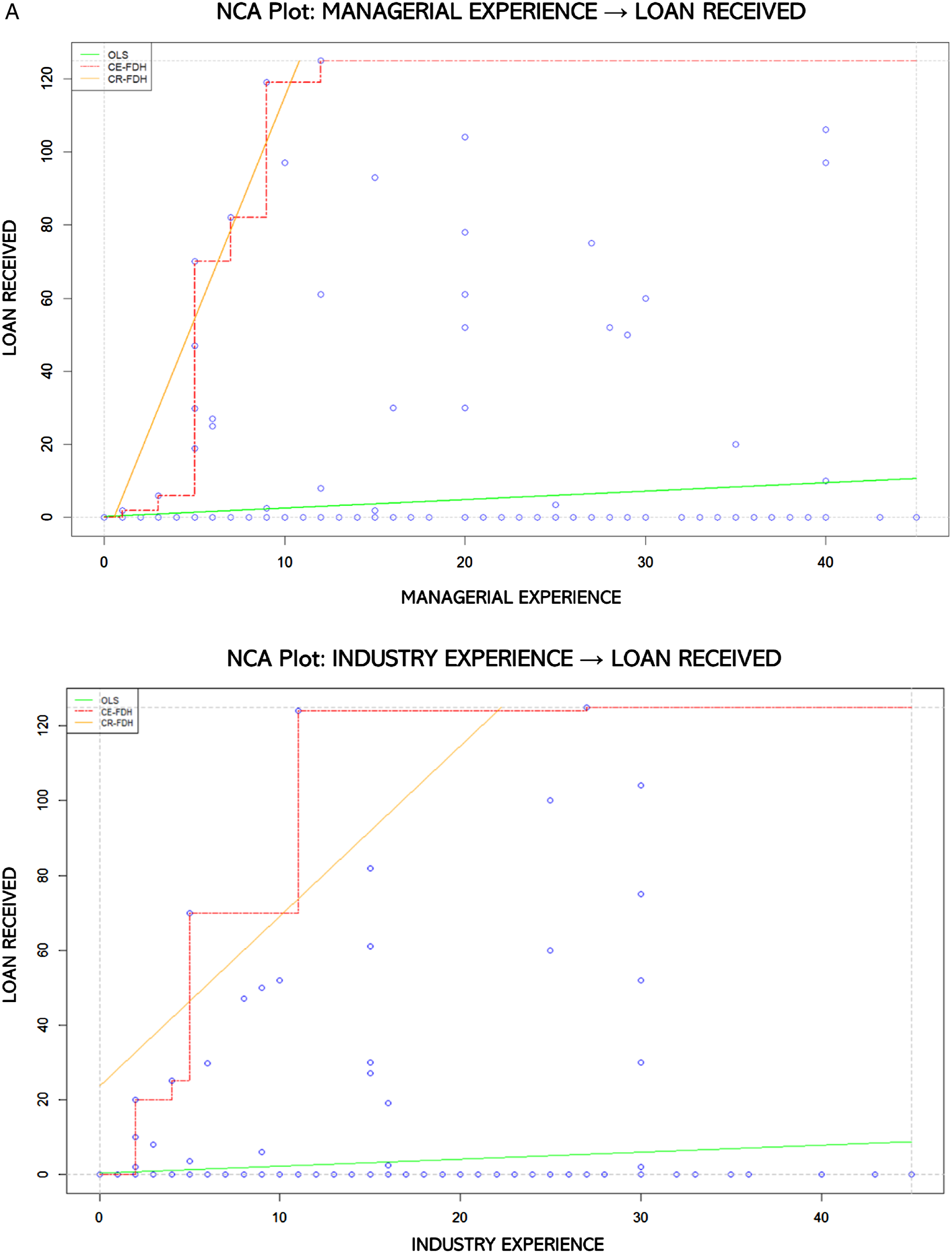

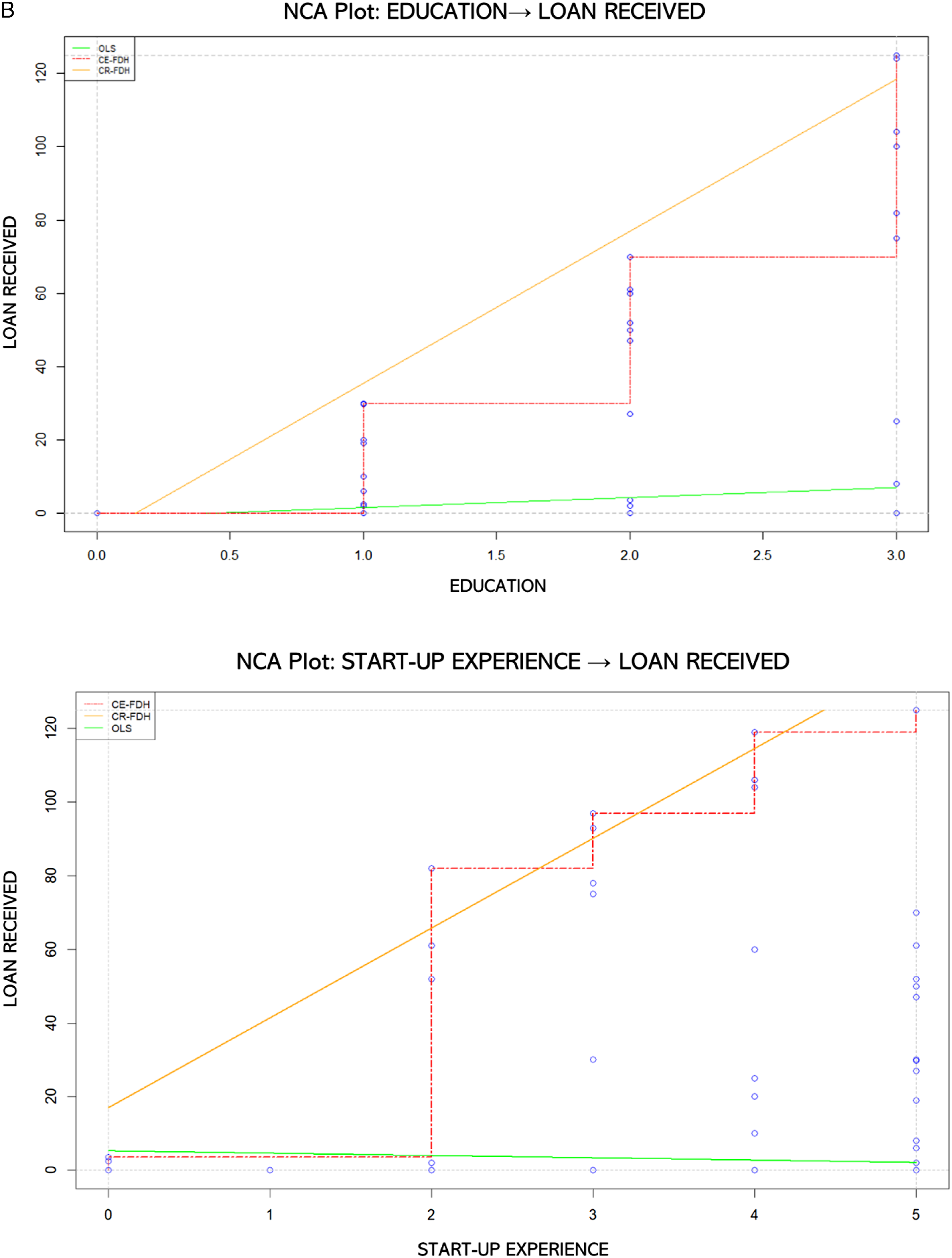

We show graphically the boundary condition for necessity (CE-FDH), and the two regressions lines (CR-FDH, and OLS regression line) for the four types of experiences and EXvEX (see Figure 1, managerial experience, industry experience, and Figure 2, education, start-up experience). The lack of empty space in the upper-left corner above the space with observations for any of our four types of experiences suggests an absence of a necessary condition. It already shows visually a linear relationship between MGNT → EXvEX (β = 0.083, p < .05), INDU → EXvEX (β = 0.090, n. s.), EDU → EXvEX (β = -0.087, p < .05), and for START → EXvEX (β = 0.010, p < .01). Table 2 presents the values for necessary conditions. A CE-FDH and a CR-FDH ceiling line of zero indicate no necessary conditions. Thus, we see consistent linear effects of experience on EXvEX activities, suggesting that more management (MGNT) and industry (INDU) experience leads to more exploitative behavior. Higher educational levels (EDU) also result in more explorative behavior. These findings are consistent with our expectations. However, our results show that the outcome is unaffected by the condition prior startup involvement (START) because more prior startup involvement increases neither explorative nor exploitative behavior. We can conclude that the association between experience and EXvEX is of the type license-to-win. Necessity of managerial and industry for the outcome exploration vs. exploitation activities. Necessity of education and startup experience for the outcome exploration vs. exploitation activities. Necessary Condition Analysis Summary for MGNT INDU, EDU, START and the Outcomes EXvEX and LOAN. Notes. Slope and intercept are not possible in linear relations; NCA shows zero values for “no” necessary conditions; zero results for the first three conditions since no necessary condition uncovered for MGNT = management, INDU = industry , EDU = education , and START = startup involvement; CE-FDH = Ceiling Envelopment—Free Disposal Hull; Straight-line CR-FDH = Ceiling Regression—Free Disposal Hull.

However, results for experience and LOAN indicate that all four experiential dimensions are necessary conditions for receiving loans (see Figure 3, managerial experience, industry experience, and Figure 4, education, start-up experience). It means that banks expect some degree of experience before giving out loans. Table 2 shows for MGNT → LOAN (d = 0.149, p < .05), INDU → LOAN (d = 0.0.44, p < .01), and EDU → LOAN (d = 0733, p < .01) we have small to very large significant values, respectively, with a high accuracy level. However, the necessity for EDU → LOAN is at a level that is high but not significant (d = 0853, n. s.). In sum, experience is a necessary condition for receiving loans. Also, other conditions cannot compensate for the conditions MGNT, INDU, EDU, or START. Thus, we conclude that experience is indeed a license-to-play for receiving loans, an important type of startup financing. Necessity of managerial and industry for the outcome loans received. Necessity of education and startup experience for the outcome loans received

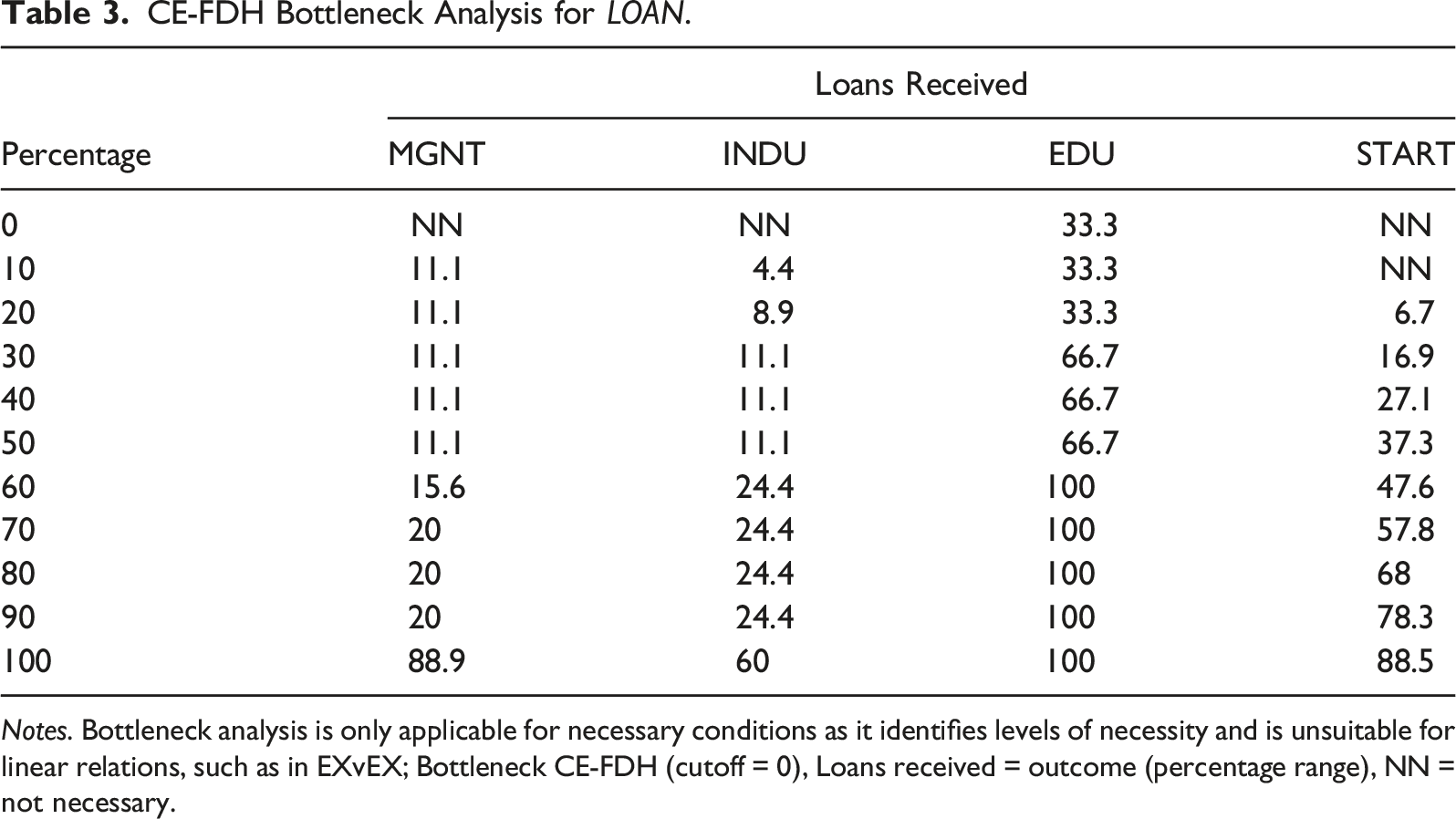

CE-FDH Bottleneck Analysis for LOAN.

Notes. Bottleneck analysis is only applicable for necessary conditions as it identifies levels of necessity and is unsuitable for linear relations, such as in EXvEX; Bottleneck CE-FDH (cutoff = 0), Loans received = outcome (percentage range), NN = not necessary.

Discussion

Scientific communities develop around generally accepted tools and techniques. Relationships between elements of our theories remain implicit until we test them with our analytical tools. Therefore, analytical tools render concepts, metaphors, frameworks, and decision criteria for our research process (Gigerenzer, 1991). In doing so, our analytical tools inform our theories, and empirical analysis guides our discovery of new relationships (Abbott, 1988). In its early days, entrepreneurship borrowed heavily from management and related disciplines due to its conceptual nascence (Lechner & Pervaiz, 2018; Shane & Venkataraman, 2000). With borrowed concepts, entrepreneurship inherited a robust methodological toolkit primarily developed for studying established firms and industries. As the field matures, we are paying closer attention to our methodologies to capture the inherent uniqueness of entrepreneurial phenomena (Crawford et al., 2015; Douglas et al., 2020; Maula & Stam, 2020; Yang & Aldrich, 2012). We join this important conversation by showcasing necessary condition analysis.

A condition is necessary for an entrepreneurial outcome when the outcome manifests only in the presence or absence of that condition. Instead of gradual changes, the new venture emergence process is characterized by many discrete and noncontinuous events, go-no-go decisions, and critical milestones—that fit well within the necessity-based paradigm. Founder’s human capital plays an essential role in this process, primarily studied using popular regression-based methods (Marvel et al., 2016). Linear analytical frameworks guided by probabilistic perspectives may suggest that more experience monotonically improves the likelihood of founders obtaining loans, all else equal. But we find that only a certain threshold of experience is necessary for the founders in our sample to receive loans. Below that decisive threshold, claiming that more experience leads to more loans is misleading. Our empirical illustration shows that a founder’s experience can be both a necessary condition (for receiving loans) and a probability raiser (for exploitation vs. exploration), depending on the outcome we study. By showcasing the dual impact of the founder’s experience, we shed new light on its neglected role as a necessary condition or license-to-play in entrepreneurial contexts. We encourage closer attention to the underlying assumptions of all our methodologies to ensure they match our explicit or implicit theoretical assumptions (Douglas et al., 2020; Maula & Stam, 2020; Shepherd & Gruber, 2020).

Figure 1 ceiling line represents the boundary condition for necessity in our empirical illustration. It indicates the impossibility of the combination X(0) and Y(1). 15 Our ceiling line progresses positively over several thresholds, suggesting that a higher educational level increases the likelihood of receiving loans beyond a threshold. Therefore, it would be reasonable to first test for “enabling” necessary conditions, followed by probabilistic “differentiating” conditions in our illustrative context. Management and entrepreneurship research is replete with such examples where necessary conditions do not preclude probabilistic perspectives. For instance, an entity must first be considered a category member (necessary condition) before attaining categorical differentiation (probability raiser) (Correll et al., 2017). Again, entrepreneurship research is often criticized for survival bias (Hmieleski & Baron, 2008). Conditions that cause an enterprise to survive or fail do not run along a continuum (Linder et al., 2020). Therefore, we can probe into the necessary condition of startup survival before investigating venture growth outcomes probabilistically. Next, a venture’s fit with a fund can be a necessary condition for its venture capital backing, while the quality of the venture team may serve as a differentiator best assessed probabilistically (Gompers et al., 2020). We will emphasize average effects when applying linear or regression-based tools to test probabilistic claims. Necessary condition analysis will offer minimum or maximum thresholds at the periphery of the observed distribution. Suppose our goal is a superior integration of our theory and methods. Then the most pertinent question to ask ourselves “is what kind of access a certain piece of evidence provides to the causal process of interest” in our study (Hedström & Ylikoski, 2010, p. 58). In answering this question, different methodologies and their underlying causal mechanisms can be complementary (Gerring, 2005). Causal pluralism can help us avoid naïve positivism (Gerring, 2005). By connecting myriad pieces of evidence, we can develop a better understanding of a phenomenon (Hedström & Ylikoski, 2010). Therefore, necessary condition analysis can be a stand-alone tool or complement regression-based methods in entrepreneurship research.

Causality in entrepreneurship is notoriously ambiguous (Salmon, 1998; Powell et al., 2006). To open the “black box” of causal mechanism, we must unpack “the cogs and wheels of the causal process through which the outcome to be explained was brought about” (Hedström & Ylikoski, 2010, p. 50–51). Such a mechanism-based explanation can help demystify entrepreneurial as well as broader organizational phenomena. 16 For instance, situational and macro-to-micro causal mechanisms emphasize social and cultural contexts within which individual actions are embedded and shape individual agency (Hedström & Ylikoski, 2010; Avgerou, 2013). Conditions that enable or restrict individual agency lie at the heart of mechanism-based explanations, offering opportunities for necessary condition analysis. One way to implement this is to approach a broader question in a piece-meal fashion and probe a phenomenon beyond the macro-level (Hedström & Ylikoski, 2010; Avgerou, 2013). Macro-level inquiry into, say, startups’ collocational gains in venture capital-rich regions (Chen et al., 2010) can incorporate micro-level necessary conditions associated with, say, organizational legitimacy (Bitektine et al., 2020) or entrepreneurial cognition (Mitchell et al., 2002). Furthermore, in a mechanism-based explanation, causal mechanism often presumes “covariational patterns,” suggesting potential complementarities between correlational approaches and mechanism-based explanations (Gerring, 2005, p. 166). Necessary condition analysis can be instrumental in this regard because, besides enabling the testing of hypotheses using quantitative data, it allows us to arrive at theory from data analysis. 17 In sum, necessary condition analysis can advance mechanism-based thinking in management and offer powerful ammunition in the quantitative entrepreneurship researcher’s arsenal.

Limitations and Future Research Directions

First, we have argued in favor of methodological and causal pluralism. Specifically, we encourage more necessary condition analysis in entrepreneurship research to capture critical theoretical nuance—both as a stand-alone tool or complement to linear regression-based methodologies. But neither methodological pluralism nor necessary condition analysis is a panacea. When “causation means different things to different people then, by definition, causal arguments cannot meet” (Gerring, 2005, p. 166). As such, statistical tools are blind to methodological alternatives. Therefore, researchers must actively identify opportunities to unify various causal and methodological approaches, like probabilistic and necessity-based approaches. To implement distinct methodological strategies with different paradigms within a single study, we may have to separate our research objects into subunits to align each with the strengths of our respective statistical tools. 18 It is a worthy challenge as it allows us to move past a narrow notion of causality in entrepreneurship research. More work remains to be done to make this integration process seamless.

Second, we did not develop a new theory or contribute to human capital theory in entrepreneurship. Instead, we illustrate necessary condition analysis. Future studies can explore the relations among our various constructs. For example, an applicant can potentially secure loans using assets as collateral. Then, we might expect that wealth supplements experience, suggesting necessary conditions associated with supplemental factors. The failure to satisfy a necessary condition can be supplemented in some cases (e.g., asset-backed loans). Again, research on startup teams can investigate what level of cohesion is necessary for startup teams to function? Can cohesion be supplemented? If yes, with what? Of course, not all necessary conditions can be supplemented. We can shed new light on extant entrepreneurship theories by asking when, why, and what necessary conditions can be supplemented or complemented (Siggelkow, 2002).

Third, we do not consider mediation and moderation. While mediated and moderated relations may not contradict our arguments and illustration, they might very well contextualize them in meaningful ways. Mediators explain the mechanism through which X impacts Y. Moderators explain how effect size changes in the presence of a third variable Z. Thus, both are elements of the regression universe and a probabilistic perspective. Hence, they do not test for necessary conditions. However, entrepreneurial phenomena can be modeled as a series of necessary thresholds within local linearities, including moderated or mediated effects (e.g., the case of categorization, see Correll et al., 2017). Again, we welcome future studies in this area.

Fourth, the PSED II data has two distinct advantages for our empirical illustration. First, it covers startups that may reasonably rely upon loan financing (Davidsson, 2016). Second, it is a well-known and relevant data source for entrepreneurship research. But it also has limitations. Most notably, entrepreneurship research has moved past the PSED II data context. Contemporary aspects of new venture emergences, like crowdfunding or platform businesses, are not covered by the PSED II dataset. Therefore, even though our argument is timely, the empirical context of our illustration favors a popular dataset that informed research in the past but maybe less relevant in the future.

Fifth, necessary condition analysis may not be readily generalizable. For example, startups make performance gains from collocating in regions concentrated with venture capital firms (Chen et al., 2010). It suggests the importance of institutions and ecosystems for entrepreneurship. A critical threshold of venture capital firm concentration, for instance, may make it “possible” for startups to perform better in other data settings. But the outcome is not a “given” because a necessary condition partially explains a phenomenon. Additional conditions may also matter, and, in a different setting, a necessary condition may yield a different outcome (Avgerou 2013). In other words, necessary conditions are not sufficient conditions.

Yet necessary conditions are inextricably linked to (in)sufficient conditions (Mackie, 1965). Focusing on necessary conditions exclusively, we have neglected sufficient conditions and possible combinations like INUS conditions (an insufficient but necessary part of an unnecessary but sufficient condition). Also, set-theoretic approaches (Fiss, 2007), such as qualitative comparative analysis (Ragin, 2000), can capture necessary and sufficient conditions. We direct our readers to a vast body of research developed around these associated topics, which can enhance the study of necessary conditions in entrepreneurship.

Finally, necessary condition analysis is susceptible to sampling errors, as the ceiling techniques (CE-FDH and CR-FDH) are based on relatively small subsamples of the overall observations. Consequently, necessary condition analysis is sensitive to selection bias and measurement errors (see Dul, 2016). Also, necessary condition analysis emphasizes necessary conditions and ignores the rest—a standard limitation of other methods, like linear regression analysis. Ultimately, there is no substitute for sound theorizing.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.