Abstract

We assess how social capital relates to individuals’ initial interest in becoming an entrepreneur, formally setting up a venture, and subsequent survival of the venture. Conceptualizing and measuring entrepreneurship as a sequential process inferred from cross-sectional data for 22,878 individuals living in 110 regions across 22 European countries, we find that regional social capital is relevant for formally setting up a venture, but it is not associated with initial interest, nor with venture survival after establishment. By assuming variability and not uniformity in how social capital relates to entrepreneurship, we gain a better understanding of the contextual determinants of the venture creation process.

Entrepreneurship is a dynamic process of value creation which does not take place in a vacuum, but is embedded in its regional and national context (Baker et al., 2005; Kim et al., 2016; Welter, 2011). Establishing a business requires a wide array of distinct resources, information, and relationships at different stages (Greve & Salaff, 2003). During the process of starting a venture, entrepreneurs need to overcome distinct challenges, such as the adverse effects of uncertainty, information asymmetries, and the liability of newness (Freeman et al., 1983; Shane & Cable, 2002; Stinchcombe, 1965). The nature and intensity of these hurdles change along the venture creation process. As a result of these changing situational characteristics, only few individuals who would like to become an entrepreneur start a business, and, of this subset, not all remain in business afterwards (Aldrich & Martinez, 2001; Blanchflower et al., 2001; Levie et al., 2011).

Social capital constitutes one of the most important resources supporting (potential) entrepreneurs and enabling them to overcome these hurdles (Gedajlovic et al., 2013; Hoang & Antoncic, 2003). Social capital theory has developed two distinct theoretical lenses, at the individual (i.e., firm or personal) level and the societal level (Adler & Kwon, 2002; Portes, 1998). At the individual level, social capital is defined as an actor’s accrued goodwill of others towards them, their set of relations, and potentially accessible resources (Adler & Kwon, 2002; Burt, 1992). Higher levels of individual-level social capital make it easier for entrepreneurs to recognize potential opportunities and to get access to knowledge, information, employees, and resources such as financing (Davidsson & Honig, 2003; Shane & Cable, 2002; Stuart & Sorenson, 2005).

At the societal level, social capital is a resource which originates from associational networks, initiating and structuring social interactions, and influencing both individuals’ and collective action (Durlauf & Fafchamps, 2005; Putnam, 2000; Woolcock, 2001). Societal social capital theory stresses the benefits associated with the generation of bridging cross-cutting ties, supportive social norms, generalized trust and reciprocity, and network externalities (Knack & Keefer, 1997; Putnam, 1993, 2000). As these benefits extend beyond the associational network within which social capital is created also to non-members, societal social capital shares many of the characteristics of a public good (Putnam et al., 2000) and is considered to be a part of a society’s overall informal institutional makeup (Beugelsdijk & Maseland, 2011). The theoretical insights derived from societal social capital theory have been applied at the regional level (Malecki, 2012; Putnam, 1993) and the national level (Knack & Keefer, 1997; Kwon & Arenius, 2010).

In this paper, we focus on the influence of societal social capital at the regional level on the venture creation process. This is because persistent differences in entrepreneurship rates across regions (Andersson & Koster, 2011; Fritsch & Wyrwich, 2014, 2019) cannot be sufficiently explained by individuals’ characteristics, such as individual-level social capital (Kwon et al., 2013). A regional approach to studying the influence of societal social capital on entrepreneurship is also warranted because the socio-economic effects of societal social capital are spatially bounded (Laursen et al., 2012a; Malecki, 2012) and there are substantial differences in social capital at the regional level (Beugelsdijk & van Schaik, 2005; Putnam, 1993). Therefore, we start from the premises that, although an individual-level process, entrepreneurship is regionally embedded (Dahl & Sorenson, 2012; Feldman, 2001; Michelacci & Silva, 2007) and that regional social capital influences the venture creation process (Kwon et al., 2013). By focusing on regions as an important meso-level, we complement comparative entrepreneurship research that has traditionally used “simple two-level macro-micro research designs” (Kim et al., 2016, p. 274) to relate country-level factors to individual-level outcomes. Our focus on the regional level also has the methodological advantage that we can distinguish the effect of societal social capital as an informal institution from confounding factors such as formal institutions that vary predominantly across countries.

We conceptualize the venture creation process as a dynamic sequential process and assess how regional social capital is related to (potential) entrepreneurs’ advancement through the stages (0) never considered entrepreneurship, (1) pre-establishment, (2) young venture, and (3) an established venture. Regional social capital positively affects (potential) entrepreneur’s ability to mobilize external resources and gain access to information and knowledge. While the influence of regional social capital on entrepreneurship is generally positive (Estrin et al., 2013; Kwon & Arenius, 2010; Kwon et al., 2013), the magnitude of its impact may vary along the stages of the entrepreneurial process. We argue that as entrepreneurs are most constrained internally and externally prior to firm establishment, the positive effect of regional social capital is particularly strong in the early stages of the venture creation process. This is because the more severe the nature and degree of the constraints entrepreneurs are confronted with, the higher the value of regional social capital for entrepreneurship.

To test our hypotheses on the positive and changing relation between regional social capital and distinct stages of the venture creation process, we create a unique (cross-sectional) dataset for 22,878 individuals from 110 regions nested within 22 European countries containing information on the individual’s position in the four-staged venture creation process. We conceptualize the venture creation process by analyzing the likelihood that individuals have advanced beyond a certain entrepreneurial engagement stage, compared to individuals who are currently at this stage of engagement. To assess the influence of regional social capital on this sequential process, we use novel multilevel models with random regional and country fixed effects.

We find that regional social capital is positively associated with the likelihood that individuals have advanced beyond wanting to become an entrepreneur, but we find no evidence that regional social capital predicts the likelihood that individuals are interested in entrepreneurship, nor the odds that young ventures have survived for at least 3 years. These results confirm our hypotheses that regional social capital affects venture creation positively, but at different stages to different degrees, with regional social capital being most relevant for formally starting a venture. We also show that this effect is primarily driven by the type of regional social capital that is characterized by high network reach and diversity. Additional analyses including controls for individual-level social capital show that the effect of regional social capital is independent of the effect of individual-level social capital.

Our study extends the literature relating country- or regional-level scores of entrepreneurship to country or regional characteristics (Bosma & Schutjens, 2009, 2011; Stephan & Uhlaner, 2010) because we conceptualize and measure entrepreneurship as an individual-level phenomenon (Autio et al., 2013; Kim et al., 2016). In addition, we conceptualize entrepreneurship as a process, thereby extending static multilevel studies (Kwon et al., 2013; Stuetzer et al., 2014). While individual-level process-based conceptualizations of entrepreneurship have recently gained prominence, these studies have focused on the individual or the national level (Grilo & Thurik, 2008; Peroni et al., 2016; Stam et al., 2010; Van der Zwan et al., 2012) but have overlooked the regional level. We complement these studies by focusing on the regional social context. Specifically, we study the role of regional social capital using societal social capital theory and established societal social capital measures. In that regard, our paper complements the work of Mickiewicz et al. (2017) who link the regional established business ownership rate as a proxy for entrepreneurship capital to the individual-level entrepreneurial process in the United Kingdom.

We contribute to entrepreneurship research by introducing a regionally embedded venture creation process that highlights how the influence of the regional social environment changes over the course of the venture creation process. We combine entrepreneurship process theory (Baker et al., 2005; Baron, 2007; Bhave, 1994) with social capital theory (Knack & Keefer, 1997; Putnam, 1993, 2000) to advance comparative entrepreneurship research (Autio et al., 2013; Estrin, Korosteleva, et al., 2013; Estrin, Mickiewicz et al., 2013; Stephan & Uhlaner, 2010; Terjesen et al., 2016) by relaxing the assumption of uniformity and instead assuming variability in contextual effects across engagement stages. Our paper shows that the dynamic nature of the entrepreneurial process needs to be taken into account when theorizing on the impact of context.

Theory and Hypotheses

The Venture Creation Process

In this study, we define entrepreneurship as the regionally embedded process of new venture creation. This process is characterized by distinct identifiable stages through which (potential) entrepreneurs transition until they run an established business (Baker et al., 2005; Baron, 2007; Bhave, 1994; Greve & Salaff, 2003; Van Der Zwan et al., 2013). These stages are composed of unique situational characteristics that determine entrepreneurs’ tasks, goals, most pressing needs, internal and external constraints, as well as internal and external factors mitigating them (Baker et al., 2005; Garnsey, 1998; Hite & Hesterly, 2001).

During the venture creation process, entrepreneurs are challenged because they are typically internally resource-constrained (Fairlie & Krashinsky, 2012) and suffer from the liability of newness (Freeman et al., 1983; Stinchcombe, 1965). Moreover, entrepreneurship is an uncertain process which is also characterized by pronounced information asymmetries. This complicates the interactions between entrepreneurs and potential stakeholders (Shane & Cable, 2002) such as resource holders, partners, and employees (Stuart & Sorenson, 2005). The nature and intensity of these hurdles and constraints vary across the stages of the process (Aldrich & Auster, 1986), as a result of which the impact of the determinants of entrepreneurship changes over the course of the venture creation process (Grilo & Thurik, 2008; Mickiewicz et al., 2017; Van Der Zwan et al., 2013).

The stages of the venture creation process can be classified by means of theoretically grounded transition points, for example, formally registering a business. A transition to the next stage only takes place once resource and information acquisition, as well as organizing and learning, have advanced to a sufficient degree (Bhave, 1994; Peroni et al., 2016). Drawing on Shepherd et al.’s (2019) recent meta-framework distinguishing between initiation, engagement, and performance of entrepreneurial activity and on previous research (Baron, 2007; Baron & Markman, 2005; Davidsson & Honig, 2003; Garnsey, 1998; Ucbasaran et al., 2001), we conceptualize the venture creation process as consisting of the transitions between the following stages: (0) not considering entrepreneurship, (1) pre-establishment, (2) young venture, and (3) established venture.

The transition from not considering entrepreneurship to the pre-establishment stage and moving further through the venture creation process marks the starting point of the process. This occurs if individuals change their intentions and/or identify a suitable potential opportunity which they want to exploit (Ajzen, 1991; Kirzner, 1997; Shane & Venkataraman, 2000; Ucbasaran et al., 2001).

Once individuals have identified or created potential opportunities, they enter the pre-establishment stage which is characterized by thinking about the potential venture, discussing it with others to get support and feedback, and organizing efforts (Birley, 1985). In this stage, information asymmetries and the liability of newness are most severe (Aldrich & Auster, 1986). Entrepreneurs seek access to resources, information, and knowledge, but have limited internal resources or credible signals to indicate the viability of their undertaking and their own quality, which increases resources holders’ and potential partners’ reluctance to enter into a relationship with or to support the entrepreneur (Hoang & Antoncic, 2003). Individuals move from the pre-establishment stage to the young venture stage once they reach their strategic goals of acquiring information, know-how, and the required resources and manage to formally launch the venture. This implies that the transition to the young venture stage is not only driven by the entrepreneur’s intentions but is also highly dependent upon whether external actors can be convinced to support the entrepreneur.

After entrepreneurs have formally registered the venture, they enter the young venture stage which is characterized by efforts to ensure the survival of the business and gear it towards growth (Aldrich & Martinez, 2001; Stam, 2007). The extent of uncertainty, information asymmetries, and the liability of newness fall as the process unfolds and as the young venture develops and grows (Aldrich & Auster, 1986; Hite & Hesterly, 2001). Moreover, the entrepreneur’s ability to acquire resources and to establish relations with key stakeholders improves as the business develops observable properties such as resources (e.g., patents) and gains its first prominent stakeholders (e.g., reputable venture capitalists) (Hsu & Ziedonis, 2013; Shane & Cable, 2002; Stuart et al., 1999). The entrepreneurship literature typically considers young ventures that have operated for a few years to have become established (Grilo & Thurik, 2008; Reynolds et al., 2005; Van der Zwan et al., 2012). Therefore, the last step in the venture creation process (from young venture to established venture) takes place once the business has survived the first years. In our study on venture emergence, this final step marks the end of the venture creation process.

Social Capital at the Regional Level

Entrepreneurship is contextually embedded. Institutions as the “humanly devised constraints that structure political, economic and social interactions” (North, 1991, p. 97) influence entrepreneurship. Institutions consist of formal institutions, such as laws and property rights, and informal institutions such as norms and networks. Societal social capital constitutes an important part of informal institutions which describes the structure and quality of relations in society (Knack & Keefer, 1997; Kwon & Arenius, 2010; Putnam, 2000).

Societal social capital facilitates resource mobilization, (tacit) knowledge transmission, and information spillovers (Estrin et al., 2013; Knack & Keefer, 1997; Kwon & Arenius, 2010; Kwon et al., 2013; Vedula & Frid, 2019). Conceptually, societal social capital is associated with well-developed civic or associational networks that create weak (Granovetter, 1973), cross-cutting (Blau & Schwartz, 1984), and bridging ties (Putnam, 2000). These networks facilitate repeated interactions among heterogeneous individuals of different education, occupation, status, and background who otherwise would not have interacted. While these relationships are created in a specific context and for a specific purpose, once they exist, they can also be utilized in another context and for another purpose. For this reason, these relations are also referred to as multiplex relationships (Coleman, 1988; Portes, 1998; Uzzi, 1997), meaning that relationships developed within one context, such as an environmental association, are of economic value also in another context, such as starting a business. In contrast to individual social capital which generates private benefits (Burt, 1992), societal social capital shares many of the characteristics of a public good (Coleman, 1988; Kwon et al., 2013; Putnam, 1993; Putnam et al., 2000).

Repeated interactions within associational networks are the structural foundation for the positive externalities associated with societal social capital (Durlauf & Fafchamps, 2005; Putnam, 2000; Woolcock, 2001). In addition to creating the abovementioned cross-cutting ties, associational networks foster strong norms of cooperation as well as generalized trust and reciprocity (Paxton, 2007; Putnam, 2000). As Putnam (1993, p. 89–90) notes, “associations instill in their members habits of cooperation, solidarity, and public-spiritedness.” These effects extend beyond the associational network and benefit society at large (Durlauf & Fafchamps, 2005; Putnam et al., 2000; Woolcock, 2001).

The benefits associated with societal social capital are enhanced by network reach and density (Burt, 2005; Coleman, 1988). In societies rich in social capital, information about cooperation or lack thereof spreads quickly, providing a platform for learning about cooperative or opportunistic behavior (Kim et al., 2016; Paxton, 1999). Large network reach, density, and overlapping third-party ties enhance access to this type of information, facilitating ex-ante partner selection and increasing ex-post monitoring effectiveness. By increasing reputational concerns, deterring opportunistic behavior, and making its sanctioning easier, more effective, and less costly, higher network density improves the compliance of business partners, generates trust, and enables transactions that otherwise may not have taken place (Coleman, 1988; Granovetter, 1985).

In the context of entrepreneurship, societal social capital has an important regional (i.e., sub-national) dimension. One reason to take a regional approach is that the mechanisms through which social capital affects individuals and organizations are spatially bounded and of regional nature (Laursen et al., 2012a; Malecki, 2012). Formation and persistence of personal relationships are enhanced by geographical proximity (Rivera et al., 2010), and the transmission of tacit knowledge quickly decays with distance (Almeida & Kogut, 1999; Jaffe et al., 1993). Social capital research has also shown that societal social capital differs between regions Beugelsdijk & van Schaik, 2005; Putnam, 1993). Furthermore, entrepreneurship is an individual-level process, but strongly regionally embedded (Bosma & Schutjens, 2009; Feldman, 2001; Saxenian, 1994) as evidenced by persistent regional differences in entrepreneurship (Andersson & Koster, 2011; Fotopoulos, 2014; Fritsch & Wyrwich, 2014, Fritsch & Wyrwich, 2019) and their deeply-rooted historical antecedents (Stuetzer et al., 2016). The regional embeddedness of entrepreneurship is also reflected in the observations that the share of entrepreneurs starting their venture in the region where they were born is significantly higher than the share of wage-laborers who are employed in their home region (Michelacci & Silva, 2007) and that entrepreneurs perform better if they have a longer tenure in the region where they start the venture (Dahl & Sorenson, 2012). Therefore, the regional level presents an important meso-level in between the individual and the national level to assess the influence of social capital on entrepreneurship (Kim et al., 2016; Malecki, 2012).

Regional Social Capital and the Venture Creation Process

The relevance of regional social capital for the venture creation process is contingent upon the situational characteristics and hurdles faced by entrepreneurs in each stage.

Transitioning from never having considered entrepreneurship to thinking about entrepreneurship and taking first active steps requires the ability to gain access to a wide array of information to identify a suitable opportunity (Kirzner, 1997; Mickiewicz et al., 2017; Shane & Venkataraman, 2000; Ucbasaran et al., 2001). Regional social capital is beneficial in this context because the discovery of suitable business opportunities depends not only on entrepreneurs’ own experience and knowledge but also on the cumulative diversified experience and advice of others they can tap (Bhave, 1994; Garnsey, 1998; Leyden et al., 2014). The more diverse the pool of ideas and information individuals are exposed to, the higher the probability they will identify a profitable opportunity and seek to become an entrepreneur (Leyden et al., 2014). Through repeated interactions among heterogeneous individuals, associations foster information spillovers, (tacit) knowledge transmission, and interactive learning (Malecki, 2012). Close contacts, such as family members and friends, are likely to hold similar and thus redundant information. Conversely, more distant contacts are likely to have access to non-redundant and hence more valuable information and also a wider range of distinct resources (Blau & Schwartz, 1984; Granovetter, 1973). Moreover, the transmission of tacit knowledge requires regular personal contact and is facilitated by high levels of regional social capital (Laursen et al., 2012a). In sum, regional social capital supports individuals to become potential entrepreneurs because cross-cutting ties facilitate access to valuable non-redundant information and norms of cooperation.

The transition from thinking about entrepreneurship to formally starting a venture and developing it further is influenced by the ability to (a) mobilize resources, (b) gain access to information and knowledge, and (c) develop relationships with key stakeholders. Opportunity identification is meaningless unless potential entrepreneurs seek to exploit them, and exploitation requires resource mobilization (Aldrich & Martinez, 2001). However, most entrepreneurs are internally resource-constrained (Fairlie & Krashinsky, 2012) and mobilization of external resources is typically severely obstructed during the initial stages of starting a venture. Entrepreneurs need to gain access to a wide range of information from a variety of sources, such as information about market conditions, technological developments, or support options, to advance venture foundation and development. Transfers of (tacit) knowledge from external stakeholders are required to foster the development of routines and capabilities and to overcome the liabilities of newness (Aldrich & Auster, 1986; Freeman et al., 1983; Stinchcombe, 1965). The development of relations with key stakeholders is however impeded at this stage as potential employees, business partners, and other stakeholders may shy away from engaging with nascent entrepreneurs in light of lack of information about them (Hite & Hesterly, 2001), which is associated with high transaction costs. The key challenge for entrepreneurs is to assemble the required inputs and convince stakeholders of the viability of their venture idea and their own quality (Hoang & Antoncic, 2003; Stuart & Sorenson, 2005). Regional social capital facilitates overcoming these challenges because it fosters resource mobilization, information and knowledge transmission, and networking. Thus, regional social capital is highly relevant for the transition from wanting to start a business to formally launching it and developing it afterwards.

In the transition from a young venture to an established venture, entrepreneurs are still subject to the adverse conditions related to uncertainty, information asymmetries, and the liability of newness. We, hence, predict regional social capital to enhance the survival odds of young businesses. However, the adverse conditions are less pronounced for formally established enterprises than during the early stages of the venture creation process (Aldrich & Auster, 1986; Hite & Hesterly, 2001). This is because the entrepreneur can increasingly rely on the venture’s internal capabilities and resources and on strategic partnerships which previously were not available. For this reason, we expect regional social capital to be less important for the young venture’s survival odds as compared to formal venture launch.

The above discussion leads us to hypothesize that regional social capital is positively related to entrepreneurship, but that the magnitude of its impact varies across the stages of the venture creation process. Formally,

The literature on societal social capital has distinguished between societal social capital of a connected nature and societal social capital of an isolated nature (Paxton, 2002, 2007; Putnam, 1993). We extend our argument on regional social capital by arguing that connected regional social capital has a stronger positive relation with entrepreneurship than isolated regional social capital (Kim et al., 2016; Kwon et al., 2013). As explained earlier, a larger network reach generates more bridging ties among heterogeneous individuals. Connected social capital is characterized by social ties between a variety of networks through their members’ multiple memberships (Kwon et al., 2013; Paxton, 2002). Connected social capital hence cuts through social boundaries (cf. Blau & Schwartz, 1984), increasing network reach and network diversity. These interlinkages are of vital importance for accessing non-redundant information, for knowledge spillovers, for resource acquisition from diverse sources, and for the diffusion of norms of cooperation, solidarity, as well as generalized trust and reciprocity beyond the associational network.

Conversely, isolated social capital is of an insular nature. Members of a given association do not belong to other organizations and little exchange takes place beyond the focal networks. Besides generating fewer of the beneficial effects associated with cross-cutting associational networks, isolated associations may even lead to in-group biases, potentially triggering out-group hostility, which reduces cooperation in general and constitutes part of the “dark side” of social capital (Fukuyama, 2001; Kwon et al., 2013; Paxton, 2007; Portes, 1998). This leads us to our third hypothesis:

Data and Method

Empirical Strategy

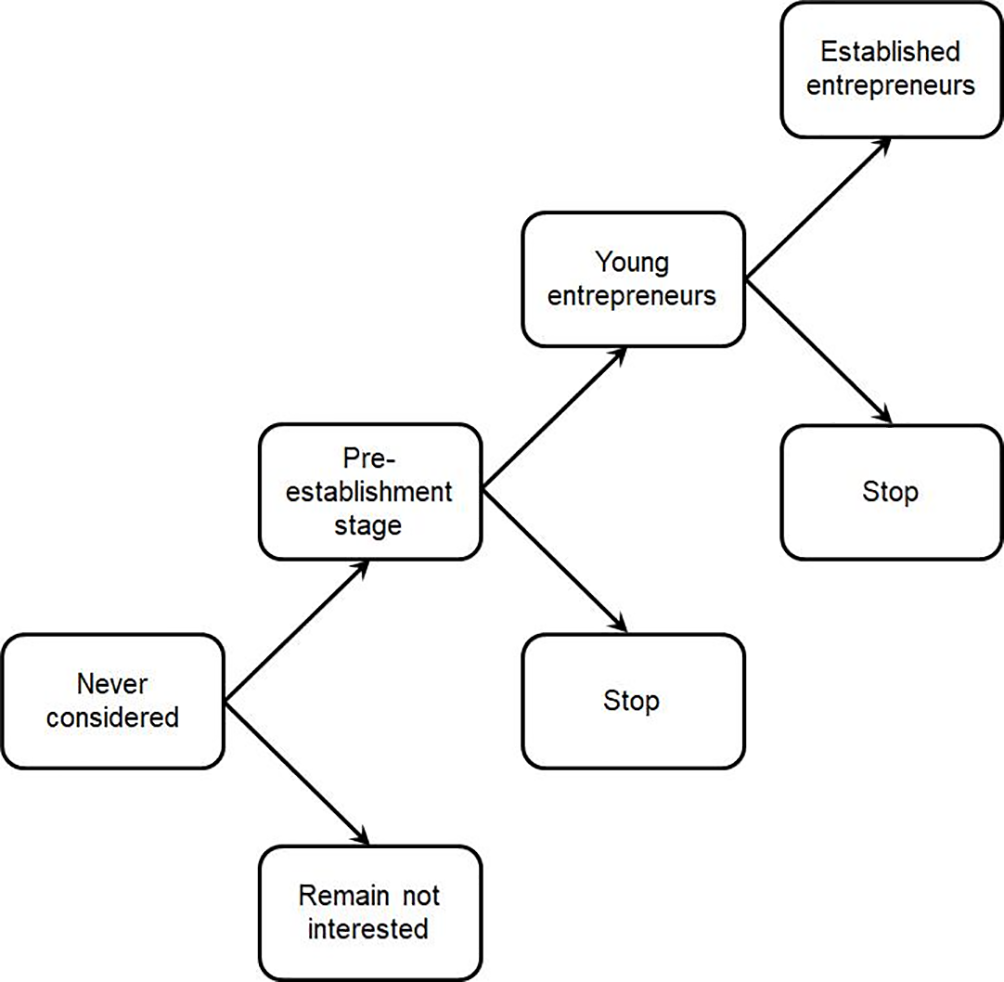

We conceptualize the venture creation process as a sequence of engagement stages that proxy for the underlying situational characteristics that entrepreneurs face. The key idea is that only a certain share of the population is interested in becoming an entrepreneur, and just a fraction of this subset is going to start a venture, and yet another smaller subset of those who start a business is going to survive for an extended period (Peroni et al., 2016; Van der Zwan et al., 2012, 2013). Hence, we conceptualize the venture creation process as a sequence of comparisons that proxy for transitions from lower to higher levels of entrepreneurial engagement which we illustrate in Figure 1.

The venture creation process.

The four stages of the venture creation process are (0) individuals who never considered entrepreneurship; (1) individuals in the pre-establishment stage who are thinking about entrepreneurship and/or engaged in organizing and planning; (2) young entrepreneurs, who founded their business less than 3 years ago; and (3) established owner-managers who have been running their business for more than 3 years. Individuals can exit this process at any time. 1 To reach Stage 3 —running an established venture— individuals first need to advance through the intermediate stages of setting up their business. By applying this sequential logic, we test our prediction regarding the positive and changing role of social capital in the venture creation process.

Sample

We use individual-level entrepreneurship data from the Eurobarometer Flash Surveys #192, #283, and #354 (Eurobarometer, 2007, Eurobarometer, 2010, Eurobarometer, 2012), complemented with regional social capital data generated from the European Values Study (EVS, 2015), and matched with regional control variables from Eurostat’s regional database (Eurostat, 2017).

The Eurobarometer Flash Surveys have been used extensively in comparative entrepreneurship research (Block et al., 2019; Gohmann, 2012; Stam et al., 2010; Van der Zwan et al., 2012, 2013; Walter & Block, 2016). One attractive feature of the Eurobarometer Flash Surveys is that they contain information on distinct entrepreneurial engagement stages, which range from people who have never considered becoming an entrepreneur to people who are running established businesses. We use this information to construct the ordered sequential multistage venture creation process.

We have information on the region of residence of individuals which allows us to link individuals with characteristics of their region, in particular the regional level of social capital, and thus to treat entrepreneurship as regionally embedded. 2 Pooling the abovementioned three waves of the survey to achieve better sample coverage, we base our analysis on the population aged 18 to 64 years and we exclude retired people. Our final database is of repeated cross-sectional nature and consists of 22,878 individuals located in 110 regions in 22 European countries. 3

Dependent Variables

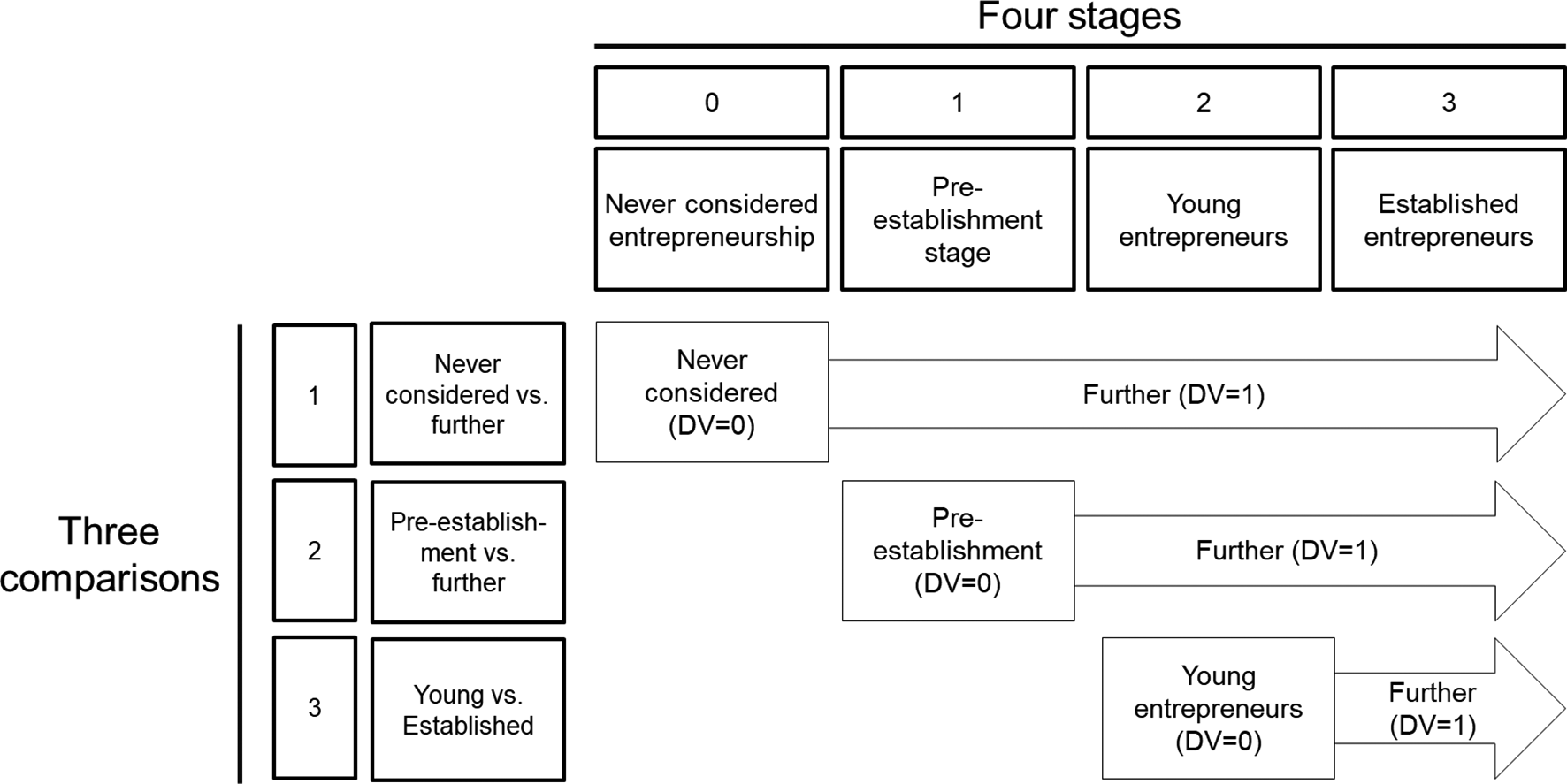

Following the proposed stage model, our dependent variables proxy for individuals’ moving from one stage of the venture creation process to higher engagement stages as dichotomous outcomes. That is, we operationalize our dependent variables such that they reflect comparisons between adjacent (sequential) stages from lower to higher levels of entrepreneurial engagement. By comparing people who currently are in one stage with those who have advanced to a higher level of entrepreneurial engagement we assess which factors contribute to a successful advancement through the venture creation process. Since we have four stages, we make three such comparisons, namely:

The dependent variable takes a value of zero for those individuals who are currently in the respective stage and a value one for individuals who have advanced further. This sequential logic enables us to explicitly incorporate the final outcome into the model and is graphically illustrated in Figure 2.

Modeling the stages and comparisons of the venture creation process.

Our approach implies that we do not consider individuals that are currently in an engagement stage prior to the focal comparison in our estimations. Consequently, our sample gets more restrictive by design as we move through the venture creation process. 4

Independent Variables

Regional Social Capital

We measure regional social capital as regional average membership in voluntary associations. 5 In line with Knack and Keefer (1997), Putnam (1993, 2000), and follow-up research (Beugelsdijk & van Schaik, 2005; Kwon & Arenius, 2010), we consider the following associations: welfare organizations, religious organizations, cultural activities, trade unions, political parties and groups, local community action, third world development and human rights groups, environment, ecology, and animal rights groups, professional associations, youth work, sports and recreation associations, women’s groups, and health organizations. To construct this measure, we pool data from the third (1999-2001) and the fourth (2008-2010) EVS survey waves. 6 In total, we use EVS information from 51,047 individuals located in 110 regions and 22 countries for which we have entrepreneurship data to obtain a regionally representative sample. By utilizing information on the region of residence of the survey respondent, we are able to aggregate the individual-level EVS information to the regional level and match it to the Eurobarometer Flash Surveys. The average number of observations per region we use in generating the regional social capital measure is 464.

Connected and Isolated Regional Social Capital

To test our third hypothesis and to assess the importance of the connectedness of regional social capital stemming from associational networks, we classify the abovementioned associations as connected or isolated based on their members’ multiple memberships (Kwon et al., 2013; Paxton, 2002). To do so, we calculate each association’s connectedness score as the average number of their members’ memberships in other associations. For example, an individual can be a member of a sports club, and also a member of an environmental association and a political party, meaning two memberships in other associations. Third world development and human rights groups are the most connected with a connectedness score of 3.6, implying that the average member of this association is at the same time a member of 3.6 other associations. On the other hand, sports and recreation groups are the least connected with a connectedness score of 1.6. We classify an association as connected if its connectedness score is above or equal to the median connectedness score across all associations, which is 2.5, and as isolated if its connectedness score is below the median. 7

The following associations are classified as connected: welfare organizations, local community action, third world development and human rights groups, environment, ecology, and animal rights groups, youth work, women’s groups, and health organizations. On the other hand, religious organizations, cultural activities, trade unions, political parties and groups, professional associations, and sports and recreation associations are classified as isolated. We take the regional mean membership in connected and isolated associations by linking individuals’ memberships in associations to the above classification. If an individual is embedded in both a connected and an isolated association, we classify this individual as connected since this captures networks and possible multiplier effects more adequately.

Control Variables

We include control variables at the individual, regional, and country level. At the individual level, we include a standard series of sociodemographic characteristics which have been shown to correlate with entrepreneurship (Parker, 2018). Specifically, we control for age and age-squared, gender, and education. We measure education by using an ordered 4-step scale of the age at which the individual finished full-time education ranging between (1) no formal education, (2) up to age 15, (3) between age 16 and 19, and (4) over 20 years of age. We also control for current occupation by including dummies for individuals in full-time education, who stay at home full-time, and people in (active) unemployment. 8 Finally, we control for parental self-employment by including a dummy variable indicating if a person’s parents (either mother or father or both) are or were self-employed.

Regional control variables were obtained from Eurostat’s regional database (Eurostat, 2017). We include (log) regional gross domestic product (GDP) per capita (Hundt & Sternberg, 2016), as well as regional human capital measured in average years of schooling. 9 We also control for the regional share of employment in R&D (Audretsch & Keilbach, 2007) and the regional unemployment rate (Stuetzer et al., 2014). As a region’s industrial structure may affect entrepreneurship (Chinitz, 1961), we also control for the share of employment in the industrial sector (of the population aged 25–64). 10 Furthermore, we control for agglomeration effects proxied for by population density. Finally, we control for the population share of young adults, defined as those between 18 years and 35 years of age. We lag all regional control variables by 1 year to reduce potential endogeneity concerns. Thus, control variables for the years 2006, 2009, and 2011 are matched to the Flash Eurobarometer data from 2007, 2010, and 2012, respectively.

We control for country effects by including 21 (N − 1) country dummies. These country fixed effects control for differences in formal institutions which influence entrepreneurship (Djankov et al., 2002; Estrin et al., 2017; Levie & Autio, 2011), such as property rights protection, rule of law, or formal entry barriers, as well as a host of other potentially confounding effects, which vary primarily at the country level. By including country fixed effects and focusing on sub-national variation we are able to disentangle the effect of regional social capital from confounding factors such as formal institutions.

Method

We estimate the influence of individual- and regional-level variables on the likelihood that individuals have advanced beyond a certain engagement stage in the venture creation process by comparing individuals who are in a given stage with individuals who have advanced further. Individuals are nested in regions and countries, which necessitates the estimation of multilevel models (Snijders & Bosker, 2012). Specifically, we estimate the following mixed-effects multilevel logit model:

where i, r, c, and y denote individuals, regions, countries, and survey waves, respectively.

Results

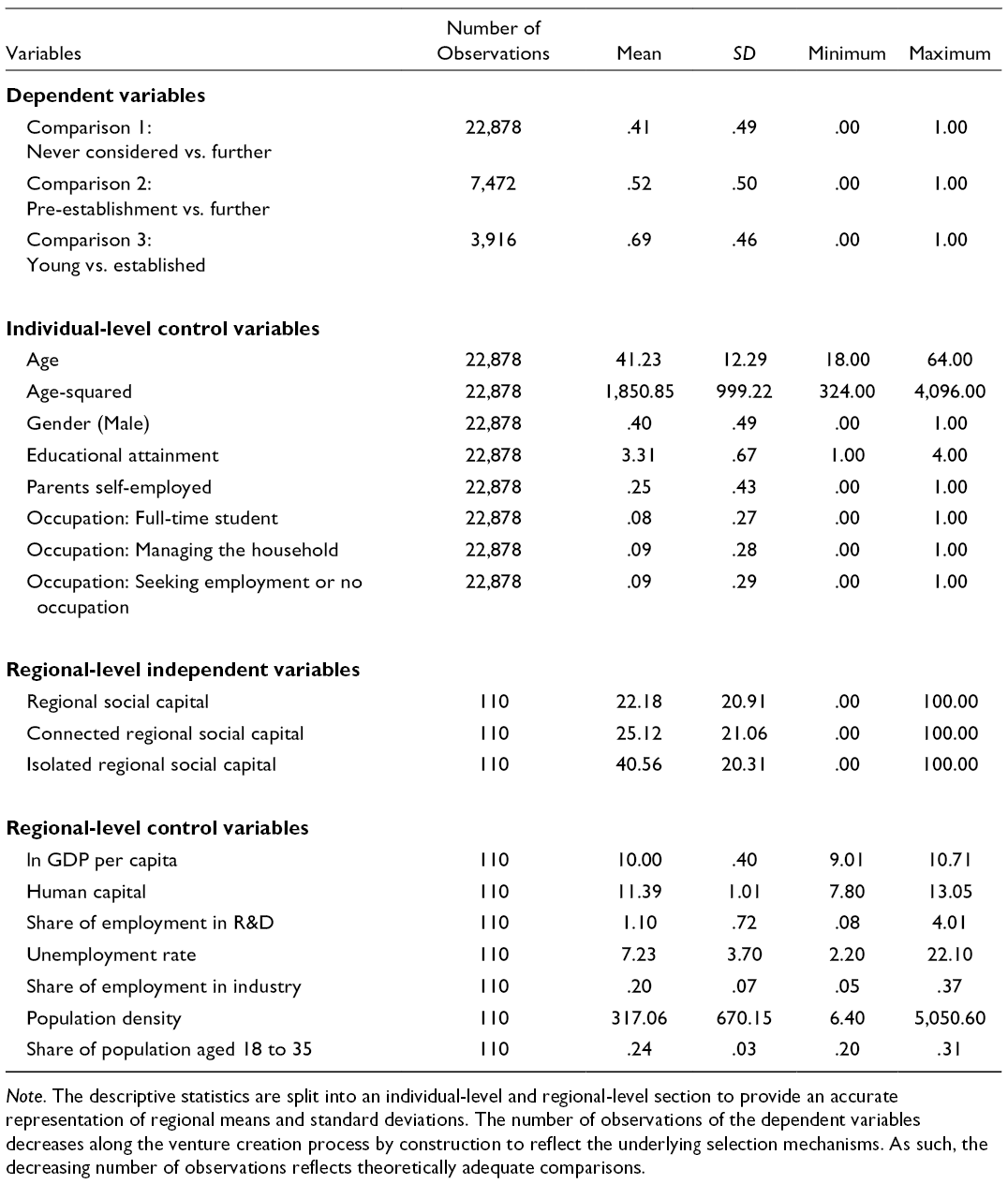

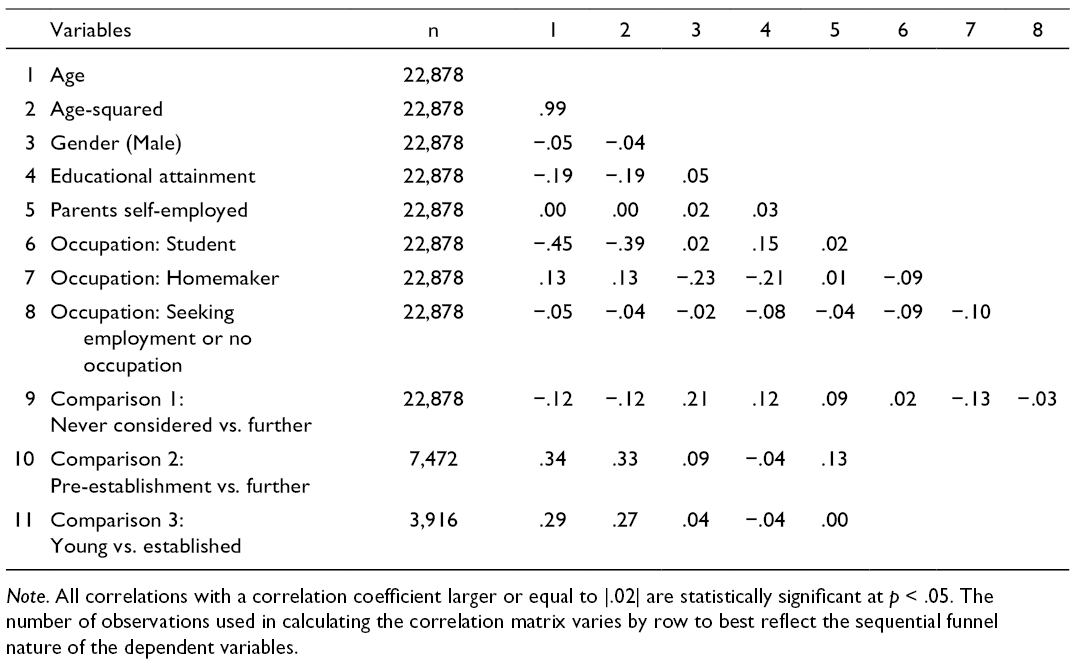

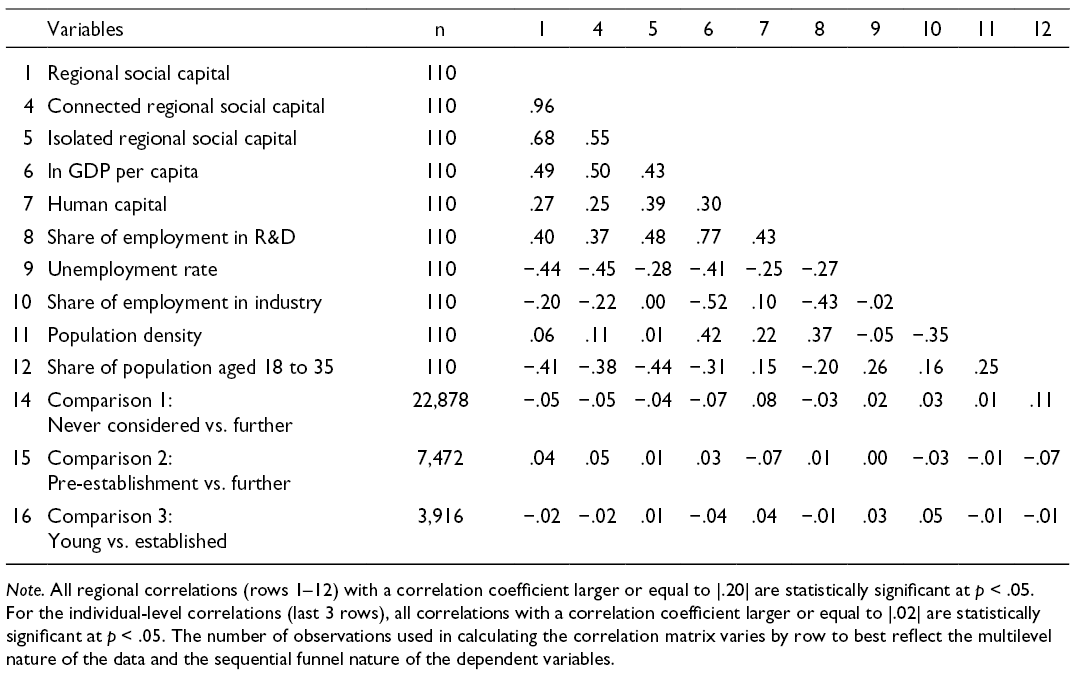

Table 1 presents descriptive statistics for all variables. Correlation matrices are presented in Table 2 (individual level) and Table 3 (regional level). To assess multicollinearity, variance inflation factors (VIFs) were computed for all individual and regional variables. All VIFs were below the critical threshold of 5, thus indicating that multicollinearity is not an issue.

Summary Statistics.

Note. The descriptive statistics are split into an individual-level and regional-level section to provide an accurate representation of regional means and standard deviations. The number of observations of the dependent variables decreases along the venture creation process by construction to reflect the underlying selection mechanisms. As such, the decreasing number of observations reflects theoretically adequate comparisons.

Individual-Level Correlation Table.

Note. All correlations with a correlation coefficient larger or equal to |.02| are statistically significant at p < .05. The number of observations used in calculating the correlation matrix varies by row to best reflect the sequential funnel nature of the dependent variables.

Regional-Level Correlation Table.

Note. All regional correlations (rows 1–12) with a correlation coefficient larger or equal to |.20| are statistically significant at p < .05. For the individual-level correlations (last 3 rows), all correlations with a correlation coefficient larger or equal to |.02| are statistically significant at p < .05. The number of observations used in calculating the correlation matrix varies by row to best reflect the multilevel nature of the data and the sequential funnel nature of the dependent variables.

Intraclass Correlation Coefficients

To calculate the respective shares of individual-, regional-, and national-level variance for the three dependent variables, we estimate empty multilevel models including only random terms at the regional and at the country level. This enables us to establish whether or not there are autonomous contextual effects at the regional and national level. The share of variance explained by regional effects is 4.6% for the likelihood that individuals have become interested and engaged in entrepreneurship (Comparison 1), 4.9% for the odds that individuals have moved beyond wanting to start a venture (Comparison 2), and 1.6% for the likelihood that young ventures have become established (Comparison 3). The intraclass correlation coefficients for the country level are 4.3%, 4.8%, and 1.6%, respectively. While these intraclass correlation coefficients can be classified as small in an absolute sense (Peterson et al., 2012), they are in line with extant research. Hundt and Sternberg (2016) report intraclass correlation coefficients between 1.4% and 2.1% at the regional level and between 3.0% and 5.1% at the country level. Likelihood-ratio tests confirm the relevance of higher-order (national and regional) effects and thus the need to use multilevel models for all three dependent variables (p < .000). The statistical relevance of regions corroborates our theoretical premise of the regionally embedded nature of entrepreneurship (Feldman, 2001; Fritsch & Storey, 2014; Saxenian, 1994).

Estimation Results

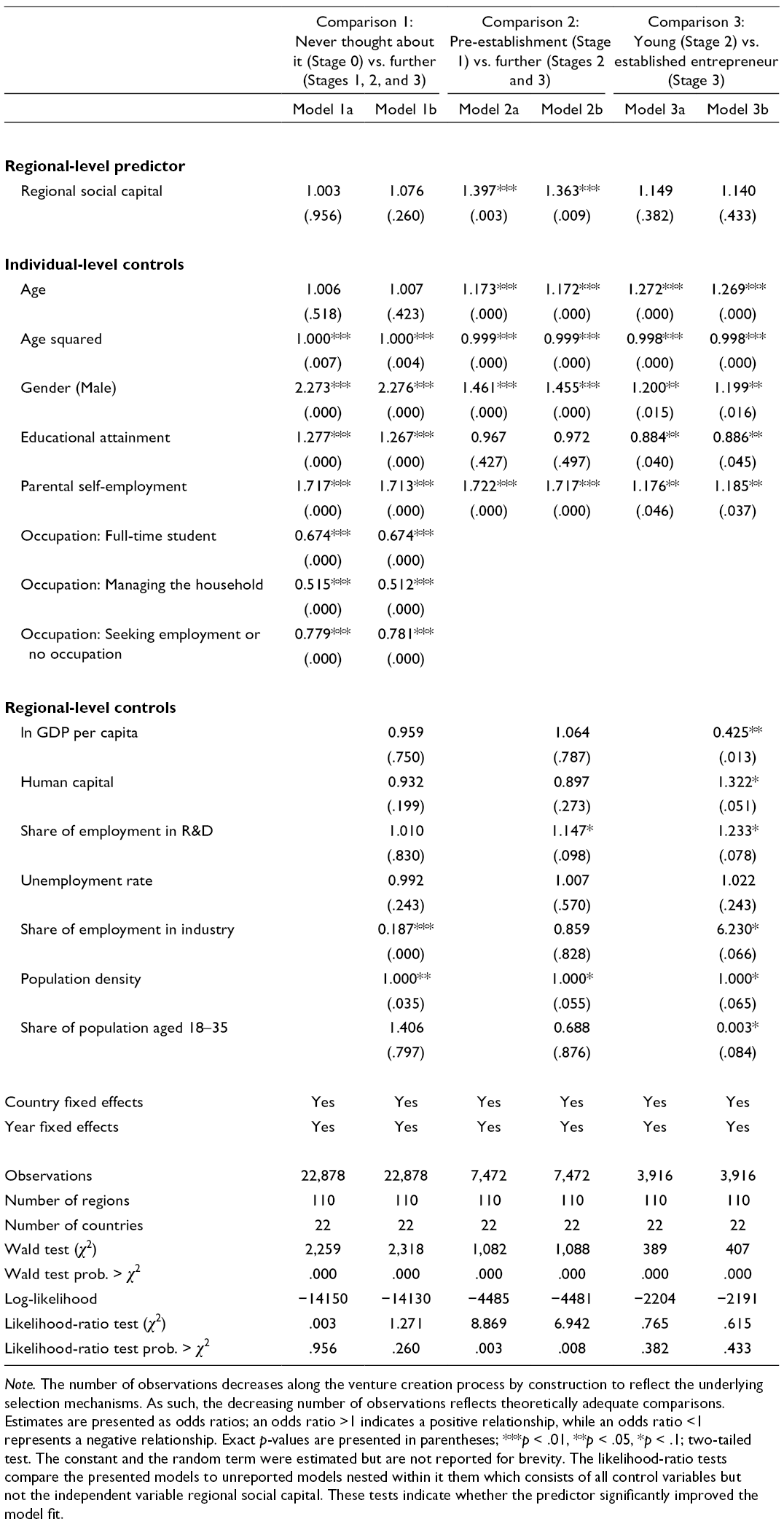

Our hypotheses predict a positive but stage-specific effect of regional social capital on the venture creation process. Specifically, our first hypothesis predicts that the impact of regional social capital on the likelihood that individuals have advanced beyond the pre-establishment stage and formally started a venture (Comparison 2) is larger than the impact of regional social capital on the likelihood that individuals have moved beyond not considering entrepreneurship towards active engagement (Comparison 1). Hypothesis 2 predicts that the effect of social capital on the likelihood of having moved beyond pre-establishment (Comparison 2) is larger than its impact on the likelihood of a young venture having become established (Comparison 3). Models 1a, 2a, and 3a of Table 4 report the direct effects of regional social capital related to Comparisons 1, 2, and 3 after controlling for individuals’ characteristics. Models 1b, 2b, and 3b in Table 4 show the corresponding results when controlling not only for individual- but also regional-level characteristics. The results for regional social capital are stable across the model specifications.

Multilevel Logistic Regression on the Relation Between Social Capital and the Different Stages of the Venture Creation Process (odds ratios and p-values).

Note. The number of observations decreases along the venture creation process by construction to reflect the underlying selection mechanisms. As such, the decreasing number of observations reflects theoretically adequate comparisons. Estimates are presented as odds ratios; an odds ratio >1 indicates a positive relationship, while an odds ratio <1 represents a negative relationship. Exact p-values are presented in parentheses; ***p < .01, **p < .05, *p < .1; two-tailed test. The constant and the random term were estimated but are not reported for brevity. The likelihood-ratio tests compare the presented models to unreported models nested within it them which consists of all control variables but not the independent variable regional social capital. These tests indicate whether the predictor significantly improved the model fit.

We find a positive significant effect of regional social capital on the likelihood that individuals have advanced beyond the pre-establishment stage to higher engagement levels by formally having started a venture (Comparison 2; odds ratio: 1.363; p = .009). All else equal, a one standard deviation increase in regional social capital increases the likelihood that an individual has progressed beyond the pre-establishment stage by 36% ((1 − 1.363) × 100). We do not observe significant effects of regional social capital when comparing individuals who are not considering entrepreneurship with individuals who have become interested and engaged in entrepreneurship (Comparison 1; odds ratio: 1.076; p = .260), or when comparing young ventures with established ventures (Comparison 3; odds ratio: 1.140; p = .433).

We formally test whether the effect of regional social capital differs for these three comparisons. We reject the null hypothesis of equal effects of regional social capital in Comparison 2 and Comparison 1 (Model 2b vs. Model 1b: p = .083), but we cannot reject the null of no difference between the effects of regional social capital in Comparison 2 and Comparison 3 (Model 2b vs. Model 3b: p = .387) due to the large standard error of the coefficient estimate for regional social capital in Model 3b. Likelihood-ratio tests show, though, that adding regional social capital to models containing only the individual-level and regional-level control variables significantly improves the model fit for Comparison 2 (p = .008), but not in Comparison 1 or Comparison 3.

We conclude that there is evidence for a positive but changing effect of regional social capital. Regional social capital has the largest effect on the likelihood of having moved beyond the pre-establishment stage by formally establishing a venture (Comparison 2), but we find no evidence that social capital influences the likelihood of becoming interested and engaged in entrepreneurship (Comparison 1) or the likelihood of growing from a young venture to an established venture (Comparison 3). These findings support Hypotheses 1 and 2.

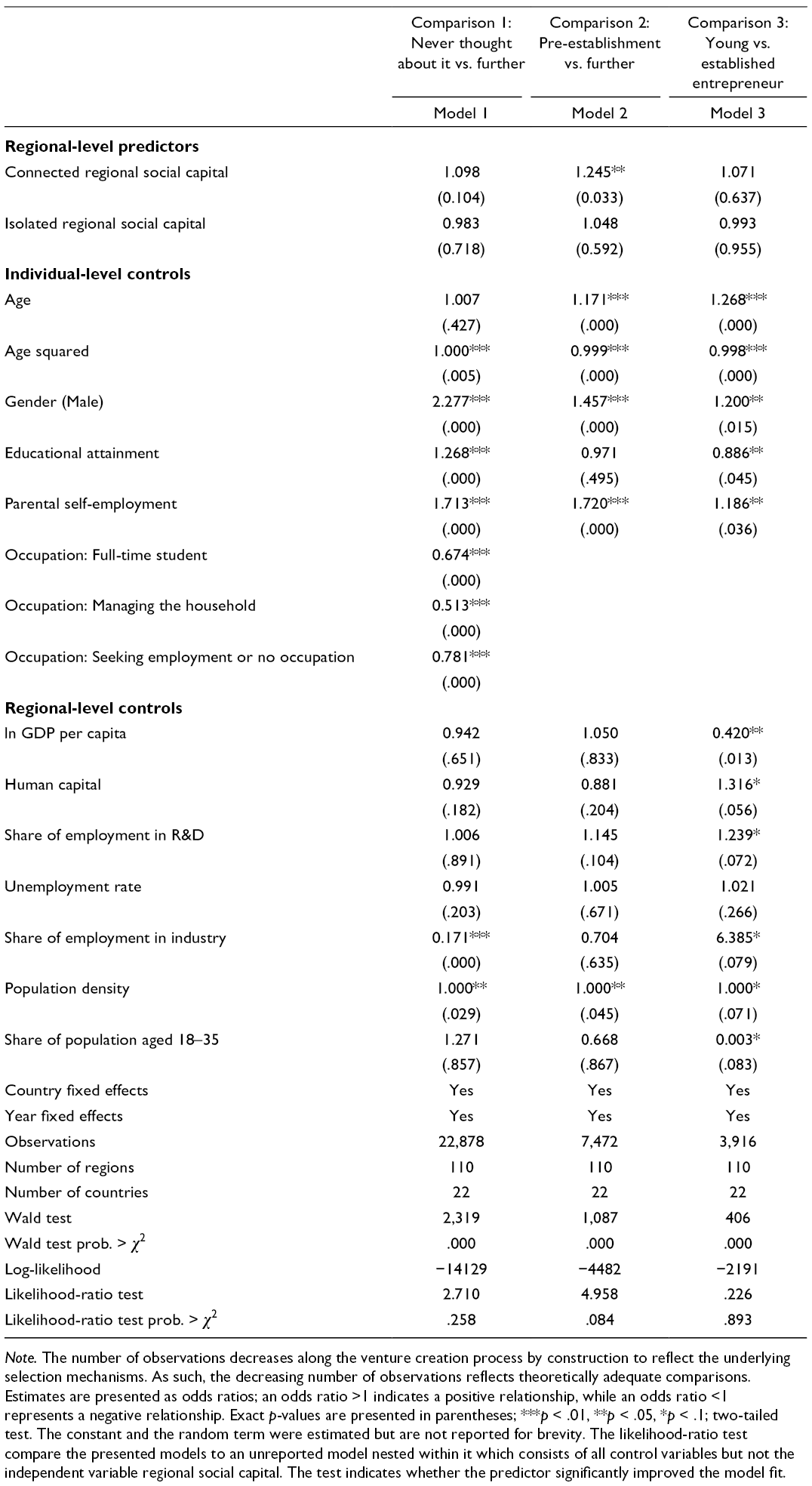

Our third hypothesis relates to the differential effects of connected and isolated social capital. The results are presented in Table 5. For brevity and readability, we only present the horserace regressions in which both connected and isolated regional social capital are included. Regional social capital of the connected kind is positively and significantly related to the likelihood of having moved beyond the pre-establishment stage (Comparison 2; odds ratio: 1.245; p = .033), whereas regional social capital of the isolated kind is not (odds ratio: 1.048; p = .592). Neither connected nor isolated regional social capital exert a statistically significant effect on initial interested and engagement in entrepreneurship (Comparison 1; odds ratio: 1.098; p = .104, and odds ratio: 0.983; p = .718, respectively). We also do not find significant effects of connected or isolated regional social capital on the likelihood that young ventures have become established (Comparison 3; odds ratio: 1.071; p = .637, and odds ratio: 0.993; p = .955, respectively). This supports Hypothesis 3.

Multilevel Logistic Regression on the Relation Between Social Capital and the Different Stages of the Venture Creation Process for Different Types of Social Capital (odds ratios and p-values).

Note. The number of observations decreases along the venture creation process by construction to reflect the underlying selection mechanisms. As such, the decreasing number of observations reflects theoretically adequate comparisons. Estimates are presented as odds ratios; an odds ratio >1 indicates a positive relationship, while an odds ratio <1 represents a negative relationship. Exact p-values are presented in parentheses; ***p < .01, **p < .05, *p < .1; two-tailed test. The constant and the random term were estimated but are not reported for brevity. The likelihood-ratio test compare the presented models to an unreported model nested within it which consists of all control variables but not the independent variable regional social capital. The test indicates whether the predictor significantly improved the model fit.

Beyond the hypothesized relationships, the control variables exhibit interesting patterns as shown in Table 4. At the individual level, we find that the inverse-U-shaped relationship between age and our dependent variables gets more pronounced at higher stages of entrepreneurial engagement levels. Moreover, we observe that the gender gap in entrepreneurship decreases over the venture creation process. The effect of educational attainment on entrepreneurship is contingent upon the degree of engagement. More educated individuals are more likely to think about entrepreneurship, but their likelihood of running an established business is statistically lower. The effect of parental self-employment is positive and significant for all comparisons.

Robustness Analysis

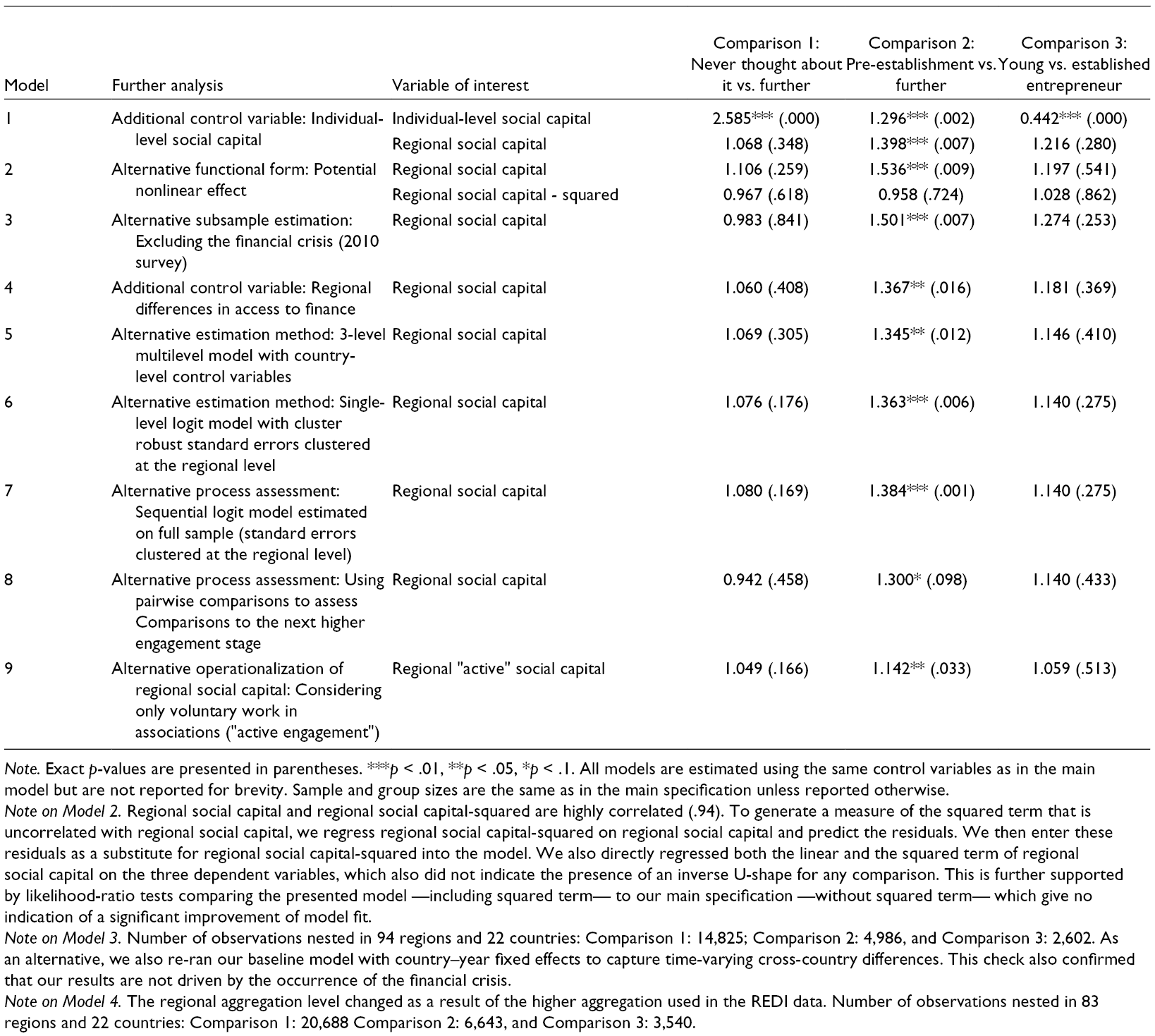

To corroborate our findings, we run a number of additional tests. The results are presented in Table 6. For brevity and readability, we present only the coefficients of interest of the fully specified models.

Robustness Analyses (odds ratios and p-values).

Note. Exact p-values are presented in parentheses. ***p < .01, **p < .05, *p < .1. All models are estimated using the same control variables as in the main model but are not reported for brevity. Sample and group sizes are the same as in the main specification unless reported otherwise.

Note on Model 2. Regional social capital and regional social capital-squared are highly correlated (.94). To generate a measure of the squared term that is uncorrelated with regional social capital, we regress regional social capital-squared on regional social capital and predict the residuals. We then enter these residuals as a substitute for regional social capital-squared into the model. We also directly regressed both the linear and the squared term of regional social capital on the three dependent variables, which also did not indicate the presence of an inverse U-shape for any comparison. This is further supported by likelihood-ratio tests comparing the presented model —including squared term— to our main specification —without squared term— which give no indication of a significant improvement of model fit.

Note on Model 3. Number of observations nested in 94 regions and 22 countries: Comparison 1: 14,825; Comparison 2: 4,986, and Comparison 3: 2,602. As an alternative, we also re-ran our baseline model with country–year fixed effects to capture time-varying cross-country differences. This check also confirmed that our results are not driven by the occurrence of the financial crisis.

Note on Model 4. The regional aggregation level changed as a result of the higher aggregation used in the REDI data. Number of observations nested in 83 regions and 22 countries: Comparison 1: 20,688 Comparison 2: 6,643, and Comparison 3: 3,540.

One alternative explanation for our regional social capital effect is that it may proxy for individual-level social capital. 12 As our database does not contain a variable capturing individual-level social capital, we apply multiple-imputation techniques (Rubin, 1987; Schafer, 1999). We predict individual-level social capital scores for the individuals in our Flash Eurobarometer sample by using information on individuals’ connectedness to other entrepreneurs which is a frequently used proxy for individual-level social capital (Arenius & Minniti, 2005; Estrin et al., 2013), from the Global Entrepreneurship Monitor (GEM) 2011 and 2012 surveys (Reynolds et al., 2005). 13 In the first stage, we use the GEM sample of 95,309 individuals from 20 countries (all countries used in this study except for the Czech Republic and Bulgaria) and regress individuals’ social capital on individuals’ characteristics —the same variables we used as controls in Table 4— and in which stage of the venture creation process individuals are —coded as before and shown in Figure 2—. This first stage imputation (logit) regression predicts 70% of the individual-level social capital variable correctly, which indicates a good fit. We then use the estimated relationships to multiple-impute individual-level social capital scores for the individuals in our Flash Eurobarometer sample (Rubin, 1987; Schafer, 1999) and re-estimate our main model with individual-level social capital as an additional control variable. 14 Results are presented in Model 1 in Table 6. Individual-level social capital is a significant predictor in Comparison 2 (odds ratio: 1.296; p = .002). Its inclusion, however, does not alter the effect of regional social capital in Comparison 2 (odds ratio: 1.398; p = .007). Hence, we have no reason to believe that our measure of regional social capital only picks up variation in individual-level social capital.

Second, we test whether the positive effects of regional social capital are nonlinear. We argued that regional social capital facilitates entrepreneurship by fostering norms of cooperation, generalized reciprocity, and through externalities associated with network reach and density. Yet, the benefits associated with regional social capital may be offset for very high levels of regional social capital as it may be costly to honor the obligations resulting from a large heterogeneous network (Malecki, 2012; Uzzi, 1997). Thus, the relationship between regional social capital and the likelihood of transitioning through the various stages of the venture creation process may follow an inverse U-shape (Laursen et al., 2012b). Regression results including a nonlinear term of regional social capital are presented in Model 2 in Table 6. There is no evidence of a nonlinear influence of regional social capital, which is corroborated by likelihood-ratio tests indicating that the additional term does not improve the model fit for any of the three comparisons (p = .618; p = .725; p = .862, respectively).

Third, we test whether our results are affected by the 2009–2010 economic recession which occurred in our sample period. To do so, we exclude all observations from the 2010 survey wave and re-estimate our main specification using only information from the survey waves collected before and after the European debt crisis (collected in 2007 and 2012). 15 Results are presented in Model 3 in Table 6. Using this subset of 14,825 observations nested in 94 regions and 22 countries, we continue to observe a positive and significant effect of regional social capital in Comparison 2 (odds ratio: 1.501; p = .007). Hence, the European debt crisis does not bias our main findings.

Fourth, we test whether our results are robust to controlling for sub-national differences in entrepreneurial financing. While access to finance is overwhelmingly determined at the country level (which we control for using country fixed effects), there may be regional differences. To empirically control for regional differences, we use the regional entrepreneurial financing indicator from the Regional Entrepreneurship and Development Index (REDI) project (Szerb et al., 2013). The REDI uses a higher regional aggregation and no data are available for Bulgaria, Romania, and Slovenia. Thus, we retain 20,688 individuals nested in 83 regions and add regional entrepreneurial finance as an additional control variable. As can be seen from the results of Model 4 in Table 6, our main results regarding social capital are unaffected by this (odds ratio: 1.367; p = .016).

Finally, we run various robustness checks of empirical nature which we also present in Table 6. In Model 5, we employ a three-level quasi-fixed effects multilevel model by substituting the country fixed effects for random country terms and country-level controls. For the latter, we utilize the same (lagged) variables as at the regional level, and we control additionally for institutional quality at the country level. This variable is measured as the first principal component of the six Worldwide Governance Indicators (Kaufmann et al., 2011). 16 In Model 6, we re-estimate the main model using a (single-level) logit model with robust standard errors clustered at the regional level. In Model 7, we estimate a sequential logit model (Agresti, 2010; Mare, 1981; Tutz, 1991) where all comparisons are estimated simultaneously (Buis, 2007). We cluster the standard errors at the regional level. In Model 8, we make pairwise comparisons between individuals in one stage of the venture creation process and individuals in the subsequent stage, excluding those who are already at a more advanced stage. 17 Finally, in Model 9, we utilize an alternative operationalization of regional social capital by following Beugelsdijk and van Schaik (2005). We consider only those individuals who work voluntarily in associations —rather than being members, as in our main indicator— to capture so-called “active” social capital.

None of these changes alter our main findings; regional social capital positively and significantly influences the likelihood that individuals have moved beyond the pre-establishment stage by formally establishing a venture (Comparison 2), but has no influence on developing an initial interest and getting engaged in entrepreneurship (Comparison 1) or on the likelihood of venture survival (Comparison 3). Formally testing whether the effect of regional social capital differs across these three comparisons, we corroborate our previous findings: We reject the null hypothesis that the effect of regional social capital is the same in Comparisons 1 and 2, but we cannot reject the null of no differences in the effect of regional social capital in Comparisons 2 and 3.

Discussion

This study integrates the dynamic process view (Bhave, 1994; Greve & Salaff, 2003) with the contextualized multilevel conceptualization of entrepreneurship (Autio et al., 2013; Estrin et al., 2013; Kwon & Arenius, 2010) against a background of societal social capital theory (Putnam, 1993, 2000) to introduce the regionally embedded venture creation process. We predict that regional social capital has a positive influence on the likelihood of advancing through the venture creation process, and the effect should be largest when entrepreneurs seek to move from thinking about entrepreneurship to formally establishing a business.

We test our theoretical predictions using data from 22,878 individuals located in 110 regions within 22 European countries. Our empirical analysis documents a positive yet changing influence of regional social capital on the venture creation process. The effect is largest when comparing individuals who have become interested and engaged in entrepreneurship with individuals who have formally launched and developed a venture. If two otherwise identical individuals attempt to formally launch a venture, the person doing so in a region characterized by higher levels of regional social capital has higher odds of succeeding. We also report stronger positive effects of regional social capital of the connected type on entrepreneurship than of regional social capital of the isolated type. This is in line with our theoretical argument highlighting enhanced information, knowledge, and resource flows, as well as positive externalities associated with interconnected cross-cutting network membership in civic associations.

Limitations

Ideally, we would have used panel data to explore how regional social capital is related to the venture creation process. Unfortunately, none of the existing panel data sets such as the Panel Study of Entrepreneurial Dynamics I and II (Reynolds & Curtin, 2008) can be used as they only provide information for single countries and a substantially smaller number of individuals. This lack of panel data explains our choice to leverage cross-sectional data to relate regional social capital to individuals’ steps in the venture creation process (see also e.g. Mickiewicz et al., 2017; Peroni et al., 2016; Van Der Zwan et al., 2013). Future research using longitudinal designs would be desirable and enable researchers to follow individuals as they transition through the venture creation process, rather than inferring individuals’ likelihood of transitioning indirectly based on comparisons between individuals in different entrepreneurial engagement stages. This would allow for more in-depth analyses of how the regional social environment influences entrepreneurship.

While our study finds positive effects of social capital on the venture creation process we cannot be sure that they are indeed of a causal nature as hypothesized by our theory. Yet, given that individuals cannot directly influence the social capital in their region in the short- and medium run, and in light of the fact that we control for a host of individual- and regional-level and all country-level characteristics, we are confident to have presented robust evidence for the hypothesized relations.

We pay particular attention to the spatial scale by moving from the national level of analysis (e.g. Estrin et al., 2013; Kwon & Arenius, 2010) to regions as an important meso-level (Kim et al., 2016; Kwon et al., 2013). We note that the geographical scale of assessing societal social capital effects is not entirely clear and that social capital may operate at even lower levels of disaggregation such as communities and neighborhoods (Kim et al., 2016; Malecki, 2012; Mickiewicz et al., 2017). We have focused on structural social capital (Putnam, 2000; Woolcock, 2001) to inform the mechanisms operating at the regional level, but we note that future work may also assess alternative social capital constructs such as generalized trust. We follow the tradition of assessing societal social capital, which is rooted in sociology, political science, and economics (Knack & Keefer, 1997, Kwon et al., 2013; Paxton, 1999, 2002; Putnam, 2000). Yet we note that insights from thick contextualized studies may offer complementary insights (Anderson & Jack, 2002; Anderson et al., 2007).

Contributions

Our findings contribute to comparative entrepreneurship research in three ways, collectively leading to an important extension of comparative entrepreneurship theory. First, our result on the changing influence of regional social capital on venture emergence over the venture creation process extends Kwon et al. (2013) by unpacking the venture creation process. Our finding that regional social capital is most relevant when entrepreneurs attempt to assemble the various information, resources, and knowledge needed to formally start their business complements individual-level research documenting that entrepreneurs heavily utilize their networks and contacts prior to firm foundation (Greve & Salaff, 2003).

Second, our study suggests that regional social capital that was generated in a noneconomic context can successfully be deployed in an economic context to foster the acquisition of resources, knowledge, and information. The finding of a stronger effect of regional social capital of the connected type furthermore highlights the positive externalities associated with interconnected cross-cutting associations and the public goods nature of regional social capital (Kwon et al., 2013; Paxton, 2002).

Third, our approach in this paper allows us to distinguish the effects of regional social capital on different transitions during the venture creation process. This provides a methodological advantage over extant approaches in the comparative entrepreneurship literature where the underlying process of establishing a venture is frequently inferred from an empirical relation between macro-level independent variables and either intermediate indicators, such as GEM’s Total Entrepreneurial Activity, or final outcomes, such as self-employment indicators. A drawback of these approaches is that one has to either assume that the influence of the determinants of entrepreneurship is stable over the entire venture creation process or interpret the found effects as net effects. If no evidence of a relationship between a potential antecedent and entrepreneurship is found, this is commonly interpreted as evidence for the absence of an effect. Yet, our study shows that this conclusion may be premature as it could also be explained by offsetting effects during the distinct stages of the venture creation process.

Collectively, these contributions lead us to rethink a key assumption in entrepreneurship theory: the (implicit) assumption of a uniform impact of contextual factors on the different stages of the venture creation process. By demonstrating that the effect of certain contextual characteristics —specifically, regional social capital— changes over the course of the venture creation process we highlight the need to relax the assumption of uniformity in comparative entrepreneurship theory. Doing so is a natural evolution of entrepreneurship theory. Recent advancements highlight the need to unpack the venture creation process into different stages (Baker et al., 2005; Mickiewicz et al., 2017) and stress the importance of contextual embeddedness (Kim et al., 2016; Welter, 2011). Uniting these perspectives, the theoretical implication of our article is the need to relax the assumption of uniformity by assuming variability of contextual effects on the multi-staged venture creation process.

Such variability is not open-ended. A critical condition for incorporating variability in comparative entrepreneurship theory is the theoretical link between entrepreneurial process theory and contextual theory. Social capital theory provides us with a clear description of the mechanisms at the societal level while entrepreneurial process theory informs us on the mechanisms relevant in the various stages at the individual level. We think this approach applies to other research questions as well. For example, institutional theory and its different institutional domains (Scott, 1995, 2014) can be used to explore the role of isomorphic pressures, while cultural value theory and its multiple cultural dimensions (e.g., Hofstede, 2001; Schwartz, 1994, 1999; for reviews see Beugelsdijk, Kostova, Roth et al., 2017; Kirkman, Lowe, Gibson et al., 2006) can be used to explore how specific societal values relate to the different stages of the venture creation process. Incorporating the idea of variability into comparative entrepreneurship research requires theorizing on how each of these domains or dimensions relate to the different stages of the venture creation process.

Implications

Entrepreneurship promotion programs are a priority of many governments and international organizations (European Commission, 2013; OECD, 2010). Whereas many policy initiatives have been directed towards improving formal institutions, our study highlights the role of regional social capital, a regional resource stemming from associational networks. Regional social capital is malleable and subject to less stability than for example (entrepreneurial) culture and it may be strengthened by enhancing the conditions for membership in voluntary organizations. In implementing such policies, it is important to focus on facilitating membership in associations that generate frequent personal contacts between their members and across associations, rather than membership in isolated special-interest organizations whose members never meet personally. Policy interventions such as the provision of physical meeting spaces that can be used by multiple associations and subsidies for associations could enhance membership in voluntary associations and foster the emergence of social capital.

Second, the contextually embedded process perspective developed in our paper offers a way to enhance the development and evaluation of policy interventions targeted at fostering entrepreneurship. Our approach provides fertile ground for assessing the influence of entrepreneurship promotion programs and entrepreneurial ecosystems from a dynamic perspective. When developing group-, regional-, or national-level interventions, such as subsidies, training, and networking programs, the process perspective should be taken into consideration. Interventions that aim to raise entrepreneurial potential may not necessarily be sustainable in the sense that they lead to successful established businesses. Entrepreneurial intentions are also not necessarily a good measure of subsequent entrepreneurial action and survival. Evidence-based policy-making would benefit from a multistaged dynamic assessment of interventions that delivers a more comprehensive picture than the analysis of intermediate or final outcomes.

In conclusion, this study puts forward a perspective that positions entrepreneurship as a dynamic and regionally embedded process. Regional social capital facilitates entrepreneurship, but its impact is conditional upon the specific situational characteristics entrepreneurs are confronted with.

Supplemental Material

Supplementary Material 1 - Supplemental material for The Changing Role of Social Capital During the Venture Creation Process: A Multilevel Study

Supplemental material, Supplementary Material 1, for The Changing Role of Social Capital During the Venture Creation Process: A Multilevel Study by Johannes Kleinhempel, Sjoerd Beugelsdijk and Mariko J. Klasing in Entrepreneurship Theory and Practice

Footnotes

Acknowledgements

The authors would like to thank the editor, Erik Stam, the anonymous reviewers, Saul Estrin and Tobias Grohmann, as well as participants at the Academy of Management Conference 2019, Babson College Entrepreneurship Conference 2018, RENT XXXII 2018, European International Business Academy Conference 2018; and seminar participants at Carlos III University of Madrid, the University of Groningen, and the University of Manchester for comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.