Abstract

Professional athletes are workers: sport is their job. Yet they are excluded from workers’ compensation schemes. This denies them the safety net provided to other Australian workers. In a world in which sport has been corporatised and commercialised, their exclusion is inequitable and anachronistic. At the same time, however, sport is different. The frequency with which injuries occur, and the speed with which they must be treated and athletes returned to play (work), do not lend themselves to bureaucratic compensation schemes. What is needed is a bespoke scheme – one tailored to professional sports’ unique needs and risk profile.

The committee encourages professional sports organisations to ensure their athletes have insurance coverage for head trauma. The committee also encourages state and territory governments to engage with professional sporting organisations to explore how the general exclusion of professional sports people from various state and territory workers’ compensation schemes could be removed.

1

This was the September 2023 recommendation of the Senate Community Affairs References Committee inquiry into concussions and repeated head trauma in contact sports – a recommendation reached after considering 92 submissions and hearing from 87 witnesses over four days of public hearings.

In its response to the inquiry report, the federal government stated that while it does not have responsibility for the matters outlined in the recommendation, it will raise them with professional sporting codes and discuss them with state and territory governments. 2

Yet for all the rhetoric, there has been no evident progress. 3 In some respects this is not surprising. Federal, state and territory governments are unlikely to embrace a recommendation that could potentially add new and uncertain liabilities to their already financially stressed workers’ compensation schemes. 4 Nor are the sports organisations that employ sportspeople (principally clubs competing in team-based leagues) likely to entertain new and uncertain insurance premiums. What is somewhat surprising, however, is the lack of enthusiasm shown by athlete representatives. It has not featured prominently on their agendas. Maybe it has been placed in the ‘too hard basket’?

The purpose of this article is to remove the issue from the too hard basket and to provide a much-needed starting point for addressing the Senate Committee’s recommendation. It does so in three parts. First, the article outlines the factors that led the Committee to the above recommendation. Second, the article focuses on one of those factors – sportspeople’s exclusion from state and territory workers’ compensation schemes – and explains why that exclusion today is inequitable and ‘anachronistic'. 5 And third, the article outlines what a future sport injury insurance scheme might look like.

The basis for the Senate Committee’s recommendation

The Senate Committee’s recommendation is based on two key conclusions: (1) that sport-related concussion and head trauma is a significant public health issue; 6 and (2) that existing insurance, compensation and support arrangements are deficient and inadequate. 7

With respect to the first factor, the Committee concluded: There is clear evidence of a causal link between repeated head trauma and concussions and subsequent neurodegenerative diseases such as CTE [chronic traumatic encephalopathy]. While important research questions remain regarding the degree of causation and the nature of long-term impacts, these questions should not be used to undermine the fundamental nature of that link.

8

And with respect to the second factor, the Committee highlighted the following points: • The inadequacy of insurance, compensation and other supports provided by sports organisations. The Committee noted that insurance, compensation and other support mechanisms varied according to the level of competition being played and the financial resources of the organisation – and that while some sports had established funds to assist athletes suffering hardship (including from the long-term effects of concussion and repeated head traumas), which funds sports organisations tout as evidence they are addressing the issue, payouts from these so-called hardship funds are discretionary, their continued existence contingent, and their adequacy unknown;

9

• The inadequacy of the private insurance market. Here the Committee made two important observations. First, that while collective bargaining agreements commonly place contractual obligations upon athletes to take out and maintain top level private health insurance, and upon clubs and leagues to pay any excess medical costs, these obligations generally cease between six and 18 months after the expiry of the athlete’s contract and well before the long-term effects of concussion and repeated head-trauma reveal themselves and the need for insurance is most acute.

10

And second, while a number of sport superannuation plans provide athletes with total and permanent disability insurance cover, the terms of those policies can exclude injuries caused by sports related concussions and head trauma

11

– a likelihood that has only increased since the Committee’s report, with Zurich Insurance Group’s July 2024 announcement that its Active policy (a policy designed specifically for persons living active – that is, sporty – lives) will no longer cover concussion-related injuries for people playing high-contact sports such as Australian rules football, rugby and boxing; ‘the uncertain health impacts and risks associated with concussion events from playing high-contact sports and the subsequent development of chronic traumatic encephalopathy (CTE)’ being the driving force behind its decision.

12

• The inequitable exclusion of sportspeople from state and territory workers’ compensation schemes. I will turn to this in the second part of the article. • The speculative nature of civil litigation. The Committee noted numerous procedural and substantive barriers faced by athletes seeking common law remedies for concussion and head trauma-related claims that render litigation speculative and a sub-optimal mechanism for securing compensation and support.

13

Exclusion from state and territory workers’ compensation schemes

The exclusions of athletes from state and territory workers’ compensation schemes were introduced in the mid-1970s – a time of growing professionalism of sport in this country – and in response to a series of decisions that found professional athletes were entitled to workers’ compensation at a time when the prevailing industry understanding was that they were not covered. This raised a number of issues and concerns. 14

First was the spectre of potential personal liability of committee members for compensation payments and damages awards to injured athletes – a risk heightened by sports organisations generally being unincorporated at the time. However, today, and almost without exception, sports organisations are incorporated. This change in the factual matrix renders as redundant this rationale for exclusion.

Another justification was a perception that sport is not work. Again, today, professional sportspeople are recognised as workers and employees. There is High Court authority to the point 15 and, with the notable exception of workers’ compensation, the full array of labour laws apply to professional sports organisations and their employee athletes – from obligations to pay income tax and superannuation to statutory obligations to provide a safe workplace. 16

Then there was the justification that most athletes have alternative insurance arrangements in place. The inadequacies of these arrangements have already been discussed.

And nor do sports’ high rates of injury or an athlete’s consent to the risk of that injury constitute valid grounds for exclusion. Workers’ compensation schemes originally were designed to cover – and continue to cover – workers in high-risk industries and occupations. The exclusion of athletes on this ground runs counter to the raison d’etre of workers’ compensation schemes. A high risk of injury is more a compelling reason for inclusion than exclusion. Imagine excluding mining and construction workers because their workplaces are too risky?

This brings us to the (in)capacity of sports organisations to pay workers’ compensation premiums. No doubt the premiums that would attach to many sports would be high. In New Zealand, for example, where its universal no-fault accident compensation scheme covers sporting activities, those activities have the highest claims costs and therefore highest premium rates in the scheme. 17

However, with sports professionalism have come greater financial rewards. Some professional Australian sporting codes measure their revenue in the hundreds of millions of dollars. 18 For them, the issue of capacity to pay arguably no longer arises. But the emphasis here is on the word ‘some’. Not all sports have shared in the spoils of sports’ commercialisation. Some, maybe many, sports organisations may have capacity-to-pay issues. But is this a valid reason for an exemption? Workers’ compensation schemes do not exempt other struggling businesses – let alone provide a blanket exemption for all employers, regardless of revenue. This is more a factor to be taken into account in the design of any scheme, rather than for a blanket exemption.

And this brings us to the final justification proffered at the time of their introduction, that these would be temporary measures pending an alternative scheme. However, only one jurisdiction has introduced an alternative scheme – New South Wales’ Sporting Injuries Insurance Scheme – a no-fault compensation system available to professional and amateur athletes who are registered members of a sporting organisation registered with the Scheme. 19 The Scheme has been described as reflecting a balance struck in the interests of social justice – generous to those who compete as amateurs, providing compensation for injuries that otherwise might not have been compensable, but harsh on professional athletes, providing significantly less compensation than otherwise would be available to them under workers’ compensation. 20 The harshness of the Scheme has led some sports organisations to either replace or supplement its benefits with private insurance. 21 But must it be so harsh?

It is inequitable that professional sportspeople are denied the safety net provided to other Australian workers. In a world in which sport is a sophisticated undertaking, corporatised and commercialised, there is little in the way of rational principle justifying sportspeople’s continued exclusion from coverage. 22

At the same time, sport is different. The frequency with which injuries occur, and the speed at which they must be treated and athletes rehabilitated and returned to play (work), do not lend themselves to bureaucratic compensation schemes. What is needed is a bespoke scheme – one that is tailored to professional sports’ unique needs and risk profile, but which also reflects that, for the professional athlete, sport is their job, and concussion and head trauma is a workplace injury risk.

So, what might this bespoke scheme look like? It is to this question that the article now turns.

A better way forward: A bespoke hybrid private–public scheme

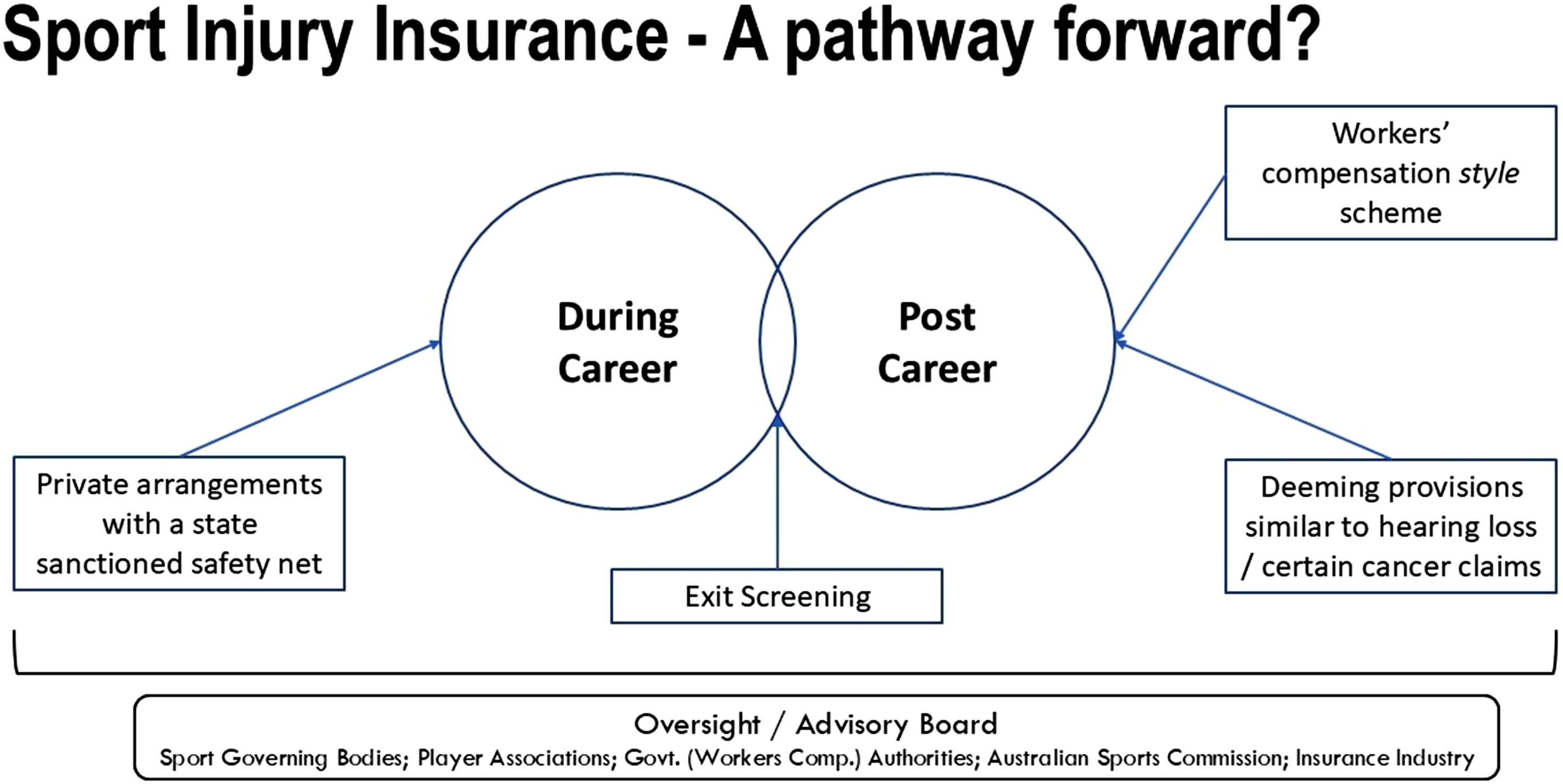

Figure 1 illustrates the key elements of what a future sport injury insurance scheme might look like. What a future sport injury insurance scheme might look like.

Each of its key elements are now explained, starting with the differentiation between during-career and post-career coverage.

During career

During an athlete’s career, private arrangements should prevail – a mix of contractual injury payments and private insurance. Sports need the speed and flexibility they afford. That professional athletes should be covered by top level private health insurance is highly desirable. However, governments should not mandate that sports organisations provide that insurance. Instead, it should be left to contractual negotiations between sports organisations and athlete associations, noting though that this – as is currently the case – will mean insurance and compensation arrangements for professional athletes will vary according to the financial capacity of the sport and the athlete’s bargaining power. This invariably will mean less generous insurance arrangements for athletes competing in sports with less revenue – and where the athletes are often female and/or part-timers.

However, athletes with less bargaining power should be protected by a state sanctioned safety net. Workers’ compensation can be that safety net. This can be achieved by including sports organisations within state and territory workers’ compensation schemes but allowing them to opt out of those schemes if they can establish, to the satisfaction of an appropriate Australian government regulator, that they have in place suitable alternative insurance and compensation arrangements for their athletes.

Precedents exist around which such a scheme could be built. For example, federal, state and territory workers’ compensation schemes provide for employers self-insuring workers’ compensation claims. The federal scheme in particular could be extended to sports organisations providing a national workers’ compensation option for national sporting codes.

Post-career

When the employer-employee nexus is severed, a workers’ compensation-style scheme could apply. There would be an employer premium and government underwriting (the private sector having demonstrated an unwillingness to do so), together with outsourced claims management – maybe to specialist agents.

Working out the details of such a scheme would require significant work – including, among other things, and as the Senate Committee envisaged, determining the financial impact such a reform would have on the various sports organisations across Australia. And all of this would require a significant amount of data to risk rate sports and their risk management processes to establish premium rates.

Exit screening

One thing that would assist in this regard – and would be an important element of any scheme – is end-of-career exit screening of athletes. This would facilitate the early identification, intervention and management of potential high-risk claimants. Better management would also reduce costs, and premiums, and the risk of litigation.

Premium rates

As is the case with workers’ compensation schemes, premiums would be calculated by reference to: • the industry rate – based on the performance of the industry in which the sports organisation operates – which leaves open the possibility for the sporting community to be broken down into different risk-rated industries, with Australian rules football and rugby, for example, having a higher industry rate than, say, cricket, basketball and netball; • the employer’s (sports organisation’s) rateable remuneration – how much it pays its employees – generally being defined broadly to include wages, salaries, superannuation and other benefits payable to workers; and • the employer’s performance rating – where an employer’s individual performance (based on its claims history) is considered relative to other employers operating in the same industry. The larger an individual employer’s rateable remuneration, the greater the weight given to its performance rating (past experience). This allows larger sports organisations to more directly benefit from improvements they make to their injury prevention and management systems, while protecting smaller sports organisations from the volatility that can attach to having few but large claims.

Calculated in this manner, premiums would strike a reasonable balance between industry and individual employer experience. It would also incentivise knowledge transfer between employers (clubs) within an industry (sport), in an effort to reduce that sport’s industry rate – for the benefit of all. Injury prevention, treatment and rehabilitation should not be thought of as a source of competitive advantage.

Deeming provisions

There could also be provisions that deem concussion-related injuries to be due to the athlete’s employment. These provisions would mirror provisions that already exist in workers’ compensation schemes that deem certain diseases to be work-related (for example, cancers associated with work as a firefighter, and hearing loss associated with working in occupations exposed to sustained loud noise). 23

Government oversight

The scheme should be overseen, and the post-career element administered, by a government – maybe workers’ compensation – authority (or authorities, if administered at a state and territory level). There is also the potential to link self-insurance to Australian Sports Commission recognition thereby integrating and leveraging the role of the Commission as the lead Australian government agency responsible for supporting sport and building its governance capability.

Industry advisory board

The government oversight bodies would be supported in their work by an Industry Advisory Board comprising representatives of sport governing bodies, athlete associations and the insurance industry.

Conclusion: Where to from here?

The injury insurance scheme proposed in this article is, in effect, a private–public partnership, reflective of the Senate Committee’s assessment that while sports in Australia are largely governed by private organisations, the significant public health issues involved with sport-related concussion and head trauma necessitate a role for government. 24 It brings professional sports organisations and governments together in a coordinated manner to produce a bespoke injury insurance scheme tailored to the unique circumstances and needs of professional sports and sportspeople. It would provide all Australian professional athletes with insurance and compensation arrangements no less generous than those applying to other Australian workers, and athletes and professional sports organisations with the financial security of government underwriting.

So, how do we make this happen? A working group – mirroring the proposed Industry Advisory Board (above) – should be established to further design and develop the scheme. There also needs to be further research. Important will be actuarial work to size what a premium for insuring athletes might look like. Also valuable would be comparative analyses of other jurisdictions. The United States, for example, has a variety of state-based approaches from which we could learn. 25 There is much work to be done. The time to start is now.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.