Abstract

The Corporations (Aboriginal and Torres Strait Islander) Act 2006 (Cth) is not currently equipped to empower Indigenous Australians to set up their for-profit businesses under its regime due to its rigidity and interventionist approach. This article argues the need for a change. A proposal is put forward to allow for the creation of a new type of corporation under the existing legislative framework for Indigenous entrepreneurs to run their for-profit businesses in a culturally appropriate way.

Indigenous Australians may incorporate Aboriginal and Torres Strait Islander corporations (ATSI corporations) under the Corporations (Aboriginal and Torres Strait Islander) Act 2006 (Cth) (CATSI Act). This current legislation is supposed to empower Indigenous Australians by allowing ATSI corporations to adopt rules that support Indigenous culture and values. 1 As a result, Indigenous Australians are able to take ownership, develop and administer programs that provide essential services to the community, including in the areas of health, education, employment, training, community services and housing.

However, the legislation is also heavily focused on improving ‘governance and capacity’ in the Indigenous corporate sector. 2 Ensuring and enhancing accountability of Indigenous enterprises registered under its predecessor, the Aboriginal Councils and Associations Act 1976 (Cth), was a major driver behind the introduction of the CATSI Act. Consequently, the focus of the current legislative framework centres around maximising alignment where practicable with the Corporations Act 2001 (Cth) (Corporations Act) – the mainstream legislation governing the regulation of companies in Australia – in terms of accountability and corporate governance. 3

While both the CATSI Act and the Corporations Act allow the establishment of for-profit and not-for-profit entities, most entities registered under the CATSI Act are not-for-profit organisations providing essential services to their communities. 4 As this legislation reflects to a large extent the provisions present under the mainstream corporate law legislation, one may question why Indigenous Australians are not using this form of enterprise to set up their for-profit businesses.

Accordingly, this article focuses on this question and discusses the need for reforming the CATSI Act to become more business friendly to Indigenous entrepreneurs. It first assesses the limitations faced by Indigenous Australians when they wish to incorporate their for-profit entities under the CATSI Act and then considers whether there is a need to adapt the legislation to support for-profit endeavours. The article then considers the amendments that need to take place for the legislation to promote the establishment of ATSI for-profit corporations.

Why are ATSI for-profit corporations unpopular?

Even though the explanatory memorandum describes the CATSI Act as a ‘modern incorporation statute’ that is supposed to ‘reflect cultural practices’, 5 the CATSI Act has not been successful in promoting the establishment of for-profit entrepreneurship within Indigenous communities due to the inflexibility of the regime.

Despite the modernisation of the legislation, the CATSI Act remains a rigid legislation that requires entities to conform to certain rules which do not support the promotion of for-profit entities at different stages. As will be highlighted below, lack of conformity will result in an interventionist approach by ORIC (Office of the Registrar of Indigenous Corporations) into the affairs of the corporations as noted below.

Registration

Rigidity is apparent from the very beginning with the ATSI corporation requiring at least five members for the entity to be set up. 6 This may be an acceptable requirement when a corporation is providing essential services to the community as, through their membership, members of that community may need to be involved in the way services are provided. However, the requirement does not promote Indigenous for-profit entrepreneurship where one or two Indigenous people may wish to set up a business. This requirement can be contrasted with the Corporations Act where the minimum number of members needed in a corporation is one, irrespective of the type or size of the company. 7

While deviation from the minimal number of members is possible under the CATSI Act, it requires receipt of an exemption from the Registrar of Indigenous Corporations (Registrar) – an exemption that may be withdrawn by the Registrar down the track. 8 Furthermore, even when such an application complies with all the requirements for registration, the Registrar may still reject the application based on discretionary grounds such as the belief that the entity should be registered under a different statute or that the registration is contrary to the public interest. 9 This discretion does not exist in the establishment of mainstream corporations where meeting the registration criteria automatically leads to the creation of a company.

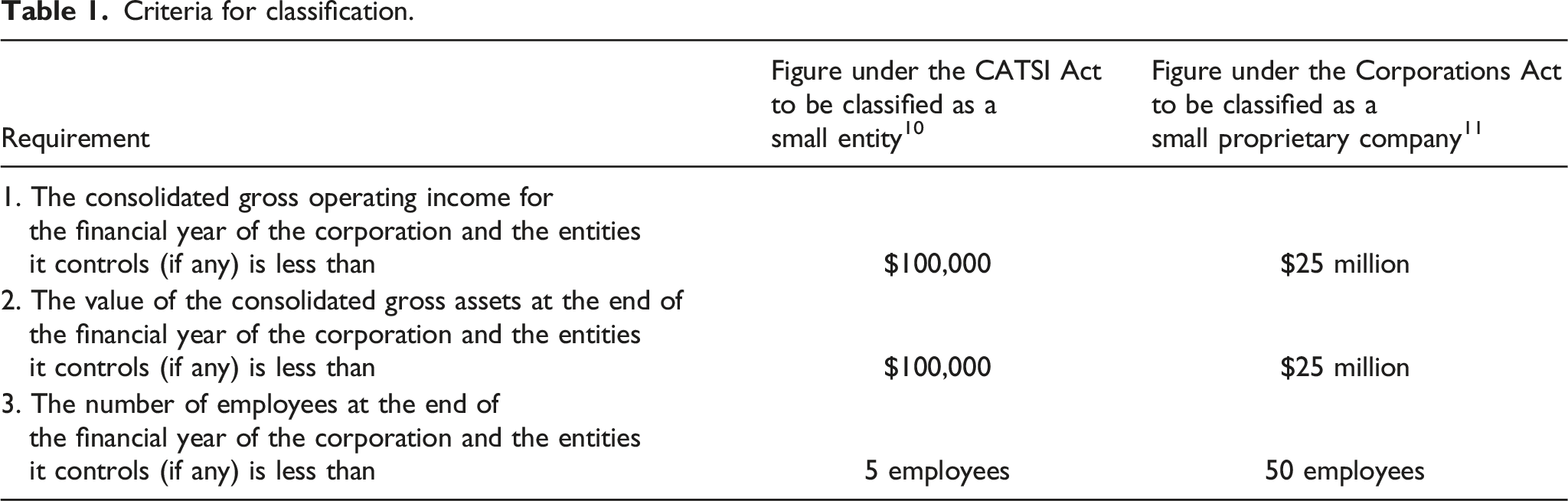

Classification

Criteria for classification.

Accordingly, a small proprietary company may remain classified as small even when it has an exponential growth while a small ATSI corporation is converted to a medium corporation when the $100,000 threshold is met. Consequently, the figures included under the CATSI Act are not supportive of small business success because they will force such businesses to move to higher accountability standards once they start generating some form of income and/or expanding their employee base. Furthermore, small ATSI corporations only have the benefit of reduced financial reporting requirements if they remain below the consolidated gross operating income of $5 million per financial year. 12 This can be contrasted with small proprietary companies who are exempt from reporting requirements irrespective of their income. Additionally, small proprietary companies benefit from other exemptions including the fact that they are not required to hold annual general meetings and they do not need to comply with the rules attached to related parties’ transactions. Therefore, these companies may provide more support for entrepreneurs wishing to set up their businesses as their regulatory framework is more business friendly.

It should be noted that issues with the classification of ATSI corporations have been highlighted by numerous reviews. For instance, the Technical Review of the CATSI Act noted that the size of the ATSI corporations’ classification was inadequate because it does not address ‘the differences between the types of, and activities undertaken by,’ the ATSI corporations. 13

Similarly, the CATSI Act Review Final Report also critiqued the classification noting: Under the CATSI Act, a corporation is classified as small, medium or large based on whether it meets thresholds for any two of three criteria relating to income, assets and number of employees. A corporation’s size determines aspects of its governance requirements under the CATSI Act such as the nature of contact details they are required to provide to the Registrar, and how information held by the corporation should be stored and made available to members. However, a corporation’s reporting requirements is based on its size and income – also a determinant of size. This can result in a situation where a corporation is categorised as small according to asset and staffing criteria thresholds, but then have more reporting obligations due to its income level. Not only is this confusing, but with so many factors to take account of, it can be difficult for corporations to self-assess in preparing for reporting.

14

The report, instead, recommended changing the classification regime of these corporations to align it with the one applying under the Australian Charities and Not-for-profits Commission. 15 However, while this approach is feasible for not-for-profit entities, it does not support the establishment of for-profit ATSI corporations as the proposed classification is catering for not-for-profit entities’ needs only.

Interventionist approach

The Registrar may intervene in the private affairs of the corporation if it believes that the rule book 16 is inappropriate, there is oppression within the organisation or if the entity is struggling financially. 17 This interventionist approach may be acceptable in the case of not-for-profit entities where accountability is needed as these entities are providing essential services to the community, especially in remote areas. 18 However, they are not required in a for-profit setting where interventionist measures may be counterintuitive and may prevent entrepreneurship. In contrast, the Corporations Act does not impose interventionist measures within its regime and the Australian Securities and Investments Commission, Australia’s corporate and financial services regulator, does not intervene in the private affairs of a company except in instances where there is misconduct.

Profit distribution

Last, as the CATSI Act does not provide for shareholding by members, when the corporation is liquidated, ATSI for-profit corporations have usually left the distribution of profit to the discretion of directors, the liquidator or the members. 19 The inability of members to hold shares once again may hinder investments in ATSI corporations as returns are not guaranteed or protected by the legislative framework.

Why is a legislative scheme needed to cater for ATSI for-profit corporations?

Due to the rigidity of the legislative framework, Indigenous Australians choose to operate their for-profit enterprises outside the CATSI Act using mainstream forms of business such as companies and partnerships. However, does this mean that the law does not need to cater for Indigenous for-profit entities? The answer is ‘no’ as this will be a step backward in the empowerment of Indigenous Australians, as will be discussed in the next sections.

Economic empowerment

Article 20 of the United Nations Declaration on the Rights of Indigenous Peoples states that ‘Indigenous peoples have the right … to engage freely in all their traditional and other economic activities.’ 20 This issue of economic empowerment is often overlooked. One way to remedy this is for Indigenous Australians to have a structure that is specifically designed to allow them to run their businesses in a manner that reflects their values and cultures. While the need for incorporation itself has raised a debate concerning the appropriateness of imposing such a business structure on Indigenous Australians, 21 incorporation may provide ‘a formally and legally uniform institutional model which meets the requirements of a single national strategy’ while allowing Indigenous Australians to incorporate their values, cultures and traditions into the running of the enterprise. 22 Furthermore, the setting up of culturally appropriate corporations may promote the success of these enterprises as social norms usually have a motivational effect on the operation of the corporation, especially when the laws reflect or allow the implementation of cultural values within the enterprise’s operation. 23

Closing the Gap

Additionally, reforming the CATSI Act to better cater for a for-profit business structure would help achieve one of the goals of the National Agreement on Closing the Gap relating to building ‘strong economic participation and development of Aboriginal and Torres Strait Islander people and communities’. 24 Relying on the CATSI Act as a means of facilitating this aim may lead to the employment of more Indigenous Australians and may result in more self-managed and owned Indigenous businesses. This may also empower Indigenous Australians to maintain their distinctive cultural practices while running their enterprise. Depending on the purpose of the enterprise, it may also promote economic relationship with their land.

Position

Consequently, the CATSI Act has a role to play in the promotion of for-profit entities. This was supported by the Law Council of Australia when it noted that ‘in order to truly meet the special measure characteristics [of the CATSI Act], further work needs to be done on accommodating the specifically Indigenous needs for hybrids’ or mixed entities that may support Indigenous Australians to run their businesses. 25

The latest review of the CATSI Act which was conducted by the National Indigenous Australians Agency in 2020 was supportive of this initiative and noted that there ‘may be merit in exploring the recommendation … to establish a special class of [for-profit] corporation under the CATSI Act’. 26

What is needed?

For the CATSI Act to support the incorporation of Indigenous for-profit businesses, the National Indigenous Australians Agency rightly noted that a range of elements need to be considered: • provisions of the CATSI Act that should not apply to this class of [for-profit] corporation; • new provisions that would need to be added to the CATSI Act to support this class of corporation; and • capacity building and other types of support that would be required from the Registrar and ORIC for this class of corporation.

27

These considerations are essential to ensure that the legislation is flexible and has the necessary structure to promote Indigenous for-profit entities.

New class of corporation

For the CATSI Act to attract for-profit enterprises, a new form of ATSI corporation will be required under the statute. This is necessary as the CATSI Act currently only distinguishes between small, medium and large corporations. The liability of members is decided at the time of registration of the corporation where the application will note whether the members and former members are held liable towards the payment of the debt of the company. 28 Three options are raised below: reproducing the model under the Corporations Act; drawing lessons from the Māori model; and designing a new model to cater for for-profit social enterprises.

In view of the possible complexity of for-profit business and the need for them to be able to raise funds and share profit with their members, a new type of ATSI corporation based on the concept of a limited liability company by shares may be put forward. In such instances, incorporation may provide the Indigenous enterprise with perpetual succession while limiting members’ liability. The issue of shares offers the business starting capital with opportunities to raise further funds in the future through the issue of shares and debentures. Indigenous members will have a percentage ownership in the corporation’s business. It will also allow for the establishment of one member companies without the need to apply for an exemption from the Registrar.

Other forms may also be more suitable. In New Zealand for instance, Māori complex business structuring provides an opportunity to reach a balance between profit maximisation and Māori values, cultures and tradition. 29 Depending on the purpose of an organisation, a Māori business may conduct commercial activities under the form of a corporation and then pass the profit to a private trust that will distribute such profit to the beneficiaries. 30 In 2006, the New Zealand Law Commission proposed another model for Māori corporations (or Waka Umanga). 31 The proposal allowed for the establishment of a legal entity tailored to meet the organisational needs of Māori tribes and other groups that manage communal Māori assets. 32 Māori concepts were to be incorporated in the legislation, ensuring that Māori ideas become an operational part of the Western regime. This model was not adopted in the end as there was a change in government which was of the view that there was no need for such a model. It considered instead that adequate Māori business structures were already in place. 33 Australia, however, may benefit from such a model as it better caters for culturally appropriate structures for Indigenous for-profit businesses.

The CATSI Act could also introduce a new structure that is designed to promote Indigenous for-profit social enterprises. These entities are hybrid enterprises serving a social cause while generating profits to their members. 34 This form of enterprise is more sustainable than a not-for-profit entity as the latter has to rely on grants, donations and federal and state programs to grow. In contrast, a for-profit social enterprise will control its own development and scale.

These for-profit social enterprises currently struggle to find a place in Australia as the mainstream legislation, the Corporations Act, promotes shareholder primacy over social good. Accordingly registering such entities under the Corporations Act may be problematic as it does not cater for this type of entity. 35

More flexibility

As noted previously in this article, the current regime is very rigid and imposes high standards of accountability on all types of corporations including small ATSI corporations. A more fit-for-purpose regime is needed where the accountability requirements are scaffolded depending on the needs of the corporation. Furthermore, a review of directors’ duties is needed to ensure that the duties take into account Indigenous culture and the purpose for which an Indigenous corporation is run. 36

Furthermore, the CATSI Act should not subject for-profit enterprises to the interventionist approach that currently exists within the legislation when dealing with the internal management and affairs of the entity. For instance, the Registrar’s interventionist approach regarding their need to assess the appropriateness of the rule book, including their alteration, 37 should be removed to truly empower Indigenous Australians. Members of an ATSI corporation should be able to set out the rules they believe are best for the running of their entities within the confines of the legislative regime without the Registrar exercising any discretion on this matter.

In relation to Indigenous for-profit enterprises under the CATSI Act, the Registrar should also take a less interventionist approach when regulating insolvent corporations. Currently, they can put an ATSI corporation under special administration, taking away the autonomy that directors have in running the corporation in the hope of saving the entity. While well-intentioned, it is another paternalistic approach to regulation that should be removed. This will help make the legislation more aligned with the Corporations Act which does not impose a similar requirement for any type of entities registered under it. In addition, a change in the legislative approach will also send the message to Indigenous people that the legislation is ready to help promote and nurture entrepreneurship.

Capacity building

As part of their functions, the Registrar provides educational programs to corporations under s 658-1(e) of the CATSI Act. These programs have been viewed positively by participants as they help raise corporate governance awareness in the running of ATSI corporations. 38 This support, which is not replicated in mainstream corporate legislation, may be an excellent tool to help Indigenous entrepreneurs set up their for-profit businesses. However, the educational program should be more nuanced to cater for the context within which organisations are operating.

For instance, regarding for-profit entities, the Registrar may offer a special program for Indigenous Australians wishing to set up their businesses. This program may be based around contextual education where information is provided in a way that allows the learners to build the knowledge based on their own experiences. This approach could motivate learners as it will allow them to express their ideas, determine their internal management rules and relate them to the regulatory framework without the need to rely on the Registrar’s intervention.

Conclusion

Prescriptive rules and a heavy-handed approach to regulation may be appropriate to ensure the legitimacy and accountability of ATSI corporations that rely significantly on external government sources of funding. However, this same approach is problematic in the context of for-profit entities. While Indigenous Australians are able to set up their for-profit businesses under different mainstream legislation, creating a legislative framework under the CATSI Act – which promotes such enterprises – would be beneficial to ensure that Indigenous Australians have a business structure that is culturally appropriate and fits their economic needs.

To achieve this, fundamental changes need to take place within the CATSI Act to enable the creation of such institutions. The structure must be sufficiently flexible to allow Indigenous peoples to incorporate their culture and traditions in the running of the organisation. In doing so, the enterprise may be able to promote the self-determination of Indigenous Australians, with the role of Registrar limited to capacity building and taking action in case of misconduct by entities and their directors.

It has been 50 years since the first report of the Aboriginal Land Rights Commission highlighted that to meet Indigenous peoples’ requirements ‘there is an obvious need for provisions for incorporation. Further, laws relating to incorporation under the Companies Acts are inappropriate for most Aboriginal purposes.’ 39 These words seem to have been forgotten when designing the CATSI Act given that, while the legislation attempted to create appropriate laws for Indigenous enterprises, legislators took an overly interventionist approach to regulation of all types of ATSI corporations and did not leave room for for-profit entities. The effect is that the CATSI Act does not support Indigenous entrepreneurship and economic empowerment and therefore a review and a rethink of this approach is needed.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.