Abstract

The purpose of this study is to explore changes in standard setting in South Africa using a regulatory theory perspective. The article focuses on three events: the adoption of the International Financial Reporting Standards, the adoption of the International Financial Reporting Standards for Small and Medium-sized Enterprises, and the change in standard setting with control of standard setting passing from the accounting profession to the Financial Reporting Standards Council. The methodology is qualitative, using primary and secondary sources of information. The findings show that elements of and changes in these three events reflect regulatory theory's sub-category of public interest theory, although elements of private interest theory, in particular interest group capture theory, are present. The importance of this study is that it discusses recent developments in standard setting in South Africa using a regulatory theory lens and provides an alternative viewpoint when analysing standard setting in other jurisdictions.

Introduction

Studies on the regulation of standard setting in different jurisdictions have used different lenses or theoretical frameworks to provide historical analyses of the adoption of International Financial Reporting Standards (IFRS) or the International Financial Reporting Standard for Small and Medium-sized Entities (IFRS for SMEs). Hassan et al. (2014) used an institutional perspective to analyse the decision to adopt IFRS in Iraq, Stainbank (2017) used institutional theory to investigate IFRS for SMEs adoption in African countries, Sanada (2018) focused on the legitimacy of the private sector to set standards in Japan, Giner and Mora (2020) examined political interference in Spanish private entities’ financial reporting as a justification of being in the public interest arguing that it goes beyond the traditional agency framework and Wijekoon et al. (2022) used an institutional sociology perspective to examine IFRS for SMEs adoption in Sri Lanka.

South African studies on standard setting in South Africa are those by Samkin (1996), Gloeck (2003), Stainbank (2010), Verhoef (2011), and Harber et al. (2023). Samkin (1996) reported on the standard setting arrangements that were in place then, while Gloeck (2003) focused on the need for public accountability in standard setting arrangements. Stainbank (2010) concentrated only on the standard setting arrangements which led to the adoption of IFRS for SMEs, Verhoef (2011) focused on the relationship between government and the accounting profession over the period 1904 to 1951, and Harber et al. (2023) examined the relationship between the audit regulator and the Big 4 firms during the debate on auditor rotation.

Bushman and Landsman (2010: 11) suggest that it is unlikely that one regulation solution will fit all countries, as jurisdictions ‘differ in many respects including political and legal regimes, institutional development, corruption, and culture’. As examples, they cite the Financial Accounting Standards Board, which was privately funded until the Sarbanes-Oxley Act of 2002 was passed, which then provided for mandatory funding from the Securities and Exchange Commission of the United States, and the International Accounting Standards Board, which is funded by the private sector (Bushman and Landsman, 2010: 20, 21).

Sharma and Samkin (2020) argue that, in general, accounting research in the context of less developed countries is limited, with some exceptions. This study, set in South Africa, a developing country, contributes to the literature by adding new context to prior South African studies (Gloeck, 2003; Samkin, 1996; Stainbank, 2010; Verhoef, 2011) by providing a more recent history of the development of standard setting in South Africa using a regulatory theory lens. This study describes the corporate law changes and changes in the standard setting arrangements in South Africa using a regulatory theory lens during a period of corporate law reform; it thus provides a useful addition to the limited publications on the regulation of standard setting both in South Africa and abroad, and in addition, it adds to accounting regulation theories using a country-specific context. While previous studies have used external factors such as international influence or internal economic factors as the rationale for adoption of accounting standards (Giner and Mora, 2020; Hassan et al., 2014; Sanada, 2018; Stainbank, 2017; Wijekoon et al., 2022), this study focuses on internal influences using insights from regulatory theories. It also adds to the discussion on whether standard setting should be the domain of the private or the public sector and on which theoretical framework best fits such an analysis. While there are different lenses or theoretical viewpoints that could be used to examine the regulation of standard setting, the lens chosen in this current study is regulation theory as reporting requirements in South Africa were governed by a combination of regulations, firstly from a self-governing professional body, the South African Institute of Chartered Accountants (SAICA), augmented by regulations for listed companies set by the Johannesburg Stock Exchange (JSE), both bodies in the private sector, together with legislation and lastly, by the Financial Reporting Standards Council (FRSC), a standard setting body created by the Companies Act, 71, 2008 (Department of Trade and Industry [DTI], 2009). 1

In South Africa, although financial reporting is regulated by statute (DTI, 1973), for many years, arrangements for standard setting were the domain of the private sector through the Accounting Practices Board (APB), which represented several independent organisations. Although the APB was a private body, its secretariat function was provided by the Accounting Practices Committee (APC), a committee of SAICA. The APC carried out research to inform the APB's decisions and functioned as the Technical Accounting Committee of SAICA. The advent of the Companies Act, 71 of 2008 (DTI, 2009), introduced a new standard setting body to South Africa, the FRSC. The members of the FRSC are appointed by the Minister of Finance. This removed standard setting from the purview of the private sector to that of the government.

In 1994, the first democratic elections took place in South Africa. In anticipation of the opening of the South African economy to new foreign investment, South Africa began aligning South African Generally Accepted Accounting Practice (SA GAAP) with international reporting standards in 1993 (Prather-Kinsey, 2006). This harmonisation process was completed in June 2004, and the APB then issued IFRS as SA GAAP without any amendments. Subsequently, in terms of the Companies Act, 71 of 2008, IFRS was made mandatory, without any amendments, for certain companies.

In 2007, South Africa adopted the draft IFRS for SMEs for use by limited interest companies. The impetus for this came from an auditing perspective, as, until the Companies Act No. 71 of 2008 (DTI, 2009) was implemented, all widely held (i.e., public companies) and limited interest companies (i.e., private companies) required an audit. The APB agreed that the draft IFRS for SMEs would be issued as a statement of GAAP with an effective date tied to the Corporate Laws Amendment Act, but allowing for early adoption, thus allowing auditors to express an opinion on financial statements prepared using the draft IFRS for SMEs (SAICA, 2007a, 2007b).

These developments in the corporate reporting and standard setting arrangements provide an opportunity to explore the nature and reasons for the changes. The aim of this article is to explore the changes in standard setting arrangements in South Africa, which led to the adoption of IFRS and IFRS for SMEs and subsequent standard setting arrangements using regulatory theory as the theoretical lens.

Studies into standard setting have used different lenses or theoretical viewpoints to investigate standard setting in different jurisdictions (Giner and Mora, 2020; Hassan et al., 2014; Sanada, 2018; Stainbank, 2017; Wijekoon et al., 2022). The lens adopted in this current study is regulation theory, as reporting requirements in South Africa were regulated by a combination of requirements from both private and public bodies, a self-governing professional body, the JSE, and by legislation.

The remainder of the article is organised as follows: The article next provides a brief history of the South African standard setting process with a focus on the adoption of IFRS, IFRS for SMEs, and the establishment of the FRSC. This is followed by a section that explains the research method. Then, regulatory theory is described together with the literature review. The article then explores the adoption of IFRS, IFRS for SMEs, and standard setting arrangements in South Africa using a regulatory theory lens.

Standard setting in South Africa – a brief history (1887–2022)

Various events, such as the discovery of diamonds and gold in the nineteenth century, combined with the establishment of the JSE in 1887, highlighted the need for accountants and auditors (SAICA, 2023). In 1894, the Institute of Accountants and Auditors in the South African Republic was established, followed by the South African Committee of the Society of Accountants in the Cape in 1896 (SAICA, 2023). In 1910, when the ‘Union of South Africa created a political union of the four separate geographical areas, each of the Transvaal, Orange Free State, and the British colonies of the Cape and Natal had formed local accounting bodies’ (SAICA, 2023).

In 1921, the four accounting societies (Transvaal, Orange Free State, Cape and Natal) agreed to establish the South African Accounting Societies’ General Examining Board to enforce standards within the profession, and the Free State, Cape, and Transvaal accounting societies agreed to jointly pursue legal recognition of a national accounting body by Parliament. In 1926, the Companies Act was passed, and in 1927, the Chartered Accountants Designation (Private Act) 13 of 1927 was promulgated, allowing members of the four provincial societies to use the title of Chartered Accountant (South Africa), or CA(SA). In 1945, the four provincial societies and the Rhodesian Society of Accountants created the Joint Council of the Chartered Societies of South Africa (Joint Council). The promulgation in 1951 of the Public Accountants’ and Auditors’ Act created the Public Accountants’ and Auditors’ Board (PAAB), set up to regulate the accountancy profession and provide for a single register of public accountants (SAICA, 2023).

Samkin (1996) writes that 1962 can be considered the starting date for the formal development of South African statements of accounting practice when the Joint Council appointed a standing committee for the purposes of preparing statements on auditing and accounting. In 1966, the Joint Council was renamed the National Council of Chartered Accountants (National Council). In 1971, the National Council appointed the Accounting Principles Committee and assigned to it the development of South African accounting standards (Samkin, 1996). Samkin (1996) explains that difficulties surrounding the meaning of ‘principles’ led the National Council to change the name of the Accounting Principles Committee to the Accounting Standards Committee, and then in 1972 to the APC. To make compliance with accounting practice mandatory, the Accounting Standards Committee lobbied the Company Law Commission, the body responsible for redrafting the Companies Act to legislate the requirement that financial statements conform to generally accepted accounting practice (Woodhouse, 1972a). As a result, Section 286(3) of the Companies Act, 61 of 1973 required that the ‘annual financial statements of a company shall, in conformity with generally accepted accounting practice, fairly present the state of affairs of the company and its business as at the end of the financial year concerned and the profit or loss of the company for that financial year and shall for that purpose be in accordance with and include at least the matters prescribed by Schedule 4, in so far as they are applicable, and comply with any other requirements of this Act’ (DTI, 1973).

The accounting profession realised that failure to establish acceptable accounting standards could lead to this function being assumed by another body, or even government (Vieler, 1977: 156), and they viewed themselves as best able to codify accounting practices (Woodhouse, 1972b: 167, as cited by Samkin, 1996). This led to a decision in 1972 to form the APB (Woodhouse, 1972a), whose purpose would be to define generally accepted accounting practice.

To represent all preparers of financial statements, the National Council approached other interested parties, such as the JSE and other associations representing commerce, industry and mining, to serve on the APB (Woodhouse, 1972c; Vieler, 1977: 155), allowing standard setting to be guided not only by chartered accountants. Samkin (1996) viewed 1973 as being the start of ‘the new age’ in South African accounting standard setting, with the promulgation of the Companies Act, Act 61 of 1973, and the formation of the International Accounting Standards Committee. The APB was a private body tasked with developing statements of GAAP.

The APB had a diverse membership. 2 Its chairman was non-voting, did not represent any constituent body, and was generally a retired member of SAICA. All other members of the APB were entitled to a single vote. However, the secretarial functions of the APB were provided by SAICA (through the APC) and, according to Blumberg (1995: 2), also provided the bulk of the funding required for the standard setting process. In 2003, in reply to an article which appeared in the Business Report, the then Executive President of SAICA indicated that the APB is an independent body ‘consisting of a wide array of constituent bodies and is funded by participating organisations’ (Sehoole, 2003).

The APC's membership comprised a Chair (who was an academic), five representatives of the auditing profession, five representatives from Commerce and Industry, one representative from the banking sector, one IFRS consultant, and one representative of the JSE. These latter two representatives were considered users of financial statements. There were also eight ex officio members, of whom five were SAICA employees. The objective of the APC is to prepare and submit with the intention to influence outcomes, on behalf of SAICA, comments on exposure drafts or discussion papers or any other appropriate documents or legislation issued by the IFRS Foundation structures, the FRSC, the DTI, the National Treasury, the JSE or other bodies, taking the views of local commentators into consideration (SAICA, 2017).

In 1980, the four Chartered Societies replaced the National Council with the SAICA. The SAICA thus became the primary representative organisation of all South African chartered accountants, with the APC and the APB as the agents of accounting standard setting in South Africa. From 1980 onwards, SAICA, through the APC and APB, managed the standard setting process in South Africa by issuing discussion papers, exposure drafts and SA GAAP. While the APB approved SA GAAP for issue in South Africa, SAICA was responsible for releasing any discussion papers or exposure drafts on the topic under consideration.

The harmonisation process, initiated in 1993, was completed in June 2004, and the APB then decided to issue IFRS as SA GAAP without any amendments (SAICA, 2004a). This harmonisation process ensured that there were only a few minor differences between SA GAAP and IFRS, which were mainly editorial and related to implementation dates and additional disclosure requirements (SAICA, 2003a). Subsequently, a dual numbering system was used, comprising either the International Accounting Standard or IFRS number, followed by the relevant South African AC number in brackets. This was done as SA GAAP was then an exact replica of the relevant IAS or IFRS (SAICA, 2004a). The JSE, South Africa's only stock exchange, revised its listing requirements during this period and required all companies listed on the JSE 3 to apply IFRS for their financial years commencing on or after 1 January 2005 (Meyer, Stiglingh and Venter, 2006).

In 1999, SAICA sought legal opinion as to whether the requirement in the 1973 Companies Act, that the financial statements of companies be prepared in conformity with SA GAAP, required companies to comply with SA GAAP, as companies could depart from SA GAAP provided the particulars of the departure, effects, and reasons therefore were provided. Legal opinion confirmed that the financial statements should comply with SA GAAP; however, only if there were material departures from SA GAAP would additional disclosures be required. This confirmed that there was no statutory enforcement for SA GAAP in terms of the 1973 Companies Act (United Nations Conference on Trade and Development, 2007).

A period of corporate law reform followed, some of which had implications for small and medium-sized entities (SMEs) (DTI, 2007). Differential reporting had appeared as an agenda item in 2000 as at that time, all companies, regardless of size, form and to whom their financial statements were available, were required to apply SA GAAP (substantively IFRS) (DTI, 1973). The Corporate Laws Amendment Act 24 of 2006 (DTI, 2006), which concluded Phase 1 of a two-phase process in reforming corporate law by providing interim amendments to the Companies Act 61 of 1973, introduced two types of companies for financial reporting purposes, the widely held company and the limited interest company.

Widely held companies would use SA GAAP (substantively IFRS) as opposed to limited interest companies, which could use accounting standards developed for limited interest companies (DTI, 2006). As these standards had yet to be developed, a transitional provision was provided by paragraph 56(3)(a) of Schedule 4 which allowed a limited interest company to prepare its financial statements in accordance with a set of accounting practices which complied with the framework for the preparation and presentation of financial statements included in financial reporting standards. To cater for this, in 2007, SAICA issued the IASB's ED of an IFRS for SMEs (IASB, 2007) as ED 222 and invited comments on a proposed process. SAICA's view was that limited interest companies could, in the interim period, either continue to comply with IFRS, or adopt the IASB's draft ED. This would be only for an interim period until the FRSC (the official standard setting body which would replace the APB) was established in terms of the Corporate Laws Amendment Act 24 of 2006 and would issue standards for limited purpose companies (SAICA, 2007a). The matter was urgent as, until the Companies Act No. 71 of 2008 (DTI, 2009) was implemented, all widely held and limited interest companies would require an audit. If small and medium-sized companies required an audit, then these companies would need to use a framework or transitional financial reporting standards on which auditors would be able to express an opinion on fair presentation. After various public consultations facilitated by SAICA, the APB agreed that the ED on IFRS for SMEs would be issued as a statement of GAAP with an effective date tied to the Corporate Laws Amendment Act but allowing for early adoption (SAICA, 2007b). Regarding a final standard being issued by the IASB, the APB agreed that once a final standard was issued, the Statement of GAAP would be updated to ensure that the South African framework was consistent with the international standard. Widely held companies (i.e., public companies) were thus required to comply with full IFRS, and limited interest companies (i.e., private companies) were required to comply with the proposed IFRS for SMEs (SAICA, 2007a).

Phase 2 of the corporate law reform culminated in the release of the Companies Act, 71 of 2008, which came into effect in 1 May 2011 and established the FRSC as the legally appointed financial reporting standard-setter in South Africa. In South Africa, setting financial reporting standards for public sector entities is the preserve of the Accounting Standards Board, set up in terms of the Public Finance Management Act. The Companies Regulations (DTI, 2011) prescribes the specific financial statements to be used by state-owned entities, and profit and non-profit companies based on a public interest score, whether it is listed, and whether the financial statements are internally or independently compiled. The financial reporting frameworks which were mandated for use were:

IFRS as issued by the IASB, IFRS for SMEs as issued by the IASB, or a Financial Reporting Standard determined by the company for so long as no financial reporting standard was prescribed.

The FRSC is therefore not required to endorse or reject new IFRSs/amendments to IFRSs or to the IFRS for SMEs/amendments to IFRS for SMEs, as the Act is prescriptive as to the compliance with these standards for specific entities as discussed above. The FRSC therefore reviews any newly issued IFRSs, amendments to IFRSs, or amendments to IFRS for SMEs (IASB, 2009) and assesses the impact thereof in a South African context with a view to determining whether local guidance is required. In addition to this, the FRSC may consider the need for local guidance where there is a need for clarity or where practice has arisen (from FRSC agenda item 2). According to the FRSC's (DTI, 2016) rules of procedures, it may consider the need for interpretations where there is a need for clarity or where practice has arisen.

In 2012, the APB withdrew SA GAAP and began a winding up process (APB and FRSC, 2012). However, the APC continued its work by acting as a secretariat to the FRSC. A close working arrangement continued between SAICA and the FRSC until 2015 with all SAICA comment letters being noted by the FRSC, the FRSC attending APC meetings, and if the FRSC agreed with APC commentary, it endorsed the APC commentary. A Memorandum of Understanding between SAICA and the FRSC was then endorsed to formalise their working arrangements, with the FRSC moving towards greater independence by establishing its own Financial Reporting Technical Committee. However, from 2018 until 2021, the FRSC was dormant and only in 2022 did the Department of Trade, Industry and Competition advertise for and appoint new FRSC members.

These three major developments (the adoption of IFRS, the adoption of IFRS for SMEs and the establishment of the FRSC) subsequent standard setting arrangements are discussed in this article.

Research method

This study uses a qualitative approach to explore the history of standard setting in South Africa using a regulatory theory framework. For the analysis, both primary and secondary sources of literature were used. Primary sources of data for this study were the minutes and agenda documents available on the website of the FRSC and which were in the public domain at the time the minutes and agenda documents were being reviewed. Subsequently these documents were removed and are no longer accessible on the DTI website. Minutes and agenda documents of the APC were not examined as these are not in the public domain, nor are they accessible to ordinary SAICA members. Secondary sources of information included results of surveys supplied on request by SAICA. From the analysis of the primary and secondary sources of literature, three main events dominating the standard setting arena were identified. These were the adoption of IFRS, the adoption of IFRS for SMEs and the establishment of the FRSC, the standard setting body. These three events are analysed using the lens of regulatory theories which are used to place the article within a theoretical framework.

The article next presents the literature review and firstly discusses regulation theory and the two main sub-categories of regulation theories, namely public interest theory and private interest theory. The discussion includes regulatory capture theory that is often considered a form of private interest theory. After this discussion, examples of these theories’ applications in standard setting reported in prior literature are reviewed.

Literature review

In accounting, any rules that govern the form and/or content of information is a form of regulation. Examples are legislative rules (in a Companies Act), listing rules (of a stock exchange), and disclosure rules (such as those found in accounting standards). The form that the accounting rules take has implications for their mode of regulation.

Various reasons have been proposed for the necessity of regulating financial accounting practices, such as the need for investor protection and the implementation of standardised practices which enhance comparability. Two main categories of theory attempt to describe who benefits from such regulation (Deegan, 2013: 45; Hantke-Domas, 2003; Riahi-Belkaoui, 2005: 135): public interest theories and private interest theories. The following section reviews these two main regulatory theories together with studies that have used them as a theoretical lens or studies that could fit into these theoretical viewpoints.

Public interest theory views accounting information as a public good and takes the viewpoint that the regulators’ main objective is to protect and benefit the public (Gaffikin, 2005). However, because this information is publicly available and for the use of anyone, such as investment analysts and investors, information, and especially that relating to disclosures, may be under-produced. This requires the imposition of mandatory reporting requirements (Samkin, 1996). Regulation is thus a response to the public demand for information to correct discriminatory or ineffective disclosure practices (Samkin, 1996).

Gaffikin (2008: 8) considers the private interest theory approach as ‘the products of relationships among different groups and between such groups and the state’. In this approach, the affected groups consider that regulation is ‘competition for power’ rather than for the public interest. Chalmers et al. (2012) argue that in this theory, the parties who may be negatively affected by legislation use political influence to promote outcomes for their own benefit.

A specific form of private interest theory is regulatory capture theory, although it is often considered a separate theory of regulation (Chalmers et al., 2012). Regulatory capture theories argue that, even though regulation may be introduced to protect the public interest, subsequent regulatory mechanisms are controlled (i.e., captured) by the interest groups affected most by the regulation. Regulatory capture theory is based on the following two premises. Firstly, members pursue their own self-interest by lobbying regulators for regulations that increase their wealth (Samkin, 1996). Secondly, the government has no role to play in the regulatory process. Interest groups vie for control of the government's coercive powers to maximise their wealth distribution. While the purpose of regulation is ostensibly to protect the public interest, this is, in fact, not achieved, and the regulatee takes control of the regulator to protect its own interests (Samkin, 1996).

Countries such as the United States, Australia and England provide examples of regulatory capture theory. In the 1970s, the US Congress investigated the allegation that accounting regulations had been captured by the big ‘8’ (Ramanna, 2015). In Australia, Walker (1987) argued that although the establishment of the Australian Accounting Standards Review Board in 1984 was to ensure the protection of the public interest, the Australian Accounting Standards Review Board was successfully captured by the accounting profession, which Walker (1987) saw as the regulated industry. Walker (1987) suggested that the reason for this capture is that the accounting profession found it necessary to legitimise accounting standards by providing them with legislative backing. On the other hand, the accounting profession had an economic interest in retaining the standard setting process rather than abdicating this power to government control. What resulted was not regulatory intervention in the accounting standard setting process to protect the public interest, but rather the capture of the standard setting process by an elite group, the accounting profession, for its own gain. These findings are consistent with Willmott's (1985) study of the English accounting profession. Willmott (1985:63) concluded that the ‘outcome of this investigation has been the revelation of an elite group that in effect is unaccountable to the general public, and which is constrained only by the fear of state intervention’.

Chalmers et al. (2012) explored the ability of regulatory theories to explain financial accounting standards development into general purpose water accounting standard setting. They found that water industries dominated the initial stages of the standard setting process, but did not discount the possibility that if there were to be a sole standard setting body appointed subsequently, that this could indicate regulatory capture.

Sanada (2018: 339), who provided a historical narrative of standard setting in Japan using the lens of legality and noted that four sets of accounting standards are permitted for consolidated financial statements of listed companies, referred to a ‘hybridization’ between statutory and professional control in the Japanese standard setting environment, where there is a ‘legally incomplete ex ante delegation to the private sector standard-setting bodies and ex post endorsement by the public sector’.

The studies above endorse the viewpoint of Bushman and Landsman (2010: 11) that it is unlikely that one regulation solution will fit all jurisdictions and may also indicate that the adoption of different accounting standards within jurisdictions fits different solutions. Turning to South Africa, the article next describes South African studies (Gloeck, 2003; Stainbank, 2010; Verhoef, 2011) on standard setting.

Gloeck's (2003) study examined past practices and proposed reforms encompassed in the Proposed Financial Reporting Bill. His study focused on public accountability. He concluded that public accountability was not being addressed in the proposed bill and blamed the standard setting practices for this. He argued that it was necessary to target any reforms at the standard setting process and at the accounting and auditing standard setting bodies. He was also of the opinion that an Accounting Profession Act was the priority for the government.

Stainbank (2010) focused only on the standard setting processes which led to the adoption process of the draft IFRS for SMEs as a standard. She argued that although this was being consistent with the public-interest theories of regulation, an element of the interest-group capture theory was present as SAICA sought exposure ‘in the media, locally and internationally, with its proclamation that South Africa was the first country to use the exposure draft as a standard’ (Stainbank, 2010: 67). If the adoption of the proposed IFRS for SMEs benefited the auditing profession to allow auditors to express their opinion, ‘then the influence of the auditing profession on this process would also indicate an element of interest-group capture theories’ (Stainbank, 2010: 67). The main reason for this conclusion was that the adoption of the draft form of IFRS for SMEs benefited the auditing profession as auditors were required to express an opinion on a certain category of companies which were allowed to use a different reporting framework in terms of the Corporate Laws Amendment Act (DTI, 2006), and at that time the profession did not have a different reporting framework for use by auditors. This then indicated an element of interest-group capture theory, that is, the auditing profession had captured the process to suit themselves, but that it was in the public interest.

Verhoef (2011) provides a description of the relationship between the government and the accounting profession over the period 1901 to 1951. Verhoef's (2011: 40) study focused on the processes of the government and the accounting profession, which culminated in the Public Accountants’ and Auditors’ Act, which set up the Public Accountants’ and Auditors’ Board, responsible for the registration of accountants and auditors. The government thus succeeded in establishing some form of regulation over the profession in the public interest, and the profession gained statutory recognition and made registration with it a prerequisite for practising rights. In 2005, South Africa enacted the Auditing Profession Act, 26 of 2005, which established the Independent Regulatory Board for Auditors (IRBA), which superseded the Public Accountants’ and Auditors’ Board. Although an Auditing Professions Act had now been established, an Accounting Professions Act had not been established despite recommendations from the World Bank (2003; 2013) and academia (Gloeck 2003).

To conclude this section, standard setting processes do not fit neatly into only one form of regulatory theory to the exclusion of another. For example, Chalmers et al. (2012) found that while water industries may dominate early development (public interest), later regulatory capture does not necessarily conflict with public interest benefits. Stainbank (2010) argued that the standard setting process, which led to the adoption of the draft IFRS for SMEs, was both in the public interest (the necessity to reduce the audit burden of limited purpose companies) and in the private interest (the accounting and auditing profession benefited). Sanada's (2018: 339) reference to a ‘hybridization’ between statutory and professional control in the unique Japanese accounting environment is possibly like the South Africa situation, where control of standard setting was achieved by the accounting profession and tacitly condoned by the government, which exercised statutory control.

Results and discussion

As identified in the research method section, the discussion that follows focuses on the adoption of IFRS, the adoption of IFRS for SMEs, and developments in the standard setting arrangements using the lens of regulatory theories.

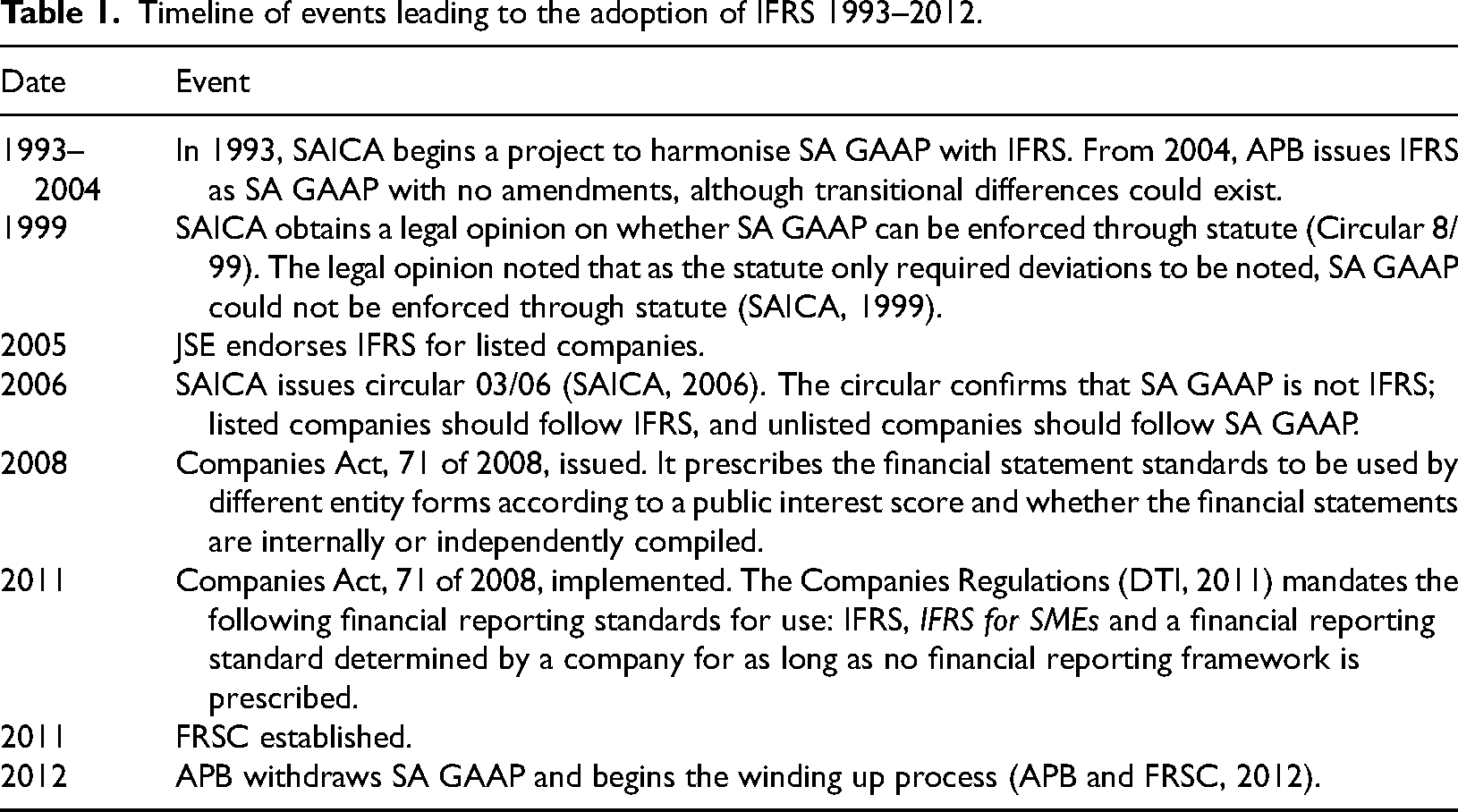

The adoption of IFRS 1993–2012

Table 1 shows a timeline of the important developments in the standard setting arrangements leading to the adoption of IFRS.

Timeline of events leading to the adoption of IFRS 1993–2012.

The main events underpinning the adoption of IFRS in South Africa, as described earlier in this article, are shown in Table 1. This shows that SAICA and the JSE were influential in ensuring that IFRS was adopted prior to any government regulation. By adopting IFRS, Samkin (1996) is of the opinion that SAICA took a short-term point of view and speculates that it may have been because it feared political interference. He argued that from a long-term perspective, if the IASB sets the standards, then the standard setting role is delegated to one of lobbying the IASB. After the APB took the decision in 2004 to issue IFRS as SA GAAP without any amendment, Ludolph (2006), representing the accounting profession, argued that the decision to adopt IFRS was driven by the need for South African companies to attract foreign investment, to provide credibility to the financial statements of South African companies in the global market and to do away with the need for dual-listed companies to prepare their financial statements using more than one accounting framework. These arguments from Ludolph (2006) may indicate that the profession believed adopting IFRS was in the public interest, as the adoption would serve several stakeholders. The finding that SA GAAP is not IFRS, together with the widespread use of IFRS worldwide, would also suggest that the early adoption of IFRS was in the public interest.

The decision in 2005 of the JSE to require listed companies to prepare their financial statements according to IFRS preceded the Companies Regulations (DTI, 2011) requirements, which were tied to the implementation date of the Companies Act, 71 of 2008. This required the adoption of IFRS by certain companies according to various criteria. As IFRS had already been adopted by the JSE and SA GAAP had already been aligned with IFRS, this enactment could not be seen as government intervention. Verhoef (2012) argues that the accounting profession, ‘in close collaboration with the international bodies, collaborated with the state in designing a new statutory framework of professional regulation and accountability. The profession in South Africa, as represented by SAICA, together with the statutory regulator, the … IRBA, repositioned itself to become leader in the implementation of IFRS and IFRS for SMEs’. This would suggest that private interest theory was also present, as the profession would be seen as the South African leader in standard setting.

In the South African context, government regulation in the accounting standard setting process could be justified under the public interest theory if there were corporate collapses and if government intervention is seen as necessary to rectify failures in the market for accounting information. Gloeck (2003) highlighted the many corporate scandals in South Africa over the years. The state capture debacle in South Africa and chartered accountants’ roles in state capture were subject to enquiries by both SAICA and IRBA (SAICA 2018). However, with the establishment of the FRSC, the government is now the de facto standard setter.

Returning to Table 1, until 2011, the de facto standard setter was the APB, and subsequently, the FRSC. However, although the Companies Act 1973 required companies to prepare their financial statements in conformity with SA GAAP, this requirement lacked statutory enforcement. As SAICA and the APB were private bodies, to get legal backing for accounting standards, it was necessary to go the legislative route. It is possible that, as IFRS was already the practice in South Africa, the profession would want to have IFRS and IFRS for SMEs mandated for use in the new legislation.

The legislated adoption of IFRS met the needs of several stakeholders. Firstly, it met the needs of the government, which had as one of its stated objectives to modernise company law (DTI, 2004, 2007), and the adoption of IFRS could be seen as achieving this objective, that is, adopting a world-class, widely accepted financial reporting framework. Secondly, it met the needs of the accounting profession, which needed legal backing for the standards to enforce the standards and provide its members with an international accounting framework that was widely adopted. SAICA sees itself as the pre-eminent professional accountancy organisation in South Africa, and it needs to provide a service to its members who are mainly preparers and auditors. Thirdly, it confirmed to the JSE that its early decision to make application of IFRS a listing requirement had been the correct one.

To conclude this section, the decision to adopt IFRS fits both the public interest theory (in that the current legislation was insufficient in mandating application of the then SA GAAP) and private interest capture theory in that the regulator served the interests of the regulatee by mandating the use of IFRS for listed companies and other companies depending on various criteria. While the adoption of IFRS has not prevented subsequent corporate collapses due to the misapplication of accounting principles (Barac and Moloi, 2010), the very public corporate collapses at that time may have played some role in the mandatory requirement of IFRS through legislation.

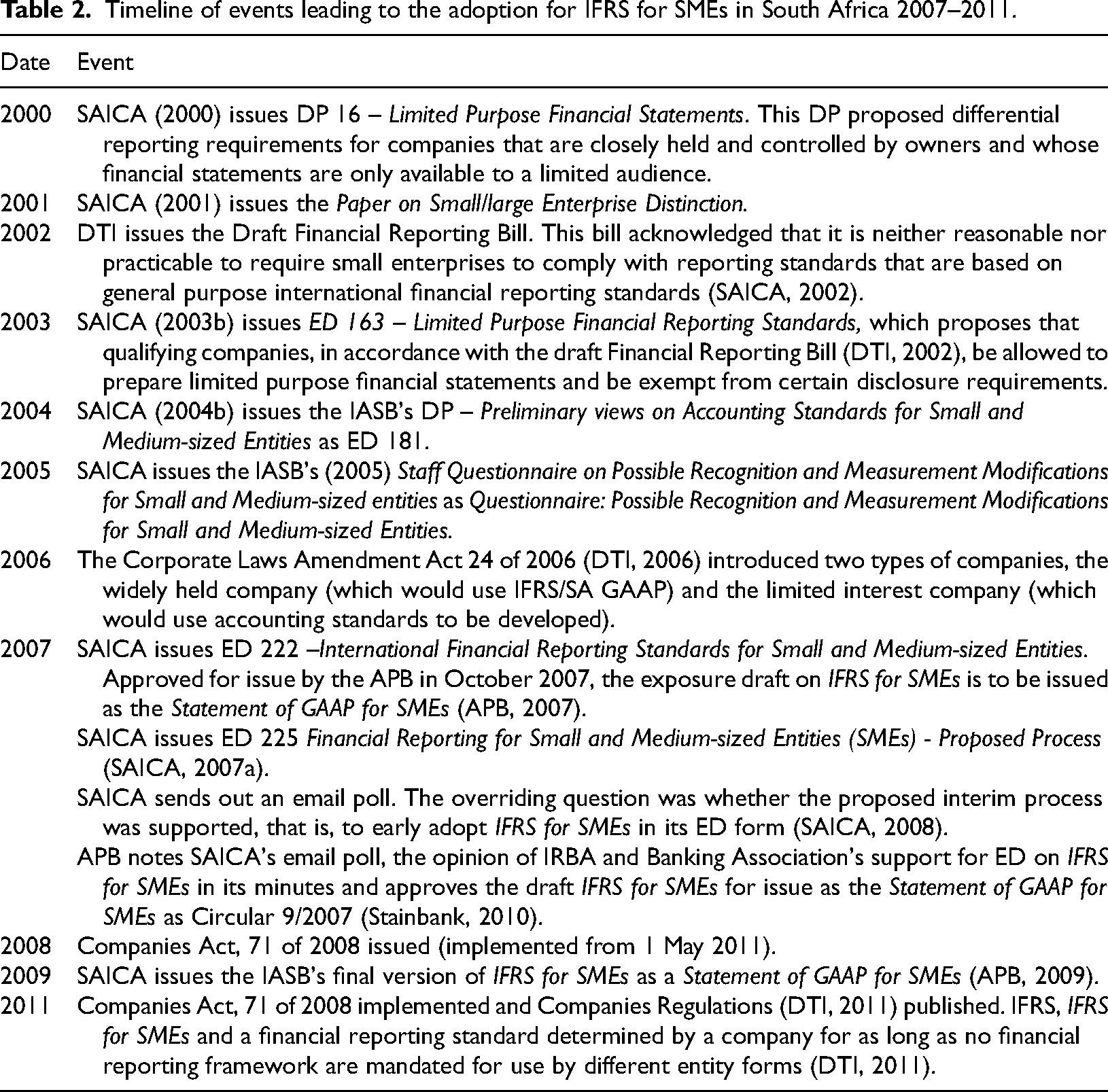

The adoption of IFRS for SMEs 2007–2011

The main events underpinning the adoption of IFRS for SMEs in South Africa, as described earlier in this article, are shown in Table 2.

Timeline of events leading to the adoption for IFRS for SMEs in South Africa 2007–2011.

Table 2 shows that research carried out by SAICA (2007a) provided the APB with the impetus to early adopt the proposed IFRS for SMEs. In its minutes dated the 7 August 2007, the APB noted that the SAICA had sent out an email poll requesting members to vote online on whether they agreed with ED 225 (i.e., whether they agreed with the proposed process) (APB, 2007). Of the 175 members who voted, 144 (82%) were in favour of the proposal to adopt the ED on IFRS for SMEs. The APB noted that a recurring theme in the comment letters was that, although it may not be the ideal solution to adopt an ED as a Statement of GAAP, it was currently the best alternative and would provide relief for financial accounting by SMEs, and particularly those that were limited interest companies. The APB also noted that 800 people had attended discussion forums held throughout South Africa and that there had been strong support for issuing IFRS for SMEs in its exposure draft form.

The APB (2007) minutes noted that the IRBA had questioned whether the IFRS for SMEs would constitute a fair presentation framework for the purpose of the auditor expressing an opinion of financial statements prepared in accordance with it. The statutory audit standard-setter of the IRBA, the Committee for Auditing Standards, believed the exposure draft would be an acceptable framework provided it was updated with any future changes to the final international standard, and the framework was described as a framework for entities other than those with public accountability, irrespective of their size. The minutes (APB, 2007) also noted that the Banking Association South Africa supported the exposure draft on IFRS for SMEs, as they believed that financial statements prepared in accordance with it would satisfy the banks’ credit departments when granting credit to SMEs. These deliberations of the APB led it to unanimously (as required at that time) agree that the exposure draft on IFRS for SMEs be issued as a statement of GAAP with an effective date tied to the Corporate Laws Amendment Act, but permitting early adoption. One weakness of this approach was that any research undertaken to early adopt the exposure draft now underpinned the final statement.

The above analysis highlights the unique reporting environment of private companies in South Africa and the necessity for relief from the burden of complying with IFRS, but reporting in such a way that an auditor would be able to express an opinion on the financial statements. Applying a regulatory theory perspective to the above narrative, the release of the Corporate Laws Amendment Act (DTI, 2006) prompted the necessity to find a suitable framework for limited interest companies, although the accounting profession had been considering a differential framework for several years (SAICA, 2004b). This may indicate that the regulation was in response to public demand (i.e., to provide relief to private companies from the onerous provisions of IFRS). However, after the promulgation of the Act, the body responsible for standard setting used mainly research and opinions generated by SAICA for their decision to early-adopt the draft IFRS for SMEs. The main beneficiary of this decision was SAICA, as at that time only SAICA members could be members of IRBA. IRBA also benefited as it now had a framework to use on which its registered auditors could express an opinion. SAICA also used the opportunity to market itself locally and internationally with its proclamation that South Africa was the first country to use the exposure draft as a standard (Stainbank, 2010).

The points above indicate that although the APB at that time was the standard setter, both SAICA and IRBA benefited from the decision, which was based on research provided to the APB through the APC. Both IRBA and SAICA managed to capture the process for the benefit of their members, an indication of private interest capture theory. If, on the other hand, the reason for its adoption was in the public interest, then this would indicate elements of public interest theory. Limited interest companies did benefit in that they now had a less onerous accounting framework they could use; however, most of the respondents to the consultative documents issued by SAICA could not be considered owners and/or users of limited interest companies’ financial statements as the viewpoints of the profession (or preparers of financial information) were used to guide the standard setting decisions (Stainbank, 2010), and therefore elements of capture are present. The analysis of the events up to 2007, leading up to the adoption of IFRS for SMEs, may reflect elements of private interest capture theory and public interest theory. The decision of the government to embody IFRS for SMEs in law would reflect the public interest theory. The analysis also shows that the profession was quick to respond to the need for a framework that limited interest companies could use, whereas the government took three years from enacting the Companies Act, 71 of 2008, to implementation (DTI, 2011).

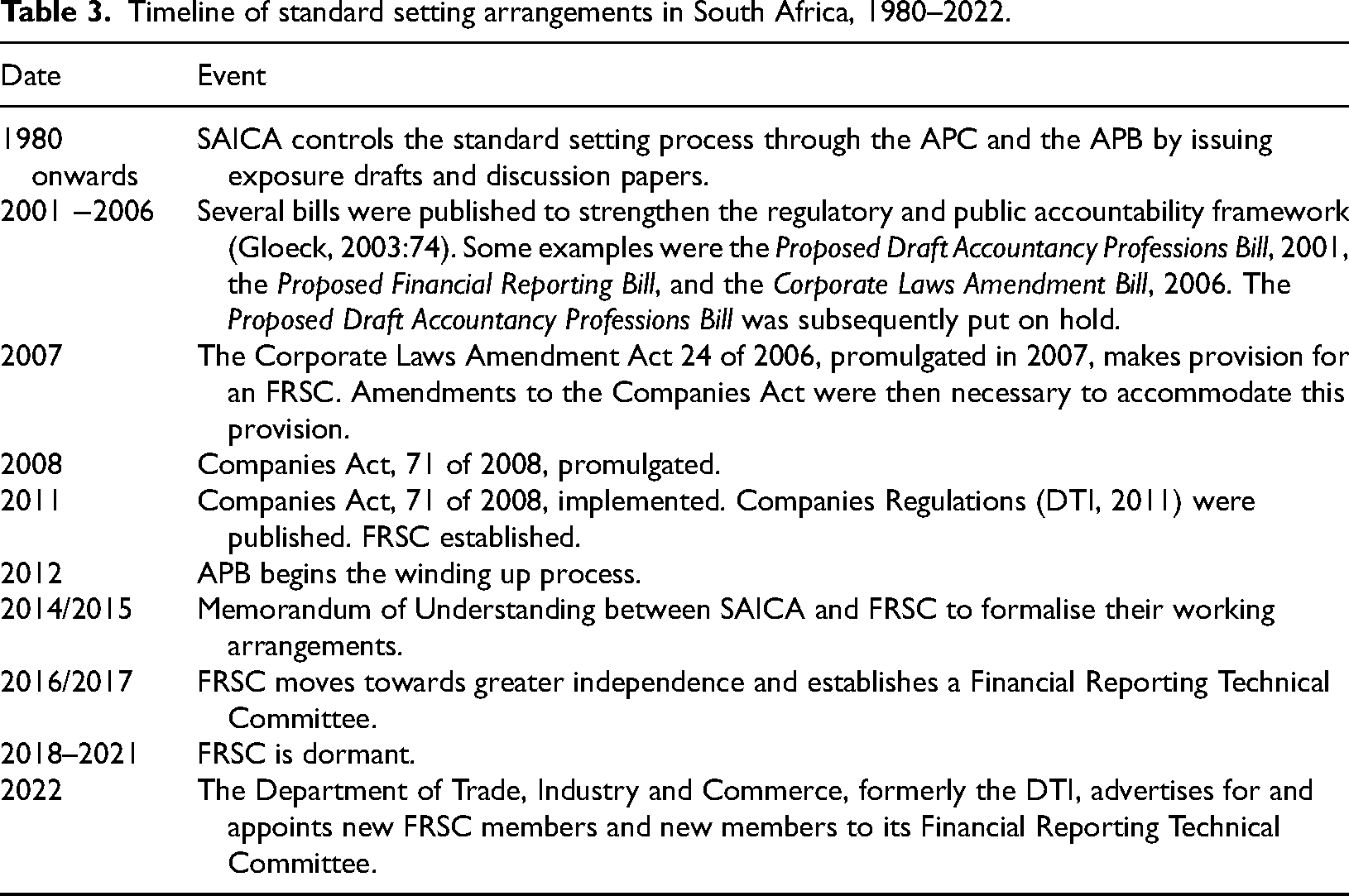

Standard setting arrangements in South Africa 1980–2022

The main events underpinning standard setting in South Africa were described earlier in this article. From the earlier discussion, the Joint Council formed in 1945 and renamed the National Council of Chartered Accountants in 1966, was renamed SAICA in 1980. From 1980 to 2012, SAICA controlled the standard setting process through the APC and the APB by issuing exposure drafts and discussion papers. Table 3 shows a timeline of important standard setting arrangements in South Africa from 1980 to 2022. The Companies Act, 71 of 2008, identified two types of companies, profit companies and non-profit companies, and allowed the Minister, after consulting with the FRSC, to establish different standards applicable to different categories of companies. These standards were published in the Companies Regulations (DTI, 2011).

Timeline of standard setting arrangements in South Africa, 1980–2022.

Gloeck (2003) condemned the standard setting process of SAICA, which controlled the process from 1980, for several reasons. These were because the standard setting process was secret, minutes and agendas were not available, members were selected rather than elected, members served in their personal capacities and did not represent any interest group, members had to sign secrecy declarations, there were no public representatives, comments had to be made in writing as there were no open sessions, the process of evaluating comments was subjective and unknown, and comments were not weighted according to their source.

Gloeck (2003) also criticised the proposed membership of the FRSC as indicated in the proposed Financial Reporting Bill which, was to be four audit practitioners, two preparers of public companies’ financial statements, two preparers of private companies’ (or personal liability) financial statements, four holders of securities or creditors who can be expected to rely on financial statements, two experts in company laws, one person representing the Financial Services Board and one person representing the JSE. He argued that it should include, amongst others, the South African Revenue Service, organised labour, academics, and the public. He suggested that FRSC members should not be partners/senior staff from the big auditing firms, accountability must be defined, and that an Accountancy Profession Act is missing from the proposed legislation. This last point was recommended by the World Bank in both its ROSC reports (World Bank, 2003, 2013).

The proposed membership of the FRSC was legislated in the Companies Act, 71 of 2008, and was unchanged from what had been previously proposed. At its inception in 2011, it was mainly chartered accountants who met the criteria for membership, resulting in the FRSC being populated mostly by chartered accountants, which would indicate that they were members of SAICA, with its first chair being a partner in one of the Big 4 accounting firms. This may indicate that SAICA, which had controlled standard setting through the APC and the APB, did not need to be the standard setter, as the FRSC was dominated by its members. The composition of the current FRSC is populated again with mostly chartered accountants, with its current chairperson also a chartered accountant (SAICA, 2022).

The composition of the APB, and now the FRSC, may suggest that the accounting profession, represented only by SAICA, may have had a continuing influence on the standard setting process, although the financial reporting standards to be used were now fixed in law. Although the 2015 operating procedures of the FRSC allowed for the establishment of a sub-committee to be chaired by a member of the FRSC and a Technical Secretariat, ‘[o]nce a project has formally been added to the FRSC work programme, an FRSC member will be assigned to Chair the sub-committee and the Technical Secretariat will support the Chair in leading the project’ (DTI, 2016), this task was informally handled by SAICA, which then formalised its arrangements with the FRSC by entering a Memorandum of Understanding with it.

According to the Memorandum of Understanding:

The FRSC attends the APC meetings, FRSC proposes to include the Financial Reporting Pronouncements (i.e., accounting matters unique to South Africa) in the Companies Act Regulations, and All SAICA comment letters are noted by the FRSC.

Although an analysis of the agenda items could infer that SAICA dominates the agenda, there is evidence that the FRSC does have contrary viewpoints on occasion, and agreement with SAICA does not signal SAICA dominance, as the issue could be one that has few controversial aspects to it (DTI, 2015). The minutes of the FRSC (7 July 2015) note that it is important that they be seen as independent and that it is important to establish its own technical committee (DTI, 2015). The minutes also noted that the former FRSC chair has had meetings with SAICA as to SAICA's role in standard setting, and that he would also meet with the South African Institute of Professional Accountants (DTI, 2015). The current chair, a member of SAICA, was appointed in 2022 (SAICA, 2022).

As the Companies Regulations, 2011 prescribed the application of IFRS or IFRS for SME with respect to all companies that require financial reporting standards (DTI, 2011), the FRSC has no role in setting accounting standards. The FRSC does, however, have an important role in participating in and influencing the IASB's standard setting process. The FRSC's due process, published in 2016, refers to several different stakeholder constituents with which it may liaise, signifying a future relationship that is more inclusive of other professional accountancy organisations and related accounting bodies (DTI, 2016). To fulfil its role, the FRSC draws on the expertise and technical resources of South African accountancy bodies, regulators, and business and investment professionals through its Financial Reporting Technical Committee (DTI, 2017). A perusal of the 2017 members of the technical committee does show the membership of two additional professional bodies to that of SAICA, which may indicate some attempt at inclusivity by the FRSC (DTI, 2017). Having its own Financial Reporting Technical Taskforce may indicate a more independent FRSC going forward.

The FRSC has a history of underfunding and capacity constraints (World Bank, 2013). The World Bank (2013: 29) noted that: ‘The Minister has appointed members of the FRSC, although he has yet to provide the FRSC with the necessary infrastructure to fulfil its mandate. … . Despite being supported by the Department of Trade and Industry, the FRSC has not yet been allocated a secretariat or budget support necessary to fulfil its mandate.’

It is possible that this allowed SAICA to step in and provide secretariat support to the FRSC from its inaugural meeting until recently, and was an expedient move by the FRSC in view of its lack of capacity.

The role of SAICA may have been reduced to that of a standard-taker, but it continued to play an important role with its presence on the IASB. Previously, the APB enjoyed a permanent position on the IASB's board (Zeff, 2012). Now, this position is the prerogative of the FRSC; however, it is still filled by a chartered accountant and its leadership in two publications of the IASB, IFRS for SMEs and the Guide on Applying IFRS for SMEs for Micro Entities (IASB, 2013) in the form of a toolkit, has allowed the SAICA to play an important role with its continued presence on the IASB. Having a SAICA member of the APC sub-committee on SMEs who was also on the IASB's SMEs implementation group would have allowed SAICA to share its expertise in this area (SAICA, 2014).

Using regulatory theories to explore the participants or members of the various committees and boards involved in standard setting and subsequent developments after the establishment of the FRSC, it is possible that the dominance of SAICA in firstly the APC and the APB, and subsequently the FRSC, through both the membership of the FRSC and the Memorandum of Understanding between it and the FRSC, may have allowed the SAICA to keep standard setting as its personal domain (private interest capture theory). However, with the 2016 publication of the FRSC's due process and the reference to different stakeholder constituents which it may liaise with, together with other professional bodies as members of its Financial Reporting Technical Committee (DTI, 2017), may indicate a more independent FRSC going forward. If independence requires institutional safeguards, appointment safeguards, financial support, basic authority and political factors (Rahman, 1992), it may be some time before all these factors are addressed and standard setting is seen as being wholly in the interest of the public.

Summary, conclusions, limitations and further research

This study explores the changes in South African standard setting processes using regulatory theories to guide the discussion. It is argued that the adoption of IFRS and IFRS for SMEs was in the public interest (public interest theory). However, the adoption of IFRS benefited several bodies in the corporate reporting and auditing arena, suggesting that not only was the adoption in the public interest, but that it also served the interests of the JSE and the accounting and auditing profession. Looking specifically at the adoption of IFRS for SMEs, the exposure that SAICA sought at that time in the media, locally and internationally, with its proclamation that South Africa was the first country to use the exposure draft as a standard, may indicate an element of interest-group capture theory. The adoption of the draft IFRS for SMEs was mainly to benefit IRBA and the auditing profession (to facilitate the expression of the auditor's opinion), and thus the influence of the auditing profession on this process would also indicate an element of private interest theory, and in particular capture theory.

It may be argued that the current standard setting process in South Africa is best described by public interest theory (the APB was, and now the FRSC is an independent body representing a wide range of interests). However, membership of the FRSC is skewed towards the auditing and accounting profession, who would mostly be members of SAICA. The Memorandum of Understanding between the FRSC and SAICA indicates interest group capture theory (especially as the other PAOs in South Africa were excluded from this process). However, the Rules of Procedure published in 2016 show the intention of the FRSC to establish liaison relationships with a wider group of stakeholders.

The analysis shows that public interest theory is the dominant regulatory theory in South Africa and that adopting IFRS and IFRS for SMEs was because of expediency rather than research. While standard setting in South Africa is legally the domain of the FRSC, it was substantially underpinned by SAICA, with other PAOs excluded, providing evidence of interest group capture theory. Sanada (2018: 339) referred to a ‘hybridization’ between statutory and professional control in the unique Japanese accounting environment. This is possibly comparable to the role taken by the accounting profession in developing guidelines (legally incomplete ex ante) for unique South African accounting issues, which were subsequently endorsed by the FRSC (ex post endorsement), and which shows that the expertise of the accounting profession is welcomed by the FRSC. Such a hybridisation could be inferred in South Africa, where a close working relationship exists between the accounting profession and the FRSC, where the FRSC may be considered a willing hostage rather than a ‘captured’ entity. The findings show, therefore, that public interest theory and private interest theory are not necessarily in direct opposition to each other, and that elements of both theories may become dominant during different phases of the standard setting process.

Current weaknesses in the South African reporting landscape are the lack of enforcement of accounting standards (although a Financial Reporting Investigations Panel formed by the JSE examines the published financial statements of listed JSE companies for compliance with IFRS) and the fragmented nature of the various professional accountancy bodies in South Africa, as noted by the World Bank (2013). The World Bank (2013) has recommended that there be enacted in South Africa, an Accounting Professions Act, like that of the 2005 Auditing Professions Act.

A limitation of this article is that not all the processes of the APB, FRSC, and SAICA may have been examined. It is possible that some of the members of the APB and the FRSC may have conducted their own (unreported) research into IFRS and the users of SMEs’ financial statements and their needs. It is possible that other PAOs in South Africa were invited by SAICA to be part of the APC, yet did not take up this opportunity. Finally, other theories, such as institutional theory, may have been more relevant to the discussion.

Further research could consider how other PAOs could become part of the standard setting landscape in South Africa or whether they have another role to play. Interviewing the various members of the affected bodies may provide different viewpoints on the scenarios outlined in this article or a deeper understanding of the forces at play in the South African regulatory environment.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Notes

Appendix: Acronyms

| APB | Accounting Practices Board |

| APC | Accounting Practices Committee |

| DTI | Department of Trade and Industry |

| FRSC | Financial Reporting Standards Council |

| GAAP | Generally Accepted Accounting Practice |

| IFRS | International Financial Reporting Standards |

| IFRS for SMEs | International Financial Reporting Standard for Small and Medium-sized Entities |

| IRBA | Independent Regulatory Board for Auditors |

| JSE | Johannesburg Stock Exchange |

| PAAB | Public Accountants’ and Auditors’ Board |

| ROSC | Report on the Observance of Standards and Codes |

| SA GAAP | South African Generally Accepted Accounting Practice |

| SAICA | South African Institute of Chartered Accountants |