Abstract

Our article is a historical, narrative account of the context of, the expectations for, and the process of implementation of the New Zealand Government's adoption of accrual-based whole-of-government financial reporting. It also documents the results as they were assessed in contemporaneous official and quasi-official studies that the prior expectations were met in relation to expectations for impact on fiscal performance and position, transparency, and sustainability. Our article also supports the conclusion that expectations were met in relation to certain aspects of departmental performance, though this was not universally the case for departmental efficiency.

Keywords

Introduction

This article addresses the question of whether the introduction of accrual accounting by the New Zealand Government met the expectations that were held for it at the time. The expectations are captured in the reasons given for undertaking the reforms, of which accrual accounting was a part, namely, to improve the financial and non-financial performance of government departments and agencies, and to improve the fiscal performance and position of the government as a whole.

The introduction of accrual-based financial reporting in the New Zealand Government dates to the 1980s and 1990s and was enacted in the Public Finance Act 1989 (the PFA or ‘the Act’), which formalised what were then termed the ‘Financial Management Reforms’. These reforms were a package that comprised significantly more than the whole-of-government and accrual accounting reforms, as they also included reform of the budget and appropriation processes and extensive delegation of financial management authority to departments, amongst other changes. Importantly, in relation to this article, the PFA required the production of accrual-based financial statements for the New Zealand Government. Prior to the Financial Management Reforms, financial reporting by the government was fund accounting on a cash basis (Lye et al., 2005).

The New Zealand case provides a useful and insightful example of the impact of whole-of-government accrual accounting. This is especially the case as New Zealand was the first country where a national government introduced accrual concepts not just into its accounting, but also into its budgeting and appropriations (Newberry, 2014). The PFA required that government accounting be based on New Zealand generally accepted accounting practice (GAAP), which was at that time designed for the private sector, being well before the development of International Public Sector Accounting Standards (IPSAS). The subsequent adoption of IPSAS by the New Zealand Government occurred in 2014/2015. The novel contribution of our article is the articulation of the expectations and their realisation for whole-of-government accrual accounting in the context of a reform process in which whole-of-government accounting was fully integrated into an accrual-based public financial management system. This contribution serves to fill a gap in the literature, there being no account of the success of the New Zealand Government's accounting reforms against the expectations that were held for them at the time. This is potentially of value to policymakers who wish to understand the nature, context and success of the accounting reforms in New Zealand.

Part of the motivation for this article is to document the reform process and the expectations held for that process at the time it was undertaken. While more recent literature presents analysis of whole-of-government accounting and financial management in New Zealand from a range of perspectives (Newberry, 2014; Sharma, 2021), the authors consider that there is value in documenting the expectations for the reforms and the contemporaneous assessment of their effectiveness, as these are now some distance in the past.

In the next sections, we outline the research methodology and then the context of the whole-of-government accounting reform. We then classify the expectations of the reforms into two categories: (1) the micro perspective – expectations for improved departmental performance and (2) the macro perspective – expectations for improved fiscal policy and management. The achievement of expectations at both levels was also expected to lead to enhanced financial transparency and sustainability. There were also expectations regarding the further evolution of the reforms after initial implementation, which will be referred to only briefly in this article.

Research methodology

This article is a narrative history of the expectations held for, and reported results of, the whole-of-government financial reporting component of the reform process undertaken by the New Zealand Government in the late 1980s and 1990s.

It seeks to provide a factual description of the key elements of the reform process and relevant elements of its context, as well as contemporaneous assessments of the effectiveness of the reforms. The implementation strategy for the reforms is also described, as this could be expected to influence the success of the reforms and is therefore helpful in understanding the reported assessments of the reform's effectiveness.

We rely on documentation analysis as the method to establish the expectations that were held for the whole-of-government accounting reform at the time the PFA was developed and implemented. We also rely heavily on official and quasi-official documentation for the analysis of whether the expectations of whole government accounting were seen to be met, with our primary focus being on the 15 years after complete implementation – the period from 1994 to 2010.

There have been a number of studies which describe and assess the wider public management reforms, the expectations held for the reforms and the degree to which those expectations were realised (e.g. Brumby et al., 1996; Buhr, 2012; Hay, 1992; International Federation of Accountants, 1994; McKinlay, 2000; McKinnon, 2003; Schick, 1996; Scott et al., 1997). While this article draws on these studies and recognises the accounting reforms as a component of a wider set of reforms, its focus is specifically on the accounting reforms.

Context

As the New Zealand reforms date back to the 1980s, it is necessary to describe the context in which the expectations were formed if the rationale for the reforms is to be properly understood. Key elements of this context are:

The country faced a severe economic and fiscal crisis, crystallising around the 1984 General Election, which created an environment conducive to change. Following the 1984 General Election, the (centre-left) Labour Government initiated a radical program of micro-economic reform. Within the accounting profession and the public sector, there was existing awareness of the need for financial management reform.

The economic and fiscal crisis was the result of features of the economy such as poor productivity, high levels of tariffs and controls and ineffective stabilisation policies (Scott, 1996). One of the consequences of these factors was weak fiscal performance (in 1984, a (cash) deficit of 9 per cent of gross domestic product (GDP) (see Reserve Bank Bulletin, December 1984) or an adjusted financial balance of −6 per cent (see the Treasury, Fiscal Time Series data, July 2023) and an increasing level of debt (in 1984 central government debt was approximately 60 per cent of GDP (see the Treasury, Fiscal Time Series data, July 2023). In addition to the growing government deficits and public debt, New Zealand also experienced double-digit inflation and a downgrade in its credit rating in 1983 (Lye et al., 2005). From the fifth-highest standard of living in the Western world in the early 1950s, New Zealand's ranking fell to 25th by the late 1980s (Buhr, 2012). These factors had created a fiscal imperative to improve the performance of the government at both macro- and micro levels. This imperative was reflected in a high level of political commitment to the reform program on the part of the Labour Government and, in relation to the financial management reforms, bipartisan political support, with the (then) National Party Opposition also supporting the legislation.

The micro-economic reform program of the Labour Government during the 1980s has been well described (Scott, 1996). The public management component of this reform program was driven by the ministers’ assessment that the public sector management system suffered from: confused and conflicting objectives; centralised authority stultifying innovation and efficiency; over-reliance on often obstructive bureaucratic rules and procedures; and an unaccountable public service (The Treasury, 1987). The public management reform program re-shaped education, health, transport, defence and other sectors. As part of these reforms, the State-Owned Enterprise Act 1986 led to the creation of state-owned enterprises (SOEs), which were established as companies under the Companies Act 1993, with boards of directors selected for their commercial expertise. Section 4 of the SOE Act 1986 specified that their primary objective was to be as profitable and efficient as comparable businesses that are not owned by the Crown. The SOEs demonstrated improved performance in the form of returns on capital and improvements in the level and quality of services (Evans et al., 1996). Ministers perceived this as evidence of the potential gains from enhanced governance and management systems and contributed to the expectations held for subsequent reforms of the core state sector through the State Sector Act 1988 and the PFA.

Concern about the quality of accounting and financial management in the New Zealand public sector had been increasing in the decade prior to the PFA. In 1978, the Controller and Auditor-General published a report that was highly critical of financial management within the government (Controller and Auditor-General, 1978). While this report did not explicitly call for the Government to adopt whole-of-government accrual accounting, it triggered a discussion of public sector accounting and financial management within the accounting profession and the public sector. Contributing to this discussion were a New Zealand Planning Council paper on measuring the cost of government services (Ball, 1981) and the (then) New Zealand Society of Accountants developed a Statement of Public Sector Accounting Concepts (New Zealand Society of Accountants, 1987). Ball (1981) argues that accrual measures of service cost are superior to cash; however, this study did not recommend the full adoption of the accrual basis for government financial reporting. The Statement of Public Sector Accounting Concepts supported the full adoption of accrual-based financial reporting by the government and its agencies, except for assets classified as ‘community assets’. These developments created an environment that was supportive of the subsequent Financial Management Reforms, though in the event those reforms quickly superseded the developments in the profession (Hay, 1992).

Also supportive were the professionalisation of the Audit Office (Green and Singleton, 2009) and the establishment of the Financial Management Support Service (McKinnon, 2003), whose role was to assist departments to improve the quality of their financial management systems. Further, the debate within New Zealand was informed by what (relatively little) international precedent there was for national governments to adopt accrual accounting for non-commercial sub-entities or accrual-based whole-of-government accounting, and by discussion of the use of accrual accounting at the subnational level. The USA had taken steps in this direction at the national level with the passage in 1956 of legislation requiring executive agencies to account on an accrual basis (US General Accounting Office, 1970), though in the late 1980s, implementation of these reforms was, at best, incomplete. There was also debate at the state and local government level (Drebin et al., 1981), and some use of accrual accounting for certain funds, but it was not until the issuance in 1999 of the Government Accounting Standards Board (GASB) Statement No. 34, Basic Financial Statements – and Management's Discussion and Analysis – for State and Local Governments that comprehensive accrual-based financial statements for the whole of the government were required for state and local governments (International Public Sector Accounting Standards Board, 2006). Nevertheless, knowledge of these and other international developments informed the New Zealand debate.

An additional element of context is that the whole-of-government accounting reforms were designed as one element of an integrated public financial management system, rather than as a stand-alone reform, and that the public financial management system was itself seen as a sub-system of the wider public management system (Ball and Pallot, 1996; McCulloch and Ball, 1992). The changes to the public management system were given effect through two pieces of legislation – the State Sector Act 1988 and the PFA 1989, which together formed the basis for the new system of performance management and accountability (Scott, 2001). This further element of context is important in that the success or failure of the accounting reforms was, in part, conditional on other elements of the financial management and wider public management reforms, such as the dependence of the accounting reforms on access to skilled human resources, the availability of which was determined by the public sector employment arrangements. Notwithstanding that the accounting reforms were embedded in this wider set of reforms, the focus of this article is on the accounting reforms.

Expectations

The expectations for the whole-of-government accounting reforms can be classified into two major categories: (1) the micro perspective – expectations for improved departmental performance and (2) the macro perspective – expectations for improved fiscal policy and management. The basis for these two categories of expectations is described in the two subsections below.

Integral to these two perspectives were two further categories of expectation, which warrant mention – expectations for enhanced financial transparency at both micro- and macro levels, and an expectation for enhanced financial sustainability of the government. These two additional perspectives will be addressed in separate subsections below, where the results are discussed.

All these expectations were, however, most often expressed in relation to the financial management and wider public management reforms, rather than being specifically and solely related to the accounting reforms. Notwithstanding this, in the description of the expectations that follows, and in the description of the results, the focus will primarily be placed on the accounting reforms.

The micro perspective – improved departmental performance

The 1987 Briefing to the Incoming Government (Treasury, 1987) outlined the types of change the Treasury saw as necessary to get better performance from the public sector. If the Government wishes to have a public sector capable of producing high quality advice and managing its own affairs on a basis comparable with private sector efficiency, major changes in the nature of administration are essential. Some fundamental changes to the systems of financial management, performance assessment and pay-fixing are imperative. (The Treasury, 1987: 49–50)

The concept of departmental performance that underpinned the PFA had several key features, one of which was critical to the adoption of accrual accounting. It distinguished two elements of performance: performance from the perspective of the owner of the entity, and performance from the perspective of the customer or consumer of the products or services produced by the entity (Scott, 2001; The Treasury, 1989, 2011). This distinction was critical to the decision to move to accrual accounting, as without accrual accounting, it was not possible to measure key elements of performance from the perspective of either owner (capital maintenance) or customer (full cost of services).

Further, and linked to the intent to strengthen accountability, performance measured ex-post was seen to be more effective if it could be compared with expected (ex-ante) performance, implying the need for budgeting to be on the same basis as reporting. However, given that the budget was given formal authority through parliamentary appropriations, which were the legal authority for and constraint on spending, appropriations, too, were changed to an accrual basis. The rationale for this was that it reinforced the role of Parliament in relation to public spending and ensured that the public financial management system conveyed clear and consistent signals to managers on the performance expected of them. It strengthened the role of Parliament in three ways – by ensuring that all resource consumption required parliamentary approval (giving away a non-cash asset would require appropriation), by specifying more closely (via the specification of output classes) what services the appropriation was funding, and by distinguishing clearly which appropriations were within departmental authority (departmental outputs) and which were not (e.g. benefit payments) and therefore to whom Parliament was granting authority to incur costs.

The macro perspective – improved fiscal policy and management

An improvement in departmental performance was expected to result in improved efficiency and financial control, thereby contributing to improved aggregate fiscal performance. However, accrual accounting at the whole-of-government level was also seen as contributing directly to improved fiscal policy and management, recognising the value of a balance sheet approach to fiscal policy and the use of net worth (the difference between total assets and total liabilities) as a comprehensive measure of fiscal position.

Before the Public Finance Bill was drafted, the expectation that accrual-based information would contribute to fiscal policy was developing within the Treasury. In addressing deficit targets, the Treasury stated: While maintaining the Government's net worth constant in real terms ensures that current decisions will not make future generation's debt burden worse than the present one, there is no presumption that the Government's net worth is at an appropriate level now. Without complete information about the Government's balance sheet, including contingent liabilities, it is impossible to assess the level of the Government's net worth. However, the fact that past borrowing has largely been undertaken to fund current consumption makes it likely that the level of debt is high relative to the value of the Government's assets. This consideration suggests that a deficit level that actually improves the Government's net worth … is desirable. (The Treasury, 1987: 238–239)

An internal Treasury paper dated 13 February 1988, which sought to summarise the state of play in relation to financial management reform design, noted the following in a section on fiscal strategy: ‘A considerable amount of work has been devoted toward elaborating fiscal strategy in terms of a “net worth” concept. This work has been set out in Annexes to the 1986 and 1987 Budgets and the 1987 Post Election Briefing…’ (The Treasury, 1988: 3).

In considering the accounting implications of this (net worth) approach, the paper notes: There would be several advantages of moving to such an approach. First, it would facilitate the separation of decisions about current and capital transactions that the net worth approach invites. … Second, a movement toward accrual-based accounting along corporate lines would require that this be done at the individual department and agency level. In addition to facilitating better decision-making at the strategic level, this would provide better information about departments’ use of resources and allow better monitoring of their performance. Third, it would avoid, or at least discourage, the use of accounting sleight-of-hand to make the budget look better than it is (because this would be more difficult) and it would avoid embarrassment where cash accounting makes it looks worse than it is. (The Treasury, 1988: 6)

While the rationale for the move to accrual accounting initially lay principally in the expectation of improved performance by government departments and agencies, as the reform progressed attention moved to improvements in overall fiscal management to the extent that one of the designers of the reforms asserted that ‘accrual accounting for the whole-of-government will not amount to much more than an interesting accounting exercise unless the information is used for the purposes of economic management’ (McKinnon, 2003: 401).

The significance of the quotations above lies in their confirmation that the Treasury saw balance sheet information as important in improving fiscal management and hence fiscal performance and position. Without a transition to accrual accounting, this balance sheet information would not be available to decision-makers.

The expectations of accounting reforms in relation to fiscal policy were reinforced and increased in 1994 when the Fiscal Responsibility Act (FRA) was passed by a newly re-elected (centre-right) National Government. This Act established a set of principles for responsible fiscal management, most of which were based on accrual metrics – revenue, expense, operating balance and net worth, although the principles did not specify a numerical value for those metrics. Debt was also measured in accrual terms, so the debt principle also relied on accrual metrics.

The passage of this Act and its subsequent incorporation within the PFA gave greater importance to the fiscal policy and management dimension of the accounting reforms. So also did the requirement, established contemporaneously with the FRA via an amendment to the PFA, for the government to produce monthly (accrual-based) financial statements. This enabled regular monitoring of the government's performance within a fiscal year, making it more useful for making in-year adjustments to the fiscal track.

Summary of expectations

It is difficult to disentangle the expectations held for the introduction of whole-of-government accounting from the expectations of the wider financial management and public sector management reforms, especially as the accounting reforms were integral to achieving the benefits of other reform elements. Nevertheless, from the description above of the expectations associated with the introduction of whole-of-government accrual accounting, these expectations can be summarised to include at least:

Improved departmental performance, including greater efficiency in service delivery and enhanced management of assets; Improved fiscal performance and position, measured by reference to the principles of responsible fiscal management specified in the FRA and, in particular, the levels of debt and net worth. This improved performance and position was expected to generate more sustainable public finances with, as a consequence, a lower burden passed to future generations; The accounting changes underpinning the expectations for improved departmental and fiscal performance would lead to improved financial transparency and greater financial accountability from both departments and the government as a whole; and Improved fiscal performance at the macro-level would lead to the government having a stronger balance sheet, making it more fiscally sustainable and resilient.

The set of changes would, in the words of the then Auditor-General, ‘give effect to the most fundamental changes to financial management practices seen in New Zealand's history. These reforms are enormous, ambitious, and, in large part, unprecedented anywhere in the world’ (Controller and Auditor-General cited in Schick, 1996: 2). Consistent with this assessment, there was an expectation that the benefits of the reforms would be substantial.

Implementation

The implementation strategy for the reforms was developed with reference to the wider reform program, and it is important to understand how the results of the reforms were achieved. The elements most significant in relation to the adoption of accrual accounting are described below. 1

A key element of the implementation strategy, embedded in the PFA through the limited time period within which non-accrual appropriations would be available, was moving rapidly to implement the reforms at the departmental level (Scott et al., 1997). This speed of implementation was enabled by the bipartisan support the bill received in Parliament. Coupled with speed was the comprehensiveness of the change at the departmental level, with departments being required to move to an accrual basis at the same time for their budgets, appropriations and financial reporting. The rationale for this was that the accrual-based information would, from the beginning, be useful for decision-making and accountability purposes, being the basis on which in-year performance was monitored both within the department and by the Treasury. It also ensured consistency between ex-ante statements of intent and ex-post reports on performance, thus avoiding the conflicting signals that would have arisen had the budget and appropriations remained on a cash basis while reporting moved to an accrual basis. This approach also avoided the costs and negative motivational effects associated with requiring management to produce accrual-based information for year-end financial statements that they did not need for budget and appropriations monitoring, that is, for operational management purposes.

The Act gave departments a maximum of two years to develop accrual-based accounting systems, with the provision that the system must be capable of reliably monitoring departmental performance relative to accrual-based budgets and appropriations. Effectively, this meant all departments were preparing for a one-time switch from a cash-based to an accrual-based financial management system. Prior to these reforms, the cash-based government accounting system was run by the Treasury, so effectively departments were, for the first time, developing their own accounting systems. These systems needed to be accrual-based, and because they were required to monitor expenses incurred in relation to output appropriations, they needed to have a cost accounting capability. They also needed to be able to supply the Treasury with the accrual information it needed for budgeting and whole-of-government financial reporting purposes.

The PFA was developed alongside the State Sector Act 1988, which gave departmental chief executives radically greater authority in relation to the acquisition and employment of resources (inputs), including staff resources, while imposing accountability for the delivery of outputs. This expanded authority enabled chief executives to acquire the expertise to design and implement accrual-based financial management systems at a speed which would not have been possible under the previous public service employment arrangements (Scott et al., 1997). Given the novelty and challenge of the task facing departments, virtually all departmental chief executives replaced their chief financial officers. In fact, while the legislation gave departments two years to develop their own accrual-based systems, this was achieved by most within a year and by all departments within 18 months (Warren, 1994).

This rapid change for departments was coupled with a slightly slower implementation process in the move to accrual budgeting for the government. While departments were allocated budgets and appropriations on an accrual basis within two years, the whole-of-government budget moved to an accrual basis in 1994, with the financial statements for the year ended 30 June 1995 having the first budget: actual comparison. This slower time frame was for two reasons:

It provided time for all departments to move to the accrual basis, which was necessary to produce a whole-of-government budget or set of financial statements on an accrual basis; and It recognised the reputational risks associated with moving the principal financial event in the annual cycle (the budget) to an accrual basis before there was confidence in the accrual numbers being produced at the sub-entity level.

From an accounting perspective, one of the design features that enabled rapid and effective implementation was the requirement in the Act that financial reporting at both the departmental and whole-of-government levels was in accordance with GAAP in New Zealand (Warren, 1994). This facilitated the recruitment of accounting personnel who were familiar with the (accrual) accounting practices being implemented, the use of accounting software already in use within corporations and SOEs, and the development of specific accounting policies within the constraints of GAAP. A further benefit of adopting GAAP was that, being set independently of government, it removed accounting practices from the political sphere, reducing the ability of ministers to seek to influence accounting choices in order to present a view of performance and position more favourable to the government.

While New Zealand GAAP at the time was established for reporting by private sector entities, it nevertheless enabled the establishment, within GAAP, of accounting policies that reflected both the principles underlying accrual accounting and the differences between the public and private sectors (where those had implications for accounting treatments).

Also supporting rapid and effective implementation was the creation within the Treasury of a financial management assurance function that provided support for the development of departmental accounting systems and that signed off on the departmental readiness to move to an accrual basis of budgeting, appropriations and financial reporting (Warren, 1994). This assurance function both provided support to departments in their transition process, ensuring that they understood clearly the Treasury requirements, and gave Treasury confidence that the systems being put in place would meet the needs of whole-of-government budgeting and reporting.

Results

There have been many reviews of New Zealand's public management reforms of the 1980s and 1990s. For the purposes of this article, documenting the results of the reforms relative to the expectations held for them at the time draws heavily on these contemporaneous reviews. Those conducted in the relatively early years following the reforms (Schick, 1996; State Services Commission Steering Group, 1991) largely evaluated the reforms against the expectations of the time and were also conducted with an awareness of the system that had existed prior to the reforms.

Prior to describing whether the expectations relating to departmental performance and aggregate fiscal management have been met, it is useful to describe the conclusions that reviews of the wider reforms reached in relation to the accounting aspects of the reforms.

A decade after the passage of the PFA, a newly elected Labour Government commissioned a review of the public sector – The Review of the Centre. Rennie (2020) noted that review contained a summary of recent reviews of the public management system, and it is striking how many of those narratives both recognised the strengths of the earlier reform period but pointed to a common set of weaknesses within the public management system. (Rennie, 2020: 3)

In the context of this article, it is notable that none of these multiple reviews expressed reservations about the move to accrual budgeting, appropriations and accounting and the development of whole-of-government accounting, or suggested changes thereto. In 2011, a decade after The Review of the Centre, a further review (Better Public Services) also saw avenues for improvement in the public management system, but again expressed no concerns about the use of accrual budgeting, appropriations and accounting or whole-of-government financial reporting. These reviews did suggest changes to other aspects of the PFA, for example, amending the appropriations system to give greater flexibility.

More recently, the public financial management system has been evaluated against more contemporary criteria than the expectations at the time the reforms were carried out (refer to The Treasury, He Tirohanga Mokopuna, 2021: The Treasury's combined Statement on the Long-term Fiscal Position and Long-term Insights Briefing). However, again, the accounting dimensions of the system have not been questioned.

Perhaps the most widely cited review of the reforms (Schick, 1996) notes that the move to accrual-based financial reporting, budgeting and appropriations is one of the major management innovations pioneered in the New Zealand State sector since the late 1980s’ and that ‘(w)ithin about eighteen months after enactment of the Public Finance Act in 1989, all departments had shifted from cash accounting and budgeting to an accrual basis’ (Schick, 1996: 2). He also notes that ‘New Zealand has been the only country to move in tandem on both accounting and budgeting reform. Accrual budgeting significantly escalated the stakes in financial management reform, for the basis of decisions had to be altered, not only the form of financial statements. This bold recommendation actually facilitated reform by giving managers a clear message that they must quickly develop information systems to support full cost-based accounting and budgeting’. (Schick, 1996: 21)

Stace and Norman's (1997) empirical study of the views of senior managers on the public sector reforms produced a ‘scorecard’ of the changes. The summary scorecard showed ‘Financial management – the use of accrual accounting’ as ‘the undisputed success story, despite concerns about the cost involved … with one person terming them the “only unqualified success” of the public sector changes’ (Stace and Norman, 1997: 25).

McKinlay (2000) evaluates the theory and practice of the New Zealand public sector management reforms and identifies several areas where the practical application of the reforms has led to unintended consequences. On the introduction of accrual accounting, he concludes: ‘This part of the New Zealand reforms can really be regarded as an unqualified success’ (McKinlay, 2000: 7). And: New Zealand led the way in the adoption of accrual accounting for the public sector. That has been an outstanding success, as have other aspects of public sector financial management, including one which has not been covered in this presentation, the Fiscal Responsibility Act which underpins central government fiscal discipline by imposing a high measure of transparency and setting statutory standards for responsible fiscal management. (McKinlay, 2000: 33)

Departmental performance

There are no metrics that report aggregate departmental performance in the same way as can be done for aggregate fiscal performance. And, while fiscal performance can be measured directly using accounting information, departmental performance cannot.

In relation to ownership performance, while the cost of services can be measured with accrual reporting, efficiency measurement requires specification of the services, that is, it requires measurement of inputs and outputs. In this sense, the expectation of improved departmental performance requires accounting reform as well as the clarification and measurement of outputs. The extensive range of different outputs produced by the government makes aggregate efficiency measures impracticable.

However, there is evidence concerning changes in departmental performance, even if it cannot be aggregated: One does not have to search far for efficiency gains in the reformed State sector. Most departments have reduced staffing levels and operating budgets without lowering the volume or quality of public services. New Zealand managers are convinced that they are doing more with less – in some cases, with a lot less – and that they have been able to reduce costs because of their new flexibility in managing resources. (Schick, 1996: 4) the data which is currently available indicates that the reforms have brought significant gains in many areas. There is evidence, for instance, of greater productive efficiency (especially in the commercial parts of the public sector), improvements in the quality of certain services (e.g. the time taken to process applications for passports and welfare benefits has been drastically reduced), better expenditure control, better management of departmental budgets, greater managerial accountability, and major improvements in the quality of information available to policy makers…. (Boston, 1999: 8)

A review (Price Waterhouse Management Consultants, 1993) conducted after the regime was fully in place and there had been time to see its impact, concluded: ‘There are sufficient examples of the way in which the charge has influenced behavior to state unequivocally that the concept has been successful and that it is important to continue the regime and where possible improve upon it’(Price Waterhouse Management Consultants, 1993: 1). A study (Morris, 1995) of the capital charge alongside cash management reforms found that these led to savings of NZ$31 million per year in interest costs.

The second aspect of ownership performance is the quality of financial control. One dimension of this is adherence to budget (appropriation) limits. In the period before the reforms, overspending was the norm, and, as in many other countries, a limited level of overspending was seen as being advantageous in that it provided evidence that the current budget was insufficient and supported a need for a budget increase. In the period immediately following the PFA, the level of unappropriated expenditure fell, notwithstanding that budgets were significantly constrained during this period. This pattern of managing within appropriations became entrenched, evidencing both the incentives operating on managers and their ability to manage costs when they have authority to manage inputs.

The ‘purchase’ or service delivery dimension of departmental performance was also an important element of the reforms. The essence of this was the distinction in the management system between outputs and outcomes. Outcomes provided the rationale for government intervention, and outputs (goods and services) were one, albeit major, form of intervention. The role of outputs and outcomes has been controversial from the initial passage of the Act and was a matter of concern to Schick and many other commentators. Indeed, this has remained an area of concern until the present day.

Boston (2000) noted gains in the efficiency of output production (important from the owner's perspective) but also the quality (including timeliness) of the services themselves. Other studies supported these assertions to some degree (Brumby et al., 1996; Cangiano, 1996); however, the general conclusion on this issue suggested performance improvements were variable across departments, with little or no improvement in some.

Whole-of-government fiscal performance

The full implementation of the accounting reforms at a whole-of-government level was completed in 1994, the year in which the FRA was passed. A consequence of the FRA was to further integrate the financial reporting and the fiscal forecasting of the government. Not only is the same GAAP presentation used for both the fiscal forecasts and the financial statements, but the prior-year financial statements receive an audit opinion by the end of the first quarter, enabling an update of the forecasts to influence the budget strategy for the forthcoming year. There is integration of the budget formation, budget execution and budget reporting phases of the annual process.

In evaluating whether expectations were met, a comparison can be made between the 15-year period before the full implementation of the reforms and the 15-year period following the reforms. The latter period runs through until 2008, the year preceding the global financial crisis. In the 15-year period before 1994, the adjusted financial balance, which is the summary cash-based metric for financial performance prior to the introduction of accrual-based reporting, had been consistently in deficit, with annual deficits ranging from 1.3 per cent to 6.1 per cent of GDP. The mean deficit was 3.2 per cent of GDP. This measure changed incrementally over time, partly in response to political pressures, being prior to the legal requirement that the government's financial reporting comply with GAAP. In the 15-year period following the move, the operating balance, which is the summary accrual-based metric for financial performance, was consistently in surplus, ranging from 0.9 per cent to 5.8 per cent of GDP, with a mean of 2.6 per cent. Excluding gains and losses, there was a surplus in every year except 1994, with a range from −0.6 per cent to 4.5 per cent of GDP and a mean of 2.4 per cent of GDP. 2

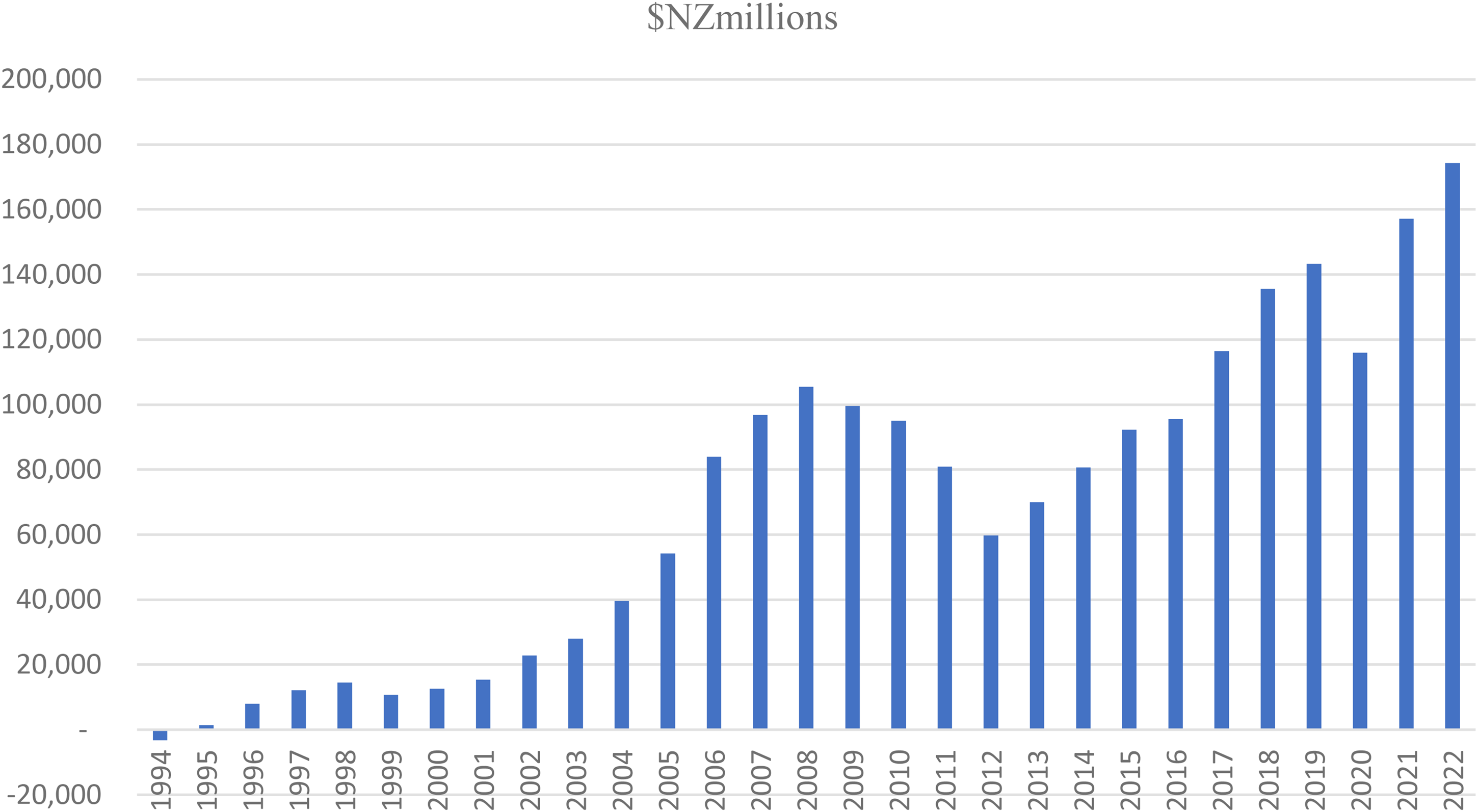

Unsurprisingly, a similar pattern is reflected in fiscal position. Using the (former) core Crown net debt metric – the only metric for fiscal position that is reported by the Treasury for the full 30-year period from 1979 to 2008, debt can be seen to rise in every year except two between 1979 and 1993, from NZ $2.5 billion to NZ $37.2 billion, and it then decreases every year from 1994 to 2008, from NZ$35.4 billion to NZ$0.02 billion. Total Crown net worth (Figure 1), a more comprehensive measure of fiscal position, not available until the introduction of accrual accounting, was negative NZ$3.3 billion in 1994 (following two decades of deficits), became positive in 1995, and then increased consistently through the period to 2008, when it stood at NZ$105.5 billion, equivalent to 55.8 per cent of GDP. In 1999, net worth declined by approximately NZ$4 billion as a result of an accounting policy change, recognising the Accident Compensation Corporation liability.

Total crown net worth 1994–2022.

The full suite of micro-economic reforms carried out during the 1984–1994 period was extensive and fundamentally changed the New Zealand economy as well as the operations of the government. The improvements in fiscal performance and position described above might conceivably have occurred without the adoption of an accrual-based financial management system. However, it is highly improbable that the poor fiscal performance prior to the reforms would have so thoroughly and contemporaneously resolved itself without the changes designed specifically to address those problems – including the move to an accrual basis for the financial management system.

Transparency

The move to accrual-based reporting and the presentation of whole-of-government financial statements substantially increased the comprehensiveness of the financial reporting, encompassing as it did the reporting of a full statement of financial performance, a statement of financial position, cash flow statements, plus several other statements such as the statement of contingent liabilities and statement of borrowing. This change in accounting approach represents, by its nature, a dramatic increase in transparency.

In the New Zealand case, this change is magnified by the incorporation of accrual numbers in a range of fiscal planning and budgetary documents, such as economic and fiscal updates (i.e. these updates are produced twice a year, first with the budget and then at the half-year, and also ahead of any general election), investment statements and statements of long-term fiscal position. These statements enable enhanced transparency, and therefore accountability, as the actual results for a period can be compared with those budgeted or forecast.

Further, the transparency associated with the shift to accrual reporting is reinforced by the production of monthly financial statements by the government. This reporting enables the accrual information to be used publicly for in-year monitoring of financial performance, enabling management action where warranted.

Finally, the transparency of the New Zealand Government's financial reporting is enhanced by the unbroken record of unqualified audit opinions at the whole-of-government level. There have been relatively few qualified opinions at the sub-entity level, further supporting the overall reliability of the reported financial information. In comparable countries, there have been occasional, or in some cases continuous, audit concerns leading to qualifications or disclaimers of opinion.

In the period immediately following the reforms, there was recognition of the significant increase in budget transparency (Campos and Pradham, 1997). This conclusion has been supported by the ranking New Zealand has received in the Open Budget Survey. New Zealand has ranked first equal in a number of recent years, though in the most recent (2023) publication, it ranks second. It should be noted that the methodology for this survey gives no credit for the additional information provided where the country budgets and reports on an accrual basis rather than a cash basis, notwithstanding the significant increase in transparency this yields, for example, information on property, plant and equipment.

Financial sustainability

This section addresses the impact of the accounting reforms on the financial sustainability of the Government. Financial sustainability has been defined by the Office of the Auditor-General (2013) as follows: …Public sector financial sustainability is the financial capacity of the public sector to meet its current obligations, to withstand shocks, and to maintain service, debt, and commitment levels at reasonable levels relative to both national expectations and likely future income, while maintaining public confidence….

The sustainability of the government's finances is most tested by crises. In the period since the passage of the Act, New Zealand has faced four crises: the Asian Economic Crisis (1997), the Global Financial Crisis (2008), the Canterbury earthquakes (2010 and 2011) and the Covid pandemic (2020). Using net worth as the best indicator of sustainability, the Global Financial Crisis and the Canterbury earthquakes had the largest impact on the government's fiscal position, both in terms of the size of the net worth impact and the period taken to recover from the shock, as shown in Figure 1.

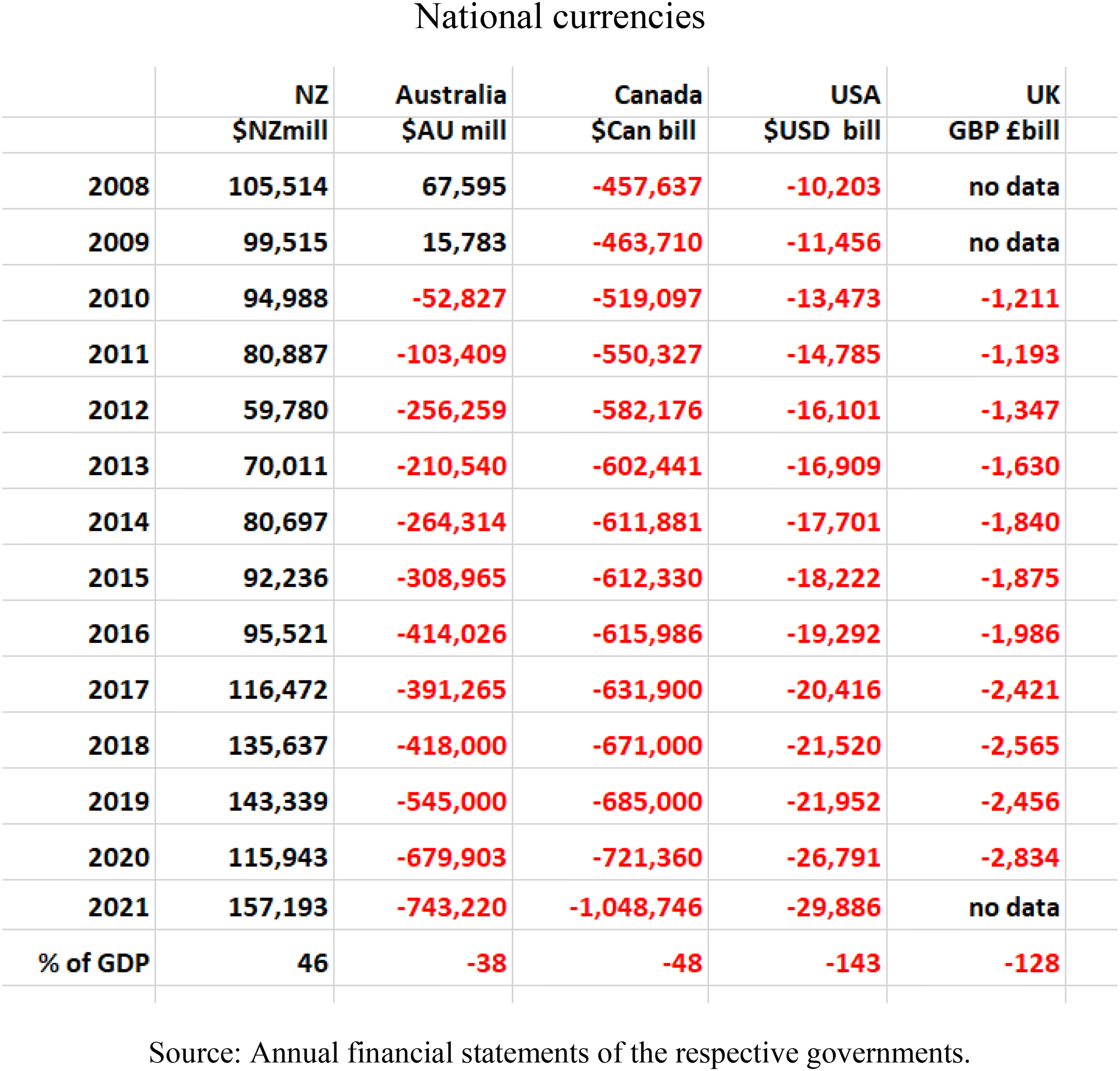

The government's financial position has recovered well from all these shocks, continuing to grow in nominal dollars. It has also maintained a positive and comparatively strong position relative to other countries. For example, total net worth at the end of the 2021/2022 financial year is positive and equivalent to 48.5 per cent of GDP, whereas the figures for comparable countries such as Australia, Canada, the UK and the USA are all significantly negative. While there are significant differences in the accounting standards and policies that underpin these numbers, all of which are sourced directly from the respective governments audited financial statements, as well as differences in the political structures of the different countries, the magnitude of the difference between New Zealand and the rest is nevertheless significant, at least in so far as it is the most comprehensive metric of fiscal position reported in all these countries.

Figures 1 and 2 demonstrate that the New Zealand Government built a strong net worth position over the three decades since the accounting reforms were introduced; strong relative to both its own past and to that of select comparative countries. From a New Zealand perspective, it is the trajectory of its own net worth that is most relevant and relates to the expectations held for the reforms.

Government net worth 2008–2021. National currencies.

The strength relative to other central governments and the trajectory relative to other governments raise interesting research questions about the apparent success of the New Zealand reforms relative to other countries that have similarly moved to produce accrual-based financial statements.

Conclusions

The results identified above suggest that in New Zealand, the expectations held for accrual accounting and whole-of-government accounting at the time they were introduced were substantially realised.

The enhanced fiscal performance at the whole-of-government level, leading to greater financial sustainability and improved financial transparency at both micro- and macro levels, can be seen as ‘expectations met’. The New Zealand case demonstrates that accounting can have a significant impact on the quality of financial decision-making and on financial outcomes. However, this conclusion is in the context where accounting reforms are an integrated element of a wider reform of public financial management and public management, a context that differs from other countries. There is also evidence from the cited reviews of improved asset management and financial control, as well as improved efficiency of departmental operations, though this latter is a more qualified conclusion, as the gains cited are not achieved by all departments.

What the New Zealand experience demonstrates is that, when designed as a component of a public financial management and wider public management system, and with a suitable implementation strategy, whole-of-government accrual-based financial information systems (accrual budgeting, appropriations and reporting) can play a significant role in improving the fiscal performance of a government, and through that the outcomes sought by its citizens. Many other governments that have introduced accrual reporting at the whole-of-government level have not had similar outcomes. For example, all the countries with which New Zealand is compared in Figure 2 have accrual-based financial reporting, yet their fiscal outcomes appear markedly different.

This article differs from the extant literature in that it documents the expectations for the accounting reforms at the time they were developed and implemented and reports the contemporaneous assessments of the extent to which those expectations were met. It also emphasises the importance of the context within which the accounting reforms occurred, and the implementation strategy employed.

This conclusion generates topics for future research. A key topic is the causal factors leading to the New Zealand outcomes (as compared with other countries), including the role of the integrated design of the financial management system and the implementation strategy of the reforms. The The Organisation for Economic Co-operation and Development, in its surveys of accrual experience of member countries (Moretti, 2016), has identified that the majority of countries that have adopted accrual reporting see significant benefit in terms of transparency, but much less so in relation to macro-fiscal purposes: …Most of countries that responded to the question on this issue indicated that the accrual information is not used or used only in a limited way for establishing fiscal forecasts. In many countries, the cash budget balance and net lending remain indeed the key fiscal figures, and focus most of the political debate…. (Moretti, 2016: 26)

Another potential research topic is the manner in which the New Zealand reforms gave increased prominence in fiscal management to accrual numbers in general, and net worth in particular. A further topic is the role of the principles of responsible fiscal management in building on the information base provided by the PFA. A final potential research topic is the role and impact of monthly accrual reporting as a mechanism for in-year budget monitoring and fiscal control.