Abstract

This empirical historical study uses prosopography to identify the backgrounds of a group of 15 chartered accountants who served in the Special Operations Executive (SOE) during the Second World War. Social capital ideas are used as the lens to explore these backgrounds. We discover that all 15 chartered accountants (CAs) were men, from middle-class professional families, who mostly attended public schools. They were chosen to join SOE because of their education, professional accounting training and relevant post-qualification experience. Most of the CAs served as accountants within SOE, where they facilitated SOE's clandestine financial warfare. Two of the CAs were SOE agents who saw action in Europe during 1944, with one being killed. The article demonstrates a prevalence of social capital, and old boys’ networks, but notes that this may have expedited the work of the SOE in challenging times.

Keywords

Introduction

This article outlines the findings of a prosopographical study exploring the background characteristics of a group of 15 British chartered accountants (CAs) who served with the Special Operations Executive (SOE) during the Second World War. The article is set in the broader context of professionalisation (Larson, 1977; Matthews, 2017; Matthews et al., 1998; Richardson, 2017a), social capital (Bourdieu, 1986) and the turbulent political, social and economic context of the 1920s and 1930s (Gardiner, 2011; Overy, 2009), the time period when the majority of these CAs were educated, trained and qualified. Prosopography is a method of studying a group of people by analysing their shared characteristics, rather than their individual lives. Previous prosopographical studies in accounting history have focused on the key players who drove the development of professional accounting associations in England, Scotland, Australia, Canada and the USA (Carnegie and Edwards, 2001; Carnegie et al., 2003; Edwards et al., 2006; Lee, 2006; Richardson, 1989; Walker, 2020), or those who have been major contributors to the accounting profession (Cobbin and Burrows, 2020; Parker, 1980, 2022; Parker et al., 2012). There have been calls for more prosopographical research in accounting history (Carnegie, 2019; Carnegie and McBride, 2023; Carnegie and Napier, 2017; McBride and Verma, 2021). This article answers these calls, it builds on previous prosopographical studies in focusing on a group of chartered accountants, it contributes by extending these studies to accountants in a historically important organisation that contributed to war efforts via financial warfare. The aim of the research is to investigate the background and networks or social capital of these chartered accountants in order to discover any commonalities and interconnections, determining the role of social capital in their recruitment and in the activities of their jobs. The research contributes to the literature using social capital ideas to explore the rationale for the recruitment of these particular accountants to SOE and to investigate the factors that influenced the roles they performed in SOE. It does this by analysing a variety of archival sources to set a context and in order to determine any shared social capital, exploring their family and social backgrounds; general education; professional chartered accountancy training, their pre-Second World War post-qualification work experience and their roles in the SOE.

The SOE was established in total secrecy in July 1940. An historically crucial organisation, its role, defined in a memorandum submitted to the British War Cabinet on July 19 1940, was ‘to coordinate all action, by way of subversion and sabotage, against the enemy overseas’ (W.P. (40) 271; quoted in West, 1993: 14–15). The hope of its main sponsor, the newly appointed British Prime Minister Winston Churchill, was that SOE would ‘set Europe ablaze’ (Dalton, 1957: 366). SOE was charged with organising unconventional, paramilitary and irregular warfare with no holds barred (Gubbins, 1948) from its Headquarters in Baker Street, London, under its official title of the Inter Services Research Bureau.

Initially, all funding for SOE came via the Secret Vote controlled by HM Treasury and outside normal parliamentary scrutiny (TNA HS 8/1017; Mackenzie and Millar, 2000). However as SOE grew, it developed more creative ways of financing its global operations, including trading foreign currency in black markets (TNA HS 8/354; Cruickshank, 1986; Murphy, 2005), dealing in designer watches and diamonds, and liquidating frozen Chinese bank accounts in India (Wharton-Tigar and Wilson, 1987). SOE spent over £21million between 1940 and 1945 from the Secret Vote alone, (Piper et al., 2023) and by 1944 had grown into a highly complex, multi-faceted, multinational organisation, employing over 10,000 staff and operating in Western and Eastern Europe, South East Asia, Africa and the Americas (Foot, 1984). The growth of SOE between 1940 and 1944 required a significant increase in the number of specialist training centres, as well as specialist centres for Wireless and Scientific Research (Station 1X), Arms (Station V1) and Devices and Special Stores (Station X11). In addition, each country in which SOE operated had a designated Section with its own support team. Each Section, training centre and specialist centre was responsible for producing and submitting monthly financial accounts to SOE's Director of Finance, John Franklyn Venner, FCA based in Baker Street (TNA HS8/1017). Venner was a partner at Edward Moore and Sons Chartered Accountants prior to the war and was held in high regard by those who knew him. Correspondence in Venner's SOE file (TNA HS 9/1524/7) identifies that Venner, ‘is thoroughly trusted by the Treasury and has carried out his duties in a most masterly way’.

Venner was not the only chartered accountant employed by SOE. This article observes that SOE's financial warfare was led and orchestrated by chartered accountants, who used their social capital, their networks, family and business connections, public school education, chartered accountancy training and post qualification business experience to obtain their place within SOE, and in the delivery of their leadership roles. From the archival records it can be observed that this group of chartered accountants did not work alone. The authors have identified incorporated accountants, cost and works accountants, audit clerks and bookkeepers employed by SOE, who all played a vital role in the implementation of SOE's financial warfare. It will be of future research value to explore these non-chartered accountant roles for ‘the experiences of the ‘voices from below’ (Carnegie and Napier, 2012: 346). In answering calls for research investigating social capital in accounting (de Villiers et al., 2022), this article consciously focuses on the chartered accountants serving in SOE to investigate any similar background characteristics of family, social standing, education and training and any networks or social capital.

The article offers contributions to the accounting history literature. First, it introduces these high-ranking individuals who were practising accounting and financial management within the SOE in time of war. This responds to calls for more micro-histories and prosopographies for analysis in accounting history (e.g., Anderson and Walker, 2009; Carnegie and Edwards, 2001; Carnegie et al., 2003; Carnegie and McBride, 2023). Second, the article develops ideas of social capital in the field of accounting history (e.g., Bryer, 2000a, 2000b, 2013a, 2013b; Edwards and Walker, 2010; Xu and Xu, 2008) and answers calls for social capital inspired insights and approaches for accounting history microhistories. Finally, this research adds to the literature on accounting during times of war and develops this by focusing on the accountants, whereas previous accounting history literature relates to the application of existing accounting knowledge or the development of new accounting knowledge (e.g., Cobbin and Burrows, 2018; Funnell and Chwastiak, 2010, 2015; Funnell and Walker, 2020; McBride, 2021; McBride et al., 2016).

The article is structured as follows. After this introduction, the next section reviews the literature associated with the development of the profession for the context and background of the chartered accountants working for SOE. Part of this is a brief explanation of social capital, which highlights the importance of social connections and relationships in shaping individual and collective outcomes. There is a broader background and context section, providing historical context to the time period of study, the influence of the Great War and the economic, political and social context. The next section details the research methods and data collection, noting possible project limitations. There is then a structured analysis of the findings, the background data collected for each CA and a discussion comparing the background characteristics and their social capital. The final section provides conclusions.

The profession and social capital

The professionalisation process

The rise of the professional accountant in the UK is a topic that has received a lot of attention in the literature (Edwards, 2010; Larson, 1977; Macdonald, 1984, 1985, 1995; Matthews, 2017; Matthews et al., 1998; Perkin, 1990; Richardson, 2017a). Professionalisation involves the formalisation of knowledge, with the requirement for qualifications based on education, examinations and a regulatory body with the power to admit and discipline members. The professional project was a process by which producers of special services sought to constitute and control a market for their expertise (Larson, 1977). With social closure, the process of exclusion of individuals or groups to prevent access to some benefit (Weber, 1949), and credentialism, the need to gain a certain credential or qualification to carry out the work, was used to control access to that work and to the associated benefit of performing the work (Parkin, 2019).

The required training was an important element of the professionalisation of accountancy. The introduction of onerous examinations, lengthy vocational training and significant financial hurdles combined together confined membership to the wealthier sections of society.

Social capital

Social capital relates to links, relationships and networks. It exists and develops from the social connections between individuals (Hanifan, 1916). Social capital can arise from relationships, personal, professional or organisational and negatively can exclude, dominate and perpetrate power (Bourdieu, 1986). Professional bodies obtain and build social capital among their members with common educational experiences, professional development, referral networks and, more generally, nurture a sense of professional identity among practitioners (Lawrence, 2004; Richardson, 2017b; Richardson and Jones, 2007). Social capital refers to the networks of relationships among people and the norms of reciprocity and trustworthiness that arise from them. It is a concept used in sociology, political science, economics and other fields to describe the value that individuals derive from their connections within social networks (Portes, 2000). Bourdieu (1986: 248) defines social capital as ‘the aggregate of the actual or potential resources which are linked to possession of a durable network of more or less institutionalized relationships of mutual acquaintance or recognition’. Bourdieu understood social capital as belonging to the individual and coming from social position and status. Social capital facilitates people to influence a group or individual who mobilises the resources of an organisation. Social capital becomes available to those who expend effort to move to positions of power and status and develop goodwill to achieve this (Bourdieu, 1986). For Bourdieu social capital is linked with class and other forms of differentiation, associated with benefit or advancement.

Accounting historians have shown an interest in the social background and class of the early British Accountants who led the development of chartered accountancy professional bodies in the UK (Anderson and Walker, 2009; Edwards and Walker, 2010; Lee, 1995, 2004, 2021; Matthews et al., 1998; Walker, 2020). The literature demonstrates how the social background of CAs in professional bodies changed in their early years of existence in order to construct the conditions of social closure and exclusivity required to deliver the well-qualified chartered accountant (Anderson et al., 2005: 5) associated with the Institute's professional project (Larson, 1977; Matthews, 2017).

Anderson and Walker (2009: 38) note that, among the founding fathers of the Institute of Chartered Accountants in England and Wales (ICAEW) in 1880, three members (16%) had upper-class fathers, with 61.7 per cent originating from the middle classes and 22.3 per cent from the working class. They determine that the early chartered accountancy profession was a comparatively open and accessible vocation. However, once established, they conclude (2009: 43) that ‘further institutional isolation was necessary and the ICAEW soon became associated with elitism and constructing a closed profession’.

The early Scottish chartered accountants formed the first of their three societies earlier than the ICAEW, (The Incorporated Society of Accountants in Edinburgh 1854; The Institute of Accountants and Actuaries in Glasgow 1855 and The Society of Accountants in Aberdeen 1867). Anderson and Walker (2009: 35) report that 18 per cent came from the upper class or nobility with only 1.7 per cent from the working class. Lee (2004) highlights that, as the number of Scottish CAs grew, they increasingly recruited men from lower middle- and working-class backgrounds, and the Institute of The Chartered Accountants of Scotland (ISOS) (1984: 111) states that this was especially true of the Institute of Accountants and Actuaries in Glasgow. By the 1930s, 13 per cent of the Glaswegian CA student intake was from working-class backgrounds (Cairncross, 1937).

Whilst most accounting historians accept the concept of professional exclusiveness, Matthews (2017) argues that the CAs never achieved a monopoly of the accountancy market and their training was not designed to exclude the lower classes. Despite this, Jacobs (2003: 572–573) argues that the chartered societies ensured that entry to their ranks was closed to any but the sons of the wealthier classes and effectively a class ceiling was established to prevent entry by the working class.

Women were excluded during the first two decades of the twentieth century, as socio-economic, constitutional and legal arguments were deployed to resist their admission and, despite reforming legislation, more enduring social and cultural obstacles to membership remained within chartered accountant firms (Hayes and Jacobs, 2017; Haynes, 2017; Kirkham and Loft, 1993; Shackleton, 1999; Virtanen, 2009; Walker, 2006, 2008).

For the chartered accountants in this study, social capital links and networks may have been generated both through their class, social standing and their professional qualification.

Background historical context

The shadow of the Great War

McBride and Verma (2021) emphasise the importance of looking at accounting in its historical context so that an understanding of the past can lead to comprehension of the present and foresight for the future. Most of the CAs undertook their education and accountancy training during the 1920s and 1930s. These were turbulent times, economically, politically and socially, not just in Great Britain but across the world. The period has been described by historians as being the Morbid Age, highlighting ‘a crisis of civilization’ (Overy, 2009: 363). The 1920s began in the shadow of the Great War. Over a million British lives had been lost between 1914 and 1918, with the highest ratio of fatalities amongst the commissioned officers educated at public schools. Seldon and Walsh (2013), calculate that over 35,000 pupils from Public Schools died in the Great War at an attrition rate of 20 per cent of those who enlisted, compared to 11 per cent for other groups of enlisted men. Public Schools erected memorials to this lost generation, held annual remembrance services and in some cases awarded prizes named in honour of their Great War dead. One such prize was the Geoffrey Gunther Vision Prize for Art, awarded by Eton College in honour of the artist who served with the Grenadier Guards, was killed on November 4, 1918 and had been awarded the Military Cross for conspicuous gallantry (The London Gazette, 31 January 1919). In a twist of fate, this prize was won in 1927 by one of SOE's CAs, Christopher Blathwayt (Eton College Register). At least two of the CAs featured in this article lost close family relatives in the Great War; John Venner lost two cousins and Mostyn Davies's father was killed in action in 1917. With these losses at the public schools the CAs attended being highlighted and lauded, this may be a background factor in their decisions to serve when war broke out again in 1939.

Economic, political and social context

By 1926 the optimism and brief economic boom following the end of the Great War had turned to despair, leading to the General Strike in that year which saw 1.7 million people protest against low pay and poor working conditions (Laybourn, 1993). The 1930s started with the Great Depression, leading to further reductions in pay and employment for working-class families in the traditional heavy industries of coal mining, shipbuilding, iron and steel trades and textiles, and unemployment climbed to almost 3.5 million by 1932 (Temin, 2016). It was particularly acute in the Northeast, the lowlands of Scotland and the mining valleys of Wales. The government seemed incapable of any solution and reluctant to invest in public works to provide jobs, instead introducing the Means Test in 1931 which divided families and led to widespread hardship and bitterness (Weldon, 2021). The response was a series of hunger marches by which the unemployed sought to draw attention to their plight. Despite significant expansion of the right to vote in 1918 and 1928 and the emergence of the Labour Party, this time period saw mostly minority governments with little authority (Reynolds, 2014). The impotence of central government encouraged the growth of extremist political parties – the British Union of Fascists led by Sir Oswald Mosley and the Communist Party of Great Britain which started to attract young intellectuals to its core membership of industrial workers. But neither ever achieved mass support (Gardiner, 2011). The worsening political situation in Germany throughout the 1930s was a portent for a future war and it was in this turbulent world that the SOE CAs began their education, training and careers in the business world. There are many current parallels to the time period of study, in terms of economic uncertainty, increasing poverty, political instability and a war in Europe. It is the authors’ belief, (also Cordery et al., 2023), that this provides further reason to study the lives of these SOE accountants from 100 years ago in order to see the lessons they can provide today's generation of accountants.

The methods used to collect and analyse the data used in this study are discussed in the next section of this article.

Research method

Prosopography

Stone (1971: 46) defines prosopography as ‘the investigation of the common background characteristics of a group of actors in history by means of a collective study of their lives.’ Common background characteristics include date and place of birth, date and place of death, marital status, place and type of residence, educational setting and levels, ethnicity, personal wealth, occupation and religion. The Times Literary Supplement (1970: 1326) observed prosopography was ‘a term borrowed from the ancient historians’, adding that, to the prosopographer, ‘the group is held to be more interesting than the individual or institution’. Whilst accounting is a human activity, conducted by individuals who have varying degrees of influence and social standing (Carnegie, 2019), prosopography suggests that there might be further insights to be gained from exploring accountants working in a connected group.

Stone (1971: 47–48) states that prosopography has developed into two main schools: the ‘elitist school’, concerned with small group dynamics or ties of family, marriage and economic ties of a restricted number of individuals, and the ‘mass school’, concerned with a large number of people about which nothing very detailed or intimate can be known, the voices from below. The common interest of both schools is the focus on the group rather than the individual or the institution. Prosopography is therefore concerned with exploring patterns underpinning the relationships and connections of a well-defined group of individuals (Carnegie and McBride, 2023). By focusing on the chartered accountants who served in SOE, this article consciously adopts a social capital approach. The main reason for concentrating on chartered accountants in this study is that the authors believe that these leading figures in the SOE may be an interconnected group, likely to share common background characteristics and social capital. There is however scope for a more ‘voices from below’ approach to future research (Carnegie and McBride, 2023) to explore the contribution made by the other types of accountants, clerks and bookkeepers employed by the SOE.

Prosopography has been used in accounting history studies, mainly tracing the development of the founding associations of Chartered Accountants (Carnegie and Edwards, 2001; Carnegie et al., 2003; Edwards et al., 2006; Lee, 2006; Richardson, 1989; Walker, 2020) or key individuals who drove the development of the accounting profession (Cobbin and Burrows, 2020; Parker, 1980, 2022; Parker et al., 2012). The approach has also been utilised in the literature on business history in the study of business leaders (Mills, 1945, 1956) as well as professionalisation (Fellman, 2014). Prosopography, however, remains a relatively underused research method for accounting historians (Carnegie and McBride, 2023) and accordingly, prosopography in accounting history remains in short supply despite its investigative potential. Carnegie and Napier (2017) state that considerable scope exists for the conduct of prosopographical research in accounting history across a wide array of different groups of actors in accounting's long past. By utilising both prosopography and social capital, this study provides insights on how the social capital of this group of chartered accountants enabled them to obtain roles within the SOE, to then shape these roles and facilitate working together.

Archival and bibliographic research and sources

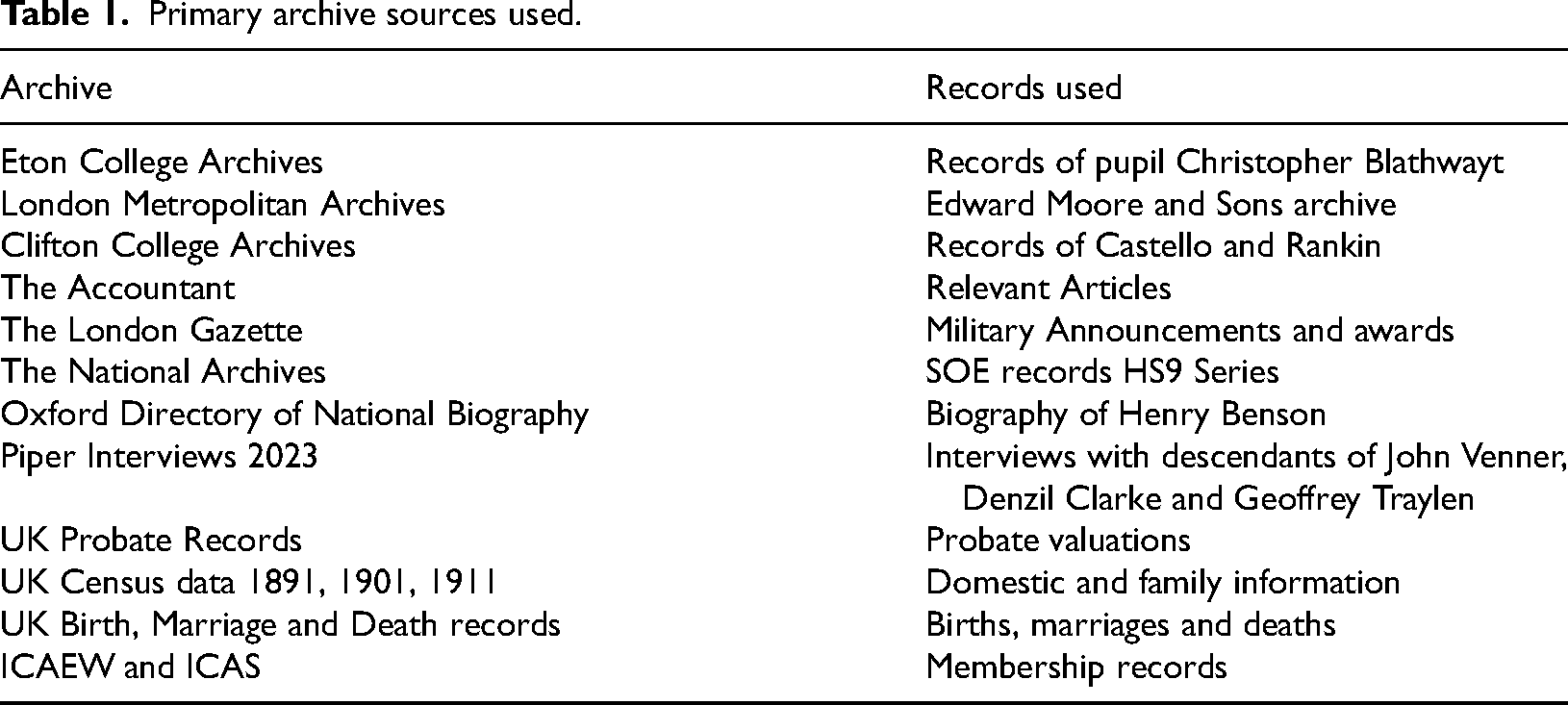

Prosopography requires the detailed examination of relevant and accessible primary information on the background characteristics of each individual in the group being studied. The sources of this information can include genealogical websites (births, marriages, deaths, census data, probate), institutional archives, newspaper archives and the memories/documents of living family members. Cowman (2012) identifies two potential limitations associated with all prosopography studies. The first relates to deficiencies in the data and the availability of relevant material in the archives. The second limitation is that the quantity of archive material might vary for each individual, leading to an unbalanced analysis allowing the better represented sources to dominate the narrative.

A wide variety of archival sources has been used in this study, to generate as wide an information base as possible for each individual. SOE files for all 15 CAs were located and analysed, and genealogical searches on all 15 men have been undertaken and compared with data from ICAEW and ICAS to triangulate the relevant information for accuracy. The archives used include The National Archives, London Metropolitan Archive (for Edward Moore and Sons archive), ICAEW and ICAS and 11 Public School archives. These archives are not complete, so there are gaps in the data, for example, where information is missing in SOE files. There is also more information available for those CAs with prominent careers (Benson, Clarke), and there is also more information available for those who worked at Edward Moore and Sons (Venner, Traylen, Snow and Price), where many records were retained. Independent verification of details was provided by the libraries and archive service at ICAEW and ICAS. Following ethical approval from the University of Portsmouth, individual telephone interviews were conducted with living relatives of three of the CAs (Venner, Clarke and Traylen), adding some richness to the data available. The data was explored to find common background characteristics, with consideration of family, education, accounting training and post-qualification experience, and information on the roles undertaken in SOE by each of the CAs. We conducted a thematic analysis (Braun and Clarke, 2006) of the documents found in the archives to interrogate the text and identify themes. This included careful reading of the documents to familiarise with the data, noting initial ideas and starting to see recurring patterns or topics. Then the rereading and recording of relevant information captured the themes related to prosopography and the influence of social capital. These themes were reviewed to ensure they accurately represented the archival data.

This article investigates 15 CAs who are known to have served in SOE. However, it is likely that there were more CAs who served in SOE who, at the point when the primary research was undertaken, remained unidentified. The authors believe that this potential limitation should not invalidate the article's findings, as no new background characteristics emerged from the last two CAs identified (Bisset and Blathwayt), leading the authors to conclude that ‘saturation’ (Saunders et al., 2018: 1894) in the data had been reached, and that further data collection could be discontinued (Table 1).

Primary archive sources used.

Findings and analysis

Unlike the existing and well-established secret services MI5 and the Secret Intelligence Service (SIS, now known as MI6), who were accountable to the Home Office and Foreign Office respectively, SOE was directly accountable to the new post of Minister of Economic Warfare, who in July 1940 was Labour MP Hugh Dalton, and so through him SOE had a direct line of access to the new Prime Minister, Winston Churchill.

In August 1940 Dalton brought in public school-educated Sir Frank Nelson, who had a business background in the City of London and had served in SIS, to be SOE's first Chief Executive. The SOE recruited many of its early recruits from Legal and Accounting firms in the City of London. Given Sir Frank Nelson's business connections with the City of London and the need to recruit in total secrecy, this was unsurprising. These recruits would have been considered as being the ‘right type of people’ having had similar privileged social, educational and professional backgrounds. It is also likely that many recruits would have known each other in civilian life and would have had the same social, business and cultural networks. In many ways, SOE recruitment was linked to the ‘old boys’ network’ and could be seen as ‘jobs for the boys’ Gladwyn (1972: 106). This reference to social capital networks, is highlighted in the idea, ‘that (the fact) they all had the same start did something to facilitate relationships and thus promote efficiency’.

The authors initially identified one of the first CAs who served in SOE, Henry Benson (Benson, 1989), which then led to John Franklyn Venner, SOE's Director of Finance, who is mentioned in Benson (1989: 37) as a ‘good friend’. Research in the National Archives identified a further three chartered accountants who worked with Venner at SOE HQ in Baker Street (Traylen, Snow and Price) and a Scottish CA who served with SOE overseas in Force 136 (Anderson). A further seven were identified from an SOE staff database archive, (Clarke, Webster Davies, Donavan, Castello, Bisset and Blathwayt), and two more by the archivist at Clifton College (Rankin and Frank). Eleven of the chartered accountants qualified in England and four qualified in Scotland. These accountants did indeed share background characteristics, networks and social capital. 1

This section provides an analysis of the data for each of the background characteristics explored. This is then followed by a discussion of each of these further findings.

Family and social background

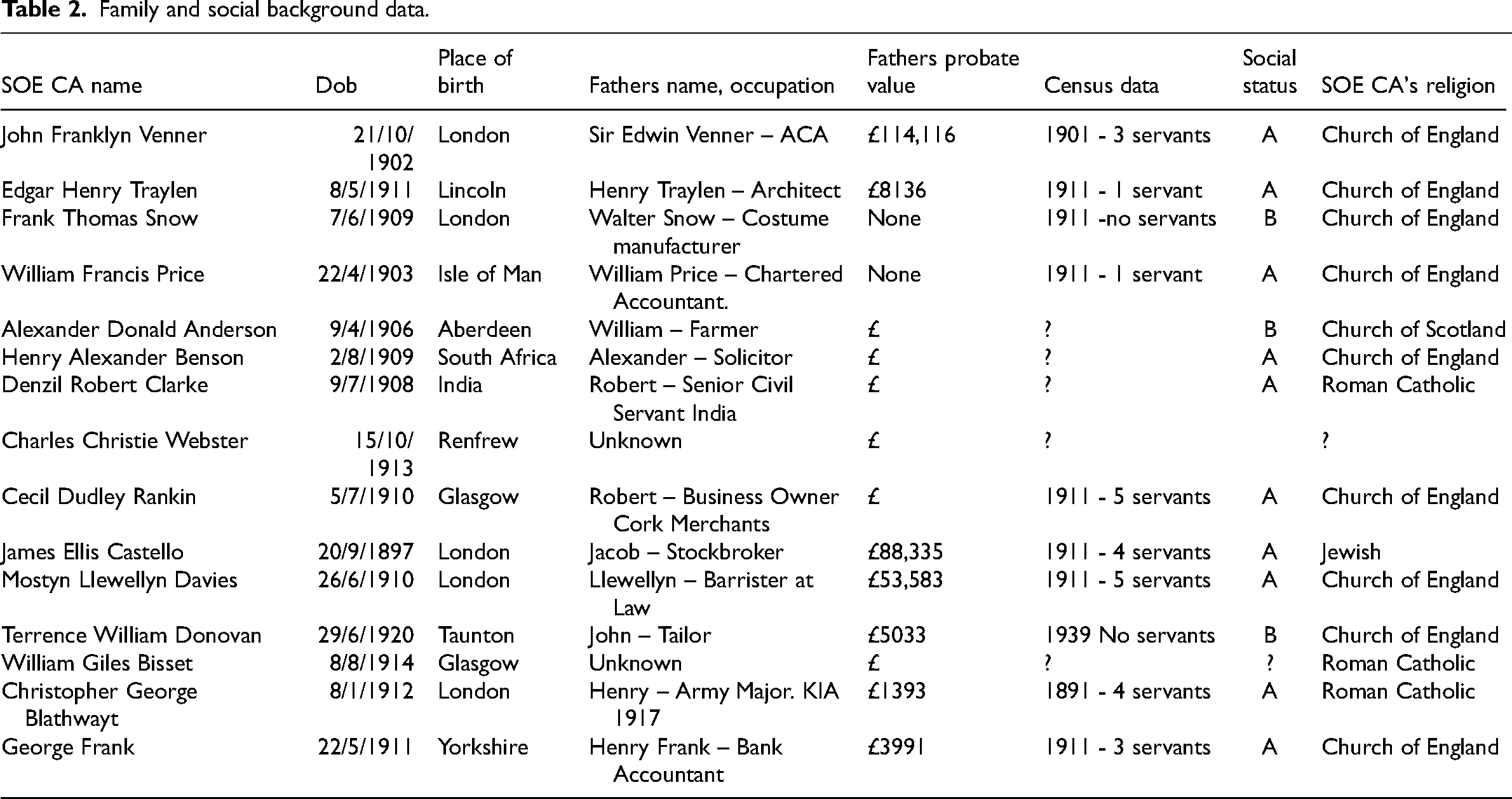

Despite the attempt in Glasgow to widen the entry path for men from working-class backgrounds to the chartered accountancy profession, the fact remains that analysing the social class of chartered accountants in the first 40 years of the twentieth century means dealing with elite men of the profession (Matthews, 2019) and the Priesthood of the Industry (Matthews et al., 1998) (Table 2).

Family and social background data.

All 15 CAs were male; 14/15 of the SOE CAs were born in the first 20 years of the twentieth century, with the majority born in the UK and those born overseas (Benson and Clarke) having British parents living and working abroad in South Africa and India respectively. The majority of their fathers, where their occupation was known, were in professional or senior business roles, for example, chartered accountant, architect, stockbroker or barrister. UK Census records from 1901 and 1911 identified that eight of the families employed domestic servants and cooks. Probate information provides evidence of high wealth (Venner, Castello and Davies) but also evidence of more modest means (Traylen, Donovan, Blathwayt and Frank). The majority of the CAs were of the Christian faith (nine Church of England, one Church of Scotland, and three Roman Catholic) with one being of the Jewish faith.

The social status of the family of each CA was analysed using the ABC1 system of classifications of occupation (Meier and Moy, 2004; Reynolds, 1991), and as anticipated in the literature, all of the families sit at category A or B, defined as: -

Professional people, very senior managers in business or commerce or top-level civil servants (upper middle class). Middle management executives in large organisations with appropriate qualifications; principal officers in local government and civil service, top management or owners of business concerns, educational and service establishments (middle class).

The information available supports the idea of social capital, with the social background of most CAs in the early twentieth century as being that of the upper to middle and middle classes, with parents who could provide the financial support required to sustain an articled clerk's education and training. These accountants came from backgrounds where social capital could be leveraged and the affordance of a professional qualification built on increasing the social capital networks was available to them.

Education

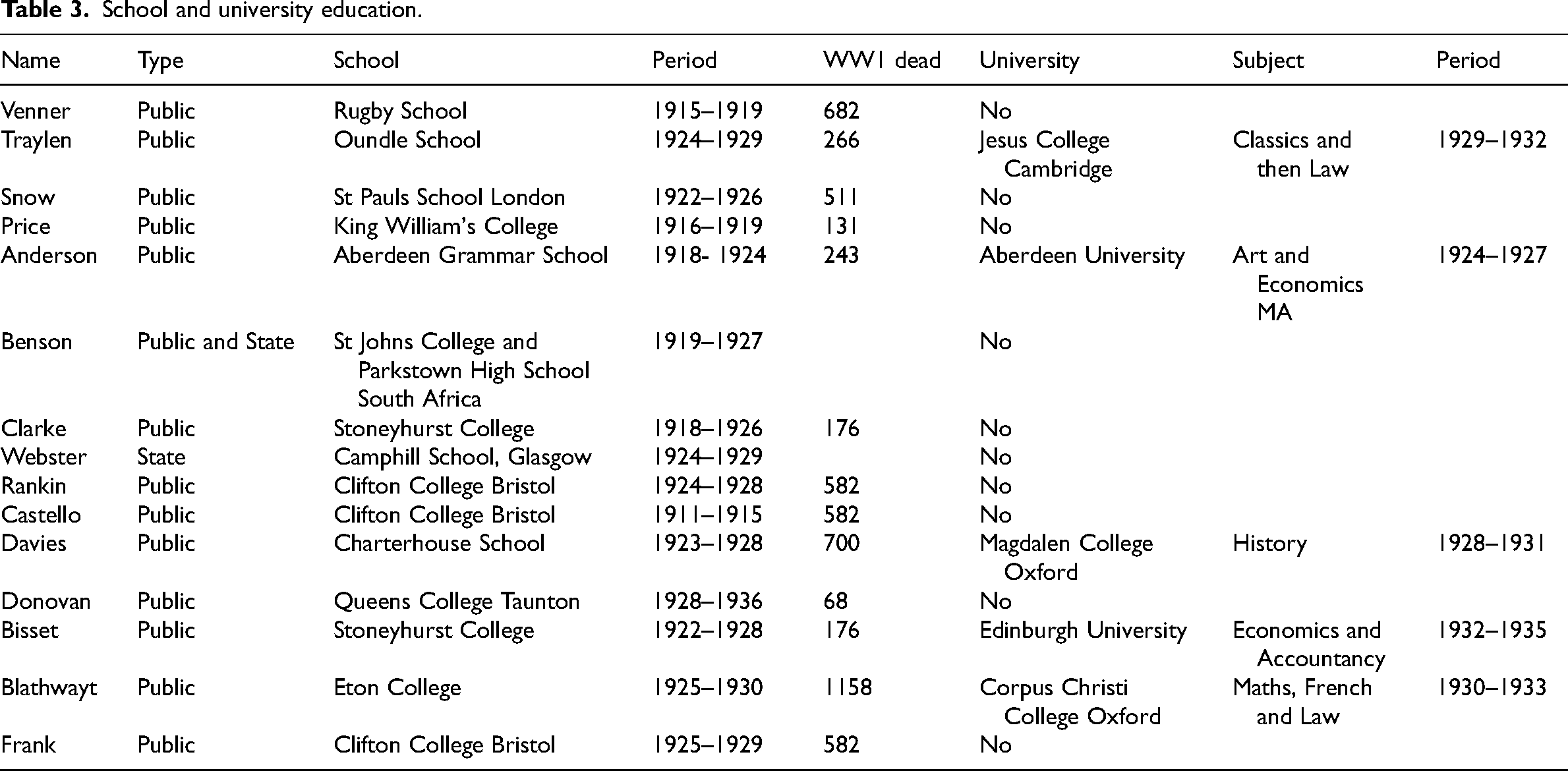

The educational and financial requirements required any articled clerk or apprentice to come from a family of financial standing, who could afford to pay for a private education, the initial premium, ongoing salary support and membership fees. This is reflected in the background characteristics of the SOE CAs, with regard to schools and education (Table 3).

School and university education.

A high proportion, 13 of the 15 CAs, attended fee-paying public schools. Only two of the 15 CAs (Benson and Webster) did not attend a Public School, although Benson began his education at St John's Preparatory College and only transferred to a state school when his parents had cash flow problems (Oxford Directory of National Biography). The one exception is Charles Webster who attended Camphill School in Glasgow, a state school, before commencing his apprenticeship for the Institute of Chartered Accountants of Scotland (1984), writing about the Institute of Chartered Accounts of Scotland, states that The Glasgow Institute adopted a much more meritocratic approach to recruitment, where it was understood no premium fee would be charged, thus making the profession more accessible to families with lower incomes. Webster is the only exception for this group of CAs. He gained social capital through this access to education. The public schools attended by the other 13 CAs include some of the most prestigious in the UK and fees for all of these schools would have been only affordable to the wealthiest families. A public school education was a prerequisite for building the social capital of these chartered accountants.

Ten of the CAs went straight from school into articles or apprenticeships, with five going on to study at elite universities. The university subjects chosen include a number of art/social science-based subjects along with law. One CA (Bisset) studied accountancy at university, although it is unlikely that this was an accounting degree, as accounting as an academic discipline in universities of the UK is relatively recent (Stevenson et al., 2018), mainly emerging after World War 2 (Zeff, 1997). The first Professor of Accounting in Scotland was a part-time position, from 1919 at the University of Edinburgh (Zeff, 1997), where Bisset studied. In an interview with Edgar Traylen's son (Piper et al., 2023), he claimed that the reason his father switched from studying classics at Oxford to Law and then accountancy, was as a result of a conversation with one of his CA uncles who told him that in the uncertain world of the 1930s, he needed a stable career in chartered accountancy.

Chartered accountancy training

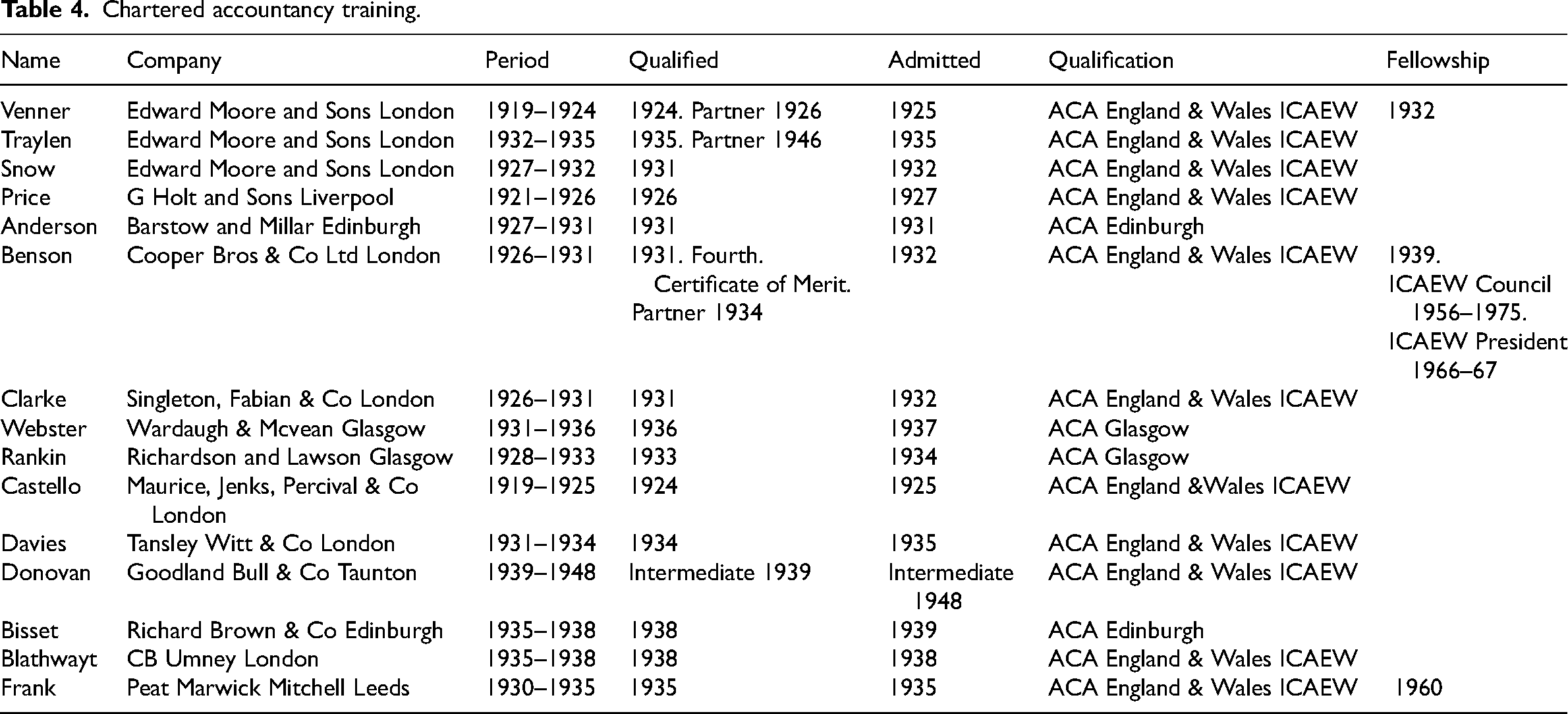

The main feature of the training was the requirement that the accounting clerk (ICAEW) or accounting apprentice (Scotland) was articled to an existing qualified member of the relevant institute for a period of five years, (reduced to 3 years for a university graduate), who acted as a training mentor. For this, the family of the articled clerk/apprentice was usually expected to pay a one-off premium, of up to 450 guineas, depending on the prestige of the firm (Murphy, 1938). Walker (2020) states that the payment of substantial apprenticeship fees in Edinburgh was deemed to provide evidence of vocational commitment, pecuniary independence and gentility, with Anderson et al. (2005) claiming the premium helped ensure the requirements of the right kind of person by denying access to those without necessary financial support. The clerk and mentor entered into an article's agreement which gave both parties obligations and responsibilities. The period of articled clerkship provided trainees with the opportunity to apply their knowledge and develop skills in the areas that the education process was not intended to test (Anderson et al., 2005).

Using the precedent set by the Scottish Institutes, the ICAEW established three levels of exam (preliminary, intermediate and final) in order to ‘secure public confidence in an assured level of competency’ (The Accountant, 1879: 4). The preliminary examination was designed to, ‘test whether the person desirous of entering the profession has received such an education as will render him a fit member of the profession, and is therefore confined to such educational subjects as may be considered the basis of culture’ (The Accountant, 1896: 29). Preliminary subjects included English, arithmetic, algebra, geography, history, a language (in Scotland this was Latin) and a science, (Murphy, 1938). According to Webb and Webb (1917), the scope of the preliminary exam had the effect of excluding 80‒90% of the UK population. In 1930, the time around most of the SOE CAs were in training, the content of final exams included advanced bookkeeping and accountancy (Limited Companies, Partnerships, Executorship and associated law); auditing; taxation, costing and foreign exchanges; Company Law; law relating to bankruptcy and mercantile law (Murphy, 1938). The skills and knowledge developed by vocational training and exams were very useful for SOE and is reflected in the roles that this group of CAs performed there.

The number of Chartered Accountants identified so far as serving in SOE is 52. This is a small fraction of the total SOE workforce estimated to be over 10,000 (Foot, 1984), but chartered accountancy was a reserved occupation. There is some evidence of the scarcity of chartered accountants serving in the armed forces in Clarke's file, where his desire to serve is seen as ‘rare’ and a role in SOE ‘was more useful to his country than his current audit role within British American Tobacco’ (TNA HS9/322/1) (Table 4).

Chartered accountancy training.

Eleven of the CAs trained and qualified with the ICAEW, two with the Institute of Accountants and Actuaries in Glasgow and two with The Society of Accountants in Edinburgh. Eight trained with firms based in London, two each in Glasgow and Edinburgh and one each in Liverpool, Leeds and Taunton. Most trained in practices independently of each other, but three of the CAs (Venner, Traylen and Snow) trained with Edward Moore and Sons in London. The Edward Moore archives (LMA CLC/B/MS29382/001) confirm that Venner became a partner in 1926 and was associated with the training of Traylen and Snow. Family connections and social capital in the recruitment and training process are also evident, as Venner's mother Ethel Mary Moore and Traylen's mother Githa Muriel Moore were both daughters of Edward Moore, the founder of Edward Moore and Sons Chartered Accountants. The importance of family connections is also evident for Henry Benson, whose mother, Florence Mary Cooper, was the daughter of Francis Cooper, a founding Partner with Cooper Brothers in 1871. Henry Benson was articled to Cooper Brothers in 1926 and according to Benson the 500-guinea premium fee was waived (Benson, 1989). School connections also existed; for example, Clarke and Bisset attended Stoneyhurst College and overlapped for 4 years, so there is a possibility they knew each other. The same can be said of Rankin and Frank who were both at Clifton College at the same time. There is clear evidence of social capital existing and being generated for these accountants.

Most non-graduates qualified within a 5-year period, with those attending university qualifying in 3 years. With regard to remuneration during training, the Edward Moore Archives (LMA CLC/B/MS29382/001) show that the only remuneration Venner, Traylen and Snow received whilst training was a Christmas bonus of £10 p.a. Supporting the view that significant family wealth was a prerequisite for a trainee-chartered accountant.

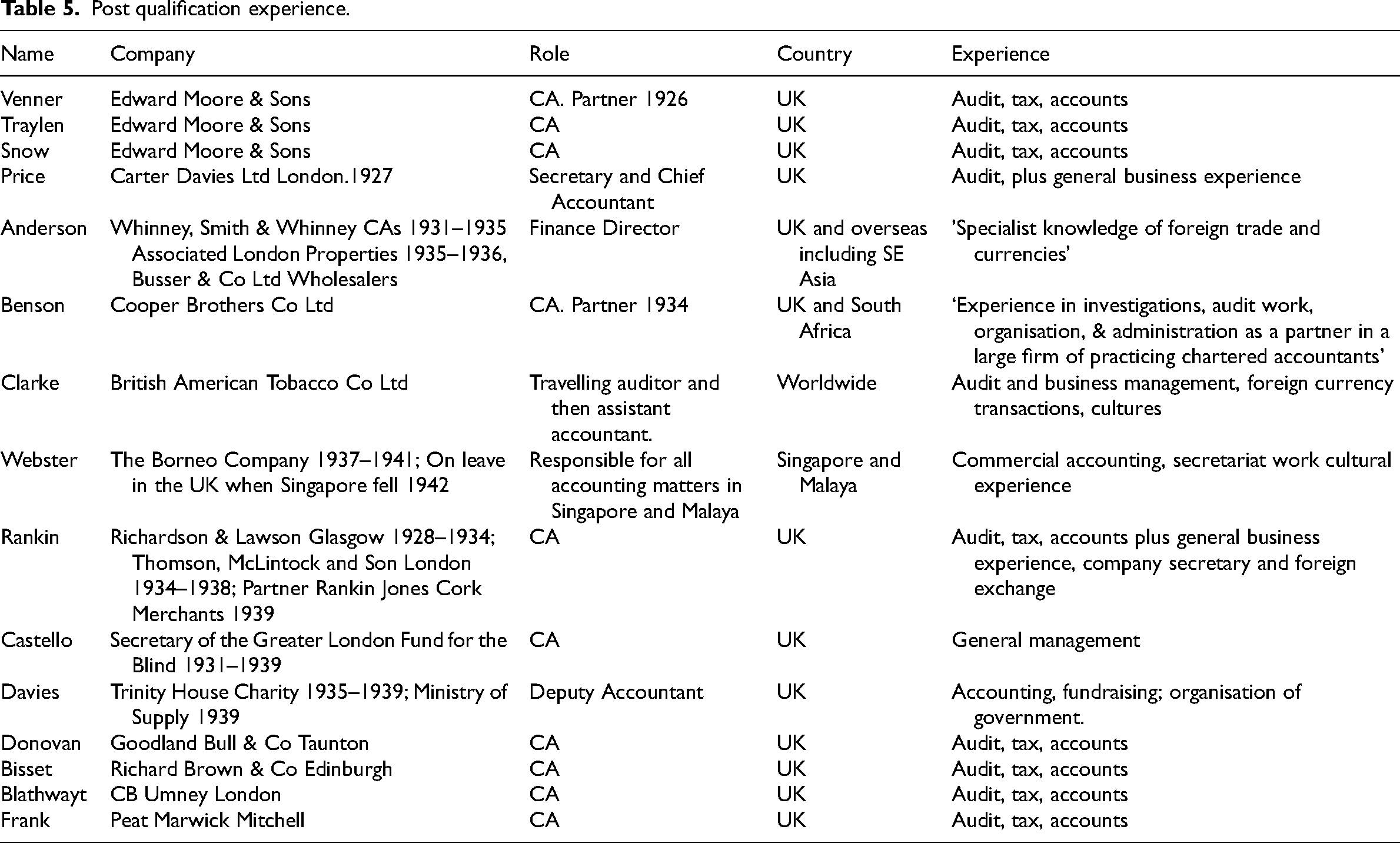

Post-qualification experience to 1939

By the late 1920s, the combination of practical experience and theoretical knowledge had made CAs very attractive to employers recruiting for senior management roles in the industrial and financial world (The Accountant, 1929: 485) (Table 5). This would have made any CA an attractive recruit for the rapidly growing, complex and globalised SOE. By the mid-1930s the trend of CAs taking up senior managerial posts in commerce, finance and industry, using their knowledge of auditing and accountancy, had been detected (Matthews et al., 1997, 1998). The reasons for this were the growing size and complexity of organisations, the creaming off by the accounting sector of some of the brightest middle-class public and grammar schoolboys and the view that chartered accountancy training was perceived as highly effective management training. These roles would have not just been UK-based but would have also included senior management roles abroad. In the 1930s the British Empire was ubiquitous, especially in India and Southeast Asia, with many opportunities for senior executive employment. For those SOE CAs who operated overseas, some previous experience of working in another culture and country may have been required and, as SOE developed its expertise in black market foreign currency transactions, experience of having conducted such transactions legitimately would also have been a benefit.

Post qualification experience.

There is evidence in the SOE files that the accounting knowledge and experience of the chartered accountants were highly valued and useful in the task that they undertook. For example, Rankin was in charge of the Finance section of Force 133, based in Cairo. A report in his SOE file states that he is: well qualified for this role by his professional qualifications and experience as a chartered accountant, as well as his qualities and knowledge. This is a specialist appointment where not only is control of large sums involved in complicated transactions, but guidance has to be given on matters of financial policy. (TNA/HS9/1229/1)

Benson undertook the complete reorganisation of the accounting system in the organisation in New York and South America, and is the hardest working officer I have ever had the good fortune to have serving under me. (TNA HS9/129/6)

The analysis includes the pre-war post qualification working experience of the 15 CAs. Eight of the CAs remained exclusively in public practice in the UK post qualification, although one (Rankin) moved company and location to London. Continuing in practice would have given the CAs the opportunity to further develop their accountancy, audit, financial reporting and taxation skills as well as their business management knowledge and networks. This would have provided them with the accountancy knowledge and experience they needed to be effective within SOE.

Two of the CAs (Anderson and Rankin) stayed in public practice for a short while before moving into broader business roles. Five of the CAs (Price, Clarke, Webster, Castello and Davies) moved immediately after qualification into broader roles, where they would have had the opportunity to develop general management skills, operate in different organisational cultures and gain experience of international trade. Importantly, two of these (Clarke and Webster) worked overseas and so had the opportunity to gain specialist knowledge of working and living in foreign cultures as well as foreign currency transactions.

There is evidence in the SOE files of pre-war experience in overseas trade, which would have required legitimately undertaking foreign currency transactions. For example, Webster was employed by the Borneo Company from 1937 and was ‘responsible for all accounting matters in relation to exports of rubber from Malaya’ (TNA HS9/1567/6), Anderson's SOE application form states, in the section titled Special Knowledge and Experience, ‘Foreign Trade and currencies’ (TNA HS9/32/5) and Clarke was a travelling auditor with British American Tobacco from 1932–1940, visiting India, Burma, Malta, Gibraltar, Denmark, USA, Jamaica, Venezuela and Colombia (TNA HS9/322/1).

This experience would have been invaluable to SOE, especially for those working overseas in SOE's SE Asia Section Force 136, where, according to John Venner, ‘manipulation of Chinese National Dollars on the black market was saving over £650,000 a month or £7.5 million a year for the UK Government’ (TNA HS8/354).

SOE's financial warfare was led and orchestrated by John Venner FCA, SOE's Director of Finance, from 1940 to 1945. Venner used the accounting orthodoxy of financial controls, recording of transactions and regular reporting to build a strong bond of trust and confidence with the Treasury and Bank of England. This provided space for Venner to develop unorthodox financing schemes, including black market foreign currency transactions (Piper et al., 2023). In China, this work was supported by Anderson, who is described in his SOE file as ‘an administrator with a particular flare for higher financial matters’. The social capital gained by these men from their professional qualifications was leveraged by their highly relevant post qualification experience, enhancing their suitability for recruitment into the SOE.

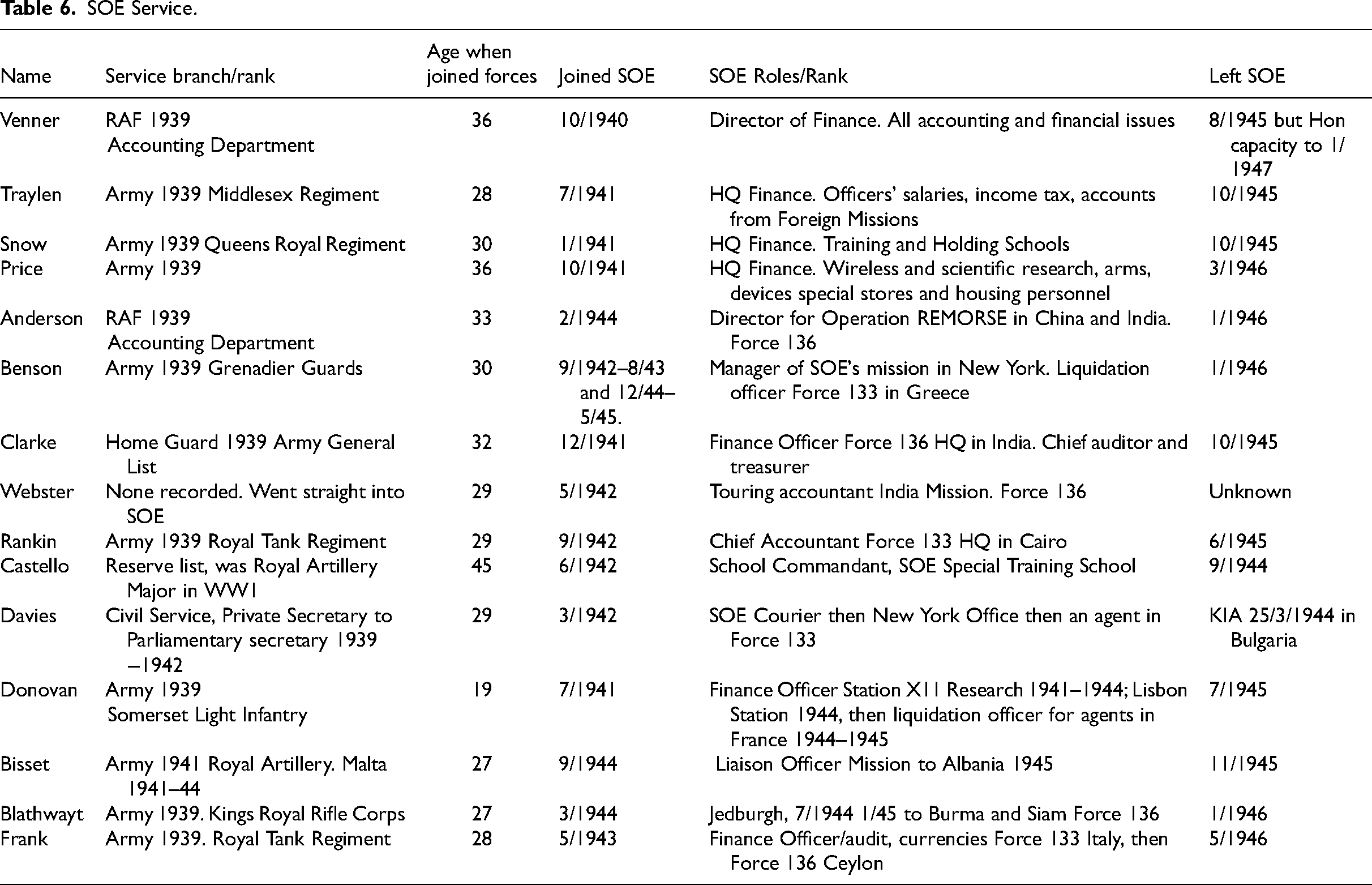

SOE service

It is clear from the standard SOE application form that overseas experience was valued for all SOE operatives (Table 6). Questions on the form requested information on the applicant's language qualifications and knowledge of foreign countries (TNA HS9/32/5).

SOE Service.

The roles undertaken by the 15 CAs fall into three categories. Accounting roles based in the UK, accounting roles based overseas and accountants who were SOE agents in the field. The UK-based accounting roles were located either at SOE HQ in Baker Street London or in one of SOE's training Schools. The HQ-based roles provided financial support for SOE's UK-based operations, involving the preparation of budget estimates, recording of transactions, payments to all personnel and preparation of monthly accounts (TNA HS8/1017). All these activities would have been routine for these well-qualified chartered accountants, most of whom remained in public practice post qualification.

Eight of the CAs operated as accountants overseas. Five of these (Benson, Rankin, Donovan, Bisset and Frank) were initially based in Europe with Force 133 (Mediterranean and Balkans) and their SOE files highlight their main roles involved handling and accounting for large amounts of cash in local currencies to support SOE operations. The three recruited for accounting roles with Force 136 in Asia either had extensive pre-war experience of international trade and foreign currencies (Anderson), experience of working for the global company British American Tobacco (Clarke) or experience of working in Singapore and Malaya with the Borneo Company (Webster).

Two of the CAs (Davies and Blathwayt) were recruited as agents by SOE. Blathwayt volunteered and was trained as a Jedburgh, (the name given to agents who were dropped behind enemy lines during the Normandy campaign of 1944). For his actions on 8 August in leading an ambush against German forces, Blathwayt was awarded the Military Cross for his ‘outstanding qualities of gallantry and leadership’, (HS9/163/5). Mostyn Davies was recruited into SOE from his senior role in the Civil Service. He spent time with Benson in New York, before training as an agent and parachuting into the Balkans in 1944, where he was killed in action in June 1944 and awarded a posthumous Distinguished Service Order (HS9/401/5).

Conclusions

This study responds to the call for more microhistories and prosopographies for analysis in accounting history and answers the calls for social capital-inspired insights and approaches in accounting history microhistories. Using a variety of archival sources, the study focuses on a group of chartered accountants who served in the historically important SOE during the Second World War. These 15 CAs were men, with social capital from their particular social backgrounds and education, enhanced by the social capital generated with their professional qualification. This social capital assisted them to first obtain and then to inform their roles within the SOE. Investigation of their background characteristics showed that these elite men were, mostly, born into wealthy professional families who were able to financially support their sons through a public school education (and, for some, university education as well) and several years of unpaid training. Only one of the CAs attended a state school and he qualified via the Glasgow Institute, which had always adopted a more meritocratic approach to its students, often not charging registration fees and so reducing this barrier to entry.

In addition to a common educational experience, this group of men experienced similar accountancy training and vocational experience, studied the same subjects and went through the same examination experience, thus benefiting from the social capital generated with professional membership (de Villiers et al., 2022). This common ground and consistent approach to accounting would have made them very attractive to SOE as it developed its role in financial warfare (Piper et al., 2023). All of the CAs had significant post qualification experience and three of the CAs also had relevant overseas work experience in Asia, making them ideal recruits for Force 136 and its black-market foreign currency transaction operations in India and China, which were so profitable for SOE and the UK Government.

The article offers a number of contributions to the accounting history literature. First, by introducing these high-ranking individuals who were practising accounting and financial management within the SOE in a time of war and second, by developing ideas of social capital in the field of accounting. This research also adds to the literature on accounting during times of war and develops this by focusing on the accountants and the roles they performed, contrasting with previous accounting histories, which have been related to the application of existing accounting knowledge or the development of new accounting knowledge.

This article demonstrates how the social capital of the 15 SOE accountants was located in their common characteristics of family background, education, professional training and post-qualification experience. These shared characteristics were very important, as they facilitated being recruited into SOE, which extensively used the old boys’ network. Their social capital and common background characteristics would also have been shared by SOE's leadership (Political, Civil Service, Executive and Military) and so would have helped them to fit into the organisational culture and way of operating. It was jobs for the boys, but the fact that they all had the same start may have expedited the work of SOE in challenging times, when social capital and professional practice may have mobilised resources within this organisation.

Footnotes

Data Availability

All datasets used in this paper are available from the public sources cited in the text, apart from the transcripts of the telephone interviews with the descendants of three of the SOE accountants. The interview transcription datasets generated during the current study are available from the corresponding author upon reasonable request.

Ethical considerations

Ethical approval to undertake research interviews with living descendants of SOE accountants was obtained from the University of Portsmouth Research Ethics Committee on July 2, 2020, with approval number BAL/2020/29/PIPER and reaffirmed on 6 February 2023. Respondents were provided with information about the research in advance and gave their verbal consent to participate voluntarily before starting telephone interviews, which were recorded and transcribed. Participants gave their verbal consent for publication of any relevant content from the interviews, as part of the consent process.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

Eton College Archives

London Metropolitan Archive

CLC/B/162/MS29382/001-003 Monthly Salaries Book 1909–1955. Moore's Rowland Predecessors: Edward Moore and Sons archive papers.

The Accountant

The Accountant, 26 April 1879, p. 4.

The Accountant, 11 January 1896, p. 29

The Accountant, 19 October 1929, p. 485

The London Gazette

The London Gazette, 31 January 1919, p. 1662.

The National Archives

TNA HS 8/354: Finance: Acquisition of foreign currency. London, UK: National Archives.

TNA HS 8/1017: Papers leading up to J Hanbury Williams’, Deputy Chief of SOE, report on SOE. London, UK: National Archives.

TNA HS9/32/5: Alexander Donald Stewart Anderson. London, UK: National Archives.

TNA HS9/129/6: Henry Alexander Benson. London, UK: National Archives.

TNA HS9/158/5: William Giles Bisset. London, UK: National Archives.

TNA HS9/163/5: Christopher George Wynter Blathwayt. London, UK: National Archives.

TNA HS9/279/5: Ellis James Castello. London, UK: National Archives.

TNA HS9/322/1: Denzil Robert Noble Clarke. London, UK: National Archives.

TNA HS9/401/5: Mostyn Llewellyn Davies. London, UK: National Archives.

TNA HS9/442/7: Terrence William John Donovan. London, UK: National Archives.

TNA HS9/539/1: George Frank. London, UK: National Archives.

TNA HS9/1211/6: William Francis Price. London, UK: National Archives.

TNA HS9/1229/1: Cecil Dudley Rankin. London, UK: National Archives.

TNAHS9/1387/2: Frank Thomas Snow. London, UK: National Archives.

TNA HS9/1481/5: Henry Edgar Traylen. London, UK: National Archives.

TNA HS 9/1524/7: John Franklyn Venner. London, UK: National Archives.

TNA HS9/1567/6: Charles Christie Webster. London, UK: National Archives.

Oxford Directory of National Biography

Piper interviews -

Interviews in January 2023.