Abstract

Annual reports are crucial for corporate accountability, and for firms to obtain their social licence to operate. Although research has identified the internal company drivers of annual reporting, we know less about the way Australian annual reports developed as a long-term, collective practice. Through a historical, cross-sectional content analysis, this article examines the impact of external institutional pressures on the annual reports of large Australian corporations. Interpreting the results with new institutional theory (NIT), I find that coercive pressure from company regulations and societal expectations, and normative pressures from the accounting profession, have improved standards of corporate accountability. Simultaneously, normative pressures encouraged companies to use annual reports for corporate public relations. This has contributed to annual reports that are homogenous in content but with conflicting audiences and objectives. The analysis highlights the institutionalisation and historical path dependencies of annual reports and contextualises current concerns over disclosure quality and transparency.

Introduction

Annual reports are crucial for corporate accountability and for firms to obtain their social licence to operate (Hall and Jeanneret, 2015). Although other mediums of disclosure – prospectuses, company magazines, websites and sustainability reports – have come and gone, annual reports have endured as the most important way for corporations to manage their relationships with society (Andrew et al., 2012; Chan et al., 2014; Ghauri et al., 2021). As such, annual reports have attracted significant interest, with regulators governing aspects of their content, professional associations recommending styles of disclosure, and employees, media and institutional investors paying close heed to what is said (and, often more importantly, what is left out) (Cortese and Andrew, 2020; de Silva Lokuwaduge and de Silva, 2020; Jackson et al., 2020). However, there are serious concerns about the quality of voluntary disclosures, with community, environmental and diversity disclosures areas of significant public concern but largely unregulated in form or content (Chan et al., 2014; Deegan, 2017; Deegan and Rankin, 1996; Kent and Zunker, 2013; Lim et al., 2017; Yang et al., 2021).

This research contributes to recent efforts to understand annual reporting as a long-term, collective, institutionalised practice. Research on the internal firm drivers of annual reporting (Ali et al., 2017; Chan et al., 2014; Young and Marais, 2012) have been expanded by work that examines the broader socio-cultural and institutional determinants of annual reports such as regulation, activism and the accounting profession (Burdon and Sorour, 2020; Cho et al., 2015; Dagiliene and Nedzinskienė, 2018; de Villiers and Alexander, 2014). In Australia, similarly, most historical research on annual reports has discussed relevant institutional factors without grounding these in annual report source material (Anderson, 1998; McQueen, 2001), or has focused on internal company processes for single case studies (Dyball, 1998; Fahey, 2019; Guthrie and Parker, 1989; Tilling and Tilt, 2010). The literature, as it stands, lacks an understanding of the way Australian annual reports developed as a long-term, collective, institutionalised practice.

Through a historical, cross-sectional content analysis of large company annual reports, this article examines the impact of external institutional pressures on collective annual reporting practices for large Australian corporations. Interpreting the results with new institutional theory (NIT), it argues that coercive pressure from company regulations and societal expectations, and normative ‘best practice’ recommendations from the accounting profession, have aimed to improve standards of corporate accountability. On the other hand, normative pressures from professional and industry associations have encouraged companies to use annual reports for corporate public relations. Although annual reports changed gradually and unevenly due to various internal company pressures, the convergence on a shared reporting practice demonstrates the importance of institutional isomorphisms for company disclosure.

This article will progress as follows. The Literature Review reviews relevant research, the Theoretical Framework outlines the use of NIT to understand collective reporting practices, and the Data and methods section discusses the mixed-methods content analysis of historical annual report data. The Results section examines the empirical material, with the Conclusion arguing that across the twentieth century, annual reporting progressed in three phases. In the first half of the twentieth century, coercive pressure from regulators and a lack of professional or societal pressure encouraged the production of short, austere annual reports. Between 1952 and 1986, competing institutional objectives – namely the intensification of regulatory requirements and accounting standards, alongside normative pressure for the use of annual reports for public relations – split reports into glossy narrative sections and austere financial disclosures. From the 1980s, regulations, societal expectations and best practice recommendations expanded the obligations of companies, and gradually colonised narrative sections with new standards of accountability. Although these have been necessary and welcome developments, encroaching on sections of the report historically dedicated to PR has contributed to competing disclosure motivations.

This article reveals the institutional mechanisms and historical path dependencies of contemporary disclosures and contextualises individual reports within a shared practice. It also makes a theoretical contribution, complicating the majority of NIT research by examining the way that isomorphisms contributed to a homogenisation of annual reports content, alongside divergence in audience and purpose. Finally, this article makes a practical contribution, with the institutionalised conflict in reporting purposes relevant to current concerns over disclosure quality and transparency.

Literature review

Annual reports have been studied by scholars in a variety of disciplines to understand organisational accountability. Annual reports can be vehicles for compliance with regulated financial disclosure (Al-Akra et al., 2010; Game et al., 2018), and environmental, safety and governance standards (Abraham and Shrives, 2014; Choi et al., 2013; Collett and Hrasky, 2005; Cortese and Andrew, 2020; de Silva Lokuwaduge and de Silva, 2020; Frost, 2007; Islam et al., 2021; Jackson et al., 2020). Some have studied voluntary disclosures – alongside correspondence, branding, advertising and mission statements – for meeting public expectations, managing scandals and constructing corporate identities (Breitbarth et al., 2010; Craig and Amernic, 2021; David, 2001; Spear and Roper, 2013; Spence, 2007).

Much of the research on voluntary disclosures has focused on the increase in corporate social responsibility (CSR) reporting in recent decades, with narrative sections used to either placate criticism or respond to the needs of diverse stakeholders (Andrew et al., 2012; Chan et al., 2014; Ghauri et al., 2021). Research has been concerned with the quality of voluntary disclosure (Chan et al., 2014; Deegan and Rankin, 1996; Kent and Zunker, 2013; Lim et al., 2017), with determinants including firm size, profitability, industry and public profile (Ali et al., 2017; Baalouch et al., 2019; Broberg et al., 2010; Campbell et al., 2006; Chan et al., 2014; Choi et al., 2013; da Silva Monteiro and Aibar-Guzmán, 2010; Young and Marais, 2012). Disclosure has also been linked to legitimacy gaps, or the use of narrative sections to manage crises (Andrew et al., 2012; Islam et al., 2022; Lodhia and Mitchell, 2022). Historical research has, similarly, focused on single firms or industries to understand the way companies have constructed culture, responded to stakeholders and managed scandals (Barnes and Higgins, 2020; Currie, 2019; Moreno and Quinn, 2020).

While the analysis of firm-level drivers dominates, some research has examined the broader socio-cultural and structural determinants of voluntary disclosure. Research has found that political differences, business culture, industry mix, regulations and professional standards have influenced annual reports between countries and regions (Adnan et al., 2018; Ashcroft, 2012; Cho et al., 2015; Gerged, 2021; Golob and Bartlett, 2007; Mishra, 2019). Others have highlighted the globalisation of annual reports, with multinationals and international standards contributing to a convergence in narrative sections between countries (Ahern and Clarke, 2013; Ali et al., 2017; Cortese and Andrew, 2020; Tashman et al., 2019; Tschopp and Huefner, 2015). Historical research on the impact of regulations (Morf et al., 2013) and the accounting profession (Cheung et al., 2010; Goldthwaite, 2015; Mishra, 2019) have similarly analysed the relationship between annual reports and their socio-cultural environment.

A sub-set of research on the socio-cultural and structural drivers of annual reporting applies new institutional theory (NIT) as an explanatory lens. Institutions, as Kılıç et al. (2021: 116) argue, can lead to a ‘homogenization of corporate reporting practices’, with convergence or divergence of annual reporting practice, depending on the institutional context. Studies have examined the role of coercive (regulation, public activism, competitive conditions), mimetic (large companies or multinational firms) and normative pressures (industry and professional standards) in governing the reporting practices of companies in particular institutional environments (Burdon and Sorour, 2020; Carpenter and Feroz, 2001; Dagiliene and Nedzinskienė, 2018; de Villiers and Alexander, 2014; Flynn and Walker, 2020; Fogarty and Rogers, 2005; Halkos and Skouloudis, 2016; Khan et al., 2020; Kolk and Perego, 2010; Laine, 2009; Moreno and Quinn, 2020). This includes Australian research, with de Villiers and Alexander (2014) arguing that the convergence of CSR reporting amongst mining companies in Australia and South Africa was primarily shaped by normative isomorphism (de Villiers and Alexander, 2014). NIT research is generally contemporary, with little analysis of the long-term institutional isomorphisms that have influenced annual reports.

The literature, as it stands, lacks an understanding of the way Australian annual reports developed as a long-term, collective, institutionalised practice. Due to challenges with the availability and collection of archival annual report data, longitudinal studies of cohorts of annual reports are rare (de Villiers and Alexander, 2014; Khan et al., 2020; Kılıç et al., 2021). In Australia, contemporary studies have discussed the role of regulation, stock exchange rules, professional standards and activism for Australian annual reports over a short period of time (Bae Choi et al., 2013; Deegan and Blomquist, 2006; Deegan and Gordon, 1996; Deegan and Rankin, 1996; Frost, 2007). Some research has discussed the general historical processes shaping annual reports, though this lacks an empirical base drawn from annual reports (Anderson, 1998; Cheung et al., 2010; McQueen, 2001; Nehme and Wee, 2008). Empirical historical studies have generally focused on single firms to understand the way companies have constructed culture, responded to stakeholders, and managed scandals. Fahey (2019), for example, examined the pragmatic and adaptive communication approach of Australian multinational General Motors; Dyball (1998) the way reports reflected and reproduced consumerist culture in the post-WWII decades; Tilling and Tilt (2010) the establishment of legitimacy for tobacco company Rothmans Ltd; and Guthrie and Parker (1989) the way BHP managed their environmental obligations and relationship with society throughout the twentieth century.

Through a historical, cross-sectional analysis of annual reports for large Australian corporations, this article contributes to the existing literature in three ways. It complements our understanding of Australian accounting history by situating contemporary annual reports in the long-run progress of this organisational form, contextualises the history of individual company reports within a shared annual reporting practice and provides empirical evidence for the institutional mechanisms that have influenced shared disclosure practices.

Theoretical framework

Modern annual reports are part statutory audited financial statements, and part symbolic ‘mediascapes and ideoscapes’ that provoke ‘interpretive and emotional reactions’ from readers (David, 2001: 195). Non-compulsory narrative sections are largely discretionary, with the CEO's statement, a summary of operations, and the community, environmental and diversity reports responding to myriad strategic and symbolic concerns. Stakeholder theory, the most common theoretical explanation, argues that companies make voluntary disclosures to address and build relationships with various stakeholders (Stanton and Stanton, 2002; Tsang et al., 2023). Legitimacy theory, on the other hand, argues that companies make voluntary disclosures primarily to meet public expectations and placate criticism (Deegan, 2019). Impression management argues that reports are used to construct belief systems that affect how readers view the company, the industry, or corporations more generally (Ali et al., 2017; Cho et al., 2015; da Silva Monteiro and Aibar-Guzmán, 2010; Deegan, 2002, 2019; Kumarasinghe and Samkin, 2020; Michelon and Parbonetti, 2012; Preston and Young, 2000; Tashman et al., 2019). Empirical research has found that these and other firm-specific motivations are often intertwined, with each a simplification of the complex strategic, cultural, professional and operational factors that influence each company's outward-facing communication (Andrew et al., 2012; Broberg et al., 2010; da Silva Monteiro and Aibar-Guzmán, 2010; Golob and Bartlett, 2007). While important for understanding the firm-level motivations governing annual reports, these theoretical frameworks have limited application for understanding collective disclosure practices.

This article uses new institutional theory (NIT) as a lens to understand the collective annual reporting practices of large Australian corporations. NIT argues that institutions provide the rules of the game for social thought and action, guiding collective behaviour into established procedures (DiMaggio and Powell, 1983; Meyer and Rowan, 1977; Scott, 1995). Organisations, according to NIT, not only make strategic and market-based decisions, but operate within a relational framework of norms, values and assumptions about acceptable behaviour (DiMaggio and Powell, 1983; Flynn and Walker, 2020; Meyer and Rowan, 1977; Scott, 1995). Regulators and the public can coerce firms to behave in a certain way; professional associations can establish best practice procedures; and competition between firms can lead them to mimic one another or those deemed more powerful (DiMaggio and Powell, 1983). Corporate decisions are thus not entirely internal nor rational but are dependent on the pressures of the external ‘iron cage’. In addition to empirical support for the impact of institutions on annual reports (Burdon and Sorour, 2020; Khan et al., 2020; Kılıç et al., 2021), the choice of theoretical framework responds to the specifics of the case. Although each company was undoubtedly subject to specific strategic, reputational and operational pressures, data on cohorts of annual report data over time prompts a focus on the external institutional environment, rather than firm-specific factors (Khan et al., 2020).

In their analysis of the dynamic evolution of organisations, DiMaggio and Powell (1983) argue that organisations tend to become more similar to one another over time, with isomorphisms creating an environment where ‘individual efforts to deal rationally with uncertainty […] often lead, in the aggregate, to homogeneity in structure, culture and output’ (DiMaggio and Powell, 1983: 144). Coercive isomorphisms arise from pressure placed by powerful or critical stakeholders. Mimetic pressures involve firms seeking to imitate others or model past successful performance. Normative pressure stems from organisations conforming to ‘best practice’ procedures legitimised through professional structures (DiMaggio and Powell, 1983; Scott, 1995). This article focuses on external institutional isomorphisms, or those related to Australia's macro socio-political environment. It disregards mimetic pressure as a firm-level institutional pressure unsuitable for consideration with cohort-level, benchmarked data. Annual reports, in this case, have been governed by coercive pressure from company regulations, and expectations from shareholders, customers, employees and broader society. Normative isomorphisms have resulted from standards set by the accounting and public relations professions, annual report awards criteria and external certification committees.

Institutions are not static but continuously change through the process of institutionalisation. Changes in institutional pillars can influence the overarching system in which companies operate, and the social practices, norms, obligations and activities that take on a ‘rule like status’ (Meyer and Rowan, 1977: 341; Scott, 1995: 13). This includes annual reports, with changes in the external environment – including new regulations, emerging crises and the interests of various activist groups – able to influence the shared disclosure practices of large Australian corporations. Although much of the empirical research has used institutional theory to study the ‘startling homogeneity of organizational forms and practices’(DiMaggio and Powell, 1983: 148), isomorphisms often intermingle to accelerate or contradict one another (Greenwood and Meyer, 2008). Historical research can illuminate the real-world complexity of institutionalisation, with this article complicating the majority of institutional theory research by examining the way that isomorphisms contributed to homogeneity in annual report content, but pushed reports in competing directions with regard to their audience and objective.

Data and methods

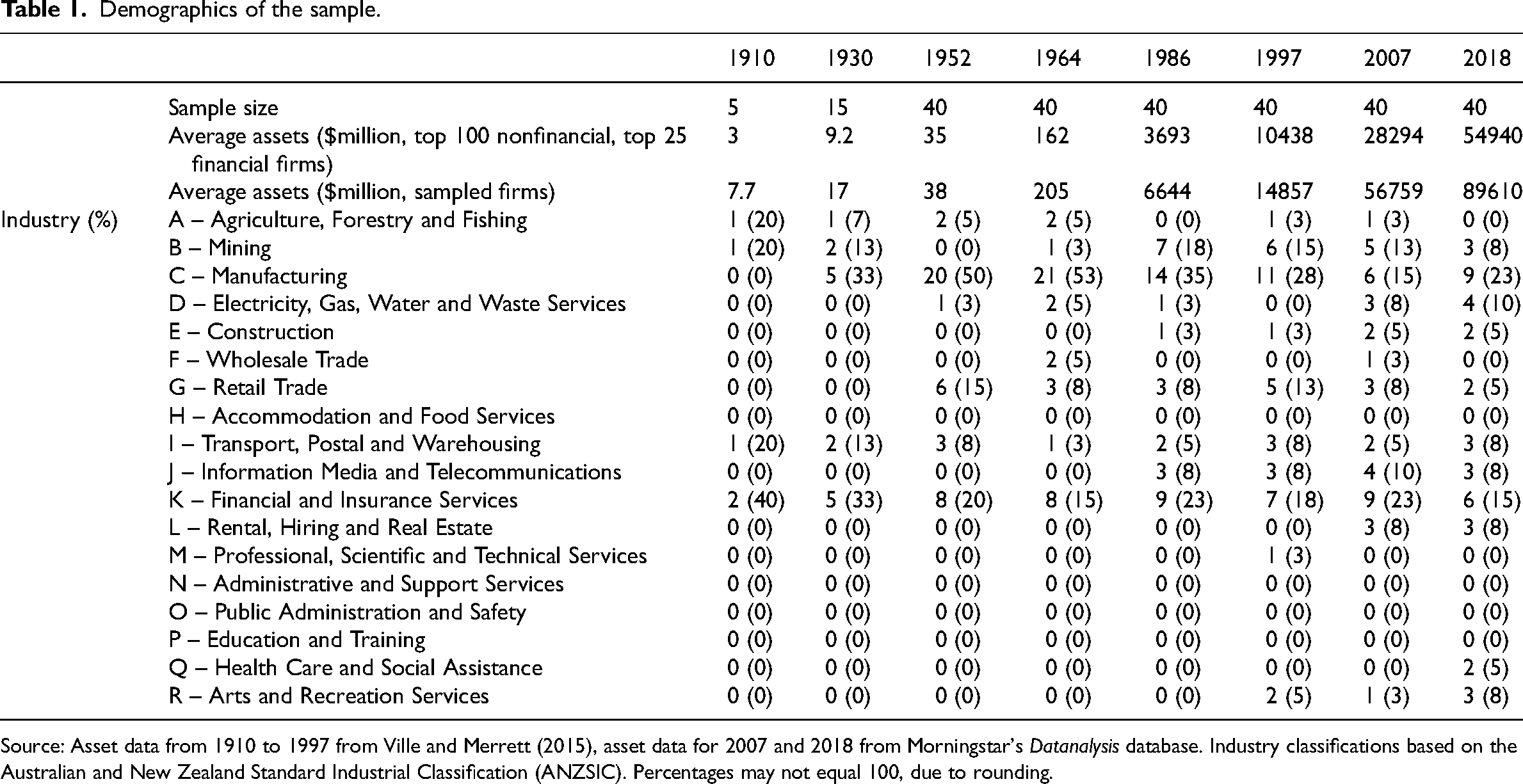

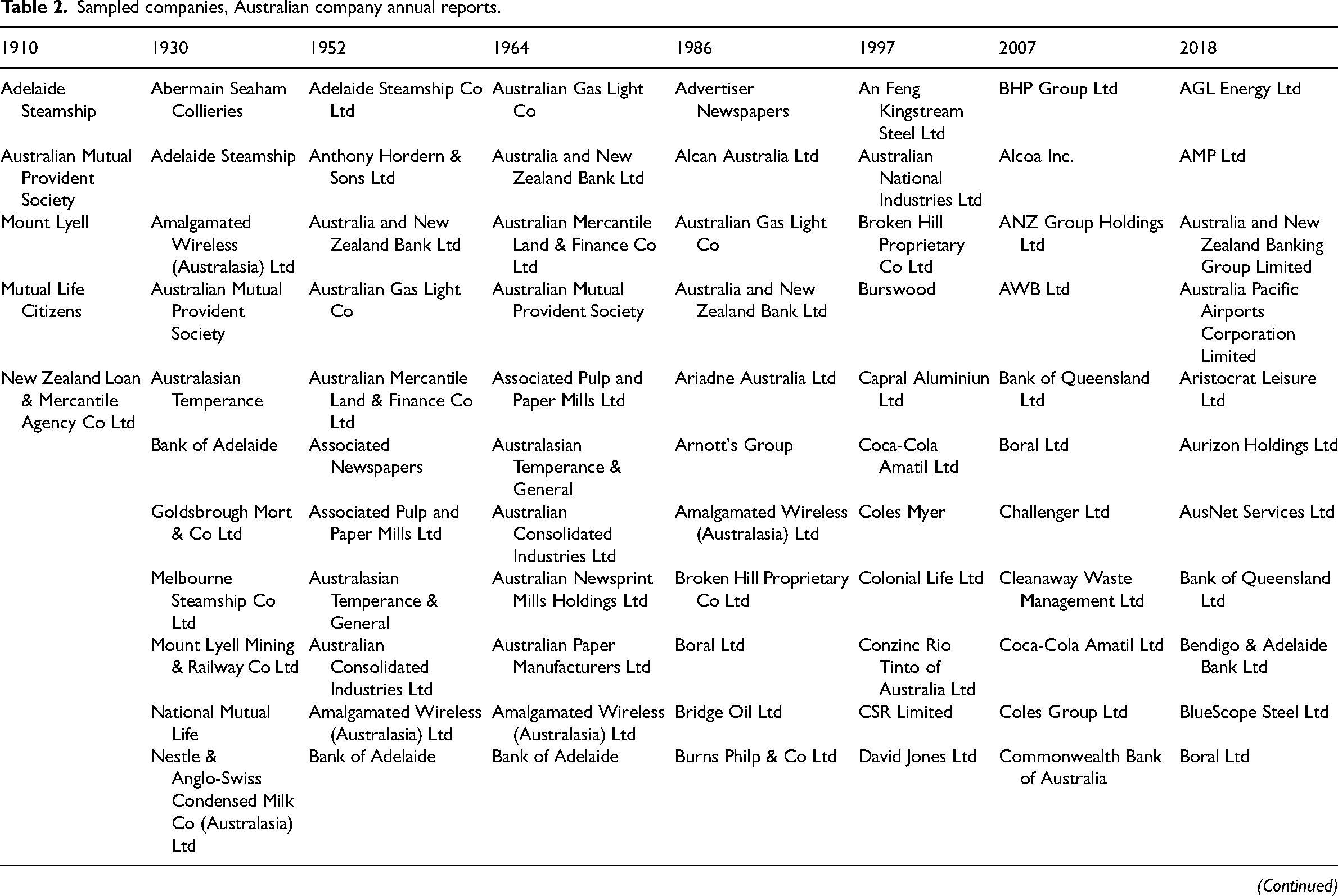

This article uses a mixed-methods approach to understand changes in, and the influence of external institutional pressures on, collective annual reporting practices. Quantitative content analysis was performed on annual reports for a sample of top Australian firms in various benchmark years between 1910 and 2018 (Table 1). The group of firms, from which the sample of annual reports was drawn, includes Australia's top 100 ‘non-financial’ companies, and the top 25 financial firms, ranked based on total assets, at eight benchmarks from 1910 up to the present (1910, 1930, 1952, 1964, 1986, 1997, 2007, 2018). From these lists of 125 top firms, 40 annual reports were selected for each benchmark from 1952 to 2018, with smaller sample sizes for earlier benchmarks due to the availability of records (five in 1910 and 15 in 1930) (Table 2). Each year has a sample comparable to similar work on collective disclosure practice, with the benchmarks contributing a rare longitudinal perspective (de Villiers and Alexander, 2014; Khan et al. 2020; Kılıç et al., 2021). Although sampled companies were not entirely representative of the group of top firms, each sample includes a mix of firms in different industries and of different sizes.

Demographics of the sample.

Source: Asset data from 1910 to 1997 from Ville and Merrett (2015), asset data for 2007 and 2018 from Morningstar's Datanalysis database. Industry classifications based on the Australian and New Zealand Standard Industrial Classification (ANZSIC). Percentages may not equal 100, due to rounding.

Sampled companies, Australian company annual reports.

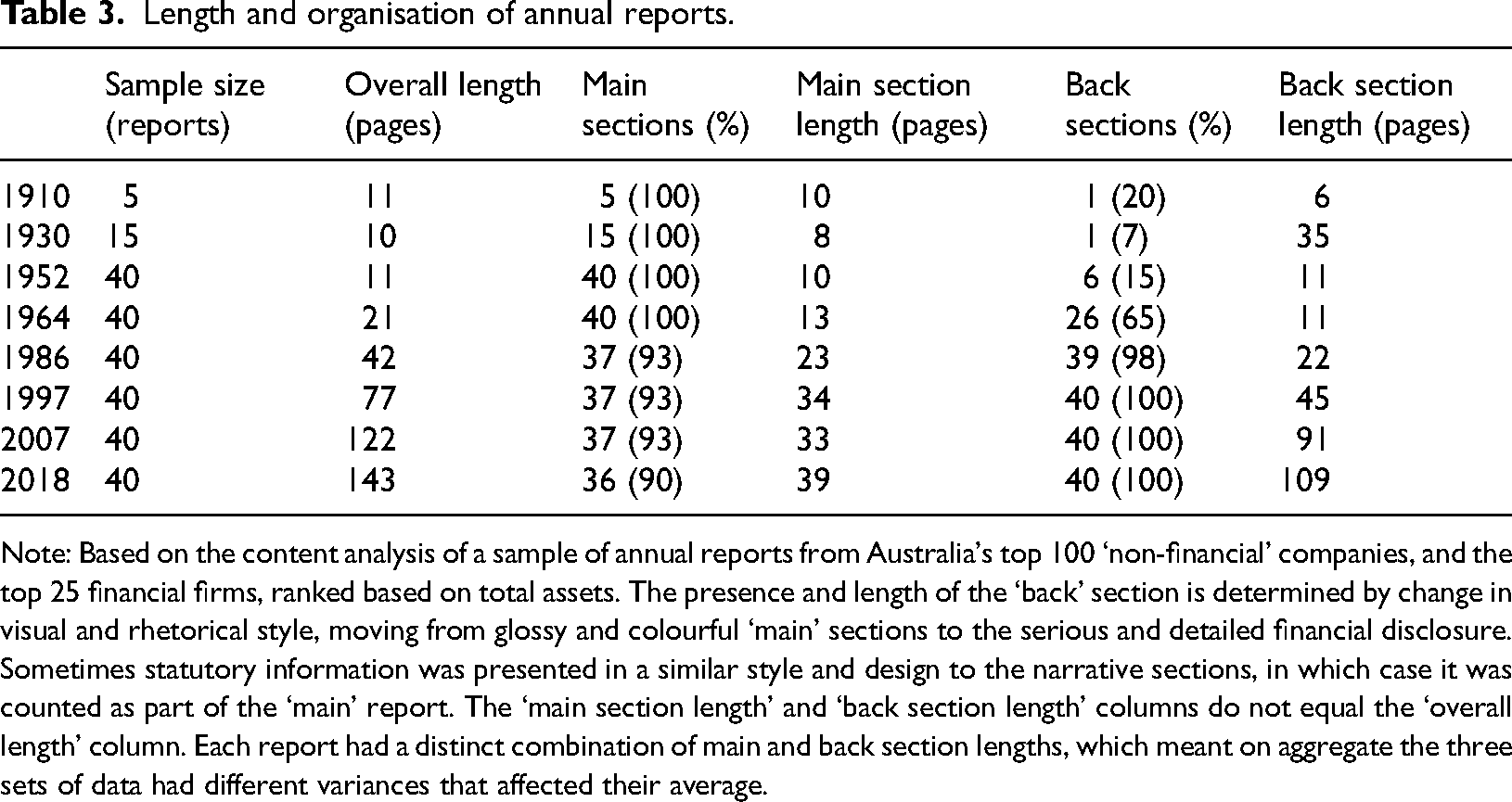

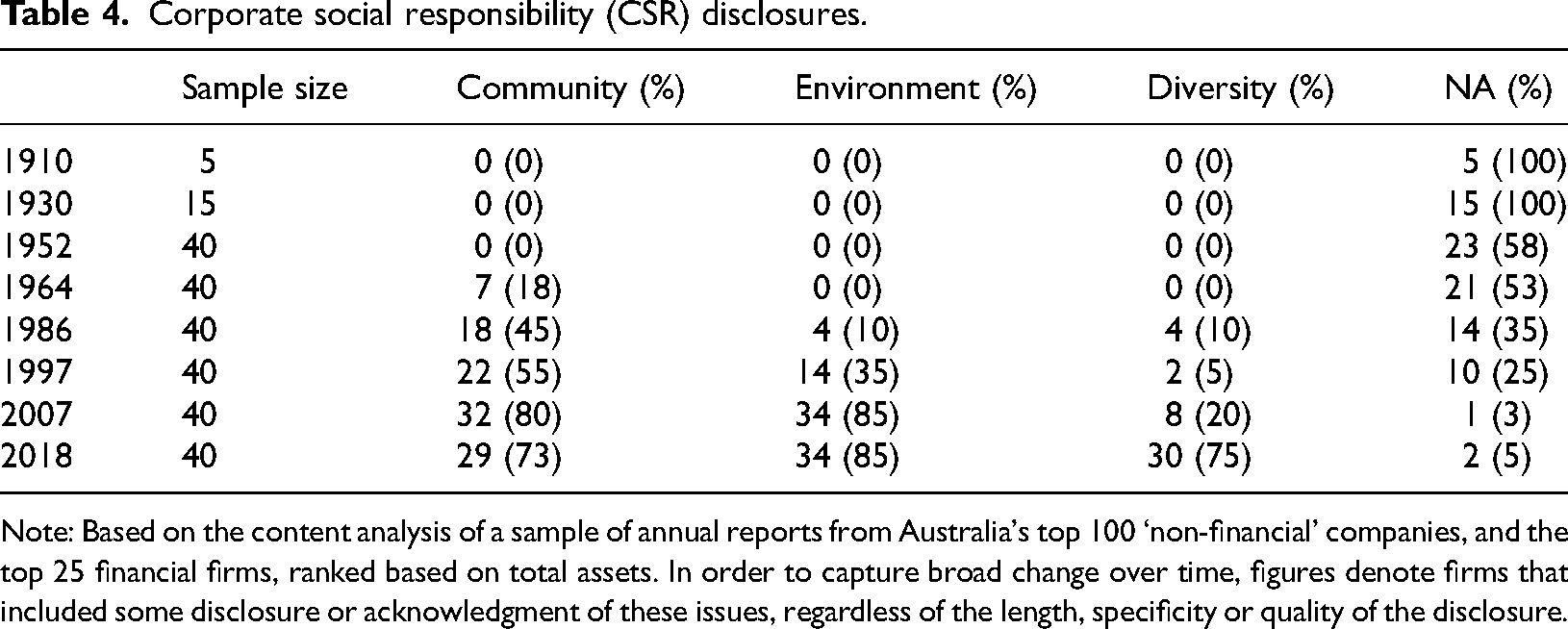

The content analysis identified the overall form and composition of reports, and the issues addressed in non-mandated narrative sections (similar to Dyball, 1998; Moreno and Quinn, 2020; Spear and Roper, 2013). Length and organisation (Table 3) identified the length of the report, and the relative length of the main (narrative sections) and back (regulated disclosures) sections. The main and back sections were not always distinct (see below), but were identified by a change in visual and rhetorical style, moving from glossy and colourful narrative sections to serious and detailed balance sheets and statutory requirements. Corporate social responsibility (CSR) disclosures were identified by identifying any non-financial or non-operational content in the main section of the report (Table 4). In some reports there was zero non-operational content, in others, there were a dozen or more separate issues, programs and initiatives. After reviewing the initial identification of all non-operational content, data were then grouped into three main categories based on the common features of corporate social responsibility reporting: community disclosures involved corporate philanthropy and sponsorship of community programs; environment included environmental performance or management strategies; and diversity included disclosure of initiatives to support workplace equality for marginalised groups (see also Guthrie and Parker, 1989; Morf et al., 2013).

Length and organisation of annual reports.

Note: Based on the content analysis of a sample of annual reports from Australia's top 100 ‘non-financial’ companies, and the top 25 financial firms, ranked based on total assets. The presence and length of the ‘back’ section is determined by change in visual and rhetorical style, moving from glossy and colourful ‘main’ sections to the serious and detailed financial disclosure. Sometimes statutory information was presented in a similar style and design to the narrative sections, in which case it was counted as part of the ‘main’ report. The ‘main section length’ and ‘back section length’ columns do not equal the ‘overall length’ column. Each report had a distinct combination of main and back section lengths, which meant on aggregate the three sets of data had different variances that affected their average.

Corporate social responsibility (CSR) disclosures.

Note: Based on the content analysis of a sample of annual reports from Australia's top 100 ‘non-financial’ companies, and the top 25 financial firms, ranked based on total assets. In order to capture broad change over time, figures denote firms that included some disclosure or acknowledgment of these issues, regardless of the length, specificity or quality of the disclosure.

As DiMaggio and Powell (1983) have argued, institutions encourage organisations to exhibit similar behaviour, even if the reasons for this change are not explicitly acknowledged. Annual reports present a particular challenge for direct observation, as the genre dictates companies appear forward-thinking and proactive, even if they are reacting to their institutional environment (Stanton and Stanton, 2002). As such, most studies that use cohort data and NIT identify the main features of annual reports and contextualise this observed evidence with information on the institutional environment (Dagiliene and Nedzinskienė, 2018; de Villiers and Alexander, 2014; Fogarty and Rogers, 2005; Kılıç et al., 2021; Kolk and Perego, 2014; Laine, 2009; Moreno and Quinn, 2020). Some studies have identified instances where institutional forces are directly acknowledged in company communication, though these are often associated with instances of scandal or non-compliance that suit reactive language (Burdon and Sorour, 2020; Flynn and Walker, 2020). In the context of voluntary disclosures, explicit acknowledgment is often reserved for the most stringent isomorphisms, and likely ‘do not […] represent the sum-total of […] institutional pressures’ (de Villiers and Alexander, 2014; Flynn and Walker, 2020: 300).

This article combines direct and indirect observation, with some explicit acknowledgment of institutional forces complemented by discussion of the range of isomorphisms influencing annual reporting standards of the time. The data have been contextualised with contemporary media and industry commentary that identify salient aspects of the coercive and normative environment. Qualitative data from annual reports are used to demonstrate typical rhetorical devices and have been analysed through the lens of NIT. In practice, text was primarily assessed for why companies included a particular type of disclosure. This focused on identifying institutional pressures, including regulations, external expectations or industry recommendations. In some cases, qualitative data established a direct link between institutional isomorphism and the annual report output. However, in line with previous research, this direct evidence likely understates the true presence of isomorphism, with companies rarely self-reflective in reporting and opting to simply implement changes in content without identifying a reason. The presence of a collective reporting practice, despite a myriad of internal strategic concerns, suggests the importance of institutional pressures for company annual reports (Dagiliene and Nedzinskienė, 2018; de Villiers and Alexander, 2014; Fogarty and Rogers, 2005).

Results

The statutory document

Annual reports in Australia were initially a basic statutory document. Coercive pressure prompted the initial production of annual reports, with the misadventures of the 1880s property boom and 1890s depression encouraging the colony of Victoria to enshrine the production of a brief but accurate balance sheet (Anderson, 1998; McQueen, 2001). The contents of the balance sheet became mandatory in the late-1920s, and over the intervening generation various State Companies Acts mandated increasingly specific parts of the balance sheet and profit and loss statements (Anderson, 1998). Stock Exchange listing rules were an additional coercive mechanism that dictated the content of annual reports in the early twentieth century, with the ‘rudimentary’ stock exchange listing rules requiring a basic balance sheet as a means of protecting investors (Anderson, 1998: 528).

Few other isomorphisms were acting on annual reports at this time. Accounting bodies formed as early as 1885, but were not yet active in establishing normative pressure for company disclosure (Anderson, 1998). Australian public expectations were also limited, with the corporate image primarily projected through the company prospectus rather than annual reports. Companies paid ‘lavish attention’ to the appearance and content of the prospectus, with commissioned paintings and hyperbolic writing from journalists and novelists creating stories about the company's benefit to stakeholders and broader society (McQueen, 2001: 75; see also Mishra, 2019; Morf et al., 2013). Company magazines and advertising similarly employed cutting-edge printing and design technology to connect with shareholders, customers and employees (Fahey, 2019). Thus, the statutory necessity to produce a balance sheet, combined with little pressure for its use in company public relations, meant annual reports in the first half of the twentieth century were uniformly ‘dry and unimaginative’ (McQueen, 2001: 77).

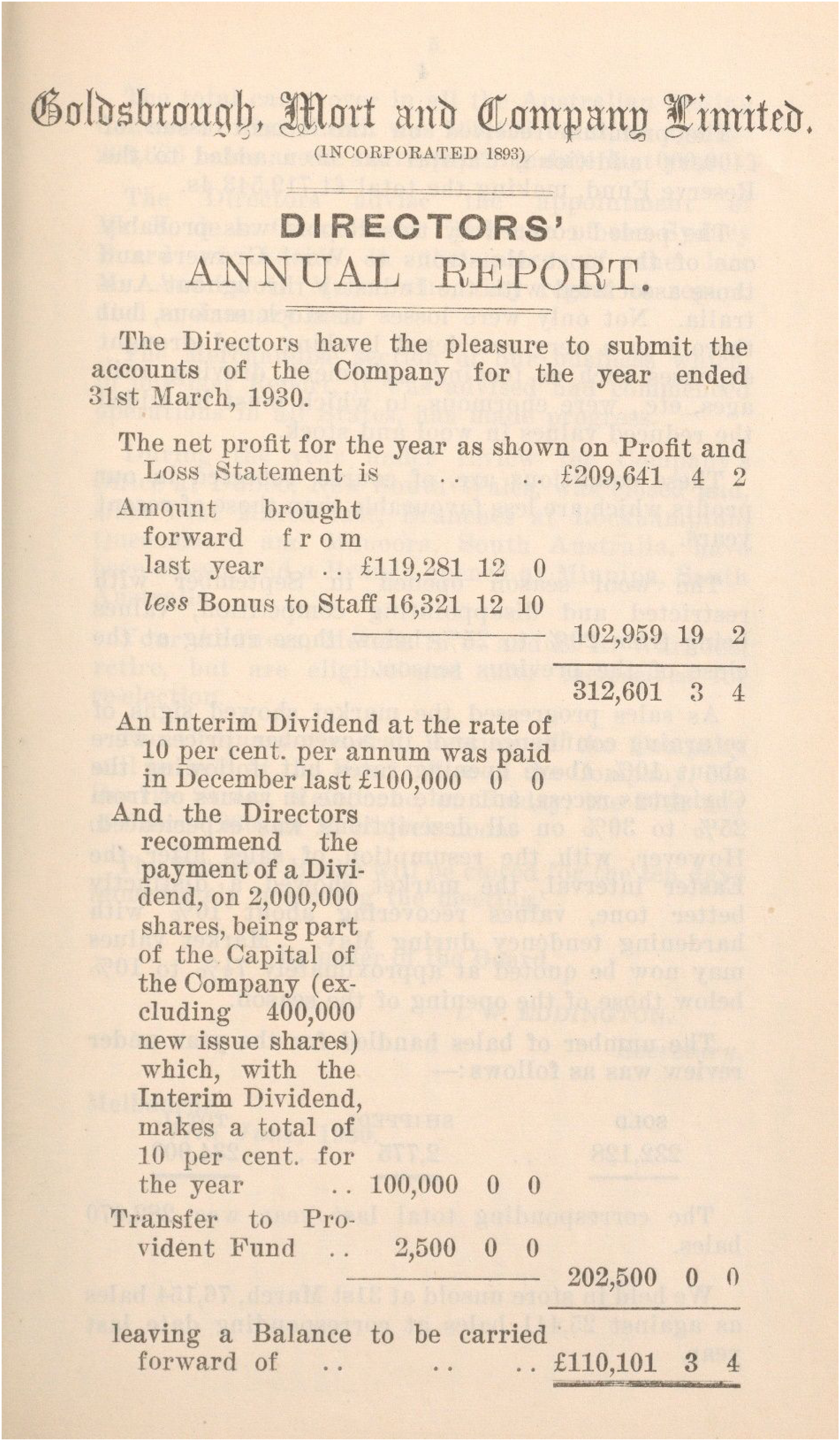

Annual reports in the first half of the twentieth century reflected this institutional environment. As displayed in a typical example in Figure 1, and the data in Table 3, reports in 1910 were printed in black and white on small paper leaflets, with uniform font and layout, a brief balance sheet and cursory reports from directors of around two pages. Reports directly acknowledged external coercive pressures, with mention of the relevant State's Companies Act that guided the preparation of their financial statements. For example, Goldsbrough Mort's (1930: 8) general manager acknowledged the importance of Victorian company law, noting that the ‘accompanying Statement and Balance-sheet [sic] of the Company’ adhered to the provisions of the ‘Act of the Parliament of Victoria’. While not a direct discussion, reports at this time also reflected the lack of normative pressure, acknowledging that the balance sheet exhibited a ‘true and correct view’ of the company’s health, but with little specificity regarding accounting standards. Over the next half-century, the form and content of annual reports had changed little, with an average length of around 10–11 pages between 1910 and 1952, and with most of this taken up by the balance sheet (Table 3).

Goldsbrough Mort and Company Ltd annual report, 1930.

The dichotomy of purpose

From the 1950s to the 1980s, institutional pressures encouraged the transformation of annual reports from a unified (if uninspired) statutory document to, simultaneously, a more stringent accountability instrument and a key method of company public relations communication. Developments in company law and the accounting profession on one hand, and the public relations profession on the other, contributed to a new typical type of annual report, with the division of sections based on the competing objectives of transparent information and glossy storytelling.

Mid-century coercive isomorphisms emphasised standardised financial disclosure. Disclosure requirements had periodically intensified throughout the first half of the twentieth century and the various state-based acts were brought together under the Uniform Companies Act in 1961. The Act standardised the contents of financial statements and the Director's report, increased the extent of financial reporting and required accounts to be accompanied by a statement from the principal accounting officer (Anderson, 1998; Cheung et al., 2010). From 1970, the ‘vagueness’ and ‘inconsistency’ of company accounting standards were addressed, with the various State stock exchanges adjusting their listing rules to require the publication of accounts in accordance with accounting standards of the time (The Canberra Times, 1969: 27). In the 1980s, normative pressures intensified, with the accounting profession granted legislative power to approve standards for company accounts (Anderson, 1998).

Adherence to these institutional isomorphisms was observable in annual reports of the mid-twentieth century. Companies directly acknowledged company regulation, particularly the ‘provisions of the Companies Act, 1961’ in the preparation of their report (see, e.g., AWA 1964: 6). Average length of reports doubled from 11 to 21 pages in the decade between 1952 and 1964, and doubled again in the two decades to 1986 (Table 3). Much of this comprised the increased scale and specificity of financial disclosures, with the space dedicated to the balance sheet and profit and loss statements increasing from 11 to 22 pages between 1952 and 1986 (Table 3). Compliance with normative pressure was observable in the proliferation of notes to the statements of account, with detailed descriptions – comprising multiple pages of text – of the accounting principles used in the preparation of the balance sheet. Companies directly acknowledged these normative pressures, with new notes that the financial statements had been made, for example, ‘in accordance with Australian Accounting Standards and applicable Approved Accounting Standards’ (AGL 1986: 31).

Alongside intensified accounting standards, annual reports were also encouraged to act as public relations documents. Throughout the twentieth century, the prospectus – once the outlet for marketing and imagination – increasingly became the domain of lawyers rather than designers and journalists (Fahey, 2019; McQueen, 2001: 80). Meanwhile, the public relations profession established normative pressure for the production of annual report narrative sections (Crawford and Macnamara, 2014; Fahey, 2019). Professional bodies recommended the use of annual reports for corporate public relations, with the Australian Institute of Management (AIM) introducing their highly influential Annual Report Awards in 1950. AIM acknowledged the need, in the post-war period, for companies to secure goodwill from consumers, employees, and the new middle-class investing public (Anderson, 2005). They recommended companies disclose more information than required by law, and that this disclosure should enhance public trust by communicating good ‘employee-employer relations’, and the ‘important place of private enterprise in the community’ (AIM newsletter 1950: 1, cited in Anderson, 2005). Similarly, the Victorian Institute for Public Affairs argued that they should show ‘how the nation, consumers, suppliers, management, employes [sic] and investors benefit from the enterprise’ (The Advertiser, 1951: 13), and The Herald noted with approval annual reports that created a ‘general understanding of industry and the way it works for all classes’ (The Herald, 1953: 6).

The content analysis reveals that annual reports consistently and collectively transformed into public relations documents in the mid-twentieth century. Reports were divided into discernible main (narrative) and back (mandated disclosure) sections from the 1950s, with 15 per cent of the sample containing discernible narrative sections – presenting a summary of company activities in a visually and physically distinct section – in 1952; 65 per cent a decade later in 1964; and 98 per cent of the sample in 1986 (Table 3). Figure 2 presents a typical mid-century annual report, demonstrating companies’ experimentation with the display of financial information in a visually-appealing manner. New narrative sections reflected industry recommendations by exploring the company's value to Australian society through employment and ownership, and for those who purchased products. For example, in 1952, General Motors-Holden extended their balance sheet and operational description of earlier eras, arguing that their plant expansion program would have a ‘tremendous and beneficial impact […] on Australian industry’ (GHM, 1952: 5). In 1964, Commonwealth Industrial Gases included a section on ‘Serving Australia’, arguing that as the ‘major supplier of gases and equipment for use in industry and medicine, […] CIG has a growing and vital stake in Australia’ (Commonwealth Industrial Gases, 1964: 19). In their section titled ‘some of our people who serve you’, AMP mentioned the ‘scope of the Society's various services to its members and to the communities in which AMP operates’ (AMP, 1964: 11). AGL argued that their natural gas product was the ‘silent servant’ behind the scenes of important community initiatives (AGL, 1964: 8). The Commercial Bank of Australia (1964: 13) invoked a wide range of beneficiaries – including ‘the man on the land, the industrialist, the exporter and importer, those engaged in commercial enterprises, the investor, the housewife, the student, the employee, the traveller, the migrant, the overseas visitor’ – and implied that their provision of banking services was a community service rather than a profit-maximising activity.

Felt and Textiles annual report, 1964.

Narrative sections were also used to connect with employees. Disclosures of staff wellbeing first appeared in this sample in the 1950s (Table 4), with David Jones, for example, changing their dismissive attitude towards staff seeking basic wage increases (David Jones, 1952: 2), to recording their ‘appreciation to all members of the staff for their efforts’ (David Jones, 1965: 6). General Motors-Holden was the first in the sample to outline strategies to achieve ‘high morale’ such as safety improvements, loyalty incentives, training and development (Fahey, 2019; GMH, 1952: 7–8). By 1964, 25 per cent of sampled companies disclosed employee wellbeing initiatives with, for example, Myer outlining training and welfare improvements and acknowledging that the ‘success of our business is a tribute to the loyalty, efficiency and energy of the 20,000 or so men and women who make up the Myer team’ (Myer, 1964: 9). By 1986, disclosure of employee wellbeing activities increased to almost half of all reports, with this the most prevalent non-operational narrative section at the time (Table 4).

In some cases, companies directly acknowledged the new public relations objective of annual reports. For example, Foy and Gibson (1953: 3) acknowledged their aim of using the report to establish a narrative about the company, that ‘the [staff] benefits briefly described on these pages […] go far to explain why you so often hear it said, “Foy's is a good place to work”’. In a similar way, Dunlop (1962: 2) noted that they aimed to use the report to connect with stakeholders, arguing that ‘we hope to show, in this report, the extent to which service dominated what we do’. However, for the most part, new narrative sections were introduced with little fanfare. Discussions of community benefit appeared spontaneously between the 1950s and the 1980s, with companies simply including the new sections rather than discussing the reasons they did so. Although there is a lack of direct evidence, the observed convergence on a similar report form indicates the presence of a collective, institutionalised practice (Dagiliene and Nedzinskienė, 2018; de Villiers and Alexander, 2014; Fogarty and Rogers, 2005). Demonstratively, by the 1980s mainstream media outlets reported on the now-entrenched standards of annual reporting, arguing that they reflected ‘high public relations philosophy, with lashings of marketing hype for the company's directions and quality of work, its relationships with its employees and its role in the community’ (Adamson, 1987: 68).

Expanding accountability

The transformation of annual reports into corporate public relations documents was the foundation for CSR reporting as it emerged in the late twentieth and early twenty-first centuries. Although some form of corporate social reporting had been present in Australian companies since the late-nineteenth century (Guthrie and Parker, 1989; Morf et al., 2013), from the 1980s companies’ earlier acknowledgment of customers, employees and Australian society expanded in scope and specificity. Industry recommendations quickly made the link between public relations and CSR reporting, with the AIM annual report awards recommending disclosure on ‘how the company was socially responsible’, including ‘environment, employment policies, and community involvement’ (AIM, 1981: 13–14, cited in Anderson, 2005). At the same time, shareholder activism, industry recommendations and government regulations established a range of institutional pressures for companies to engage with, and report on, socially responsible initiatives as a form of corporate accountability. Although this was remarkably successful at encouraging the disclosure of CSR activities – from around half of the reports in 1964, to 95 per cent of the sample in 2018 (Table 4) – encroaching on narrative sections forced corporate accountability to sit alongside (and sometimes in conflict with) the use of narrative sections for corporate public relations.

Community

Over time, disclosure of societal benefits expanded to outward-looking corporate philanthropy activities. In the 1970s and 1980s, normative best practice principles from the AIM annual report awards encouraged companies to disclose community involvement activities (Anderson, 2005). Coercive pressure in the form of societal expectations to be ‘good corporate citizens’ also increased, with public outcry at the greed, corruption and ostentatious wealth of the corporate raiders pressuring corporations to ‘demonstrate the human face of market capitalism’ by giving back to society (AFR, 1988: 16; Bongiorno, 2015; Sykes, 1994; Wright, 2022). In the 1990s, commentary acknowledged that neoliberalism and the withdrawal of Western governments from their social obligations placed external pressure on corporations to improve the ‘social balances of the countries in which they operate’ (Lagan, 1997: 15; see also Nehme and Wee, 2008). The Howard Australian Federal government also established coercive pressure and extended the tax incentives for charitable giving with the explicit aim of encouraging corporations to fill gaps in the newly stripped-back welfare sector (Eastway, 1999: 84).

Industry insiders were quick to transform these calls for external accountability into an opportunity for corporate public relations. Australian business media established normative pressure, recording the success of companies who disclosed efforts to secure their social license to operate. Corporate philanthropy, it was argued, would not only benefit society but the donor as well, through an ‘improved external image’ (Lagan, 1997: 15). Lines were blurred between philanthropy and commercially-minded corporate sponsorships, with Tilston (1998: 1) consistently reporting that ‘almost all companies mentioned enhancement of their image within the community as one reason for spending shareholders’ money on worthy causes’. Companies were encouraged to ensure a ‘values match between themselves and their consumers’ (Lagan, 1997: 15), with Lend Lease chairman Stuart Hornery arguing that philanthropy earned back their money spent ‘any number of times over’ by helping the company to ‘build a strong reputation’ (Eastway, 1999: 84). In 2000, the Sydney Morning Herald reported that ‘being socially responsible in the long term is likely to pay off. It's good for reputation, employee morale and community relations’ (Horin, 2000: 43). Although external isomorphisms all encouraged community disclosures, they did so with competing institutional objectives – the industry focus on promoting corporate reputation conflicted with government and societal pressures to ensure corporate accountability.

Multifaceted pressure towards corporate citizenship increased annual report community disclosures. Disclosure of community activities increased from a single report in 1964 to 45 per cent of the sample in the 1980s and to 80 per cent of the sample by 2007 (Table 4). Community sections were often introduced with little discussion, with companies portraying the community as an important stakeholder and themselves as good corporate citizens, through sustained, ongoing contributions to society. Advertiser Newspapers (1986: 19), for example, acknowledged the importance of their ongoing charitable contributions and commented that ‘the group continues to be an integral part of the community it serves by its support of charitable, artistic and sporting bodies’. Woodside (1997: 51) similarly reported on their work to ‘maintain their programme of support for a variety of community and charitable organisations’, and Coles Myer (1997: 26) acknowledged their ‘long history of supporting the communities in which it operates’.

In some cases, companies acknowledged the role of external societal pressures in driving community reporting. For example, BHP (2007: 116) argued that ‘companies are […] facing heightened public scrutiny; and increasingly, our social and moral obligations are being shaped by stakeholders’ expectations’. Similarly, in 2018, Wesfarmers Chairman Michael Chaney argued that their ‘commitment to take care of […] the communities in which we operate’ was driven by external expectations to engage in ‘good behaviour’ (Wesfarmers, 2018: 9). Companies also acknowledged industry recommendations, by making it clear that their reports were driven by corporate reputation and the wish to appear to be contributing to society. Companies made little distinction between marketing opportunities and genuine concern for the community, with Santos, for example, arguing that they became involved in charity or sponsorship only when it was clear that it could be used in ‘symbolic form’ to ‘remind the community of the contribution Santos is making’ (Santos, 1986: 29). Similarly, Pioneer International argued that reporting on their commitment to various charitable organisations yielded a ‘return’ through ‘improvements in community relations and closer relations with government and customers’ (Pioneer International, 1997: 13). Community disclosures were thus institutionalised to meet both corporate citizenship expectations, as well as public relations ‘best practice’ guidelines.

Environment

The environmental movement was the first to actively politicise consumers (Lagan, 1997: 15). From the 1970s, firms in so-called ‘dirty’ industries were targets of criticism by environmental groups, with activists addressing specific incidents of pollution or biodiversity loss (Deegan and Gordon, 1996; Guthrie and Parker, 1989; Nehme and Wee, 2008; Tilt, 1997). Throughout the 1990s, both coercive and normative pressures for environmental reporting expanded. The focus shifted from specific incidents to a holistic approach of ‘sustainable development’, with issues such as global warming increasing scrutiny of the ‘environmental liability and reporting’ of Australian companies (Jay, 1997: 38; see also Taberner, 1996). In late 1994 the Federal Government introduced the Greenhouse Challenge; a series of one-on-one, voluntary, co-operative emissions reduction targets (Callick, 1995; Griffin, 1997; Martin, 1996). This program was holistic in scope, but primarily targeted companies in the high-risk mining and manufacturing industries (Griffin, 1997; Martin, 1996).

Normative pressure followed, with groups such as the Mineral Council of Australia initiating an environmental code of conduct in 1996; and the training of accounting professionals expanding to include environmental reporting (Deegan, 1999: 44). There was a ‘proliferation of frameworks and guidelines’ (Taberner, 1996: 21), including by the NSW State government, the International Chamber of Commerce, and the UN Environment Program (UNEP), and in 1997, the Australian Annual Report Awards made its first award for an environmental report (Jay, 1997; Taberner, 1996). Meanwhile, external pressures for corporate accountability were transformed into an opportunity for positive public relations. Environmental disclosures were recommended as a ‘central competitive and strategic issue for business’ (Taberner, 1996: 21), and a ‘valuable public relations tool for many of our largest corporates’ (Johnson, 1999: 2). There was a contemporary acknowledgment of the competing institutional objectives of environmental reports, with disclosures seen as poor quality and rarely discussing anything other than ‘self laudatory’ material (Lawson, 1996: 9; Deegan and Rankin, 1996).

In the 2000s, intensifying lobbying by environmental groups prompted additional coercive pressure in the form of regulation, with the Australian government enacting Section 299(1)(f) of the Corporations Law in 1998, requiring companies subject to any ‘particular and significant’ environmental regulation to report on their performance (Frost, 2007; regulations were enacted at a similar time elsewhere, see Ashcroft, 2012; Choi et al., 2013; Tilt, 1997). Between 2006 and 2014, the Federal government required 450 high-energy companies to report on efficiency improvements through the Energy Efficiency Opportunities Act (2006). The Australian Stock Exchange (ASX) Corporate Governance Principles and Recommendations (2014: 30) extended the formal legislative requirements, recommending companies report on their ‘environmental and social sustainability risks’ from 2014. Mainstream public concern intensified alongside the United Nations Paris Climate Accords in 2015, with governments around the world, including Australia, signing a treaty designed to limit climate change. Australia implemented a range of regulations and incentives to reduce emissions by 28 per cent before 2030 (DCCEEW, 2023). Reflecting public concern about environmental issues, particularly climate change, shareholder activism become increasingly common (see, e.g., Slezak, 2017). In September 2018, the Australian Institute of Company Directors (AICD) reported that ‘mainstream investors and corporate regulators are beginning to demand a step up in climate risk fluency from directors, and more meaningful disclosures in annual reports’ (AICD, 2018).

Normative pressures, in the form of reporting standards, also proliferated in the twenty-first century. International standards such as the Global Reporting Initiative (est. 1997), the Carbon Disclosure Project (est. 2002), the United Nations Principles of Responsible Investing (est. 2005), the Climate Disclosure Standards Board (est. 2007), and the UN Sustainable Development Goals (est. 2015) provided comprehensive, verifiable guidelines for environmental disclosure. Local professional groups, including the AICD, the Australian Accounting Standards Board (AASB), the Australian Council of Superannuation Investors (ACSI), the Governance Institute of Australia, and Financial Services Council (FSC) trained directors in their duties regarding environmental expectations (McElrea, 2021; Tilt, 1997). Although the proliferation of coercive and normative pressures has been criticised for being ‘complex and overwhelming’, their scope and intensity have ensured most companies are expected to report on their environmental performance (The Reporting Exchange, 2018: 1).

Changes in institutional pressures were reflected in environmental disclosures from the 1980s onwards. In 1986, environmental reporting was limited in scope, and reflected the industry- and incident-specific environmental activism of the late-twentieth century. Disclosures were generally defensive, with narrative sections used to address past incidents rather than proactive environmental management. For example, in 1986 the Chairman of Energy Resources Australia responded to public concern regarding their pollution of waterways near Kakadu National Park, arguing that the ‘discharge of water from No. 4 retention pond […] contained no hazardous chemicals and the radioactive content was at levels similar to those in the natural waters of the region’ (Conkey, 1985; ERA, 1986: 4). Similarly, in 1988 Comalco responded to a ‘major incident’ at their Boyne Island smelter that damaged their emission control precipitator and led to the release of partially treated gases (Comalco, 1988: 36). Woodside Petroleum, similarly, outlined a number of programs designed to remedy the company's environmental impact, including external assessment of air, soil and water toxins, and a ‘botanical monitoring programme’ to regenerate native plants (Woodside, 1985: 14).

In the decade to 1997, environmental reporting expanded from 10–35 per cent of the sample. Reflecting the industry-specific expectations of the time, 79 per cent of environmental reports were from companies in high-risk industries such as mining and manufacturing, far exceeding the presence of these industries in the overall sample (sectors B and C comprised 43 per cent of sampled reports, see Table 1). Reports were focused on specific incidents as well as new holistic sustainability principles, with James Hardie (1997: 30–1) noting that ‘no major environmental incidents occurred in the past year’, while also developing new systems to meet ‘ecologically sustainable development criteria’. Companies acknowledged external coercive pressures, with Santos noting that, in carrying out their operations, ‘the community rightly expects that the company will behave properly’ (Santos, 1997: 5, 22). Pioneer International (1997: 11) similarly noted that they attempt to ‘stay ahead of reasonable community expectations’, as well as honour their agreement with the ‘Federal Government for voluntary reduction of its greenhouse gas emissions’. BHP noted that their environmental strategy was shaped by both normative and coercive pressures, namely ‘tougher standards of environmental performance’ and the ‘changing expectations of society’ respectively (1997: 6). Although companies stated that they were primarily driven by environmental accountability, at times they admitted the public relations functions of their environmental reports (Pheasant, 1998: 20; Rio Tinto, 1997: 7).

Increased stringency of coercive and normative pressures in the 2000s and 2010s was associated with an increase in the prevalence of environmental disclosures. Reports expanded to 85 per cent of the sample in 2007 and 2018, and firms across all industry groups were equally as likely to disclose their environmental performance (Table 4). Twenty-first-century environmental reporting reflected coercive pressures by commenting on the ‘particular and significant’ environmental laws governing their operations. ‘Compliance with environmental regulations’ was seen as the minimum standard (Fortescue, 2018: 47; Wesfarmers, 2007: 40), with Qantas (2018: 49) acknowledging their ‘environmental obligations’ were shaped by ‘a range of Commonwealth, State, Territory and international environmental legislation’. Companies also acknowledged coercive pressures in the form of Federal government initiatives, including, in 2007, the Energy Efficiency Opportunities (EEO) program (see, e.g., Coles, 2007: 14; Commonwealth Bank, 2007:48; Newcrest, 2007: 40; Wesfarmers, 2007: 40) and, in 2018, emissions targets under the Paris Climate Change agreement (Bank of Queensland, 2018: 21; BlueScope, 2018: 6; Fortescue, 2018: 54). Companies deliberately adhered to normative pressures by acknowledging, for example, the international Carbon Disclosure Project (Crown Resorts, 2018: 21; Wesfarmers, 2007: 40), Global Reporting Initiative (Fortescue, 2018: 48; LendLease, 2007: 41) and UN Sustainable Development Goals (Boral, 2018: 20; Goodman, 2018: 73) that guided their sustainability reports.

Companies, in some instances, acknowledged the public expectations guiding their environmental disclosures. Wesfarmers (2007: 40) argued that their ‘greenhouse risks and opportunities assessment’ procedures were driven by ‘increased public and political focus […] on climate change’. Coles (2007: 14) argued that their ‘environmental considerations’ were guided by the ‘growing concern’ of customers, employees and shareholders with climate change. BHP (2007: 115), similarly, opened their environmental report by acknowledging the ‘critical environmental concerns’ of ‘scientists, governments, our local communities and employees’. In 2018, Boral argued that their sustainability report was crucial for ‘meeting the expectations of our stakeholders’ (Boral, 2018: 20) and Fortescue (2018: 54) acknowledged their reporting was guided by ‘the growing stakeholder interest in business action on climate change’. In these instances, companies acknowledged that it was not simply the act of environmental management that was necessary but the perception of it in the form of disclosure. Environmental disclosures thus offered companies a way to comply with regulations and expectations as well as conform to professional norms by using reports to serve their corporate reputation.

Diversity

Diversity disclosures were an extension of the mid-century focus on staff retention and wellbeing. In the 1970s, activism from the second-wave feminist Women's Movement established coercive pressure to address gender diversity in the workplace (Du Plessis et al., 2014; Taksa and Groutsis, 2017). Legislative policy changes followed in the 1980s, with the Commonwealth Sex Discrimination Act (1984) preventing unequal pay; and the Affirmative Action (Equal Employment Opportunity for Women) Act (1986) intending to dismantle barriers that limited women's opportunities in the workplace. The latter covered a range of public and private sector institutions, and employers were required to develop and implement an affirmative action program for women and then report on progress to the Affirmative Action agency. While the Act was non-binding, sanctions for non-compliance included ineligibility for federal government contracts or assistance (Sheridan, 1998). Industry associations soon adopted a proactive ‘self-regulation’ approach to gender equality, with the Business Council of Australia establishing a Council for Equal Employment Opportunity with the aim of demonstrating ‘a genuine commitment by the private sector to affirmative action programs’ (Diversity Council Australia, 2023). The Council's activities operated as normative pressure, providing recommendations, expertise and consultation to improve company policy on gender equality (Taksa and Groutsis, 2017).

In the 2000s and 2010s, there was some expansion of the scope of workplace diversity expectations. Ideals of ‘productive diversity’ translated the earlier emphasis on equality and human rights into the language of business, with the successful ‘management’ of a range of differences – including multiculturalism, Indigenous reconciliation, disability and LGBTQIA + recognition – seen as necessary for innovation and productive stakeholder relationships (Taksa and Groutsis, 2017: 11). The Diversity Council of Australia – established in 2005 from the Council for Equal Employment Opportunity – became the peak body leading diversity and inclusion in the workplace, applying normative pressure through membership, advocacy, advice and events. Their remit has been broad, encouraging ‘employers to create more diverse and inclusive workplaces’ for all in society who are ‘historically disadvantaged or underrepresented’ (Diversity Council Australia, 2018: 1). Public and government attention on national Indigenous reconciliation – active from the 1990s – was adopted by the corporate sector in the form of Reconciliation Action Plans (RAPs). The governing body, Reconciliation Australia, implemented a program of voluntary organisational plans that seek to show respect, develop relationships, and create opportunities for Indigenous Australians (Lloyd, 2018). Since 2006, more than 1000 organisations covering 20 per cent of the Australian workforce have adopted RAPs, which create shared value by accessing new markets and employing a workforce that is representative of the community (Armstrong, 2016). Coercive pressures in the form of public and government attention, combined with normative pressure in the form of best practice principles from Reconciliation Australia, have encouraged corporations to address Indigenous dispossession and disadvantage in a systematic way.

Although the scope of diversity expectations expanded, gender equality received most of the external institutional attention in the 2010s. Women in leadership was seen as a priority for neoliberal feminism in the twenty-first century, with coercive pressure in the form of shareholder activism, government inquiries and attention from the Australian Human Rights Commission (AHRC) encouraging companies to address women in leadership (Du Plessis et al., 2014; Wright, 2021). The 2012 Workplace Gender Equality Act (which superseded the Equal Opportunity Act and the Affirmative Action Act) has required employers with 100 more employees to report against gender equality indicators, including pay equality and the gender composition of the workforce. The Workplace Gender Equality Agency (WGEA), the government department that administers the Act, has worked with employers to ensure compliance (coercive pressure) and has implemented a voluntary Employer of Choice program that externally recognises organisations that actively commit to workplace gender equality (normative pressure) (WGEA, 2023). Additional normative pressures have followed, with the ASX revising their Corporate Governance Principles and Recommendations in 2010 to encourage firms to monitor, disclose and establish policies to improve the number of women in leadership at the executive and board level. The Australian Institute of Company Directors has monitored the number of women on boards and set highly-publicised targets for the sector from 2015. A range of other professional bodies, including Women on Boards (established 2001), Chief Executive Women (established 1985) and Male Champions of Change (established 2010) have supported industry efforts towards women in corporate leadership (Du Plessis et al., 2014; Ross-Smith and Bridge, 2008; Sheridan et al., 2014, 2021). At the same time, normative pressures also made the link between women in leadership and corporate reputation with, for example, the WGEA arguing that gender diversity can contribute to ‘enhanced organisational reputation’; and The Australian reporting that the issue of women on board can often ‘make or break the reputation of companies’ (The Australian, 2018: 24; WGEA, 2018). Women in leadership have become the key indicator of a corporation's commitment to diversity and inclusion.

The prevalence and type of diversity disclosures have reflected the institutional environment. Although diversity reports were uncommon in the 1980s, 1990s and 2000s, those who did disclose made note of the external pressures influencing their report (Table 4). ‘Affirmative action’ and ‘equal employment opportunity’ measures were mentioned, including coercive pressures in the form of the Commonwealth Government legislation (BHP, 1985: 24; Commonwealth Bank, 1986: 28; Rio Tinto, 2007: 90; Woodside, 1997: 49). Some acknowledged normative pressures, including collaboration with the Business Council of Australia on pilot Affirmative Action programs (State Bank of Victoria, 1986: 45; Westpac, 1986: 17). The stated rationale for diversity disclosures was split between companies advocating for ‘equality of men and women, migrants and the disabled’ (Commonwealth Bank, 1986: 28) and the ‘business case’; that ‘workforce demographic diversity […] helps us stay focused on finding better solutions to meet their differing needs’ (Westpac, 1997: 33).

In the decade between 2007 and 2018, diversity disclosures became part of the shared annual reporting practice (Table 4). Diversity reports quadrupled from 20–75 per cent of the sample, with companies outlining programs to assist those marginalised based on gender, sexuality, age, ethnicity, disability and religion. For example, Crown (2018: 19) reported on their ‘whole-of-business’ approach to diversity and inclusion, including specific employment programs for Indigenous and disabled employees and staff networks for LGBTQIA+, parents and those with cultural and linguistic diversity. Normative pressures – in the form of external standards and recognition – were recorded, with AMP (2018: 11) noting their implementation of best practice principles from the Diversity Council of Australia, and Woolworths (2018: 11) including their award-winning policy for LGBTI inclusion. In instances where it was discussed explicitly, workplace diversity was rationalised based on the ‘business case’. Boral (2018: 22), for example, argued that ‘a diverse workforce helps us deliver higher performance by fostering a more creative, flexible and innovative culture’. Newcrest (2018: 19), similarly, conflated diversity with business success, arguing that it helped ‘explore, develop and produce more gold safely and profitably’.

Although reports addressed a range of diversities, the vast majority of reports addressed gender diversity and women in leadership. Of the 30 companies that included diversity disclosures in 2018, all of them discussed gender diversity and 26 (87%) addressed women in leadership roles. To compare, 13 (43%) companies addressed Indigenous employment; eight (27%) companies addressed LGBTI issues; four (10%) addressed ethnicity; and two (5%) companies respectively noted age and disability. Sonic Healthcare, for example, reflected the societal focus on gender relations, with their ‘current objective […] to monitor and maintain the percentage of females in senior leadership positions at a level greater than 40%’ (2018: 55). AusNet (2018: 11), similarly, argued that improving the number of women in senior management roles was the ‘key pillar of [their] diversity approach’. The stringency of institutional pressures for gender equality was evident in reports, with companies noting coercive pressures in the form of compliance with the Workplace Gender Equality Act (Caltex, 2018: 26; Commonwealth Bank, 2018: 39; Seven Group, 2018; Treasury Wine Estates, 2018: 32). A range of normative pressures was also acknowledged, including the WGEA's ‘Employer of Choice’ citation (LendLease, 2018: 49; Mirvac, 2018: 30; Origin Energy, 2018: 94; Tabcorp, 2018: 25), compliance with ASX Corporate Governance principles (Treasury Wine Estates, 2018: 32), and the Male Champions of Change program (Coca-Cola Amatil, 2018: 6; Crown, 2018: 19; Newcrest, 2018: 19).

Indigenous reconciliation was another specific area of focus, with the normative pressure from Reconciliation Australia contributing to disclosure of RAPs across companies in the sample (Boral, 2018: 22; Caltex, 2018: 26; Commonwealth Bank, 2018: 39; Mirvac, 2018: 30; Woodside, 2018: 54). Wesfarmers, for example, reported on progress against their first RAP in 2009, with initiatives across employment, procurement and partnerships to ‘make every business a place where Indigenous people feel welcomed and valued’ (Wesfarmers, 2018: 59). As with other forms of voluntary disclosure, the publicity of diversity activities was as important as the activities themselves. Caltex (2018: 27), for example, argued that the ‘RAP is a public declaration of our commitment to reconciliation’. Tabcorp (2018: 25), similarly, noted that the WGEA ‘Employer of Choice’ citation was important because it ‘recognises our achievements in working towards a diverse workplace’, and Mirvac (2018: 30) argued that the ‘prestigious’ citation ‘once again recognised’ their efforts towards gender equality. Westpac (2018: 35) argued that diversity was not only a strategic necessity but crucial for public relations, helping them to deliver ‘the best customer experience, improved financial performance and a stronger corporate reputation’. As with community and environmental disclosures, diversity disclosures conformed with institutional isomorphisms designed to use annual reports to hold corporations accountable, while also adhering to professional norms regarding their use for public relations.

Conclusions

This article contributes to research on organisational accountability and accounting history to provide a rare, longitudinal perspective on the collective annual reporting practice of Australia's large corporations. Interpreting the qualitative and quantitative content analysis through NIT, we find that coercive pressure from company regulations and societal expectations and normative ‘best practice’ recommendations from the accounting profession have aimed to improve standards of corporate accountability. On the other hand, normative pressures from professional and industry associations have encouraged companies to use annual reports for corporate public relations. Although annual reports changed gradually and unevenly, the convergence on a shared practice demonstrates the importance of institutional isomorphisms for company disclosure.

The content analysis reveals that annual reporting in Australia progressed in three phases. Between 1910 and 1952, coercive pressure from regulators encouraged the production of short, austere financial reports. Between 1952 and 1986, the intensification of regulatory requirements and accounting standards, alongside normative recommendations from the public relations profession, split reports into ‘narrative’ sections and austere financial disclosures. From the 1980s, expansion of the regulatory, professional and societal obligations gradually introduced standards of corporate accountability to narrative sections. A range of coercive and normative pressures compelled companies to report on their community, environmental and diversity performance. Companies used these narrative sections to simultaneously meet coercive and normative expectations of accountability, as well as normative recommendations regarding positive public relations.

This article contributes to Australian accounting history by revealing the historical path dependencies of contemporary disclosures and contextualising individual reports within a shared practice. The observed homogeneity in content, but the dichotomy of purpose, also has important contemporary implications. In particular, the confluence of accountability and public relations in annual reports is relevant to current concerns over disclosure quality and transparency (Chan et al., 2014; Deegan, 2017; Deegan and Rankin, 1996; Kent and Zunker, 2013; Lim et al., 2017; Yang et al., 2021). Future research directions could include the extent of the conflict between the different reporting objectives, or the historical institutionalisation of annual reporting in other nations and regions.

Footnotes

Acknowledgements

Many thanks to Christopher Monnox for research assistance, the University of Wollongong’s Colonial and Settler Studies (CASS) Work in Progress group, and three anonymous referees for valuable feedback on this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Macquarie University Research Fellowship.