Abstract

This article reports the research process, methodology and findings of a digital investigation of a Venetian merchant's journal and ledger from the first half of the fifteenth century. Several unexpected findings resulted, including a cash account that had a continuous credit balance for almost a year, and cessation of the journal for two months during a lengthy period when the business appeared to downsize and shrink before re-emerging after the journal was restarted. The contributions of this article relate (1) to its presentation of a digital research methodology that can be utilised by anyone with an interest in exploring beneath the numbers of archival account books; and (2) as exemplified in the unexpected findings, to the benefit of adopting this digital methodology that presents the journal and ledger in a way never previously attempted, vastly increasing the opportunities for investigation and discovery compared to traditional approaches and methods.

Keywords

Prelim

In fifteenth-century Venice, the new year was celebrated at the beginning of March. The original dates are used throughout this article.

Introduction

This article reports the results of a digitally based study of the account books of a Venetian merchant in the early fifteenth century. Late-medieval Venice was where the method of double entry used today, and where the two main account books used until the recent computerisation of bookkeeping, originated. While double entry was in use in different forms in other regions of medieval northern Italy, it was the Venetian libro doppio method that spread across Europe. This happened because it was the only one of those approaches described in more than one million estimated copies of 860 editions of bookkeeping manuals published in Europe before 1800 (Jeannin, 1991; Sangster, 2022). Yet, despite the unquestionably significant importance of medieval Venetian bookkeeping and accounting practice to modern accounting, very little is known of either.

This is, in part, due to a relative lack of surviving sources – in double entry, there is almost nothing before 1400 and less than 20 known account books from the fifteenth century. Studying those sources that are available requires considerable time and effort in deciphering a form of cursive handwriting that resembles shorthand and requires months of dedicated study to comprehend the sources. In addition, skills in the language are needed before the handwriting can be transcribed. Not surprisingly, very few accounting historians have the ability to read the handwriting of medieval Venetian merchants. For those who do not speak at least one of the Romance languages, the reading, transcribing and translation needs to be done by someone else, which means that they must also visit the archive, ideally at the same time. Another problem is access. In Venice, the State Archive is open in summer from 08:30 to 18:00 three days a week and from 08:30 to 14:00 two days a week and less in winter. However, the material in the archive cannot be borrowed and, if someone has already requested what you want to see or it has been misplaced, days may be wasted waiting for the requested material. Consequently, while those living near Venice can easily study what is there, those from further afield must spend several weeks in the archive making sense of what they can see, with all the costs that may entail. As will be described in this article, one possible solution is to photograph or scan what they wish to study when it is available.

Perhaps understandably, no accounting scholars have ever published detailed studies investigating these sources, though historians and, in particular, economic historians have examined some of them for their research agendas, including Lane (1944, 1977); Lane and Mueller (1985); Mueller (1997); Montemezzo (2012, 2014, 2015); and Ryabova (2016, 2018a, 2018b, 2019). Most studies on early forms of double entry bookkeeping were conducted in the first half of the twentieth century, most notably by Besta (1916) and De Roover (1956); and summarised to a large extent by Martinelli (1974), who included 20 pages of description and translated extracts from Andrea Barbarigo's first ledger and journal (Martinelli, 1974: 867–886) – the focus of study for this article. While these studies provided some awareness of bookkeeping, they provided no insights concerning its use. This was highlighted by Raymond De Roover in 1956 (114), who wrote that the literature on medieval double entry bookkeeping was largely about the form of entries and the procedures followed in the bookkeeping. It did not seek understanding or explanation, nor did it investigate anomalies, and little has changed to the present day. Consequently, there is still an enormous amount to be learnt about medieval Italian bookkeeping, not least in Venice.

The study reported in this article was initially motivated by a desire to discover whether, through a new digital research methodology we had developed, examination of the business records of one early-fifteenth-century Venetian merchant might bring insights to an accounting audience of a type that earlier analogue studies, principally by non-accountants, have failed to provide. For example, in terms of what these accounts tell us about the purpose they served; whether the quality of the bookkeeping was important, or simply that a record was kept; whether the bookkeeping itself was important to the business or to merchants; what types of accounts they kept – did they keep accounts for non-current assets, for example, or bad debts, and how were they recorded; what motivated the closure of the ledger; were merchants concerned about knowing their costs; whether the bookkeeping treatment of indirect costs differed from the treatment of direct costs; whether there were any unexpected features in the bookkeeping or in the data recorded; and, with respect to these and other similar questions, why?

Our attention was drawn to Andrea Barbarigo because, uniquely among Venetian fifteenth-century wholesale merchants, he closed a ledger before it was full; and the reason for his doing this is unknown (Lane, 1944). Why it was closed is the question we set out to answer by analysing its content in the 50-month period before this occurred. The cash account was selected for analysis, initially because Pacioli (1494) stated it was the largest one in a Venetian merchant's ledger, but also because it can never have a credit balance, though that feature was considered unlikely to identify anything of interest beyond pinpointing possible short timing differences between movements of cash and their being recorded in the ledger. However, soon after we began to examine it, our attention was drawn to an unexpected and difficult-to-believe feature that our digitalised methodology vividly highlighted: during three extended periods, the cash account had a credit balance.

Apart from broader contributions to the literature of this article, its primary contributions are twofold: firstly, in its use of a new digital research methodology developed specifically for in-depth investigation of medieval account books, with their poorly aligned rows and columns and difficult-to-read cursive script. This methodology is equally applicable to account books of later periods where its implementation would be considerably easier. Secondly, the power of discovery and explanation it illustrates when deep analysis of such account books is conducted using this digital methodology.

The next section of the article presents a brief biography of the merchant, his account books and his bookkeeping. This is followed by details of the digital research methodology adopted. Then, several features identified during our investigation are presented and discussed, along with the benefits that we perceived arose from our adopting a fully digitised research methodology. The article ends with a discussion, conclusion and recommendation for further research.

Andrea Barbarigo 1

Beginning with 200 ducats his mother gave him as seed money, by 1430 Andrea Barbarigo had a net worth of more than 1,600 ducats. By August 1440, this had risen to approximately 7,000 ducats (Lane, 1944: 184–185); and, by the time of his death in October 1449, he had amassed a fortune estimated to be 12,000 ducats (Lane, 1944: 185–186). He was never one of the leading Venetian merchants of his day. His mercantile career began from the bottom as he gradually used his networks and the resources he could assemble to achieve a good standard of living for himself and, in later years, his family. That he was able to do so was, not least, because of his heritage.

Andrea Barbarigo was born in Venice in 1399 into a family of Venetian nobility that had a prominent position in Crete. His family was left impoverished after his father, Nicolò Barbarigo, was found guilty of dereliction of duty when commanding a fleet of merchant galleys returning from Alexandria in December 1417 laden with valuable cargo, particularly spice. During the journey, it was decided to take a more dangerous channel to speed up its return. When one of the galleys was shipwrecked, his standing orders were to immediately mount a rescue. Instead, he continued the voyage to Venice, sending only a small boat back to look for survivors. The State imposed a fine of 10,000 ducats, resulting in financial ruin, disgrace and an end to his career. At that time, his son Andrea was just over 18 years old.

His privileged upbringing gave him an education that prepared him for life either in the service of the state or as a merchant. He served as a bowman on merchant galleys, which prepared him for a mercantile career, giving him insights into the practices on the galleys that carried merchants and goods to and from North Africa, the Middle East, the Ottoman Empire, the islands of the Mediterranean, France, Iberia, England and northern mainland Europe. He learnt about loading and unloading, measures to take to protect goods and maximise opportunities, and things to avoid. Most importantly, he began to develop a network of contacts, both experienced merchants and apprentices like himself, which was an essential ingredient for anyone then seeking to become an international merchant. After his apprenticeship, he embarked on a legal education culminating in his working for the Venetian state as an arbitrator in legal disputes between merchants, which equipped him with knowledge of mercantile law, extended his networks and provided him with more insights into mercantile behaviour, attitude, practice and risks. Many of these skills are evident in his surviving correspondence.

The merchant and his account books

Having reached 30 years of age, satisfied that he had demonstrated to himself that he had the ability to focus primarily on a mercantile career, in late 1430 he transferred the list of balances from his previous small yellow notebook marked ‘X’ into a new, 640-page ledger, marked ‘A’. Entries were recorded in the money of account for Venetian wholesale trade, where 1 lira = 10 ducats; and the lira and its sub-units, the soldi, denari and piccolo were in the ratio of 1:20:12:32 (Lane and Mueller, 1985). Barbarigo adopted the Venetian account structure of a bilateral ledger, whereby the debit and credit of an account are on facing pages, or kartas, 2 and both are given the same karta number. Depending on their assumed size, several accounts could be placed on each page, each one separated by a solid horizontal line.

The balances were transferred from the yellow notebook without the use of an account for profits and losses. As a result, not only were several venture accounts open due to the omnipresent delay in notification of costs and revenues from distant agents, expense account balances were transferred as debit balances into the new ledger. Similar in concept to a trial balance, the total debits equalled the total credits in his bilancio (balance account), the account containing all the opening balances that were created on the first karta of the ledger. His capital account had a balance of exactly 20 lire (200 ducats), being the amount given to him by his mother when he first started to trade. Profits that had been recognised were transferred separately from the yellow notebook, amounting to 80 lire 11 soldi two denari five piccoli. After making off-setting adjustments for ventures-in-progress, the loss of a ship and more than 1,000 ducats (100 lire) of expense balances, his net worth when the new ledger was opened has been estimated to be 167 lire six soldi two denari 24 piccoli (Lane, 1944: 183). Much of this was invested in voyages and inventory. He only had just over 24 lire in liquid resources: one lire seven soldi in cash; and 22 lire 13 soldi five denari six piccoli in his current account at the bank. His operating capital was significantly greater than his net worth of 167 lire. A loan of 62 lire 15 soldi 5 denari 19 piccoli from his bankers raised it to more than 230 lire, or 2,300 ducats. He used agents to engage in wholesale trade in the major markets, made extensive use of bills of exchange to move funds and relied on his bankers to provide loans and an overdraft, selling goods through them to effectively give them security over his debt. He also engaged in retail trade in Venice. All his business activities were recorded in his ledger and journal, which are the only two account books he maintained.

Closing the ledger and checking for errors

After four years and two months, on the final day of February 1434, before it was full, he closed his ledger. He reopened it the next day, 1st March 1435, in the same book. In closing the book, he did not close expense and income accounts and transfer them to an account for profits and losses. He simply balanced all open accounts and entered the balances into his bilancio, which is the same process as was described above when he transferred the balances from his previous yellow notebook marked ‘X’. Before doing so, he spent at least three days checking all the entries. Among the 995 entries for transactions in the cash account, he found and corrected 15 errors, but failed to detect three others, including one in the calculation of the balance on 26th February 1434 when it was carried down to the last karta of the account prior to final checks and ledger closing. The three errors resulted in the cash balance on 28th February 1434 (£19 s7 d5 p26) being overstated by £4 s1 d11 p12 (4.1 lire).

Once he had prepared his closing bilancio, he did not total the two sides, which suggests he proceeded with the rest of the closure process without checking that the totals agreed. He then used it as the source for all the entries that opened accounts in the continuation of the ledger. In each case, both a debit and a credit entry were made. If a closing balance was a debit, it was debited to the re-opened account and a credit was entered in an opening bilancio created for this exercise; vice versa if the closing balance was a credit. After completing this process, the two sides of the opening bilancio were totalled. As it contains the contra entries to all the entries made for the closing balances in new accounts, the debit balances are on the right and the credit balances are on the left, that is, it is the mirror image of the closing bilancio. The total of the debit balances (£976 s10 d6 p31) was £3 s1 d0 p18 more than that of the credit balances. There is no evidence that Barbarigo subsequently tried to find the cause of his bilancio failing to balance. It appears to have been sufficiently close to doing so for him not to be concerned. As he had just spent three days going through the entire ledger, he would have realised how difficult it would be to find what may only have been a very small number of relatively insignificant errors.

The next section presents the research method adopted in this study.

Research method, digitalisation and problems overcome

The principal research method adopted in this study is digital-archival-hermeneutics. Underpinning the approach, entries in the account books were linked together using logical-analytical modelling. This is an analogue (i.e., manual) approach developed by this research team for the purpose of enabling entries in the account books to be traced visually between accounts and books, and from page to page. By adopting this approach, flowcharts are created that show the movements of data and information into, across and out of the entire accounting system. So, for example, you can plot the source of each entry into an account, and the location of any entry from that account, indicating the account books involved and where within them each entry lies, so illustrating how each account interacts with other parts of the bookkeeping system. This makes entries and their sources visually clear in a way that is not possible if you only have the original set of account books (Kuter et al., 2019, 2020, 2022). The usefulness we had previously found from using this framework informed how we designed the routines we developed in the study reported here.

Firstly, digitised images were made of all pages of the original hand-written Journal A and Ledger A found in the State Archive of Venice. Initially, these were photographs, which took two days to complete but, a lack of clarity in some of the images led to a further three days being spent taking scanned images of both books with widely available portable scanning equipment costing US$300. 3 Next, as a first step towards creating multiple linked spreadsheets containing the data from both the journal and the ledger, after developing power queries and VBA macros 4 in an Excel spreadsheet, the entries in the journal were keyed into it from the digitised images. The data entered was then checked by someone other than the person who entered it. To provide an indication of the scale of this exercise, it took about 10 days to record approximately 2,500 journal entries in the spreadsheet. The data recorded was checked while working with it during the following two months. Overall, in terms of the time actually spent doing so, data input and the checking took approximately one month. However, the elapsed time was nearer three months. This reflects the time needed to become immersed in the data and the nuances of the bookkeeping before truly detailed investigation could begin.

There are several advantages in this digital approach. While it could be done just as accurately manually using pen and paper, the linearity of a manual approach is far more time-consuming and more prone to making errors – only one thing can be done at a time and having someone else check not just numbers but also the transcription of a text is far easier if digitised sources are used and digital records kept, both of which can be duplicated at will and checked in parallel while carrying-on with the rest of the investigation. For example, reading the Roman numerals in the money column of these books is not a simple task. It is very easy to get confused when, for example, counting the number of “i”s there are in vij (7) and iij (3) and distinguishing between them when the cursive style of the handwriting connects all these numerals together rather than, for example, setting down separately the v and each i in viij (8). 5

The handwritten alignment of these numbers, both vertically and horizontally is also not consistent. Consequently, even identifying which number applies to which row is difficult, never mind whether a number belongs to the column for, say, soldi, or the column for denari. Anyone trying to add-up the amounts in the money column with, say, 30 entries involving lire, soldi, denari and piccoli in the ratio of 1:20:12:32, would struggle to do so quickly, never mind accurately. Doing so requires handling numbers in base-32, base-12 and base-20, along with inconsistently aligned entries in the vertical columns. When we tested this on one such page, one of our research team tried to do it four times, and got three different totals, none of which was correct. The spreadsheet instantly provided the correct total.

As we had scanned images of the account books, the checking of the numbers we had entered in the spreadsheet was done without needing to stop work on the account book to do so. The same applied to the checking of the transcripts of the entries. If you tried to do what we did using the original analogue account books as your source, you would need to decipher each number and the accompanying text before you could do what you wanted to do. Furthermore, you would only be able to have the numbers you identified, or the text you transcribed checked by someone else if they were in the archive with you. And to do that, you would need to stop working on the account book so that they could look at it. By scanning the account books and then using those images as our source when transcribing the text and entering the numbers into a spreadsheet, then having someone else check what had been done was correct, we were able to focus on what the entries were for. The alternative was to spend time transcribing the text from the original source and identifying the amount of each entry, one-at-a-time, in situ in the archive – a far less efficient and consequently much slower approach demanding presence in the archive and impossible elsewhere. By adopting the digital approach, we could do everything wherever we wished, so saving both time and the expenses of travelling to-and-from the archive.

The next stage of our methodology

The Venetian libro doppio paired bookkeeping system is defined by its unique characteristic that the only external source for entries in the ledger is the journal. Whether or not this pairing was consistently applied was assessed in the next stage of our methodology. Focusing on the cash account, there were 895 entries involving cash in the journal, which were all now in our spreadsheet. These digitised journal entries were then used as the source to create a computer-generated version of the cash account. In theory, this should have left only balances and correcting entries to be added for it to match the analogue ledger account.

To confirm whether that was the case, we compared our computer-generated cash account to the one in the hand-written ledger, and identified all entries in the latter that were not in the former. From them, we eliminated balances carried down and brought down, and corrected entries made within or between accounts in the ledger. At this point, we were left with over 90 entries that apparently did not come from the journal or from within the ledger. For each of those entries, using the data in the analogue ledger, we then searched the digitised journal seeking entries not labelled as being for the cash account, looking for the contra account name and karta, amount and approximate date. None were found. We then entered into our computer-generated cash account all those entries in the hand-written ledger account that were not from the journal.

This process enabled us to swiftly refute the assumption that Barbarigo was consistently using that libro doppio paired bookkeeping system first described by Benedetto Cotrugli in 1458, then by Luca Pacioli in 1494 and by every Italian author of a manual on double entry bookkeeping in the sixteenth and seventeenth centuries.

Had we instead adopted an analogue research methodology, to have made this discovery would have required that a full audit was conducted involving manual checking of every entry from the journal to the ledger, and from the ledger to the journal. The complexity of doing so in the context of these two account books cannot be overstated. While manually checking entries from the journal to the ledger is theoretically possible, the entries in the ledger sometimes have different dates from the journal – for example, two entries dated 7th August 1434 in the journal were dated 30th August when entered into the cash account in the ledger. Occasionally, a journal entry provided account numbers in the left margin that were changed when the entry was made in the ledger but remained unchanged in the journal. In addition, Barbarigo occasionally failed to make both entries in the ledger even though he scored across the journal entry twice to indicate that he had done so. From the alternative perspective of the ledger, there are no indications in the ledger of the page in the journal that entries come from. 6

The link reference between the two account books – the date – should, in theory, overcome these problems but, as mentioned above, the dates Barbarigo entered were not consistently the same in both books. Furthermore, not all entries are recorded in the journal in chronological order, and neither are some in the ledger. In addition, even when an entry was from the journal, Barbarigo occasionally failed to record the correct amount in both ledger accounts – for example, both may have the same incorrect amount, or one may be correct and the other wrong. Searching in the journal for the source of an entry in the ledger is so difficult, an economic historian who had spent four years studying these account books concluded (Lane, 1944: 162): when an entry in the ledger cannot be found under that date in the journal, we cannot be sure it is not somewhere out of chronological order.

Our digitisation of the entries in spreadsheets overcame that problem. With a few keystrokes, we could search the entire journal. In contrast, anyone searching manually would have to go through all the entries on a potentially large number of kartas in the journal. This would take several minutes particularly because, as mentioned above, the Roman numerals in the ledger are not perfectly aligned, either vertically or horizontally. This digitisation was what facilitated our being able to confirm that some entries in the ledger had no source entry in the journal, and identify which ones those were. In doing so, a second research question emerged that would have taken significantly longer to identify using an analogue research methodology: why had Barbarigo failed to apply the libro doppio method consistently?

Construction of the digitised journal and ledger

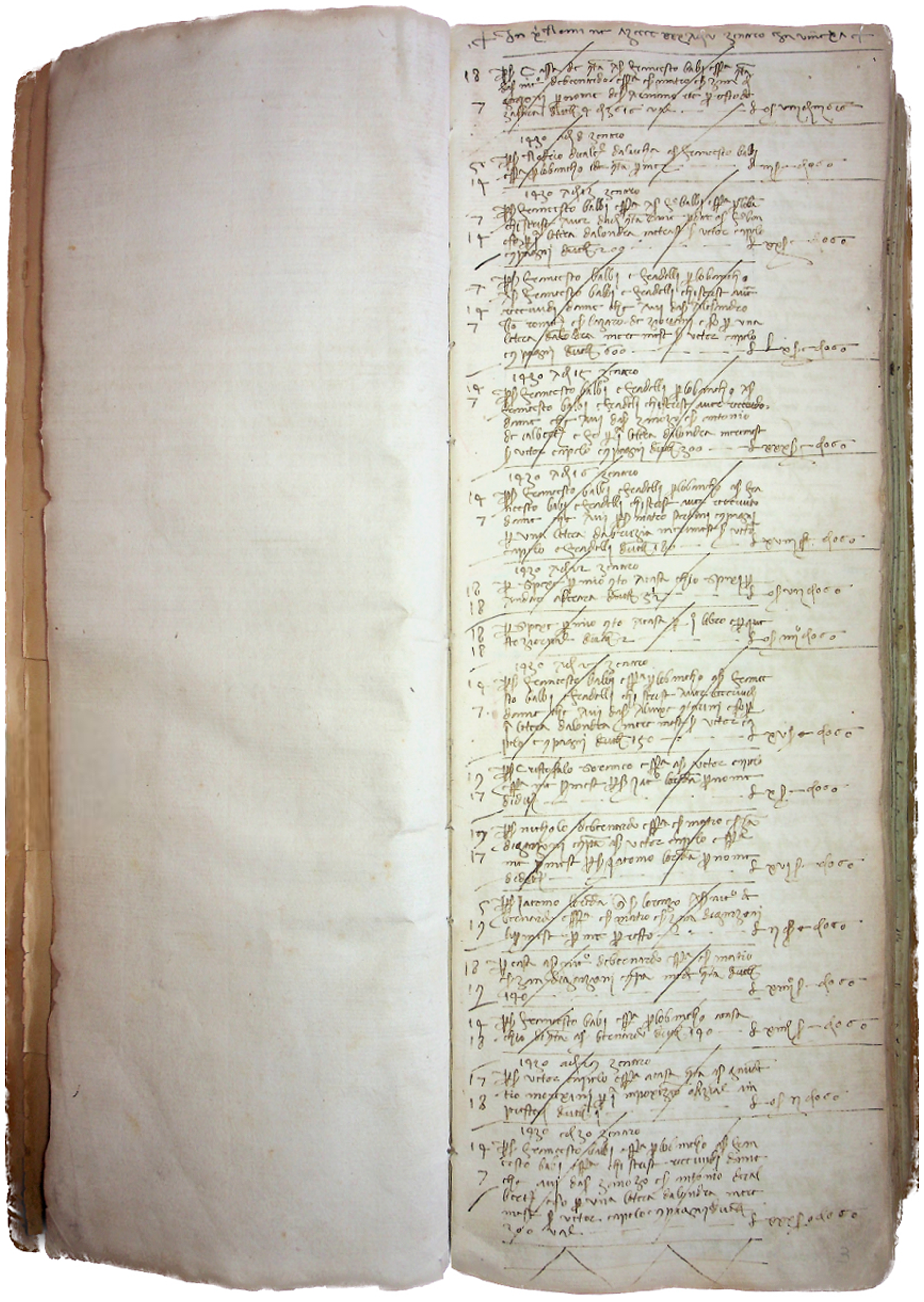

All analysis of the account entries in this article uses our computer-generated digitally created version of the cash account in Barbarigo's Ledger A, our digitised Journal A and our digital images of that ledger and the journal. To demonstrate the use of our programme and the result of its use, presented on the right in Figure 1 is the first-page containing entries in Barbarigo's journal, karta 3d. 7

Karta 3 of Journal A belonging to Andrea Barbarigo.

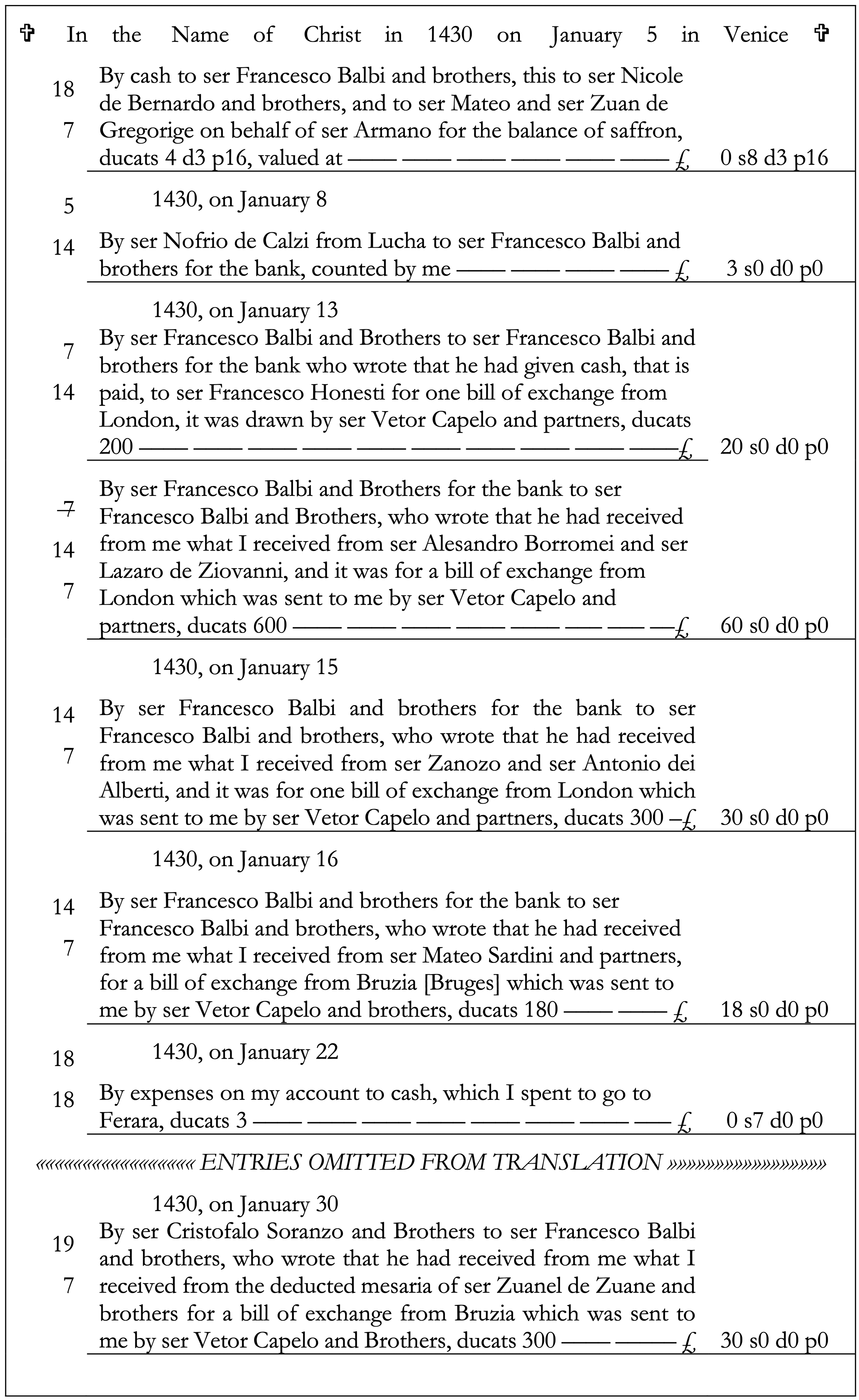

Figure 2 contains a partial translation of the entries on the page, formatted as in the original, with the ledger accounts indicated on the left. 8

Partial translation of karta 3 of Journal A belonging to Andrea Barbarigo.

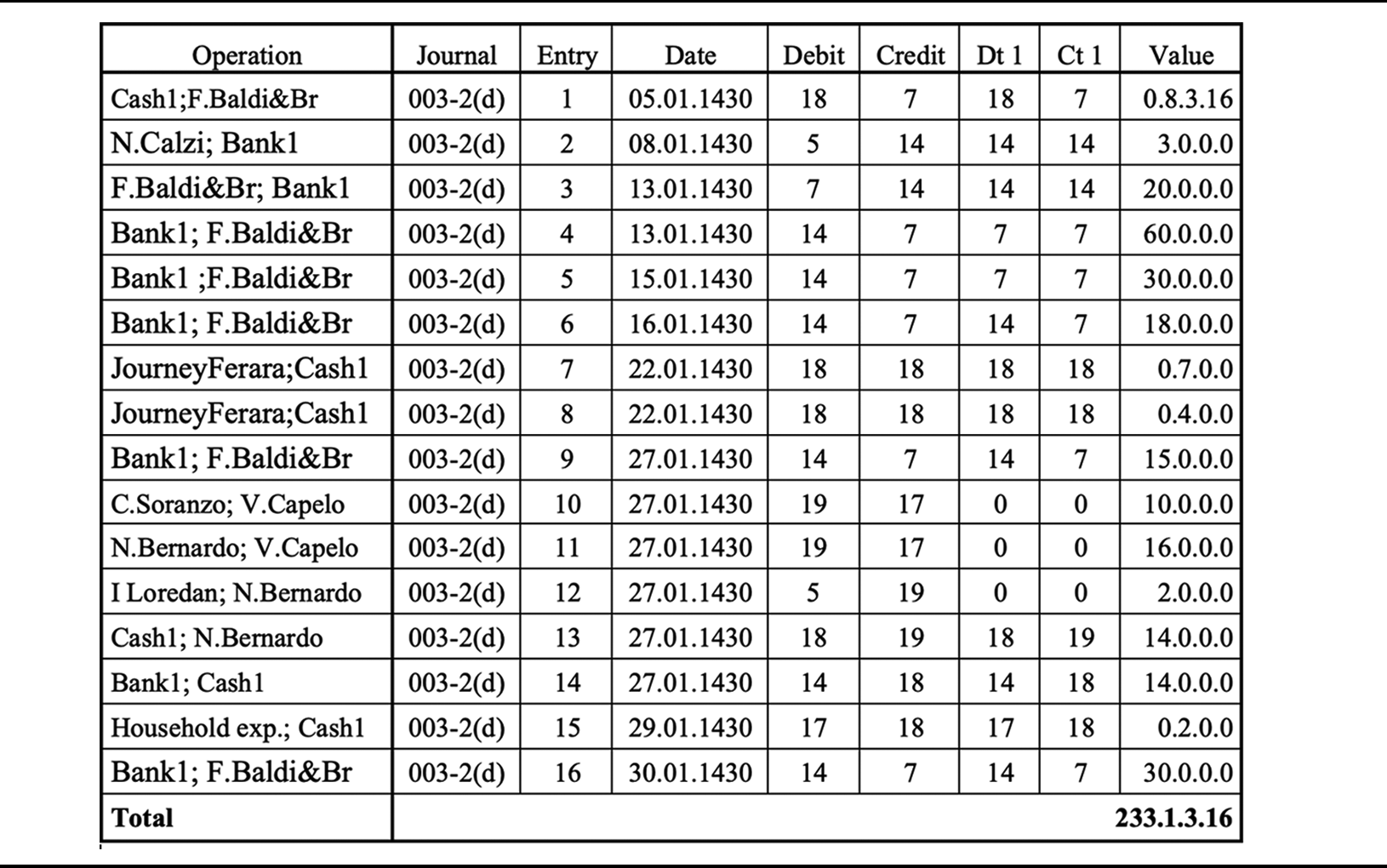

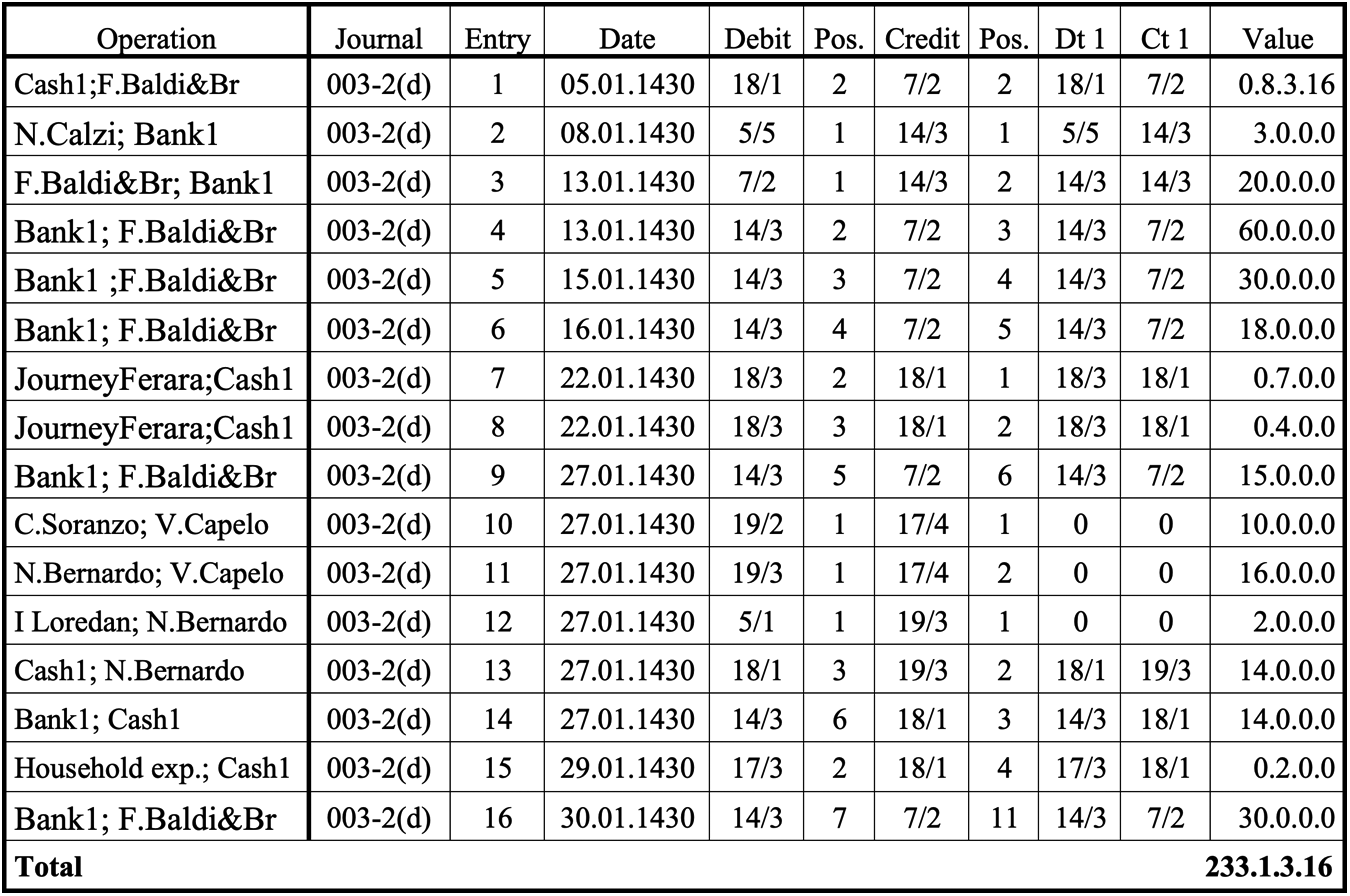

As can be seen in Figures 1 and 2, the journal contained three columns: the karta numbers in the ledger where each debit and credit entry was recorded; the detail of the transaction with the amount in ducats; and the amount recalculated in the money of account – lire di grossi. Table 1 presents our digitised version of this page. The first column (‘Operation’) briefly describes the content of each entry – the account names and occasionally its nature – without going into the full details of what is in the analogue original version. ‘Entry’ indicates where each entry lies in the page. Where an entry involved a book transfer between two personal accounts in the ledger, a zero was recorded in columns Dt1 and Ct1. Otherwise, those columns duplicate what is in the columns labelled Debit and Credit.

Journal, stage 1: karta 3d of the original analogue journal as recorded in the digitised journal.

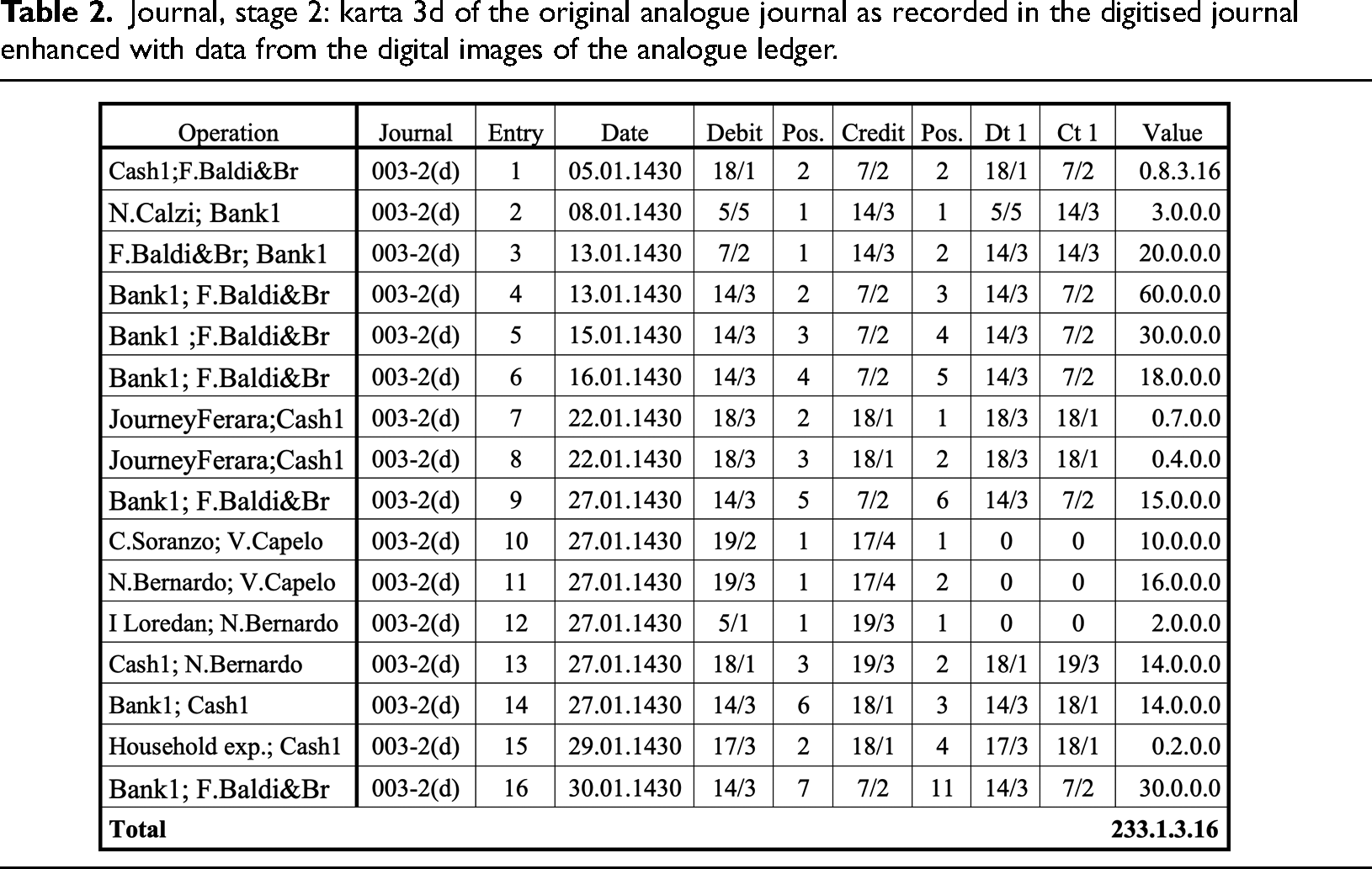

As shown in Table 2, the digitised journal was then enhanced by the addition of more information, this time from the ledger. The first involved distinguishing between accounts maintained on the same karta, which was the case on virtually all kartas of the ledger: the data in the columns for debit and credit were amended to include the position of the account within that karta in the format x/y. For example, the first journal entry in Table 2 shows that cash is account one on karta 18 of the ledger and that the account for Francesco Balbi and Brothers is the second account on karta 7, represented in the table as 18/1 and 7/2. In addition, to facilitate finding an individual journal entry in an account in the ledger, two separate ‘Position’ (‘Pos’) fields were created in the computer-digitised journal, one for the debit, the other for the credit. These showed the sequence of each entry in the individual ledger account.

Journal, stage 2: karta 3d of the original analogue journal as recorded in the digitised journal enhanced with data from the digital images of the analogue ledger.

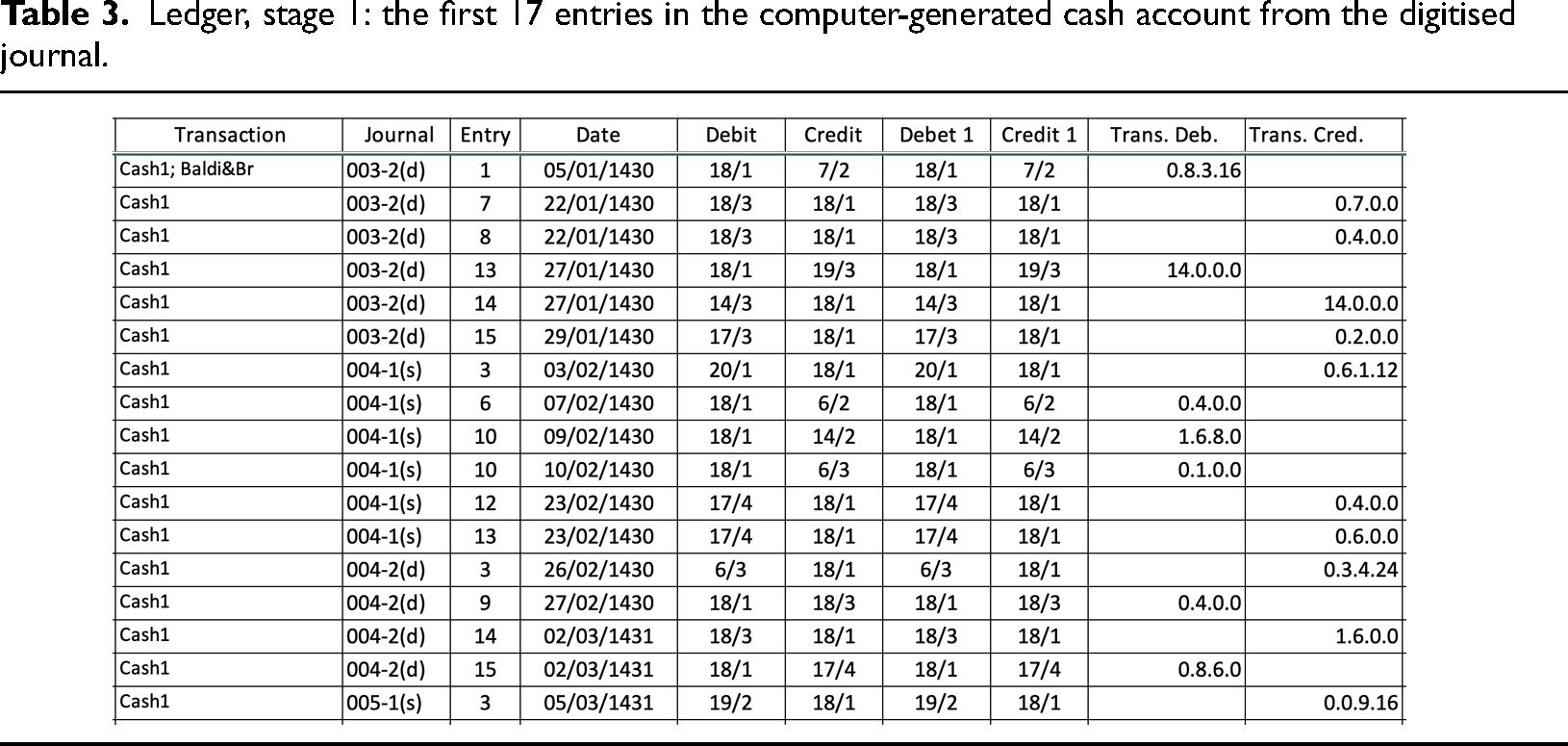

The computer-generated cash account contains columns for similar fields to those in our digitised journal. Table 3 shows the first 17 entries from the journal in the cash account on karta 18 of the ledger. An additional two columns were created, ‘Debet 1’ and ‘Credit 1’. They were used later to indicate where in the ledger the entries were actually made if that differed from what was indicated in the journal.

Ledger, stage 1: the first 17 entries in the computer-generated cash account from the digitised journal.

Following this process of digitisation, in addition to overcoming the difficulties mentioned above when seeking to verify the entries in both account books, far greater flexibility resulted in how the data contained in those account books could be analysed. Thus, the entries in the digitised ledger, for example, can be viewed either in the original sequence of Barbarigo's ledger, or in the order of the dates of their occurrence and, within the dates, by the sequence number of their appearance on the karta in the journal. The latter option was used to determine the consistency of dating and sequencing between the two books. When we did this, we found that the entries in the ledger sometimes matched neither the dates nor the sequence of entries in the journal. This confirmed two of the difficulties faced by anyone trying to manually verify the entries made between the two account books and may, at least partially, explain why Frederic Lane (1944) had found doing so impossible when working back from the ledger to the journal.

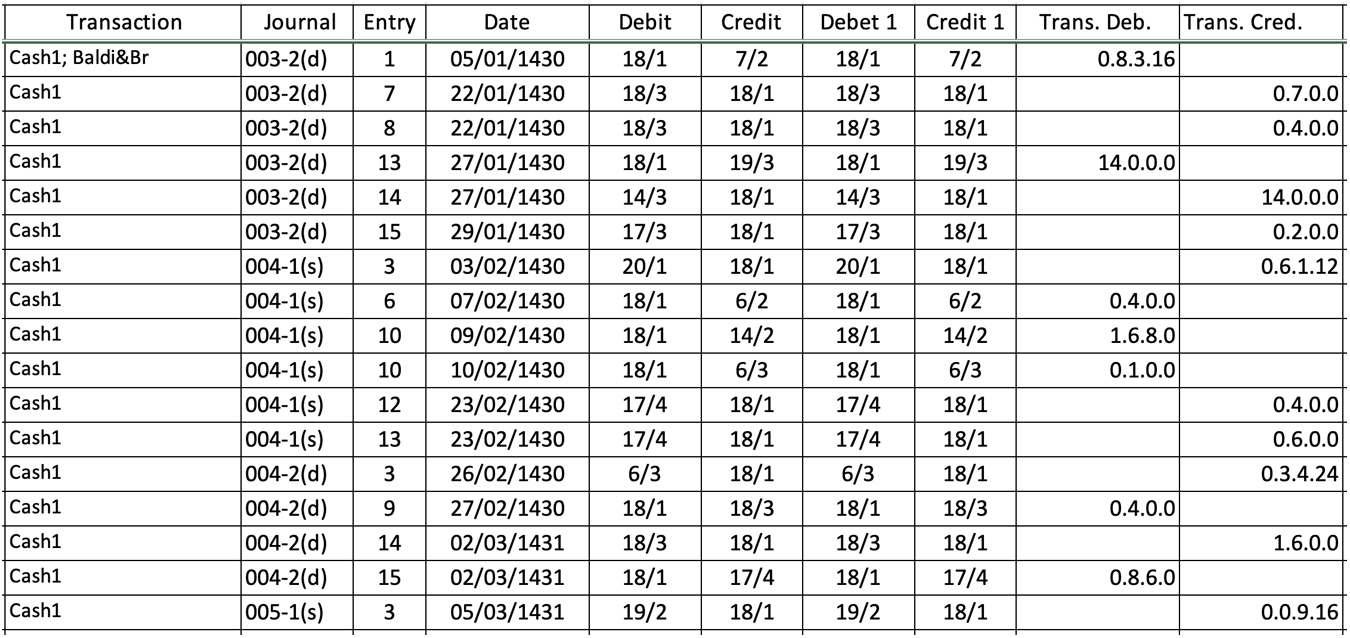

After creating the computer-generated cash account from the digitised journal, the opening balance recorded in the account was inserted. As shown in Table 4, this enabled a running total balance to be calculated.

Ledger, stage 2: the opening balance (‘Saldo’) is added and the running balance is calculated.

In the course of this phase of our investigation, we confirmed one very specific role of the Venetian journal in the fifteenth century: it was used to record transactions, and nothing else. There was not an account book anywhere else that had such a single purpose relating to entries made in the ledger. All the transactions recorded in it flowed from it into the ledger. However, as previously mentioned, we found several entries in the ledger that did not originate from the journal and were not for balances or correction of errors. We explored this further while focusing our attention on an unexpected anomaly we identified in the cash account.

The cash account

The cash account was opened on karta 18. There are three accounts on the karta, of which the cash account is the first. The first debit entry for £1 s6 is the balance of cash carried forward from the previous ledger, that is Yellow Notebook ‘X’. As with all the opening entries, its contra entry is in the bilancio, the list of opening balances contained in the Conto saldo debitori e creditori on karta 1. Because it is not the result of a transaction, there is no entry for it in the journal. Instead, the accounts were opened using double entry from the closing bilancio in the previous Yellow Notebook as the source of the two entries.

The cash account on karta 18 contains 22 debit entries and 30 credit entries, of which two are the opening and closing balances. All the other 50 entries originated in the journal. The computer-calculated Total debits and Total credits of those entries are equal; and the Total calculated by Barbarigo when he balanced the account on karta 18, of £60 s5 d9 p10, is equal to the amount calculated in our computerised version, as is the balance carried down for its continuation on karta 24.

The running balance generated by our programme confirmed the continuous presence of a debit balance on the first two kartas of the cash account, 18 and 24, and no errors in postings to the ledger, balance calculation or totals. On the third karta of the account, 32, we identified an error that arose when the account was closed on 17th August 1431. The addition of the total debit side was too high by £1 s12: £68 s8 d11 p27 instead of £66 s16 d11 p27. Barbarigo only found the error over three-and-a-half years later, when he was checking all the entries in the ledger at the end of February 1434. He then corrected the total and made an adjusting single entry in the cash account on karta 141. An error in calculating a balance on an account in this ledger with so many entries would not normally be obvious, and his arithmetic was generally very sound, if prone to the odd error. He is likely, at first at least, to have been reasonably confident in his ability to add up two pages of entries and calculate the balance, and may not have felt it necessary to check his calculations. But, when presented 21 months later with clear evidence that he had made a significant mistake, he simply noted that something was wrong. This occurred when he discovered that his cash account in the ledger had a credit balance.

Credit balances in the cash account

Closing credit balances

A debit balance was found by Barbarigo on each of the first eight kartas of the cash account. However, on 25th May 1433, when he closed the account for the ninth time, on karta 84, he found a credit balance of £0 s17 d10 p18. To the left of the balance, Barbarigo drew a very large asterisk; and repeated that symbol when he re-opened the account on karta 95. However, despite knowing that the balance was wrong, there is no indication that he attempted to discover the cause of his error until he checked the entire ledger almost two years later. As shown below, the next three times he balanced the account, it had a credit balance. Almost 11 months, and four kartas later, he finally found a debit balance when he closed the account. Thereafter, his closing balance on the cash account was always a debit.

Ignoring an entry made in error that was immediately cancelled, the penultimate entry on karta 120 was made on 14th April 1434. It was a debit of 4 lire. This established a debit balance on the account in Barbarigo's ledger and the final entry, a debit for 10 lire, resulted in the closing debit balance as shown in Table 5.

Credit balances on the cash account.

Barbarigo clearly neither relied on the account to tell him how much cash he had nor attempted to reconcile his cash held against the record in his ledger when he calculated the balance on the account. For him, the cash account may have served the primary purpose of maintaining consistent double entry in recording all transactions. Yet, that does not explain why he did not apparently attempt to discover the reason for the negative balance. And there was yet more to this than at first appeared. Barbarigo was seeing final balances, not continuous balances. When we looked more closely at our computer-generated replica of the cash account, we discovered that the situation was far more divergent from logic and accepted wisdom than he would have realised.

Daily credit balances

Two digitised versions of the cash account were prepared. In one, the timings of all entries mirror those in the analogue ledger. It is a digitised replica. The other includes all corrections and adjustments. Barbarigo entered them in the ledger when he discovered them, which was mainly during the three days he spent closing the ledger after 50 months of trading. In contrast, we entered them in our version when the transactions to which they related occurred. In doing so, we assumed that the sequence of the entries in the journal reflected the timing of each transaction relative to the others. We also assumed that when a large amount of cash was received on the same date as payments were made, the receipt occurred first. Subject to these two assumptions, this version tells us how much cash Barbarigo should have had when each transaction was originally recorded. Across the 50 months, while the ledger was open, the average amount of each of the 995 cash transactions recorded was 2.35 lire (i.e., 23.5 ducats).

Using this adjusted running balance version of the cash account, we revisited the credit balances identified by Barbarigo and discovered that they began 11 days earlier than he realised, on 14th May 1433, and ended after the aforementioned debit entry for 10 lire was made on 19th April 1434. By that date, the adjusted running balance on the cash account had been a credit for 340 days. During this time, 202 transactions had occurred involving cash, 151 of which were payments. 9 The largest credit balance was £35 s9 d5 p2 (35.47 lire) on 18th February. There is no indication that Barbarigo was aware he had been over-spending his cash during those 47 weeks – he must have had cash when each of the 151 payments was made, which indicates he had at least 35.47 lire more in cash than had been recorded in his cash account.

Before proceeding further, we utilised the graphic generator in Excel to see if a visual representation of the account might reveal more. It was hoped that it would enable us to see more clearly the extended periods during which Barbarigo apparently spent cash he did not have, pinpoint the largest amounts and balances, and generally attain far greater clarity than was possible by simply looking at the balances at the foot of each karta in the original analogue ledger, or even at the adjusted running balances in our spreadsheet.

A graphical approach

The graph was annotated to isolate any extended periods of ongoing credit balances. It is shown in Figure 3. On examining it, we immediately noticed that the continuous pattern of relatively small receipts and payments evident throughout those 340 days was not typical elsewhere. Our first thoughts were that it appeared he was winding down his business, though he may have simply switched to using his bank account rather than cash to manage the financial side of his business. The graph also revealed two other previously unidentified periods during which there was a continuous credit balance on the account.

Adjusted running balance on the cash account for the 50 months to 28 February 1434 (1431–1435 in a modern calendar).

Two other extended periods of credit balances on the cash account

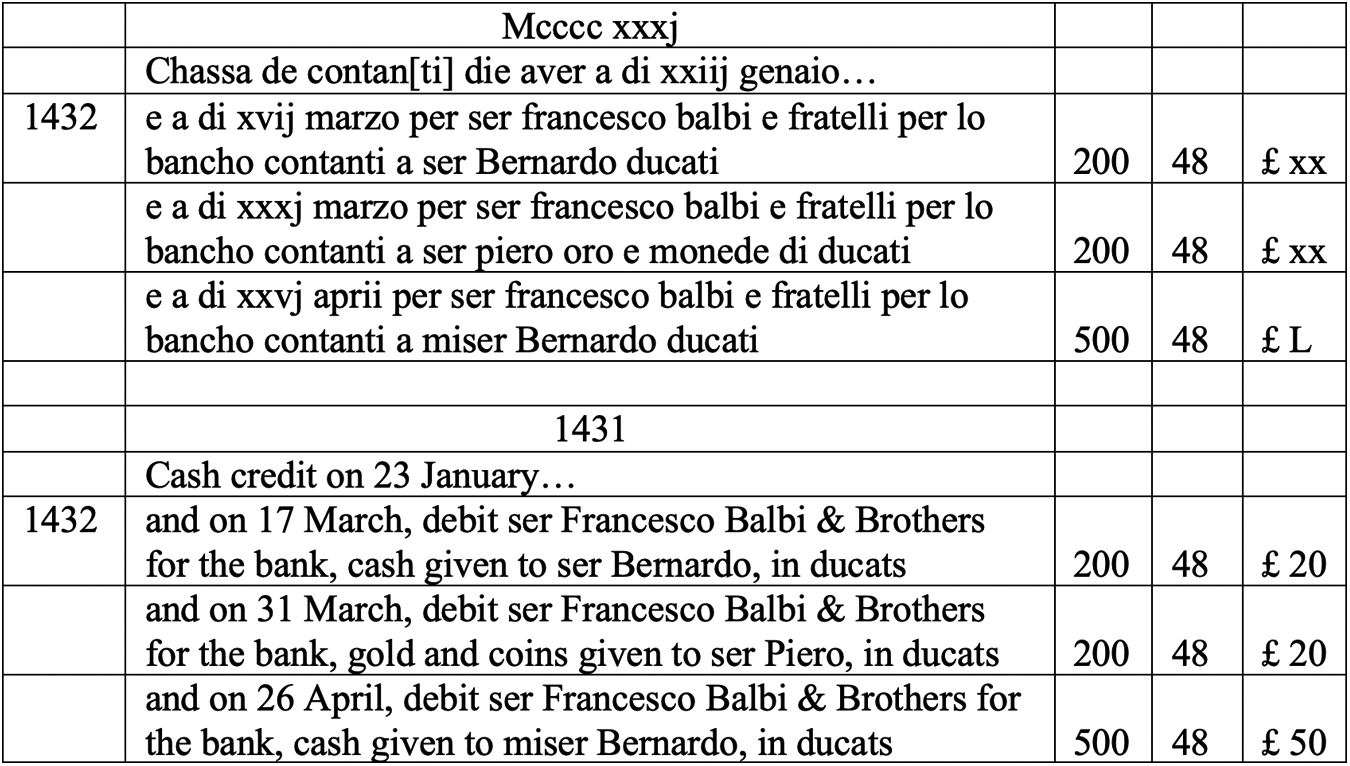

As can be seen in Figure 3, there were two other periods when Barbarigo's cash account had an ongoing credit balance. The first was recorded on a single karta of the ledger, karta 51. The karta opened on 23rd January 1431 and as would be expected for a cash account, the running balance continued in debit for 51 days. Then, on 13th March 1432, 14 months before Barbarigo first identified a credit balance on the account, the balance became a credit of £2 s2 d10 p28. Thereafter, for 47 days, with the exception of one day towards the end, the balance was consistently a credit, only reverting to continuous debit following two receipts totalling 53 lire 6 soldi on 29th April. The account on karta 51 was closed the next day and a balance of £10 s19 d8 p6 was recorded. As a result, Barbarigo was unaware that he had had a credit balance on his cash account for almost 7 weeks. He was also unaware that the closing balance he had calculated was overstated by almost 4 lire. During that time, there were 57 cash transactions, 37 of them payments. 10 The largest credit balance on the account was £37 s9 d4 p20 on 8th April (labelled 37.47 lire in Figure 3), though it is possible it had reached £43 s19 d7 p2 on 29th April before the receipt that day of the aforementioned 53 lire 6 soldi. This finding increased our estimate of the additional cash he held to at least 37.47 lire, perhaps 43.98 lire, rather than our previous estimate of 35.47 lire.

If cash flow were a problem, you might expect to see cash being introduced before the largest payments, and deposits of cash into the bank account to have been delayed. Neither occurred in this period. Looking at the pattern of movement of the balance, it was clear that the three largest deposits of cash into Barbarigo's bank account during these 47 days were responsible for the credit balances. Without those bank deposits (shown in Table 6) removing his cash from circulation, the account would not have had a credit balance on any day during this period. Those payments totalled 90 lire and were paid between 17th March and 26th April, most likely relating to bills of exchange by which Barbarigo moved funds to his agents and speculated on the exchange (Lane, 1944). While that suggests a reason for the deposits of cash being made in the bank, it does not explain how that was possible when Barbarigo apparently did not have sufficient cash to do so.

Three large credit entries in the cash account on karta 51 with debits to the bank account on karta 48.

Payments of this nature that removed his cash from circulation ceased thereafter, perhaps reflecting an increasing awareness that he had to be careful in how he spent his cash, and avoid making large payments into his bank when he was short of cash. Nevertheless, the impact of these three deposits on the logic of his cash balance lasted two years and eight months, until late December 1434.

The third period of an extended running credit balance

As can be seen from the graph in Figure 3, the third period of an extended running credit balance lasted slightly longer than the first: 52 days, from 21st August until 13th October 1434. During this period, 40 transactions involved cash, and 24 of them were payments. 11 The largest credit balance during the period was 34 lire.

Most of the higher value transactions occurred between 11th and 18th September, where there was a clearly organised series of transactions involving obtaining two short-term private loans totalling 41.6 lire that he paid into the bank account, presumably so that he could withdraw the amount of cash he needed to invest in two voyages. He invested 95.75 lire in the voyages, managing to withdraw from his bank the funds not provided by the loans, thanks to what appear to be exchange gains of 41 lire being credited to his account at the bank which meant that the overdraft of just over 10 lire these voyage investment transactions had created was eliminated. This left sufficient funds in the bank for him to withdraw and use to repay the first of the two loans on 18th September. Over the course of eight days, he successfully invested in the two voyages while retaining control over his cash to the point that his running balance had improved by 0.17 lire (from a credit balance of 4 lire). These eight days were when the highest value cash transaction occurred because he wanted to invest in the voyages and did so by withdrawing virtually all his funds from the bank. His closing bank balance on 18th September was 2.79 lire.

Barbarigo clearly had a good relationship with his bankers. While not part of our analysis, the closing balance on his bank account on 17th December 1432 had been a debit of 587.9 lire, and even higher four months earlier, when it was 614.85 lire, but these were exceptions. He often had an overdraft and the contortions he went through to invest in those two voyages provide some insight into how he used the two sources, and his network, when he needed to, and could do so to good effect. Looking at the 50-month period presented in Figure 3, it is evident from many of the labelled spikes how he used his cash, investing it almost immediately when he had it, mostly in deposits in his bank but some, as described above, being withdrawals in cash from the bank immediately invested in trade.

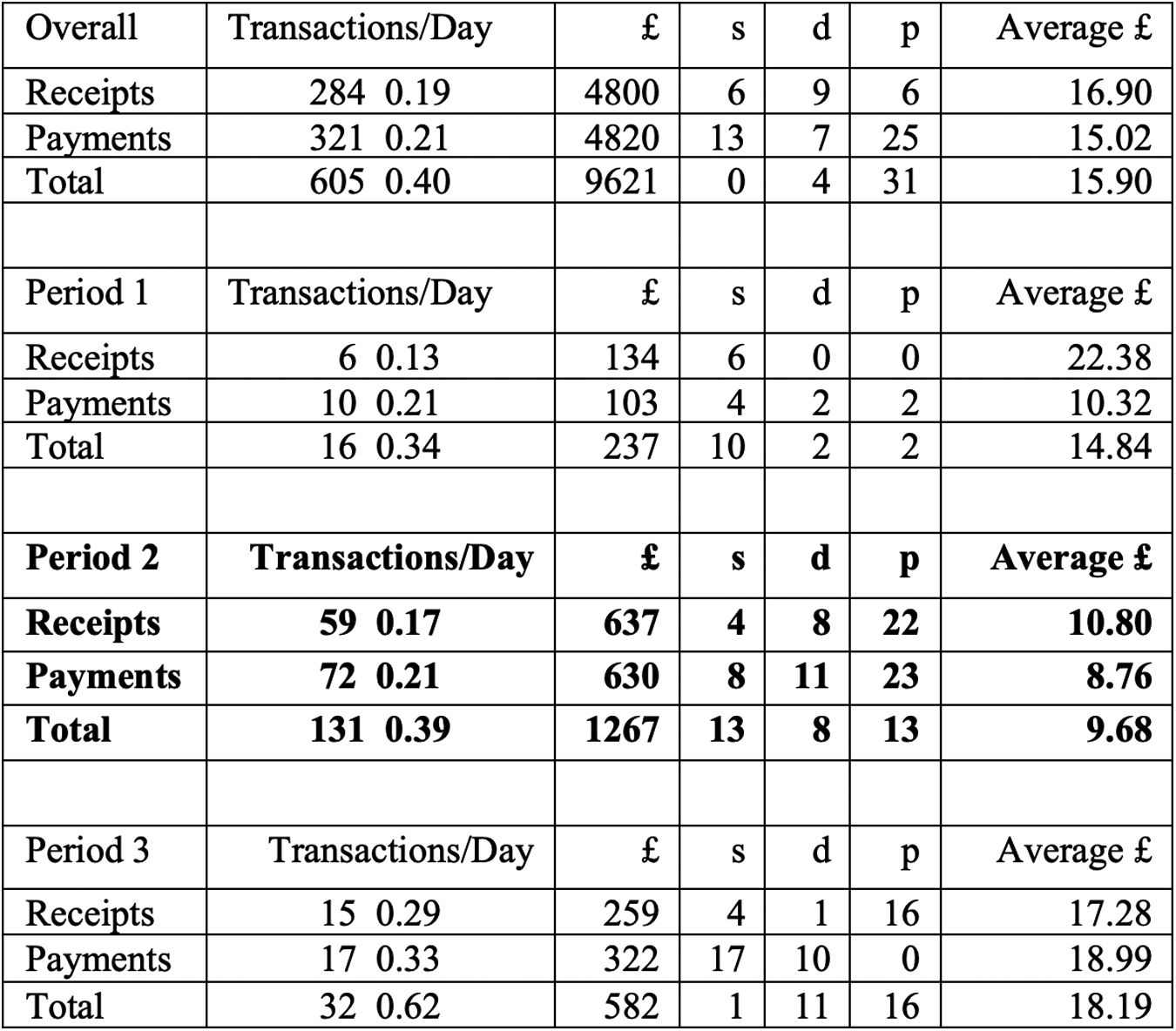

Cash transaction numbers and amounts across the 50-month period when the ledger was open

The data used in this study not only presents an overview of the cash flows, it also provides information on the volume and value of transactions. Our analysis of these features was supplemented by our digitised version of the bank accounts, which we prepared after discovering distinct differences between the three periods and between them and the overall 50 months that passed before Barbarigo closed his ledger.

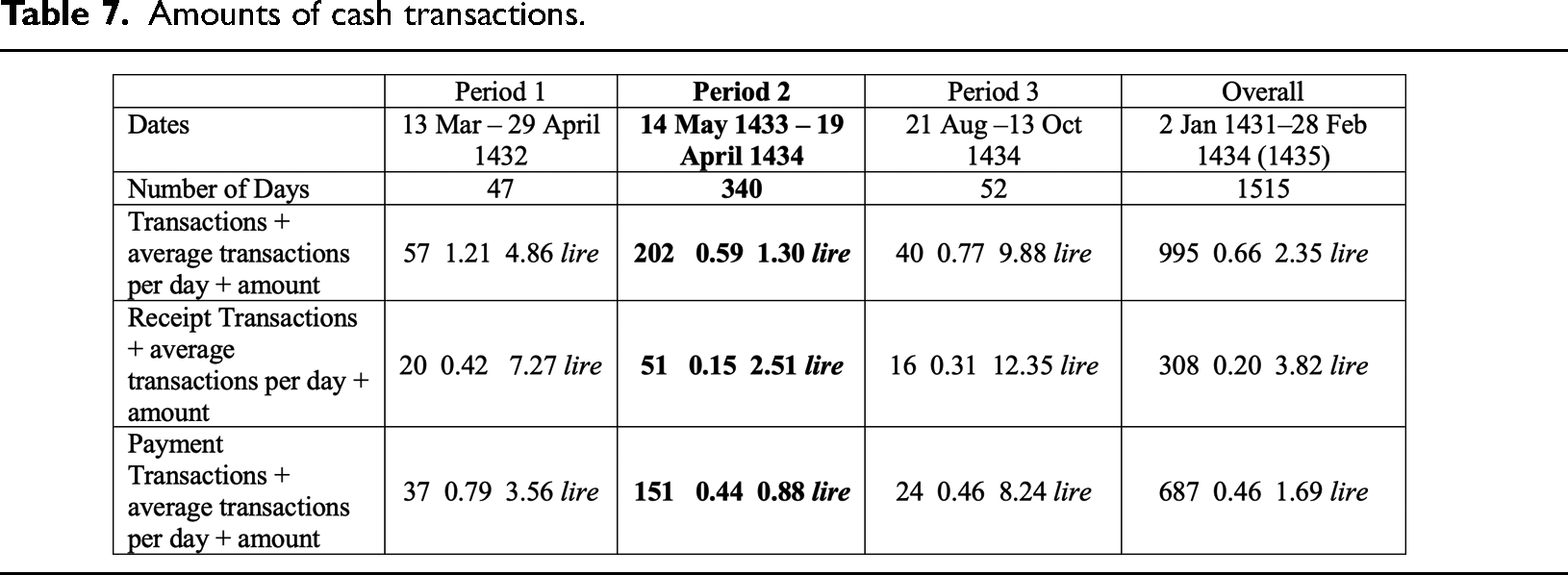

The graph in Figure 3 showed that his cash balance could vary considerably in a very short period, and within the three credit cash balance periods the number of transactions and the amount of each transaction varied, presumably because of a change in the focus of his activity or in how he settled transactions. As shown in Table 7 which provides more detail about the transaction data already discussed, looking at the amount of each cash transaction, the average cash expense in Period 1 was four times that of Period 2, and in Period 3 it was nine times that of Period 2. The average amount of each cash transaction in Period 2 was just over half the average during the entire 50 months, whereas, in Period 1 it was double and, in Period 3 more than four times the average.

Amounts of cash transactions.

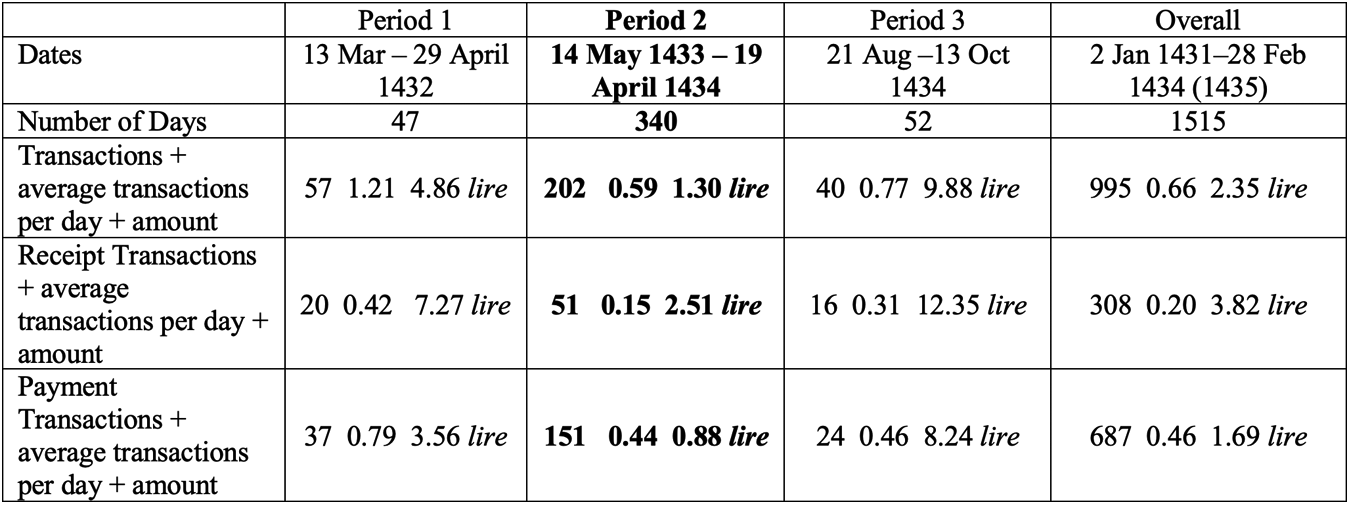

These differences could have arisen because the bank was being used more in Period 2, but Table 8, which summarises the pattern of bank transactions, shows that it was not.

Bank transactions overall (1515 days) versus during periods 1 (47 days), 2 (340 days) and 3 (52 days).

While the average number of daily bank transactions was similar, except in Period 3 when they were much greater, the average bank transaction amount in Period 2 was 39 per cent below the overall average, 35 per cent below the average for Period 1 and 47 per cent below the average for Period 3. Comparing daily transactions per period using the bank compared to cash, the number of bank transactions per day in Period 2 was similar to the number in Period 1 and overall; whereas the number of cash transactions per day in Period 2 was similar to those in Period 3 and overall. On the basis of this analysis of both cash and bank transactions, there is no doubt that Period 2 was a period of smaller value activity. Period 3 appears to be a period of expanding activity, not so much in volume as in value, both in cash and through the bank.

Another issue relevant to this analysis concerns the journal. Period 2 embraced a two-month period we identified when Barbarigo stopped using the journal from the end of December 1433. As shown on the left in Figure 4, that page in the journal is clearly marked off as discontinued. 12

Final journal entries on 30 December 1433 on the left and the sign indicating discontinuation of its use.

Discussion

This analysis, including the two-month cessation of use of the journal, supports our first impression of Period 2 when we created the graph shown in Figure 3: that it appears to be one in which the business was winding down. Barbarigo's cessation of the journal could be interpreted as indicating he had decided to focus on retail trade for which there was no legal expectation of use of a journal, or even wind-down his business altogether. It seems implausible that he could have switched from cash and bank settlement and used instead credit from suppliers to fund his activities for almost a year. Apart from the difficulties a relatively minor wholesale merchant would have had in doing so, especially one still building his network and business, his cessation of use of the journal refutes that possibility because it was the primary account book in the eyes of the Venetian state in the event of a dispute (Antinori, 2004). Andrea Barbarigo, by training and profession an advocate who acted for the Venetian state in tribunals concerning mercantile disputes (Lane, 1944), would have been well aware of the law.

Assuming that he did not switch to reliance on supplier credit during Period 2, it seems plausible that he lost enthusiasm for the wholesale side of his business around the time he discovered the cash account had a credit balance in late May 1433. He then began to focus more on retail trade (with its much lower volumes and potential profits) and decided at the end of December 1433 that he would switch to retail permanently, so stopped using his journal; but, during the next two months, he had a change of heart and began to start to slowly recover his cash position. In August 1434, he resolved to put all his effort into restarting his wholesale trade, which led to the explosion in average cash and bank transaction amounts in Period 3. Whether or not this conclusion is supported by the rest of Barbarigo's ledger is the focus of future research.

Two final issues to consider are the existence of credit balances on Barbarigo's cash account and the closure of his ledger before it was full.

The credit balances

If the credit balances on the cash account were bookkeeping errors, Barbarigo never found them. Nor did we find any that explained the credit balances when we checked the entries both for cash and for bank, and the transfers between them. Discussing Barbarigo's business ten years later, in 1442, Frederic C. Lane suggested he had run out of ‘pocket money’ when he pawned a ring to raise 10 ducats (Lane, 1944: 29). But, the concept of a Venetian wholesale merchant having some pocket money stashed away does not resonate with an approach to business that involved recording all possessions in the ledger (Pacioli, 1494). Although difficult to be precise, the largest confirmed credit cash balance of 37.47 lire or 374.7 ducats was equivalent to the combined median annual salary of seven university professors in late fifteenth-century Italy (Sangster, 2007: 132) or 25 times the annual salary of the bookkeeper of a Venetian charity in 1518 (Lusiani et al., 2023: 7). In either case, it was a considerable amount of money to have at home under a floorboard or a mattress.

Barbarigo's reaction – the asterisk he drew in the ledger – when he discovered the credit balance indicated that he did not believe it was possible, which means he must have had cash at that time, and every other time he balanced the account as well, if for no reason other than it is impossible to have a credit balance on a cash account other than by mistake. He did have at least 37.47 lire more cash than his ledger account indicated in April 1432; still had at least 35.47 lire more in February 1433; and at least 34 lire more in September 1434. Assuming he kept as little cash as possible, this would suggest he had, perhaps, as much as 40 lire more in cash than was recorded in his cash account.

It is possible that he posted a receipt of that amount to a different account in error, but we have not found any errors of that type. Delays in posting entries from the journal to the ledger could explain something of this nature that lasted a few days, but not two that lasted several weeks, and another that lasted almost a year. His bank account was never more than 1 lire out of balance, and that would have been checked with the bank's own record. Our comparison of the transfers between cash and his bank found no discrepancies, which indicates that he did not forget to enter a transfer of cash to himself from his bank account, or vice-versa. On balance, he most likely forgot to record a cash sale or a refund from a supplier, or perhaps, a cash receipt from an agent. But, would he not have been reminded about such a large amount when he discovered his cash account had a credit balance?

Perhaps there is another explanation: fifteenth-century Venetian wholesale merchants are believed to have recorded all their possessions in their ledger. If their business subsequently went bankrupt, tribunals would have used their accounts to identify available resources, leaving the merchant penniless. That risk may be why Barbarigo never purchased his home, though his wife did so soon after his death (Lane, 1944: 21, 34). For the same reason, could he have also kept a secret reserve of cash? He never reconciled his cash balance in the ledger to the cash he held. Perhaps the asterisk he noted against the credit balance was his reaction to realising that he no longer had as much in his secret cash reserve as he had hoped.

Perhaps further investigation of the ledger will reveal something both Barbarigo and this research team have overlooked. Until then, on this point, we can only speculate.

Closure of the ledger before it was full

As mentioned at the beginning of this article, Barbarigo is the only fifteenth-century Venetian wholesale merchant known to have closed his ledger before it was full. And it was immediately re-opened. It has been speculated elsewhere (Lane, 1944: 174) that he closed it at that time in order to assess his wealth prior to marriage. Whether or not that was the case, it was only in 1439 that he married. The five years that passed between the two events may suggest that he did not believe he was sufficiently wealthy in 1434, but this is inconsistent with his subsequent failure to again close the ledger before he married, only doing so in 1440. However, the temporary cessation of the journal at the end of December 1433 may be connected to it.

Barbarigo restarted using the journal two months later, on 6th March 1434, effectively at the beginning of the Venetian New Year. He kept it and the ledger open for 12 months, until the end of that Venetian calendar year. During those two months without a journal, his business had continued and he made no fewer entries in his cash account than would have been expected in any two-month period. If, as suggested above, he had decided to move away from wholesale trade and focus on retail, but, after two months, decided to try again, he may have given himself another year as a wholesale merchant, and then looked at where he stood. This would explain why he started to use the journal again and why he closed the half-full ledger, at the end of February one year later. When he did, only five entries had been written on the page he was using in the journal. Unlike what he did when he temporarily ceased using it, this time he did not score out the rest of the page. Instead, he left it blank and made the next entry, which was on 3rd March 1435, at the top of the next page. Assuming this is what motivated him to close the ledger when it was only half-full, what he saw when he prepared his bilancio must have satisfied him that he was doing well.

An alternative explanation for this temporary closure of the ledger, supported by the meticulous approach he took when checking every entry, evident in the markings in his ledger, may have been that he wanted to ensure his bookkeeping was sound, particularly as he had been aware for 19 months that there was a problem with his cash account. This would be very plausible. His bookkeeping was very much that of someone learning to perfect the application of the method. Someone who, from time to time, forgot to follow the tenets of the method; who occasionally found it difficult to sum the amounts on kartas; who endeavoured to identify and correct all errors, but never quite managed to do so; and accepted the ‘truth’ in personal accounts when they varied from his record in his account for cash, even when the original details recorded in his journal indicated that the different amount entered in his cash account was correct. It would not be surprising if this were why he decided to close his ledger temporarily after 50 months, but it is unlikely the reason will ever be confirmed unless someone discovers some previously unidentified records in the Venetian archives. That may seem improbable, but over 160 previously unknown medieval account books were discovered there in 2022. 13 On balance, it seems most likely that he was motivated to close the ledger by a combination of these two explanations, rather than either one on its own.

Finally

This article contributes on two main fronts. Firstly, in its presentation and description of a new digital research methodology that can be utilised by anyone with an interest in exploring beneath the numbers of archival account books of any period; and secondly, by the confirmation of its usefulness in the unexpected findings reported in this article only identifiable because the digital research methodology described here was adopted, presenting the journal and ledger in a way never previously attempted or achieved.

The analysis conducted in the study reported here was only possible by embracing that digital methodology. Doing so made achievable in less than three months which our experience of over a decade working manually in Italian medieval archives tells us would otherwise have taken many more months, if not years of effort. It would have been virtually impossible to conduct this analysis by hand, which is one reason that it has not been done previously, despite this journal and ledger having been extensively studied, especially by Frederic C. Lane, but also, far more superficially and on a far lesser scale, by accounting historians including Alfieri (1891), Besta (1916), De Roover (1946), Zerbi (1952) and Martinelli (1974). A similar digital methodology can be adopted with any account book, and there are over 3,000 in Florence alone from before 1500, any of which could reveal facets of medieval business, bookkeeping and accounting that have not previously been identified.

However, it is perhaps the Venetian archive that would be most informative. From what Pacioli wrote about it in 1494, it is known how the Venetian paired libro doppio bookkeeping system embracing the journal with its ledger operated in theory. But, no one has studied to such a detailed extent as this how consistently the other surviving medieval Venetian account books adhere to that approach. Andrea Barbarigo presents a surprising exception with his two-month temporary abandonment of the journal. Others may have done so too, but for other reasons. Future research adopting a digital methodology such as ours would be well-equipped to find out.

In closing, some might argue that adopting this digital methodology is prone to human interpretations and errors, but we would argue that if done with care and appropriately checked there is no reason why doing so should be open to errors and misinterpretation any more than if an analogue manual approach were adopted, or anything in-between; and, to the heart of the benefits of this methodology, recording data in account books digitally offers all the power of the software to locate errors, conduct analytical routines, interrogate the data and generate reports automatically on a scale and complexity that a manual methodology could never match.