Abstract

A special issue of an academic journal is a collection of scholarly articles on a specific topic within the journal's scope. Special issues could take the form of an entire issue or a themed section of an issue. These issues provide a venue for research on emerging areas, highlight important subdisciplines, or describe new cross-disciplinary applications. While literature about the special issues of accounting journals tends to emphasise the research developments in the designated fields, this contribution uses reflexivity to develop a broader discourse about the role and the phases of development of a special issue, through the eyes of the scholars directly involved. It explores our ‘behind-the-scenes’ work as guest editors, our individual perspectives on the challenges and advantages of editing a special issue for us as guest editors, the authors, the journal's editors, and the research community represented by the journal of reference, in influencing public opinion and promoting critical thinking.

Introduction

Special issues (sometimes referred to as thematic issues) of academic journals are collections of academic articles on a specific topic within the scope of the journal. Special issues could take the form of an entire issue or a themed section of an issue. Carnegie (2012: 216), following Olk and Griffith (2004) (who themselves followed Fleck, 1979) used the military metaphor of the vanguard to suggest that special issues have the ability to represent the ‘advance guard’ of research, by both ‘stimulat[ing] research in little developed or emerging fields’ and ‘stimulat[ing] and illuminat[ing] path-breaking directions on more developed themes that may not have been otherwise initiated’. The publishers of Accounting History encourage their journal editors to publish special issues as ‘a great way to focus attention on a hot topic’ (SAGE Publishing, 2023). Although scepticism has been expressed with respect to the desirability of frequent special issues in the management field (Priem, 2006), there is a strong view that, at least within accounting, ‘innovative special issues … have often created new and exciting research fields’ (Carnegie and Napier, 2017: 1662).

In some cases, special issues (or identified thematic sections of individual issues) are put together by the main editors of a journal from regular submissions that happen to address a common theme. The editors may provide an introductory commentary on the articles included in the thematic issue or section, commission a commentary from independent scholars, or simply include a title page identifying the special issue or section. However, many publishers (including SAGE – see SAGE Publishing, 2023) encourage journal editors to appoint guest editors with responsibility for specific special issues. Such appointments may represent initiatives on the part of the main editors, who identify a topic and then seek appropriate guest editors, or they may reflect proposals from potential guest editors. Even without specific guest editors, there may be a ‘Call for Papers’ (CFP) soliciting submissions on a circumscribed theme. In some cases, special issues may be linked to conferences or workshops, where articles presented at the event may be developed for publication in a designated issue of a journal.

Special issues bring unique perspectives to thought in the field, by pushing the boundaries of the discipline, ‘path-breaking’ and encouraging ‘new fields of research’ (Guthrie and Parker, 2012: 17), which may mean ‘moving into new areas, addressing neglected subjects, challenging conventional wisdom and signalling important research directions for scholars’ (Guthrie and Parker, 2017: 4).

Special issues in the accounting literature have been analysed mainly in terms of their contribution to the research development in designated fields (Carnegie, 2012, 2019a; Carnegie and Napier, 2017) with the aim of assessing their impact and progression. However, a comprehensive understanding of their standing in the journal's publication and dissemination strategy should include the reflections of journal editors about their visions and guest editors’ hands-on narratives regarding the development of special issues and their own behind-the-scenes experience. That is why the unique self-reflection, presented in the following sections of this article, will be referred to as the collective voice (‘we’/‘our’/‘ours’) of the Accounting History guest editors contributing to this article. Beattie and Davison (2015: 655) attribute an important role to narratives and, within narratives, to storytelling (see also Boje, 2008; Smith et al., 2010). They highlight how autoethnographic narrative as a source material ‘had previously been relatively or entirely neglected’ (Beattie and Davison, 2015: 655) although storytelling ‘is a specific narrative form of particular significance because stories help people make sense of events’ (Beattie and Davison, 2015: 655). Haynes (2011, 2017) adds that autoethnography should be regarded as both a process and the output of research where the researchers (us, as guest editors in this case) form the subjects of lived enquiry in their specific context.

Careful attention is devoted by editors-in-chief of accounting journals to the choice of topics and guest editors. For example, the editors of the Accounting, Auditing & Accountability Journal (AAAJ) have observed: ‘We typically appoint guest editors three to four years in advance of a theme issue publication date. They undertake significant and lengthy preparation from the design of the theme issue concept right through to the CFP, the reviewing process and final publication. It is a ‘rigorous, challenging and lengthy process’ (Guthrie and Parker, 2012: 17). The ‘Meeting the editors of… Accounting, Auditing & Accountability Journal’ interview of Lee Parker and James Guthrie (2009) uncovers the reflexivity and engagement that accompany the editorship ‘risks’ of undertaking a special issue: ‘In addition, we have been prepared to innovate, to take risks, to experiment with new “breaking” subject areas, experimental formats and special theme issues’. However, this reflexivity and explicit narrative sentiment rarely emerge in journal articles or other forms of publication. Exceptions include Gendron's (2018) sensemaking of ‘The elusive nature of critical (accounting) research’ and Guthrie et al.'s (2004) contribution to The Real Life Guide to Accounting Research.

Contributing to a special issue, whether as a guest editor or as an author, may provide advantages, namely:

Intellectual direction: the special issue provides an opportunity to influence how people think about a topic, by defining the scope of the special issue, contributing an editorial or a positioning article to the special issue as a guest editor, and by submitting contributions that align with the special issue topic as an author. Exposure: the special issue associates the names of the guest editor and the contributors with the topic in the minds of the wider scholarly community. Readership: articles from the special issue will continue to be read for many years, and there is evidence that articles from special issues tend to be more widely cited than articles from normal issues (SAGE Publishing, 2023). Academic experience: guest editing a special issue may contribute to career progression.

While these aspects represent outputs and outcomes that contribute to the long-run impact of a special issue, this article aims to shed light on the factors that contribute to the success in the sense that a proposed special issue ultimately materialises in published form, from the viewpoint and experience of guest editors.

We aim to enhance a broader narrative about the role and the phases of development of a special issue, through our eyes and our narrated experience as scholars directly involved. We explore our ‘behind-the-scenes’ work as guest editors, our individual perspectives on the challenges and advantages of a special issue for prospective guest editors, and our perception of the authors, journal editors, and research community represented by the journal of reference, in influencing public opinion, and promoting critical thinking. This contribution is therefore based on our individual experience as guest editors of special issues that have appeared in Accounting History and on the panel discussion ‘What makes special a special issue?’ that ensued at the 11th Accounting History International Conference (AHIC) in Portsmouth, UK, 6–9 September 2022.

This article develops as follows: the next section provides the historical context and retrospective of the special issues published in Accounting History as a background to their role in broadening the reach and scope of the journal. The methodological choices, with specific reference to the storytelling narrative and autoethnography perspective utilised for this article, are then presented. We have devoted specific reflections to the trade-offs to be considered when elaborating a topic for a special issue, followed by our actual conception of topics tied to the enhancement of an existing debate within the journal, a new stream of research or an AHIC. That section is followed by our perception of quality and scientific rigour, our relationship with the journal editors and the overall opportunities offered by the special issue after release. A concluding section summarises rather than re-theorises the contribution of this article.

The historical context of special issues in Accounting History

The scholarly study of the history of accounting has benefited over the past 40 years from several special thematic issues of important generalist journals, which have helped to create and develop a distinct research agenda for the field. Anthony Hopwood, as founder and editor-in-chief of Accounting, Organizations and Society (AOS), encouraged new approaches to historical accounting research and supported this by compiling several special issues or sections. The first of these was the special issue ‘Accounting, Knowledge, Power’ (1986). A subsequent special issue was compiled from articles originally presented at the second Interdisciplinary Perspectives on Accounting Conference (Manchester, 1988), with the title ‘The New Accounting History’ (1991). Hopwood invited the organisers of the conference to write an introduction to the special issue (Miller et al., 1991), and this issue is often regarded as the catalyst for the ‘new accounting history’ approach (Bertalan and Napier, 2016; see also Edwards, 2023). Hopwood followed up this special issue with a thematic section ‘Accounting, Calculation and Institutions: Historical Studies’ (1993). Among the articles in this section was the influential agenda-setting article ‘Genealogies of calculation’ (Miller and Napier, 1993).

Although Hopwood tended to avoid guest editors in AOS, the special issues of AAAJ from the beginning used guest editors. As Carnegie (2012, 2019a) has observed, the founding editors of AAAJ, Lee Parker and James Guthrie, saw special issues as one of their key strategies for enhancing the reputation of the journal and expanding innovative scholarship in the field of accounting. The first special issue of AAAJ to address historical approaches to accounting research was ‘Accounting History into the Twenty-first Century’ (1996), which was co-edited by Christopher Napier and Garry Carnegie. This contained another important agenda-setting article ‘Critical and interpretive histories’ (Carnegie and Napier, 1996) and a further five diverse studies.

The AAAJ special issue appeared alongside the first issue of the relaunched journal Accounting History, under the editorship of Garry Carnegie. With the experience of the AAAJ special issue behind him, Carnegie considered that special issues, with invited guest editors, could play a key role in enhancing the new journal. Christopher Napier proposed a special issue ‘Accounting, Regulation and Law in Historical Perspective’ for publication in 1998. This would coincide with the fiftieth anniversary of the Companies Act 1948, which revolutionised financial reporting and auditing in the United Kingdom and was highly influential for accounting regulation throughout the Commonwealth. Understanding the historical development of regulation was one of Napier's central research interests at the time (see, e.g., Napier, 1995, 1998; Napier and Noke, 1992). As well as a CFP in the second issue of the journal (November 1996), Napier contacted various scholars who were interested in historical accounting research and were working on issues related to the regulation of accounting, and the special issue appeared as volume 3, issue 1 in May 1998. Napier supplied a brief editorial introduction, and the special issue contained five substantive articles.

The next special issue of Accounting History, ‘Accounting in Crises’, was stimulated by the 1997 Asian financial crisis (see, e.g., Haggard, 2000). The guest editor, Stephen Walker, assembled a special issue (volume 5, issue 2, November 2000) containing contributions covering crises in the nineteenth and twentieth centuries across a range of countries, illustrating how accounting could be involved in both managing ongoing crises and enhancing subsequent regulation. There have been over 20 subsequent special issues in Accounting History, and those published until 2023 are listed in Appendix 1. Most of these special issues have been initiated by proposals from prospective guest editors, who, in conjunction with the editors of Accounting History, have developed a CFP. This is published in the journal and often circulated to members of the Accounting and Finance Association of Australia and New Zealand's Accounting History Special Interest Group and other subscribers via social media.

As well as encouraging special issues, Carnegie (2019b: 526) also saw the establishment of ‘journal-associated international conferences, colloquia and symposia’ as ‘a key strategy in developing the international orientation and standing of the journal’. The first AHIC was held in Melbourne in 1999. For the fifth AHIC, which took place in Banff in 2007, there was an identified theme, ‘Accounting in Other Places, Accounting by Other Peoples’, and the CFP for the conference mentioned that the conference convenor, Nola Buhr, would be guest editor for a special issue including articles falling within the conference theme. This was published in 2009 as the journal's first double issue, reflecting the interest in the theme and high quality of submissions to the conference. Since then, each AHIC has led to a special issue on that conference's theme, with the conference convenors typically acting as guest editors.

In addition to special issues on topics proposed by potential guest editors and special issues emerging from AHIC events, one special issue was in effect a compilation of submissions already under review by the journal and did not involve a specific CFP. This was the special issue ‘Perspectives and Reflections on Accounting's Past in Europe’, published in 2009, and guest-edited by Elena Giovannoni and Angelo Riccaboni. This special issue was unusual for Accounting History in having a geographical theme, although issues studying accounting's history in specific countries were frequently published by Accounting, Business & Financial History (Edwards, 2023). The guest editors provided a lengthy introductory article (Giovannoni and Riccaboni, 2009), which reviewed in detail the geographical coverage of articles in specialist English-language accounting history journals in the period 2005–2008. The issue itself contained studies examining accounting from a historical perspective in Finland, Italy, Portugal, Romania and Russia.

The importance of special issues for Accounting History in broadening out the research field and encouraging both new and more established researchers, often from non-Anglophone countries, has been recognised in several retrospective reviews. Bisman (2012), surveying the first 15 years of the journal, commented on how special issues can be used by the journal's editors to help in directing research into new areas, while Fowler and Keeper (2016), looking back over the journal's first 20 years, suggested that special issues were important in widening the range of potential contributors. Special issues of Accounting History providing opportunities for research in areas such as sport (2016) and entertainment (2021) have helped to emphasise how accounting operates as a wide social practice rather than being limited to more conventional business, government and not-for-profit settings. Special issues can also encourage research that revisits well-established fields to provide new insights. A good example of this was the special issue ‘The Emergence of Accounting as a Global Profession’ (2014), guest-edited by Paul Miranti, which reflected recent developments in thinking theoretically about the process of professionalisation and the diverse forms in which accounting has become a profession around the world.

The rest of this article addresses the challenges we face as guest editors in preparing an effective special issue of Accounting History, from the development of the original idea and CFP, through encouraging submissions, to ensuring quality. The role of a special issue does not end with publication. We consider how special issues can have longer-term impacts on the accounting history research community and more broadly. The article is based on our experiences as guest editors, journal editors, contributors to special issues and conference organisers for Accounting History and other journals over many years. In the next section of the article we explain the methodological choices underpinning the present contribution.

Our methodological choices

Our article builds on the lived experiences of guest editors of special issues in Accounting History, therefore enabling ‘the researchers themselves to form a subject of lived inquiry within the context of accounting and its environs’ (Haynes, 2017: 215). In this respect, we can consider that the article builds on narratives and storytelling. Beattie and Davison (2015) refer to storytelling (see also Eshraghi and Taffler, 2015; Gabriel, 2000) as a specific form of narrative (Boje, 2008: 1) in which stories are a ‘key part of members sensemaking’ and a means to allow them to ‘supplement individual memories’.

Current literature in accounting offers examples of storytelling in accounting education studies (Freeman and Burkette, 2019; Miley, 2009; Suwardy et al., 2013; Taylor et al., 2018), and with reference to data visualisation and rhetorical analysis of accounting and accounts (El-Wakeel et al., 2020; Reiter, 1997; Smith, 2011; Smith et al., 2010). Other examples can be found in the accounting history field (Cronon, 2013; Funnell, 1998; Haynes, 2012; McWatters and Lemarchand, 2010). Autoethnographic storytelling (Gabriel, 2000; Weick, 1995) is a genre that helps people to make sense of events by using the premise that ‘knowledge about the social and human world cannot exist independent of the knower; that we cannot know or tell anything without (in some way) being involved and implicated in the knowing and the telling’ (Douglas and Carless, 2013: 84). Furthermore, storytelling can ‘capitalise on one of the unique opportunities that autoethnography provides: to learn about the general – the social, cultural and political – through an exploration of the personal’ (Douglas and Carless, 2013: 84–85). Jones (2005: 765) suggests that ‘autoethnography is setting a scene, telling a story, weaving intricate connections among life … experience and theory … hoping for readers who will bring the same careful attention to your words in the context of their own lives’.

We follow the counsel of Douglas and Carless (2013: 85) by sharing stories from key aspects of our own histories of guest editors of Accounting History. These ‘stories’ relate to key choices of guest editing a special issue, namely (1) choice of topics, by balancing trade-offs typical of the field; (2) development of the special issue, depending on its origin and specific challenges; (3) quality rigour; (4) benefits emerging after publication. In recalling these moments in the life-cycle of our guest editors’ role, we are motivated by (a) an initial sense or awareness that something was missing from the academic writings and communications we were studying and accessing, namely a storytelling autoethnographic approach to journal special issues; (b) the opportunity to build on our significant exposure or encounter with special issues in Accounting History as guest editors; (c) thus, the possibility of offering to our community an informed view of the practical steps, and ethical challenges that can arise in developing a special issue. This storytelling is ethnographic in the sense that it concerns the representation of our identity as scholars and our reflections, in the context of the guest editorship of Accounting History special issues. Where appropriate, we have put our experiences as guest editors for Accounting History into the context of our work as journal editors and guest editors of other journals.

Haynes (2017) outlines how autoethnography is both a research process and a product of research. The autoethnographic storytelling presented in the current article is based on our lived experiences that cover various periods of time, therefore we acknowledge that it is partial, situated, and incomplete. Nonetheless, it provides a starting place to consider how and why special issues are developed while recognising the kind of challenges and rewards they have, that other prospective guest editors are likely to experience.

Therefore, this article provides a kind of journey through the life cycle of special issues as experienced by guest editors. We hold fast to the conviction that evoking the personal can illuminate the general (Haynes, 2011), and we hope that our storytelling will resonate in some way with readers, and perhaps chime with their own experience. Therefore, we use the ‘we’ voice in the representation of what we understand as ‘being in charge of’ and ‘dealing with’ a special issue, how we relate to sensitive subjects such as journal editors, authors and reviewers, and how we cope with sensitive questions of validity and quality of our special issues, linking these matters with our own subjectivity, while engaging a form of collective authorship. These concerns, and several concrete issues in the presentation and representation of our perspectives, are covered in this article. Emotions are revealed in narratives of memoirs associated with both the conception and the development of a special issue, and relationships that emerged as a consequence.

Haynes (2011: 135) points out: ‘We identify with our work through the use of personal experience and intellectual ownership, and we are identified with our work through … others’. The present article builds on that, by extending our ‘editorial’ self in the context of our own special issues: setting an editorial agenda, designing avenues for future research, and acting as a filter of knowledge in line with the objectives negotiated with the journal editors. As a result, this article is ‘a personal, intuitive knowledge deriving from a knowing subject situated in a specific social context’ (Haynes, 2011: 134). The social context of editing a special issue includes a specific group of peers (authors and reviewers), a shared culture (based on the interest already existing and newly stimulated in the topic), and, at the same time, a dialogical and evaluative culture inherent to the reviewing process.

The panel discussion ‘What makes special a special issue?’ that ensued at the 11th AHIC in Portsmouth, UK, 6–9 September 2022, was preceded by a formal selection by the journal editors of potential guest editors who were likely to be able to participate in person at the conference, which was the first AHIC conference following the COVID-19 pandemic restrictions. We held individual and group online conversations in preparation for the panel discussion, which originally involved a larger group of willing participants, some of whom had to pull out, owing to subsequent issues with travel and other arrangements. The informal online conversations helped us to finalise the line of questioning of the panel chair, to be followed during the panel discussion and to ascertain our preferences as guest editors for sharing some of our own experiences. We loosely drove these conversations based on the chronological development of a special issue.

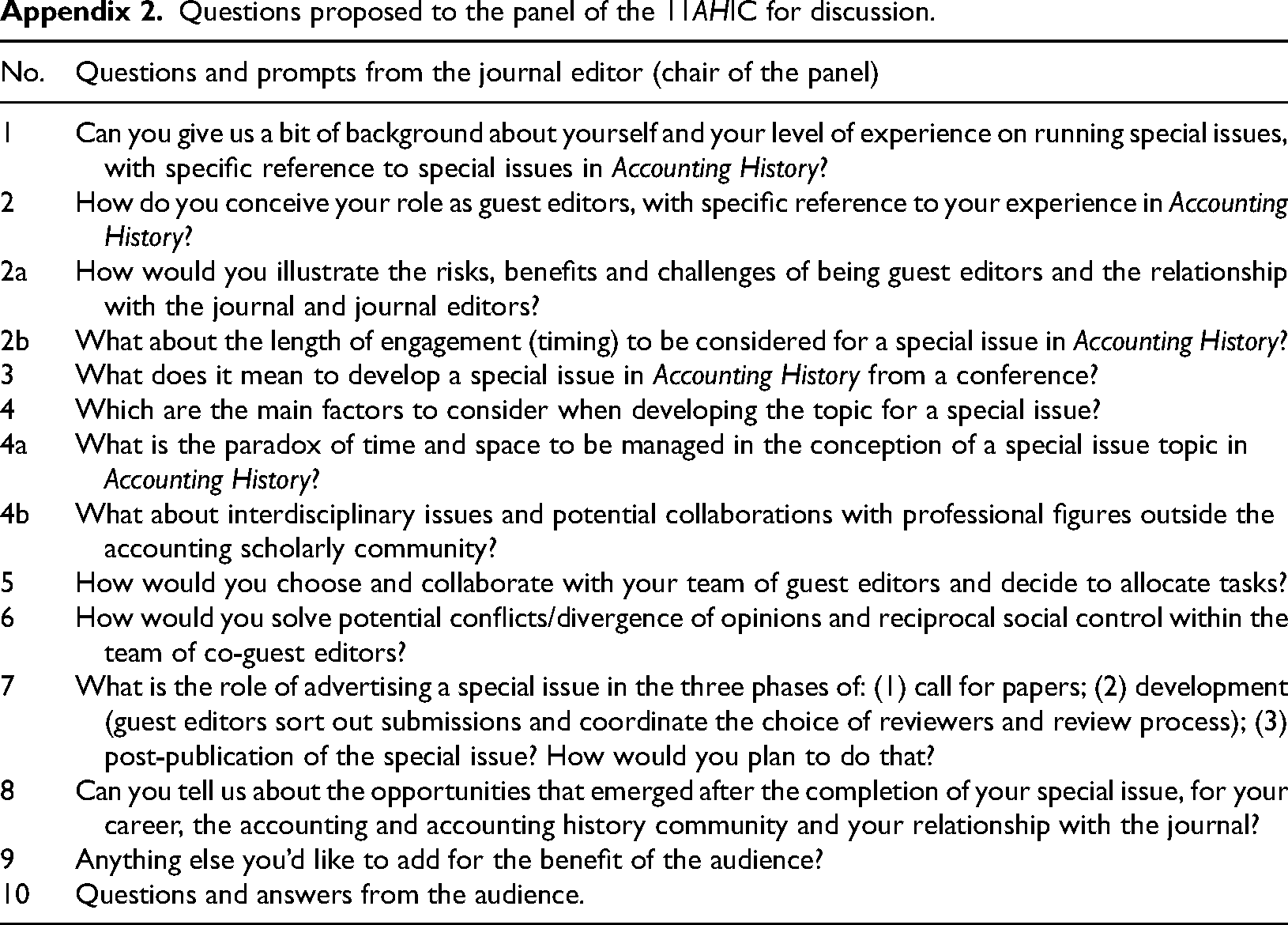

Meanwhile, we noticed that several remarks emerged in terms of how the special issue topic related to our personal histories, our style of working with co-guest editors, our level of seniority, networking, and experience in the field, our personal strategies for dealing with quality issues while maintaining a gatekeeper role, and our perceived long-term outcomes of developing a special issue from a conference. We took handwritten notes during these conversations (instead of recording and transcribing them), given the sensitivity of these insights for the publishing and dissemination strategy of the journal, and for the depth of personal information and emotions we shared. Taking notes ensured that we felt more open to sharing our experiences. We transcribed the notes into a Word document and their systemisation drove the round-table questions from the live panel chair, as illustrated in Appendix 2. Our face-to-face panel conversation and interaction with the audience during the conference, together with later online meetings and communication exchanges, provided further basis for the present article.

Trade-offs in choosing topics for special issues in Accounting History

Conceptualising a special issue

We believe that the conceptualisation of a special issue implies that its topic is conceived having in mind the community of reference of a particular journal. That community is represented by scholars who publish, review and refer to a certain journal for their research. Our goal as guest editors is to stimulate creativity and disseminate new culture (Olk and Griffith, 2004: 120) through the special issue, by proposing innovative research that otherwise would be overlooked (Priem, 2006: 384). So, the choice of the topic affects the risks and opportunities associated with the success of the special issue.

As guest editors, we must agree on identifying the breadth of the topic within a spectrum of possibilities. On the one hand, a special issue may be intended to deepen a specific topic, by stimulating innovation in the scientific community that refers to the topic and by encouraging researchers to look far ahead (Carnegie, 2019b: 528). In turn, this enhances the reputation of the journal, especially when it targets a niche of scholars (Priem, 2006: 388). On the other hand, the potential constraint of a specific topic means that there might not be a sizable community with the will and capacity to create a sufficient critical mass of potential publications. This is especially so when any related sources must be identified and data must be newly collected, which may be perceived to require a disproportionate effort towards the development of a contribution for the special issue with respect to the specified deadline.

The choice of the topic for a special issue is reflected here in relation to the breadth and size of the community of reference to which the special issue is addressed. Our reasoning includes two conditions: (a) the number of scholars potentially interested in the special issue, which refers to scholars who usually deal with a particular field of research and represent the usual readers of the journal; and (b) the opportunity to stimulate a debate that includes other scholars, whose research interests may be close to or relatively more distant from the interests of the scholars traditionally involved with that journal. This opportunity often gives rise to interdisciplinary research (Baskerville et al., 2017). Even if the exact breadth and size of the interested community for a special issue is not easily detected, we acknowledge that the community of active scholars in accounting history is a relatively small subset of the broader accounting research community, to say nothing of scholars located in other disciplines who may potentially be interested in the topic of a special issue.

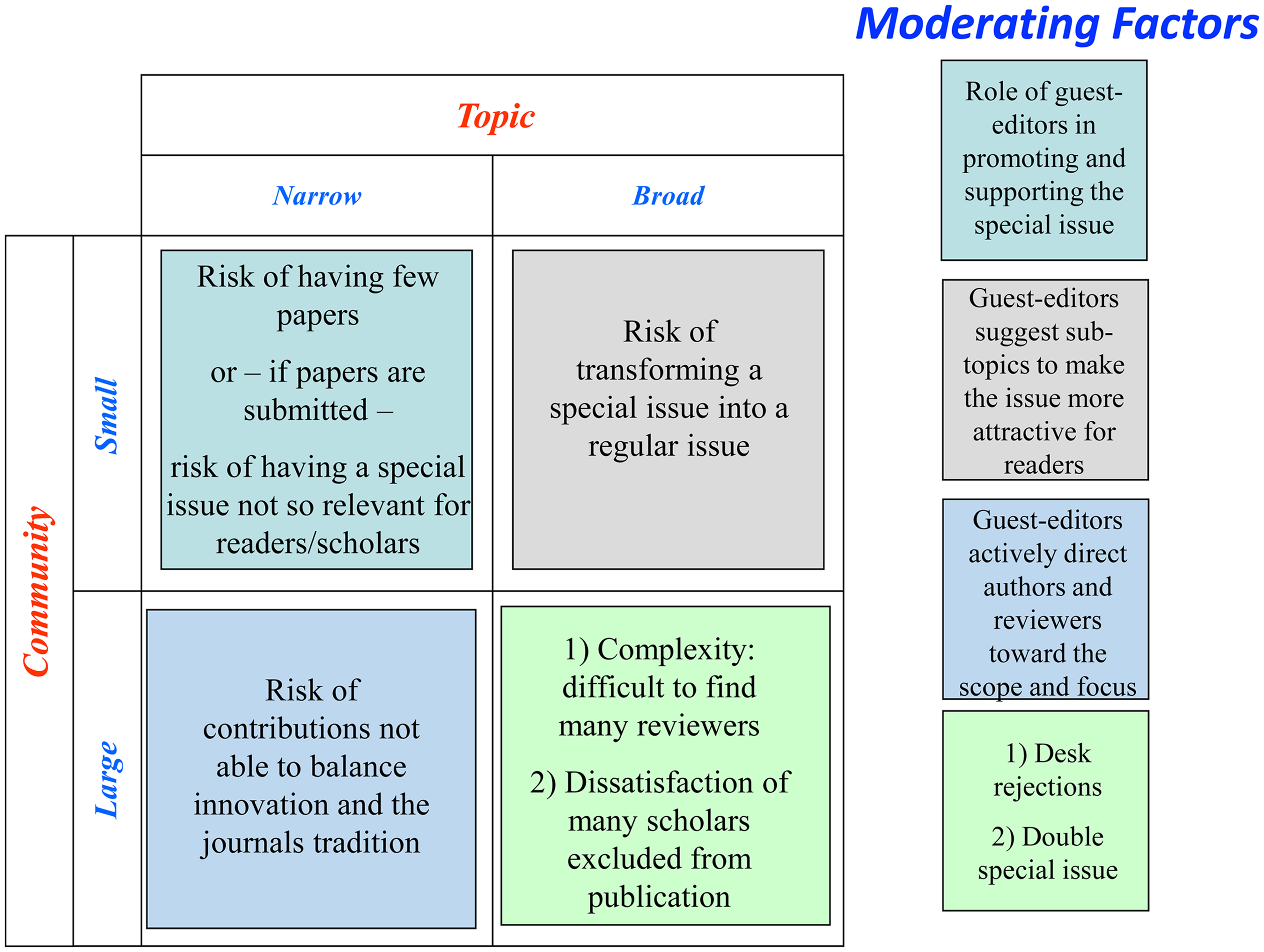

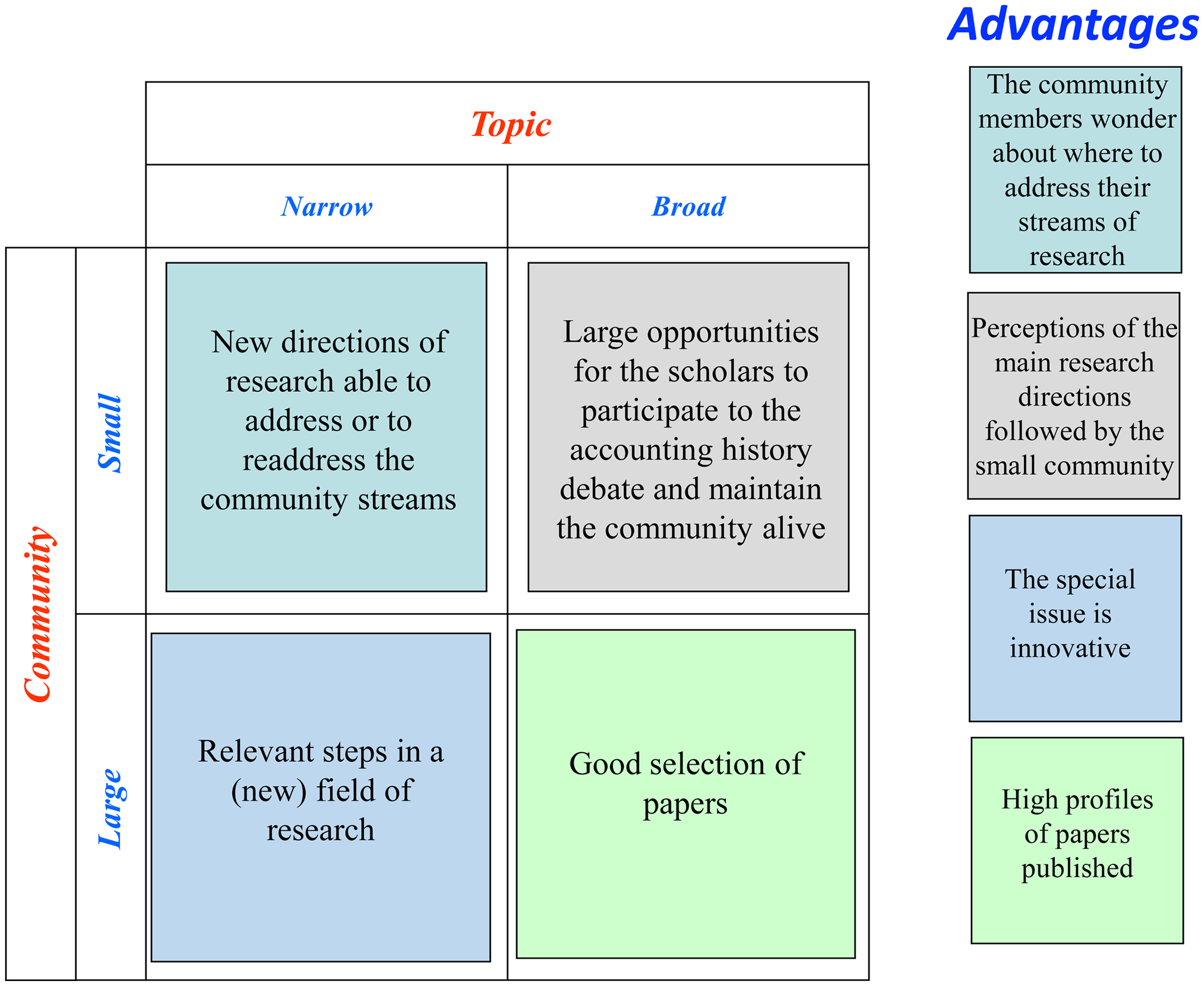

The identification of risks and opportunities of a special issue

We explain the identification of the risks and opportunities related to the combination of the topic (narrow or broad) and the breadth and size of the community (small/specialist or large/generalist) through two matrices: Figures 1 and 2, respectively. In developing these figures, we have drawn on our scholarly knowledge of both specialist and generalist journals, both of which may publish research in accounting history. The narrow/broad distinction relates to how tightly focused the topic of the special issue is, as demonstrated through the examples that follow. In distinguishing small and large communities of scholars who may be interested in a special issue, we consider that the overall accounting history community is small by reference to all accounting researchers, and we acknowledge that, within the accounting history community, there may be smaller groups of scholars with interests in specific topics. For example, some accounting historians may focus on financial reporting, others on decision-making within organisations, and others on the emergence of the accounting profession, to give just three examples.

Special issue risks.

Special issue opportunities.

The first, top-left quadrant of both matrices reflects situations in which, as guest editors, we may choose a narrow topic, addressed to a small community of scholars. In these situations, the primary risk borne by guest editors (Figure 1) is that few articles are submitted for the special issue, which may mean that the proposed special issue does not appear. A secondary risk, even for a special issue that successfully emerges, is that it generates only limited interest (as evidenced by the number of downloads and citations), and therefore has only a limited impact on the overall relevance and reputation of the journal. This is just the opposite of the effect a special issue should produce (Carnegie, 2019a: 2204). As a counterbalance to this risk, this situation can offer us the opportunity (Figure 2) to identify new research streams to direct or re-direct the community of scholars towards areas previously neglected or not yet considered. Our effort as guest editors may be focused on continuously promoting and supporting the special issue, as this is a critical factor of success, both during the collection of articles (guest editors may, e.g., approach researchers known to be interested in the topic and encourage submissions) and after publication. An example of a special issue that adopted a quite narrow focus is ‘Accounting's Past in Sport’ (volume 21 issue 1, 2016).

The second, top-right quadrant of both matrices (Figures 1 and 2) refers to a small community of scholars, where we, as guest editors, aim at broadening the boundaries of a topic, to avoid the above-mentioned risks of choosing a narrow topic. The breadth of the topic makes it possible to target all members of the journal's traditional community, and the special issue can be imagined as a sub-topic of one of the traditional intellectual debates that animate the journal. The sub-topic may include areas not immediately considered by those debates or add a new perspective to them, with the aim of making the special issue broader and more attractive to potential submitters. This frequently happens in special issues connected to conferences, to allow for a greater number of scholars to address or re-address their current research to the novel (but still broad) suggested direction and then to develop their new ideas as part of the conference and the special issue. While the risk of this situation is that the special issue becomes like a regular issue (Figure 1), there may be different positive outcomes (Figure 2): the special issue gives a stimulus to the community of scholars who participated to the conference and keeps it lively. Many of the special issues listed in Appendix 1 can be referred to this second quadrant: some of the topics intend to develop the link between accounting history and themes generally explored by accounting scholars, such as ‘Accounting and the State’ (volume 17 issues 1–2, 2012), or ‘The Emergence of Accounting as a Global Profession’ (volume 19, issues 1–2, 2014).

The third, bottom-left quadrant of both matrices (Figures 1 and 2) depicts situations in which a special issue is addressed to a large (generalist) community of scholars but with a narrow topic: such a special issue is probably intended to encourage progress in new but narrow fields of research (Figure 2). It stimulates a large community to compete on specific themes, allowing us, as guest editors, to have a potentially good selection of submissions thanks to the size of the community of reference and the breadth of the community's interests. We are conceived as the gatekeepers of the level of innovation within the narrow topic, but we may continue to receive more traditional submissions, thus facing the risk of an ineffective selection (Figure 1). In these situations, we must actively lead the selection of contributions, being able to balance innovation and the journal's traditions. We would also retain leadership over the direction of these special issues. Through our editorial remarks during the reviewing process, we may specifically direct authors and reviewers towards the scope and focus of the special issue. For example, the special issue ‘Accounting and Accountability in Local Government’ provided an opportunity for researchers of contemporary issues relating to local government to explore their area of interest from a historical perspective.

In the fourth, bottom-right quadrant of both matrices (Figures 1 and 2), we, as guest editors, aim to expand a topic for a large community. While these situations may attract many submissions, we may face the challenge of finding an adequate number of reviewers (without conflicts of interest with the high number of potential authors), especially in the initial phases of the special issue. As guest editors, we need to be sure to draw on an adequate list of potential reviewers, to be selected in a timely manner to ensure effective reviews. During the review process, we may run the risk of dissatisfying a large portion of the research community of reference if the special issue is constrained in terms of the number of articles that can be accepted, and if several articles are not selected (Figure 1). We, as guest editors, may consider the possibility of overcoming space constraints through the proposal of a double-special issue or the possibility of shifting some quality submissions (less pertinent to the special issue) to a regular issue. In these situations, special issues may contribute to and become more like regular issues of the journal (Figure 2). Both the use of a double issue and the inclusion of some submissions to the special issue in regular issues of the journal were seen for ‘Accounting in Other Places, Accounting by Other Peoples’ (volume 14, issues 1–2, 2009). The conference from which this special issue emerged provided an opportunity for researchers in fields such as accounting in emerging economies to adopt a historical approach to a very wide range of topics.

Special issues in Accounting History are more likely than not to fall within the first two quadrants of Figures 1 and 2, as they are likely to be directed mainly to the existing small community of accounting historians or even to more specialist sub-communities. Notwithstanding, accounting history is both a global and a local discipline (Giovannoni and Riccaboni, 2009), meaning that it appeals on an international level while having roots in national (local) traditions. Historical accounting research transcends more typical general research in accounting by paying attention to periods other than the present and has often been ahead of more ‘mainstream’ research in examining accounting in geographical locations beyond the ‘West’ and organisational forms beyond the business corporation. Consequently, the time/space dimension of history plays a relevant role (Lai and Samkin, 2017) in different geographical and cultural regions of the world, and this has been reflected in special issues such as ‘Perspectives and Reflections on Accounting's Past in Europe’ (volume 14, issue 4, 2009) and ‘Accounting History and the Enlightenment’ (volume 24, issue 2, 2019).

The novelty of a special issue

In accounting history, the novelty of a special issue should reflect different settings and perspectives so as to continue disseminating new knowledge while contributing to the diversity of the journal (Carnegie, 2019b: 528). However, given the size and breadth of the international accounting history (specialist) community, it may be challenging to avoid selecting a too narrow topic for a special issue.

As guest editors, we need to be aware of the current or ongoing research on the chosen special issue topic. For a novel topic based on a current debate, it may be appropriate to set a tight submission deadline, so that contributions are more likely to have an immediate impact. On the other hand, a later deadline may allow authors to respond to a fully developed debate. Following the review process, we have also to manage author expectations regarding the degree of novelty of the special issue topic at the time of publication. Special issues may be completed and collated into a publication well after the original submissions are received. In that case, the role of ‘online first’ publication may be useful in bridging this temporal gap and maintaining the novelty and freshness of the topic.

As a result of these reflections, we argue that the breadth and size of the scientific community and the topic of a special issue are somehow inversely related. A special issue in accounting history is ‘special’ because it has a target theme, but it seeks to avoid being too specific (i.e., it does not determine at the same time a specific location, topic and timeframe), so that it has a good probability of success (meaning that it will attract sufficient high-quality submissions, which can be published together as a special issue). Paradoxically, the specificity of a special issue in accounting history may be perceived as a ‘de-specialisation’, for instance, by avoiding constraining the special issue into relatively short timeframes. This speaks to why a special issue linked to a conference may have a broad topic, potentially attracting a critical mass of submissions, and thus paving the way for the subsequent success of the special issue. The next section of the article considers how a good special issue topic may be developed by potential guest editors.

How to develop a good special issue topic

Under-researched areas

We believe that identifying under-researched areas is not difficult for an experienced researcher, especially one who attends conferences regularly. They can see the opportunities, the developing areas, the new ideas. If they read widely enough, they can see what is happening in related fields like economic, business and management history, as well as wider fields such as Renaissance studies, and find themes that would work well in an accounting context.

What comes next is more difficult. The editors of the journal need to be convinced but, more important still, a co-guest editor might be needed, who is similarly interested in the theme; and, while having only one guest editor involved has often proven successful, as with authorship, the role is arguably enhanced by the addition of a second or a third person. It also offers an opportunity for an experienced scholar to mentor and develop the skills and knowledge of someone less experienced. For the journal editors, it is the idea that is important, not who does the legwork of putting the special issue together. But the CFP cannot be finalised until all the guest editors are on board. We suggest that teams of guest editors work best if the team is decided before the proposal is received by the journal editors. In an under-researched area, finding a second guest editor should be easy for established researchers with well-developed networks, but is more of a challenge for those without that experience. For the latter, an approach to the editors may be the only way to secure a second guest editor, but it is not an ideal situation.

Then comes the biggest problem: finding potential authors. This is not a problem for the journal editors, it is one that we, as guest editors, need to address. In an under-researched area, which hopefully most special issues are, we need to cast our net for authors very wide. There is no point in relying entirely on the CFP. What works best is word-of-mouth – the personal touch. There may be a few researchers already working on the theme and trying to publish who may be approached. There may be others who already write about the theme, but it is secondary to their main interest. Digitisation/digitalisation is an example, as many researchers today engage with both of these to some extent, but they may have never considered them to represent a research theme in their own right. We can also go outside the discipline and encourage or even specifically invite contributions from those whose experience makes them suitable authors on the theme. Inviting scholars from other fields tends to work best if they are invited to speak at a conference organised on the theme.

Taking all these points together, the ideal approach to proposing a special issue addressing an under-researched area is identifying the topic, finding someone to share the role of guest editor, and identifying potential authors, all before the proposal is made to the editors. With that solid foundation, the problem of finding contributors on under-researched themes – which are under-researched for a reason – can be minimised.

Guest editors and their areas of expertise

We, as guest editors, should be passionate about the theme of our special issues. We need deep knowledge of the topic to be able to differentiate between relevant and non-relevant contributions. We need deep awareness of the literature to be able to observe where it is absent, and to identify suitable potential authors and reviewers. Someone whose expertise is solely in mediaeval Italian accounting history, for example, would not be an ideal choice for guest editor of a special issue on bookkeeping in English monasteries in the thirteenth and fourteenth centuries. Expertise on the theme of a special issue matters for authors and reviewers and, most of all, for us, guest editors.

Topics developed from international conferences

Many of us have been guest editors of special issues based on past iterations of the AHIC, of which, as noted in Appendix 1, there have been six. Ohe of the recent conferences has been the 10th AHIC in Paris in 2019. The conference theme was ‘Accounting and Work’, which became ‘Accounting and Work in Historical Perspective’ for the special issue, with a specific focus on the interface between accounting, work and people.

First of all, choosing a theme for the conference is a decision that is paired with choosing a location. Should the conference be somewhere less represented on the ‘publications’ map, which could help in achieving greater exposure for the location and develop links with local networks? Or should the conference be somewhere already well known for particular expertise, in a place easily accessible for a great number of inter-continental participants?

The theme of a special issue linked with a conference is negotiated at several levels and at different moments, among the editors of the journal, the organising committee and the scientific panel. If the CFP of a ‘standard’ special issue can propose a niche theme, for special issues linked to conferences there is a much more important role: to bring the accounting history community together. Therefore, there is a potential danger of diluting specialisation. This can be overcome by a clear positioning from the start, in terms of diversity.

Articles have different levels of development, so we need to arbitrate between the calendar constraints of the special issue (often very tight), the theme, and the editorial agenda. Some articles could have an excellent fit, but be very underdeveloped, others may have already been submitted to the journal between the moment of the conference and the call for the special issue. Traces of this arbitration can be found in publications that fit the theme of the special issue but appear in regular issues of the same journal, or other journals, before or after the publication of the special issue – this can come from the constraints of delays (especially when close to the publication date of the issue), or from starting to answer the agenda set by the special issue (the references can be a marker), or can just reflect a very topical area. Whatever the reason, there is a beneficial effect on successfully carrying on the agenda of the special issue. Moreover, articles can benefit from the presentation at the conference and can be improved based on the comments and suggestions received, including by expanding data collection and analysis, and by a better framing in the light of the conference topic.

For the special issue emerging from the 10th AHIC, some of the ingredients of the conference were reflected. This included an opening out to other disciplinary areas through the plenary address, which involved the participation of guest speakers prominent in the field of labour law, together with opening the debate on the links and interest of accounting history for practitioners (with a dedicated workshop). The resulting theme of the special issue was a variation of the theme of the conference. In some cases, the theme of the special issue linked to a conference can focus on a particular aspect, chronology or methodology. In the case of the special issue that developed from the 10th AHIC, it was important to broaden the spectrum, to enable more diversity in the participation (in terms of settings of the study and of the authors, chronologies, and affiliation to different groups, such as practitioners and scholars from other fields), in line with the signature of the conference.

Addressing issues of quality with special issues in Accounting History

One of the original roles of special issues was to populate gaps in literature, particularly through identifying new research themes. In our opinion, over time, this emphasis has tended to shift among a variety of topics, to attract authors and a positive response to calls for papers to enable the final selection published to be at a high level of quality. But that has its downside: experienced writers on a theme are the least likely to write anything truly ‘new’. The special issue may be full of ‘good’ articles, but none of them is likely to add very much to what is already known and understood. From a readership perspective, the quality of output is acceptable, but the quality of contribution is not. And it is the latter that all journals should be striving to achieve.

A route to have a sufficient number of articles to enable the final published selection to demonstrate a high level of quality is to develop special issues from themed conferences. As mentioned before, it has always been difficult to get this right, with articles presented at specially themed conferences that are rushed, sometimes under-researched, and often in need of fresh thinking and new ideas. Those adopting this route as guest editors have all sorts of quality issues of which journal editors need to be aware. The key point is that the conference submission is generally less developed: articles may have been only lightly reviewed for the conference. Guest editors often work with potential authors to ensure that their conference submissions are revised appropriately to bring them up to the standard of journal submissions. As guest editors we may argue, and so will authors if pushed, that this counts as one round of review. But, if the standard of the typical conference article is compared to the standard of the typical article submitted to a journal, the former is a working paper, and the latter is, at least in the dreams of the authors, the finished article. The latter is generally far better developed than the former, but this is to be expected, as authors often submit their work to conferences with the purpose of visibility and gaining wide comments from other conference participants, knowing that their work can be improved. To maintain the quality of themed conference-based special issues, guest editors (and journal editors) need to be firm.

Then there is the inclusion of the invited keynote or plenary speech. Such contributions are often not really research articles at all, in the sense that they may not have uncovered new historical material and developed new knowledge. Keynote addresses may contribute by reviewing existing literature, identifying gaps, and setting out research agendas, but they are often critical commentaries by ‘big names’ invited because their contributions to the journal are seen as enhancing its reputation. Critiques well done can be useful to the research community, but they still need to be reviewed to ensure they meet the quality expected from publications in the journal.

Special issues that aim to address under-researched areas, including new themes, are attractive to guest editors for whom the topic is a specialism or an area of great personal interest. Having an opportunity to have your own field of research given prominence in this way should stimulate interest in your own work. Working with the authors interested in your topic widens your networks, as does working with the reviewers. And, if you can establish a conference or, arguably better still, a workshop on the topic at which prospective authors present their research and have it critiqued, you may establish the topic as something of wider interest that may become accepted into the mainstream of the field. In this way, the guest editors will be provided with a research path after publication that supports the development of their careers, and the potential for very high-quality articles in the special issue is arguably greater than would otherwise be possible.

Editors tend to be open to special issue proposals from experienced researchers, but we have observed that, in many journals, it is often the editors who come up with the ideas and then try to find people to act as guest editors. The motivation of such invited guest editors is not the same as when it is their own idea. But invited guest editors, genuinely interested in the proposed theme, will likely know who has researched and published on the topic. We should know who to approach as potential authors and who to select as reviewers. If the rigour of the traditional review process is maintained, the quality of the published articles should be apparent.

There is a danger, however, that guest editors are not sufficiently aware of who is working on or close to the theme of their special issue. As a result, they may be more likely to invite inappropriate reviewers, with obvious implications for quality. In addition, finding the response to the CFP is very low, rather than inviting contributions from those actively developing new research within the theme, guest editors may approach those already established in the wider field, who can put together something that looks respectable on the special issue theme. Or, not knowing who is researching the theme and being less than well aware of the relevant literature, guest editors may send submissions out for review that barely relate to the theme, or that do so, but include nothing new. The quality of the article when published may satisfy its immediate audience, but it will not satisfy those who have expertise in the topic. A knowledgeable research community will recognise poor quality.

The quality of special issues is also a constant problem for journal editors, not least because some guest editors may not have any editorial experience, and editing is a specialist subjectively founded role that cannot be learnt by rote or applied as an algorithm. In our experience as editors and guest editors of other journals, one solution is for the final decision on each article to be retained by the editors, with us, guest editors, only allowed to recommend acceptance. This approach works well in maintaining quality, but in some journals guest editors have resigned when uninformed journal editors overruled their recommendations, throwing the entire special issue into chaos. Some journals apply rules to the process to overcome the inexperience of some guest editors. It is important that as guest editors, we understand the journal policy concerning acceptance before we begin and, if it is not declared to us, that we discover what it is. The quality of the review process is what makes or breaks the quality of a special issue, but high-quality reviews are likely to be obtained only when our choice of reviewers is appropriate, and this implies that we know their field very well.

Opportunities offered by special issues after publication

As editors of a special issue, we are often seen as having a role of gatekeeping, but we also act as gate-openers, by creating a space in which we invite peers to contribute. Sometimes, this space may be an emerging field, therefore opening a completely new direction and ‘market’. Encouraging participation is combined with ensuring strict respect for the usual standards of academic writing, and the specific standards of a particular journal, such as Accounting History, in this case. This often leads us to jointly develop strategies with the journal editors in line with their editorial agendas.

In the case of the special issue arising from the 10th AHIC, the diversity of profiles is an example. The guest editors wished to include practitioners and prominent scholars from other fields (particularly labour law). Opening the gates was therefore exciting, and it came with a responsibility to accept exposure to other ways of researching and writing, from different fields and communities. However, this created valuable opportunities to introduce new theories and methods, and to create a dialogue, and potentially build a new audience for publications in our field.

Other opportunities deriving from editing a special issue are linked to shaping the field, networking, personal development and expertise, and publication spin-offs. Editing special issues is a powerful tool for driving knowledge creation and shaping the field. In the case of the 10th AHIC special issue, for example, the guest editors were able to promote a topic (labour accounting and accounting for labour) which is not yet well represented in accounting history research, and where there are strong national traditions. They could also make the borders of disciplines and communities more permeable, by opening the issue to practitioners and scholars from other fields.

Our experience of editing special issues provided opportunities to create connections, especially with the journal editors. Connections with authors and reviewers are mediated and based on shared knowledge and standards. Another important outcome was gaining experience, obtaining personal exposure and building legitimacy as part of our professional/expert development process. This can be particularly important for more junior profiles, and it can help positioning and being identified with a particular expertise.

There are also possible direct spin-offs from editing a special issue. The publication of the special issue is by no means the end of the story for us, as guest editors. Often, the theme of the special issue will have a wider resonance, allowing us to take the theme further. For example, following the special issue on ‘Accounting and Work in Historical Perspective’, one of the guest editors was able to mount a workshop on accounting history for the interest of practitioners, while connections created with the journal made it possible to invite one of the co-editors of the journal to give a presentation on national accounting history traditions. Finally, the present article can be considered as an example of a spin-off, relying on our reflexive account of our experience with editing special issues.

We believe that guest editing a special issue can also have personal outcomes. Guest editing can be therapeutic. One of us undertook our guest editing duties during the COVID-19 pandemic, a time of isolation and uncertainty, and found that the experience provided opportunities for human interaction and a target that provided structure and helped to ‘project the future’ through times of crisis. Records and documents produced during the process of planning the special issue and seeing submissions through the review process to the final production of the special issue are a true chronicle of the pandemic. We not only reflect on our strategies for coping with unusual situations but also, through the pace of revisions, the tone of discussions and the use of narratives in the various communications, we reflect individual survival strategies as an academic in different zones of the world, creating a sense of both the universal and the exceptional.

Acting as a guest editor also provides insights into the process of being managed as an academic. Reflexivity helps us to better understand the value of these activities, often included in ‘academic citizenship’, or ‘contributions in the life of the institution and community’, and to include this understanding in our practice. For instance, brief introductory editorials are typically not counted as academic articles or scientific productions, as they are regarded as coming within a different genre of writing. However, this can be problematic for emerging scholars in a world of ‘publish or perish’, and contributions as guest editors need to be properly recognised. Editing a special issue should represent an effort that is rewarded in terms of career progression, even if it may be ‘paid for’ differently.

Conclusion

In this article, we have attempted to provide a unique self-reflection (Haynes, 2011, 2017) on the challenges and opportunities and behind-the-scenes considerations that accompany the development of journal special issues, with particular reference to Accounting History. The privileged perspective adopted is the collective voice (referred to as ‘we’/‘our’/‘ours’) of the guest editors of the panel discussion ‘What makes special a special issue?’ that took place at the 11th AHIC in Portsmouth, UK, 6–9 September 2022. While this autoethnographic storytelling does not pretend to be comprehensive, it has enlightened aspects of the process and final outcomes that have rarely been investigated from this point of view. We were motivated by the conviction that self-reflection is a beneficial exercise of personal and scholarly growth.

Our detailed retrospective of the special issues in Accounting History since its inception shed light on the breadth of the knowledge developed through the publishing and dissemination strategy of the journal. Then, we looked back at our personal experience to contemplate our behaviour, the observed behaviour of the ‘stakeholders’ of special issues, the consequences and lessons learnt. While we originally considered the chronological sequence of a special issue ‘life cycle’, the insights offered by this article cover deeper understandings of topics, assurance of quality, networking and communication.

In particular, we considered the fine line between success (namely the publication of the special issue) and failure (a CFP that does not lead to publication) of a special issue and pointed out the several steps of negotiations and risk management, which intervene between us, as co-guest editors, guest editors and journal editors, us and authors, us and reviewers and finally the journal and its readership in determining the above-mentioned success.

Three sources of inspiration for special issues were pointed out as being completely new topics, related to under-researched areas, topics that fall into the main area of expertise of the guest editors and topics related to a former AHIC, which involve specific challenges. Each one of these sources of inspiration in the accounting history field faces a ‘time/space paradox’ which should be considered in relation to the specialisation/small size of the scientific community of reference, as revealed by the matrices illustrated earlier in the article, which explore risks and opportunities of special issues. The paradox is explained in terms of the advantages of a narrow or a broad topic to be deepened through a range of historical periods and geographical/cultural sites that preserve the appeal of the topics for a critical mass of contributors.

We regarded as factors of success of a special issue the closeness of the chosen topic to our personal research interests as scholars, the ‘functioning’ relationship between co-guest editors, our ability to rely on both personal scholarship and sound advice of the journal editors when establishing a coherent policy of editorial decisions above submissions and acting as quality gatekeepers.

The article finally outlined the relevance of the outcomes with respect to the successful outputs (release of the special issue) in the form of a newly acquired interdisciplinary network beyond our academic and accounting field, academic experience, personal growth, demonstration of leadership, and opportunities for career advancement.

In this sense, we believe a special issue is not far from an artistic production, and can be, like in the musical comedy The Producers (2005), so well-known to accountants, either a flop or a success. There is the programme (the special issue's CFP), the producers (us, the guest editors), and the cast (authors, reviewers), and then there are the critics and the public (journal readership), who are not identifiable in terms of applause and ovations, but through reviews, word-of-mouth, and subsequent citations.

We propose that further opportunities for self-reflection and investigation may involve other depictions of ‘success’ in relation to special issues and deepen specific aspects or relationships within the network which stems from each special issue.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Questions proposed to the panel of the 11AHIC for discussion.

| No. | Questions and prompts from the journal editor (chair of the panel) |

|---|---|

| 1 | Can you give us a bit of background about yourself and your level of experience on running special issues, with specific reference to special issues in Accounting History? |

| 2 | How do you conceive your role as guest editors, with specific reference to your experience in Accounting History? |

| 2a | How would you illustrate the risks, benefits and challenges of being guest editors and the relationship with the journal and journal editors? |

| 2b | What about the length of engagement (timing) to be considered for a special issue in Accounting History? |

| 3 | What does it mean to develop a special issue in Accounting History from a conference? |

| 4 | Which are the main factors to consider when developing the topic for a special issue? |

| 4a | What is the paradox of time and space to be managed in the conception of a special issue topic in Accounting History? |

| 4b | What about interdisciplinary issues and potential collaborations with professional figures outside the accounting scholarly community? |

| 5 | How would you choose and collaborate with your team of guest editors and decide to allocate tasks? |

| 6 | How would you solve potential conflicts/divergence of opinions and reciprocal social control within the team of co-guest editors? |

| 7 | What is the role of advertising a special issue in the three phases of: (1) call for papers; (2) development (guest editors sort out submissions and coordinate the choice of reviewers and review process); (3) post-publication of the special issue? How would you plan to do that? |

| 8 | Can you tell us about the opportunities that emerged after the completion of your special issue, for your career, the accounting and accounting history community and your relationship with the journal? |

| 9 | Anything else you’d like to add for the benefit of the audience? |

| 10 | Questions and answers from the audience. |