Abstract

This article explores the impact of federal government policy and societal trends on cost practices and management techniques used to support business structures within the United States between 1933 and 1939. These dates reflect the influence of the Great Depression in the USA. Specifically, we explore the influence of the National Industrial Recovery Act (1933) on the development of costing and pricing policies from the perspective of the social rule system theory. Using this theory and source documents from the ‘New Deal’ period and the National Industrial Recovery Act, the article explores the costing assumptions underlying the Act's definition of ‘cost’. The Act was enforced through government policy (1933 to 1935) and supported by the Blue Eagle symbol throughout the period. This resulted in a pseudo-competitive market structure where Blue Eagle costing (full cost recovery and earning a ‘fair and reasonable’ profit) became the basis for market pricing and business management.

Keywords

Introduction

What is a ‘relevant costing’ system? The last two decades of the twentieth century witnessed an intense dialogue surrounding the relevance of current management accounting and control systems. There was also a plethora of suggestions about how best to ‘fix’ these ailing systems (Cooper, 1989; Johnson and Kaplan, 1987; Johnson, 1992; Noreen et al., 1995; Shank and Govindarajan, 1993). This dialogue focused on how to adapt accounting-based calculative practices to better provide the type of information needed by companies competing in the global marketplace and how this information could be transferred through the educational environment (Napier, 2011; MacDonald and Richardson, 2011). The economic impact of globalisation provides the backdrop for the urgency and thrust of the messages delivered by these ‘new accounting practices.’ Unless changes are made to our ‘accountings’, they argue, the future will be bleak indeed (Carnegie, 2014; MacDonald and Richardson, 2011; Napier, 2011). In addition, new developments in our knowledge of the environmental and social effects of businesses and products now also factor into our definition of ‘relevant costs’.

Even in the early twenty-first century, the commercial world is undergoing significant changes. The rapid decline of major mining and manufacturing industries (e.g. steel, coal, electronics and automobiles), the displacement of major segments of the working population and the loss of competitive power caused by the onslaught of foreign competition are some of the powerful forces reshaping business practices in the US and other Western countries (Borjas and Ramey, 1995). The radical upheaval in the American market that followed the development of global markets harks back to an earlier time of crisis in US economic history: the Great Depression of 1929. The decline of major industries, displacement of the working population and loss of competitive power all represent significant shifts in the economic stature and health of the United States. This article focuses on The Great Depression and the subsequent National Industrial Recovery Act (NIRA) (1933). Specifically, the market rules (formal and informal) set down in response to the economic crisis of the Great Depression took into account a largely different view of ‘costs’ from those that the late twentieth-century authors were discussing.

The period under review, in terms of political, economic and accounting aspects, has been thoroughly analysed for many years (Gifford, 1983). The research methods used by the various authors encapsulated institutional economics (Commons, 1931), new institutional economics (Coase, 1998) and organisational economics (Posner, 2010). The Kingston and Caballero (2008) article compares the approaches of transition economics to identify how they fit the causes, processes and outcomes of institutional change, specifically, evolutionary change. This builds on the work of Hodgson (2007) who examined to what extent mainstream economics has moved in an evolutionary and institutional direction.

Hodgson (2007: 7) concludes that there are signs ‘of a gestalt shift in the social sciences, where rules are seen as constitutive of social reality’. This provides, through the social rule system theory, an opportunity to develop an evolutionary and institutional view of this period. Using the lens of the social rule system theory (Burns, 1986; Burns and Flam, 1987a, 1987b), and the phrases and thoughts from source documents from the period of the ‘New Deal 1 ’ and the NIRA, the article explores the displacement of the competitive market, and the consequent abandonment of one set of theories of cost that this macroeconomic movement entailed.

Specifically, the ‘cost’ theories that were displaced were based on the specific circumstances of the firm doing the manufacturing. For a contemporary and detailed discussion of the historical development of cost accounting, we recommend Garner (1947). In this article, we refer to the idea in 1915 that a proper cost depended on the individual circumstances of the firm producing the goods. In contrast, the National Recovery Administration (N.R.A.) was responsible for administering NIRA and adopted an industry-wide approach: There is this peculiarity about the N.R.A. principle. Not only do companies and localities compete with each other…but whole industries also so compete. For this reason when a change like N.R.A. comes along–raising wages, shortening hours and inevitably increasing costs – one company in an industry cannot accept it unless practically all other companies in that industry accept it. (Johnson, 1935: 253).

The next section of this article (section ‘The Great Depression and the New Deal: A social rule system theory perspective’) explores the history of the NIRA (which used the ‘Blue Eagle’ 3 as a symbol that those companies complying with it could display) and subsequent war-based price stabilisation boards. 4 The social rule theory is briefly explained as a lens through which to explore the NIRA program. The section discusses the 1920s economy in the United States as a prequel to the Great Depression. It then examines the Great Depression and the rise of NIRA as a reaction to the unemployment and low wages that came with the Great Depression. The article then moves to the specifics of the NIRA and its ongoing program (both when legally enforced and when a voluntary code and marketing symbol through the National Recovery Administration (N.R.A.) and the Blue Eagle. The article explores the assumptions around using the Blue Eagle costing model to define a ‘fair price’. The differences in possible (subjective) assumptions around the term ‘fair price’ are explored. The section then discusses the history of the Blue Eagle from legally enforceable and popular to ruled unconstitutional and treated with some suspicion. However, the Blue Eagle continued as a voluntary program and marketing symbol for some time. Section ‘Social rule system theory and the creation of markets in the United States’ then discusses the Blue Eagle program in the context of New Deal Economics. Section ‘Social rule system theory and the creation of markets in the United States’ concludes with a discussion of the Blue Eagle-based costing system's implications for the competitiveness (or lack thereof) alongside international goods and services.

Section ‘Market structuration and the NIRA’ of this article places Blue Eagle costing within the context of wider concerns with management accounting. This article finishes with a note that the NIRA represented a radical upheaval in costing in the United States, and before it can be thought that such radical upheavals lie purely in history, that there are possible future radical upheavals in costing systems to come. For example, ideas that the cost of sustainability and justice for future generations should be included in costing models in the future.

The Great Depression and the New Deal: a social rule system theory perspective

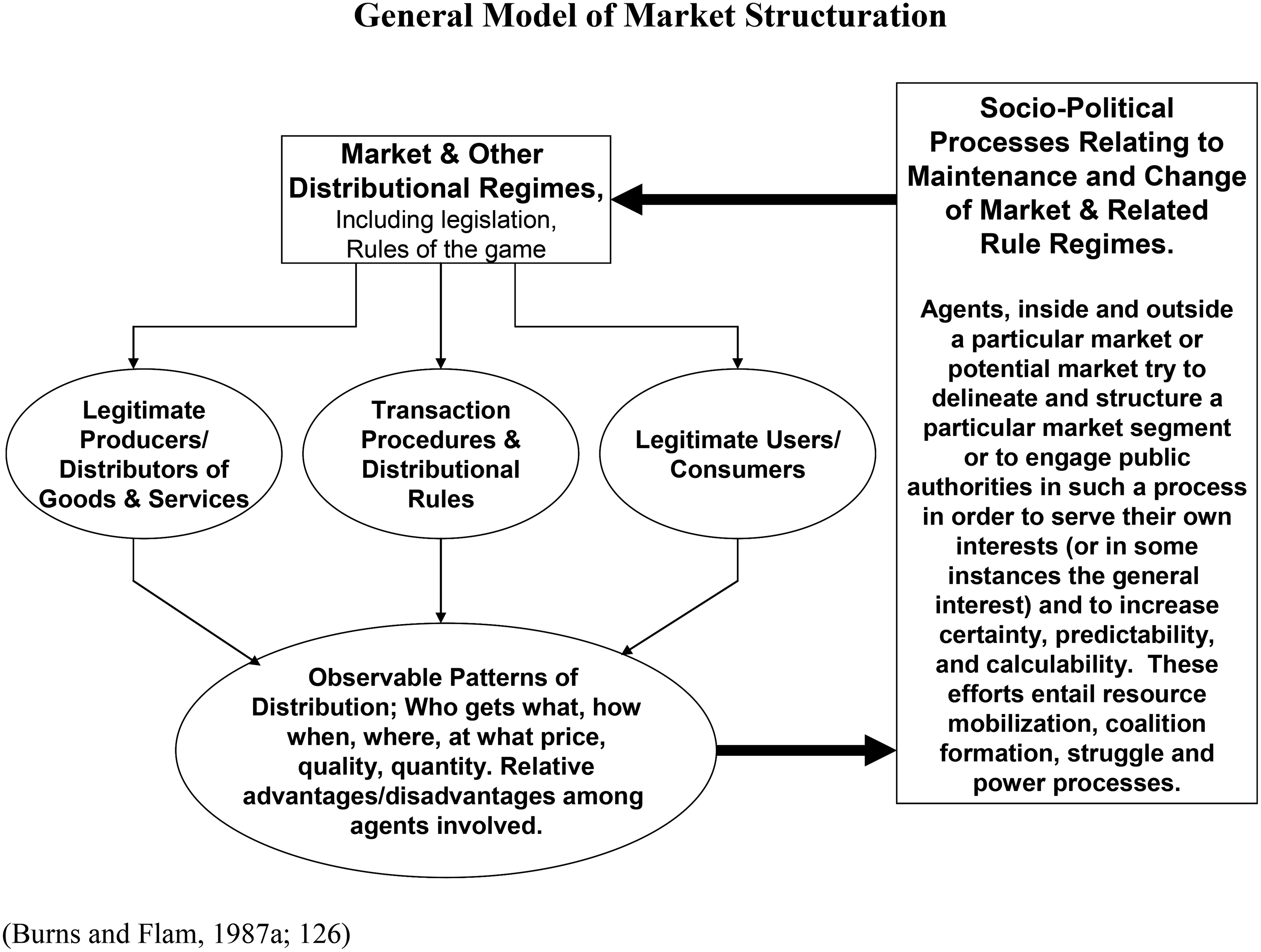

The social rule system theory focuses on the development of markets as defined by the context, or cultures, in which they emerge (see Figure 1). A body of literature explores the socio-political processes relating to the maintenance and change of markets and related rule regimes (Alvesson and Spicer, 2019; Beckert, 2010; Burns and Flam, 1987a; King and Pearce, 2010). According to social rule theory, market rule formation is caused by various factors. These are legal and administrative acts created and implemented through political and government processes, by the collusion of groups of sellers and/or buyers who establish rules of market entry and rules for procedures and transactions; the influence of norms, including informal rules, that are supported by a status group; and the granting of credit and access to contracts within the economic system. Burns and Flam (1987a) note that such market rules affect transaction costs and imply that there is the potential for increased prices due to the impact of these rule-based social agreements on the supply and demand relationships within a market.

General model of market structuration (Burns and Flam, 1987a: 126).

At the heart of the argument that market relationships can be shaped by social rules (rather than economics) is the belief that ‘markets are social organisations, structured and regulated by more or less well-defined social rule systems’ (Burns and Flam, 1987a: 125). Burns and Flam also suggest that there are two basic ways that this market organisation may be brought about (Burns and Flam, 1987a: 127):

Strategic structuring – informal or formal, whereby social agents, including the state, establish a rule regime regulating market access and transactions. Emergent structuring, whereby participants discover or adopt similar strategies within bounded rationality and situations with certain opportunity and incentive structures. Social networks and ecological properties result in relatively well-defined aggregate performance characteristics.

The social rule system theory provides a useful framework for analysing the development of markets and insights into the forces that can bring about changes in the social structuring, or rule systems that govern their functioning (see Figure 1).

Social rule system theory and the creation of markets in the United States

A laissez-faire free market structure has increasingly dominated perceptions as a defining feature of the developed capitalistic model. It has been used to frame economic transactions within the United States during the 1920s (Brand, 1988; Henry, 2008). Writing about this period, Prothro (1954) emphasises that this formative period in the American economy was characterised by traditional business concerns with economic liberty and the preservation of private property, without a hint of any orientation towards, or desire for, increased business to government relations. Consistent with the ‘rugged individualism’ that defined the developing social structure of the United States, the American marketplace and the businesses that comprised it were left to function with minimal interference from outside forces (Prothro, 1954).

The resulting ‘neoclassical’ market model (Baker, 1984) within the US was built on a minimal set of market rules, open micro-networks and undifferentiated macro-networks of buyers and sellers as the basis of its structuration. Facing minimal transaction costs and situational constraints, such a neoclassical market is depicted as a ‘hyper-rationality’ based on the tacit agreement of rule-abiding participants for its functioning (Baker, 1984). Within the neoclassical structure, there is no reason to expect standardisation in costing or accounting practices unless such standardisation supports the efforts of the micro-networks of buyers and sellers in reducing their market transaction costs (Burns, 1986; Burns and Flam, 1987a, 1987b).

At the heart of this cost debate was a belief that customers would not pay a company for its waste. This theme was the need to separate productive costs from various forms of the cost of waste. This led to a heated debate on the proper treatment of the cost of idleness (waste and unused capacity) in 1919 (Miller, 1998; Vollmers, 1996). Idle capacity cost aside, the fact that ‘cost’ as a construct appears to serve a central role in management decision-making and analysis is pertinent here. Therefore, the various forms of cost accounting during the early 1900s and the management practices they supported were driven by the need for information to make decisions within the organisation, not by government or professionally defined accounting rules. Cost was perceived as a concrete representation

5

of economic reality. Roos (1937: 87) pointed out that, in reality, the term ‘cost’ was far from concrete or agreed upon: On July 31, 1933, DuBrul had previously urged that the N.R.A. appoint a joint committee of the American Economic Association, the American Institute of Accountancy, and the National Association of Cost Accountants, to bring in recommendations on controversial questions pertaining to cost. In particular, he had pointed out that the accounting and economic professions were both divided on many basic questions of cost determination and said that, if codes were allowed to contain carelessly worded provisions, the effort to enforce them would result in confusion and tend to discredit the whole program. (Roos, 1937: 87)

Market structuration and the NIRA

By 1933, the United States was in the fourth year of the most serious economic depression it had ever faced. Lyon et al. (1935) suggested that this crisis led to the election and installation of a new administration that was sceptical of the rugged individualism of the past and convinced that a greater degree of collective action was the solution the ailing economy needed. The term ‘New Deal’ was instigated by President Roosevelt during the Great Depression to describe a series of projects and programs to improve prosperity and became the hallmark phrase denoting the policies, rules, regulations and sanctions to reshape the United States' market structure.

One of the central pieces of legislation of the ‘New Deal’ was the NIRA. The NIRA targeted the perceived ‘predatory competition’ of the pre-Great Depression era, which Roosevelt and his followers argued to be the major cause of this market failure (Johnson, 1935: 160). Coupled with an increasing concern for the advancing ‘rationalisation’ of American industry between 1922 and 1929 (e.g. the displacement of men by machinery; Lyon et al., 1935), a defensible basis for redefining the marketplace rules was defined. The result was an attack on free market competition, the perceived causal factor in the economic collapse.

The NIRA was the backbone of this anti-free market movement, representing a visible and direct development of rules to reshape the market economy (Brand, 1988; Johnson, 1935; Lyon et al., 1935). One of the main enforcing mechanisms of the NIRA, as defined and structured by Hugh S. Johnson, its director, was the development of many ‘cost protection’ codes. These codes covered various topics, including fair completion, working conditions, regulation of petroleum pipelines and products, public works administration and construction of transportation projects. In all, 352 separate code items dealing with the concept of ‘cost’ were developed during the two short years the NIRA functioned (Lyon et al., 1935).

Developing uniform costing practices, then, served as the backbone of the NIRA's attack on the perceived inadequacies of the free market structure. It was not simply any form of costing that served this purpose – it was Blue Eagle's version of costing that became the ‘accepted’ means of measuring, hence setting prices based on incurred costs plus ‘reasonable’ profit. Two important points need clarification at this point. Firstly, Roos (1937) noted that Blue Eagle's version of costing tended actually to be somewhat inflated above full cost recovery and included an element of profit: As a result of a variety of difficult situations involving cost and the insistence of businessmen that Congress intended to authorise them to prohibit sales below cost, we find General Johnson in June 1933 offering to sanction the banning of such sales, but declaring that if extortionate profits were attempted he would be forced to intervene. Therefore, we must conclude that Johnson approved such codes as lumber and timber products and bituminous coal, believing that they only outlawed sales at losing prices. But, as we shall see, here and in nearly all industries the definition of cost was such as to include some profit, so that actually minimum prices were set; indeed, the ‘cost,’ below which sales were not to be made, almost always included too liberal an allowance for some item. (Roos, 1937: 249)

The second point to raise from Roos (1937: 251) is his discussion of the degree of subjectivity inherent in this ‘accepted’ means of measuring cost: DuBrul realised, however, that the problem of cost determination would continue to plague the N.R.A. and during September, 1933 urged various officials to give serious attention to the problems involved. As a result, on Sept. 12, 1933, Victor S. von Szeliski, the chief statistician, presented a memorandum particularly significant because it recognised the tremendous complexity of the problem of prohibiting sales below individual cost and yet attempted arbitrary definitions which received considerable attention from N.R.A. officials. We find him including the usual direct manufacturing expenses - cost of raw materials, wages, fuel, power, and supplies, salaries other than those of officers and major executives, and commissions, and then arbitrarily specifying that if prices of materials or rates of compensation for personnel changed during a month, values at the end of the month should be used. As items of overhead expense he listed taxes, insurance, officers’ salaries and salaries of major executives not to exceed $17,500 each per annum, interest on borrowed money, and advertising arbitrarily limited to a certain per cent of the direct operating costs, the exact figure to depend upon the nature of the industry. To determine the unit cost below which sales could not be made, he proposed that the sum of the direct and indirect costs as defined above should be divided by (a) the average number of units produced per week, month, or other period during the past six years, or (b) the production for the given week, month, or other period, whichever of (a)and (b) was higher. Moreover, to allow for the liquidation of excessive inventories, he suggested that each code contain a provision reading: ‘In order to liquidate an excessive inventory, sales can be made at - (the figure to be set for each industry) per cent below cost as above defined.’ Finally, he expressed willingness to permit sales at any price to satisfy creditors’ demands.

The implications of this change in the role and Blue Eagle method of costing were clearly noted and understood by those shaping the economy, as detailed by Lyon et al. (1935: 588): It is highly probable that in every instance in which the N.R.A. guaranteed cost protection to industries it was expected that such protection would bring about a price higher than the competitive price. It is needless to say, therefore, that it is in effect price fixing. Unless the cost systems, the use of which was required by individuals, included elements of cost that

Within the formation and functioning of the NIRA, full cost recovery played a pivotal role in redefining the competitive marketplace. The NIRA could provide a potential explanation for the apparently radical and troubling shift away from a rich, economics-based theory of costing, as detailed and promoted by Church (1930), Gantt (1915), and Clark (1923), towards the modern accounting-centred system.

6

It was a change designed not to improve business performance, but rather to change radically the structure of the laissez-faire free market system that had hitherto been the foundation of the American economy. In the words of N.R.A. Director, Hugh S. Johnson (also known as General Johnson): In March, 1933, we could no longer afford to sit and do nothing about millions and millions of frugal hard-working people who has been cut off from their livelihood. We could no longer say, ‘Let them work out their salvation.’ Economic and mechanical progress has outstripped political process and taken that salvation completely away. Any political system has failed when people can no longer live under it by their own efforts. For five years a very large proportion of our people have not been able so to live. We must substitute for the old safety valve of free land and new horizons a new safety valve of economic readjustment and direction of these great forces. There is no other alternative to shipwreck. The need for immediate and effective action is still upon us, and the need for wise direction will always remain. We are permanently in a new era. (Johnson, 1935: 7)

The Blue Eagle flies (briefly)

By September 1933, the Blue Eagle flew high, with over two million businesses signing Blue Eagle Blanket Codes and collecting their Blue Eagle posters, banners and badges (Watkins 1999). There were also Blues Eagle movie reels, Blue Eagle floats in parades, school children taking public pledges 7 and an enormous Blue Eagle pyramid in New Orleans 8 . This enthusiasm was not to last long, however.

The NIRA was transitory, at least as far as enforcing the terms of the NIRA legally went. Signed into law as a temporary action in June of 1933, the NIRA was nullified in 1935 on the heels of a series of legal and legislative battles that brought its constitutionality directly into question, as suggested by the following: The NIRA was declared unconstitutional as an excessive delegation of law-making power to private groups and government agencies. (Lowi, 1971: 75)

Reforming the market: the Blue Eagle survives symbolically

Roos (1937), Former Director of Research for NIRA, provides a fascinating insider's view of the strengths and weaknesses of NIRA and its many unintended consequences: A warning is, therefore, given to planners, first to consider fully themselves the ramifications of their proposals and, second, to encourage the widest possible debate on the issues involved, lest the ‘cure’ itself transcend in pain the disease. It is the failure of the Roosevelt Administration to recognise this principle, from the far reaching but contradictory NIRA, rushed through Congress almost without debate, to the President's cry against the Supreme Court when its inevitable decisions destroyed the monstrosity, that during 1934 and 1935 had kept business in a churn, prevented re-employment, and, consequently retarded American development. (Roos, 1937: 471–472)

Burns and Flam (1987a) state that unwritten rules and informal norms are one way that rule regimes can pursue the active shaping of supply and demand curves through the active determination of, or interference with, market prices. In other words, it is possible that the influence of the NIRA on both the market and the costing practices that defined it may have remained in force through the operation of an informal set of rules conveyed through the Blue Eagle symbol.

Business and New Deal economics

The symbol of the Blue Eagle was a mechanism for the continued influence of the NIRA beyond 1935, including its pursuit of uniform costing methods as embodied in full cost recovery. To gain acceptance from business, though, the increased costs of doing business inherent in the New Deal legislation had to pass through to the public through price increases that effectively moved prices above the competitive market level. To create acceptance of the NIRA by business, companies were allowed to pursue a ‘reasonable profit’ based on Blue Eagle (full cost plus profit) recovery of both ‘earned’ and ‘unearned’ costs (Lyon et al., 1935). In other words, in agreeing to abide by the NIRA (no longer legally enforceable) and to signal this adherence through the display of the Blue Eagle signal, a business was rewarded with the hope of a guaranteed profit (or return) on all of its costs (including a degree of wastage), whether value-adding or not.

The implicit agreement to overturn the market as the basis for price setting, replacing it with a full cost recovery plus ‘reasonable profit’ mode of operation, is the essential element of the NIRA and its impact on the extant market economy of pre-1933 America. Contemporary texts (Dubofsky, Melvyn and Dulles, 1999; Morris, 2004; Shogan, 2006) noted that the goal of the NIRA was to redefine the concept of ‘fair’ competition and to weed out the predators that were charged with the destruction of the economy. In essence, the businesses who subscribed to the NIRA and its symbol (the Blue Eagle) agreed to disengage from the market-based pricing mechanisms that formed the basis of the neoclassical, laissez-faire form of market competition, replacing it with a ‘full cost plus reasonable profit’ price mechanism. Cost accounting practices played a role in shaping the New Deal economy and its pseudo-competitive market structure.

By tacitly agreeing to compete on a cost plus profit based definition of market value, or price, business was creating a safety net for itself that would effectively remove it from the harsh realities of the free market system. The redefinition of price to reflect full cost recovery plus ‘reasonable profit’ based on full cost provided businesses with a means to stabilise and improve their financial performance. In its early phases, the NIRA was supported by nationally prominent businesses (Swenson, 1997) because the businesses themselves stood to benefit. The impact of the New Deal policies on wages and prices was investigated by Cole and Ohanian (2004), who found these policies significantly increased both wages and prices. Comparing sectors covered by the policies to sectors not covered, they found that in sectors covered by policies, real wages and relative prices rose significantly after the NIRA was adopted and remained high throughout the New Deal. Further, in sectors such as coal and farming, which were not covered by the New Deal, policies, wages and prices did not rise over the same period. Cole and Ohanian (2004) calculated that wages in the covered sectors (Cole and Ohanian, 2004) rose between 24 and 33 per cent by 1939, and relative prices rose eight to ten per cent between 1924 and 1933 and were about 11 to 12 per cent above their 1929 levels in 1939.

The Blue Eagle, Blue Eagle costing, and its implications

The key to the reforms driven by the NIRA was the intense desire to get people back to work (Johnson, 1935; Richberg, 1934; Slichter, 1934). This was not an unreasonable goal, given the dire straits of the American economy. Hooked on the various efforts to increase both employment and wages (e.g. the Works Progress Administration, the creation of the Securities and Exchange Commission, and a large number of public works), the New Deal's attack on the free market system was consistently driven by the belief that the essence of a fair and sustainable market economy lay in full employment. People were desperate for work, and businesses were desperate for consumers. It was not a time for lofty ideals but for action (Johnson, 1935; Richberg, 1934).

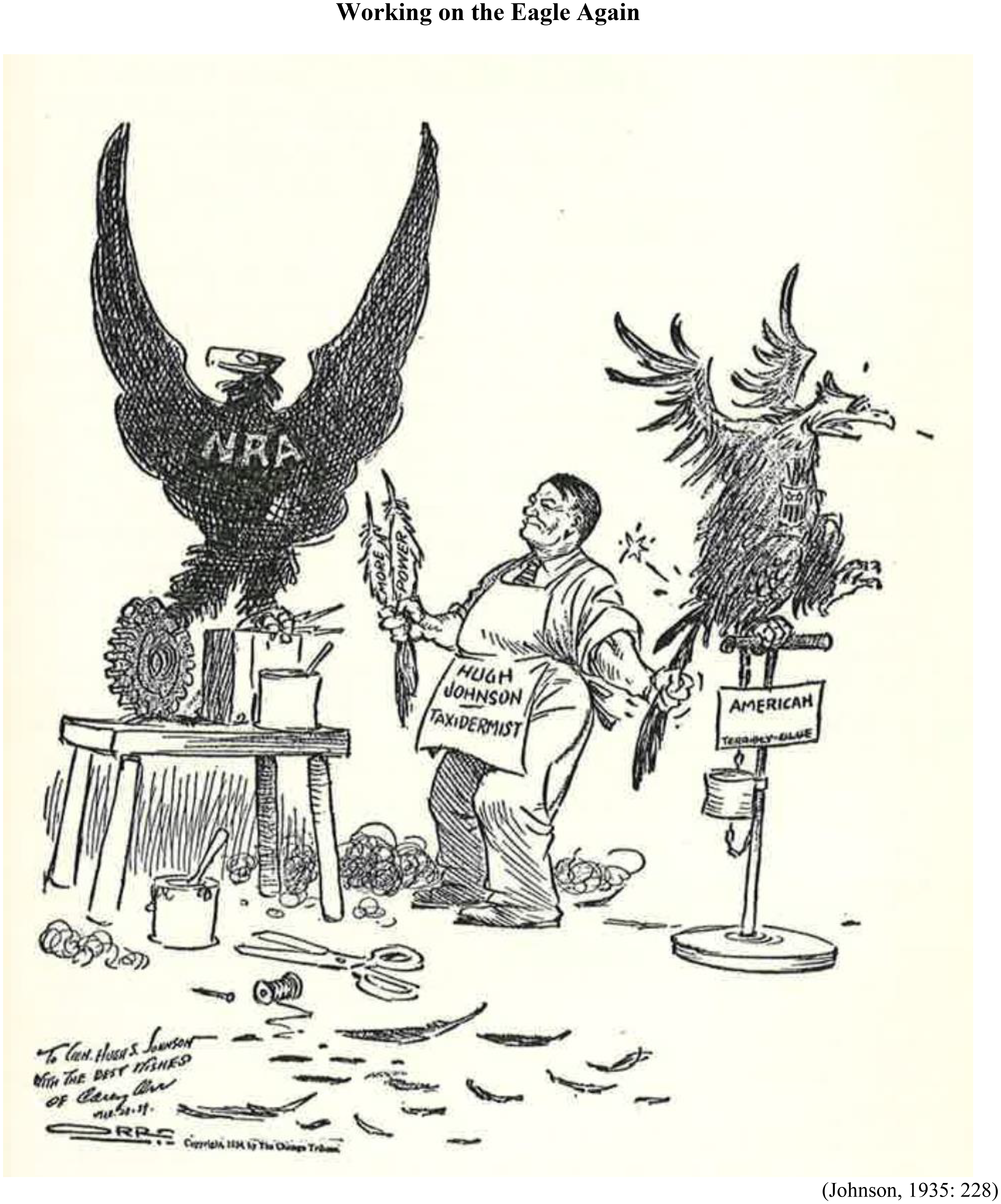

Yet, the Blue Eagle and the costplus profit based, pseudo-competitive market structure that emerged from this period had several problematic implications. The first is effectively captured in a cartoon in Hugh S. Johnson's 10 autobiography (Johnson, 1935: 229) (see Figure 2). The cartoon, captioned ‘Working on the Eagle Again’, depicts Johnson removing feathers from the American Eagle to create the symbol of the National Recovery Administration, the Blue Eagle. Cartoonists of the time made much of the anti-capitalist (see Figure 3) tone of some of the NIRA policies.

Working on the Eagle Again (Johnson, 1935: 228).

1935 Saturday Evening Post cartoon by Herbert Johnson.

The primary issue of concern represented by the NIRA and its ‘enforcer,’ the Blue Eagle, was that they sought to undermine the capitalist state. NIRA associated the laissez-faire capitalism (the dominant social rule system of the United States preceding the New Deal) with the failure and unemployment of the Great Depression. This was a choice consciously made by Johnson. A cost plus profit based, governmentally redefined economic structure was then held up as the solution to the ills of the Great Depression, implemented through the NIRA and symbolised by the Blue Eagle.

Accounting methods played a major role in this quest to reshape American social and economic structures (Johnson, 1935; Lyon et al., 1935). The Blue Eagle non-market-based costing model (including some profit and wastage) became the basis for competition within the post-Great Depression economy. As long as all industrialists agreed to adhere to this costing ideal, which was in their self-interest, NIRA suggested that the economic order would be restored, and all would benefit. This was the underlying logic that drove the New Deal proponents. Roosevelt stated, ‘the NIRA was to restructure the economy for all time.’ And perhaps it might have, had the United States been able to avoid or defend itself against the onslaught of the global marketplace (which, of course, did not subscribe to the Blue Eagle definition of ‘cost’).

To refer to Roos (1937: 249) in his reflection on NIRA, the pushing of the policy of ‘no sales below full cost’ was not at all a naïve one by the business leaders of the time: [I]t must be made clear that businessmen repeatedly urged the outlawing of sales below cost and, in general, they considered liberal depreciation, interest, rent, and taxes to be proper items of cost.’ A considerable number admitted that such a ‘cost’ was arbitrary, but a few agreed with General [Hugh S.] Johnson that everyone knew what his costs were, or could hire an accountant to find out. Whenever anyone challenged Johnson's contention that it was possible to determine accurate production or selling expense, he brushed all arguments aside and declared anew his dogma. It was extremely difficult therefore, for the N.R.A. to develop a satisfactory cost policy. (Roos, 1937: 249)

The effect of the NIRA on the fall of management accounting

Some see the NIRA and the Blue Eagle as representing an intentional form of restructuring of the American economic system away from laissez-faire, or free market capitalism, to a more general political–economic model (Burns and Flam, 1987a, 1987b) premised on government interference in markets. Reinforcing these formal policies was the adoption of informal norms that suggested that Blue Eagle costing become the basis for setting ‘fair’ market prices (Johnson, 1935; Lyon et al., 1935). In this process, economics-based costing, which argued that the market equilibrium price would not accommodate excessive levels of cost or waste, fell into disuse. This may have resulted in an almost religious adherence to Blue Eagle-based pricing and its assurance that a company should earn a reasonable profit. Implementing the NIRA and the Blue Eagle principles resulted in a major market fracturing and reconstruction of the guiding social rule system within the United States economy.

The Blue Eagle falls into disfavour

It will be seen from the discussion in sections ‘Social rule system theory and the creation of markets in the United States’ and ‘Market structuration and the NIRA’ of this article that ‘Blue Eagle costing’ had little to do with the costing models that preceded it. This could account for some apparent amnesia that surrounds management accounting today. Specifically, the rich history of dialogue surrounding the economics of cost that defined the pre-1933 world of accounting has no ultimate demand or purpose in a market system that defined competitive price as what a company spent plus a fair return.

The marked fissure is striking among the accounting literature in the twentieth century. The existence of some powerful, all-encompassing force is necessary to explain why the wisdom of writers such as Church (1930), Clark (1923) and Gantt (1915) fell into disuse and, ultimately, largely disappeared from the late twentieth-century management accounting literature.

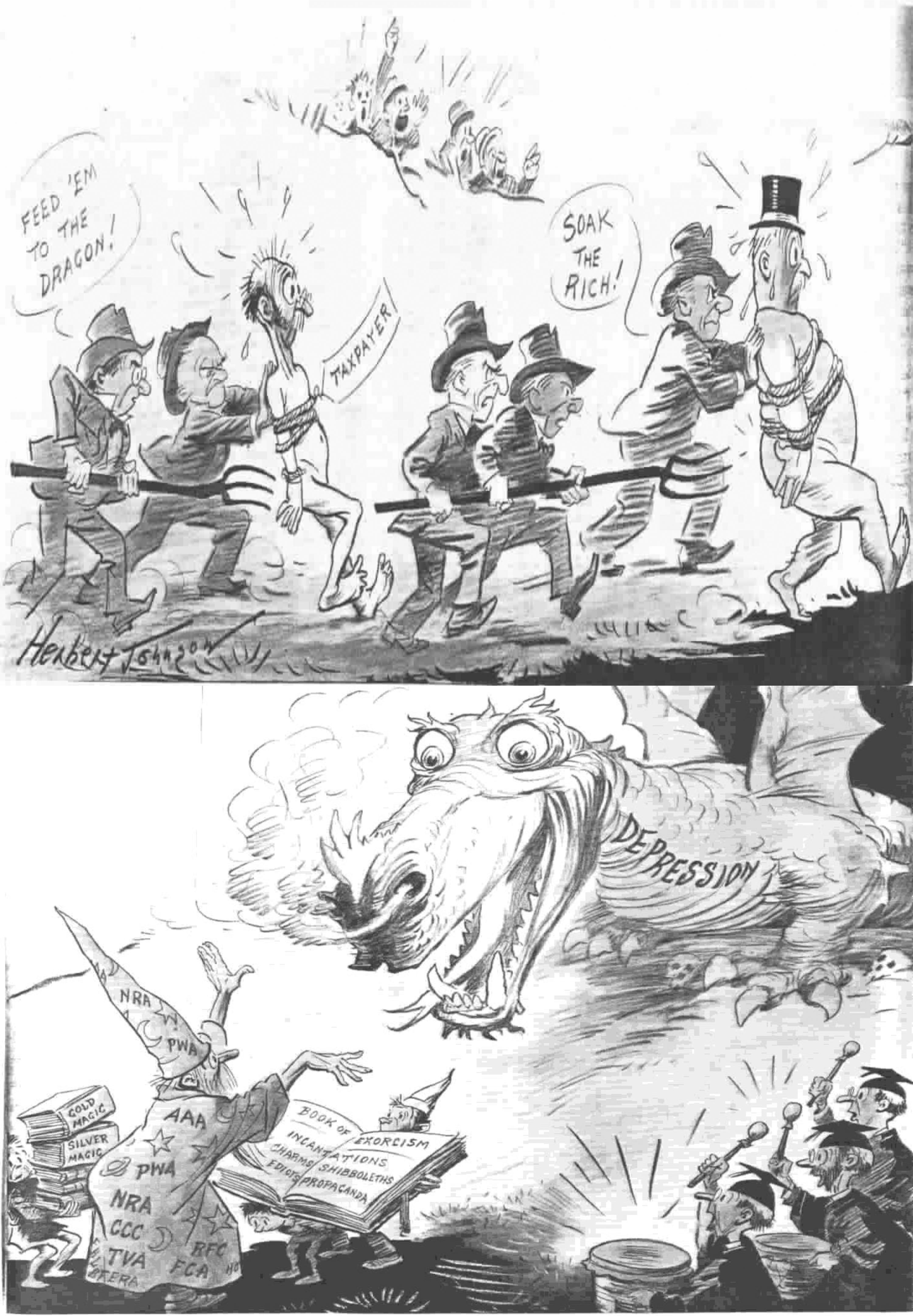

By 1934, a level of scepticism by the press, the public and the resignation of about half of the staff of the N.R.A. enhanced this disfavour. 11 Looking at the political cartoons of the time, it is interesting to see the breadth of conspiracy theories attributed to NIRA. From the 1935 cartoons of conservative cartoonist, (and not to be confused with Hugh S. Johnson, one of the leaders of N.R.A.), Herbert Johnson (Figures 4 and 5), it can be seen that N.R.A. was accused of influences from groups such as labour unions, radicals, utopian dreamers, communists and political barons.

Too Many Gardeners cartoon by Herbert Johnson (1935).

Herbert Johnson (1935).

Many have argued that the S.E.C. Acts of 1933 and 1934 were responsible for this decline in management accounting compared to financial accounting (Johnson and Kaplan, 1987). Yet, a careful reading of these Acts betrays no global prescription for ‘full cost recovery.’ Only the NIRA, which specifically promoted and relied upon the logic of the Blue Eagle version of full cost recovery (plus ‘reasonable’ profits) in its framing and operation, provides a reasonable explanation for this major change in the role and definition of relevant management accounting data. In redefining the set of social rules that defined the market economy in the United States, Roosevelt, with the intent of restoring employment in the Great Depression-era United States of America, employed full cost accounting methods to define and stabilise the pseudo-competitive market structure. In linking cost to a new social rule system, Roosevelt created the platform for adherence to full cost (plus) recovery methods. Yet, as Johnson (1992) suggests, this apparent ‘blind adherence’ to the Blue Eagle version of full cost (plus) recovery logic later proved a handicap in the global marketplace 12 .

Redefining management accounting post-Blue Eagle

Johnson and Kaplan (1987) argue that the combination of these events led to the apparent loss of knowledge that significant and valuable alternatives to the Blue Eagle costing methods might be usefully applied. This series of arguments might be seen as a set of unfounded claims, yet it is a common theme that runs strongly through the late twentieth-century management accounting literature (e.g. Cooper, 1989; Johnson, 1992; Johnson and Kaplan, 1987; Shank and Govindarajan, 1993). Johnson and Kaplan (1987) appeared to have made this logic, with the perceived ‘fall’ of management accounting becoming the basis for a rebirth of the economic theory of cost.

Trends within the United States in the later twentieth century suggested that economic theories of cost were undergoing a rebirth as one basis for the effective management of competitive business in a global market. For instance, target costing (Sakurai, 1989) is an economic model that suggests that companies should work from the market to establish their price and profit and, hence, allowable cost expectations for a product even before it is launched. Target costing was one way a company could begin to focus on cost, not as a naturally recoverable expense of doing business, but as a constraint, or cap, on the perceived value of goods and services. In this model, cost is sacrificed to gain the market price; a loss is sustained when such cost exceeds the market-determined value of the good or service. Target costing started from the belief in a free market economy with supply and demand curves set by perceived product value or consumer utility functions rather than the current cost of the resources consumed to create that good or service.

A related innovation in management accounting, strategic cost management (Shank, 1989; Shank and Govindarajan, 1991, 1993), suggested that competitive advantage can be gained by redefining the structure of an industry's value chain. Once again, this approach builds from the belief that predatory practices that seek to disrupt a market's structure or existing rule system represent acceptable, desirable, competitive actions. The logic of strategic cost management adheres to the description of behaviour that would occur in a market with weak moral commitments (Burns and Flam, 1987a).

It is noted by Gomes (2008) and Miller (1994: 1) that accounting cannot be regarded as a neutral practice. It is influenced by and influences: ‘Accounting practices create the costs and the returns whose reality actors and agents are asked to acknowledge and respond to…’ As each of the major costing innovations in management accounting takes hold, whether the rise of activity-based costing in the late twentieth century discussed above or the rise of social and environmentally inclusive costing systems in the twenty-first century (see Vosselman (2014) and Mook (2007)), a strong element of subjectivity remains. This article aims to illustrate that change and subjectivity in management accounting remain important and examine a key shift in management accounting and costing brought about by the advent of the Great Depression in the United States of America from 1933 to 1939. The differences in possible (subjective) assumptions around ‘fair price’ are real, present and evolving. This article presents one historical example of this.

It is also interesting to reflect on the level of debate and passion that the N.R.A. generated as we reflect on the N.R.A. program: [T]he National Industrial Recovery Act became law on Jun. 16, 1933, a large area of American industry and trade had come under its sweeping powers. Four hundred and fifty codes had become statutes. Five million employers and twentythree million workers were subject to its supervision - in this far-flung effort, amid a grave emergency, ‘for the preservation of American standards.’ Acclaimed by both industry and labor at its inception as a ‘New Magna Carta,’ it became the object of the most intemperate adulation and most violent condemnation. No institution has been accorded more space in the discussions of the press within an equal period of time. Reaching with its broad powers into the farthest corner of economic life, it was the most bitterly debated governmental agency in American history. (Roos, 1937: ix)

13

An eye to the future

This article traced the historical development of the market economy from a costing perspective within the United States. It examined a radical upheaval that effectively redefined the basis for competition. The Great Depression and one of the Roosevelt Government's key Acts in response to the Great Depression, the NIRA, represented a deliberate restructuring of the laissez-faire market consistent with social rule system theory (Burns and Flam, 1987a, 1987b). This period was characterised by a pseudo-competitive market where fair competition was defined by full cost recovery with a built-in expectation for a ‘reasonable’ profit. This economic model was driven not by the iron laws of the marketplace but rather by tacit agreement on a prescribed set of market rules and norms. While views as to which economic outcomes remain substantially political and prone to subjective interpretation remain varied (Hopper and Powell, 1985; Hopwood and Miller, 1994), the difference in dominance between application of the NIRA concepts of full cost recovery (plus profit) and the late twentieth-century management accounting focus on strategic cost management and activity-based costing models is stark. Suppose the initial promise of a twenty-first-century impulse towards sustainability and social costs continues, for example, the work of Vosselman (2014) and Mook (2007), it is likely that the concept of what a ‘cost’ encompasses and how it is determined will again be reevaluated. In that case, we can expect the calculative basis of ‘cost’ to shift again as the idea of ‘cost’ from a social and environmental perspective rather than from a purely organisational perspective may gain influence.

In recasting economic history in this light, the constitutive role played by accounting-based theories of cost becomes evident. Specifically, Blue Eagle costing (full cost plus a ‘reasonable’ amount of profit), which was perhaps not an economically-sound basis for competition in a global laissez-faire free market, was a primary tool for enforcing the rules of the New Deal. This conclusion, of course, must be balanced against the social and ethical aims that the NIRA was designed to achieve in the Great Depression-Era USA.