Abstract

The much-maligned cost-plus contract used in the procurement of defence assets has received little attention in the accounting history literature focused on accounting and the military in times of war. An extensive archive of a World War 2 contract between the Australian government and the UK De Havilland Aircraft Company for the supply of Tiger Moth airframes provides an opportunity to investigate important features of this contract, including cost recording and disclosure, monitoring of cost data by government inspectors, resolution of uncontracted events and evidence of government action to mitigate risks associated with this form of contracting. We also broaden the extant literature on open-book accounting on the premise that government access to the contractor's costing system constitutes a strong subset of this phenomenon. Finally, the batch-costing techniques utilised show strong evidence of ‘learning’ in respect of direct labour costs, consistent with this feature of cost behaviour in aircraft assembly.

Keywords

Introduction

Governmental decisions in times of war are made in environments characterised by uncertainty and urgency, circumstances wholly different from those pertaining to the calmer context of peace. Procurement decisions for defence resources made under crisis-management conditions invariably test existing contractual orthodoxies, justifying departures from standard processes. With strategic and operational uncertainties unfolding in real time, alternative approaches to a multitude of decision areas may be both appropriate and necessary.

The defence procurement market, particularly for expensive items of military hardware, has special features. The demand side is ‘dominated by the single large customer [the government] … that has regulation, taxation and coercive powers’ (Demski and Magee, 1992: 732). These coercive powers, which are most likely to be invoked in wartime, are often referred to as reserve or sovereign powers. On the supply side, there may be very few enterprises with the capacity to provide specialised assets, a condition of monopsony. In the more restricted situation of a single buyer and a single supplier – not unusual with defence contracting and particularly relevant to our case study – we have a bilateral monopoly, for which Baumol and Binder (1988: 812) saw economic theory providing little guidance about negotiating strategies, with outcomes depending ‘partly on economic logic, partly on … relative power … partly on the skill and preparation of the negotiators, and partly on luck’.

In these circumstances, both contractual parties face dilemmas. Governments must recognise that dealing with few or single suppliers creates circumstances that could be exploited through opportunistic or predatory behaviour (Crocker and Reynolds, 1993), particularly when contracts are incomplete. On the other hand, contractors need to be cognisant of the powers held by governments that provide the ability to pre-empt opportunistic behaviour and potentially, via sovereign authority, compel supply via sequestration or direction of productive capacity. In short, the availability of such extraordinary powers enables governments ‘to get on with the job’ and, in extremis, to activate the ‘whatever it takes, whatever it costs’ doctrine if circumstances so dictate.

While, in peacetime, the competitive open-tender system for obtaining defence resources is widely ‘regarded as the best procedure’ (Marriner, 1980: 135), it is usually ‘slow and cumbersome’ (Taggart, 1941: 35). Wartime constraints often render open-tender impractical and subject to breakdown (Loft, 1986). The alternative cost-plus methodology, with supplier profit calculated either as a percentage of cost or the addition of a fixed fee on manufacturing costs, has been used widely in wartime defence procurement for at least a century. It was used extensively during World War 1 by the Ministry of Munitions in the UK (Boyns, 2005; Loft, 1986; Marriner, 1980) and the War Department and the Department of the Navy in the US (Taggart, 1941). It is a similar story with subsequent wars. As a policy approach, it provides relative convenience, ‘speed and flexibility’ (Scantlebury, 1943: 292; Taggart, 1941: 35) 1 and, according to Robbins (1950: 40) ‘at the outset, there is not the time to fire anything else up’.

Although the cost-plus approach is consistent with the ‘whatever it takes’ doctrine, it is fraught with the embedded risks that flow from unpredictable contractor behaviour. The ‘palpable objections to this method’ (Robbins, 1950: 40) demand risk-mitigation protocols if governments are to minimise the political and financial consequences of cost overruns on open-ended cost-plus contracts. Such steps could include, inter alia, rearrangement of institutional structures, ex-ante decisions regarding reimbursable costs, regular disclosure of costs as contracts proceed, timely ex-post verification of costs, pre-determined strictly controlled profit mark-ups and incentives for contractors to minimise costs.

With World War 2 as the historical lens, we contribute to the growing accounting history literature primarily focused on the links between accounting in wartime and accounting and the military. Specifically, we augment the very limited branch of this literature focused on cost-plus contracting. Particularly regarding scope, this oeuvre is restricted in a number of ways. While Marriner (1980), Loft (1986) and Boyns (2005) refer to the cost-plus methodology as a contracting option in the context of the development of costing during World War 1, they provide no details of actual contracts or real-world costing data. Early in World War 2, Taggart (1941) 2 reported on costing processes within the US defence realm. Although he likely had access to costing data, he focused on processes rather than actual costs. Half a century later, the Accounting Review in October 1992 hosted a forum on accounting for US defence contracts that, again, adopted a purely theoretical approach to potential contractor behaviour with respect to costs (Chwastiak, 1996).

The analysis of an extensive and publicly available archive of an early World War 2 Australian procurement contract that we undertake provides a unique opportunity to address this gap in the accounting history literature. The contract itself, between aircraft manufacturer DeHavilland Aircraft Pty Ltd (DeH) and the government of the Commonwealth of Australia (CW), was for the supply of Tiger Moth aircraft for pilot training purposes. The contractual detail provides a window through which the processes of contract evolution, cost disclosures, monitoring by government agencies, cost-reduction incentives and dispute resolution can be observed and analysed.

We commence our study by outlining the historical context within which the DeH-CW contract evolved, highlighting the multiple institutional changes that were made in the inter-war years as Australia, well aware of the dramatically changing geo-political landscape in Europe, readied itself for the possibility of total mobilisation. Next is a review of the existing scholarly literature focusing on twentieth-century costing in wartime settings as background to an explanation of the research methodology adopted. We then provide a chronology of significant events and reports related to the contract. An analysis of the progress of the contract follows, first as it relates to procurement in general in Australia in the early stages of World War 2, progressing to events related to the specific agreement, with particular focus on the costing methodology adopted by DeH that was subject to CW's monitoring. The penultimate section consists of a summary of the key findings, together with further analysis, showing, inter alia, that DeH's direct-labour disclosures provide powerful evidence that learning occurred as the contract progressed. Finally, we offer concluding comments and suggestions for further research.

Historical context

In the aftermath of World War I, and following public disquiet regarding war profiteering, particularly in the UK (Arnold, 2014) and the US (Meyer, 2017; Taggart, 1941), the complexity of managing large defence-procurement contracts and the potential for them to be mishandled was not lost on the CW. During the inter-war years, a number of changes were made to the institutional arrangements established to manage defence procurement.

Immediately after World War 1, the Board of Factory Administration was created to administer the four government munitions factories that had been judiciously retained after the conflict. Reconstituted as the Munitions Supply Board in August 1921 (Butlin, 1955; Ross, 1995), this board was responsible for, inter alia, ‘the control of contracts’ (Hasluck, 1952: 453). Government procurement processes were again transformed in May 1926 with the establishment of the Contract Board ‘to invite public tenders or quotations or otherwise arrange for the performance of services or purchase of supplies for the department [of Defence]’ (Hasluck, 1952: 452).

Further, and in anticipation of wholesale mobilisation of industry in the event of all-out war, the Principal Supply Officers Committee (PSOC) was established in March 1933 ‘to advise … on measures designed to ensure that both government factories and commercial industry would be able to provide munitions on a scale adequate for the country's defence’ (Mellor, 1958: 27–8). The third step in the pre-war re-organisation of procurement generally, and munitions specifically, came in early 1938 with the establishment of the high-level Advisory Panel on Industrial Organisation to advise on the ‘broader principles of the work of the PSOC’ (Hasluck, 1952: 446).

At the outbreak of war in September 1939, Australia faced enormous challenges in bringing the economy onto a war footing. Extraordinary levels of expenditure would be required (Grey, 1999), largely for the procurement of materials for the Armed Forces. The munitions manufacturing capacity in the country was limited to the four CW-owned establishments which, collectively, could not deliver self-sufficiency. The bulk of supply would have to be sourced from the private sector which, hitherto, had been deliberately excluded from the manufacture and supply of munitions. 3

Cognisant of these complexities, the CW decided in September 1939 to suspend the preferred open-tender system administered by the Contract Board in favour of contracting on the much-maligned cost-plus basis. Henceforth, all contracts were to be written on a cost-of-production-plus-a-percentage-of-cost basis in full knowledge of the potential challenges and risks the approach entailed, particularly when it came to defining allowable costs, specifying acceptable profit margins and managing contractor behaviour.

Much of the expenditure about to be incurred in this revised manner would be on air services and various configurations of aircraft. 4 Gillison (1962) reports that in the lead-up to World War 2, the CW was committed to the expansion of the Royal Australian Air Force (RAAF), but Stephens (2001) notes, critically, that the country's dependence on UK technology was a significant limitation to this commitment being met. Local aircraft manufacturing capacity then comprised only three relatively small entities. Consequently, there was limited capacity to increase output in a timely manner if circumstances became more urgent (Mellor, 1958).

This local manufacturing triumvirate comprised the Aircraft Construction Branch (ACB), 5 the Commonwealth Aircraft Corporation (CAC) and DeH. The ACB was replaced in March 1940 with the Aircraft Production Commission (APC), a statutory body established under the remit of the Minister of Supply and Development. By August 1941 the APC was fabricating Bristol Beaufort bombers under licence from the UK manufacturer. From July 1939, the privately-owned CAC was producing what was known domestically as the Wirraway, an advanced two-engine trainer, with limited combat capability, based on a US design (Abbott and Bamforth, 2022). Some 755 units of this aircraft would be manufactured in the next seven years (Hill, 1998).

The final member of this grouping was the Australian subsidiary of the UK-parented DeH which had operated in Australia since 1927. In the inter-war years, DeH had been assembling DH-82 Tiger Moths and DH-94 Moth Minors for the UK and Australian markets. In early 1939, the company provided 20 Tiger Moths to the RAAF, largely assembled from parts imported from the UK but with mainplanes (main wings) fabricated locally (Mellor, 1958). The Tiger Moth, a single-engine dual-cockpit biplane with no combat capability, was the initial trainer of choice for both the UK's Royal Air Force and the RAAF. 6 That the Tiger Moth was the only basic trainer considered by the RAAF, and DeH was the only supplier, meant that the relationship between the parties was that of bilateral monopoly.

The level of familiarity with the Tiger Moth by the RAAF as operator, and experience with assembly, and to a limited degree, manufacture, by DeH, is important background to our analysis of contractual relations during 1939–41 between the CW and DeH. This contract, commencing with a ‘handshake’ agreement in early October 1939, was initially for the procurement, via local manufacture, of 350 Tiger Moth aircraft which was quickly revised to airframes only (aircraft less engines and instruments), then expanded to 450 airframes. The contract, which was written on a cost-plus basis consistent with the September 1939 policy change, was followed by additional orders from the UK government for 581 airframes. To retain tractability, we restrict our coverage to the RAAF order for 450 airframes.

Literature review

The small but emerging body of work focusing on the links between accounting and the military, and accounting and war, provides the backdrop to our investigation. Within a World War 2 context, the Cobbin and Burrows (2018) review of the literature in this domain cites investigations covering efficiency (Cobbin, 2009; Foreman, 2001; Miley and Read, 2012; Tyson and Fleischman, 2006), accounting procedures (Cinquini et al., 2016; Djatej and Sarikas, 2009; McWatters and Foreman, 2005), gender (Flesher and Previtts, 2014; Ikin et al., 2012) and culpability (Lippman and Wilson, 2007; Tyson and Fleischman, 2006).

Wartime settings have provided fertile ground for scholarly investigations into costs and costing. It is often argued that the events of World War 1 and the inter-war years influenced the events of World War 2 and its aftermath. For example, Marriner (1980: 139) articulates the extensive efforts made by the Ministry of Munitions in the UK during World War 1, including its claim to have so improved costing practices in munitions factories that, by war's end, it had ‘introduced British industry to best-practice cost accounting’. Marriner (1980) cautions that this claim is debatable and that, post-war, costing practices regressed. Similarly, Loft (1986: 165) suggested that costing had attained a very high profile and ‘come into the light’ in the war years, playing a critical role in measuring costs and identifying profiteering. Loft noted also that costing played a significant role in post-war reconstruction in Britain but that its legacy may be problematic. Marriner (1980) and Loft (1986) were the focus of Boyns (2005: 128) who provided an additional argument that ‘accounting change [costing] was generally evolutionary in nature, and that any changes … were merely part of on-going evolutionary changes’. Fleischman and Tyson (2000), in the context of a UK-US comparison of costing during and immediately after the war, concur with both Marriner (1980) and Loft (1986), finding that costing made a significant contribution to the war effort, albeit to a greater extent in the UK than the US, but they retain reservations as to the enduring legacy derived from the war effort.

In relation to World War 2, the cost coverage is slim. At a national level, two articles deal with the exercise of sovereign power in extremis. Djatej and Sarikas (2009) describe how the totalitarian Soviet Union pursued a policy of victory at all costs in which failure was not condoned. Further, a costing methodology that dramatically simplified the allocation of common costs was ruthlessly imposed on armaments suppliers in a process that bore no resemblance to reality. Similarly, Cinquini et al. (2016) examine how the Italian Fascist regime imposed a unified costing system imported from Nazi Germany, intended more as a means of control over all manufacturing activity than as a resource for delivering accurate measures of costs.

At the firm level, first-hand experience in the major US defence contractor, Basic Magnesium, Incorporated (BMI), was the basis for Fagerberg's (1990) report on important contributions made by cost accountants and costing to the war effort. He provides rare real-world details of the BMI's costing structure, nature of costs and product-flow patterns. In another single-firm study, Fleischman and Marquette's (2003) analysis of the Sperry Corporation, a major US defence contractor, demonstrated how a supplier claiming to utilise advanced management techniques did not apply standard costing, including variance analysis, as part of its purported scientific-management methodologies.

Just before the US entered World War 2, Taggart (1941) provided a contemporaneous, in-house account of the approach to cost-plus contracts adopted by the US government as it scaled up production to provide vast amounts of defence resources to the UK and its Allies under the Lend-Lease programme. From an insider's perspective, Taggart (1941) reported the use of a variety of strategies to counter supplier-profiteering that characterised procurement during World War 1 (Arnold, 2014; Meyer, 2017). Among these strategies were: cost-plus-fixed-fee contracts which capped profits but not costs; incentivising cost reductions by sharing cost savings between governments and contractors; specifying allowable elements of cost; fixed-price contracts; and specifically outlawing cost-plus-percentage-of-cost contracts. Another potential strategy, identified only with Britain was the so-called target price system (Taggart, 1941).

While Taggart's (1941) Accounting Review article was inexplicably overlooked in the same journal's 1992 forum on Accounting for Defense Contracts, the latter can be seen as a follow-up to his work but within the wider context of procurement in both peace- and war-time settings. Primary contributions were provided by Thomas and Tung (1992), Rogerson (1992) and Reichelstein (1992), with Demski and Magee (1992) and Lichtenberg (1992) providing alternative perspectives. Generally, the forum adopted a theoretical approach, emphasising strategies used by contractors in dealing with governments, and by governments in countering suppliers’ profiteering attempts. Particularly highlighted was the potential for suppliers with both government and non-government customers to pad out programme costs to governments (Rogerson, 1992; Thomas and Tung, 1992). This cost-shifting was achieved, for example, through charging higher labour and/or overhead rates on government contracts (Rogerson, 1992) or manipulating pension costs between government and non-government contracts (Thomas and Tung, 1992). These theoretical views were supported by Lichtenberg's (1992) empirical analysis that showed high rates of profitability employed by defence contractors, irrespective of whether they also engaged in non-government projects. Demski and Magee (1992: 732) observed that ‘pricing practices [costing-plus] in this industry [defence] may lead to serious distortions’. 7 As to why these distortions occur, Rogerson (1992: 672) observed that ‘auditing is very poorly equipped to deal with this type of behaviour … [it] is relatively good at determining whether the firm actually spent as much as it projected … [but] relatively poor at determining whether any expenditure that actually occurred was necessary’. This assertion raises the obvious question of what alternative cost-verification procedures should be implemented. The literature on this point is virtually non-existent, another informational void that we attempt to remedy.

These pre-2000 contributions dealt with procurement generally and provided little real-world cost data or details of wartime buyer-seller interactions in relation to specific programmes. Several more recent contributions partly fill this void. Vollmers et al. (2016: 735) investigated Italian World War 1 contracting processes for naval and military hardware with a major contractor, Ansaldo, in an ethos characterised by ‘lobbying, collusion, bribery and private interests … instead of efficiency, accountability and honesty’. Contracts were awarded by non-competitive private-treaty processes. In making bids, Ansaldo, while ostensibly using cost-plus pricing, failed to allocate all overhead cost pools to products. While Ansaldo extensively cost-shifted between products, ironically the major consequence of its approach was severe under-costing of products, causing it considerable financial distress. Predictably, there was no governmental monitoring of the suppliers’ financial claims.

The investigation by Noguchi and Boyns (2012) of Japan's financing of strategically important maritime and aviation services during 1928–1945 focused on budgetary processes and utilisation. These services were undertaken by semi-public entities which received annual subsidies based on budgeted revenues and expenditures. Pre-1938, budgets prepared for this external purpose were not utilised internally for control purposes and were, invariably, highly inaccurate. Changes in the organisational structure of aviation during 1938–41 expanded the operations of the key provider, Japan Airways, but also brought much tighter bureaucratic scrutiny, improved the detail and quality of budget estimates and enhanced the role of budgets for internal control.

Relatedly, the account of Noguchi et al. (2015) of World War 2 controls on Japanese industry showed that, for Mitsubishi's Nagoya Engine Factory, the Japanese government instituted a regime of strict controls, including oversight of cost-plus contracts. Controls included profit caps of approximately five per cent, the government having the statutory right to inspect accounting records and the supplier receiving a one-third share of any cost-savings on contracts. However, no detail is provided regarding the extent to which these provisions were exercised.

The picture that emerges from the accounting-related procurement literature is of incentives to overcharge on cost-plus contracts, confirmed by limited empirical evidence that this occurred. Nevertheless, this literature is characterised by a paucity of disclosure data because investigations to date have lacked in-depth analyses of actual programmes based on archival data. A related coverage void concerns the extent to which contractual disclosures were actually made, and the degree to which they were subject to examination either by conventional auditing or alternative assurance/inspection processes. Likewise, manifestations of sovereign power in contractual negotiations and processes have received little attention. Similarly, studies are lacking on how contractual negotiations and relations play out in bilateral monopolies, particularly for financial matters for which there are no express contractual provisions.

In addition to the primary governmental procurement focus of our investigation, our analysis potentially complements an area of accounting research that we consider to be ahistorical: open-book accounting (OBA). OBA has been defined by Caglio and Ditillo (2012: 62, n.1) as ‘all “private” management accounting information exchanged between collaborating firms’ and described by Agndal and Nilsson (2010: 149) as a ‘purchasing tool’. Elaborating on this concept, Windolph and Moeller (2012) view OBA as a strategy in which enterprises increasingly specialise in core competencies while contracting out (or outsourcing) activities considered non-core to legally separate entities beyond the firm's boundaries.

Arguably, any cost disclosures associated with cost-plus procurement contracts, particularly when buyers have access to suppliers’ costing systems and source documents, have OBA characteristics. Yet OBA has neither a presence in the accounting history historiography nor links to the procurement literature. From a historical perspective, we consider contestable the assertion by Kajuter and Kulmala (2005: 182) that OBA is ‘a fairly new phenomenon … disclosing this [cost] data to supply chain partners is a practice that appeared with the spread of lean production and supply in the 1990s’. We show that OBA – defined broadly – has a much longer history.

Methodology and archival sources

The principal source of our case study material is file MP287/1, 219 Part 2 in the National Archives of Australia (hereafter the archive or NAA), containing 249 pages of documents, including duplicates, related to the contract which, essentially, constitutes the CW's record of its dealings with DeH. Although the archive contains few original documents from DeH, the CW's responses frequently refer to communications from DeH, including dates and key points facilitating the construction of a reasonably comprehensive chronology. Despite the final signed contract not having been located, exchanges in the archive indicate that DeH executed the final contract for signing by the CW in late April 1942, 8 almost a year after all the contracted work had been completed. Overall, the archive provides a rich source for examining a wartime cost-plus contract from a variety of perspectives.

Each author separately reviewed all archival documents to identify inclusions pertaining to negotiations over contract terms especially in relation to costs or profits; cost disclosures sought or provided; levels of physical production achieved; monitoring and assurance/cost inspection processes; and examples of what could be construed as the exercise of sovereign power. 9 When compared, there was a high degree of unanimity with differences resolved by discussion.

Being able to draw on a comprehensive and publicly accessible archive meant that the problem of data collection was obviated, and we did not have to engage in what Scapens (1990: 274) termed the ‘social process’ of interviews to collect data. Nor was there any commercial-confidentiality constraint on the use of archival information. However, we acknowledge the limitation raised by Otley and Berry (1994: 48) in relation to single-organisation case studies: that ‘the context is particular’, affecting the generalisability of any findings. In our analysis, we draw attention to relevant particularities when attempting to draw lessons for contemporary theory and practice.

Key participants

De Havilland Aircraft Pty Ltd (DeH)

As the Australia-based fully owned subsidiary of its UK parent, 10 DeH had operated in Sydney, New South Wales, since 1930 (Mellor, 1958; Sharp, 1960) where all Tiger Moth production activity occurred. Prior to October 1939, DeH's Australian operations had largely involved assembling aircraft from imported components augmented by local manufacturers for relatively small orders. DeH also had approximately 30 tradesmen employed on servicing an average of 20 aircraft per month. For the quadrennium ending 30 June 1939, DeH's annual sales turnover averaged £66,000 11 (Jones to Chairman, Accountancy Advisory Panel, 24 November 1939). At prevailing prices, the October 1939 order – later estimated to take 21 months to complete – was likely to generate revenue of at least £450,000, requiring a roughly fourfold increase in DeH's operations. While many components, particularly engines and instruments, would still be imported initially, there was to be increased local content, largely through sub-contractors, with final assembly by DeH.

Correspondence involving the company was conducted by its general manager, Major A Murray Jones, 12 who in earlier careers had been variously a pharmacist, highly decorated World War 1 aviator, commanding officer of the main RAAF air base adjacent to Melbourne and then superintendent of flying operations in the Department of Civil Aviation (Isaacs, 1983).

The Commonwealth of Australia (CW)

While all contractual negotiations and processes were in the name of the CW, in practice these roles were conducted by its specialist agencies, primarily the APC and the Accountancy Advisory Panel (the Panel) in the Department of Supply and Development.

The APC was established on 21 March 1940 to control the production of aircraft and aero engines in Australia. During 1940–41 much of its correspondence was via either its chairman, HW (later Sir Harold) Clapp, a former Chief Commissioner of the Victorian Railways (Adam-Smith, 1981), or its deputy-chairman, JS (later Sir John) Storey, 13 previously director of manufacturing for General Motors Holden (GMH), the Australian subsidiary of the US General Motors Corporation (Lack, 2002). Also featured in the chronology is the APC's cost accountant, F Gundill, 14 who had primary responsibility for monitoring and assessing DeH's financial claims and disclosures, AV Smith, 15 APC Commissioner and F Saleeba, Principal Legal Officer for the APC.

The Panel was established on 25 May 1939 under the Supply and Development Act 1939, 16 ‘to advise on the scheme of costing and profit control for the production of munitions by private industry in an emergency’. 17 It was established three months before the commencement of hostilities to provide technical accountancy advice designed to pre-empt the profiteering that occurred in World War 1 procurement contracts while remunerating private contractors on a fair and reasonable basis in a timely manner. Five members were appointed to the Panel. Three prominent practising chartered accountants, EV (later Sir Edwin) Nixon (chairman), SW Griffith and TD Hadley, whose audit clients included leading manufacturers, were joined by DJ Nolan, the head of the Sydney County Council's electricity authority, and LA Schumer, the general manager of a large national road-transport firm and author of Cost Accounting (Schumer, 1935), the first major cost accounting text published in Australia (Anderson, 2002). While panellists had no apparent first-hand knowledge of aircraft production, their collective experience was in other respects broadly based.

Contractual events and developments

On 8 September 1939, five days after Australia declared war on Germany the Panel presented its first report

18

(Accountancy Advisory Panel, First Report, 1939a) outlining what were, from the CW's standpoint, the desirable principles of procurement contracts in general, namely:

An allowed rate of profit of at least 4 per cent, ‘although this percentage may need to be varied’; Target costs being set and revised as production progressed; Savings from productivity improvements being shared, providing an incentive for suppliers to lower costs; Benchmarking (including international comparisons); The Commonwealth has the right to inspect contractors’ and subcontractors books and accounts.

Although it was not explicitly stated in the report, these principles are all consistent with the concept of cost-plus contracting. The final principle, the right to inspect contractors’ books and accounts, represents a very strong form of OBA, although this provision was framed as an (optional) reserve power. The similarity between these principles and those cited by Noguchi et al. (2015) of World War 2 controls of Mitsubishi's Nagoya Engine Factory is striking, notably concerning profit margins, the right to inspect accounting records, and the sharing of cost-savings between the parties. Similarly, the setting and revision of target costs resemble the British practice referred to by Taggart (1941), although whether the contemporary British approach actually pre-dated the Panel's first report is unknown.

Contract development

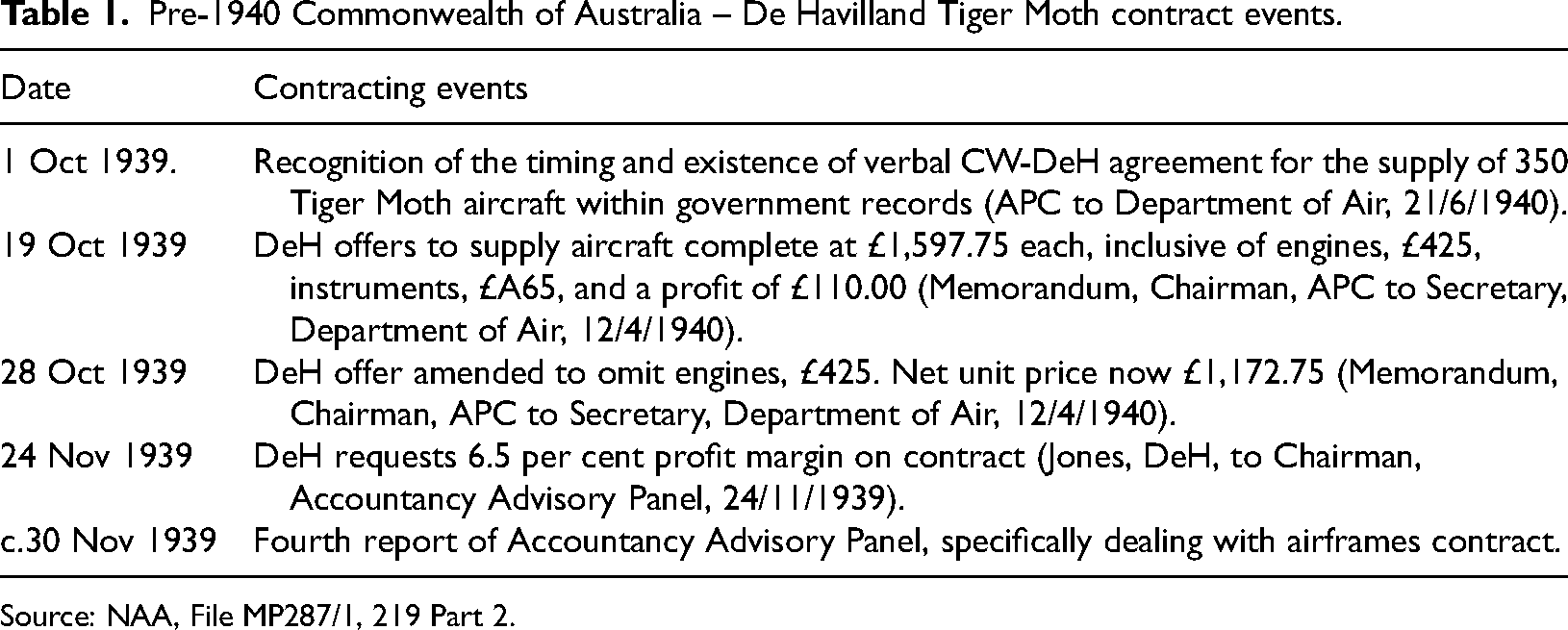

While the early engagements had been informal and verbal, CW War Cabinet Minute No. 32 dated 10 October 1939 placed on record the prior discussions between the CW and DeH, thus formally approving the ‘arrangements for the manufacture of 350 Tiger Moth airframes’. (NAA: A5954, 803/1). Early events in relation to the airframes contract are set out in Table 1.

Pre-1940 Commonwealth of Australia – De Havilland Tiger Moth contract events.

Source: NAA, File MP287/1, 219 Part 2.

Curiously, the first reference in the archive to the initial CW-DeH ‘handshake’ agreement is, as noted in Table 1, a much later record (APC to Department of Air, 21 June 1940) which described how: On the 1st October 1939, [actually 10 October], War Cabinet approved of the local manufacture of 350 Tiger Moth Airframes, and the General Manager of De Havilland Aircraft Pty Ltd (Major Murray Jones) was verbally advised to proceed with manufacture on the basis of minimum profit – a target cost and savings to be shared on an agreed basis.

Particularly noteworthy are both the informality of the initial agreement and its brevity with only a selection of the desirable contractual principles as recommended in the Panel's first report, referenced. No specific metric for the rate of profit was recorded. Nor was there any mention of the CW having the right to inspect DeH's books and accounts, although this element may have been assumed by the parties. Moreover, the record is inaccurate in referring to the manufacture of airframes. DeH's offer of 19 October 1939 was clearly for complete aircraft, suggesting that this was the basis of initial CW-DeH discussions. The offer was amended, without challenge, eleven days later to omit engines.

The Panel's first report referring to a minimum profit rate of 4 per cent with the possibility of variations, created an obvious area of negotiation between the parties. DeH's initial offer to provide complete aircraft for £1,597.75, including a unit profit of £110, implied a profit margin of 7.39 per cent (£110/£1,487.75). DeH's subsequent request on 24 November 1939, with engines omitted, was for a profit rate of 6.5 per cent. This was among the matters discussed at Panel-DeH meetings on 23–25 November 1939 which resulted in the Panel's fourth report (Accountancy Advisory Panel. Report No. 4, 1939b), specifically directed at the Tiger Moth contract. In contrast to the Panel's first report, which had the status of a Command Paper (one presented to parliament), the fourth report was more in the nature of a record of a meeting, although this is not to downplay its importance as a contractual element. A key passage in the fourth report (Accountancy Advisory Panel. Report No. 4, 1939b: 1–2) was that: The Panel is of the opinion that it may not be possible to arrive at a reliable estimate of cost on the completion of the first 50 airframes. It is reasonable to assume that as the work proceeds efficiency will improve and for this reason it recommends that the Airframes should be costed in batches so that the cost may be frequently reviewed. The following allocation has been discussed with and agreed to by the General Manager of the Company:

(a) The first 50 Airframes to be supplied at a firm price; (b) On completion of the first 50 Airframes a Target Cost should be fixed which should apply to the second batch of 50 Airframes; (c) On completion of the second batch of 50 Airframes the Target Cost should be reviewed and, if necessary, amended and each amended cost should apply to a third batch of 100 Airframes; (d) On completion of the third batch of 100 Airframes, the Target Cost should again be reviewed and, if necessary, amended … [to] apply to a fourth and final batch of 150 Airframes.

It is emphasised that the term target costs as used by the Panel in relation to future costs differs from what it nowadays suggests to management accountants, that is, a holistic approach to design, supply-chain management and manufacturing to produce a new product to fill a market niche at a competitive price (Burrows and Chenhall, 2012). In the Panel's first report (Accountancy Advisory Panel. Report No. 4, 1939a: 6), target costs were defined as ‘the sum of direct materials, direct wages, overhead charges and administrative expenses based on a high but attainable standard of efficiency and on a stated volume of production’. 19 While this definition embodies elements of standard-costing principles, targets were not intended to be incorporated into DeH's costing system in the manner of standard costs. Rather, targets were simply benchmarks intended to incentivise DeH to lower costs. Targets/benchmarks were the reference points to be used for the purpose of calculating the parties’ shares of any cost savings when actual costs were below benchmarks. However, at this stage, no sharing formula had been determined. Presumably, if costs were above benchmarks, then DeH would be reimbursed for its actual costs plus the final agreed profit margin.

Although the report notes DeH's agreement with the concept of batch costing, it also records disagreement in relation to the rate of profit. The Panel recommended that DeH receive a profit of five per cent on cost – identical to that allowed on Japanese defence contracts (Noguchi et al., 2015) – but with interest on capital and borrowings excluded from the cost base.

The Panel's first report had flagged that contractors’ and subcontractors’ books and accounts should be open to the CW's inspection. In the Panel's fourth report (Accountancy Advisory Panel. Report No. 4, 1939b: 5) this requirement was phrased as the CW having ‘the right to inspect the books and accounts of the Contractor and, if required, of any sub-contractor’. Significantly, this imperative was still framed as a reserve power: while the CW had the right to inspect, it did not follow automatically that this right would be exercised.

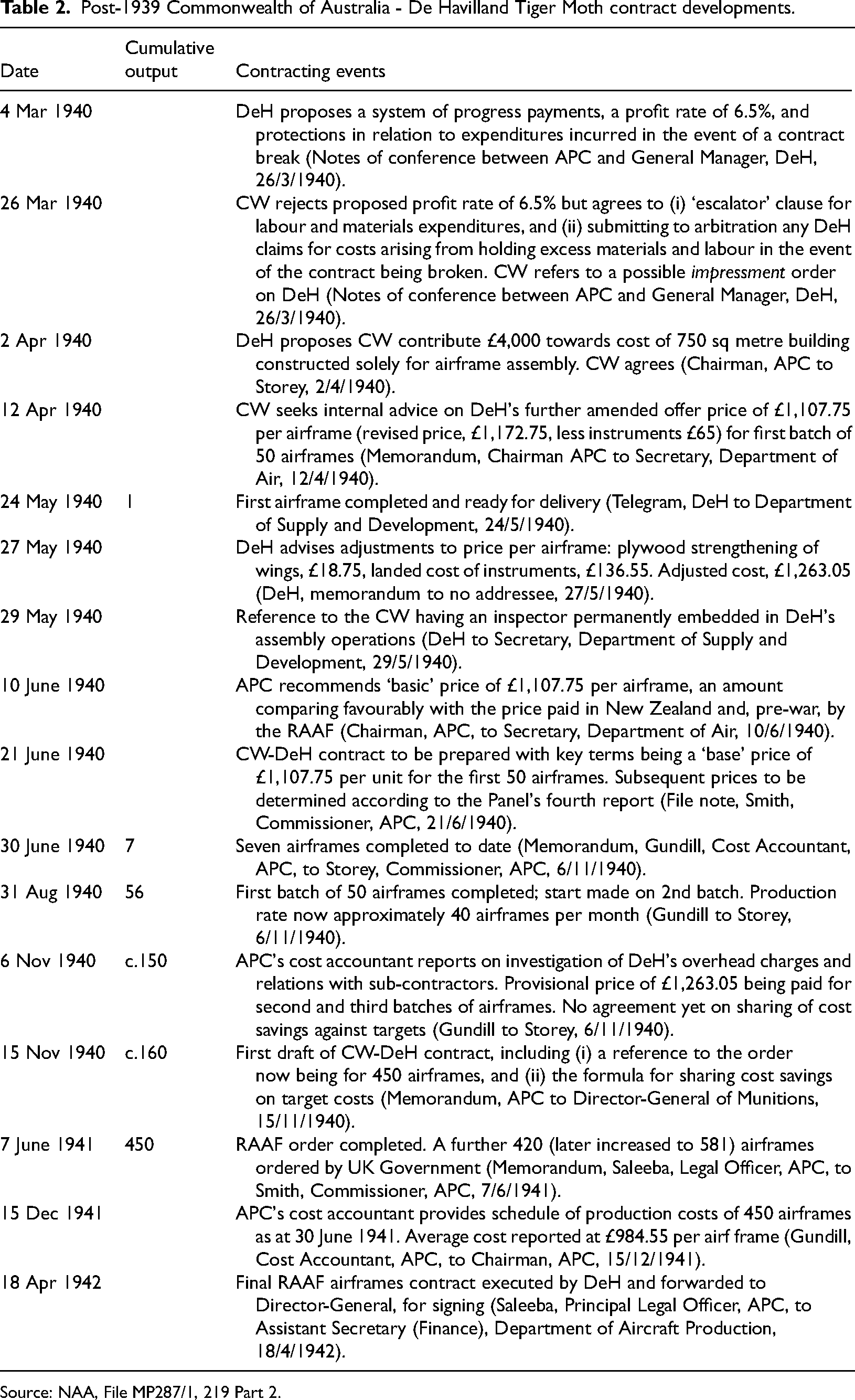

As to the costing detail required of DeH for both actual and target costs, the Panel recommended that direct material, direct labour, other direct expenses and overhead expenses be shown separately. Allowable overhead expenses were defined as ‘such proportion of all other expenses incurred by the Company as may fairly be attributed to any particular Airframe or batch of Airframes’ (Accountancy Advisory Panel. Report No. 4, 1939b: 2). Subsequent contractual developments are summarised in Table 2 with cumulative output (sometimes estimated on the basis of a production of 40 airframes per month) shown to provide context.

Post-1939 Commonwealth of Australia - De Havilland Tiger Moth contract developments.

Source: NAA, File MP287/1, 219 Part 2.

The record of CW-DeH discussions on 4 March 1940, as well as referencing DeH's requested profit rate of 6.5 per cent, also includes the only explicit reference in the archive to the possible use of sovereign power. The actual words were: Mr Smith [of the APC] pointed out that the commission has gone a long way in meeting all the suggestions put forward by the Company. It would be unsatisfactory from all angles if the government were compelled to place an impressment order on the Company (emphasis added).

The Oxford English Dictionary's definition of impressment – to ‘seize (goods) etc.) for royal or public service’ – certainly implies a serious threat if the use of the word was considered and deliberate. While the CW undoubtedly had the sovereign power to sequester DeH's resources, it would have faced formidable consequences had it done so. Another sovereign power – the UK government – would doubtless have objected to this treatment of a subsidiary of one of its key defence contractors. Further, DeH was still in the process of receiving components from its UK parent which may have been disinclined to continue deliveries. Finally, any prospect of future CW-DeH collaborations would have been imperilled. 20

The first record in the archive of any access by the CW to DeH's private accounting information is a 1200-word memorandum, supported by five schedules, dated 6 November 1940, prepared by the APC's cost accountant, F Gundill, following an investigation into the costs of the first 50 airframes claimed by DeH (Gundill to Storey, 6 November 1940). The memo noted that agreement had still to be reached on (i) DeH's claim that interest on borrowings should be included in the costs of production, and (ii) how cost savings against targets should be distributed between the parties, and that aggregate airframes production had been 7 units to 30 June and 56 units to 31 August.

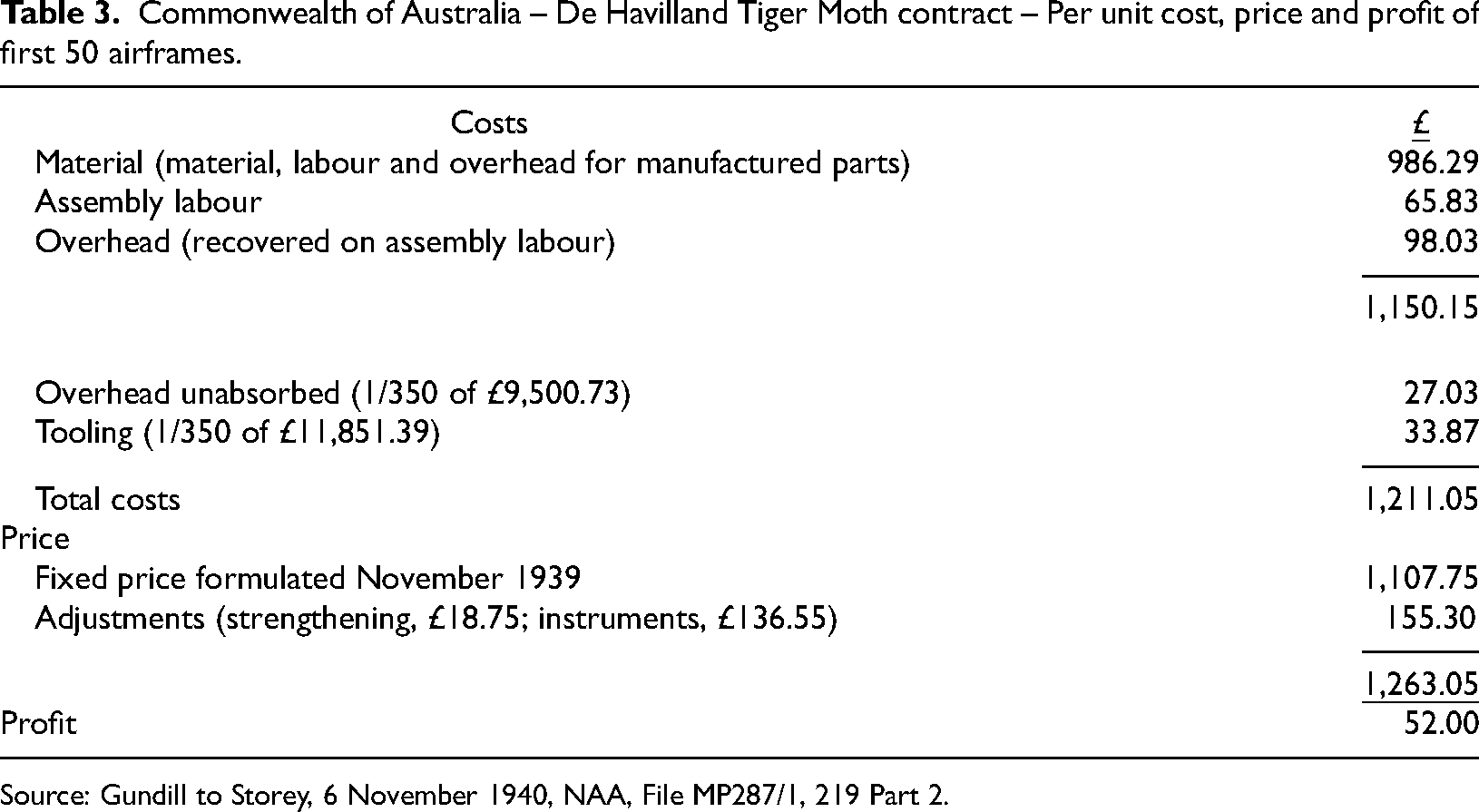

Schedule I attached to the memo showed the average unit cost and profit to DeH of the first 50 airframes. The details, slightly reformatted, appear in Table 3.

Commonwealth of Australia – De Havilland Tiger Moth contract – Per unit cost, price and profit of first 50 airframes.

Source: Gundill to Storey, 6 November 1940, NAA, File MP287/1, 219 Part 2.

Context to these amounts is provided by Gundill's covering notes and five schedules, detailing capital and overhead expenditures, depreciation rates and lists of sub-contractors. His coverage largely concerned overheads, which were essentially divided into three pools: general overheads, factory overheads and depreciation of buildings, the latter slightly anomalous given that the CW had committed to pay £4000 towards the cost of the specially constructed building which had a book value of £4800. DeH would then have to pay rental to the CW, so depreciation may have been an interim charge while rental arrangements were being finalised.

DeH's overheads incurred for operations to 31 August 1940 totalled £55,812, comprising general overheads, £16,841, factory overheads, £37,728 and depreciation £1,243. General overheads, with interest as a line item, encompassed all DeH's activities, including its ongoing repairs and maintenance work. Factory overheads and depreciation are related solely to the airframes programme. In its preliminary cost figures, DeH had allocated £10,426 of general overheads to the airframes programme, some 61.9 per cent of the total. In his calculations for Table 3, Gundill had deducted interest of £1,539, leaving £8,887 of general overheads charged to the programme, a rate of 58.1 per cent of allowable general overhead (£8,887/£15,302). It can be inferred that Gundill considered that the general overhead charged to the airframe contract was reasonable in relation to the proportion of DeH's business represented by the RAAF order.

The archive holds no clear statement concerning which parts were fabricated by DeH as opposed to sub-contractors. CW-DeH exchanges over the specifications for materials utilised for wings and fuselages suggest that these components were fabricated by DeH itself in the building dedicated to the programme. Gundill's listing of 62 sub-contractors shows that tyres and tanks for fuel and oil were among the items sub-contracted. Separately, engines and instruments were supplied at the CW's expense.

Another gap in the archive is information concerning DeH's internal costing system. From Gundill's examination of overhead, it is clear that factory overhead was the largest single expense item. While it is not precisely comparing like with like, a simple comparison between the total production cost allowed for the first 50 units, £60,550 (50 × £1,211) with factory overheads to 31 August, £37,727 (for 57 airframes plus work-in-progress), illustrates the latter's dominance over materials and direct labour. As between fabrication and assembly, comparing assembly overhead charged to the first 50 units, £4,900 (50 × £98), and total factory overhead for the programme, £37,727, indicates that most factory overhead was charged to fabrication rather than assembly. In Table 3, the (imputed) overhead absorption rate for the assembly operation was 148.9 per cent of direct labour (£98.03/£65.83), suggesting that the intended rate may have been 150 per cent but that a slight arithmetic inaccuracy occurred.

A further aspect of overhead accounting explained in Gundill's memo was that, out of total overheads of £47,549 incurred to 31 August 1940, some £9,500.73 remained unrecovered at the end of this period. Gundill observed that: This over-run could reasonably be regarded as ‘preliminary expense’ in getting premises ready for production at a higher rate, training of employees, etc., and sundry non-recurring expenses, and, for this reason, it is proposed to spread the amount equally over the production of the 350 airframes originally contracted for. This method is preferred, as it gives a definite starting point, from an accounting standpoint, from 1st September for future cost calculations.

This treatment apparently met with Gundill's acquiescence. More broadly, it accords with Williamson's (1979: 240) concept of a set-up cost whose benefits ‘can be realized only so long as the relationship between the buyer and seller … can be maintained’. As such, under-absorbed overhead can be considered as a relationship-specific asset arising from an accounting artefact. Evident from Table 3 is the similar treatment applied to programme-specific tooling, £11,851, which is allocated over the first 350 units rather than being included in the more general overhead rates.

Table 3 shows that the earlier agreed amount of £1,107.75 remained the default unit price with subsequent variations, such as wing stiffening, treated as variations payable by the CW. The inclusion of the cost of instruments indicates that, notwithstanding earlier intentions, DeH rather than the CW had procured these components for which it sought reimbursement.

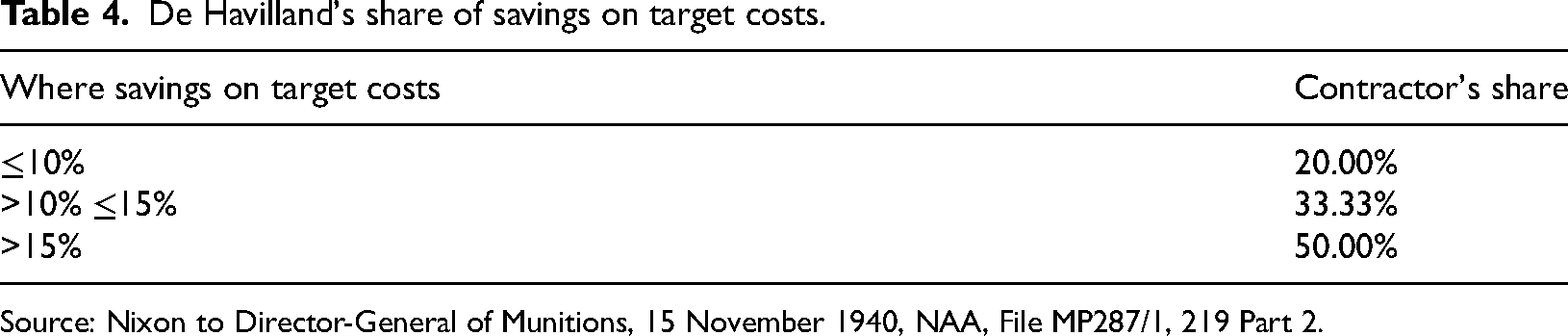

The extent to which production had outrun contractual processes is illustrated by agreement as to the sharing of cost savings against targets only being reached on 15 November 1940, by which time approximately 160 airframes had been completed. The actual formula is shown in Table 4.

De Havilland's share of savings on target costs.

Source: Nixon to Director-General of Munitions, 15 November 1940, NAA, File MP287/1, 219 Part 2.

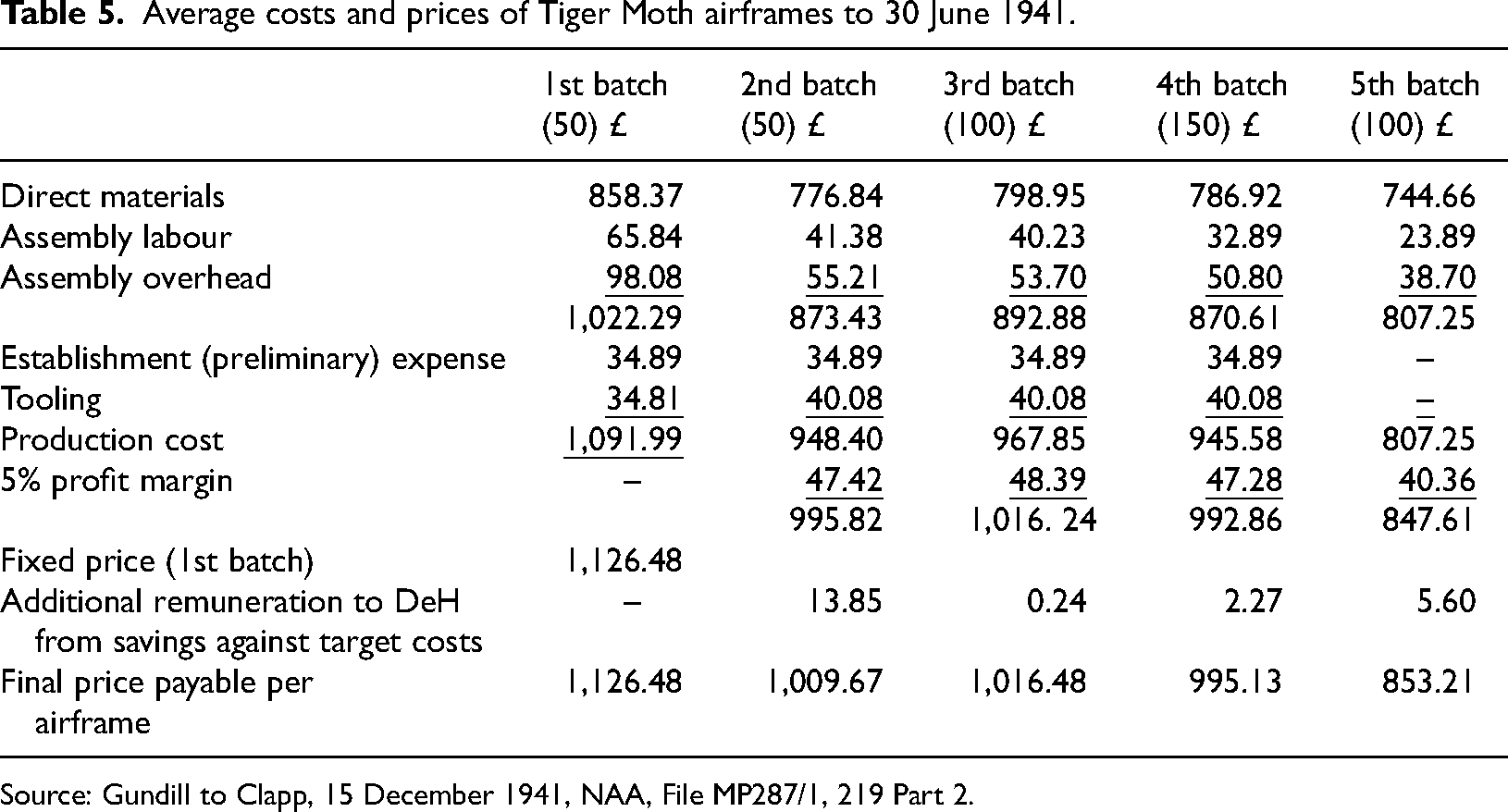

The next cost disclosure appearing in the archive, dated 15 December 1941, comprises a schedule showing the costs of, and prices paid for, the 450 airframes which had been completed by 30 June 1941. Slightly reformatted, it is shown in Table 5.

Average costs and prices of Tiger Moth airframes to 30 June 1941.

Source: Gundill to Clapp, 15 December 1941, NAA, File MP287/1, 219 Part 2.

One obvious difference compared with the earlier disclosures shown in Table 3 is that the average unit material cost for the first 50 units has been revised down to £858.37 from the original £986.29. The major causes of this reduction of £127.91 could have been finalising the bill of materials or eliminating the contract variations of £155.30 relating to instruments and wing stiffening which Table 3 suggests were included in the original material costs. Alternatively, deliberately overstating material costs for the first 50 units may have been an opportunistic act by DeH to maximise its early payments from the CW.

Another difference, but with no accompanying explanation, is that overheads for batches two and three were applied at an imputed rate of 133.33 per cent of assembly labour compared to 148.9 per cent used for the first batch, whereas for batches four and five the respective overhead rates were 154 per cent and 162 per cent. Unlike Table 3 which included unabsorbed overhead of £9,500, Table 5 shows no figure for under- or over-absorbed overhead. Had the former occurred, DeH would undoubtedly have sought additional compensation. A possible explanation for the anomalous overhead rates applied to batches four and five is that they were calculated so as to exactly apply overhead incurred over the RAAF order. If so, there must have been discussions between the parties which were undocumented. Gundill's covering notes to the information summarised in Table 5 make no mention of any forensic investigation of DeH's costs similar to that undertaken in connection with Table 3, suggesting that the Table 3 monitoring was a once-only process.

Table 5 also indicates that DeH bettered target costs, and earned additional remuneration, on all batches following the first batch. However, the modest sums involved suggest that all amounts fell into the first band of the formula shown in Table 4, that is, cost savings of less than 10 per cent on target costs, of which the contractor's share was 20 per cent. This impression is confirmed by Gundill's covering note which states that ‘savings on target prices have been shared, the Company receiving 20 per cent of the total savings and only in the case of the second batch has any substantial amount been allowed to the Contractor’ (Gundill to Clapp, 15 December 1941).

Discussion of findings

Gundill's detailed inspection of DeH's costing records, overhead treatments and relations with sub-contractors went well beyond what could be expected of an external auditor. As such it represents additional monitoring by a costing expert and can be regarded as a particularly strong form of OBA. He appears to have had full access to what would normally be regarded as private accounting information.

While it is impossible to be definitive in the absence of individual cost-line data about DeH's total operations, including its regular maintenance and repair work, Gundill's involvement and the fact that all Tiger Moth assembly and in-house fabrication occurred in the building erected specifically for this purpose would have largely constrained any over-charging by DeH through the tactic of cost-shifting cited by Rogerson (1992) and Thomas and Tung (1992) in connection with US defence procurement. Although cost shifting through DeH over-charging general overheads to the airframes contract remains a possibility, the fact that Gundill made no objection to the allocation suggests that he found it reasonable. Further support for this proposition lies in the fact that the archive is absent any evidence of conflict or dispute over claims for payment as batches were completed. Material within the archive suggests that as costs were agreed upon, claims for payment were settled in a timely manner and that the process of oversight facilitated the government philosophy of remunerating DeH on a fair and reasonable basis. DeH was evidently satisfied with the remuneration outcomes.

Another element of contract monitoring emerging from the airframes contract is physical inspection. The responsible body for aircraft certification was the CW's Aeronautical Inspection Department (AID) (Mellor, 1958). Where this process occurred for the airframes contract is indicated in correspondence relating to DeH's first claim for a progress payment which referred inter alia to the AID's ‘resident Inspector-in-Charge’ (DeH to Department of Supply and Development, 29 May 1940). The implication is that the CW had a quality-control inspector permanently embedded within DeH, monitoring its assembly operations. This additional monitoring element does not appear to have been the subject of research interest in the procurement and OBA literature.

With hindsight, the costing guidelines provided by the Panel's first and fourth reports were important elements in creating a contractual template between the parties and obviating many areas of potential dispute. The sophistication of the CW's dealings with DeH is evident in the incentive provided to the latter to achieve cost reductions and to share the savings that resulted. Contrasted with Taggart's (1941) revelation of the US practice of sharing cost savings via a simple 50:50 split and the Noguchi et al. (2015) observation of a 1:2 sharing of savings between the contractor and government, the level of sophistication embedded in the CW-DeH sharing arrangement is apparent as it comprised a three-band formula with equal sharing only applying if cost savings exceeded 15 per cent of target cost.

Despite these inputs from the Panel, there were inevitably contractual gaps needing to be settled by negotiations between the parties. Obvious examples concern the programme-specific investments and commitments that DeH was required to make which would have had diminished value outside the contract. The construction costs of a dedicated building, the losses on labour and materials resources held in the event of a contract break and under-absorbed overhead are all examples of asset-specificity, but it appears resolution occurred expeditiously with no obvious disagreement between the parties.

In only two areas – including interest as an expense and the allowable rate of profit – did disagreement persist, with the CW's position on interest prevailing, but modified in relation to the profit rate. While the possibility of the CW exercising sovereign power was raised on one occasion, this line of action was not pursued. In terms of the relative powers possessed by the bilateral monopolists, the CW was probably in the stronger position given DeH was always guaranteed a profit and would have been unwilling to break the contract once major resources had been committed to the programme, particularly given the possibility of follow-up orders. 21 That Gundill unilaterally deleted interest charges from DeH's claimed expenses is indicative of the CW's stronger powers.

An unexpected finding, not obvious from the foregoing chronology, is that contrary to the impression given by Table 5 showing DeH's share of cost savings for batches two to five, there is no evidence the parties ever met to reset target costs after the completion of each batch. Missing from the otherwise comprehensive archive is any mention or record of CW-DeH meetings to review and reset targets. Relevantly, the following extract from Gundill's report (Gundill to Storey, 6 November 1940) on DeH's costing system records that: The first and second batches of 50 each have already been delivered, and some of the third batch. Payment for the second batch and those of the third has been made at £1263 per frame, although this price was fixed only in connection with the first batch … so that the Company would not be inconvenienced while the target price of the second and third batches was being established. As it is anticipated that the cost of the second batch of 50 will decrease considerably below that of the first, it is intended to proceed with obtaining the cost of the second batch so that financial adjustment can be made, against the target price to be established. (emphasis added)

Evidently, ex-ante targets were not set prior to the commencement of batches two and three, in which case they must have been set ex-post. The absence of any record of meetings between the parties to set ex-ante targets for batches four and five raises doubts about whether such meetings ever occurred. While it is impossible to be conclusive, it seems that, contrary to what had been contractually agreed, no meetings were held to set ex-ante target costs.

If this contention is correct, then what is the likeliest explanation for formal processes being ignored? Tables 1 and 2 show an ethos – predictable in a wartime setting – of prioritising production and letting contractual processes catch up later. In Gundill's words, ‘production was started hurriedly’ (Gundill to Storey, 6 November 1940). Arguably, this catch-up ethos also applied to targets. Economic theory supports this proposition. The formal contract anticipated a series of meetings to negotiate targets to provide a basis for determining DeH's share of any cost savings against targets. Coase (1937) provided compelling arguments as to why production is invariably organised to avoid frequent negotiations over prices. By avoiding such potentially time-consuming and disputatious steps, the parties were acting in accordance with Coasian theory.

From another perspective, the failure to comply with a key contractual term is an example at the micro level of the phenomenon that Antonelli et al. (2014) describe at the macro level of Italy's failure to observe parliamentary budgetary and audit reporting requirements in relation to World War 1 wartime expenditures in general, and dealings with key armaments suppliers in particular. While the socio-political explanations advanced by Antonelli et al. (2014) might have influenced this failure, our view is that at the micro level of setting benchmark costs/prices, Coase (1937) has the stronger explanatory power.

If targets were set ex-post, it is instructive that DeH always bettered targets by modest amounts, even for batch three for which labour efficiency stalled and material costs rose. To the extent that ex-ante target costs were not set, DeH was denied the opportunity to increase its remuneration by its share of any cost savings against targets. Thus, setting purported targets ex-post, but above DeH's actual costs, can be regarded as a form of additional compensation to the firm. Our calculations (not shown) reveal that DeH's additional remuneration from this source increased its return from five per cent to 5.4 per cent of production costs. Doubtless, such a step would have required high-level approval within the APC.

Reference was made earlier to the possibility that, in preparing its fourth report dealing specifically with the airframe contract, the Panel had been alerted to the concept of learning as described by Wright (1936). Irrespective of whether or not that conjecture is correct, the assembly-labour data shown in Table 4 demonstrates that learning did occur on the first 450 airframes, even allowing for its temporary cessation with batch three. Using the iterative process developed by the US Army Logistics Management Centre (Liao, 1988), a learning rate of 0.819 has been calculated for assembly-labour for the first 450 airframes. However, had the learning rate been calculated after the completion of the first 100 airframes (batches one and two) it would have been 0.794; after the completion of batch three it would have weakened to 0.844. Clearly, had the learning rate for the first 100 airframes been used as a planning tool by DeH, subsequent cost reductions would have been overestimated.

The learning rates calculated for the airframe contract can be compared with Reinhardt's (1973: 824) assertion, made in connection with an analysis of Lockheed's Tri-Star programme, that ‘for complex modern aircraft, learning rates between 75% and 78% are typical’. The implication, perhaps unsurprising, is that Tiger Moth assembly was less complex than the construction of modern jet-powered passenger aircraft and, accordingly, provided less scope for learning.

Conclusion and suggestions for further research

The CW-DeH exchanges provide a highly transparent example of the evolution and subsequent operation of a World War 2 cost-plus procurement contract. In terms of contracting theory, the initial contract was highly informal and moved towards completion only slowly under the wartime ethos of prioritising ‘getting on with the job’ while leaving contractual formalities to be finalised later. The first draft of the contract, including the formula for sharing cost savings between the parties, was prepared some 13 months after the initial CW-DeH ‘handshake’ agreement by which time approximately 160 of the ultimate RAAF order for 450 airframes had been completed. The formal contract was executed by DeH in April 1942, at least 10 months after the RAAF order was completed.

As well as the actual disclosures appearing to be far more detailed than any appearing in the extant procurement and OBA literature, an unexpected finding is that the parties probably disregarded a potentially time-consuming contractual term, requiring ex-ante agreement on subsequent target costs, in favour of ex-post adjustments in order to expedite the delivery of airframes and (modestly) increase DeH's remuneration. War-time exigencies would have had a major impact in this regard. It would be interesting to learn of other instances, including the relevant circumstances, in which formal contractual terms were disregarded. Irrespective of whether or not the inspiration for the target-cost concept was the UK example cited by Taggart (1941), UK applications of the concept could make for useful comparisons.

The scope and frequency of contract monitoring certainly warrant wider enquiries. The CW's senior cost accountant, Gundill, was shown to have played a pivotal quasi-forensic role in thoroughly investigating DeH's costing systems and dealings with sub-contractors. However, it seems that this was a once-only investigation. Separately, physical monitoring of production for safety and quality-control purposes was an additional assurance element in the airframe contract, suggesting another area of research: the extent to which monitoring of accounting disclosures is supplemented by quality control of physical output.

That Gundill-type access was an intentional feature of CW-contractor agreements in World War 2 is evident from the fifth Report of the Accountancy Advisory Panel (1939c) which dealt with who would actually conduct inspections. Concerned that there was insufficient capacity in the CW bureaucracy to undertake this task, the Panel recommended co-opting contractors’ auditors on the understanding that, in this role, the latter were agents of the CW, not contractors. Presumably, in this extended role, auditors would be required to go beyond the tasks and enquiries undertaken in regular external audits to include transactions within cost systems, particularly allocations between government and non-government contracts. This would address to some extent the reservation noted earlier by Rogerson (1992) of the external auditor's capacity to determine whether costs incurred had been correctly or accurately apportioned to products consistent with the contractual terms.

Another area for further research is that the pattern of reductions in assembly-labour costs shown in Table 5 is largely consistent with the operation of the learning curve (Andress, 1954; Baloff and Kennelly, 1967) except for a discontinuity with batch three. Given the rich contextual data available about assembly operations for the DeH-produced airframes, the causes of the batch three discontinuity, together with seeming negative learning with the additional UK order for 581 airframes, costed in three batches, have the potential to increase understanding of the circumstances in which learning does, and does not occur, particularly given Richardson's (1988: 610) observation that there is ‘no underlying theory that learning should follow a constant learning curve’. A linked investigation would attempt to identify DeH's variable overhead to see whether learning effects extended to this cost element.

The learning curve remains strongly identified with aircraft production. Among global manufacturers, Airbus Industries and Boeing are the duo most likely to be using the concept for planning and financial reporting purposes. Indeed, Boeing's use of programme accounting for financial statement purposes appears to embody an expectation of learning (Ostrower, 2016). Both manufacturers recently suffered breaks and other discontinuities in production due to the effects of the Covid-19 pandemic. For Boeing, these problems overlapped with it having to cease, then restart, production of its 737-Max 8 model due to disasters in 2018 and 2019 caused by faulty flight-management software. The consequent interruptions to learning are likely to have impacted both manufacturers’ financial statements, creating a research challenge to determine the extent to which this occurred.

More generally, it is unlikely that the DeH airframe contract was unique in terms of defence procurement in World War 2. The archives relating to other World War 2 procurement contracts in Australia and elsewhere could be a rich source of information regarding the nature and frequency of cost disclosures, and the extent they were subject to special inspection and verification processes. One obvious complement to the airframe's agreement is the contract for the Gypsy Moth engines which powered the Tiger Moths. While these engines were initially imported, those for later orders were made in Melbourne by GMH (Mellor, 1958). Other complements are DeH's subsequent contracts with the CW for the production of troop-carrying gliders and Mosquito fighter-bombers and the various contracts entered into between the CW and CAC for the supply of aircraft. 22

Our contention that cost-plus procurement contracts embedded with cost monitoring provisions represent a subset of OBA arrangements opens another gap in the accounting history literature. Windolph and Moeller's (2012: 49) assertion that ‘OBA is still a fairly new practice, appearing with the spread of lean production and supply in the 1990s’, is true only in the limited context they describe. OBA, defined more broadly to include the disclosures occurring in cost-plus contracts, certainly lacks a detailed history. The earliest example known to us concerns neither outsourcing nor government procurement. It is contained in Roll's (1930/1968: 75) description of a 1778 licence agreement by which a Cornish copper mine used a Boulton & Watt (B&W) steam engine to drain its underground workings. Cost savings derived from the purported efficiency of the machinery were to be shared 2:1 between the miner and B&W. Importantly, the agreement included the provision that the miner's books ‘were to be liable to … [B&W's] inspection’. 23

That the 1778 licence agreement, like that between the CW and DeH, included the right by one party to inspect the other's books as a reserve power, indicates another OBA research area: the extent to which both outsourcing and procurement contracts include such reserve powers and the degree to which such rights are exercised. An important area of outsourcing in Australia concerns the distribution requirements of enterprises such as supermarket chains, brewers, oil refiners and fuel importers. All need to transport products from central warehouses, manufacturing plants and depots to multiple retail outlets. Invariably, this task is outsourced to specialist road-transport operators. In one case known to the authors, the contractual arrangements between the parties include the equal sharing of any productivity gains. Relatedly, the contract gives the non-transport party's auditors the right to access the haulier's books in the event of any dissatisfaction with the information provided.

The availability of the rich CW-DeH archive has enabled us to investigate a significant, early-war defence procurement contract that had been transacted on a cost-plus basis. Although cost-plus has limitations as a contracting methodology and, as a consequence, its use is extremely limited if not prohibited in peacetime, it retains currency today and, arguably, would again become the default methodology if governments were confronted with a major global conflict. By judicious management, it can be used effectively by governments in times of extreme emergency when a ‘whatever it takes approach’ is considered necessary.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Notes

Correction (August 2024):

Article updated to correct a sentence in Notes section.