Abstract

Michel Foucault's work had a strong influence not only in philosophy but also in a wide range of humanistic and social disciplines, including accounting. Notably, the first studies which brought Foucault's thought to the attention of interdisciplinary accounting scholars were historical. This article documents how Foucault's ideas have directly inspired accounting history scholars, how the latter have interpreted and brought Foucault's work into their field as well as what future research paths may lie ahead. The article offers a systematisation of how the complex ideas of Foucault have been translated into eight key themes that have provided a crucial interpretive prism to many studies in accounting history. In doing so, it assists scholars wishing to familiarise themselves with Foucault's work and employ it in their research.

Introduction

Michel Foucault was a French philosopher, historian and political activist associated with structuralist and post-structuralist movements. Structuralism is a theoretical approach that identifies patterns in social arrangements, most notably language (i.e., structures), while post-structuralism builds on the insights of structuralism, and holds all meaning to be fluid rather than universal and predictable. Post-structuralism discards the idea of interpreting reality within pre-established, socially constructed structures. As one of the leading thinkers of the twentieth century, Foucault had a significant impact on different and diverse fields. His academic formation and work were strongly interdisciplinary, spanning philosophy, psychology, sociology and history (Miller, 1986), but his ideas travelled even farther and provided fertile ground to business disciplines, especially management, organisation and accounting studies. The literature reviews by Bowden and Stevenson-Clarke (2021) and Raffnsøe et al. (2019), along with a special issue of Foucault Studies in 2012, exemplify Foucault's relevance for management and organisation studies. In accounting, his work appealed particularly to those scholars who sought to broaden the scope of accounting beyond its technicalities and conceive of it as a social practice (Hopwood, 1983), one which is ‘both a consequence of, and an active agent within, a dynamic and contested social world coupled with a proclivity for change’ (Roslender and Dillard, 2003: 327). Foucault's work has been crucial to accounting scholars pursuing an interdisciplinary, ‘alternative’ agenda (Gendron, 2018; Maran et al., 2023). These scholars no longer see accounting as a neutral, value-free technique in the pursuit of rational decision-making but give consideration ‘to questions of power, influence and control’ (Hopwood, 1976: 3), thereby investigating accounting and its interconnections with existing ideologies and broader social discourses. Foucault’s thought has been widely disseminated in accounting studies, including by means of journal articles – the main focus of this study – but also handbooks and edited collections (Bigoni and Funnell, 2017; McKinlay and Pezet, 2017; Roslender, 2017; Stacchezzini, 2012) and book chapters (Fleischman et al., 2017; Hoskin, 2017; Knights and Bloom, 2017; Wilson, 2021).

Foucault is known for his analysis of power relations and the mechanisms through which power seeps deep into society and influences, often in unseen ways, how individuals and social groups conduct themselves. Particularly important for accounting studies, Foucault analysed extensively the relationship between power and knowledge (Loft, 1986), and how accounting is enlisted by those in power to disseminate and popularise specific discourses via a wide array of institutions such as prisons, the army, schools, medical facilities and factories. These discourses, in turn, end up reinforcing the system of power that generated them ‘by holding in place the categories and identities upon which it rests’ (Hardy and Phillips, 2004: 299). Within knowledge-based forms of power, accounting occupies a prominent place because of its ability to render abstract phenomena visible and amenable to calculation, classification and intervention (Rose and Miller, 1992). The contributions of Foucault's theoretical toolkit to accounting studies have not been limited to several concepts that have great explanatory potential but extend to methodological matters. His genealogical method has been adopted by researchers seeking to appreciate the role of accounting within a wide network of actors, institutions and forms of power. Foucault's work has enabled accounting researchers to expose the contributions of accounting practices to the reproduction of unequal power relations and also to problematise assumptions that enable the ‘smooth passage of regimes of truth’ (Smart, 1983: 135).

In his analysis of modern institutions, dominant discourses and ways to exercise power and influence in society, Foucault engaged in great detail with historical matters, often to connect different, dispersed events out of which contemporary beliefs emerged. It is unsurprising that, although Foucault's work impacted research on many aspects of accounting (Chiapello and Baker, 2011; McKinlay and Pezet, 2010), the dissemination of his ideas began with studies that were clearly historical. Thus, in our article, accounting history literature is conceived of as an engine for promoting innovation in accounting research.

This study documents specifically the influence of Foucault's thought on the accounting history literature. It enlightens how Foucault's ideas have directly inspired accounting history scholars, how the latter have interpreted and brought Foucault's work into their field as well as what future research paths may lie ahead. To achieve its goals, the article carries out a structured literature review (Massaro et al., 2016), comprising bibliometric and manual analyses, of the articles which refer to Foucault appearing in accounting journals that are ranked three-star or above in the 2021 Chartered Association of Business Schools Academic Journal Guide, the so-called ABS list, and in specialist accounting history journals, between 1980 and the end of 2022. The sample includes articles that can be considered as historical, and which directly mobilise Foucault's thought to pursue their aims. The article identifies the key Foucauldian themes mobilised by accounting historians, maps how these themes evolved and suggests how they could be developed by future historical research (Maran et al., 2023; Marrone et al., 2020). Moreover, it documents the geographical locations and historical periods considered by historical work inspired by Foucault, along with the key outlets and authors that contributed to the dissemination of Foucault's ideas within the accounting history literature, beyond localised geographical affiliations as in Rappazzo et al. (2023).

This article provides two main contributions to the accounting literature. It offers a systematisation of Foucault's thought and how it has been translated into themes that have provided a crucial interpretive prism to many studies of accounting history. Foucault has authored several books and articles and, as one of the most prominent French public intellectuals of the twentieth century (Chiapello and Baker, 2011), has featured in many interviews. This resulted in an immense scholarly output, often non-linear and characterised by a high level of complexity, which in turn inspired a multifaceted scientific production by accounting historians. Such rich work warrants careful analysis and systematisation. Moreover, by tracing the key Foucauldian themes used by accounting historians, their evolution and future prospects, the study provides further impetus to the dissemination of Foucault's thought in the field of accounting history by inspiring future research works. In particular, the article presents a useful map for scholars, including junior ones, who wish to familiarise themselves with Foucault's ideas and understand if and how these can contribute to their research agenda.

The reminder of the article is organised as follows. The next section details the research method. This is followed by an analysis of the evolution of work inspired by Foucault in terms of number of articles, key outlets and authors, main themes and geographical and temporal spread of such contributions. The main themes drawn from the French philosopher's work that have attracted the attention of accounting historians are then presented. For each of them, a brief theoretical explanation is provided, which is followed by an analysis of the ways in which each concept has been mobilised in accounting history. The last section offers some concluding remarks and avenues for future research.

Method

This study started with the creation of a comprehensive data set consisting of accounting history articles that have been informed by Foucault's thought. Although Foucault's ideas have inspired scholars in different ways, we have focused on the direct impact of Foucault's work on accounting history research by limiting our analysis to studies that have drawn on Foucault's original concepts. Research that is based on Foucault-inspired studies and mobilised the French philosopher's work only in an indirect fashion via studies from other authors has been excluded. 1 The construction of the data set was carried out in three main steps. First, we ran a search on Scopus (Table 1A), which is considered one of the world's leading databases of journal articles and citations (Zhu and Liu, 2020). We ran a query string, which searched for articles that contained the word ‘Foucault’ (and its derivatives) in the title, abstract and keywords and/or that included work by Foucault in their references. Following thorough manual checks, the search was refined to exclude articles citing authors other than the French philosopher Michel Foucault. 2 We have considered a time span that started from the decade when the first Foucauldian studies appeared (Armstrong, 1994) to the last complete year at the date of writing (1980–2022), 3 which ensured that both early studies that drew upon Foucault as well as current research trends are captured. The search was limited to all journals labelled in the 2021 ABS list as belonging to the field of accounting and with a rating of three or more stars. The ABS list is widely used internationally and, despite the limitations of journal guides (Maran et al., 2023; Picard et al., 2019), work appearing in outlets listed as three or more stars is normally considered of high quality (Rowlinson et al., 2015). Given the goal of the article, this list has been integrated with specialist accounting history journals, although these are listed as two-star in the ABS list, namely Accounting History, Accounting History Review, 4 and Accounting Historians Journal. Taken together, the selected journals ensure a broad representation of the accounting discipline across multiple scholarly communities. This initial search resulted in a sample of 771 articles.

The second step consisted of an analysis of the 771 articles aiming at identifying those with a historical focus. Drawing on Maran and Leoni (2019), we classified accounting history articles as those that focused on events occurring at least 15 years before the publication of the study. When articles investigated events over a period that started in the past and reached the present day, these were classified as historical if the time span considered was such that most of the events under analysis had occurred at least 15 years before the publication date of the article. This criterion ensured that the sample only included articles with a strong historical focus and which could have been considered historical even at the time of writing. Consistent with this choice, only studies with an identifiable historical case that could have been interpreted in the light of Foucault's thought were selected, hence editorials, conceptual articles or literature reviews were excluded from the sample. This study adopts a broad definition of case study, one which is not limited to the analysis of specific organisations/entities, but also embraces events and social phenomena, such as colonialism, the development of cost accounting or the invention of writing. The classification of the articles was carried out by two of the authors who read the abstract and introduction of each article and, whenever needed, the rest of the article. Given the significant number of articles involved, these two authors first checked each other's work for consistency, then the remaining author performed a spot check to ensure the robustness of the final sample. Overall, 261 accounting history articles were identified. Due to the way in which the original sample was created, within those 261 articles were works that engaged with Foucault in different ways, from simple citations to a full-blown mobilisation of his ideas as a theoretical lens.

In the last step of the construction of the data set, we sought to focus only on articles that drew upon Foucault's thought as a theoretical framework which was used to interpret the case analysed in the article and provide theoretical and/or practical contributions. Articles were considered to have applied Foucault’s thought if Foucault's works were emphasised and cited in the theoretical framework and discussion sections. The discussion section was carefully analysed to appreciate whether the authors employed the concepts they had explained in the theoretical framework section in their reading of the findings. If the article did not have a theoretical framework section, the introduction and literature review sections were checked to identify any Foucauldian themes that guided the analysis of the results. If the article did not have a discussion section, we focused on the findings and conclusion sections. Moreover, for an article to be classified as having used Foucault, the French philosopher's work must have informed at least one of the theoretical lenses on which the article was based. These analyses were performed by reading the 261 full articles. Each author analysed one-third of the 261 articles and then checked the classification done by the other two authors. Any discrepancies in the classification were discussed and agreed upon. We therefore identified 117 articles that constitute our data set on accounting history literature directly inspired by Foucault's work. The final data set provided the basis for the identification of the Foucauldian themes mobilised by accounting scholars and their evolution over time. The complexity and interconnectedness of Foucauldian concepts means that it is difficult to recognise clear-cut themes emerging from the French philosopher's extensive scientific production. The identification of specific themes stemming from Foucault's wide-ranging thought cannot be completely unambiguous.

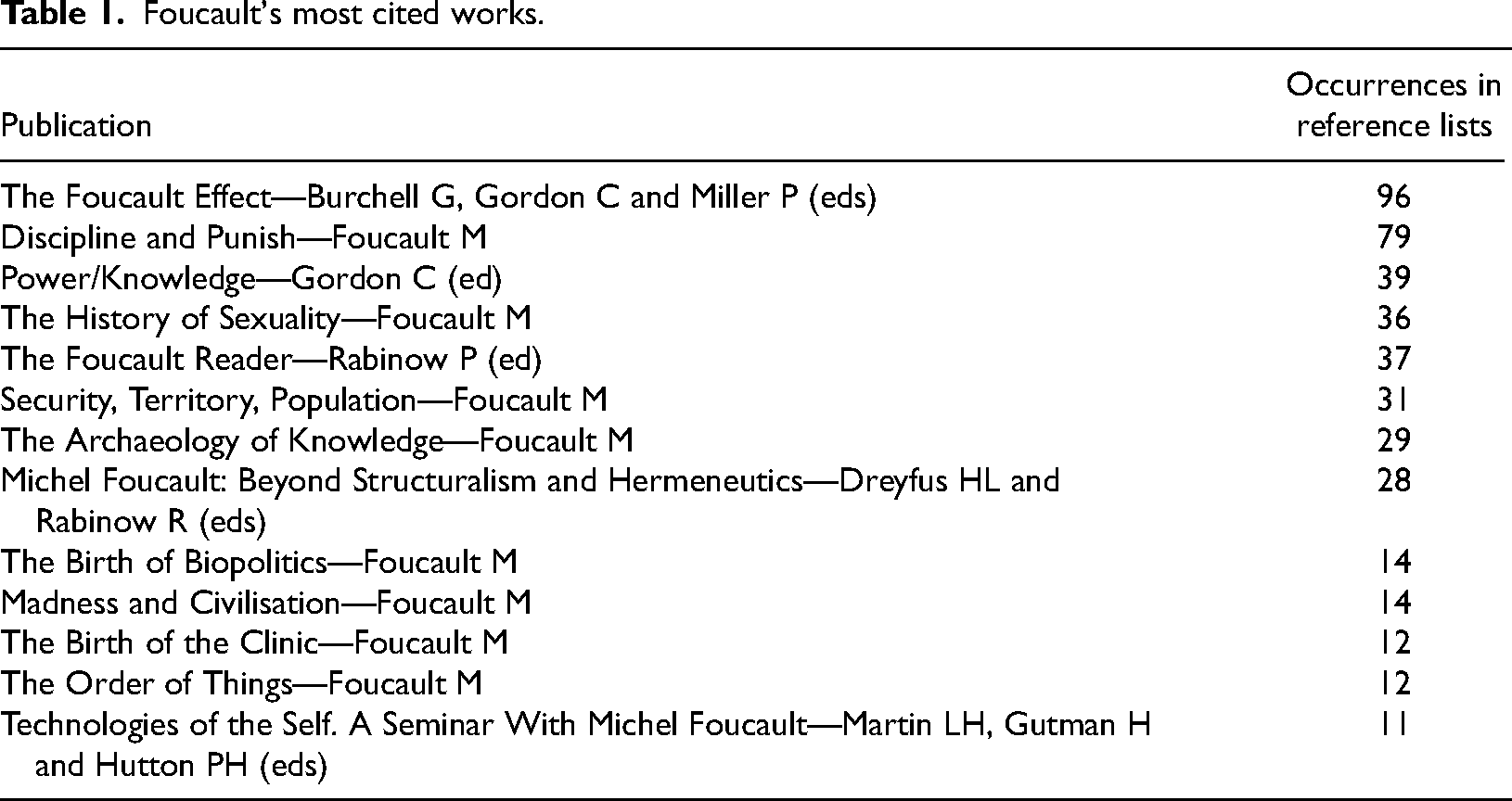

The themes were identified through a combination of two processes. Firstly, by using the bibliometric package R we analysed the references of the 117 articles and highlighted the works of Foucault that are most cited in our data set (Table 1).

Foucault's most cited works.

This evidence has been combined with a study of the 117 articles and the authors’ knowledge of Foucault, whose work they have used in several research projects. Seven key Foucauldian themes were identified, namely (1) governmentality; (2) disciplinary power; (3) power/knowledge; (4) discourse; (5) biopower; (6) technologies of the self; and (7) genealogy. A residual category (8) other themes was created, comprising Foucauldian concepts that did not completely fit into the other categories. 5 The identification of Foucauldian themes within the 117 articles was first carried out by one author, then checked by another author, with further random checks done by the remaining author. To facilitate the interpretation of the results, we decided to limit each article to two themes. In the limited number of cases where more than two themes were present, we focused on the two that were prevalently used in the discussion of the case informing the article. Lastly, the authors met to discuss any disagreement in the selection of themes.

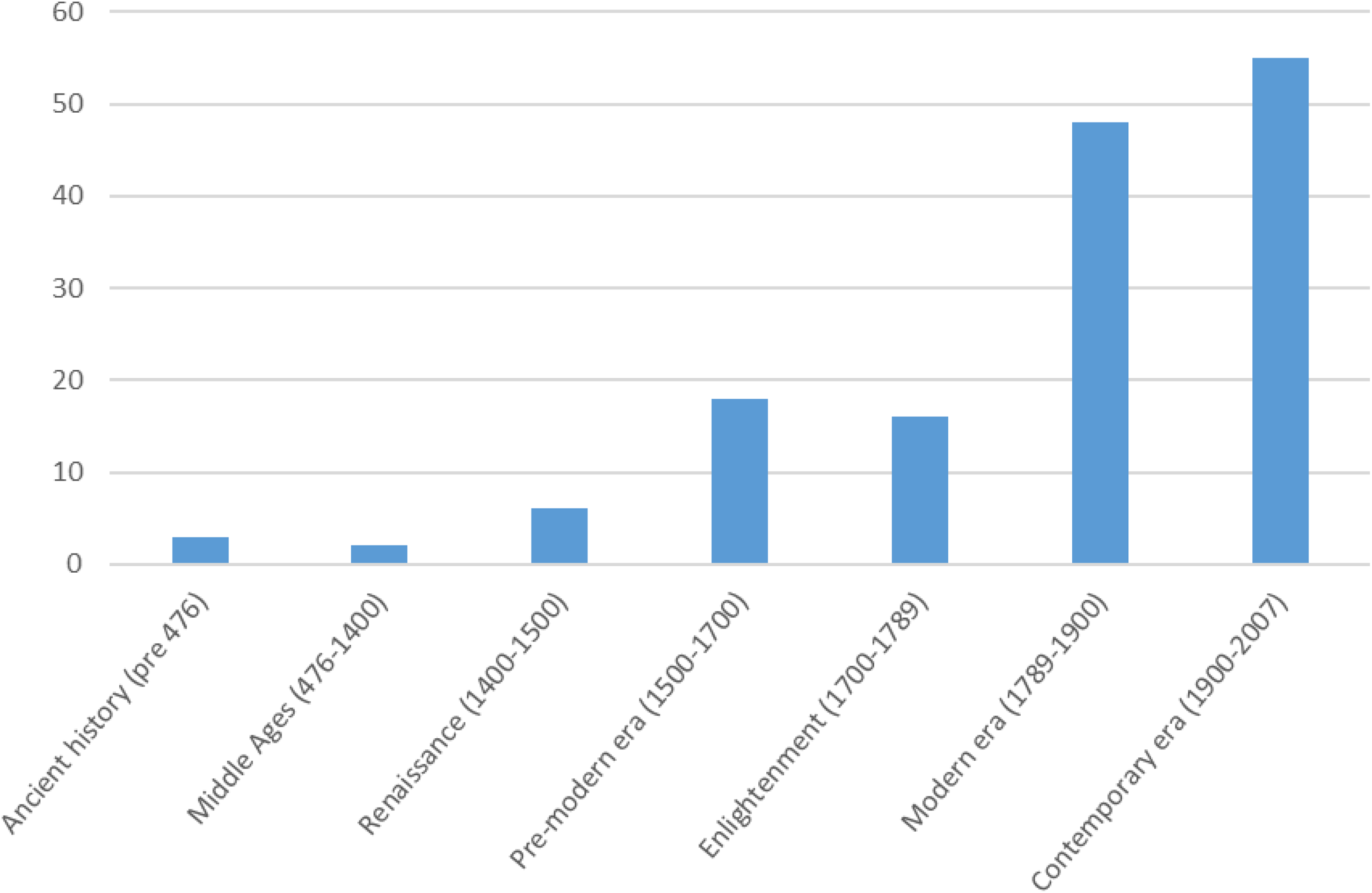

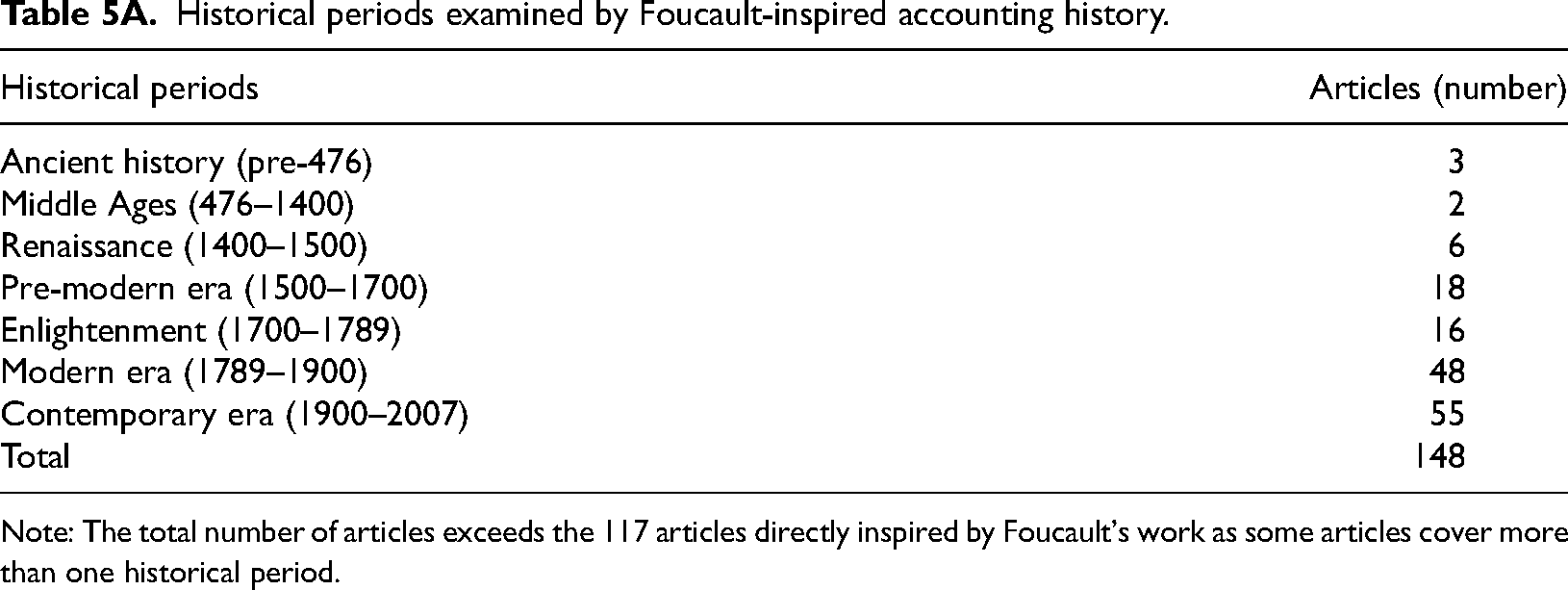

The data set was also analysed to appreciate the geographical locations examined by Foucault-inspired accounting history. For each article, we indicated in which of the five main continents the case study analysed was located (Africa, Americas, Asia, Europe and Oceania). The articles were further classified according to the historical periods they investigated. We adopted a customised periodisation which started from the internationally accepted periodisation which, excluding prehistory, considers four periods: Ancient history (3500BC–476AD), Middle Ages (476–1492), Modern Age (1492–1789) and Contemporary Age (post-1789). We then modified these categories to consider periods that Foucault (2007) considers relevant in his genealogy of power relations. The milestones in Foucault's genealogy are the beginning of the crisis of the pastorate in the Renaissance; the birth of the Administrative State in the sixteenth to seventeenth centuries; the Enlightenment, with the birth of new discourses, such as cameralism and mercantilism; the rise of governmental technologies in the nineteenth century; and the birth of the liberal, governmentalised State in the twentieth century. Consistently, we defined the following historical periods: Ancient history (3500BC–476AD), Middle Ages (476–1400), Renaissance (1400–1500), Pre-modern era (1500–1700), Enlightenment (1700–1789), Modern era (1789–1900) and Contemporary era (1900–2007) 6 . Each author classified one-third of the articles and cross-checks and discussions of ambiguous cases were carried out to ensure consistency.

Foucault in accounting history

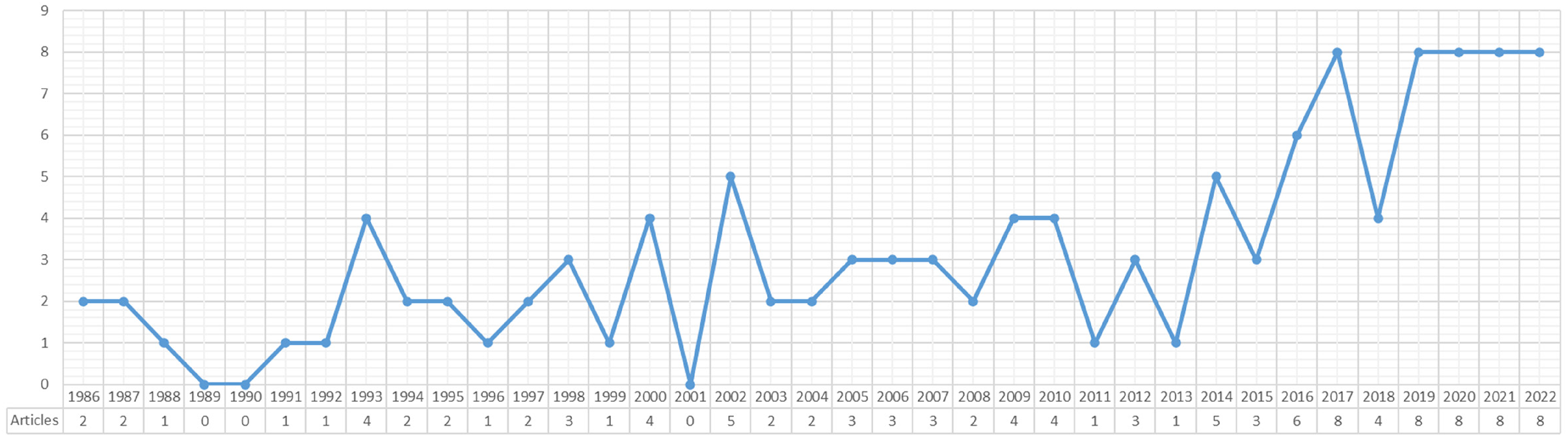

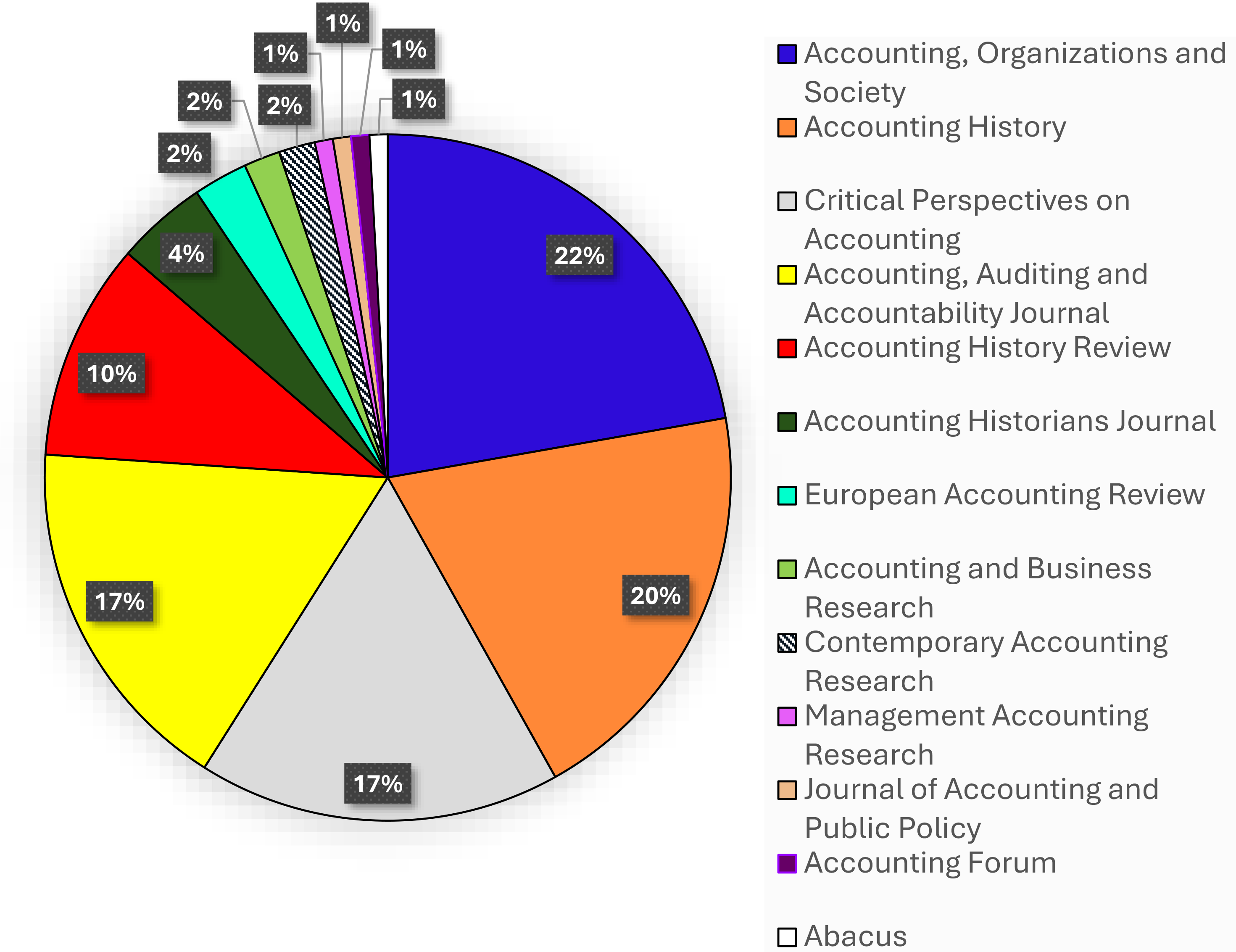

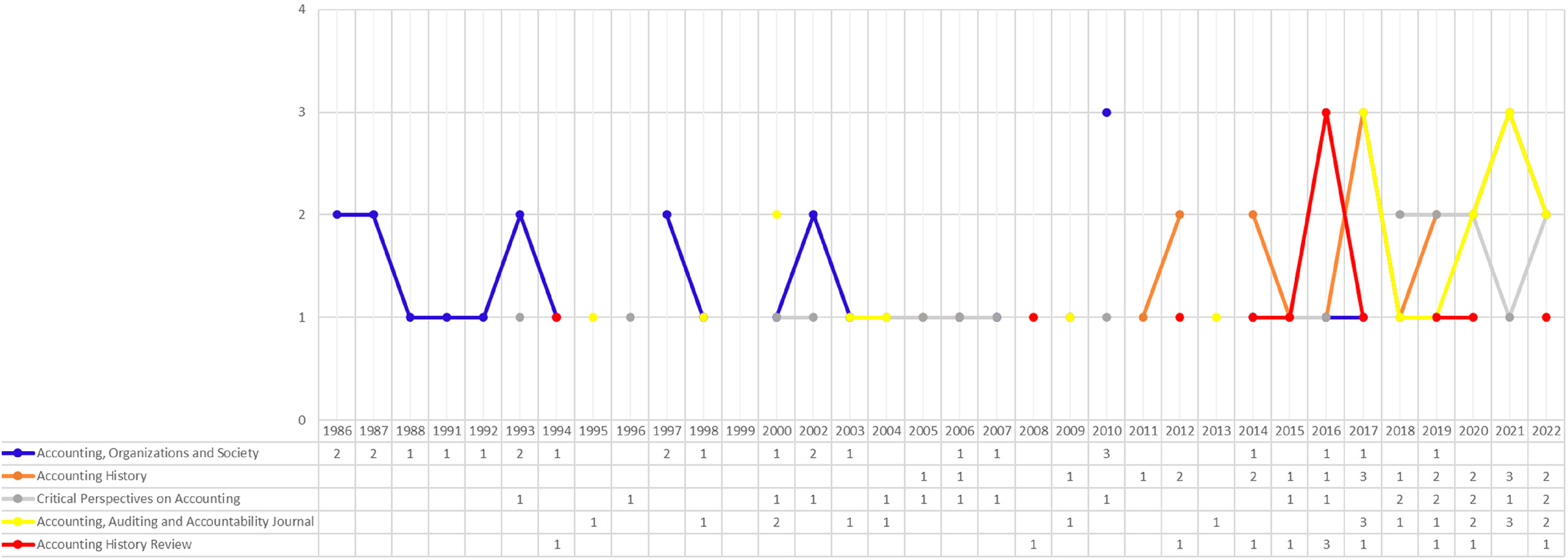

Foucault's thought has influenced the accounting literature since 1986 when the first studies that mobilised the French philosopher's thought appeared. As noted above, the first Foucauldian studies were developed from a historical perspective, which testifies to the crucial contributions and innovative potential of accounting history in the service of the interdisciplinary agenda. Following these ground-breaking studies, interest in Foucault's thought started to grow in the 1990s with two to four articles per annum, except for four ‘lighter’ years. Interest increased significantly in the first decade of the 2000s, with a peak of eight articles in 2017 and between 2019 and 2022 (Figure 1). Foucauldian accounting history is therefore a mature but vital field, and the French philosopher's influence is still strong almost 40 years after his first appearance. The main outlets that contributed to the dissemination of Foucauldian studies have been Accounting, Organizations and Society, Accounting History, Critical Perspectives on Accounting, Accounting, Auditing & Accountability Journal and Accounting History Review, which, taken together, have published 86 per cent of Foucault-based accounting history (Figure 2 and Table 2A). This is hardly surprising for, with the only exception of Accounting History Review, which publishes both traditional and new accounting history studies, these outlets are the leading journals in interdisciplinary accounting research and therefore welcome work inspired by understandings that are not limited to accounting scholarship (Maran and Leoni, 2019; Maran et al., 2023). A very prolific author like Foucault, whose wide-ranging work offers philosophical, sociological and historical insights, provided fertile ground for journals that are interested in investigating accounting in close connection with broader social discourses. Faithful to its tradition of innovation, Accounting, Organizations and Society has been the forerunner of the mobilisation of Foucauldian themes in accounting history (Figure 3), although it appears that the journal has almost completely abandoned Foucault-inspired accounting history, perhaps reflecting a less marked interest for accounting history altogether or the journal's constant search for new approaches, along with a stronger focus in recent times on quantitative research, which is at odds with Foucault's epistemological beliefs (Maran et al., 2023). This has not caused the demise of Foucault's thought and this space has been occupied by the other four outlets.

Annual scientific production.

Journals that have published accounting history Foucault-based studies.

Main outlets’ trend.

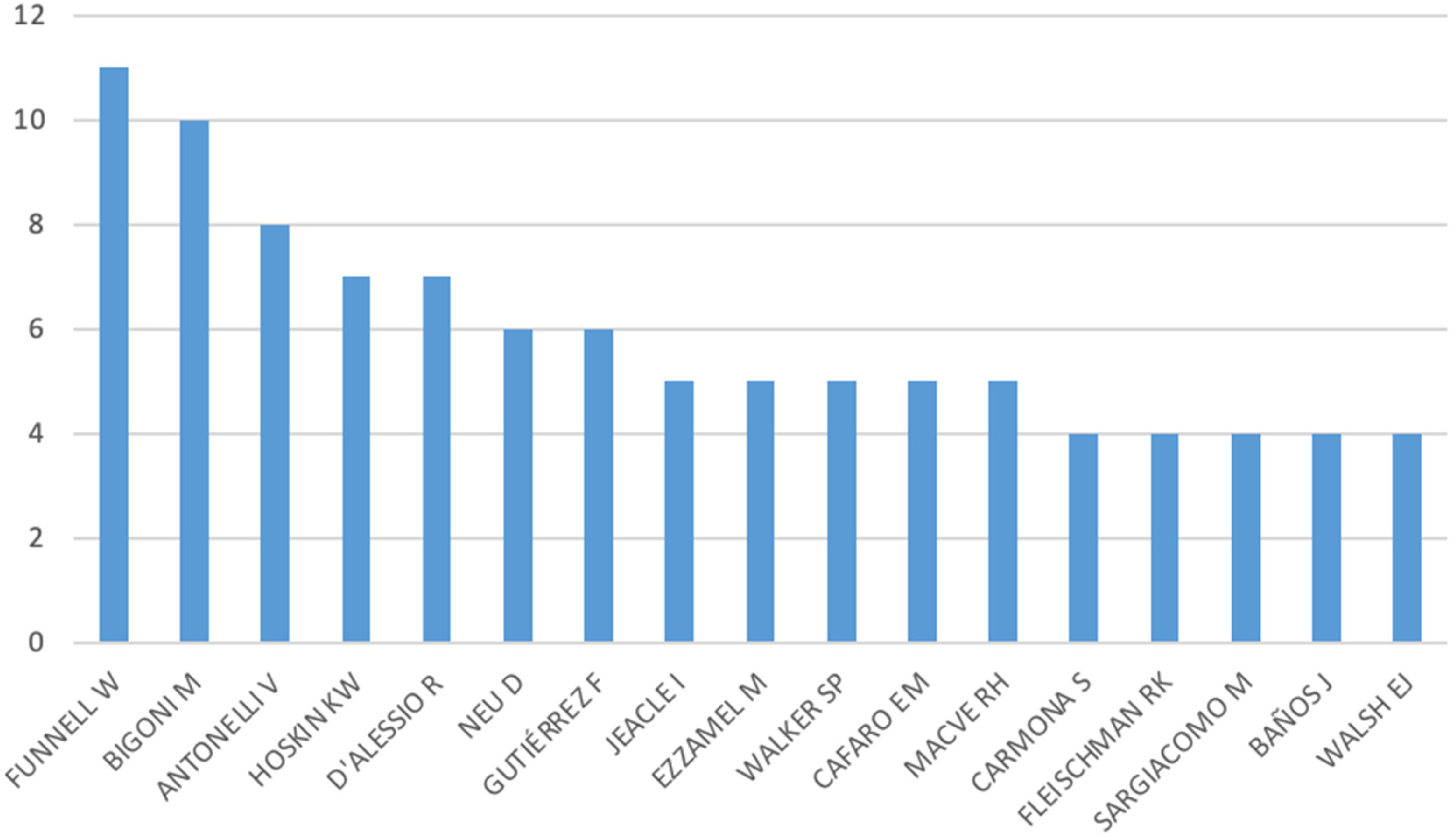

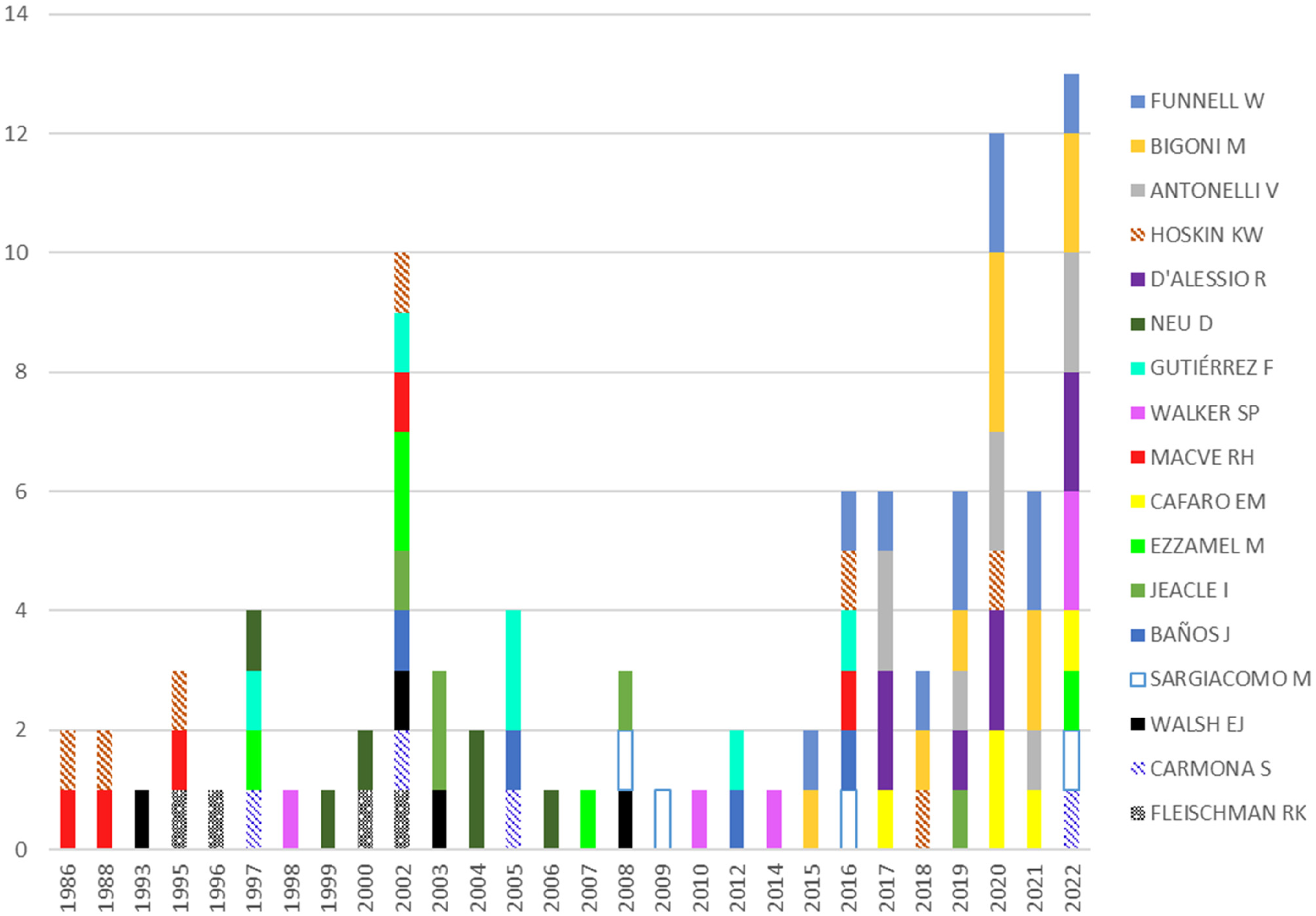

The more active accounting historians engaging with Foucauldian themes are affiliated with universities located in Canada, Italy, the UK and Spain (Figure 4). The trend of their publications reveals two main waves of Foucault-inspired research (Figure 5). The first was mostly fuelled by the contributions of Keith Hoskin, Dean Neu, Ingrid Jeacle, Mahmoud Ezzamel, Stephen Walker, Richard Macve, Salvador Carmona, Eamonn Walsh and Richard Fleischman. 7 Under the thought leadership of these authors, a second wave of authors appeared from the first decade of the 2000s which, behind the most prolific Foucauldian author, Warwick Funnell, has a strong presence of Italian (see also Rappazzo et al., 2023) and Spanish authors, including Michele Bigoni, Valerio Antonelli, Raffaele D’Alessio, Emanuela Mattia Cafaro, 8 Massimo Sargiacomo, Fernando Gutiérrez and Juan Baños. This further demonstrates the importance of Foucault's thought in accounting history, which has travelled far beyond the Anglo-Saxon countries where most of the first leading authors were located and has started to attract the attention of accounting scholars. The work of Foucault has now inspired a new contingent of southern European authors who are particularly interested in the investigation of accounting and power relations in history (Bigoni and Funnell, 2018).

Authors who have mobilised Foucault's thought.

Trend of publications by authors in figure 4.

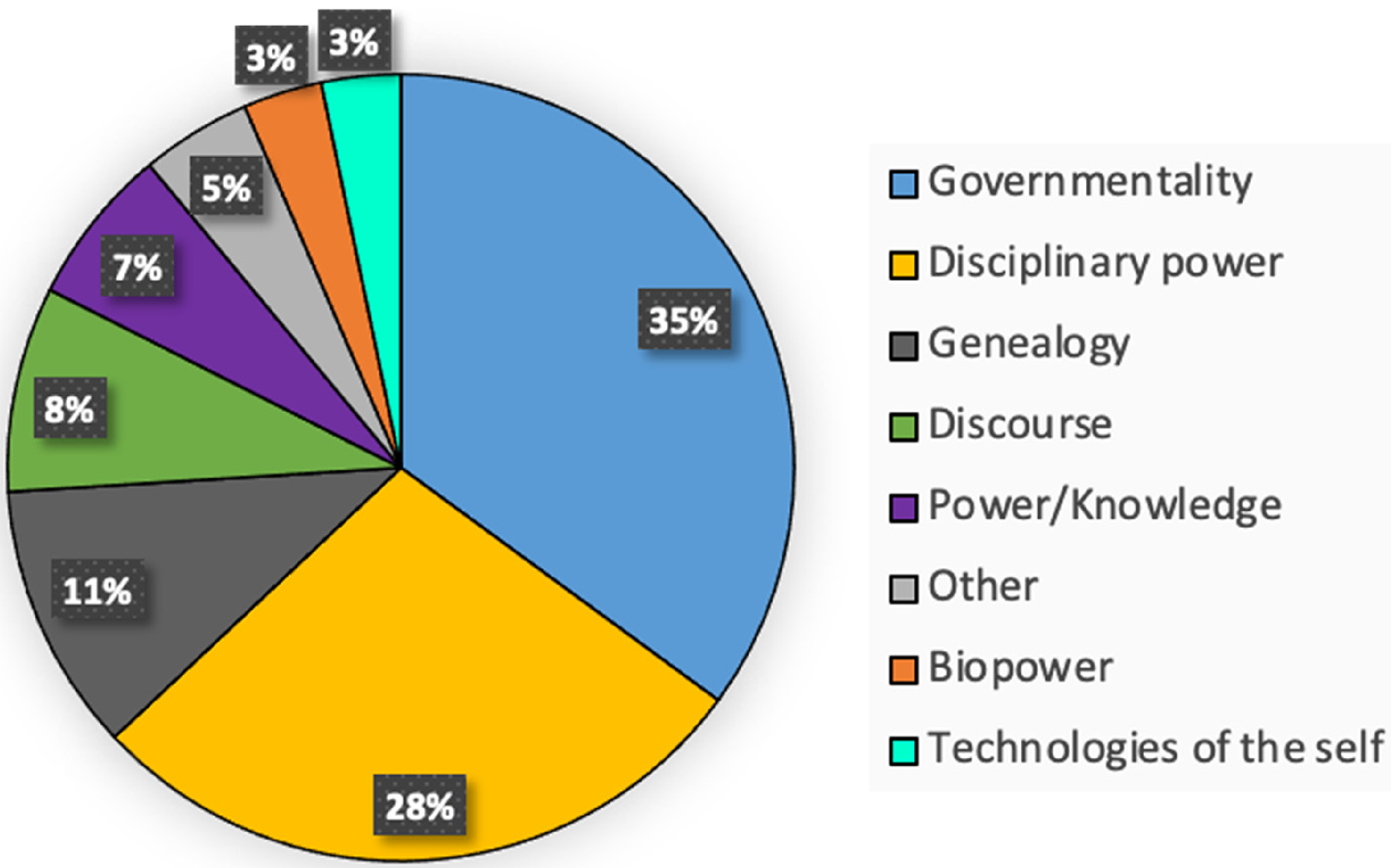

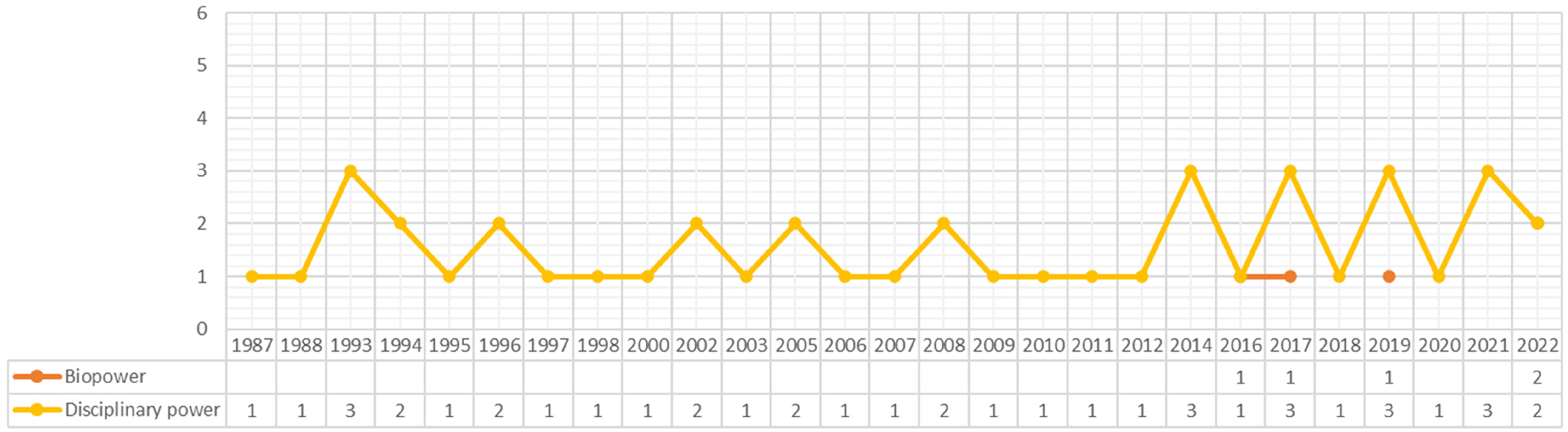

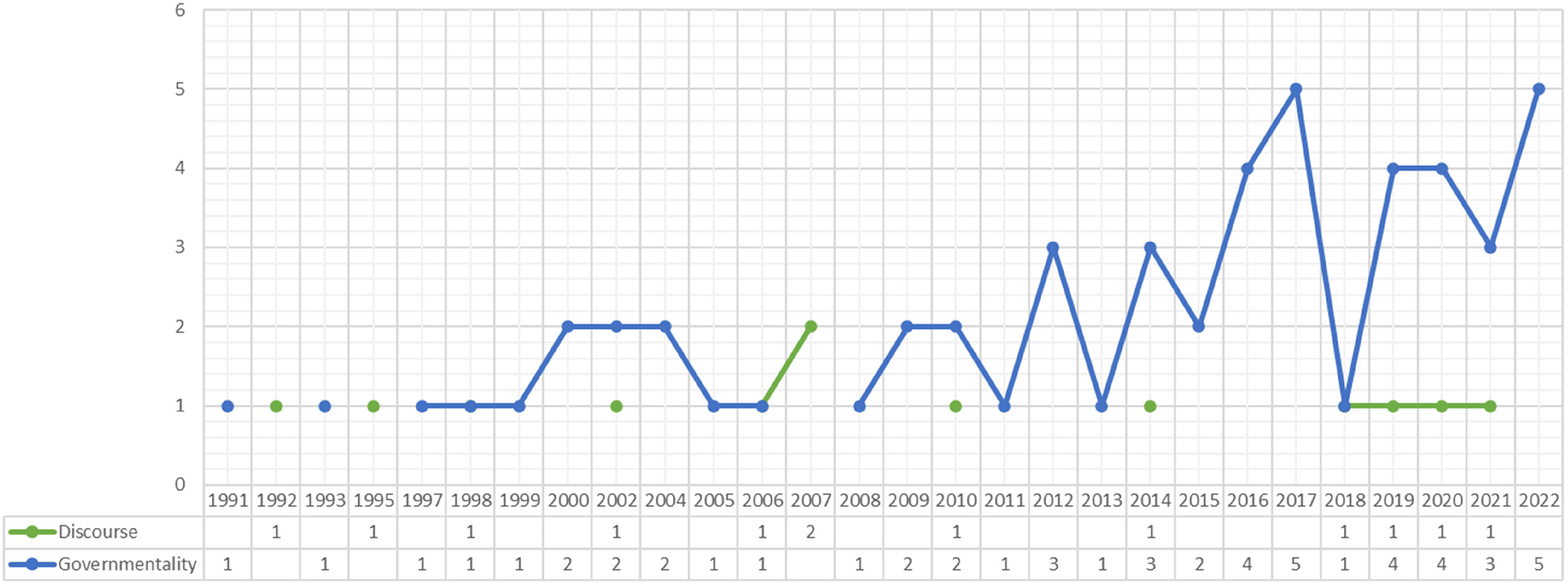

Among the main Foucauldian themes identified in this study, it is clear how governmentality and disciplinary power are by far the most investigated. These have inspired more than 60 per cent of Foucauldian accounting history studies (Figure 6 and Table 3A). Although this may be the consequence of such themes having become widely known and seen as a safe or fashionable framework, especially in recent times, the significant diversity of contexts and places to which these concepts have been applied demonstrates their explanatory potential. Disciplinary power has exerted a constant influence on accounting history (Figure 7). The importance of this concept is hard to overestimate as it has been one of the pillars of pioneering studies that have started to challenge the traditional view of accounting as a neutral technique and emphasise accounting as a social practice and a means to normalise the conduct of individuals within institutions such as factories and schools. The Foucauldian theme of governmentality has emerged as a new trend since the 2000s, perhaps reflecting the availability and diffusion of translations of the 1977–1978 course Sécurité, Territoire, Population in different languages or edited collections of works on the topic. The theme of governmentality helped research to move beyond the traditional Foucault-based historical studies on accounting as a means of disciplinary normalisation in enclosed institutions and start investigations of the contributions of accounting to the exercise of power by States over large territories and populations (Figure 8).

Foucauldian themes.

Theme trends: biopower and disciplinary power.

Theme trends: discourse and governmentality.

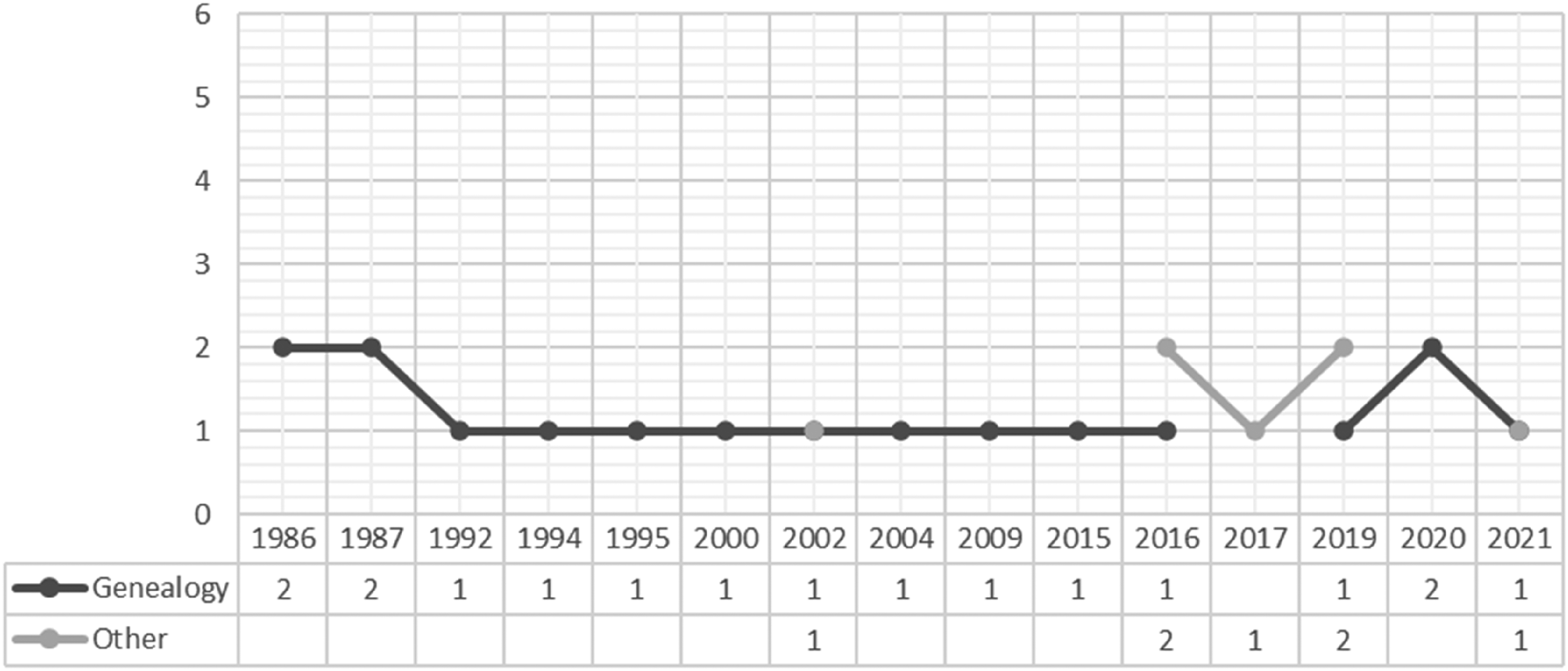

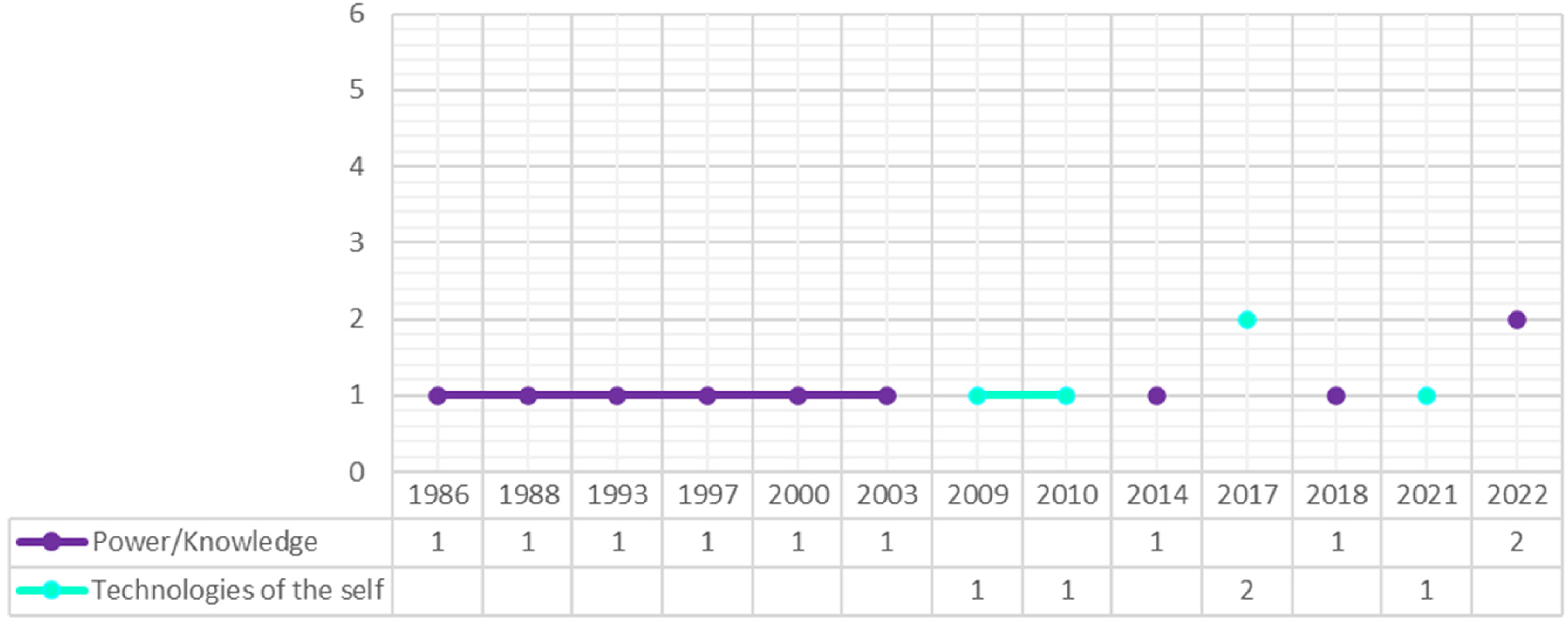

Power/knowledge, at least until the 2000s, has been often investigated in combination with disciplinary power (Figures 7 and 10) as these two themes are interconnected. However, whilst power/knowledge concentrates on Foucault's overarching understanding of the interrelations between knowledge systems and power relations, in accounting history disciplinary power has as its main focus the specific application of knowledge practices for controlling individuals (Hoskin and Macve, 1986), which has been favoured by scholars, especially in recent times. The other Foucauldian themes, discourse, genealogy, biopower and technologies of the self, had a spotty and less marked influence on accounting history studies (Figures 7 to 10). They have not yet been fully developed by accounting historians as they are based on lesser-known aspects of Foucault's thought.

Theme trends: genealogy and other.

Theme trends: power/knowledge and technologies of the self.

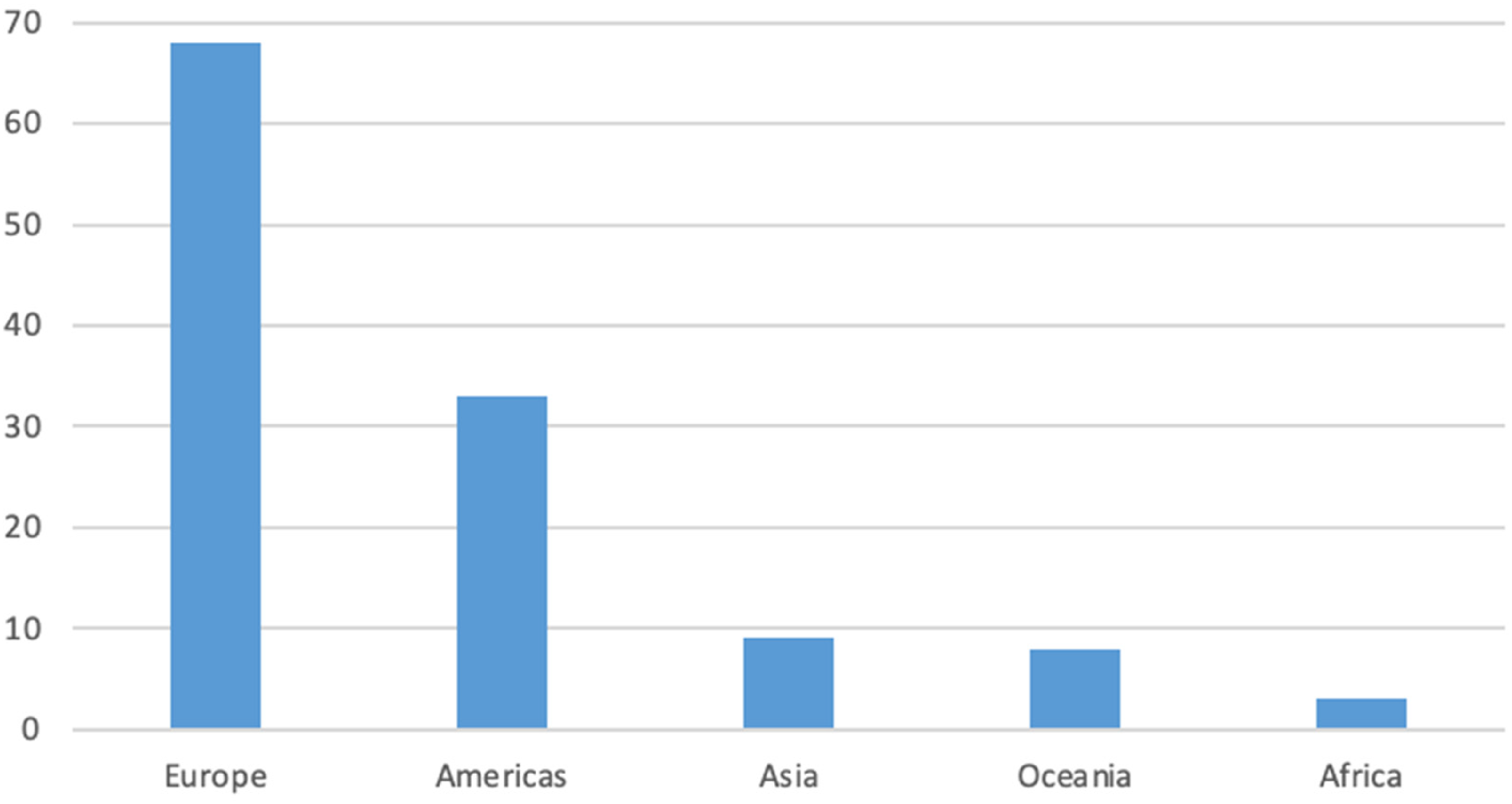

The case studies analysed by Foucault-inspired accounting history are mainly located within Europe and the Americas (Figure 11 and Table 4A), and investigate, in particular, the Pre-modern (1500–1700), Modern (1789–1900) and Contemporary eras (1900–2007) (Figure 12 and Table 5A). Several works have explored the Pre-modern era to shed light on the rise of the modern State in Italy, with an emphasis on the transition from a ‘State of justice’ to an ‘Administrative State’. Moreover, the interest of accounting historians in investigating the origins of modern forms of accounting explains the choice to focus on the Modern and Contemporary eras, especially through case studies located in Anglo-American contexts, where current management and cost accounting practices rose. At the same time, the location of the study tends to reflect the nationality of the authors, who prefer to focus on contexts that are familiar to them and on which they can easily find data. Data availability also seems to influence the choice of the historical period, for documents relating to the distant past are hard and time-consuming to find, often not digitised and require the assistance of a historian or archivist for their translation.

Geographical locations examined by Foucault-inspired accounting history.

Historical periods examined by Foucault-inspired accounting history.

Key Foucauldian themes in accounting history

Governmentality

Considering Foucault's extensive œuvre, his understanding of governmentality has been crucial in informing research into the ways in which power has been exercised on individuals and populations at different time-space junctions. In his popular definition, Foucault (1991: 102) conceives of governmentality as: the ensemble formed by the institutions, procedures, analyses and reflections, the calculations and tactics that allow the exercise of this very specific albeit complex form of power, which has as its target population, as its principal form of knowledge of political economy, and as its essential technical means apparatuses of security.

In the view of Foucault (1991, 2007) this new technique of government arose in the eighteenth century, with its key object being the population and not the territory of a State; at the same time, the main purpose of government shifted from the act of government in itself to the promotion of the well-being, growth and health of the population. As a result, governing in a rational way means that the population must be considered as a living phenomenon that has to be understood and mastered according to a specific form of knowledge, which Foucault labels ‘political economy’. The constants and regularities in the population such as birth and death rates, morbidity rates and migrations need to be known to inform action. Apparatuses of security then insert the phenomena of the population within a series of probable events, and the cost of potential actions of power is calculated. Lastly, an average that is considered as optimal is identified and pursued (Foucault, 2007). Governmentality as a technology of government requires ‘intervening in the delicate balance of social and economic processes no more, and no less, than is required to adjust, optimize and sustain them’ (Foucault, 1991: 93).

Scholars who have mobilised Foucault's concept of governmentality have often considered the State as a prime target for understanding the place of accounting in the pursuit of governmental goals. Much of this research has drawn upon the work of Peter Miller and Nikolas Rose, most especially their conceptualisation of political rationalities, programmes of government and technologies of government. The starting point of an analysis of government is represented by the identification of political rationalities, which constitute the overarching values and principles informing government action (Miller and Rose, 1990; Rose and Miller, 1992). These political rationalities are nevertheless abstract, hence, they need to be detailed in more concrete programmes of government, to which purpose the role of experts, such as economists, accountants and auditors, is crucial (Radcliffe, 1998; Sargiacomo and Walker, 2022). Not only does the intervention by experts help in turning ideals and beliefs into action, but it also ensures that decisions enshrined in programmes of government look rational and disinterested. Technologies of government as ‘the complex of mundane programmes, calculations, techniques, apparatuses, documents and procedures through which authorities seek to embody and give effect to governmental ambitions’ (Rose and Miller, 1992: 177) are then mobilised to intervene in the phenomena to be governed. Miller and Rose's conceptualisation of accounting as a technology of government owes much to the work of Latour on ‘action at a distance’. When action is to be exerted on distant settings, knowledge of such settings is essential (Latour, 1988). To Latour, knowledge is ‘whatever is mobilised to act upon [a] setting’ (Latour, 1988: 160). As a result, accounting practices as a technology of government are a means to accumulate knowledge of distant locales by representing and translating the elements of the context to be acted upon, thereby enabling action by powerful agents. Accounting documents can be collected in ‘centres of calculation’ where accounting numbers are accumulated, aggregated and compared, thereby facilitating control (Rose, 1991). Accounting history research has devoted significant effort in showing how accounting has been (and still is) a crucial technology of government that helps to make the problems of government thinkable and susceptible to intervention and to inculcate in individuals new mentalities and behaviours that are consistent with the objectives of those in power or the overarching values of a society (Knights and Vurdubakis, 1993).

Already in the sixteenth century Farnese State of Abruzzo, Italy, accounting was mobilised to pursue the modernisation of the country. Accounting practices ensured a steady flow of revenue by tackling fraud and holding key bureaucrats accountable for their behaviour (Sargiacomo, 2008), and also enabled the sovereign to check the activity of magistrates and other officials in the State's justice system (Sargiacomo, 2009). Work by Antonelli et al. (2020) investigated accounting technologies that ensured that private companies building and managing railways in the nineteenth-century Papal States did not merely focus on profit but also on making sure that train journeys would be widely accessible to all citizens. This was consistent with the Pope's programmes of government which sought to promote economic development and increase the prestige of the Pope himself. Similarly, in the nineteenth-century Ottoman Empire, accounting technologies were used to centralise control of crucial social institutions, the waqfs (Yayla, 2011). So important is the role of accounting in allowing control by means of knowledge accumulated in centres of calculation that when the flow of accounting numbers ceased in the eighteenth-century New Settlements of Sierra Morena and Andalucia, the programme aiming at promoting agricultural development and settler self-sufficiently abruptly halted (Álvarez-Dardet et al., 2002). Agriculture was also central in Fascist Italy when the regime pursued the country's self-sufficiency by reclaiming marshy lands and promoting rural life. The production of financial and non-financial information soon became crucial in enabling the government to shape the conduct of rural populations in the pursuit of the efficient exploitation of new lands (Sargiacomo et al., 2016). Accounting practices have therefore supported different programmes of government that were underpinned by rationalities ranging from mercantilism to Fascist corporatism: the malleability and adaptability of accounting technologies mean that they can be effectively employed in mastering populations independently from the discourse that informs the functioning of an institution (Baños et al., 2005). The representational properties of accounting as a technology of government have also been exploited in dealing with matters of realpolitik as in the case of a barter proposed by the King of Spain to the Duke of Mantua in the seventeenth century. A detailed report on the target land's wealth and population, along with issues around defending the new dominion meant that the Duke rejected the proposal (Lai et al., 2012).

An important characteristic of accounting inscriptions is their ability to travel easily, which is crucial in accumulating knowledge about distant people and places, thereby significantly reducing the physical and conceptual distance between bureaucrats and politicians located in the capital city and their agents and populations in the field (Neu and Graham, 2006; Preston et al., 1997). Accounting provided essential contributions to the management of large empires, as in the case of the eighteenth-century Portuguese empire, where common accounting rules were implemented to ease colonial administration and force individuals to pursue the goals of the motherland (Gomes et al., 2014). Accounting and accountability practices have also been mobilised by empires to control labour and space from a distance in state-owned enterprises and in the management of crucial infrastructure (Bujaki and McConomy, 2022; Rossi and Sangster, 2023). The use of accounting information in imperial contexts has also been found to have a significant impact on the lives of those inhabiting conquered lands. Research on nineteenth-century Canada shows how accounting practices enabled the problematisation of indigenous populations as an object of government, the cost of which could be cut (Neu, 1999). At the same time, technologies of government based on the rationality of accounting can be used to intervene in the customs of indigenous populations, thereby incorporating them into the moral universe of the conqueror and making rule and the appropriation of their resources easier (Greer and McNicholas, 2017; Neu, 2000a; Neu and Graham, 2004; O’Regan, 2010). This use of accounting information can have distressing consequences, including the perpetuation of slavery (Silva et al., 2019), the marginalisation of women (Davie, 2017) and cultural genocide (Neu, 2000b), with accounting's instrumental rationality and neutral appearance a crucial means to ensure that those involved in the use of information can distance themselves from the consequences of their actions (Neu and Graham, 2004).

Foucault-inspired literature has also investigated the functioning of accounting in relation to non-profit institutions, which both central and local governments have often used to implement policy (Cordery, 2019; Manetti et al., 2017). In her analysis of an Italian charitable organisation between the sixteenth and seventeenth centuries, Servalli (2013) showed how accounting practices gave visibility to the problem of the poor and were employed to map the poor living in the city of Bergamo and intervene in their behaviour, with the goal of protecting social equilibrium. Educational institutions were also closely monitored through the establishment of accounting and accountability requirements, given their crucial role in creating active members of society; not only did these practices enable the efficient management of the institution, but also allowed those in power to assess how these institutions discharged their functions and if money was used solely for furthering their mission (Capocchi et al., 2022; Semeraro and Gregorini, 2021). Research into the ‘governamentalisation of the State’ (Foucault, 2007: 144) shows how technologies of government were in use well before the advent of the liberal State which, according to Foucault (2007), is the site where governmentality matured, and were enlisted in the pursuit of a variety of goals which were not limited to supporting the economy (Manetti et al., 2020).

Despite the effectiveness of accounting in turning abstract programmes of government into practice, research has warned against a deterministic approach to the study of governmental power. Neu and Heincke (2004: 203) note that ‘techniques of governance are eternally optimistic but perpetually failing’ as the ‘the differing capitals and interests of the various social groups encourage both the less than uniform adoption of … policies and frequent policy reversals’. The use of financial and monetary relations as techniques of government may become extremely costly in times of high resistance. Policies implemented by means of written technologies of government can also have unintended consequences. In sixteenth-century England the use of budgets, corn surveys and certificates, which were mobilised to tackle famine but were not coupled with adequate control on rich merchants who stockpiled grain in times of shortages, ended up becoming a means of control of lower classes and of perpetuation of both social and economic differentials (Bisman, 2012). At the same time, governmentality tools may be slow to adapt and achieve their goals because of their links with past structures (Cordery, 2019).

Scholars have also questioned the alleged linear relationship connecting political rationalities, programmes of government and technologies of government. Such linear relationship is often taken for granted in accounting history studies mobilising governmentality. French rule in parts of nineteenth-century Italy shows how Napoleon used accounting techniques to ensure the centralisation of resources and the exploitation of conquered lands to fund his wars, even if his political discourse revolved around highly desirable concepts such as freedom, happiness and self-determination (Maran et al., 2016). As a result, political discourses can be de-coupled from technologies of government whereby the former can be used to ensure the committed allegiance of individuals in their subjugation whilst the latter are enlisted as a less visible tool to pursue the real interests of those in power (Di Cimbrini et al., 2020). New perspectives on governmentality have also sought to highlight the importance of key actors in the articulation of political rationalities into programmes and technologies of government, a process that requires the intervention of individuals with both technical and social skills, whilst research tends to overshadow the role of agency consistent with Foucault's impersonal understanding of power relations (Free et al., 2020). The transnational character of accounting-based forms of governance that is allowed by accounting regimes and rhetoric has also been highlighted (Free et al., 2020; Malmmose, 2015).

Recent literature has started to explore the roots of governmentality to appreciate how the exercise of power by the State evolved over time. The concept of Raison d’État has been particularly important. According to Foucault (2007), Raison d’État as a new art of government developed in the sixteenth century, when the ‘State of justice’ started to evolve into the ‘Administrative State’. The main goal of having power was no longer protecting the link between the ruler and their domain, but increasing the forces of the State so that it could successfully compete both militarily and economically against others: to govern according to the principle of Raison d’État is to arrange things so that the state becomes sturdy and permanent, so that it becomes wealthy, and so that it becomes strong in the face of everything that may destroy it. (Foucault, 2008: 4)

To this purpose, the law, which simply states what is forbidden, was no longer sufficient and new tools, such as new bureaucratic bodies, regulations, letters and, crucially, accounting practices were needed to enable the ruler to prescribe in detail how individuals were to conduct themselves. Detailed accounting practices were implemented in Spain in 1730 for the control of the production of coins, with accountants at State mints required to manage 12 different books. This would have helped to stabilise the value of Spanish coins and support the national economy, consistent with mercantilist beliefs of the time (Baños and Gutiérrez, 2012).

Raison d’État also informed the way in which Cosimo I de’ Medici and his sons ruled the Grand Duchy of Tuscany between the sixteenth and seventeenth centuries. As he reopened the University of Pisa, Grand Duke Cosimo I issued a new statute that placed the management of the institution in the hands of the students. Nevertheless, thanks to a parallel accounting system and the creation of an ad hoc, scarcely visible bureaucratic apparatus, the Grand Duke and his successors made sure that the main resources of the University remained in the hands of the ruler, who shaped the life of his key institution by means of several, detailed interventions (Bigoni et al., 2018). Environmental regulations enacted by means of accounting were also enlisted in Ducal attempts to reinforce their State. As in the rationality of Raison d’État, the protection of the environment was not an end in itself, but a means to ensure that the population could stay healthy, which in turn would have benefitted the power and wealth of the country. By placing a newly created bureaucratic body in charge of safeguarding the Pisan territory and documenting any breaches in environmental laws, the Grand Dukes created the conditions for ‘multiplying life’ and strengthening their State (Bigoni et al., 2023).

Work on the roots of governmentality has explored Foucault's (2007) concept of pastoral power, which the French philosopher considers the genealogical core of modern forms of control. Pastoral power arose with Christianity and was exercised by a ‘pastor’ on a moving ‘flock’, thereby representing the first form of power that was exercised specifically on individuals rather than on a territory. The goal of pastoral power is deceptively benevolent as it aims at the salvation of every believer, for which purpose the pastor has to exercise strict control on each ‘sheep’ individually and on the whole flock. Pastoral power is both individualising and totalising. At the same time, the sheep have to abide by the law of God by following their pastor, to whom they owe unconditional obedience, thereby denying their self-will. Lastly, pastoral power is based on a constant extraction of the believer's truth about themselves, which enables the pastor to direct the soul of his sheep (Foucault, 2007). In the fifteenth-century Diocese of Ferrara, a careful analysis of books of revenues and expenses and detailed inventories of parish properties enabled the bishop to understand the dedication of each priest to his sacred duty and direct the conscience of the latter in a detailed way, thereby reinforcing the priest's subjugation to his pastor (Bigoni and Funnell, 2015). Other work has focused on truth-telling as a means to exercise power within the Christian pastorate (Bento da Silva et al., 2017; Bigoni et al., 2021a). In more recent times, scholars have drawn from Foucault's understanding of pastoral power to analyse reforms that ended up forcing individuals to internalise codes of behaviour that were consistent with the growth of capital markets and neoliberal priorities (Graham, 2010; Himick, 2009; Nikidehaghani and Hui, 2017).

Disciplinary power

In Discipline and Punish, Foucault (1979) contrasts disciplinary power with the traditional understandings of sovereign power. Unlike governmentality, which focuses on populations, disciplinary power concerns individuals: ‘we are never dealing with a mass, with a group, or even to tell the truth, with a multiplicity: we are only ever dealing with individuals’ (Foucault, 2006: 75). In opposition to political theories which take the individual as a given for the purpose of constructing sovereignty, Foucault shows that the individual is first and foremost a construction of disciplinary power. The individual is an effect of this form of power rather than the raw material upon which it impinges. Foucault (1979: 170) writes: ‘discipline “makes” individuals; it is the specific technique of a power that regards individuals as objects and as instruments of its exercise’. Therefore, disciplinary power produces individuals as its objects, objectives and instruments. Disciplinary power yields such effects by targeting bodies: ‘what is essential in all power is that ultimately its point of application is always the body’ (Foucault, 2006: 14). Nevertheless, pastoral power also treats the body as an object of care (Foucault, 2007) and sovereign power sets its sights on the body as an object of violence or honour (Foucault, 2006). What distinguishes disciplinary power from these other modalities of power is its endeavour meticulously to control the activities of bodies to create a particular relationship between utility and docility, whereby increases in utility correspond to increases in docility and vice versa (Hoffman, 2011).

Making the body ‘more obedient as it becomes more useful, and conversely’ (Foucault, 1979: 138) entails increasing the skills and aptitudes of bodies without allowing such skills to serve as a source of resistance. Disciplinary power controls the body of an individual but also its individuality, the amalgam of qualities that render an individual distinct from others (Arendt, 1985). This individuality consists of cellular, organic, genetic and combinatory traits (Hoffman, 2011). For instance, power creates a cellular form of individuality by ordering individuals in space (‘the art of distribution’). It does so by creating different, enclosed spaces through the use of walls or gates as in the case of barracks or factories (Foucault, 1979). Subsequently, each space is allocated to individuals who perform specific functions to make them as useful as possible (Foucault, 1979). This was well exemplified by the eighteenth-century Oberkampf manufactory at Jouy, which was ‘made up of a series of workshops specified according to each broad type of operation: the printers, the handlers, the colourists, the women who touched up the design, the engravers, the dyers’ (Foucault, 1979: 145). This cellular individuality rests on the division of individuals from others, based on the functional distribution of space within the production process. This aspect is explored by Carmona et al. (1997, 2002) through their examination of the spatial and accounting practices and their disciplinary implications at the Royal Tobacco Factory (Spain) in the eighteenth century. Another example of cellular individuality is the ranking of individuals, such as by assigning seats to students in a classroom according to their rank, grades and behaviour (Foucault, 1979). Walker (2010) depicted in detail the techniques for recording, monitoring and governing the school pupil in the early to mid-twentieth-century US through a study on child accounting texts published in the US in the same period. Madonna et al. (2014) paid specific attention to the reproduction of a meticulous system of student accountability for moral and organisational obligations at the University of Ferrara (Italy) between the eighteenth and nineteenth centuries.

Individuality is also controlled through a temporal enclosure afforded by the use of timetables and the partitioning of activities into minutes and seconds (Foucault, 1979), and by breaking down movements of the body into a number of acts, which are connected to the temporal imperatives. For instance, Foucault (1979) refers to the duration and length of the steps of marching soldiers. Therefore, the human body becomes a machine, the functioning of which can be optimised, calculated, improved and re-constructed through incessant training: ‘discipline produces subjected and practiced bodies, “docile” bodies’ (Foucault, 1979: 138). Disciplinary power is intertwined with punishment: departures from correct behaviour are punished, and failure to adhere to rules established on the basis of regularities observed over time is punished. An interesting example of punishment, documented by Lazzini and Nicoliello (2021), was the public shaming of the misconduct and theft by the trustee Angelo Ferrari, which even took the form of a commemorative plaque erected at the entrance of Galliera Hospital (Italy) by the founder, Duchess Maria Brignole Sale. Gratification is used in addition to punishment for the purpose of establishing a hierarchy of good and bad subjects (Sargiacomo, 2008).

Confinement or isolation of undesirable individuals or behaviours are alternative forms of punishment, as illustrated by Baker (2016) in his study on the evolution of French hospitals between the sixteenth and eighteenth centuries. Hospitals were originally established as a charitable form of care for the increasing number of beggars and vagrants outside French cities following civil wars. While they represented a solution to the widespread problems of poverty, begging and vagabondage, they soon evolved into centralised means of confinement of the poor and mentally ill within newly constructed buildings, located in the cities where religious orders, municipal officials and aristocrats could easily exercise repression. In the studies considered, disciplinary power, even in the form of punishments, does not subject the body to extreme violence, it is not external or spectacular. So, it differs from earlier forms of bodily manipulation such as public tortures, slavery and hanging. The target subject is not mutilated or coerced, but, through detailed training, their body produces new kinds of gestures, habits and skills.

Disciplinary power judges according to the norm, not intended as a legal concept, but as a standard of behaviour that allows for the measurement of behaviour as normal or abnormal: ‘the norm introduces, as a useful imperative and as a result of measurement, all the shading of individual differences’ (Foucault, 1979: 184). This is further explored by Bigoni et al. (2020) and Fabre and Labardin (2019). Bigoni et al. (2020) adopted a disciplinary power approach to study the prison systems in the major Italian States in the early nineteenth century. Accounting practices were used to re-construct ‘deviant’ individuals consistent with the moral priorities of the liberal bourgeois society of the time. Inmates were to learn the benefits of looking after themselves and become a ‘productive’ member of society. Fabre and Labardin (2019) highlighted the normalising practices in the penal colonies of French Guiana. They uncovered a double-faced aspect of the colonial penal system: on the one hand, French public opinion was presented with a utopian view of penal colonies as moralising and profitable institutions; on the other hand, local practices normalised a widespread system of corruption to keep the penal colonies under control. A similar contrast was identified by Carmona and Gutiérrez (2005) in their analysis of the outsourcing by the King of Spain of a portion of tobacco production to poor Catholic nuns in the nineteenth century. Whilst the decision was ostensibly motivated by drawing on arguments of compassion, the practice served as a deterrent to gender conflict within tobacco manufacturing and exploited the disciplinary tradition of nunneries.

Crucial to the exercise of disciplinary power is the ‘normalising gaze’, which rests on techniques of hierarchical observation and normalising judgement and ‘manifests the subjection of those who are perceived as objects and the objectification of those who are subjected’ (Foucault, 1979: 184–185). The examination is considered as ‘the ceremony of objectification’ (Foucault, 1979: 187), it constitutes individuality through an administrative apparatus that produces dense layers of documentation, such as medical or student records (Funnell et al., 2017, 2019). Writing makes it possible to describe individuals as objects and track their development or lack of progress. The examination implies documents that forge the individual as a set of measurements, gaps and marks. This applies to a range of organisations and individuals: Hopper and Macintosh (1993) exemplified the application of a normalising gaze to the managers of the International Telephone and Telegraph multinational firm as a personal goal of its CEO, Harold Geneen. McKinlay and Wilson (2006) argued that the expansion of the branch network of British retail banks until WWI favoured the emergence of management bureaucracies or ‘the bureaucratic career’ rather than technological development. That was the ‘modern response’ to bank organisational growth since it applied industrial discipline to large-scale manual data processing. The increasing complexity of financial control over the clerks’ functions increased the volume of receipts, dockets, hand-written copies and the organisational routines and reporting devices to monitor clerks’ discipline.

Foucault identified the shift from a society (prior to the sixteenth century) in which disciplinary power played a marginal role from within religious communities to a society (beginning in the eighteenth century) in which it played a preponderant role from a myriad of institutions, such as educational institutions, colonial establishments and military organisations. Foucault (1979) explained that disciplinary power began to function as a technique for the formation of ‘useful’ individuals and not simply for the prevention of desertion, theft or other social problems. Then, disciplinary power began to bear on society as a whole through a new apparatus concerned with individual behaviour (Foucault, 1979). Foucault found the formula for the generalisation of the exercise of disciplinary power in Jeremy Bentham's architectural plan for the model prison, the Panopticon, published in 1791. By inducing in the inmates an awareness of their own constant visibility, the Panopticon compels them to self-regulate without any violence or ostentatious display of force (Foucault, 1979). Albeit in the context of a factory, Taylor's Principles of Scientific Management (1911) abounds with examples of disciplinary power and networks of gazes that facilitate hierarchical observation. Several articles explored the linkages between disciplinary power and forms of Taylorism by investigating the emergence of the economic man (Bhimani, 1994) and the governable worker (Edwards, 2018). Specific attention is directed towards the reorganisation of the workers’ space to facilitate supervision and partitioning of tasks (Carmona et al., 1997, 2002), and of the employees’ space, either offices (Parker and Jeacle, 2019) or accounting clerks’ workstations (Labardin, 2014). From the perspective of the profession, Lambert (2021) and McKinlay and Wilson (2006) investigated the emergence of proxy advisors and British retail bank bureaucratic careers respectively. Lambert (2021) emphasised the emergence of proxy advisors which make visible to investors, through voting platforms, observations of corporations and their executives’ choices on a global scale. In turn, proxy advisors provide performance examinations to corporations and their executives by normalising investors’ judgement and ritualising this examination during corporations’ annual meetings.

Studies on disciplinary power also debated the origins of costing practices, especially for human labour (Miller and O’Leary, 1987). They mostly refer to the British (and US) industrial revolution, with a focus on factories (Fleischman, 2000; Fleischman et al., 1995, 1996; Walker and Mitchell, 1998; Walsh and Stewart, 1993). Other studies have identified a link between military academies and the spread of cost accounting (Hoskin and Macve, 1988). Fleischman (2000) clarified how in these contributions Foucauldian disciplinary power is discussed in contrast or in combination with other paradigms, such as the Marxist (labour process, see Hooks and Stewart, 2007) and the economic rationalist (neo-classical, see Walker and Mitchell, 1998). For instance, Hooks and Stewart (2007) highlighted how at the Chelsea sugar refinery, the voice of labour was silenced in the first two decades of the twentieth century and self-deception was designed to justify and insulate the hierarchy of the company. Walker and Mitchell (1998) argued that trade unions supported the employers of the British printing industry during the early twentieth century in the quest for a cost-based solution to the issue of excessive price competition in the printing sector. Fleischman et al. (1996) noted that the study of disciplinary power insists on establishing the actual point of transfer of engineering standards development (for materials and machine efficiency) to human behaviour, and in particular labour. This is also the point furthered by Fúnez's (2005) study of the Royal Tobacco Factory (Spain), an organisation that had been investigated by Carmona et al. (1997). Alternative evidence is offered by Antonelli et al. (2017), who showed how accounting enabled the coexistence of utopian socialism and capitalism in a nineteenth-century Italian silk factory.

Accounting has been often depicted as a means for exercising disciplinary power. Although most of the studies inspired by Foucauldian disciplinary power concern the poor, the disabled, the mentally ill and the ‘new slaves’, Gallhofer and Haslam (1994), by referring to the original work of Bentham, questioned the conception of accounting as a tool with potentially detrimental social consequences versus its potentialities for a better future. Baker and Rennie (2017) observed how the introduction of an accounting technology in the Province of Canada enabled a transition from a colonial sovereign rule to a more responsible form of government. Walker (2014) showed that accounting was used in the US in the 1930s and 1940s as a moralising and surveillance practice but, at the same time, as a tool to address poverty and achieve individual, familial and national betterment at a time of economic and social crisis. In their analysis of the US in the 1920s and 1930s, Jeacle and Walsh (2002) demonstrated how a new mode of record-keeping played a decisive role in the creation of an alternative to local knowledge in the granting of credit. Walsh and Jeacle (2003) and Jeacle and Walsh (2008) further studied the implications of the retail price inventory method introduced by US department stores in the 1920s and 1930s and then adopted in the UK and Ireland on consumers’ behaviour. They argued that the technique facilitated retail innovations such as self-service shopping. Servalli and Gitto (2021) focused on the pivotal role of accounting in managing fishing activities along the Adriatic Sea coastline (Italy) in the eighteenth century. They highlighted how the use of accounting ensured the provision of food in the Papal States while promoting the active protection of the stock of fish by quantifying data in fishery management: fish, fishermen, fishermen's tools and estimation of fish catch.

Power/knowledge

The understanding of disciplinary power is linked to the concept of power/knowledge, which has been seen by Eribon (1991: 127) as ‘an anchoring device for the unity Foucault gave to his work’. Foucault (1978, 1980a) does not consider knowledge formation to be a neutral phenomenon, as his play on the word ‘discipline’ (at once a branch of knowledge and a system of correction and control) exemplifies: the exercise of power itself creates and causes to emerge new objects of knowledge and accumulates new bodies of information … the exercise of power perpetually creates knowledge and, conversely, knowledge constantly induces effects of power …. It is not possible for power to be exercised without knowledge, it is impossible for knowledge not to engender power. (Foucault, 1980a: 52)

As a result, knowledge is integral to the operation of power (Townley, 1993). From this perspective, procedures for the formation and accumulation of knowledge, including the scientific method, are not neutral instruments (Steffy and Grimes, 1992; Townley, 1993). Scientific discourse and the institutions that produce it are part of the taken-for-granted assumptions about knowledge that should be questioned (Knights, 1992). Procedures for investigation and research, supported by the use of accounting statements and tables, can operate as a technique of power. This is clarified by Foucault (2003: 25) as he explained that: power constantly asks questions and questions us; it constantly investigates and records; it institutionalizes the search for the truth, professionalizes it, and rewards it. … In a different sense, we are also subject to the truth in the sense that truth lays down the law: it is the discourse of truth that decides, at least in part; it conveys and propels effects of power.

According to Townley (1993), the concept of power/knowledge has two implications: first, by showing how the mechanisms of disciplinary power are simultaneously instruments for the formation and accumulation of knowledge (coterminous to each other), Foucault challenges the positivist portrayal of them as independent. Second, power creates objects through the desire to know. As such, power is not conceived as negative but as generative: ‘in fact, power produces; it produces reality; it produces domains of objects and rituals of truth. The individual and the knowledge that may be gained of him belong to its production’ (Foucault, 1979: 194). The works of Lazzini et al. (2018), Hooper and Pratt (1993), Hoskin and Macve (1986), Jeacle (2003) and Carmona et al. (2023) are mainly concerned with the concept of power/knowledge. The works of Capocchi et al. (2022), McKinstry (2014), Ursell (2000), Carmona et al. (1997) and Hoskin and Macve (1988), although engaging with governmentality, discourse, genealogy and disciplinary power, also mobilise Foucault's insights on power/knowledge. For instance, Carmona et al. (2023) contended that the Spanish Inquisition between the sixteenth and seventeenth centuries shaped a form of power/knowledge as a politico-religious inquiry for truth. Such inquiry was shaped by the notion of infraction. Carmona et al. (2023) revealed that accounting and financial conditions mediated the processes of prosecution, punishment and imprisonment. The financial and social status of individuals impacted the inquisitorial decisions about the infractions.

To understand the exact meaning of power/knowledge, it is necessary to engage in a little translation from the French. Foucault (1972) was originally interested in how a particular type of implicit knowledge, the savoir, or common sense of time/space/people that permeates a historical period, shapes the connaissance that is institutionalised in the disciplines that make up the human sciences, including natural (e.g., biology) and social (e.g., psychology) sciences. The word pouvoir, translated as ‘power’, implies in French a potentiality. Hoskin and Macve (1986) deepen this passage between savoir, connaissance and pouvoir by studying the developments of accounting technologies from medieval times to modern history. They focus on the techniques that embodied forms of textual re-writing such as the usage of the alphanumeric system, double-entry bookkeeping and the introduction of formal examinations and mathematical marks to legitimate the profession of accountancy.

Educational systems are crucial means for the reproduction of power relations based on the production of specific forms of knowledge. In such systems, individuals have become both objects and subjects in the development of knowledge (McPhail, 1999). Foucault (1972: 227) considers every educational system ‘a political means of maintaining or of modifying the appropriation of discourse, with the knowledge and the powers it carries with it’. Lazzini et al. (2018) focused on the Italian education system between the nineteenth and twentieth centuries. They showed that the government intervened in the education system, in particular in relation to the study of accounting in the high schools of commerce, to spread values and ideas that were consistent with specific political beliefs. This included, under the Fascist regime, the creation of new mandatory courses having a clear Fascist orientation, such as corporative economics and corporative law or the identification of specific access paths to the degree in business and economics. Similar issues are analysed by Capocchi et al. (2022) in relation to the educational system of the Duchy of Lucca in the nineteenth century, where the Duchess Maria Luisa di Borbone attempted to instil Christian morality by influencing the behaviour of teachers and students in the creation of a new a regime of truth. Hoskin and Macve (1988) focused on the US Military Academy at West Point, whose graduates reproduced in society the grammatocentric and panoptic system for human accountability developed at the academy. The authors revealed how the creation of new power/knowledge relations in the nineteenth century and the diffusion of disciplinary techniques originated from elite US schools.

Other work that mobilised Foucault's understanding of power/knowledge analysed contexts as diverse as agriculture, architecture and television, thereby showing how far the ideas of the French philosophers have travelled. In The Archaeology of Knowledge, Foucault (1972) analysed how the assignment of subjective positions provides individuals with different possibilities for the exercise of power. In this vein, Hooper and Pratt (1993) emphasised the role of accounting in the growth of agricultural capitalism in New Zealand between 1926 and 1935 by studying its function of control, discipline and adjudication rather than calculation. They indicated that accounting rules and procedures, while establishing exchanges and facilitating transactions, served particular interest groups and facilitated European dominance over the Māori people. Jeacle (2003) identified a connection between the diffusion of the Georgian architectural style in the UK and its colonies and accounting. Such connection is embodied in the builders’ price book as a deployment of calculative norms, standards and accountabilities among an array of actors. It is argued that the geometric proportion and standardised façade of the Georgian classic architectural style reflected the standard construction costs established through the builders’ price book. Ursell (2000) focused on British broadcasting. When the ethos and bodies of knowledge informing legitimate practices in broadcasting shifted from public service to commercial enterprise, the goal of broadcasting was no longer spreading culture but becoming economically competitive. Consistently, costing techniques and accountants acquired much more weight and power.

Discourse

Foucault (1972, 1981) has drawn attention to the interrelation between power and discourse. In his analysis of discourse, he was not simply concerned with the grammatical and linguistic analysis of the statements of which discourses are made, but with ‘the rules which determine which statements are accepted as meaningful and true in a particular historical epoch’ (Phillips and Jorgensen, 2002: 12). Discourses ‘systematically form the objects of which they speak’ (Foucault, 1972: 49), they do not merely mirror an already existing external reality but make it ‘manifest, nameable and describable’ (Foucault, 1972: 41) thereby enabling individuals to make sense of such reality. Discourse is inextricably linked to a society's regime of truth, which identifies the accepted ways of talking about different objects of knowledge, the procedures that can be used to ‘produce’ truth and the ways in which it is possible to discriminate between true and false statements (Foucault, 1980b). Discourses govern how individuals can talk or conduct themselves within a society and, at the same time, rule out any alternative way to do so (Hall, 2001). As a result, the production of knowledge through discourse shapes social systems and has power implications (Foucault, 1979); the fundamental role of discourse in the construction of power/knowledge effects is reinforced by Foucault, to whom ‘it is in discourse that power and knowledge are joined together’ (Foucault, 1978: 100). The production of discourse within a society is always immanent to power, for control of the procedures through which discourse is selected, organised and disseminated ensures the reproduction of the existing social system (Foucault, 1972, 1981). At the same time power relations cannot ‘be established, consolidated nor implemented without the production, accumulation, circulation and functioning of a discourse’ (Foucault, 1980c: 93). This means that although regimes of truth may vary over time, the relationship between discourse and power remains fixed for they always support each other. Discourse is both an effect and an instrument of power for it is power that gives meaning and legitimacy to specific forms of discourse whilst the latter spreads the values and beliefs of dominant elites (Hook, 2001).

Research has started to conceive of accounting as discourse, one which has constitutive properties and gives substance to the phenomena it represents. Accounting as discourse has significant effects on organisations and organisational actors alike. Thanks to accounting's aura of objectivity and its link with desirable concepts such as efficiency and wealth, it is difficult to challenge accounting discourses, which are often mobilised in the implementation of liberal and neoliberal reforms. In providing different interpretations of the rise of the Financial Management Initiative, which was inaugurated in the 1980s to reform the structuring and running of UK Civil Service departments, McSweeney and Duncan (1998) showed how the Initiative could be the result of multiple interweaving language games, especially those revolving around the ‘economic liberal gospel’. However, accounting discourses can be used to ‘hide as well as reveal financial reality’ (Hooper and Pratt, 1995: 33). This was the case with the New Zealand Native Land Company at the end of the nineteenth century, where accounting information was not used to show shareholders the actual achievements of the organisation but was a discursive tool that legitimised the activities of those who controlled the company and constructed an illusion of satisfactory performance (Hooper and Pratt, 1995).

Research also investigated the interrelationship between ideological discourses and accounting in the context of totalitarian States. Studies have revealed how accounting discourses are malleable and, far from depicting an objective reality, are imbued with the values of those in power and in turn produce truth effects. Bigoni et al. (2021b) investigated accounting practices at the world-renowned Alla Scala Opera House in Milan during Fascism. The financial statements of the Opera House were used to produce a discourse that sought to present the Alla Scala as a ‘moral entity’ that was committed to its function within the Fascist State regardless of its cost. The new regime of truth brought by the Fascists also influenced what could be said, and information that was potentially embarrassing for the regime, although vital for the financial well-being of the organisation, disappeared from the Alla Scala Opera House's financial statements. Ezzamel et al. (2007) focused on the transition from Maoism to Dengism in China and how accounting was understood and used. Under Mao, the primacy of discourses that privileged the class struggle and a State-driven economy meant that accounting was seen as a product of corrupted Western capitalism which needed to be adapted to the needs of a communist country. With Deng and the opening of the country to the West, accounting was returned to its primary function of protecting property rights and enabling the distribution of wealth. The shift of regimes of truth and their impact on discourses surrounding wealth in the Bible has inspired work by Baker (2006). If in the Old Testament Abraham's wealth is praised as it was derived from his covenant with God, in the New Testament wealth is often linked with sin, and the only way to enter heaven is through poverty. This new focus, which emphasises the value of humility and self-renunciation could be justified by the attempt of the Church to create docile bodies as it sought to replace the Roman Empire in ruling over the known world.

The concept of discourse has also been mobilised to investigate the relationship between professional accountancy firms and their clients. Foucauldian understandings have enabled an analysis of the use of discursive practices as conscious political strategies that aim at the monopolisation of knowledge as a source of power (Ding et al., 2020). This was well exemplified by the case of the rise and development of the Institute of Chartered Accountants of Scotland (McKinstry, 2014). The development of an early discourse of superiority by the Edinburgh profession, culminating in the foundation of a new professional body, was instrumental in defending its monopoly of bankruptcy work. This discourse was further sustained by the Institute's successful defence of its right to exclusive use of the term ‘chartered accountant’ and by its ‘monopoly over competence’ achieved by conducting examinations. Despite the tight relationship between discourse and power, whilst discourse reinforces power, it also ‘undermines and exposes it, renders it fragile and makes it possible to thwart it’ (Foucault, 1978: 101). McKinstry (2007) sees in B. S. Johnson's novel Christie Malry's Own Double Entry a poignant critique of dominant discursive statements that supported the aims and methods of capitalistic businesses and the role of accountancy as a promoter of efficiency and competition, regardless of the impacts on human beings. McKinstry's (2007) work reveals how discourses can become a starting point for strategies seeking to oppose power (Papi et al., 2019).

Other work that has mobilised Foucault's understanding of discourse has also considered other original contexts. This is the case with Edgley's (2010) investigation of judicial cases on taxable business profits. The analysis of the truth games at play in these cases shows that ‘the outcome of judge-made practice codes may be contingent upon a number of case-specific variables, such as who spoke and how, who did not speak and what was not said’ (Edgley, 2010: 571). Notably, there appears to be a relationship between the power of those delivering persuasive arguments and wealth. Bassnett et al. (2018) focused on the first forms of writing in Uruk to reflect on accounting as non-glottographic writing and the related issues around glottographic translation. In particular, the authors identified Uruk as an ‘accounting state’ in which the first forms of naming and counting ensured that rulers could govern ‘through the mathematised regularisation and coordination of action made possible only after and through the invention of this new form of non-glottographic accounting statement’ (Bassnett et al., 2018: 2094).

Biopower

To Foucault (1978, 2003, 2008), biopower, that is power exercised over life, represents the core of the exercise of power in modern society. From the eighteenth century the main goal of having power became ‘putting life to work’ (Cooper, 2015), which required new techniques based on statistics to understand and master the lives of entire populations. Although techniques that seek to individualise are still compatible with biopower, the defining characteristic of the exercise of biopower, which Foucault (2003: 243) labels ‘biopolitics’, is totalisation: after a first seizure of power over the body in an individualizing mode, we have a second seizure of power that is not individualizing but, if you like, massifying, that is directed not at man-as-body but at man-as-species … we have, at the end of [the 18th] century, the emergence of something that is no longer an anatomo-politics of the human body, but what I would call a “biopolitics” of the human race.

Biopower represents a technology that ‘targets the body as an organism with its abilities and the body as part of broader biological processes’ (Bigoni and Funnell, 2015: 163), with the ultimate goal of understanding and including the phenomena that characterise the lives of the population into political calculus. Biopower has a deceptively benign appearance as it seeks to protect life and enable it to thrive, as demonstrated by interventions by governments that include bans on smoking in public places, vaccination campaigns and recent lockdown measures to protect citizens from COVID-19 (Antonelli et al., 2022). Nevertheless, it does not consider the real life that individuals live but rather ‘the body imbued with the mechanics of life and serving as the basis of the biological processes: propagation, births and mortality, the level of health, life expectancy and longevity, with all the conditions that can cause these to vary’ (Foucault, 1978: 139). As a result, biopower promotes a utilitarian understanding of life, which is important only insofar as it contributes to the economy and society and reinforces the State.

In the accounting history literature, biopower has been explored in two main sites: mental asylums and totalitarian regimes. The birth of social sciences is a crucial passage in the development of biopolitical techniques as they enabled the creation of a caesura in the population. The generation of new groups of individuals who were defined by specific characteristics allowed the exercise of power and control over them. In particular, psychiatry as a new science and body of knowledge on ‘deviant’ individuals gave rise to a new class, the mentally ill (Foucault, 2006). Funnell et al. (2017, 2019) analysed two nineteenth-century mental asylums where new medical techniques were experimented with. Medical statistics informed the functioning of the institutions as they were widely used to classify people based on their illness and provide evidence of the results of the new therapies being implemented, which were a measure of the progress made by individuals towards ‘sanity’ and, hence, return to society. The main goal of these mental asylums was to re-educate individuals so that, on release, they would be able to sustain themselves without the assistance of the State, which was a burden to taxpayers. Accounting practices also performed an external function when they were used to justify costs incurred for containing the phenomenon of madness within acceptable limits, thereby demonstrating that mental asylums deserved public funding.