Abstract

Introduction

This special issue on Accounting for Natural Disasters: An Historical Perspective originates from the observation that, regardless of the vast archives of surviving records about natural disasters, accounting history research has tended to almost neglect their study totally (Quarantelli, 1998; Schenk, 2007). Natural disasters are primarily social phenomena and also identifiable in social terms (Quarantelli and Dynes, 1977: 24). Indeed, in prior centuries, natural disasters have struck different territories, organisations and societies, thus challenging the existence of human beings, businesses, local, regional, national and global systems.

For centuries, till the recent 2023 Morocco earthquake and Lybian storm/flood, the rhythm of life has been punctuated by the sudden, rapid and destructive effects of natural disasters, such as earthquakes (Sargiacomo, 2011, 2015; Sargiacomo and Walker, 2022; Sargiacomo et al., 2014), tsunamis, hurricanes (Baker, 2014; Perkiss and Moerman, 2020), bushfires (Taylor et al., 2014), floods (Lai et al., 2014; Sciulli, 2018) and volcanic eruptions. Regrettably, besides these latter calamities, there are also natural catastrophic events, such as droughts (Walker, 2014) and epidemics, such as plague, cholera, typhoid fever, Spanish flu, HIV (Rahaman et al., 2010) and others. They have marked the calendar of global history, provoking death tolls and economic and social impacts, which are comparable – if not worse – than the (still ongoing) Covid-19 disaster (see, for instance, Grossi et al., 2020; Leoni et al., 2021; Parker, 2020; Sargiacomo et al., 2021a; Servalli, 2020; Yu, 2020). It will suffice to remember that in 1347–1351, the bubonic plague provoked a death toll of around 200 million people, who were 30 per cent of the world population at the time (Gottfried, 1985; Snowden, 2019). Often, natural disasters are interconnected: the US Dust Bowl in the mid-1930s unleashed plagues of jackrabbits and grasshoppers and triggered influenza, dust pneumonia and lung diseases which often proved fatal (Worster, 2004). History is rich with evidence about natural disasters, however, to date, only a few scattered studies in accounting history have closely examined the relationships between accounting and these catastrophic events.

The ‘call for papers’ for this special issue sought to stimulate robust and rigorous work on this theme, making use of diverse theoretical and methodological perspectives and encouraging studies from within or across specific countries or regions. The topics advanced in the ‘call for papers’ included, but were not limited to the following:

the use of accounting, accountability and calculative practices by the state, local governments, non-governmental agencies, businesses, households and other organisations such as hospitals and not-for-profit organisations, to measure the economic effects of the disaster in which they have been involved; the linkages between disaster's costing and funding activities of the involved governmental and non-governmental organisations, to provide relief and recovery to the affected territories and populations; the use of accounting practices to support the interventions during the emergency and/or the recovery stages, as well as the use of accountability, auditing and/or control mechanisms in these processes; the role played by and collaboration between accountants and other experts at the local, regional, national and supranational levels, during and after the emergency, in order to design technologies of government and governance to meet public interest needs; the interrelations between accounting and urban planning during and after the emergency; the use of accounting, accountability and reporting practices to fuel the re-launch of the territories and populations affected and pave the way for the subsequent reconfiguration of the entire ecosystem.

Preparing the ‘call for papers’ stimulated a further analysis of the published historical research on the theme, aimed at identifying the main topics and trends in historical research about natural disasters, the extent of adoption of particular theoretical perspectives, the nature of sources examined, the periods of time investigated and the main contributions of published research on accounting's past within natural disasters’ settings (Sargiacomo et al., 2021b).

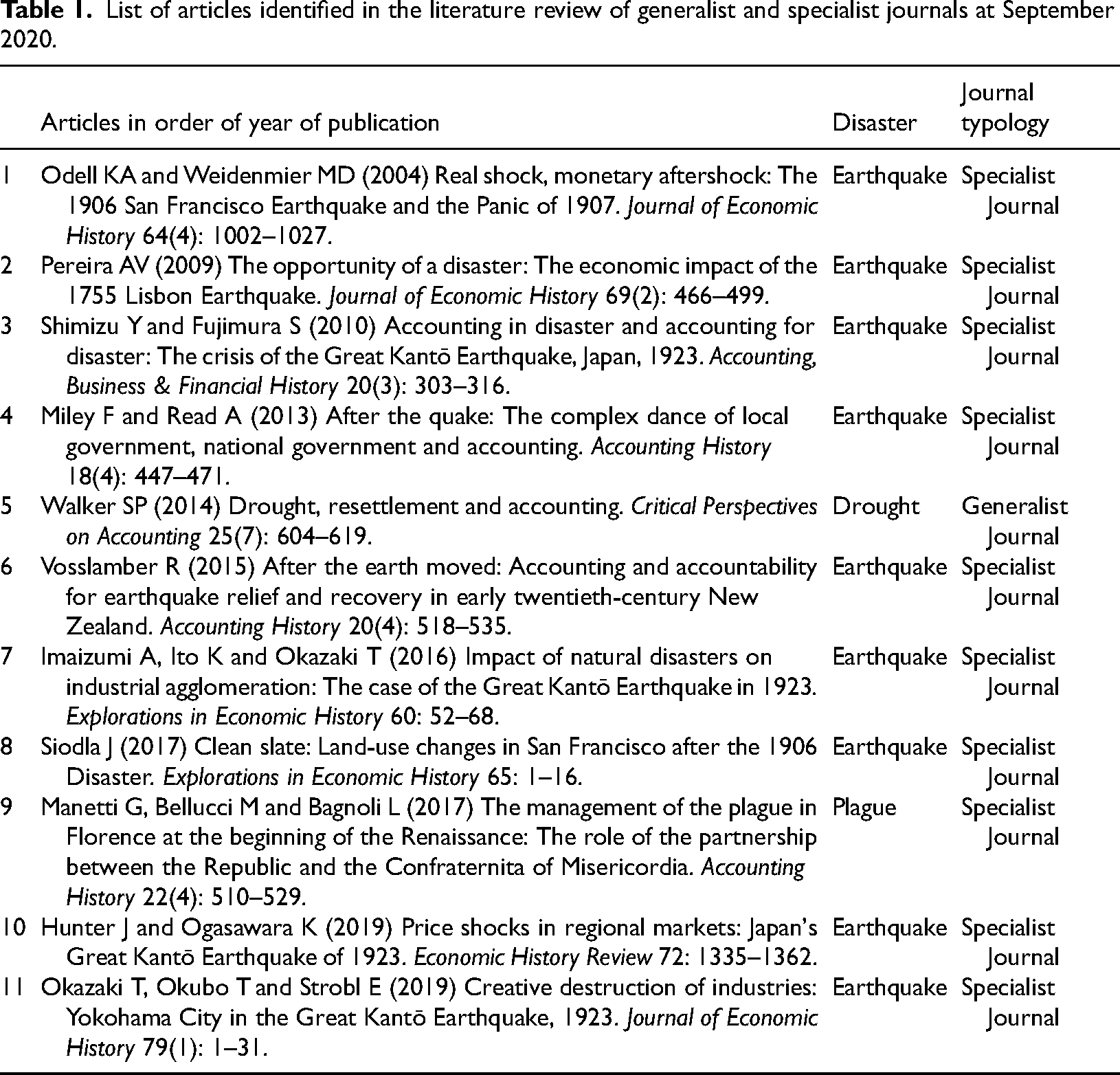

This analysis was based on a set of specialist and generalist journals: 17 specialist journals 1 listed by the Chartered Association of Business Schools’ ABS 2018 Guide and classified within the cluster labelled as ‘History & Economic History’ were analysed together with a list of 18 generalist accounting journals 2 from the ABS ‘Accountancy’ cluster; 11 relevant articles were identified on the theme, as shown in Table 1 (Sargiacomo et al., 2021b: 185).

List of articles identified in the literature review of generalist and specialist journals at September 2020.

Glancing through Table 1, it immediately emerged that only a few journals – namely, Accounting History, Accounting Business & Financial History (now Accounting History Review), Critical Perspectives on Accounting, Economic History Review, Explorations in Economic History and Journal of Economic History – have published a small number of articles on natural catastrophes, thus confirming that the ‘natural disaster’ area of research had been almost totally neglected till September 2020, when the observation period on the 35 selected journals was concluded. Moreover, it immediately appeared that most studies were addressed to earthquakes (i.e., Hunter and Ogasawara, 2019; Imaizumi et al., 2016; Miley and Read, 2013; Odell and Weidenmier, 2004; Okazaki et al., 2019; Pereira, 2009; Shimizu and Fujimura, 2010; Siodla, 2017; Vosslamber, 2015), thus leaving most natural calamities completely overlooked by existing historical research in accounting, business and economic history journals. By comparing a search on ‘sudden … rapid, and destructive … natural forces, such as floods, hurricanes, volcanic eruptions and earthquakes’ with ‘slow moving disasters such as droughts … and epidemics’ (Pfister, 2006: 35), it emerged that a few exceptions about non-earthquakes calamities included only Walker (2014) on early twentieth century US droughts and Manetti et al. (2017) on late sixteenth-early seventeenth century Florence plague.

The analysis of the existing literature also highlighted a strong concentration of studies addressed to the same loci of investigation (e.g., 1929–1931 New Zealand's earthquakes; Great Kantō earthquake), thus witnessing more interest in a very small number of disaster places, and leaving an open highway to accounting historians willing to roll up their sleeves and examine new archives containing unexplored records on disasters, which have never been studied. Importantly, this analysis provided researchers with clear ideas not only on new places and disasters to be investigated but also on archives containing records of prior major calamities partially examined, and that might have been objects of subsequent analysis, using a different perspective.

With the above analysis as a point of reference, further research was called for with new disasters’ foci and loci to be investigated, by offering a partial and incomplete list of new studies to be undertaken in the near future (Sargiacomo et al., 2021b, Table 6: 194–195) from which authors could take inspiration to develop their studies.

The analysis of the articles accepted in this special issue

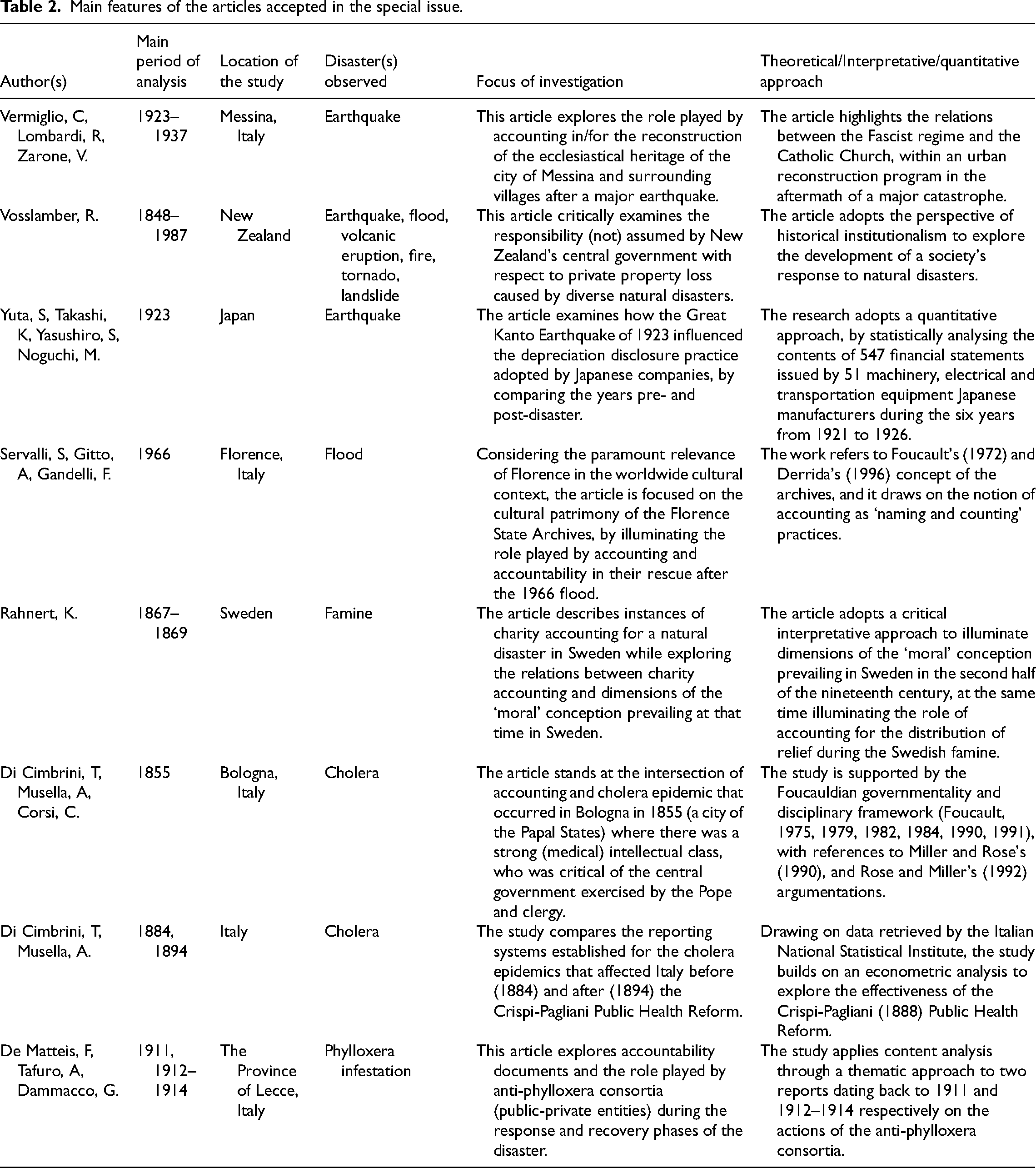

By way of adding to the publications listed in Table 1, the eight articles of this special issue of Accounting History embrace different themes, foci and loci of disasters. Importantly, they are informed by both specific theoretical perspectives, and critical interpretative approaches, as well as quantitative analyses. The articles are focused on the nineteenth and twentieth centuries and provide insights from four countries: Italy, with five studies, New Zealand, Sweden and Japan.

Importantly, the eight articles in this special issue reflect the changes occurring within accounting history research in general, by recognising that accounting is also a social practice with implications for organisational and social functioning, besides being perceived as a technical practice. The main features of the articles accepted for this special issue are summarised in Table 2.

Main features of the articles accepted in the special issue.

A brief comment on each of the articles accepted for the special issue follows.

The article by Vermiglio et al. (2024) is situated in Italy, during the twentieth century, and it is focused on the urban reconstruction program in the aftermath of the 1908 major earthquake. Importantly, the study highlights the interrelations between the Fascist Regime and the Catholic Church, at a time when the emergency drove public attention to the reconstruction of the ecclesiastical heritage of the city of Messina and surrounding villages. This peculiar perspective is pursued through a wide range of primary and secondary sources, which have helped to examine the role played by accounting and calculative practices during the development of the reconstruction program that was promoted not only by the government but also by the new metropolitan Archbishopric of Messina. In doing so, this research adds new lenses to elucidate the interrelations among accounting, disasters and urban reconstruction. At the same time, it outlines the use of the reconstruction plan of churches and main buildings by the Fascist regime, as a tool to gather consensus among the Catholic electorate.

Positioned between nineteenth and twentieth-century New Zealand, the article by Vosslamber (2024) critically examines the responsibility of the New Zealand central government in private property loss caused by diverse 1848–1987 natural disasters, ranging from earthquakes to floods, volcanic eruption, fires, tornados and landslides. The analysis concerns the financial relief provided by diverse governments to New Zealanders who suffered a loss due to a natural disaster. The article emphasises that the state did not assume responsibility for private property loss in New Zealand, from early settlement until 1990, although some changes occurred during the very long observational period. The author, rather than focusing on a single disaster event or a specific disaster type, explores a range of disasters, through the lens of historical institutionalism. This adds to the research agenda of accounting for natural disasters, by investigating governmental responses and relief policies across 140 years.

Early twentieth-century Japan is the focus of the article by Yuta et al. (2024), who sought to ascertain whether or not the depreciation disclosure practices deployed by Japanese companies after WWI have been affected by the sudden and massive impact of the 1923 Great Kanto earthquake. By statistically examining the contents of 547 financial statements issued by 51 machinery, electrical and transportation equipment manufacturers during the 1921–1926 time span, the authors have tried to examine if and how this large-scale exogenous natural shock has affected and shaped corporate accounting practices. The comparison of the accounting practices in the years before and after the shock shows that the enormous damage triggered by the Great Kanto earthquake discouraged companies from disclosing depreciation expenses, either by diminishing them or by missing the opportunity to recognise them at all, thus ascribing them to a minor record in the financial statements.

Servalli et al. (2024) aim to explore the role of accounting for natural disasters by focusing on the 1966 Florence flood. Building on Foucault's (1979) and Derrida's (1996) concept of the archives and drawing on the notion of accounting as ‘naming and counting’ practices, the authors investigate the role that accounting, and accountability practices had in the rescue of the cultural patrimony enshrined in the Florence State Archives. The analysis shows the role played by accounting to save the Florentine archival patrimony, in particular, whilst the adopted ‘naming and counting’ practices allowed them to identify and inventory the damaged documentation, accountability activities offered researchers knowledge on historical documents that were not available for investigation. This article aptly highlights that the cultural patrimony of one of the most important cities in the worldwide cultural context has been returned to its community of reference through the deployment of accounting practices which enabled the exercise of the power of re-‘consignation’.

Focusing on a time when dimensions of ‘moral’ conception were characterising nineteenth century Sweden, the article by Rahnert (2024) aims to provide a portrayal of instances of charity accounting as related to the Swedish famine of 1867–1869. The research builds on the accounts of the Stockholm Relief Committee for Norrland, a purposely built temporary charity organisation set up during and for the disaster. The author highlights how ‘moral’ conceptions affected not only the distribution of relief but also what was accounted for. Moreover, and most importantly, the study shows precise charity features, supporting the view that accounting was used to increase the ‘moral’ reputation of those donors’ classes who acted in the interest of those in need. By doing so, the article emphasises not only accounting technical distributive and allocative properties but also the role played by accounting as a social and moral practice with broader implications for a community affected by a disaster.

Di Cimbrini et al. (2024) analyse the case of a cholera epidemic that occurred in Bologna in 1855. The Italian scenario of this investigation offers peculiar features for a natural disaster case, starting from the presence in Bologna – a city of the Papal States – of an influential medical intellectual class, who was critical of the central government policies exercised by the Pope and his clergy. By building on a wide range of primary and secondary sources available in Bologna in the Municipal Library of the Archiginnasio, State Archives and Municipal Historical Archives, the authors emphasise how the accounting for and of the epidemic challenged the original hierarchical power structures of the Papal States. The study also outlines how the deployment of medical-administrative accounting technologies enabled the medical establishment to replace the clergy and local aristocracy in the governing body of the city, thus paving the way for the future removal of local ecclesiastic and noble control of its administration.

In another study situated in nineteenth century Italy, Di Cimbrini and Musella (2024) complement and extend the prior analysis of the medical establishment in Bologna during cholera, by examining the extant reporting systems for the cholera epidemics before (1884) and after (1894) the Crispi-Pagliani Public Health Reform of 1888. This reform profoundly transformed prior practices by establishing a new pyramidal information system, where a strong concentration of medical professionals was asked to scientifically validate the data at all hierarchical levels of the information processing. Building their research on an econometric analysis of the data retrieved by the Italian National Statistical Institute, the authors prove the broader effectiveness of the new reporting system vìs-à-vìs the prior one. In particular, the new system was more effective in guiding the central government allocation of the medical staff in the territories where the epidemic was more acute, thus appearing more effective in terms of the containment of death. On the one hand, the article adds to our knowledge concerning the reporting systems implemented by governments to prevent or contain contagion during epidemics; on the other hand, the article supports the use of econometrics in accounting history.

De Matteis et al. (2024) deal with the interrelations of accountability and hybrid organisations (consortia) to face and prevent viticulture epidemics. In the context of the phylloxera infestation disaster of Apulia region (Italy), their article investigates the functioning of anti-phylloxera consortia (public–private entities) during the response and recovery phases of the disaster. At the same time, they explore the informative value and characteristics of accountability documents about the consortia activities. The actions of the anti-phylloxera consortia are examined through a content analysis that applies a thematic approach to two reports dating back to 1911 and 1912–1914. In terms of the history of hybrid organisations, the article demonstrates the effectiveness of public-private collaborations enacted by the consortia to better manage natural disasters’ impact, while reducing this impact on organisations and societies. Using the accountability perspective, the article highlights that the documents investigated have a relevant informative capacity, supporting knowledge dissemination and coordinated actions during the phylloxera infestation period.

Conclusions and call for further research

The challenges and avenues for future research identified in Sargiacomo et al. (2021b) continue at the time of this editorial. Undoubtedly, the eight articles published in this special issue add to the scarce accounting history literature on disasters, but historical investigations on natural disasters are still underdeveloped. It will suffice to glance through the literature map depicted in Table 6 of Sargiacomo et al. (2021b: 194–195) to figure out how many histories of natural disasters still need to be unveiled. At this stage, there are still no studies in generalist/specialist journals on tsunamis (e.g., Phuket, Thailand, 2004) and volcanic eruptions (e.g., Azores Islands, Portugal, 1957–1958), in historical perspective, despite the enormous impact they have had in history on organisations and societies.

In terms of loci of investigation, with the exception of the novel article on the earthquake from Japan, we still continue to see very few articles from the Middle East (i.e., Ayalon, 2017) and/or based on Asian countries (i.e., China, India and Pakistan, Indonesia, Thailand, Vietnam and others). Analogously, some kinds of disasters, like floods, are neglected in spite of a general rising historical literature on natural disasters (e.g., Courtney, 2019; Janku, 2007). Whilst this special issue features an increasing number of studies on hitherto unexplored Italian sites of investigation and a work based on Sweden, there is still much to learn about the history of European cities and catastrophes (Massard-Guilbaud et al., 2002).

Considering the high number of natural disasters in the US, and the few existing exceptions of studies developed by economic historians on earthquakes (i.e., Odell and Weidenmier, 2004; Siodla, 2017) and by accounting historians on droughts (Walker, 2014), there is the need to pursue new studies on disasters from an accounting perspective. For example, there are rare studies on contemporary storms and floods (Baker, 2014; Perkiss and Moerman, 2020; Sciulli, 2018) and there is still much to learn about their effects on factories, houses, railways, the accounting profession and societies in general. The same observation can be repeated for earthquakes.

With these premises, there is still much to learn – from an accounting perspective – about the impact of the 1913 Great Dayton flood (see Bell, 2008), the 1927 Great Mississippi flood (see Barry, 1998) and California's early and late twentieth century earthquakes (i.e., San Francisco, 1908; Long Beach, 1933; San Fernando, 1971). Finally, the absence of studies on droughts and famine in Africa (van Apeldoorn, 1981) is noticeable.

I suggest a further differentiation of disasters loci of investigation, but in terms of foci of investigation, I continue to support the suggestions in Sargiacomo et al. (2021b), as follows:

Accounting and calculations for the measurement of the comprehensive economic impact of disasters; Costing of industries, analysis of technological change and impact on industrial agglomerates in the aftermath of disasters; Accounting and the historical impact on land use and houses/business reconstruction in the economics of the devastated cities/regional areas or accounting, city reconstruction and disasters; Disasters, migration(s), relocation(s) and accounting; Accounting, charities and the role of not-for-profit organisations after natural disasters; Accounting, family/household business and post-disaster economic re-launch; Accounting and financial history of the impact of external shocks on financial markets; The role played by and collaboration between accountants and other experts at the local, regional and national levels, during and after the emergency, in order to design technologies of government and governance to meet public interest needs; Auditing and control mechanisms in the allocation of public monies destined to fund the emergency and recovery of/from the impact of natural disasters.

More studies – on all disaster types – may concern the interplay of local governments and central governments, which seems to be almost completely neglected (Gomes and Sargiacomo, 2013) in the literature about disasters. To date, there are no comparative studies that have concurrently analysed accounting systems of diverse disaster types in various countries. I acknowledge that historical examinations have concerned comparative histories of disasters in Europe and Asia (Schenk, 2017), confirming the need for future studies on ‘Comparative International Accounting History of Disasters’ research (Carnegie and Napier, 2002). Considering the warnings raised by the United Nations Office for Disasters Risk Reduction (UNDRR, 2019), and the increasing number of natural disasters that have been threatening the world till the end of 2023, I urge further historical research on the theme, since understanding the past might help policymakers and experts to better comprehend and guide our present and future (Abramitzky, 2015).

Finally, I want to take this opportunity to acknowledge the support and impetus provided by the joint editors of the journal Carolyn Cordery, Carolyn Fowler and Laura Maran on this special issue and the assistance of the editorial assistant, Anna Burnett. I also wish to thank the reviewers for their thorough work and congratulate the authors for all their effort in developing and publishing their research for this ‘very special issue’.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.