Abstract

The purpose of this systematic literature review on ‘indigenous peoples and accounting’ is to identify major themes and derive insights to guide future research and policy agendas. We also investigate whether accounting has been used by the indigenous peoples for emancipation. Seventy-one peer-reviewed journal articles are categorised into three clusters (imperialism, accounting profession and need for emancipation) and analysed. This review positions accounting not as a mere neutral, benign, technical practice but as a racist and ethnocentric tool through the context in which it has been practised. Accounting was an integral part of imperial rule, inheriting colonial structures and separating and reducing indigenous peoples from their own cultures and structures. Indigenous accountants remain severely under-represented; indigenous autonomy, voice and participation are vital for transforming the ethnocentric systems that have led to the devaluation of indigenous peoples. For effecting change we identify a need to focus on forward-looking solutions and how indigenous cultural values can contribute to a more enabling accounting.

Keywords

Introduction

Scientific and technological development in the eighteenth and nineteenth century in Europe facilitated the age of the colonial empires (Brockway, 1979). As a result, between 1800 and 1914 the amount of the world's land surface controlled by Europeans increased from 35 to 84 per cent (Fieldhouse, 1973). Although military force formed the backdrop against which technologies of government were deployed in the remote colonies, the continual use of military force would likely have been too costly to maintain. Along with the hardware (guns) of imperial control, there was other software which influenced the process of imperial expansion, accounting being one of them (Bell et al., 1995). Indigenous peoples came to be known as a ‘site for cost cutting’ (Neu, 1999: 66) and accounting was used for cost control and as a form of administrative imperialism (Horvath, 1972).

The term ‘indigenous’ is a much-contested term (Bello-Bravo, 2019). It carries a span of meanings – it conveys a sense of original or first inhabitants who become ‘the inferior inhabitants of a place subjected to alien political power or conquest’ (Thornberry, 2013: 37). It further implicates significance of historical movement, characteristic cultural identification, attachment to land, the community right, and the relevance of discrimination or objectification by outsiders (Thornberry, 2013). The United Nations Forum on indigenous issues recognises that when people of different cultures or ethnic origins arrived, the latter became dominant through conquest, occupation, settlement or other means (United Nations Forum, 2021). Colonialism was carried out in the name of an essentialised European racial superiority (Bell, 2004: 123), wherein indigenous cultures were considered ‘savage’ and ‘primitive’. Indigenous peoples in most former colonies have a shared history of dispossession and devastation. 1 While there has been increasing interest in the impact of colonialisation on indigenous peoples around the world, with a particular focus on restoring justice, 2 due to the differentiating issues of indigenous people from dominant cultures, there is a need to ‘better understand how colonialism continues to structure the relationship between governments and indigenous peoples’ (Greer and Neu, 2009: 480).

With regards to accounting, researchers have highlighted its positioning within processes of colonialism and imperialism, suggesting that accounting discourses and technologies have been used to influence and control indigenous peoples (see Davie, 2005a; Fleischman and Tyson, 2004; Neu, 2000a). Accounting allowed a form of selective visibility which identified the value and identity of the property but not the lives behind the numbers, thereby dehumanising them and in turn allowing bureaucrats to be removed from the consequences of their actions (Antonelli et al., 2018).

This article analyses the literature on ‘indigenous peoples and accounting’ to examine the impact accounting has had on indigenous culture, identity, existence and professional participation. In line with other accounting literature reviews (e.g. Cuozzo et al., 2017; Goyal and Kumar, 2020; Wolf et al., 2020), this article adopts a systematic approach to review the articles. Given the ‘complex differences between groups of indigenous people’ (Gallhofer et al., 2000: 384) our aim is to explore the major themes of research in this area rather than providing in-depth and critical examination of the articles.

Accounting can be broadly defined as recording, classifying and interpreting monetary transactions that are set in a framework. It has been long-understood and taught as a technical practice undertaken to provide information for external and internal stakeholders, but it is also increasingly being recognised as a social and moral practice (Carnegie et al., 2021). Carnegie et al. (2021) further argue that it is progressively conceived as an instrument of power and control, and as a pervasive, enabling and disabling social phenomenon. Particularly, our literature review indicates that accounting has been used by European powers, mainly Britain, to exercise control over their indigenous peoples and their territory.

The world's first professional accountancy body was established in Scotland in 1854 (Paris, 2016); others followed in England and Wales in 1880 and the United States, Canada, Australia and Aotearoa New Zealand during the 1880s and 1890s (Vidwans and Whiting, 2022). Thus, accounting in the nineteenth century was part of a new colonial discourse (Hooper and Pratt, 1995). Many colonial accountants hailed from the United Kingdom and accounting practices followed British accounting in the colonies (Cooper, 2010; McNicholas and Barrett, 2005; Richardson, 1989). Entry was restricted to those who met stringent requirements such as educational credentials, examination passes and work experience requirements (Chua and Poullaos, 1998; McKeen and Richardson, 1998). These closure strategies also used criteria unrelated to competence or merit to exclude people from practice (Richardson, 2017; Vidwans and Whiting, 2022) and as a result indigenous participation was limited.

Accounting history research is broad and diverse in the subjects it addresses, the methods it uses, the theories chosen to inform it, and the periods and places it studies (Carnegie et al., 2020). There is an increasing realisation that accounting and accountability systems, like many other aspects of social and political life, are complex, multidimensional and paradoxical (Greer and Patel, 2000). A key motivation for this article is to address the call for research to examine the positioning of accounting in colonial processes and to contribute to current policy debates about government indigenous relations. We highlight the ways in which the colonial powers used accounting as a tool for imperialism and professional closure, and the increasing need for emancipation. We resonate with the call by Lombardi and Cooper (2015: 96) who state that for indigenous peoples, ‘it may take another 200 years to achieve the same quality of life indicators as those of non-Indigenous peoples, but an initiative to create change in the space of accounting is urgently needed’. Therefore, it is important to understand the research that has been undertaken in this space and strengthen the knowledge base to bring about change for tomorrow.

The remainder of the article is structured as follows. The next section discusses the research questions and method employed. This is followed by a thematic analysis of the reviewed articles in terms of their characteristics and the findings. The last section draws conclusions, outlines the limitations of the article, and presents implications for future research.

Methodology

Research questions and method

A literature review was conducted with the main aim to identify the body of academic literature on ‘indigenous peoples and accounting’ that exists globally, and develop insights (Massaro et al., 2016; Tranfield et al., 2003). There are several approaches to conducting a literature review that differ in terms of the rules applied (Massaro et al., 2016). To identify a suitable method for this article, various approaches were explored that have been used to review accounting literature including meta-analysis (see Khlif and Chalmers, 2015), structured literature review (e.g. Ascani et al., 2021; Cuozzo et al., 2017; Massaro et al., 2016), systematic literature review (e.g. Goyal and Kumar, 2020; Wen, 2021; Wolf et al., 2020), and the literature reviews by Apostolou et al. (2019) and Paisey and Paisey (2004). A systematic literature review was chosen due to its focus on identifying key contributions to a field, rather than offering ‘a statistical procedure for synthesising findings’ (Tranfield et al., 2003: 209) as meta-analysis does. Further, systematic literature reviews can extract ‘insights from a variety of studies in a replicable, transparent and inclusive process’ (Wen, 2021: 240) strengthening the knowledge base.

The research questions (RQ), below, are guided by the motivation outlined in the Introduction section.

What research has been undertaken examining indigenous peoples and accounting?

What impact has accounting had on indigenous peoples?

Literature search

The literature search for research on ‘indigenous peoples and accounting’ followed several steps and was not restricted to a specific time period, journal type or journal ranking (Kubicek and Machek, 2018b; Wolf et al., 2020). Search criteria included limiting the search to peer-reviewed articles written in English, which were available in full text. To identify the relevant literature, two databases (Science Direct and ProQuest) were chosen based on their coverage of accounting journals and their popularity in accounting and business research. The limitations of our search criteria are acknowledged in the last section of the article. Using synonyms for ‘indigenous’, the following keywords were searched, and where possible based on the database settings this keyword search was restricted to the title, abstract and keywords of articles: (accountancy or accountants or accounting) AND (indigenous or Māori or native or black or non-white or aboriginal or ‘first nations’).

The search identified 676 articles. Articles that contributed to the understanding of how accounting practices were used as a tool for imperialism and the position of indigenous peoples in accounting were included. A series of screening steps were applied to determine articles for exclusion (Ascani et al., 2021; Wolf et al., 2020) including identifying duplicates, sorting articles by relevance, reviewing the abstract, the title and keywords for relevance, and reviewing the full article. Several articles were found to be irrelevant to indigenous peoples and accounting, including out-of-context use of the synonyms for indigenous. Examples include articles that used the terms digital native, Black's theory, black money, black box, black hole, black and white, or native India in a context that was not relevant to the subject of this literature review.

The final sample of 71 articles was imported into the reference management software Endnote (Wen, 2021), and article characteristics were extracted into a spreadsheet for further analysis.

Analytical framework

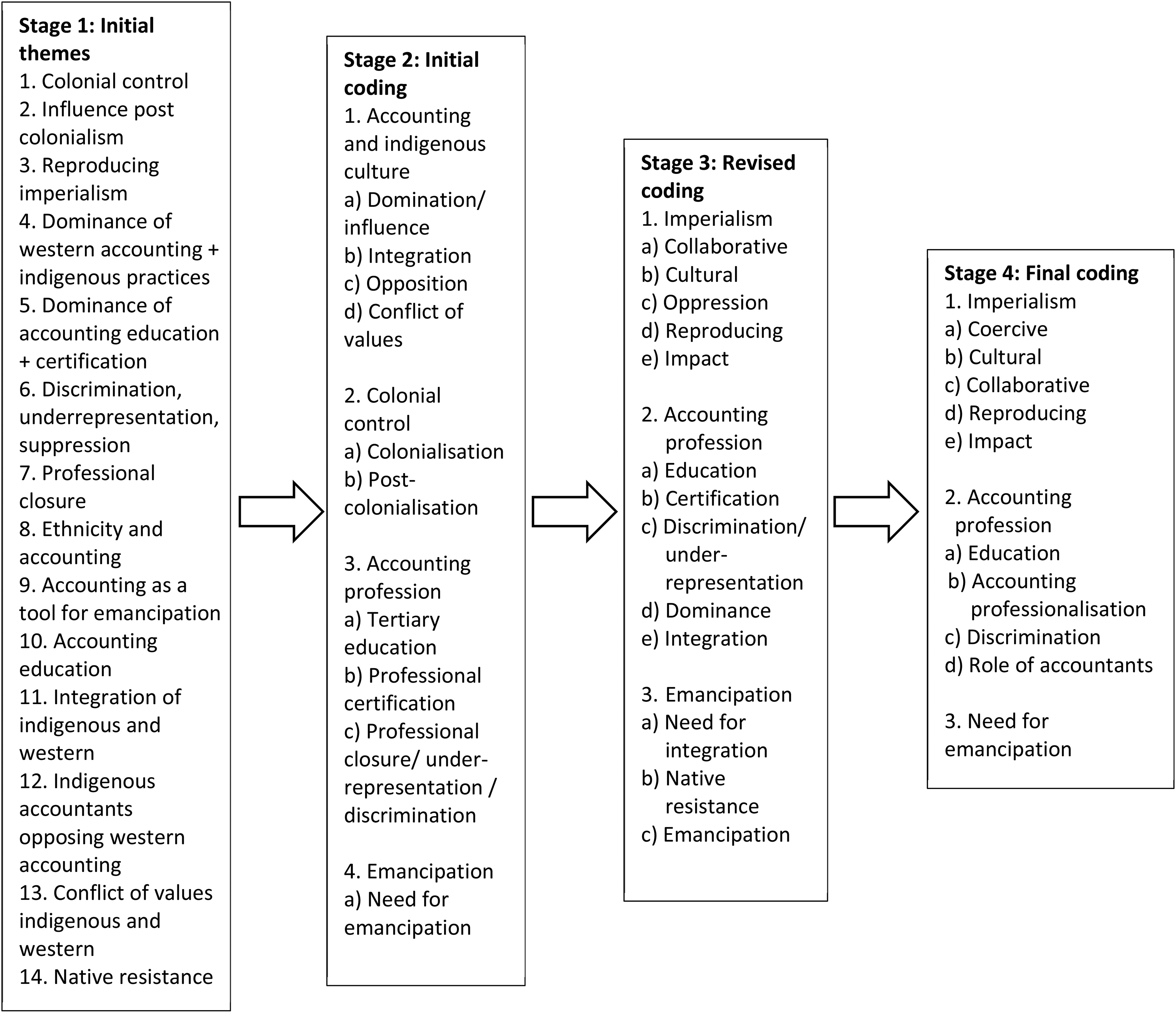

Once the final sample was identified, thematic analysis was undertaken to review the articles using a four-stage process to classify articles into clusters and sub-clusters, as shown in Figure 1. First, an initial review of the title, abstract and keywords of the 71 articles was undertaken by the researchers (two authors and a research assistant) with different backgrounds and familiarity with the key concepts in this project. This identified 14 initial themes. There was no attempt to predetermine or define any of the themes used. The researchers discussed the differences in initial themes assigned to articles and full agreement was reached as to the dominant theme applied to each article. Second, these initial themes, some of which were overlapping, were grouped into clusters and sub-clusters. Articles were coded according to which sub-cluster their dominant initial theme/s related. Stage three involved reviewing each article to identify the dominant theme. This resulted in the regrouping of some of the articles and the renaming of some of the clusters and sub-clusters. For example, ‘colonial control’ was renamed using the broader term ‘imperialism’. 3 Finally, in stage four, an in-depth analysis of the articles resulted in some articles being re-coded to different clusters or sub-clusters to ensure a more meaningful grouping of articles. The final coding consists of three clusters that were named based on the overarching theme of the sub-clusters.

Four-stage coding process.

To ensure the reliability of the analytical framework, Krippendorff's alpha (K-alpha) was applied (Krippendorff, 2018; Massaro et al., 2016). The K-alpha is an inter-coder reliability test and helps to assess the quality of coding, reducing differences that may be caused by the coding instructions or personal bias of the researchers. K-alpha scores of above 0.800 indicate results are reliable, while K-alpha scores between 0.667 and 0.800 indicate that only tentative conclusions can be drawn. The K-alpha was calculated at stage one prior to any discussions between the researchers and again at stage four of the coding, and was 0.4726 and 1.000, respectively.

Characteristics of the reviewed articles

Several characteristics of the 71 articles reviewed are presented below including the journals, publication impact, the indigenous peoples, publication timeframe, theoretical framework and methods employed by the articles (Apostolou et al., 2019; Wolf et al., 2020).

Journals

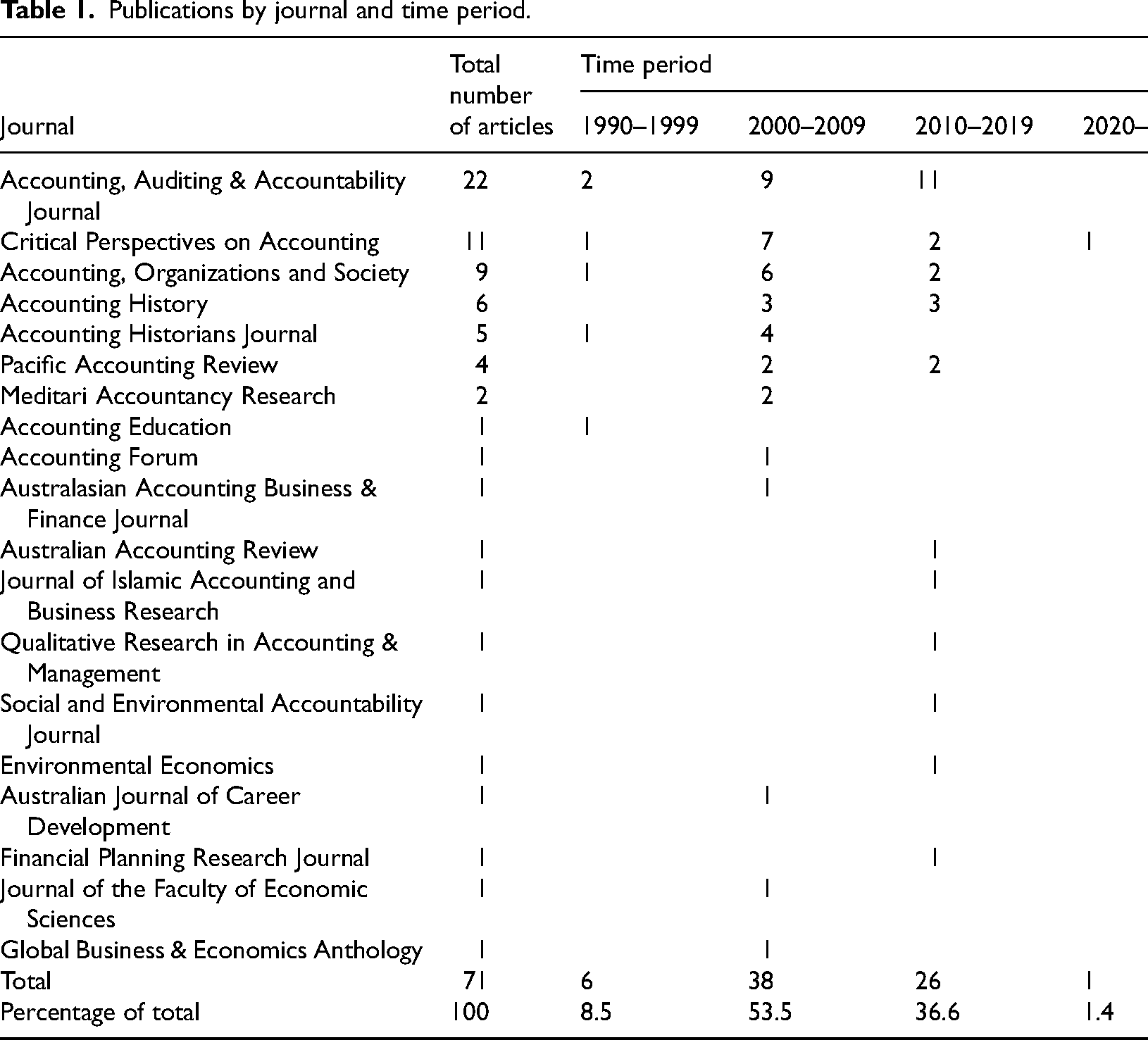

The number of publications in each journal is shown in Table 1. The 71 articles were published in 19 journals, with the majority (14 journals) being accounting journals. The Accounting, Auditing & Accountability Journal was the dominant journal, publishing 22 articles. Critical Perspectives on Accounting, publishing 11 articles, and Accounting, Organizations and Society, publishing 9 articles, concluded the top three journals. Twelve journals published only one article each, representing 17 per cent of the total articles reviewed.

Publications by journal and time period.

Publication impact

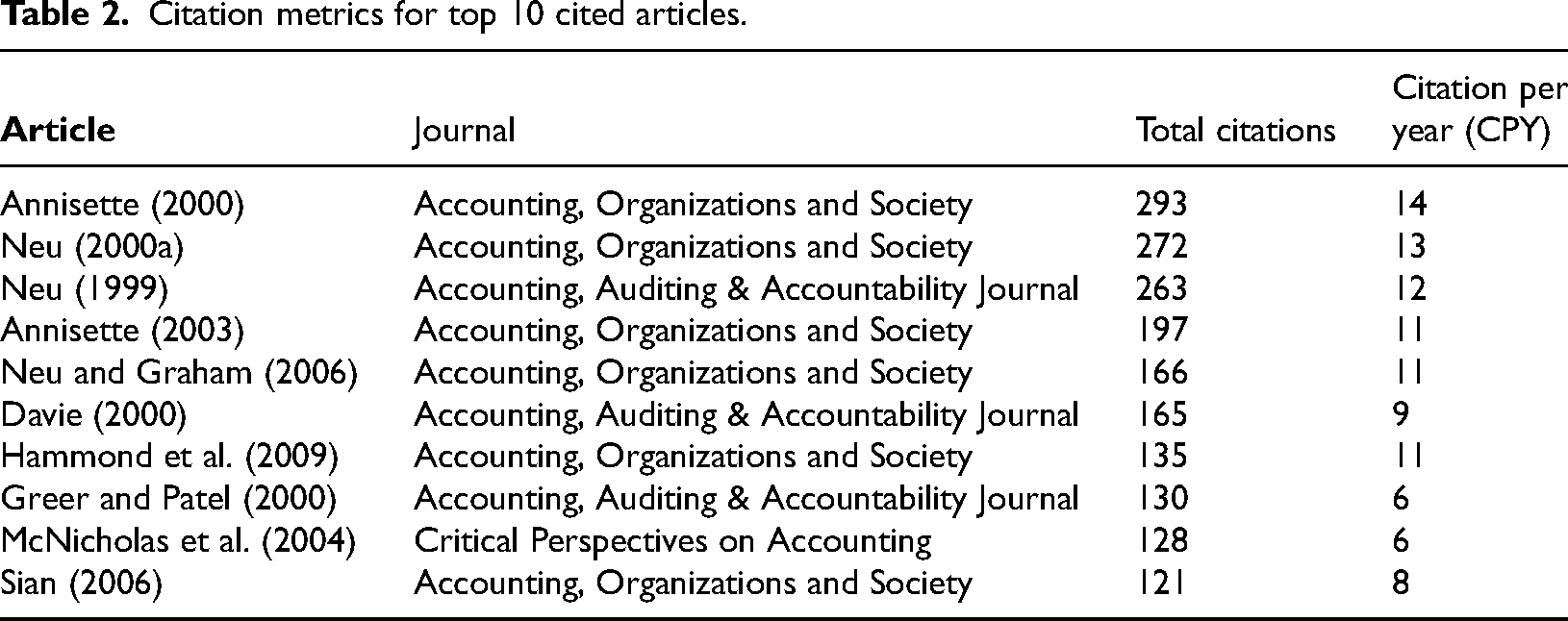

Citation metrics, including total citations and citations per year (CPY), allow researchers to understand how the literature has developed by examining the impact over time (Massaro et al., 2016). Several citation indexes can be used for this process including Thomson Reuters, Scopus, Web of Science, or Google Scholar (Dumay, 2014). This article, in line with others including Ascani et al. (2021) and Cuozzo et al. (2017), uses Google Scholar as it has a wider and more comprehensive coverage of publications and provides an easier comparison to results of other literature reviews (Dumay, 2014). Table 2 shows the citation metrics of the top 10 cited articles. The CPY is derived by dividing the number of years between the publication year and 2021 by the total citations (Ascani et al., 2021).

Citation metrics for top 10 cited articles.

Authors

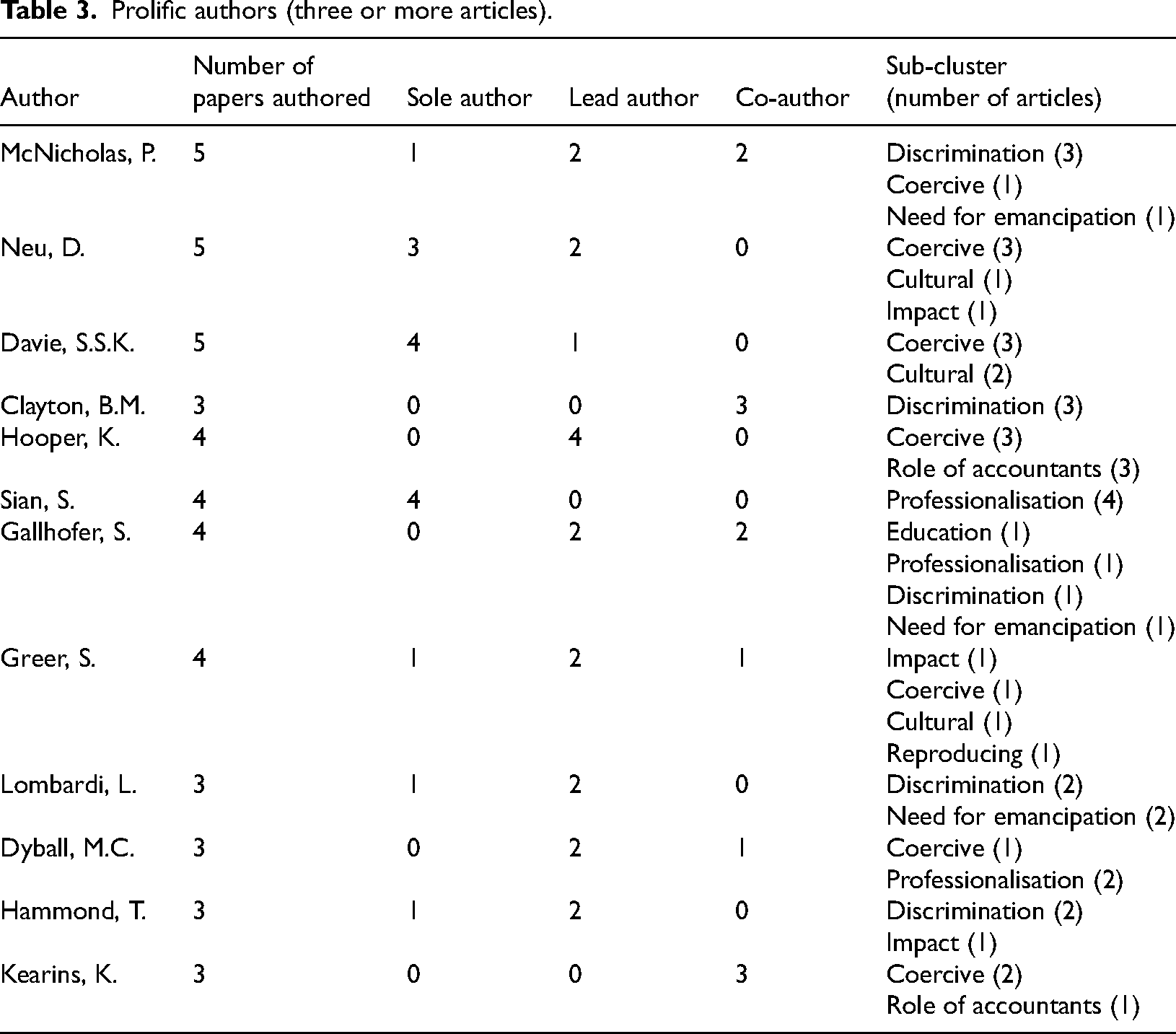

Thirty-eight per cent of the articles were sole authored, 38 per cent had two co-authors, 16 per cent had three co-authors, four per cent had four co-authors and three per cent had five co-authors. Of the 25 prolific authors publishing three or more articles, 10 authors published articles in the same sub-cluster, four authors published articles in the same cluster but in different sub-clusters, 10 authors published articles in two of the clusters, and one author published in all three clusters. Table 3 shows this for prolific authors publishing more than three articles. There were seven author teams publishing two to three articles each. This shows a limited number of researchers are actively engaged with examining the effects of accounting on indigenous people.

Prolific authors (three or more articles).

The article authorship and citations do not appear to be equally distributed. Six of the prolific authors in Table 3 also have an article in the top 10 most cited articles shown in Table 2. The presence of dominant authors in this research field indicates that the ideas and findings of a few scholars may be influencing the research agenda (Cuozzo et al., 2017; Serenko and Dumay, 2015).

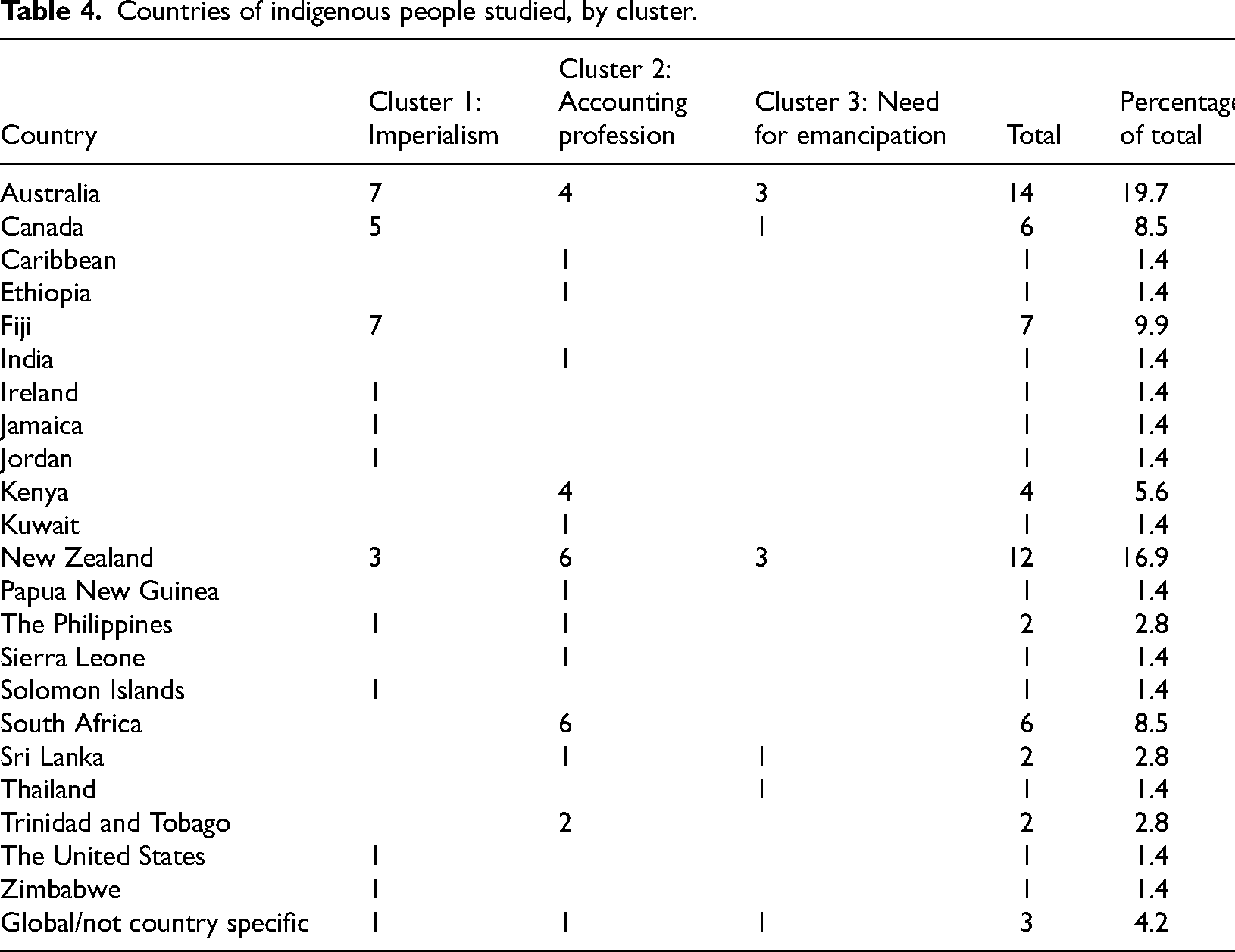

Countries

A wide range of indigenous peoples from various countries are included in the articles reviewed as shown in Table 4. The dominant countries are Australia (19.7%) and Aotearoa New Zealand (16.9%). As a continent, Africa is dominated by South Africa (43% of the articles), while the Pacific Islands are dominated by Fiji (70% of the articles).

Countries of indigenous people studied, by cluster.

Publication timeframe

As noted in the method section above, no specific timeframe was set for the inclusion criteria. The search criteria led to identification of articles published from 1995 onwards. This timeframe aligns with Buhr (2011) who notes that the literature on accounting and indigenous people is less than two decades old. Thirty-eight articles (53.5%) were published between 2000 and 2009, and 26 articles (36.6%) were published between 2010 and 2019.

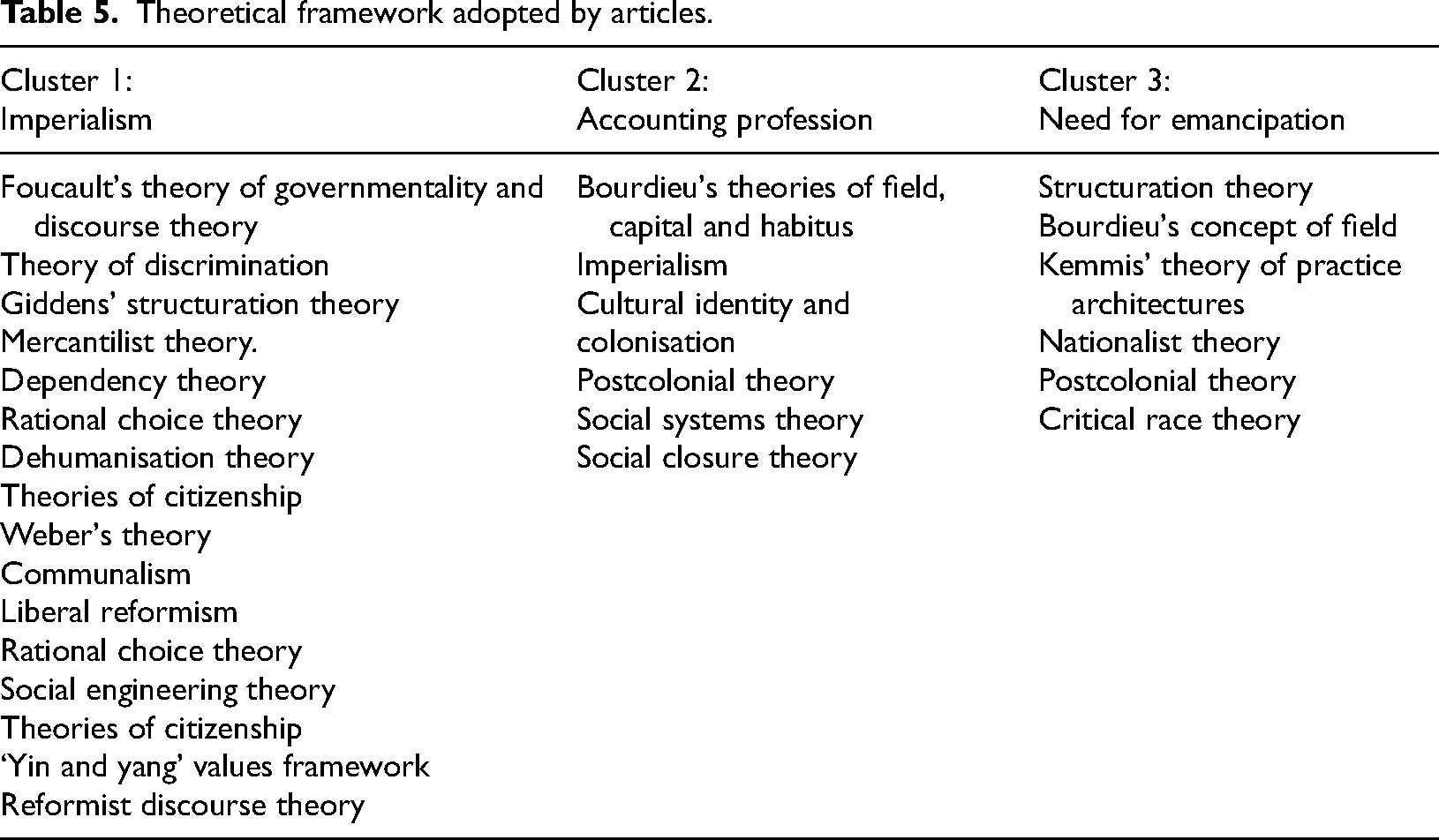

Theoretical framework

The different theoretical frameworks adopted by the articles are shown in Table 5. Many of the articles adopted either a colonialism, imperialism, or a Foucauldian perspective. As Neu (2000b) suggests Foucault's concept of governmentality is used not as an overarching theory but as a ‘field of investigation’ to situate techniques of government within the colonial context under consideration. Theories of institutionalised patterns of discrimination are used to tell a story about how accounting becomes part of discourse orientations that are deeply rooted in notions of racial identity and differentiation (Neu and Graham, 2004). However, these perspectives have been questioned. For example, Davie (2000) challenges the theory of imperialism due to its Eurocentric focus, and Gibson (2000) challenges the value-neutral paradigm in positive accounting theory.

Theoretical framework adopted by articles.

Methods employed by the articles

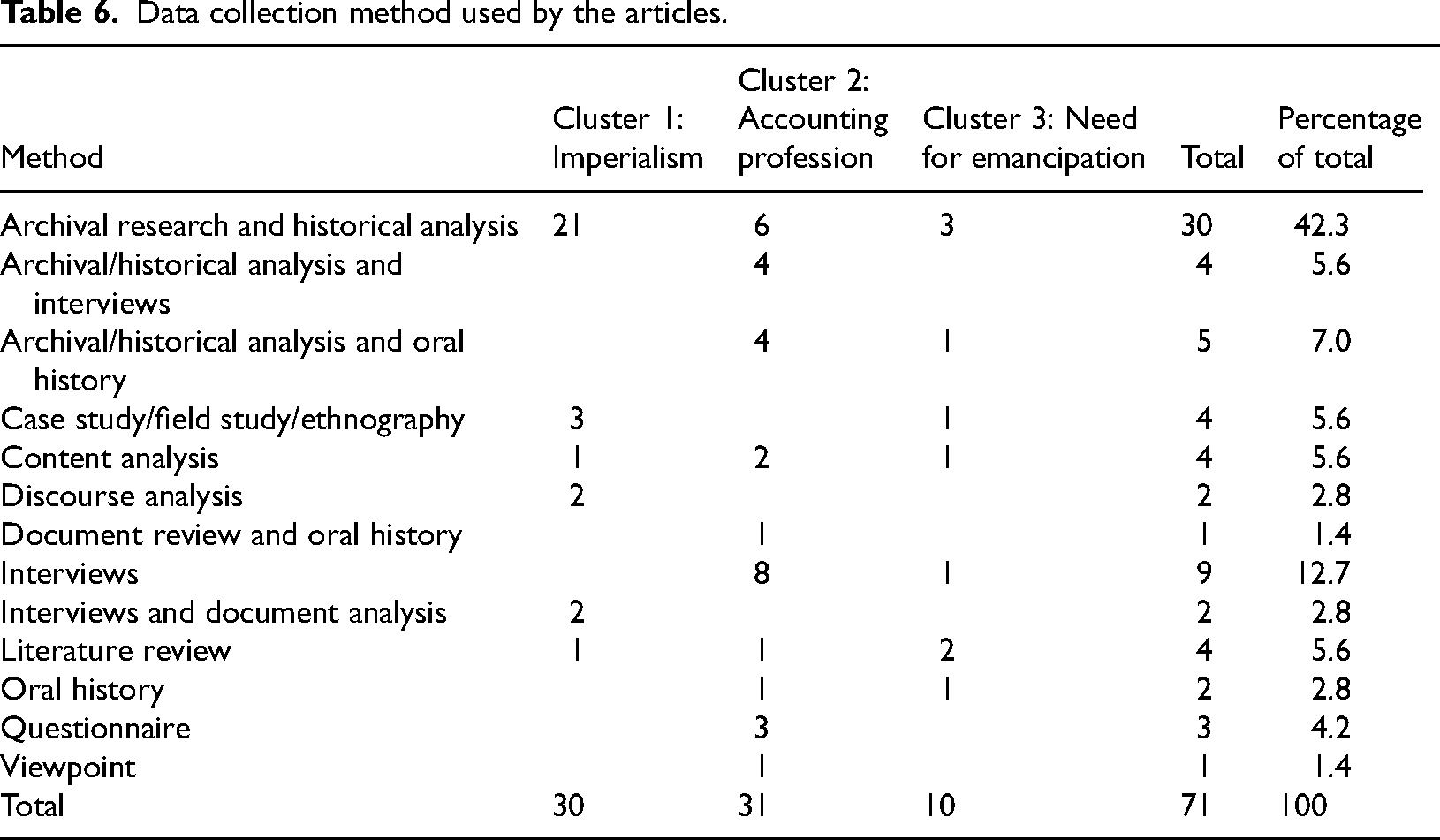

The research method adopted is shown in Table 6. Not all articles explicitly stated the method employed, particularly those using an archival research or historical analysis. The most common method across all articles and for articles in Clusters 1 and 3 was ‘archival research/historical analyses. ‘Interviews’ were the most common method for articles in Cluster 2.

Data collection method used by the articles.

Findings of the reviewed articles

The 71 reviewed articles focus on issues associated with the colonisation of indigenous peoples that were affected by accounting practices and systems, the accounting profession and/or accountants. These issues include the role of accounting in different forms of imperialism (30 articles in Cluster 1), the role of accounting education, accountants and the accounting profession in the discrimination of indigenous peoples (31 articles in Cluster 2), and the need for emancipation of indigenous peoples (10 articles in Cluster 3).

Cluster 1: Imperialism

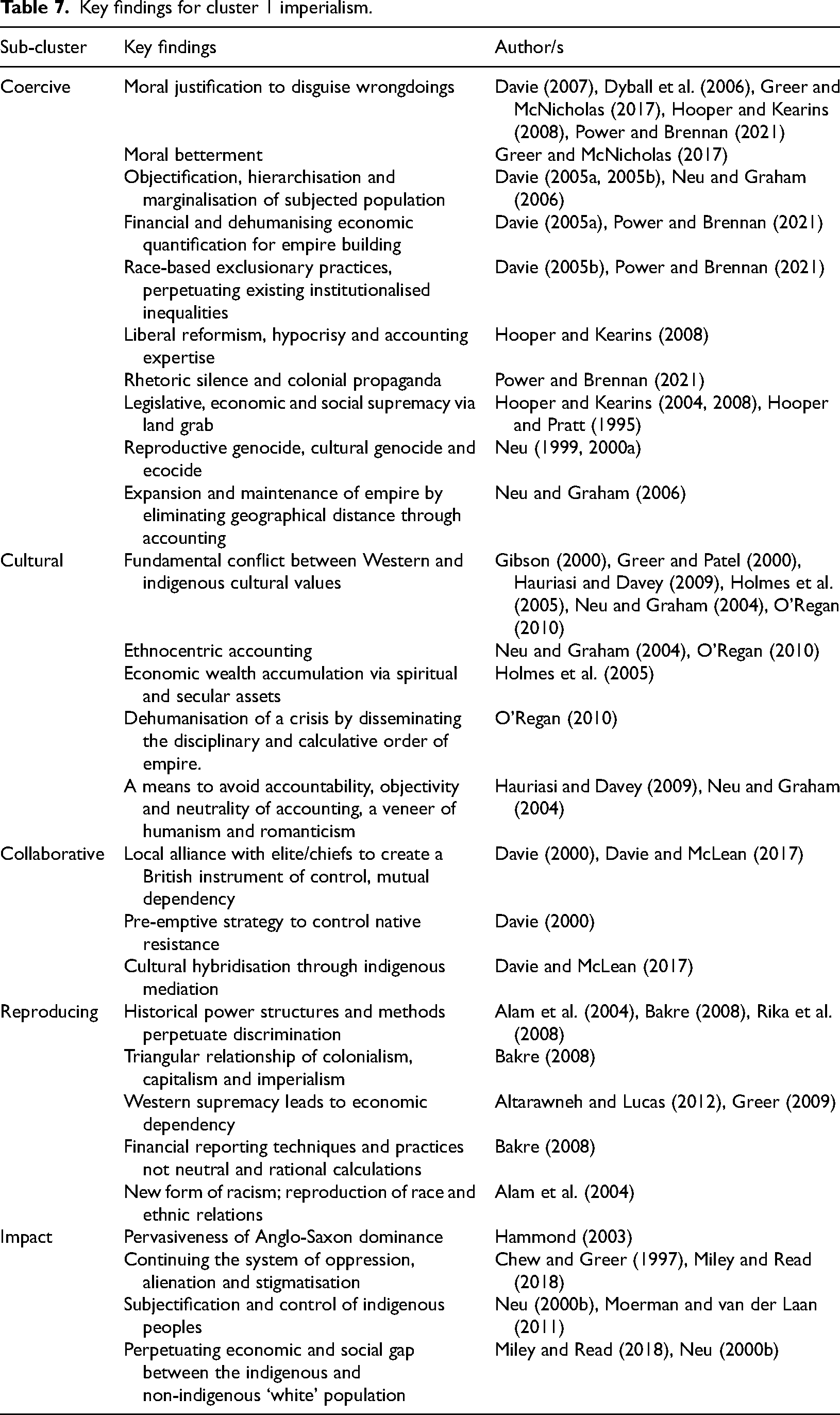

The principal theme of this cluster is to examine how accounting was used by the colonial rulers as a tool to govern the newly acquired territories. As noted earlier, accounting practices corroborated with a suite of government technologies in establishing the empire. It enabled imperialist power and control while disabling indigenous agency, voice and ownership of their own resources. The act of translating colonial government policies into practice was accomplished in myriad ways; the 30 articles in the five sub-clusters below explain these in detail. Table 7 presents the key findings in this cluster.

Key findings for cluster 1 imperialism.

Sub-cluster 1: Coercive imperialism

As the colonial rulers tried to establish their authority in the colonies and expand the empire, force was necessary as (naturally) there was resistance from the indigenous peoples. Accounting frameworks facilitated cost effective means to transfer resources into imperialist ownership resulting in a shift of control of indigenous peoples’ economic and social behaviours.

The 12 articles in this sub-cluster cover Australia (Greer and McNicholas 2017), Fiji (Davie, 2005a, 2005b, 2007), Aotearoa New Zealand (Hooper and Kearins, 2004, 2008; Hooper and Pratt, 1995), Zimbabwe (Power and Brennan, 2021), Canada (Neu, 1999, 2000a; Neu and Graham, 2006) and the Philippines (Dyball et al., 2006).

Greer and McNicholas (2017) examine how accounting helped to organise and administer programmes for the indenture of Aboriginal children in New South Wales, Australia. Specifically, the analysis illustrates how accounting made possible the removal of children from the Aboriginal communities to institutions of training and places of forced indenture under government-negotiated labour contracts. They conclude that, in keeping with a pastoral focus, the usage of the accounting information was framed vis-à-vis the notions of moral betterment.

Davie (2005a, 2005b, 2007) primarily examines the colonial functions of accounting in British-ruled Fiji, and claims that accounting and imperialism were mutually constitutive for empire building as accounting opened new possibilities through which relations of power and exploitation could be justified and perpetuated. Davie (2005a) analyses how financial economic quantification using accounting concepts and analysis has always been an essential and integral part of effective policies and activities for Britain's empire building, highlighting the ways in which accounting helped translate imperial forms of oppression and injustice into everyday work practice. Davie (2005b) criticises the ways in which accounting's calculative interrelationships and explanations promoted race-based exclusionary practices. The article highlights accounting's enrolment in processes of preferencing that assume hegemonic and exclusive strategies based on pre-existing patterns of chiefly power. Davie (2007) further shows how accounting calculations were indiscernible from exploitative and oppressive acts of organising indigenous labour for colonial purposes, concluding that accounting is not in itself racist but can become racist through the context in which it is practised.

Hooper co-authored three articles; Hooper and Pratt (1995) and Hooper and Kearins (2004, 2008) focusing on the grabbing of land in Aotearoa New Zealand and examining how accounting helped British rulers to establish legislative, economic and social supremacy over the Māori. Hooper and Pratt (1995) investigate the conflict between the European directors and Māori shareholders of the New Zealand Native Land Company from 1882 to 1890. They argue that accounting techniques made lies look like truths, or ‘deeds of charity’ which persuaded Māori to exchange their land for shares – contemporary media reports described the exchange as ‘philanthropy’ (Hooper and Pratt, 1995: 11). Augmenting the theme of the land grab, Hooper and Kearins (2004, 2008) show how the British Empire benefitted from large capital gains from on-selling the land bought cheaply from Māori beginning in 1860 to the end of 1870. This was done mainly via oppressive forms of wealth taxation which in turn disadvantaged the Māori by expropriating the most valuable asset in their possession – land. Further focusing on the period 1885–1911 in New Zealand, Hooper and Kearins (2008) link liberal reformism, hypocrisy and accounting expertise as key elements in a potent formula contributing to Māori losing much of their remaining land, with ownership decreasing from 30 per cent of New Zealand's land area in 1890 to just seven per cent 30 years later. They compare the British rulers to Lewis Carroll's greedy and hypocritical Walrus and Māori as the unfortunate victims whose land was gradually ‘swallowed’ – and whose wellbeing suffered immensely. They conclude that the tendency of accounting is to serve its masters, by distributing assets in favour of the rulers.

In analysing annual report narratives of the British South Africa Company in Zimbabwe over a 35-year period, Power and Brennan (2021) argue that accounting was used to promulgate colonial propaganda and mask exploitation of the colony's native population for its distant London audience. By treating the ‘native mind’ as not a human mind (Power and Brennan, 2021: 2), an imperial discourse justified white supremacy over indigenous peoples on the grounds of a higher civilisation. The authors examine the role of accounting in dehumanising human beings through quantification, rhetoric silence and in perpetuating racial discriminatory practices.

Examining the status of First Nation's people in Canada, Neu (1999) asserts that accounting techniques were central to the military machinery of empire and British Imperialism. Neu (2000a) advances his argument by documenting the way accounting techniques were implicated in the consequent reproductive and cultural genocide, and ecocide. Governing remote colonies was a big challenge to the colonisers, not only geographic distance, but cultural, conceptual and political relations were enacted and extended through administrative accounting procedures. Neu and Graham (2006) further investigate how the federal government used accounting to manage existing political territory, and also to acquire new geographical territory, and convert it into politically governable space by eliminating the effective distances involved. The British Empire used accounting to construct a certain image of distant domains. The authors conclude that accounting technologies acted not only as a carrier of new practices but helped transfer these practices from the centre to peripheral sites.

Dyball et al.'s (2006) article investigates Filipinos (with three centuries of Spanish colonial experience) dealing with a new coloniser, the United States. The analysis examines a formative period (1898–1924) of the US occupation of the Philippines. They explore how accounting can also be enrolled in processes of civil disobedience and passive resistance by the colonised, expressed through the ‘not’ doing of accounting (Dyball et al., 2006: 48). However, this was conveniently regarded by Americans as a ‘failure’ of the Filipinos to do ‘good governance’ and counted as evidence that they were not yet ready to govern themselves, resulting in the United States continuing its rule until 1946.

Sub-cluster 2: Cultural imperialism

This sub-cluster highlights the tension between dominant Western accounting concepts and indigenous values and its impact on indigenous peoples. The six articles in this sub-cluster are set in Australia (Gibson, 2000; Greer and Patel, 2000), Ireland (O’Regan, 2010), the Solomon Islands (Hauriasi and Davey, 2009), Canada (Neu and Graham, 2004) and the United States (Holmes et al., 2005).

The articles critically examine indigenous and colonial cultural differences and the impact of dominance of Western concepts of accounting on the indigenous peoples. O’Regan (2010: 416) argues that the ethnocentric colonisers tried to enforce their ideas with an aim to improve the ‘moral habits’ of the native Irish in relation to work. Accounting laid the basis for interventions by the imperial power intended to ‘civilise’ the native Gaelic population as well as recalcitrant Anglo-Irish landlords. By implementing a range of intrusive controls and reducing a human catastrophe to a series of numbers and reports, accountants actively dehumanised a crisis, while simultaneously disseminating the disciplinary and calculative order of empire. O’Regan (2010: 428) concludes that the ‘dense mass of petty accountability’ that characterised this edifice was intended to control costs and to limit the access of native labourers to relief.

Gibson (2000) argues that Australia's Aboriginals viewed themselves as custodians, not owners of the land. For them, the need for food, shelter, social contact and spiritual enrichment are all provided by the land. However, in contrast, land ownership, physical shelters, and personal possessions are the very basis of Western societies which accounting espouses. Using a yin-yang approach, Greer and Patel (2000) maintain that indigenous values (yin-based), which encompass sharing, relationships, kinship, cooperation, coexistence and egalitarianism, are in marked contrast to the mainstream Western yang-based values of accounting and accountability systems which focus on individualism, achievement and independence. Similarly, Hauriasi and Davey (2009) elucidate the objectivity and neutrality of accounting, profit and wealth maximisation as the bottom-line, and the underlying basis of competition for efficiency and effectiveness which stands in contrast with indigenous peoples’ values.

Neu and Graham (2004) present accounting techniques as a set of practices, situated within bureaucratic systems that permit the exercise of government, and help bureaucrats create a veneer of humanism and romanticism that largely strip indigenous peoples of their agency and centralise the control of their lives. They conclude that actions are not clearly immoral or unethical – morals or ethics simply do not logically or structurally enter the equation.

Religion was an effective enabler for colonial rulers to establish and expand their territories. 4 However, in this review there is only one article centred on religion and how accounting extracted power from the indigenous peoples and led them to exchange their native beliefs for Western values (Holmes et al., 2005). Holmes et al. (2005) argue that a complex of accounting measures – account books, inventories of accumulated wealth, and detailed instructions for production performance – were used to inculcate Western values ultimately causing the Coahuiltecan Indians to abandon their native beliefs. Spiritual assets (number of natives baptised) and secular assets (physical structures, agricultural products and livestock accumulated) reflected the importance placed by Western societies on economic wealth accumulation and disregard for native culture. The authors conclude that as a result, 150 Coahuiltecan tribes ceased to exist as a distinct culture by the early nineteenth century.

Sub-cluster 3: Collaborative imperialism

The two articles in this sub-cluster examine how accounting was used as a tool for imperialism by collaborating with the pre-existing power structures, discussing how the colonisers cemented their base in their remote colonies. When the European settlers arrived in these remote colonies, they soon realised that wielding power from a distance was daunting, mainly due to the unequal number of indigenous peoples and colonisers. 5 Thus, their minority position was a driving force for co-opting the local elite or chiefs to exercise control over the indigenous peoples.

Davie (2000) critically examines how accounting enabled a collaborative system of imperialism in Fiji. Indigenous resistance was managed using the Fijian elitist structure as a British instrument of control. Through accounting collaboration, the chiefs could enjoy a ‘special immunity’, and the British could exploit human and natural resources for empire building (Davie, 2000: 349). This win-win-lose strategy was advantageous to the settlers and local elite while marginalising the indigenous peoples and was an effective pre-emptive strategy to control native resistance. Davie and McLean (2017) discuss how cultural hybridisation and local alliances led to marginalisation of the indigenous peoples, while empowering indigenous salaried chiefs to become despotic and predatory rulers. They conclude that mutual dependency between local traditional authority and colonial administrators facilitated the global imperial order.

Sub-cluster 4: Reproducing imperialism

This sub-cluster examines how accounting and control systems were replicated in the post-colonial era as newly independent nations found themselves still dependent on former rulers/systems. This builds on the previous sub-cluster as accounting systems and historical alliances between indigenous chiefs/elites and colonial rulers are replicated in the post-independence era. The face of the ruler changed but not the methods nor discrimination.

The five articles in this sub-cluster are set in former British colonies 6 – Jordan (Altarawneh and Lucas, 2012), Jamaica (Bakre, 2008), Fiji (Alam et al., 2004; Rika et al., 2008) and Australia (Greer, 2009). The researchers argue that independence from the British Empire did not result in equality and justice to all the indigenous peoples irrespective of whether, at the time of independence, they were a majority (Jordan, Jamaica and Fiji) or a minority (Australia). Accounting systems perpetuated and hinder overall development.

Altarawneh and Lucas (2012) argue that despite having established one of the earliest Islamic banks, Jordan was forced to follow a Western accounting system to serve the interest of external (Western) parties and that was inconsistent with the values and principles of Islam. This indirectly reproduces imperialism as Jordan's economic and accounting policy has to meet the demands and priorities of the agencies of Western developed nations. A possible reason is the pressure to follow normative processes using International Financial Reporting Standards to help gain investors’ confidence. The authors conclude that this reflects the economic dependency of developing countries on former Western colonial powers. Similarly, Bakre (2008) challenges the notion that financial reporting techniques and practices are neutral and rational calculations. The advent of independence does not necessarily mean that financial control methods are withdrawn with formal decolonisation. There is pressure to entrench even more than what already exists to fit the requirements of international mobility of capital. Bakre (2008) concludes that the continued use of accounting technologies dictated and enforced by Western economic powers, with the aid of the local elite is implicated in the recent corporate failures in Jamaica, leading to the triangular relationship of colonialism, capitalism and imperialism.

Alam et al. (2004) discuss how the historically constituted social structures through collaboration between British colonial rulers and the indigenous chiefs continue in Fiji. The colonial administrative processes protect the indigenous people, but it has given rise to a new form of racism against the indented Indian labourers brought by the British. Using a case study of the Fiji Development Bank the authors conclude that its management accounting controls contribute to the reproduction or reconstitution of race and ethnic relations hindering social and economic development. Similarly, Rika et al. (2008) examine the efficacy of the Fijian Administration established by the British rulers for controlling indigenous Fijians. Long after independence in 1970, the system continues to be used for the purpose of control. Indigenous Fijians are held accountable for their contributions and penalised for shortfalls with no corresponding accountability for the administration.

Greer (2009) examines how accounting practices manipulated the income and spending of Aboriginal women between 1928 and the 1960s. The focus is on how accounting practices helped extend political dominion over indigenous women through interventions. Greer (2009) argues that accounting disabled Aboriginal economic dependency and engendered dependency on government, concluding that accounting thus played a part in social engineering of indigenous peoples even after colonial rule ended.

Sub-cluster 5: Impact of imperialism

The four sub-clusters discussed above lead to the final sub-cluster, the on-going impact of imperialism. The five articles in this sub-cluster are set in Australia (Chew and Greer, 1997; Miley and Read, 2018; Moerman and Van Der Laan, 2011), Canada (Neu, 2000b) and a global perspective by Hammond (2003).

Chew and Greer (1997) investigate the enforcement of a Western form of accountability on the Australian Aboriginal and Torres Strait Islander (ATSI) peoples. They argue that although the ATSI Commission was set up in 1990 for the wellbeing of the ATSI peoples, it has continued the system of oppression and alienation, and that accounting is implicated in this process. Miley and Read (2018) examine the relationship between accounting and stigma. The failure of accounting mechanisms, by intensifying indigenous poverty, contributed to the economic and social gap between the indigenous and non-indigenous ‘white’ population. The visible signs of this gap, occasioned by indigenous poverty, reinforced that the indigenous population was the other in a society where non-indigenous interests determined power structures. Both authors conclude on a hopeful note that the presence of accounting mechanisms cannot eradicate the past, nor fix the present, but can create an environment where financial abuse does not occur. This is particularly important as society cannot be deemed to be functioning to its full potential if some parts of it are oppressed.

In a case study of Baryulgil, a mining site in Australia, Moerman and Van Der Laan (2011) investigate the broader institutional accountability that arises from paternalistic attitudes. They demonstrate how accounting was used to avoid accountability towards the native population and played a role in its subjugation. It exposes colonial exploitation of indigenous labour, highlighting the role of accounting in facilitating corporate profit-making, often at the expense of human rights.

Neu (2000b) analyses the present-day crisis by examining a historical period (1830–1860) in colonial Canada. He claims that the issue of land ownership has not disappeared; First Nation's peoples continue to struggle against unilateral decisions made by the federal government regarding the amount of annuity payments to be received for lands previously ceded. Neu concludes that accounting discourses and techniques played a significant role in the subjectification and control of indigenous peoples which continues today.

Using a global perspective, Hammond (2003: 15) investigates the impact of accounting on groups oppressed due to their race, gender and class to demonstrate the past ‘pervasiveness of Anglo-Saxon dominance’. Hammond (2003) asserts that accounting was used explicitly to define and construct issues that affected marginalised groups and kept them on the far margins of the profession. She cautions that conducting research is not enough to ameliorate this and advises that studies of accounting's past should be used to effect change in the future.

Summary of Cluster 1: Imperialism

Collectively, the 30 articles in this cluster outline the critical role of accounting practices in helping colonial rulers marginalise indigenous peoples around the world. The evidence presented above develops further understanding of accounting's uses in complex and dynamic social, cultural, economic and political processes. Accounting provided a very practical way of measuring, monitoring and expressing in economic terms the governance of colonial rule. This partly facilitated legislative, economic and social supremacy by the end of the nineteenth century. Accounting practices and traditions were utilised without any serious consideration of the actual circumstances and needs of the indigenous peoples; needs of the empire were paramount. An essential resource – land – was manipulated for establishing and expanding the empire, resulting in gains to colonial rulers and allies, and losses to indigenous peoples. By threatening the core indigenous values, accounting nullified what was of value to the indigenous. Thus, the different forms of imperialism led to continued oppression and marginalisation of indigenous peoples in many former colonies.

Cluster 2: Accounting profession

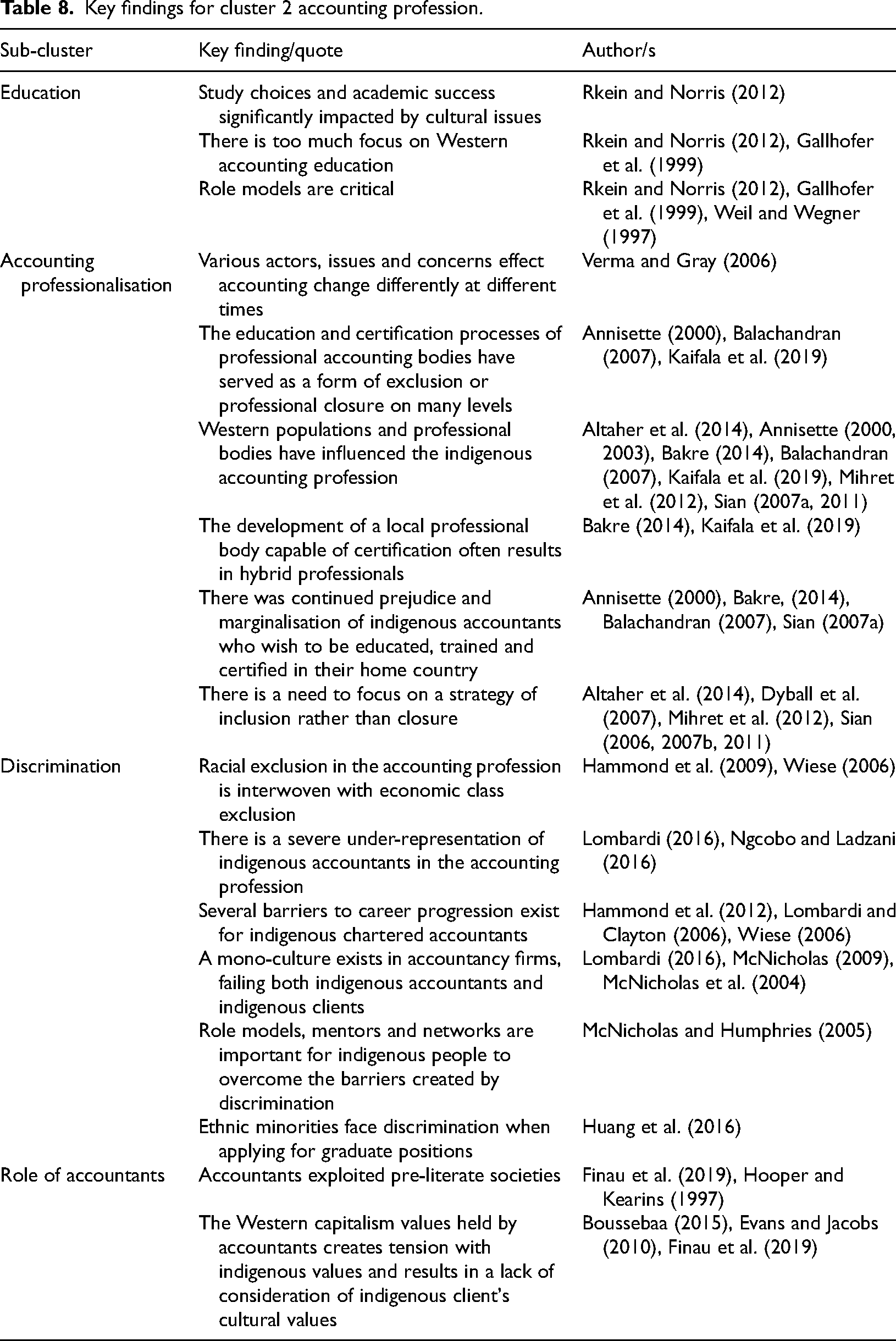

Acting in the public interest is a distinguishing ‘mark’ of the accountancy profession, and integrity and objectivity are fundamental principles for professional conduct (International Ethics Standard Board of Accountants, 2021), In this second cluster, there is evidence that these fundamental principles were not observed and the development of professional bodies created marginalisation and discrimination towards indigenous accountants through the dominance of British qualified accountants in indigenous communities. There is a total of 31 articles across four sub-clusters that focus on the under-representation of indigenous peoples in accounting education and ultimately the accounting profession, the development of professional accounting bodies and the resulting professional closure that exists, the barriers indigenous accountants face due to discrimination – perceived or visual, and the role of accountants and accounting in emancipation. The key findings from the articles are summarised in Table 8 below.

Key findings for cluster 2 accounting profession.

Sub-cluster 1: Education

The three articles in the sub-cluster of education cover a 15-year time period from 1997 to 2012 and discuss the under-representation in educational settings of the indigenous population of Australia (Rkein and Norris, 2012), Aotearoa New Zealand (Gallhofer et al., 1999) and South Africa (Weil and Wegner, 1997). High school accounting education (Rkein and Norris, 2012), university accounting education (Gallhofer et al., 1999) and educational issues and academic support structures for entering the profession (Weil and Wegner, 1997) are explored.

The articles highlight ‘that diverse cultural issues have significant impact’ (Rkein and Norris, 2012: 95) on both students’ study choices and their academic success. Numerous cultural factors need to be considered and addressed to increase the number of indigenous peoples studying accounting and entering the accounting profession. The ‘hidden curriculum in Western accounting education’ (Rkein and Norris, 2012: 105) is one of the contributors to the under-representation of indigenous peoples. The focus of accounting education on Western accounting practices and principles is a form of ‘insensitive cultural imperialism’ (Gallhofer et al., 1999: 774) and they argue there is a critical need to change accounting education to be more reflective of culture, rather than expecting the reverse to occur. The cultural differences between indigenous and Western populations (discussed in Cluster 1, Sub-cluster 2: Cultural imperialism) include the concept of value or currency, the usefulness of accounting knowledge and skills to the indigenous community (Rkein and Norris, 2012), the approach to learning in the indigenous population, and the importance of family (Gallhofer et al., 1999; Rkein and Norris, 2012). The presence of role models to motivate indigenous students to undertake accounting education and succeed is identified as critical (Gallhofer et al., 1999; Rkein and Norris, 2012; Weil and Wegner, 1997). As well as the cultural differences, cognitive factors (Weil and Wegner, 1997) and socioeconomic influences (Rkein and Norris, 2012) are also identified as important.

Sub-cluster 2: Accounting professionalisation

The process of professionalisation has been explored through one or more perspectives – functionalist, interactionist and/or critical (Mihret et al., 2012). These perspectives have been applied to accounting professionalisation and the examination of the development of the accounting profession in different settings. The education and certification processes of professional accounting bodies have served as a form of exclusion or professional closure, as well as controlling the knowledge base (Annisette, 2000).

The 13 articles in this sub-cluster highlight the various actors, issues and concerns that effect accounting change (Verma and Gray, 2006), and how this change has resulted in accounting professionalisation. The development of professional accounting bodies in Kenya (Sian, 2006, 2007a, 2007b, 2011), Trinidad and Tobago (Annisette, 2000, 2003), India (Verma and Gray, 2006), Ethiopia (Mihret et al., 2012), Sri Lanka (Balachandran, 2007), Kuwait (Altaher et al., 2014), Sierra Leone (Kaifala et al., 2019), the Philippines (Dyball et al., 2007) and the Caribbean (Bakre, 2014) are explored. Different forms of racial exclusion or limited participation exist, which are sometimes interwoven with economic class exclusion (Annisette, 2003).

Accounting professionalisation follows a set of distinct phases or stages specific to the context and these are influenced by the socio-economic and political environments in place at the time. Balachandran (2007) argues that the questionable relevance of British principles and systems to the British economy highlights how inappropriate they are for different contexts. Hence, the complex nature of establishing indigenous professional accounting bodies in a developing country has been found to be plagued with issues of exclusion and professional closure often affected by a lack of legislation and statutory power, as well as the influence of Western populations and legacies of imperialism (Annisette, 2000; Balachandran, 2007). Western influence has occurred through imported accounting expertise – often as a result of a lack of indigenous accountants at the time (Altaher et al., 2014; Mihret et al., 2012), British expatriate accountants dominating membership (Annisette, 2003; Sian, 2007a, 2011), Western educated indigenous accountants returning home (Balachandran, 2007), the presence of international accounting firms in the local region (Bakre, 2014), and Western professional bodies either operating in the developing country (Balachandran, 2007) or providing qualifications for professional accountants that work in the developing country (Annisette, 2000). This intermeshing of Western and indigenous peoples also extends to indigenous professional accounting bodies using a Western accounting education and/or examination process (e.g. that of the UK-based Association of Chartered Certified Accountants [ACCA]) as their own process (Annisette, 2000; Bakre, 2014; Kaifala et al., 2019). However, in India ‘British qualifications were not adopted, and ACCA qualifications were not recognized’ (Verma and Gray, 2006: 152).

As can be seen, exclusion can occur on many levels. The development of a local professional body capable of certification has been continuously threatened by several forces (Bakre, 2014). In the case of Kaifala et al. (2019: 2116) who explore the perspective of the accounting professionals rather than the accounting profession, the result is ‘a postcolonial third space in which hybrid professional identities’ are constructed that intermesh ‘the global with the local’ (Kaifala et al., 2019: 2133). However, the result is often a continued prejudice (Sian, 2007a) and marginalisation of indigenous accountants who wish to be educated, trained and certified in their home country (Annisette, 2000; Bakre, 2014; Balachandran, 2007). Attempts to overcome discrimination by offering alternative pathways to the accounting profession contribute to discrimination and create a ‘fragmented profession’ (Annisette, 2003: 669).

Consequently, it is recommended, particularly in the initial stages of development, which professional accounting bodies focus on a strategy of inclusion rather than closure (Mihret et al., 2012). A critical example supporting this is Kenya, where strong political concerns reversed strategy and a colonial professional accounting body was forced to abandon professional closure in favour of openness (Sian, 2006, 2007b, 2011). Sian (2006, 2007b) found that this move to inclusion was the result of the Government acting ‘to meet demands for restitution for past discrimination against Africans’ (Sian, 2007b: 866). However, despite the inclusion, the indigenous population still experienced discrimination (discussed further in Sub-cluster 3) (Sian, 2007b). A reversal of the exclusion of indigenous people was also found in Kuwait by Altaher et al. (2014) where a lack of political intervention helped to preserve the Kuwaiti culture and exclude non-Kuwaitis as acting members of the accounting profession. Yet, the inclusion of indigenous people in the accounting profession in the Philippines did not have the precursors noted above and was not the result of reversal as in Kenya (Sian, 2006, 2007b, 2011) or Kuwait (Altaher et al., 2014). However, political interests were at play and combined with wholly Filipino legislature, ‘a form of native resistance’ led to the professionalisation of accounting in the Philippines for Filipinos (Dyball et al., 2007: 415).

Sub-cluster 3: Discrimination

Discrimination in the accounting profession is the dominant sub-cluster in Cluster 2, with 11 articles addressing discrimination of indigenous peoples through examining the existence of severe under-representation, barriers to advancing careers and social exclusion in the accounting profession in South Africa (|Hammond et al., 2009, 2012; Ngcobo and Ladzani, 2016; Sadler, 2002; Wiese, 2006), Aotearoa New Zealand (Huang et al., 2016; McNicholas, 2009; McNicholas and Humphries, 2005; McNicholas et al., 2004) and Australia (Lombardi, 2016; Lombardi and Clayton, 2006). The under-representation in the accounting profession of indigenous accountants means ‘there simply has not been enough of them to supply accounting services across a large number of Indigenous people and organizations’ (Lombardi, 2016: 1337). For example, in South Africa in 2014, only 7.84 per cent of registered chartered accountants were black (Ngcobo and Ladzani, 2016: 21). Most of the articles in this sub-cluster include first-hand accounts from members of the accounting profession of discrimination. Reports focus on sharing the lived experiences and capturing and preserving them before they are forgotten or rewritten by others.

Despite the indigenous peoples of South Africa being a majority population, the social closure 7 in South Africa has led to a strong interaction of economic class with professional closure such that financial and status barriers are often indistinguishable from cultural or race barriers (Hammond et al., 2009), and similarly, the perception different races have about each other is not always distinguishable from visible discrimination (Wiese, 2006: 164). Although there has been limited progress and transformation, Wiese (2006: 164) claims that the situation has ‘improved immensely’. Similarly, as highlighted by Hammond et al. (2012: 347), the US accounting profession has a more optimistic view of the transformation that has occurred than the black chartered accountants who faced ‘discrimination, poverty, rudeness, despair, solidarity, community, and unique challenges.’ Wiese (2006) found that black trainee accountants are satisfied with the level of training they receive, but they struggle to excel in their accounting careers due to lack of exposure, mistrust, lack of support, lack of business skills, cultural differences and language barriers. Similarly, Sadler (2002: 159) found several barriers to career progression exist for black chartered accountants including ‘discrimination in respect of job assignments, racial bias, a lack of black mentors and the resistance of the clients’. Using a different research perspective, Ngcobo and Ladzani (2016), in examining the capability of professional charters to support economic transformation in South Africa, found that the accountancy profession had set aggressive targets on employment equity and skills development compared with other sectors such as the financial and construction sectors.

Barriers to a successful accounting career also exist for the indigenous peoples of Australia, with Lombardi and Clayton (2006: 68) identifying ‘the school experience, the cost of education, natural ability with numbers, the image of the accountant, the lack of role models and support, the community pull and the relevance of accounting to Indigenous Australians’ as the key barriers. Māori have also experienced limited inclusion in the accounting profession, and, like other indigenous peoples and ethnic minorities, they face barriers to entry and career progression. Some of these educational barriers were highlighted in Sub-cluster 1, and others include the monocultural policies, systems and practices that continue to exist in accountancy firms, the continued impact of colonisation, and ‘institutional racism’ (McNicholas et al., 2004: 89). This creates difficulties for indigenous accountants wanting to contribute to their indigenous communities and organisations as the monoculture fails to accept the cultural needs of indigenous accountants as well as indigenous clients (Lombardi, 2016; McNicholas, 2009; McNicholas et al., 2004). Discrimination in the accounting profession in New Zealand is not just prevalent in the Māori population – as identified by Huang et al. (2016), other ethnic minorities also face discrimination when applying for graduate positions. Like the educational barriers identified earlier, McNicholas and Humphries (2005: 31) identified that role models, mentors, and associations can overcome the barriers created by discrimination, recommending the formation of ‘networks of Māori accountants’ as one solution.

Sub-cluster 4: Role of accountants

As well as the accounting profession, the four articles in this sub-cluster show that accountants themselves have played a role in imperialism and reproducing imperialism (Boussebaa, 2015). This is evidenced by exploitations of pre-literate societies which resulted in a redistribution of resources (Hooper and Kearins, 1997) and land dispossession during the colonial period (Finau et al., 2019). One contributing factor was the lack of professional regulation of accountants in colonial New Zealand and other countries, which acted as an impetus for accountants to exercise discretion and freedom on how best to apply accounting techniques to serve their elite clients (Hooper and Kearins, 1997). However, more concerning is the lack of a ‘need to satisfy a wider interest group’ (Hooper and Kearins, 1997: 270). In their unusual approach of analysing poetry, Evans and Jacobs (2010: 378) note accountants as ‘having lost their sense of self and soul’. The Western capitalist values that focus on a system of ’market transactions and formal agreements’ (Finau et al., 2019: 1559) and are held by professional services firms (Boussebaa, 2015) and accountants (Evans and Jacobs, 2010) create tension with the indigenous values. As alluded to in Sub-cluster 3, this monoculture results in a lack of consideration and understanding of the client's cultural values. In a display of exploitation and reproduction of dominance through collaboration with indigenous elites, accountants used accounting practices to design lease agreements that minimised royalty payments to the indigenous landowners in Papua New Guinea – exploiting indigenous customs and the lack of literacy of the indigenous peoples (Finau et al., 2019).

Summary of Cluster 2: Accounting profession

Through this cluster, the influence of Western accounting systems and practices on indigenous peoples is outlined as a form of ‘insensitive cultural imperialism’ (Gallhofer et al., 1999: 774) that has led to Western accountants exploiting and marginalising indigenous accountants. The dominance of Western thinking has resulted in accounting education and accounting systems and practices that are not fit for purpose for indigenous accountants or their indigenous clients or communities. While some steps have been undertaken to reverse professional closure, indigenous accountants remain severely under-represented, and more action needs to be undertaken to ensure accounting practices and systems, accountants and the accounting profession, develop an awareness and consciousness of indigenous cultural values that is reflected in their practices. There is a need for role models, mentors and networks for indigenous peoples to help them to overcome the many barriers that exist to a successful career in the accounting profession.

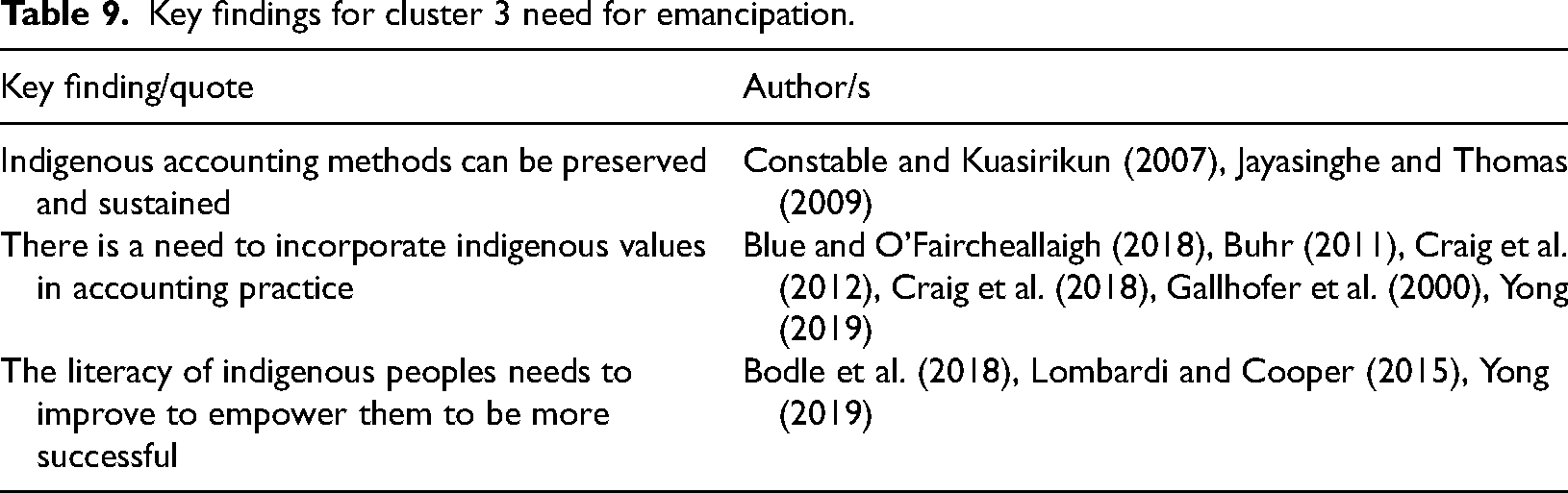

Cluster 3: Need for emancipation

Earlier discussions have highlighted the inadequacy of Western accounting practices and systems and the lack of inclusion of indigenous cultural values in accounting. Further, the effects on indigenous peoples of the exploitation of accounting practices and systems and accountants, and the under-representation of indigenous peoples and exclusion of cultural values in the accounting profession was discussed earlier. However, accounting can redeem some of its past and present injustices (Buhr, 2011) and the 10 articles in this cluster explore the need to focus on forward-looking solutions and how indigenous cultural values can contribute to a more enabling accounting and more effective reporting to all stakeholders (Bodle et al., 2018; Buhr, 2011; Craig et al., 2018; Gallhofer et al., 2000). As noted by Gallhofer et al. (2000: 382), there is a need ‘to learn from the cultures of indigenous peoples’, however Craig et al. (2018: 441) note that ‘whether, and if so how, indigenous values should be incorporated in accounting and accountability reports is under-explored’. The key findings from the articles in this cluster are summarised in Table 9 below.

Key findings for cluster 3 need for emancipation.

Important insights into how accounting contributes to ‘the construction of political and national identity’ are obtained from mid-nineteenth century Thailand, where ‘indigenous accounting methods and structures’ remained despite increasing foreign mercantile influence (Constable and Kuasirikun, 2007: 574). The culturally influenced Siamese accounts promoted an ‘elite sense of Siamese national unity’ (Constable and Kuasirikun, 2007: 592) through an awareness and consciousness of cultural practice and values (Constable and Kuasirikun, 2007). Jayasinghe and Thomas (2009) show how the preservation and sustenance of indigenous accounting systems can be explained by the strongly prevailing patronage political system mobilised in the subaltern village's social structure in Sri Lanka, making people unable or unwilling to change their behaviour and practice either individually or collectively.

Contrary to the current Western-influenced accounting that is prevalent in several countries, ‘accounting reflecting indigenous cultures would respect the particular values of different cultures as well as reflecting universal values’ (Gallhofer et al., 2000: 397). Noteworthy is that indigenous cultural values, ‘with their wider more holistic world view’ (Craig et al., 2012: 1041), embody many of the principles that have been included in environmental accounting, sustainability and integrated reporting (Craig et al., 2012; Craig et al., 2018). Thus, the development of different forms of reporting can better serve not only the indigenous peoples but also the environment and society (Bodle et al., 2018; Craig et al., 2018; Gallhofer et al., 2000). Consequently, indigenous cultural values should be drawn upon to inform the future of accounting and accountability (Craig et al., 2018) and provide ‘alternatives to orthodox Western thinking’ (Craig et al., 2012: 1042).

However, changing practices requires the voices of indigenous peoples to be amplified (Blue and O’Faircheallaigh, 2018). The latter requires ‘Indigenous autonomy’ through the inclusion of indigenous epistemologies and knowledge in financial education (Blue and O’Faircheallaigh, 2018: 40). Further, informed participation and decision making can be achieved by improving the literacy – financial and commercial – of indigenous peoples (Bodle et al., 2018). Cluster 2 discussed the changes needed in accounting education and Lombardi and Cooper (2015: 84) highlight that accounting can ‘play a positive part in building the financial capacity’ of indigenous peoples. Providing indigenous peoples with improved financial literacy and accounting skills contributes to ‘economic development and empowerment’ (Lombardi and Cooper, 2015: 84) and enables them to be able to play and master ‘the rules of the game’ (Lombardi and Cooper, 2015: 96).

Accounting also has a role to play in ensuring the success of indigenous businesses (Bodle et al., 2018; Yong, 2019), however more cultural sensitivity is required along with contextualised accounting services, as cultural values are often the barrier to long-term success especially in a Western environment (Yong, 2019). Bodle et al. (2018) discuss indigenous intangible assets and the need to include Elders in the valuing of such assets. Their proposed accountability model incorporates ‘cultural, social and environmental measures’ (Bodle et al., 2018: 35) and they claim that ‘a systematic transformation of accounting practices [is] part of the solution’ (Bodle et al., 2018: 36). Similarly, Craig et al. (2012) call for a rethinking of the concept of an asset to enable the Māori cultural view of taonga to be recognised. 8 Likewise, Buhr (2011: 152) notes the time has come to ‘pursue accounting “by” Indigenous peoples rather than accounting “for” Indigenous peoples’.

Summary of Cluster 3: Need for emancipation

The articles in this cluster have demonstrated a need to empower indigenous peoples through the inclusion of indigenous cultures and values in accounting practices, and through improving their financial and commercial literacy and financial capacity. A review of indigenous cultural values identifies a more holistic view than that of Western accounting. This should be considered to better serve not only the indigenous peoples but also the environment and society. There is a call for a rethinking of Western accounting practices and the inclusion of alternative, more holistic views.

Conclusions, limitations and future research

It is evident in this systematic literature review that the body of literature is slowly growing, however from a global point of view, indigenous people remain underrepresented in the accounting literature. The articles reviewed investigated issues related to a narrow focus on ‘indigenous peoples and accounting’ with an emphasis on oppressed ethnic groups within dominant cultures. Through a review of 71 articles on ‘indigenous peoples and accounting’ this article contributes to the existing body of literature in three distinct ways.

First, this review highlights the role of accounting as a tool of imperialism which operated in several ways – coercive, cultural, collaborative and reproducing imperialism. These practices have led to the continual impact of accounting on indigenous peoples in the post-colonial period. Accounting was used to improve the ‘moral habits’ of the indigenous peoples. Co-opting bureaucratic machinery, accounting dispossessed them of their most valuable tangible asset – land – and led to their subjugation, subjectification, marginalisation and disempowerment. It effectively inherited colonial systems and separated and reduced indigenous peoples from their own cultures and structures. Thus, accounting helped reinforce, reproduce and perpetuate colonial power.

Second, the dominance of imported Western accounting systems marginalised indigenous peoples in the accounting profession. For example, in Australia, a nation where 3.3 per cent of the population is indigenous only 0.02 per cent of accountants identify as such (Parkes, 2018); and in South Africa where the indigenous peoples are in majority (81%), the black Chartered Accountants remain underrepresented (about 16%) (South Africa Gateway, n.d.; South African Institute of Chartered Accountants, 2022). The main reasons identified are lack of education and opportunities, professional closure, lack of exposure, mistrust, lack of support and business skills, cultural differences, language barriers, institutional and racial bias, lack of role models and professional networks. As noted earlier, accountants played a major role by deploying accounting techniques to serve their clients, mainly colonial population and disadvantaging and disfavouring indigenous peoples.

Third, on an optimistic note, there is a growing awareness that there is an urgent need to change. The key measures are employment equity and skills development of indigenous peoples in the profession. Further, it is being recognised that accounting can better serve not only the indigenous peoples but also the environment and society. But this will need a new form of accounting, as the status quo will not work. Researchers and practitioners are increasingly recognising that it is imperative to contextualise and align accounting practices with indigenous cultures. Indigenous autonomy, voice and participation is vital for transforming the ethnocentric systems that have led to the devaluation of indigenous people.

All the articles reviewed here provide important insights into how accounting was an integral part of Imperial rule. In addition to being a technical practice, accounting was deeply embedded as a colonial practice. Supporting the conclusions of Lombardi and Cooper (2015: 87), our findings also ‘draw attention to the negative and detrimental impact that accounting has historically had on Indigenous peoples’. Thus, this review positions accounting not as a mere neutral, benign, technical practice with a narrow focus but as a racist and ethnocentric tool having a much wider impact on indigenous peoples and political agendas. Colonial attitudes have persisted into the ‘post-colonial’ era and represent one of the most serious obstacles to global economic development. It is important to study this in the twenty-first century as it has proven to have a continual effect on indigenous peoples. We concur with Carnegie et al. (2021) that accounting is more influential than many people may think, and it has a potential to create a better world consistent with a more balanced perspective on the planet, people and profit.

As with any research, a systematic literature review has its limitations. The scope of this study was limited to a review of ‘indigenous peoples and accounting’ and the findings are limited by the choices made during the search, exclusion, clustering and writing process used. All stages were conducted methodically and were documented, making it possible for them to be repeated. However, the processes involved a level of subjectivity that may result in differences when undertaken by others. Further, our search criteria involved specific databases, keywords, the article title and abstract, peer-reviewed journal articles, and publications in the English-language. This may have reduced the number of articles identified in the 1990s and earlier due to keywords not being used by all journals until later. Other publication outlets, languages and search criteria may have resulted in identifying further literature on indigenous peoples and accounting. For example, Sadler and Erasmus (2003, 2005) is relevant work that was not captured by the search criteria. Similarly, Greer and Neu's (2009) significant work on indigenous peoples and accounting was not considered for the current review as it is a book chapter, not a peer reviewed journal article.

History is thought-provoking, and like Hammond (2003: 20), our first response at seeing prolific literature in a narrow focus on ‘indigenous peoples and accounting’ was ‘pleasure’ and ‘hope’ that the growing body of literature will help achieve change and remedy the wrongdoings, giving voice and agency to the indigenous peoples globally. Efforts should be made by people with power – politicians, business communities, professional bodies, social scientists and researchers – to bring about a positive change. Specifically, future research can explore the impact accounting has had on indigenous peoples from a gender perspective. In addition, identifying the ethnicity of authors in this field and how indigenous authors can be supported would also be beneficial to progressing issues. There is also the potential for using field research to explore how accounting can be emancipatory for indigenous peoples.

Footnotes

Acknowledgements

We acknowledge the contribution of Priscilla Creppy in the initial stages of the project. The constructive feedback of the two anonymous reviewers has helped to improve the quality of this manuscript and we are thankful to them for their comments.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: We acknowledge the research assistant funding provided by Lincoln University, New Zealand.