Abstract

This article seeks to determine how much we understand of Pacioli's purpose, and to clarify what he wrote justifying his preparation and publication of his ‘bookkeeping treatise’ in 1494. The context that motivated Pacioli to prepare his treatise is identified: why he published it and for whom. A new critical translation of the first chapter is presented, revealing statements omitted from the translations, and terms misunderstood. Its primary contribution is the clearer overview of fifteenth century Venetian business and bookkeeping practice and of the treatise than is currently presented in the accounting history literature. This should lead to new understanding of the role and purpose of using double entry in European trade during the fourteenth and fifteenth centuries, and thereafter. Finally, all 10 translations of the treatise evaluated, including the five in English, were found to be unreliable. Anyone using these translations needs to refer continuously to the original text and to how it has been translated into other languages.

Introduction

In the accounting history literature, double entry's 1 role in the medieval marketplace is acknowledged, but never fully understood. Consequently, there is disbelief that double entry was superior to other methods used to record business transactions – see, for example, Yamey (1975). This is due, at least in part, to the vague and insubstantial manner in which the medieval marketplace and the organisation of medieval trade is covered in that literature, particularly the Venetian marketplace. While the economic history literature of the past 90 years provides a rich tapestry of those topics, seldom is it ever referred to or utilised by accounting historians. Even in the considerable body of literature on the link between double entry and capitalism, the inclusion in this debate of what is known about the medieval marketplace, the organisation of medieval trade, and the manner in which medieval merchants kept account, is superficial, if it is referred to at all. In all likelihood, as is evident in the literature, this is because accounting historians of medieval bookkeeping have seldom viewed anything as important other than the manner in which account books were kept and how much they resonated with modern practice (De Roover, 1956, 1958).

Another focal point in this literature is Pacioli's much discussed double entry bookkeeping treatise of 1494, De computis et scripturis (Concerning Bookkeeping and Records). A product of the commercial environment of late-fifteenth century Venice, it describes many of the issues a wholesale merchant had to address at that time, such as how to register account books, how to deal with transaction tax officials, how to place book values on items for which no cost was known, what records to maintain relating to voyages, and how to identify the amount to use when recording a barter transaction. It also describes several types of records that had to be kept, and how to keep them, over and above the records maintained of transactions in the books of account.

In keeping with the focus elsewhere, despite Pacioli's undoubted knowledge of medieval Venetian commercial practice, his treatise is not used as a source for discussion of double entry's role in the marketplace. Instead, discussion focuses on what it omits, on contradictions within in it, on how what it describes differs from bookkeeping practice in Tuscany, and on whether it was written, or simply compiled by Pacioli. As we shall show in this article, if scholars had, instead, studied and understood what Pacioli wrote when he justified its publication, double entry's role in the medieval marketplace might have been understood and its superiority over simpler bookkeeping methods acknowledged, rather than dismissed.

One reason this has not occurred is that the English language translations of the treatise do not indicate that there is anything significant in it that might contribute to this topic, other than that Pacioli believed that the merchants in Urbino had need of some instruction in double entry. As we shall show, not only is that assumption incorrect, 2 the translations are misleadingly incorrect, and incomplete. This is particularly so in Chapter 1, where Pacioli explains why he prepared his treatise and whom it is for. Thus, in the expectation that his motivation might be clearer were a new translation prepared, this article presents the first complete translation into English of Pacioli's introductory chapter. The findings will be presented later but, the finding of most importance to future scholars is that none of the current English language translations should be treated as reliable.

So pervasive is the impact of the misleading translations of Pacioli's treatise upon the accounting history literature that we could never list all those whose work has unwittingly embraced flawed understanding or interpretation. It would therefore be unfair, partial, and biased to provide citations to previous studies as examples of what we are criticising in this article, which is why we do not do so.

Next, in order to establish the context surrounding Pacioli's purpose in preparing his treatise, we review how accounting historians have addressed the environment, or context of the late-medieval marketplace in which double entry was used; how an eminent business historian, three economic historians, an eminent accounting scholar, and two accounting historians of the second half of the twentieth century have viewed the medieval accounting history literature; and how scholars of accounting history have assessed Pacioli's text. 3

What the accounting history literature tells us

Medieval bookkeepers often did queer things. Perhaps they had good reasons for doing what they did, but we no longer understand their practices because we have a different point of view and accounting has progressed since the Middle Ages. (De Roover, 1958: 42)

The accounting history of late-medieval Italy contains very little about the world surrounding the bookkeeping that is its focus. Giovanni Rossi (1896) and A. C. Littleton (1933) both discussed some contextual factors when they wrote about the catalysts that combined to facilitate the emergence of double entry, but did so in very little detail; and, what they wrote related to the twelfth century rather than the fourteenth and fifteenth centuries, which is the period from which the vast majority of the evidence of medieval bookkeeping practice has survived. For those centuries, it is the works of business historian, Raymond De Roover, that are principally used by accounting historians. Over four decades, he wrote extensively (e.g., 1937, 1946, 1953, 1956, 1963, 1974) about medieval bookkeeping, trade, bills of exchange, and business. His sources were the surviving account books and records of Tuscan firms, principally those of the Medici Bank (1397–1494). However, always more of a business historian than an accounting historian, de Roover did not study or write in any detail about how the context surrounding business impacted medieval bookkeeping practice. No other source has been significantly utilised by accounting historians to fill this gap. Thus, for example, focusing on Venice, anyone reading the accounting history literature will struggle to find any references to the works of specialists in the organisation of medieval Venetian trade – local and international, and its marketplaces, such as Frederic C. Lane, Gino Luzzatto, and Reinhold Mueller.

In sum, the accounting history literature tells us how Venetians kept account. It does not tell us about how the context surrounding business or business forms impacted bookkeeping and accounting practice. Why the Venetian bookkeepers did what they did has never been adequately explained, not even to the extent that it has been in regard to their counterparts in Tuscany. This can be seen in the one contextual factor recognised in this literature: because large Tuscan partnerships were established for relatively short periods, they calculated their profits so that they could be distributed among the partners. Arguably, this is the only exception to De Roover’s (1958) observation, quoted above, that accounting historians did not know any good reason for medieval bookkeepers doing what they did. 4

These characteristics of this literature have led to its being criticised for lacking any awareness of the problems of business (Lane, 1944); parochialism and bias (Antinori, 1959, 2003, 2004); being teleologically present-minded (Pilla, 1974); being teleological and descriptive rather than critical (Hopwood, 1987); ignoring the books of account and, instead, relying on Pacioli's treatise (Martinelli, 1974) while swirling around in a vacuum devoid of context (Goldthwaite, 2018). All those scholars were criticising the body of literature that they had read. All of them write as if it is the entire body of that literature, not some of it, nor a lot of it but, all of it. This lack of knowledge of surrounding context linked to bookkeeping practice is why de Roover, and accounting historians in general, have not understood what motivated medieval Italian bookkeepers to adopt the practices they used. It is why they dismiss, as Basil Yamey did in 1975, the claims of those who did know what motivated them. Without knowledge of context, it is impossible to understand or explain why certain practices were adopted while others that accountants today might consider important, even essential, were not.

Understandably, the absence of significant contextual details in their publications gives those writing about the history of medieval accounting very little to discuss beyond the technicalities of the records they describe; and the contrast between the practices identified and how account records and reports are kept and prepared today. That is what medieval accounting historians of all nationalities have done. It is evident from this literature that Italian bookkeeping practice changed between 1200 and 1500 but, explaining ‘why’ has never been adequately attempted, nor achieved. Ignoring this mystery and based on the apparent assumption that there is nothing to be learnt from medieval bookkeeping practice that would be relevant today, most early modern 5 and modern studies of accounting history that refer back to medieval times use Pacioli's treatise as their normative starting point (Goldthwaite, 2018; Martinelli, 1974).

While Pacioli's treatise may have been the roots from which the method of double entry was spread beyond its Italian beginnings in the almost 800 editions of bookkeeping manuals published between 1500 and 1800 (Jeannin, 1991), it does not reflect either the reality or the diversity of double entry as practiced by Italians in the fifteenth century. For example, the use of Pacioli's treatise in this literature as the model of Italian double entry at the end of the fifteenth century ignores the fact that medieval Tuscan business, bookkeeping, account books, and accounting practice were not the same as those of Venice – there was no ‘Italian model’. It also ignores the existence of far greater complexity in actual Venetian practice than is evident in what Pacioli describes (Lane, 1944).

Perhaps its recognition as a faithful reflection of medieval Venetian practice by two very eminent Italian accounting historians – Fabio Besta (1916) and Carlo Antinori (2004) – explains why it is used in this way by accounting historians. Yet, as with how the medieval marketplace is covered in the accounting history literature, anyone looking at what has been written about Pacioli and his treatise will detect a superficiality concerning the surrounding context, a vagueness in any discussion of his purpose when he published it, and an absence of agreement on either the intended readership or the value of the treatise as an instructional device. For instance, on the basis that periodic financial statements were prepared by medieval Tuscan partnerships, the treatise has been criticised ‘as a reference text for merchants … [who] might have welcomed guidance’ (Yamey, 2010: 150) and for not containing instructions in how to prepare them (De Roover, 1944). The explanation de Roover offered – that the treatise is an introductory textbook – implicitly indicates that he believed that periodic financial statements were also prepared by merchants in Venice. This was what Yamey (2010: 150.) also believed when, citing de Roover, he criticised Pacioli for failing to mention ‘various features of accounting to be found in 15th century Italy’. In doing so, he not only reinforced the view created by de Roover that financial statements were prepared in Venice, he extended it to embrace all of Italy.

To conclude, in all this literature, the surrounding context seldom features in conclusions reached concerning the quality or purpose of the treatise, or in the criticisms that it receives. The bookkeeping method and system that Pacioli presents is understood, but not why he published it, nor what benefit it might bring to those who adopted it. Pacioli says relatively little about how commerce itself was conducted or of the infrastructure in place to facilitate it. Instead, implicit in the treatise, Pacioli assumed his readers would already have much of that knowledge. Framing the contextual information to use, Pacioli did not write about how Tuscans, the Genoese, or Italians from Lombardy managed the records of their business. He wrote exclusively about Venice. Therefore, the only contextual factors relevant to this study are Venetian – in Venice and of Venice – and, in particular, how business was conducted in the Venetian international wholesale market at the Rialto. The medieval economic history literature, and the medieval literatures of societies and markets published over the past 90 years, must be consulted for that missing contextual information. As we shall demonstrate, when that commercial context is added to Pacioli's text, it is clear how focused he was on providing something that was fit for purpose, something that would be truly useful to those who placed their trust in it.

Given its importance in the history of accounting, this article introduces that literature to support its analysis of the purpose of Pacioli's treatise. We begin with an overview of the Venetian commercial world for which the treatise was written.

Venice, the economic capital of the world

In the fourteenth and fifteenth century, Venice was the centre of the economic world (Braudel, 1984). Prices and exchange rates fluctuated with the State-orchestrated arrival and departure of the fleets, and in response to correspondence and rumours relating to anything that might impact supply, demand, or the value of money: Although Venice could be called a city of perpetual fairs, as Antwerp was later, in the sense that both trade and the

In Venice, the Campo San Giacomo di Rialto was where wholesale merchants and international merchants went about their business (Braudel, 1984; Lane, 1968; Romano, 2015). Not surprisingly, it was not only where most commercial transactions, large and small, were negotiated (Mueller, 1997), it was where merchants heard the news and gossip essential to their business (Lane, 1973). This was where the ‘big business’ was conducted. Merchants had to earn the right to be there, had to follow "a set of unspoken rules that informed and shaped the behaviour of the parties involved" (Romano, 2015: 111), and they feared the consequences if that right was withdrawn: Being excluded from the right to go to the Rialto meant, as it is said in numerous requests for pardon, being deprived of the possibility of practicing large-scale trade. (Luzzatto, 1961: 78)

These merchants did not only have to be seen to be conforming to custom. If they were to be successful, they had to manage their affairs in the most efficient and effective way. One issue that they all had to address was a shortage of cash for the volume of trade that took place (Lane, 1968; Luzzatto, 1961). Consequently, they did everything possible to avoid using cash, and did so with the assistance of the banchi di scripta, also known as banche del giro (transfer banks), that positioned themselves beside the market.

6

An eyewitness account from a traveller passing through Venice in the 1490s described how this system worked: The moneychangers are seated around the square, and they hold the money that merchants consigned to them in order to avoid the counting out of cash. When one merchant pays off another, he gives that person an assignment in bank, so that very little cash passes among the merchants. (Mueller, 1997: 5)

These merchants also managed their working capital carefully, for example becoming overdrawn at their bank if necessary to take-up an opportunity to make a profit or avoid a loss (Ryabova, 2020). Both the merchants and the bankers needed very orderly records of their affairs to participate successfully in this process. For merchants, this involved keeping detailed records of their transactions; contracts, some notarised, others not; their correspondence; promissory notes; and any bills of exchange they issued. And, in a virtually cashless trading environment, they needed to know what credit they had, not just with their bank but, also, with other merchants. By doing so and using it effectively, they were able to embrace opportunity and fully engage in the clearing process that was a key part of the marketplace.

Bookkeeping and other records kept in the wholesale marketplace

In order to avoid confusion, the activities of trade and the clearing process that followed required that a consistently applied method of keeping account was used by all the parties involved. This included use of the same money of account, 7 the gold-based lira di grossi a oro. Otherwise, disputes would have been frequent, settlement would have been disrupted, and the credit-based economic structure of the marketplace would have struggled to operate effectively.

By the early fifteenth century, the manner in which entries were made in personal accounts had been standardised in Venice: Within the Venetian circle [of wholesale merchants] … there was ‘a commonly known “language” of accounting’. Each [merchant] knew what ought to be in the other's books concerning a transaction in which both were involved. Both used the arrangement of debits and credits in parallel columns, debits left, credits right, and clarified the duality of entries by cross references to the matching debit or credit for each entry. (Lane, 1977: 181)

Double entry gave a merchant the ability to see what he needed in order to conduct his business efficiently; and all surviving Venetian medieval wholesale merchant account books are in double entry (Lane, 1944, 1977). The trail to the evidence that is built into the Venetian double entry system, both from account to account, and from entry to supporting evidence makes it superior to other forms of bookkeeping (Lane, 1977). This was especially so in a credit-based marketplace like the Rialto, where a merchant needed to know his credit position swiftly at any given time. He also had to be able to prove it in the short timeframe that may have existed to take-up opportunities to make profit or avoid loss, and to participate efficiently in the clearing process.

Without the adoption of double entry, Venetian trade would never have flourished to the extent that it was the centre of European trade for at least 150 years, during which credit, offset, and bank transfers were dominant facilitating forces. None of these can be securely managed with simple forms of bookkeeping. Consequently, it is inconceivable that the banks, upon whom the wholesale merchants depended to facilitate the movement of funds from one merchant to another, did not use double entry. The merchants who traded in this marketplace used it as well (Antinori, 2004; Besta, 1916; Lane, 1944, 1977; Pacioli, 1494). 8

Doing bookkeeping well is a higher level of skill than understanding bookkeeping entries. The account books that have survived indicate that the merchants acted as their own bookkeepers.

9

However, it is likely that some began trading as wholesale merchants without the skill to do bookkeeping well, perhaps overcoming this weakness by employing a bookkeeper. As we will show later in this article, it is therefore understandable that when writing for newcomers to this marketplace, Pacioli

Thus, "it was easy for a [merchant] to compare his record of accounts with that of his banker" (Mueller, 1997: 7); and for merchants to do so with each other, which Pacioli indicates they did in Chapter 7 of his treatise. 10 He also alludes to this in Chapter 23 and, in particular, in Chapter 36, when he presents one of the rules of Venetian trade: no entry can be made in double entry that creates a debtor or sets limitations or conditions to an entry in the account of a creditor without the permission of the account holder.

The importance of double entry for wholesale Venetian merchants is echoed by Tagliente (1525a), who begins his manual on double entry by stating that knowing double entry, 'was necessary for our magnificent patricians 11 and other [wholesale] merchants". In contrast, in his manual on single entry, also published in 1525 (Tagliente, 1525b), he makes it clear that it was for retail merchants: ‘merchants and artisans accustomed to working in their shops’. He then presents single, not double entries for that environment in the different money of account used for retail trade.

The wholesale merchants also understood the supporting evidence that may have been provided to them, and they knew where to find their own supporting evidence, if required. As we shall show later, this need for those operating in this marketplace to maintain well-organised business records is something Pacioli emphasises in the Introduction to his treatise: any merchant who lacked double entry account books and did not keep his other records in good order would struggle to enter, never mind survive in the Venetian wholesale marketplace.

The retail marketplace

Retail trade in Venice was very different. Located in San Polo and San Marco (Luzzatto, 1961), one obvious difference was that a smaller number of banchi di scripta, located in San Marco, served the retail market (Luzzatto, 1961: 100). A much more significant difference involved the money of account used to record transactions. Where trade in the wholesale Rialto market was recorded in lire di grossi a oro, a gold-based money of account of which one lira equalled

Pacioli and the wholesale marketplace

In 1494, with the intention of providing merchants with the tools they needed to participate in the wholesale market at the Rialto, Luca Pacioli published his treatise, De computis et scripturis. We know it was written for this Venetian market because of the money of account he uses – lire di grossi a oro. The treatise provided its readers with instructions in double entry bookkeeping, of the records they needed to keep, and in how to do so in an orderly way. It enfranchised would-be wholesale merchants and struggling wholesale merchants who, without those skills, had very little possibility of surviving in this marketplace for local wholesale and international merchants. Apart from patricians, it also provided what was needed for any retail merchants who purchased their goods in the Rialto and aspired to one day become wholesale merchants.

As time passed, Pacioli's treatise was replaced by others, but Pacioli was never forgotten. He was mentioned in bookkeeping manuals in Italy in the sixteenth and early seventeenth centuries; and in France, for example, in the late seventeenth century (Hernández Esteve, 1994). In the nineteenth century, when Russians, Germans, and Italians rediscovered Pacioli's treatise, they recognised it for the foundation stone of modern accounting that it represents. It became a topic of great interest and debate. Since then, it has been transcribed at least four times, and translated many more, into at least 14 languages (Sangster, 2007) but, as the findings of this study will show, it has never been fully understood.

The next section presents an overview of, arguably, the four most important and influential publications produced in 1994 to celebrate the 500th anniversary of the printing of Pacioli's treatise. This is followed by a description of the methodology adopted in this study and of the issues faced in pursuing that methodology. We then present our translation of the first chapter of Pacioli's treatise, with no critical commentary, so that it may be read without distraction in the manner intended. This is followed by a comparative analysis of translations of key sections of the chapter by the five English-language translators, and by translators into German, French, Italian, Spanish, and Russian. Finally, conclusions are presented.

The Appendix to the article presents the critical version of our translation, so that the justification for the words used may be understood. The five English translations are: Geijsbeek (1914); Crivelli (1924); Brown and Johnston (1963); Cripps (1994) and Von Gebsattel (1994). The five non-English translations we examined were: Pendorf (1933) (German); Haulotte and Stevelinck (1962) (French); Antinori (1990, 1994) (Italian); Hernández Esteve (1994) (Spanish); and Kuter (2009) (Russian). In addition, we examined Yamey’s (1994) partial translation into English (see below).

What we found was that all the translations we examined had misunderstood what Pacioli wrote in his first chapter and, consequently, misunderstood the content and purpose of the treatise. We looked more closely at the five English translations and found that they all omitted some text and inserted some that was not in the original. The translators who prepared each of the 10 translations we examined all perceive it is about double entry in the form of a manual on double entry for all merchants; and that what Pacioli says about maths in this chapter relates to being able to do double entry. It is none of these. It is a manual for wholesale merchants about how to organise all their business records, including their account books, so that information on transactions can easily be found. In the chapter, Pacioli also emphasises, un-noticed in the literature, the importance of good working capital management; and, misunderstood in the literature, being good at mathematics and quick at doing calculations, something he returns to in Chapter 34, where he emphasises the importance of wholesale merchants forcing themselves to learn the maths, particularly if they are not good at keeping accounts. The maths were needed, not just for the relatively simple maths needed to record entries of transactions and to identify balances on accounts but, to ensure that all the calculations undertaken in business were correct.

– new translations and a new transcription

In 1994, to accompany a new translation into English by Antonia von Gebsattel and, concurrently, to accompany a new critical transcription by Annalisa Conterio, Basil Yamey wrote a commentary on Pacioli's bookkeeping treatise. The English translation and the critical transcription, each accompanied by the commentary, were published in separate books and sold as a 3-part set, along with a book on Venetian State auditing between the sixteenth and eighteenth centuries by Andrea Zannini. In his commentary, Yamey surprisingly made no use of Von Gebsattel’s (1994) translation, preferring instead to use the first English translation by Geijsbeek (1914). He presented his own translation when he disagreed with Geijsbeek's, which he did several times (Yamey, 1994).

The translation by Von Gebsattel, perhaps because she learnt from the mistakes and omissions in earlier English translations, overcame many of their limitations and brought greater clarity to Pacioli's text for English-speaking readers than before. Concurrently, Esteban Hernández Esteve (1994) published a critical edition and translation of the treatise into Spanish. That same year, Carlo Antinori republished his modern Italian translation, previously published in 1990; and Annalisa Conterio’s (1994) critical transcription provided a more informative replication of the source than previous transcriptions, all of which are far easier to read than the original. However, none of the transcriptions are identical; and all, even if only to a small extent, correct or modernise the text. Anyone wishing to know what Pacioli wrote, must still have recourse to the original.

After these four publications , scholars had what they needed to understand Pacioli's treatise in ways they never had before. For any accounting historian interested in studying Pacioli's treatise in depth, or any part of it, 1994 should have represented the beginnings of a new dawn in understanding of what the treatise is; of what it serves to do; of what it tells us about the Venetian commercial world in the late fifteenth century; and of the instructions within it. Unfortunately, it did not.

Of the many studies by accounting historians since 1994, only a few have referred to any of these sources. Instead, most English language scholars continue to use Geijsbeek's translation of 1914 which, for most of this period, was freely available online. 13 A secondary aim of this article is, therefore, to draw attention to these four publications of 1994, so that future scholars of this topic may seek out and use the best available sources, rather than those that simply happen to be easy to obtain.

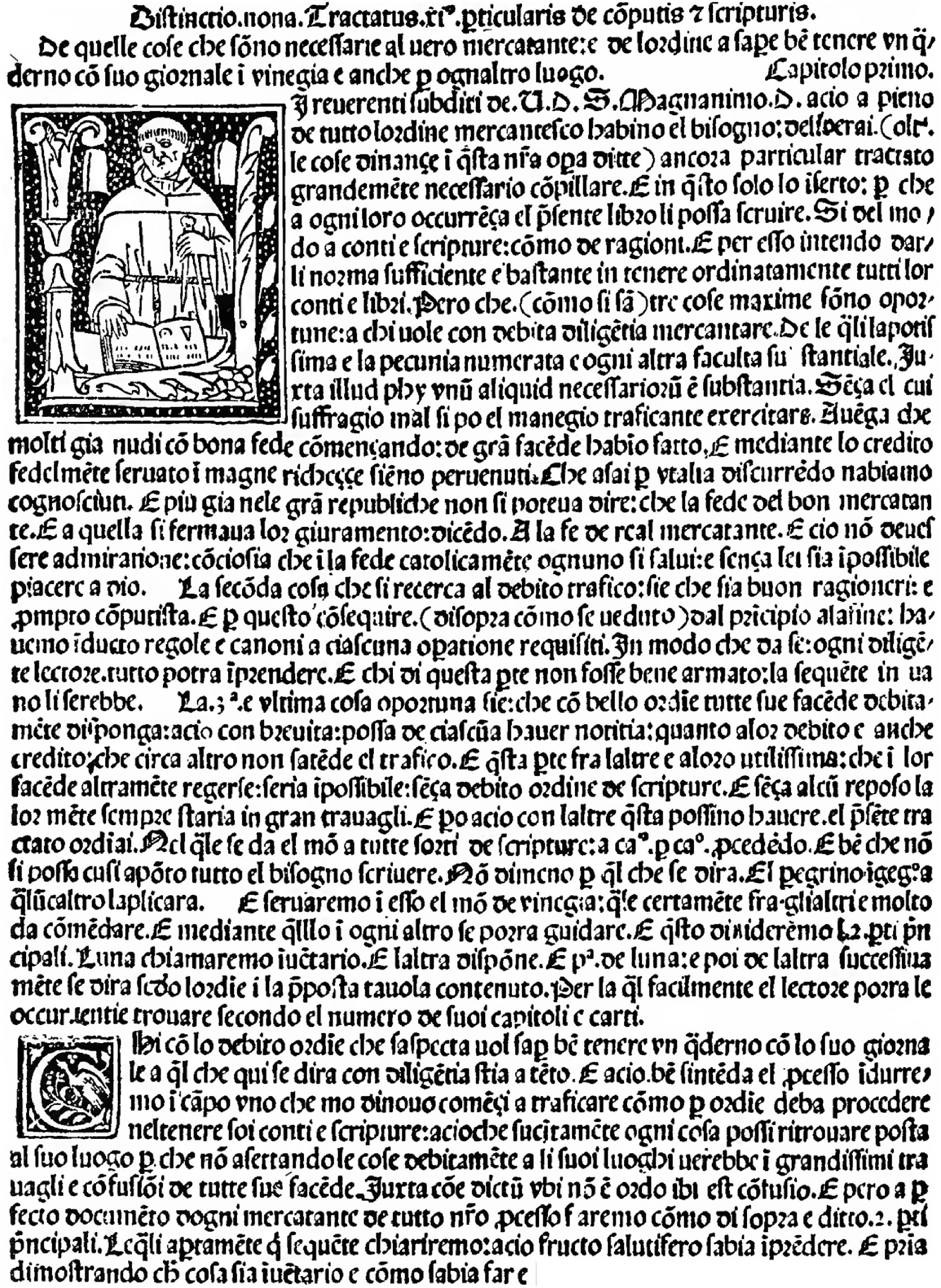

In this study, we focus on what Pacioli says in his opening chapter, particularly about the qualities needed to be a true (vero) merchant and about the focus of the rest of the treatise. In order to do so, we used literary hermeneutics, analysing the text, looking beyond the words for context within and outwith the treatise that may help us to have a clearer understanding of what it was that Pacioli was endeavouring to do, and why. Primarily, we focus on the words and terms he used, how he used them, and when. The outcome is a differently focused translation of the introductory chapter from those currently available; one that we have endeavoured to make consistent with the treatise as a whole, and with the environment, or context, in and for which it was written. The same cannot be said for any of the previous attempts to translate this chapter that we have seen. Our findings are important because, not only are they informed by what is known about the context in and for which it was written, they enrich what is known about bookkeeping's role in medieval wholesale trade. In turn, this should lead to an improved understanding of the role and purpose of using double entry in European trade during the fourteenth and fifteenth centuries, and thereafter. Figure 1 presents the first chapter of Pacioli's treatise as printed in 1494.

Pacioli's first chapter (1494). Source: Geijsbeek (1914: 32).

Methodology

Because we were seeking understanding of and about written text, literary hermeneutics was the research method adopted in this study. As anyone will find if they try to decipher the words in Figure 1 without considerable experience of doing so, reading Pacioli's treatise is a very lengthy and laborious process. First, the reader must learn to distinguish the gothic lettering, not only its style but, also, the irregularity of the typeface caused by inconsistencies between the multiple dies of some letters that make it hard to distinguish, for example, between an ‘i’, a ‘c’, an ‘e’, and an ‘l’; and some letters have more than one design. For instance, an ‘r’ in one form looks like ‘r’; in another, it looks like ‘z’. Beyond the typeface, the reader faces the challenge of a large number of abbreviations – five to six every line. These abbreviations were carried over from medieval merchantesca script, the handwriting style used by merchants – effectively a form of shorthand – which made their use in a printed book written for merchants by Pacioli, a former merchant's apprentice (Sangster, 2021), understandable. Some are subtle, some very obvious, and some are ambiguous and need the surrounding text and context to be understood if you wish to be sure what they represent.

Once the text had been deciphered, the problem became one of understanding the words that are being used, then the phrases in which they appear. When read successfully, the text is said to be easily understood by an Italian speaker (Tomasin, 1994; Belloni, 1994) – which probably explains why there is only one known translation of the treatise into modern Italian, but four transcriptions. However, language is forever changing and there are ‘false friends’ 14 within the treatise that go to the heart of misunderstandings that we present in this article. There is also at least one error made by the 1494 typesetter in Chapter 1 that could lead the unwary into major misunderstanding. Even inserting punctuation, of which there is relatively little in the original, can change the meaning, and needs to be done with considerable care.

Taking all this into account, it is not a surprise that there are innumerable differences between the five English translations. But, it was a surprise to discover that in their translations of Chapter 1, as mentioned above, all five of these English language translators omit statements and all five add text that is not there.

Translating Pacioli's treatise

In preparing his commentary, Basil Yamey (1994) indicated in a footnote that he referred to Florence Edler's Glossary of Mediæval Terms of Business (1934), something he acknowledges doing on four different occasions. Pacioli's treatise was among the sources used by Edler. In her Glossary she provides definitions for some Venetian fifteenth century terms, including computista and ragioniere (Edler, 1934). Both terms are used by Pacioli. In the latter case, Edler points out that he did so using a different spelling, ‘ragioneri’. Yamey used Edler's definition of that term in his commentary, as did Von Gebsattel, presumably because she had access to the same sources as Yamey. However, it was misunderstood by all the other English language translators, and also the translators of five non-English translations we examined. All of them appear to have relied on an assumption that the word in 1494 had the same meaning as it does today: accountant. It did not. The impact of this mistake in the translations has caused the importance of being able to do bookkeeping well to be vastly overstated in the literature about Pacioli's treatise.

This mistake has been known to this research team for some time and was the catalyst for this study. In the light of it, we resolved to minimise this potential ‘false friend’ problem by having the non-Italian member of the research team prepare the first translation of the chapter; and, at the same time investigate the etymology of the terms used by Pacioli, doing so with the assistance of dictionaries published as close to 1494 as we could find. That is, we identified the contemporary English translation and then investigated what the English word meant at that time. The Italian member of the research team than reviewed and amended the translation as appropriate.

We could identify no fifteenth century Italian dictionaries, but we found two from the sixteenth century: Filippo Venuti's (1565) Dittionario volgare and Latino and Iohn Florio’s (1598) A worlde of wordes, or, Most copious, and exact dictionarie in Italian and English. Florio's dictionary is particularly useful as it is heavily derived from fifteenth century literary sources, which meant that many of his translations were informed by the meaning and use of the Italian words in the fifteenth century. We also used LATdict, 15 the Online Latin Dictionary, 16 and the Tesoro della Lingua Italiana delle Origini. 17 To verify the validity of their use and to check that their meaning at that time was still in use today, the Online Etymology Dictionary [OED] 18 was used to identify the origins of the English words provided by Florio as being equivalent to Pacioli's. As a final check, we used Florence Edler's Glossary.

In addition, we benefited from several years of experience working in archives, reading, transcribing, and translating other medieval texts, which provided us with both experience in reading merchantesca script and an awareness of the language and the context.

Latin is part of medieval Italian dialects and Pacioli includes many Latin words and phrases in his treatise. In previous studies on manuscripts from the same period, we had found Google Translate to be useful in recognising Latin words. Consequently, at first we used it, phrase by phrase, switching between Italian and Latin, as appropriate. However, Pacioli's language is a mixture of Tuscan and Venetian dialect, Latin, and Latinised Italian words. This proved too complex for the online translator. Florio's dictionary quickly became the primary source and was instrumental in discovering ‘false friends’. Google Translate was relegated to occasionally assisting with troublesome phrases and for translating Latin terms, for which we also used the two online Latin dictionaries mentioned above. Used together, these three Latin translators identified by omission the Latinised Italian.

Throughout this process, we maintained our hermeneutic approach. Chapter 1 was read dozens of times, both the original text from the 1494 and the 1523 printing, each time correcting the transcriptions we had prepared until we arrived at a transcription that we perceived to be fully consistent with the 1494 original. The same approach of reading and rereading was adopted in developing our translation: seeking understanding of each term and phrase in the context of the rest of the chapter, and the commercial, economic, and financial world for which it was produced.

Transcribing and translating Pacioli's first chapter

Several problems in the way Pacioli's treatise is written and printed impacted our progress. Transcription problems became greater after our transcription had been completed. Some words are joined as if they are one single word, others are printed with a space separating the letters into two groups – an example can be seen at the end of Figure 1, when the word ‘fare’ is split into ‘far’ and ‘e’. In addition, as exemplified by Edler (1934: 238), the spelling quite often differs from that of the dictionaries; and some words used are not in those dictionaries. Consequently, the meaning of words and phrases were sometimes very difficult to determine. This, in turn, made some phrases difficult to understand, which sowed seeds of doubts that the transcription was correct. As a result, several times while translating the text, we had to revisit the transcription and confirm its accuracy. We avoided consulting any of the printed transcriptions until we finally agreed on our own, after our translation was completed. When we did, we discovered modernisations and adjustments to the text that confirmed that we had been correct to prepare our own transcription first.

Che circa altro non satende el trafico

One of the most problematic pieces of text in Chapter 1 is the statement, ‘che circa altro non satende el trafico’ (‘because, concerning anything else, trade has no need’). 19 In print, the ‘s’ and ‘atende’ are joined. Today, this would be written with an apostrophe after the ‘s’ (see, e.g., Conterio, 1994). However, the five English language translators do not appear to have realised this. The ‘s’ uses the old form of an ‘f’ without the horizontal line; and the ‘t’ is very easily misread as ‘c’. On the basis of how they translated the entire phrase, those translators all probably read ‘satende’ as the word ‘facende’ (business), noted that this is broadly equivalent in meaning to ‘trafico’ (trade), realised that they could not understand the statement, and so either omitted it, or ignored satende/facende in their translations. In contrast, in his Italian translation, Antinori (1990: 15) translates the statement as, ‘poiché di altro non abbisogna il commercio’ (‘because trade has no need of anything else’).

This statement typifies how difficult translating the treatise can be; and the manner in which each translator dealt with it differs greatly. This also highlights a potential problem for anyone reading these translations, not just of this passage of text but, the treatise as a whole. We shall return to this passage later when we present examples of problems in the translations.

The next section presents our translation (Figure 2). Others may disagree with some of it. Some will no doubt find other ways to express what it says, as the translators whose work we critique did. However, we do not omit any word or phrase from the original which, irrespective of any disagreement over the meaning of individual words or phrases, means that this translation is more complete than the others. We also have a far greater understanding of the context surrounding the text than was possible, even as recently as 1994, when the last of the English language translations was published. This is followed by an analysis of ten translations of this chapter, five in English, plus one each in German, French, Italian, Spanish, and Russian. Our findings indicate just how deeply the misunderstandings of the text have become embedded in a literature that depends on them for its existence. To address any concerns about the appropriateness of our translation, as previously mentioned, a critical version is presented in the Appendix, indicating why meanings were selected and the sources of those meanings.

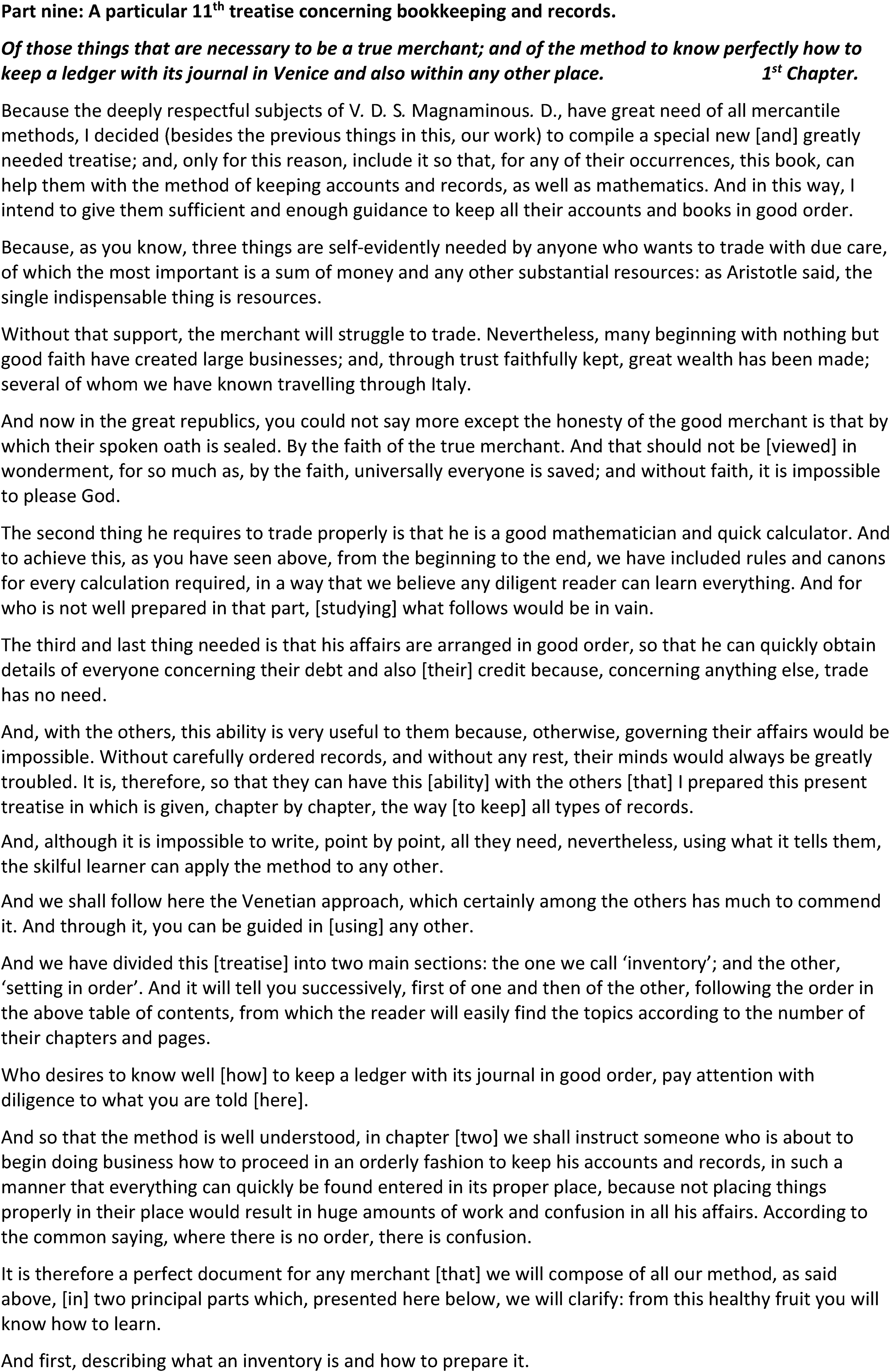

Translation of Pacioli (1494) Chapter 1 by the authors.

The translated text of Pacioli's first chapter

What has been overlooked or misunderstood in Chapter 1 of the treatise

One problem for anyone reading any of the five English language translations of Pacioli's treatise is that they are all written as if the sole important topic in the treatise is double entry bookkeeping. This appears to have influenced the translations as their authors sought to maintain the focus they believed to be appropriate. Yet, Pacioli is very clear from the beginning of the treatise, in its title, the title of Chapter 1 and, as is evident from reading through that chapter, that the focus is much broader than double entry: it is on keeping orderly records, that can be easily found, pertaining to any aspect of the business, including bookkeeping.

From the outset, Pacioli justifies the combination of commercial mathematics and his treatise in one book, Summa Arithmetica. He emphasises the importance of being good and quick at doing calculations if someone is to be considered a true merchant. He makes it clear that if a merchant cannot do the mathematics, his business is doomed, and learning what is in the treatise would be pointless. However, if he can do the maths, keeps all his affairs in good order (including the use of double entry bookkeeping), and honours his oaths, he can be considered a true merchant and, by implication, can be a successful one. That is the overall message of Chapter 1. It has little to do with an ability to do double entry bookkeeping: while the account books and all other business records should be kept as they are kept in the wholesale marketplace of Venice, there is no indication in this chapter that the merchant himself should be doing the bookkeeping. His responsibility to himself is to keep all his affairs in good order, and keep his word, which is not the impression anyone will get from reading the English translations.

In contrast to the title of the treatise: ‘Concerning bookkeeping and records’, where ‘bookkeeping’ is mentioned first, in the title of Chapter 1 Pacioli places the initial emphasis on business before mentioning bookkeeping: ‘Of those things that are necessary to be a true merchant; and of the method to know perfectly how to keep a ledger with its journal …’. This message is repeated and extended to other records after the opening address, when Pacioli explains what benefits the inclusion of the treatise in Summa Arithmetica gives merchants (emphasis added): ‘… so that,

Examples of omissions and misunderstandings in the translations of Chapter 1, and in the literature, include ones relating to mathematics, the marketplace, and other records.

Mathematics

None of the five English translations recognises how Pacioli situates the treatise within a book of practical mathematics. He declares that through his book he is providing merchants with a complete resource to meet their mathematical needs, their bookkeeping needs, and their need to maintain orderly records of all their affairs. When Pacioli writes that he only includes this treatise in his book, ‘so that, for any of their occurrences,

The marketplace and other records

The treatise is more than a manual of bookkeeping. It is a manual on how to maintain all the records of a business. None of these ten translators, and no-one we are aware of who has written about the treatise, has defined it in these terms. Yet, anyone who reads the treatise carefully, and with an open mind, will appreciate that it goes beyond the keeping of accounts, dealing also, for example, with maintaining records of, among other things, letters, bills of exchange, promises, promissory notes, agreements, conditional transactions, receipts, important papers, reminders, items lent, and items borrowed. Adding weight to this emphasis that Pacioli places on all records, a similar importance was placed on these other records by the international wholesale merchant Benedetto Cotrugli (1458) in his manuscript book, The Art of Trade. 20 Furthermore, anyone who looks at the large volume of surviving business records of fourteenth and fifteenth century wholesale and international Italian merchants, such as Francesco di Marco Datini, 21 will see that these topics included by Pacioli do, indeed, describe the types of records a merchant who traded in the international wholesale marketplace needed to keep; and those records were much more than simply the books of account.

Misunderstandings aside, there is one major problem in these translations that impacts much of what has been written about the treatise. It concerns how four terms and phrases, in particular, have been mistranslated, especially into English.

Misleading translations

Translating ‘scripturis’

The first of these four terms and phrases is the Latin word ‘scripturis’, which appears in the title of the treatise. The contemporary translation into Italian was ‘scritture’. Edler (1934: 266) presents the medieval meaning of ‘scritture’ as ‘records’, making the point that it meant, "the records scripture, a writing, a writte, the writing or making of a booke, the stile or maner of the writing of any author. Also any kind of indenture, evidence or hand-writing.

Based on both sources, the meaning of ‘scripturis’ was ‘written records other than those made in account books’. In the body of the treatise, Pacioli used an Italianised form of ‘scripturis’: ‘scripture’. He used it four times in Chapter 1. From our analysis, its meaning is the same as ‘scritture’, that is, ‘records’. This becomes particularly clear when Pacioli wrote: E in questo solo lo inserto; per che a ogni loro occurrença el presente libro li possa servire. Si del modo a

and, only for this reason, include it [the treatise] so that, for any of their occurrences, this book [Summa Arithmetica], can help them with the method of keeping

In this statement, he uses ‘conti’ for ‘accounts’, ‘scripture’ for ‘records’, and ‘ragioni’ for ‘mathematics’.

Three of the five English language translators failed to define ‘scripture’ correctly. One of the others, Von Gebsattel (1994), initially translated it as ‘records’ but, then changed the translation to ‘accounts’, and then ‘entries’ (twice). Another (Cripps, 1994) who did not translate it initially, translated it subsequently as ‘double entry’, ‘accounting transactions’ and, finally, as ‘records’. As suggested above, it would be reasonable to conclude that the translators were influenced by the perception that the treatise is about double entry bookkeeping, and that they endeavoured to fit their translations into that framework, even if doing so required them to omit the term or change the translation they had previously used.

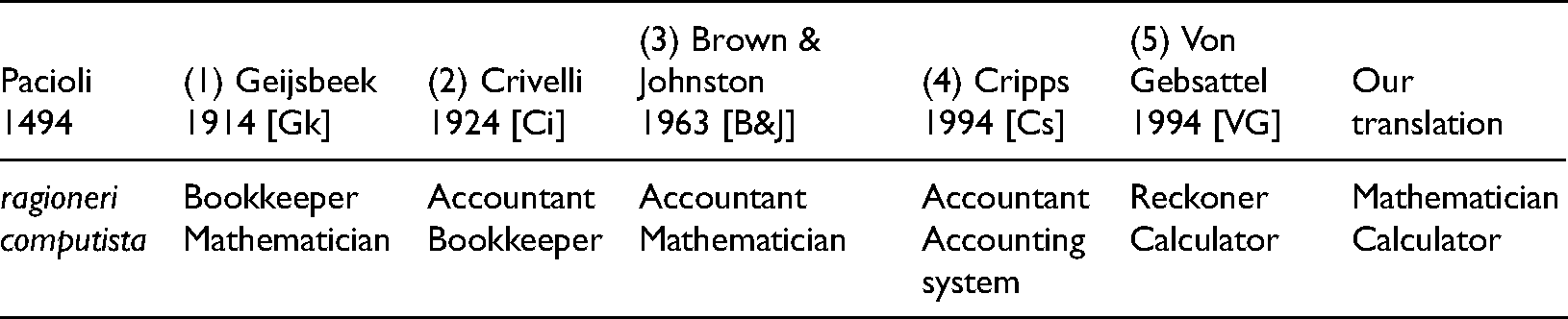

Translating ‘ragioneri’ and ‘computista’

The second and third terms whose English translations have had a significant negative impact on understanding are the aforementioned ‘ragioneri’, and the word ‘computista’. Both of these appear in the statement: la seconda cosa che si recerca al debito trafico: sie che sia buon ragioneri; e prompto computista. the second thing he [a merchant] requires to trade properly is that he is a good ‘ragioneri’ and quick ‘computista’.

(The ‘first thing’, or quality that a true merchant required, ‘a sum of money and any other substantial resources’, was understood by all these translators.)

The contemporary translation of ‘ragioneri’ was ‘reckoner’, what we today would call a ‘mathematician’. A ‘computista’ was a ‘calculator’. The phrase is saying that merchants needed to be good at mathematics and quick at doing calculations. Neither term is referring to being a bookkeeper, nor being an accountant, both of which are prominent in the translations.

In Venice at that time, the title given to a bookkeeper was a ‘scrivano’ or a ‘quadernier’. Pacioli consistently used the term ‘quaderniero’ when he referred to a bookkeeper; de Raphaeli used ‘quadernier’ in his double entry manual of 1475 (Sangster, 2018); and the new position of ‘quadernier’ was established in 1475 in the administration of the Scuola Grande di San Marco as a subordinate of the scrivano with the responsibility of making entries in its double entry ledger from the journal (Takami, 2017), presumably previously a task undertaken by the scrivano.

The last person to publish a translation in English, Von Gebsattel (1994), was the sole exception. She correctly translated the terms as ‘reckoner’ and ‘calculator’.

Table 1 shows how these two terms are defined in the five English translations.

The five English translations of ragioneri and computista.

The translators appear to be focusing on accounting, while Pacioli is focusing on business. Perhaps they would have worded their translations differently had they known the importance of these two skills for merchants in fifteenth century Venice. There were multiple weights and measures, two quite different moneys of account, multiple currencies in circulation, constantly changing exchange rates, indirect taxes, fees, commissions, interest rates, financial instruments, freight costs, insurance, risk, trust, and many other factors in play. Merchants had to be able to bring any or all of them into their calculations when negotiating purchases and sales. (See, e.g., Braudel, 1984; Lane, 1944; Lane and Mueller, 1985; Luzzatto, 1961; Mueller, 1997)

As previously indicated, those terms are presented together by Pacioli as the second quality necessary of any merchant. When the translators shifted to Pacioli's third and final quality, they carried forward their misunderstanding.

Keeping records in good order

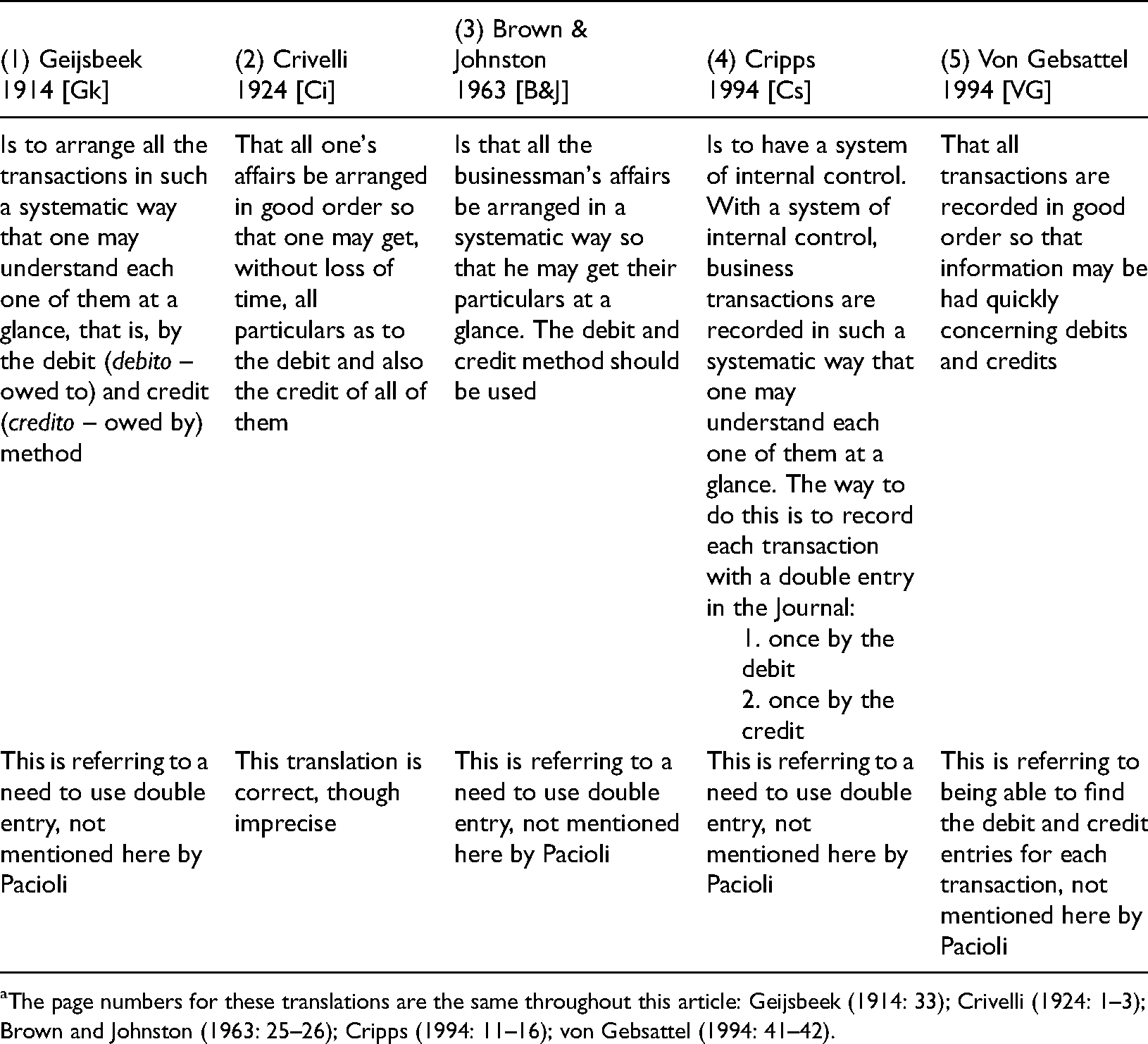

Pacioli wrote that this third quality of a true merchant was, ‘che con bello ordine tutte sue facende debitamente disponga: acio con brevita: possa de ciascuna haver notitia: quanto alor debito e anche credito’ – ‘that his affairs are arranged in good order, so that he can quickly obtain details of everyone concerning their debt and also [their] credit.’ Pacioli is not here indicating that a merchant needed to use double entry, though that is what most of the translators believed.

Their translations are shown in Table 2, with a brief comment on each translation in the final row.

The five English translations of Pacioli’s third essential quality of a true merchant. a

The page numbers for these translations are the same throughout this article: Geijsbeek (1914: 33); Crivelli (1924: 1–3); Brown and Johnston (1963: 25–26); Cripps (1994: 11–16); von Gebsattel (1994: 41–42).

This misunderstanding continued with Pacioli's concluding comment about this third quality.

Knowing what is essential for trade

As mentioned earlier, after his third quality, Pacioli wrote: ‘che circa altro non satende el trafico’ – ‘because concerning anything else, trade has no need’. Table 3 shows the variety in the five English translations of this statement. None of those who translated it were correct. In doing so, it also highlights another problem of which most scholars using these translations are likely unaware: omissions of text that is not understood and not indicated as having been omitted by the translator.

An example of the variation between the five English translators.

Someone who did not translate the treatise but wrote extensively about it was Basil Yamey. In his commentary of 1994, he translates and discusses these necessary mercantile qualities. The first quality is considered next.

Yamey's commentary on these terms and phrases, and on the first essential mercantile quality

Yamey correctly translated ‘computis’ as ‘bookkeeping’ but, although he used Edler's Glossary, and Edler was emphatic about the meaning of ‘scritture’ being ‘records’, not bookkeeping records, Yamey (1994) incorrectly translates the term ‘scripturis’ in the title of the treatise as ‘accounts’. This dual emphasis on accounting in his translation of the title of the treatise may have impacted his interpretation of the text when he described Pacioli's three essential mercantile qualities (Yamey, 1994). The second of these qualities has two components: ‘ragioneri’ and ‘computista’. As a result, to translate the three qualities, four definitions are needed, not three. When doing so, Yamey oversimplified the first three definitions and was incorrect on the fourth.

About the first quality, Pacioli wrote: ‘la potissima e la pecunia numerata e ogni altra faculta substantiale’ – ‘the most important is a sum of money and any other substantial resources’. Geijsbeek’s (1914: 33) translation of the first quality is ‘cash or any equivalent’. After this statement, Pacioli moved into a discussion of credit, beginning with a reference to merchants who were successful despite having no capital of their own because they obtained credit and managed it well. In doing so, he clearly distinguished between internal and external resources, highlighted the importance of credit, and emphasised the importance of being trustworthy. 22 For Pacioli's audience, credit was essential for trade; and it is short-term working capital sourced by credit from suppliers (and banks), and its management 23 that Pacioli is referring to when he discusses credit. Yamey (1994: 97) does not refer to Geijsbeek’s (1914) translation, makes no mention of Pacioli's discussion of credit, and defines the first quality using the term, ‘capital’. Pacioli was referring to, and wrote about, much more than ‘capital’.

When Yamey (1994: 97) lists qualities two and three, he provides his own translations: ‘knowledge of arithmetic; and knowledge of bookkeeping’. Like his use of ‘capital’ for the first quality, Yamey's compression of the definitions of ‘ragioneri’ and ‘computista’, both of which he understood correctly, into one phrase – ‘knowledge of arithmetic’ – is problematic. It does not express the intended meaning of either phrase: having knowledge of something is not the same as being good at doing it, nor being quick at doing it.

He then discusses the problems in translating this passage, explaining how he arrived at his translation of the second quality, ‘knowledge of arithmetic’, and repeating his third quality. In doing so, he does use the phrase, ‘good at arithmetic’, but he does not mention speed when writing about calculating: Pacioli's description of the second of the ‘three things’ (tre cose) that are necessary for the true merchant has caused some difficulties of interpretation. Pacioli writes that the merchant should be a buon ragioneri e prompto computista. This seems to be saying the same thing in two different ways, namely that is that the merchant must be a good bookkeeper; and this is especially odd because

In incorrectly defining the third quality as ‘knowledge of bookkeeping’, he implicitly accepts that Geijsbeek's translation, which he is using, is correct, though he greatly oversimplifies what Geijsbeek wrote: to arrange all the transactions in such a systematic way that one may understand each one of them at a glance, that is, by the debit (debito – owed to) and credit (credito – owed by) method. (Geijsbeek, 1914: 33)

Yamey further develops his thinking on this third ‘thing’ later in his commentary, when he refers to the eminent Italian accounting historian, Federigo Melis (1950: 629–630), who interpreted it as relating to a knowledge of the administration of the business. Yamey disagrees, concluding: But this reading [by Melis] does not square with the clear indication in the text that the third ‘thing’ is the subject-matter of the rest of De scripturis, namely the keeping of accounts in good order. (Yamey, 1994: 99)

On this point, Melis, not Yamey, is correct. There is no ‘indication in the text that the third “thing” is … keeping of accounts in good order.’

In adopting this stance concerning Melis, Yamey perpetuated the misunderstanding that Pacioli's third quality referred to a merchant needing to be a good bookkeeper when it actually refers to keeping orderly records of all his affairs, not just his records of transactions. Since 1994, no-one has published a new translation in English of Pacioli's treatise, and no-one has questioned Yamey's commentary on, nor his translation of the three qualities needed by any merchant, neither of which convey the points that Pacioli was making.

Thus, based on our translation (Figure 2), Pacioli stated that three things are self-evidently necessary to be considered a true merchant: (1) a sum of money and any other substantial resources, though sound working capital management can achieve the same outcome; (2) to be a good mathematician and quick calculator; and (3) to arrange his affairs in good order. Von Gebsattel (1994) correctly identified the first and second but narrowed the third to refer only to bookkeeping. The other English language translators understood the first, struggled with the second, and only one was able to translate the third. Yamey oversimplified both the first and second, though clearly understood them. He did not understand the third.

Having considered the translations into English, we then looked to see if translators into other languages had been more successful in translating Pacioli's second and third qualities.

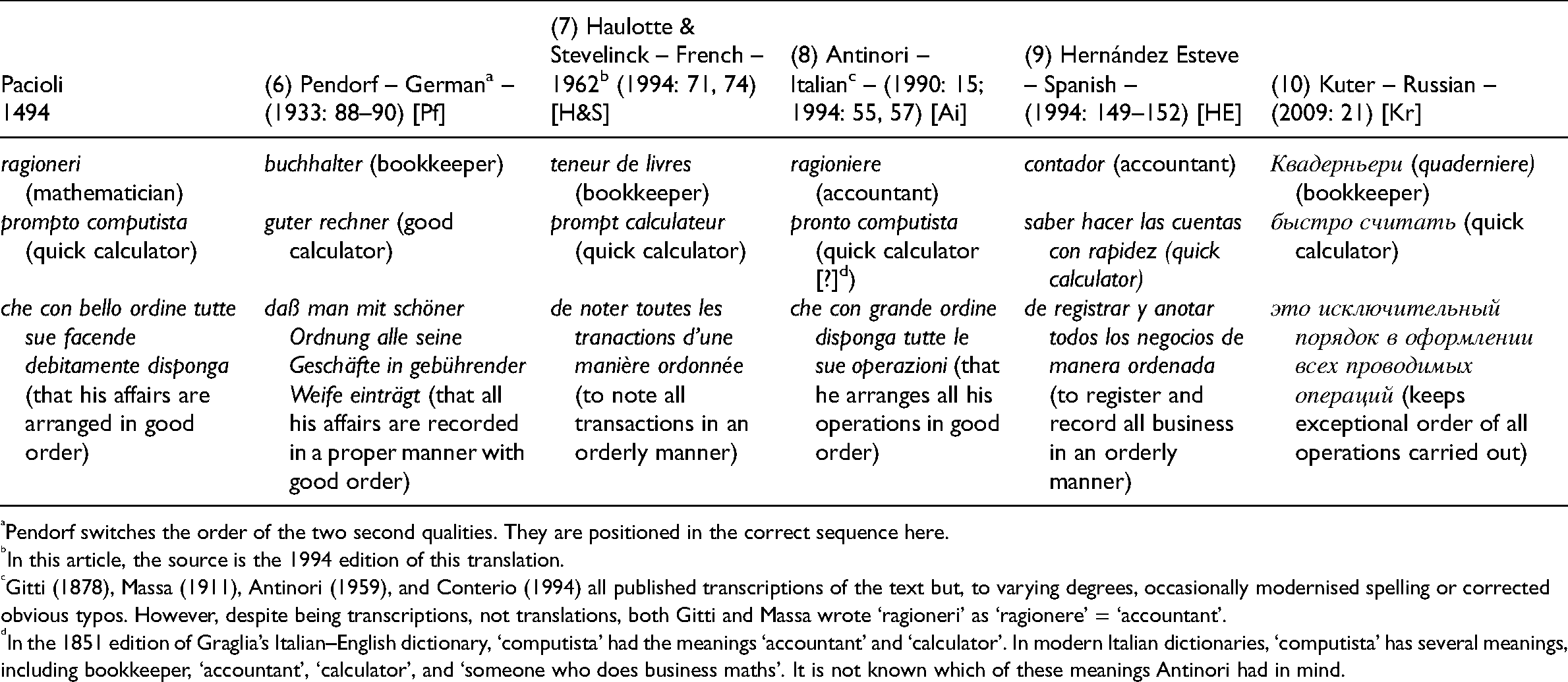

Translations in other languages

Table 4 presents translations of the second and third of the essential mercantile qualities in German, French, Italian, Spanish, and Russian.

The five non-English translations of the second and third essential mercantile qualities.

Pendorf switches the order of the two second qualities. They are positioned in the correct sequence here.

In this article, the source is the 1994 edition of this translation.

Gitti (1878), Massa (1911), Antinori (1959), and Conterio (1994) all published transcriptions of the text but, to varying degrees, occasionally modernised spelling or corrected obvious typos. However, despite being transcriptions, not translations, both Gitti and Massa wrote ‘ragioneri’ as ‘ragionere’ = ‘accountant’.

In the 1851 edition of Graglia’s Italian-English dictionary, ‘computista’ had the meanings ‘accountant’ and ‘calculator’. In modern Italian dictionaries, ‘computista’ has several meanings, including bookkeeper, ‘accountant’, ‘calculator’, and ‘someone who does business maths’. It is not known which of these meanings Antinori had in mind.

Considering the 10 translators, Table 5 summarises our assessment of the accuracy of their translations. It uses the numbering adopted in the previous tables.

Summary of the 10 translations of the second and third essential mercantile quality.

As can be seen in Table 5, nine of the ten translators mistranslated ‘ragioneri’ (mathematician). They all believed it to mean ‘accountant’ or ‘bookkeeper’. Only one of the five English-language translators identified the meaning of ‘computista’ whereas, the German, French, Spanish, and Russian translators correctly translated it as ‘calculator’. 24 Only one of the five English-language translators understood Pacioli's third quality, along with two others: the Italian and Russian translators. The other seven translators thought it was about using double entry or record-keeping.

Why clarifying these misunderstandings is important

As we have shown, we found that all the translations we looked at are misleading. Similar problems were identified with several of the points made by Yamey in 1994 who was, in effect, providing his own translation of what he saw as the key points in the first chapter. The literature based on the mistranslations tells us that this was a treatise on double entry and that being able to do double entry was an essential quality of a true merchant, retail or wholesale, along with having sufficient resources and being good at mathematics. This paints a very misleading picture of what a fifteenth century Venetian merchant needed to be. It also offers no explanation of why double entry was used. By correcting these misunderstandings, we present a clear image of what such a merchant had to be, and of why double entry was used.

Taking who Pacioli was writing for first, aspiring wholesale merchants, not retail merchants other than those who aspired to become wholesale merchants, there is no evidence that Venetian retail merchants used double entry. Secondly, he did not suggest that merchants had to be good at bookkeeping, or that they had to have sufficient resources to be true merchants. In fact, as previously mentioned, in Chapter 34, in another section that has been poorly translated, he states that if the bookkeeping is not good, being a good mathematician was essential, because that would enable mistakes to be identified quickly. To Pacioli, being a good mathematician was far more important for a wholesale merchant than being good at bookkeeping. For him, it was sound working capital management, being trustworthy, good at maths, quick at calculations, and well organised in keeping records that mattered, especially the latter which he viewed as being the key to success, and the most fundamental of all the qualities a wholesale merchant could have.

If our new translation of Chapter 1 is combined with knowledge and understanding of context, contrary to a literature that currently believes double entry was rarely used until the mid-nineteenth century (e.g., Dobie and Oldroyd, 2020; Yamey, 1949), it is clear that double entry was the method used by all the wholesale merchants and the banks operating in the most important commercial centre in Europe during the fourteenth and fifteenth centuries (Braudel, 1984): the Venetian wholesale marketplace. Double entry was used by those merchants as part of an organised system of keeping records. Both double entry and the record keeping system of which it was part had, as their primary goals, (1) maintaining control over debt, both to avoid unnecessary losses and to grasp opportunities through efficient working capital management; (2) to verify the validity and veracity of the actions undertaken and recorded by distant agents, factors, and partners; and (3) to meet any need for supporting evidence (Sangster, 2022).

There are several reasons why clarifying what Pacioli wrote is important. Firstly, doing so removes confusion and pointless speculation concerning what Pacioli viewed as essential qualities and makes it clear that these were qualities of a merchant, not a bookkeeper, nor an accountant; and his use of the money of account for wholesale trade makes it clear that he is describing and writing for wholesale merchants, not all merchants. This means that it is the context surrounding wholesale trade in Venice that needs to be considered if seeking an explanation for why double entry was used.

Secondly, it is important because it reveals that Pacioli was not saying that a merchant had to know how to do double entry bookkeeping. He was saying that a merchant who sought to operate in the Venetian wholesale marketplace had to conform: keep all his affairs in good order and his account books in double entry. Most operating in that marketplace would have had businesses of a size large enough to afford to employ someone skilled in the method, typically a current or former apprentice, as had undoubtedly been the case for Pacioli himself 30 years earlier (Sangster, 2021). However, any merchants who participated in person in the marketplace rather than relying on agents, would have needed to understand the entries in a double entry ledger, even if they did not personally make the entries in their own. From the evidence concerning the penmanship of extant medieval Italian account books, 25 these merchants were well-versed in the ways of double entry.

When the supporting evidence mentioned earlier is added – the fact that all surviving Venetian medieval wholesale merchant account books are in double entry and the impossibility of operating an extremely busy and vibrant credit-based marketplace unless double entry was in universal use – it can be seen why Pacioli (1494), Besta (1916), Antinori (2004), and Lane (1944, 1977) all indicate that double entry was the bookkeeping method of the Venetian wholesale marketplace, just as it was in Tuscany, and for the same reasons as in Venice; and the distant agents, factors, and partners used it as well (Lane, 1977). However, only in Venice was it built on the foundation of the ‘libro doppio’: the ledger with its journal, which Pacioli and those who followed after him taught. 26

The third and, possibly, most significant reason why clarifying what Pacioli wrote is important is to raise awareness that keeping orderly records of everything was what mattered. If all a merchant's affairs were not in order, it would be very difficult to (a) trade effectively in a credit-based economy; (b) maintain respect in the case of a dispute; (c) manipulate working capital; (d) grasp opportunities or (e) avoid unnecessary losses. Double entry was only a part of that. Both Pacioli (1494) and Cotrugli (1458) place much emphasis on this need for records to be kept in an orderly fashion. And both emphasised the importance of double entry which, as well recognised, brings order and clarity to our understanding of records created of financial transactions (Lane, 1977; Yamey, 1964). It also makes it easy to identify debtors and creditors, and the amounts involved. For a merchant, knowing what amount was involved was only the start. His other records provided evidence of the existence of the obligation, whether it was in the form of letters, promissory notes, contracts, or something else. This is what Pacioli is telling us when he writes: The third and last thing needed is that his affairs are arranged in good order, so that he can quickly obtain details of everyone concerning their debt and also [their] credit because, concerning anything else, trade has no need.

Concluding comments

Our findings should lead to new understanding of the role and purpose of using double entry in European trade during the fourteenth and fifteenth centuries, and thereafter. During the fifteenth century, being involved in commerce was the most coveted aspiration of Venetian patricians (Luzzatto, 1961), the noble families who ruled the State, for whom, for example, the existence of a merchants’ guild would have been meaningless. The State was their guild (Byrne, 2004). Pacioli's treatise was not written for small local retailers. It was written for people with access to funds and other resources, their own or belonging to someone else, who aspired to trade in the Venetian wholesale marketplace at the Rialto, and abroad. This is implicit in the money of account used in the text, the lira di grossi a oro, the Venetian money of account of wholesale and international trade. Other examples from the treatise that confirm this include the absence of any discussion of how to keep account books for a shop until Chapter 23; and the inclusion in the opening inventory of 1000 ducats in cash, which is far more than a retail merchant would have; plus jewels, precious stones, silverware, woollen clothing and cloaks of the merchant and his family, feather beds, chests of ginger, a house, and farmlands; all valued in ducats.

Being able to do business in the Venetian wholesale marketplace, where international trade took place, involved maintaining accounts in the manner of that marketplace, that is, in double entry, while also keeping orderly records of everything else. The latter was every bit as important as the former, if not more so. Pacioli published his treatise to provide merchants with instruction in how to order their affairs so that they could enter and survive in that marketplace. It was not simply to instruct them in double entry.

To this point in time, double entry's role in that marketplace has never been fully understood in the accounting history literature, nor has its apparent absence from the retail market. Instead, there is a vagueness in the portrayal of the organisation of Venetian trade in that literature, and a disbelief that double entry was particularly useful as a recording method, other than in providing organised data that could be turned into financial reports – see Yamey (1975), and Lane’s (1977) rebuttal of this perception. It is hoped that the clarity we offer of Pacioli's introductory chapter may bring realisation to this field that double entry was much more than the conduit to producing financial reports we view it as today. It was part of the toolkit of a merchant who wanted to enter and survive in the wholesale marketplace of Venice. That is a message we can take at face value from Pacioli, and one we should if we truly want to understand the origins of modern accounting that stem from his publishing of the treatise in 1494.

Despite the view previously expressed that Pacioli's text is easy to understand once transcribed, this was not our experience. When we approached an eminent economic historian, with over 40 years’ experience of working in the Venetian archives, for his views on the readability of Pacioli's language, his response confirmed our impression: This is nasty stuff for me but would be so even for a true philologist. Pacioli is a Tuscan talking about Venetian material, in a mix-up of Tuscan and Venetian dialects. (personal communication)

It is little wonder that the English translators omitted some of the text.

We endeavoured to remain as true as possible to the original text and avoided rewriting it in modern phrasing wherever we could. This explains, for example, some of the differences between our translation and the one prepared in Italian by Carlo Antinori (1990, 1994). However, such is the ambiguity inherent in Pacioli's language, there will be places in our translation with which others may not agree. Nevertheless, this study has highlighted issues with the existing translations, particularly in English, that go beyond different opinions on the meanings of words and phrases. In places, those translations are significantly misleading. They are also incomplete.

For accounting historians who have relied and continue to rely on the English translations, our analysis has revealed several examples that highlight the dangers of doing so. When this is added to a general lack of awareness in this literature of fifteenth century Venetian mercantile practice, our findings should raise significant doubts about some, if not much of what has been written concerning the nature and purpose of Pacioli's treatise. It should also raise considerable doubt about what has been written about the purpose and benefit of using double entry. Doubt not just concerning the fifteenth century but, also, early modern Europe when, as Esteban Hernández Esteve (1994) points out, merchants continued to want to know how to record transactions, not how to prepare financial statements.

Deflecting attention from these observations, some might argue that the obvious consistencies across these translations implies that they are correct, and we are wrong, no matter how difficult it may be to maintain that argument when the justification for our translation, presented in the Appendix, is considered. However, that would be to argue that they are more reliable than the translations into other languages we include here, which is unsustainable.

The overall conclusion from this analysis is that anyone using these English translations needs to refer continuously to the original text and to how it has been translated into other languages. Until such times as someone prepares a new translation into English that takes full account of the meanings of words and phrases in the fifteenth century, and of the context in which and for which the treatise was written, this is the only way in which real understanding of the nature, content, and purpose of Pacioli's treatise will be possible for anyone for whom English is their only language.

Footnotes

Acknowledgments

The authors would like to thank Massimo Ciambotti, Esteban Hernández Esteve, Anna Falcioni, Richard Goldthwaite, Marina Gurskaya, Mikhail Kuter, Nicoletta Marcelli, Reinhold Mueller, Gary Previts, Marina Ryabova; participants at the April 2021 Academy of Accounting Historians webinar, the 67th Annual Meeting of the Renaissance Society of America, the 26th Journées d’histoire du management et des organisations (JHMO), the British Accounting & Finance Association Annual Conference 2021; attendees at seminars at the University of Ulster and the London School of Economics; and Joint Editor Carolyn Fowler for her understanding and helpful advice.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.