Abstract

The emergence of an internal control system to guide operations along the Rideau Canal beginning in 1832 is examined through analysis of a book of directives (the Order Book) maintained by the lockmaster at the Isthmus lockstation. The Orders guided the work of the lockmaster and established general controls and control activities. Orders for adequate documents and records, physical control over assets and records, and proper authorization of activities were common. Orders are seen as efforts by British Royal Engineers, who were geographically removed from the oversight of the Rideau Canal Office, to discipline civilian lockmasters and to encourage lockmasters to govern themselves. Comparing the Order Book to Orders and Regulations in place in 1831 for the Royal Engineers also highlights similarities between expectations of Royal Engineers and those established for the civilian workforce under their direction, indicating a transfer of accounting technologies from the Royal Engineers to the civilian workforce.

Introduction

We examine the transfer of control technologies and labour processes from the British Royal Engineers to the civilian workforce on the Rideau Canal in the period 1832–1854 based upon a primary source accounting artefact (Francis and Samkin, 2014), the Order Book – Isthmus (hereafter Order Book). We explore how these technologies served to encourage governmentality and discipline among a geographically distributed workforce that needed close coordination to facilitate transportation on the 202-kilometre canal. This article broadens research on accounting and the military (Cobbin and Burrows, 2018) and the emergence of internal control systems and labour processes in the first half of the nineteenth century. Most historical research on accounting and the military has focused on British Navy or Army services. We extend this to show how internal controls in place at the time for the Royal Engineers were transferred to civilian workers during the early operation of the Rideau Canal. We categorize orders in the Order Book of a single lockstation according to broad categories of internal control, including the general control environment and control activities. Achieving effective internal control depends both on disciplining individuals responsible for implementing controls and having them discipline themselves to behave in a manner consistent with internal control objectives. We employ Foucault’s (1991) concepts of discipline and governmentality, and Miller and O’Leary’s (1987) on the construction of ‘governable persons’, to explain civilian employees’ compliance with internal controls. We utilize Robson’s concept of action at a distance (1992) to show how controls function when oversight is exercised remotely due to geographic distance.

Our first contribution is our identification of the transfer of control practices from the military to civilian workers in a non-war period. Our second contribution is our explicit focus on the Royal Engineers, which extends the work on accounting and the military to this branch of the British military and confirms ‘the importance of the role of military engineers in management history’ (Lemarchand, 2002: 26). Our third contribution is our assessment of a broad system of internal control practices, including the general control environment and specific control activities. For most papers on accounting and the military, control systems and internal control practices are addressed secondarily as part of broader research objectives (e.g., Black, 2015; Mayer-Sommer, 2010; Scorgie and Reiss, 1997). Furthermore, we focus on labour processes to show how discipline and self-discipline (Foucault, 1979) are fostered through the control practices, and how these controls function at a distance (Robson, 1992). We note most controls in the Order Book are intended to regulate and control human activity, rather than costs. We provide examples of how surveillance, discipline and normalization (Foucault, 1979, and Macintosh, 2005) affect power dynamics in a setting not previously explored in accounting research (i.e., an 1800s setting that relies much more on control systems and documentation than physical monitoring; for example, Walsh and Stewart, 1993).

The remaining part of this article proceeds as follows: the next section describes the context for the Rideau Canal’s construction and early operations; a discussion of principles of internal control being used by the Royal Engineers at the time follows. Relevant literature on accounting and the military and internal control is presented next. We then describe our method, and present findings and interpretations. A final section concludes and offers suggestions for future research.

Context

The Rideau Canal – construction

The connection between the Rideau Canal and the military is intimate. Planning for the canal began during the War of 1812 which recognized the need for a secure transportation corridor at some distance from the St. Lawrence River (which forms the boundary between Canada and the United States) (Legget, 1986). The canal’s purpose was to enable troops and supplies to move safely, securely and rapidly to the British Naval base at Kingston, Ontario, from which point troops and supplies could sail Lake Ontario to the heart of Upper Canada at Fort York (present-day Toronto). The Rideau Canal avoided the narrowest part of the St. Lawrence River, across which it was feared a future invasion of Canada by the United States would take place. The approximate route of the Rideau Canal was mapped out as early as 1783 (Legget, 1986), preliminary estimates were developed in 1823–1824 (Bujaki, 2015) and detailed plans and estimates were prepared beginning in 1826. The canal was built as a military undertaking ‘in anticipation of war as the tangible means by which future wartime capabilities can be delivered or as a deterrent against potential aggression’ (Cobbin and Burrows, 2018: 3).

The Rideau Canal was constructed (1826–1832) under the superintendence of the British Royal Engineers in the colony of Upper Canada (now the Province of Ontario, Canada). 1 Managing the canal’s operations required coordinating activities through 49 locks, grouped around 24 lockstations, each managed by its own lockmaster. Water levels, labour processes and maintenance activities all required coordination. A particular challenge ‘was the lack of communication between lockstations. Messages had to be carried between lockstation[s] by a person on foot, on horseback or boat’ (Watson, 2019: The Early Years, para. 4). From its opening in May 1832 until its transfer to civilian control under the Province of Ontario in 1854, the Rideau Canal operated under the auspices of the British Royal Engineers (Tulloch, 1981). Despite its military roots, the Rideau Canal ultimately transported predominantly commercial goods. While manufactured goods typically transited the canal from Bytown (now Ottawa) to Kingston, natural resources, particularly logs for the British Royal Navy, moved north through the canal. 2

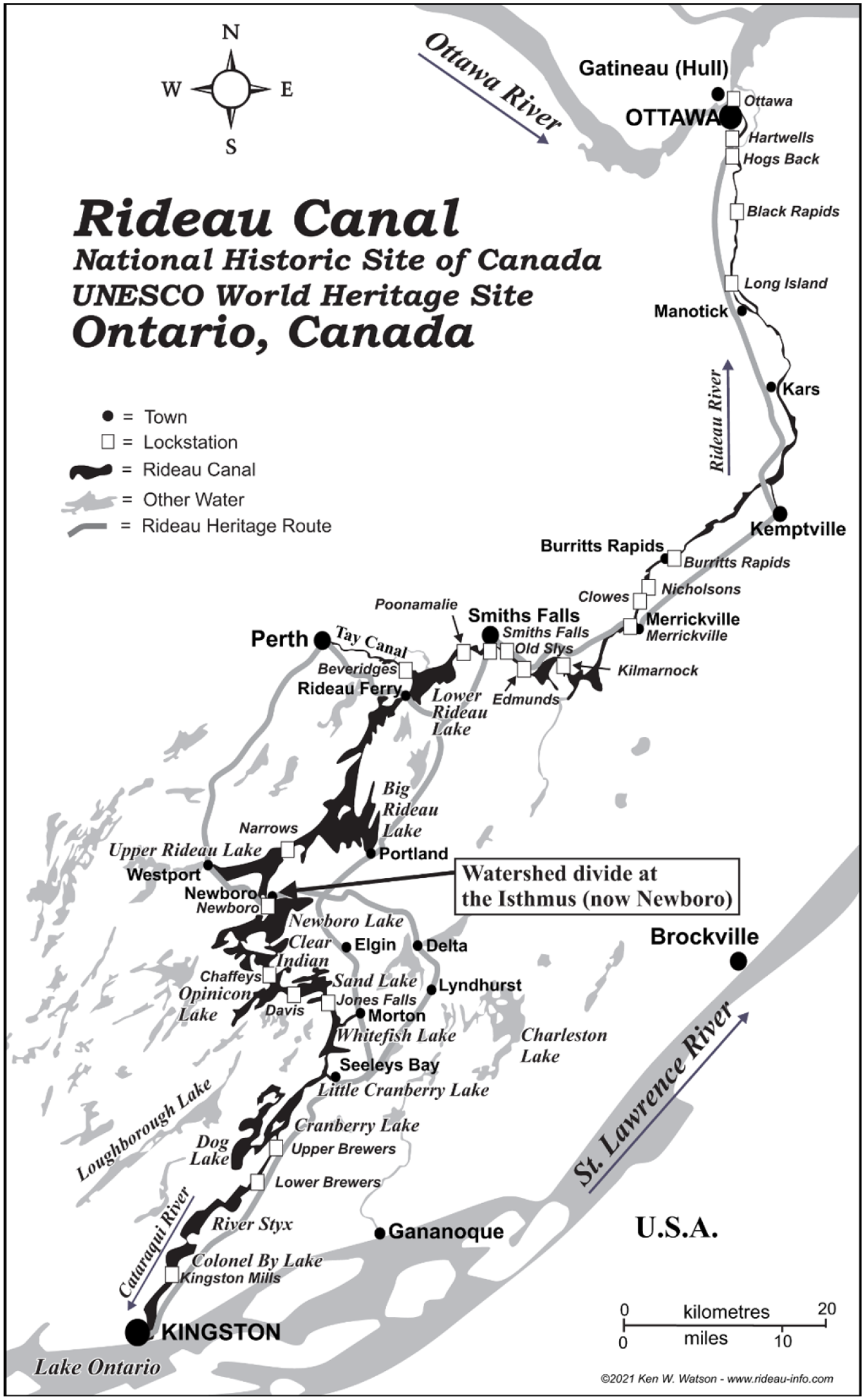

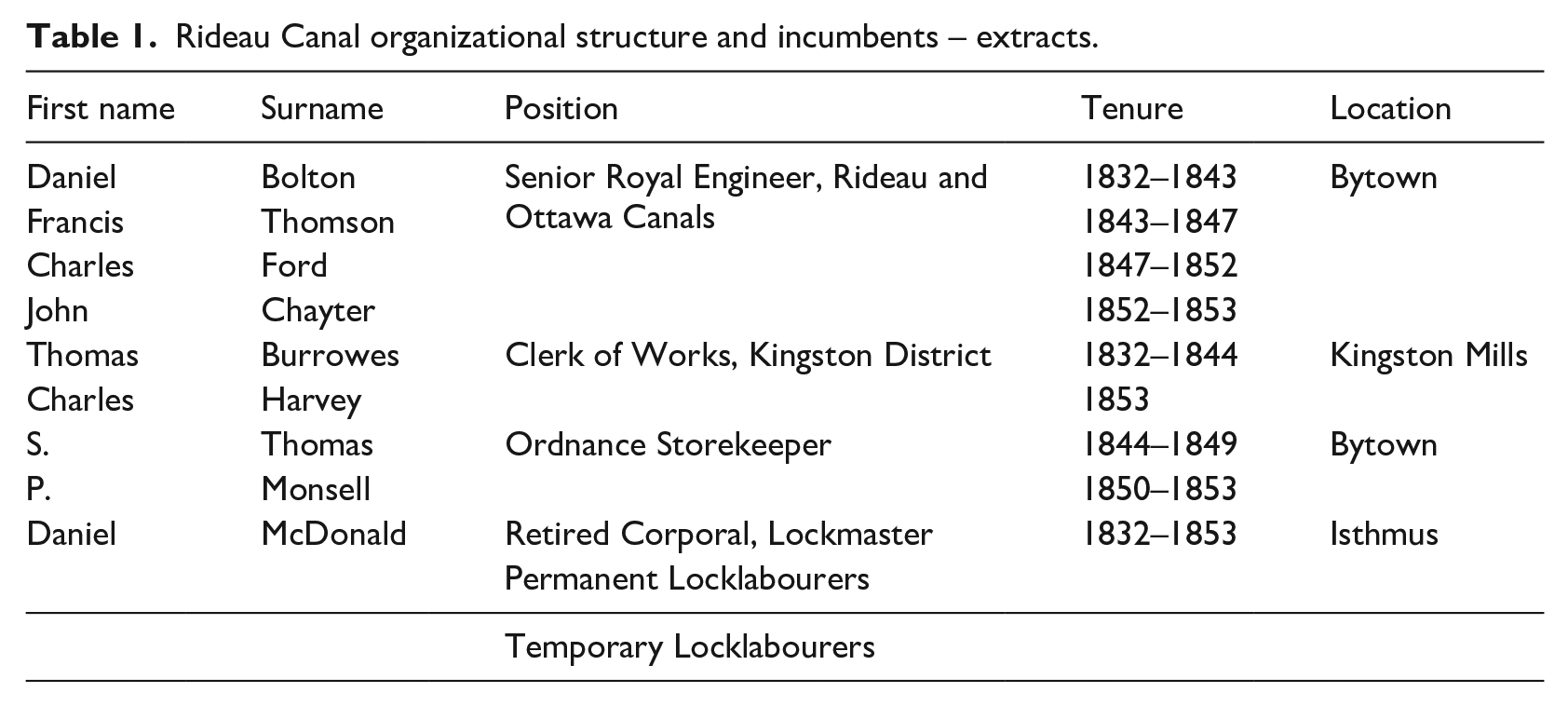

The Royal Engineers in Canada were headquartered at Quebec City. A Royal Engineers Office was established at Bytown to oversee the Rideau Canal. Captain (later Major) Daniel Bolton was Senior Royal Engineer for the Rideau Canal, John Burrowes was Overseer of Works and William Clegg was Clerk. To manage operations, the canal was divided into northern and southern sections. The northern section was managed from Bytown and the southern section from the southernmost lockstation, Kingston Mills. The watershed between the canal’s north- and south-flowing waters was at the Isthmus locksite (see Figure 1). 3 The Isthmus was overseen from Kingston Mills. Table 1 identifies individuals responsible for operations and internal control on the Rideau Canal and at the Isthmus lockstation, by position and tenure.

Rideau Canal system – Ottawa to Kingston, showing the location of the Isthmus.

Rideau Canal organizational structure and incumbents – extracts.

The Isthmus was of critical importance given its location on the watershed. A military blockhouse was built in 1832–1833 at the Isthmus for defence, one of only four built on the Rideau Canal. In addition, the Isthmus was one of seven locations designated to store supplies to support canal maintenance (Order Book, 2 March 1836). 4 Daniel McDonald, retired Corporal of the Royal Sappers and Miners, was Lockmaster at the Isthmus from 1832 to 1853, the period under study. McDonald, who had been employed on the construction of the Rideau Canal, was recommended for the lockmaster position by Lieutenant-Colonel John By, the Royal Engineer responsible for designing and superintending its construction.

In the early years of its operation, orders for the running of the Rideau Canal were given by Captain Bolton and generally written up by William Clegg. These orders covered labour processes, documentation and authorization requirements. They were transmitted from the Rideau Canal Office (RCO) at Bytown or from one of the canal’s two district offices. Orders would transit the canal from lockstation to lockstation, with lockmasters required to copy each order into an Order Book to be maintained at the lockstation (‘. . . this order to be copied in the journals of the Lockmasters, this order to be signed and passed from station to station’, 10 March 1834). Our analysis is based on the Order Book, Isthmus (n.d.; Queen’s University Archives, Fonds F01571, CA ON00239) in which orders from July 1832 to March 1854 were recorded. At the Isthmus, lockmaster McDonald was responsible for copying these orders into the Order Book. Most orders related to the canal as a whole, while some were specific to the Isthmus. An Order Book would have existed for each of the 24 individual lockstations of the canal. As far as we are aware, the Order Book, Isthmus is the only one to have survived.

The Rideau Canal – objectives and control

The British Royal Engineers were charged with governance and management of the Rideau Canal. As noted, the canal was constructed with the primary objective of offering a secure water link between Ottawa and Kingston to enable the movement of troops and supplies should the United States try to invade Canada. A secondary objective for the canal was to generate a profit based upon tolls for water-based transportation of goods and settlers (Legget, 1986; Tulloch, 1981). These broad objectives were to be implemented throughout the navigation season in Canada (usually late April to November). We examine how general controls and control activities for the canal were manifest in the Order Book and consider how control was to be achieved at a distance through discipline and governmentality. We undertake this examination in the context of the controls governing the activities of the Royal Engineers at the time, as documented in Orders and Regulations for the Guidance of the Corps of Royal Engineers and Royal Sappers and Miners at Home and Abroad (Office of Ordnance, 1831, hereafter referred to as Orders and Regulations).

The Royal Engineers’ Orders and Regulations

The British War Office published the Orders and Regulations on 24 September 1831, while the Rideau Canal was under construction under the superintendence of the Royal Engineers. Once the canal opened on 22 May 1832, the canal operations continued to be overseen by the Royal Engineers. Although lockmasters and lock labourers were civilians, many had previously been involved in the canal’s construction and many lockmasters were former members of the British military. Thus, the Orders and Regulations served as a codification of practices – many of them control practices – in effect for the Royal Engineers during the early years of the canal’s operations.

The Orders and Regulations (1831) informed, directed and constrained the activities of all Royal Engineering officers: The Master General having approved of the following Orders and Regulations for the guidance of the Corps of Royal Engineers and Royal Sappers and Miners, desires that every Officer belonging to those Corps shall provide himself with a Copy of them; that he shall make himself thoroughly acquainted with their contents; and that no deviation from them shall be allowed. (p. 1)

The Orders and Regulations (1831) are organized into 30 sections and 42 accompanying appendices, covering a wide range of circumstances. The orders set out the frequency, format and types of paper to be used for various reports to be prepared and submitted (half-yearly reports, monthly reports, estimates); requirements for handling official correspondence and books (timely acknowledgement of receipt of correspondence, preparation of duplicates, informing officers of new orders relevant to their activities); and specifics in terms of formatting replies (each subject requires its own separate letter, the paragraphs need to be numbered, and signatures are to be ‘in a clear and legible character’ (Orders and Regulations, 1831: 26)). The orders also include requirements for the recording and retention of various types of documents (‘All Official Letters, Reports, Returns and Vouchers . . . to be entered in proper Books, and preserved in the Office at each Station . . . All Circulars, General Orders, or other Official Letters, permanently affecting the routine of business are to be kept in Books, separate from the mass of General Correspondence, so as to be of easy reference’ (Orders and Regulations, 1831: 28–29)). This last requirement reflects the compilation of orders in the Order Book – Isthmus, the basis of this study.

Literature review

Accounting and the military

Cobbin and Burrows’ (2018) review of papers on accounting and the military calls for additional research in this area. In particular, they identified only 10 articles addressing accounting and the military in peacetime. There is also a paucity of research on the use of internal controls in the early nineteenth century. We extend work in these areas using a single-site case study to examine internal controls during the early peacetime operation of the Rideau Canal. We focus on a microhistory of the Rideau Canal based upon the Order Book, to examine how the establishment of controls over labour and work processes contributed to control over individuals from a distance and the transfer of accounting technology from the Royal Engineers to the canal’s civilian workforce.

Cobbin and Burrows (2018) note prior research on accounting in the military during peacetime focused on ‘four accounting themes – procedures, costing, disclosure and efficiency’ (Cobbin and Burrows, 2018: 13). We add to this coverage by examining workplace internal controls and oversight practices during the first decades of the Rideau Canal’s operation. Cobbin and Burrows (2018) argue ‘Advancements emerging from the demands of the military during peacetime are likely to emerge in a measured manner unaffected by the urgencies of war and so may have lasting impacts’ (p. 11). We assess developments in accounting (broadly defined to include internal control and reporting) in the context of the Rideau Canal through orders documented in the Order Book. This examination is informed by Foucault’s (1991) concepts of discipline and governmentality, as well as Robson’s (1992) concept of action at a distance. Cobbin and Burrows (2018) note that ‘The linkages between accounting, the military and war stem directly from the centrality of logistics to the ongoing maintenance of the military and the day-to-day prosecution of war, and accounting’s position within that realm’ (p. 2). Ohl (1994) emphasized that ‘effective management systems that include both soldiers and civilians [are those] that successfully organize . . . supply links’ (p. 3).

Foreman (2002) focused on the transfer of accounting technologies between government military factories in Australia in 1910–1916. Regarding the transfer of technologies, Foreman (2002) noted ‘technology transfer may . . . include useful knowledge, including systems and procedures, and more specifically accounting systems and procedures’ (p. 34). Foreman concluded that accounting systems developed based on both the internal organizational contexts and external environments in which they were situated. The embeddedness of accounting systems is a theme picked up subsequently by Cinquini et al. (2016) and Djatej and Sarikas (2009). Foreman, building on Carnegie and Parker (1996), observed the transfer of accounting technologies between military factories was facilitated by ready access to, and a clear understanding of, the originating system. Furthermore, Black and Edwards (2016) noted that individuals moving from government to industry or vice versa were frequently responsible for ‘transferring accounting technology from one to the other’ (p. 307).

Within research on accounting and the military, a number of insights on audit and control practices have been documented. These observations have appeared within papers that have a broad focus on accounting. In contrast, our article is the first in this area to examine internal controls in depth. Scorgie and Reiss (1997) identified the importance of prior naval experience on accounting and control over inventory in the first penal colony in Australia in 1788. Specifically, they noted the first Commissary in the colony ‘drew on his prior experience in the navy and applied it to the management of the government store’ (Scorgie and Reiss, 1997: 66). A particularly strong feature of the naval system for control over inventory (or stores) was that no items could be issued without authorization. Mayer-Sommer (2010) examined the case of Isaac Henderson, a civilian Navy Agent and government disbursing officer during the US Civil War who was accused of defrauding the government. Mayer-Sommer identified a lack of segregation of incompatible duties in disbursement processing, noting clerks who approved disbursements also audited these disbursements. He concluded the control system was focused on maintaining an appearance of effective, efficient operations and functioned primarily as a legitimizing activity. We next turn to a brief review of literature on internal control.

Internal control

A brief history of internal control

Prior research provides some indication of the origins and evolution of accounting controls. Jones (2008) finds evidence of the ‘general concept of internal control and specific principles (such as authorisation, division of responsibility and observation) [being] well-entrenched in medieval England’ (p. 1056). He describes basic control activities in the thirteenth century suggestive of defined areas of responsibility, and expectations for documentation, authorisation, segregation of incompatible duties and safeguarding assets.

Cobbin and Burrows (2010) note that prior to the Audit Acts of 1832, 1846 and 1866, the focus in examining public expenditures in Britain was on stewardship of public funds, rather than efficiency or effective administration. Prior to 1846, these requirements focused predominately on checks that ‘departmental financial procedures had been followed; all expenditures were correctly authorised and total spending had not exceeded the total amount appropriated by parliament’ (Funnell, 1997: 16). Black and Edwards (2016) also noted an emphasis on authorization.

Technologies of audit or verification were also identified in prior research. Funnell (1997) noted that public sector audit requirements arose beginning in 1832 in the British Navy, then migrated to the British Army. Black (2015) identified auditors’ ticks on paylists and found that when British Army accounts were audited by the Office of Military Accounts, ‘each entry was supported either by an auditor’s red tick or observation’ (p. 73). Black and Edwards (2016) follow the careers of two civil servant accountants who worked together in the War Office of Victorian Britain. The accountants helped develop accounting practices in the 1860s such as tracking production costs for military expenditures and assessing make or buy decisions for guns supplied by the Royal Gun Factory. In describing the transfer of accounting practices from the private sector to the public sector and vice versa, Black and Edwards noted audit activities were common, but audit reports were frequently confined to the single word ‘Examined’.

Many military control procedures in the late-eighteenth and early nineteenth centuries focused on controls over assets (including inventory or stores). Scorgie and Reiss (1997) noted the importance of controls to manage inventory during the establishment of the first penal colony in Australia. Black (2015) noted many non-officer members of the British Army possessed the literacy and numeracy skills needed to keep detailed clerical records, including over stores, as required following financial reforms in the late 1700s designed to enhance parliamentary control over the military. Heier (2010) identified the importance of protecting and rebuilding railway assets during the Civil War in the United States. Djatej and Sarikas (2009) observed extraordinarily strict recordkeeping in Soviet accounting during World War II was part of a focus on protecting assets, needed due to shortages of raw materials and resources.

Schoderbek (1994) notes trial and error was relied upon in 1801–1802 to refine administrative and record keeping practices associated with the Land Act of 1800. Some checks and balances were used by land officers to detect errors, including preparation of duplicate receipts sent to the Treasury Department (‘Treasury’) and preparation of certificates of payment by Treasury. While individual land offices provided some internal control, oversight by Treasury was seen as ‘critical’ (Schoderbek, 1994: 210).

Internal control and governmentality

Foucault’s (1991) writings on discipline address how individuals come to discipline or control themselves and their activities. In this way, disciplinary technologies (Graham, 2010) achieve ‘the submission of bodies through the control of ideas’ (Foucault, 1991: 102). Governmentality (Foucault, 1991) is ‘the mentalities, rationalities and techniques through which subjects are controlled or governed’ (Gomes et al., 2014: 90). Governmentality is thought to function through mechanisms making individuals and their actions visible to those able to discipline bodies into ‘governable people’ (Foucault, 1991; Miller and O’Leary, 1987). Graham (2010) defined accounting as an ‘assemblage of calculative practices used to produce periodic reports within a relationship of accountability’ (p. 25). Accountability relationships imply differences in power between individuals and those to whom they report. Neu and Heincke (2004) applied governmentality concepts to subaltern or subordinate groups. Among their definition of ‘subordinate’ are groups subordinated in terms of their office or position. Given strict hierarchical relationships within the military, concepts of governmentality may be particularly apt in describing internal control in such environments.

Internal control from a distance

According to Miller and Rose (1990), accounting internal control systems ‘allow knowledge of distant sites to be mobilised and brought home to centres of calculation’ (p. 9), which facilitates control at a distance (Robson, 1992). Gomes et al. (2014) note ‘it is the quantitative orientation of accounting which facilitates the use of inscriptions, including accounting writing, numbers, lists and reports, in the form of accounting documents, to assist in enabling action at a distance’ (p. 91). Mouritsen et al. (2001) understand inscriptions as all narratives and numbers by which individuals are subject to calculation and discipline. Gallhofer and Haslam (1996) consider the form and structure of accounting statements and reports, including the use of prescribed formats, headings and columns as devices that make performance visible and subject to discipline. Graham (2010) describes ‘banal technologies’ as ways of knowing an individual and having individuals discipline themselves. Mennicken and Miller (2012) call these ‘technologies of calculation’ and note the political nature of these technologies which are used for ‘intervening in economic and social life’ (p. 6). Neu and Heincke (2004) consider reporting requirements a ‘technique of governmentality’ which translates policies into administrative practices and result in indirect power.

We next describe the method by which we explore the transfer of internal controls from the Royal Engineers to civilians in the context of the operation of the Rideau Canal in a manner that promoted discipline and governmentality at a distance.

Method

Beginning with an ‘opportunistic discovery’ (Francis and Samkin, 2014; Freeman, 1986) of an accounting artefact as part of a larger project on the Rideau Canal (Bujaki, 2010, 2015), we expanded our exploration to consider the social and organizational context in which the Order Book was situated. 5 We concur with Francis and Samkin (2014) that ‘Artefacts are a rich source of historical information as they provide insights into the lives of individuals and organizations’ (p. 410). We undertake a microhistorical study of this artefact (Hollister and Schultz, 2007; Samkin, 2010).

Hollister and Schultz (2007) use microhistory in connection to the records of two stores in the 1790s. They focus on issues of power and control among the residents of a rural community, including unequal treatment of residents at the stores based on gender. They also describe basic accounting relating to inventory and customer accounts receivable. Samkin (2010) describes microhistory as using a reduced scale of observation, such as an event or locality to help convey the lived experiences of everyday life to readers. He uses microhistory to assess the transfer of British-style accounting technology in the late-eighteenth and early nineteenth century by John Pringle of the East India Company. A microhistory approach allows us to focus on the local context of the Rideau Canal, specifically the Isthmus lockstation, in the early years of the canal’s operation. It also allows us to examine the context in which lockmaster Daniel McDonald worked and to observe the transfer of control systems and labour processes from the Royal Engineers to civilian canal workers.

We obtained a copy of the Order Book and had it transcribed from its original handwritten form to a typed, digital copy, preserving the original formatting and pagination to the extent possible. 6 The Order Book is the focal point for our microhistory; it provides insight into the lived experiences of individuals involved with the Rideau Canal from 1832–1854. The Order Book was subject to multiple close readings (Amernic and Craig, 2006) by the authors. We focused on identifying internal control measures, labour processes, and administrative and reporting practices on the Rideau Canal. A research assistant worked under our guidance to classify each order according to type of control practice. To assess the canal’s internal controls, labour processes and administrative practices, compared to similar practices at the time, we also examined a copy of the Orders and Regulations (1831) and identified similar orders.

Findings and interpretation – Order Book

Order Book, Isthmus – Overview of contents

The Order Book was maintained by the lockmaster at the Isthmus lockstation. It consists of a single leather-bound book with 246 pages. The first entry is dated 27 July 1832 and the final entry is 31 March 1854. Generally, one or two orders are recorded per page. The Rideau Canal officially opened 22 May 1832, therefore the Order Book includes orders issued from almost the inception of the canal’s operations until responsibility for the canal was transferred to the Province of Ontario. The pages in the Order Book are hand-numbered sequentially beginning at 1 and continuing until 175; after this point, no further pages are numbered. The Order Book has an ‘Index of Orders’ (i.e., a table of contents) at the beginning of the book. This index includes a chronological listing of each order, the year and date of its issue, by whom the order was given, the purpose of each order, and the page or folio number on which the order is written. This unpaginated index continues for 15 pages before page 1 of the Orders is introduced. The Index of Orders continues for three additional pages at the very back of the book.

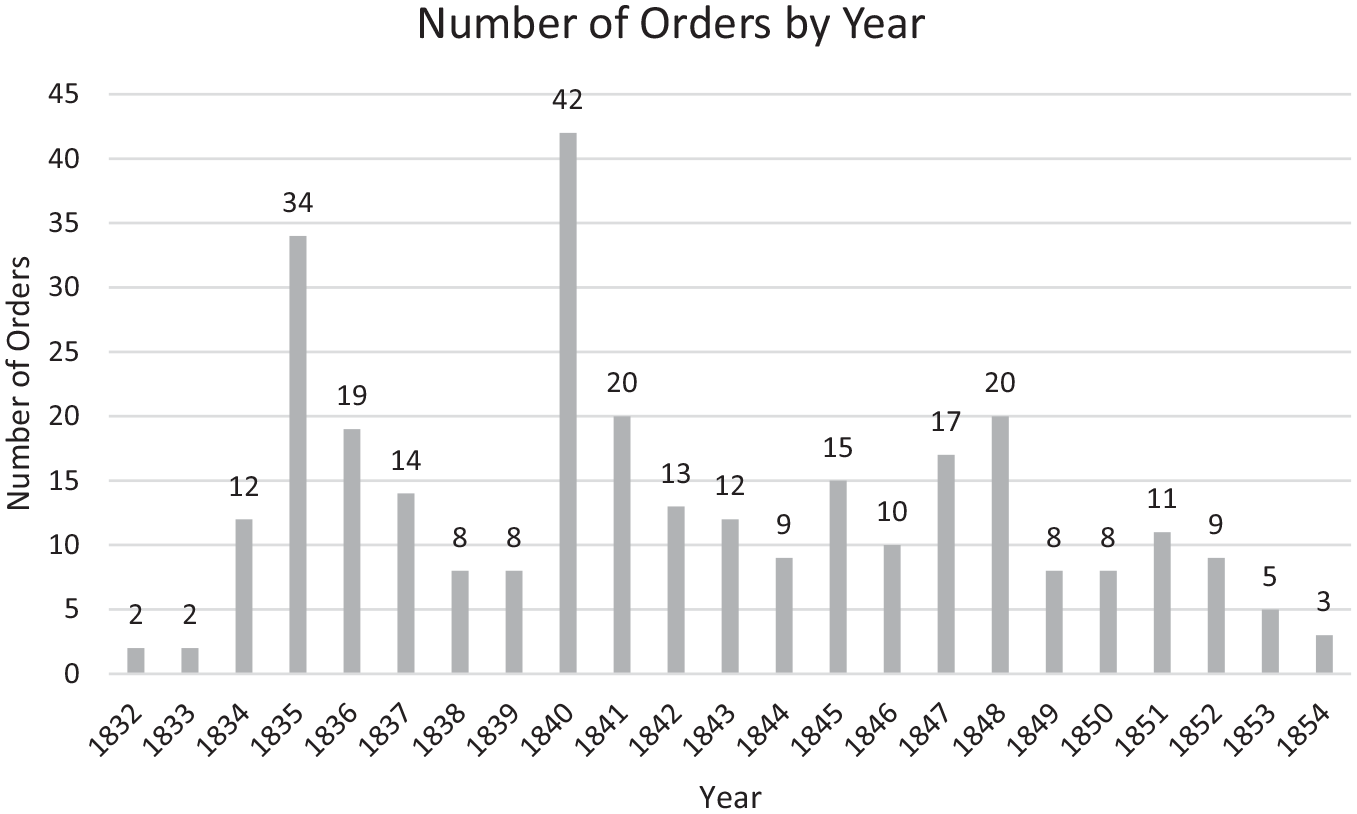

The Order Book contains 301 orders spanning the years 1832–1854. Figure 2 illustrates the distribution of orders by year. An average of 13 orders were issued each year; however, the years 1835 and 1840 had significantly more orders, 34 in 1835 and 42 in 1840. The large number of orders in those years relate to several maintenance and staffing issues experienced. We also examined the distribution of orders written each month. The greatest number of individual orders were issued in April and November, corresponding to the canal’s seasonal opening and closing.

Number of orders entered by year.

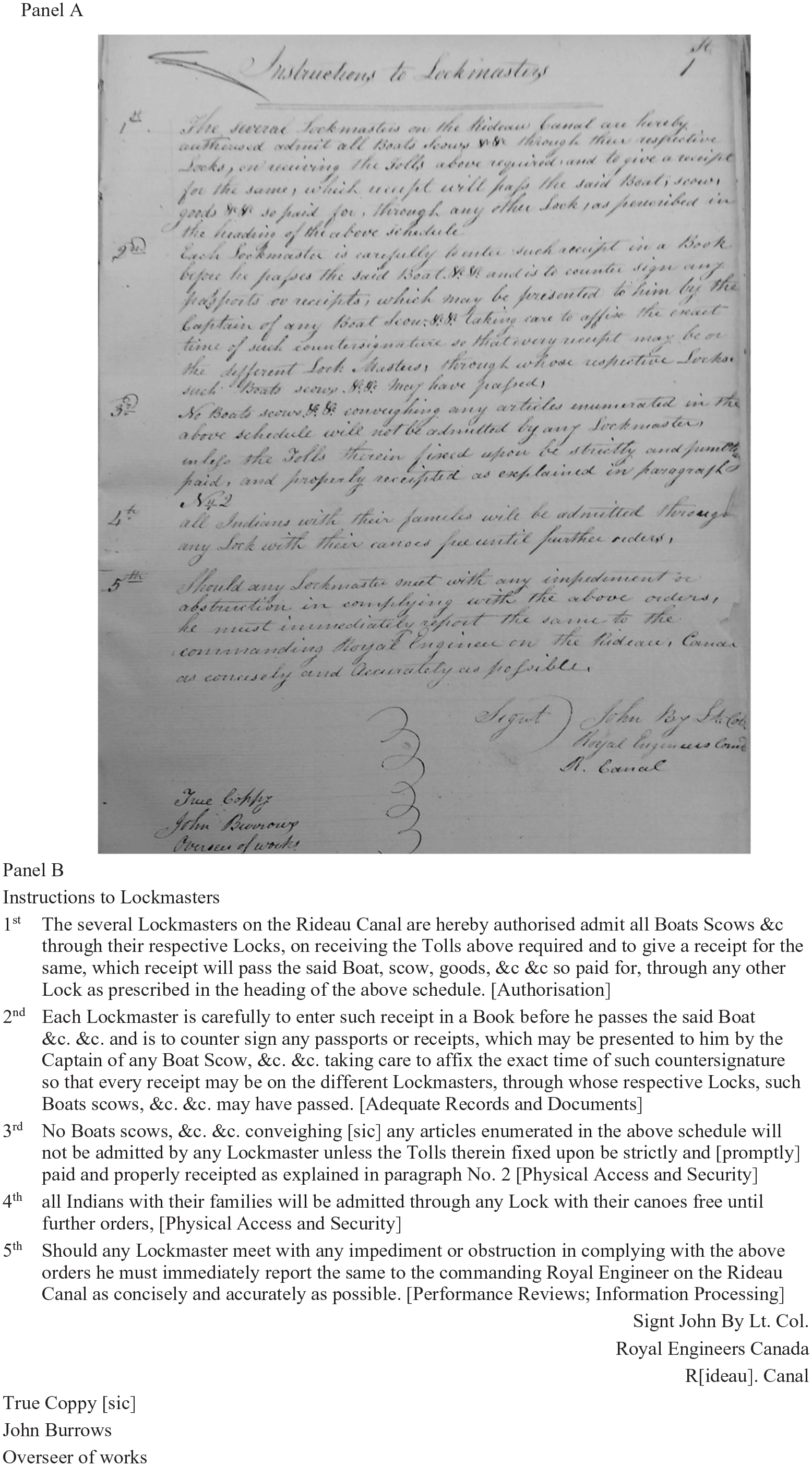

The first order in the Order Book is not dated. It is signed by the Royal Engineer who superintended the canal’s design and construction, Lieutenant-Colonel John By. As By was recalled to England in May 1832 to answer concerns related to overspending during the canal’s construction (Legget, 1986; Mark, 1998), the order ‘Instructions to Lockmasters’ is the only order issued over his signature. This order sets out five general instructions all lockmasters are to follow. Figure 3 presents an image and transcription of this order. The order addresses collecting and recording tolls from boats or scows, issuing receipts, granting free passage to Indians and their canoes, and reporting any challenges faced to the commanding Royal Engineer. 7

Panel A: Original image of ‘Instructions to Lockmasters’. Panel B: Transcription of ‘Instructions to Lockmasters’ [relevant control activities].

Orders by internal control classification

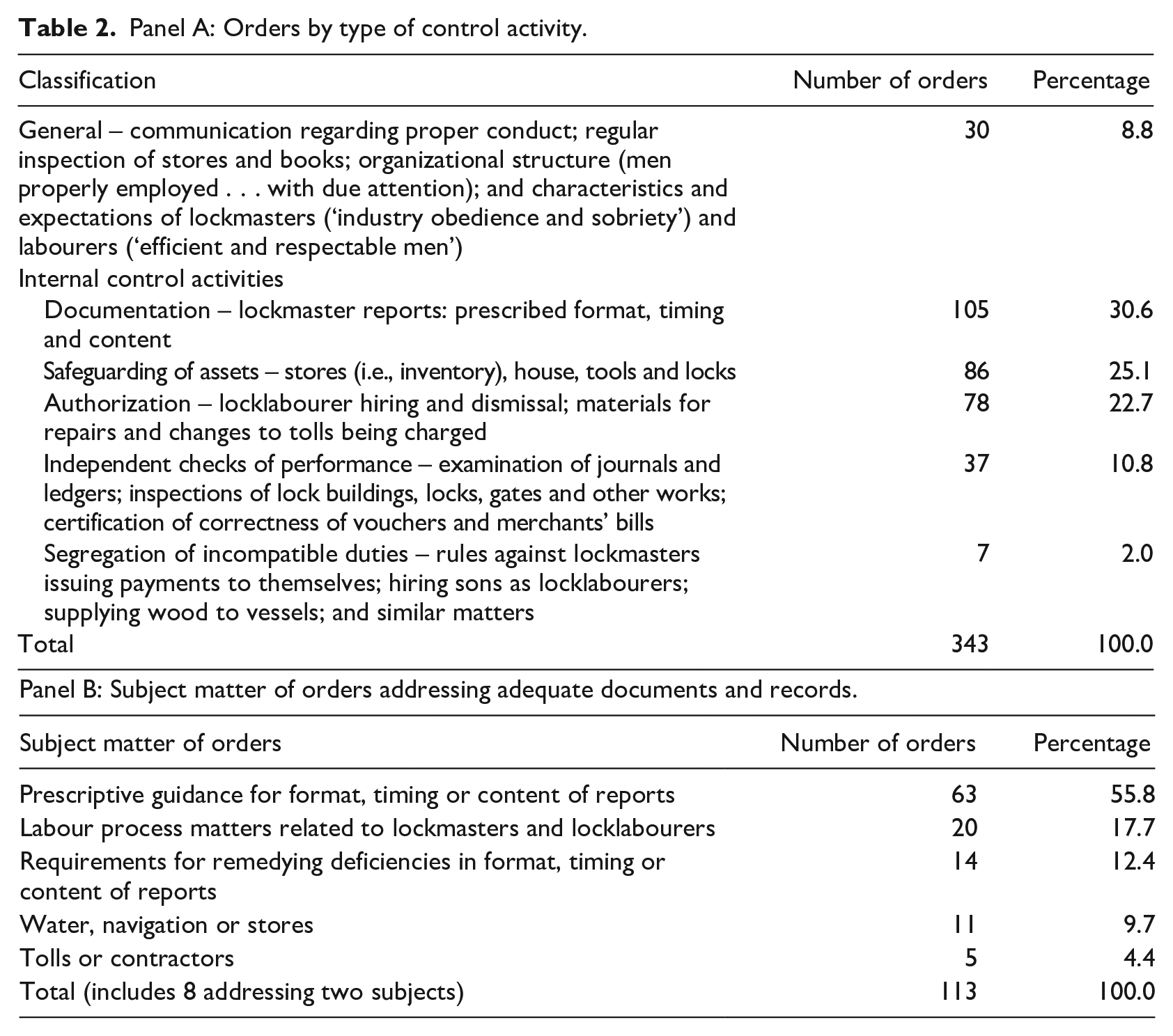

Each of the orders in the Order Book was classified according to whether it addresses general controls or one of five internal control activities (documentation, safeguarding assets, authorization, independent checks of performance and segregation of incompatible duties). These classifications parallel the groupings used by Jones (2008) to categorize controls used in medieval Britain. 8 Table 2 provides an overview of orders by internal control classification. Some orders address several internal control activities, so are included in multiple classifications.

Panel A: Orders by type of control activity.

General controls are addressed in 30 orders (Table 2, Panel A). Over 100 orders address documentation (Table 2, Panel B). This focus on documentation is not surprising as the Order Book covers the canal’s initial operating period when expectations for what information to collect and communicate were developed. The second largest category of orders addresses safeguarding assets including stores (i.e., inventory), tools and the locks. Additional orders address authorization, independent checks of performance and segregation of incompatible duties. We elaborate on the general controls next. Internal control activities are addressed below in a separate section.

Findings and interpretation – general controls

General controls address proper conduct and list characteristics and other expectations of lockmasters and locklabourers. General controls are intended to influence the ‘control consciousness’ of people, suggesting employees are to internalize these and govern themselves accordingly (Foucault, 1991). The general controls, together with the more specific control activities discussed subsequently, enhanced the ability to remotely exert surveillance, punishment, discipline and normalization (Foucault, 1979; Macintosh, 2005) over lockmasters and locklabourers. We describe illustrative orders below, grouped by category of general controls.

Communication of proper conduct and expectations

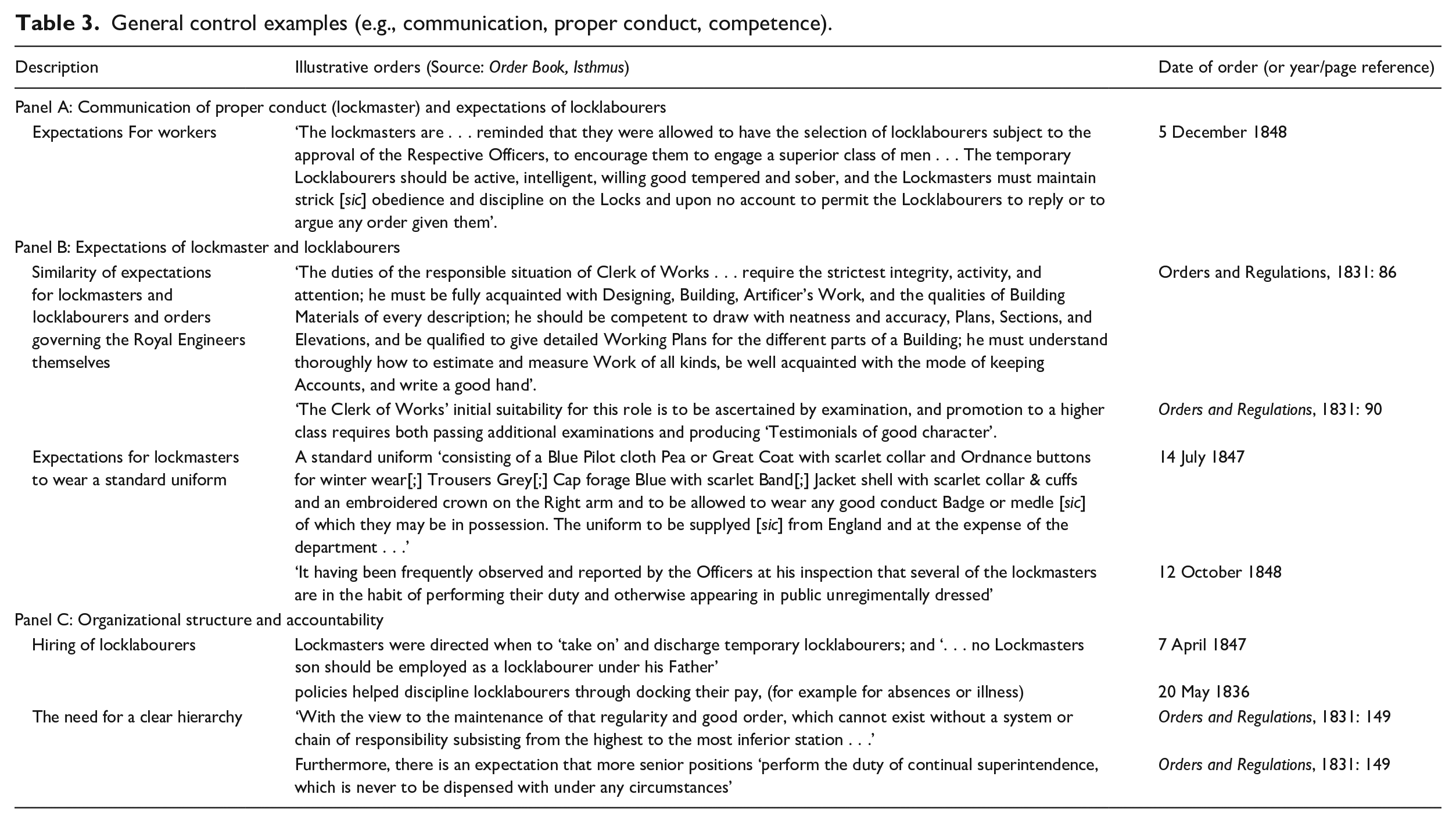

Although Black (2015) notes there were more literate soldiers in the British Army in the early 1800s than previously thought, many workers on the canal were illiterate. This was particularly true for temporary locklabourers (usually hired as workers for the navigation season only). Expectations regarding proper conduct were communicated in writing to lockmasters, who were to communicate these expectations to their labourers verbally. Orders under this category of general controls addressed matters such as punishment: the suspension of a locklabourer for ‘highly improper conduct’ (25 March 1838) and the communication of this to other locklabourers; discipline: the need for ‘the utmost vigilance’ (27 September 1841) to ensure protection of the canal works (infrastructure); normalization through the description of characteristics of desirable labourers; and prohibitions against lockmasters employing relatives as labourers or engaging in political activities. Each of these orders seeks to discipline lockmasters and locklabourers ‘at a distance’ (Robson, 1992), even when no representatives from the RCO were on site. Additional examples of general controls are provided in Table 3, Panel A. The characteristics of a ‘superior class of men’ noted in Table 3, Panel A, suggest locklabourers should be subject to both discipline by the lockmaster and self-discipline (Foucault, 1991). That example also indicates orders were intended to intervene in economic and social life (Mennicken and Miller, 2012) along the canal.

General control examples (e.g., communication, proper conduct, competence).

Expectations of lockmaster and locklabourers

Several canal orders address competence. In approving an exception when a temporary locklabourer was appointed to a permanent locklabourer’s position, the usual competencies required of permanent workers are made clear: literacy, ‘good character’ and self-discipline, comprising ‘industry, obedience and sobriety’ (15 November 1847). Concerns related to intoxication among locklabourers were not uncommon. In one order, two locklabourers were reprimanded for intoxication and for ‘using disrespectful language (interspersed with Oaths) with reference to the Officers of the Royal Engineers’ (25 May 1849). When repair work on the canal took place after the season, it was preferable temporary locklabourers be hired to assist permanent locklabourers to complete these repairs (16 November 1840). This helped ensure competent individuals completed the repairs. Numerous orders reproach lockmasters for inadequacies in maintaining their journals, as the presentation of inadequate information made it ‘extremely difficult’ (26 May 1842) to monitor their performance. Directions for maintaining their books in the future (26 May 1842) taught them how they should govern themselves going forward.

As we examine only orders issued to lockmasters, it is not possible to assess directly the involvement of Royal Engineers in governing the canal. However, there are indications of surveillance by engineering officers regularly conducting inspections of locksites and lockmasters’ records (2 March 1836). Several orders illustrate the approach taken by Royal Engineers in directing activities on the canal. For example, Captain Bolton issued a number of directives to lockmasters in 1836. His first observation expressed dissatisfaction with the lack of care taken by several lockmasters in their duties (2 March 1836). He reprimands the lockmasters and reminds them to be more disciplined in their activities and recordkeeping. In addition, he reminds lockmasters their activities are subject to periodic monitoring and disciplinary action. Generally, orders reiterate management’s expectations of workers at the beginning of each navigation season and locklabourers are reminded that ‘zeal’ and ‘devotion’ (23 March 1849) are expected of them. Failing this, even permanent employees were subject to discipline and dismissal.

Although most orders addressed the performance and behaviour of lockmasters and locklabourers, one order indicated the Rideau Canal officers were also concerned about working conditions encountered by lockmasters. In particular, the officers expressed concern about verbal abuse directed at lockmasters by individuals passing through the canal. While the officers communicated support for lockmasters in conducting their duties, they also reminded lockmasters to exercise self-discipline (be ‘decorus’, ‘conciliatory’ and ‘abstain from speaking’ (11 September 1844)) in discharging their duties. Other indications of management’s attitude towards labourers are evident in the officers’ concern for workers in two orders issued in 1847. The first addresses introducing a form of pension, while the second touches on the possibility of medical benefits. An additional order in 1851 instructed lockmasters to be ‘most particular in not permitting a [lock] gate to be moved on any account until vessels approaching the Locks have lost their head way [stopped moving forward], or are properly secured’ (4 November 1851). This order was issued following the injury of a locklabourer, which was ‘of a similar nature [to an accident which] occurred in 1842 on the Ottawa Canal by which the man lost his life’ (4 November 1851). Finally, concern for canal workers’ employment prospects was expressed in 1853, in the lead up to transfer of the Rideau Canal to the Province of Ontario. These orders indicate concern for safety, the need for assistance during the transition between military and civilian oversight of canal operations, and that good conduct and self-discipline are to be rewarded with pensions. Many of these orders regarding expectations for lockmasters and locklabourers are similar to orders governing the Royal Engineers at the time. Additional examples are provided in Table 3, Panel B.

Organizational structure and accountability

Orders in the Order Book were generally directives addressed to lockmasters as a group. Orders directed lockmasters in their work and indicated the limits of their authority, their responsibilities and the extent to which they were to be held accountable. Orders established expectations for lockmasters, served to discipline lockmasters and locklabourers, and encouraged governmentality when their work could not be observed directly. Occasionally, individual lockmasters were singled out – either for approbation or censure.

Lockmasters were responsible for sending documents or reports to other stations and the RCO. After a ‘letter of importance’ went missing, an Order was circulated that All the letters &c on the public service directed to be forwarded to any particular or from Station should be sent by persons connected with the Department and not with strangers, as they cannot be held responsible for the safe delivery of them . . . (5 October 1851)

This order helped to ensure communications were not disrupted or delayed.

Orders constrained lockmasters’ authority regarding staffing matters. Lockmasters were able to select locklabourers, subject to the complement set by the RCO. For example, the Lockmaster at the Isthmus was authorized to hire two temporary labourers (13 April 1844). However, lockmasters were not able to dismiss locklabourers (5 December 1848). Further examples of orders concerning interactions with locklabourers are presented in Table 3, Panel C (including a clear hierarchy of positions that seems to have been transferred from the military Orders and Regulations to those governing civilian workers on the canal).

Lockmasters were accountable to the Royal Engineers. When there were changes in military staff appointments, lockmasters were told to whom they should now submit their reports (17 January 1837). Thus, a formal organizational structure and clear expectations for responsibility, authority and accountability were established. In addition, written warnings were provided about the consequences of individuals failing to perform their duties. For example, ‘The [senior] Royal Engineer . . . find[s] fault with the Lockmaster of the Detached Lock at Smiths Falls and if not more attentive he will be discharged’ (24 March 1840). Furthermore, The lockmasters on the canal are cautioned against this irregularity [absence from their station without leave] and should it come under the notice of the respective officers that any deviation is made from this order a report of the circumstance will immediately be made to the master General and Board with a recommendation that the party should be removed from his station. (4 July 1844)

The Order Book communicated expected standards for lockstation staff for how they are to conduct and discipline themselves and how they are disciplined. These expectations are to be met, even when officers overseeing the canal were not present. This was done, in part, through periodic inspections of locksites and lockmasters’ records.

Findings and interpretation – internal control activities

We now turn to an examination of specific internal control activities in the Order Book. These control activities complement orders addressing general controls, and comprise adequate documentation, physical control over assets and records, authorization, independent checks of performance, and segregation of incompatible duties. We provide examples of orders relating to each of these five types of control activities.

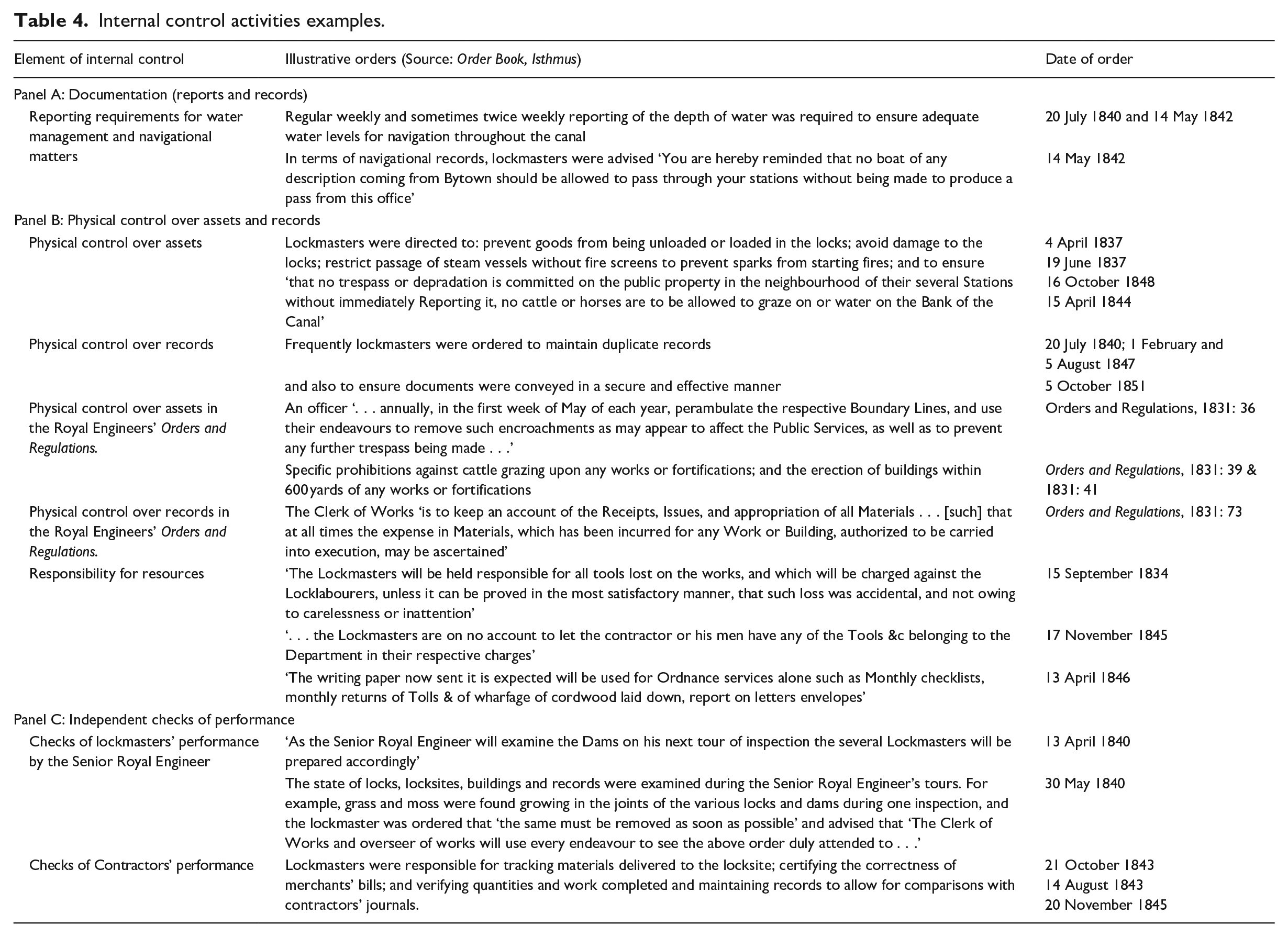

Documentation

The largest number of orders in the Order Book address requirements for adequate documents and records (for an overview, see Table 2, Panel A). Given the number of orders related to adequate documents and records, we further classified these into subcategories (see Table 2, Panel B). Over half of the orders related to keeping adequate documents and records, prescribing the format, timing or content of reports to be provided to the RCO. Human resource matters were the second most common topic addressed in orders relating to adequate documents and records, while orders requiring lockmasters to address deficiencies in the formatting, timing or content of reports were next most frequent. When combined, guidance on reporting makes up 68.2 per cent of orders focused on adequate documents and records. Significantly fewer orders address water management, navigation, management of stores, tolls or contractors. Each of these subcategories of orders is explored in additional detail below.

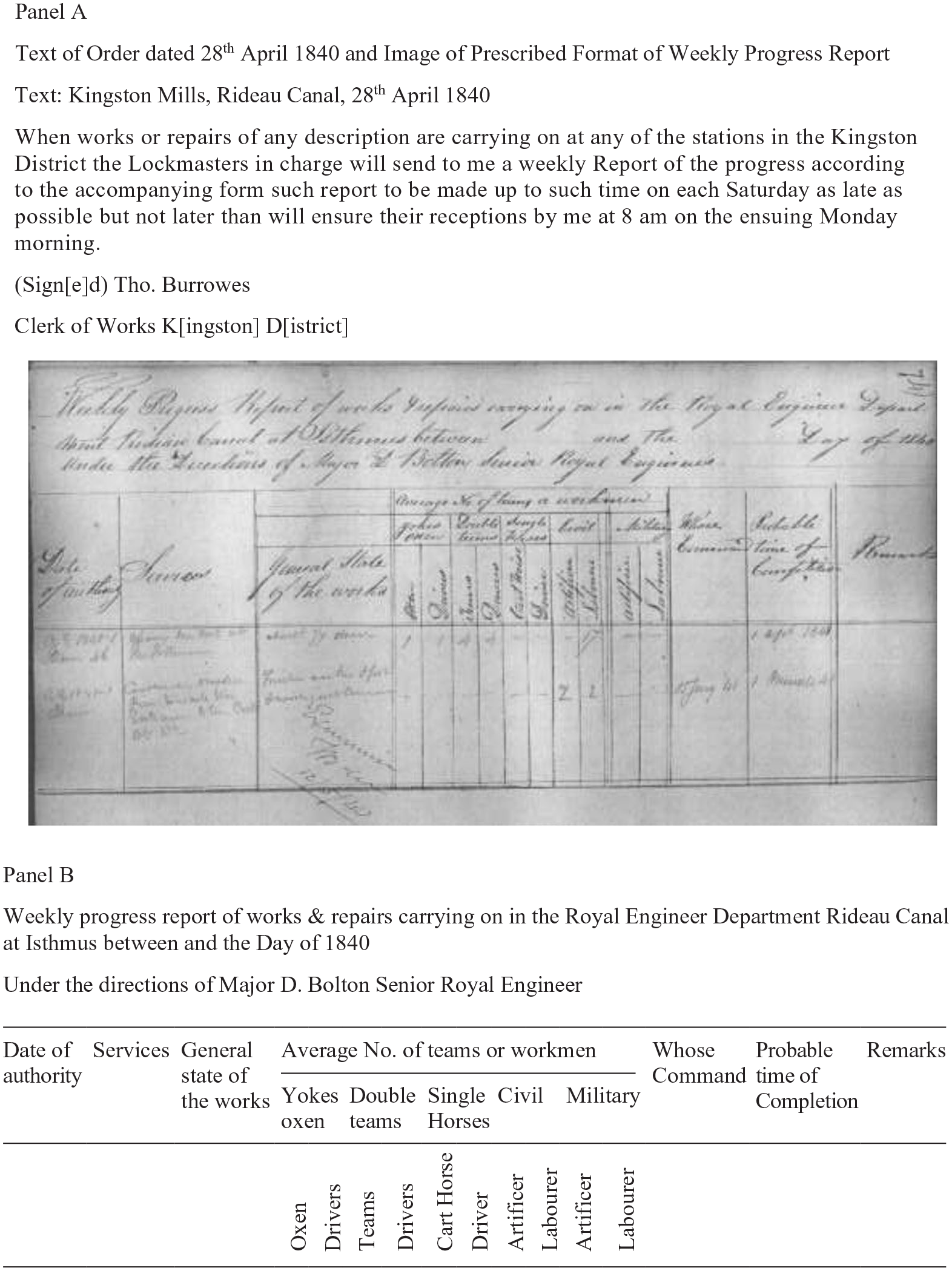

The first order recorded in the Order Book described the general nature of reporting to take place at each lockstation (see Figure 3). These general instructions were refined at a later date, for example, ‘Returns of Lock dues to be transmitted in duplicate to this office as soon as possible after each month’ (10 June 1834); ‘transmit to me with as little delay as possible Statements in duplicate made agreeable to annexed form of all receipts and expenditures of stores, materials, tools and in their respective charge’ (28 December 1834); and several examples were provided that illustrated the format in which various reports were to be prepared. From a governmentality perspective, reports sent by lockmasters to the RCO made the lockmasters’ activities visible and enabled their activities to be monitored and controlled from a distance. Standardized reporting templates facilitated surveillance and oversight of lockmasters and their activities. Gallhofer and Haslam (1996) note the visual structure and form of reporting helps make performance visible and more readily subject to normalization and discipline. The large number of orders on reporting and reporting deficiencies reflect disciplinary practices on the canal (see Figure 4 for an example of a prescribed weekly reporting format).

Panel A: Weekly progress report. Panel B: Transcript of Format Weekly Progress Report of Works.

In several instances, deficiencies in the format, timeliness or content of reports were noted in the orders, usually along with calls for greater care in reporting (e.g., 19 December 1835). Sometimes these instances referred explicitly to deficiencies, and in other cases, the deficiencies need to be inferred. For example, the order ‘The Lockmasters will be carefull [sic] in keeping the check of Horses and Oxen separate list from Locklabourers, in future, that is in separate paper . . .’ (26 March 1835) suggests lists of men and livestock had been combined. Other orders clearly indicate the required reporting format has not been adhered to (15 June 1840). Orders striving to ensure adequate documents and records are usually prescriptive, though some are remedial. These orders seek to standardize procedures and discipline lockmasters’ reporting behaviours.

Directives regarding adequate documents and records related to labour matters included the format in which the list of temporary locklabourers was to be submitted (April 1838) and notification of punishment in the form of suspension notices (‘In consequence of the highly improper conduct of Locklabourer Baldwyn the senior Royal Engineer Considers it necessary to suspend him for three months’ (25 May 1838)). Lockmasters were further directed to ‘enter the above [disciplinary action] in their journals and will read it to their several locklabourers’ (25 May 1838), thus communicating norms of proper conduct. Other reporting requirements addressed reporting annually on inventory at their lockstation (30 March 1848). Orders regulate the daily, weekly, monthly and seasonal activities of lockmasters; mandatory reports document activities to make their performance visible. Additional orders addressing reporting requirements for water management and navigational matters are illustrated in Table 4, Panel A.

Internal control activities examples.

The final category of records and documents addresses collection of tolls from boats transiting the canal and certifying work done by contractors. Requirements for adequate documents and records helped define expectations and discipline lockmasters. In addition, these requirements helped make the activities of locklabourers, lockmasters, contractors and canal users visible to, and subject to discipline by, officers at the RCO.

Comparing the above internal control activities to documentation in the Orders and Regulations for Royal Engineers, we note extensive attention is paid to the preparation and communication of estimates (Orders and Regulations, 1831: Section VIII). Section XIII also addresses contracts and contractors and specifies that officers are to request proposals from parties interested and capable of performing work or providing materials. The Orders and Regulations also anticipated problems in documentation. Section XVI required ‘All deficiency of necessary Records is to be immediately reported; and Commanding Engineers, in visiting detached Stations, are enjoined to be particular in seeing, that the Records are kept in a clear and distinct manner’ (Orders and Regulations, 1831: 76). Section XXX in the Orders and Regulations addresses the necessary books, and their size, to be maintained by each Company of Royal Engineers. Among the books listed, the most relevant to the Rideau Canal’s operations is the ‘Orderly Book’, a long book, bound or clasped, with a Sheep leather cover ‘in which are to be entered the . . . Orders of the Station’ (Orders and Regulations, 1831: 163). The technology of this book is subsequently transferred (Samkin, 2010) to the Order Book – Isthmus.

Physical control over assets and records

The second largest category of orders addressing control activities focused on physical controls over custody or access to assets or records (as noted in Table 2). Lockmasters were responsible for the maintenance of, and restricting access to, their

locksites and surrounding land. Lockmasters had custody and control over several types of assets: stores, tools (2 March 1836) and houses. Four locksites, including the Isthmus, also had blockhouses built for protection of the canal. Subcategories of orders addressing physical controls included those focused on restricting unauthorized access to the canal or other assets, protecting canal infrastructure from damage, the lockmaster’s responsibility for resources under his charge, and records of tolls collected and vessels passing through the locks.

Maintaining physical control over assets and records helps ensure canal assets are available for use when needed, not used inappropriately or by unauthorized individuals, and that proper control over records is maintained. The greatest number of these orders relate to unauthorized access to canal lands or assets. Orders to prevent unauthorized access, prohibited depositing wood for the use of steam boats on the canal (10 March 1834), ensured houses were adequately secured (18 September 1835), maintained control of tools and stores at the lockstation (2 March 1836), and addressed regaining control over canal houses when lock personnel change (14 July 1848). Additional examples of controls to ensure physical control over assets and records are provided in Table 4, Panel B.

One way to encourage the protection of assets and records is to clearly identify the individual responsible for resources under their charge. Generally, this was the lockmaster. For example, ‘Lockmaster Broad will proceed to Black Rapids and take charge of that Station Receiving over from L[ock]master Clegg the stores & Tools &c &c’ (15 October 1840). Lockmasters were also clearly identified as responsible for tools located on site (15 September 1834; 17 November 1845) and for resources such as writing paper (13 April 1846). These orders served to outline lockmasters’ responsibilities and discipline their activities.

A focus on physical control over assets and records is also evident in the Royal Engineers’ Orders and Regulations. For examples, see Table 4, Panel B. These examples are consistent with Black’s (2015) observation that control over supply was one of Parliament’s primary concerns in its efforts to exercise oversight of the British military in the late-eighteenth and early nineteenth centuries.

Authorization

Seventy-eight of the orders for the operation of the canal represent control activities addressing authorization. Most of these orders addressed labour processes, frequently the taking on, or laying off, of temporary locklabourers (e.g., 7 April 1847). Orders addressing authorization related to stores or materials were next most common, followed by orders authorizing the passage of boats through the canal. Three orders addressed tolls and one authorized a uniform for lockmasters to wear. For example, lockmasters were authorized to select temporary locklabourers within the complement of staff approved by the RCO (7 April 1847). Some orders signalled the limits of lockmasters’ authority, for example, their inability to purchase supplies (15 September 1834) or dismiss labourers (5 December 1848) without authorization. Within the limits of their authority, however, lockmasters had considerable discretion.

Lockmasters are alone responsible, that the navigation of the Canal is not unnecessarily impeded – Therefore the[y] have full authority to suspend as a temporary measure for the security [protection] of the works or in order to pass Boats &c what ever repairs may be in execution . . . (10 July 1837)

In contrast, Section VII of the Orders and Regulations for Royal Engineers addresses authorisations for work or repair, for example, commanding that where Works or Repairs may become necessary that have not been sanctioned by the Master General or Board, the Engineer must not, of his own accord, undertake to perform them . . . [and] he is on no account to incur any expense, to be charged to the Ordnance, that they have not previously authorised. (Orders and Regulations, 1831: 44)

Thus, the lockmasters enjoyed greater authority over emergency repairs than engineering officers.

Independent checks of performance

Thirty-seven orders included in the Order Book addressed independent checks of performance. Most of these related to lockmasters’ performance. This reflects the hierarchical reporting structure on the canal, under which civilian lockmasters reported directly to the Royal Engineers. Three orders address independent checks of locklabourers’ work. Other orders addressed lockmasters’ independent verification and certification of work done by contractors engaged for repair work at their locksite. Additional orders addressed independent checks of tolls, tools, buildings, inventory and upcoming inspections of books. Independent checks of performance in the Order Book include checks by Rideau Canal officers of lockmasters’ work and records, checks of locklabourers’ work by lockmasters, verification of contractors’ performance and records by lockmasters, and verification of records and activities related to resources under the control of lockmasters, such as the collection and remittance of tolls, and proper recordkeeping for inventory stores.

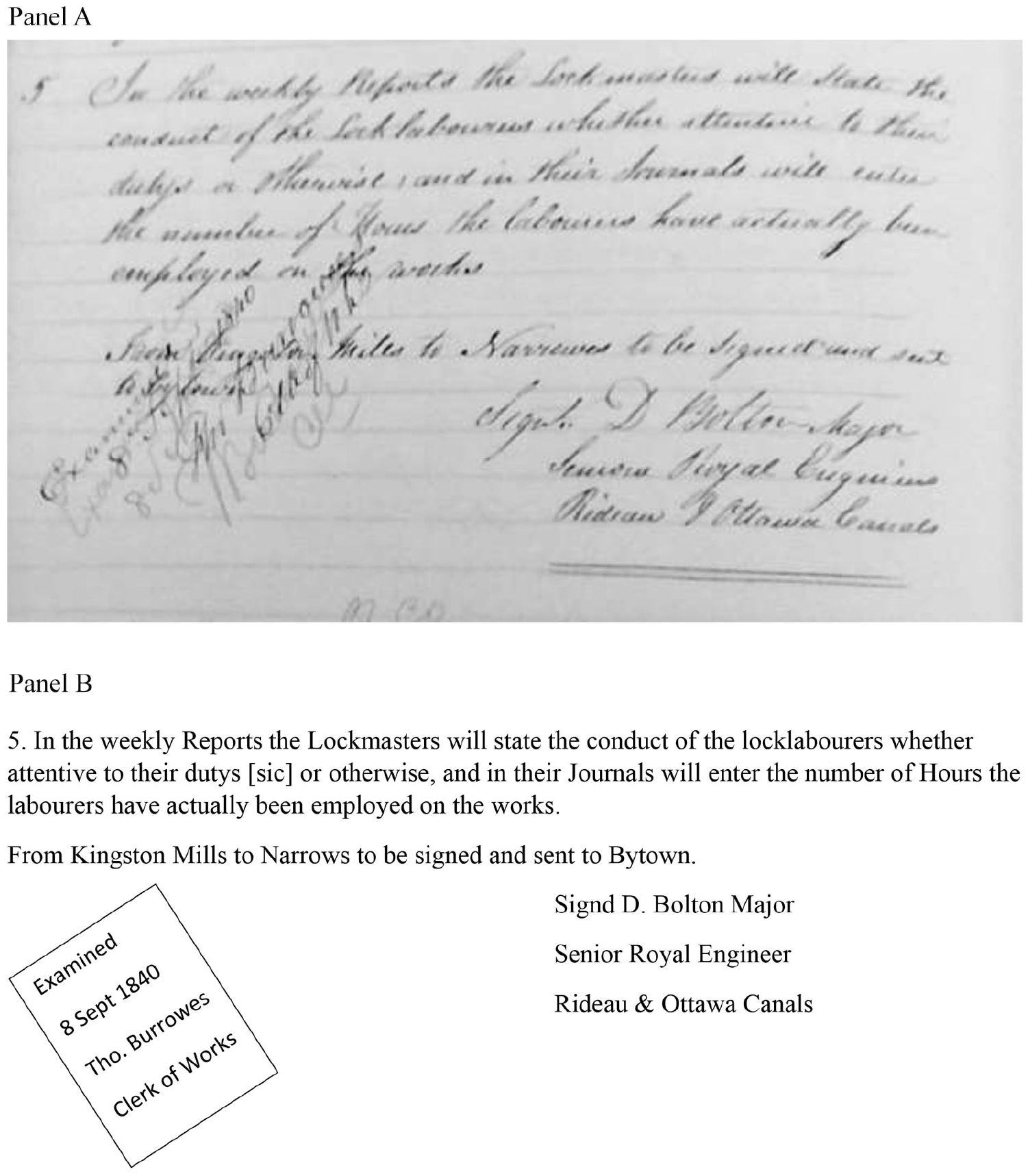

Numerous orders indicate lockmasters’ records or their locksites are to be inspected (e.g., 9 May 1835; 28 August 1840), remind lockmasters that periodic counts of stores are expected (29 April 1841), explanations (or payment) for any shortages will be required (2 March 1836) and advise lockmasters their performance is being monitored (19 August 1837). In these ways, lockmasters were put on notice their actions were subject to oversight.

Evidence of inspection was noted in the margins of several orders in the Order Book. For example, see the sideways-written marginal note ‘Examined 8 Sept 1840 Tho[mas]. Burrowes Clerk of Works’ over an order dated 14 August 1840 in Figure 5. Inspections and orders issued requiring action or remediation served as ‘calculative practices’ (Graham, 2010) to discipline lockmasters’ actions. The use of the single word ‘Examined’ as evidence of inspection is consistent with audit practices in use at the Royal Gun Factory in the 1860s (Black and Edwards, 2016). Although independent checks of performance required physical inspection of locations and records by Rideau Canal officers, they informed lockmasters’ activities even when officers were absent.

Panel A: Image of order dated 14 August 1840, showing evidence in margin of examination on 8 September 1840. Panel B: Transcription of 14 August 1840 order and marginal note showing evidence of examination 8 September 1840.

Surveillance, including independent checks of performance, took place at many levels on the canal. Lockmasters’ actions were verified by canal officers. In turn, lockmasters verified the performance of locklabourers. For example, locklabourers were to focus on their ‘public duty’ during work hours (30 May 1840), and lockmasters were to inspect the works at their locksite daily to identify and address any defects (17 March 1845). Lockmasters also conducted independent checks of work done by contractors (see examples in Table 4, Panel C), verified quantities of goods passing through the canal and calculated tolls, especially for the movement of timber or logs (22 March 1836; 24 February 1840).

Both the narratives and numbers (Gomes et al., 2014) produced or certified by the lockmasters were components of the disciplinary system of internal controls. Lockmasters were enmeshed in independent checks of performance. Their own performance was monitored and verified, and they in turn monitored and verified the work of others. Unlike early single-site factory settings such as the New Lanark Cotton Factory (Walsh and Stewart, 1993) and Wedgwood (Macintosh, 2005), the widely separated canal locksites presented challenges that were addressed using quasi-military practices to make the activities of lockmasters, locklabourers, contractors and canal users visible at a distance.

There are strong similarities between the orders in the Order Book relating to independent checks of performance and requirements in the Orders and Regulations for the Royal Engineers. For example, several orders in the Orders and Regulations address the need for documents to be examined and signed off on. In particular, Section IV of the Orders and Regulations deals with inspections. Annual inspections are required to describe ‘the actual State of the Fortifications, Magazines, Storehouse, . . . Cisterns, Aqueducts, and Buildings of every description’ (Orders and Regulations, 1831: 30). This is similar to requirements for inspections and reports on all structures and buildings at each lockstation. In addition, the Orders and Regulations require work performed by contractors to be measured and certified ‘so as to form an efficient Check against any overcharge by the Contractors, in regard to Day Work or Materials’ (Orders and Regulations, 1831: 32). Comparable requirements for lockmasters to verify contractors’ works and measurements exist in the Order Book. 9

Segregation of incompatible duties

Only seven orders in the Order Book addressed segregation of incompatible duties, making this the smallest category of control activities. These orders generally specify which activities should not be undertaken by the same individual. As the division of duties between military officers, civilian lockmasters, permanent and temporary locklabourers were rigidly determined based on their formal positions, it makes sense relatively few orders were needed to address segregation of incompatible duties. In fact, we found no orders directly addressing segregation of incompatible duties in the Orders and Regulations. Orders mandating segregation of incompatible duties on the canal addressed concerns with lockmasters both collecting and recording tolls (16 May 1836; 28 September 1836); being authorized to receive locklabourers’ wages and also making out powers of attorney to facilitate this (25 April 1837); supplying wood to steam vessels operating on the canal and having discretion over where wood could be placed on the canal (5 February 1845); as well as directly overseeing locklabourers to whom they were related (7 April 1847).

In some cases, the orders explicitly prohibited conflicting activities, while in other circumstances, restrictions were placed on the incompatible duties (lockmasters could accept wages on behalf of labourers, but were not to authorize this themselves). There were, however, some incompatible duties that could not be carried out by different individuals at the lockstation. In particular, the lockmaster’s duties necessitated him both collecting and recording tolls, as he may have been the only literate employee on site. In the absence of opportunities for segregation of some incompatible duties, and given limitations on physical surveillance due to the distances involved, other internal control mechanisms were introduced. For example, lockmasters were asked to swear oaths before a justice of the peace, or to issue affidavits attesting to the veracity of their reports, particularly relating to tolls collected. The prescribed format for such oaths included the following wording: [he] ‘. . . maketh oath and saith that the before mentioned is a true and faithful statement of the several sums received by him on account of Lock dues within the period from [blank] to [blank]’ (16 May 1836). Internal controls addressing the segregation of incompatible duties served to constrain lockmasters’ discretion and limit their opportunities to take financial or personal advantage of their positions. However, the effectiveness of these controls was limited because the actions of lockmasters were not always observable. When this was the case, the general controls which had been established served to support the control activities, by ensuring lockmasters were clear on their ethical obligations (e.g., by swearing an oath or signing an affidavit), ensuring their competence and characteristics (including literacy, sobriety, honesty and commitment to the canal), and clarifying their authorities and accountabilities.

Conclusion and directions for future research

Our study focuses on a non-war period and considers the control systems implemented to foster operational efficiency in preparation for possible military conflict. The canal was intended to serve both military and civilian uses, and the control system needed to accommodate and reflect both uses. We identify controls relevant to the general control environment, as well as more specific control activities. This singular focus on controls is unique in the accounting and military literature. We focus on the following aspects of the control system and control technologies: the transfer of accounting technologies from the Royal Engineers to the canal workforce; the control environment; authorization; examination; custody of assets; record keeping; and segregation of incompatible duties. Many orders address controls over documentation, safeguarding assets and authorization. We find relatively few controls addressed segregation of incompatible duties in the Order Book. We conclude this lack is primarily due to the strict hierarchical division of duties existing on the Rideau Canal, and the fact the Order Book is directed only at one hierarchical level, the lockmaster, whose work was to be controlled, quantified and verified. In addition, we find most controls in the Order Book are non-financial controls, intended to regulate human activity and labour processes, rather than costs.

The microhistory of the early operations of the Rideau Canal’s Isthmus lockstation provides evidence that internal controls, inscriptions, calculative practices, narratives and numbers were used to discipline the canal’s operations and employees. In particular, directives in the Order Book illustrate how lockmasters were disciplined and encouraged to discipline themselves, in a manner consistent with governmentality (Foucault, 1991). The microhistory also demonstrates how internal controls over the canal’s operations exerted their influence at a distance (Robson, 1992) at a time when communications were challenging and in a geographic space where oversight needed to be exercised from afar. Internal controls facilitated surveillance of lockmasters’ activities, and the orders provided a structure to normalize behaviour (by disciplining operations and labour processes on the canal and punishing improper conduct). At the same time, the Order Book makes it clear the effectiveness of internal control had limitations. For example, a degree of trust in the lockmasters was needed, and many orders were reissued annually, suggesting lack of compliance by some lockmasters. Other orders expressed dissatisfaction or disappointment in the actions, or inactions, of individual lockmasters or lockmasters generally.

We extend prior work undertaken on accounting and the military based on the Royal Navy and Army (Funnell, 1997; Scorgie and Reiss, 1997) to the British Royal Engineers. We focus specifically on internal control practices and find control technologies were transferred from the Royal Engineers to civilian workers on the Rideau Canal during peacetime. On the canal, civilian lockmasters were subordinate to the military officers overseeing the canal and the ‘calculative practices’ established in the Order Book construct the lockmasters as ‘subalterns’ (Neu and Heincke, 2004), subject to discipline and governmentality. Specifically, the general controls and control activities prescribed in the Order Book – Isthmus helped constrain and monitor lockmasters’ performance, inculcate discipline and encourage governmentality at a distance. The Orders and Regulations governing engineering officers served as a relevant source of administrative and control practices which guided development of controls governing management of the canal and its workers in the early years of its operation. Procedures introduced in the canal’s early years of operation reflect transference of important aspects of the internal control requirements for Royal Engineers themselves, as codified in their Orders and Regulations. For the Rideau Canal, the transfer of accounting technologies to a civilian workforce was facilitated as most of the lockmasters had previously been members of the Royal Engineers or the Corps of Sappers and Miners, thus they would have been familiar with the Orders and Regulations. This expands works done by Foreman (2002), who noted the transfer of accounting technologies to military factories during wartime, and Black and Edwards (2016) who described the transfer of such technologies between private and public sectors.

Several additional avenues for future research are suggested by these findings. Although Foucault (1991) notes discipline and techniques of governmentality can be resisted, we noted only limited evidence of resistance in the orders recorded in the Order Book. The Order Book is a direct copy of orders issued by military officers from the RCO. As such, efforts at resistance usually would not be evident in this documentary source. Some indication of resistance, however, exists in orders which mention past transgressions and call for remedial actions or revised behaviours by lockmasters. For example, in 1847, lockmasters were to begin wearing a standard uniform; this presented some disciplinary challenges and provides evidence of some resistance on the part of certain lockmasters. As our focus is on evidence of internal controls in the Order Book, we do not explore lockmasters’ strategies of resistance further. However, a more detailed investigation of resistance to internal control practices is warranted. In addition, it would be interesting to see the extent to which internal control procedures transferred from the military were maintained once the canal’s operations were transferred to civilian control in 1854. A third avenue for future research would be to examine overspending during the building of the canal. The canal cost more than four times the original estimates for its construction (Legget, 1986), suggesting some lack of control over spending; however, no rigorous accounting research has yet examined the full range of reasons for this overspending. Furthermore, Cobbin and Burrows (2018) identified the dearth of research on accounting and the military in ‘the non-state or private sector’. The Rideau Canal was built predominantly by civilian contractors under the oversight of the Royal Engineers. Business and accounting records for John Redpath, a contractor on the canal, survive. Analysis of these records could enhance our understanding of the role of the private sector in relation to the military in peacetime.

Footnotes

Acknowledgements

We thank the Social Sciences and Humanities Research Council of Canada and the CPA Ontario Centre for Capital Markets and Behavioural Decision Making Research for financial support. We thank reviewers and participants at the World Canals Conference, Athlone, Ireland, September 2018; the 10th Accounting History International Conference, Paris, France, September 2019; and colleagues in the Professional Accounting Research Group, Sprott School of Business, for their helpful comments. We are very appreciative of the transcription work done by members of the Fall 2013, HIST 2809 class on The Historian’s Craft at Carleton University under the direction of Dr Shawn Graham. This collaborative effort both built skills for the class members and greatly advanced work on this project. We very much appreciate the support of Ken W. Watson who created and maintains the website Rideau-info.com on a volunteer basis and who not only granted permission for us to use one of his maps in the paper, but who modified the map to meet our needs. We also thank Heather Leroux for her excellent work as research assistant.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article aside from financial support for the research detailed in the acknowledgements above.