Abstract

This article examines how the rise of FinTech companies has affected the power of commercial banks. Specifically, we employ comparative case studies of Kenya and Nigeria to explore how the rise of FinTechs has affected banks’ ability to exercise control over the emerging digital financial infrastructure. We find that cross-national variation in the relationship between the state and private sector in the allocation of economic resources has led to cross-national differences in the regulatory framework for digital financial services, which in turn explain differences in banks’ ability to control the emerging digital financial infrastructure. Our article makes an empirical contribution by studying how banks’ power is affected by digitalisation in under-researched middle-income country contexts and contributes to broader theoretical discussions about the changing power and purpose of banks in the digital era.

Keywords

Introduction

How has the rise of FinTechs affected the power of commercial banks? Since the Global Financial Crisis of 2008/2009, a combination of factors, notably greater regulatory scrutiny of the banking sector, has catalysed the growth of non-bank institutions employing digital technology in the provision of financial services, commonly referred to as FinTechs. When FinTechs began to enter segments such as payments and lending, which hitherto were part of banks’ core business operations, they seemed to have considerable potential to outcompete and reduce the reliance on banks (Arner et al., 2016; Clarke and Tooker, 2018).

Recent research, however, highlights that the rise of FinTechs has not ushered in the end of banking. Banks have addressed the competitive challenge posed by FinTechs by embracing digitalisation and engaging with them through partnership and competition (Brandl and Dieterich, 2023; Langley and Leyshon, 2021; Larsson et al., 2023; McKinsey, 2022).

While extant research sheds light on the strategic responses of banks to the challenge posed by FinTechs, the emphasis has been placed on cross-national similarities in explaining the continued importance of banks. A closer look, however, reveals that even in the context of the macro-trend of digitalisation, there is considerable variation across countries in the positions banks occupy in their digitalising financial systems and thus in their importance for economic development.

Against this background, this paper examines cross-national differences in the impact of the rise of FinTechs on banks and highlights how political and economic structures shape this variation. We employ comparative case studies of two African countries, Kenya and Nigeria, because the region has received only limited attention in political economy research examining the effect of FinTechs on the banking sector. While African cases have featured prominently in political economy debates about FinTechs (see Akolgo, 2023; Roitman et al., 2025) and the relationship between banks and FinTechs is often touched on in these debates, these relations have not been the central object of analysis. Specifically, we explore how the rise of FinTechs has affected banks’ digital infrastructural power resources (DIPRs), a term we use, building on Rahman (2018) and Kemmerling and Trampusch (2023) to capture corporate power flowing from financial institutions’ control of the emerging digital financial infrastructure. Given that infrastructural control provides an important basis for the exercise of political power as key societal agents rely on it (Abels, 2024; Valdez, 2023), getting a better understanding of the impact of the rise of FinTechs on banks’ DIPRs will tell us about both their ability to exercise political power and the purpose of banks in the era of digitalisation. Our analysis reveals that cross-national variation in the relationship between the state and private sector in driving economic development has led to cross-national differences in the regulation of digital financial services, which in turn has led to cross-national differences in banks’ ability to control the emerging DIPRs. We argue that while banks in both Kenya and Nigeria have been empowered in absolute terms by increasing their DIPRs, FinTechs’ relative gains vis-à-vis banks in DIPRs have been greater in Kenya than in Nigeria.

Our paper speaks to broader theoretical discussions about the changing power of banks in the digital era. With the increasing digitalisation of the financial sector, the boundaries between FinTechs and banks become increasingly blurred, and so do the notions of structural power, which is based on the contribution of a firm to economic growth, and infrastructural power. The structural importance of banks for economic development also increasingly flows from their control of DIPRs. We also make an empirical contribution by shedding light on the political impacts of digitalisation on banks in middle-income countries, which are under-researched.

The next section reviews the existing literature on the impact of the rise of FinTech on banks, underscoring the additional insights we might gain from paying closer attention to cross-national variation in political and economic structure. Next, we introduce our argument about the impact of the public–private balance in finance on banks’ DIPRs. In the sections that follow, we present our comparative case studies of Kenya and Nigeria. The final section concludes.

Revisiting the impact of FinTechs on the power of banks

From the late 2000s, FinTechs’ entry into core banking areas like payments and lending was increasingly viewed in academic and policy circles as a significant competitive threat to traditional banks. Two factors allowed FinTechs to reduce the costs of financial services provision and thus to compete effectively with incumbent banks: Their business models, centring on the exploitation of technology and data, and less stringent regulation than for the banking sector (Arner et al., 2016). Policymakers and development organisations also welcomed the rise of FinTechs in Developing and Emerging Economies (DEEs) as they were seen to increase financial inclusion (Bernards, 2019; Gabor and Brooks, 2017).

The answer of recent research to the question of whether banks have become obsolete with the rise of FinTechs is a resounding no. Across the globe, banks continue to play an important role, providing credit for the private sector in emerging economies (Narayanaswamy and Miryugin, 2021: 2), dominating some technology-intensive segments such as cross-border payments (Brandl and Hornuff, 2020) and holding geo-economic significance in major economies (Massoc, 2022).

Scholarship and market participants have, for developed countries and DEEs alike, identified two main factors that have helped banks to maintain their continued importance against the background of a growing FinTech sector. First is the digitalisation of banks’ operations, including through the ‘platformisation’ of their activities (Hendrikse et al., 2018; Kemmerling and Trampusch, 2023; Langley and Leyshon, 2021; Westermeier, 2020). Platformisation refers to the shifting of activities to the digital infrastructure that allows platform firms to mediate between producers and consumers of goods, services and information (Langley and Leyshon, 2016). Second is the formation of partnerships, often through acquisitions, majority or minority investments, between banks and FinTechs happening in both developed and DEEs (Langley and Leyshon, 2021; Larsson et al., 2023; McKinsey, 2022). This body of work has taught us a great deal about banks’ strategic responses to FinTechs and the reasons for their continued dominance.

There is, however, room to contribute to the emerging literature on the impact of the rise of FinTechs on banks by injecting further nuance into the debate and considering the role of politics. In an effort to identify broader trends, scholarship has so far largely placed the accent on cross-national similarities (Hendrikse et al., 2018; Langley and Leyshon, 2021; Larsson et al., 2023). Yet a closer look at the roles that banks play in different countries reveals that even in the context of the macro-trend of digitalisation, there is considerable cross-country variation. In particular, there are cross-national differences in the extent to which FinTechs have reduced banks’ dominance in the provision of payment services and credit, and to which they have been able to gain DIPRs. As a result, we see cross-national variation in the extent to which banks have lost their privileged position as drivers of economic activity to FinTechs.

Our analysis builds on, but also departs from, extant research. Not only do we seek to explain cross-national variation as opposed to similarities in the impact of the rise of FinTechs on banks, but we also give greater consideration to how variation in political-economic contexts leads to varied impacts of the rise of FinTechs on banks. In addition, we also seek to address the question of implications for banks’ political power more directly and thus connect more to studies of the political power of business. Existing research on the power of business in the era of digitalisation has focused on tech companies such as Uber (Valdez, 2023) and Amazon (Culpepper and Thelen, 2020). Yet, digitalisation not only creates new digital behemoths but also digitalises the business models of traditional firms (Kemmerling and Trampusch, 2023; Westermeier, 2020). As a result, some firms are able to gain DIPRs – the potential to exercise corporate power derived from the control of digital infrastructure. Controlling digital infrastructure, which refers to the information technologies and organisational structures that enable a wide range of downstream activities for users (Tilson et al., 2010), amounts to controlling the backbone of much social and economic activity in modern life (Rahman, 2018, 1622; Bernards and Campbell-Verduyn, 2019, 4; Petry, 2022). It is an important basis of corporate political power in the digital era because firms that control digital infrastructure as intermediaries determine the terms of usage to the infrastructure on which governments, businesses and individuals rely (Bernards and Campbell-Verduyn, 2019; Petry, 2022; Rahman, 2018; Valdez, 2023) and are able to survey their users (Farrell and Newman, 2019; Westermeier, 2020). Thus, while in the classical literature on business power, structural power refers to the ability of firms to exercise political power because they may reduce economic growth by limiting their economic activity (Block, 1977; Lindblom, 1977), infrastructural power differs conceptually. It refers to the ability of firms to exercise political power through infrastructural control, notably because they may act as gatekeepers to services and data on which users rely for various reasons, such as convenience (Culpepper and Thelen, 2020), business activities or, in the case of states, security (Abels, 2024; Farrell and Newman, 2019).

Explaining variation in banks’ DIPRs

What explains cross-national variation in the impact of a rising FinTech sector on banks’ DIPRs? Much of the existing research on the impact of the rise of FinTechs on banks has focused on banks’ strategies of competition, adaptation and cooperation to explain the role of banks in the national and international political economy. However, banks’ strategic behaviour is shaped by the political-economic context. In fact, literature on the politics of platform capitalism suggests that different national political-economic configurations foster different cross-national patterns of digitalisation and thus different power relationships between the state, tech companies and the traditional, incumbent players (Kemmerling and Trampusch, 2023; Rahman and Thelen, 2019).

In particular, there is an emerging strand of research on the rise of tech companies that underscores the role of regulatory context in shaping the development of the tech industry and its ecosystem. Rahman and Thelen (2019) highlight, amongst other factors, the role of consumer-oriented antitrust regulations behind the growth of tech companies in the context of the US. Valdez (2023), for instance, argues that previous regulations in the for-hire vehicles sector shape Uber’s infrastructural power. Macartney et al. (2022) find that regulatory policy had an impact on the extent to which the entry of FinTechs provided a competitive challenge to banks in corporate bond trading.

While these studies shed light on the role of institutions in shaping the behaviour and power of firms in the era of digitalisation, they also raise the important question of where these institutional frameworks come from. What explains the reactions of regulators to new digital actors or products, which then subsequently define the regulatory space for incumbents? One important factor is power dynamics. Emerging research on the rise of tech companies has, in particular, highlighted how both tech companies and traditional institutions seek to exercise instrumental power to shape the regulation of digital innovations (Thelen, 2018; Valdez, 2023). Instrumental power refers to the use of political voice and action by businesses, including lobbying and the deployment of resources to shape policy. 1

However, financial regulators do not design regulations of financial innovations in the form of a new digital actor or service by considering merely who speaks loudly about an issue. Rather than being passive respondents to firms using political voice, regulators will defend the domains under their purview vis-à-vis other actors. In particular, they consider two questions. First, is it worth listening to those actors exercising their voice to shape regulation? We argue that the assessment of the importance of listening to one actor’s policy preferences is not only shaped by instrumental power resources but also by their perceived importance for economic growth, and thus their structural power. Actors who are structurally more powerful, as economic development depends on them, are thus more likely to be given an opportunity or forum to exercise instrumental power than actors who are less structurally powerful. Second, to what extent and in what ways should there be regulatory constraints on financial innovation to enhance its impact on economic development? The answer of financial regulators to this question depends, just like the answer to the previous question, on the public–private balance in finance, and thus, a structural feature of the economy.

The public–private balance captures the extent to which the state, as opposed to the private sector, plays a central role in driving economic development through the allocation of resources. If the public–private balance is tilted towards the private sector, the private sector plays a more central role in driving economic development by allocating economic resources. In this context, the structural power of private actors is, ceteris paribus, higher and regulators are more likely to listen to them when they exercise voice and to impose fewer constraints on financial innovation as the private sector is considered to drive economic development. If the public–private balance is tilted towards the state, the reverse is the case: The state then plays a more central role in driving economic development by allocating economic resources. Therefore, the structural power of private actors is, ceteris paribus, lower and regulators are less likely to listen to them when they exercise voice. In such a context, regulators are also more likely to place constraints on financial innovation because the state, rather than the private sector, is considered to drive economic development and seeks to steer the allocation of resources in line with the state’s development priorities.

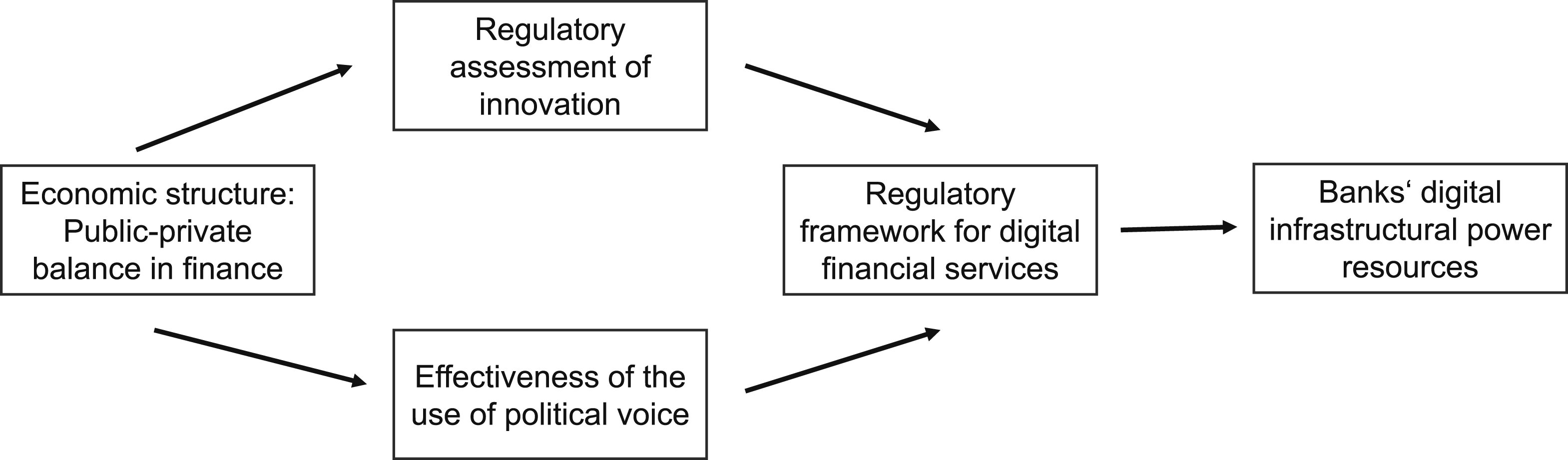

Based on this reasoning, our central argument, summarised in Figure 1, is that the public–private balance in finance shapes two factors, namely, the regulatory assessment of financial innovation and the ability of financial industry players to use political voice effectively. Both factors, in turn, shape the regulatory framework for digital financial services and, as a result, banks’ DIPRs. In other words, where the public–private balance is tilted towards the private sector, we expect a greater openness of financial regulators to financial innovation, including from non-bank entities, and thus a greater willingness to bear the risks associated with that openness, enhancing the space for the growth of the FinTech industry. Explaining variation in banks’ DIPRs.

Methodology

To examine how the rise of FinTechs has affected banks’ DIPRs and the factors that help to account for cross-national variation in DIPRs, we employ case studies, combining within-case analyses that reconstruct the processes of banks’ development of DIPRs as well as comparative case studies of Kenya and Nigeria. We chose Nigeria and Kenya as cases for two reasons. First, these two countries are at the forefront of the digital transformation of finance in Africa (McKinsey, 2022), and the impact of the rise of FinTechs on banks should be evident. Second, while the two countries are similar with respect to several alternative explanations for banks’ DIPRs, such as being middle-income economies with some large FinTechs and a domestically owned banking sector, they vary significantly in their regulation of digital finance, a central intervening variable in our framework. This pattern of variation supports causal inference in line with the most similar method (Seawright and Gerring, 2008).

Our analysis draws on various types of data, notably: policy documents such as central bank reports and regulations, companies’ annual reports and websites, industry reports, news reports and country-level statistical data. We also conducted 23 semi-structured online interviews with FinTechs, banks and regulators in 2023 and 2024 to collect information about key players in the digital financial services industry, market structure, the rationale behind the design of regulation and their ability to exercise structural, instrumental and digital infrastructural power. Our interview questions focused on a) organisational resources and lobbying activities to assess the potential to exercise instrumental power; b) stakeholders’ perceptions of banks’ and FinTechs’ contribution to economic development to assess the potential to exercise structural and instrumental power; and c) on the extent to which banks and FinTechs are able to control the emerging digital financial infrastructure to assess their DIPRs. To identify interviewees, we relied on a combination of using existing research networks and snowballing. In selecting interviewees, our criteria were expertise and the size of the financial institution, because we sought to interview representatives of financial institutions with different sizes in line with the diversity of the industry.

We consider two dimensions to assess the ability of a financial institution to control digital financial infrastructure. First, building on Kemmerling and Trampusch (2023), whether the financial institution occupies a central position as intermediary on a digital platform. The indicator here is whether the financial institution acts as an intermediary by controlling a platform – that is, a digital infrastructure that enables two or more groups to interact (Srnicek, 2016). As Petry (2022: 322) notes: ‘Whoever controls financial market infrastructures has significant power to shape financial markets and their socio-economic outcomes’. The second dimension, the centrality of the platform in the ecosystem of digital finance, is inspired by applications of network theory (Oatley et al., 2013). Infrastructures create, as Abels (2024: 849) explains, ‘patterns of dependency and allow actors in control of critical hubs to exploit this (…)’. At one end of the spectrum lies a financial institution that controls a platform which is connected to all other financial institutions at about the same degree as other platforms. In this system, no single platform company would attract substantially more users than any other. At the other end of the spectrum lies a financial institution that controls a platform which is connected to all other financial institutions to a higher degree than other platforms. In this system, one platform company would attract substantially more users than any other. Controlling a platform in the ecosystem of digital finance that is more central in the ecosystem is then suggestive of greater infrastructural control than controlling a node with fewer users. The main indicator we use is the number of users on the platform.

Kenya’s banking sector and the rise of FinTechs

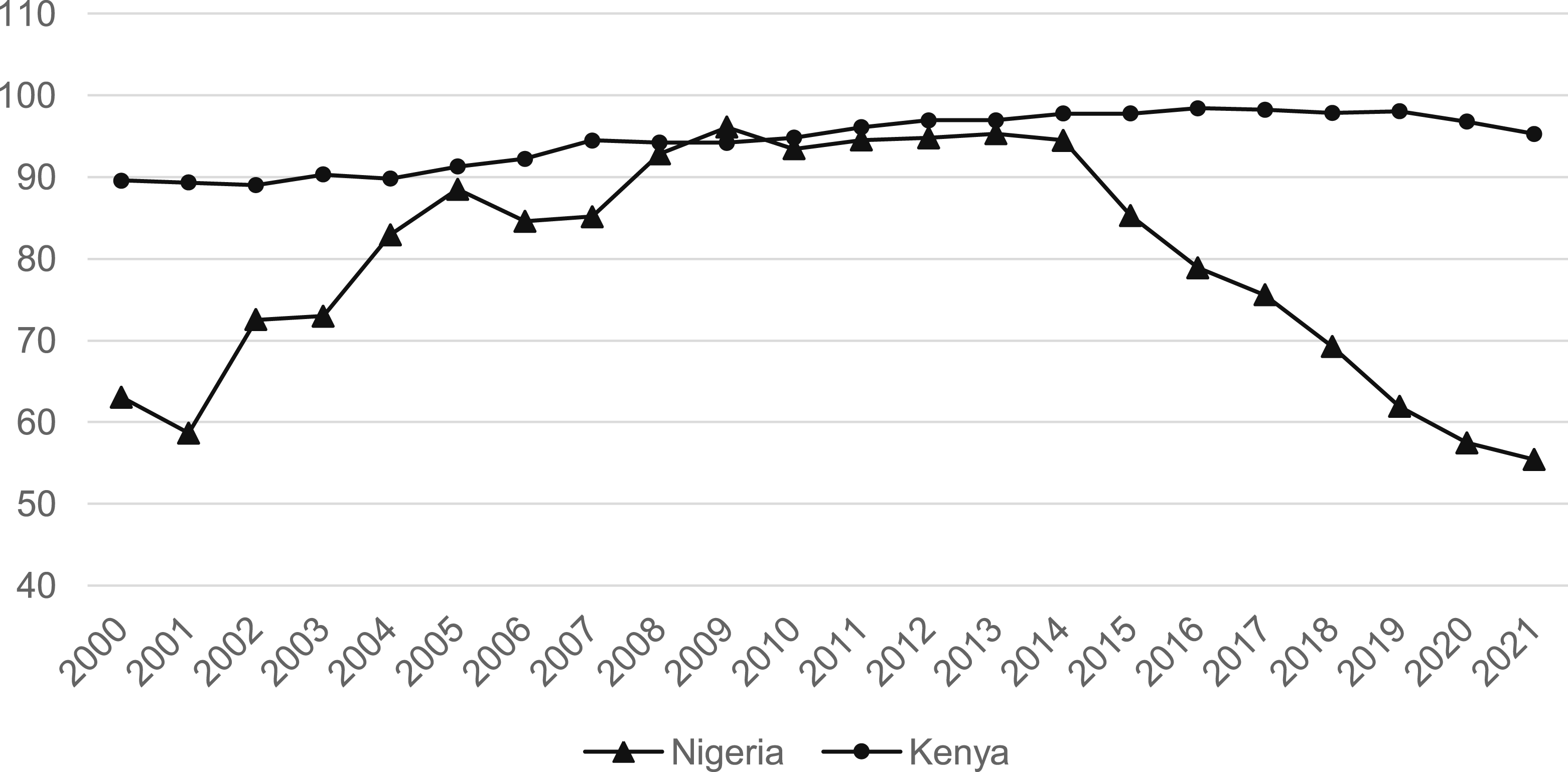

The starting point of our case study of Kenya is, in line with our model depicted in Figure 1, the public–private balance in finance. One indicator of this is the ratio of deposit money bank assets divided by the total of deposit money bank assets plus central bank assets. This ratio captures the funds controlled by the central bank as a share of all bank assets, and therefore the funds over which the central bank has discretion, as opposed to the banks as the other main financial intermediaries (Boone, 2005). Given that the banking sectors in Kenya and Nigeria are largely privatised, this indicator captures central banks’ control over financial assets in an economy and thus the power of central banks relative to private financial institutions. The assets of central banks are a good proxy for state control over economic resources because central banks are state authorities. The higher the ratio, the fewer the assets controlled by the central bank and thus the higher the tilt in the public–private balance towards the private sector. As Figure 2 shows, this ratio has historically been higher in Kenya than in Nigeria. The tilt of the public–private balance towards the private sector has long historical roots (Brownbridge, 1998), with Kenya being, for instance, one of the few African countries that did not seek to fully nationalise its banking sector at the time of independence. Ratio of deposit money bank assets to the sum of deposit money bank assets and central bank assets (%) (Source: World Bank (2022)).

The lack of a strong natural resource sector, the struggling manufacturing sector and the broad market-based ideology help to explain the government’s emphasis on finance as a driver of development (Republic of Kenya, 2013). Every 5 years, the government issues a financial sector strategy suggestive of the central role and structural power of financial institutions in Kenya’s private-sector-led growth model. The instrumental and structural power of banks and the largest FinTech, Safaricom, are underpinned by two additional factors. First, a broad section of Kenya’s elite has shares in these institutions (Tyce, 2020). Second, banks and Safaricom pay a high level of taxes, estimated at 36% and 7% of tax revenue, respectively, in 2022 (Upadhyaya et al., 2025).

The political economy of regulating digital financial services

The development of digital financial services in Kenya begins with the story of the mobile money product M-PESA, introduced by Safaricom, a mobile network operator (MNO), in 2007. Mobile money enables users to transfer funds via mobile phones without a bank account or smartphone. When assessing M-PESA as a financial innovation, the Central Bank of Kenya (CBK), as the regulator, had to assess its implications for economic development and financial stability. In 2006, before the launch of M-PESA, about 27% of adults had access to formal financial services and were thus ‘financially included’ (CBK, KNBS and FSD Kenya, 2021). Therefore, from the perspective of the CBK, banks were not fulfilling their role to expand their services. When banks objected to the permission of M-PESA, the CBK was able to resist banks’ lobbying, arguing that banks had failed to increase financial inclusion (Ndung’u, 2021). Due to the emphasis on private sector-led growth, the CBK also had a positive assessment of financial innovation. The then CBK Governor Prof. Njuguna Ndung’u decided to institute a light-touch regulatory model for M-PESA (Ndung’u, 2021), where the CBK simply gave a ‘letter of no objection’ to Safaricom (Tyce, 2020). Furthermore, the commitment to financial inclusion was not only from the Governor but also from President Kibaki himself, who was steeped in the ideology of market-led development (Tyce, 2020). The regulatory support allowed M-PESA, and as a result, Safaricom, to flourish. The total value of mobile money transactions in 2019 was just over US$40bn, which compares with a GDP of US$88bn in 2018 (Paelo and Roberts, 2022). The high level of adoption of mobile money and agency banking increased financial access in 2021 to 81% of the population (CBK, KNBS and FSD Kenya, 2021).

More recently, Kenya witnessed the growth of standalone FinTechs, that is, FinTechs that don’t have partnerships with either Safaricom or banks. Most of them are in the domain of digital payments (e.g. Cellulant), micro-asset financing (e.g. M-KOPA) and digital credit (e.g. Tala). The regulation of standalone FinTechs can be characterised as ‘cautious permissiveness through flexibility and forbearance’ (Mwencha et al., 2019). The supportive regulatory environment for FinTechs that don’t have official partnerships with Safaricom suggests that it is not only Safaricom’s use of political voice but also regulators’ belief in private sector-led growth that explains regulatory outcomes. As a FinTech owner reflected, regulators are keen to allow innovation until evidence of mischief emerges (Interview 15). The CBK issues payment service provider (PSP) licences, but the conditions for a PSP licence are much less stringent than for a bank, requiring, for instance, far lower minimum capital requirements (Upadhyaya et al., 2025). The CBK reaffirmed its pro-private sector-innovation approach in a recent strategy paper, explicitly stating that it will foster FinTech development through a test-and-learn approach (CBK, 2022). Following the rise of M-Shwari – a digital credit product that is a partnership between a bank and Safaricom (and discussed in more detail below) – many standalone FinTechs started providing digital credit. The CBK initially took a hands-off approach to digital credit, similar to its response to M-PESA. As problems like unfair blacklisting of borrowers became more common, regulation began in April 2021. By 2024, 51 digital credit providers were licensed, while 480 applications were still under review (CBK, 2024). While the new rules have curbed some of the worst practices, the market remains large since unlicensed lenders with pending applications are still allowed to operate (Upadhyaya et al., 2025).

Safaricom’s M-PESA has come to play a dominant role due to its centralised position in the emerging digital infrastructure. Recent regulations to enhance competition, like compulsory interoperability with other mobile money providers, have not reduced Safaricom’s market dominance as expected (Paelo and Roberts, 2022). As Safaricom controls 95% of retail mobile money volumes in the country (Mazer and Garz, 2024), standalone FinTechs and banks face strong incentives to establish links to Safaricom. One Fintech entrepreneur remarked, ‘M-PESA today is really a platform…(…) that creates rails for both FinTechs and other financial institutions’ (Interview 17). Therefore, even standalone FinTechs or banks that do not have partnerships with Safaricom usually use the platform to distribute funds (Interviews 9, 15 and 17). The Kenyan government supported Safaricom in gaining DIPRs and sees it as a partner in fulfilling its mandates, using, for instance, its infrastructure for welfare payments (Breckenridge, 2019; Interview 15).

Banks’ DIPRs

Kenyan banks have used a variety of strategies to respond to the rise of FinTechs. Recognising that the rise of M-PESA was based on the use of a country-wide third-party agent network, Kenyan banks exercised voice to request a regulation which allowed them to also use third-party agents. The CBK was responsive, enacting the Agency Banking Regulation in 2010. By December 2015, 17 commercial banks had contracted 40,592 agents (CBK, 2015).

A second strategy by banks was the launch of Pesalink, a cooperative payment platform developed by the Kenya Bankers’ Association with strong donor support (FSD Kenya, 2021). Pesalink enables low-cost transfers between bank accounts, offering a cheaper alternative to M-PESA. However, its impact has been limited due to slow rollout, inter-bank trust issues and low customer uptake (Interview 9; Interview 14). In 2024, Pesalink processed 8.2 million individual payments compared to 28.33 billion transactions on M-PESA (Pesalink, 2025; Safaricom, 2024).

Banks’ third type of strategy is to invest heavily in technology and also start in-house FinTechs as a subsidiary (Interview 2, Interview 12). For example, NCBA has started LOOP, KCB Bank has started VOOMA and Equity Bank has started FinServe (Mwencha et al., 2019). The CBK has taken a market-friendly regulatory stance, exempting banks’ in-house FinTech operations from new licensing requirements. However, in-house FinTechs are yet to reveal their benefits to banks in terms of profits (Interview 17).

The fourth and most successful strategy for some banks has been collaborating with Safaricom through M-PESA. NCBA Bank partnered with Safaricom to launch M-Shwari in 2012, the first digital credit product in Kenya and globally, transforming NCBA from a niche corporate bank into the bank with the highest number of customers (Florence D). This success spurred other partnerships, such as KCB-M-PESA in 2015, which helped KCB regain its position as the bank with the largest customer base. In 2019, NCBA and KCB also partnered with Safaricom to launch the overdraft service Fuliza. Together, M-Shwari, KCB-M-PESA and Fuliza now control over 95% of Kenya’s digital credit market (Mazer and Garz, 2024), highlighting Safaricom’s infrastructural control. Notably, the regulation of digital credit emerging from 2021 onwards did not affect bank-Safaricom partnerships as they were considered already regulated products (Florence D), reinforcing Safaricom’s dominance. Equity Bank, Kenya’s second-largest bank by asset size, also partnered with another MNO, Airtel, to establish Equitel. However, the success of this venture has been relatively limited (Interview 21), underscoring the dominance of Safaricom. As a financial inclusion expert remarked, ‘linkage [with Safaricom] became more of what I called a “hygiene factor,” something that the bank has to have, in order to keep its customers happy…they didn’t have a choice’ (Interview 9).

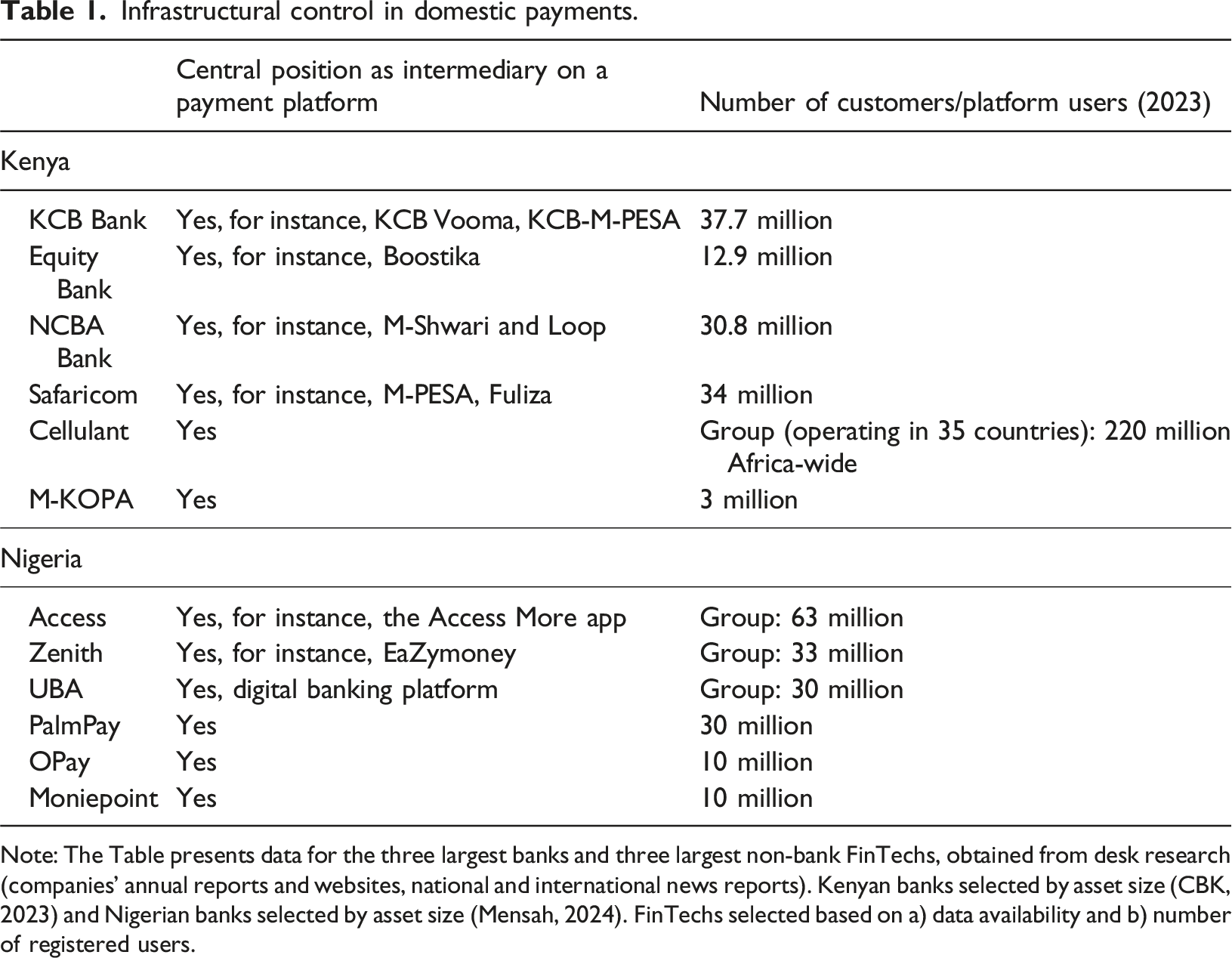

Infrastructural control in domestic payments.

Note: The Table presents data for the three largest banks and three largest non-bank FinTechs, obtained from desk research (companies’ annual reports and websites, national and international news reports). Kenyan banks selected by asset size (CBK, 2023) and Nigerian banks selected by asset size (Mensah, 2024). FinTechs selected based on a) data availability and b) number of registered users.

Despite these data limitations, Table 1 helps, in combination with our qualitative data, to illustrate our claim for the domain of domestic retail payments that banks in Kenya have not been as successful in increasing their DIPRs as the dominant FinTech, Safaricom. Banks’ strategies to develop the cooperative platform Pesalink and to start their own in-house FinTechs have not been that successful, as they have not been able to capture significant market share or develop products that are highly adopted. Therefore, these strategies have had limited success in increasing banks’ DIPRs. Banks’ investment in their own agency banking networks, in contrast, has helped them enhance their DIPRs by expanding the user base. This success is reflected in financial inclusion data, which shows that the use of banks has increased from 14% to 441 between 2006 and 2021 (CBK, KNBS and FSD Kenya, 2021). Importantly, the strategy of collaborating with Safaricom to provide the digital credit products M-Shwari, KCB-M-PESA and Fuliza has greatly benefited some banks in terms of both increasing the number of customers and profits. In 2023, the two main partner banks, KCB and NCBA, accounted for 40% and 32.5% of total customer accounts in the market, respectively (CBK, 2023). Yet only a few banks have managed to develop these collaborations, with Safaricom ultimately deciding who they partner with. Therefore, not all banks have been able to significantly increase their DIPRs.

Finally, the value and volume of transactions are suggestive of the distribution of DIPRs. Banks conduct a significant portion of digital transactions in the high-value space. They increased their use of the real-time gross settlement (RTGS) system, a digital infrastructure for interbank transactions and high-value, corporate and cross-border transactions, after the CBK upgraded it in 2020. In 2022, the total value of mobile money transactions in Kenya was 19% of RTGS transactions (CBK, 2022), indicating the limits of Safaricom’s reach. However, the CBK, not the banks, owns RTGS (CBK, 2022). In terms of volume, Safaricom sits at the centre of the emerging digital financial infrastructure with over 32.9 million transactions compared to 6.4 million transactions on RTGS in 2022 (CBK, 2022).

Thus, Kenyan banks remain significant players in the financial sector and have gained DIPRs as they have invested in platformisation. Yet, they have to some extent become reliant on Safaricom’s digital financial infrastructure, over which they have limited control, as Safaricom controls the terms of usage. In sum, some Kenyan banks gained in absolute terms in DIPRs but not as much as one large FinTech, Safaricom, which occupies a central position in the emerging digital infrastructure.

Nigeria’s banking sector and the rise of FinTechs

It is difficult to understand the politics of finance in Nigeria without recognising the extent to which the public–private balance is tilted towards the state. While the commercial banking sector was privatised by the early 2000s, the state continues to play a significant role in the allocation of financial resources, foremost through the Central Bank of Nigeria (CBN). As Figure 2 shows, central bank assets have historically been sizable compared to the assets of deposit money banks, and the central bank has used its power to steer economic resources towards preferred actors and sectors. The state’s command of considerable resources originates in its access to oil revenues, as Nigeria is Africa’s largest oil exporter. While in 2018 oil only made up 9% of GDP, it accounted for over 76% of exports and 54% of government revenue (EITI, 2023). This is not to say that Nigerian banks have little structural power. From the perspective of the CBN, banks are, in the context of Nigeria’s bank-based financial system, envisaged to play an important role in financing the weakly developed real economy and diversifying the economy away from oil (Dafe and Rethel 2022). Except that banks have not sufficiently lived up to this expectation. Therefore, the CBN conceives of itself as playing a central role in steering economic development (Moses-Ashike, 2022; Sanusi, 2010).

The political economy of regulating digital financial services

In Nigeria, as in Kenya, the first competitive challenge to traditional banks from FinTechs arose in the late 2000s in the payments segment, in the form of mobile money. At that time, other domestic FinTechs such as SystemSpecs and Interswitch operated in the payment space but focused on products to facilitate inter-bank transactions and did not target the retail market. The largest MNOs in the Nigerian market, the South African MTN and the Indian Airtel, were interested in offering mobile money services to the retail mass market as they could leverage their telecommunications and agent infrastructure. Offering financial services to the mass market was not part of banks’ business strategy since risk-adjusted returns were considered too low (Interviews 3 and 18). In fact, in 2008, only 30% of Nigeria’s adult population was banked (EFinA, 2008). Nonetheless, banks considered mobile money as a competitive challenge because they were concerned that it would offer MNOs access to customers to whom they could then provide digital banking services (Interview 1).

While Nigeria’s central bankers followed the developments in Kenya closely, their regulatory approach towards mobile money differed significantly. The CBN developed mobile money regulations in 2009 before allowing the service and designed them more stringently, excluding MNOs from leading the provision of mobile money (CBN, 2009, 2015). 2 Instead, both banks and non-banks with a CBN licence were permitted to lead the provision of mobile money services, but had to adhere to CBN guidelines. The role of MNOs was restricted to providing the telecommunications infrastructure for scheme operators.

From the perspective of the CBN, more stringent mobile money regulation than in Kenya was necessary as it considered the financial sector as inherently fragile and self-regulation as insufficient (Sanusi, 2010). The CBN argued that ‘the expected volume of Mobile Payments transactions in a large market as Nigeria had the potential to introduce systemic risk to the entire payments system and as such the Bank-centric models (with stringent controls) are encouraged over and above the T'elco-led which the CBN has little or no control over’ (Jimoh, 2013). By excluding MNOs, the CBN sought to reduce ‘the regulatory gaps/lapses that could occur with a Telecoms organization running a mobile payments solution’ (Obaigbona, 2010).

The prominent role of the state in driving economic development not only shaped the regulatory assessment of mobile money but also limited the ability of MNOs and banks to exercise political voice effectively. MTN, as the dominant and highly profitable MNO, certainly had the financial resources to lobby Nigerian state officials. Yet the CBN did not have a regular exchange with MNOs as they were under the regulatory purview of the Nigerian Communications Commission. Moreover, lobbying was also undermined by the CBN’s view that it was important to regulate the power of Telcos rather than relying on market forces. The CBN’s perspective was that ‘Telcos may have undue advantage in ruling out any form of competition against its own product through either blocking out the other players in the industry or overpricing its network access so as to give its own product undue commercial advantage’ (Jimoh, 2013). As in Kenya, Nigeria’s banks lobbied extensively against an MNO-led model of mobile money regulation (Saigal, 2014; Interview 4), and the regular exchanges with the CBN and economic resources most likely facilitated their exercise of instrumental power. However, the banking sector’s ability to lobby effectively was constrained as the regulators allowed non-bank financial institutions to run mobile money services even though some, like Interswitch, were large payment companies with some control of digital infrastructure. The strong emphasis on KYC and consumer protection regulations, which are costly for banks providing mobile money, also suggests that regulators failed to heed banks’ preferences for loose regulation.

The dominance of the state in steering the allocation of economic resources in Nigeria also helps to explain the regulation of other digital financial services. Nigeria’s FinTech sector began to grow significantly in the mid-2010s, especially in payments and digital lending. As the FinTech industry developed, so did the CBN’s FinTech regulation. Importantly, the regulatory regime in Nigeria is more stringent than the one in Kenya, and it positions banks more centrally in Nigeria’s ecosystem of digital finance. As one FinTech founder sums it up, ‘there is no FinTech company in Nigeria that can grow outside of the banks in Nigeria, it is not possible because of the way our regulatory body has designed it. So, for example, every FinTech company must have a settlement bank (…)’ (Interview 7). Another example of the stringency of regulation is the CBN’s introduction of a Bank Verification Number (BVN) in 2014. The CBN introduced the BVN, which gives each user of financial services a unique identity across the Nigerian financial industry to support the stability and integrity of the banking system (CBN, 2017). Users must obtain their BVN to access FinTech or banking services.

The CBN’s evolving licensing system also epitomises the stringency of regulation. It includes, for instance, a Switching and Processing Licence, a Mobile Money Operator Licence, a Payment Solution Services Licence and a Payment Services Bank (PSB) Licence. The underlying rationale is to regulate according to activity, rather than by the type of institution. As a senior central banker explains, ‘(..) if you want to offer full banking services - foreign exchange, corporate finance, corporate banking - the only way you could do it is that you just have a full banking licence’ (Interview 11). Each licence specifies the rights and obligations of applicants, such as minimum capital requirements. Importantly, the licensing regime also specifies that mobile money, payment services providers and digital lenders need to keep the customers’ funds at a domestic bank settlement account, ensuring banks have a central role in the emerging ecosystem of digital finance. As is the case in Kenya, FinTechs are not allowed to take deposits. As a venture capitalist focussing on African FinTechs explains, ‘just banks have a deposit base. So they have the financial muscle, the FinTechs haven’t really been able to crack that’ (Interview 13). The PSB framework, issued in 2021, allows FinTechs and, for the first time, MNOs to take deposits and offer digital payment services. Notwithstanding, this framework includes such formal restrictions as the prohibition to lend and the requirement to operate a minimum of 25% of financial service touch points in rural areas, underscoring the dominant role of the CBN in steering how FinTechs allocate resources. 3

It is easy to imagine that instrumental power helps explain the central role of banks in Nigeria’s emerging regulatory regime of digital finance. FinTechs have indeed not been effective in using voice to shape regulation. In part, this is due to a lack of concerted political action. The membership of Nigeria’s FinTech Association, for instance, is diverse, comprising large banks like Access Bank, small digital financial services start-ups and large FinTechs like PalmPay, which challenges the aggregation of diverse preferences (Interview 5). As one FinTech founder explains, ‘everybody engages the regulators individually’ (Interview 7), highlighting the limits to collective action. Moreover, FinTechs lack close professional relationships with central bankers and do not meet the CBN regularly. That said, it is also difficult to argue that the existing regulation is biased in favour of banks since the regulatory requirements broadly reflect the risk profile of activities rather than the type of provider. Moreover, the CBN’s regulatory framework for digital finance includes some policies that support the development of FinTechs and conflict with the interests of banks, suggesting that their instrumental power was also limited. One example is the CBN’s development of open banking regulation, which specifies the conditions under which banks share information with other financial entities to enhance competition in the financial sector and to which banks are, as one FinTech representative and former banker explains, ‘absolutely opposed’ (Interview 1). Thus, in explaining the regulatory system, it is useful to look beyond financial institutions’ instrumental power and consider the role of Nigeria’s public–private balance, as reflected in the CBN’s view that corporate self-regulation is insufficient and that the central bank needs to steer the sector to enhance its contribution to economic development. Without stringent regulation, FinTechs would, as a regulator explains, ‘become a threat to the stability of the financial system (..) we can’t have a situation where inadvertently, knowingly or unknowingly, activities of that nature create credibility issues within the system’ (Interview 11).

Banks’ DIPRs

One important response of banks to the rise of FinTechs has been to digitise banking operations by investing in their own digital infrastructure. This digital infrastructure notably includes Nigeria’s central switch, the Nigeria Inter-Bank Settlement System (NIBSS), which is owned by all licensed banks and the CBN. It also includes online banking platforms to which FinTechs are able to connect, and the digital infrastructure for international payments. By expanding digital banking for retail customers, banks compete directly with FinTechs. In addition, the federal and state governments also rely on banks’ digital infrastructure for all payments (Interview 7). Another element is the digitalisation of corporate banking, which is highly important because it gives banks a first-mover advantage compared to FinTechs and is centred on a more profitable business segment than retail banking. A key source of bank profitability is ‘big-ticket transactions with oil and gas, big-ticket transactions with telecoms, which is not the space that FinTechs are currently operating in’ (Interview 5). This segment also includes large-scale cross-border corporate transactions. In particular, a few banks such as Access Bank focus on developing digital platforms for cross-border payments in areas such as trade finance (Access Bank, 2022: 5). Expanding the digital financial infrastructure for cross-border financial transactions to link Nigerian companies to the international economy, in areas such as trade finance is also an important source of structural power. As a former bank CEO explains, the ‘argument for a financial institution that is catalysing trade across the continent is a very powerful one to be made to governments and regulators’ (Interview 3). This suggests that banks’ DIPRs may become an important basis for structural power in digitalising economies.

By exploiting the stringent licensing regime, banks were able to tie FinTechs to their digital infrastructure. Such partnerships allow FinTechs to benefit from the bank’s brand name and associated trust while also allowing them to avoid having to get a licence which comes with higher regulatory requirements. Banks can benefit as well. As a former banker explains, ‘the bank can shift that FinTech relationship to its own payment commerce and say, go to my [licensed] switching company and engage’ (Interview 1). Some banks also only make their APIs available to their FinTech partners for a fee.

Moreover, banks have also established FinTech subsidiaries exploiting their existing digital infrastructure. In 2011, the CBN introduced the model of a holding company in the banking sector. Shifting to a holding company allows the parent bank to coordinate and manage all the subordinated units, and has allowed banks to spin off more lightly regulated FinTechs. As a former senior banker explains, an off-spun FinTech derives its customers from the parent bank and utilises the infrastructure of the parent bank, with, for instance, the payments departments of a bank becoming a company on its own (Interview 1).

Banks’ strategic responses have allowed banks to gain DIPRs, as also Table 1 shows. Banks have developed their own digital platforms in both retail and corporate payment domains. In international and domestic corporate payments and transactions involving the public sector, the platforms of banks continue, as explained above, to dominate over FinTechs in terms of their user base. Even in domestic payments involving retail customers, where major FinTechs have gained DIPRs, banks continue to play a significant role, as evidenced by the large number of users on their various digital banking platforms. Importantly, and in contrast to Kenya, banks’ growth of their user base in domestic payments is not dependent on linking to major FinTech platforms, as no single financial institution controls a platform which is connected to leading financial institutions to an outstanding degree. The result is, in terms of ownership, a more decentralised digital finance ecosystem with several important nodes. In this system, banks compete with FinTechs and set the terms in their partnerships with FinTechs.

Kenya and Nigeria in comparative perspective

The impact of the rise of FinTechs on banks’ DIPRs differs significantly across Kenya and Nigeria. In both Kenya and Nigeria, banks have gained DIPRs in absolute terms. In particular, in both countries, large financial transactions between businesses, whether domestic or cross-border, are conducted on banks’ or central banks’ platforms, not FinTech platforms. In addition, banks developed digital banking platforms and apps offering specialised services.

However, comparing quantitative data on user numbers and qualitative data on partnership models of major institutions provides a more nuanced picture. This data suggests that in Kenya, the relative DIPR gains of the FinTech sector or more specifically, Safaricom, vis-à-vis banks are higher than the relative gains of FinTechs vis-à-vis banks in Nigeria. Safaricom controls a central node in Kenya’s emerging digital infrastructure, intermediating between many users, including banks and retail users. Importantly, the number of users on banks’ platforms has increased due to partnerships with Safaricom. In contrast, in Nigeria, the ownership of the emerging digital infrastructure is more decentralised, encompassing many nodes with significant user numbers which are less connected to each other.

The origins of this difference in the impact of the rise of FinTechs on banks’ DIPRs lie in differences in the regulatory systems of the two countries, which in turn result from differences in the public–private balance in finance. In Kenya, the private sector has historically played a more dominant role in the allocation of financial resources. In a context where banks had not played their envisaged role in promoting economic development by enhancing financial inclusion, public authorities listened to Safaricom, which had developed M-PESA to address this challenge. Successful deployment of instrumental power, combined with the view that private sector innovation rather than state intervention should enhance financial inclusion, limited regulation, which supported the growth of Safaricom’s digital finance platform. While Safaricom’s political connections facilitated the exercise of instrumental power, the supportive regulatory environment cannot be solely explained by Safaricom’s political connections as the authorities developed a market-friendly regulatory framework that supported the growth of digital financial services other than Safaricom, such as standalone FinTechs. In this context, a digital financial services sector could emerge with limited regulatory constraints, allowing Safaricom as a dominant player to grow and develop partnerships with banks under the terms it sets.

In Nigeria, in contrast, the public–private balance in finance has historically been tilted towards the state, with the CBN playing a more central role in steering the allocation of financial resources. In this context, the instrumental power of banks was limited because, in the eyes of regulators, banks had not played their envisaged role in promoting economic development by enhancing financial inclusion. Meanwhile, the effectiveness of FinTechs’ lobbying for more favourable regulation was also limited. Partly because of the lack of cohesion in the FinTech sector, but also because central bankers believed that the contribution of their financial innovations would be limited without stringent regulation. The resulting regulatory regime reflects the belief that the state plays a central role in driving economic development by steering the allocation of resources, as is reflected in the elaborated licensing regime and the requirement for PSBs to serve rural areas. In this context, a digital financial services sector could emerge with significant regulatory constraints on financial institutions, limiting the emergence of one dominant player to which others seek to connect. As such, the two cases not only show how DIPRs shape the ability to exercise structural power but also how historical power relationships shape regulatory preferences with regard to financial innovation.

Conclusion

Using in-depth comparative case studies of Kenya and Nigeria, two countries at the forefront of the digital transformation of finance in Africa, this article explores how the rise of FinTech has affected banks’ DIPRs. We find that cross-country variation in the public–private balance leads to variation in the regulation of digital finance, which in turn has implications for banks’ ability to gain control of the emerging digital infrastructure. As a result, banks in both Kenya and Nigeria have gained DIPRs, but the relative gains of the FinTech sector in DIPRs vis-à-vis banks are higher in Kenya than in Nigeria.

The analysis pursued in this article advances a still nascent research agenda on the changing power and purpose of banks in the era of platform capitalism. We do so by looking beyond developed countries and studying DEEs as well as beyond cross-national similarities to explain cross-national variation in outcomes for banks. Moreover, our analysis contributes in analytical terms to this research agenda. First, by shedding light on the historical and structural roots of emerging ecosystems of digital finance. Second, by highlighting the importance of looking beyond the instrumental power and structural power of financial institutions to consider their DIPRs. Third, by advancing the conceptualisation of DIPRs. Specifically, we propose a measure of the extent to which financial institutions have gained such resources.

Our findings have two major implications. First, they show how porous the boundaries between infrastructural and structural power are in the era of platform capitalism. DIPRs are conceptually distinct from structural power. Yet DIPRs may become an important source of structural power because, in digital capitalism, a company’s control of digital infrastructure may allow it to not only shape social interactions but also economic development, because economic activity comes to rely on the infrastructure. Second, our cases also show that while financial regulators have considerable power to shape the development of the FinTech industry and thus the future relative (infra)structural power resources of players within that industry, historical power relationships shape regulatory preferences with regard to financial innovation. Thus, the extent to which regulators use the opportunity to reshape power relationships as financial sectors digitalise has long-term, structural roots.

Footnotes

Acknowledgements

We are very grateful to our interviewees for their time and sharing of valuable expertise and to Rosienna Sham for research assistance. In addition, we would like to thank the participants of the workshop ‘Power struggles and transformative forces: The transformations of the banking sector’ at the University of St Gallen (26–27 October), Sebastian Heidebrecht, Juvaria Jaffri, Michael Kemmerling, Timo Seidl, Alexa Zeitz and two anonymous reviewers for helpful comments. Special thanks also go to Elsa Massoc and Kerem Coban for their support.

Consent to participate

The authors declare that they obtained free and informed consent in verbal format from their interviewees.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge the support from the Independent Social Research Foundation (ISRF) through a flexible grant for small groups (FG11) for this research project.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.