Abstract

This article demonstrates that financial development in the United States has heightened the vulnerability of both sides of regional banks’ balance sheets to financial market fluctuations, drawing on the concept of financial circulation of bank deposits. It first argues that financial development provides diversified short-term investment channels for non-financial sectors to manage their liquid asset holdings. Since banks intermediate money circulation, changes in liquid asset portfolios inevitably result in sudden inflows and outflows of deposits to these banks. These deposit flows are highly clustered during specific financial phases and are subject to financial volatilities rather than local business cycles, making regional banks’ liabilities volatile with market fluctuations. Second, to mitigate increased deposit instability, regional banks hold a higher proportion of marketable securities to manage liquidity. But the mark-to-market nature of security prices further puts potential instability on the asset side of banks’ balance sheets. Extremely, the sudden volatility in the financial markets could simultaneously cause deposit flights and choke off refinancing capability, causing a bank run.

Keywords

Introduction

Over the past four decades, the size distribution of banks in the United States has undergone significant transformation (McCord and Prescott, 2014). According to the FDIC Call Report, between 1980 and 2022, the number of banks insured by the Federal Deposit Insurance Corporation (FDIC) dropped from 14,000 to approximately 4,000, with regional banks comprising the majority of this decline. Regional banks are recognized in the economic geography literature for their high managerial expertise and strong proficiency in serving local borrowers, attributed to their superior access to local borrowers’ information 1 (Flögel, 2018; Mayer et al., 2021). Despite the numerous advantages of regional banks, why has their number in the United States declined so dramatically?

Regional bank instability is often attributed in the literature to external speculative financial flows (Dow, 1987), regulatory evasion driven by financial innovations (Bryan et al., 2017), or significant regulatory changes (Bieri, 2017). This article, however, offers an alternative perspective. It argues that in a financially advanced, market-based economy with a fragmented banking system, 2 such as the United States, regional bank instability is fundamentally rooted in the dynamics of financial circulation of bank deposits and the inherently unstable nature of bank balance sheets brought about by financial development.

This analysis examines deposit circulation and structural changes in the balance sheets of regional banks to provide a systematic understanding. It is grounded in balance sheet accounting principles and Chick’s (1992) evolutionary perspective on banking, which identifies five stages of development aligned with transformations in the monetary system. While not strictly adhering to Chick’s classification, this article draws on her ideas to demonstrate that banking development is intrinsically linked to the evolution of the monetary system, with operational models adapting to its structural changes over time.

In this article, “financial development” refers to the structural changes in the US financial system since the 1970s, driven by financial innovations and regulatory shifts. This contrasts with the mainstream view, which perceives financial development as a linear progression from deregulation and financial innovations to easing borrowing constraints, diversifying investment channels, and ultimately stimulating economic growth (King and Levine, 1993; Pagano, 1993). This article holds that while financial innovations and deregulation drive the rapid expansion of financial assets and channels, financial development—viewed as a structural transformation of the financial system—fundamentally alters the operational dynamics and balance sheet structures of financial institutions, particularly in this article, regional banks.

To examine the impact of financial development on regional banks, this article begins with a simplified framework that excludes financial development. It demonstrates that the lending structures of regional banks are influenced by local economic conditions and business cycles. While inter-regional trade may cause imbalances in regional balance-of-payment accounts, the interbank market is crucial in managing such deposit movements. Thus, regional banks’ instability stems largely from undiversified asset structures vulnerable to short-term speculative deposits from outside their operational areas.

By examining how financial development impacts the liquid asset management of non-bank sectors, this paper presents two arguments. First, it contends that financial development provides diversified investment channels for non-bank sectors to manage their liquid assets. It then draws on the financial circulation of bank deposits to analyze how the transformation of liquid asset portfolios intensifies the challenges regional banks encounter in managing liabilities. Here, the financial circulation of bank deposits refers to the circulation process within the financial system, where demand deposits are exchanged for financial instruments to earn monetary returns and are recycled back into current account balances.

Second, regional banks have to seek a way to grapple with financial development to bear down the incremental instability of deposits. By holding more marketable securities and relying on short-term refinancings (repos), regional banks have greater autonomy to cope with increasingly volatile liabilities. The reliance on and holding of securities to manage liquidity generates two potential outcomes. On the one hand, regional banks gain from liquidity surges during financial booms, significantly enhancing their lending capacity. On the other hand, financial market volatility can trigger a rapid outflow of deposits and a decline in security valuations, depleting liquidity and impairing refinancing capabilities. Hence, regional bank instability may stem not only from external speculative financial flows but also from the financial circulation of deposits and the inherently unstable balance sheet structures shaped by financial development.

The article proceeds as follows. The next section discusses the literature on regional banking. The subsequent section introduces the regional banking framework excluding the influences of financial development. This is followed by another section that introduces the influences of financial development. The main argument unfolds in the following section, which demonstrates how the financial circulation of bank deposits and financial development generate unstable balance sheet structures for regional banks. The penultimate section presents two policy implications and one recommendation for regional banks. The final section concludes.

The geography of money and banking

Research on regional financial disparities and instabilities has been a longstanding tradition in economic geography and heterodox economics (Dymski and Shabani, 2017; Leyshon and Thrift, 1997; Martin, 2011; Sokol, 2013). Generally, there are two interwoven strands in the literature, of which one underscores the influences of the geographical distribution of financial institutions on local economic growth, while the other focuses on the origins of regional financial instability (Dow, 1987; Dymski, 2005; Flögel, 2018; Martin, 2015).

The Post-Keynesian framework, analogous to economic geography, acknowledges that “location” transcends mere physical distance, encompassing social, relational networks, and structural dimensions via uncertainty and liquidity preference for borrowing and lending (Dymski and Kaltenbrunner, 2021; Nogueira et al., 2015). The Post-Keynesian approach emphasizes that financial agglomeration generates uneven loans availability among regions because of different degrees of liquidity preference (Chick and Dow, 1988; Dow, 1987). It classifies regions into the “financial core” that dominates a country’s industries, businesses, and financial services and “peripheries” that rely on the core for financial services. It posits that the concentration of financial institutions in the financial core effectively reduces perceived uncertainty for both borrowers and banks of the core. Since liquidity preference levels are closely linked to perceived uncertainty, this reduction in uncertainty leads banks and entrepreneurs in the core to exhibit lower liquidity preferences. Consequently, lower liquidity preferences in the core increases both banks’ willingness to lend and borrowers’ willingness to borrow, resulting in higher levels of loan issuance. In contrast, peripheral regions face challenges in loan granting due to the higher liquidity preferences of local bankers and entrepreneurs. Hence, disadvantaged peripheral regions experience more pronounced funding gaps compared to the financial core.

Research by economic geographers primarily focuses on how and to what extent information influences local proximity between banks and firms, as well as its impact on the allocation of bank credit. This focus stems from the recognition in the literature that the distinctive value of the regional banking system lies in its information and lending expertise (Dymski, 2018; Garmaise and Moskowitz, 2004; Leyshon and Pollard, 2000; Pollard, 2003).

The economic geography literature suggests that, unlike “hard information,” which can be efficiently transmitted, “soft information” is embedded in local environments and requires banks to integrate into regional social networks. This integration enables local bankers to reduce information costs and better support local firms, underscoring that information technology and standardized lending practices cannot fully overcome geographic information barriers (Pollard, 2007; Zazzaro, 1997).

In this regard, the local socio-economic relational networks serve as efficient conduits for the transmission of soft information, nurturing mutual trust, facilitating knowledge sharing, enabling the utilization of social capital, and ultimately supporting well-informed credit decision-making (Degryse et al., 2009; Uzzi and Lancaster, 2003; Zhao and Jones-Evans, 2017). As borrowers inherently possess better localized knowledge about project prospects and collateral quality, the centralized financial system cannot perfectly transmit information from local borrowers to arms-length lenders, thereby hindering credit availability for local borrowers (Alessandrini et al., 2009, 2010; Papi et al., 2017).

To some extent, although the Post-Keynesian and economic geographers investigate the issue from different approaches, they tend to agree that the hitherto continuous concentration trend of financial institutions toward financial centers in those market-based economies exacerbates the financing difficulties faced by enterprises in underdeveloped areas (Dow, 1999; Klagge and Martin, 2005).

In theoretical frameworks where regional banks leverage local networks to mitigate uncertainty and information asymmetry, the literature often attributes the generation of financial risks to factors beyond the regional level. These risks arise from the sudden movement of speculative financial flows between developed and peripheral regions under the core-periphery model (Cerpa Vielma and Dymski, 2022; Chick and Dow, 1988; Dow, 1987), external investment portfolios from current account surplus countries in the global savings glut literature (French et al., 2011), or the extraction of labor value by international financial centers and the use of financial structures designed to evade regulatory oversight in economic geography literature (Bieri, 2017; Bryan et al., 2017; Haberly and Wójcik, 2017; Sokol, 2013).

While the existing literature provides a solid theoretical foundation for understanding the influence of money and finance on regional economic growth and instability, the division of the monetary system into financial cores and peripheries, or the overemphasis on geography in relation to information accessibility, limits its capacity for comprehensive and systematic analysis (Dymski, 2018). Dividing the monetary system based solely on regional differences in information and regulation is unreliable, as instability can spread across regions (Bryan et al., 2017; Martin, 2011, 2015). The analysis below provides a coherent and systematic examination of the complex relationship between the financial system and regional banking, grounded in an evolutionary perspective on banking and finance.

The regional banking system: A framework excluding financial development

Bank lending

Banks are believed to serve as focal points for unraveling the complex socio-economic milieu in the economic geography literature, as they act as the bridge connecting all parties involved in the capitalist production model (Leyshon and Pollard, 2000). This perspective aligns with the Post-Keynesian monetary endogeneity approach, which asserts that the demand for bank loans drives money creation (Lavoie, 2014). Building on the economic geography and Post-Keynesian approaches, this section examines regional banking dynamics prior to the emergence of financial development in the 1970s.

In the monetary endogeneity model, money created through bank lending for production is recycled back to capitalists via industrial production and sales, with the cycle completing as the money is destroyed through capitalists’ repayment to the banking system (Rochon, 1999). While the endogenous theory emphasizes that money demand drives money creation, it also recognizes that banks can only create money for borrowers who meet their eligibility requirements (Lavoie, 2014; Palley, 2002). Banks evaluate customers’ creditworthiness and base loan terms and amounts on their potential profitability, with financial viability serving as a prerequisite for loan access (Parguez and Seccareccia, 2000). When no eligible borrowers exist, or banks prioritize safety over risk, they may resort to credit rationing (Chick and Dow, 2002).

Requiring qualified collateral is a key risk mitigation strategy for banks (Benmelech and Bergman, 2009), as collateral quality and valuation significantly reduce the risks associated with assessing borrowers’ uncertain profits. Federal Reserve Y-14 data indicates that 84% of commercial and industrial loans are secured, with higher collateral quality lowering interest rates (Luck and Santos, 2019). Economic geographers highlight real estate, deeply embedded in local socio-economic networks, as pivotal collateral. Land-based assets, shaped by housing prices and property market depth, are commonly used to secure loans and reduce borrowing costs (Dicken and Malmberg, 2001).

In this regard, local economic growth impacts regional banks by expanding the pool of eligible borrowers and improving access to creditworthy collateral for securing loans. Within the endogenous money framework, regional growth and business cycles influence money creation, as banks adjust lending standards and loan issuance to regional variations in business scale, profitability, and development prospects. Thus, bank deposit creation is closely tied to local business demand.

Bank refinancing

As regional production grows and inter-regional trade expands, income and expenditure disparities between regions may emerge, causing imbalances in regional balance-of-payment arrangements or exhibiting certain periodic patterns (Thirlwall, 1978, 2012). Assuming all business transactions occur exclusively through the banking system without cash withdrawals, these disparities can generate cyclical or continuous inflows and outflows of bank deposits across regions. Deposit outflows necessitate regional banks to transfer limited reserves to surplus-region banks, prompting deficit-region banks to engage in the interbank market to address inter-regional payment demands and alleviate the impact of cross-regional deposit outflows.

Given the numerous participants in the interbank market, any regional bank with ample liquidity can provide short-term liquidity to a regional bank experiencing a reserve shortfall; it does not necessarily need to be the bank receiving deposit inflows from a current account surplus (Kohler, 2022).

By addressing liquidity shortfalls from current account deficits through the interbank market, regional banks can enhance their local lending capacity and effectively manage cyclical fluctuations in reserve flows associated with inter-regional business cycles (Chick, 1992, 2013). Therefore, the interbank market bridges regions with diverse business cycles, addressing periodic liquidity imbalances and fostering national banking interconnectedness, thereby overcoming geographical boundaries and shortening lending intervals.

Bank instability

In this regional banking framework, instability stems mainly from disparities in speculative investment opportunities and regional variations in monetary wealth accumulation (Dymski and Shabani, 2017). These disparities in inter-regional speculative investments primarily stem from the discovery of untapped natural resources or fluctuations in property prices. Hence, certain regions may attract speculative deposit inflows from areas with surplus monetary wealth but limited profitable investment opportunities (Chick and Dow, 1988; Dow, 1987).

While the inflow of external speculative deposits into a particular area can positively impact local asset prices or stimulate the expansion of bank loans, the abrupt withdrawal of deposits can trigger a rapid decline in local asset prices and an upsurge in non-performing loans. Since regional banks’ assets are tied to local economy, the absence of diversified loan structures makes regional banks vulnerable to sudden local economic fluctuations. Thus, this may result in the potential emergence of a regional banking crisis, only due to the failure of certain types of loans.

To conclude, in this regional banking framework, loan issuance predominantly reflects the local business cycle, while inter-regional deposit flows are shaped by balance-of-payment dynamics between regions. The evolution of the interbank market has fostered an interconnected network, enabling regional banks to manage cross-regional deposit fluctuations and coordinate liquidity with other regional banks from different regions.

Regional bank instability often arises from speculative short-term deposit flows from other regions. The speculative inflows can temporarily inflate regional asset prices beyond their underlying business conditions. However, abrupt deposit outflows leave regional banks particularly vulnerable due to their lending portfolios’ heavy reliance on the value of local assets.

Financial development

Financial development initially refers to the expansion of long-term financing mechanisms in the capital market, which channel substantial long-term funding into large industrial corporations. The burgeoning development of the stock market and corporate security market allows industrial capitalists to finance investments without solely relying on their own capital or bank loans. This access to long-term financing alleviated the significant constraints industrial capitalists faced within the banking system in the late nineteenth century (Minsky, 1995; Toporowski, 2020).

Since the late 1970s, particularly in the United States, high inflation and the draconian monetary policy of the Volcker Shock rendered traditional bank deposits unsafe for mitigating increasing interest rate risks (Wray, 2009). Meanwhile, to revitalize the sluggish economy, subsequent regulatory transformations aimed at building a more market-oriented economy fostered a lenient regulatory climate where banks and non-bank financial institutions (NBFIs) could compete more freely and comprehensively. The Riegle-Neal Act of 1994 eliminated restrictions on interstate banking operations (Bieri, 2017), and the Financial Services Modernization Act of 1999 lifted the prohibition on commercial banks operating alongside other NBFIs (Cerpa Vielma et al., 2019). These policies, which remove previous restrictions on cross-market and mixed operations between banks and NBFIs, aim to foster a dynamic financial system that promotes efficient growth. Hence, these policies and the resulting financial innovations have initiated another phase of financial development within the US financial system.

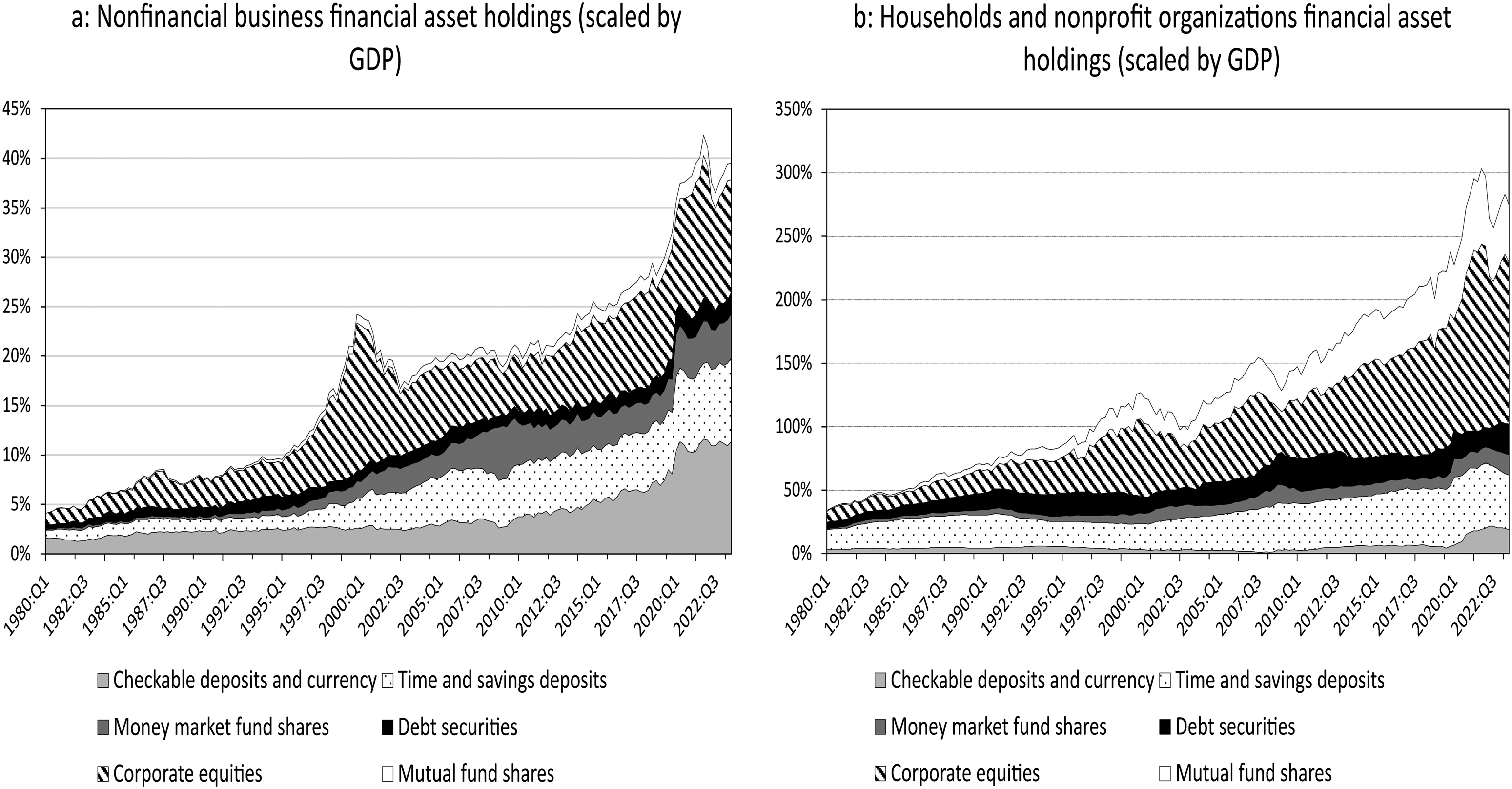

The Financial Accounts data suggest that the US non-financial sectors hold an increasingly higher amount of liquid assets relative to GDP. Figure 1(a) shows that the ratio of financial liquid assets owned by US non-financial businesses in relation to GDP has risen from less than 6% in 1980 to 40% in 2023. The household sector has experienced even more astonishing growth. As depicted in Figure 1(b), the ratio soared from 34% in 1980 to around 300% in 2023. Not only has the total amount of liquid assets increased, but market-based asset allocation channels other than bank deposits are also becoming increasingly prominent. This trend indicates that the US non-financial sectors are accumulating more liquid assets while significantly diversifying their investment channels for retained earnings. The liquid asset holdings by US non-financial sectors. Source: US financial accounts (see: https://www.federalreserve.gov/releases/z1/), Federal Reserve Bank at St. Louis (see: https://fred.stlouisfed.org/series/GDP). Own calculation.

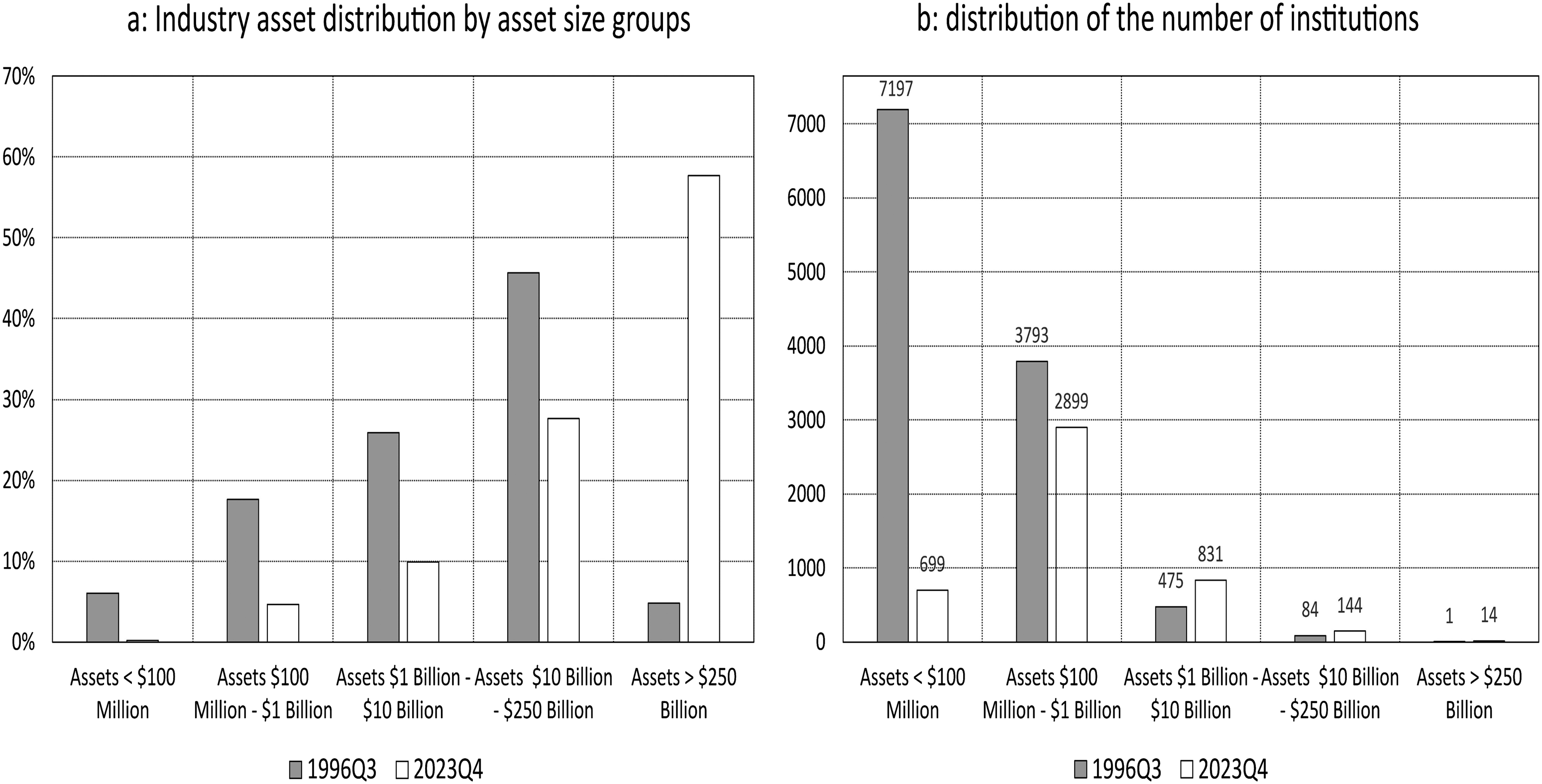

While the expansion of non-bank financial investments provides new and broader channels for private sectors to manage liquid asset portfolios and hedge risks, financial development brings more than merely increasing the volume and variety of financial assets to the system. If the expansion of financial assets is seen as the cumulative outcome of structural changes within the financial system, then the banking sector, as an intermediary of the system, will inevitably have its structure and operational dynamics impacted and co-evolve with these changes. Figure 2(a) and 2(b) illustrate the ongoing decline of small and medium-sized banks, which predominantly consist of regional banks within the American banking system.

3

The next section will delve into how financial development introduces new vulnerabilities to the balance sheets of regional banks. The distribution of bank asset and the distribution of the number of banks by asset size groups. Source: FDIC (See: https://www.fdic.gov/analysis/quarterly-banking-profile/index.html).

The regional banking system: structural changes brought about by financial development

Bank lending

Despite the profound changes in liquid asset management for non-financial sectors brought about by financial development, several factors contribute to regional banks’ lending practices remaining closely tied to regional business cycles in the absence of speculative euphoria.

Firstly, while regional banks may have lost some corporate customers, they often find themselves with limited alternatives, leading them to expand either mortgage lending or personal loan businesses. These loans closely correlate with local economic growth under normal economic conditions.

Secondly, addressing lending uncertainties requires regional banks to understand the regulatory, institutional, and socio-economic networks in their areas of operation to mitigate risks. Much of this knowledge is “soft information,” crucial for assessing borrower profitability and collateral value, thus reducing risks when granting loans (Pollard, 2007). Consequently, acquiring essential borrower information and reducing potential risks can be achieved by embedding the bank’s management within the invisible and tacit socio-economic fabrics of the operational region (Dymski and Kaltenbrunner, 2021; Pollard, 2003).

Third, since financial development does not change the endogenous nature of deposit creation, borrowers’ demand for loans and banks’ loan issuance still largely depend on the economic conditions and business cycles within their regions. During local economic booms, banks may find many high-quality borrowers seeking loans, while in downturns, the number of eligible borrowers may decline. Thus, banks’ lending structures are primarily shaped by regional business cycles, as they depend on eligible customers to initiate borrowing and generate new loans.

Bank liabilities

While regional banks remain crucial for granting loans to support regional economic growth, the diversification of financing channels driven by financial development has fundamentally altered their operational environment. Minsky (1995: 361) stated that “a basic aspect of the structure of capitalist economies is given by interrelated balance sheets, income statements, and the time series of cash flow commitments embodied in the financial instrument.” This indicates that structural changes in liquid asset management within non-financial sectors inevitably affect the financial sector, leading to changes in cash flows and structural adjustments within capitalist intermediaries—banks. The impact on regional banks first appears on the liability side of their balance sheets through the financial circulation of deposits.

In the works of Fisher (1928), Keynes (1930/1971), Kalecki (1941), and Minsky (1957), money circulation is divided into industrial and financial circulation, based on the nature of the products exchanged. Industrial circulation involves using money to acquire real goods and services, whereas financial circulation refers to the purchase and exchange of financial assets and recycled back to money balances. Given that bank deposits are primarily used as a means of payment today, the term “financial circulation” can be more precisely defined as “the financial circulation of bank deposits.” This refers to the process within the financial system in which demand deposits are exchanged for financial instruments to generate monetary returns and subsequently recycled back into current account balances.

In the context of financial circulation, the general principle is that when interest rates on all financial instruments, including term deposits, are very low, money is likely to be retained in current accounts as demand deposits. However, if financial instruments offer higher interest rates—after accounting for investment costs—compared to term deposit rates, bank deposits are likely to be transferred into non-bank financial instruments (Keynes, 1930/1971; Kalecki, 1941, 1954; Sawyer, 2001; Toporowski, 2022).

In the era of Keynes and Kalecki, financial instruments were largely limited to term deposits, bonds and stocks. However, financial development, especially with the rise of NBFIs, has diversified the range of available financial products, offering investment options with varying maturities, risks, and interest rates. The emergence of these diverse investment products, particularly fixed-income-like products such as money market fund shares and mutual fund shares, has significantly increased the variety and quantity of investment options available to investors along the yield curve.

Along the yield curve, investors can find products beyond term deposits that match their risk, return, and maturity preferences. Thus, term deposits have shifted to serve as a reference point on the yield curve for comparison with other financial products, rather than being one of the few available investment options as in the past. Compared to term deposits, investors may choose shorter-term financial instruments with slightly lower rates or products with the same maturity but higher interest rates and relatively greater risks, enabling interest rate arbitrage along the yield curve while aligning investments with their risk tolerance.

In addition to fixed-income instruments, investors may opt to enter markets such as the stock market or cryptocurrency markets, driven by short-term capital gain expectations. In other words, the broad array of non-bank financial products available caters to the asset allocation needs of investors with diverse risk tolerances and maturity preferences, thereby substantially diminishing the role of term deposits in financial asset portfolios.

While time deposits are no longer a primary choice for financial investment, non-banks rely heavily on demand deposits for transaction clearing when switching between financial products other than term deposits. Each time investors purchase financial products, they transfer deposits from their bank current accounts to NBFIs’ bank current accounts. Conversely, when redeeming matured assets from NBFIs, investors receive a deposit transfer from the NBFIs’ banks. For non-banks, demand deposits thus function as their means of payment within the financial circulation.

However, since banks use reserves rather than deposits for interbank settlements, the transfer of bank deposits between investors’ banks and NBFIs’ banks requires regional banks to conduct corresponding reserve payments. For example, when investors transfer deposits to purchase financial products from NBFIs, peripheral regional banks must clear these transactions with financial center banks, drawing on their limited reserve holdings. Given the wide range of financial products offered by various NBFIs along the yield curve, the frequent purchasing and conversion of these products by investors compels their banks to frequently access the interbank market to settle transactions using limited reserves.

Additionally, the presence of NBFIs extends and complicates the entire chain of financial circulation. When NBFIs receive deposits from investors, they do not retain these deposits in their payment accounts as assets. Instead, they invest and allocate the received deposits based on interest rates and investment costs, using them to acquire other financial assets from various economic units. Hence, as NBFIs frequently allocate bank deposits in exchange for various financial products based on their own risk-return calculations, the regional banks that service NBFIs—similar to peripheral regional banks—must also manage frequent inflows and outflows of deposits. In other words, banks in financial centers are required to actively participate in interbank transactions, frequently transferring reserves in and out.

Monetary endogeneity theory posits that bank deposits are created through lending and extinguished through loan repayment. However, the preceding analysis of financial circulation reveals that, during the intermediate phase between deposit creation and destruction, the extended and intricate financial circulation chain imposes substantial liquidity challenges on regional banks. These challenges persist regardless of whether the banks operate in core or peripheral regions and occur without directly affecting the processes of deposit creation or destruction.

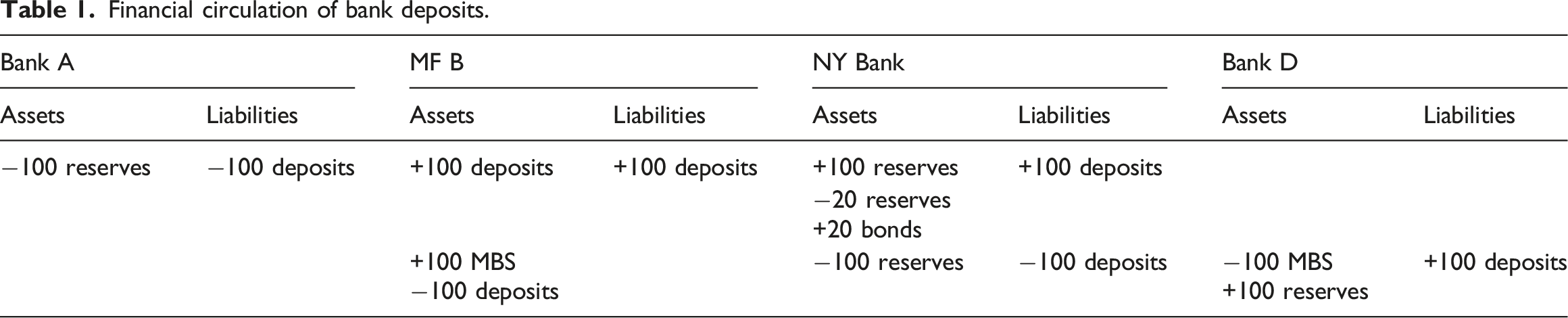

Financial circulation of bank deposits.

Suppose depositors at Bank A decide to transfer their demand deposits to MF B in exchange for mutual fund shares after comparing the yield and maturity between term deposits at Bank A and MF shares. Since MF B is not a bank, the deposits transfer is facilitated by its bank—NY Bank. This means that Bank A, as the depositor’s bank, transfers reserves to MF B’s bank, NY Bank, for interbank settlement. This transaction causes simultaneous changes in the balance sheets of Bank A, MF B, and NY Bank. Bank A records a reduction in both reserves and deposits, while NY Bank records an increase in reserves along with a corresponding increase in deposits. Meanwhile, MF B records an equivalent increase in deposits on both sides of its balance sheet.

Suppose MF B does not immediately allocate the deposits received but instead waits for investment opportunities in the financial market to build its portfolio. During this period, assuming NY Bank already holds a certain proportion of cash and reserves, and given that the number of eligible borrowers in its region has not changed significantly in the short term, NY Bank decides to use a portion of the reserves it received to purchase bonds for higher returns. By utilizing only, a portion of these reserves to exchange for bonds, NY Bank also participates in the financial circulation process.

Subsequently, MF B decides to allocate all the deposits it received by purchasing mortgage-backed securities (MBS) from another regional bank, Bank D. This transaction requires NY Bank, acting as MF B’s bank, to transfer reserves to Bank D. Since NY Bank has already used part of its reserves to purchase bonds, it must access the interbank market for short-term liquidity if its reserves are insufficient; otherwise, it will face a liquidity crisis. 5

Thus, even in this simple example, what initially appears to be a straightforward transfer of bank deposits for mutual fund shares involves the coordination of three banks through two interbank settlements, each requiring corresponding transfers of bank reserves. Both Bank A and NY Bank need to maintain sufficient liquidity positions to manage interbank settlements; otherwise, they risk facing a liquidity crisis.

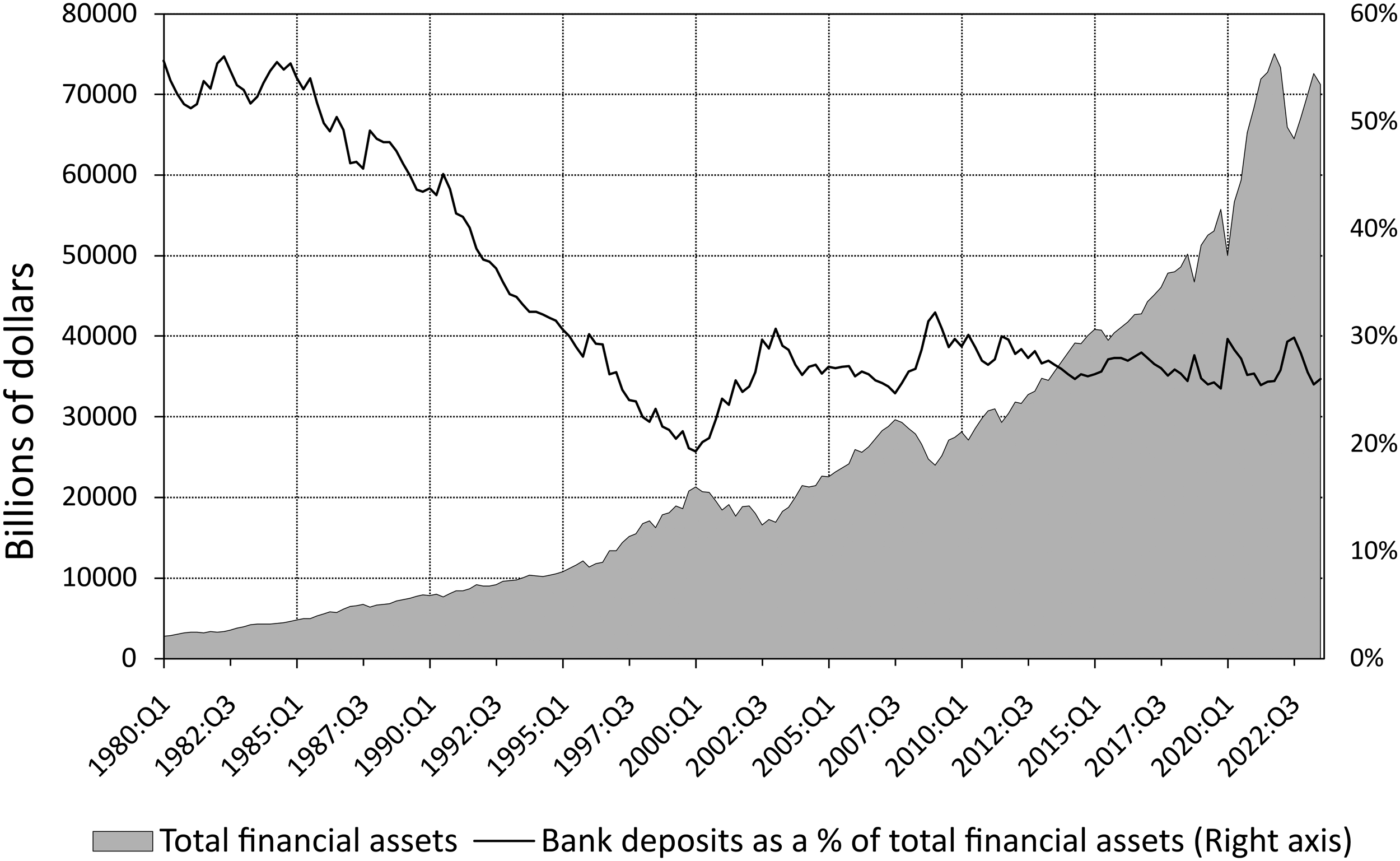

Figure 3 depicts the shift in the proportion of US non-financial sectors’ bank deposits to total financial asset holdings and the growth of total financial assets. Since 1980, total bank deposits as a percentage of total financial assets declined from 56% to the lowest point—19% in 2000. While this ratio rebounded after 2000, it has since remained within the 20% to 30% range. In contrast to the relatively stable ratio of bank deposits to total financial asset holdings since the new millennium, the total amount of financial assets has surged from approximately 20 trillion to 75 trillion over the same period. The total amount of financial asset holdings and the ratio of bank deposits to total financial assets held by non-financial sectors. Source: US financial accounts. Own calculation.

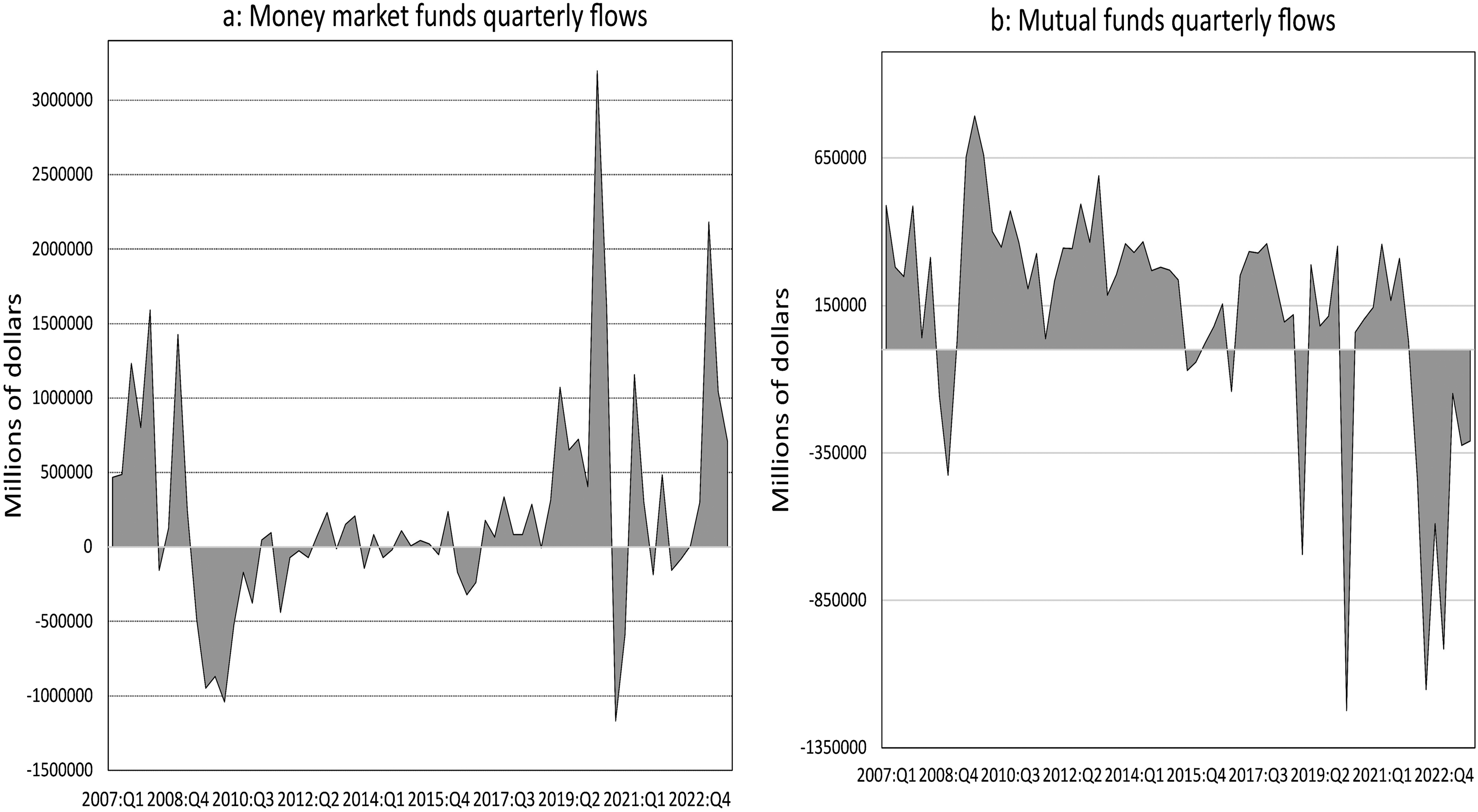

Figure 4 illustrates the patterns of inflows and outflows of money market funds and mutual funds between 2007 and 2022. It is evident that these financial flows show highly concentrated patterns in specific periods. Notably, between 2010 and 2018, the financial flows of MMFs remained stable, whereas significant inflows and outflows occurred during the periods from 2007 to 2010 and from 2019 to 2022. In contrast, MFs experienced nearly continuous substantial increases from 2007 to 2017 but faced extreme and concentrated outflows beginning in 2018. Since neither MMFs nor MFs are banks, if their investors are spread across different regions, these inflows and outflows require corresponding regional banks to facilitate interbank settlements. When these funds experience significant inflows, it indicates that peripheral banks are facing deposit outflows. Conversely, when these funds experience significant outflows, the regional banks associated with these funds also encounter large deposit withdrawals. In other words, whether these movements are inflows or outflows, the sharp and concentrated fluctuations in financial flows are directly correlated with significant fluctuations in the bank deposits and liquidity positions of the corresponding banks. Money market funds and mutual funds quarterly flows. Source: US financial accounts. Own calculation.

As argued above, bank deposits serve not only as financial instruments but also as transaction intermediaries for NBFIs and the non-financial private sector. This indicates that the substantial growth in liquid financial assets, combined with a relatively stable proportion of bank deposits, inevitably leads to more frequent shifts between bank deposits and financial products at the aggregate level. Unlike routine business transactions, these deposit movements are concentrated in specific financial periods and primarily driven by fluctuations in financial markets, which are more unpredictable and volatile. As a result, modern regional banks face increased challenges in effectively managing sudden deposit transfers and the associated interbank settlements. 6 Failure to meet these deposit transfer demands can result in severe liquidity risks, compelling regional banks to explore new refinancing channels to manage these fluctuating deposit structures.

Bank refinancing and unstable balance sheet structures

The increasing amount of bank deposits circulating around different financial markets generates more irregular deposit flows for banks than traditional commercial activities. This unpredictability renders it difficult for banks to manage sudden deposit flights using conventional refinancing methods. As financial development continues to impact banks’ liability structures, they require more flexible liquidity management methods to deal with the increments of uncertainty of deposit movements.

Financial development enables banks to acquire convenient refinancing channels by providing long-term marketable securities as collateral in the interbank market. Repos (repurchase agreements) are collateralized borrowing through which bonds are pledged at the interbank market for liquidity and bought back at a slightly higher price after a short period. The value a bank could borrow through repo lending largely depends on the market valuation of the security the bank provides. Holding marketable securities empowers banks to promptly tap into the market to address liquidity shortages because repos reduce interbank lending costs and enhance overall market liquidity (Gabor, 2016; Gorton and Metrick, 2012).

While the marketable securities held by banks expand the liquidity availability and relieve the pressure on regional banks to manage unpredicted deposit fluctuations, the holding and dependence on securities, in return, exposes the banks’ asset side of balance sheets to changes in financial markets. It is true that relying on repos lifts restrictions on deposit volatility and delegates greater autonomy to launch new lending for regional banks when the overall market liquidity condition is abundant (Adrian and Shin, 2010; Shin, 2008). However, the mark-to-market nature of these securities also makes the valuation of the securities held by banks go in tandem with the market fluctuations, thereby putting financial volatility into the asset side of the balance sheets along with the underlying regional economic cycles.

The volatility of tradable assets held by banks paves the way for banks to rely more heavily on short-term market refinancing and greater utilization of derivatives to hedge the risks involved. Consequently, the imperative to address unstable short-term financing structures has compelled regional banks to further retain a greater quantity of and diversified ranges of marketable securities. In a sense, financial development introduces more diversified refinancing and asset management channels for banks, simultaneously necessitating a heavier dependence of banks on financial markets (Toporowski, 2010). As a result, a substantial portion of banks’ asset sides is influenced by fluctuations in financial cycles rather than solely by local business cycles.

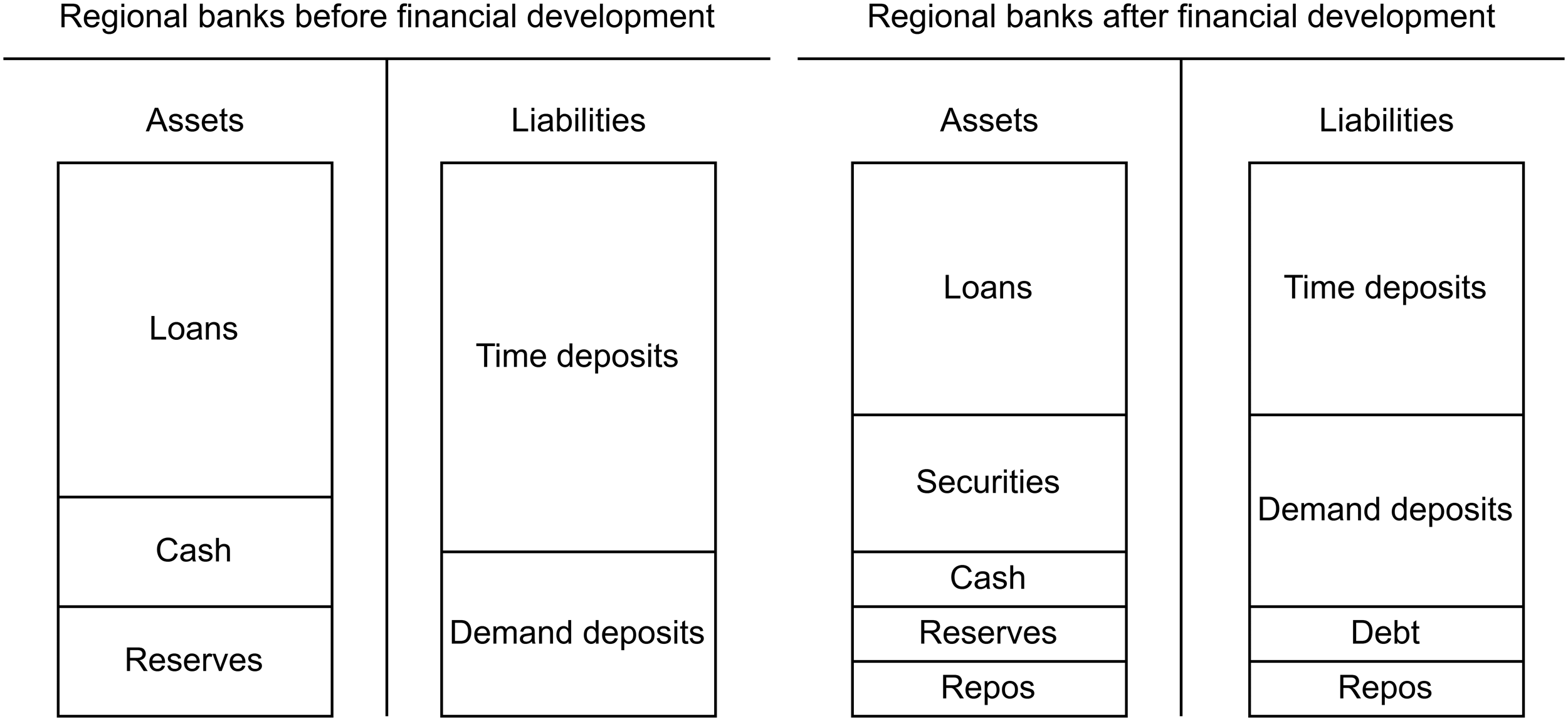

Figure 5 compares the balance sheet structures of regional banks before and after incorporating the influences of financial development. Notably, security holdings emerge in and gradually constitute a more significant portion of the bank’s assets, while the relative proportion of time deposits experiences a decline. The structural changes in regional banks’ balance sheets and the non-bank sectors’ liquid asset management suggest that both sides of regional banks’ balance sheets are subject to financial market volatilities rather than solely the underlying regional economic fluctuations. The comparison of regional banks’ balance sheets before and after incorporating the influences of financial development. Source: own elaboration.

During extreme market fluctuations, abrupt changes in the spread between financial instrument returns and time deposit interest rates can trigger significant and sudden shifts in deposit movements. For example, a sharp increase in the spread may cause deposit outflows from peripheral regional banks, while a rapid narrowing of the spread or heightened financial market risks could prompt investors to redeem financial products from NBFIs, resulting in deposit outflows from the regional banks where these NBFIs are based. Regardless of the type of regional bank affected, their reliance on securities for refinancing makes them particularly vulnerable to such deposit movements, as the same factors—changes in interest rates and risk levels—can significantly impact the valuation of their securities holdings, thereby undermining their ability to obtain refinancing in the interbank market. Combined with the reduction in refinancing capability, deposit outflows could rapidly drain banks’ reserves and trigger a liquidity crisis within a short timeframe. 7 Therefore, while securities held by regional banks provide liquidity during periods of financial prosperity, they also introduce instability during financial distress due to value fluctuations. Consequently, both sides of their balance sheets are now exposed to financial market volatility rather than being exclusively influenced by regional business cycles.

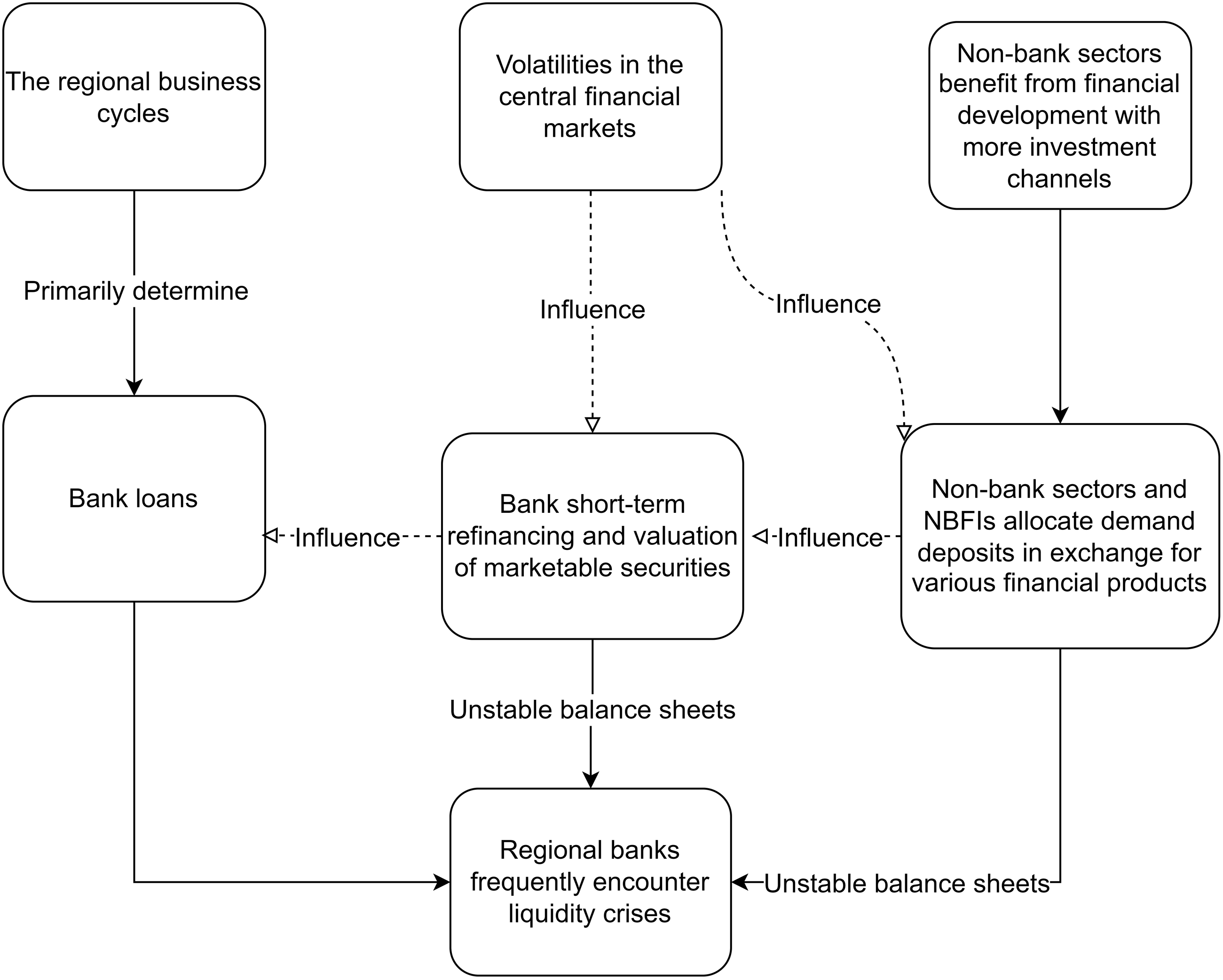

Figure 6 illustrates how the financial circulation of bank deposits adds instability to the regional banking system. Financial development initially offers regional non-bank sectors more financial investment channels for managing their liquid assets. The frequent and volatile exchange between bank demand deposits and financial instruments directly impacts the liquidity positions of different regional banks. To address these deposit movements, regional banks maintain a larger proportion of securities for interbank refinancing and liquidity management. This reliance on repos and securities enables regional banks to expand loan issuance and relax lending criteria during periods of abundant market liquidity, thereby influencing credit availability for regional businesses. However, this balance sheet structure also makes banks vulnerable to market volatility, potentially triggering liquidity crises during periods of financial turbulence. The instability of regional banks after financial development. Own elaboration.

Implications for financial stability

The traditional approach to preventing bank failure involves restricting banks from taking excessively risky loans or lending beyond their capital base. While Post-Keynesians acknowledge that money is endogenously created by banks, they also recognize that a bank’s failure stems from the poor quality of its assets being too risky (Lavoie, 2014). Although the 2008 financial crisis highlighted new changes introduced by financial development and NBFIs to banking operations, policy recommendations such as limiting banks’ leverage ratios or restricting their use of repos for financing long-term projects remain closely focused on bank lending activities (Gorton and Metrick, 2012; Shin, 2009). However, this article highlights that deposit fluctuations and liquidity crises in regional banks, driven by financial circulation, are unrelated to asset quality or bank leverage levels. Current regulatory measures are inadequate to address this issue. To stabilize the balance sheets of regional banks and enhance their resilience, two policy approaches can be implemented.

First, the Basel Accord assigns different risk weights to bank assets: commercial loans carry the highest, corporate bonds a moderate, and OECD government bonds a zero-risk weight. As banks’ equity requirements are tied to risk-weighted assets, riskier assets necessitate more capital (Drumond, 2009). Additionally, in calculating liquidity ratios, Basel III further classifies bonds, common stock, and reserves as high-quality liquid assets (HQLA) across three categories (1, 2A, and 2B), with government bonds and reserves placed in the highest tier (BCBS, 2013). This regulation framework, to some extent, incentivizes banks to increase their bond holdings. However, as demonstrated earlier, bond valuations can fluctuate with deposit outflows, meaning that holding large amounts of bonds may worsen regional banks’ liquidity positions rather than improve them during market turbulence. Liquidity ratio calculations for regional banks should, therefore, be refined to include only cash and reserves as Level 1 assets. Additionally, regulation could implement a required reserve ratio adjusted specifically for demand deposits. Since, as suggested by the monetary endogeneity model, the reserve ratio cannot limit a bank’s ability to grant loans, this new reserve ratio only aims to ensure that reserves are proportionate to the volume of demand deposits held. The thrust of these two adjustments is to promote the use of reserves and cash, rather than marketable securities, as the primary liquidity buffer.

Second, since interest rate changes are crucial for both deposit movements and bond valuations, active monetary policy can destabilize regional banks by rapidly altering rates and shifting investor risk perceptions. Significant interest rate changes can result in substantial deposit movements and reduce the refinancing capacity of regional banks during market turbulence. To mitigate these side effects, the central bank could enhance liquidity support for small and regional banks when raising interest rates. Similar to the Fed’s seasonal discount facility, the central bank could establish a new discount facility specifically for regional banks, allowing them to use bonds as collateral at face value with interest rates closer to the lower band of official rates. This would provide regional banks with affordable liquidity when facing liquidity crises. However, unlike other discount facilities, this tool should be temporary and activated only during periods of significant market volatility or interest rate hikes to prevent regional banks from using it for arbitrage.

For regional banks, while regional banks may demonstrate greater efficiency within local communities compared to larger bank holding groups (Chick, 2013; Flögel, 2018), they face significant challenges in managing liquidity crises triggered by financial circulation, which are not necessarily tied to asset quality or management expertise. Therefore, regional banks should adopt a conservative approach by prioritizing higher reserve levels over bonds as liquid assets. Banks like NY Bank discussed in this article should also be cautious of large deposit inflows, such as those from cryptocurrency investors rejected by larger banks. These banks should either limit these inflows relative to their capacity or set a daily transfer limit for each account based on their operational scope.

Conclusion

Regional banks are integral to the broader financial system, and shifts within this landscape inevitably impact their structures. Although regional banks embed themselves in local socio-economic environments to enhance management expertise and lending efficiency, systemic developments in the financial system can undermine micro-level management proficiency and stability. As financial development fosters a more interconnected monetary system and creates unstable balance sheet structures for regional banks, financial markets exert an increasingly pervasive influence on them.

This paper examines how financial development has led to unstable balance sheet structures in the US regional banking system. It argues that structural changes in the financial system have introduced new instabilities beyond the stop-and-go nature of speculative financial flows from external regions. The paper first demonstrates that regional banks’ lending structures are closely linked to local economic conditions and business cycles within a framework that excludes financial development. It highlights that regional bank instability in this framework stems from sudden shocks to their undiversified asset structures caused by short-term speculative deposit inflows from other regions.

It then argues that financial development has provided non-bank sectors with a wide range of investment opportunities. Drawing on the concept - financial circulation of bank deposits, it examines how changes in liquid asset portfolios complicate liability management for regional banks. It further contends that regional banks have to hold more securities to manage increasingly volatile deposits. While regional banks may enhance their liquidity positions by increasing securities holdings and using repos, this strategy presents two possible outcomes: benefiting from market liquidity during booms or suffering from deposit outflows and falling securities values during financial turbulence. Given the new instability challenges faced by regional banks, this article offers two policy recommendations and one specific suggestion for regional banks.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.