Abstract

To confront global challenges and to assert itself more firmly on the international stage, the EU has not only expanded its overall budget for external action. It has also increasingly deployed de-risking instruments, like blending and guarantees, aimed at leveraging financial resources from other actors. This raises important questions regarding the governance of European external finance. To unpack these issues, this paper reviews the rise and consolidation of blending and guarantees in the institutional and budgetary architecture of EU development policy. It traces how these instruments – originally conceived as vehicles for leveraging private sector finance – have instead led to the rise of European development banks, most notably the European Investment Bank. We argue that development banks offer a middle-ground, as the European Commission seeks to manage the tensions and trade-offs between leveraging financial resources, on the one hand, and retaining a strong steering role in its external action, on the other.

Keywords

Introduction

In 2021, the European Union (EU) created the Neighborhood, Development and International Cooperation Instrument (NDICI, also referred to as ‘Global Europe’), including an upgraded version of the European Fund for Sustainable Development (EFSD), the EFSD+. They represent additional innovations within the EU’s external financing landscape, which has been continuously changing since the 2008 global economic crisis. Only few studies have explored these transformations, their causes and implications 1 . Particularly, the functioning of innovative financial instruments within the new ‘Global Europe’ approach, such as blending facilities and guarantees, has been neglected. Given their centrality, this is a significant gap. Not only have they grown substantially in volume, but they are also central to the goal of leveraging private capital to meet development policy goals and to sustain the new geopolitical turn of the EU (e.g. Haroche, 2023).

The emerging literature on financialization of aid has investigated the global diffusion of financial mechanisms for development interventions as well as their main consequences (e.g. Allami and Cibils, 2018; Gabor, 2021, Allami and Cibils, 2018; Gabor, 2021, 2023 ). Embedded in what Gabor (2021) labels as the ‘Wall Street Consensus’, these reforms and practices support a new paradigm in development policy – ‘development as de-risking’ – that promotes the structuration of the ‘de-risking state’ in the Global South. However, this strand of literature has mainly focused on their role in reshaping the discourse and practice of development aid more broadly (e.g. Keucheyan, 2018; Mawdsley, 2018), including some albeit limited empirical analysis of their deployment in recipient countries (e.g. Gabor and Sylla, 2023; Löscher, 2019; Newman, 2020). It has focused less attention on how this has affected the roles and relationships of different actors within the donor landscape. Within this context, the EU represents a particularly relevant case. It is not only the world’s largest provider of overseas development aid (ODA), it has also played a pioneering role in the deployment of de-risking instruments – or so-called private sector instruments (see OECD, 2023) – in its development cooperation (EC, 2014). Moreover, it has done this in close partnership with the European Investment Bank (EIB). Conceived as a public investment bank for its member states, this has led to a significant evolution in the EIB’s role, increasingly assuming the role of the EU’s de facto development bank. While there are studies on the implications of this emerging apparatus within the EU (e.g. Cooiman, 2023; Di Carlo and Schmitz, 2023; Lepont and Thiemann, 2024; Mertens and Thiemann, 2019), there is no fine-grained analysis of the impact of new financial instruments on the development finance landscape and the sector’s governance and politics.

In this paper, we contribute to filling this gap with an analysis of the evolving use and governance of two key approaches to de-risking in ODA: blended finance and guarantees. Aimed at leveraging private financial resources, these instruments have provided an expanding domain for public development banks. In this vein, we place a particular focus on how these instruments are reshaping the role of development banks in general and the EIB specifically within European development finance. We argue that these de-risking instruments reveal an important tension between two partly countervailing trends. On the one hand, the EU is seeking to significantly scale-up European development finance. This is a response to China’s increasing global financial footprint as well the financing needs to meet the objectives of the Paris Agreement and the Sustainable Development Goals. On the other hand, intensifying geopolitical rivalry means that the EU is keen to ensure that European development finance aligns more closely with the EU’s geostrategic interests. While the use of de-risking instruments to leverage private resources responds to the former goal, its role in supporting the latter is less straightforward, as our subsequent analysis reveals.

In the next section of the paper, we situate the discussion on new financial instruments within the debate on the changing forms of state intervention in Europe and on the evolving role and priorities of the EU as an international actor. Next, we illustrate the rise and consolidation of blending and guarantees in the institutional and budgetary architecture of the EU development policy. We highlight the main drivers of this process, which include internal developments as well as the way in which the EU responded to a more challenging external environment. This is followed by a review of the main actors involved in these approaches. Somewhat counterintuitively, these are not private actors but a group of primarily European multilateral and bilateral development banks. The following section further explores their evolving role by analysing the governance of the major EU blending instruments and of the new guarantee mechanisms established by the EFSD+. We illustrate some limits and trade-offs inherent to the governance system and practices of the EU blending and guarantees approaches. Empirically, this section builds on documents from the EU institutions and a set of 12 in-depth interviews with staff from the European Commission (EC) and European development finance institutions (DFIs) (see Annex I).

Finally, in the conclusion, we reassess our findings and discuss their broader implications for EU development policy and the current debate on the financialization and geopoliticization of aid (e.g. Bougrea et al., 2022; Jakupec et al., 2024). We argue that blending in the EU has gradually shifted from a means to leverage private resources towards an instrument intended to promote coordination and political steering within the European development landscape. This has prompted the EU to scale-up guarantees to better leverage private resources; a move that has been combined – yet again – with additional governance features intended to increase political steering by the EC. Nevertheless, development banks maintain a key role in orienting blending and guarantee operations thanks to their expertise and resources, raising questions of accountability, transparency and ownership within EU development policy.

De-risking instruments and the evolving role and objectives of the EU as an international actor

Changes in the international political economy have reinvigorated debates about the role of the EU as an international actor. The rise of China has led to increasing geoeconomic rivalry between Washington and Beijing, leaving the EU struggling to define its stance in global affairs. Amongst other things, the EU is under pressure to confront the challenge posed by China’s Belt and Road Initiative. This has given rise to the Global Gateway Strategy, which seeks to mobilize up to €300 billion of investments in non-EU countries (EC, 2021a). This way the EU is seeking to provide a European answer to China’s large-scale financing of infrastructure in the Global South and retain its influence and provide investment opportunities for European firms in these countries (e.g. Flint and Zhu, 2019; Tagliapietra, 2021).

It is thereby also expanding beyond its traditional role as a so-called regulatory power or market power. According to these conceptualizations, an important source of EU influence has been the attraction of its large single market and the ability of the EC to leverage it for promoting its regulatory regimes and rules aligned with EU preferences and interests (e.g. Bradford, 2012; Damro, 2012, 2015; Goldthau and Sitter 2018; Serrano et al., 2017; Young, 2015). While not obsolete, it is increasingly recognized that the EU’s single market alone is unable to ensure its leadership position in a global economy dominated by geopolitical rivalry. Instead, scholars have argued that it has developed a set of ‘catalytic’ capacities, which the EU has deployed to leverage the resources of other actors (Prontera and Quitzow, 2023; see also Prontera and Quitzow, 2022). Building on this, the concept of ‘catalytic power’ refers to the mobilization of partners and their resources to pursue external objectives. Blended finance and guarantees represent an important example of this approach in EU external financing. Blended finance refers to a collaborative approach to financing based on the combination of EU-funded grant-based components with loans or equity from other sources, while guarantees represent the agreement to cover the risks of default in lending operations. Both aim to leverage scarce resources to help unlock financing by other partners, thereby increasing the scale of investment and impact. By doing so, the EU can also leverage its political influence in targeted countries.

This practice in EU external financing has followed a similar trend in its domestic practices. In a somewhat delayed response to the global financial crisis, the EC launched the Juncker Plan, officially known as the Investment Plan for Europe, in 2014. Through the European Fund for Strategic Investments (EFSI) – the plan’s financial arm – it aimed to close the large ‘investment gap’ in the European Union (EFSI, 2016). Since the EU did not have the ability to generate its own resources and member states were subject to EU-level restrictions on expanding their public debt, development banks took on a pivotal role in the plan, with the EIB taking centre stage. As Mertens and Thiemann put it, the plan engaged development banks as ‘anchor investors for volatile capital markets, absorbing idiosyncratic as well as conjunctural risks to channel self-recursive finance into the “real economy”’ (Mertens and Thiemann, 2018: 186). This has led to what they call ‘off-balance sheet policy making’ (Ibid, 2018: 189), where the development banks, backed by guarantees from the EU budget, help leverage funds by reducing risks for private investors.

In subsequent years, this logic of intervention and its institutional apparatus have been expanded, resulting in what Lepont and Thiemann (2024) call the ‘European Investor State’. This aims at mobilizing private finance to fill ‘investment gaps’ and achieve strategic goals through financial instruments for leveraging limited public funds and de-risking investments, such as loans, guarantees, equity activities and public–private partnerships. Several of these practices were not entirely new, but only recently consolidated into a coherent apparatus. This European Investor State – conceived as a multi-level configuration comprising the EU and the member states – emerged as a functional response by the European elites to the challenges posed by a changing international environment and a series of crises. It has been influenced by ideological preferences for market-oriented policy and by institutional and budget constraints of the EU architecture, preventing the development of more direct forms of public intervention. The consolidation of this approach has shifted the EU role from a regulator to an ‘investor’, but it has also increased the centrality of development banks. As the main implementing agents of the European Investment State, they can strongly influence investment decisions, weakening accountability and transparency and limiting public officials’ steering capacity (Mertens and Thiemann, 2018; Lepont and Thiemann, 2024; see also Prontera and Quitzow, 2022).

Similar trends, questions and challenges arise in EU external action. Aiming to mobilize the resources of external actors in the face of budget constraints, instruments like blending and guarantees imply a reduced level of control by the EC over investment projects. At the same time, these instruments allow the EC to engage these actors and their resources in pursuit of EU foreign policy objectives. Against this background, public development banks have emerged as key partners for the EC in its foreign engagements, combining additional financial firepower with public oversight. The EIB, which is governed by the 27 EU Member States, appears particularly suitable in this regard. But also national development banks, like Germany’s KfW or the French AFD, enable strong policy alignment. Compared to the EIB, with its narrow external lending mandate and limited expertise in the field, these two banks also offer important experience in the sphere of international development. Despite calls to create a more dedicated European development bank (Wieser et al., 2019), Member States have chosen to work within this existing set of financial institutions, presumably in an effort by large donor countries to retain their own influence (Hodson and Howarth, 2023).

As a second-best alternative, the EC has launched the Team Europe approach, where it seeks to position itself as a critical node and leader within a joint programming approach under the umbrella of the Global Gateway Strategy. Working alongside blending and guarantees, the Team Europe approach reflects the Commission’s effort to leverage resources beyond its direct control to maximize the scope of its influence within institutional and budget constraints. In their discussion of this new approach, Hodson and Howarth (2023) suggest that the reliance on this collaborative approach can be construed as both a strength and a weakness. From a traditional intergovernmental perspective, it can be seen as the failure to move towards more ambitious forms of supranational integration and the unwillingness to delegate authority to the EC. From the perspective of ‘new intergovernmentalism’ (e.g. Bickerton et al., 2015), however, cooperation – rather than integration – can be seen as a more active and hence more meaningful form of engagement within a shared European development agenda.

In the following, we build on this discussion to present an empirical investigation of how the use of blended finance and guarantees has evolved within the EU external financing architecture. Unlike the literature on financialization of aid – which focuses on the changing structural relations between state and private capital and its consequences, especially in the Global South (e.g. Allami and Cibils, 2018; Gabor, 2021) – we offer a more fine-grained analysis on the origins and development of these financial tools and on how they continue to reshape the relationship between the EC and its partners. First, we focus on the genealogy of these approaches, highlighting their drivers and patterns of expansion. Although guarantees and blending are not new instruments per se, we illustrate how they have been gradually expanded and consolidated in the EU apparatus for external action. Like the recent scholarship on the changing forms of state intervention within the EU (e.g. Di Carlo and Schmitz, 2023; Lepont and Thiemann, 2024; Prontera and Quitzow, 2022), we consider the interplay between internal and external developments, as well as the role of ideological preferences and institutional constrains in these processes. We also address the internal-external nexus (e.g. Herranz-Surrallés 2015), which translated innovations emerging in the EU domestic governance in its foreign engagements. This was especially evident after 2008 economic crisis under the Junker Commission, when the logic of leveraging, de-risking, and public private-partnerships diffused throughout EU domestic and external action. Next, we highlight the prominent role of development banks in the implementation of blending and guarantees, mirroring their rise within the EU. Finally, we offer a detailed discussion of the governance system established for the management of blending and guarantees. The structuration of this system highlights the emergence of a coherent apparatus for promoting strategic investments abroad, which does not match the standard account of the EU as a ‘global regulator’ or market power. However, our analysis also reveals a clear tension between the aim of asserting a stronger EU-level steering role and increasing its leverage and impact. In pursuit of these partially contradictory goals, the EC has vacillated between experimentation for increased impact and measures to reign in its partners to reassert control. It engages in an ongoing process of renegotiating its relationship with the EIB and other development banks.

The rise of blended finance and guarantees in EU development cooperation

While blending is a more recent instrument in EU development cooperation, guarantees have been a part of the European external financing architecture since 1977 when the EC first established the EIB’s external lending mandate (ELM), backing it with an external action guarantee. Converted in 1994 into the Guarantee Fund for External Action (GFEA), this enabled the EIB to carry out its external lending activities, while maintaining its high credit rating. It did not yet signal a shift to new forms of financial cooperation. Rather, EU grants and EIB loans, disbursed directly to the targeted recipients in traditional financing arrangements, remained the instruments of choice. This started to change around 2005, in tandem with a rise in overall development funding. ODA expenditure by the EU has more than tripled over the course of the past 15 years, increasing from slightly over €8 billion in 2007 to almost €29 billion in 2024, according to the OECD reporting system.

Around the same period, the Commission began experimenting with blended finance, which combines or ‘blends’ different types of financial instruments, including grants, loans and equity, as a means to leverage private resources for development goals. EIB quickly emerged as a central driver behind these developments. From the late 1990s, the EIB had already gained substantial experience as a promoter of large infrastructural projects within Europe, developing expertise on how to blend EU funds within public–private partnerships arrangements (Liebe and Howarth, 2020). Externally, the EU took a first step in this direction in 2003, when it created the African, Caribbean and Pacific (ACP) Investment Facility under the Cotonou Agreement. This facility targeted mainly the private sector and aimed at supporting large infrastructure projects. It was funded by the European Development Fund (EDF) with contributions paid by the member states. However, management control was handed to the EIB. In 2005, the ‘European Consensus on Development’ highlighted the need ‘to consider the most promising options for innovative sources of financing for development’ including ‘innovative public-private financing mechanisms’ (European Union, 2005: 12-20). Also, it acknowledged the important role of the EIB ‘in the implementation of Community aid, through investments in private and public enterprises in developing countries’ (European Union, 2005: 24). This led to the launch, in 2006, of the Global Energy Efficiency and Renewable Energy Fund (GEEREF). The GEEREF represented a so-called Fund-of-Funds and was implemented by the EIB and its European Investment Fund (EC, 2006). Since its inception, it has provided public equity in order to attract additional private equity to a series of regional funds for investments in renewable energy and energy efficiency projects in developing countries.

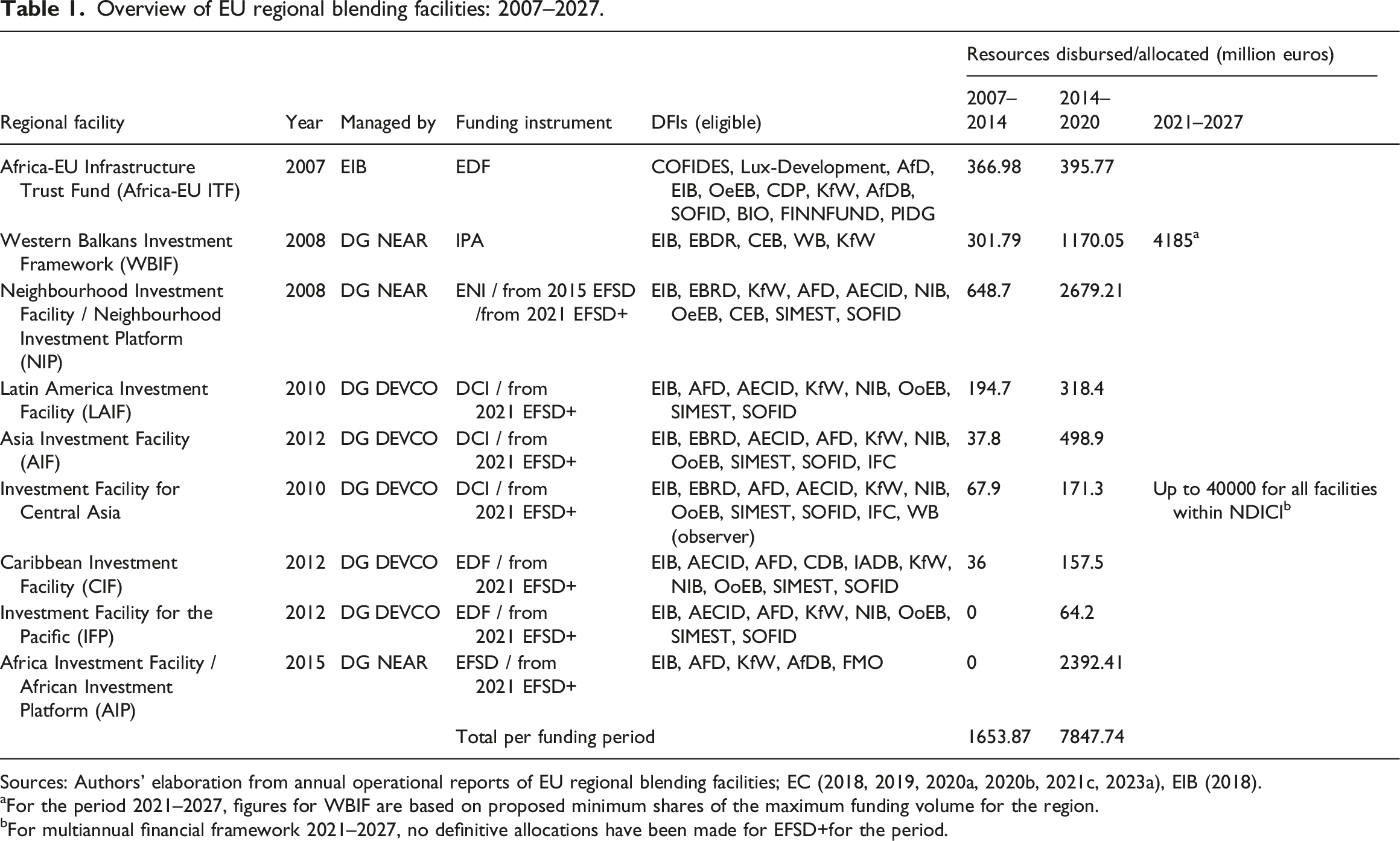

Overview of EU regional blending facilities: 2007–2027.

Sources: Authors’ elaboration from annual operational reports of EU regional blending facilities; EC (2018, 2019, 2020a, 2020b, 2021c, 2023a), EIB (2018).

aFor the period 2021–2027, figures for WBIF are based on proposed minimum shares of the maximum funding volume for the region.

bFor multiannual financial framework 2021–2027, no definitive allocations have been made for EFSD+for the period.

Blended finance received a further push with the launch of the EU ‘Agenda for Change’ in 2011. The ‘Agenda for Change’ – for the first time – explicitly mentioned blending as a mechanism ‘to boost financial resources for development’ and ‘leveraging private sector activity and resources’ (EC, 2011: 8). The EC was committed to expanding blending instruments, regarding them as effective tools for increasing its impact abroad. In 2012, it created the ‘EU Platform for Blending in External Cooperation (EUBEC)’, bringing together the member states and the European External Action Service (EEAS). In its 2014 Communication ‘A Stronger Role of the Private Sector in Achieving Inclusive and Sustainable Growth in Developing Countries’, the Commission recognised blending as ‘an important vehicle for leveraging additional resources for development and increasing the impact of EU aid’ (EC, 2014: 15). It stressed the need to cooperate with financial institutions to increase ‘the catalytic effect of blending in crowding in more private financing’ (EC, 2014: 15). For the multi-annual budget period from 2014 to 2020, the EU allocated €5 billion for blending, resulting in annual disbursements of more than €500 million in 2014, more than 10 times the first allocation in 2007.

This trend accelerated with the post-2015 Development Agenda and the External Investment Plan (EIP) of 2016. The centrepiece of the EIP, the EFSD, was modelled after the EFSI, the main financing vehicle of the domestic Investment Plan for Europe. Like EFSI, it focused on the use of EU funds to leverage other financial resources to support large-scale investment projects in cooperation with development financial institutions (Prontera and Quitzow, 2023). It not only included an additional €2.6 billion for blending operations but also a novel guarantee fund comprising €750 million. This guarantee fund could be utilized by financial institutions to guarantee lending in selected sectors and mainly targeting small- and medium-sized enterprises, a novel use of the instrument.

Although both instruments were considered a success, blended finance expanded more rapidly in the following years. With the launch of the EFSD, blended finance jumped to €1.6 billion for the year 2017, reaching more than 40 times the original allocation in 2007. By the end of the funding period, the EFSD had allocated 94% of its budget to blending operations and 6% to guarantees (EC, 2021b). The EFSD also served to streamline the budgetary and governance framework for blending facilities (see also below). The NIF and the African Investment Facility (AIF) (which had replaced the Africa-EU Infrastructure Trust Fund in 2015) were put under the EFSD and renamed the Neighborhood Investment Platform (NIP) and African Investment Platform (AIP). Unlike its predecessor, the latter was managed by the EC. Both initiatives were intended to fill investment ‘gaps’ and leverage financing for the achievement of the Sustainable Development Goals (EIB, 2016).

The EIP, however, also articulated geopolitical goals, particularly countering the rising influence of China in Africa and the EU’s neighbourhood, as motivations for its launch. The regulation establishing the EFSD (Regulation, 2017/1601) indicated that its purpose was ‘in line with the Union Global Strategy for Foreign and Security Policy’ (EEAS, 2016). This strategy had embraced the idea that leveraging financial resources was very important for EU foreign policy, aiming to ‘catalyse strategic investment through public-private partnerships’ (EEAS, 2016: 26). In 2017, the ‘New European Consensus on Development’ reasserted the role of blending as a key means to implement the 2030 Agenda and the Paris Agreement (European Union, 2017: 39). It also underlined the importance of closer cooperation between the EU, the member states, the EIB and other development banks for implementing blending activities.

The institutionalization of blending – and its shift from the niche of development cooperation to the wider machinery of the EU foreign and security policy – continued with the appointment of the von der Leyen Commission. The 2021–2027 multiannual budget, issued in the wake of the COVID-19 crisis, allocated €44,635 billion for blending operations under the EFSD+ and the Western Balkans Investment Facility (WBIF). The EFSD+, a consolidated version of the EFSD, combined all the existing regional blending facilities under a common budget instrument and governance framework (with the exception of the WBIF; see below). The EFSD+ and blending were also put at the centre of the 2021 Global Gateway Strategy: the main geopolitical effort of the Commission to the challenge posed by China’s engagement with external partners along its Belt and Road Initiative. As mentioned above, this was combined with the Team Europe approach to bring together the EU, its Member States with their financial and development institutions, including the EIB and the EBRD.

Finally, the EFSD + significantly increased the budget for guarantees, created a streamlined governance system and expanded its geographic coverage. A Common Provisioning Fund (CPF) was set up to finance a consolidated External Action Guarantee. The CPF received a funding envelope of €10 billion to provide guarantees for operations worth up to €53 billion until 2027, a ten-fold increase compared to the previous funding period. Of these, €35 billion were earmarked for EFSD + guarantees that back an exclusive ‘EIB window’ for overseas sovereign lending, and €13 billion were allocated for the so-called EFSD+ ‘open architecture’ (also known as ‘Team Europe Guarantees’). The latter focuses on mobilizing private investments by providing guarantees for additional capital that is crowded in by a range of implementing partners, that is, international financial institutions and European development banks (including the EIB, which can also participate in the ‘open architecture’).

The evolving landscape of blending and guarantees and the role of development banks

Interestingly, to date, the expansion of blended finance and guarantees has not proceeded in tandem with the intended leverage of private finance. This comes in spite of the fact that these instruments were explicitly developed as vehicles for catalysing private investment in sustainable infrastructure. This was the case only at a very early, experimental stage. GEEREF, the first blending initiative, utilized €132 million in equity from the EU, Norway and Germany to mobilize €1 billion in additional public equity, €500 million in private equity and further €1.5 billion in project-level lending from public and private sources (GEEREF Impact Report, 2020). This approach to blending – focused primarily on leveraging private finance for investments in sustainable projects – has continued at a very modest scale within the thematic blending facilities ElectriFI and AgriFI. Based on debt- and equity-based contributions from the EU budget, these facilities aim to catalyse investment in early-stage projects and companies in the field of energy access and the agri-food sector. In the funding period from 2016 to 2020, they only accounted for less than 2% of the EU’s blending contributions.

The vast majority of the EU blending operations have been channelled through the various regional blending facilities mentioned in the previous section. Rather than unlocking private finance, these facilities have developed into platforms to facilitate a novel form of cooperation between the EC and various public banks within its overseas development financing. In the context of these facilities and platforms the EU provides grant-funding in combination with loans from a range of development banks. These blending operations target mainly infrastructure, which are supported by the EU via investment grants, technical assistance for project preparation, equity or, to a lesser extent, interest rate subsidies (only 1% of blending provided by the EFSD). In these blending operations, the grant component is required to fulfil the principle of additionality. This means that it should be additional either in that ‘it makes the difference between a project going ahead’ or that it ‘improves a project’s design, quality, timing, sustainability, innovation, impact and/or scale’ (EC, 2015: 5). Their contribution to leveraging private capital, however, is minimal. This – surprising and arguably disappointing – fact is also reflected in the way the Commission communicates the results of these operations. It does not distinguish between funds mobilized from private sources or public development banks, thereby muddling the reporting of this central indicator. An exception to this is the first EFSD report for the year 2017. Here the data reveals that only 14% of the funds that were leveraged came from private sources, with the remainder coming from DFIs.

In other words, the EC has tacitly abandoned its goal of financial leverage in its original sense, that is, catalysing private sector investment. Instead, the EC now identifies four major non-financial objectives for its blending engagement: non-financial leverage, policy leverage, visibility and aid effectiveness (EC, 2015). Non-financial leverage refers to the additional value that an EU grant can offer to a given investment operation by enhancing its sustainability and development impact, while policy leverage refers to the additional influence it provides for promoting policy reforms in line with EU objectives. The latter is reinforced by increasing the visibility of EU development funding. Finally, aid effectiveness refers to the role of blending operations as a vehicle for facilitating cooperation and hence coordination among donor agencies.

The increasing prominence of non-financial objectives has gone hand-in-hand with the development of institutional mechanisms for ensuring adherence to EU strategies and objectives. In particular, the EC has established a stringent assessment process for granting financial institutions the capability of functioning as a lead financial institution in its blending operations. This so-called pillar assessment has led to a relatively short list of mainly European DFIs that have achieved eligibility for leading EU blending operations. Moreover, European DFIs are given priority as lead institutions in blending operations. In practice, this means that the vast majority of blending operations are led by the EIB, EBRD, French AFD and German KfW (EC, 2015; European Parliament, 2022a). Via these entities, the EC seeks to increase the scale of its engagements in partner countries, while ensuring adherence to its objectives, principles and modalities of aid delivery. In other words, it has forfeited its original goal of financial leverage for the ability to better steer its operations.

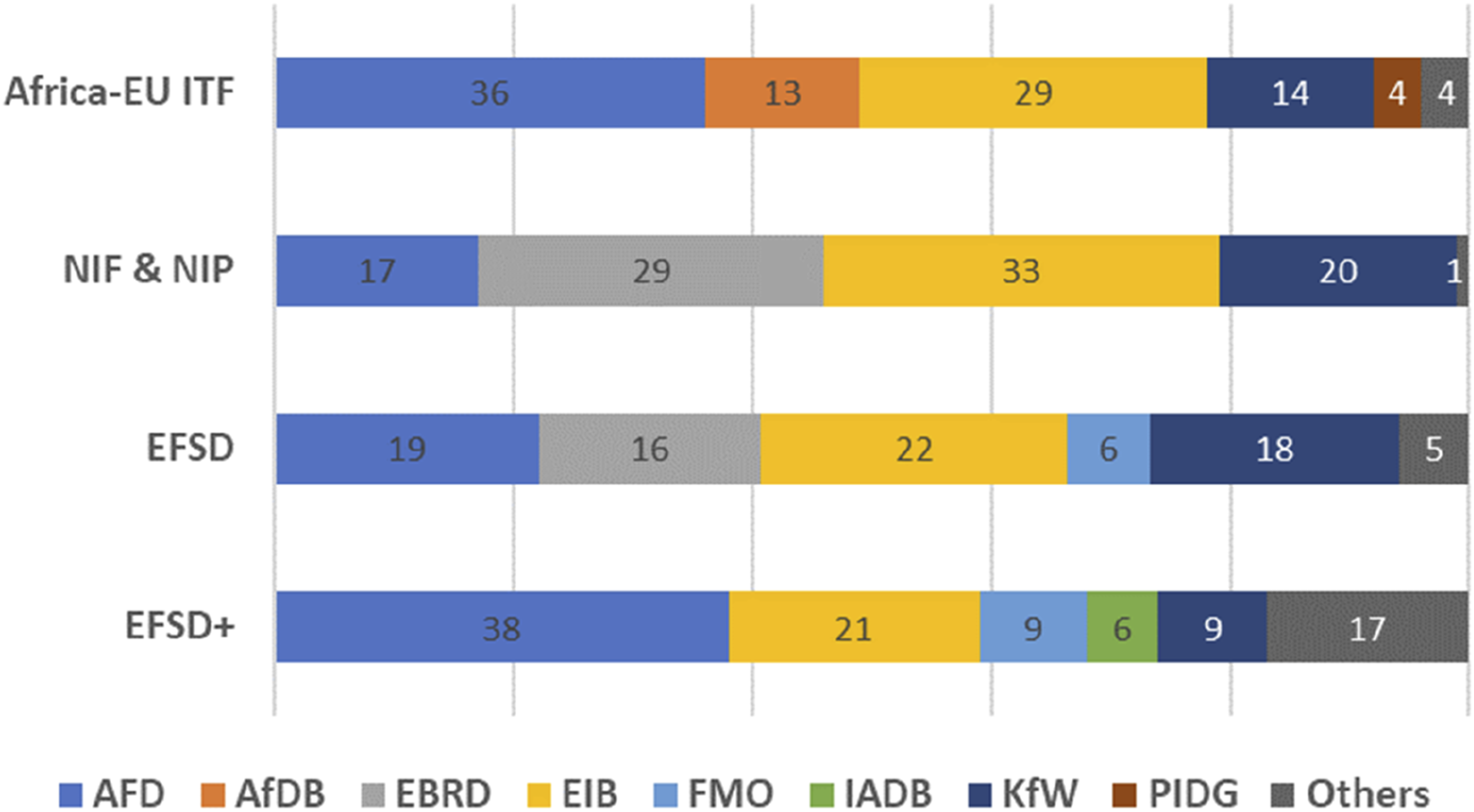

This has also translated into a significant increase in the EIB’s presence within the European development finance landscape. As the implementing agency for the GEEREF and the Africa-EU ITF, the EIB found itself playing a pioneering role in the shift towards these new financing modalities. In the NIF and the NIP, the EIB led approximately one third of projects, followed by EBRD with 28% and KfW and AFD with approximately 20% each. The EFSD reveals a similar distribution with the same four financial institutions in the lead. Some changes have emerged within EFSD+ – with AFD significantly increasing its share of projects – yet the share of EIB projects has remained stable at approximately 20% (see Figure 1 below). Share of projects in major EU blending facilities, by leading DFI, in percent.

This prominent role of the EIB has been confirmed with the EFSD + guarantees. Not only the majority of guarantees are earmarked for its operations (under the ‘EIB window’), but the EIB can also take part in the ‘open window’ architecture, which was originally conceived precisely to extend the EU financial partners beyond the usual European DFIs. In this vein, the EIB continues to be the favoured EU partner. Although the EC is not represented on the EIB’s Board of Governors, the bank is subject to EU-level regulations, which guide its strategy and policies. It is, therefore, considered a ‘policy-taker’ (EIB, 2020; Liebe and Howarth, 2019). A decision of the European Council and Parliament set out detailed guidelines for EIB lending operations in developing and emerging countries under its External Lending Mandate. No other bank is aligned to EU policies to this degree. The EIB has no representation from the EU’s international development community or from recipient countries, however. According to an expert assessment of the European development finance landscape conducted in 2019, the EIB lacked a framework for accounting for the impact of its operations in developing countries. Nevertheless, it now operates in more than 140 countries (EIB, 2022) and has offices in 25 developing and emerging economies. Approximately 10% of its annual disbursements go to non-EU countries (EIB, 2022).

The governance of blending and guarantees

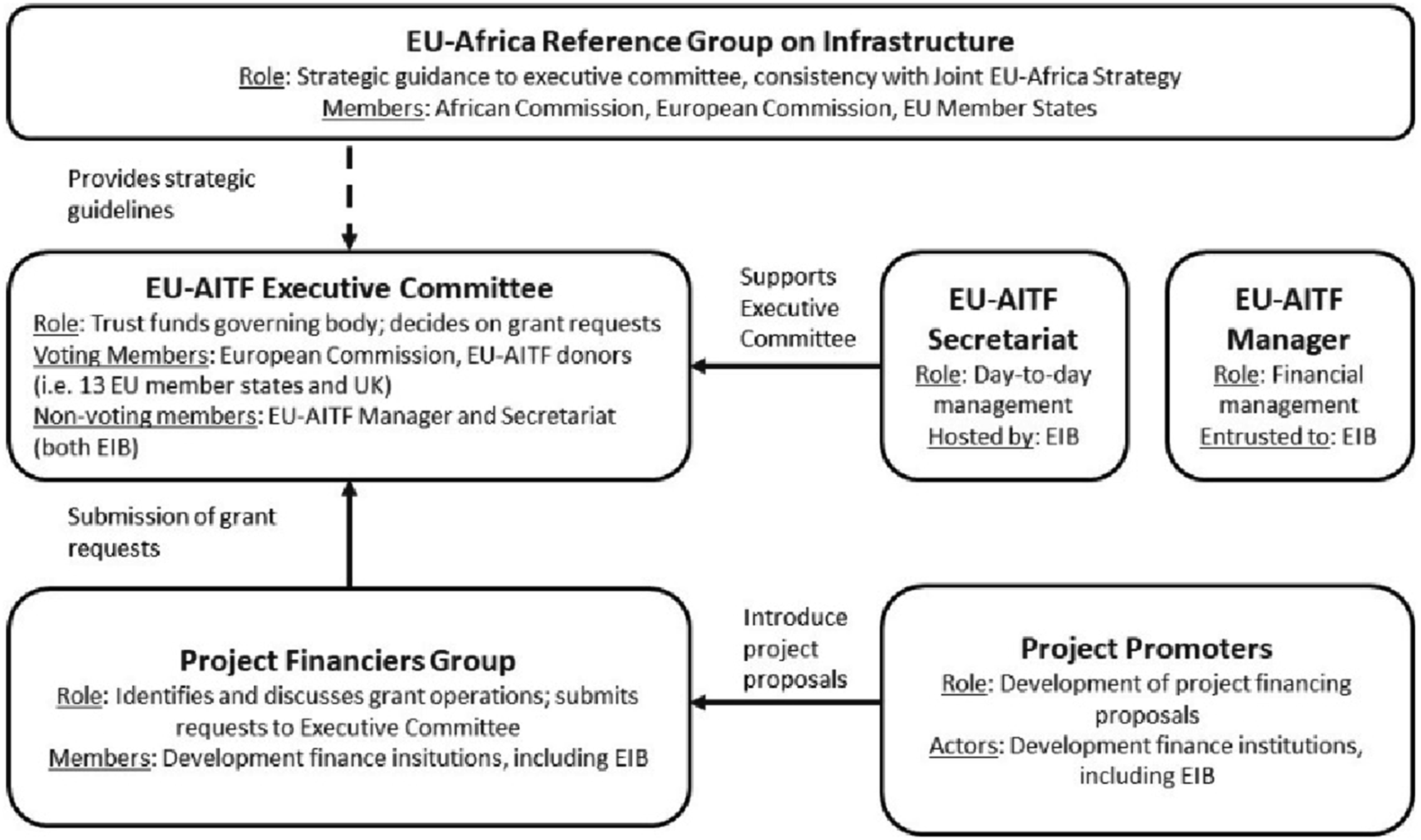

The prominent role of the EIB and other development banks is not limited to their role in promoting and structuring individual projects. It has also given development banks, and the EIB in particular, a central position in the broader governance of EU-supported blending operations. As already indicated, this role was particularly prominent in the Africa-EU Infrastructure Trust Fund. Although it represented a multi-donor initiative, the EIB acted as the trust fund manager and hosted its secretariat (Figure 2). In those capacities, the EIB was also represented in the executive committee and the governing body, albeit in a non-voting capacity. Along with other DFIs, it was represented in the Project Financiers Group, responsible for selecting projects and grant requests for approval by the Executive Committee. The EIB was instrumental in shaping the development of this new mode of EU-overseas development financing. Especially in the early stages of European blending operations, EIB was critical in shaping the actual pipeline of projects and thus in determining the allocation of EU grant funding (Interview No. 2). At this stage, the EC had little experience or expertise in assessing financial proposals against the principle of additionality it aimed to uphold (Interview No. 1.5). Governance of the EU-Africa Infrastructure Trust Fund (EU-AITF).

Over time, however, the EU has developed an increasingly streamlined governance framework for its growing portfolio of blending operations (Interview No. 5). Building on the experience of the EU-AITF, subsequent blending facilities were placed directly under the control of the EC, which became the host for the respective secretariats. In 2011 the EC also created a new Financial Instruments Unit in DG DEVCO (now Directorate-General for International Partnerships, DG INTPA) and strengthen its capacity to govern the facilities (EC, 2012). To ensure alignment with the EU’s strategic goals, the EEAS joined the EC as co-chair of the strategic boards of the various facilities. As illustrated, in a further step towards strengthening the influence of the Commission and the EEAS, the launch of the EIP saw the consolidation of the two largest blending facilities, the NIP and AIP, within the EFSD. The EFSD + has further centralized blending operations under a single governance framework. Only the WBIF, which supports EU accession countries in the Western Balkans, has retained a separate governance system.

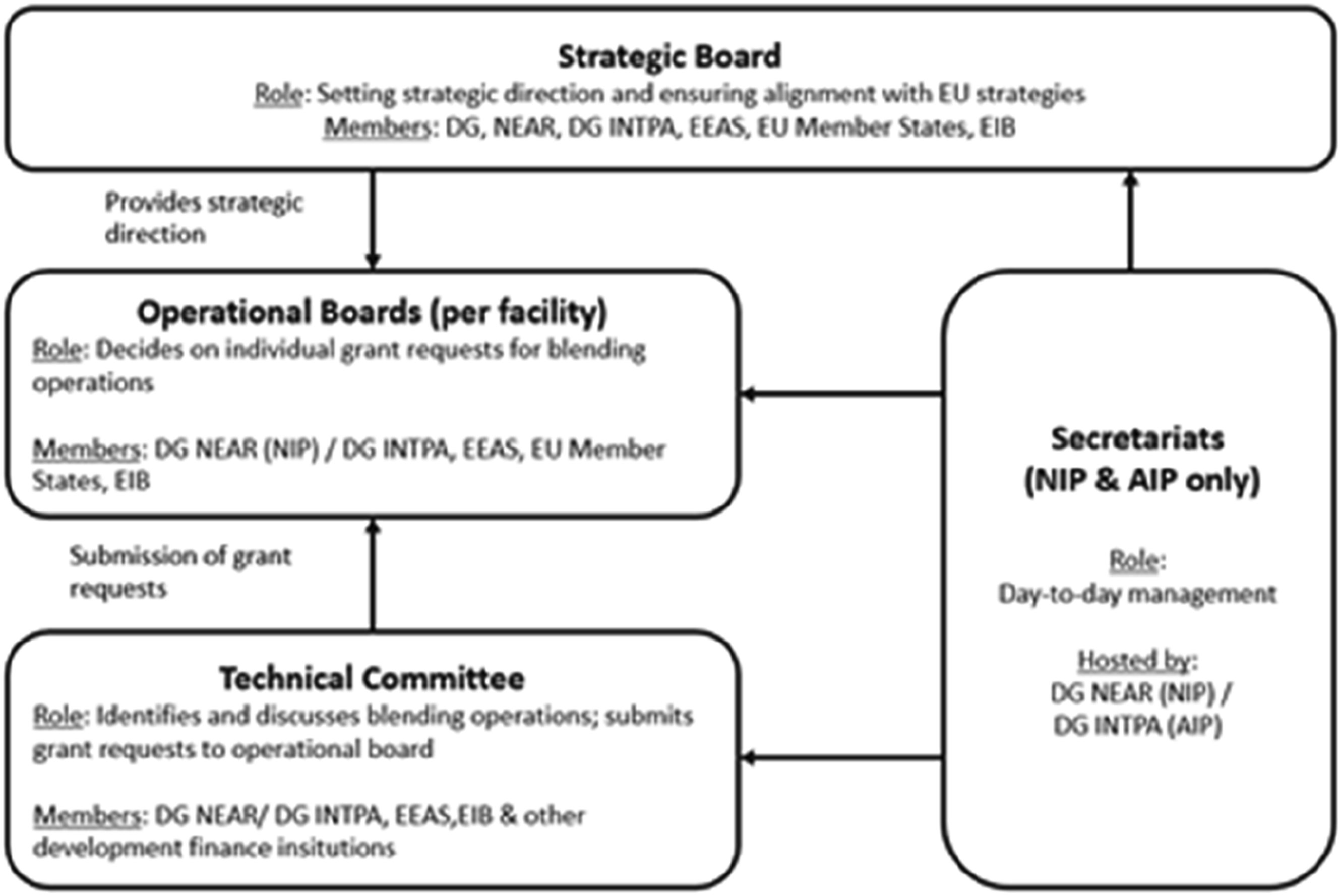

Like its predecessor, the EFSD+ is based on a three-tier architecture composed of a Strategic Board, regional Operational Boards and corresponding technical committees (Figure 3). The Strategic Board sets the overall strategic directions for the EFSD+, which combines all major blending facilities. It is jointly chaired by representatives of DG INTPA, DG NEAR and the EEAS. DG NEAR and DG INTPA, respectively, also host the secretariats of NIP and the AIP. In addition, the member states and the EIB are represented in the Strategic Board, while partner countries and other stakeholders may participate as observers upon request. Operational Boards are responsible for issuing opinions on project proposals and approving grants for the regional facilities. It includes the EC, the EEAS and the member states as voting members and financial institutions as observers. Technical committees, consisting of the Commission, EEAS and financial institutions, meet regularly to establish a project pipeline and select projects for approval by the Operational Board (Interview No. 9). The pipeline of projects is developed in consultation with partner countries and their EU delegations (Interview No. 10). The projects, hence, balance national priorities – as defined by the government in charge – and EU priorities and strategic orientations. The governance system of the EU blending facilities under the EFSD+.

The governance system reflects the inherent tension between the EC’s aim of leveraging additional resources and competencies of financial partners, on the one hand, and the challenge of retaining a degree of control over operations that have grown in both size and number, on the other. Given the important role played by DFIs in the process of project preparation, they have retained a significant degree of de facto influence over portfolio development. In this vein, the governance system has established regular and structured interactions between the Commission and these financial institutions, allowing the Commission to increase its influence within the governance of blending operations over time (Interview No. 10).

Despite increasing EU influence over its development partners, the question remains whether this has increased the Commission’s ability to pursue strategic foreign policy goals. In the past, the regulations creating the external financing instruments defined principles and objectives in alignment with the fundamental principles of the EU, such as promoting sustainable development, democracy and the rule of law in recipient countries and supporting the implementation of multilateral agreements, most notably the SDGs and the Paris Agreement. These have offered important guidance for EU officials (Interview No. 3). While ensuring the alignment with the EU’s norms and values, it has not necessarily provided a framework for pursuing more targeted economic and political interests.

The EC has also recognized this. The NDICI has the explicit mandate to help the EU respond rapidly to crises and to pursue ‘Union foreign policy needs and priorities’ (EU Regulation, 2021/947, Article 3, Paragraph 2d), and it emphasizes political steering within a so-called ‘policy first’ approach. This strengthens the voice of the EEAS within the governance system of external finance generally and blended finance specifically. The EU’s Global Gateway Strategy – which relies on the EFSD+ – seeks to further strengthen the geostrategic dimension of external financing. It aims to promote sustainable projects that ‘can be delivered with high standards, good governance and transparency’ (EC/EEAS, 2021: 1). But also to enhance the EU’s ‘own interests’ and ‘strengthening the resilience of its supply chains’ (EC/EEAS, 2021: 3), a pillar of the EU’s drive towards ‘open strategic autonomy’ and for addressing China’s ‘growing assertiveness’ (European Parliament, 2022b: 1). Given their prominent role in EFSD+, European DFIs and the EIB should become prominent vehicles of the emerging EU geopolitical turn. To facilitate this, the Team Europe approach has created a more structured dialogue – at high-political level (e.g. Director General, Vice President) – among the European DFIs and between them and the EC (Interview No. 9).

Despite the continued rise of EIB and European DFIs, the recent expansion of guarantees, with the EFSD+, also signals a careful return to the original agenda of leveraging private sector funds. Moreover, the ‘open architecture’ allows the EC to introduce competition among financial actors (Interview No. 9). However, again, these efforts have been matched by governance innovations aimed at ensuring political steering by the EU. For the EFSD+, the EC has established a process to ensure coordination in EIB operations, increasing its influence compared to those conducted under the traditional External Lending Mandate (Interview No. 10). For the latter, consultations were in place, but the EIB was more autonomous in its decisions. The new governance system for the EFSD + involves a three-step process (Interview No. 10; see also EC, 2023b). First, the EC and the EIB initiate a discussion on projects included in the EIB pipeline. In a second step, called ‘Article 19’, a more detailed discussion on specific projects takes place 2 . At this stage, the EC can gather more information about the projects. These are also shared through an inter-service consultation – managed by the Directorate-General for Economic and Financial Affairs (DG ECFIN). After receiving the green light from the EC, the EIB conducts additional analysis on the projects. In a final step, the EC approves the guarantees for the selected projects.

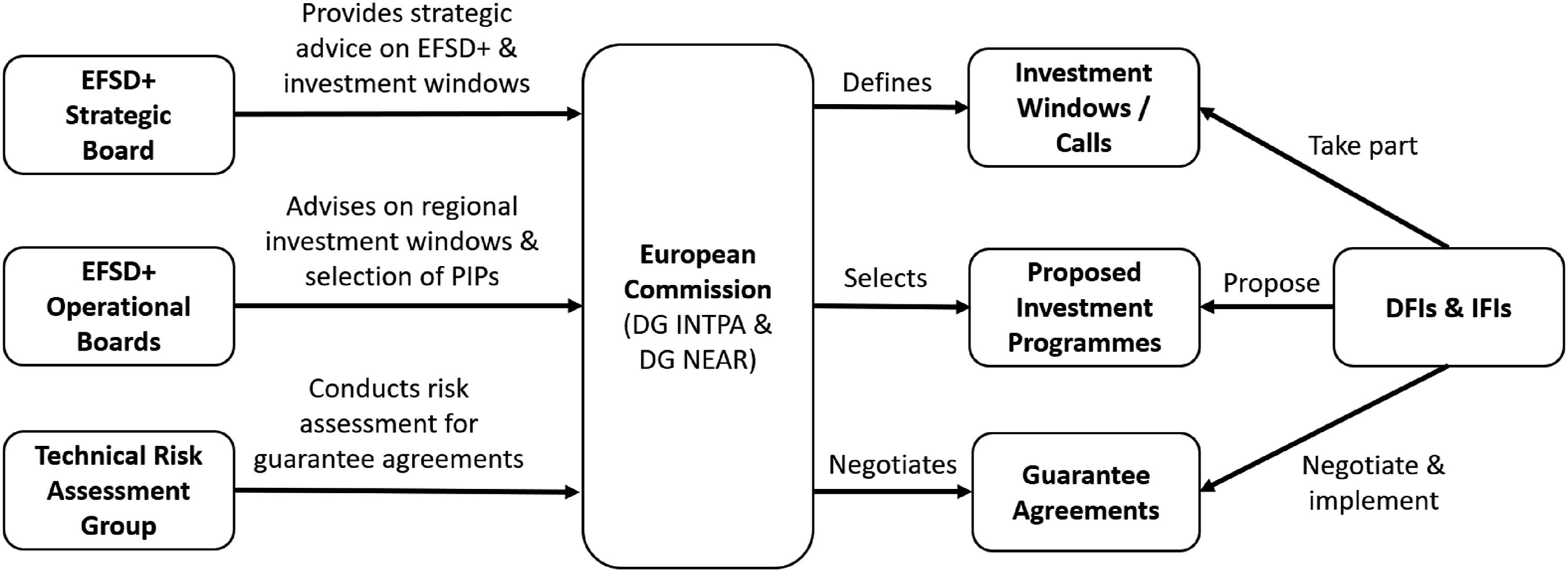

For other DFIs participating in the ‘open architecture’ a separate system has been established (Figure 4, Interview No. 10; see also EC, 2023b; EC/HRVP, 2023). The challenging process of ‘pillar assessment’ for accrediting financial partners remains intact, which limits the potential implementing partners. The EFSD + Strategic Board and the EC decide on the content and focus of the ‘investment windows’ for the subsequent call for proposals for the financial institutions. Financial institutions then present ‘Proposed Investment Programmes’ (PIPs) for each call (the first calls were launched in 2022–23). These PIPs should be approved by the EFSD + Operational Board, which assesses the proposed investments on its ability to contribute to NDICI’s thematic and geographic priorities and to deliver on Global Gateway objectives. The application form requires applicants to specify to which Team Europe Initiative the investment might contribute. Finally, the EC negotiates ‘Guarantee Agreements’ with each partner and discusses regularly on progress and pipeline development. For these tasks, the EC has consolidated its expertise on the matter. In 2022, it established a Guarantee Risk Expert Group supporting both DG INTPA and DG NEAR and finalised secondment/appointment arrangements with six partner financial institutions. A similar group already existed but previously operated under the EIB (Interview No. 10). The ‘Guarantee Agreements’ include several parameters – for example, eligibility criteria for the supported project or targeted sectors, risk coverage or pricing – that ‘factually influence the pipeline of investments developed by the implementing partner’ (EC/HRVP, 2023: 17; Interview No. 10). Implementing partners, however, maintain a degree of autonomy in identifying specific projects, which they want to support under their portfolio guarantee (EC/HRVP, 2023). At the same time, the EC can offer ‘policy discounts’ (i.e. discounts on the costs for the guarantee) to incentive the partners to pursue specific goals in their portfolio, such as investing in certain countries or prioritising specific issues or promoting the participation of other partners in Team Europe initiatives (Interview No. 10). The governance system of the EU guarantees under the EFSD+ ‘open architecture’.

Within these constraints, the emerging guarantee operations have reassumed the mission of catalysing private investment. Examples include the KfW-sponsored African Local Currency Bond Fund and Finnfund’s Africa Connected program. Both have the objective of channelling private investment into the African market. Finnfund’s private capital stands at 15%, aiming to reach a share of 50% by 2030 (Finnfund, 2023). While it remains to be seen whether this represents a new turn towards the original blended finance agenda, it reveals the tension between the goal of leverage and impact, on the one hand, and the assertion of control and strategic guidance, on the other. Having developed a streamlined governance framework to ensure oversight, the Commission is beginning to venture further afield, presumably testing the ability to unlock the originally targeted synergies.

Conclusions

The rise of blending and guarantees in the EU development cooperation is part of a global trend towards the financialization of aid. This trend – to which the EU itself contributed (e.g. Orbie et al., 2022) – has triggered an intense debate on the shortcomings and risks posed by the diffusion of new financial mechanisms that aim at increasing the involvement of private actors in development policy. Despite its rhetoric, EU approaches have only had a limited role in targeting private finance. Although this was the original driver behind EU experimentation with blending, the EU soon changed its rationale: from leveraging private resources to increasing the Commission’s ability to coordinating European development policy actors within a Team Europe approach. The EU blending instruments primarily serve this goal by targeting development banks and steering their actions towards the EU preferred policy objectives. This shift has been accompanied by an increasing geopoliticization of aid, which has resulted in a further centralization of the governance framework for blending operations.

Nevertheless, by shaping the pipeline of projects, development banks in general and the EIB specifically maintain a key role in blending operations. These operations also provide additional resources for national development banks (most prominently the French AFD and the German KfW) as well as the possibility for member states to influence the EC’s aid portfolio. Indeed, the member states are not only represented in the Strategic Board of the EFSD/EFSD + but also – unlike the EC – on the board of the EIB. As argued above, this increasing cooperation, further illustrated by the Team Europe approach, is in line with expectations of new intergovernmentalism; it can be seen as an active form of coordination by member states within a shared European development and foreign policy agenda in response to a more challenging international environment. This response has not resulted in more supranational integration, however, as the establishment of a new EU development bank or the delegation of new powers to the EU in the field of international cooperation might have. This trend mirrors the dynamics described by the scholarship on the new forms of state interventionism within the EU (e.g. Di Carlo and Schmitz, 2023; Lepont and Thiemann, 2024; Mertens and Thiemann, 2019; Prontera and Quitzow, 2022), where coordination, networking and hybrid modes of governance have been detected as preferred means for promoting strategic investments rather than more centralised supranational solutions (e.g. an EU Sovereignty Fund), which have been opposed by member states (Strupczewski, 2023). At the same time, the expansion of these modalities of aid delivery poses new problems of transparency, ownership and democratic accountability for EU development policy. The EIB – which emerged as a central actor in blending and guarantees approaches – has no representation from the development community nor developing countries. The European Parliament has only recently been involved in the governance system for blending and guarantees and only with an observer status. To increase its role, it has obliged the Commission to ensure an independent external evaluation of the EFSD and to engage in an annual consultation with external stakeholders and civil society organisations (European Parliament, 2022a). However, financial instruments like blending and guarantees are characterised by a complex governance system – with the involvement of several institutional actors (EU and national) and financial entities in their decision-making – which renders accountability a difficult challenge (e.g. Andersen et al., 2019). These concerns have been echoed by civil society organizations that have criticized the ‘unclear accountability structures and limited transparency’ of such approaches, the ‘low evidence’ on their ‘development impact’ and the risks they pose in terms of local ownership and reduced investments in public services and social initiatives (Concord, 2021).

Similar questions might be raised regarding the growing importance of guarantees, as the EC seeks to reemphasize its original objective of leveraging private sector finance, particularly with the EFSD+ ‘open architecture’. In contrast to blending operations, or those covered by the EFSD + guarantee for the EIB, the EC does not screen individual investments but works with eligible financial partners to establish dedicated funding programs in alignment with its broader priorities. This implies a lower degree of control by the EU. To address this problem, the EC has yet again developed a system of governance, largely mirroring the one established for the blending operations. As the use of guarantees continues to expand, this will give rise to the same tension between the Commission’s attempts to ensure its political steering, on the one hand, and the aim to increase financial leverage, on the other. Moreover, it will intensify problems of democratic oversight, transparency and ownership in the overall EU development policy.

Although not the focus of this paper, this discussion also sheds light on the broader questions addressed by scholars of financialization. Rather than merely a question of how the logic of the markets and finance penetrate different policy spheres and governance logics, it points to the fact that the governance of financialization matters. Rather than pointing to a general trend of reduced autonomy of developing countries vis-à-vis transnational financial players, as suggested by Gabor (2021), the financialization of aid gives rise to a new political economy of aid with evolving roles of different actors. As this paper has demonstrated, the apparent shift to new financial instruments is exposed to important countervailing trends. This has yielded the rather counterintuitive outcome of increasing political control by the EC over development banks. In other words, macro-level developments may be misleading and warrant more in-depth empirical research into the politics and governance of specific instruments and actors in the field.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.