Abstract

In the rapidly evolving realm of financial technology, blockchain integration has catalyzed transformative changes. This study delves into the intricate relationship between traditional banks and the blockchain technology. Drawing from the perspectives of International Political Economy (IPE) and Science and Technology Studies (STS), this study understands the blockchain technology through the lens of infrastructure, where power dynamics are constantly shaped by the entity wielding the strongest agency. This analysis delves into how traditional banks strategically leverage blockchain not only for technological integration but to exert control. Grounded in the concept of “power of social interaction,” this study reveals how and why banks secure a central position within this evolving infrastructure, dynamically influencing the interplay between technology and financial institutions. A focal point of this exploration is the tokenization process, which illustrates how banks actively engage with blockchain, seamlessly integrating it into their structures to shape the infrastructure narratives. By contributing insights into the implications of blockchain adoption by traditional banks, this study enhances understanding of power dynamics within financial infrastructures and their transformative potential, underscoring the process of infrastructuring governing the endeavor to attain a central position within an infrastructure.

Introduction

The emergence of Bitcoin in January 2009 aimed to lay the foundation for a groundbreaking financial system, challenging skepticism surrounding traditional financial intermediation. As a digital currency on a peer-to-peer network, Bitcoin enables borderless transactions through secure and immutable mathematical algorithms (Kayal and Rohilla, 2021). Despite its expanding applications, the cryptocurrency’s inherent volatility has raised uncertainties about its safe-haven asset classification. This volatility prompted the development of new protocols to address these concerns. As such, while the blockchain technology underpinning Bitcoin marked a significant innovation, the true transformation of the financial landscape occurred with the introduction of the Ethereum whitepaper in 2014. Ethereum established the decentralized finance (DeFi) ecosystem, driven by its unique Turing-complete scripting language. DeFi represents a revolutionary financial paradigm, enabling trustless and borderless transactions through smart contracts (Jensen et al., 2021). Functioning as code-based agreements, smart contracts operate in a self-executing and self-enforcing manner, introducing a new era of automation and reliability (Allen et al., 2020).

As such, this novel technology has opened up new avenues for both research and practical implications. However, the IPE literature exploring blockchain technology has been relatively limited, primarily focusing on Bitcoin and its financial ramifications (Campbell-Verduyn, 2018; Golumbia, 2015; Rotta and Paraná, 2022; Swartz, 2018; Tapscott and Tapscott, 2016). Only recently have authors started to overcome this limitation and explore the specific role of blockchain technology in new cross-border payments (Brandl and Dieterich, 2023), the implications and motivations of corporations using blockchain technology for developing new services, such as Amazon AWS (Beaumier and Kalomeni, 2022), or the role of blockchain technology in the micro-level epistemic coordinative function of Chinese markets (Gruin, 2021). Some papers also examine this technology beyond traditional IPE journals (e.g., Hayes, 2019; Langley and Leyshon, 2017). These latter papers indeed surpass the focused analysis of Bitcoin, delving into areas like money and payments (Clarke and Tooker, 2018), the growing role of blockchain and FinTech in the transformation or “Appleization” of finance (Hendrikse et al., 2018), or the internationalization of currencies (Deng, 2023). Moreover, it is argued in various strands of literature influenced by STS that all novel technologies, including the blockchain, carry a mundane or social characteristic (MacKenzie, 2009; Muniesa et al., 2007). This observation is important as it highlights that a technology is influenced by specific prevailing narratives. In this context, the incipient libertarian narratives governing blockchain technology had the ability to impact the central position of banks in the financial system. It is precisely this dynamic that prompted banks to respond to the challenges posed by emerging blockchain or even FinTech technologies (e.g., Bassens and Hendrikse, 2022; Campbell-Verduyn, 2018).

As such, this paper aims to emphasize this response by examining tokenization, a crucial yet overlooked component of blockchain technology in IPE or STS literature. Tokenization was chosen because it facilitates the transformation of bank loans and other financial instruments, such as covered bonds, into real-world assets (RWAs). This process serves as a lens through which power dynamics between banks and emerging technologies can be analyzed.

In more detail, this paper adopts an IPE and STS framework to explore banks’ involvement in tokenization processes, emphasizing an infrastructural and power dynamics perspective. Examining blockchain technology as an infrastructure allows a comprehensive understanding of its ongoing evolution shaped by social and technical factors but also by power dynamics. Specifically, power dynamics refer to the endeavors of actors with the strongest agency to secure centrality within an infrastructure, shaping its narratives and subsequent development, which highlights the process of ‘infrastructuring' (Pipek and Wulf, 2009). Tokenization contributes to the ongoing process of infrastructuring by integrating blockchain technologies into the traditional operations of banks, thereby shaping the trajectory of this infrastructure and forging far-reaching networks and applications, aligning now with banks’ narratives.

For more theoretical clarity, this paper analyzes power dynamics through the concept of “power of social interaction” (Duggan et al., 2022). This concept of power is particularly relevant in elucidating how actors within an ecosystem actively shape and mold the evolving infrastructure through dynamic interactions. Specifically, departing from a purely coercive power view—where an actor employs sanctions and incentives to compel another actor to act against its natural inclination (Dahl, 1957; Dallas et al., 2019)—this paper embraces the concept of “power of social interaction”, balancing it with an agent-based structural power, which is an actor’s capacity to shape underlying structures in line with its interests and narratives (Duggan et al., 2022). In the context of this paper, this occurs not through a Dahl-ian act of power but by leveraging sector-specific characteristics, such as lobbying capacity of banks and their abilities to position their technologies at the core of financial transformations.

As such, the main argument of this paper is that traditional banks use their lobbying and technological capacities—which grant them the strongest agency—to exert “power of social interaction” within the blockchain technology, particularly evident in the process of tokenization. By integrating blockchain technology into their operations, banks shape power dynamics, influencing narratives and standards within this ecosystem. This integration of blockchain and the shaping of narratives reflect a fluid and contingent process of infrastructuring, where banks actively participate in and contribute to the subsequent development of this novel infrastructure, consolidating their narratives, control, and authority. This proactive strategy of banks helps mitigate potential disruptions that might emerge if blockchain technology were to develop independently. Thus, this approach aims to illustrate that the banking system’s adoption of blockchain technology extends well beyond cost-effectiveness, as previously argued (e.g., Lin et al., 2022).

To support this theoretical argument, primary data sources will be employed, including non-peer-reviewed articles and relevant blog posts within the DeFi ecosystem, as well as articles from supranational institutions, such as Bank of International Settlements (BiS) or Federal Reserve (Fed). Secondary sources, including peer-reviewed papers from reputable journals and relevant books, will also contribute to the analysis. Moreover, for more theoretical clarity, the paper analyzes two case studies that revolve around the interaction between Huntington Valley Bank (HVB) and Société Générale Forge (SocGen-Forge) with the MakerDAO protocol. These case studies show that traditional banks like HVB and SocGen go beyond mere technological integration. Driven by the recognition of blockchain’s disruptive potential, they actively seek to integrate themselves into the very fabric of this infrastructure, advancing their goals and control by providing the financial instruments slated for tokenization.

The novelty of this paper lies in its comprehensive examination of how traditional banks, exemplified by HVB and SocGen, actively employ blockchain technology not only to integrate with emerging trends like tokenization but also to assert their authority, control, and leverage over this evolving infrastructure. This exploration provides a unique perspective on the strategic maneuvers that banks undertake to maintain relevance and dominance in the changing financial landscape, while highlighting the interplay between technology and financial institutions. By delving into these aspects, this paper contributes to a deeper understanding of the dynamics reshaping the banking industry and provides insights into the potential risks and opportunities that arise from its engagement with innovative technologies, in line with the existing literature (Bassens and Hendrikse, 2022; Campbell-Verduyn, 2018). This contribution holds increased significance as the IPE literature still grapples with a gap concerning the role played by emerging technologies in finance and their role in shaping the structural power of this sector, as also argued by Bernards and Campbell-Verduyn (2019).

Second, this study contributes to the IPE and STS literatures by exploring the interplay of infrastructures and power dynamics (Beaumier and Kalomeni, 2022; Bernards and Campbell-Verduyn, 2019; Coombs, 2016). By using the concept of infrastructuring and recognizing infrastructures as dynamic entities with inherent political agency, constantly evolving rather than remaining static, significantly impacts our understanding of power dynamics within financial infrastructures. This perspective suggests a nuanced interplay between different actors and the infrastructural systems, emphasizing that power relations are not solely predetermined but co-shaped by ongoing interactions, which gives rise to the infrastructuring process. In this context, prioritizing “power of social interaction” unveils a complex, competitive landscape where actors vie for the centrality within an infrastructure, influencing its narratives and evolution.

Third, this paper introduces a novel analysis of tokenization, a concept underexplored in both IPE and STS literature. Tokenization’s significance extends beyond power dynamics, offering insights into the evolving financial landscape and the impact of emerging technologies like blockchain. Studying tokenization is crucial for understanding its implications for financial practices, market structures, and regulatory frameworks, contributing to a deeper understanding of the intersection between finance and novel technologies.

The article proceeds as follows. The first section explores the technical components that provide the basis for the infrastructural analysis in this paper. The second section analyzes blockchain technology from an infrastructural perspective. The third section explores blockchain’s evolution from a libertarian origin to an entity with inherent political agency, exploring the power dynamics involved in the relationship between banks and this novel infrastructure. The fourth section delves into the empirical analysis of the relationship between HVB and SocGen and the MakerDAO protocol. The fifth section concludes.

Blockchain and the evolution towards the Turing-based smart contracts

This section aims to analyze the technical components that have propelled the development of Ethereum technology, smart contracts, tokenization, and stablecoins. This lays the groundwork for the infrastructural analysis of the relationship between banks and the blockchain technology, as explored in the following sections.

The crypto ecosystem initially revolved around Bitcoin, using a distributed ledger technology (DLT). But what marked a transformative moment was the introduction of the Ethereum whitepaper in 2014, featuring a virtual Turing machine designed to execute tailored software code within its blockchain environment (Pinna et al., 2019). Ethereum fostered an ecosystem facilitating trustless transactions of information, money, and assets (Bistarelli et al., 2020). The advent of Ethereum also gave birth to smart contracts which were defined as computerized transaction protocols designed to enable the digital encoding of agreements between parties, facilitating automated transactions without the need for central authority oversight (Khan et al., 2021).

Various smart contract providers are available, yet the Ethereum protocol stands out as the most widely adopted. Pioneering peer-to-peer financial contracting (Chen and Bellavitis, 2020), Ethereum’s protocol extends beyond cryptocurrency intermediation. The evolution of smart contracts has led to the rise of DeFi, offering a novel approach to financial services by bypassing traditional centralized intermediaries and relying on automated protocols (Born and Vendrell Simon, 2022). DeFi encompasses the creation, distribution, and utilization of decentralized financial services enabled by smart contracts.

DeFi effectively engendered a (crypto)-financial system that broadened the “scope of the market” (Diaz-Rainey et al., 2015: I). Preceding Ethereum, a centralized crypto-finance ecosystem (CeFi) dominated, with intermediaries playing a central role. However, Ethereum’s introduction led to the emergence of decentralized platforms and exchanges (DEXs), replacing these intermediaries (for a detailed overview, see Aramonte et al., 2021), also opening this technology to the traditional financial system.

In this manner, DeFi plays a pivotal role in engendering more intricate digital financial services, predominantly owing to the versatility of smart contracts, which are capable of performing a diverse array of computational tasks (Pinna et al., 2019). Specifically, DeFi’s foundation lies not in intermediaries, but in open interoperable protocols, and by extension, decentralized applications (DApps). The absence of intermediaries underscores how this novel digital architecture fosters a transparent, smart contract-based financial system, essentially diminishing the requirement for custodians, central clearing houses, or escrow services (Schär, 2021). Consequently, trust is cultivated by encoding predefined contractual rules and maintaining exclusive authority over the assets governed by a smart contract, effectively nullifying counterparty risk. This decentralization translates into remarkably low transaction costs (Allen et al., 2020). These contracts can be tailored to store crypto-assets and release them upon the occurrence of predetermined events.

Ultimately, as a natural evolution within DeFi, we witnessed the emergence of tokenization and RWAs. Tokenization facilitates the conversion of real assets, such as banking loans and financial instruments, into digital securities represented by ERC-20 tokens (Gundiuc, 2022), giving rise to RWAs. Specifically, it signifies the process wherein smart contracts on the blockchain are employed to create a virtual representation of a specific asset in the form of a token (The Tokenizer, 2019). Specifically, in such cases, tokens can act like digital certificates of ownership that are stored on blockchain (ChainLink, 2023). 1

This tokenization process benefits all sort of assets, facilitating fractional ownership of tokenized assets and yielding a more transparent price discovery (Liao and Caramichael, 2022). Moreover, tokenized private securities can be traded more smoothly on secondary markets, eliminating the administrative complexities associated with conventional private securities. Furthermore, tokenized private securities stand to gain enhanced liquidity without compromising their cost-effectiveness (The Tokenizer, 2019).

But in a broader context, the integration and the use of these DeFi applications would have faced yet again challenges arising from cryptocurrencies volatility. This challenge has been effectively mitigated through the adoption of stablecoins, which are briefly defined as digital currencies recorded on DLTs that are pegged to a reference value (Liao and Caramichael, 2022). These stablecoins aim to maintain a 1:1 value with a tangible asset, which can encompass fiat currencies, stock indices, or equities. Stablecoins come in various forms (Arner et al., 2020; Gruenwald et al., 2022). The first type is custodial stablecoins, also known as fiat-backed stablecoins. These are backed by a range of cash-equivalent assets, such as bank deposits or even Treasury bills, seeking to provide crypto-to-fiat 1:1 conversion. Algorithmic-backed stablecoins form the second type, often relying on on-chain algorithms to maintain a constant value by adjusting the stablecoins supply. The third type comprises crypto-backed stablecoins, the case of Dai, which represents the stablecoin of MakerDAO, crucial for the two case studies discussed in this paper. For instance, this stablecoin employs overcollateralization, where users deposit 150% of another cryptocurrency’s value to ensure stability through automatic liquidation if collateralization falls below the specified ratio (Rosenberg and Pandl, 2022), ensuring Dai’s stability. This stablecoin will be the subject of the following analysis.

The infrastructural perspective on the banking-blockchain linkage

This section aims to examine blockchain technology through an infrastructural lens, a necessity for a comprehensive understanding of how the banking system aims to attain centrality and shapes this technology in line with its narratives and goals.

In this paper, infrastructures are understood as socio-technical systems, an assemblage of objects and practices that act in the background, “structuring relations through enabling some forms of actions and constraining others” (Gjesvik, 2023: 728). Infrastructures are regarded as socio-technical systems, aligning with the tradition established by other authors (Beaumier and Kalomeni, 2022; Bernards and Campbell-Verduyn, 2019). Specifically, insights from IPE and STS literatures are integrated to comprehend infrastructures as having a relational component, as they consist of bundles of both physical, non-human objects, as well as an array of human practices (Bernards and Campbell-Verduyn, 2019). This decision was made because these research bodies delve into the agency of infrastructures, placing equal emphasis on their structuring capacity (De Goede, 2021). Thus, building upon this definition, the aim is to move beyond the analysis of the mere materiality of infrastructures (Bernards and Campbell-Verduyn, 2019). For instance, when addressing blockchain technology as an infrastructure, given its central role in this paper, this paper comprehends it as encompassing diverse software, computers, mining centers—all erected upon the foundation of the internet infrastructure. Nevertheless, these technological artifacts coalesce into an infrastructural assemblage solely when stemming from human practices, actions, or thoughts (e.g., Beaumier and Kalomeni, 2022). As every infrastructure has a human or mundane component, it embeds particular functions, constraints or narratives (Bedford, 2019), highlighting the significance of the system’s functionality rather than its form.

As such, an infrastructure can be better understood through the functions it fulfills rather than its form. Within this context, this paper recognizes that infrastructures encompass not only efficiency improvements; they actively “shape, enable, and constrain (…) power in specific ways” (De Goede, 2021: 355). To delve deeper, there is an argument that any infrastructure should ideally exhibit uniformity, implying complete harmonization to minimize transactional costs and friction (Krarup, 2019). This paper concurs with this viewpoint. However, this perspective extends further to assert that these systems possess an ingrained political agency. A case in this point is the global payment infrastructure. For instance, existing papers contend that a certain reliance on global intermediaries exists for cross-border payments, fostering distinctive power dynamics (Brandl and Dieterich, 2023). As such, this ingrained political agency of infrastructures is intimately connected to a power component. Specifically, decisions made during the development of an infrastructure are not merely technical; they carry socio-political implications, influencing which entities wield authority, what agent benefits most from the infrastructure, and how the overall infrastructure is structured, hence the ingrained political agency aforementioned. Therefore, the development of infrastructures actively participates in shaping uneven power relations. However, this power within an infrastructure is not static but rather grown and shaped by ongoing interactions among economic agents with different degrees of agency.

This interpretation of infrastructures containing a power component contradicts certain perspectives asserting that “infrastructures don’t do anything, per se” (Bernards and Campbell-Verduyn, 2019: 777). In reality, most infrastructures are used to shape forms of governance and, significantly, accumulation strategies (Bernards and Campbell-Verduyn, 2019). Therefore, this paper highlights that these systems shape and are shaped by the interaction between two or more economic actors. This is relevant particularly when emphasizing the importance of decisions about encoding, standardizing, categorization, and scaling of infrastructures (Star, 1999). The notion of scaling is particularly pertinent in the context of this paper, as infrastructures are receptive to connection and enabling interactions for the development of new applications of an infrastructure.

This scaling involves a power renegotiation within an infrastructure. Specifically, it is argued that globalization and digitalization of financial markets consistently result in the emergence of new types of actors and a shift in the roles of existing ones (Brandl and Dieterich, 2023). This helps us in considering how new technologies are propelled by “internal patterns of political economy (e.g., accumulation and governance)” (Bernards and Campbell-Verduyn, 2019: 776). These patterns are linked to power dynamics, as multiple entities strive to control an infrastructure to attain financial advantages or power. Hence, it is contended that there is a power dynamic underlying the shaping of an infrastructure, and for this purpose, the actors “draw upon whatever organizational, cultural, economic, political, or material resources they can access from their position within multiple, overlapping fields” (Pinzur, 2021: 647). Precisely, within the realm of financial infrastructures there are actors endeavoring to exert influence to secure diverse infrastructural advantages (Pinzur, 2021), as exemplified by the banking system in this paper. Therefore, it can be argued that these infrastructures are constantly influenced by internal power dynamics, reflecting a multifaceted competition that reshapes both the entities occupying central positions and the manner in which that centrality operates (Gjesvik, 2023).

However, this control or power does not pertain to the architectural regulation imposed by the code, as argued before (Lessig, 1999). Instead, it originates from the premise than an infrastructure is inherently (re)distributive. To be more specific, an infrastructure is dynamic, consistently in a state of potentiality. As this system expands, private actors or social groups closely intertwined with its functioning may witness their leeway broadened, as the novel attribute of the infrastructure opens up fresh possibilities, enhancing the agency and power of these groups or actors (Edwards et al., 2009). Consequently, this paper challenges the essentialist notion that presumes the original vision of the technology designer will remain fixed. In contrast, aligning with the approach of Beaumier and Kalomeni (2022), this paper underscores the ever-present element of the creative behavior. To be more precise, infrastructures are not rigid structures; they are continuously built upon preexisting systems, while also facilitating a dynamic process in which new actors actively seek to shape them. Therefore, to more comprehensively encapsulate the dynamic nature of these systems, this paper draws upon the concept of infrastructuring. This concept encapsulates the reality than an infrastructure is not built but rather grown. It recognizes that numerous social, technological, and political innovations are amalgamated to forge far-reaching networks and applications, underscoring the existence of dynamism in the “situated practical work of developing and using an infrastructure” (Karasti et al., 2016: 4).

In the context of this paper, what is discussed is the emergence of the tokenization and the banking’s system interest in adopting this technological advancement to leverage its power. To clarify, this paper asserts that tokenization and smart contracts naturally arose due to the innovation of the technology’s participants. Banks only recognized the chance to control this infrastructure after these developments. Specifically, tokenization affirms the potential character of the blockchain infrastructure, signifying an extension of the infrastructure embodied at the moment t0 by the technology and the narratives behind Bitcoin. With the emergence of this new dimension in blockchain technology, banks identified a novel avenue for exercising control. Specifically, the banking system now seeks to establish its dominance over this novel infrastructure while pursuing one main objective. The main objective is related to subverting the original intent behind the creation of blockchain technology, particularly Bitcoin. This original intent was to address the challenges posed by banks in the aftermath of GFC and potentially even replace them.

It is well-known that banks have been central to the global financial system for centuries, serving as intermediaries that facilitate transactions, provide loans and even settlement services. With the emergence of blockchain technology, especially of tokenization, there is a potential for new financial systems to emerge that may bypass traditional banks. As such, by engaging in an infrastructuring process and asserting authority over blockchain, banks can position themselves to adapt and integrate these innovations while preserving their core in the financial ecosystem, changing the narratives behind this technology in the process. Hence, if the original intent of blockchain technology was to offer an alternative to the conventional banking system, in line with libertarian principles, the current reality reveals that banks are now pursuing the utilization of this novel infrastructure to exert control. Therefore, by using blockchain technology, banks can centralize this infrastructure and can create new nodes of power by exploiting the asymmetries within this relationship (Gjesvik, 2023), hence the ongoing process of infrastructuring.

The power dynamics within the infrastructural approach to blockchain technology

It is argued that the blockchain technology aimed to relocate the power of any single sovereign entity, as well as that of corporations, into the hands of users, establishing an extra-statist economic model based on private initiative (Shapiro, 2022). This is why it has been also argued that blockchain technology is the result of an ideological connection with crypto-anarchists engineers and thinkers from the United States of 1980s and 1990s (Vidan and Lehdonvirta, 2019). However, the ideology steering this infrastructure underpinning Bitcoin defies conventional or classically modernist expression. Instead, it adopts the guise of a techno-utopian idea, aspiring to construct an impersonal economy devoid of centralized governing authority (Vidan and Lehdonvirta, 2019). On the contrary, other authors see the opposite and view that blockchain technology possesses a robust political essence, hence the idea of this infrastructure being nothing but politics masquerading as technology (Golumbia, 2015). This perspective emerges due to the concentration of power at the level of code. More explicitly, blockchain technology illuminates the ascendancy of code as the foremost instrument for regulating the conduct of economic actors (De Filippi and Hassan, 2016). Nevertheless, as this paper already argued, the crux lies not in the code itself, but rather in the dynamics of power and the unique interpretation furnished by such a system.

This perspective encapsulates the core of the STS approach. Specifically, it has been previously argued that diverse social groups can furnish distinct interpretation of a technology, interpretations intrinsically intertwined with narratives (Reijers and Coeckelbergh, 2018). In this context, a narrative envisions the prospective interpretation tied to the infrastructure represented by the blockchain technology, encompassing how diverse social groups envision its future applications and how this vision can be imposed on others. This interpretation underscores that human agency takes the forefront and that the functionality of an infrastructure is molded or “co-produced” (Jasanoff, 2015: 16) through the interplay of various social groups and their narratives (Reijers and Coeckelbergh, 2018). That is why it could be argued that the actual configuration of an infrastructure “emerges from its dynamic interactions with social, political, and legal domains” (Kohl, 2021: 22), giving rise to distinctive interpretations. As such, this infrastructure commenced with a cypher-punk or a libertarian ethos aimed at eradicating all intermediaries (Swartz, 2018) and advancing a utopian societal vision (Dodd, 2015). Nonetheless, it has been impacted by a plethora of new narratives, underscoring its application in diverse economic endeavors (Swan, 2015). This is exemplified by China’s state-developed national reputation system and the adoption of blockchain technology by law enforcement for “predictive policing” (Manski and Manski, 2018: 158). Similarly, corporations have started adopting the same technology, with Amazon AWS standing out as a prime example. It epitomizes the quintessential illustration of blockchain technology provided by private tech companies, representing a form of corporate governance (Beaumier and Kalomeni, 2022).

This is the reason why this study adopts a nuanced perspective on power dynamics and the process of infrastructuring, aligning with the transition from the traditional “power of influence” to a more contemporary “power of social interaction,” power that is constituted primarily by ideas and narratives (Duggan et al., 2022). In the literature, particularly in IPE, various types of power have been extensively discussed. One such power is ideational power, defined by agents’ ability to influence other actors’ normative and cognitive beliefs through the use of ideational elements, rather than merely coercing or structuring relations without discourse (Carstensen and Schmidt, 2018). Other authors discuss structural power, which is defined as the power to shape and determine the structures in which other states or agents interact (Strange, 1994), and this is extensively analyzed in relation to finance, arguing that this power resides in the central position the financial sector occupies in the legitimate functioning of an economy (Pagliari and Young, 2016). Additionally, Braun (2020) highlights the existence of infrastructural power, which is linked to the mutual influence exerted by two actors or sectors over each other. For instance, in the case of repurchase agreement (repo) markets and the European Central Bank (ECB), it has been argued that “(…) infrastructural power operates via policymakers’ expectation that harming particular markets would blunt their own policy instruments and thus diminish their control over the economy” (Braun, 2020: 400). Furthermore, in the broader theoretical literature on power, another crucial concept is coercive power, wherein an actor employs sanctions and incentives to compel another actor to do something it would otherwise not do (Dahl, 1957; Dallas et al., 2019). Although these approaches to power are insightful, the distinctiveness of “power of social interaction” (Duggan et al., 2022) employed in this paper lies in its focus on the nuanced dynamics of actors competing for centrality to influence the trajectory and development of an infrastructure. Specifically, unlike traditional forms of power that focus on beliefs, institutional positions, or coercive measures, power of social interaction recognizes the multifaceted, fluid and contingent nature of power relations that is co-constructed through ongoing interactions and negotiations among agents with a different degree of agency within an infrastructure. It underscores how these interactions influence the evolution of power dynamics and ultimately shape the trajectory of the infrastructure. It is precisely this fluid understanding that contrasts this power with traditional understanding of structural power (Strange, 1994), which emphasizes the enduring and institutionalized structures in which certain actors or institutions exert influence. As such, the “power of social interaction” becomes paramount for understanding how infrastructures are constantly evolving and adapting, highlighting the process of infrastructuring.

In more detail, the crucial distinction is that this “power of social interaction” is balanced by an “agent-based power” that is represented in this context by banks (Duggan et al., 2022). Specifically, the agent-based power underscores the capacity of banks to exert influence not just through traditional power structures but by actively participating in and altering the trajectory and the narratives of the infrastructure, in line with their interests. In this context, banks’ interest is to remain at the core of the financial system even in the era of novel technologies. By integration blockchain and tokenization into their operations, banks contribute to the reconfiguration of socio-political conditions within this infrastructure. As such, this behavior gives rise to novel infrastructure narratives. For instance, blockchain was initially conceived as a decentralized, trustless system that carried the socio-political ideologies of its creation, often aligned with crypto-anarchist or libertarian principles. But banks are not passive recipients of technological change but active participants shaping the course and the narratives involved in the blockchain’s evolution, and this is where the process of infrastructuring resides.

Specifically, as traditional banks embrace and integrate blockchain technology, they contribute to a shift in the perceived nature of this infrastructure. The blockchain technology, once envisioned as a realm free from centralized authority, is now becoming entwined with traditional financial structures. In this context, banks play a pivotal role in redefining the narrative around blockchain, emphasizing collaboration rather than disruption. In detail, banks bring a more collaborative and regulated approach to the decentralized ethos of blockchain, departing it from the initial crypto-anarchist principles. This collaboration implies an acknowledgment of the benefits of regulatory frameworks, risk management, and institutional stability. The ideological underpinning in this evolving context emphasizes a pragmatic integration of blockchain within the existing financial ecosystem, fostering a narrative that envisions a future where decentralized technologies work in tandem with traditional financial entities. This proves that market infrastructures do not maintain neutrality; instead, they represent arenas of contention influenced by the perspectives and desires of those with the power to shape them (Pinzur, 2021).

As such, the focus shifts to the ability of individual actors within the financial infrastructure to actively mold and transform it. This capacity extends beyond the traditional understanding of a Dahl-ian power as a force imposed by other actors onto passive entities. Instead, it recognizes the agency of actors to shape an infrastructure according to their interests and ideas, but also based on the ability to gain and hold a central position in an infrastructure and to exploit the uneven relationships within such a system (Gjesvik, 2023). The blockchain’s journey, from its cypher-punk or libertarian roots to narratives of sovereignty and corporate governance, exemplifies how diverse entities contribute to the ongoing evolution of this infrastructure.

However, one question remains open for this argument. What specifically has led banks to gain a central position in this novel infrastructure? This paper argues that there are two reasons, but not the solely ones. The first one is the ability to lobby and the second one is the ability of banks to position their technologies at the core of financial transformations.

In the case of their ability to lobby, banking institutions engage in extensive lobbying processes to establish a framework for financial technologization while also aiming to maintain barriers targeting activities specific to banks, such as deposits, loans, or asset management functions (Hendrikse et al., 2018). Through this lobby, banks assert their influence and reinforce their central position within the potential development of blockchain infrastructure. It is argued so because only banks possess the banking instruments to be transformed into RWAs, namely bank loans or other wholesale banking funding instruments, such as covered bonds. This made them essential for the development of tokenization processes in the financial sector, shaping further the power dynamics and the narratives involved.

The second reason is the ability of banks to position their technologies at the core of financial transformations. After the GFC, traditional banking institutions found themselves at a crossroads. The crisis shattered trust in traditional banking systems, leaving a void that was quickly filled by the rise of disruptive FinTech companies and the crypto ecosystem (Hendrikse et al., 2018). These new companies represented a fundamental shift in the financial landscape, driven by technological innovations and a fresh approach to financial services. Sensing this fundamental shift, banks realized they needed to adapt, thus pursuing a restructuring of the business model to meet the demands of these new rapidly evolving markets. As such, concepts like platform, integration, and openness became central to their strategies as they sought to rebuild trust and demonstrate relevance in the digital age. Otherwise put, this led these institutions to streamline their networked infrastructures, mimicking the model promoted by these disruptive segments and adapting to the disruptors’ conception of control (Hendrikse et al., 2018). This adaptability lies in their organizational capacity and financial resources. Unlike smaller disruptors, banks possess extensive resources, both in terms of capital and talent. As such, the organizational resilience, extensive resources, and the imitation of disruptors allow banks to not only weather the challenges presented by new technologies but also to strategically incorporate these technologies into their existing frameworks, shaping new infrastructures (Edwards et al., 2009).

In more detail, banks have robust technologies, and their available resources and talent pool enable them to incorporate or be incorporated much more easily into blockchain technology, depending on the banks’ objectives and preferences. An illustrative example in this case is SocGen-Forge, developed by the Société Générale Group, which offers institutional issuers and investors the ability to manage financial products on the blockchain and bridge capital markets with digital assets—through tokenization. It is built upon a legal and technical framework designed to ensure full legal and regulatory compliance (SocGen-Forge, 2024). Another relevant example is the Tokenized Collateral Network (TCN) introduced by J.P. Morgan, which is an in-house blockchain-based tokenization application, enabling investors to turn all sort of financial instruments or products—such as money market fund shares—into digital tokens (Prashant, 2023). Therefore, by integrating blockchain into their own banking technologies, banking institutions gain the authority to influence the development of new standards, norms, protocols, or guidelines in this new blockchain infrastructure, shaping the narrative of this infrastructure around acceptable standards within the traditional banking industry. Moreover, banks have an extensive networking reach, allowing them to form new strategic partnerships, and through these, they can obtain support from a broader network of stakeholders, further solidifying their narrative within this ecosystem. This reaffirms the process of infrastructuring within a framework of “power as social interaction,” highlighting bank’s capacity to integrate themselves into a novel infrastructure and reshape its underlying narratives and structures.

For more theoretical clarity, this paradigmatic shift recognizes that power relations are not static but emerge from ongoing interactions among different actors within the financial ecosystem. In essence, the central position of banks within financial infrastructures is intricately linked to their ability to leverage the “power of social interaction.” By actively participating in collaborative efforts, negotiating with other actors, and strategically deploying their resources, banks assert their influence over the narratives that govern the evolution of the banking system and the blockchain infrastructure. Therefore, through lobbying capabilities and positioning their own technology at the core of financial transformations, banks precisely control how the new infrastructure evolves, highlighting that these afford banks the strongest agency. This underscores the fluid and contingent nature of power dynamics, where agency and interaction play pivotal roles in shaping the ongoing development of an infrastructure.

Power dynamics and the digital linkage between the banking system and RWAs

As this paper ventures into the empirical realm, the focus shifts to two notable case studies: HVB and SocGen-Forge. In that vein, this section seeks to illuminates their purposeful efforts, not merely for technological integration but as a calculated move to establish control and authority within this novel infrastructure. Recognizing the inherent power dynamics in every infrastructure, banks consciously position themselves as pivotal actors in its unfolding narrative. By doing so, they navigate the evolving landscape, ensuring that the trajectory of this infrastructure aligns harmoniously with their objectives. Banks were able to do this due to their ability to exert “power of social interaction,” highlighting that power is not a unidirectional force dictated solely by structured features; instead, it is co-shaped through the agency of actors within the infrastructure. Delving deeper, this exploration unveils how these banking institutions emerge as central stakeholders, leveraging their role as key providers of financial instruments and collateralized loans—effectively playing the role of RWA. This strategic involvement not only safeguards them against potential disruptions but also places them at the forefront of shaping the advancements in tokenization and the broader landscape of this infrastructure represented by the blockchain technology.

HVB and MakerDAO

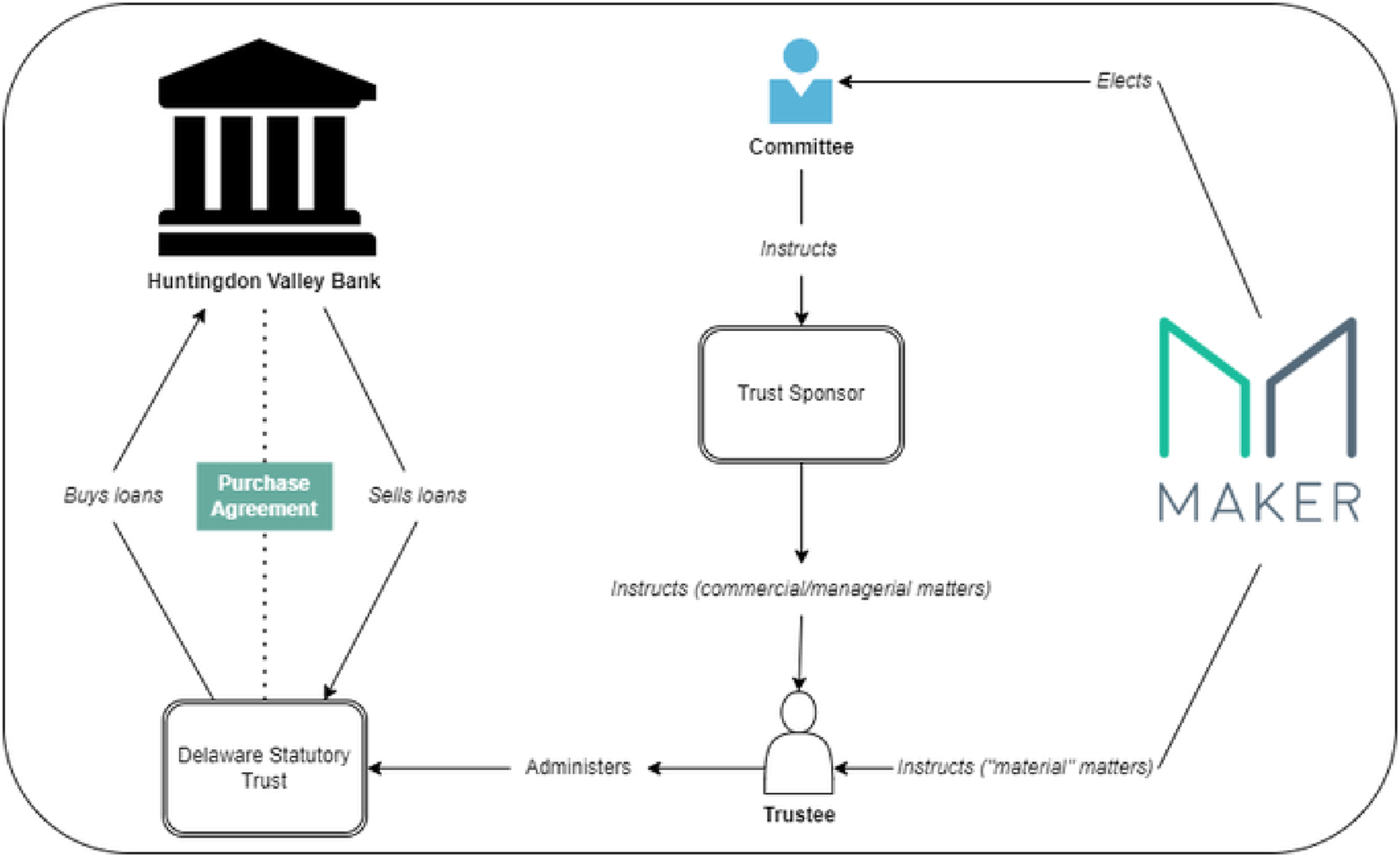

The first such digital linkage took place in July 2022. During that month the decision was taken, by vote, to make an active collaboration between a traditional bank and the MakerDAO protocol. Specifically, it was voted that a bank be integrated into the Maker protocol (Fernau, 2022). This bank is called HVB and it is based in Pennsylvania. It is held by HV Bancorp, Inc. and has a diversified portfolio, operating in residential mortgages, commerce lending, business or asset-based lending. As part of the deal, MakerDAO created a Dai vault with a total value of $100m for HVB. But the goal is to expand the initial debt ceiling from $100m to $1bn, in the near future. This marked the inaugural collaboration between a regulated US financial institution and a decentralized digital currency, specifically Dai (Globe News Wire, 2022). This groundbreaking collaboration underscores the convergence of traditional banking infrastructure with decentralized digital currencies.

This integration allows the bank to borrow via DeFi using its assets as collateral. Specifically, through this collaboration, the loans originated by the bank are accepted as collateral in the MakerDAO protocol. This allows HVB to engage in a process called “loan syndication,” but though smart contracts this time. Through syndication, the bank originates a loan but instead of retaining it in full, the originating bank retains just a fraction of a loan and “sells the remaining share to a syndicate of investors” (Ivashina and Scharfstein, 2010: 57), in this case, to the Maker protocol. This operation brings with it certain benefits, and the most important is the risk sharing. Since the bank must retain risk-adjusted capital for any loan originated, this risk sharing scheme allows a bank to extend the loan supply with greater ease. Specifically, through syndication, the risks assumed by the bank are diminished. Equally, not only risk sharing is important through this syndication, but also the bank’s ability to finance itself through the participation of institutional investors in the acquisition of loans initiated by the bank (Ivashina and Scharfstein, 2010).

But how exactly does this process unfold? The Maker protocol and HVB decided to create a trust in Delaware called Multi-Bank Participation Trust (MBPTrust), and this Trust was created for the benefit of MakerDAO. The MBPTrust represents a bankruptcy-remote vehicle, and in addition a corporate Trustee will be used to verify whether MBPTrust’s actions are consistent with the agreement between the parties (MakerDAO, 2022).

Through this vehicle, HVB gains access to Dai stablecoins. Specifically, this legal vehicle gives the Maker protocol the opportunity to participate in the loans originated by HVB (‘participating loans’), according to the First Portfolio Purchase Agreement signed between the two entities. For instance, after HVB originates mortgage loans, they can be considered loans for participation in the Maker protocol. If these loans are deemed appropriate, the MBPTrust has the opportunity to obtain up to 50% of the value of these loans, receiving a certificate of participation in exchange. In exchange for giving up a fraction of a loan, HVB receives Dai, in parity with the value of the sold fraction of that loan. Then, the originating bank, HVB in this case, can convert those Dai to US-Dollar (USD) and use that additional capital to write more loans (Fernau, 2022). In this way, HVB gets rid of the loan limit that was set at $7m per borrower relationship (Newar, 2022). This collaborative relationship will focus on expanding the portfolio of residential and commercial mortgages, but also small and medium enterprises loans, with fixed and floating rates. In this way, this digital linkage can support the mortgage market and beyond, as the $1bn debt ceiling will be used to diversify the loan portfolio of HVB (Alto, 2022). Equally, not all loans are eligible for this collaboration. In more detail, MakerDAO only accepts loans with a score of 6, according to a risk rating scale developed internally by HVB, which represents an “acceptable risk.” Therefore, all loans originated by HVB in its ordinary course of business comply with the bank’s credit policy and loan origination guidelines (Di, 2022). It has been argued that engagement in this protocol enables this bank to originate larger supply of loans that otherwise may have been too large to be funded by themselves (Alto, 2022). Figure 1. Illustrates how the MakerDAO/HVB ecosystem works: Source: Alto (2022).

But the benefits do not just stop at HVB. MakerDAO, before this collaboration, did not have the right to write USD-denominated loans to borrowers. But as it has obtained the right to up to 50% of certain “participating loans,” MakerDAO gets exposure in real financial positions, which means that they actually get involved in the lending processes. But MakerDAO will also get an important income from vault fees which are associated with maintaining the vault and minting Dai (Newar, 2022).

This collaborative effort has proven fruitful. Specifically, by the end of January 2023, the partnership yielded positive outcomes. Looking at the prevalent loan types, business loans took the lead at 56.5%, followed by investment real estate loans at 40.4%, and construction loans at 3.1%. Geographically-wise, the loan portfolio is split between Pennsylvania, with 71.1%, followed by New Jersey, with 22.2%, Connecticut, with 4.9%, and New Hampshire, with 1.8% (Maker, 2023).

As such, this relationship showcases the meticulous structuring required for regulatory compliance and risk management in this hybrid financial landscape. This collaborative effort not only highlights the adaptability of traditional banks to novel technologies but also underscores their role in steering the direction of this infrastructure. It signifies a deliberate exercise of power through technological integration, where banks navigate the intricate interplay between traditional financial norms and the transformative potential of blockchain technology.

SocGen-Forge and MakerDAO

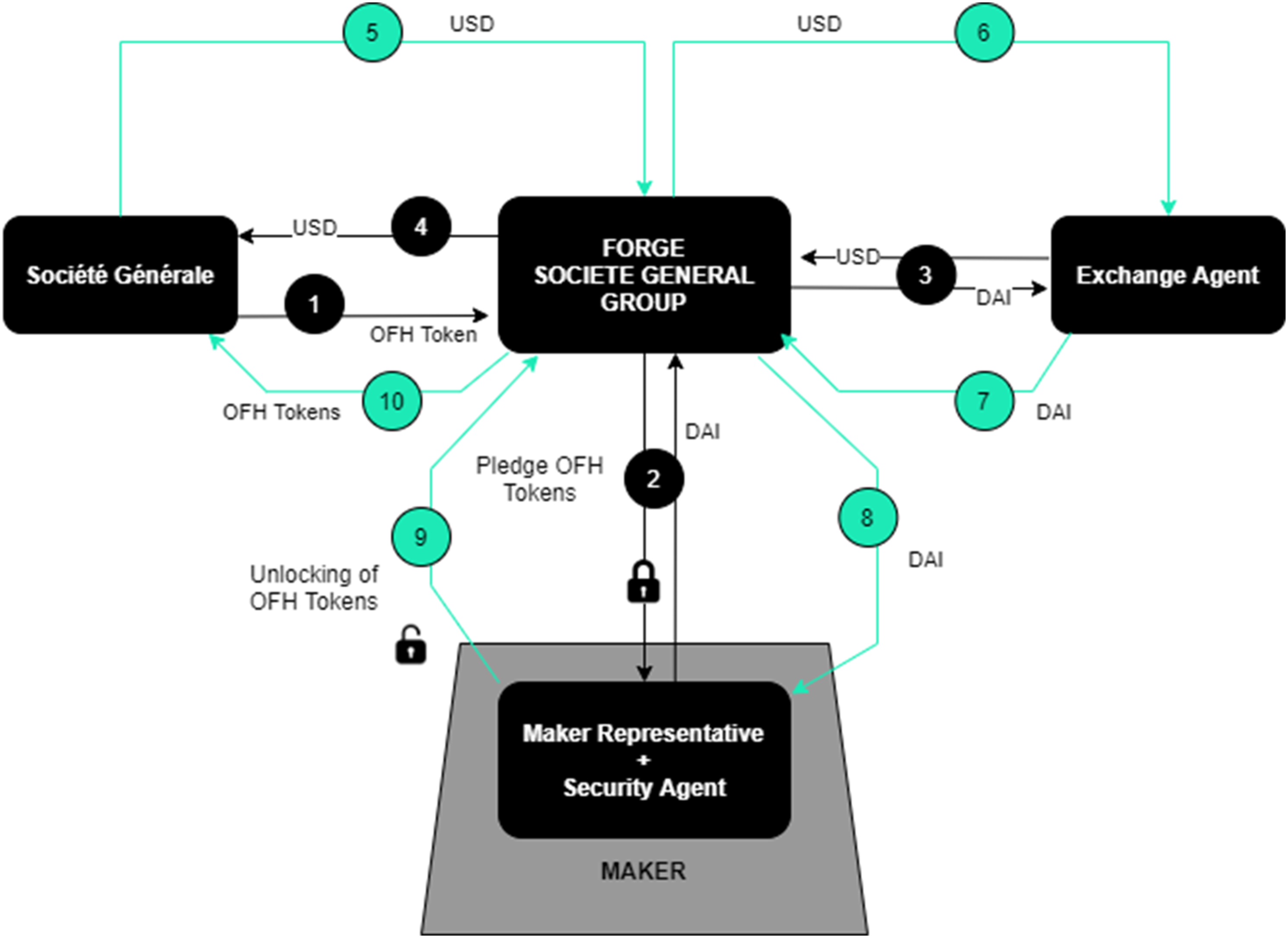

However, this relationship is not solely built on bank loans. The Maker protocol has also initiated collaborations with European banks. Specifically, during the same period as with HVB, the decision was made for MakerDAO to onboard EUR-denominated covered bonds backed by real estate debt and issued by SocGen. There covered bonds represented RWAs. Covered bonds are securities “issued by a bank or similar institution that provides on-balance sheet funding of assets” (Gambro et al., 2009: 59). This collaboration officially began in December 2022, at which point SocGen-Forge, a subsidiary of the SocGen, started testing the Maker Vault. However, SocGen-Forge, a regulated subsidiary of the banks specializing in digital assets, submitted the application back in October 2021. This partnership evolved naturally as SocGen has been at the forefront of experimenting with blockchain assets, being one of the very first banks to issue bond-backed tokens on Ethereum blockchain as early as 2019 (Thurman, 2021).

But how exactly did this relationship work? SocGen-Forge aimed to refinance covered bonds held by SocGen in the form of Security Tokens, called obligations de financement de l’habitat (OFH) token, issued on the Ethereum public blockchain. The tokens that SocGen has submitted for application as collateral were issued in May 2020, carry a fixed rate of 0% and are set to mature in May 2025, earning an AAA rating from both Moody’s and Fitch rating agencies (Thurman, 2021). These tokens were marked-to-market, implying that during the entire collaboration, SocGen-Forge had to daily assess the market value of these tokens. If they did not fully cover the Dai debt, SocGen-Forge had to either provide additional OFH tokens as collateral or make a partial debt repayment (SIA Partners, 2021).

Figure 2 illustrates the detailed interaction between SocGen-Forge and MakerDAO. In the initial step, SocGen provided covered bonds to the Forge division, which were then forwarded to MakerDAO—in exchange for Dai—and to a security agent or trustee, as required by French law to enforce loan terms on Maker’s behalf (Thurman, 2021). Subsequently, Forge transferred these stablecoins to the Exchange Agent, receiving USD in return. These USDs are paid to SocGen. Towards the end of the process, as shown in the green numbers in the Figure 2, SocGen remits USD back to Forge division, and Forge, in turn, sent them to the Exchange Agent, which converted USD back into Dai. Finally, these stablecoins were returned to MakerDAO, which released tokenized covered bonds back to Forge. Forge completed this cycle by returning the tokens to SocGen (SIA Partners, 2021). illustrates the development of the relationship between SocGen-Forge and MakerDAO: Source: SIA Partners, 2021.

Specifically, SocGen-Forge funded this loan by borrowing Dai from MakerDAO using these OFH Tokens as loan collateral (SocGen Forge, 2023). To provide details, similar to the case of HVB, SocGen-Forge gained access to a vault with a credit limit of $30m in Dai (Wagner, 2023). This vault was overcollateralized and so backed by €40m in bonds in the form of OFH tokens. SocGen used this vault for the first time in January 2023, withdrawing $7m worth of Dai (Wagner, 2023). This vault was closed after April 2023. However, this relationship proved to be a genuine success, indicating that banks will continue to use blockchain technology. Moreover, a representative from SocGen-Forge argued that this technology opens new avenue for banks, as it demonstrated that on-chain refinancing markets could be opened to real money asset owners, in full compliance with banking standards (Haig, 2023).

Besides these case studies, additional case studies showcasing the interconnectedness of banks with tokenization can also be explored. For instance, Standard Chartered announced in July 2023 that a group of investors has bought up to $500m worth of tokenized trade-finance assets posted on the Ethereum blockchain (DigFin, 2023). This came shortly after Bank of America announced that tokenization will reshape the global financial system and is part of its long-term strategy (Bank of America Institute, 2023).

SocGen-Forge’s collaboration with MakerDAO highlights the infrastructural shift in traditional banking. By tokenizing EUR-denominated covered bonds as RWAs, banks assert strategic control in the evolving infrastructure. This active role in tokenizing real financial assets reflects their power play to shape blockchain technology’s narrative. Specifically, the proactive engagement of SocGen-Forge in the tokenization process fosters a narrative of collaborative and regulated integration within the decentralized realm of blockchain. This collaboration signifies recognition of the advantages associated with regulatory framework and effective risk management.

As a synthesis, these case studies underscore the traditional banking system’s strategic immersion into this emerging infrastructure, imprinting established financial practices, norms, and goals onto this infrastructure. This deliberate engagement by banks serves to influence and steer the narratives of blockchain technology, exemplifying their pursuit of a central role within this evolving infrastructure.

Concluding remarks

In conclusion, this paper aimed to capture the power dynamics and infrastructuring processes that impact an infrastructure. These power dynamics are inherently tied to the different degree of agency participants hold, meaning that within an infrastructure, there is a constant competition for centrality. These power dynamics have been analyzed using the concept of “power of social interaction,” which asserts that these dynamics are constantly shaped by the interaction among agents within an infrastructure. It has also been argued that banks wield the strongest agency and have been able to attain centrality within this infrastructure due to their lobbying capacity and their ability to position their technologies at the core of financial transformations. Moving forward, this theoretical analysis was substantiated by empirical examination of relationship between HVB and SocGen and emerging protocols, exemplified by MakerDAO. These partnerships not only highlight a deliberate embrace of blockchain technology and tokenization, but also unveil the proactive measures banks take to establish authority, control, and leverage within the evolving infrastructure.

As such, this transition to RWAs and tokenization symbolizes more than a mere adaptation; it signifies a concerted effort by banks to redefine their role in the digital era, aligning with the argument of some other authors (Bassens and Hendrikse, 2022; Campbell-Verduyn, 2018). Actively engaging in the creation and management of tokenized assets, particularly stablecoins backed by RWAs, banks secure a central position in shaping the future of the blockchain infrastructure. Beyond technological integration, banks play a crucial role in infrastructuring processes, actively bundling different infrastructures and impacting the narratives behind them.

As such, the novelty of this paper lies not only in its comprehensive examination of these strategic maneuvers but also in its contribution to the field of IPE (e.g., Beaumier and Kalomeni, 2022; Bernards and Campbell-Verduyn, 2019). By recognizing infrastructures as dynamics entities with inherent political agency, constantly evolving rather than remaining static, the paper challenges conventional views of power within financial infrastructures. The introduction of the concept of “power of social interaction” emphasizes ongoing interactions as co-shapers of power relations. Moreover, this paper presented a unique analysis of tokenization, an underexplored concept in IPE and STS literature. Understanding tokenization is crucial for grasping its implications on financial practices, market structures, and regulatory frameworks, advancing our understanding of finance-technology intersections.

As we navigate this transformative landscape, it is evident that the synergy between banks and DeFi protocols represents a pivotal moment in reshaping the control mechanism within financial infrastructures. The strategic collaborations observed underscore the transformative potential of blockchain and decentralized technologies, redefining traditional structures and control dynamics within financial systems. Monitoring how these control dynamics evolve will provide valuable insights into the continued integration of traditional banking with the blockchain and the evolving nature of power within financial infrastructures.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.