Abstract

The literature on demand-driven growth models, while an important contribution to comparative political economy, places too much emphasis on developed countries and too little on the international political economic context. To extend these models to the periphery, where international influence is especially important, it is suggested that theories of hegemony and dependency be incorporated into the analysis. The main argument is that international relationships can limit the ability of peripheral countries to produce more sophisticated goods and attain high-income status. The nature of the limits varies with the needs of the hegemon (or rising hegemon), which are met via three dependency mechanisms: markets, leverage, and linkage. The proposed approach is illustrated by a study of Latin America from 1990 to 2020. After following a consumption-led model from the end of WWII until the debt crisis of the 1980s, a new export-led model was introduced in the 1990s, with different variants in the northern and southern parts of the hemisphere and different “winners” and “losers.” In the 1990s, US dominance favored Mexico through its incorporation into US industrial value chains, while China’s entrance into the region after 2000 privileged South America’s commodity producers. The trade and financial advantages afforded the two subregions by the respective powers were offset by negative aspects of the dependent relationships. Mexico’s sophisticated industries financed by US FDI benefited only certain enclaves in the country, while South America suffered reprimarization and deindustrialization through its new links with China.

Introduction

Growth models in peripheral capitalist countries constitute a crucial agenda for policy makers as well as for scholars in the 21st century. 1 If these countries are to achieve a better living standard for their citizens, their governments and private-sector leaders need to devise growth models or strategies that will enable them to strengthen their economies and share the gains in a relatively even way. Attempts to do so have a long history, but most peripheral countries have been unsuccessful, so the agenda remains on the table today.

If growth models per se are important for peripheral countries, what about the literature on growth models within the comparative political economy (CPE) tradition? The most useful contribution to this literature is the recent volume edited by Baccaro et al, (2022), hereafter BBP. On the positive side, BBP makes two advances. It restores the growth focus on demand, and it provides a useful framework for the comparative analysis of drivers of growth (domestic consumption vs exports). At the same time, it has two significant weaknesses from the peripheral perspective. It focuses heavily on industrial countries, especially western Europe, and it concentrates on domestic aspects of growth while neglecting the international political economy (IPE) context in which growth occurs.

The special issue of which this article is part aims to extend the European-focused literature to peripheral countries and to study the differences involved. My article tackles the second problem, focusing on the international context that peripheral countries face. While BBP begins to close the CPE-IPE gap, its international analysis only provides a starting point. To deepen the analysis, I bring in some literature not considered by BBP or other versions of the growth model literature, and I emphasize changes in the international political economy facing peripheral countries.

The article focuses on Latin America in the period after the 1980s debt crisis. The new literature introduced involves hegemony and dependency, which are important both because hegemons can skew development models in dependent countries and because hegemonic and other significant changes have occurred in the last three decades. In the 21st century, in contrast with the 20th, US hegemony in the region (and the international system more generally) is being challenged by an increasingly powerful China. More competition opens new opportunities for peripheral countries in export markets, finance, and new partners to help them integrate into the international political economy in more advantageous ways. In addition, rising and declining hegemons vary in factor endowments, political systems, and experience in the world; these differences vary the opportunities—but also the challenges—in the international sphere.

Other international changes involve trade and finance. Trade no longer focuses primarily on two countries but involves a much more complex web known as global value chains (GVCs). In addition, trade in services is of growing importance, including financial services, one aspect of what some call the “financialization” of the international economy. Finance itself has also changed with the shifting constellation of hegemonic powers. The west primarily exports capital to peripheral countries through private channels: foreign direct investment (FDI) together with equity and bond issues. In the case of China, the public sector is the main source of finance for the periphery: FDI from state-owned enterprises (SOEs) and loans from government banks.

The main argument of the article is that trade and financial relationships between hegemon and peripheral countries place limits on the ability of the latter to achieve dynamic growth and upgrade their productive capabilities. These relationships can also limit the possibility of more equal distribution of growth—which is a crucial topic but cannot be addressed here to the extent it deserves for lack of space. The nature of the limits varies according to the characteristics and needs of the hegemonic powers: export markets, access to natural resources, and/or increased production efficiency. The satisfaction of these needs is brought about through several dependency mechanisms: markets, leverage, and linkage. Peripheral countries have varying abilities to support hegemonic needs, leading to different kinds of relationships. In the vast majority of cases, however, the needs of the hegemonic countries take precedence, limiting options in the periphery.

The article begins with a critical discussion of the existing literature on growth models and my proposed additions. It then looks briefly at the drivers of economic growth in Latin America in the early postwar years, and the role of the international political economy, as background for the analysis of development experiences in the last three decades. The latter period, in turn, is divided into two parts. The first—the 1990s—examines the situation when US (and European) dominance continued from the earlier years. The second period—the first two decades of the 2000s—turns to the new context as China began to challenge the west. The conclusions discuss how analysis of Latin America can help understand growth models and how growth models can help understand Latin America.

A theoretical prelude

The basic thrust of the growth model (GM) approach is to (re)emphasize the role of aggregate demand in determining economic growth rates. This is, of course, a return to the Keynesian analysis that dominated economics during the early postwar period. 2 Leading proponents of a GM/demand approach identify two basic growth models: consumption-led and export-led (Baccaro and Pontusson, 2016). The consumption-led model relies on wages to provide the necessary demand to stimulate investment and growth, so a certain level of equality between capital and labor is necessary for the model to function. The export-led model, in contrast, finds its demand outside the domestic economy. Consequently, equality is less relevant or even prejudicial since high wages reduce export competitiveness. Thus, the models have implications for distribution as well as growth, but we focus mainly on the latter. 3

Even though export-led growth in particular must rely on the international economy, the GM literature tends to be part of the CPE tradition that pays little attention to the ways in which IPE affects economic growth. BBP begins to remedy this problem, as scholars in their volume challenge the lack of attention to international factors with respect to growth models, arguing that both CPE and IPE must be considered or even that IPE should be seen as the main driver. In particular, Schwartz and Blyth (2022) discuss four levels of IPE involvement in growth models. The first level involves independent responses from individual countries to international problems or shocks. The second brings in the fallacy of composition to suggest that not all countries can follow the same response pattern, or a crisis may result. At the third level, the question of power becomes important. Specifically, “the world is not composed of equal-sized units with equal power and resources” (Schwartz and Blyth, 2022: 104). Given such differences, a dominant (external) actor may try to impose a growth model or to shape domestic actors’ behavior. The fourth level moves toward the system itself where growth is a property of both country and system.

Two literatures, while directly related to the third and fourth levels of the Schwartz-Blyth framework, have not been brought together with GM discussions: the analysis of hegemony and of dependency in the capitalist periphery. The literature on hegemony has multiple variants, but two can be considered foundational. One, based on work by Kindleberger (1973) and Gilpin (1981), considers hegemony as leadership. It is primarily interested in the role of the hegemonic country in providing stability to the system as a whole, especially through the provision of public goods. 4 The second variant derives from analyses by Cox (1983) and Arrighi (1990), both of whom draw on Antonio Gramsci. Dominance rather than leadership is the key concept in this variant, but it is “dominance plus,” according to Gramsci and followers. “It is the power associated with dominance expanded by the exercise of ‘intellectual and moral leadership’” (Arrighi, 1990: 366).

The focus on the system level in both approaches limits their usefulness for our purposes, but the Cox/Arrighi version is more relevant through the concept of dominance and resulting connections to dependency. Also, both theories link to our analysis via cycles of hegemony. That is, a hegemon can be displaced through war or other means, with shifts from Dutch to British to US hegemony generally being identified. This article considers the implications of a relative decline in US hegemony in the face of a surging China.

The writings of Arrighi, and colleagues in the “world system” school, are closely related to dependency analysis. Although they view capitalism as constituting a world system, they stress the hierarchical nature of the system with a core, semi-periphery, and periphery defining winners and losers. These are also major categories in dependency analysis. The concept of dependency per se emerged from Latin America in the 1960s to analyze the region’s relationship with Britain and the United States. Like hegemony, dependency analysis has variants; Palma (1978) identifies two. One is a “theory of Latin American underdevelopment” (Frank, 1967), which views development in the core and periphery as antithetical. The other (Cardoso and Faletto, 1979) argues that development of a highly unequal kind can occur in the periphery through an alliance between external and internal actors. I rely on the second as the more realistic account of the world.

Cardoso and Faletto (1979: XX) define dependency: “From an economic point of view, a system is dependent when the accumulation and expansion of capital cannot find its essential dynamic inside the system.” Madariaga and Palestini (2021: Chp. 1) discuss three reasons for reviving the dependency approach to discuss peripheral development (or lack thereof). First is the focus on inequality between actors and sectors, which is inherent in the core-periphery distinction. Second, dependency seeks to connect national and international levels of analysis. Indeed, they specifically say that dependency helps bridge the CPE-IPE divide. Third, dependency is a perspective coming out of the periphery rather than being developed in Europe or the United States and superimposed on peripheral country experiences—if the latter are considered at all. Recently, it has been suggested that the concept of dependency is useful not only for understanding UK and US relations with the periphery in the 19th and 20th centuries, but also the new role of China in the 21st century.

To revive dependency analysis, which had fallen out of academic favor partly due to lack of mechanisms to explain how it functions, Stallings, (2020) suggests three mechanisms that characterize a dependent relationship: markets, leverage, and linkage. Markets—especially for trade and finance—provide the vital prerequisites for economic growth. Leverage manifests itself when powerful countries set out to influence the behavior of less powerful ones; it involves the direct use of political and/or economic power. Linkage is the set of relationships—ideas, education, employment, and living experiences—whereby actors in dependent countries come to identify their interests with those of a more powerful country. All three were found in Latin America in the period under analysis, with market access the dominant mechanism but leverage and linkage as complements. Over time in the US case, a shift took place from leverage toward linkage as international norms made the use of force less acceptable. For China, leverage was never viable in Latin America for geographical and historical reasons, so markets and linkage were used. Through these mechanisms, hegemonic powers pursued their own interests in peripheral countries, often resulting in lower growth, greater inequality, and higher volatility in the latter.

A final strand of GM literature that is important for our purposes involves financialization or the increasing importance of the financial sector in all aspects of the economy and society. Ban and Helgadottir (2022) argue that one of the main problems with the CPE literature about growth models is that it considers finance only in a very narrow way. Schwartz and Blyth (2022) agree, saying that an important part of IPE analysis—in contrast to CPE studies—is focused on money and financial dynamics. Financialization can be considered at the national or international level. In either case, it leads to de-emphasizing production and productive investment in favor of earning profits through the circulation of money. In turn, this provides greater access to finance for borrowers. Global financial centers are the archetypical example of international financialization, but the growing international role of banks and equity markets is more important in quantitative terms. These international financial markets constitute an important aspect of the dependency approach.

The article focuses on growth models in Latin America and finds aspects of the GM literature to be useful. First, the BBP consumption and export-based models provide a comparative framework for the study of growth models. Second, the Schwartz and Blyth analysis of the connections between international and comparative political economy offers a fruitful starting point for a deeper analysis of the relationship. Third, the discussion of financialization provides a complement to the study of financial relations of dependency. At the same time, I argue that the growth model approach needs to be adapted if it is to be extended to peripheral countries. In particular, I advocate the incorporation of theories of hegemony and dependency to help explain limits on development potential in the periphery.

Background: From the end of WWII to the debt crisis

Like Europe, Latin America experienced a “Golden Age” in the early postwar period. Economic historian Rosemary Thorp (1998: 159) put it this way: “Latin American economic performance during the three decades that followed the Second World War was outstanding. From 1945-73, continental GDP grew at 5.3% a year, while output per capita rose at nearly 3%. This was unprecedented for Latin America, just as the developed country growth record was the fastest ever.” She went on to say that the manufacturing sector became the engine of growth, leading to labor productivity gains, higher real wages, and stronger labor unions. OPEC’s price increase in 1973 caused serious problems for Latin American oil importers, but they were able to borrow their way to continued prosperity till the end of the decade. The second oil shock in 1979-80, however, brought profound changes to the region. The debt crisis of the 1980s led to a “lost decade,” when per capita income did not grow at all, and to the introduction of a new growth model.

After World War II, Latin American governments were eager to build on the ad hoc industrialization that had occurred during the Great Depression. The idea was to industrialize through substitution of products previously imported (import substitution industrialization or ISI). This would require governments to take a more active role in the economy, but foreign capital would also have to be a partner because the region lacked finance and technology. Participation in the industrialization drive varied according to the size and strength of different economies. For those wanting to industrialize further, import tariffs were a key policy tool. Another crucial policy involved finance for new industries. Given the lack of local capital markets and limited access to international financial markets because of earlier defaults, governments revised legislation to attract multinational corporations (MNCs). Mainly coming from the United States, MNCs soon flooded into the region. 5

The ISI growth model was based on consumption of two kinds: wages and government expenditure. 6 Although no full set of demand accounting statistics exists for the period, some partial data are available. According to Alarco Tosoni (2014), the wage share of GDP for the region averaged about 41% from 1950 to 1972, at which point it began a steady decline toward 35% in 2010. At the same time, fiscal deficits were large and growing from the 1950s through the 1970s. Thorp (1998: 170) reports that weighted-average deficits for the six largest countries in 1960 were 6.3% of GDP, rising to 8.5% in 1970. While the wage share was high and fiscal deficits were increasing, the export share of GDP was falling. In 1945, the export ratio was 17%, tumbling to a low of 7% in 1975 (Thorp, 1998: 160). By contrast, imports rose since the new industries required capital goods, technology, and other inputs that could not be produced domestically. The combination led to trade and current account deficits that grew much larger in the 1970s. 7

After the 1973 oil shock, debt rose rapidly in the region as oil importers borrowed on the international capital markets to maintain their growth rates. Foreign currency debt in Latin America rose from US$7 billion in 1960 to US$314 billion in 1982. Debt service increased from 18% of export revenue to 59% (Bulmer-Thomas, 2014: 389). The debt further fed demand in the region, mainly through deficit financing for SOEs. This situation drove external deficits and increased inflation. By the beginning of the 1980s, it was no longer possible to service the debt, given the lack of export revenue. 8 The debt crisis of the 1980s marked the end of the ISI period.

Latin America’s inability to sustain the high growth that characterized the first three postwar decades was due in large part to its dependent position in the world economy. Postwar problems were also attributable to domestic political arrangements, of course, but the political situation was closely linked to Latin America’s international relations. The role of MNCs was crucial. MNCs joined forces with local capital and state actors to produce consumer goods for local markets, earning high profits behind protective tariff barriers (Evans, 1979). While Latin American governments wanted firms to export to earn foreign exchange, MNCs saw little to gain. At the same time, new industries were heavily reliant on imports. The combination led to balance-of-payments problems, stop-go cycles, and the inability to achieve sustained growth. While these problems were mainly based on Latin America’s insertion into international markets, the political leverage component of dependency was also found in the postwar period. As detailed by Kinzer (2006), US interventions to combat governments seen to deviate from a capitalist path included Guatemala (1954), Cuba (1960), Dominican Republic (1965), and Chile (1973).

After 1973 oil shock, the characteristics of Latin American dependency changed, reflecting the new financialization of the global economy. The Eurodollar market, which started in the 1960s, provided space for unregulated financial transactions. Loans were generally priced at floating interest rates, passing risk onto borrowers. The Euromarkets burgeoned after the oil shock as OPEC oil exporters deposited their vastly expanded revenues there. The banks, in turn, had to find customers, and eager borrowers in Latin America seemed to provide a win-win situation. In reality, the borrowing splurge led to disastrous consequences for borrowing countries. The need to service their escalating debts resulted in a decade of austerity, rapidly growing poverty, and exceptionally high unemployment. The crisis provided dramatic evidence of Latin America’s dependent position as international banks joined with their governments and international financial institutions (IMF and World Bank) to enforce debt service—a clear example of economic leverage (Ocampo et al., 2014).

An export-led growth model under western hegemony (1990s)

Latin America’s emergence from the debt crisis featured a new growth model and a new insertion into the international political economy. The reasons for the adoption of the new model are controversial, ranging from it being forced upon Latin American countries by external actors to local governments and business leaders seeing no alternative after the lost decade of the 1980s (Stallings and Peres, 2000: 37-39). Characteristics of the new model were declining consumption, as the wage share fell and fiscal deficits were reduced, plus a substantial rise in exports as a share of GDP. Trade deficits continued, but they were smaller and could be financed by returning capital inflows.

Together with the export-led model was a more open economy in general and a parallel change toward a smaller state. The assumption was that foreign capital, in collaboration with the local private sector, could restore growth to the region. The state’s role would be to create a positive environment for business through a reform agenda and to balance macroeconomic accounts. Among the reforms anticipated, the most important were liberalization of imports and privatization of SOEs. Together, proponents of the new model argued, these reforms were necessary—and perhaps sufficient—conditions for development. It is noteworthy that development was no longer defined as industrialization, but as growth—accompanied by increased productivity, better jobs and living standards, and greater equity. 9

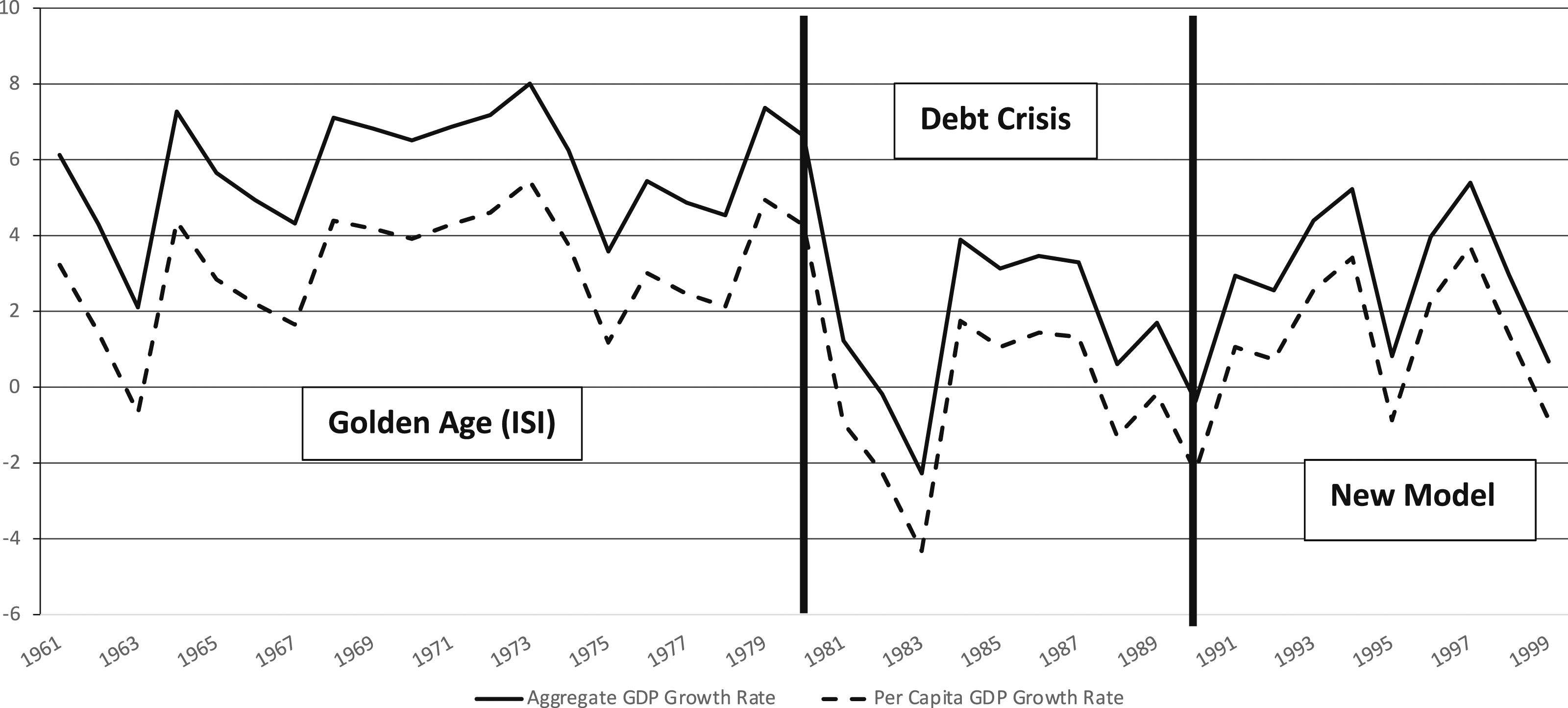

Growth did pick up in comparison with the disastrous 1980s, but it was much slower than during the Golden Age and quite volatile. Figure 1 shows aggregate and per capita GDP growth rates between 1961 (the earliest year for which comparable data are available) and 1999. It begins with the high growth of the 1960s and 1970s (5.8% aggregate and 3.2% per capita on average), followed by the lost decade of the 1980s (1.1% and −0.5%). Focusing on the 1990s, we find a mediocre performance (3.2% and 1.5%). In part, this was because some countries in the region adopted the new model with enthusiasm and generally did better, while others held back (Stallings and Peres, 2000). In addition, regional performance was uneven as national and international financial crises brought negative consequences: Mexico’s peso devaluation crisis in 1994, which spilled over to other countries of the region, and the Asian financial crisis of 1997-98. Ironically, the latter had a longer lasting impact in Latin America than in Asia itself, since it was followed by crises in Brazil and Argentina. Latin American GDP and GDP per capita growth rates, 1961-99 (%). Source: World Bank (online).

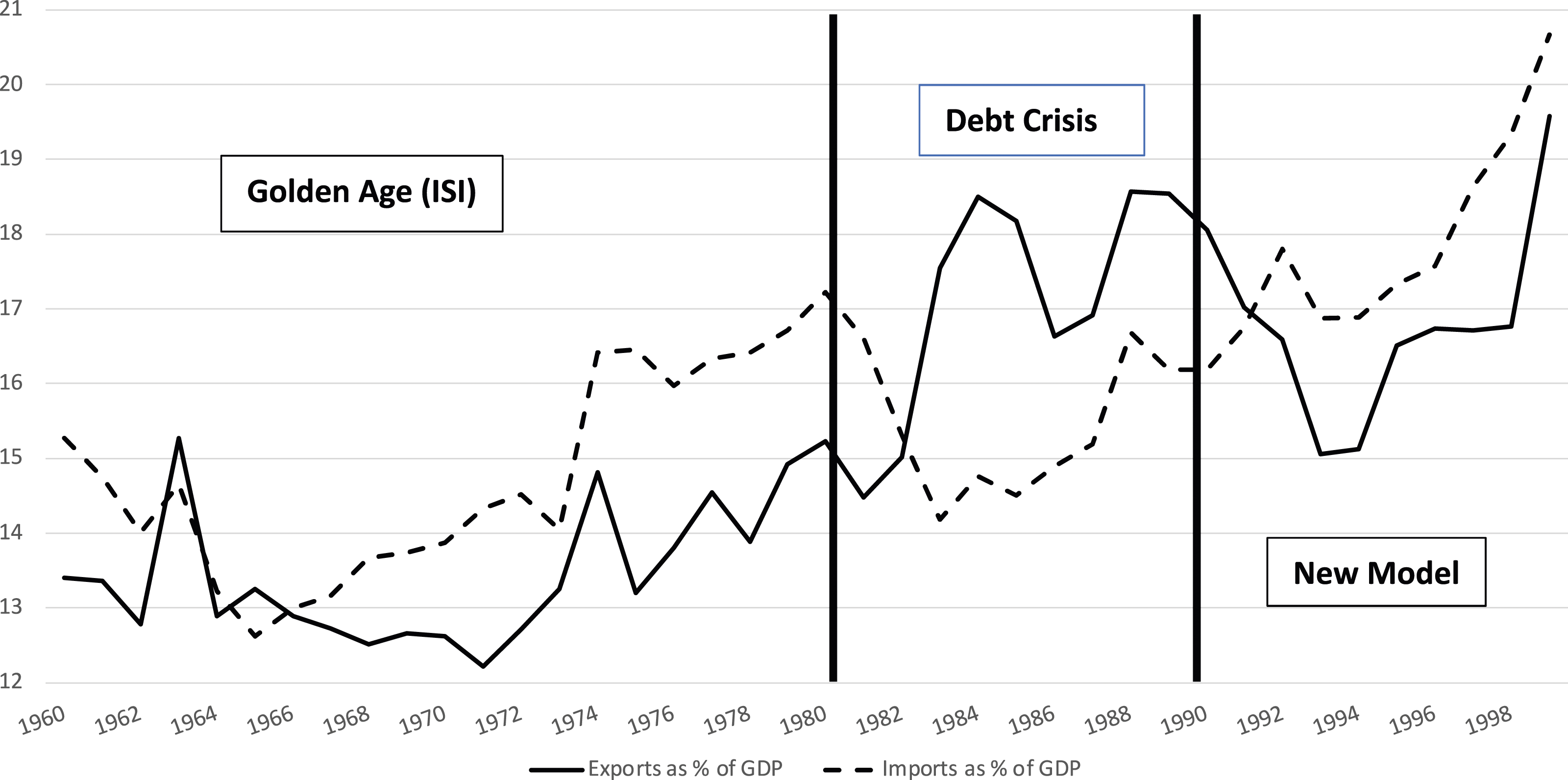

Figure 2 turns to the changing performance of international trade: exports and imports of goods and services as a share of GDP. Export ratios were generally low and exceeded by import ratios in the earlier period, although there was some increase in both after the first oil shock. In the 1980s, by contrast, exports rose sharply and exceeded imports, as regional governments attempted to meet debt service requirements by promoting exports and suppressing imports. Both ratios were inflated by the smaller denominator as GDP stagnated. In the 1990s, the traditional pattern of imports dominating exports returned, but exports themselves improved their performance substantially. Indeed, by the end of the decade, the export ratio had reached its highest level since the ISI period started, as a reflection of the new growth model. Latin American exports and imports as share of GDP, 1960-99 (%). Source: World Bank (online).

Another way of analyzing the change in consumption and exports in the two periods is to examine the sources of economic growth. Bértola and Ocampo (2012) provide decompositions for 1957-80, which show strong dominance of consumption over exports (5.3% vs 0.3%). A similar decomposition for the 1990s (ECLAC, online) points to the change in growth models in the 1990s as exports dominated consumption (6.8% vs 3.0%).

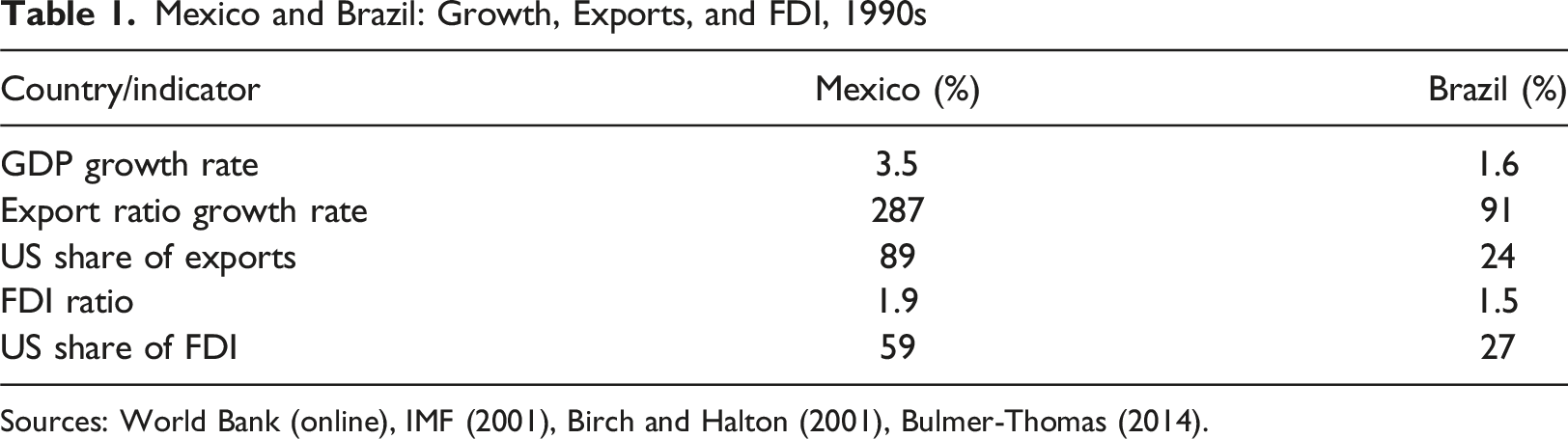

Analyzing the new growth model that emerged in Latin America in the 1990s requires drawing a major distinction between Mexico and Central America on the one hand and South America on the other. That is, there were two variants of the new model. The northern-tier countries became tied into US-based GVCs. Mexico’s role involved sophisticated industrial goods—such as autos, aircraft, and electronics—while Central America (and the Dominican Republic) were linked to traditional apparel and textile industries. In both cases, new institutional arrangements locked in these economic relationships. Mexico joined the United States and Canada in the North American Free Trade Area (NAFTA) in 1994, while Central America and the DR linked up with the United States in the Central American Free Trade Area (CAFTA-DR) 10 years later. More generally, the US market was critical for exports from Mexico (89% of total Mexican sales were in the United States in 2000) and from Central America (65%) (calculated from IMF, 2001).

South America had a much more diversified set of partners and few institutional or GVC links beyond the region. Brazil, the largest country in South America, was the iconic example. In 2000, only 24% of its exports went to the United States, while 27% went to Europe and 35% to non-oil developing countries including the region itself. A similar situation prevailed in the three other South American countries that joined Brazil to form the Southern Common Market (Mercosur) in 1991. Even Chile, which had stronger US relations than the Mercosur bloc, sent only 17% of its exports to that country with the rest divided among Europe, Asia, and the region. The northern-tier nations in South America (Colombia and Venezuela) were located in between: 51% of their exports were sold in the US market in both cases. As these data suggest, there are important differences within the subregions, but they are beyond the scope of this article. 10 A related difference between the two subregions involved the sectoral composition of their exports, partly because of the demand characteristics of their trade partners. While Mexico and Central America were strong industrial exporters to the US market, South America relied heavily on commodities sent to Europe and Asia.

Foreign capital flows were also an important part of the new growth model since Latin America lacked its own sources of finance and had to depend on international markets. Foreign capital largely dried up during the debt crisis, except for loans made as part of debt restructuring, but by the early 1990s FDI and bond issues began to supplement foreign exchange earned through exports. A major attraction was the privatization of many SOEs that were purchased by foreign investors. Total net FDI inflows during the decade were US$424 billion (calculated from World Bank, online). Early in the decade US firms represented nearly three quarters of inflows. The allocation of US investment was divided about equally between Mexico and Brazil. Later in the decade, European investment exceeded that of the United States in Southern Cone countries, with most of it going to Brazil, but US firms remained the largest source of FDI in Mexico and Central America (Birch and Halton, 2001: 16).

Bond issues were the second largest type of capital inflow to Latin America in the 1990s, as the financialization process reverted to instruments used in the 19th and early 20th centuries. Investors were attracted back to the region by high returns and the economic reform agenda; regional borrowers issued nearly US$280 billion by the end of the decade, as bonds replaced bank loans as the main source of capital for governments. In 1999, for example, 76% of regional issues were sovereigns and only 24% were corporates. The bonds were priced as spreads over a floating base rate, again passing risk onto borrowers (Bustillo and Velloso, 2000).

The result of the new export-led growth model, supplemented by the resumption of capital flows, was renewed economic growth in the 1990s. But, as we have seen, that growth was lower than in the ISI period and punctured by two major financial crises. Moreover, the low growth following the Asian crisis continued into the early 2000s. Neither the Mexican-Central American model, based on industrial exports, nor the South American one, based on commodities, was able to deliver the sustained growth that was hoped for, so they clearly could not underwrite a strengthening/upgrading of regional production systems. The reasons varied in the two cases.

Mexico (and Central America to a lesser extent) appeared to be major export successes. Export volume in Mexico increased by 287% between 1990 and 2000, while that of the four main Central American countries rose by 161% (Bulmer-Thomas, 2014: 408). Part of the Mexican increase was due to the NAFTA agreement. Mexico’s share of the US import market rose from 7% when NAFTA became operational in 1994 to 11% at the end of the decade, while its share of US FDI increased from 11% to 38% (Stallings, 2023). A key problem for Mexico, however, was the lack of value added in its exports. It mainly assembled imported inputs, which limited the impact on the rest of the economy due to the absence of backward and forward linkages. In addition, the sophisticated plants set up through North American integration were enclaves whose benefits were not spread to other sectors and regions of the country (Blecker, 2016).

The situation in South America differed. First, export growth was lower than in Mexico and even Central America; export volume in the seven major South American economies grew only 91% in the 1990s (Bulmer-Thomas, 2014: 408). Second, the export basket differed across the two subregions. European and Asian countries that bought most of South America’s exports were interested in their natural resources, so the new export-led model provided few incentives to diversify economies and upgrade skills and technology. Third, the new regional integration scheme (Mercosur) did not offer the same support that North American integration did. Some industrial products were sold among Mercosur members, but quality problems were serious since competition was limited by the group’s common external tariff.

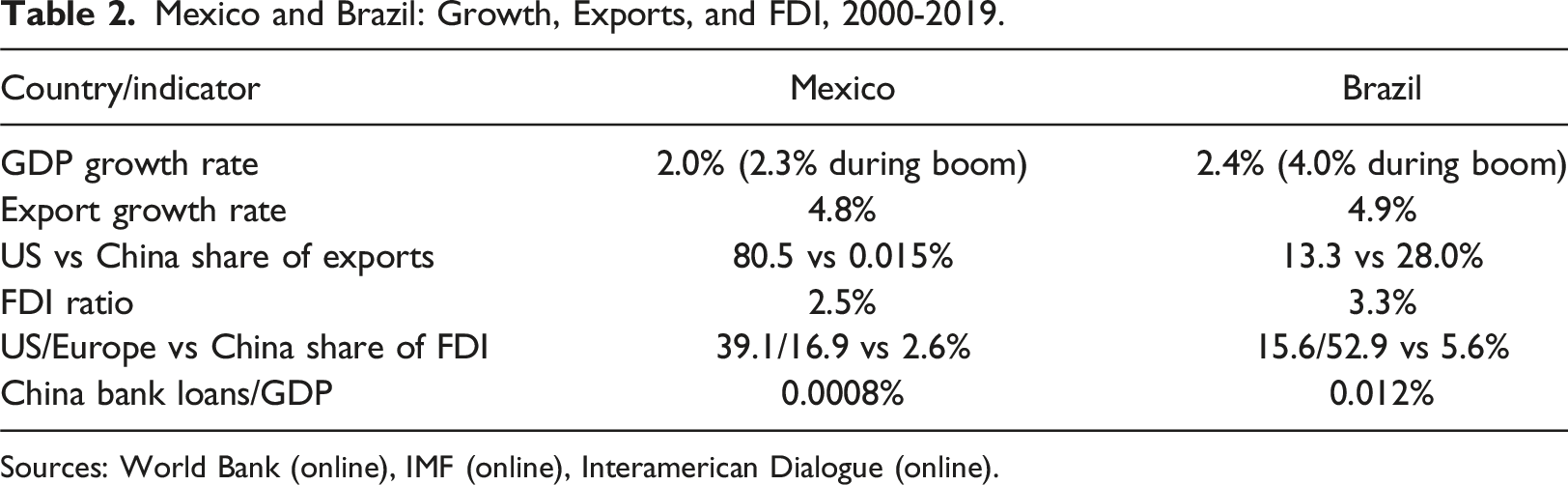

Mexico and Brazil: Growth, Exports, and FDI, 1990s

In general, the 1990s—which were the final years of nearly exclusive western hegemony in Latin America—proved disappointing, as neither version of the new model was able to sustain robust economic expansion. The turn toward exports as the main growth driver meant that international markets were crucial, and they were not very dynamic with several international crises breaking an initial positive trajectory. Mexico was a partial exception, as indicated previously, but its relatively high growth was disrupted by its own international financial crisis in 1994-95. At the same time, Latin America’s domestic economies lost steam as governments sought to tame deficits and inflation to attract the foreign investment on which they were increasingly reliant. Thus, Latin America’s insertion into international markets continued to play a key role in their performance, but other aspects of the dependency relationship shifted from an emphasis on leverage, prominent during the previous period, to linkage mechanisms. For example, US-trained economists assumed important roles in their countries, and they sought guidance from international financial institutions in implementing the new model; consequently, the use of leverage was less often needed.

An export-led growth model with increased Chinese influence (2000s)

The growth model in Latin America in the new century saw both continuity and change with respect to the 1990s. The export-led model itself continued, but it began to operate within a new international context. China entered the region in a major way around the year 2000 in response to its need for minerals and agricultural goods and expanded markets for its industrial products. 11 The result was new opportunities and challenges for Latin America in both trade and finance. Between 2000 and 2019 (the last “normal” year before the pandemic), trade between Latin America and China increased more than 20-fold, with China replacing the United States as the largest export market for five South American countries and becoming a major source of finance for the subregion. The impact of the new relationship showed up in a particularly dramatic way during the so-called China Boom in 2004-13. Latin America’s growth accelerated, employment increased, and the poverty rate fell. After 2013, however, the old stop-go pattern recurred (Stallings, 2020).

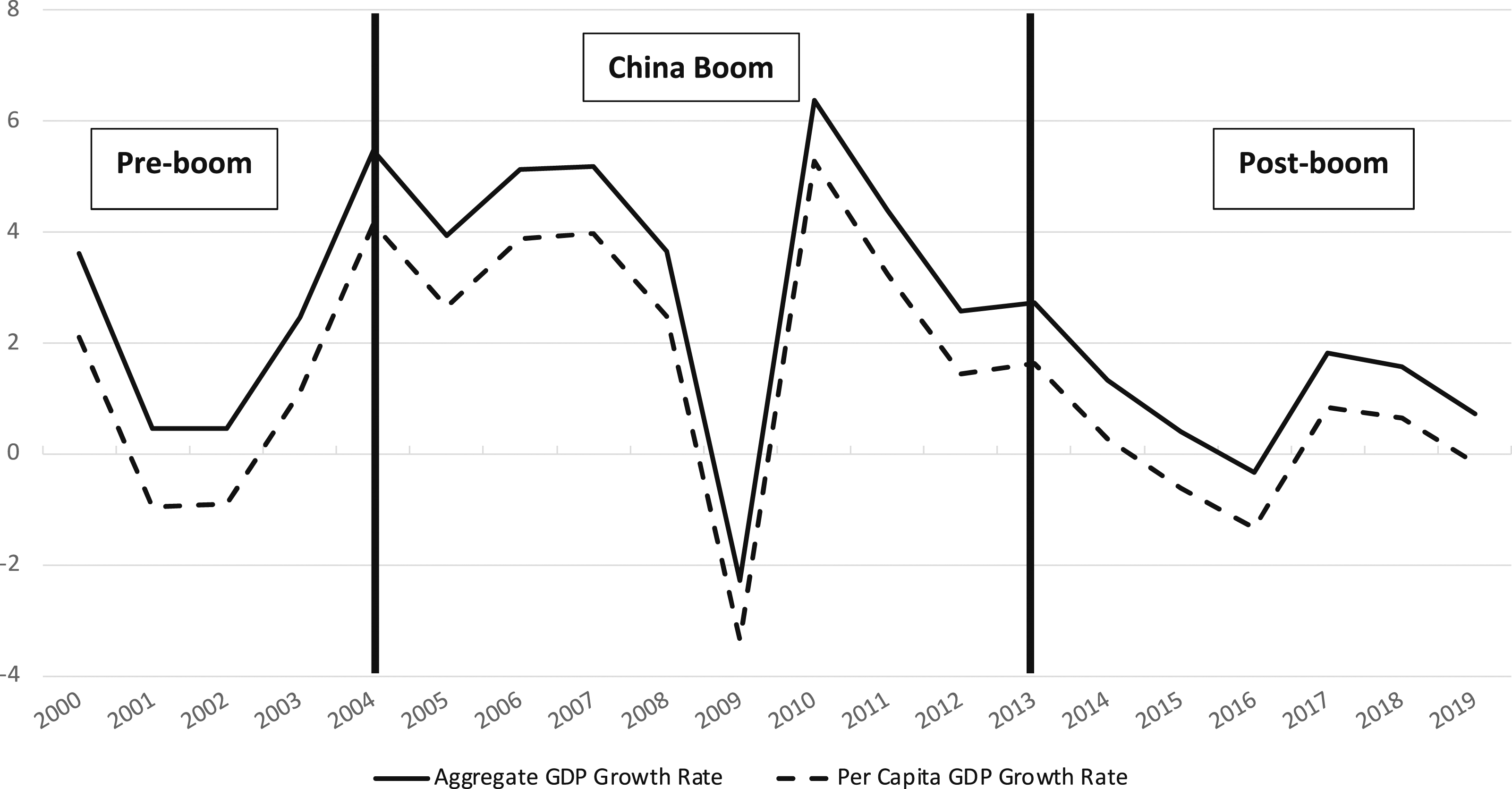

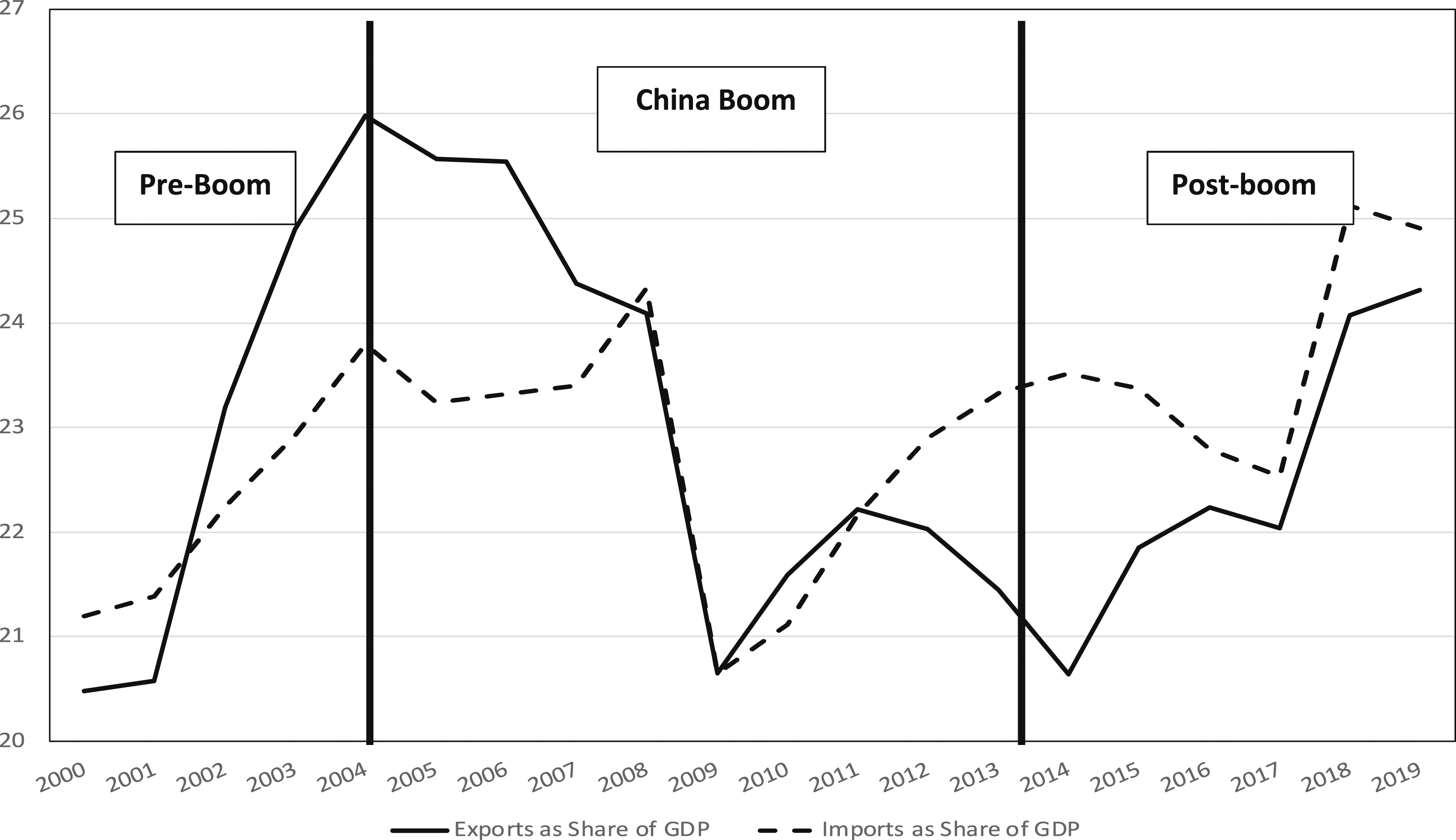

Figures 3 and 4 extend the data from the previous section. Figure 3 shows growth rates of Latin America’s aggregate and per capita GDP between 2000 and 2019. The high growth years were in 2004-13, as the region’s exports boomed in response to Chinese demand, which also elevated export prices. While substantially better than the 1990s, the 21st century growth record was inferior to that of the postwar Golden Age. The 2000-19 period was undermined by a V-shaped crash in 2009, reflecting the global financial crisis. On the positive side, it has been suggested that Latin America’s trade relations with China kept the region from suffering another lost decade (Myers and Gallagher, 2020). Latin American GDP and GDP Per Capita Growth Rates, 2000-19 (%). Source: World Bank (online). Latin American exports and imports as share of GDP, 2000-19 (%). Source: World Bank (online).

Figure 4 demonstrates the substantial quantitative boost that Latin America’s export-led model got from the region’s relationship with China. The export ratio reached a peak of 26.4% in 2004, well above anything seen since the postwar era began. It remained above 24% till the 2009 crash and then rose again in an uneven way until the pandemic struck. Moreover, in the pre-2009 period, the export ratio exceeded that of imports, meaning that the net macroeconomic stimulus to GDP growth from external demand was positive in addition to the job creation and other positive spillovers from the production of the exports. We can again supplement Figure 4 with a decomposition of economic growth (ECLAC, online). It indicates that exports continued to dominate consumption, but by a smaller amount than in the 1990s (3.7% vs 2.6%).

As before, we divide the analysis into northern (Mexico-Central America) and southern (South America) countries, but winners and losers were reversed in the 2000s. Most of the new interactions between China and the region centered on South America’s commodity exporters. They had the minerals and agricultural goods that China needed to support its economy; the resulting export boom led to increased growth in those countries. South American nations also stepped up their imports from China, which were mainly industrial goods, but their external accounts tended to be relatively balanced. China signed FTAs with two of its most important partners in the subregion: Chile and Peru. It also made other attempts to institutionalize relationships through the Community of Latin American and Caribbean States (CELAC by its Spanish acronym), setting up the China-CELAC Forum that produced several action plans for increased cooperation. But this forum was a pale shadow compared to the FTAs that united Mexico and Central America with the United States.

While trade flourished between China and South America, Mexico and Central America were left behind. China’s own industrial products were similar to those of Mexico and Central America, so the latter did not benefit from the new export market as South America did. Since the northern countries increased their imports from China, the result was extremely large trade deficits; Mexico’s deficit with China in 2015 was US$55 billion or 4.7% of its GDP (IMF, 2016). Another problem was even more damaging—China began to displace Mexico in the US market. During the early years of the NAFTA agreement (1994-2000), Mexico’s share of US imports grew rapidly, but the pattern changed from 2000 until the beginning of the Trump government’s anti-China policies. In 2000, Mexico accounted for 11% of US imports, rising only to 13% in 2015. At the same time, China’s share rose from 8% to 22% as its subsidized industrial exports made it increasingly difficult for Mexico to compete in its major market (Stallings, 2023).

Chinese finance soon began to arrive in South America to back up trade relations through FDI in oil and mining and loans to finance transport infrastructure to get the products to market in China. Unlike US and European firms, which are private entities although they can call on their governments for limited support, most Chinese FDI is carried out by SOEs. This characteristic gives them a different set of priorities; most importantly, short-term profits are less important. In addition, they get financial and other kinds of assistance from their government. From 2005 to 2019, total FDI inflows from China were about US$150 billion (around 5% of FDI from all sources). As with trade, the distribution of Chinese FDI across countries was very uneven. Over half went to Brazil alone, followed by Peru and Argentina. Sectoral allocation has diversified somewhat in recent years, especially toward energy and some manufacturing projects (Dussel Peters, 2023).

A new kind of finance from China was loans from government-owned policy banks; after 2013, these loans were often put under the umbrella of the Belt and Road Initiative (BRI), China’s vast program to expand its global economic and political clout. 12 Between 2005 and 2019, gross loan volume totaled US$138 billion (Inter-American Dialogue, online), slightly less than FDI inflows. While the loans were again very concentrated by country, the recipients differed. Four borrowers represented 92% of all loans to the region between 2005 and 2019: Venezuela alone received 45%, followed by Brazil, Argentina, and Ecuador. With the partial exception of Brazil, the main recipients could not access international capital markets because of their high risk and anti-western policies; China became their lender of last resort. Most loans went to finance oil, gas, coal, mining, and renewable energy projects together with infrastructure (mainly transportation). For developing-country governments, loans are valuable because they usually provide resources that they themselves can control, similar to sovereign bonds issued in western markets. While Chinese officials insist their loans do not have macroeconomic conditions as western loans often do, they have commercial conditions such as requiring use of Chinese companies and Chinese equipment. Moreover, many loans are backed by borrowing countries’ commodities; oil-backed loans are especially common (Kaplan, 2021).

Mexico and Brazil: Growth, Exports, and FDI, 2000-2019.

China’s entry into Latin America has provided substantial benefits to a limited number of countries, although that number is expanding. For example, several Central America countries have switched diplomatic relations from Taiwan to China and been amply rewarded. Together, Chinese market access and finance helped to lift the region out of its slump at the end of the 1990s and early 2000s. In turn, the high growth rates led to lower unemployment and poverty during the boom years: unemployment fell from 10% to 7% of the labor force, while poverty fell from 43% to 29% of the population. After the boom ended, however, both began to rise again (Stallings, 2020). China’s increased role enabled countries in the region to diversify their political and economic linkages, which can provide some loosening of dependency relations. There is also evidence that China’s policy banks help combat some of the worst aspects of financialization through their “patient capital” approach (Kaplan, 2021). 13

Nonetheless, the impact has not been all positive, even for South America’s “winners.” South American governments worry about deindustrialization and the reprimarization of their economies, as the industries they struggled to create have been undermined by industrial imports from China (Cooney, 2021). The volatility of commodity prices, and thus of the economies themselves, is well known. In addition, Chinese investment projects have proved worse for the environment than foreign investment in general (Ray, 2017), and issues with the rights of workers and indigenous communities are more common (Sanborn and Chonn, 2017). On the Mexican side, as already indicated, the impact of China has been even more problematic. Mexican exports to China are miniscule, while their import volume is large and growing, and China has eroded Mexico’s share of the US market. Unlike its southern neighbors, Mexico has received little Chinese investment, so it continues to rely on the United States for finance as well as trade. Given the relatively slow growth of the US economy compared to China, this puts Mexico at a disadvantage despite the GVC stimulus for certain sectors.

Overall, the new international political economic environment in which the two versions of Latin America’s export-led model operated in the 21st century has had a mixed impact. Trade relations with China have been more problematic than those with the United States because of their sectoral composition. In the case of China, trade is mainly of the inter-industry type—involving commodity exports from Latin America in exchange for industrial goods from China. 14 The United States, by contrast, engages more in intra-industry trade with Latin America—both exporting and importing industrial goods. With respect to financial flows, China has more state-controlled money to invest and lend in Latin America than does the west, although FDI stocks remain strongly in US and European favor. Politically, the benefits of having more diversified international economic and political relations—and thus more options with respect to development policies—should not be minimized.

“Dependency with Chinese characteristics” is both similar to and different than its US counterpart. In both cases, the main mechanism is power over markets for Latin American trade and finance. Market access can be combined with economic leverage if the hegemon or aspiring hegemon feels more pressure is required to satisfy its needs. In general, however, both US and Chinese market power in the 21st century has been supplemented by linkage rather than leverage. China’s geographical location and newcomer status in the region mean that economic and particularly political leverage are not very feasible, so it has sought to construct linkages with governments and private actors in the region through high-level visits, media, scholarships, and other exchanges. Western countries can rely on long historical relationships in education, work, and living experiences. But the aim on both sides is the same—to persuade Latin American actors of the advantages in working with one side or the other. Likewise, in both cases, the needs of hegemons dominate those of peripheral countries.

Conclusions

In this article, I analyze growth models in postwar Latin America. While I argue that the growth model literature is useful in providing a framework for comparative analysis and a starting point for studying relationships between comparative and international political economy, I also point to problems from the viewpoint of peripheral countries: the emphasis on the industrial world and the relative lack of attention to international constraints despite some movement in that direction. With a focus on the second problem, I propose the inclusion of literature on hegemony and dependency to better understand the relationships and impediments to growth in peripheral countries, especially Latin America. Of course, external constraints cannot completely explain Latin America’s failure to dynamize its economies. What is missing—for lack of space and the degree of complexity when working with some 30 countries—is the incorporation of domestic political relationships. A country case or small-N study would be more amenable to their inclusion, which is clearly crucial for a full analysis. (e.g., Sierra, 2022; Wise, 2020).

I argue that the region has had two growth models in the 70 years since World War II. The first was a consumption-led model, characterized by import-substitution industrialization and some trade and financial relations with the United States and Europe. That model prevailed from around 1950 to 1973, when the first OPEC oil crisis put substantial balance-of-payments pressure on the majority of Latin American countries as oil importers. The consumption-based model was extended, however, by borrowing on international capital markets until it collapsed in the 1980s debt crisis. The second was an export-led model after 1990. The latter period was divided into 10 years of trade and finance with the west and 20 years of increasing Chinese presence. Growth patterns showed the most positive period was under the consumption-led model. While the worst years were the debt crisis of the 1980s, the 1990s can be characterized as mediocre and highly volatile. High growth rates did not return until China’s arrival after 2000, but even the China boom did not match the postwar Golden Age; moreover, growth fell off again after the boom ended, and poverty and unemployment rose.

Latin America has always been a very heterogeneous region, but heterogeneity became central in the three decades between 1990 and 2019 with pendular swings between a situation favoring the northern half of the region (Mexico and Central America) in the 1990s and another favoring the southern half (South America) in the 2000s. The differences reflected two variants of Latin America’s export-led model—industrial exports in the north and commodities in the south. Moreover, the two subregions were tied into the international political economy in different ways through relations with the United States and China.

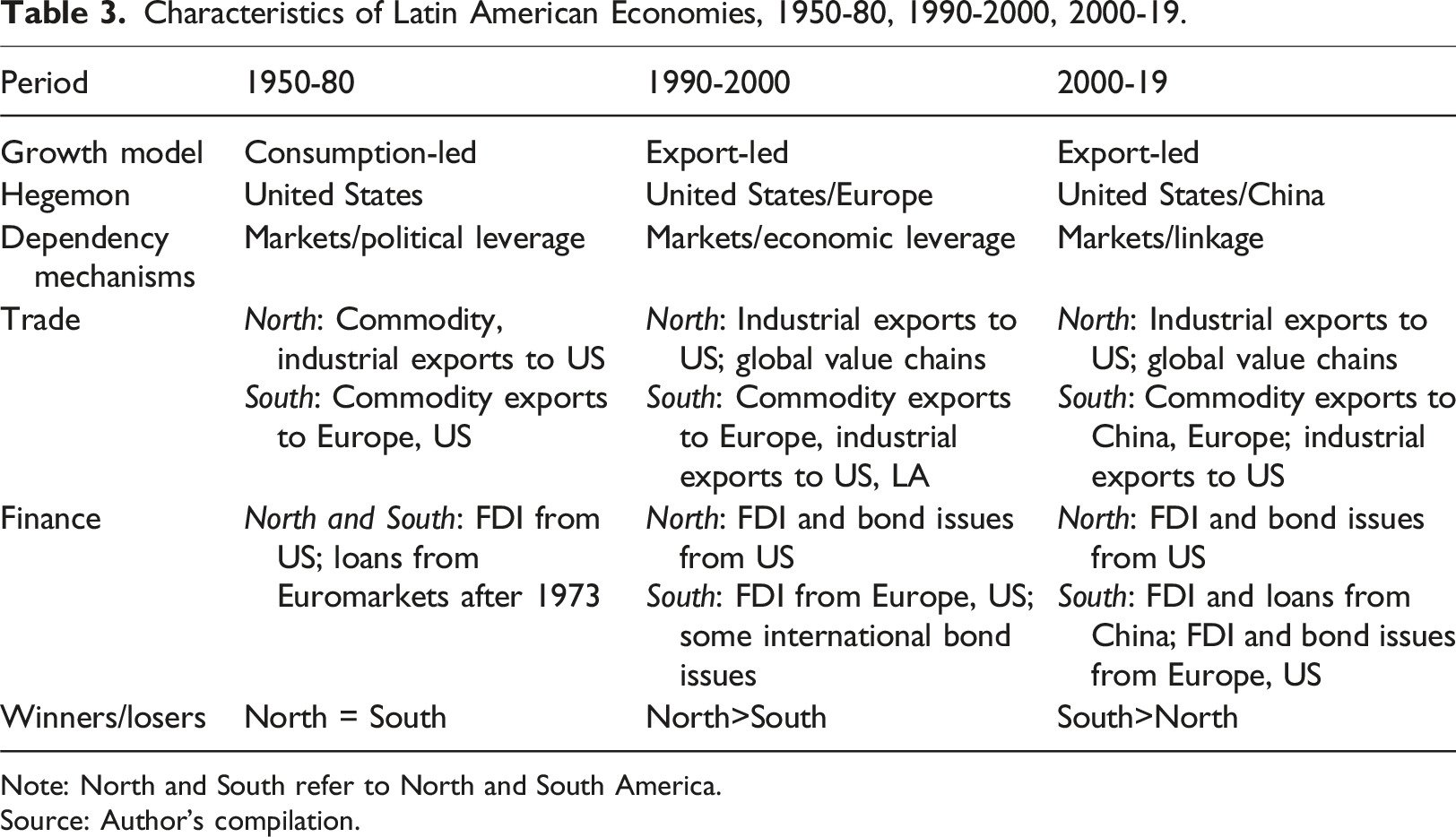

Characteristics of Latin American Economies, 1950-80, 1990-2000, 2000-19.

Note: North and South refer to North and South America.

Source: Author’s compilation.

How does a study of Latin America help to understand growth models in peripheral capitalist countries, and how does the GM literature help to understand Latin America? The main argument is that the international political economic context limits the ability of peripheral countries to devise growth models to achieve high-income status and more sophisticated production of goods and services. The nature of the limits varies with the needs and characteristics of hegemons or contenders, which are reflected in trade and financial patterns. At the same time, dependency relationships have shifted. While control over markets for trade and finance remains the principal dependency mechanism, political and economic leverage were complements early on, while linkage has overtaken the use of leverage more recently. Of course, characteristics of individual peripheral countries themselves—such as geography, size, infrastructure, and skill level—are also important for determining the nature of relationships, but they are beyond the scope of this article.

In the 1950-80 period, the United States and Europe were successful enough through consumption-led growth and trade amongst themselves that they did not need peripheral countries to any significant extent. Nonetheless, the United States did intervene in the region on occasion to assure countries remained on a capitalist path. Latin American economies were able to follow consumption-led growth models and take advantage of advanced-country dynamism for limited export markets and capital flows. They appeared to be very successful with impressive achievements in industrial development in the largest countries, accompanied by relatively high wages and thus lower inequality, but the model was unsustainable as the debt crisis demonstrated.

In the 1990s, a new export-led model emerged in Latin America, but it had differing variants in northern and southern parts of the hemisphere. An important explanation was new needs of the existing hegemon (United States) and the rising one (China). US firms needed to increase their efficiency in response to growing competition from Europe and Asia, so they incorporated Mexico into their value chains to lower their costs through cheaper labor. The new arrangements appeared beneficial for both sides. Sophisticated new production facilities were established in Mexico, and these facilities resulted in more competitive US firms. The problem for Mexico was that the process led to enclaves and lack of development for the country as a whole, since backward and forward linkages were limited. In addition, China’s growing presence after the turn of the century began to undermine Mexico’s privileged position in the US market.

South American countries tried to develop a more independent export-led model in the 1990s (with some help from Europe), but they had limited success. It was only when China entered the region in a major way after 2000 that growth in Brazil and other South America countries began to accelerate through exports to China and finance from that country. China entered South America for different reasons than the United States went to Mexico. China’s firms were already highly efficient but needed minerals and agricultural resources to support production at home and feed the population together with new markets for Chinese manufactured goods. The downside for Brazil, and South America more broadly, was a return to reliance on volatile commodity exports and “premature deindustrialization” as Rodrik (2016) had warned. As in Mexico, enclaves were introduced in South America, where those producing commodities benefited while those in declining industries paid the cost.

In summary, the literature on hegemony and dependency should complement the growth model approach when it is extended to peripheral countries. One of the main differences between Europe and Latin America—or between the industrial and developing worlds—is the latter’s greater reliance on international trade and finance to keep domestic economies functioning, especially under export-led growth. A hegemon’s control over access to these markets is the fundamental mechanism of dependency. Nonetheless, when peripheral economies make attempts to strengthen their economies in ways that hegemonic powers perceive as threatening, other mechanisms are available. They include political or economic leverage, which the United States used in earlier periods, but today both the United States and China are more likely to utilize linkage relationships to persuade peripheral governments and economic elites to follow their preferred policies. The US–China rivalry has become very intense, and Latin American countries may be able to take advantage in pursuit of development objectives.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.