Abstract

Recent years have seen a resurgent debate on economic planning in the age of digitalization and climate crisis and an extremely dynamic research community has formed around the theme of planning. Although the notion that “planning is already endemic in capitalism” has originally sparked the debate, the literature has mostly focused on theory and models of postcapitalist economic planning, not on how planning in capitalism actually works. Considering the financial system as one of the ways capitalism “plans,” this paper will expand on a rather dispersed series of observations by different commentators that “finance is a form of planning,” that central banks share similarities with “central planners” and that horizontal ownership across markets turns index funds into universal owners with the capacity to steer economic development. I will first argue that financialization has strongly influenced how contemporary economic planning works. Against this background, the text will then elaborate on how finance’s capacity for economic coordination makes it a potential tool for transformation towards increasing social and democratic control over the economy. In doing so, this paper connects the new debate on economic planning to the academic literature on financialization and the democratization of finance.

Economic planning: A new field of research

The economic social sciences have for a while now deconstructed the binary of free market capitalism versus centrally planned socialism, which is so central to the “narrow window of the neoliberal imagination” (Mitchell 1999). Markets are much older than capitalism (Abu-Lughod 1989; Pomeranz 2000; Arrighi 2007; Graeber 2011) and are in principle compatible with social ownership of the means of production (Bockman 2011; Bockman et al., 2016). The particular form markets take under capitalism is not particularly “free,” with leading companies in the world economy having historically relied on state power to prevent “free competition” in order to increase profits (Braudel 1977; Wallerstein 2004). Women, ethnic and sexual minorities and much of the formerly colonized world have historically been excluded from equal participation in markets (Robinson 2000; Federici 2004; Virdee 2019), which is related to the fact that the majority of care work, non-human nature, racialized dispossession and political goods are treated as free but unrecognized gifts for market economies (Fraser 2013, 2014).

More recently, a resurgent debate on economic planning in the age of digitalization has tackled the other side of the “market-planning-binary” and an extremely dynamic research community has formed around the theme of planning (e.g., Benanav 2022; Bensussan et al., 2022; Dapprich 2022; Fuchs 2020; Groos 2021; Grünberg 2023; Hahnel 2021; Jones 2020; Laibman 2022; Laibman and Campbell 2022; Morozov 2019; Sorg 2022a, 2022b; Vettese and Pendergrass 2022). Although it is mostly equated with Gosplan central planning, economic planning can be central or decentral, authoritarian or democratic, it can complement or replace markets and particular forms of it are already endemic under capitalism (Jameson 2009, 420ff; Bratton 2016, 327ff; Phillips and Rozworksi, 2019; Jones 2020). Based on these premises, the new planning literature has explored the possibility of postcapitalist and democratic varieties of planning, partially building on slightly older models of democratic negotiation (Devine 1988, 2002), cyber-socialism (Cockshott and Cottrell 1993), participatory economics (Albert and Hahnel 1991), and multilevel democratic iterative coordination (Laibman 2002). There has been a particular focus on the possibility of digital technologies such as artificial intelligence, big data, or feedback infrastructures to solve the economic calculation problem (Groos, 2021; Morozov, 2019; Saros, 2014; Sorg, 2022a). More recently, however, authors have also advocated for planning in order to avoid ecological breakdown (Vettese and Pendergrass 2022; Sorg, 2022a; Krahé 2022; Planning for Entropy 2022).

With the literature largely focusing on theory and models of postcapitalist economic planning, little work has been done to investigate how planning actually works in capitalism. Indeed, when work refers to empirical reality at all it is mostly to discuss the history of varieties of really existing state socialism or post-war Keynesian macroeconomic management (e.g., Devine 1988). In addition, the literature’s focus on desirable models and end results does not develop trajectories of how to actually move towards economies featuring elements of democratic planning. This paper will argue that finance constitutes a particularly interesting case for both of these gaps.

Considering the financial system as one of the ways capitalism “plans,” this paper will expand on a rather dispersed series of observations by different commentators that “finance is a form of planning” (Mason 2016), that central banks share similarities with “central planners” (Braun 2018, 2021a, 2022a; Phillips and Rozworksi, 2019; Bastani 2019) and that horizontal ownership across markets turns index funds into universal owners with the capacity to steer economic development (Mason 2016; Phillips and Rozworksi, 2019; Bastani 2019; Braun 2021b, 2022b). I will argue that financialization has strongly influenced how contemporary economic planning works, but also that finance’s capacity for economic coordination makes it an important tool for transformation. In doing so, this paper connects the new debate on economic planning to the academic literature on financialization (Van der Zwan 2014; Auvray et al., 2021) and the democratization of finance (Block 2019a).

Section two of this paper will develop the conceptual framework to theorize economic planning in capitalism. I will argue that planning in capitalism has to be understood as an ensemble of public planning for overall accumulation, atomistic private planning for profit and market forces. Section three will introduce the general role of finance for planning and discuss how financialization has transformed planning in recent decades. This includes the role of the rise of shareholder value and asset managers for private planning and the importance of central banks and private credit for public planning. Against this background, section four will then analyze how a democratization of finance could contribute to a democratization of public and private planning, and also to tame or abolish market forces. The final section will connect this analysis to trajectories of transformation via social and democratic control over finance.

Theorizing capitalist planning and the role of finance within it

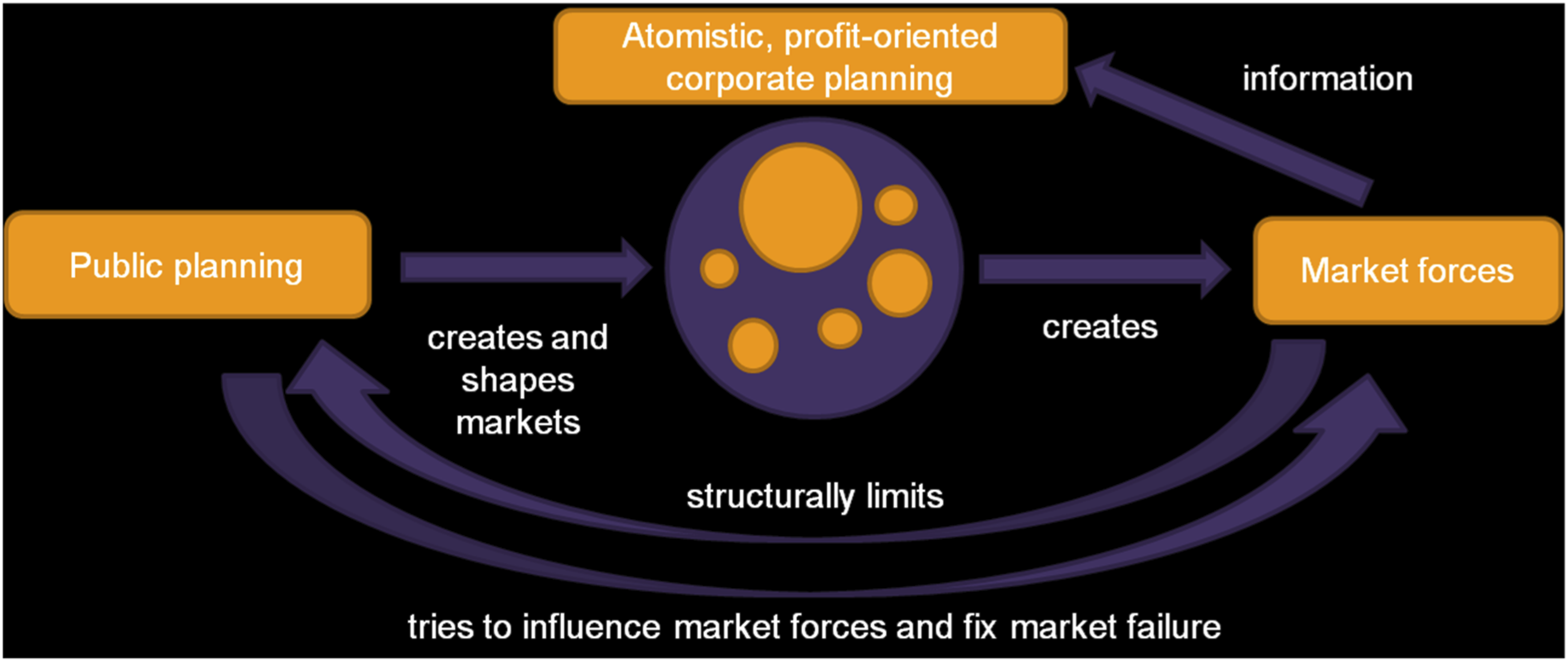

Capitalism as a social system is a particular combination of planning and market. It combines direct ex ante allocation of resources within companies with the ex post valuation of commodities on a market (Mandel 1986; Bensussan et al., 2022). However, the particular combination of the two varies according to space and time. Indeed, Mandel (1986) identified the “growing socialization of labour” as the pivotal capitalist development since the Industrial Revolution, precipitating a “dramatic extension of the planned organization of work,” with transnational corporations planning the allocation of labor, resources, and machines across vast supply chains. Mandel was neither the only renowned economist to identify capitalism as “decentralized planning by many separate persons” (Hayek 1945) mediated by markets, nor the only one to observe that the realm of planning has historically expanded in capitalism (e.g., Coase 1937; Chandler 1977; Simon 1991).

While planning has since largely disappeared from political economy (Bensussan et al., 2022) and management and organization studies (Cummings and Daellenbach 2009), 1 a newly (re-)emerging literature on economic planning seems to have rediscovered Mandel’s observation of an increasingly planned organization of work in the economic practices of corporations such as Walmart and Amazon, who coordinate transnational supply chains across the globe without internal price mechanisms (e.g., Jameson 2009, 420ff.; Bratton 2016, 327ff). The fact that these tremendously large companies coordinate their inner logistics without the internal use of price signals indicates to them that large-scale ex ante allocation, at least in principle, seems to be feasible and already exists within capitalism (Phillips and Rozworski 2019).

However, such a focus on the distribution of goods and services based on existing capacities leaves out a second important dimension of planning: changes in the productive capacity, that is, investment (Devine 1988, 2002). In capitalism, such investment is conducted atomistically by companies in competition with and ignorance of each other. Company ex ante allocation is valuated ex post on markets, meaning producers find out whether there has been demand for their commodities or not (and how much). Following this new information, producers estimate their internal capacity and future market developments and decide over investment on the basis of expected future profitability. It is this atomistic decision-making process over productive capacities that Adam Smith affirmatively termed the “invisible hand” and Marx dismissively called the “anarchy of production” (Devine 2002, 75). Such atomistic planning creates collective uncertainty for economic actors, who never reliably know about the plans and actions of other actors (Dobb 1960; Devine 1988).

This blind directionality and its potentially destructive impact on companies, communities and non-human nature leads us to the second form of planning in capitalism, that is, that deliberate practices of public authorities to “shape markets” (Mazzucato 2013) and alleviate their destructive tendencies. This distinction between corporate and public planning reflects the fact that economic and political power might be interrelated in capitalism, but they are also formally institutionally separate (Wood 1995, 19ff; Fraser 2014). This institutional separation materializes in the state and the market, each with its own modus operandi and thus a distinct logic of planning. While corporate planning continuously strives for private profits, as elaborated above, public planning creates, shapes, and protects the arenas within which corporate planning is possible in the first place. States create and govern money, provide legal frameworks for markets, protect local business from foreign competition, repress subaltern rebellions, and generally make sure markets do not destroy themselves (Fraser 2014). They also conduct a whole range of public investments that simply are not, or not yet, profitable for individual businesses or that have positive externalities, such as foundational research or the construction of electricity grids and railways (Mazzucato 2013).

Along these lines, public planning needs to be “relatively autonomous” from individual market actors in order to transcend their particular interests and reproduce the overall accumulation of capital (Offe 1975; Wright 2010). If state institutions were captured by particular business interests, they cannot effectively protect the overall system from the self-destructive tendencies of markets. This tendency for autonomy is mediated by the state’s dependence on successful capital accumulation for its functioning. Public institutions can fund their expenditures (e.g., social welfare, industrial policy, and basic administration) by having public companies generate surpluses, taxing profits and wages or by borrowing (O’Connor 1973; Roos 2019, 57). However, all of these are contingent on economic stability and growth. This explains the structural power of business in capitalist society, that is, the capacity to collectively withhold investment and credit and thus unleash economic turmoil on a state (Lindblom 1977; Block 1987; Przeworski and Wallerstein 1988). Such a threat of a “capital strike” (i.e., no investment) or a “credit strike” (i.e., no credit) can precipitate a reversal of governmental policy even when more direct business efforts at lobbying fail (for capital strike: Block 1987, 8ff; for credit strike and capital flight: see Strange 1998; Roos 2019). So it is not only corporate planning that is heavily shaped by market forces, but also public planning.

So a proper theory of planning in capitalism needs to incorporate public planning for overall accumulation, corporate planning for individual profits, and their respective dependence on market forces. Figure 1 illustrates this process. Public planning creates and shapes the arenas for atomistic corporate planning, which in turn creates market forces that readjust the playing field for future public and corporate planning. Public planning can try to shape and steer market forces in the interest of territorial accumulation, but is ultimately constrained by them. Likewise corporate planning is a “constant struggle conducted by companies against the market’s impersonal and abstract forces” (Bensussan et al., 2022). Planning in a market economy.

Popular work in the current planning debate has hinted at the ways finance influences these processes via deliberate planning by central banks and private finance (Mason 2016; Phillips and Rozworski 2019, 100ff). In addition, research in the political economy of finance has similarly indicated that finance largely serves as a “social planner” of contemporary capitalism (Braun 2018, 2022a). Finance plays a pivotal role in the allocation of societal resources and is itself split into public planning for overall accumulation (e.g., via central banks, ministries of finance and sovereign wealth funds) and atomistic planning for individual profits (e.g., via private banks, investment funds, and asset managers). Joseph Schumpeter (1939, 109f) described private finance’s role for innovation and allocation as a kind of capitalist Gosplan, that is, as the market economy’s planning agency, shifting resources from one use to another (referenced also in Mason 2016). Although investment can also be financed by retained profits, financial streams nonetheless influence the social direction of production. Bank loans, debt securities, and shares determine which economic actors and which sectors receive a larger share of collective resources to expand or readjust production. This allocation of finance does not merely mirror past profits, but expected future profitability, thus requiring a deliberate and subjective planning process among financial actors (Mason 2016).

Again, financial markets need public agencies such as finance ministries and central banks to create them in the first place and to make sure they do not destroy themselves. Recent research in critical finance has argued that, and elaborated how, central banks play a particularly important role in coordinating markets (e.g., Gabor 2010; Monnet 2018; Braun 2018, 2022a; Kalaitzake 2018; Bazot et al., 2022). Deliberate action by central banks as a non-market institution uses the price of short-term liquidity to steer markets in a particular direction (Braun 2018). Benjamin Braun (2022a) has thus followed Karl Polanyi in arguing that central banks should be interpreted as pivotal institutions of non-market coordination, “without which the market would have destroyed its own children, the business enterprises of all kinds” (Polanyi 2001, 201). Indeed, Polanyi’s famous dictum that “laissez-faire was planned; planning was not” (Polanyi 2001, 147) implies that such planning (as non-market coordination to reduce the uncertainties and irrationalities created by markets) emerges spontaneously to protect the ‘self-regulating market’ from itself.

In a historical case study of ‘central bank planning’ Monnet, (2018) has powerfully shown the role of the French Central Bank in driving industrial indicative planning in the post-war period via investment credit. This challenges the narrative that central banks have only recently become powerful technocratic planners, and instead suggests that the transformation has been in tools and objectives, from industrial policy to fighting inflation. These transformations have been associated with the financialization of capitalism, which has greatly influenced both corporate and public planning, and to which I shall now turn.

The financialization of planning

Financialization is sometimes framed as a regime of accumulation, as shareholder value-oriented corporate governance or as the financialization of everyday life (Van der Zwan 2014), but for the purposes of this paper I will define the concept as an increasing role of finance for profit-making vis-à-vis trade and commodity production (see Krippner 2011, 27ff). Critical political economists have traced the origins of financialization to the crisis of profitability in leading sectors of the post-war economy since the late 1960s (Magdoff and Sweezy, 1987; Brenner 2002) and the crisis of US hegemony reflected by the Vietnam War and oil shocks (Arrighi 2007; Krippner 2011). The latter pressured the Nixon administration to abolish the Dollar gold standard and paved the way for a fiat currency regime. The former saw non-financial corporations find less and less profitable investment possibilities for expanded reproduction and thus increasingly hold assets in liquid form, which they used to capitalize their own financial divisions (Krippner 2011; Lapavitsas 2013). Henceforth more and more non-financial firms financed investment via internal funds instead of having to rely on the financial sector (Van Treeck 2009, 923ff; Palladino 2021; Braun 2022b). 2

With non-financial corporations increasingly being able to finance investment without the help of banks, the latter started to primarily lend to each other and to households (Lapavitsas 2011, 2013). Household demand for credit grew as real wages stagnated and neoliberal reforms slashed social welfare, thus establishing a regime of privatized Keynesianism (Crouch 2009). Banks financialized household assets (e.g., housing, pensions, and savings), securitized and re-sold them (Davis 2009, 116). This vast increase in financial transactions was made possible by financial deregulation and technological innovations, with statistics and credit scores replacing qualitative methods to assess borrowers. The quality of financial planning for profits has suffered from this transformation (Lapavitsas and Dos Santos 2008), with the loss of finance’s qualitative sensorium potentially mirroring the “tacit knowledge” problem pivotal to the planning debate.

These transformations have had a series of consequences for capitalist planning as outlined above. First, corporate planning has been dominated by the primacy of maximizing shareholder value (Boyer 2005). The intellectual foundation of shareholder value is the notion that shareholders are the only corporate stakeholder with a long-term interest in corporate performance, but that they are relatively dispersed and weak (Lazonick and O'Sullivan 2000; Braun 2022b). Managers are thus able to use their control over corporate planning for their own advantage. This rationale has justified shifting surpluses towards stock buybacks (in order to increase asset value) and dividends to realign corporate planning with the interest of shareholders, which has in turn depressed corporate investment (Auvray et al., 2021). Shareholder value has also legitimized the use of profit-related pay systems as incentives for managers. While this was intended to discipline them, it has not disempowered managers but actually enriched them and turned them into allies of shareholders (Boyer 2005). Nonetheless, the overall influence of shareholders has certainly grown, which brings us to the second consequence of financialization.

Second, the power of finance to influence corporate planning has increased. Shareholders had few options to control the ex ante allocation of post-war multinationals Mandel (1986) was observing. They were relatively dispersed and could only threaten to sell their (small) shares, but with the emergence of private equity firms specializing in buyouts of publicly traded companies, downward pressures on share prices started to constitute a serious threat for managers (Braun 2022b, 637ff). In addition, the rise of institutional investors such as pension funds has concentrated shareholders and thus amplified their voice in corporate governance (Braun 2022b, 639).

More recently, the emergence of large asset management companies has further increased the concentration and influence of shareholders (Elhauge 2015; Petry et al., 2021; Fichtner and Heemskerk 2020; Braun 2021b) and thus their capacity to influence corporate planning via capital allocation. The three biggest asset managers Vanguard, BlackRock, and State Street cast roughly 25% of the votes at the shareholder meetings of S&P 500 companies, a number Lucian Bebchuk and Scott Hirst argue might increase to 40% within two decades (Bebchuk and Hirst 2019). This immense concentration of assets thwarts the threat to exit as an option for asset managers, but instead they have gained a tremendous amount of control over corporate planning and investment (Braun 2022b).

Their level of market control is paralleled by relatively diversified portfolios, which in theory places them in the perfect position to act as a social planner and reduce the uncertainties created by atomistic corporate planning. However, since they are for-profit companies themselves, they primarily aim to maximize the assets they control, their fees being calculated as a percentage of asset value (Braun 2022b). Indeed, profit-oriented horizontal ownership means that asset managers are interested in the performance of complete sectors instead of individual firms. As a consequence, asset managers seem to discourage atomistic investment in order to avoid intra-industry competition (Azar et al., 2021; Auvray et al., 2021). Politics is pivotal because monetary policy has a huge impact on asset prices, while regulation against their domination constitutes a significant risk for asset managers (Braun 2022b). This brings us to the third and fourth consequences of financialization.

Third, financialization has seen the rise of central banks (and finance ministries) as social planners. States have not been passive bystanders to financialization but have actively contributed to it via the slashing of social welfare, financial deregulation, and a turn towards monetarist policies (Arrighi 2007; Krippner 2011). With financial deregulation precipitating financial volatility and instability, central banks have acted as lenders of last resort to avoid financial breakdown (Roos 2019), but they have also generally served as a pivotal institution of non-market coordination (Braun, 2022a). In the face of increasing numbers of debt crises, central banks and the IMF (as the international lender of last resort) have provided short-term liquidity tied to conditionalities, thus proactively intervening in public policies (Roos 2019, 64ff). In doing so they have ensured public planning frees up enough resources to maintain solvency (no matter the social cost) so that crises don't diffuse along dense inter-bank lending networks.

In the post-war period central banks have used tools such as credit controls to intervene in markets ex post as part of a coherent government policy (Monnet 2018). Since the 1980s central banks have become more independent and mostly reduced their repertoire of instruments to targeting price stability (as the primary concern of financial wealth owners) via the short-term interest rate in interbank money markets (Braun 2018). The line of reasoning for central bank independence was that central banks have to be independent enough to make unpopular decisions that elected officials would not be able to make due to electoral pressures (Gilardi 2007; McNamara 2011; Kim 2022). In addition, transformations in monetary policy due to elections are feared to create uncertainty for market actors. Central bank independence has therefore placed some of the tools and tasks of public planning outside of democratic control and into the responsibility of technocratic institutions. While the possibility of efficient fiscal planning was rejected based on the assumption that “rational” market actors will predict (and thus counteract) public intervention, the same assumption has provided the foundation to justify central bank planning via expectation management (“forward guidance”) (Braun 2018). In addition, the rise of quantitative easing has signaled the return to more interventionist central bank planning via the strategic purchase of financial assets.

Fourth, the growing structural power of, and public demand for, finance have increased its capacity to limit and generally influence public planning. Financial deregulation and the dismantling of capital controls have vastly increased the amount of cross-border financial flows, while technological innovations have facilitated and accelerated them. Growing capital mobility has in turn strengthened and transnationalized the above-elaborated threat of credit strikes (Strange 1998; Roos 2019). Business-friendly policies may be rewarded with access to cheaper credit, while business-unfriendly policies may be disciplined via the relocation of capital to other jurisdictions.

At the same time, states have become increasingly dependent on the private provision of credit to fund public planning (Streeck 2015; Roos 2019, 64ff). When secular stagnation and international competition had eroded the fiscal foundation of post-war Keynesianism and Developmentalism, subsequent waves of privatization reduced the capacity for direct public planning via state-owned companies. With taxation shrinking due to lower profits and downward pressure on corporate taxes in the context of financial globalization, public planning has become increasingly financed by credit. While public debt has managed to “delay” widespread crises of legitimacy (Streeck 2017), it has also further strengthened the power of finance to influence and limit public planning. Finance prioritizes (and thus rewards) public policies that keep inflation low and maintain debt servicing at all costs (Roos 2019), which goes hand in hand with the increasing relevance and independence of central banks. In such a context public planning becomes a technocratic exercise hardly subjected to democratic control.

Two cases illustrate the combination of growing structural power of finance and increasing dependency on private credit. When the French Mitterrand administration embarked on a path of wide-ranging nationalization and industrial policy in 1981, tremendous capital flight and speculation against the franc put enormous pressure on the socialist-communist coalition (Fourcade-Gourinchas and Babb 2002, 565ff). While these policies would not have constituted an uncommon form of planning a decade earlier, the international economic context had shifted. Not wanting to increase tariffs and capital controls and risk isolation, the coalition split and the new administration instead pursued a program of privatization and austerity. In 2015, Greece experienced a similar constellation when the newly elected, Syriza-led coalition opted to end austerity and debt servicing (Roos 2019, 225ff). Despite a successful referendum to reject the bailout conditions proposed by the European Commision, European Central Bank and International Monetary Fund, the power to withhold affordable short-term credit and thus unleash turmoil convinced the administration Prime Minister Alexis Tsipras to accept the third memorandum of understanding and to maintain austerity and debt servicing.

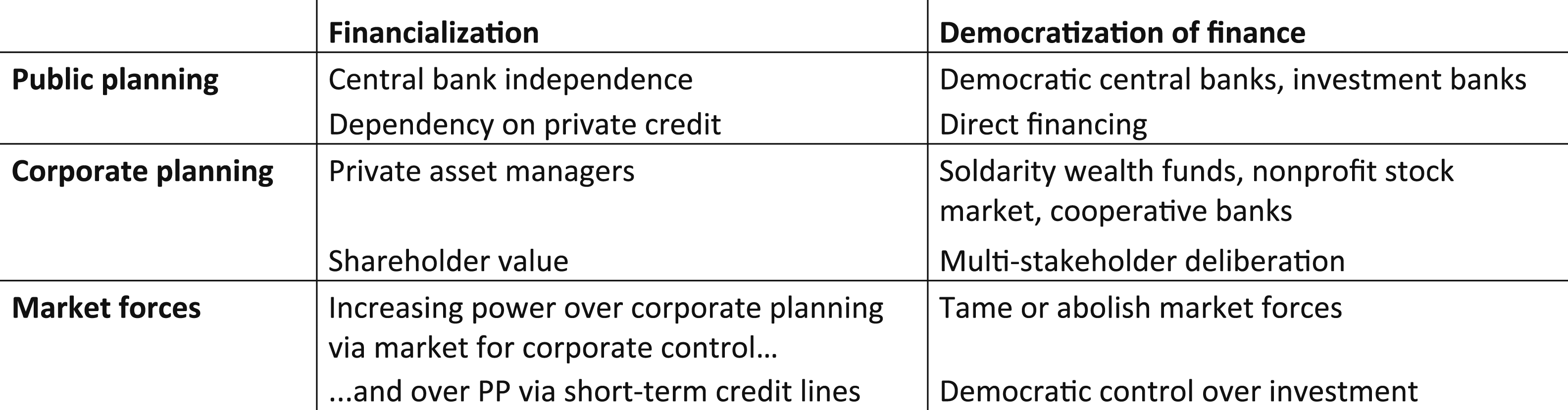

To reiterate: The rise of shareholder value corporate governance and of asset managers as horizontal private planners has transformed corporate planning, while public planning has been heavily influenced by central bank independence and public dependence on private credit. Research on financialization has empirically documented these transformations and their questionable results. The sole concentration on shareholder value has maximized manager and shareholder income, but excluded any concerns from corporate planning, including the long-term sustainability of a company, environmental issues, and the interests of other stakeholders. Related to this, shareholder value has (co-)precipitated escalating income and wealth inequality, with workers’ income share declining and CEO and shareholder income tremendously increasing over the last decades (Lin and Tomaskovic-Devey 2013).

In addition, shareholder value has depressed overall growth and investment, increased unemployment and entailed financial instability (Stockhammer 2008). Such mediocre economic performance contributed to increasing public debt levels (via bailouts, social benefits, and lower tax income) and related to this to the increasing dependence of public planning on the private provision of credit. Such dependence has closed channels for democratic participation and deliberation to shape public planning, which has to instead center on low inflation and debt servicing. Central bank independence has itself further depoliticized public planning, as technocratic planners have become shielded from democratic accountability.

In sum, financialization has thus reduced the democratic accountability of public planning, centered corporate planning on the short-term interests of managers and shareholders, depressed economic performance, and entailed economic volatility. The question is whether and how planning can be conducted in a more democratic form and directed at social and ecological needs instead of solely at shareholder value, but also whether financial planning apparatuses and their coordinative power can be appropriated for such a transformation. Any answer to these questions needs to build on a subset of the financialization literature that has suggested more social and sustainable alternatives towards a “democratization of finance” (Block 2014, 2019a; Hockett 2019). The task of such a “democratic finance” would be to provide access to cheap credit to poor and working-class households, but also to steer and fund public investment. The latter provides a link between financialization and democratic planning, as it suggests socially controlled finance as a tool for deliberate coordination and planning. As argued above, Part of the planning literature focuses on “static planning” (Benanav 2022, 196ff) as an alternative to “market exchange” (Devine 2002, 76), that is the question of which goods and services to produce and how to allocate them based on existing productive capacities. The more important question, however, is how to deliberately decide over the transformation of existing capacities, that is, over investment (Devine 2002): which sectors should shrink, disappear, grow, or emerge? It is precisely here that socially controlled finance as one of the sources of investment can become a tool for democratic planning.

Democratizing financial planning

Such an appropriation of finance for democratic planning could take a variety of forms, featuring different combinations of markets and planning. First, new forms of (post-Keynesian) macroeconomic management could see central banks be subjected to democratic control and (re-)embedded in coherent macrofinancial management featuring public investment banks. In this way their increasing role as social planners in the age of financialization would be appropriated for social, ecological, and democratic means. Second, a democratization of (increasingly concentrated) private finance could provide a tool for more sustainable financial governance and prefigure a cooperative market economy. Third, and indeed going further than one and two, part of the planning literature has suggested an overall democratization of investment as an alternative to market forces (Devine 1988, 2002; Benanav 2022). I will elaborate each in turn.

Public financial planning

Much of the Keynesian tradition was built on the insight that atomistic corporate planning entailed a total amount of investment that is too low to promote full employment (Keynes 2013; Devine 1988). Keynes’s suggestion of a “socialization of investment” would leave private corporate planning untouched, but complement it with extended public investment to fill the gap. In his own words: “It is not the ownership of the instruments of production which it is important for the State to assume. If the State is able to determine the aggregate amount of resources devoted to augmenting the instruments and the basic rate of reward to those who own them, it will have accomplished all that is necessary” (Keynes 2013, 378). In such a vision the task of public finance would be to fund investment in order to make up for the discrepancy between “full employment output” and “consumption out of this output” (Patnaik 2010). The delicate challenge for public planning would be to provide an amount of investment that is high enough to avoid unemployment and low enough to avoid inflation. Low interest rates would encourage investment and avoid a class of people who live off savings.

Such ideas overlap with modern monetary theory, which suggests an extension of public investment aiming for full employment, and (somewhat related to this) also with recent calls to put central banks back under democratic control. Since central banks already act as social planners, as the previous section and some authors argue (Mason 2016; Braun 2018; Bastani 2022; Phillips and Rozworksi, 2019), why not democratize central banks (Woodruff 2019) and use their capacity for non-market coordination for social and ecological goals (Braun 2021a)? Instead of exclusively focusing on low inflation to maintain the wealth of economic elites, central banks could constitute a “Swiss army knife” (Braun 2021a) pursuing full employment and a socio-ecological transformation. Strategic asset purchases by democratic central banks could complement public investment banks to steer investment into foundational research, sustainable technologies, and generally socially desirable sectors that are not, or not sufficiently, profitable for the private sector. This constitutes the foundation for new forms of industrial policy and indicative planning.

On the global level, a global ecological bank could provide capital for a global green new deal. Taxation on historical carbon emission would capitalize this bank and thus constitute climate (and colonial) reparations by the countries that have historically contributed to climate change to the countries that have contributed less carbon but will feel the biggest impact. However, the governance of such a bank would need to be democratic and unrelated to capital contribution in order to not extend Northern control over Southern economies via conditionalities. The governance of such institutions in general would need to marry democracy with technocracy (Braun 2021a), that is, to link financial expertise to multiple democratic interests and lived realities of other stakeholders.

Critical political economists have pointed out that there is a contradiction at the heart of such a Keynesian approach to planning, which appropriates public planning in capitalism for social (and ecological) goals but leaves the institution of private property untouched (Devine 1988, 34ff; Patnaik 2010, 9ff; Shaikh, 2016, 587). Full employment, for instance, obstructs “creative destruction” and empowers workers to claim an increasing share of surplus value, unemployment (“the sack”) ceasing to serve as a powerful threat to discipline workers (Sawyer 1985, 136ff). Such empowerment of labor eventually precipitates a crisis of profitability and/or escalating inflation, as reflected by the stagflation crisis of the 1970s. In addition to other contradictions (e.g., Devine 1988, 36ff) this leaves a single-handed democratization of public planning vulnerable to backlash from business (e.g., via capital and credit strikes) and makes an eventual escalation of social conflict likely.

Cooperative financial planning

Turning to the private financial planning conducted by banks, institutional investors and asset managers, democratization could include a mixture of public banks, financial cooperatives, and credit unions that feature democratic decision-making and allocate credit not only based on profitability but according to a variety of social goals. Such institutions could privilege worker-owned or social cooperatives in their investment and thereby successively increase the social economy sphere. In this way more and more corporate planning would be conducted in a more democratic and social manner. In addition, such an expanded social economy provides the foundation for a more substantial transformation towards social ownership, as the existence of a cooperative financial system can smoothen the turbulence unleashed by a credit strike (Block 2019b).

Already today there are different examples of large pools of capital under public or civil society control. Sovereign wealth funds such as the New Zealand Superannuation Fund, the French Deposits and Consignments Fund, or the Norwegian Pensions Fund all constitute notable state-owned investment funds, the latter owning about 1.4% of the world’s publicly listed companies. However, the large sovereign wealth funds of Saudi Arabia, United Arab Emirates, and Russia also indicate the downside of public capital pools, namely, that they can entrench authoritarian structures. Alternatively, wealth funds could also be owned by workers, such as the Quebec Solidarity Fund (Wright 2010, 225ff). The Solidarity Fund invests primarily in small and medium-sized companies, audits workplaces before investment, and illustrates how unions can be a vehicle to channel workers’ savings from for-profit into non-profit financial institutions. As a final example, the civil society attempt to establish a Californian Public Bank shows that such capital pools could also be owned on the provincial (or municipal) level and that local particularities allow for creativity (Sorg, 2022b, 2022a, 217f). The bank would have been capitalized with income from cannabis sales, which for legal reasons could not be put into banks at the federal level.

On a smaller scale, cooperative banks illustrate how corporate financial planning can be conducted in more democratic and deliberative ways. Cooperative banks have their members decide on a ‘one person, one vote’ basis. Like cooperatives in general, cooperative finance institutions could be spaces where participants learn more democratic and social ways of planning, as a prefigurative practice to transform subjectivities. Cooperatives also tend to prove more resilient to financial crises (ILO 2013; Henselmann et al., 2016). For high-risk start-up ideas one might additionally imagine a cooperative stock market that allows for diversification of risk (Block 2019b).

The principle of democratic governance could be extended to national, regional, municipal, sectoral or interest-group wealth funds. For instance, deliberative decision-making in regional investment banks could bring together representatives of workers, consumers, communities, and marginalized groups to collectively decide over regional investment. The history of social cooperatives (e.g., in Northern Italy) or more recently multi-stakeholder platform cooperatives provides lessons in multi-stakeholder decision-making over corporate planning.

However, without any transformation of market forces, democratically run wealth funds are subjected to systemic pressures that fundamentally constrain their emancipatory potential. Although the Norwegian sovereign wealth fund has refrained from investment in tobacco, nuclear arms, and coal mining, for instance, the fund is primarily governed by profitability concerns (McCarthy 2019, 618f). The fact that its 2022 losses were only soothed by sharp price increases of oil, gas, and refined products illustrates this. Along similar lines, capitalism’s primacy of profitability creates obstacles for the expansion of cooperative financial planning. Even if governments created a robust infrastructure for cooperative activity to thrive vis-à-vis the for-profit sector, which is a substantial obstacle itself, financial subsidies for the cooperative sector are limited by the state’s dependence on taxation of the for-profit sector. Cooperative finance thus needs returns in order to remain competitive with for-profit finance. In addition to limits on financial planning not primarily aimed at profitability, market forces may create substantial hierarchies between the shareholders of different financial cooperatives.

Taming or abolishing market forces via financial planning

So while public macro-financial planning could potentially steer investment and cooperative financial planning could create pools of capital that take into account social and ecological concerns, both of these strategies would be severely limited by the structural power of capital. Competing private interests, capital and credit strikes, and the institutionalized primacy of profitability would tremendously narrow the agency of democratic central banks, public investment banks, and cooperative finance. Varieties of social ownership (as ownership of society or affected stakeholders) have traditionally been suggested as the remedy for the structural power of capital. However, social ownership is in principle compatible with different modes of economic coordination: markets, planning, or different combinations of the two.

Largely privileging markets over planning, the market socialist 3 tradition (e.g., Nove 1983; Bardhan and Roemer 1992; Roemer 1996; Schweickart 2002; Varoufakis 2020) has frequently reserved a particular role for the financial sector in coordinating competition between atomistically planning but socially owned companies. Such models combine highly democratic organization of corporate planning for profit with forms of public planning that are supposed to tame market forces via their control over the financial sector. They thus concede the tacit knowledge problem of central planning most vocally articulated by the Austrian tradition (Hayek 1945; Lavoie 1985), but argue that the tacit knowledge embodied and generated by autonomous local economic actors is perfectly compatible with social ownership of the means of production.

In John Roemer’s (1994, 1996) model of market socialism, for instance, a non-capitalist stock market features as the central institution of economic coordination. A second currency (“coupons”) is distributed equally among all people once they reach adulthood. Coupons cannot be traded, exchanged for other currency, gifted, or inherited. They can only be used to buy shares in companies. People can do this by directly engaging in the stock market or handing over the administration of their coupons to non-capitalist mutual funds. Shares in turn provide people with (non-coupon) income streams, thus ensuring a more equal distribution of surplus than under capitalism. More importantly in terms of a democratization of planning, however, shares also give people the right to influence corporate planning. In addition, public planning can steer markets via the exchange rate between coupons and regular currency. When companies issue new shares, they can exchange newly received coupons for regular currency, which they can in turn use to expand or transform the productive capacities. The central bank can thus manipulate the exchange rate between different sectors in order to incentivize (discourage) investment in sectors that democratic representatives would like to grow (shrink).

David Schweickart’s (2002) model of “economic democracy” similarly features markets in goods and services, but replaces Roemer’s non-capitalist stock market with public investment funds. These funds receive capital via a flat-rate tax on the capital assets of worker-owned companies and can thereby plan the allocation of a part of the social surplus (Schweickart 2002, 50ff). Such planning via socially controlled finance may take the form of one central planning board that allocates capital according to democratically established priorities, which Schweickart (2002, 50f) deems potentially appropriate for contexts in which planning centers on a few goals that are “relatively clear and widely accepted” (one might think of climate change). But financial planning might also feature widely-distributed investment funds acting autonomously, Schweickart (2002, 51) himself advocating a mix of these two extremes. Either way, regional distribution of capital among different investment funds would be done on a per capita basis in order to ensure equal development of different regions.

In both the models of Roemer and Schweickart finance serves as a tool for planning to counterbalance the blind directionality of market economies. In the case of Roemer there is decentral planning via individuals and mutual funds on a stock market, but the model is very atomistic and does not feature moments of deliberation. Schweickart’s varieties of more central or decentral planning via public investment funds allow for more deliberative democratic negotiation over pivotal questions of social and economic life. However, both models would likely face cyclical crises, pressures for managerial hierarchy and subjectivities centered on individual advantage, which are a constitutive part of market economies (Devine 1988, 82ff).

In contrast to such planning via the strategic steering of markets, market abolitionist models advocate systematically planned economies and want to replace markets with, for instance, cybernetic-central planning (Cockshott and Cottrell 1993), associational-decentral planning (Hahnel 2021), or common-ing and stigmergy (Sutterlütti and Meretz 2023, 160ff). However, market abolitionist models that only want to abolish market forces (i.e., atomistic investment planning in new productive capacities) but allow for market exchange (i.e., companies competing and trading with each other based on existing productive capacities) to tackle the tacit knowledge problem share similarities with Schweickart’s social control over investment (e.g., Devine 1988, 2002).

Indeed, Pat Devine identifies the socialization of interdependent investment as the pivotal task of democratic economic planning. But whereas Schweickart has companies free to reinvest their retained profits, Devine advocates that all investment should be placed under democratic control because it has an impact on a variety of social groups beyond the workers in a particular enterprise (Devine 2002, 77f). Investment is thus allocated at two levels. First, democratic governments decide over the overall level of investment (vis-à-vis present consumption) and over the allocation between different sectors and regions. Growth and degrowth of different sectors, overall growth and regional distribution among other issues thus become subjects of democratic deliberation instead of leaving them to the blind directionality of markets (which may or may not be influenced by indirect planning in market societies). Second, major investment by companies can only be conducted if they are accepted by sectoral “negotiated coordination bodies.” These are governed by a set of affected interest groups, including representatives of enterprises in the sector, of public planning commissions at different scales, and of “other groups with a legitimate interest in the outcome” (Devine 2002, 78). Decisions are made on the basis of a variety of quantitative and qualitative information and thus transcend the narrow confines of profitability. In this way negotiated coordination bodies merge private-financial with private-non-financial investment planning, but also profit from information transparency and the possibility to reliably negotiate investment decisions.

Such abolition of market forces via socialization of interdependent investment provides a more durable democratization of planning than the combination of public and cooperative financial planning elaborated above. Allowing for horizontal market exchange between enterprises at the same time ensures that local information particular to time and place (the Austrian “tacit knowledge problem”) are integrated into the social planning process (Devine 2002). However, these exchanges do not determine the expenditure of social surplus, which is instead subordinated to democratic negotiation. This allows democratic planning to materially recognize spheres that are chronically undervalued in market economies, such as social reproduction and ecology, and to properly develop the foundational economy (Foundational Economy Collective 2018), thus providing universal access to democratically determined basics of life. Along these lines democratic planning would not only help coordinate interdependent sectors, but also (re-)politicize planning, increase equality and include social and ecological needs into economic decision-making.

Trajectories of transformation

In this paper I have argued that planning in capitalism consists of both atomistic corporate planning for profit and public planning for overall accumulation. These two are institutionally separate, but interdependent, and both are heavily constrained by the market forces that emerge out of atomistic corporate planning. Finance generally influences both processes by providing or withholding access to credit, but is equally split into private and public finance. Private financial planning allocates part of the social surplus for profit and fees, while public financial planning again employs its repertoire to ensure overall accumulation.

Financialization has transformed private corporate planning via the notion of shareholder value, private financial planning via the rise of asset managers as horizontal private planners, public planning via increasing public dependence on private credit, and public financial planning via the growing importance of central banks as technocratic public planners. This financialization of planning has depoliticized public planning, depressed overall growth and investment, increased unemployment, and entailed financial instability. The heterogeneous literature on the democratization of finance suggests a range of alternatives that extend the realm of deliberate social and democratic control over the economy considerably and promise more egalitarian, sustainable and democratic outcomes. Central banks could be placed under democratic control and integrated into ambitious public planning for socio-ecological transformation. Sovereign wealth funds and public investment banks could replace private asset managers and multi-stakeholder deliberation targeting social and economic need could replace shareholder value both within corporate private and financial private planning.

I have argued that the institutionalized primacy of profit and the structural power of capital will severely constrain any such effort at the democratization of planning in the tradition of Keynesianism or Modern Monetary Theory. Models based on social ownership of the means of production on the other hand are compatible with a variety of mechanisms of economic coordination. In these, finance frequently features prominently as a tool for democratic planning to reduce or replace the uncertainty precipitated by market forces, thus echoing the planning debate’s observations about the coordination capacity of finance. Such a perspective on planning differs from other models in the current planning debate in that it considers investment and dynamic planning as a pivotal issue, which essentially determines who we expend our collective capacity to produce more than we need to survive (i.e., a surplus). It stresses our interdependence, which necessitates deliberation over the general trajectory of the econom. Figure 2 summarizes the findings. Financialization and democratization of financial planning

The idea of socially controlled finance as a tool for deliberate coordination foreshadows a theory of social transformation. If finance can generally be appropriated for democratic planning of the social trajectory of the economy, it can also be used to successively channel resources from for-profit sectors towards more democratic and cooperative forms of planning for social and ecological need.

In one of the most sophisticated and widely discussed theories of social change, the late Erik Olin Wright (2010) discusses the practices of real world social experiments with alternative forms of collective coordination, from Wikipedia to public libraries, cooperatives and universal basic income. Situated at the intersection of critical social theory, social movement studies and prefigurative politics, his real utopian sociology discusses the potential of social laboratories for a deeper democratization of state, economy, and society. Such small-scale experiments with democratic deliberation have been completely neglected by the new literature on democratic planning, although cases such as participatory budgeting, community-supported agriculture, and social cooperatives provide invaluable insights into multi-stakeholder cooperative planning.

Real utopian sociology does not only deal with heterodox practices and institutional designs, but also formulates theories of social transformation. Wright (2010, 303ff) identifies three distinct ideal-type pathways: ruptural strategies to fight elites in order to abruptly break with the current order, interstitial strategies to ignore elites and built an new order within the old one, and symbiotic strategies to compromise with elites towards mutual benefit. While the three distinct strategies in no way exclude one another, and may indeed need to be combined, Wright is highly skeptical of the chances (and desirability) of ruptural transformation in high-income, liberal-representative democracies. The remaining two candidates constitute natural allies and may mutually support each other. Symbiotic strategies are pivotal to construct institutional frameworks in which the social economy is not immediately destroyed or appropriated by capitalist oligopolies. Conversely, an expanding social economy and thriving civil society provide institutional politics with the mobilizing structures and general social power to push economic elites towards social and class compromises. One may add contra Wright’s skepticism that such a dual strategy may reach its limits when there are no more mutually beneficial (or at least neutral) compromises to be fought for. At the point when capital sees its power to control atomistic planning for profit substantially threatened it may choose to unleash crippling capital and credit strikes. Such a context may necessitate a ruptural break towards a democratization of planning. But even so, a prior redistribution of social power via a symbiotic-cum-interstitial strategy would tremendously ease the turbulence to be expected from such a ruptural break and indeed increase the likeliness of its success.

In terms of democratizing financial planning this means public money creation for “non-reformist reforms” (Gorz 1967), which both expand direct public planning and at the same time provide favorable conditions for socially owned and cooperative financial institutions. If political majorities for more substantial reforms emerge in the face of ecological catastrophe, this could mean socialization of large investment funds. But in general there would need to be a successive shift of pensions, consumer credit, and private money creation from large commercial banks towards financial institutions under public, union, or civil society control. These capital pools can in turn finance the creation and expansion of socially owned and cooperative (non-financial) enterprises such as local food coops, renewable energy collectives or housing syndicates (Bastani 2020). Obtaining credit is one of the traditional problems smaller cooperatives face vis-à-vis their for-profit counterparts. Socially controlled finance creates the possibility to obtain capital without the risk of takeover that exists on stock markets and beyond large commercial banks that prefer large for-profit companies.

Public investment banks can at the same time finance the more capital-intensive and urgent transformations necessary to avert climate catastrophe. A Global Climate Bank to tax historical polluters and fund those primarily affected by climate change mentioned in the previous section illustrates the principle of reparative finance (Appel 2020; Webber et al., 2022). A democratized finance must aspire to provide preferential access to finance to historically disenfranchised groups and communities. This includes particular financing guidelines for investment and credit allocation and representatives of women, workers, and marginalized minorities in larger financial bodies.

The expansion of non-profit public and cooperative finance creates new experiences and learning processes with democratic planning. This makes it easier for movements to successively overcome ideological resistance against planning based on market ideology. Beyond the realm of ideas it also increases the chance that investment in a given political territory stays relatively stable despite capital and credit strikes (Block 2019b, 548ff). In addition, a strong cooperative financial sector can offset capital flight because it will maintain its capacity to borrow on global capital markets (under potentially higher interest rates) and can therefore thwart or smooth a currency crisis (Block 2019b, 549). Less turmoil renders visible that capital flight might not be a reasonable response to expected downturn, but deliberate sabotage. This in turn precipitates more legitimacy to impose capital controls to further reduce capital flight (Block 2019b, 549f). Either way such a context makes it more likely that non-reformist reforms retain political support long enough to survive a transition trough.

If social power were strong enough to maintain course one could imagine a transformative framework such as the Meidner Plan, which envisioned that companies would pay corporate taxes in the form of new shares into wage earner funds (Wright 2010; Warner 2022). Such an approach could successively channel shares into negotiated coordination bodies made up of representatives of multiple stakeholders such as workers, consumers, citizens, communities, and marginalized groups. These bodies would successively become majority owners of corporations and could thus increasingly coordinate investment ex ante. In the same way the Meidner Plan proposed to use some of the fund to train workers for self-management, to take over tasks of management (Guinan 2019), such a transition process would generally allow for a broader learning of self-governance in democratic planning.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.