Abstract

This article explores the metamorphosis of profit-making and profit uses in the context of retailing’s digital transition. To assess the qualitative mutations of the sector, it is not enough to focus on technological changes since the unequal operational development of firms is also the outcome of managerial strategies and financial policies. This research analyses them from an economic and accounting perspective. The contribution is twofold. First, at the conceptual level, it proposes an original combinatory outlook on value creation and value appropriation to account for the diversity of profit trajectories in the context of retail digitalization. Second, at the empirical level, it gathers essential information concerning the mutation of the sector based on a comparative analysis of the strategies and trajectories of Walmart—the industry leader—and two of its main challengers since the mid-nineties: the main historical rival, Carrefour, and the new entrant, Amazon. Stylized facts about their respective financial trajectories and a description of their engagement with digitalization enable the identification and the interpretation of their distinct dynamics. Beyond the retail sector, this article brings fresh insights to the wider literature on intellectual monopoly by questioning the nature of investment and the transformation of cost structure in the digital age.

Introduction

Modern retailing made a triumphal entry indeed into the twenty-first century. From the mid-nineties to the mid-2000s, leading western retailers’ activities were expanding rapidly with an annual growth rate in sales generally above 10%, mainly resulting from the rapid internationalization of their operations (Baud and Durand, 2012; Durand and Wrigley, 2009; Wrigley and Lowe, 2007).

However, since the 2008 financial crisis, the situation has reversed dramatically. The press has even used the term “Retail apocalypse” to depict the wave of brick-and-mortar store closures and job destruction in developed economies throughout the 2010s (Centre for Retail Research, 2020; Fertik, 2019). Diverse causes are mentioned for this trend among which are sluggish consumer spending due to rising inequalities, over-indebtedness due to leverage buyouts, and the surfeit of malls. But this sectoral trend conceals widening differences regarding the trajectories of individual firms, which suggests that, rather than a simple decline, retailing is experiencing a profound qualitative mutation. Indeed, the 2010s were the decade when the development of e-commerce finally actualized the revolutionary promises of the digital economic restructuring of the nineties (Alfonso et al., 2021).

This article explores the metamorphosis of profit-making and profit uses (O’Sullivan, 2018: pp. 787–790) in the context of retail digitalization from an economic and accounting perspective.

The nature of investment in the digital age is a complex matter, particularly because of the measurement issues that arise as a result of the increasing role of intangible assets (Corrado et al., 2012; Haskel and Westlake, 2018). In the US retail sector, Crouzet and Eberly (2019) argue that the under-accounting of investment in intangibles is why investment level appears to be inconsistent with high valuation and a rise in productivity. However, as their analysis takes place at the industry level, it doesn’t address the need to disentangle what results, in this dynamic, from the changing composition of the industry and the shift in business strategies and trajectories occurring at the firm level. This latter aspect is the focus of this article.

The contribution of this research is twofold. First, at the conceptual level, it mobilizes and reinterprets the notions of value creation and value appropriation (Björkdahl and Holmén, 2019; Foley, 2013; Lepak et al., 2007) to advance an original combinatory outlook on the diversity of profit trajectories in the context of digital transition. Second, at the empirical level, it gathers essential information concerning the mutation of the sector based on a comparative analysis of the strategies and trajectories of Walmart—the industry leader—and two of its main challengers: the main historical rival, Carrefour, and the new entrant, Amazon. Stylized facts about these firms’ financial trajectories and a narrative analysis of their engagement with digitalization allows us to identify their distinct dynamics which are then interpreted in light of the proposed conceptual framework.

Beyond the retail sector, this article brings fresh insights to the wider literature on intellectual monopoly and Big Tech (Durand and Milberg, 2020; Pagano, 2014; Petit and Teece, 2021; Rikap, 2022) concerning the nature of investment and the transformation of cost structure in the digital age.

The reasons we chose Walmart and Amazon are straightforward. Walmart is the paragon-firm of modern retailing. According to Deloitte annual Global Power of Retailing reports, it assumed the position of the world’s largest retailer in 1990 (Deloitte, 2006) and has held a position of undisputed leadership ever since. If Walmart occupies the position of the incumbent, Amazon is the main rival. The firm has “skyrocketed” from the 157th position in 2001 (Deloitte, 2018) to the top 10, where it entered in 2015 (Deloitte, 2017), before establishing itself in 2019 as the new leading challenger of Walmart (Deloitte, 2021), ahead of all other traditional retailers (Costco, Schwarz, Kroger, etc.). The fact that Amazon, which is a broader multi-industry, high-tech, company is becoming Walmart’s direct competitor (Gray and Lee, 2021; Irwin, 2017) indicates that the digitalization of the retail sector is a high-stake process involving inter-sectoral restructuring.

The choice to include Carrefour in our study allows to counter the pitfall of selection bias favoring successful businesses (Denrell, 2005), while considering a key actor of the industry. Carrefour was the 2nd largest retailer in terms of sales from 2000 until 2011. However, the firm slid to tenth in sector rankings in the following decade, 1 the period during which digitalization of the industry intensified.

Overall, the choice of the three firms provides highly contrasted cases to research firm profits strategies and business trajectories in the course of retail digitalization. With this sample, we stay within the confine of a sufficiently narrow study to allow for an in depth narrative economic and accounting analysis. Of course, the downside of this selectivity is that important dimensions of the sectoral transformation are overlooked. In particular, the role (or lack of) of digitalization in the dynamics of hard discounters (Steenkamp, 2018) should be investigated in other research.

From an empirical point of view, the analysis relies on a systematic study and comparison of the consolidated financial statements of the three firms, as disclosed on the Orbis database under the so-called detailed format. It begins with Amazon’s first 12-month annual reporting in 1995 and ends with the last pre-Covid reporting at the end of 2019. Exploiting the power of such detailed accounting data allows us to precisely delineate changes in financial and investment behavior at the firm level (Davis, 2016). Additionally, relying on accounting conventions provides a basis that enables comparisons between individual firms’ trajectories. However, relying on accounting conventions may also restrict the analysis. To better capture the firm-level dynamics that may either challenge or subsume accounting conventions, we use additional material provided by the three companies in their annual reports and a systematic examination of their acquisitions based on Marketline and press data.

The next section outlines a conceptual framework to relate profit sources and uses in the context of the digital transition. The following outlines the firms’ financial trajectories and their engagement in retail digitalization. We then explore the traces of this mutation in their cost structures and their investment behaviors. Building on these results and the proposed conceptual framework we finally elaborate and discuss three stylized scenarios regarding profit sources and uses.

Value creation and value appropriation in the age of intellectual monopoly

The role of Information Communication Technologies (ICT) in retail firms has been an issue for decades (Kjellberg et al., 2019; Nightingale et al., 2003), but in the 2010s, the digital transformation of retailing dramatically accelerated following the deployment of big data in business practices and the infusion of management technics driven by a new form of rationality called algorithmic governmentality (Rouvroy and Berns, 2013). The literature indicates that this set of technologies has a powerful impact on the structuration of the retail value chain (Mak and Max Shen, 2020; McKinsey, 2020; Reinartz et al., 2019) and redefines the modalities of engagement with customers (Arkenback, 2019; Beauvisage and Mellet, 2020; Bradlow et al., 2017; Evans and Kitchin, 2018; Grewal et al., 2017; Inman and Nikolova, 2017; Jocevski et al., 2019; Lee et al., 2015; Munandar and Khoriyah, 2020; Schildt, 2017; Shukla and Nigam, 2018). However, from a broader economic point of view, the literature doesn’t consider how investment and profit dynamics in retailing are related to these transformations. This section engages with this issue at the conceptual level unfolding the distinction between value creation and value appropriation.

The concept of “control revolution” (Beniger, 1986; Bensussan, 2022) exposes the asymmetrical evolution of industrial techniques and information systems and its consequences. One particularly salient problem in the context of digitalization is that innovation in control technology can foster value creation but does not necessarily coincide with value appropriation (Björkdahl and Holmén, 2019). In our view, such a “value slippage” (Lepak et al., 2007: p. 187) can result in a discrepancy between investment activity and profitability.

From value to intellectual monopoly rents

While we rely on a value theory inherited from the Marxist tradition, 2 we reject a substantialist conception of labor value in favor of an interpretation of value as a social relation. A stated by David Harvey, “Value is not a fixed metric to be used to describe a changing world, but (…) a social relation which embodies contradiction and uncertainty at its very center” (2006, p. 215). The exploitation of labor normalized by socially necessary working time is at the heart of capitalist valorization, but the latter evolves in an uncertain manner in space and time, according to the vagaries of competition, changing needs, socio-political battles, or technological ruptures.

Incorporating some Keynesian insights, the “Monetary Labor Theory of Value” developed by Riccardo Bellofiore articulates three main dimension of Marx’s value theory: “that value eventually comes into being with money as its phenomenal form (the monetary theory of value); that class struggle and intra-capitalist competition affect the extraction of living labor (the theory of exploitation); as well as in the essential monetary ante-validation of labour power as potential labour through the financing of production (the macro-monetary theory of capitalist production)” (Bellofiore, 2018).

For the purpose of this article, the most relevant aspect of this multifold theory is the second dimension. It states that the exploitation of living labor is the source of a global pool of surplus value for which the firms compete to access: “The prices fixed in the sphere of circulation (…) redistribute among individual firms the total amount of live labor extracted from labor power” (Bellofiore, 1989; pp. 16–17).

This approach is consistent with Duncan Foley’s remark “that capitalist exploitation generates a pool of surplus value for which each capitalist competes through some kind of business plan or market position” (Foley, 2013: p. 259). It follows that “each capitalist is in effect a free-rider on the whole system of generation of surplus value”: “One way to appropriate surplus value is to exploit productive wage workers by lowering costs through raising their productivity or depressing their wages, but this is far from the only way. The actual exploitation of productive wage workers is important because it is the mode of appropriation of surplus value that contributes indirectly to the global pool of surplus value. There are many other modes of appropriation of surplus value, such as monopolization of sectors of the market; marketing and advertising; establishment of intellectual property rights through patents, copyrights, and trademarks; ownership of scarce energy or other natural resources; superior cleverness in arranging financial transactions or structuring financial property rights; and controlling medical treatment”. (Foley, 2013: p. 260, p. 260)

One can thus distinguish between, on the one hand, actual exploitation of productive wage workers that contributes to the global pool of surplus value and, on the other hand, the appropriation of surplus value without contribution to the pool of surplus value. This dichotomy founds our conceptual distinction between value creation and value appropriation which borrows from the classical notion of rent.

In its purest form, rent has no direct relation to exploitation of productive labor; it is a pure appropriation, a pure punction in the global pool of surplus value. Foley again summarizes clearly this: “enforceable property rights that permit the owner of productive resources (often called “land” in the terminology of classical political economy) to exclude capitalists from access to those resources create “rents.” These rents are a part of the pool of surplus value generated in capitalist production, though they have no direct relation to the exploitation of productive labor in themselves.” (Foley, 2013: p. 260, p. 260)

The current use of the notion of rent derives from this classical notion to indicate abnormal capitalist profits arising out of monopoly power. Recent research insists on the role of rents in the context of digitalization since various forms of intellectual monopoly allow firms to capture rents, that is, profits in excess of the average rate of profit. Some works demonstrate the role of property rights, corporate innovation systems and technoscientific activity (Birch, 2020; Pagano, 2014; Rikap, 2020; Rikap and Lundvall, 2021) in fueling such rents.

Arising out of the process of capitalist competition, the concentration and the centralization of capital facilitate the emergence of “natural” monopolies as scale economies, network externalities and sunk costs create huge barriers to entry (Mosca, 2008). Such “natural” intellectual monopoly dynamics are at play in the context of digitalization under various combination of (1) high fixed costs and low or zero variable costs and (2) powerful network externalities and complementarities generated (Haskel and Westlake, 2018; Mosca, 2008) in the course of interactions on “two-sided markets” or even “multiple-sided markets” (Armstrong, 2006; Rochet and Tirole, 2006).

Beyond the case of Big Tech, the pervasiveness of such “natural” intellectual monopolization dynamics has also been identified in the context of Global Value Chains (GVCs). In the GVCs literature, the use of the notion of value creation and appropriation (or capture) is standard and the connection with intellectual rentiership has thus been straightforward. For instance, Buckley et al. use the term “rent” to “emphasize the potential for intangible assets to generate supernormal profits due to their nature as key inputs in value creation and appropriation in GVCs” (2022, p. 12). More specifically, Durand and Milberg (2020) make a threefold distinction. Vertical natural monopoly rents result from network externalities when the investment supporting the network exhibits return to scale and sunk costs. Intangibles-differential rents are named by analogy with the notion of differential land rent analyzed by classical economists to account for the difference of income accruing from unevenly fertile lands (Ricardo, 1817: Chapter 2). They accrue from an uneven distribution of intangibles intensity between participants in a given GVC and the resulting uneven cost dynamics. In the context of complementarity activities, this phenomenon allows most intangibles intensive firms to benefit more from collaboration than less intensive ones. Data-driven innovation rents are the benefits accruing from the enhancement of innovation capabilities derived from data centralization.

A combinatory outlook on value creation and value appropriation

This section outlines operational tools to investigate the dichotomy between production of surplus value and appropriation of surplus value at the firm level. Such conceptual framework is required to articulate the general consideration regarding value theory sketched in the previous sub-section to the empirical investigation of the uneven ability of retailers to create and appropriate value in the course of the digital transformation.

On the one hand, we propose to consider investment as a proxy for value creation. Though not reflecting immediately value creation, it is an advanced indicator of potential value creation since the aim of investment is to amplify and renovate the business model, that is, to increase productivity and/or to increase the scale of operations, thus enlarging the contribution of the firm to the global pool of surplus value. Contrastingly, declining investment—a fortiori disinvestment—implies a retreat in terms of value creation dynamics, that is, a reduced contribution to the global pool of surplus value.

On the other hand, profitability is considered as a manifestation of the ability of a firm to appropriate value, that is, to effectively punction the global pool of surplus value, which depends on the conditions of its insertion in the price system on the cost side (inputs, investment goods, and labor) and on the income side (sales). Here above normal profits correspond to value capture while below normal profits are related to value leaking. Note that the notion of profit normality does not refer to a sectoral norm but to the economy in general, since interindustry relations can interfere in the uneven ability of firms to appropriate value.

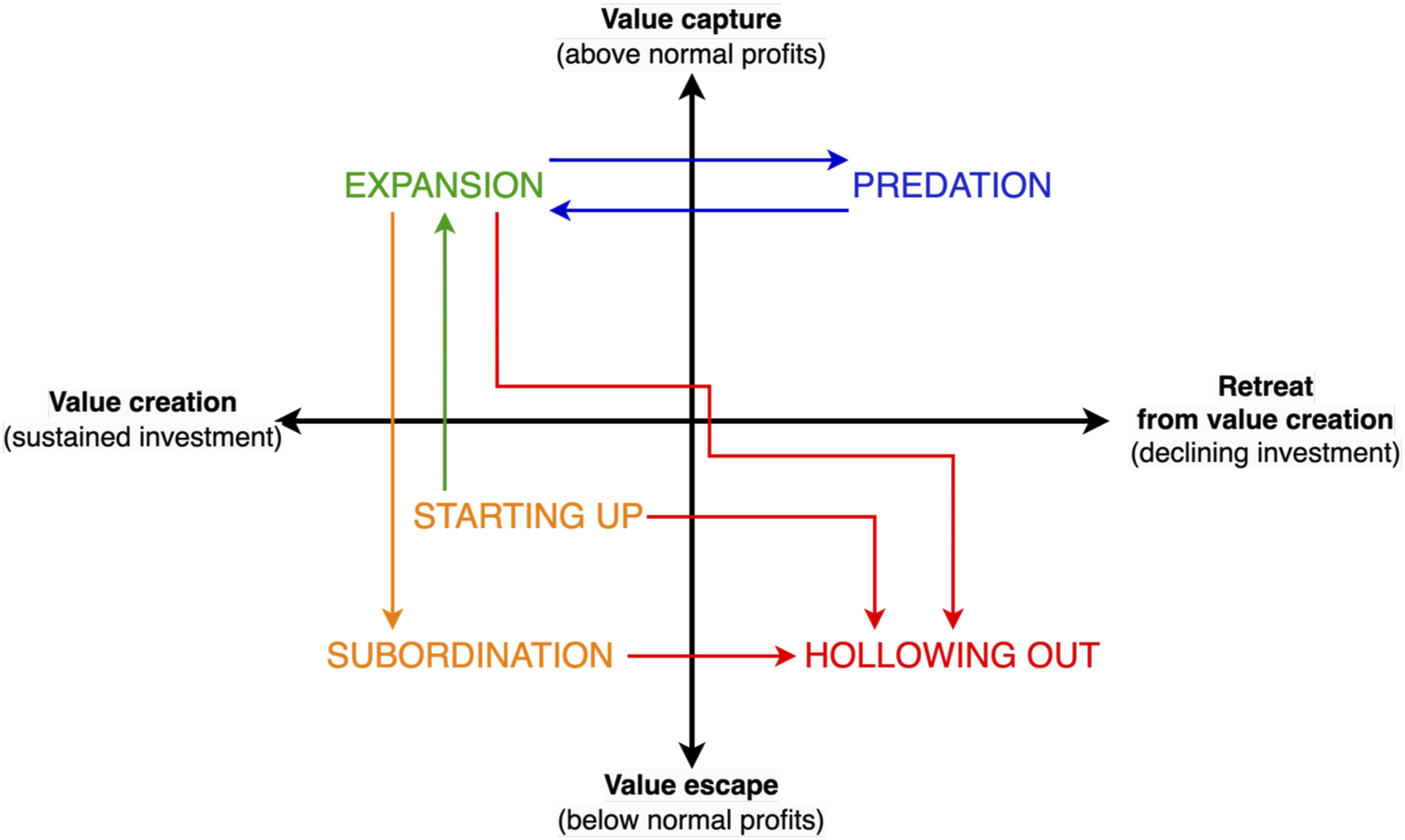

Combining these two dimensions, Figure 1 distinguishes four stylized business dynamics, where arrows indicate how a firm can move from one to another. (i) Firms can create value and appropriate it correspondingly, which allows them to expand (expansion). Indeed, sustained capital accumulation is favored by a coincidence between value creation and appropriation since the latter incentivizes further development and allows to fund the pursuit of the former. Expansion corresponds to the pursuit of business opportunities characterized by above normal profitability. (ii) It is also possible that value creation and value appropriation do not correspond. We thus have a second configuration where firms can create value but are not able to capture it. This configuration can be temporary when it corresponds to the launching of a new business, or a restructuration linked to product or process innovation (starting-up). In this case, the growth of the firm will aim at modifying the business model through the provision of new services in order to capture value (Björkdahl and Holmén, 2019) and move (green arrow) to more favorable situation of expansion. Another possibility is that this disjunction is permanent, resulting from the deterioration of the business model (orange arrow). It is then characteristic of subordinate capitals that cannot exit due to sunk cost, but manage nonetheless to survive as long as profits, although abnormally low, are above interest rates (subordination). Such configuration has been conceptualized in the context of global value chains (Starosta, 2010). (iii) In a third configuration (predation), the firm appropriates value in excess to its contribution to value creation. Such a dynamic of value capture would be reminiscent of the sabotage envisioned by Veblen when “the successful business strategist is enabled to get a little something for nothing at constantly increasing cost to the community at large” (1921, pp. 117–118). As discussed above, an appropriation of value largely disconnected from surplus value production is characteristic of rentiership. It has necessarily a relational (zero-sum game) dimension since over-appropriation of value by some firms must be met by under-appropriation elsewhere (cf configuration ii). Although from a broader social perspective the effects are negative, from the business perspective it is a successful (but reversible) upgrading from the expansion situation (blue arrows). (iv) A fourth configuration (hollowing out) reflects a situation where a business is neither investing to create value nor appropriating value, the business is then consuming itself by hollowing-out. Such a morbid involution could directly occur as a result of the unraveling of the expansion dynamics, the failure of a start-up or after a further degradation of a situation of subordination (red arrows). Business dynamics in relation to the articulation of value creation and value appropriation.

Theoretical underpinnings concerning the notion of value, value creation, value appropriation, and rent laid the ground for our conceptual framework distinguishing business dynamics according to the differentiated ability of firms to create and to appropriate value.

Following the growing literature about intellectual monopoly rentiership, we hypothesize that digitalization of retailing activities favored a growing disjunction between value creation and value appropriation. More specifically, we consider that different handlings of the digital transformation by different retail firms have dramatically affected their business dynamics through a combination of enhanced scale economies, network externalities and elevated sunk costs, which can be interpreted using our combinatory relational framework.

The uneven unfolding of Carrefour, Walmart, and Amazon’s trajectories

This section explores the trajectories of Carrefour, Walmart, and Amazon in terms of financial and operational development and engagement with digitalization and highlights the divergence arising in the 2010s. 3

Stylized facts from companies’ financial accounts

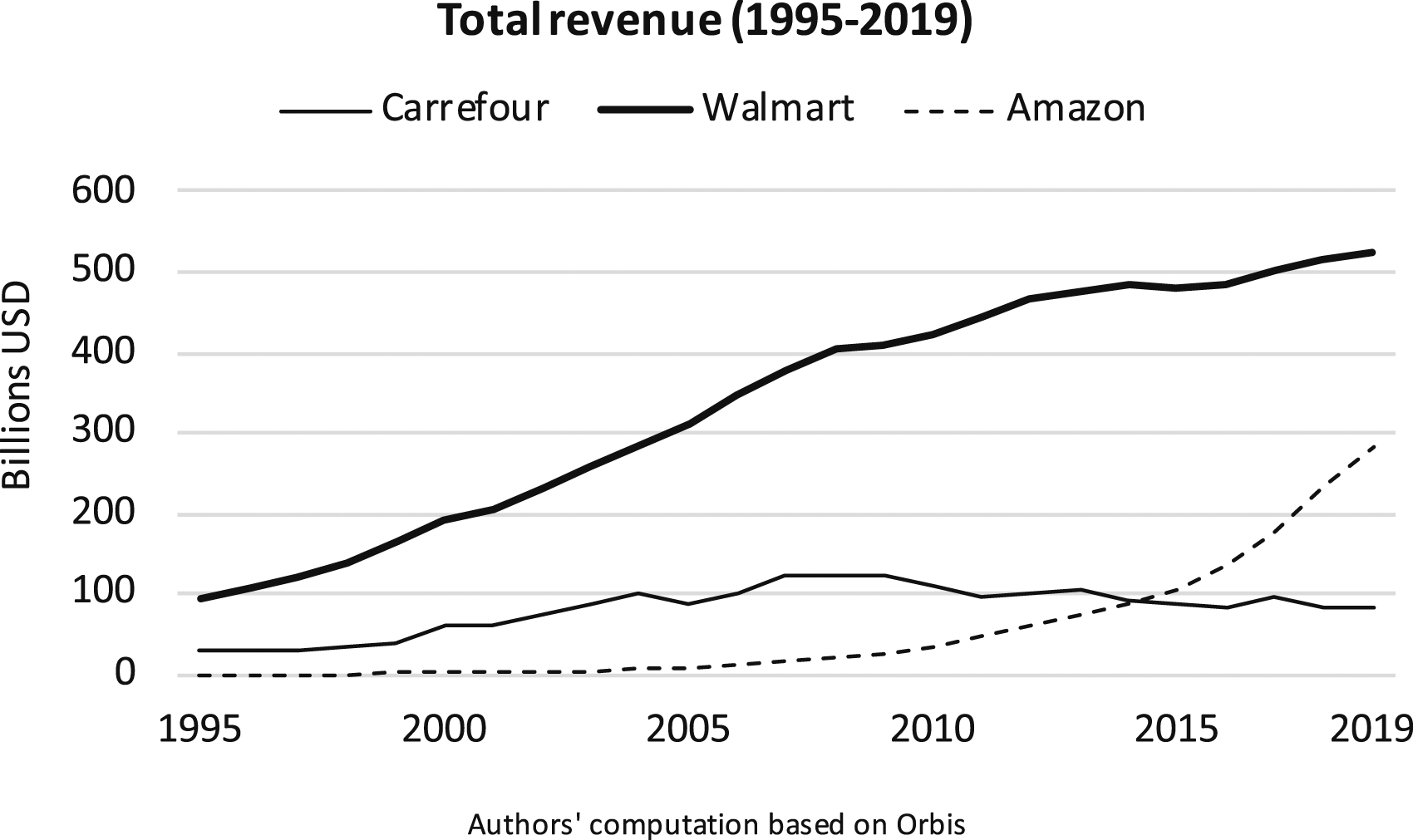

Up until the 2008 financial crisis we observe a long period of sustained total income growth for Carrefour, Walmart, and Amazon, but after that the trends diverged dramatically in terms of income (Figure 2), fixed assets growth, profitability, and returns to shareholders (see detailed analysis in Online Appendix, part 1). Carrefour, Walmart, and Amazon—Total revenue (1995–2019).

The comparison of revenue and fixed assets growth establishes a clear distinction between a rapidly expanding and internationalizing business (Amazon), a declining one (Carrefour) and an industry leader with considerably slower growth but which nevertheless pursued expansion as it focused on a handful of key markets (Walmart).

Looking at profitability, the picture is somewhat different. If Carrefour’s performance declined sharply after 2008 in terms of mark-up, ROA, and ROE, Walmart did much better than the other two firms over the whole period and in all these measurements. Interestingly, while Amazon generally performed better than Carrefour, its ROA declined markedly after 2008 as its asset turnover decelerated, indicating a transformation of its business model.

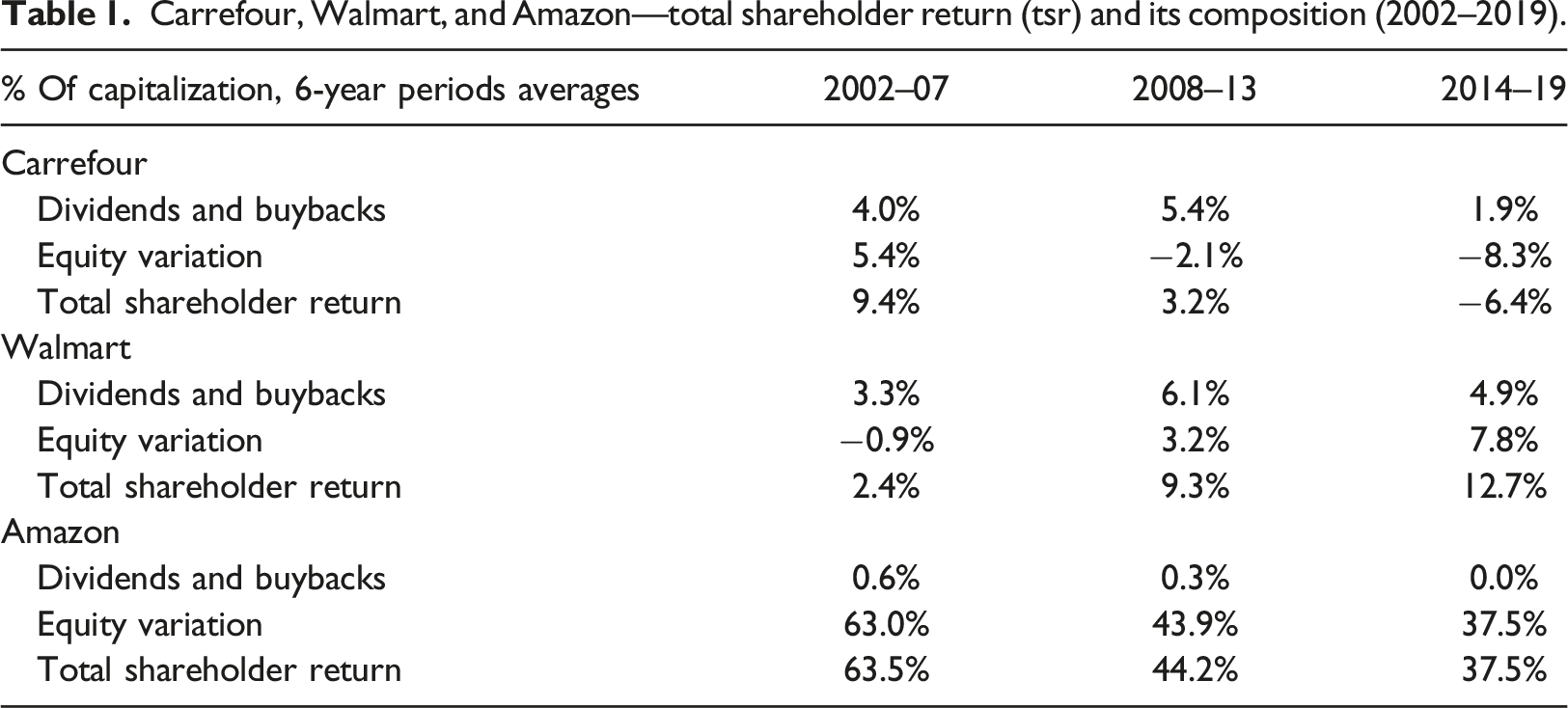

Carrefour, Walmart, and Amazon—total shareholder return (tsr) and its composition (2002–2019).

Contrary to the downsizing strategy of Carrefour, Walmart relied on its strong operational performance (see Online Appendix, Figure 4) to continue its development all over the 2008–2013 period, albeit at a slower pace (see Online Appendix, Figures 1 & 2). The firm consequently raised unprecedented amounts of profits, of which an increasing part was distributed to shareholders. Following this dynamic, the value of Walmart’s shares went up and increasingly sustained its shareholder return as the firm further reduced its growth, but maintained strong levels of profitability, in the last period.

Contrasting with these strategies of distribution, Amazon’s profits, when any, were fully dedicated to the funding of growth and completed, when necessary, by debts. Consequently, if shareholders were getting richer at a very impressive pace, this was thanks to the appreciation in the equity price and not because of the distribution of earnings.

This outline of the dynamics of revenue, fixed assets growth, profitability and value accruing to shareholders allows us to make two broad statements. First, Walmart’s slow growth and the decline for Carrefour after 2008 contrast vividly vis-à-vis the previous period of rapid and profitable expansion for both firms.

Second, the trajectories of the three firms have become highly divergent since 2008. Carrefour is rapidly descaling its operations while its profitability has plummeted which, in the last period, implies that its shareholders are getting poorer. Walmart, the industry leader, can preserve a very high level of profitability albeit with sluggish growth as it refocuses its activities. Moreover, unlike Carrefour, the firm is managing to increase its distribution to shareholders relative to its profits and to enrich its shareholders at an accelerating pace. Finally, Amazon is very rapidly expanding its operations, but this occurs with lower profitability compared to Walmart. Returns to its shareholders are almost exclusively driven by the very rapid increase in equity price.

Uneven engagement with retail digitalization

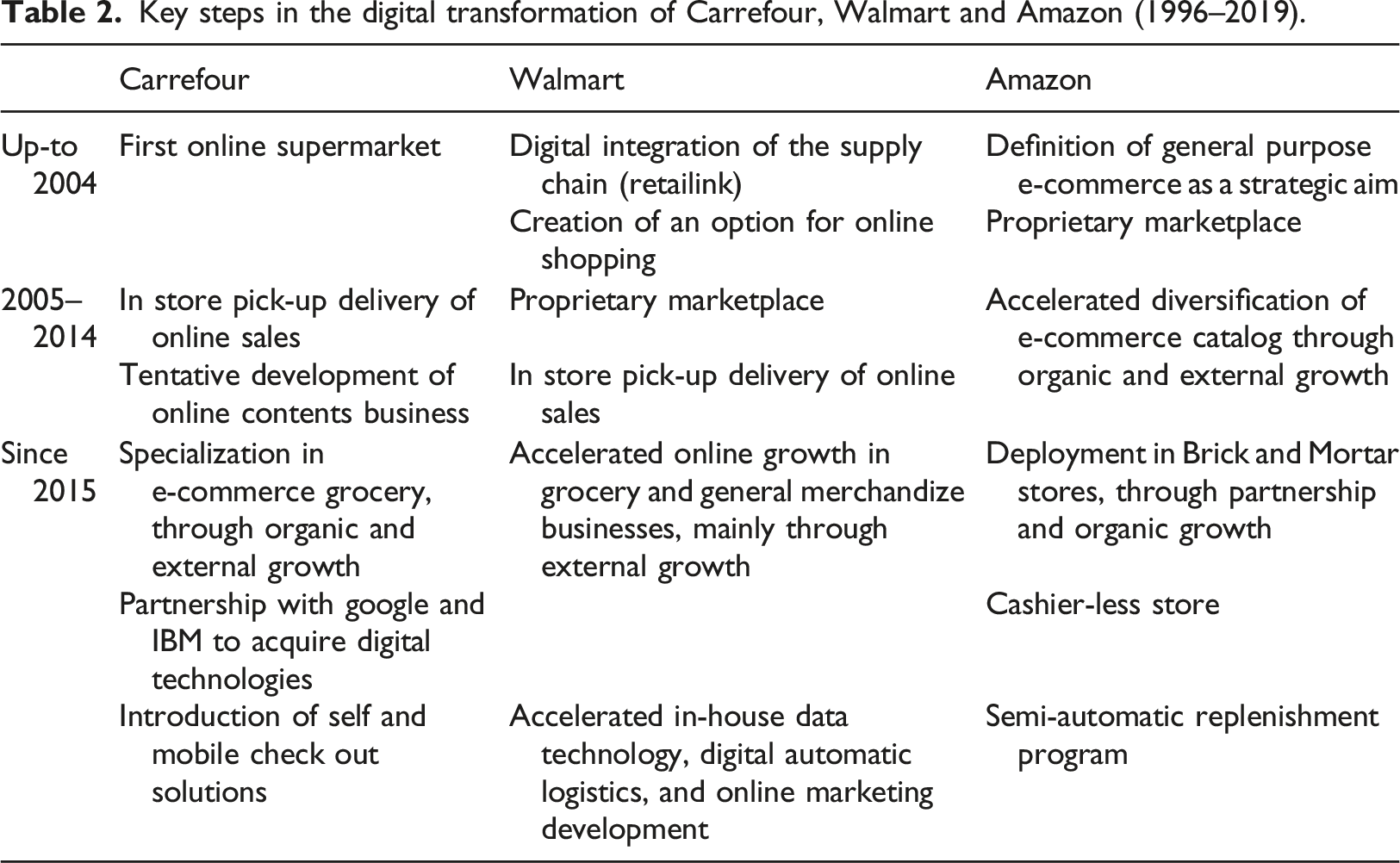

Key steps in the digital transformation of Carrefour, Walmart and Amazon (1996–2019).

First it underscores the specificities of Amazon vis-à-vis the two traditional retailers. From its inception, Amazon’s ambition was to take aim at “established and large markets”—such as general retailing and grocery—thanks to a radical and general-purpose innovation: the collection and treatment of massive digital data to guide economic transactions. Amazon was thus always a pure e-commerce player. Only after 2015 did it move to brick & mortar stores via both acquisitions and partnerships with established retailers, and by innovating with the creation of intensely digitalized physical stores and engaging more directly and physically with end consumers.

Second, it shows Carrefour lagging well behind Walmart. Carrefour entered early in the e-commerce and had already developed several specific services at the end of the 2000s. But, while Walmart accelerated its digital transformation in the 2010s, despite some important acquisitions to attempt to catch-up on digitalization, Carrefour failed in accumulating in-house capabilities. Ultimately it resigned itself to relying on partnerships with technology companies such as IBM and Google to mobilize state-of-the art digital capabilities.

Walmart is a latecomer to e-commerce. However, in the 2010s, it underwent a dramatic evolution with acquisitions at an accelerating pace. While a first objective was to enter the business of online content, it was clear that Walmart was simultaneously attempting to enhance its in-house digital capabilities to improve its core business competencies and performances in three directions: first, in purely digital technology, second in online sales know-how and three, following Amazon’s example, via the development of selling services to third parties. The accelerated development of its own marketplace since 2016 is the single most important evolution in this regard. The marketplace is driving most of Walmart’s online catalogue growth, allowing the firm to cover the long tail and to increase its income as it enlarges its customer base while it accumulates data riches crucial for innovation and market control.

The contrast between the three companies is also spectacular when one looks at their patenting activity. It is true that patents are not a strong indicator of innovation-related investment (Işık and Orhangazi, 2022: p. 892). However, the huge differentiation in that matter between the retailers leaves little room for doubt. 5 With more than 8700 patent filings between 2014 and 2019, Amazon is by far the leader in this activity. Walmart, which registered almost 2000 patent filings during the period, but only 300 during the preceding period, only recently became a significant contender. Meanwhile, Carrefour is simply not participating in the innovation race, with stagnant and negligible patenting activity and a comparatively insignificant portfolio of less than 100 patents.

Overall, engagement with digitalization closely matches the overall dynamic in terms of revenue, assets, and total shareholder return, although the internal financial logics diverge. The next section aims at better understanding the mechanisms that link these two dimensions.

Intellectual monopoly, costs, and investments in the making of retail profits

Relying on the conceptual framework presented in section 2 to look at Carrefour, Walmart, and Amazon’s financial trajectories enables a better grasp of the logic of profit-making in the context of the digitalization of retailing.

The trajectory of Carrefour is characterized by a decline in activity, profitability, and a lack of engagement in the digital transition. Downsizing and the restructuration of operations seems consistent with a hollowing-out logic aimed at reallocating capital away from this sector. But, this trajectory can be contrasted with successful profit-making strategies based on retail digitalization and the appropriation of related rents.

Profit and investment beyond accounting categories

From an economic point of view, investment is distinct from other forms of spending in that it creates an asset that provides benefits over a long period of time. But the current criteria for assets’ recognition in accounting do not perfectly match this distinction since, when they are generated internally, most of the costs associated with the creation of intangible assets should be recognized as expenses. 6 This may induce an under-accounting of investment in intangibles, as Crouzet and Eberly (2019) argue, but surely creates an asymmetry between acquired versus internally developed intangible assets, since the recognition of the former is much easier. These issues are especially consequential when dealing with investments in digital activities since it implies that, to make sense, the analysis must go beyond the accounting categories of “assets,” “capital expenditures,” and “expenses.”

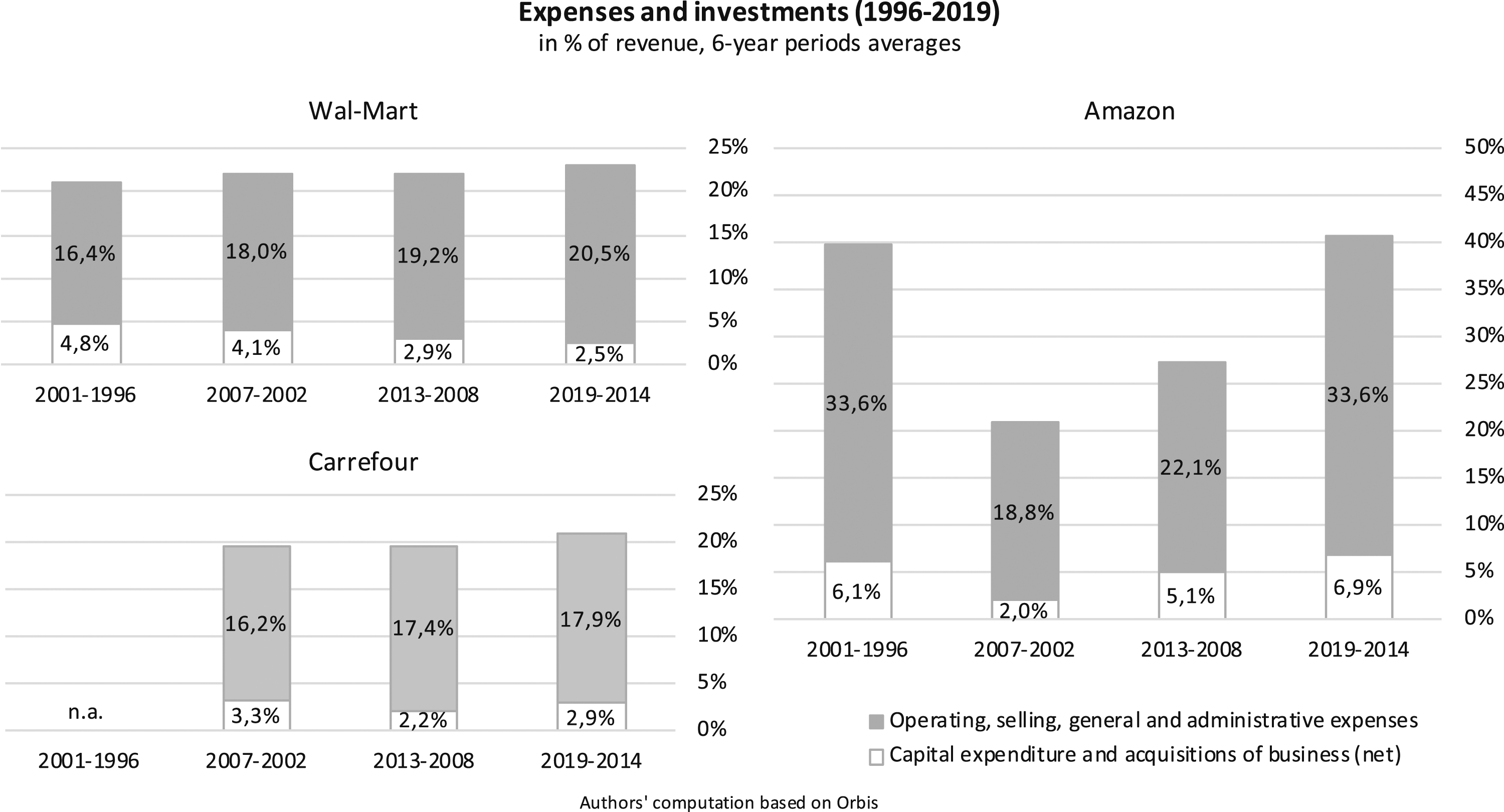

Indeed, as Figure 3 shows, relying on these accounting categories doesn’t discriminate between the divergent trajectories of Walmart and Carrefour. Both firms appear to follow identical paths that are marked by a steady rise in general expenses in relation to sales that the reduction in investment, initiated in 2008, did not fully compensate for. On the contrary, 2008 marked Amazon’s return to an impressive dynamic of both investment and spending that equaled, for the last period, its inaugural characteristics. Carrefour, Walmart, and Amazon—Expenses and investments (1996–2019).

Understanding how digitalization explains the divergent trajectories of Carrefour and Walmart as well as the strengths of Amazon and Walmart requires challenging the accounting categories of investment and expenses, and analysing the corresponding amounts from an economic point of view. To do so, we build on the information published by companies in their annual reports.

Diverging trajectories at Carrefour and Walmart

According to its Chief Executive, Doug McMillon, Walmart is “in an early stage of building a new business model” (Gray and Lee, 2021). The intense development and accumulation of digital capabilities (see 3.2 and Online Appendix, Part 2) corroborates this affirmation, which is further strengthened by the observation of certain changes occurring regarding investment policy.

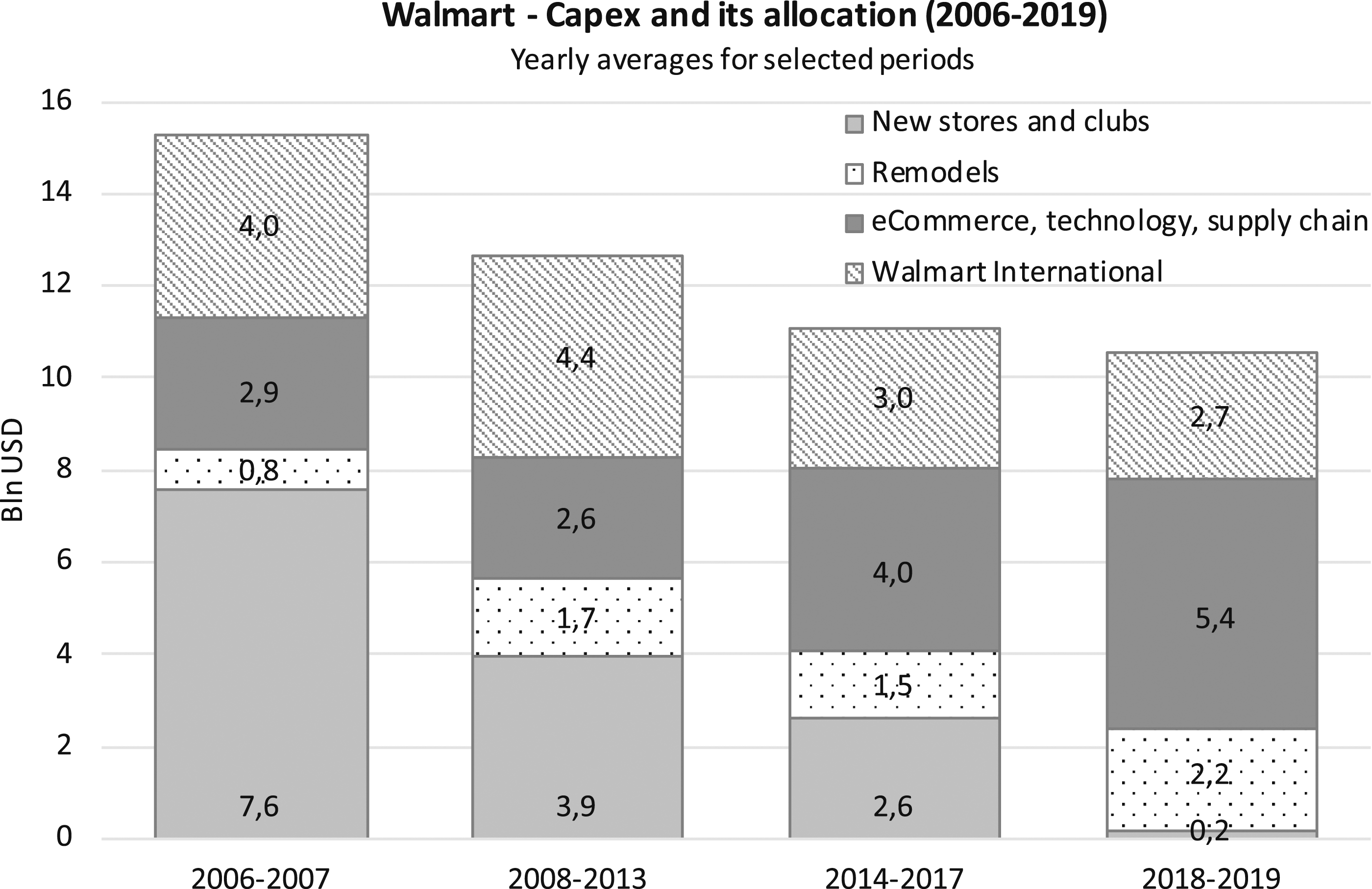

As one can see in Figure 4, the share of Capital Expenditures (Capex) dedicated to e-commerce, technology, and supply chain management surged from 2.9 billion USD in 2006–2007 to 5.4 billion in 2018–2019. In other words, while tech-related investment accounted for just 18% of Walmart Capex in 2006–2007, it represented more than half in 2018–2019. This increase is all the more pertinent that it occurred in the context of a significant decline of total Capex by one third over the same period, from 15.3 USD annually in 2006–2007 to 10.5 in 2018–2019. This evolution is also interesting as it suggests that in the context of slowing growth, a qualitative mutation of investment toward digital capabilities allowed Walmart to defend its market-share, preserve mark-up and profitability, and improve shareholder returns (see Figure 2, Table 1 and Online Appendix, Part 1). Walmart—Capex and its allocation (2006–2019).

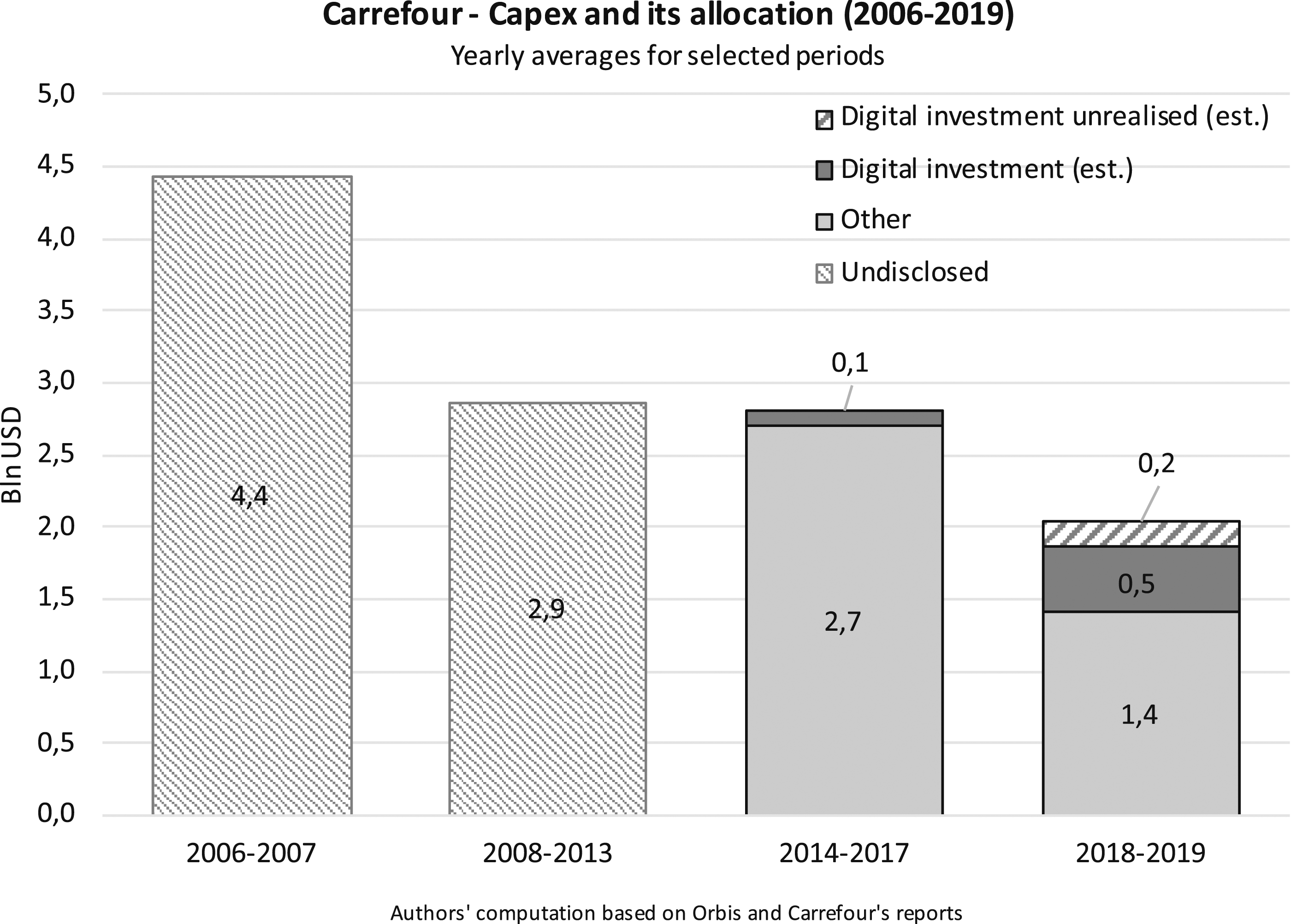

The logic of digitally focused investment observable at Walmart is very different from the downsizing trajectory of Carrefour. By withdrawing from less favorable segments, Carrefour faces downward cost rigidity that constraints its profitability and an explosion of restructuring costs (see Figure 10 in the Online Appendix) that further limits the capacity to invest. Accordingly, as shown in Figure 5, Capex decreased by more than 50% between the pre-crisis and the last period and, based on the annual reports, it can be estimated that Carrefour only dedicated 4% of its Capex to its digital transformation between 2014 and 2017, as compared to 36% for Walmart. For the last period, while Walmart was focusing more than 50% of its Capex on its digitalization, which is to say 5,4 billion USD per year, Carrefour only invested an estimated 454 million USD per year and was thus far from achieving its own stated objective (635 m$ per year on average). This first explains why Carrefour’s digitalization strategy is not as ambitious as it used to be and why the firm now mainly focuses on the development of partnerships, notably with Google and Tencent. But, the diverging trajectories between the two firms regarding their investments in digitalization also shed a new light on the apparently similar evolutions of their cost structures. Carrefour—Capex and its allocation (2006–2019).

In the case of Carrefour, downsizing, restructuring, and reduced level of investments in digital technologies did not reduce operating costs nor create growth opportunities. In the case of Walmart, operating with lower levels of investment targeted at digital competencies implies an increase in operating costs too, but, first, these cost increases are linked with digital capabilities, which are cited as one of the main drivers of cost increases for year 2018 and 2019, and, second, they are observed in a context of otherwise decreasing costs. As highlighted by Brett Biggs, the firm’s CFO, investments in wages, training, technology, and process improvements help to “increase productivity, manage inventory, reduce costs and serve customers,” which is “beginning to pay back” from 2018 onwards by putting Walmart “in a position to deliver near-term results while positioning the business for the longer term” as it continues to “leverage [its] scale” (Amazon, 2020; p.4). In other words, reduced investments focused on technology and their related operating costs allow Walmart to develop digital capabilities and accumulate intangible assets, which in turn allow to deploy resources more efficiently, to reduce costs, and to improve offer to customers, notably through e-commerce, while allowing future service enhancements.

Such an evolution characterized by increasing digitalization with diminishing CAPEX is consistent with the argument that digitalization can pave the way to rents. More specifically, here, rents linked to network effects and economies of scale provide the opportunity to raise productivity and capture value to an extent that surpass the intensity of the productive effort, while positioning the company favorably to benefit also from data-driven innovation rents on the longer term.

Building and selling in-house capabilities at Amazon

At Amazon, the technological strategy relies on both dynamic investment and enormous expenditure to build in-house capabilities. As such, since 2003, every annual report mentions that “spending in technology and content will increase.” The profit strategy is intimately interwoven with this expansionary technological drive. Its logic appears in plain English in the Management’s Discussion and Analysis of Financial Condition and Results of Operations section of its annual report: “We seek to reduce our variable costs per unit and work to leverage our fixed costs.” This formulation is reiterated in identical terms year after year since 2007 and with only minor variations before that.

While the objective of minimizing variable costs is not original, the persistent emphasis on leveraging—as opposed to reducing—fixed costs brings us to the specificities of making profits out of digital—but also logistical—capabilities. It means that the company is determined to grow and to leverage its growth, that is, to seek opportunities beyond its own activities to make profitable use of its investments. In other words, the orientation towards the leveraging of fixed costs expresses a willingness to take advantage of the versatile character of the capabilities corresponding to these fixed costs, which are “the costs necessary to build and run [its] technology infrastructure; to build, enhance, and add features to [its] online stores, web services, electronic devices, and digital offerings; and to build and optimize [its] fulfillment centers and delivery networks and other facilities” (Amazon, 2020: p.19).

Amazon’s strategy of benefitting from economies of scope, economies of scale and network effect can be traced in the composition of its sales and costs.

The spectacular growth of Amazon’s operations (Figure 2) was contemporaneous with a shift in the composition of Amazon’s operations toward service sales at the expense of product sales in the past decade. Services accounted for 9% of the firm’s revenue in 2009 and grew to 43% in 2019. 7 For that year, these were mostly constituted by third-party seller services (19% of total revenue), web services (12%) by Amazon Web Services (AWS), and subscription services (7%)—mainly Amazon Prime (Amazon, 2020: p.68).

The shift toward sales of services manifests the diversification of the profitable uses of infrastructure, computing, marketing, and algorithmic capabilities initially deployed by Amazon for the sale of products on its website. By selling its logistic, computing, and algorithmic capabilities as services, Amazon can improve its operations in several ways.

First, it benefits from scale economies beyond the limits of its own product sales operations. Such a strategy allows for a positive spiral of cumulative competitive advantages: on the one hand, the sheer size of its sales operations generates such huge economies of scale that the logistics, computing, and algorithmic services it sells are very competitive; on the other hand, the surge of scale related to the sales of these services further improves the efficiency of its own operations.

Second, it enlarges its “ecosystem of digital products and services” (Annual report 2014, p.19), paving the way for some complementarities both on the supply and the demand side. In the meantime, this allows for an enlargement of its client base along the long tail and further engagement with its various types of customers through network effects.

Three, it increases its data gathering, which allows for further improvements and refinements in its recommendation, prediction, and innovation capabilities with a consequent positive impact on its various lines of businesses.

Last but not least, these services sales are profitable, and this is all the truer where they contribute to absorb the fixed costs of developing and operating Amazon’s own structure and processes.

The impact of this “fixed cost leveraging strategy” is apparent in the evolution of Amazon’s cost structure and, more specifically, in the dramatic diminution of the cost of sales, which represented 77% of sales in 2009 and shranked to 59% a decade later. But, the counterpart of the relative diminution of these mainly variable costs has not been primarily an increase in operational profit, but rather its near complete disappearance as two items related to fixed costs—“fulfillment costs” and “technology and content”—were rapidly expanding. 8 It is only very recently that Amazon has begun to take full advantage of this new heavy fixed costs structure by succeeding to leverage them, thus not only returning to profitability, but also laying the groundwork for further leveraging and profits.

For instance, expenses in “fulfillment” costs, which are related to the operations of new fulfillment centers, customer service centers, physical stores, and payment processing systems, have risen much faster than the activity and consequently account for around 15% of sales at the end of the period against less than 10% in the previous decade. This growing internalization of logistics implies the transformation of variable costs into fixed costs. Amazon can “make” these services itself instead of buying them. But, once they have been deployed internally, the firm can sell them to third parties. The increased capacity to offer such services to third parties then contributes to covering a growing part of these fixed costs, which alleviates the burden on Amazon’s own sales. This is all the more efficient that sales by Amazon’s sellers incur higher costs as a percent of net sales than Amazon’s own sales (Annual report 2018, p.26). Thus, the logic of fixed costs leveraging explains why Amazon establishes business connections with others including direct competitors like Walmart: “Amazon Multi-Channel Fulfillment (MCF) is a lesser-known subdivision of the company’s highly successful Fulfillment By Amazon (FBA) programme. Where FBA stores, packs and delivers to Amazon customers, sometimes in as little as a day, MCF offers much the same for sales on other websites, such as Walmart, eBay, Etsy, Shopify and several others.” (Lee, 2015)

The category “technology and content” grew even more rapidly—from 5 to 13% of sales over the same period. Technology and content costs primarily concern software, content, and hardware assets that are versatile, in the sense that they can be used in “a wide variety of products and services” and allows for some “cross-functionality” and “process efficiency (…) while operating at an ever-increasing scale” (Annual report 2018, p.26). No matter that they are not recognized as constituting assets, they are explicitly regarded as investments 9 and expected to increase (Annual report 2018, p.26) to support the strategy of leveraging fixed costs previously highlighted. 10 Indeed, since cost allocation is based on usage (Annual report 2018, p.26), AWS’s clients contribute significantly to offsetting these fixed infrastructure costs, which alleviates the costs for Amazon’s other activities. Moreover, as these infrastructure costs are mainly expensed as incurred (Amazon, 2020: p.44), it also means that the costs for Amazon of the future benefits of this infrastructure have already been paid, mainly by its AWS’s current clients. From this perspective, the capacity of Amazon to offer attractive and competitive services to its AWS’s clients while being able to cover all its infrastructure costs as they are incurred shows the strength of this business model. It is against this background that the current profit level of Amazon should be analysed.

Overall, Amazon’s expansionary technological and infrastructural drive is at the very core of its profit strategy whose rationale is the leveraging of fixed costs by offering its internal services to external clients. Due to the huge economies of scale and scope associated with intangible assets and the exploitation of network effects, this strategy has proved to be very powerful and lay the ground for long term appropriation of rents.

The shift in the qualitative composition of Capex at Walmart points in the same direction. Along with the symmetric failure of Carrefour, these elements suggest that beyond the case of Amazon, the deployment of digital technologies is affecting profit-making in the retail industry through the enhancing of scale and scope economies that allows an appropriation of value to a large extent disconnected from value creation.

Discussion

Our analysis of Carrefour, Walmart and Amazon corroborates the significance of the categories of business dynamics presented in section 2. However, it also suggests that a further elaboration of these categories could prove useful in the context of the digital transition, possibly beyond retailing. With this intention we propose three stylized scenarios.

The first is derived from Carrefour’s illustrative trajectory of a previously dominant model that became obsolete due to a lack of investment. Without sufficient investment, operating performance tends to decline. As a result, the only way to serve high pay-outs to shareholders is the scaling down of operations by focusing on the most profitable business. This trajectory is consistent with the “downsize and distribute” financialisation mantra (Lazonick & O’sullivan, 2000) which stresses how the growing assertiveness of shareholder value came at the expense of non-financial corporations' investment (Aglietta, 2000; Froud et al., 2000; Lazonick, 2018).

In the context of retailing, short term emphasis on shareholder returns impedes the investment necessary to accommodate digital transformation and favors downsizing to sustain profitability. Over the course of years, the cumulative effects of the firm’s degrowth fuels a spiral of loss of scale economies and competencies. Considering (a) the crucial role of fixed cost in information infrastructure, (b) the huge economies of scale in their operations and (c) the strategic relevance of access to original data, descaling appears to be a self-defeating strategy in the field of digital competition.

Ultimately, the attempt to follow a path of sustained profits without accumulation is doomed to fail. It leads to a hollowing-out of the corporation when, in addition to decreased revenue, shareholder returns wane. The end result of such a business trajectory is either dismantling bankruptcy, absorption, or survival only as a subordinate of a dominant business, possibly from the Tech sector, or to recede on a niche market.

The second scenario is derived from Walmart’s successful transition from the old pre-digital model to the new digitalized one. In this case, a dominant incumbent has leveraged its existing capabilities and infrastructure as well as its supplier and customer bases in the course of its digital transformation.

Investment in the new intangible intensive model allows further valorizing of pre-existing resources which enables the firm to serve high pay-outs to shareholders and to fund its expansion along the new industry rationale.

In this scenario of renewed dominance, profits are not proportionate to investment. An initially dominant position allows the firm to achieve its digital transformation with a comparatively lower level of capital expenditure while rapidly compensating for the additional costs incurred through the economies of scale and network effect achieved thanks to the size of its operations. As a result, Walmart achieved its digital transformation and laid the basis for an increased domination vis-à-vis other stakeholders almost without additional costs and with a lower level of capital expenditure, which suggests an ongoing predatory dynamic.

The third scenario, inspired by Amazon, is that of a rising model. The disrupter is fully dedicated to the scaling-up of its operations with the aim of amplifying the extraction of intangible-related rents. Here, pay-out to shareholders is the least of its managers’ concerns as they retain and reinvest profits in pursuit of market dominance. Shareholders acquiesce as they are pleased by the surge in stock prices that anticipates future income and delivers immediate substantial capital gains. Profit goes hand in hand with accumulation, that is, a dynamic of expansion, at least in this phase of the conquest.

These stylized scenarios emphasize the disconnection between value creation and value appropriation in the context of an industry digitalization. Our empirical analysis provides an original way to explain these contrasted dynamics building on the notion of intellectual monopoly rents mentioned in section 2.1.

As Amazon positions itself more and more as a provider of digital and logistic services to other businesses, it accumulates what Durand and Milberg (2020) call intangibles-differential rents and vertical monopoly rents by specializing in the intangibles and infrastructure intensive segments of the value chains where the most powerful scale and scope economies take place. The resulting build-up of business-interlocking through persistent complementarities favors dynamically the profitability of Amazon vis-à-vis other firms. Indeed, it can benefit from differential rents accruing from an uneven distribution of returns to scale and of network economies which leads to an uneven cost dynamics in its favor. Overtime, such differential rents sow the seed of a shift of Amazon from a dynamic of expansion toward a dynamic of predation, where value appropriation will be increasingly disconnected from value creation.

Additionally, such mechanism could also explain why Walmart due to its sheer size was able to immediately scale-up the advantages of digitalization vis-à-vis its business partners, something which was not an option available to the same extent to Carrefour smaller operative scale and much lesser ambitious investments.

A second insight from this analysis of digitalization in retailing and its relation to profits and investment concerns the articulation of economic and accounting categories. Increases in operational expenses linked to the successful integration of innovation through new digital devices and business procedures at Walmart are an interesting example. They come along with digitalization-related capital expenditures without being recognized as investments by accounting standards. This contributes to the reduction of CAPEX for that firm, illustrating what Crouzet and Eberly (2019) call an “under-accounting” of investment. However, as Rikap (2022) recalls in the case of Amazon, if technologies-related spendings were fully accounted as assets, this would substantially increase current profits.

Depending on the criteria used for assets’ recognition, digitalized business models can therefore appear either as capital intensive or as low investment business models. But, it is important to state that, at least on the short run or as long as investments continue, due to amortization dynamics, a broader recognition of investments in intangibles spendings as assets would also, by construction, result in a higher level of profit.

Overall, both profits and investments would be higher. This shows the importance of accounting conventions but also highlights, by contrast, that the economic problem arising from differential rents, which create differentiated dynamics between value creation and value appropriation, is true puzzle and not simply an accounting artefact.

Conclusion

This article has documented how the digitalzsation of the retail sector unleashed a dramatic restructuring as some firms managed to reinvent their business model, while other failed and newcomers rapidly expanded their operations with hegemonic ambitions. But rather than a simple technological mutation, it demonstrates that this process is indissociable from the transformation of profit-making strategies.

In this article we have documented the contrasting fate of three key actors in the western retail industry: Carrefour, Walmart, and Amazon. Through the exploration of financial accounts and business strategies delineated in the companies’ reports, we have provided stylized facts about their respective financial trajectories and a description of their engagement with digitalization which has allowed us to identify three very distinct dynamics.

By dissecting the economic logic underscoring retail firms’ uneven digitalization, its translation in accounting terms and its financial implications, we brought new light to the management literature on retail digitalization and contribute more broadly to the research on intellectual monopoly. More specifically, we have provided indications of the role of differential rent arising from scale, scope and network economies linked to intangibles intensity. Interestingly, the sales of infrastructure-use as services may be related to the same logic of leveraging fixed cost. Overall this invite to consider that differential rent emerge as a crucial explanation of the dissociation between value creation and value appropriation in the context of digitalization.

In addition, our analysis of Walmart, Carrefour and Amazon’s capex and cost structures demonstrates that digitalization both challenges and subsumes accounting conventions concerning costs, investments and profits. These crucial categories for economic analysis should thus be used cautiously and as much as possible critically enlighten with complementary analytical elements.

A broader contribution is to underscore the major socioeconomic implications of the changing business dynamics related to digitalization. It invites a move beyond the “Big Tech” perspective to assess the impact of digitalization on diverse industries and mutations in the corresponding value creation and appropriation dynamics.

With the increasing concentration in the retail sector and more hierarchical relationships between businesses, digitalization is changing the condition of economic coordination with enormous consequences for workers, customers, businesses, and communities. Awareness on the part of social scientists, policymakers, and the general public on these issues pertaining to leading digital companies has been rising for a few years (for an influential example, see Khan, 2017). Nonetheless, this study highlights the fact that traditional anti-trust policy is not necessarily adequate. Although we do not share the optimism of Petit and Teece (2021) regarding the benefits of dynamic competition among Big Tech, we agree with them that the anti-trust scholarship that recommends the dismantling of businesses monopolized due to the economic logic of data collection and treatment is inappropriate. In our view, rather than weakening the forces of coordination arising from scale, scope, and network economies in digital processes, regulators should take stock of natural monopoly dynamics and look for new venue for policy to mobilize them in the pursuit of socially, ecologically, and psychologically desirable outcomes.

Supplemental Material

Supplemental Material - Profit-making, costs, and investments in the digitalization of retailing—The uneven trajectories of Carrefour, Amazon and Walmart (1995–2019)

Supplemental Material for Profit-making, costs, and investments in the digitalization of retailing—The uneven trajectories of Carrefour, Amazon and Walmart (1995–2019) by Cédric Durand, Céline Baud in Competition & Change.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.