Abstract

This paper examines the growth of the UK coworking space (CWS) sector in the context of the COVID-19 pandemic, drawing on data from a multi-year study comprising 44 interviews with CWS owners, managers, and other key economic actors. The paper offers a novel contribution by drawing on critical political economy to conceptualise CWS as capitalist enterprises providing fixed capital of an independent kind in competitive markets increasingly shaped by changing urban commercial real estate dynamics which necessitate that CWS adapt their business models to remain economically viable. The paper finds the entry of large corporate actors in the CWS sector is forcing smaller independent CWS to diversify to remain competitive. This pressure inhibits the ability of CWS to adhere to – and offer services matching – the aims of early CWS, namely the cultivation of a community of like-minded individuals who cowork to reduce rental costs and social isolation. These findings are theoretically and empirically significant as they illustrate how rapid sectoral shifts are driven by business decisions with structural causes, rather than being due to the actions of individual users of CWS or the communities they serve. These findings have implications for understanding the future of coworking and provide new insights into how competition shapes and changes the business models and competitive strategies of enterprises.

Introduction

Coworking is the process whereby individuals such as freelancers, remote workers, and ‘digital nomads’ share space and resources. Benefits include the development of social capital, the possibility of serendipitous encounters, and the creation of a sense of community as a remedy to the isolation caused by working alone (Gandini, 2015; Waters-Lynch and Duff, 2021: 384). This trend is epitomised in the rise of dedicated coworking spaces (CWS). Early forms of CWS were founded to ‘pool economic resources to reduce the cost of rent and counter isolation’ on the part of individual CWS users (De Peuter et al., 2017: 700), and it is this ideal of coworking which continues to drive and motivate many owners and managers of CWS globally.

Today, CWS number over 34,600 worldwide (Statista, 2023), with the highest concentrations in the United States, India, and the United Kingdom (UK). CWS have proliferated within urban centres across the latter in recent years, with an estimated 6,000 CWS in operation in the UK as of mid-2021 (Ellis-Moore, 2021). The volume of commercial office space dedicated to coworking in the UK will likely have doubled in the period 2019 to 2023 (Statista, 2023), and the UK CWS sector is predicted to grow at a compound annual growth rate of eight percent over the next 5 years (M-Intelligence, 2022).

The rapid global growth in CWS has attracted much academic and industry attention. Existing research has generally looked at the organisation, enactment, and experience of work inside coworking spaces, including the arrangements of physical space (Bouncken et al., 2021) and the curation of ‘community’ (Garrett et al., 2017; Spinuzzi et al., 2019), with an emphasis on user experiences (Tintiangko and Soriano, 2020), and the significance of these spaces as important sites of collaboration, entrepreneurship, and creativity within ecosystems of innovation (Bouncken et al., 2020a). A noticeable gap in the research is the lack of theorisation of CWS as enterprises competing within – and being shaped by – market dynamics, chiefly pressures to remain profitable, or at least economically viable. For instance, CWS have largely not been analysed as entities with business models that are subject to strategic change (Bouncken et al., 2020b). Moreover, insufficient academic attention has hitherto been paid to how CWS owners and managers finance and maintain their properties, attract and retain customers, engage in branding and marketing, and enhance their service provision so as to increase their competitiveness. This paper rectifies this oversight within the existing CWS literature by exploring how CWS are being compelled to adjust their strategies in the face of competitive pressures to remain profitable and viable enterprises. The paper achieves this by presenting findings from a study of CWS in the UK over the period 2019–22, comprising primary data collected from 44 interviews with CWS owners and managers, and with other actors with expert, first-hand knowledge of the commercial dynamics in the UK CWS sector.

A key theoretical contribution of our paper, which we explain in more detail in the following section, is that a deeper comprehension of the CWS phenomenon in the UK can be reached by starting with a broader political economy perspective that considers CWS as providers of ‘fixed capital of an independent kind’ (Marx, 1973: 686) to CWS users. As entities operating in a market for such provision, the viability of CWS is also shaped by their ability to valorise at the prevailing rate of profit. If CWS cannot achieve this, they must adapt to find other means to enhance their competitiveness, as must any individual capitalist entity (Harvey, 2014). This abstract conceptualisation of CWS is articulated in our paper through empirical interrogation of the concrete business models and strategies of CWS, illustrating how they are shaped by competitive pressures. Our paper reveals changes in commercial property dynamics across UK cities, wherein there has been widespread turn away from long-term commercial property leasing by larger companies as they seek more flexible office leasing solutions (Echeverri et al., 2021; Financial Times, 2023; Gupta et al., 2022) in the context of broader shifts in demand within commercial real estate markets. This analytical approach is important not only for understanding how CWS operate but also because doing so provides valuable insights into how new economic sectors and real estate markets develop, how competitive pressures apply, and how individual economic agents – in this case CWS – shape and are re-shaped by these processes.

Our research has discovered that the fragmentation and internal differentiation of the UK CWS sector is both the condition and consequence of competitive pressures. Competition has intensified because of the decomposition of the UK CWS sector into different forms of CWS. This competition then leads to a reshaping of this unevenness and recomposition of the sector as capital is progressively more concentrated in the hands of larger CWS operators. This has led to a trifurcation of the sector, comprising three main forms of CWS: those that are funded by an external organisation or benefactor (and therefore largely insulated from competitive pressures within the broader CWS sector); CWS which exist as part of larger commercial real estate providers’ portfolios; and independent CWS. A significant finding from our research is that independent CWS are adapting their business strategies in the face of competitive pressures from corporate commercial office space providers who are increasingly using the branding and inside-space designs and aesthetics of coworking as it was originally conceived as an element of their growing flexible office space offer. At the same time, independent CWS are increasingly being compelled to compete with these larger providers by attracting and retaining ‘enterprise clients’ such as remote teams of workers from larger companies, or even entire companies, to secure future flows of revenue in the short-term, flexible office space market (Instant Group, 2022). The very users of these CWS are therefore changing.

Our approach is distinctive insofar as it conceptualises and analyses the growth and transformation of CWS as a dimension of these broader urban political-economic dynamics (Engelen et al., 2017), rather than merely viewing CWS as bounded organisations in which coworking takes place. Accelerated by the COVID-19 pandemic and the widespread turn to a model of hybrid working that CWS already anticipated (Felstead, 2022), the CWS sector is rapidly transforming. In particular, our research reveals the degree to which even major CWS owners and managers are consciously moving away from the original notion of CWS as they were – and often still are – conceptualised within academic literature, namely as neutral spaces occupied by freelance workers who seek the benefits of community and collaboration. Our research reveals that this recent period of exponential CWS market growth in the UK is also a period of demise, as the original CWS business model becomes subsumed within and subordinated to a much larger corporate commercial flex-space market. Our paper, therefore, is not merely about the political-economic processes of competition that are reshaping the UK CWS market but also an insight into how the logics of capitalism operate to inhibit the emergence and development of new spatial organisations of work.

The paper is structured as follows. Section one details our theoretical framework, and reviews the existing literature on CWS, presenting the status quo ante prior to the period of accelerated change we identified during the height of the COVID-19 pandemic. It also details our methodology. Section two presents our empirical findings, which are structured around the different forms of CWS and their business models that we identify. In section three, we demonstrate the degree to which competitive market dynamics were already in evidence within the UK CWS market prior to the COVID-19 pandemic, albeit in an attenuated form that permitted various forms of collaboration between CWS themselves and with local state agencies. Section three details how competition between UK CWS that already existed in variegated forms within English cities has intensified as companies have begun to demand greater flexibility and agility from commercial office space providers in the immediate pandemic and post-pandemic context, and how CWS with different underlying business models are being forced to adapt (or not) to remain viable. The paper concludes with reflections on the future of UK CWS as businesses and for the urban-economic ecosystems in which they operate, especially as regards the emergent contradiction between coworking, as such, and the transition to a market increasingly shifting space, resources, and strategy to the provision of, what we term, ‘flex-space with a coworking element’.

Theorising and contextualising the CWS sector

Understanding the growth of the CWS sector and the operation of individual CWS first requires theorisation of the general economic dynamics in which CWS operate. Our theorisation of CWS is therefore grounded in the dynamics of capital accumulation and the valorisation and reproduction of individual businesses, or ‘capitals’, in prevailing conditions of the production of goods and services, market exchange, and competition (Pitts, 2020). In accordance with this approach, we conceptualise CWS as providers of ‘fixed capital of an independent kind’ (Marx, 1973: 686) in the wider economy. We understand ‘fixed capital’ to mean the resources into which capital is invested and which are worked upon in the labour process (Harvey, 1982: 205). This could take the form of machinery, or other commodities consumed in the course of production, but with respect to CWS we are referring to increasingly significant providers of physical office spaces which are owned and operated independently of the labour processes that take place within them and for which they are a ‘precondition of production’ (Marx, 1973: 739). As providers of fixed capital, CWS generate a service essential to contemporary capitalist organisation and accumulation by offering physical space in which other individual capitals (individual entrepreneurs or firms) can work flexibly.

To generate a profit from the substantial outlay on the physical resource itself, these providers of fixed capital must commit themselves to the maintenance, management, and ‘sweating’ of their assets (Harvey, 1982: 395). In the case of CWS, the asset is a concrete space or premises which is embedded – literally ‘fixed’ – in the built environment of a particular location. CWS can be directly owned or leased; the latter raising additional questions of sharing potential profits with landlords and investors, sharpening the requirement to eke as much value as possible out of the fixed asset itself. The competitive pressures this induces mean CWS must maintain the economic viability of their ‘fee-for-service’ enterprise (Harvey, 1982: 227; Richardson, 2021). This implies that issues of rent relations, and the cost and terms of the leasing of space, sit at the centre of any material analysis of CWS markets. Crucially, CWS face the contradiction of being fixed in particular concrete places with long-term commitments to pay rents and loans, whilst depending on footloose users who are either: mobile – the entrepreneur who scales up in pursuit of expanded profits and graduates to another premises, or; flexible – the freelancer whose uncertain cycle of projects prevents durable commitment to taking a desk. This rolling turnover is one factor shaping the competitive environment within which CWS must operate, one that is also occupied by rival CWS seeking to valorise their space, whether leased or owned, and to realise a profit to be shared with owners or investors. CWS must also reproduce their conditions of profitability within a broader market economy comprising myriad producers all subject to the vagaries and risks of engaging in capitalist enterprise, for example, technological disruptions, macroeconomic downturns, or ‘exogenous shocks’ such as a global pandemic. These conditions mean the viability and profitability of CWS as providers of fixed capital is subject to broader political-economic dynamics and transformations, perceived as both ‘opportunities and threats’ (Antoniades et al., 2018).

Our conceptualisation of CWS is distinct as existing literature has tended to foreground typologies of CWS, categorising by location, user types and mission (Avdikos and Merkel, 2020; Bouncken et al., 2018; Madelano et al., 2022; Nakano et al., 2020), and how CWS generate communities of users. A key finding from the CWS literature is that CWS are different from any other form of managed office space because they deliberately seek to create and develop a community of distinct users comprising remote workers, freelancers, and digital nomads (Bouncken and Reuschl, 2018; Cabral and Van Winden, 2016; Clifton et al. 2019). Beyond this fundamental recognition is a sizable degree of debate regarding what forms such a community might take, although a common finding is that CWS communities comprise individuals who consciously seek to benefit from various forms of interaction, cooperation, collaboration, and knowledge sharing activities (Cappellaro et al., 2019; Constantinescu and Devisch, 2018; Sankari et al., 2018).

Much of the existing literature identifies CWS communities as being for broadly instrumental entrepreneurial ends (Bouncken et al., 2020a; Jamal, 2018; Kubatova, 2016), despite disagreements regarding the different kinds of communities they generate and support. Bueno et al. (2018) find a positive influence of social interactions in coworking environments on productivity, while other literature identifies the role CWS have in start-up ecosystems and cultures of innovative entrepreneurialism concentrated in urban centres (Bednár et al., 2023; Fraiberg, 2017; Gauger et al., 2021). Research on communities of practice can illuminate this further by theorising CWS as sites where users with shared concerns regularly interact, and in doing so form a particular domain, community and prevailing practice (Brown and Duigid, 1991; Wenger, 2011) which can advance both individual and collective ends. These communities of practice can also interact with each other across broader landscapes of practice (Pyrko et al., 2019) to achieve entrepreneurial aims. Not all research is unequivocally positive about the form work undertaken in CWS takes, however. Bouncken et al. (2020b) examine work satisfaction and feelings of empowerment and autonomy among CWS users, highlighting how communities can also foster ‘darker’ aspects of entrepreneurialism such as self-exploitation and distrust. Jakonen et al. (2017: 77) conceptualise CWS as ‘affectual assemblages’ that can flounder if individuals feel their sense of achievement is inhibited by being embedded within the community, while Waters-Lynch and Duff (2021: 396) argue, similarly, that many communities are characterised by ambivalence as users struggle to reconcile the ‘common atmosphere’ of CWS with its ‘enclosure and commodification … by way of a distinctive business model’.

Existing studies of CWS therefore illustrate different ways of understanding what goes on inside CWS by looking at users and communities, and therefore why their proliferation might be explained in terms of fulfilling various economic, social, and subjective needs on the part of individual users. This highlights one of the important reasons for developing a greater understanding of CWS as sites where often precarious workers and freelancers come together to engage in work and attempt to collectively resist changing work practices within such ecosystems, highlighting how CWS are a consequence of increased flexibility in the world of work (Manolchev, 2020). It is noteworthy, for instance, that around 25% of CWS users worldwide have reportedly had their fee paid by an employer (Bouncken et al., 2021), reflecting the growing tendency toward remote or hybrid working cultures even before the COVID-19 pandemic. CWS can also be used by larger companies seeking to co-locate their workers away from headquarters, viewing CWS as ‘an innovation stimulant, a recruitment venue, and a low-overhead location for temporary project teams’ (De Peuter et al., 2017: 691). Research also notes the shift towards enterprise tenants moving into existing CWS (Leclercq-Vandelannoitte and Isaac, 2016), giving rise to the term ‘corpoworking’ (Mayerhoffer, 2020: 209). These motivations have driven the growth of the UK CWS sector, and are explored in the findings section of this paper.

Prevailing business models in the CWS sector

Our critical political-economic perspective on inter-capitalist competition cautions that prevailing accounts of entrepreneurialism in the literature on CWS – which often celebrate the actions of small-scale market interventions by individuals or small teams – are limited. This stance stems from the awareness that, in competitive markets, increased rates of profitability have a tendency to be secured through the progressive concentration and centralisation of capital by individual capitals who can leverage larger economies of scale and more advanced organisational forms that enhance their efficiency (Harvey, 2014). This applies as much to independent providers of fixed capital, such as commercial real estate and CWS, as to any other producer of commodities.

Analysing the specificities and variations of CWS business models is therefore crucial to understanding how CWS seek to remain economically viable in urban environments characterised by competitive market conditions, such as the emergence of a wider range of CWS and the new spatial offerings in UK cities. The original CWS that were established in the 2000s were often small, independently owned or leased sites set up with the aim of providing aforementioned goals of shared rental costs and fortuitous work encounters within a community of users. While this business model continues to exist, the growth and uneven development of commercial property market dynamics in Europe and North America have seen CWS become increasingly subjected to market pressures (Capdevila, 2015; Renaud et al., 2019; Zukin, 2021). Some existing research has attempted to situate the development of CWS business models and strategies within competitive real estate market dynamics. Zhou’s (2018) account of the coworking sector in Manhattan, for example, foresaw a fall in demand for office space and thus rental yields that eventually were to create huge difficulties for CWS operators that took long-term leases with traditional landlords in the hope of being compensated by increases in user fees over the longer term. Green (2016) also examined New York’s CWS market and identified a differentiation of established commercial landlords’ strategies to maximise returns from their properties: by renting to other CWS managers; by entering the CWS market directly by subdividing existing premises; or by offering self-operating shared workstations within existing offices (2016:52-4). Saiz (2020) identified how CWS provision was becoming attractive for established commercial property landlords in the US who have recently adopted a range of new modes of leasing using ‘proptech’. These included a model in which underutilised space was ‘put to work’ as shared offices, which added to real estate cashflow but put them in competition with existing commercial real estate providers, as well as a model that offered ‘flexible space-time services’ to corporations, start-ups, and SMEs in the form of ‘short-term, simplified, all-inclusive leases’ (Saiz, 2020: 336). Landlords were also using a lease arbitrage model which allows for shorter-term leasing by financialised means. These different models raised landlords’ profit rates but rendered the inflow of short-term rents susceptible to recessions or other shocks. This supports Pajevic’s (2021) suggestion that, across North America, CWS have been appropriated as a lucrative business model and office real estate strategy’ (2021: 1), albeit with a ‘disruptive’ effect on flexible working cultures and practices as well as on traditional forms of office space leasing within urban economies.

Importantly, some research draws attention to how some forms of CWS are relatively more insulated from competitive market pressures and commercial real estate dynamics. For example, that which highlights how some CWS sites have operated to provide a particular social function, such as being sites where members of antagonistic communities can come together, for example, in Northern Ireland or Eastern Europe (Šebestová et al., 2017), or to provide spaces to support marginalised groups such as BAME or female workers who are more likely to be in marginalised labour market positions (Rodríguez-Modroño, 2021). These CWS are more likely to be funded by state, charitable or philanthropic benefactors, however, and as such are largely insulated from competitive pressures to remain profitable and viable. Another organisational form often classed as part of the CWS sector are business incubators and accelerators: sites where micro- or SMEs grow to scale with direct support from larger organisations such as venture capital, or institutional investors, meaning they are relatively more insulated from competitive market pressures and commercial real estate dynamics. The following section details our methodology and how we set about analysing different forms of CWS business models in the specific case of the UK.

Methodology and research design

Our research sought to explore the forms of CWS and their business models, paying particular attention to the interplay between how CWS operate (e.g. funding strategy, marketing/branding strategy, products/services offered, location) and the broader urban-economic contexts in which they compete. We conducted this research during the COVID-19 pandemic in 2019–21, with a focus on how lockdowns, social distancing protocols, and the widespread shift to emergency remote and hybrid working practices had impacted upon the daily operations of CWS, their prevailing business models, and their strategies for the short- to medium-term. Three English city-regions were selected as sites to analyse the UK CWS market: Brighton and Hove (B&H), Bristol (BR), and Greater Manchester (GM). These city-regions were chosen as recognised hubs of CWS growth and activity, which could make possible the identification of common attributes and dynamics, while being in diffuse geographical regions of the UK (being in the South, West, and North of England, respectively) and being varied enough in terms of population, market composition, and local economic output to generate interesting analytical insights. Greater London was excluded as a possible case study due to its unrepresentative size and weight relative to other cities and regions in the UK. City-regions outside England were excluded due to significant differences in local economic governance and of prevailing responses to the COVID-19 pandemic.

Data collection comprised semi-structured interviews lasting approximately one-hour with owners and managers of CWS, complemented by interviews with other key economic actors deemed to have expert knowledge of regional and local commercial property markets and of the role of CWS within them, such as local state officials. CWS were selected following analysis of secondary data and existing research on the number, type, and location of CWS in each city. Secondary data comprised descriptive statistics on the UK CWS sector, drawn from various sources including property and flexible office space sector trade publications, and NOMIS data. These data were not the main source of data for our paper, and therefore did not shape the categories used in our thematic analysis in any meaningful way.

A range of different types of CWS were approached to be interviewed. We conducted 44 interviews in total (20 in Brighton and Hove, 14 in Bristol, and 10 in Greater Manchester), and we spoke with operators of 23 separate CWS in total (10 in Brighton and Hove, 5 in Bristol, and 9 in Greater Manchester) (see Appendix). The interview recordings were transcribed and then systematically coded using Nvivo software, which formed the basis for subsequent analysis alongside our prior review of the existing literature on CWS. We had originally intended to collect further data via participant observation within CWS themselves, but this was prevented by the lockdowns and social distancing measures introduced during the pandemic. Restrictions on data collection freed up time and resources to produce an as yet unpublished systematic literature review of 212 papers on coworking and CWS produced in the period 2000–2022; this greatly expanded our knowledge of existing research and enhanced the theoretical and empirical foundations of our project. In October 2022, we convened a coworking stakeholder workshop at which we gained feedback on our research findings, and during which we were able to obtain further, updated testimony from several CWS operators based in the Brighton and Hove area. The remainder of this article details our findings.

Business models and competition in the UK CWS market before COVID-19

Our research discovered that there are three distinct underlying business models within the UK CWS sector.

Firstly, there are CWS that are funded by an external organisation or benefactor. One prominent example is a group of CWS sponsored by a prominent high street bank, of which there are presently 30 across the UK. These CWS receive direct funding from the bank and serve as incubators for start-ups and small businesses looking to benefit from the community effects afforded by coworking and from expert advice offered within the space – the ultimate aim for the bank being to secure loyalty and banking business in the longer-term, once these start-ups ‘graduate’ from the CWS (GM1). Other such CWS receive funding from external philanthropic and commercial organisations, as well as from institutions such as the European Union through its Regional Development Fund (now being wound down due to Brexit and replaced with the less substantial Shared Prosperity Fund) (B&H7). These CWS often admit users selectively according to a predefined mission such as promoting entrepreneurialism focused on digital social innovation, a particular sector (e.g. agritech), or supporting entrepreneurs from under-represented backgrounds. These CWS often operate in partnership with, and within office premises owned by, large commercial real estate landlords; an arrangement also commonly found outside the UK (Antoniades et al., 2018: 9).

Secondly, there are large corporate CWS which are owned and directly operated by office real estate landlords as a component part of their operational portfolio. A commercial real estate constructor or landlord will commit part of a new or existing building to a CWS, with scope for cross-subsidisation across the CWS and other forms of commercial space within their premises. Larger, corporate commercial landlords can operate multiple CWS in multiple buildings within a property portfolio spanning an entire city-region, or even multiple UK cities – the International Workplace Group (IWG), formerly Regus, being a high-profile example.

Finally, there are small, independent CWS operators who do not possess a diversified portfolio of commercial real estate. These operators may own the building in which their CWS is based outright, or else they might lease the building from a traditional landlord. These CWS must maintain a certain level of user occupancy based upon a calibrated pricing model, or risk going out of business as a CWS.

Given the somewhat unique character of the first model of CWS, and that these are largely insulated from competition so long as their long-term funding by an external organisation or sponsor is secure, we focus the remainder of our analysis on the second and third models (although testimonies from operators of the first model are used to provide insights regarding the UK CWS sector as a whole).

With the exception of a single operator, all the CWS in our study opened in the pre-COVID period. Prior to 2020, the UK CWS market was already characterised by intensifying competition in the city-regions we examined. Interviewees from each of the three cities noted that ‘the marketplace [was] so competitive’ (B&H1) and ‘competition was rife’ (GM2); however, interviewees generally characterised this period as one of an increasing number of new CWS market entrants, rather than in terms of having to deal with tighter margins or reduced profit rates. Interviewees attributed CWS sector growth in the UK to changing urban-economic dynamics in the aftermath of the 2007–8 Global Financial Crisis (GFC), which resulted in a glut of underutilised or vacant commercial office space in UK city-regions. Landlords sought to generate revenue from these spaces by converting them into CWS, or by renting them out to tenants looking to operate CWS. CWS were seen as viable businesses to establish in the post-GFC landscape because – as interviewees noted – they were quick to set up, required minimal resources and staffing, and could operate simple contracts for users, often on a ‘pay-as-you-use’ model wherein desk-space was rented on a daily, weekly, or monthly basis. CWS usage was also driven by the increased remote working facilitated by new technology and was promoted by firms trying to reduce overheads by downsizing their use of office space. The growth in freelance and self-employed work following the GFC also provided an enlarged customer base for CWS in urban areas. One CWS operator commented on the speed of growth and changing perspectives of CWS users in this period: ‘[there] was a generation [of users] demanding more flexibility and wanting to work that way … we were seeing the beginnings of “digital natives” where they’re far more used to this flexible work. So, I think [sector growth] was going upwards in a steeper curve … pre-COVID’ (BR13).

A CWS operator in Bristol claimed they could already see intensified competition on the horizon before the pandemic and, with it, the threat of strain on the sense of ‘community’ that had been cultivated between CWS providers in the city (BR6). They were not the only operator who characterised the pre-pandemic period of market growth as one of less intense, attenuated competition between CWS operators. Another invoked the idea of ‘collaborative competition’ (BR14) within local CWS markets, denoting how different CWS would compete with one another for users in a general sense, but also cooperate and share knowledge with one another in recognition of shared goals. Managers of CWS often met with other CWS operators, local financiers, council officials and local business organisations in formal and informal settings to discuss common issues, across all three city-regions. Collaborative competition went further than ‘coffee and croissant’ meetings (BR14), instead encompassed sharing expertise about prevailing market conditions, the optimal configuration of physical space and furnishings within CWS, and newly emerging CWS business models (BR17; GM5). During COVID-19, these interactions shifted online and tended to focus on ‘sharing approaches to health and safety’ and how to tailor spaces to the return of users as the pandemic waned (BR14).

Pre-pandemic, some CWS operators were already looking into the benefits of a ‘partnerships and sponsorships’ model as a way of growing the CWS sector (B&H8). This included partnering with other companies to manage their existing office spaces on their behalf, mitigating the risk of exposure to long-term leases on buildings by providing a new source of revenue through a coworking offer (B&H3). One CWS operator had consulted a leading tax accountancy firm who had recommended avoiding direct ownership of real estate and to focus instead on a ‘service over space’ model based on partnership with other commercial real estate landlords (B&H3). This model was also perceived as satisfying the needs of landlords themselves, who required some level of partnership to deliver effective management and operation of the spaces at their disposal (B&H4). Other kinds of partnership with organisations outside the coworking world included one operator who was exploring ways to ‘buddy up’ with commercial landlords with spare storage space to attract individual CWS users operating in the e-commerce sector who required access to warehouses to store stock (GM1). The same operator had explored partnering with a childcare provider to attract users with young families. Elsewhere, collaboration was further evidenced by onward referrals for new members who could not be accommodated in a CWS; one CWS in Brighton even created an area on its webpage recommending other CWS in the area that could absorb surplus demand for space (B&H5).

Collaborative relations within the UK CWS market in this period already existed between CWS and local state agencies, for example, with local authorities in Brighton and Hove (B&H10) and Bristol (BR1; BR2; BR10), and with related economic development agencies (B&H17; BR11). Strong collaborative links were especially evident in Greater Manchester, in which the role of the local authority and its arms-length development organisations such as the Manchester Growth Company and MIDAS (Manchester Inward Investment Agency) was stressed in multiple CWS interviews (GM2; GM8). One Bristol-based CWS manager who was opening another branch in the northwest explained: ‘Manchester [council] are brilliant, they’re … really forward thinking in their approach to business, it’s entrepreneurial … you do need that kind of regulatory [support], you need someone to be thinking a bit more progressively…that’s what we find in Manchester’ (BR7). However, there were undoubtedly differences in the degree of institutional thickness between city-regions, with Brighton and Hove arguably showing less cooperation and coordination between local government and CWS operators.

COVID-19, accelerated change, and shifts in CWS business strategy

The lockdowns and social distancing protocols introduced in the wake of the COVID-19 outbreak in 2020 severely disrupted the operations of CWS in all three city-regions we investigated, prompting some CWS to operate on a limited basis with fewer users and enhanced health and safety measures, or, in most cases, prompting CWS to temporarily shut their doors to all users (sometimes offering services for their user communities online) (Pitts et al., 2020). The inability to organise, and thus make money from, in-person events was described as the ‘biggest hit’ taken by CWS operators during the pandemic (BR1). Many CWS echoed this sentiment but were also using enforced closures prompted by lockdowns as an opportunity to refit, expand or reconfigure their existing space, with an eye on remaining attractive to users beyond the pandemic (GM3; GM5; B&H6; BR7). Even a CWS that had reported rates of profit between 30 and 40% (GM2) was using the COVID-19 lockdowns as an opportunity to remodel space.

Larger corporate providers, for whom CWS are one part of their property portfolio, were acutely aware of the impact of the pandemic on their business model, and could instantly account for profit and loss: … occupancy is always key. So we're always aiming for around 80%. After 80%, every additional percent is £100,000 profit, every percent under is a £100,000 loss […] And because we provide short term, three months, six months, 12 months, up to 24-month contracts, the majority of my portfolios came up for renewal within the pandemic […] It's been a drop of about 12% in occupancy since April last year. And we run our financial year, October till October, I had a 6% drop since October. (GM6)

CWS in other city-regions also reported similar immediate impacts on profitability (B&H1; B&H6; BR14). Even so, larger CWS were able to remain open as they had the resources to rapidly adapt to, or demonstrate immediate compliance with, government-mandated health and safety measures (e.g. by already having HVAC systems installed in their premises) (GM5).

Smaller, independent CWS were more likely to close down operations during the pandemic due to resource constraints (GM4). The owner of one smaller CWS noted that the responses available to individual providers were largely ‘dependent on whether they own the space, how much debt they’ve got, who they owe the money to, and whether that creditor is lenient, or strict’ (BR3). Some of the smaller CWS that used the pandemic to remodel or upgrade their space did so by taking on additional lending (BR6) making use of government schemes, such as furlough, where relevant. Smaller CWS also relied on landlords providing payment holidays, or they drew on their own capital reserves if they owned their promises outright. One potential method of staying afloat during the pandemic consisted of taking a business loan on a lower interest rate than a commercial loan and then using it to take on leases, after which the leased premises were ‘chop[ped] up’ into desks or offices and then rented out to individual tenants or companies (B&H3). Some CWS reported taking loans from investors and local state organisations (e.g. B&H7). However, these lines of credit and debt were not always easy to secure. One smaller CWS reported how a major investor had to ‘bail out’ a CWS in Brighton that had made a substantial outlay on a new premises and, in attempting to recoup the costs, had charged rates that were too high to guarantee necessary occupancy rates (B&H13).

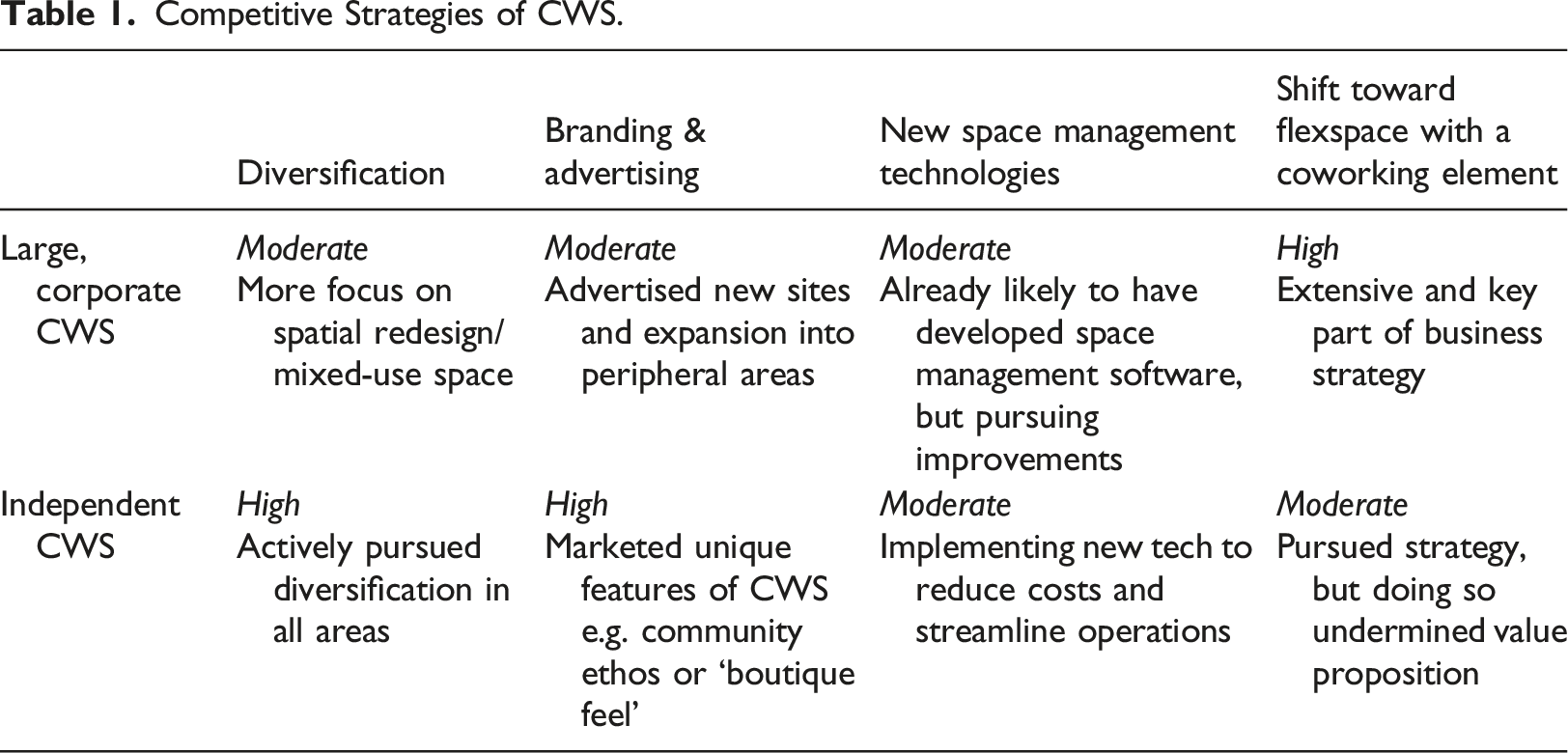

Adapting competitive strategies

Competitive Strategies of CWS.

The first strategy was diversification of coworking activities. Many of the CWS we examined were looking to diversify the range of services and activities they provide to users, such as new methods of hosting events and other related forms of community-building activities.

Both large, corporate CWS and small, independent CWS sought to diversify, with similarities and variations in terms of strategy. Smaller, independent CWS were found to be more active in pursuit of diversification in a manner which attempted to align it with the ethos and values of their CWS, so as to bring their communities along. Smaller CWS continued to ‘supplement their income’ via events, conferencing packages and meeting room hire (BR1, BR2), each of which enabled CWS to compensate for fluctuations in occupancy (BR14). More than one interviewee noted a tension between some CWS managers’ commitment to helping grow users’ businesses, and other CWS managers who seemed to be more concerned with ‘socialising and events’ (B&H1) or ‘free beers on Friday’ (GM4). Most spaces sought to diversify by organising events for public audiences beyond those who used the space on a daily basis, including those geared towards bringing in outside speakers and experts to aid users with the growth of their companies (GM6).

The capacity for CWS to diversify their activities by reconfiguring their premises was aided by UK government legislation permitting new routes through the planning process for those operators seeking to change the use of properties towards a mix of purposes. ‘Use Class E’ permitted development rights, introduced in September 2020, allowed for new forms of mixed-use real estate development. These have been more beneficial to larger, corporate CWS and have made ‘the possibility of having a yoga studio and a café and a coworking space all in the same building’ more viable for UK CWS, so ‘you don’t need to jump through hoops at the local authority’ (B&H6).

A second strategy on the part of independent CWS emerging from the pandemic saw shifts in approaches to branding and advertising. Again, similarities and differences of approach were found based on the CWS business model. Larger CWS focused their branding on the promotion of their increased size and future expansion, while smaller, independent CWS publicised the unique character of their space and were keen to promote their ‘value proposition’ for users (the value-added offered to targeted users at a cost over and above bottom-line operating costs) by assertively promoting the additional services they are offering to curate a community or to provide business expertise to users, as well as in the aesthetic of particular spaces themselves (a ‘niche’ or ‘boutique feel’, for instance). Smaller CWS operators were sensitive to the need to brand their business and to offer a value proposition that other forms of commercially available office space could not provide. Such branding often tapped into the ethos of community and shared values that is supposed to define the coworking movement, as one small CWS manager noted: ‘when [users] hear about us and what we do, and how…our values align with theirs…that’s [when] they go, “Oh, actually, yeah, there’s something better [here] than the standard corporate office”’ (BR13). One operator even reduced significant differences between large flex-office space providers and CWS to semantics: ‘you can really tell which companies are which because people who are coworking people spell it “coworking” and people who are [flex-spaces] call it “co-hyphen-working” as in, “that’s my co-worker, not [we are] coworking”’ (BR4). This stress on the value proposition of coworking could be attributed to what several independent CWS saw as an incursion into the UK CWS market of larger providers with bigger budgets and more developed and refined marketing expertise. One CWS, for example, commented that: ‘there’s been a huge uptick and spend on things like social media ad [vertising], for example’ (BRI14).

Larger, corporate CWS were also engaging in new branding exercises tied to their expansion outside of city-centre settings, reflecting the increasing competitive pressures in the CWS market (GM1). While branding campaigns by expanding larger corporates were found not to impact significantly upon CWS with external funding (GM3; GM8), some smaller, independent CWS were responding by doubling down on their commitment to a small-scale, community-focused model (e.g. B&H1; BR18). As one CWS manager explained: We know we will never compete with WeWork and we're not trying to be WeWork. In fact, we're probably trying to do the opposite…WeWork were a bit of a global corporation and they'd received sort of bad press … people wanted to distance themselves … they were looking for something a little bit more unique … where they would be treated as an individual rather than a number on the desk. (GM10)

A third competitive strategy deployed by an increasing number of CWS involved the introduction of new space management technologies within CWS. Both large and small CWS sought to implement new software solutions such as web portals and booking calendars to aid the efficiency of the management of online bookings and membership administration beyond the pandemic (BR13; GM4), and to optimise revenue through dynamic pricing software. Larger, corporate CWS, however, were found to be more likely to have technology embedded in their operations as a result of managing a broader portfolio of spaces (GM3). One small CWS recognised that to remain competitive, automated processes may have to be introduced as a lower cost alternative to hiring more staff: We have to … move with the times and get the suitable equipment in place … you don’t want to have it too labour intensive, because obviously, we want to kind of keep the desks relatively cheap. But if you’re keeping them cheaper, and… therefore affordable for people, we’ve got to make sure that we’re not…pushing our overheads massively high by having lots of staffing costs behind it. (BR13)

These new technological solutions can be bought in from third-party software companies, and we interviewed the developer of a relatively new platform that uses real-time data to offer CWS managers suggestions on a range of operational, cost-saving tweaks to their model, from deploying cleaning staff, to booking meeting rooms, to monitoring and administering membership ‘churn’, and to optimising the use of physical space given social distancing protocols – all viewable through a dashboard interface (B&H10). One CWS owner was actively marketing their own proprietary CWS management software to other CWS throughout the UK, with a view to meeting the increasing demand for fully automated, unstaffed CWS at sites outside city centres where profitability will likely depend on a ‘skinnier’ operating model (BR6).

A fourth, significant shift in the competitive strategies of UK CWS beyond the pandemic has seen a widespread shift to a market offer based on what we term, flex-space with a coworking element, and with this a recalibration of pricing models. This strategy – utilised mostly by larger, corporate CWS - refers to how large commercial real estate developers and providers with multiple premises in the city-regions we studied, together with corporate CWS who themselves lease buildings from large commercial landlords, are now offering more flexible and shorter-term leasing pricing packages to ‘enterprise clients’ in office buildings increasingly marketed with an explicit coworking branding and complete with services, facilities and aesthetics usually associated with small CWS and not with traditional office spaces (GM1; BR7). One interviewee working for one such corporate CWS provider explained how: We don’t necessarily use the term ‘coworking’ anymore … the term we use more is ‘flexible working’ … And the reason for that … is that we’re in that space in between coworking and [enterprise clients] … We find [enterprise clients] love everything about coworking, but obviously they need to do it within their own terms: i.e. they might require certain privacy [and] security measures against technology abuses. (GM4)

Smaller CWS operators see this incursion by large commercial real estate developers as a threat to what they see as the CWS sector proper, based on an authentic coworking and community-focused offer for traditional users within the CWS market. One small CWS stated: ‘there is still an enormous amount of new spaces being planned to open in the next few years. And some of them are by much larger developers [who are] looking at it in terms of mixing big traditional office space with some coworking thrown in … to make sure they can get [access to] the flexible space market’ (BR14).

The expansion of large commercial flex-space providers within the UK CWS sector is one of the key findings of our research. It has been driven by a decline in commercial clients taking out traditional leases on office space typically lasting five to 10 years during the period since the GFC and the post-Brexit referendum downturn in trade-related economic activity. This decline has been accelerated by the 2020 pandemic and the anticipated shift to more hybrid working practices and cultures, and in this context many larger office space providers have moved to offer flex-space with a coworking element.

This trend has placed fresh pressures on CWS pricing across the UK CWS sector, particularly for smaller CWS. Multiple CWS operators discussed operating costs and margins with us, revealing the intricacies of pricing as well as the tendency for prices to be equalised across the market – a sign that the CWS sector in these cities, and the viability of individual CWS within it, is regulated by a prevailing rate of profit, as we theorised above. One smaller CWS operator noted: 50% of our revenue comes from the private offices, 25% of it comes from coworking, 25% comes from events, café [sales] and any additional sales. And if our offices are full, that covers everything, and then … everything else is basically profit … And we also oversell, so if you've got 50 spaces in a CWS, then you can sell three memberships per space … when it comes to pricing pretty much every single CWS [in our locality] that has come after us has copied our pricing model. (B&H4)

A pressing challenge facing CWS managers stemmed from the ‘pay-as-you-use’ pricing model operated by most CWS prior to the pandemic. This model was popular with individual users but did not provide ‘surety of income’ (GM5). This income insecurity was a reason why CWS are increasingly compelled to seek out larger, ‘enterprise clients’ who might co-locate entire teams within a single CWS, even taking up whole floors, and with a branding strategy aimed at developing this flex-space with a coworking element model. A mid-sized CWS owner commented on how: I [now use] the [phrase] ‘coworking and flexible office’ … I think [it is] very, very challenging, without any funding, without any support to make that business model of pay-as-you-use … community focus[ed] CWS work … [so] I deliberately push ‘flexible space’ down here, because that's what we want people to come in [to]. (B&H6)

CWS have developed new pricing packages for enterprise clients looking for flex-space with a coworking element, often alongside traditional individual users’ pricing models (GM2), leading to even more aggressive forms of pricing competition (BR14). One CWS owner described their changing strategy in terms of operating in the ‘sweet spot’ between a certain rate of occupancy charged on a flexible pay-as-you-use CWS pricing model and an enterprise client occupancy rate based on a longer-term office space-leasing model (GM5). Larger, flex-space providers also use new streams of revenue from enterprise clients to cross-subsidise discounted prices for individual or early-stage start-up users (BR7). However, this dual pricing strategy is challenging for independent CWS operators who could not cross-subsidise their CWS offer in such a way (GM10; BR13). These smaller CWS also need to grapple with the dilemma of whether to pass on rises in rent, energy, and business rate costs to users – a dilemma that has worsened in the high inflation period beginning in 2021. Some interviewees, moreover, expressed fears about the survival of other CWS that were locked into longer-term leases that precluded the possibility of competing with new pricing strategies and discounted fees for individual users in such a febrile market (BR2; BR6).

Conclusions

Our research suggests that the concept of coworking, and therefore of the CWS itself, is not necessarily the optimal starting point from which to reach an understanding of how this sector operates. Rather, our research has focused on how different forms of CWS with different underlying business models compete for users in a fast-changing CWS market. We have acknowledged how users of CWS can indeed be individuals and entrepreneurs in search of some sense of shared community, as tends to be assumed within the literature. However, we have also illustrated that CWS are increasingly competing to attract enterprise clients looking for shorter-term, flexible office space leases, or to establish new working arrangements fit for the apparent transition to remote and hybrid forms of team-work – these trends having been accelerated by the COVID-19 pandemic. These developments have intensified competition within the UK CWS sector, prompting CWS to adopt new strategies to reproduce their competitiveness and viability in difficult circumstances, based on a combination of diversification of activities, shifts in approaches to branding and advertising, the introduction of new space management technologies, and, for larger CWS, the offer of flex-space with a coworking element. Our findings have illustrated the impact the latter strategy is having on the rest of the CWS sector. Both corporate and independent CWS are pursuing this approach, although the former are able to better leverage economies of scale and scope to achieve it, pointing to a tendency toward the concentration of capital within the CWS sector. This tendency highlights the limitations of understanding the significance of CWS in terms of their place within ecosystems of innovation, catering to the needs of individual entrepreneurs or digital nomads, and as curators of community. The fragmentation and differentiation of the CWS market, and its recomposition in an increasingly concentrated and competitive form, should instead be seen in the context of material dynamics associated with capitalist political economy. These centre less on the pursuit of innovation and community alone, and more on the underpinning pursuit of profitability.

A key question for the future of coworking is the extent to which these dynamics can continue to coincide with the virtuous cycle the literature sometimes posits between community and innovation. In the post-pandemic context, it is becoming more difficult for CWS providers who lack the financial independence to withstand increased competitive pressures, or for those who are unable to compete by means of diversification, discounted fees, or cross-subsidisation, to remain viable as businesses. Faced with increasingly stiffer competition from larger commercial real estate landlords entering the market, as we suggest is now the case in urban CWS markets in the UK, smaller CWS operators must adapt. CWS must be willing to innovate and diversify, to seek out whatever competitive advantage they can, or find some other means of compensating for their failure to remain profitable (through borrowing or through cross-subsidisation from other assets or sources of revenue); the alternative is closure and liquidation.

One risk for smaller, independent CWS, therefore, is that they will increasingly come to resemble flex-space providers as they are compelled to give over more of their premises to attract enterprise clients. This shift mitigates the uncertainty of pay-as-you-use pricing for small CWS, but it implies – if not necessitates – the erection of office partitions or the apportioning of entire floors within CWS to just one enterprise client. This outcome contradicts the original value proposition of coworking, based on the cultivation of community for otherwise isolated individuals in search of serendipitous encounters, knowledge-sharing opportunities, and social capital. This finding also highlights the problems facing CWS stemming from their position as immobile providers of fixed capital in a context where increasing numbers of entrants to the sector act to dilute this original value proposition.

Another risk is for UK city-regions more generally: namely, that the continued growth of larger providers offering a flex-space with a coworking element contributes to pre-existing dynamics of uneven urban development and unequal access to services within cities dominated by private commercial enterprises and institutional financial investors. Coworking, and the CWS that hold fast to its ethos, can offer much to users as bases for community formation and as remedies to social isolation, as well as to city-regions as contributors to the tax base and as sites of skills formation. To achieve these outcomes, however, CWS must remain viable as business in an increasingly competitive economic sector, and against a macroeconomic backdrop of increasing inflation and a longer-term failure by the central state to engage in proactive industrial planning for UK city-regions (Evemy et al., 2023; Yates et al., 2021).

Positively, there are indeed signs of resistance to these pressures on the part of independent CWS managers who are doubling down on the coworking concept and traditional business model even in the face of stiffer competition (Gandini and Cossu, 2021). It does, however, seem unlikely that there will be a return to the pre-pandemic context of attenuated competition within a CWS market as traditional office leasing arrangements become a thing of the past. The changing nature of competition within the UK CWS sector will therefore continue to warrant close attention.

Finally, the case of CWS shows the pressing need to contextualise within a broader set of political-economic dynamics the sometimes-hyperbolic claims about the future of work that today arise around highly specific experiences of workplace change (Cruddas and Pitts, 2020; Yates, 2022). Our study suggests that shifts in the locations, technologies, and practices of work do not erupt discontinuously from crises or sudden transformations in individual, collective, or managerial approaches to employment, but rather represent the mediation of longer-standing tendencies and contradictions in capitalist accumulation. Notably, we refer here to the power of larger capitals to enter into a new economic sector and out-compete or absorb the original enterprises within the sector, thereby undermining opportunities for genuinely new and progressive spaces and forms of work to develop. However, much seemingly epochal events like COVID-19 produce compelling stories about the evolving world of work, the superficially novel behaviours and business models that they appear to incubate cannot in and of themselves accomplish durable or meaningful changes in the objective requirements of capitalist reproduction. The case of UK CWS reveals how unfolding futures of work are both conditioned and constrained by the underpinning compulsion facing enterprises to both thrive and survive within – and sometimes against – competitive pressures.

We acknowledge our study has some limitations, notably the exclusive focus on the UK, the number of case study cities, and the primarily qualitative nature of the research. However, these elements can also be conceived of as the basis for a future research agenda, one which should include the exploration of CWS in other national contexts, including across the Global South, and a deeper analysis of the mechanics of property ownership, rental incomes, and the financing of CWS within those specific locations. This final element is often deliberately opaque and operates in a manner which benefits finance and rentier capital to the detriment of wider society. If pursued, this future research agenda will strengthen the scope for resistance and alternative forms of spatial arrangements in capitalist society more broadly.

Footnotes

Acknowledgements

We would like to thank Professor Jason Heyes for comments on an earlier version of this draft.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by an Economic & Social Research Council Digital Futures at Work Research Centre (ESRC Grant Number ES/S012532/1) research grant. This research also received funding from the Society for the Advancement of Management Studies (Early Career Researcher Engagement and Development Funding), and from The University of Manchester School of Social Science (Small Grant).