Abstract

In the 1980s, successive Australian governments began to pursue a program of microeconomic restructuring, taking their lead from the developing ‘free market’ reform projects underway in the United States and the United Kingdom. One of the prominent features of the emerging liberalisation agenda was the commercialisation and privatisation of government-owned companies and assets. In keeping with this trend, over the following decades, a series of changes have been introduced to Australia’s container ports aimed at improving their productivity and efficiency. Drawing on a series of interviews and analysis of governmental and non-governmental reports, the purpose of this study is to examine how port policy has unfolded ‘on the ground’ in Australia. The paper considers some of the ‘common sense’ economic maxims expounded for reform in relation to actual outcomes for industry stakeholders, concluding that principles and practice have diverged significantly and that many of the assumed benefits have failed to materialise.

Keywords

Introduction

In the early 1980s, successive Australian governments began to pursue microeconomic restructuring in the shape of deregulation, tax reform, privatisation, and labour market reorganisation, referred to as the turn towards ‘economic rationalism’ in Pusey’s (1991) seminal research. The momentum for this came from the developing political and economic reform agenda in the United States and the United Kingdom, which incorporated the rising primacy of ‘free market’ economics as part of a sea-change in mainstream western political orthodoxy, now commonly (though contentiously) described as the emergence of neoliberalism (Barnes et al., 2018; Cahill, 2007). In Australia, the Hilmer, 1993 provided further impetus for reform and one of the prominent features of unfolding economic liberalisation policies was the transformation of key sectors and industries where the state had previously played a role. Commercialisation and privatisation of hitherto government-owned entities became politically paradigmatic and thereafter the dominant wisdom among policy makers was that ‘everything feasible should be privatised’ (Hilmer quoted in Coorey and Khadem, 2014). This program extended to utilities (Chester, 2015), prisons (Love et al., 2000), airports (Graham, 2011; O’Donnell et al., 2011), roads (Cardew, 2017), telecommunications (Walker and Walker, 2000), banks (Fairbrother et al., 1997; Quiggin, 2001), and even national heritage areas (Darcy and Wearing, 2009), becoming the subject of much academic attention.

The political justifications for commercialisation and privatisation have remained unchanged since their emergence as hegemonic economic policy in the 1980s and 90s, centred around principles of efficiency. For example, the premise that private entities are always more efficient than public ones because of market pressures and the discipline they apply; that competition always results in increased efficiency; that the efficiencies gained from privatisation/increased competition will lead to lower prices and enhanced services for users and consumers. Budgetary reasons are also pontificated – that funds derived from the sale of state-owned assets represent value for money for the public purse and reduce government debt/interest repayments or increase credit worthiness; that funds generated from sales would be better spent on alternative projects, usually new infrastructure (Aulich and O'Flynn, 2007; Letza et al., 2004; Quiggin, 1995; Walker and Walker, 2000). However, evidence from some industries in Australia, and those in similar countries across the world, have demonstrated that these assumptions are often driven by ideology and can be problematic if reform is not managed carefully (see, for example: Araral, 2009; Bowman, 2015; Letza et al., 2004; O’Donnell et al., 2011; Von Weizsacker et al., 2006).

In keeping with the trend towards economic liberalisation, since 1989 a series of changes have been introduced to Australia’s container ports aimed at improving their productivity and efficiency. Ports are a fundamental node in national trade infrastructure, particularly important for an island nation such as Australia. In fact, 99% of Australia’s trade depends on sea transport, and between 2017 and 2019 the combined value of Australia’s seagoing international imports and exports was over $600 billion (Australian Naval Institute, 2020). While the earliest reforms were aimed at workforce and labour process rationalisation, the most significant contemporary developments have involved the construction of new terminals and introduction of additional stevedoring companies at existing container ports with the intention of encouraging greater competition (and concomitantly improved efficiency), alongside the long-term lease of responsibility for port administration through the privatisation of port authorities. From a market standpoint, one of the key issues with the privatisation and commercialisation of ports more broadly surrounds the existence of a natural monopoly at the port authority level and potential monopoly or duopoly at the cargo-handling (stevedoring) level, with implications for prospective rent fixing and price gouging by incumbents. Port reform needs to be managed prudently to ensure that political expediency and private profit do not take precedence over sustainable growth and economic benefit to the community, industry and national economy at large.

To these ends, the purpose of this study is to examine how container port reform in Australia has unfolded ‘on the ground’. It considers some of the moribund justifications expounded for reform in relation to actual outcomes for industry stakeholders, ranging from port authorities to stevedores, haulage companies to port workers, and exporters to consumers. While detailed analyses of developments at Australia’s major container ports have already been partially provided elsewhere from a port administration or governance perspective (see, for example: Chen et al., 2017; Everett and Robinson, 2006), there is a distinct lack of commentary on how successful these have proven, and less still on the repercussions for industry stakeholders (Vaggelas, 2019).

The empirical research for this study is based on a series of in-depth interviews with various stakeholders and analysis of government, regulator and non-government reports relating to developments in the Australian port industry. It concludes that the principles and practice of reform have diverged significantly and that many of the assumed benefits have failed to materialise. Before a narrative and analysis of these developments is presented, attention should turn to a critical exploration of the provenance of the ‘common sense’ market-related discourses that underpinned the policy decisions of state and federal governments alike regarding container port reform in Australia.

Common sense economics? Competition, privatisation and efficiency discourses

‘Neoliberalism’ is a controversial and nebulous term describing ‘an oft-invoked but ill-defined concept’ (Mudge, 2008: 703). It was originally coined to articulate the profound changes occurring in the political and economic orthodoxy of developed nations from the late 1970s onwards but has evolved to become a contested terrain with varied subjective meanings, encompassing everything from a program of global capitalist hegemony at one extreme to a thought abstraction or conspiracy theory at the other (see, for example: Castree, 2006; Dunn, 2017; Mirowski, 2018). Notwithstanding the controversy and complexity surrounding neoliberalism as a metanarrative, or even a definable concept, it is difficult to deny that certain economic maxims dominate the political economy of developed (and developing) nations, and that these stem principally from neoclassical economics.

The theories of efficient markets and general equilibrium that underpin neoclassical economics stress the folly of government interference and the importance of the unfettered ‘invisible hand’ of market forces in driving economic growth and moderating human behaviour. These ideas have gradually proliferated through right-leaning think tanks, consultancy firms, and supra-national monetary institutions such as the World Bank and the IMF, to become elevated to the status of an unquestionable wisdom about the nature of the economy and, indeed, society. This neoclassical ‘common sense’ (Fisher, 2009; Hall, 1979) comprises a bundle of ‘widely held beliefs – about the benefits of unfettered markets and the dangers of interventionist states, about the importance of market competition and ‘competitiveness’, about the necessity of liberalising reform’ (Schmidt, 2018: 69). A process of ‘policy contagion’ has cascaded into ‘an adaptive matrix of market-oriented and pro-corporate regulatory norms’ and the ‘colonization of commonsense understandings’, crowding out alternatives (Peck et al., 2018: 4–5). Attempts to challenge this status quo draw accusations of returning to ‘the bad old days’ of inefficiency, sluggish or flat growth, and disproportionate worker influence in organisations (Taylor and McDonald, 2022). As Cahill and Humphrys (2019) and Humphrys (2018) have documented, these precepts cut across the political spectrum in Australia, and elsewhere, to become an almost universally accepted economic model.

Many of the assumptions that underpin these dominant neoclassical discourses exist only in an idealised abstraction of how ‘the market’ should work. In reality, practice and principle often diverge significantly. Privatisation is one of the hallowed tenets of modern political and economic discourse, deemed to be intrinsically positive. If approached in a pragmatic manner, where the merits are carefully considered on a case-by-case basis, some public assets or companies might benefit from being run on a more commercial footing by a private entity, primarily in terms of profitability (Dewenter and Malatesta, 2001). However, such is the pervasive nature of the prevailing orthodoxy, privatisation is often overtly systemic in nature (Aulich and O’Flynn, 2007), adopting an approach which is ‘less about the genuine application of the economic theory of efficiency, but more about winning a political and ideological struggle’ (Letza et al., 2004: 160; see also, Knafo et al., 2019). There is also related controversy surrounding how public assets are valued prior to sale. Quiggin (1995: 23) has argued that future returns are extremely tricky to calculate, and that undervaluing is endemic, tantamount to ‘selling the family silver to pay the bills’. Asset pricing has proved a topic of some controversy in Australia where the federal government previously encouraged systemic privatisation by offering asset recycling premiums to state governments, with ports a particular target (Al-Daghlas et al., 2019; Richardson, 2015). 1

Underpinning the ‘private good, public bad’ dichotomy is the idea that the private sector is always more efficient than the public because of market forces, ‘ownership and efficiency outcomes are perceived to be inextricably linked’ (Everett and Robinson, 1998: 41, emphasis their own). Conflation of mode of ownership with efficiency is subterfuge, however – private companies, like their public counterparts, can also be run inefficiently. There is significant debate amongst academic economists whether, where market forces are brought to bear and the broader economic climate is considered, ‘government firms are intrinsically no less efficient than private firms’ (Dewenter and Malatesta, 2001: 320; see also: Letza et al., 2004; Martin and Parker, 1995). Moreover, in a sector such as the port industry, where a monopoly is virtually unavoidable at the port authority level and accompanied by the opportunity for possible vertical integration into cargo-handling duties, privatisation of the port authority function, if introduced, needs to be properly managed and regulated. Indeed, even the most strident exponents of free market economics caution against the ‘evil’ of a private monopoly (Friedman, 1982: 31).

Competition is another defining discourse of the market liberalisation model, usually credited with forcing efficiency upon market players. However, while competition ‘might be viewed as an ideal that emanates from the market, it is not something that real-world markets will safeguard if left to their own devices’. Businesses, individuals and entrepreneurs ‘are just as likely to form cartels, avoid competition or seek to suppress it, and this provides the state with an important regulatory and legal function’ (Davies, 2018: 276). Yet, despite the potential anti-competitive tendencies of market players, regulation is often juxtaposed as antithetical to efficiency (O’Keeffe, 2018; see also: Hilmer, 1993; McKinsey Australia, 2014). This has special implications for the container port industry, where duopolistic cargo-handling arrangements have historically prevailed and difficulties in fostering meaningful inter- and intra-port competition are commonplace, particularly in a geographically dispersed country such as Australia. Regulation has been conspicuously lacking as a counterweight to the market power of privatised port authorities and stevedoring incumbents at Australia’s container ports and the implications of this are discussed throughout the paper.

Both privatisation and competition are regarded as levers to increase efficiency in a sector or industry, with gains passed on to the consumer, or resulting in some broader benefit to the economy and society. However, using a stakeholder perspective, some commentators challenge the efficiency paradigm as fundamentally good. Pusey (2003) has highlighted that policies undertaken in the name of efficiency have undermined, rather than improved, the wellbeing and living standards of middle-class Australia. Beer et al. (2016) argue that worker protection and job security have suffered generally because of cost savings related to efficiency gains in organisations, while O’Keeffe (2018: 29–30) contends that, far from adding value beyond the organisation to the general public, efficiency is ‘pursued in spite of society’ and is often detrimental to ‘the needs and values of its citizens’ (emphasis their own). In relation to this study, there are serious questions surrounding whether the neoclassical dictums that have driven container port reform in Australia have benefitted consumers at all.

The contradictions apparent in the application of contemporary market-led economic theory to real-world situations are often characterised by ‘discrepancies between the utopian idealism of free-market narratives and the checkered, uneven, and variegated realities of those governing schemes and restructuring programs variously enacted in the name of competition, choice, freedom, and efficiency’ (Peck et al., 2018: 3). Such is the deviation between theory, practice and outcomes that a cadre of IMF economists recently declared that policymakers ‘must [now] be guided, not by faith, but by evidence of what has worked’ (Peck, 2018: xxiii; see also: Colford, 2016). This study seeks to examine the veracity of these deified and uniformly applied economic maxims in relation to developments in the Australian container port industry. It will emphasise that port commercialisation and privatisation in Australia has been pursued in a systemic and ideological, rather than pragmatic, manner (Aulich and O’Flynn, 2007), resulting in a series of undesirable consequences.

Method

Documentary data analysis

The data for this study was collected from two main sources. Firstly, publicly available reports concerning port and related infrastructure reform in Australia were identified and collated. These were produced by various government and non-government organisations such as the Australian Competition and Consumer Commission (ACCC), the Bureau of Infrastructure, Transport and Regional Economics (BITRE), the Productivity Commission, trade unions, haulage associations, and state governments, as well as the mainstream press. 2 Reports were analysed and coded using a qualitative approach to content analysis, and a ‘directed’ approach was employed ‘to validate or extend conceptually a theoretical framework or theory… thus helping to determine the initial coding scheme or relationships between codes’ (Hsieh and Shannon, 2005: 1278–1281).

Each of the data sources was analysed with the aid of the qualitative software NVivo, which was programmed to search for key words and their synonyms. NVivo produced hundreds of phrases and sentences with these terms, which were then manually sorted and prioritised. The outcome of this process was a series of themed statements that most clearly and concisely represented container port reform from a range of stakeholder positions at the institutional, port authority, and land-side user/customer levels.

Semi-structured interviews

The second source of data came from eighteen semi-structured interviews conducted with stakeholders from the port transport industry in Australia. Stakeholder categories had been established through the analysis of relevant documents in stage one and included representatives from port authorities, haulage companies, importers/exporters, and union officials/delegates. Once ethics approval had been obtained from the lead author’s institution, potential participants were invited via email, except for union participants, who were recruited through existing contacts within the Maritime Union of Australia (MUA). Between 2019 and 2021, interviews were conducted with stakeholders, comprising port management (4 interviewees), port workers and their representatives (6 interviewees), haulage company representatives (5 interviewees) and importers/exporters (3 interviewees). This covered almost all categories of industry stakeholders, except for stevedoring companies, who refused several invitations to participate. 3 Interviews were conducted face-to-face in some cases and via video conferencing in others, usually lasting around 1 hour. The purpose of the interviews was to ascertain what effect port reform has had on the stakeholder’s business or interests. Each of the interviews was audio recorded and then transcribed for later evaluation in relation to the themes which emerged from the documentary analysis.

Port restructuring

International trends

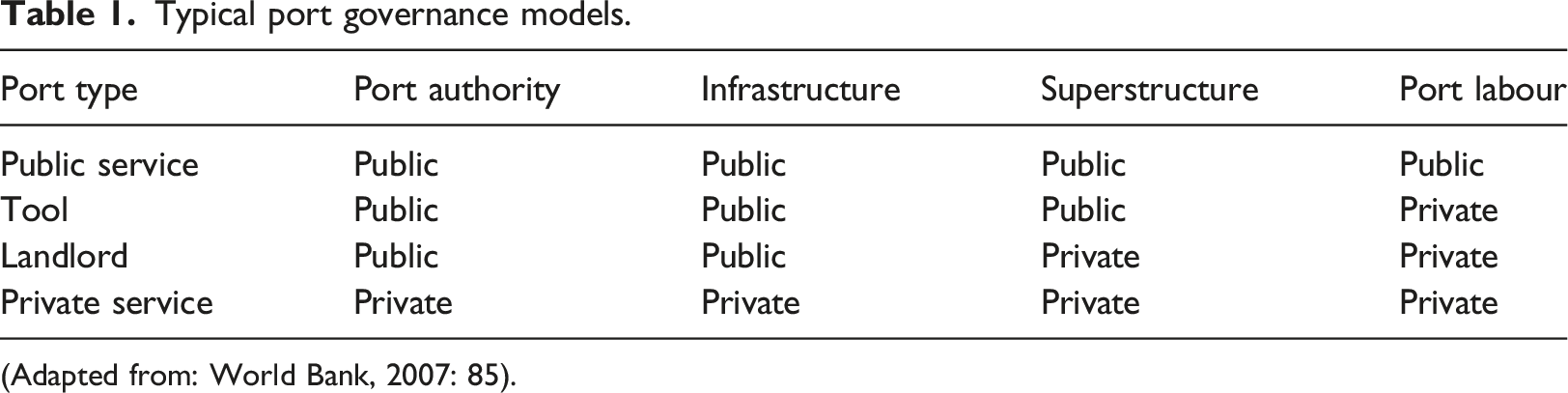

Typical port governance models.

(Adapted from: World Bank, 2007: 85).

Turnbull and Weston’s (1992: 403) comparison of major European ports observed that developing a ‘complementary system of employment regulation and state intervention generated a virtuous circle of industrial concentration, employment security, economic growth and greater economic efficiency’, suggesting that an unfettered free market approach is unsuitable for the sector, regardless of geographical location. Attempts to liberalise and further commercialise cargo-handling in Europe, under the auspices of the Port Services Directives in 2003 and 2006, were ultimately unsuccessful because of opposition from some sections of stakeholders (Pallis and Tsiotsis, 2008; Turnbull, 2006, 2010). In New Zealand, the standard-bearer of efficiency as far as Australian policy makers were concerned (Productivity Commission, 1998), a model has eventually emerged where the majority of shares in listed port authorities are in the hands of local government at all of the country’s commercial ports (Pyvis and Tull, 2017). The inappropriateness of port authority privatisation is further bolstered by evidence from some of the most efficient Asian ‘tiger’ ports, where the state retains control over port authority functions because of concerns surrounding monopolisation, foreign ownership and national security (Cullinane et al., 2005; Reveley and Tull, 2008).

Despite evidence from economically similar countries that privatisation of the port authority function does little to improve efficiency, Australian state governments have pursued short-term windfalls from these important assets, with reform strongly influenced by the dominance of market-based economic orthodoxy. The model that has prevailed in four of the five major Australian container ports has been the privatised service model, albeit with the port authority and land ‘leased’, rather than sold, to the private sector for terms of between 50 and 99 years. 4 As will be revealed in due course, reforms implemented since 2013 have delivered limited improvements, a number of unintended consequences, and episodes of political and judicial intervention.

Container port reform in Australia – privatisation, competition and efficiency discourses

Privatisation

Despite a number of reforms between 1989 and 2000, including workforce rationalisation and changes in working practices stemming from the landmark 1998 waterfront dispute, the Productivity Commission’s (2003) international benchmarking study found that the performance of Australia’s major container ports still lagged many of their regional and international counterparts. Relative inefficiency at Australia’s container ports was subsequently attributed to two elements of the way the industry was organised – lack of meaningful inter- and intra-port competition and the inefficiencies traditionally associated with public ownership.

From 2010 onwards, several of Australia’s state governments began to tender for the long-term lease of port authorities to private entities (with the exception of Flinders Ports Adelaide, which was sold in 2001). This was undertaken with considerable encouragement and financial incentive from the Liberal/National coalition federal government, part of the broader centralised asset recycling strategy outlined earlier. At the three largest container ports in the country, leases of between 50 and 99 years were sold to private interests, composed of pension, hedge and foreign investment funds. The standard justifications for privatisation of the landlord function were expounded – that the proceeds would reduce state budget deficits and related interest payments, that the funds raised could be used to finance other infrastructure projects, and that the state should offload risk to the more efficient private sector (Chester, 2015; Quiggin, 1995; Walker and Walker, 2000).

The privatisation program has already created a number of issues and concerns. As previously outlined, in the rush to recycle state assets and release funds for infrastructure projects, calculating a just price for port leases can be problematic. A prescient example of this is provided by the case of Flinders port. As the first port in Australia to be privatised, some 10 years earlier than its counterparts in other states, it could be regarded as a precedent. A 99-years lease was sold for $186 million in 2001, yet in the 2013/14 financial year alone, the port recorded a profit of $97.8 m, and paid dividends of $22 m to shareholders (MUA, 2015). Clearly, the original price paid for the lease severely underestimated future revenue at the port and represents poor value for the state government and, ultimately, the communities of South Australia. Whether lease income received by other states for their ports constitutes a fair price is too soon to discern. However, it is notable that the Port of Brisbane made a profit of $139 m in 2018, before tax, depreciation, amortisation and finance costs (Port of Brisbane, 2019). The 99-year lease sale price was $2.3bn, implying that investors will make a handsome return. At the other extreme, the bumper amount paid for the Port of Melbourne ($9.7bn for a 50-year lease) would indicate that it is inevitable that port revenues will need to rise steeply to produce a return on investment, and a key source of income is port estate rents.

As landlord, the port authority is responsible for setting rents for quay and yard space for stevedoring companies involved in cargo-handling, placing it in a position of natural monopoly. Where port authorities pass into the hands of private entities, these can exercise formidable market power and have no real responsibility to broader stakeholders beyond shareholders. This has manifested itself in large rent increases for stevedores at the major ports. For example, at Botany (Sydney) and Melbourne, Patrick Stevedores claimed that its rent had increased 140% since privatisation (ACCC, 2017). DP World also reported a 60% increase in rent at its Melbourne terminal when due for renegotiation in 2018, with rents per square metre for all stevedores increasing 15% on average in 2018-19 alone compared with the previous year (ACCC, 2019; Stevens, 2017). Meanwhile, in the 3-year period immediately proceeding privatisation at the Port of Brisbane, the port authority, Port of Brisbane Holdings Pty, reported revenue from rent had increased by 59% (Port of Brisbane, 2014).

Escalating rents have had a series of consequences for other port stakeholders. Stevedoring companies have considerable leverage over their landside customers (i.e. importers and the transport companies they hire to deliver/collect their cargo), whose patronage is dictated by the cargo owner and shipping line. Stevedores have been accused of using increased property overheads as justification to introduce disproportionate supplementary fees for terminal access, and in turn these are passed down the supply chain. For example, since Patrick introduced the industry’s first ‘terminal infrastructure levy’ at the Port of Brisbane in 2010, the price has ballooned by over two thousand per cent, from $4.95 to $110 per container. This is mirrored at its Melbourne terminal, where the charge has increased from $3.50 at its inception in 2014 to $125 as of June 2020. Meanwhile, DP World’s ‘terminal access charge’ at Botany has increased almost six-fold since privatisation in 2017, from $21.16 to $112 per container (ACCC, 2018, 2020; DP World, 2020; Patrick Stevedores, 2020). This exponential trend is shared across the three largest container throughput ports (Botany, Melbourne and Brisbane), with the two dominant stevedores generally matching each other’s fees and rises. Vehicle Booking Surcharges (VBS) of between $18 and $45 are exclusive of the access fees, meaning that the average supplementary charge levied on each imported container which passes through the terminals of DP World, Patrick and VICT at Australia’s largest ports is currently between $148 and $162. 5 The final amount can be even higher because transport companies often add an ‘administration’ mark up to cargo owners of between 10 and 20%. Indeed, ‘some [haulage] operators like the charges because they can pass larger increases on to their customers’ (Author’s interviews with road haulage representative #2, 2020). In total, stevedoring companies generated $256.4 m in revenue from infrastructure/access charges in the year to June 2020, a 51.9% rise on the previous year (ACCC, 2019, 2020).

Unsurprisingly, the proliferation of port infrastructure/access fees has attracted heavy criticism. Aside from newspaper reports that characterise them as detrimental to the good of the economy (see, for example: Lucas, 2018; Wiggins, 2019a), other industry stakeholders are apoplectic. One haulage representative described the charges, and the frequency at which they are raised, as ‘wholesale price gouging’, enabled through the ‘golden cages… [and] captive market’ that stevedores enjoy (Author’s interview with road haulage representative #2, 2020). Another criticised state government inaction in regulating terminal access prices to prevent transport companies, importers and exporters ‘being charged for things or services that don’t exist’ (Author’s interview with road haulage representative #4, 2020). The general feeling across the haulage industry is that ‘transport operators are held at ransom and forced to pay a surcharge to collect and deliver containers, with no ability to negotiate price or service’ (Whelan, 2020).

Importers and exporters bear ultimate responsibility for the port access and infrastructure charges levied by stevedores. Kingspan, a major exporter of insulation products, conducted a benchmarking survey across ports it used worldwide and ‘found that Melbourne was… one of the most expensive ports in the world for terminal handling and port service charges’, also complaining that it ‘could not compete against overseas rivals until charges were cut’ (Kingspan Insulation Australia, 2018). Kingspan’s concerns are shared by other major Australian exporters such as Bega, Visy and K-Mart (ACCC, 2018). In fact, the mounting port access fee furore encouraged the ACCC to put stevedoring companies ‘on notice’ of enforcement action if anti-competitive behaviour is suspected (Wiggins, 2019b). Ultimately, importers and exporters are ‘forced to pass this on to the consumer through higher prices in the shops’ (Author’s interview with importer/exporter #1, 2020).

To head off mounting criticism, in March 2020 DP World and Patrick renamed the fees and lowered the cost for export containers by around 20% to ‘recognise the significant challenges faced by our exporters’ due to bushfires and Covid-19 (DP World, 2020; Patrick Stevedores, 2020). However, stevedores have otherwise defended their access/infrastructure fees. In addition to higher rents, local taxes and utility costs, they face sustained pressure on the quayside, where a series of shipping line conglomerations and increased competition between stevedores lend considerable leverage to quayside customers. The result is falling revenue from this portion of their business which, they say, needs to be recouped. They also cite previous and future investments in quayside and landside facilities and infrastructure as drivers of fee hikes (ACCC, 2019; Patrick Stevedores, 2020).

For their part, privatised port authorities have either challenged the veracity of the stevedores’ claims or attempted to justify the increased rents that partially prompted the proliferation of these access charges. The Port of Melbourne maintains that the way it sets rents for tenants is ‘fair and reasonable and so represent[s] market-based prices’ and that its ‘processes for setting and reviewing market rents… clearly demonstrate that there has not been a misuse of market power’ (Port of Melbourne, 2020). This is echoed by the Port of Brisbane which maintains that ‘we are very astute about how we do our pricing and valuation… over the last 10 years we have charged a low stable rent calculation that provide long term leases for stevedores’ (Author’s interview with port management #2, 2020). NSW Ports has gone as far as to deny rent increases have even occurred, simultaneously embarking on a PR campaign that emphasises their ownership structure as benefitting ‘over six million Australian superannuation fund members’ (NSW ports, n. d.; NSW Ports, 2017). Nevertheless, in the cases of Botany and Melbourne, escalating rents could be construed as a predictable outcome of the inflated prices paid for leases.

Some states already have a voluntary price monitoring regime in place for port rents. For example, the Essential Services Commission of South Australia (ESCOSA) has been actively monitoring prices annually since Flinders port authority was privatised in 2001 (ESCOSA, 2004). As pressure mounts, other states are implementing price monitoring. The Victorian Essential Services Commission recently reported following an inquiry on port rents, unsurprisingly finding that ‘the Port of Melbourne’s exercise of its power has caused material detriment… the requirement in the Port Concession Deed for rents to reflect a “reasonable market rent” are not sufficient to constrain the Port of Melbourne from charging rents above an efficient level’ (Victorian Essential Services Commission, 2020: viii). Appetite for rent regulation appears to be growing and is increasingly on the political agenda despite the recent Productivity Commission Inquiry report surprisingly recommending against (Productivity Commission, 2022b).

Aside from rent hikes, the introduction of infrastructure charges, and the appropriateness of lease prices, there have been other issues related to privatisation of port authorities. One of the most high-profile of these involves the terms of the lease to the ports of Botany and Kembla, which were packaged together. In the year before the ports were privatised in 2013, the state-owned Sydney Ports Corporation recorded a $53m profit and the price for the leases was initially mooted as $3bn (Sydney Ports Corporation, 2012). The final sale fetched a combined $5.07bn, a price which ‘seemed extraordinary… no-one could work out why’ (Author’s interview with port management representative #1, 2019). The terms and conditions of the sale, beyond lease duration, were not made public, although the final price was widely lauded in the media, providing a boost to public perceptions of the federal and state governments’ asset recycling strategy (see, for example: MacDonald and Chessell, 2014; Owens, 2013).

A year after the Botany/Kembla deal, a 98-year lease to the Port of Newcastle, another New South Wales port predominantly used for coal exportation, was sold for $1.75bn. Newcastle had previously been proposed as a viable option to develop a container terminal to serve New South Wales (NSW Government, 2003). 6 Three years after the deal was completed, the terms of the Botany/Kembla leases were thrust into the spotlight when it was leaked to the press that they contained a clause placing limits on, and effectively preventing, Newcastle’s development as a container port (Kirkwood, 2016). It now became evident why the lease price for Botany/Kembla was significantly above market expectations – the then NSW government had surreptitiously installed a strictly confidential and anti-competitive clause into the deal to artificially inflate the price, without divulging this publicly or submitting the terms to parliamentary scrutiny (NSW parliament, 2019).

The development of Newcastle as a container port offered a rare opportunity to introduce future inter-port competition, yet it is alleged that the state government deliberately inhibited this. Packaging Port Botany and Port Kembla (located approximately 90 km away) together also removed another potential competitor to Botany and a further opportunity to foster future inter-port competition. Indeed, ‘the idea that privatisation was introducing productivity and enhancing competition was exposed as being a ruse for the consolidation of a monopoly operation at Port Botany’ (Author’s interview with port management representative #1, 2019). The fall-out from the controversial deal continues. The ACCC unsuccessfully challenged the legality of the Port Botany/Kembla lease in a Federal Court (ACCC, 2021) and it then appeared that the federal government would intervene to broker a settlement between the concerned parties (Author’s interview with port management representative #1, 2021), before this was stymied by the federal election. In November 2022, an agreement was finally reached, and legislation passed, to unpick the anti-competitive containerisation clause of the Botany deal, whereby the Port of Newcastle is required to ‘top-up’ its lease payment to the state to reflect the added value that this implies (Parliament of New South Wales, 2022; Parris, 2022). This will at least provide some relief to the public purse, offsetting the $125m that has already been paid to the consultancy firms advising on the Newcastle and Botany/Kembla lease sales (Humphries, 2017; Kirkwood, 2018).

Competition

The ACCC had consistently campaigned for measures be introduced to increase competition in the stevedoring industry, in order to improve productivity and efficiency outcomes (ACCC, 2004, 2006). It argued that there was little choice for shipping lines and exporters because Australia’s geographic scale made inter-port rivalry, the standard driver of competition-related efficiency improvements at ports elsewhere, problematic. Lack of inter-port competitive pressure was compounded by the existence of stevedoring monopolies or duopolies at most locations, that is only one or two terminal operators involved in cargo-handling at any given major container port. Since improvements in inter-port competition were difficult to harness in most states, the ACCC recommended that intra-port competition should be encouraged by introducing a third terminal operator to several of the major container ports. As it stood, incumbents enjoyed high operating profits because ‘players do not face appropriate incentives to invest in a more efficient, productive service’, to the detriment of the broader national economy (ACCC, 2011: vi).

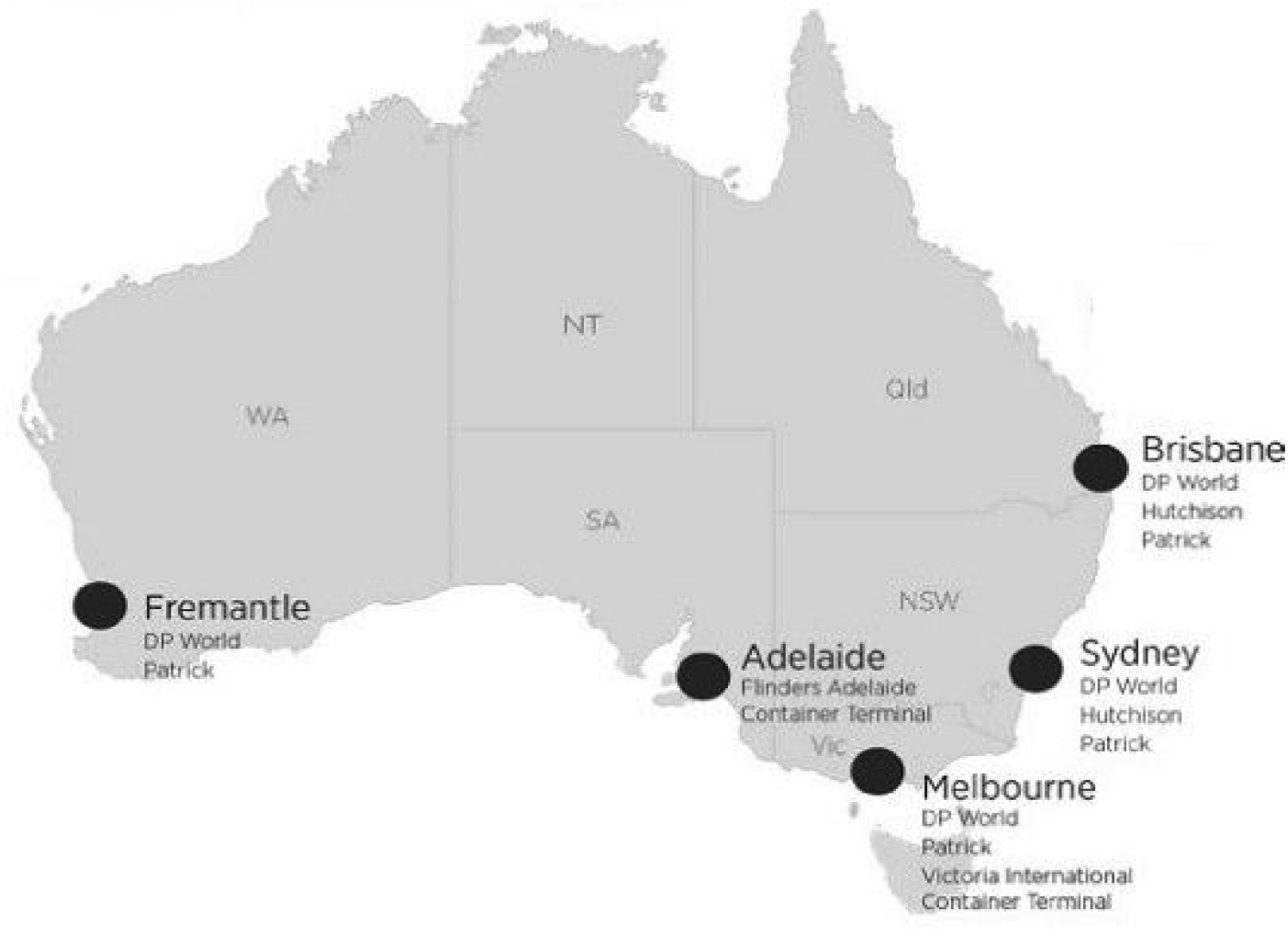

From 2005 onwards, major global stevedoring players were invited to tender to build and operate additional terminals at the three largest of the five major Australian container ports by throughput. At the ports of Brisbane and Botany, the Hong Kong-headquartered global terminal operator (GTO) Hutchison Ports won the tender to construct new-build terminals on greenfield sites and cargo-handling there began in 2013 and 2014, respectively. At the Port of Melbourne, Hutchison was unsuccessful in the tender, which was instead awarded to Victoria International Container Terminal Ltd (VICT), a joint venture comprised of another GTO, Philippines-based International Container-Terminal Services, and Australian-based propriety Anglo Ports. These terminal operators joined Patrick and DP World in handling containerised cargo at the three largest container throughput ports in Australia. At the new greenfield terminals, a significant proportion of the cargo-handling process is automated, while other stevedores at these ports have also introduced similar technology. (Figure 1)

Despite being championed as a silver bullet for enduring competition and productivity issues, the introduction of the third stevedore has not been as effective as initially hoped. Since beginning operations at Botany and Brisbane, Hutchison Ports Australia (HPA) has struggled to gain a foothold in the market. In an attempt to prise custom away from DP World and Patrick, HPA began to aggressively undercut what its competitors charged to quayside customers (i.e. shipping lines) per container. However, 2 years into commencing operations, HPA had managed to capture only a paltry three percent market share (Stevens, 2015), while quayside revenue per container lift fell by over 20% industry wide as a result of stevedore price competition and the enhanced market power of shipping lines due to conglomeration (ACCC, 2017; ACCC, 2019). As previously discussed, pressure on quayside revenue across the industry has had a reciprocal effect on the proliferation of ‘port access’ fees for landside customers. A further 5 years on, Hutchison’s current Australian market share stands at six percent and, as such, the third stevedore strategy has done little to foster competition at Brisbane and Botany, although VICT has fared better at Melbourne, increasing its share of volume at the port from 15 to 30 percent between 2019 and 2022 (ACCC, 2019, 2022). However, it is important to note that VICT’s ability to attract custom is only differentiated from HPA’s because its terminal at Webb dock is able to accommodate larger container vessels (up to 8000 TEUs), which its competitors at Melbourne cannot due to the height restrictions of the West Gate bridge (ACCC, 2016).

There are several reasons why, despite significant industry experience and presence, HPA has failed to provide effective competition. Primarily, its failure to win the tender for the third terminal at Melbourne left it at a disadvantage when attempting to attract quayside customers since shipping lines are said to prefer stevedores that can provide a ‘national’ service across the three major east coast ports, which the pre-existing incumbents can (Author’s interview with haulage representative #2, 2020; Author’s interview with port management #2, 2020). Its attempt to aggressively undercut competitors’ container handling rates also proved unsuccessful, instead encouraging a race to the bottom. HPA were forced to announce that ‘the third operator policy is not viable in the immediate future but hopefully we can work with all stakeholders to ensure the viability of the container terminal industry on the east coast over the longer term’ (ACCC, 2016; Hewett, 2015).

As previously noted, the ACCC was the driving force behind the third stevedore policy. However, questions remain whether container throughput volumes were large enough to sustain additional competition from a third stevedore in all three ports concerned, and particularly in Brisbane. Concerns surrounding the proposed policy were clearly articulated by industry stakeholders and experts at the time (Author’s interview with port management #2, 2020; Author’s interview with port management #3, 2020; Van Duyn, 2013). As the nomenclature suggests, the ACCC is intractably wedded to the neoclassical ‘common sense’ that competition will always improve efficiency, failing to account properly for the peculiarities of the industry. Although intra-port competition was regarded as necessary because of difficulties fostering inter-port competition (except in New South Wales, where possible inter-port competition was sacrificed by the state government in favour of lease price enhancement), many of the most efficient ports worldwide have only one stevedoring company engaged in container handling. Considering the status quo elsewhere and the modest container throughput volumes at Australian ports, the third stevedore initiative can be considered a prime example of ideological policy making.

The third stevedore policy and HPA’s subsequent failure to obtain meaningful market share has had a series of direct and indirect effects on other port stakeholders and the industry more broadly. Firstly, and most obviously, industrial relations have been adversely affected, as labour costs form over half the total overheads for stevedoring companies (ACCC, 2016). On 6 August 2015, HPA sacked 97 of its 224-strong Australian dock worker (wharfie) labour force overnight by text message and email (Australian Broadcasting Corporation, 2015). A three-and-a-half month-long dispute ensued, the longest in Australian waterfront history, causing significant disruption to both HPA terminals as ships were diverted to competitors. After extended negotiations between the MUA and the company at the Fair Work Commission, voluntary redundancy was offered to all HPA wharfies at Botany and Brisbane yielding 60 applicants, while those workers compulsorily terminated in August were reinstated (Author’s interview with union representative #3, 2020; Hannan, 2016).

The introduction of the third stevedore has had other implications. As previously noted, new terminals were built on greenfield sites and both HPA and VICT built technologically advanced terminals incorporating a significant degree of automation of cargo-handling. The commercial advantages that this allegedly presents new entrants, particularly in relation to manpower costs, have contributed to encouraging Patrick to semi-automate their Botany operations while, during recent enterprise bargaining, DP World have refused to give guarantees that they will not seek to automate their operations in the future (Author’s interview with union representative #1, 2019; Marin-Guzman, 2019). These developments have resulted in tortuous bargaining negotiations between stevedores and the union in the most recent round of Enterprise Bargaining Agreements, prompting rolling industrial action and uncertainty for both workers and port customers (Author’s interview with union representative #3, 2020; Marin-Guzman, 2020). The impact of automation on port efficiency will be discussed next.

Efficiency outcomes from competition and privatisation reforms

Efficiency is the primary goal of contemporary economic orthodoxy, with competition and privatisation deemed fundamental levers to achieve improvements. Intra-port competition was regarded as a panacea for the efficiency problems allegedly blighting the Australian port industry. However, as previously discussed, issues surrounding container volumes and the decentralised, state level award of new stevedoring tenders have meant that expected efficiency gains have largely failed to materialise. Automation of container terminals has escalated alongside, ostensibly pursued to capitalise on technological innovation and improve cargo-handling productivity, also chiming with the efficiency paradigm that underpins dominant political and economic discourses.

Despite initial proclamations of stevedores and equipment suppliers that automation equates to considerably more efficient and productive cargo-handling operations (ABB, n. d.; Forklift Action, 2008; Hutchison Port Holdings, 2012; Kalmar, 2005; Vrakas et al., 2021), statistics indicate that gains in this area are peculiarly modest. The Port of Brisbane actually saw a significant decline in productivity in the 3 years following the opening of Patrick’s AutoStrad terminal in summer 2005. 7 The introduction of automation at Patrick’s terminal in April 2015 also resulted in a notable fall in productivity at Port Botany, returning to (though not exceeding) pre-automation levels in 2019, while the commencement of cargo-handling at HPA’s technologically advanced terminal in November 2013 registered no significant improvements. 8 Even at VICT, the relative success story of the reforms implemented under the auspices of competition, the introduction of the ‘most advanced container terminal in the world’ provided a relatively limited boost to overall quayside productivity at the container terminals of the port (Port Strategy, 2019). 9

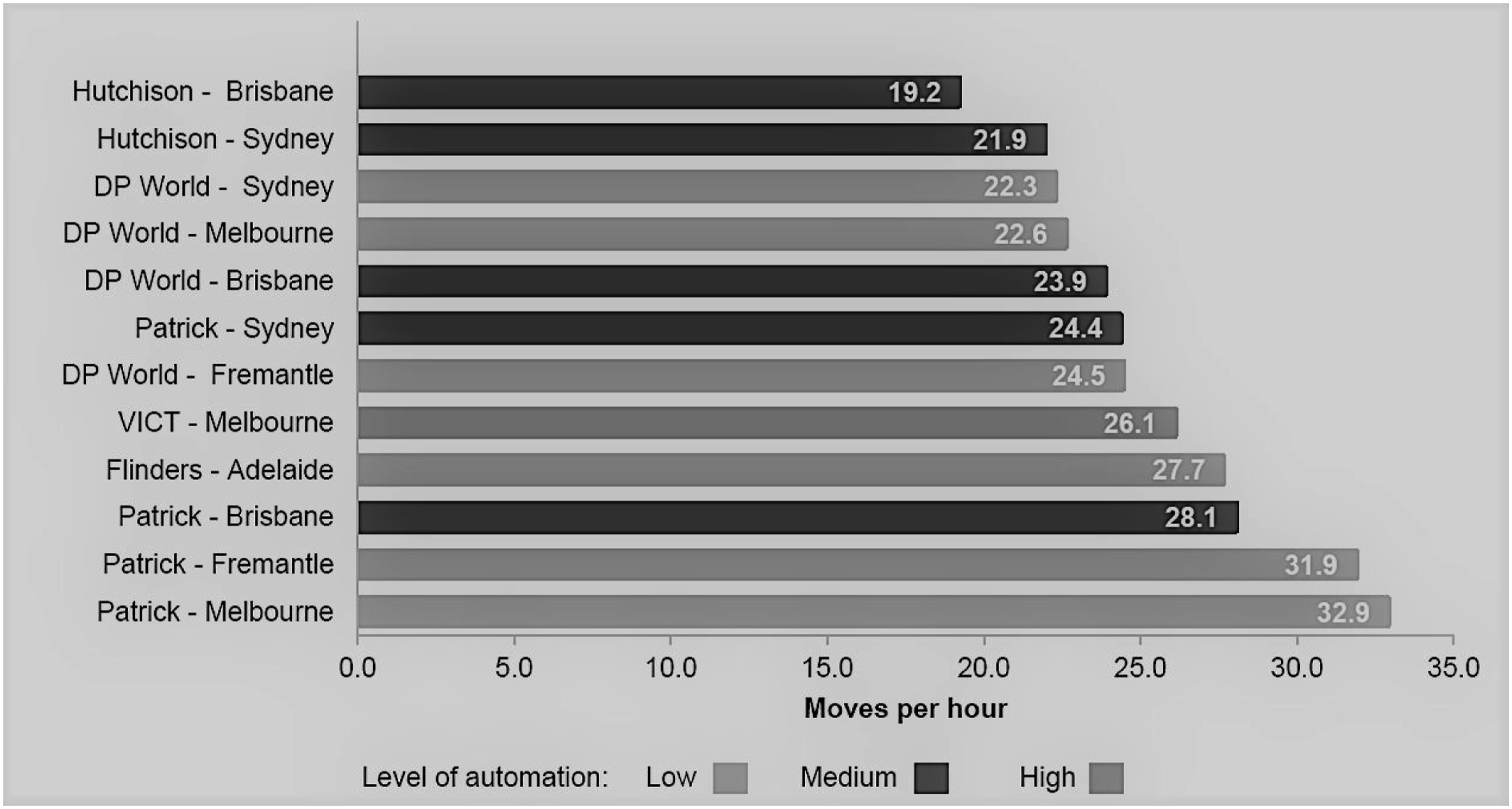

It should be noted that the only publicly available statistics regarding productivity (ACCC and BITRE reports) are provided at the aggregate port level, rather than at the individual terminal level, which stevedores record but do not share publicly, and as such give only a general insight into the impact of automation. However, the recent Productivity Commission inquiry used previously unavailable and paywalled data to calculate crane rates at all Australian container terminals. It found that ‘it is not clear from examining average gross crane rates at the major container terminals that there is any correlation with levels of automation’ (Productivity Commission, 2022a: 351). (see Figure 2) Australian container ports and terminal operators (stevedores) (Adapted from: ACCC, 2019). Gross crane rate by terminal operator – level of automation (Source: Productivity Commission, 2022a: p.351 – Figure 11.5).

Stevedoring companies have belatedly argued that negligible productivity improvements should be considered in the context of associated manpower savings, consistency of throughput and safety advantages, resulting in greater cost efficiency (Productivity Commission, 2022b). HPA and VICT have reaped some of the benefits that automation can bring in terms of a reduced labour force, with only approximately 80 wharfies deployed at the latter and 130 across the two terminals of the former, although these should be viewed in relation to the smaller volumes that these two stevedores handle. 10 Interestingly, in the press, Patrick lauded a $50m in annual labour cost savings that automation would contribute to their Botany operations and, upon its introduction in 2015, initially cut its workforce by over half to 208 (O’Sullivan, 2014). However, just 12 months later they were forced to quietly recruit 90 additional workers and others since, meaning its workforce stands at approximately 330 as of 2020 (Author’s interview with union representative #1, 2020). Juxtapose this with the estimated $350–400 m cost of automation at Patrick’s Botany terminal, a lack of meaningful productivity improvements and increasing overall operating costs, and it remains to be seen if sufficient gains have been made to warrant the size of investment (ACCC, 2019). This has led the MUA to claim that the automation of cargo-handling at Patrick’s was expedited as much for anti-union motives as for efficiency ones, particularly in the context of the historically tempestuous relationship between the company and the union (Author’s interview with union representative #1, 2019; Author’s interview with union representative #3, 2020). It is certainly noteworthy that, while less than 4% of container terminals worldwide have a degree of cargo-handling automation, Australia is a significant outlier, with 50% of its ports subject to automation of one or more stages of the cargo-handling process (Knatz et al., 2022; International Transport Forum, 2021). When automation at Botany was initially mooted, the deputy national secretary of the MUA observed that ‘a motivated and engaged workforce with the right management team can deliver the same levels of productivity, if not better, at a far lesser cost’ (Saulwick, 2015), something which appears to be borne out by the crane rate productivity statistics.

Port reform initiatives focus primarily on quayside productivity, while the broader economic impact of inefficiency elsewhere in the supply chain is often underemphasised. Stevedores face pressure from their quayside customers, and the institutions of government, to ensure quick turnaround time for ships, however, ‘the land-side task may not, by itself, provide incentives for stevedores to maintain land-side connections that provide for more efficient supply chains’ (ACCC, 2009: 46). As previously discussed, landside customers such as road haulage companies face a captive market, insofar as they have no control over which terminal they visit, instead dictated by the shipping line/cargo owner. This means they have little to no influence over stevedores and are routinely treated as second class stakeholders. Prior to 2011, drivers attending Port Botany could be forced to wait up to 6 hours for their trucks to be serviced. Stevedores penalise haulage companies when they arrive early or late to their terminals but ‘there was no two-way penalty with transport, if stevedores held up transport, it was too bad for transport. Who paid for the waiting time? We did and our customers did’ (Author’s interview with haulage representative #1, 2020).

Lack of efficiency on the landside of port supply chains became a touchstone issue for the transport industry. In New South Wales, various road haulage interests lobbied the state government to intervene over stevedores’ indifference towards issues facing landside customers. Out of this came a 2008 review by the Independent Pricing and Regulatory Tribunal (IPART, 2008), 11 later leading to legislation which introduced the Port Botany Landside Improvement Strategy (PBLIS) in 2010 (NSW government n. d.). From the landside customers’ perspective, improvements in efficiency at Port Botany’s container terminals have ‘nothing to do with privatisation… or automation’, but rather regulation (Author’s interview with haulage representative #2, 2020). PBLIS has been described as ‘the great reform of the last 20 years in terms of creating a more efficient land side’ (Author’s interview with haulage representative #3, 2020). Stevedores addressed their landside inefficiencies only once penalties of $100 per hour of delay were introduced in favour of transport companies. Although PBLIS was legislated at the state level and hence applied solely to Port Botany in New South Wales, its effects were felt across the industry. All stevedores at Botany operate terminals at other ports and have adopted the best practices developed because of PBLIS to all operations, with an eye on averting regulatory intervention in other states. However, despite PBLIS significantly improving landside efficiency at Botany, and across the industry more broadly, issues remain for landside customers, particularly relating to turnaround times at Empty Container Parks (Author’s interview with haulage representative #2, 2020; Author’s interview with haulage representative #3, 2020).

Conclusions

Port reform in Australia was underpinned by the economic justifications that have dominated political discourse since the 1980s. Privatising public assets and commercialising sectors through increased competition are viewed as common sense economic measures that will provide universal solutions to efficiency issues. However, the research presented here has highlighted some of the issues surrounding the application of neoclassical logic to the port industry, which is unique in terms of its strategic economic importance and structural opportunity for uncompetitive arrangements to proliferate. One of the key desired outcomes of liberalising reform is to promote competition-driven productivity and efficiency amongst market players, and for the benefits of this to be passed on to consumers. In the case of Australia’s container ports, none of these outcomes have been realised.

This study has a series of practical implications for port reform and public policy more broadly. From an industry-specific perspective, potential issues surrounding the rare, but increasingly proposed, phenomenon of port authority privatisation internationally are highlighted by the Australian case. Although neoclassical logic and reform have prevailed in other key sectors where public ownership was once dominant, concerns surrounding security, facilitation of trade, and broader economic ramifications, have, in most countries, encouraged governments to (at least) retain the landlord role at ports. Nevertheless, despite evidence from elsewhere, Australian policy makers have pursued a privatised port governance model, part of an ideological program of systemic privatisation.

The international literature on port privatisation has demonstrated that privatisation often does little to improve efficiency in the container ports of mature economies (Pyvis and Tull, 2017; Cheon, 2008; Cullinane et al., 2006) or to encourage investment in port infrastructure (Pallis and Vaggelas, 2022; Baird, 2013) and is usually unduly influenced by the political ideology of the government of the day (Brookes et al., 2017; Monios, 2017). These broad findings are supported by the research and analysis offered above. More specifically, the paper has documented how privatisation and lease pricing have had several other undesirable effects for port stakeholders and the downstream supply chain.

In some cases, state governments, incentivised by the federal asset recycling scheme, pursued high lease prices at the expense of broader economic and security considerations, despite the federal government’s own competition review strongly recommending against ‘maximising asset sale prices through restricting competition or allowing unregulated monopoly pricing post sale’ because it ‘amounts to an inefficient, long-term tax on infrastructure and consumers’ (Australian Government, 2015: 196). This has resulted in increased rents for stevedoring companies as investors seek returns (with profits at least partially offshored), detrimental effects on industrial relations because of reciprocal pressure on labour costs, and the introduction, then escalation, of terminal access charges that add cost inefficiencies to the supply chain and ultimately result in higher prices in the shops for Australian consumers. Where lease prices were undervalued, as was the case with earlier privatisations, privatised port authorities are reaping obscene returns at the expense of communities and taxpayers. Short-term budgetary fillips derived from public asset sales should be approached cautiously because of problems surrounding how to accurately calculate lease/sale prices, regardless of where funds recouped will be deployed (Quiggin, 1995, 2001).

Aside from questions surrounding the appositeness of port authority privatisation and lease price incentivisation, measures to introduce increased competition to the industry have largely failed, with the possible exception of VICT at Melbourne, and even this is mainly due the serendipity of situational factors, rather than competitive pressures. The third stevedore reforms were largely premised on the neoclassical principle that competition will force efficiencies onto market players. However, there are several unique features of the Australian industry that mitigate against universal application of market logic. Primarily, unlike many countries in the world, inter-port competition cannot be leveraged due to geographic scale, with the exception of New South Wales, where the then state government sought to sacrifice long-term competition for short-term financial gain. Market conditions were not necessarily suitable for the introduction of further intra-port competition either, while there is also significant evidence from high efficiency ports elsewhere, for example, in the EU, that having only one stevedoring company engaged in container handling, using a centralised pool of labour, typically results in better productivity outcomes (Turnbull, 2006, 2010). The ACCC campaigned strongly for this policy despite reservations from some stakeholders whether container throughput volumes could sustain another operator. It has been forced to concede that ‘challenges remain for the industry. In recent years, improvements in productivity have stagnated… DP World and Patrick continue to account for the vast majority of container volumes’ and that ‘it may be only the shipping lines that benefit from the additional competition between stevedores at the east coast ports’ (ACCC, 2018: 3–4), a further example of ideological, as opposed to evidence-based, policy making.

The manner in which privatisation and intensification of competition have been introduced to Australia’s container ports has added significant cost inefficiencies to the supply chain in the form of rent increases and terminal access charges. There is also no evidence of improved productivity, as measured by the crane rate, nor any meaningful efficiency gains, despite huge investment in automation across the industry. Automation was initially mooted as just that – a tool to improve productivity, yet more recently stevedoring companies and equipment manufacturers have distanced themselves from this claim, instead preferring to stress labour cost savings, which have proven to be more modest than anticipated, consistency of throughput and safety. This points to a distinct divergence in priorities between policy makers and terminal operators. The former is obsessed with the ‘crane rate’ measure of productivity and frequently points to Australia’s comparatively poor performance in international benchmarking as justification for further reform (Productivity Commission, 2022b), while terminal operators have seemingly decreased productivity by introducing automation. The levers of privatisation, competition, and automation have all failed to live up to expectations as means to improve the comparative performance of Australia’s container ports.

Where market players in a monopoly or duopoly situation are seen to be abusing their power (as seems to be the case in Australia’s container ports), regulation should be considered as a counterbalance. In late 2020, the Chairman of the ACCC went on record as saying ‘the ports were sold, usually with no control over their pricing in order to maximise the proceeds of sale. The resulting unfettered market power of some ports is costing our nation dearly… we need a new… monopoly regulation regime that would see owners of significant infrastructure with market power subject to some form of price regulation’ (ACCC, 2020). In countries with experience of privatised port authorities, regulation is advocated by port governance academics to ‘protect the nation’s interests… to ensure equitable development, good performance and fair charging’ (Monios, 2017: 87; see also: Angelopoulos, 2019; Baird, 2016).

One of the principal barriers to reasonable regulation of the market in Australia is ideology. Policy makers intrinsically wedded to the present orthodoxy hesitate because government intervention is regarded as the antithesis of market-oriented economics (Davies, 2018). The recent Productivity Commission report refused to recommend regulation of port rents, despite strident statements in favour from the ACCC and support for regulatory intervention being almost unanimous amongst landside industry stakeholders (Author’s interview with road haulage #1, #2, #3, #4; Author’s interview with importer/exporter #1, #2, #3). Overtures towards regulation have only materialised as monopolistic behaviour has become blatant, since to do so during the sale process would have had a negative effect on the lease price (Martin and Parker, 1995), a prime example of post-sale ‘negative regulation’ that could have been avoided by a sober and realistic pre-privatisation appraisal of market conditions (Turnbull, 2010). The success of PBLIS at Port Botany should demonstrate to policy makers that regulation can be instrumental in markedly improving elements of port efficiency and inhibiting misuse of market power. Nevertheless, despite overwhelming evidence and appetite for intervention, reticence remains because of the pervasiveness of contemporary economic orthodoxy. Ideologically driven application of free market maxims to a structurally unique industry with multiple opportunities for uncompetitive arrangements to proliferate is the source of Australia’s port reform debacle, and continuing adherence characterised by reluctance to regulate perpetuates it.

From a general perspective, the findings of this paper support an evidence-based, pragmatic approach to the privatisation of public assets and argues that fundamentalist adherence to free market ideology obscures a measured, even heterodox, perspective where necessary and where market structure and conditions merit. Ports are not unique here. In economically similar countries, there has been reports of mixed or limited benefits of privatisation of other key industries such as railways and utilities (see, for example: Araral, 2009; Bowman, 2015; McCartney and Stittle, 2023). Privatisation and commercialisation often increase profitability, but this disproportionately favours owners and/or shareholders, not consumers or society more broadly, and can have a series of undesirable effects for other stakeholders and the prosperity of the national economy, particularly when concerning a key sector like the ports industry. Chris Corrigan, then-Managing Director of Patrick, once justified the epochal 1998 waterfront dispute as a required defensive action against ‘the impact of waterfront rorts on ordinary Australians’ (Bonyhady, 2020). Ironically, the port reform process that the strike instigated has resulted in a state of affairs in which the average Australian consumer, and the Australian economy generally, is paying the price to a much greater extent than ever before.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.