Abstract

Political economists have long acknowledged the importance of funded pensions acting as catalysts for processes of financialization. The transformation from rule- to risk-based pension fund governance is particularly important for pension financialization. Risk-based governance involves monitoring of internal decision-making procedures by new professionals rather than compliance with highly detailed legal restrictions. Scholars of financial regulation have termed this kind of supervision ‘regulation from the inside’. Being part of the organization they monitor, internal regulators hold fundamentally ambivalent positions. Existing studies emphasize the duality of internal regulators’ role perceptions as well as their attempts to span the boundaries between themselves and other organizational actors. In this paper, we extend scholarly insights on risk-based supervision of private (non-)financial institutions to pension institutions by focusing on a peculiar form of ‘regulation from the inside’: so-called internal supervisors in Dutch occupational pension funds. Internal supervisors are pension fund functionaries, responsible for evaluating the governing board's performance and holding the board accountable. We report findings from an original survey and interview study among internal supervisors. Contrary to the formal requirement of independence between governing board and internal supervision (a ‘checks and balances’ perspective), we find that internal supervisors often adopt a ‘fusion of powers’ approach that emphasizes collaboration with the governing board. We attribute this finding not only to internal supervision’s institutional design but also to the highly networked character of Dutch pension governance.

Introduction

Pension funds are crucial financial actors in contemporary political economies. Their importance stems not only from the sheer size of their financial portfolios, that often exceeds the size of national economies. Pension funds also play an important role in processes of financialization. Pension financialization, or ‘the growing role of financial markets and financial actors in the provision of old-age pensions’ (Van der Zwan, 2020: 2), has been associated with several empirical developments. These include, but are not limited to, the transformation of defined benefit (DB) to defined contribution (DC) pension schemes as well as changes in pension institutions’ investment policies, often attributed to legal relaxations of pension investment rules (e.g. Berry, 2021; Bonizzi et al., 2021; Van der Zwan, 2020). Such changes have been associated with workers’ and retirees’ increased dependence on financial markets and, by extension, with growing investment risks in retirement provisions (e.g. Langley, 2004; Mabbett, 2021; Wiß, 2019).

The risks associated with pension financialization have not only had profound consequences for retirement benefits but also for the way pension schemes are supervised. At the national level, scholarly attention is often directed to the activities of pension regulators and supervisory authorities (e.g. Ashcroft et al., 2011; Brunner and Rocha, 2008; Queisser, 1998). Increasingly, however, pension regulation also mandates supervision and oversight within pension institutions. One example is the ‘three lines of defense model’ mandated by the EU’s IORP II Directive, whereby specific individuals are appointed to monitor a pension provider’s governing body on the so-called key functions of risk management, internal audit and the actuarial function.

The regulatory emphasis on internal oversight within pension institutions is a direct consequence of a more general shift from rule-based to risk-based supervision of pension institutions. Risk-based pension supervision is ‘a structured approach which focuses on the identification of potential risks faced by pension plans or funds and the assessment of the financial and operational factors in place to manage and mitigate those risks’ (IOPS, 2012: 4). Contrary to rule-based supervision, risk-based supervision involves monitoring of internal decision-making procedures rather than compliance with highly detailed legal restrictions (Stewart, 2010). It thereby complements a broader regulatory framework in which pension institutions enjoy large degrees of investment freedom. As a result, risk-based supervision increases the responsibility for good financial governance within pension funds (ibid.).

The emergence of risk-based supervision of pension institutions is part of a broader development within the governance of financial institutions following the Great Financial Crisis. Scholars have used the term ‘regulation from the inside’ (Chiu, 2015) or ‘regulation at the meso-level’ (Huault et al., 2012) to describe new internal control functions within financial institutions, aimed to expand the reach of the external regulator or supervisory authority. Acting as ‘internal gatekeepers’ (ibid.), professionals like compliance officers (e.g. Lenglet, 2012), internal auditors (e.g. Minto, 2018) and risk managers (e.g. Hall et al., 2015; Power, 2007) use their organizational positions to acquire inside knowledge and information, otherwise unavailable to regulators. Yet, such internal regulators are not simply placeholders for external regulators; they are themselves part of the very organization they monitor. The dual position of internal regulators is found to create ambivalence in how they interpret their roles, particularly when the organization’s private interests and values deviate from those of the external regulator (Huault et al., 2012). While internal regulators’ role perceptions in relation to other organizational actors and to the external regulator have been subject to a broad literature in organizational and management studies (Beattie et al., 2014; Mikes, 2011; Power et al., 2013; Roussy, 2013; Soh and Martinov-Bennie, 2011), less is known about the institutional conditions that shape these perceptions (Van der Voort et al., 2019).

Our goal in this paper is to extend scholarly insights on internal control functions within private (non-)financial institutions to pension institutions by focusing on a peculiar form of regulation from the inside: so-called internal supervisors (intern toezichthouders) in Dutch occupational pension funds. The Netherlands has a highly developed, three-pillar pension system that consists of three components: a PAYGO-funded statutory pension, capital-funded occupational pensions and private pensions. The focus of this paper is on the capital-funded occupational pension system. The Dutch occupational pension system is among the largest in the world: collectively, occupational pension funds hold $2.1 trillion assets under management, representing 210.3% of GDP (OECD, 2021), while individual funds like public sector fund ABP and health care fund PFZW count among the largest pension funds globally. In 2006, the Dutch Central Bank, the supervisory authority for the pension sector, was among the first to introduce risk-based supervision. The enormous size of Dutch pension funds and the growing complexities involved in the investment of their assets – both in terms of the financial products chosen and of the global reach of these investments – directly motivated DNB’s choice for this new supervisory regime (Hinz and Van Dam, 2008).

Dutch pension funds typically consist of three functions, performed by separate bodies within the fund. The governing board is responsible for the administration of the pension plan, its risk management and the representation of beneficiaries’ interests. The board either consists of members that represent the plan’s sponsors and beneficiaries, or of independent experts. The governing board is formally accountable to the representative body of the fund, known as the accountability body (verantwoordingsorgaan). The accountability body consists of representatives of the pension plan’s active members and retirees, and in some cases also the employer and/or deferred members. Members of the accountability body are either appointed by the organizations representing plan beneficiaries (e.g. labor unions and retiree organizations) or directly elected by the plan members. The accountability body evaluates board performance and offers advice on a variety of topics (e.g. remuneration policy). 1

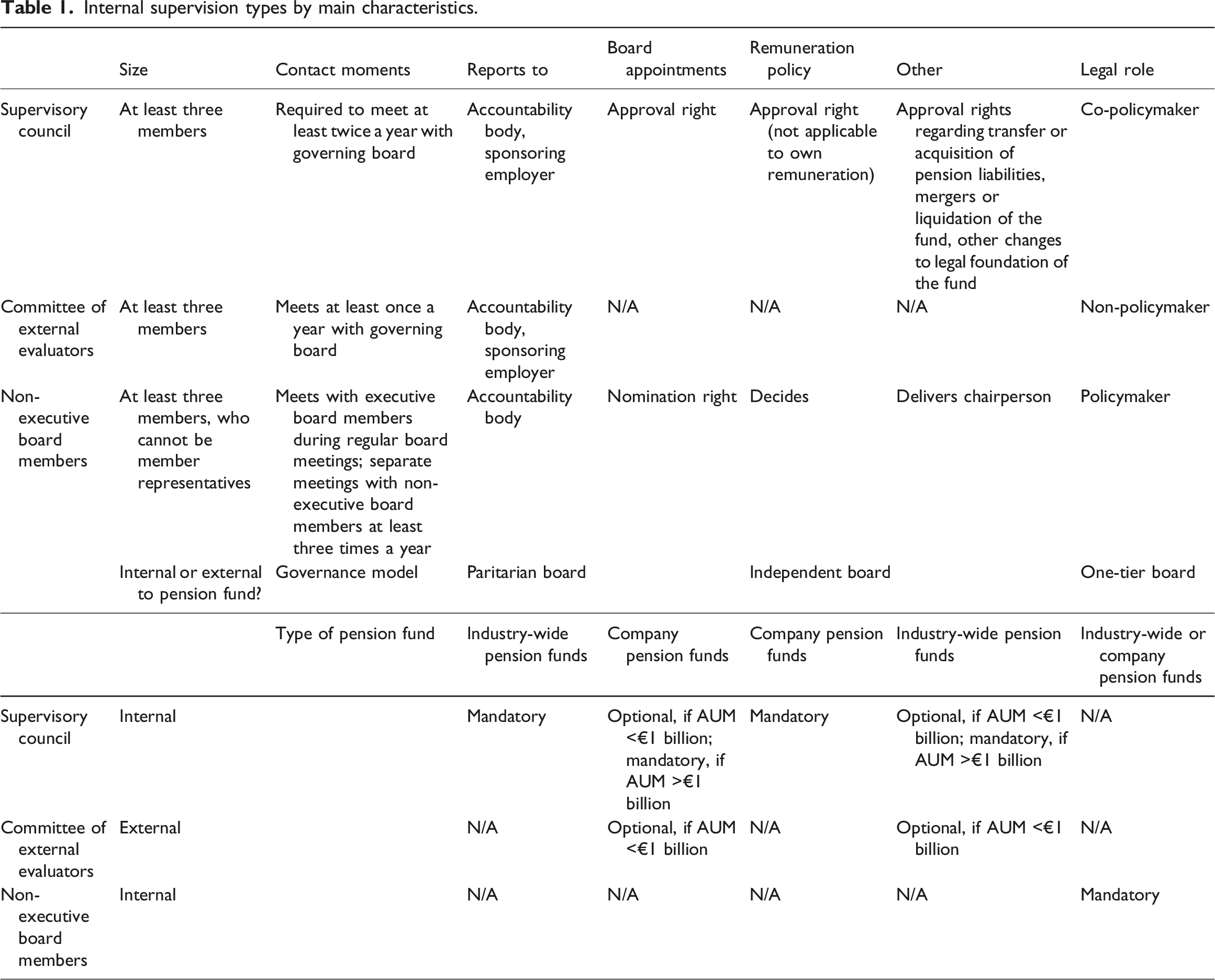

Since 2006, Dutch pension funds also have a third function: an extensive system of internal supervision that complements the supervisory and regulatory practices of the Dutch Central Bank. Central to this system of internal supervision is the role of the internal supervisor, whose formal task is to annually evaluate the pension fund board’s risk management and consideration of beneficiaries’ interests. Internal supervision can take three different institutional forms, which differ in their formal tasks and position vis-à-vis the pension fund. The visitatiecommissie is a committee of external evaluators (EE) that visits the pension fund once a year to evaluate the board’s performance. The supervisory council (raad van toezicht, SC) is the non-profit equivalent of the supervisory board in public corporations (raad van commissarissen). It is a body within the pension fund; in addition to supervising the governing board, it also plays an advisory role. Finally, some pension funds have a one-tier board structure. The task of internal supervision is performed by non-executive board members (NEB), including the chairperson. Non-executive board members are part of the governing board and hold certain decision-making powers.

In this paper, we present the findings of a survey and interview study among internal supervisors active in the Dutch pension sector. Drawing on existing studies of financial risk and regulation, we argue that internal supervisors should be considered ‘internal regulators’ in the Dutch pension system, similar to risk officers or auditors in financial corporations. As internal regulators, internal supervisors occupy dual positions within the pension fund, albeit to differing degrees depending on the institutional form internal supervision takes. How does internal supervision’s institutional design shape internal supervisors’ perceptions of their roles and responsibilities? Do internal supervisors situated more closely to the governing board perceive more ambivalence in their supervisory practices? And if so, what are the consequences for such ambivalence for pension governance? By answering these questions, the current paper contributes to existing political economy scholarship of financial governance in two ways. First, it complements existing studies by redirecting attention from external regulatory frameworks (e.g. Dorn, 2014; Mabbett, 2012; Young and Pagliari, 2017) towards internal regulation. Second, it highlights the importance of finance professionals in the enactment of financial governance. Adding to recent studies on the role of experts in changes to financial regulation (Christensen, 2021; Seabrooke and Stenström, 2022; Thiemann, 2022), we suggest that internal professional dynamics may affect wider politico-economic dynamics such as financialization.

Our findings partially confirm theoretical expectations. Contrary to the formal requirement of independence between governing board and internal supervision, board members and internal supervisors rely strongly on one another. This is particularly the case for internal supervisors in close proximity to the governing board, namely non-executive board members and supervisory council members, but less so for external evaluators. However, we attribute this mutual interdependence not solely to internal supervisors’ organizational position. Internal supervisors also respond to perceived uncertainties in the external regulatory environment by relying on informal practices of knowledge exchange, both within the pension fund itself and throughout the broader pension sector. Such exchanges are possible because internal supervisors and board members are recruited from the same pool of pension professionals. Ancillary positions, combining board memberships and supervisory positions within different pension funds, are common. The heavily networked nature of the Dutch pension sector is furthermore exacerbated by the rigid expertise requirements imposed by the Dutch Central Bank. A more independent internal supervision of pension funds therefore requires not only a reconsideration of its institutional design but also of professional dynamics within the pension sector as a whole.

Internal supervision as financial regulation

That pension funds are important drivers of financialization is by now well-established. In 2021, pension funds held a staggering $56.6 trillion in assets under management (Thinking Ahead Institute, 2022). The ongoing growth in global pension assets is not just a reflection of the expansion of occupational pension schemes and shifts from PAYGO financing to capital-funding in post-war welfare states (Ebbinghaus, 2011). It also reflects profound changes to ways in which pension assets are invested. For instance, scholars have noted shifts in pension funds’ asset allocations from a predominance of fixed-income assets (e.g. corporate or government bonds) to corporate equities and alternative assets such as real estate and private equity (Braun, 2022; McCarthy et al., 2016). The outsourcing of asset management and other investment-related tasks to financial intermediaries (Gelepithis, 2019) and the introduction of new valuation techniques (Golka and Van der Zwan, 2022) have also been associated with pension financialization.

Simultaneously, the role of the state in the regulation of pension provision has undergone profound changes. Financial deregulation has made retirement savings vulnerable to market instabilities, for instance, where investment rules for pension funds have been relaxed and pension benefits have been made dependent on investment performance. This became apparent during the Great Financial Crisis when pension funds incurred large losses. The Great Financial Crisis threatened public trust in capital-funded pensions and eroded the legitimacy of financialized pension systems (Sorsa, 2016). At the same time, few policy responses actually halted pension financialization. On the contrary: studies of post-crisis pension politics have shown a deepening of pension financialization in various European welfare states (Van der Zwan, 2020; Wiß, 2019).

Against the backdrop of financialization, governments have turned to governance as a means to manage financial risks. From more stringent liquidity and solvency requirements (Ebbinghaus and Wiß, 2011) to stricter suitability requirements and codes of conduct for trustees (Clark, 2022), public authorities have largely aimed to intervene in pension funds’ internal processes rather than tackle underlying issues of financial market instability. The term ‘risk-based supervision’ describes this new regulatory approach, whereby the state assesses pension funds’ management and mitigation of risks, not by imposing legal restrictions but rather by monitoring internal decision-making procedures (Stewart, 2010). Typical for this new regulatory regime are, for instance, the introduction of market-based valuation of pension liabilities, stringent solvency standards and a strong focus on transparency through extensive reporting requirements (Hinz and Van Dam, 2008). Here, pension regulation mirrors developments in other policy realms, associated with the emergence of the new regulatory state (Leisering and Mabbett, 2011).

The state’s shift towards risk-based supervision has been accompanied by strengthening the internal role of professions such as accountants, auditors, compliance officers and risk managers within financial institutions. Scholars of financial regulation have studied how such professionals act as ‘internal regulators’ (Chiu, 2015), putting externally formulated regulations into practice within their organizations. Such putting into practice necessarily involves a certain degree of discretion, as internal regulators interpret and translate the regulation to make it compatible with the organization (Lenglet, 2012). Through these interpretations and translations, internal regulators also define their own positions within the organization and vis-à-vis the external regulator. In their study of risk managers, for instance, Van der Voort et al. (2019) distinguish between so-called boundary spanners, who operate on the boundary between the organization and the external environment, and those who more explicitly perceive themselves as having a regulatory function. While the former hold a more antagonistic view towards the external regulator, the latter consider themselves part of the same regulatory community and maintain similar goals as the external regulator.

The consequences of internal regulators’ dual position are not straightforward. Chiu (2015) identifies three types of disjunctions that may arise from internal regulators’ discretionary practices. First, the external regulator’s expectations of the internal regulator may deviate from the everyday manner in which internal regulators perform their role within the context of their own organization (regulatory-organizational disjunction). Second, external and internal regulators may differ in their understandings of the latter’s professional responsibilities (regulatory-professional disjunction). Finally, a disjunction might occur between the internal regulator’s understanding of their professional role and the organization’s expectations regarding the scope and substance of their role (professional-organizational disjunction). Nevertheless, internal regulators’ position may also provide grounds for collaboration with others. Huault et al. (2012: 3), for instance, emphasize the mutual interdependencies between internal regulators and other organizational actors: ‘They take advantage of these interdependencies to explore, design and promote new forms of coordination and collective action’. It is important to stress that these activities may, however, feed back into wider processes of financialization. For example, the introduction of chief risk officers among large U.S. banks in the 1990s and early 2000s has been accompanied with increased investments into risky financial derivatives that fuelled the GFC: risk managers propagated a change from risk avoidance to risk management strategies that led traders to reduce their own risk monitoring (Pernell et al., 2017).

Surprisingly, studies of pension governance have not yet considered the role of internal regulators within pension institutions. Pension funds are complex institutions. As Sorsa’s (2016) survey shows, many European pension systems allow for the representation of plan members and/or sponsors in pension plan administration. Pension funds are therefore often composed of different bodies (e.g. governing board, representative body) and beholden to multiple stakeholders (plan sponsor, members, public authorities). Scholars of political economy have studied the interconnections between pension financialization and stakeholders involved in pension governance, asking, for instance, whether employer and union involvement in pension investment is a buffer or a driver of pension financialization (e.g. Anderson, 2019; Van der Zwan, 2019; Wiß, 2015). Still, to our knowledge, no politico-economic study has yet focused on the roles of professionals associated with the risk-based supervision of pension funds: not only internal supervisors but also accountants, risk managers or actuaries within pension funds.

In what follows, we study a lesser-known feature of pension governance in the Netherlands: internal supervision. Internal supervision refers to an institutional arrangement through which those responsible for managing a pension fund (the governing board) are held accountable by a group of their peers (the internal supervisors). Taking inspiration from financial regulation studies, we maintain that internal supervision can be considered a type of ‘regulation from the inside’, while internal supervisors can be considered ‘internal regulators’. Drawing equivalence with professionals like risk managers and compliance officers in private (non-)financial firms, we suggest that internal supervisors occupy ambivalent positions within pension funds, albeit to different degrees depending on internal supervision’s institutional form. Amidst this institutional diversity, how do internal supervisors perceive of their roles? And how does internal supervision’s institutional design shape the supervisor’s relationship with other bodies in the fund? In what follows, we answer these questions by presenting findings from a survey and interview study among internal supervisors active in the Dutch pension system.

Internal supervision in the Dutch pension system

The function of internal supervision is a relatively recent addition to the Dutch system of pension governance. Introduced as part of the 2006 good governance code for the Dutch pension sector, internal supervision was initially not legally mandated. Schillemans (2008) attributes the rise of internal supervisory practices in the Netherlands to the ‘agencification’ of the Dutch public sector during the 1990s: the creation of independent agencies following the privatization of formerly public tasks. According to Schillemans, ‘the more or less programmatic creation of agencies in the 1990s was accompanied by policy-efforts [sic] to balance the loss of governmental control with additional accountability arrangements’ (ibid: 176). Other scholars, however, attribute the introduction of internal supervision to the broader corporate governance movement of the 1990s (Van Montfort and Boers, 2009). The first corporate governance code in the Netherlands was established in 1993 (Code-Tabaksblat). Following its introduction, the interest organizations of the Dutch pension sector began to formulate their own behavioural guidelines for good governance. These efforts resulted in the 2006 governance principles mentioned above.

Yet, the 2006 principles of pension governance were not as successful as sectoral parties had hoped for. A 2009 evaluation showed that 20% of Dutch pension funds in fact did not have a body for internal supervision in place. Of those funds that did, most opted for an external evaluation every 3 years (Tweede Kamer der Staten-General, 2009–2010). The financial losses incurred during the Great Financial Crisis, moreover, placed a new spotlight on pension fund governance, including the function of internal supervision. Politicians demanded stronger ‘checks and balances’ between the three functions of the pension funds, including a stronger authority for internal supervision to evaluate the board’s risk management policies. They also questioned the prevalence of external evaluation committees, which they deemed ‘too light’ to evaluate ‘the large financial risks that pension funds are exposed to’ (ibid.). The tasks and responsibilities of the different types of internal supervision were therefore incorporated in the Pension Act (Pensioenwet). Additional behavioural rules were formulated in the renewed Pension Fund Code (Code Pensioenfondsen, 2013), a collaboration between the Labour Foundation and the Pension Federation.

Internal supervision types by main characteristics.

The third type of internal supervision is found in pension funds with one-tier boards. In these funds, non-executive board members perform a supervisory role vis-à-vis the executive board members. Similar to the other two forms of internal supervision, non-executive board members report to the accountability body and to the employer. In addition, non-executive board members are responsible for the chairpersonship of the board, the nomination of candidate board members and the remuneration policy for executive board members. In contrast to supervisory council members and external evaluations, however, non-executive board members are by law considered ‘policymakers’ (beleidsbepalers) of the pension fund, because they are formally part of the pension fund board. In this capacity, they combine an administrative and a supervisory role within the fund.

The hybrid forms of internal supervision have proven popular: as of 2021, more than half of Dutch pension funds had a supervisory council (41%) or one-tier board (12%), with 33% of pension funds having a committee of external evaluators (De Nederlandsche Bank, 2023). The choice between a supervisory council or committee of external evaluators is decided by the fund’s governance model and size (for an overview of governance models, see Golka and Van der Zwan, 2022). A supervisory council is mandatory for most industry-wide funds with paritarian or independent boards. In a paritarian board, seats are distributed between representatives of the sponsoring employers and unionists representing members and retirees. In independent boards, by contrast, board members do not represent the constituencies of the pension plan, but are independent financial experts. Company pension funds with paritarian and independent boards and assets under managements up to €1 billion have the choice between a supervisory council or a committee of external evaluators. Company pension funds with assets under management over €1 billion are legally obligated to have a supervisory council.

Seen from an international perspective, the Dutch system of internal supervision is one of the most extensive supervisory regimes in Europe. The OECD Guidelines for Pension Fund Governance (2009: 6), for instance, state that ‘a separate supervisory board or oversight committee may be established whose main functions are the selection and oversight of the body in charge of strategic decisions’. According to the same guidelines, such a board ‘may form part of the internal governance structure of the pension entity (as in a two-tier board system) or it may be established externally’ (ibid.). An example of the former can be found in Germany and Austria, where an Aufsichtsrat combines the functions of the Dutch accountability body and supervisory council. Here, pension funds are incorporated, making their organizational structures similar to the dual board structures of large corporations. In Spain, an external comisión de control serves as an intermediary between the plan sponsor and the commercial administrators of the plan. The Netherlands differs from both systems in that it allows for internal supervisors to operate both within the pension fund and as an external body. This institutional variation allows us to study if and how internal supervisors’ position vis-à-vis other fund bodies, most importantly the governing board, shapes perceptions and practices of internal supervision.

When the new system for internal supervision was first introduced in Parliament, legislators had a clear view of what it needed to look like. Drawing an analogy with the distribution of power between different branches of government in democratic political systems, internal supervision had to be based on checks and balances (Tweede Kamer der Staten-Generaal, 2011–2012): (1) a clear demarcation of fund bodies (board, accountability body, internal supervision) to (2) guarantee independence of internal supervision, based on (3) a formalization of internal supervisors’ tasks and powers. Illustrative of this checks and balances perspective on internal supervision is the following statement by VITP (2021), the national association of internal supervisors in the pension sector: The pension sector is undergoing a transformation to a more modern management model with mature checks & balances…. Internal supervision is thereby developing into the countervailing power against a stronger and more independently operating governing board. A strong board therefore requires strong internal supervision that can grow with the continuing professionalization of the board.

Despite its focus on independence and formalization, the regulator has created new opportunities for boundary spanning by allowing certain internal supervisors to be located close to the pension fund board. How does this paradoxical institutional design shape internal supervisors’ perceptions of their tasks and responsibilities? Drawing on studies of financial regulation, we posit that the closer the internal supervisor is positioned vis-à-vis the pension fund board, the more ambivalent the supervisor’s role perception will be (Lenglet, 2012). Specifically, we expect that external evaluators are more likely to act as internal regulators, because they are situated outside the pension fund’s organization. Non-executive board members hold a dual position as internal supervisors and board members. We therefore expect them to act as boundary spanners (Mikes, 2011; Van der Voort et al., 2019). Supervisory council members occupy a middle position: they are at some distance from the board, but their advisory role offers them the possibility to be part of policy discussions. We expect supervisory council members to act more as boundary spanners than as internal regulators, yet to show more ambiguity than non-executive board members in how they interpret their roles. In what follows, we assess our expectations against the empirical findings from our survey and interview study.

Methodology

In this paper, we report the findings of our study on internal supervision in the Dutch pension system. Goal of the study was to assess the inner workings of internal supervision in Dutch pension funds, as part of the annual review of pension fund compliance with the Netherlands’ pension sector good governance code (Code Pensioenfondsen). The study was funded by the Monitoring Committee of the Pension Fund Code (Monitoringcommissie Code Pensioenfondsen). The Monitoring Committee was created in 2014 by the Dutch Labour Foundation, a consultative body of peak-level union federations and employer associations, and the Pension Federation, the main interest organization for the Dutch pension sector. The Monitoring Committee consists of four independent members and a chairperson. The task of the Monitoring Committee is to monitor and evaluate the implementation of the good governance code by Dutch pension funds. Each reporting year, the Monitoring Committee investigates a different aspect of the good governance code. For 2022, the focus of the Monitoring Committee was on the rules for internal supervision.

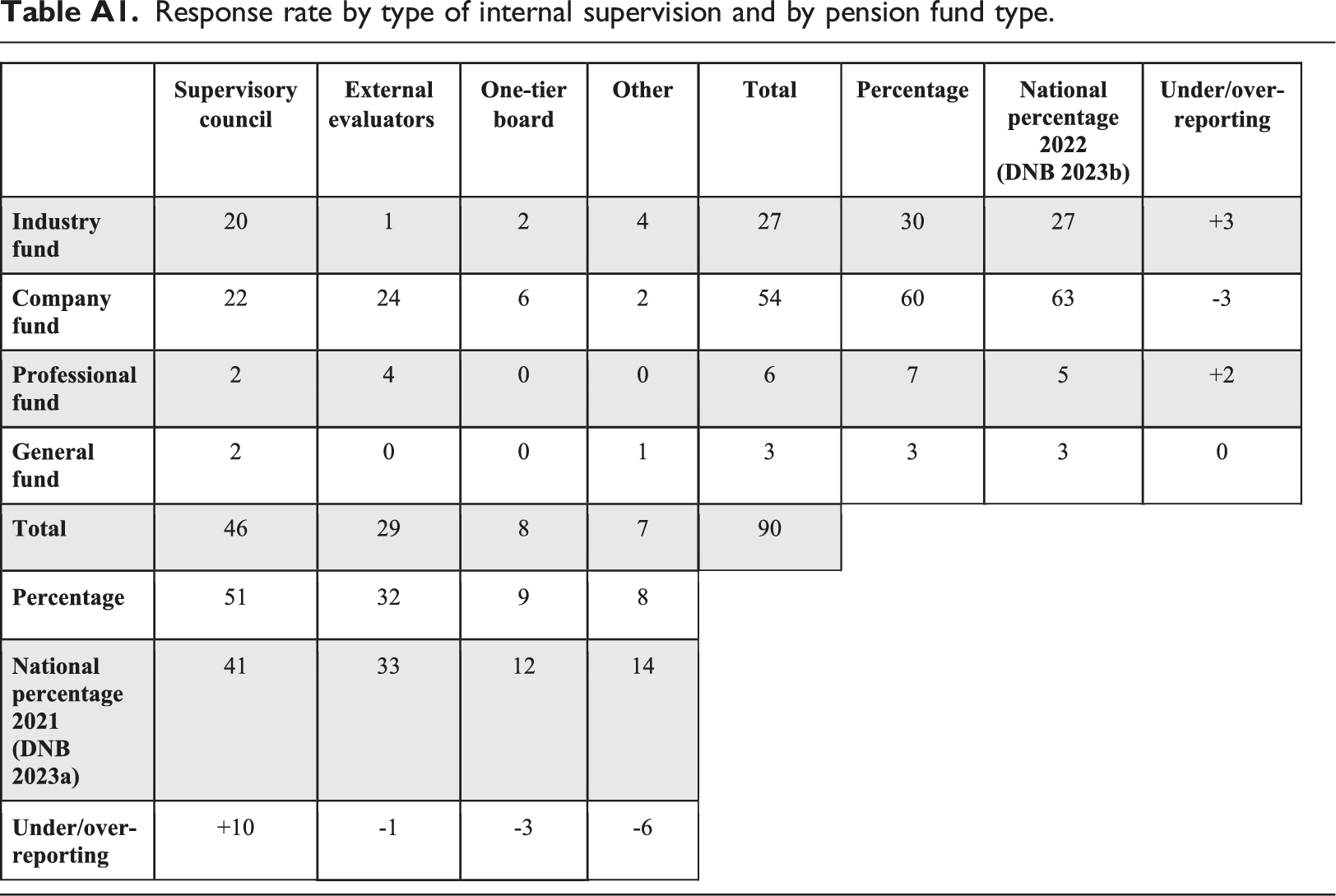

Our study consisted of a survey and in-depth interviews among internal supervisors in Dutch pension funds. All parts of the study were conducted in Dutch. Our partner organization, the Monitoring Committee of the Pension Fund Code, used its mailing list with contact information for 181 Dutch pension funds to invite the chairpersons of the supervisory bodies to voluntarily participate in our study. The invitation contained a link to an online consent form and survey, which participants were asked to complete. All participants were informed about the aim of the study, the confidential treatment of survey data and the use of research findings. Participation in the survey was voluntary and respondents did not receive compensation for participation. We received 124 submitted surveys. Of those, 34 were excluded from our sample, because they were incomplete or filled out by more than one person from the same pension fund. Our sample consisted of 90 surveys, yielding a response rate of 50%.

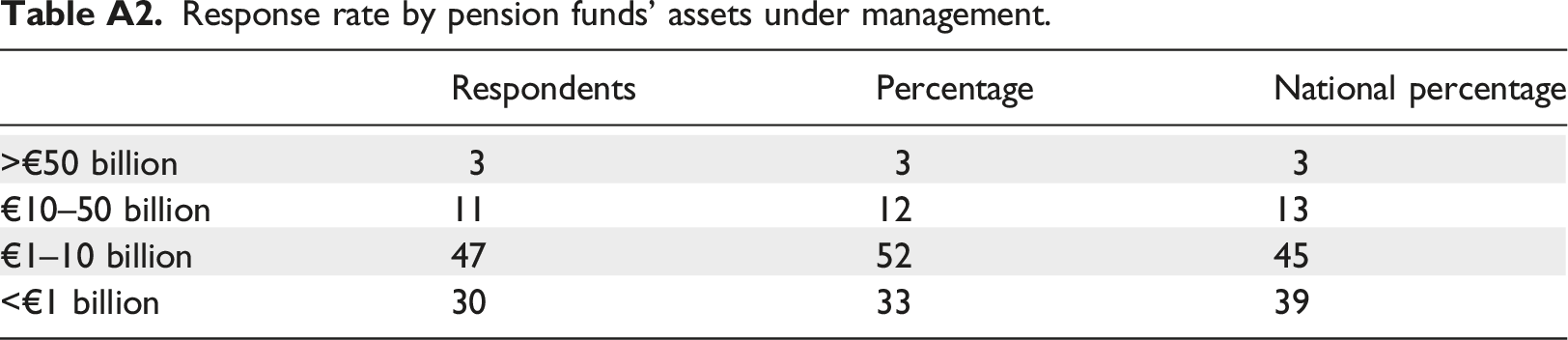

The response rates are largely consistent with the national prevalence of each form of internal supervision in the pension sector. Half of our respondents are active as supervisory council members, while around a third serve as external evaluators (see Table A1). We received few responses from non-executive board members. Consistent with the legal rules for internal supervision, respondents from supervisory councils are mostly active in industry-wide and company funds, while external evaluators are almost exclusively found in company funds. Compared to national data, our survey has a slight overrepresentation of industry-wide funds and a slight underrepresentation of company funds. We also see a slight overrepresentation of mid-sized pension funds and underrepresentation of the largest pension funds in the Netherlands (see Table A2). 2 Our findings may be less applicable to supervisors from these underrepresented funds.

Our survey consisted of both closed and open-ended questions. Closed questions either offered respondents a selection of nominal answer categories to choose from, or presented them with Likert scales to indicate agreement/disagreement with a particular statement. We then conducted a basic statistical analysis, using descriptive statistics to identify frequencies and make cross-tabulations of our data. The open survey questions typically asked respondents to clarify previously given answers or to describe specific practices. Answers to open-ended questions were first coded to identify prevailing answer categories, using open coding and axial coding. We then coded the answers again by type of internal supervision to identify underlying patterns. All survey items (translated from the original Dutch) can be found in Appendix B.

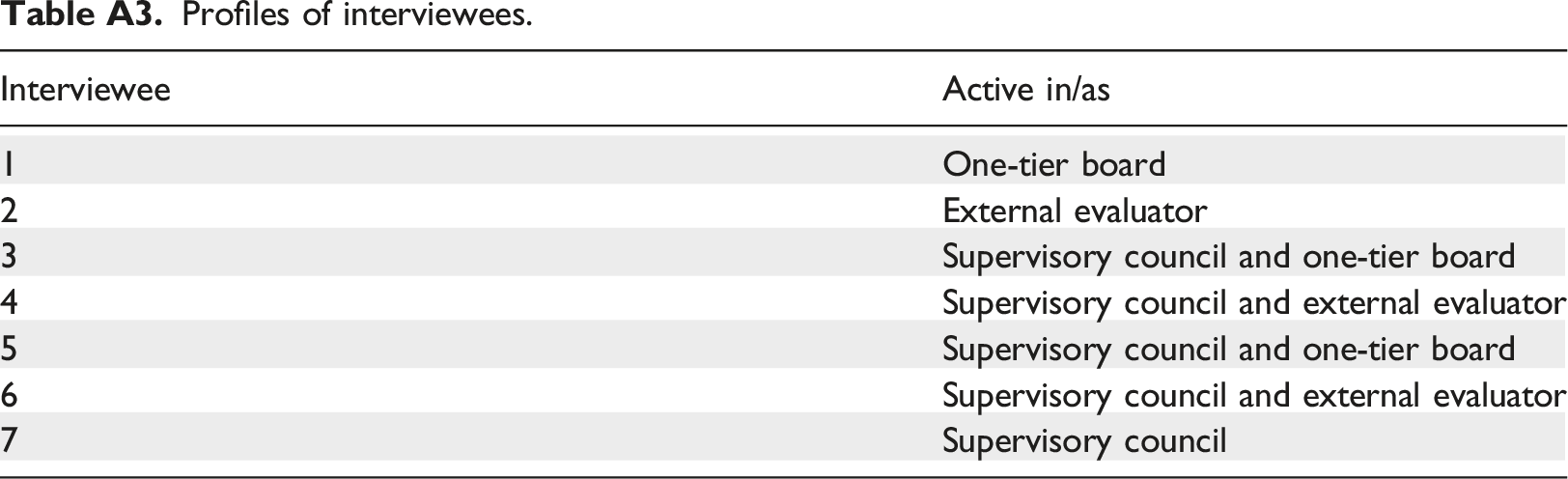

In addition to our survey, we conducted seven semi-structured interviews with internal supervisors (for anonymized profiles of the interviewees, see Table A3). Purpose of the interviews was to gain a deeper understanding of our survey results and to identify good or best practices for internal supervision. Interviews took place in July and August 2021. All interviews were conducted online. Interviews were conducted in Dutch. Prior to the interview, interviewees were asked to complete a consent form, in which they were informed about the aims of the study and use of research data. All interviewees agreed with being recorded and directly quoted in our research reports. After each interview, the recordings were transcribed verbatim. Transcripts were then anonymized, to protect the identities of the interviewees.

Two views on internal supervision

Departing from the legislator’s expectations, our research results show that internal supervision in the Netherlands can only partially be characterized by checks and balances between the various fund bodies. To be sure, a substantial number of respondents also adheres to the checks and balances view of internal supervision. These respondents mentioned the need to avoid ‘sitting in the seats of the governing board’, valued the process of holding the board accountable and emphasized formal reporting. Yet, a second group of respondents in our study emphasized communication, informal knowledge exchange and having an open culture with other fund bodies. Typical for this group of respondents is boundary spanning between supervisory and organizational functions, as expressed by a desire ‘to be a sounding board’ or ‘sparring partner’ for the governing board. We therefore dubbed this perspective the fusion of powers approach to internal supervision. In what follows, we elaborate on each perspective and suggest two possible explanations for the hybrid character of internal supervision in the Dutch pension sector.

Two approaches to internal supervision

Central to Dutch pension fund governance is the so-called ‘balanced representation of interests’ (evenwichtige belangenbehartiging). According to Art. 105 of the Pension Act, this requires fund officials to ensure that participants, retirees and employers ‘feel’ represented in a balanced manner. This principle is applicable not only to members of the governing board but also to members of the accountability body and to internal supervisors. A balanced representation of interests is generally seen as a prerequisite for guaranteeing the fund members’ trust. The Pension Fund Code, for instance, requires that ‘those who carry responsibility for the pension fund realize the trust placed in them’ (Pensioenfederatie and Stichting van de Arbeid, 2018: 13).

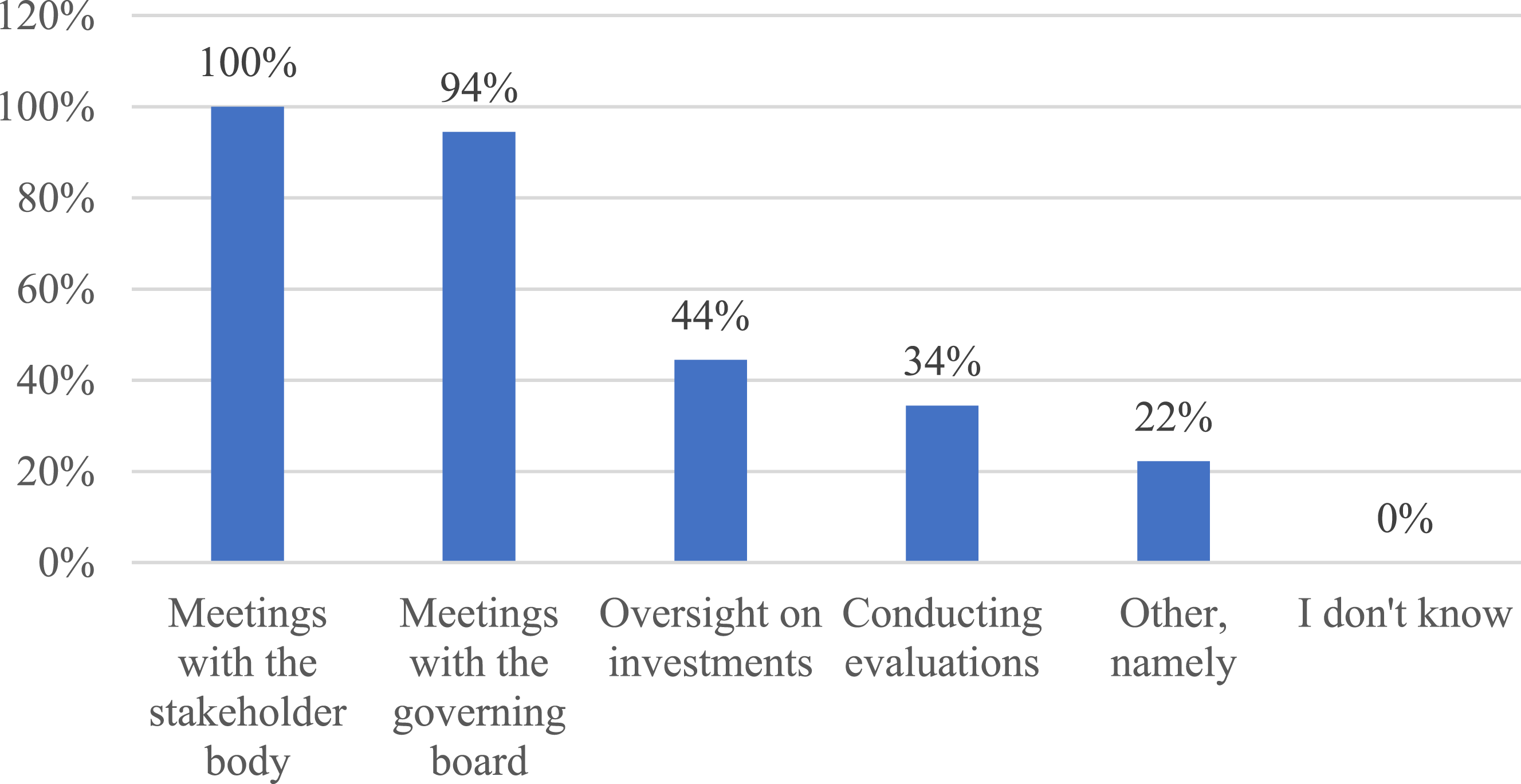

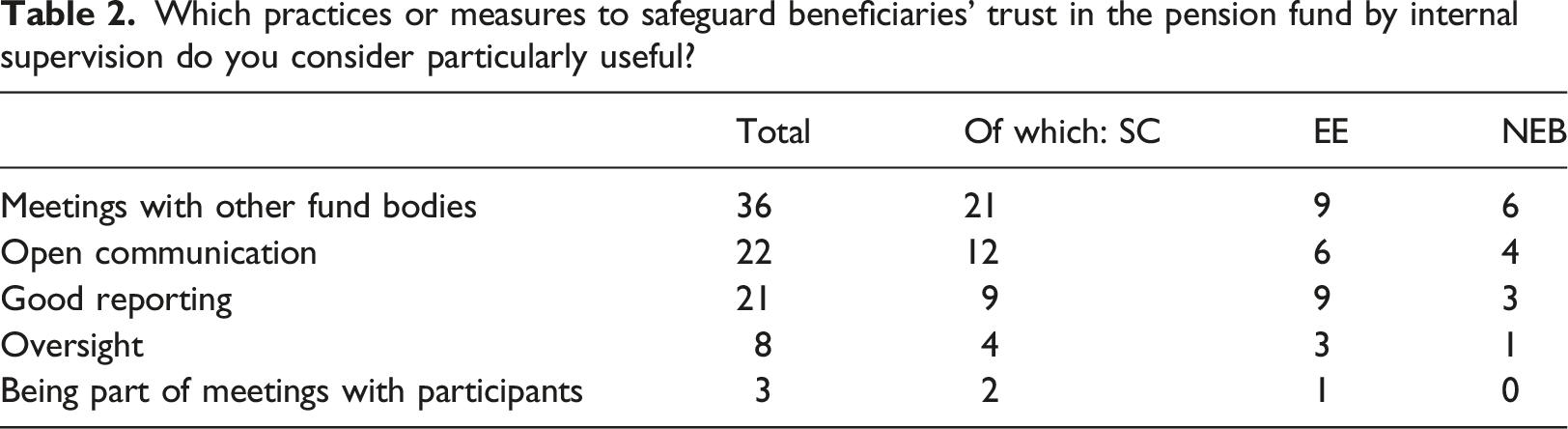

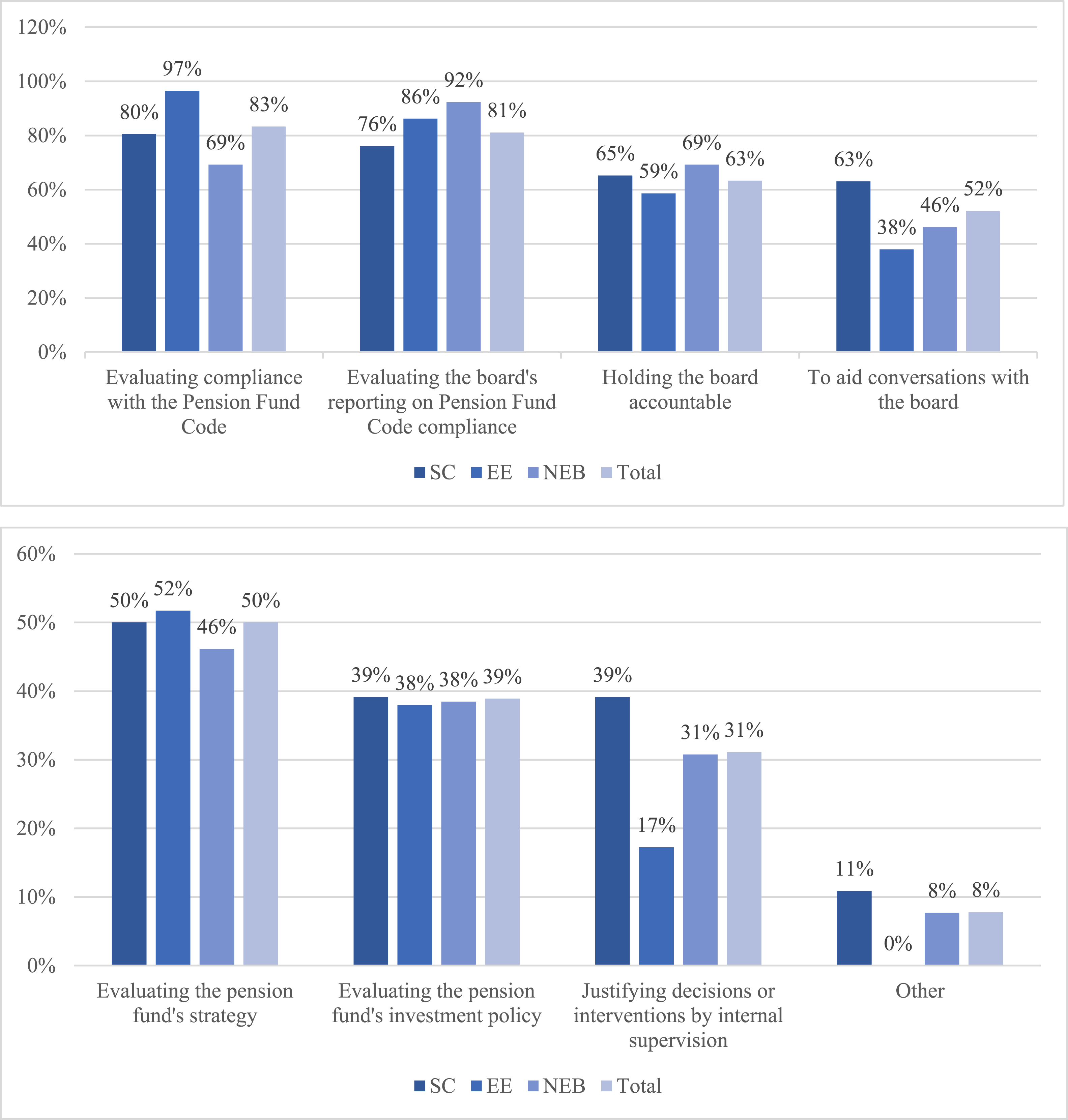

When asked about internal supervision’s activities to ensure that their organization realizes members’ trust (see Figure 1), supervisors mentioned meeting with the accountability body (100%) and the governing board (94%). Surprisingly, a much lower percentage of respondents mentioned oversight of the investments (44%). Only a minority of internal supervisors would also try to assess the effect (36%) of measures taken by the pension funds to ensure the beneficiaries’ trust; here, supervisory council members scored (26%) considerably lower than non-executive board members (46%) and external evaluations (45%). A similar pattern is visible in answers to the question ‘Which practices or measures of internal supervision do you experience as particularly useful to ensure beneficiaries’ trust in the pension fund?’ (Table 2). Here, the most commonly given answers were (1) meetings with other fund bodies; (2) open communication; and (3) good reporting. Again, oversight of investments or risk management received relatively limited attention, when compared to other answers. What does internal supervision do to safeguard that the organization takes care of beneficiaries’ trust in the pension fund? Which practices or measures to safeguard beneficiaries’ trust in the pension fund by internal supervision do you consider particularly useful?

When further analyzing these results, internal supervisors can be divided into two groups. Supervisory council members and non-executive board members in particular emphasized dialogue with other fund bodies and informal knowledge exchange. Here, respondents mentioned advisory practices such as ‘soundboarding’, ‘sparring’ and ‘benchmarking’. One internal supervisor noted, for instance: ‘It is important that internal supervision is not only oversight but is also a sounding board that advises and thinks along, and that is open to learning together. There is already enough supervision’. To facilitate this, supervisors would not only attend meetings of the governing board but also of its subordinate (and more technical) committees. They were also more likely to reach out to fund participants, for instance, by attending participant meetings, and to scrutinize the fund’s communication policies. Another internal supervisor stated: ‘I find it particularly useful to be present as a listener during the communication committee and the investment committee [meetings], to follow the actions of the communication committee and the information on the website’.

The second group of supervisors, consisting mostly of external evaluators and supervisory council members, were more explicit about achieving trust through the supervision process itself, based on a clear framework of standards, and through the communication in the annual report. These supervisors mention discussing their recommendations with the board and the accountability body, but do not undertake additional activities to better understand participant preferences. Instead, knowledge about the participant base is retrieved from existing information sources such as the annual report. This is a surprising finding, because particularly from a checks and balances perspective one would expect that supervisors are keen to gather their own information regarding participant preferences and monitor their implementation in financial investments. Instead, these internal supervisors largely exert control by defining the profiles for candidate board members, including testing candidates’ suitability, and by giving the board recommendations. The following quote by an internal supervisor represents this checks and balances perspective on internal supervision: They [the board] leave us in our role and we leave them in their role too. We raise [the issue], [because] we think it’s important. And if we find it very important, then we do it again - year after year - in our report and in our conversations. But in the end, it is the board that is in charge.

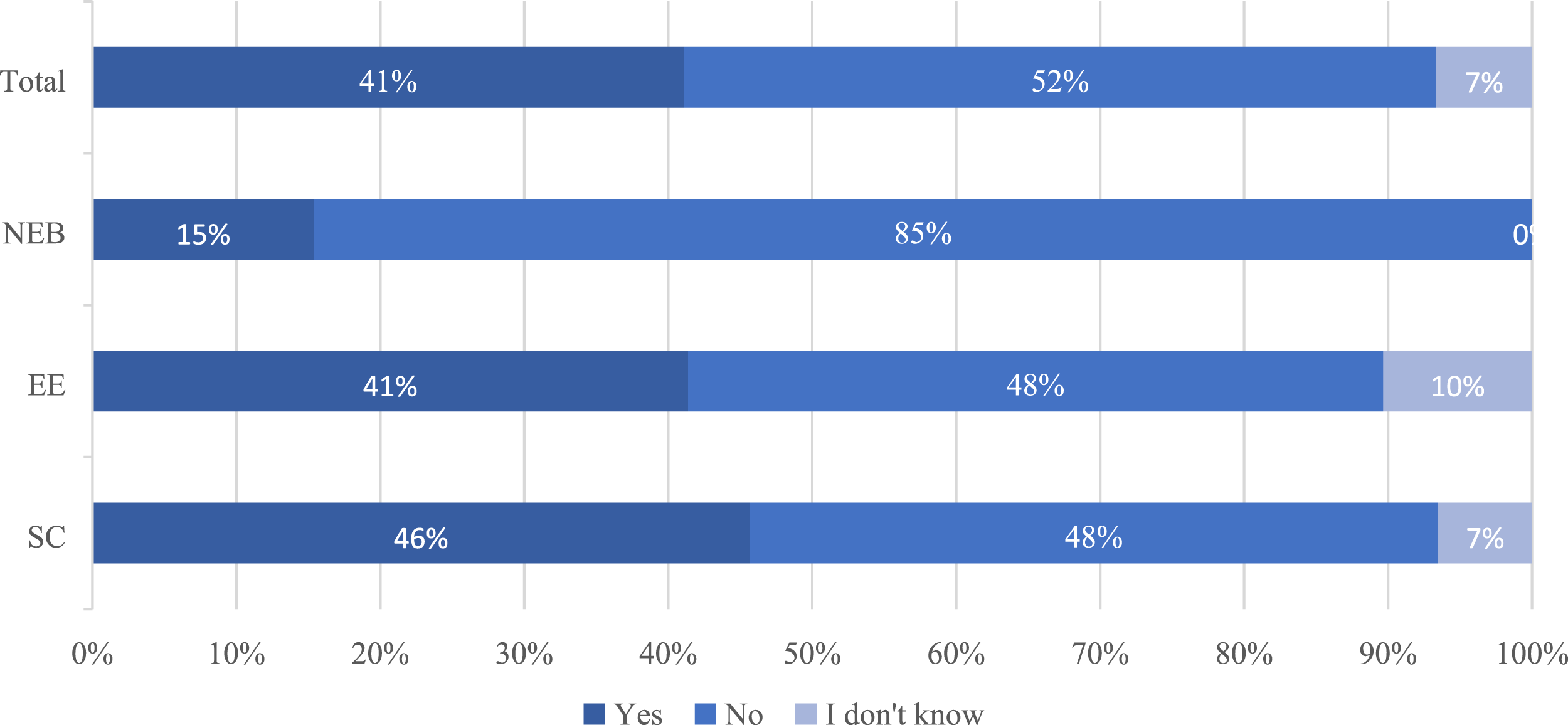

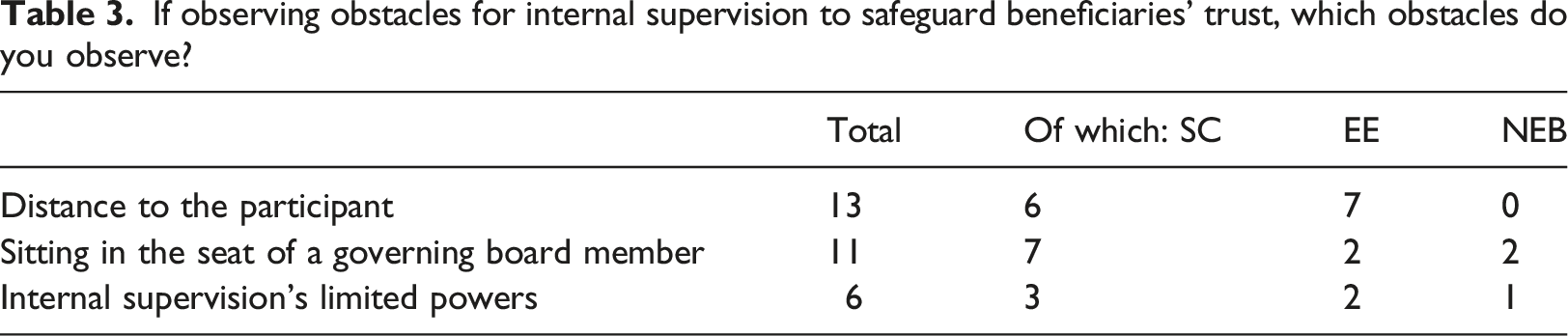

When asked about perceived obstacles for internal supervision to contribute towards the realization of member trust (Figure 2), most respondents did not identify any obstacles (52%). In their answers to the question ‘Do you perceive obstacles for internal supervision to play a larger role in ensuring beneficiaries’ trust?’, non-executive board members were more likely to answer ‘no’ (85.0%) than supervisory board members (48%) or external evaluators (48%), possibly because they have more direct access to information from the board. Where respondents did perceive obstacles (41%), answers could again be divided into the two main views of internal supervision (Table 3). Most mentioned was the perceived distance of internal supervision from the fund members, followed by the risk of interfering with the board’s actions and a perceived insufficiency of available legal instruments to provide oversight of the board. Distance from the participants was most often mentioned by supervisory council members and external evaluators: while the former more often emphasized the difficulty of entering a discussion with fund members, the latter more often emphasized the annual character of the oversight process. Supervisory council members were more fearful of interference with the board than non-executive board members and external evaluators Do you observe any obstacles for internal supervision to play a bigger role in safeguarding beneficiaries’ trust? If observing obstacles for internal supervision to safeguard beneficiaries’ trust, which obstacles do you observe?

At face value, it would make sense to associate the checks and balances perspective with external evaluators and the fusion of powers perspective with supervisory council members and non-executive board members, as the latter have the legal mandate to advise the pension fund board in addition to providing oversight. However, our study does not confirm such a clear separation: while the checks and balances perspective is indeed found more often among external evaluators (albeit certainly not exclusively), supervisory council members show a more mixed picture. The latter is also observable among non-executive board members: our study shows that non-executive board members are strongly aware of the importance of role retention and independence from executive board members. At the same time, they also express difficulty in maintaining such a clear separation in practice. Noted one internal supervisor: ‘If you are primarily a very good board member, you are not by definition a good supervisor. It requires a different role. You have to wear that hat in a different way’.

The political economy of internal supervision

Which factors could explain why a fusion of powers perspective on internal supervision has emerged in addition to the checks and balance perspective intended by Dutch lawmakers and regulators? While our study does not seek to explain the views held by internal supervisors, our results signal two developments that have contributed towards creating the hybrid system of internal supervision identified above: (1) the highly networked nature of the Dutch pension sector, which shapes recruitment practices and creates the foundations for informal knowledge exchange; and (2) legal and regulatory uncertainties stemming from ongoing pension reforms.

First, the close relationships between internal supervisors and pension fund board members as described above should be seen against the social composition of the Dutch pension sector. Internal supervisors are typically recruited from within the pension sector itself. This has two reasons. First, the 2013 Pension Fund Code introduced term limits for pension board members. Under Norm 60, board members’ terms were restricted to periods of 4 years, to be renewed twice at most. The introduction of this norm meant that a considerable group of board memberships would not be renewed upon expiration of the term, creating an influx of pension administrators in need of new functions. Second, the simultaneous strengthening of suitability requirements by the Dutch Central Bank in 2012 reduced the pool of available candidates, as few individuals from outside the pension sector possess the necessary expertise to qualify as internal supervisors.

As a result, the Dutch pension sector is characterized by a complex web of overlapping functions due to ancillary positions, whereby internal supervisors also often serve as board members of other funds. The pension regulator uses the so-called VTE (full-time equivalence) score during its suitability checks of board members and supervisors to assess the time constraints of each function. VTE scores differ by function and by size of the fund. A chairpersonship of a large pension fund, for instance, equals 0.6 VTE, while a chairpersonship of a supervisory body is 0.2 (large and small funds) and a membership is 0.1 VTE. Pension professionals are not allowed to have a VTE score that exceeds 1.0. In our sample, the average VTE score was 0.49. This means that, on average, our respondents hold between two and three supervisory functions or combine a supervisory role with a board membership of a small or large pension fund.

The highly networked nature of the Dutch pension sector has made it difficult for sector outsiders to take up positions as pension fund board members or internal supervisors. For this reason, the Pension Fund Code calls upon all pension funds to include at least one woman and at least one person under the age of 40 on the board and in the supervisory body. Nevertheless, only one third of pension funds fulfilled both these criteria for the governing board in 2020 (no data available on supervisory bodies), while 13% of funds neither had a woman or a person under 40 on the governing board (Monitoringcommissie Code Pensioenfondsen, 2022: 12). 3 Ensuring diversity within the pension fund is also internal supervision’s responsibility, albeit not exclusively: first, in light of its formal task to approve the candidate profile for the pension board and second, as internal supervision is subject to the Code’s diversity rules itself.

According to our respondents, the recruitment of persons under 40 years of age is particularly challenging. Internal supervisors attribute this difficulty to the stringent suitability criteria of the Dutch Central Bank: younger people are less likely to have acquired the knowledge and expertise required of pension fund officials. They are also less likely to have time available to take on board positions or supervisory tasks due to other work and care commitments. By contrast, many of the internal supervisors that we surveyed or interviewed are professionals who came to their role either through professional careers in the pension industry, or by holding supervisory roles in one of the various industries where similar supervisory functions are mandated by law. They either work as freelancers or are associated with specialized bureaus. This is particularly the case for external evaluators.

Yet, at the same time, respondents recognized that the pension sector itself is complicit in creating and sustaining existing networks of fund officials. One important factor here are the expertise requirements for most governing functions of pension funds (including internal supervision) that are defined and evaluated by the Dutch Central Bank. Recognizing that younger or less experienced candidates may require a longer learning process is a necessary criterion here, but should not be seen as an impediment to a candidate’s potential. Indeed, as pension funds are increasingly ascribing value to the different perspectives younger candidates bring to governing functions, this seems to be subject to change. This is even more so as the pension sector is increasingly organizing ‘breeding pools’ to allow candidates to gain necessary qualifications at a younger age. However, even as such initiatives may prove effective in recruiting persons under 40 years of age, they also contribute to a further tightening of networks between governing functions that may subsequently strengthen the fusion of power approach.

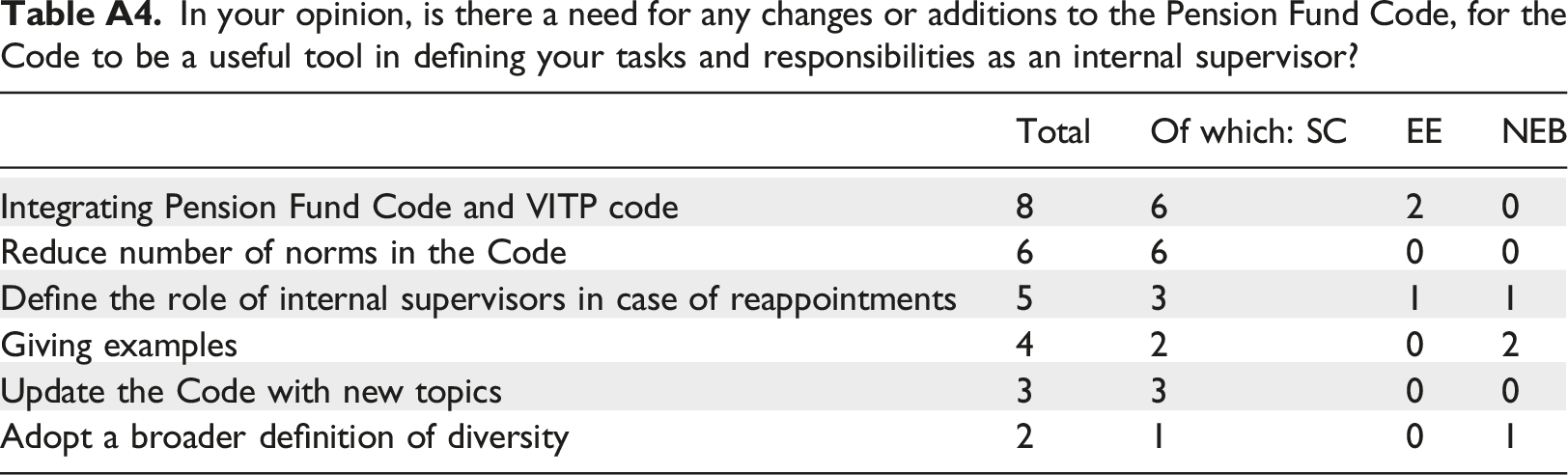

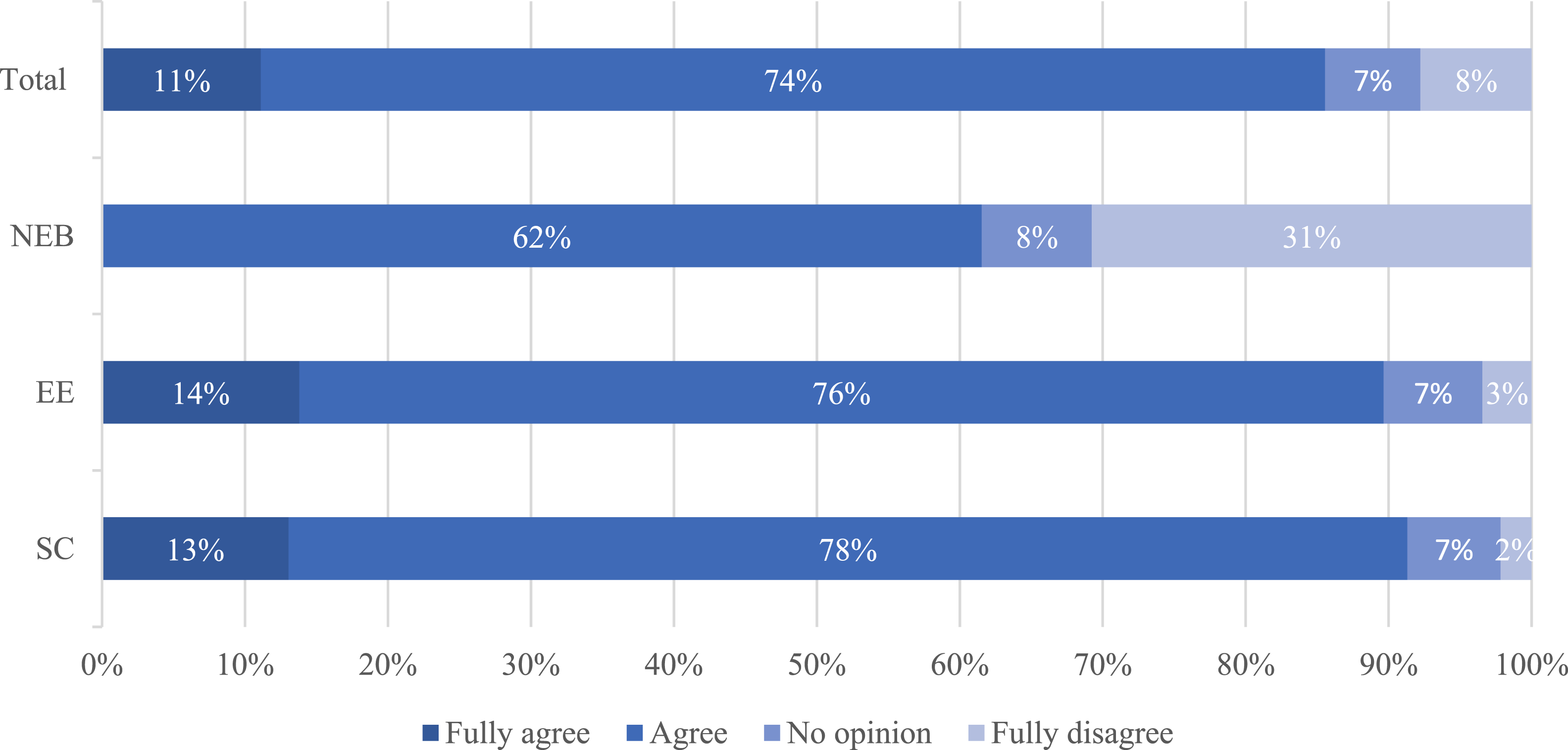

A second development incentivizing the fusion of powers approach to internal supervision are legal and regulatory uncertainties. Respondents mentioned these uncertainties in two instances: (1) in relation to the Pension Fund Code and (2) in relation to ongoing reforms in the Dutch pension sector. First, we asked survey respondents about their use of the Pension Fund Code (see Figure A1). The majority of respondents (83%) used the Code in their supervisory duties and considered the Code a useful tool (85%) (see Figure A2). Still, when asked about potential improvements to the Code, respondents emphasized (1) overlap of the Code with other professional standards (in particular, the behavioral code of the VITP); (2) the length of the Code; and (3) the difficulty of applying abstract behavioral norms to concrete everyday situation. Supervisory council members more often mentioned the first two issues, while non-executive board members more often desired concrete examples of implementing Code norms (see Table A4).

Second, internal supervisors are collectively affected by the pension reform currently underway in the Netherlands. As part of these reforms, the current DB system will be transformed into a collective DC system. This major transformation poses considerable uncertainties for pension funds, also including internal supervisors. To deal with these uncertainties, internal supervisors mentioned seeking out the opinions of their peers. Said one interviewee: ‘[The main] example is of course the new pension contract. Then we invite the board to involve us, because of course we have – myself, but my fellow council members often, too – they are also active in other funds. So you can take advantage of that, to bring out all aspects very clearly’ (Interview 4). Thus, supervisors resort to a fusion of power approach to deal with uncertainties arising from pension reform together with the pension fund boards.

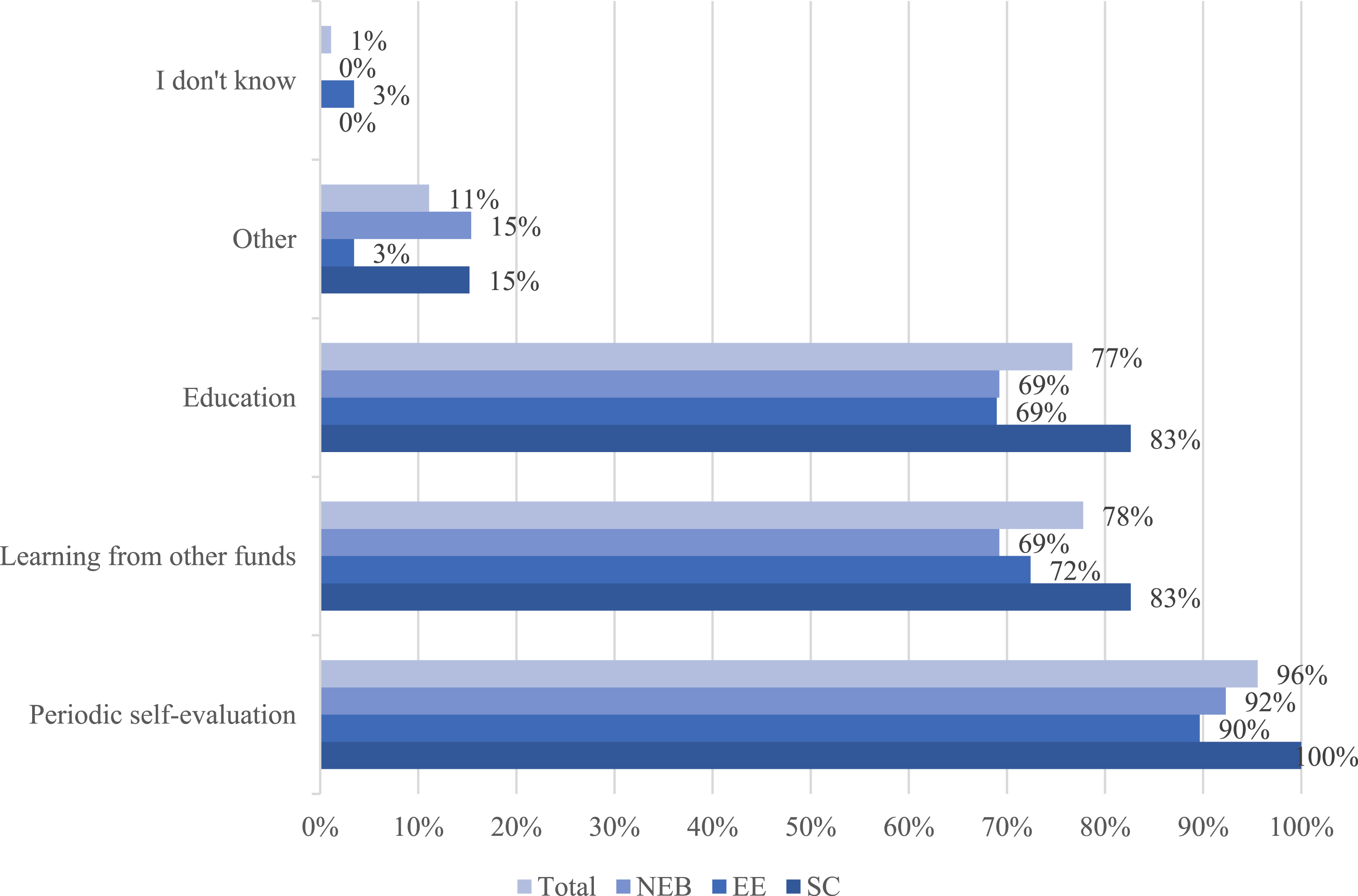

Internal supervisors seek the solution to both perceived problems in informal knowledge exchange within and outside the pension fund. When asked which measures internal supervision took to learn about new developments (Figure 3), 78% indicated learning from other funds: supervisory council members (83%) more so than external evaluators (72%). A number of respondents here explicitly referred to their ancillary functions, for instance: ‘Because we fulfill roles at various funds, a broad picture is available collectively’. Others mentioned attending organizing knowledge sessions or holding peer review meetings with other internal supervisors: ‘There are many case histories and webinars. It all helps to give more substance to that missing link of all those formal codes and legislation’. It’s noteworthy that most exchanges are with other internal supervisors from within the pension sector. Where respondents had gained supervisory experiences in other sectors, they complained that their fellow internal supervisors rarely valued learning from those other sectors and avoided knowledge exchanges beyond the pension industry. Which measures do you take to ensure that internal supervision itself is a learning part of the organization?

Linking the models of internal supervision with the availability of financial professionals on pension fund boards in our sample provides further support for this hypothesis. Our study revealed that financial professionals play a much stronger role on pension fund boards in funds with supervisory councils and one-tier boards, but much less so in funds featuring external evaluators. While only 1 of 23 Dutch pension funds using external evaluators had independent financial experts as members of their governing board (4%; no data for 6 funds in sample), this was the case for 21 of the 40 funds using a supervisory council (53%; no data for 6 funds in sample) as well as – by legal definition – for all funds using one-tier boards. 4 The presence of financial experts on governing boards of pension funds with supervisory councils and one-tier boards may point to tightening networks between financial experts and boundary spanning internal supervisors, although further research into daily interactions will be needed.

Discussion and conclusion

In this paper, we approached the topic of pension governance from the perspective of internal regulation within pension funds. To this end, we studied how the idea of the Dutch legislator to introduce internal supervision and building a countervailing power to pension fund boards has been put into practice. Financial losses following the Great Financial Crisis had significantly undermined trust in and thus the legitimacy of the financialized pension system. At first sight, the introduction of internal supervision and its formal powers has created a system of horizontal accountability, whereby internal supervisors provide ‘checks and balances’ to pension fund decision-making to ensure safeguarding of member preferences. However, our empirical analysis has revealed, that, in practice, internal supervision often – albeit not always – follows a ‘fusion of powers’ approach, whereby supervisors take more of an advisory rather than an oversight role. We attribute the emergence of this alternative view on internal supervision not merely to institutional design, but also to a decoupling of professional practices that occurs within pension funds.

The decoupling of the practice of pension fund governance from the idea of checks and balances also has implications beyond individual pension funds. As internal supervision offers a side job for former or part-time board members, it becomes a vehicle for interlockings across the pension sector. This creates a system of interlocking memberships of governing boards and supervisory bodies similar to interlocking directorates among industry corporations. As acknowledged in the large literature on interlocks, these networks play an important coordination role (e.g. Mizruchi, 1996; Lütz, 2005; Heemskerk, 2013) and increase the overall coherence and organizational density of the pension sector (Davis, 1996). This also corresponds to our finding that financial professionals play a much smaller role on those pension fund boards where external evaluators are tasked with internal supervision. Internal supervisors’ decoupling from the checks and balances perspective intended by the regulator thus seems to be linked to a tightening of financial professionals’ network structures within the pension industry.

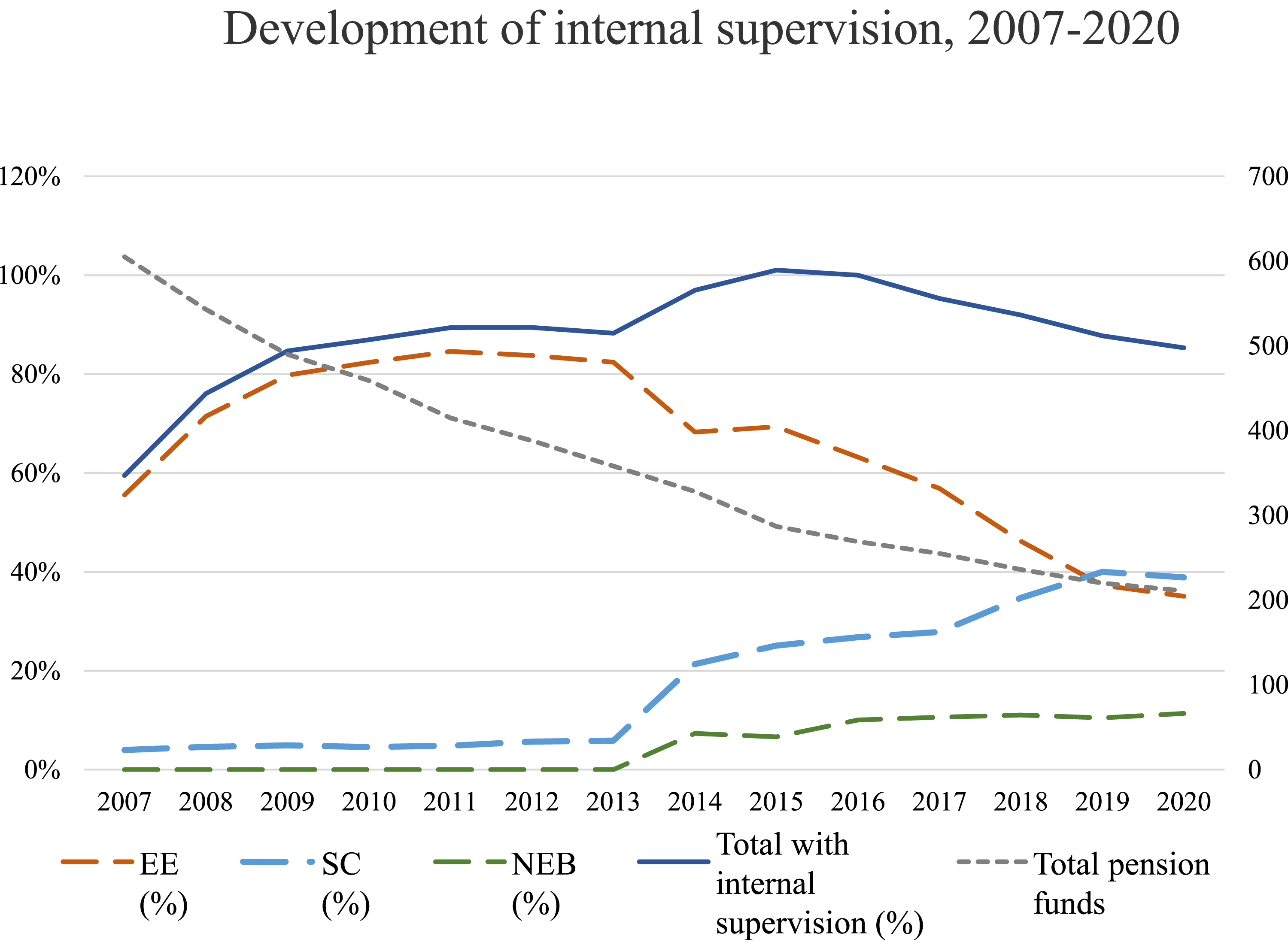

Such dynamics may be exacerbated in the future. In recent years, ongoing consolidation of the Dutch pension sector, whereby smaller pension funds have merged with larger ones, has meant that more funds are legally obligated to have a supervisory council. In addition, a growing number of pension funds have switched from paritarian or independent governance models to one-tier boards, including top-5 funds such as metalworkers’ fund PME (2014) and public sector fund ABP (2022). As a result, the number of pension funds with supervisory councils and one-tier boards has grown (see Figure A3), while committees of external evaluators are on the decline. Given the former’s proclivity for boundary spanning, a further weakening of internal supervision as independent oversight body may occur. Instead, internal supervision may evolve as a third kind of advisory and/or decision-making body within the pension fund, alongside the governing board and the accountability body.

We believe our findings may have several implications for pension governance in the Netherlands. First, conflicts of interest between the pension fund board and internal supervision may reinforce existing problems in the Dutch pension sector, if close ties between both bodies mean that internal supervisors are less likely to hold board members accountable. One area of concern, for instance, is the pension fund board’s relationship vis-à-vis its asset management firms. In recent years, Dutch pension funds have been strongly criticized for the growth in their asset management fees, particularly due to bonus payments made to private equity firms. In 2021, for instance, asset management fees for the Dutch pension sector doubled to a staggering €13.4 billion, despite great variety in investment returns The size of the bonus payments as well as the absence of a so-called malus in case of negative returns led to critical questions from, among others, Dutch parliamentarians (Sie, 2022). Given the substantial public debate surrounding asset management fees, it is surprising that few internal supervisors in our survey mention the importance of monitoring the board’s investment policies (see Figure 1).

Second, although the Netherlands has a highly institutionalized system of member representation, the proximity of internal supervision to pension fund boards may nevertheless weaken the voice of the representative body in practice. While internal supervision formally works for the accountability body, which represents active members and retirees of the fund, many internal supervisors perceived their main duty as an advisory role to the governing board. Such a role perception may lead to biases, for example, when member preferences are collected indirectly via the board rather than directly from members or from conversations with the accountability body. Recent years have also seen growing criticism of accountability body members for their perceived lack of expertise on pension matters. Where governing board members prefer internal supervisors over accountability board members as their main conversation partners, internal supervision may start to gradually replace the accountability body as main advisory body in the fund.

Both implications – a reinforcement of existing problems and a further weakening of the pension fund’s representational function – might point to an important accountability gap, that can only be identified through empirical studies of pension fund governance in practice. Our study has shown that practices of internal supervision vary significantly between pension funds. While these variations are informed by the funds’ organizational model, they cannot be reduced to it. As these internal dynamics are known to also affect politico-economic dynamics on the macro level such as financialization (Golka and Van der Zwan, 2022; Pernell et al., 2017), we call for more empirical political economy scholarship into the organizational practices of financial governance.

Our study also reveals the need for new legislative and regulatory actions. The legislator should, for instance, critically consider to what extent the co-existence of three types of internal supervision is necessary for the internal oversight of Dutch pension funds. The legislator should also clarify its expectations regarding the balanced representation of members’ interest. To what extent, for instance, should member preferences be incorporated in pension fund decision-making? How should internal supervision monitor this? And can internal supervision itself be held accountable by member representatives within the accountability body? The regulator, meanwhile, could reduce its focus on individual suitability of board members or internal supervisors and instead focus on the very recruitment practices that make the sector closed off to outsiders. Together, such measures can ensure that Dutch pension funds can maintain their unique characteristics as representative bodies, while successfully operating within the complex environment of global financial markets.

Footnotes

Acknowledgements

This project has benefited tremendously from excellent research assistance by Aalt-Jan Smits. We would like to thank the Monitoringcommissie Code Pensioenfondsen (MCPF) for their support, as well as participants of the Second LawFin Workshop ‘The Metamorphosing Landscape of Investors’ Capitalism’ at Goethe University Frankfurt, 13–14 December 2021 for their feedback on earlier versions of this paper. Our thanks also go out to the editors and three anonymous reviewers for their constructive feedback on this paper. All errors remain our own.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported in part by the Monitoringcommissie Code Pensioenfondsen (Funding to conduct annual review of Pension Fund Code).

Notes

Tables and Figures.

Response rate by type of internal supervision and by pension fund type.

Response rate by pension funds’ assets under management.

Respondents

Percentage

National percentage

>€50 billion

3

3

3

€10–50 billion

11

12

13

€1–10 billion

47

52

45

<€1 billion

30

33

39

Profiles of interviewees.

Interviewee

Active in/as

1

One-tier board

2

External evaluator

3

Supervisory council and one-tier board

4

Supervisory council and external evaluator

5

Supervisory council and one-tier board

6

Supervisory council and external evaluator

7

Supervisory council

In your opinion, is there a need for any changes or additions to the Pension Fund Code, for the Code to be a useful tool in defining your tasks and responsibilities as an internal supervisor?

Total

Of which: SC

EE

NEB

Integrating Pension Fund Code and VITP code

8

6

2

0

Reduce number of norms in the Code

6

6

0

0

Define the role of internal supervisors in case of reappointments

5

3

1

1

Giving examples

4

2

0

2

Update the Code with new topics

3

3

0

0

Adopt a broader definition of diversity

2

1

0

1

For which activities do you use the Pension Fund Code?

Answers to the statement ‘I find the Pension Code a useful tool to define my tasks and responsibilities as internal supervisor’.

Development of internal supervision, 2007–2020. Source: De Nederlandsche Bank 2023 Organisatie & Pension Funds Governance pensioenfondsen. DNB Toezichtsdata. Available at: www.dnb.nl/statistieken (accessed 23 January 2023).

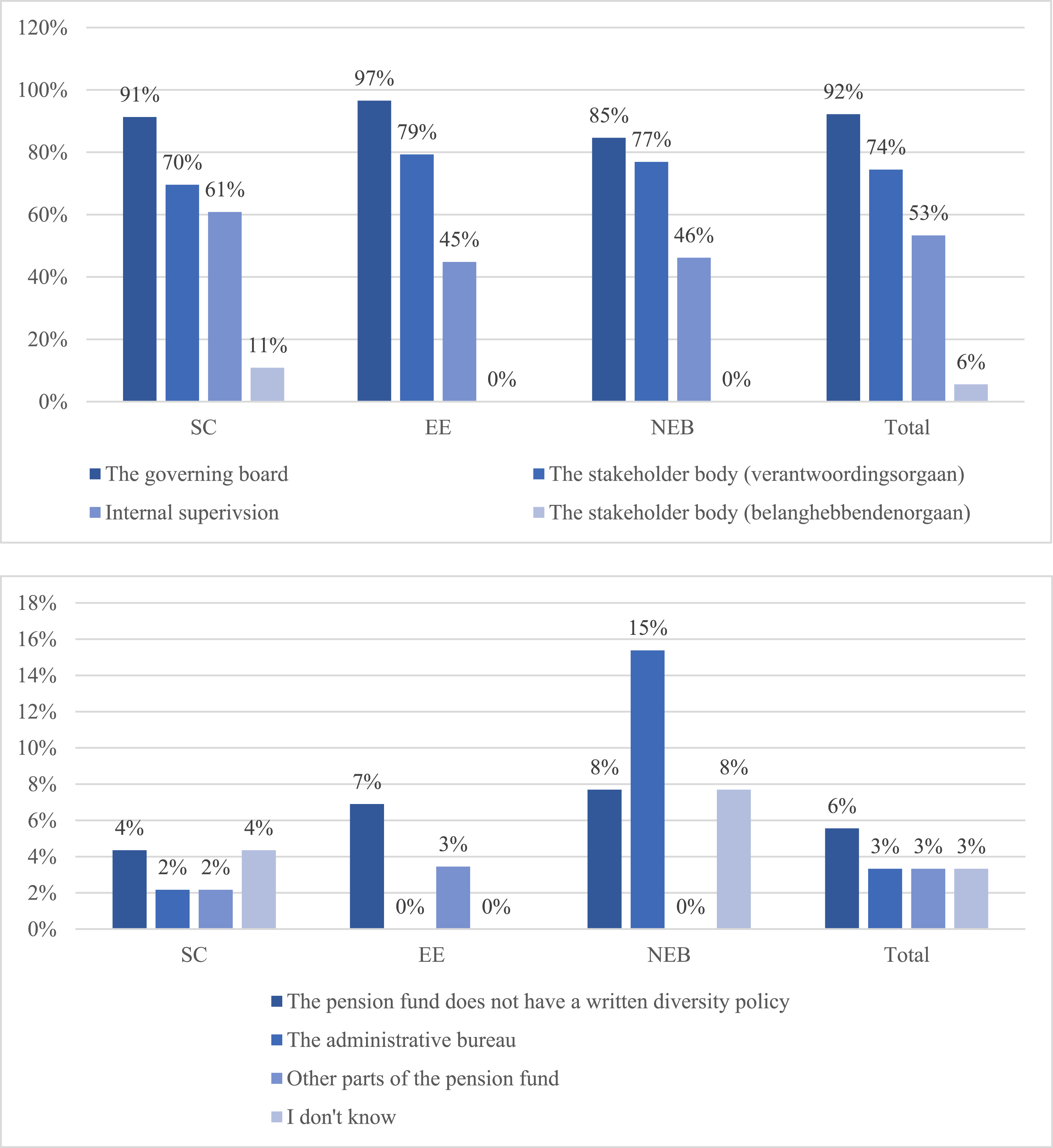

For which parts of the organization does the pension fund have a written policy and concrete goals to safeguard diversity?

Survey questions (translated by the authors from the original Dutch)

Part 0: General information 1. For which pension fund are you filling in this questionnaire? Type in your answer. 2. Which position do you hold within the pension fund? Select: chair of the supervisory council; member of the supervisory council; chair of the committee of external evaluators; member of the committee of external evaluators; non-executive board member; other, namely. 3. What is the pension fund’s fund type? Select: company pension fund; industry-wide pension fund; professional pension fund; general pension fund; other, namely. 4. Which governance model does the pension fund have? Select: paritarian non-mixed; independent non-mixed; paritarian mixed; independent mixed; reversed mixed; I don’t know. 5. How often do you have any contact with the following bodies (internal supervision/governing board/the stakeholder body (verantwoordingsorgaan)/the stakeholder body (belanghebbendenorgaan)? Select: 1–4 times a year; 5–12 times a year; biweekly; weekly; other, namely.

Part 1: General use of the Pension Fund Code 6. How do you evaluate your own knowledge of the Pension Fund Code? Select: very good; good; reasonable; mediocre; poor; very poor. 7. How do you evaluate your own knowledge of the norms for internal supervision in the Pension Fund Code? Select: very good; good; reasonable; mediocre; poor; very poor. 8. Article 47 of the Pension Fund Code states: ‘Internal supervision uses this Code in the execution of its task’. How do you implement this norm? Fill in. 9. For which activities do you use the Pension Fund Code? Select (multiple answers possible): to evaluate the pension fund’s strategy; to evaluate the pension fund’s investment policy; to evaluation compliance with the Pension Fund Code; to hold the governing board accountable; to evaluate the board’s reporting of Pension Fund Code compliance; to justify decisions or interventions by internal supervision; to aid conversations with the governing board; other, namely. 10. During which moments do you discuss the Pension Fund Code? Select (multiple answers possible): during meetings with internal supervision; during meetings with the governing board; during meetings with the stakeholder body (verantwoordingsorgaan); during meetings with the stakeholder body (belanghebbendenorgaan); other, namely. 11. Which information sources do you use, when you need information about the Pension Fund Code? Select (multiple answers possible): the Code itself; webinars; the website of the Monitoring Committee Pension Fund Code; the website of the Pension Federation; other pension funds (for instance, annual reports); other, namely. 12. What is your opinion of the following statement? ‘I find the Pension Fund Code a useful tool in defining my tasks and responsibilities as an internal supervisor’. Select: fully agree; agree; no opinion; disagree; fully disagree. 13. In your opinion, is there a need for any changes or additions to the Pension Fund Code, for the Code to be a useful tool in defining your tasks and responsibilities as an internal supervisor? Select: yes, namely; no.

Part 2: Preferences and trust of the beneficiaries 14. Regarding which subjects does the pension fund research the preferences of beneficiaries (active participants, pensioners, deferred participants)? Select (multiple answers possible): fund communications; pension benefits; the pension contract; the investments; other, namely; the pension fund does not research the preferences of beneficiaries; I don’t know.

If selected ‘the investments’: regarding which investment subjects does the pension fund research the preferences of beneficiaries? Select (multiple answers possible): investment categories; risk acceptance; sustainable and responsible investment; ethical issues; religious considerations; other, namely; I don’t know. 15. Are you familiar with the methods with which the pension fund researches the preferences of beneficiaries? If so, which ones? Select (multiple answers possible): questionnaires; roundtable discussions; focus groups; social media polls; satisfaction studies; risk acceptance measurements; other, namely; the pension fund does not research the preferences of beneficiaries; I don’t know. 16. With which frequency does the pension fund research the preferences of beneficiaries? Select: every 5 years; every 2 years; annually; other, namely; the pension fund does not research the preferences of beneficiaries; I don’t know. 17. What does internal supervision do to safeguard that the organization takes care of beneficiaries’ trust in the pension fund? Select (multiple answers possible): Discussions with the board; discussions with the stakeholder body; oversight of investments; conducting evaluations; other, namely; I don’t know. 18. Which practices or measures to safeguard beneficiary trust in the pension fund by internal supervision do you find particularly useful? Type in your answer. 19. Does internal supervision measure the effects of aforementioned practices or measures? Select: yes; no; I don’t know. 20. Do you observe any obstacles for internal supervision to play a larger role in safeguarding beneficiaries’ trust in the pension fund? Select: yes, namely; no; I don’t know. 21. How can the Pension Fund Code help internal supervision play an encouraging role in the balanced representation of interests? Type in your answer.

Part 3: Diversity and representation of beneficiaries 22. For which parts of the organization does the pension fund have a written policy and concrete goals to safeguard diversity? Select (multiple answers possible): the governing board; the stakeholder body; internal supervision; the administrative bureau; other parts, namely; the pension fund does not have a written policy and concrete goals to safeguard diversity; I don’t know.

If selected ‘the governing board’, to which board members does the diversity policy apply? Select: all board members; representative board members; independent board members; I don’t know.

Does internal supervision fulfil the written policy and concrete goals to safeguard diversity? If not, in what ways does internal supervision deviate? Select: yes; no, namely. 23. Which personal characteristics does the diversity policy pertain to? Select (multiple answers possible): sex; age; education; professional background; ethnicity; religion; other, namely. 24. Are you familiar with the personal characteristics of specific cohorts of the beneficiaries? Select: yes; no. 25. Does the internal supervision take measure to become familiar with the personal characteristics of the pension fund’s beneficiaries? If so, which ones? Select: yes, namely; no; I don’t know. 26. Which measures does the internal supervision take to realize diversity and representation of beneficiaries within the pension fund? Type in your answer. 27. Theme 5 of the Pension Fund Code defines diversity within fund bodies in terms of education, professional background, personality, sex and age. Do you find this definition sufficient? Select: yes; no; I am not familiar with this definition. If selected ‘no’: how could the definition of diversity in the Pension Fund Code be improved? Type in your answer. 28. Do you observe any obstacles for internal supervision to play a larger role in realizing diversity within fund bodies? If so, which obstacles? Select: yes, namely; no; I don’t know. 29. Which measures or practices of internal supervision do you find particularly useful in realizing diversity and representation of beneficiaries? Type in your answer. 30. How can the Pension Fund Code play an encouraging role in this area for internal supervision? Please type in your answer.

Part 4: The learning organization 31. Theme 4 of the Pension Fund Code states that a pension fund needs to be a ‘learning organization’. In what way does the pension fund comply with this obligation? Type in your answer. 32. Which measures does the pension fund’s governing board take to ensure that it is a learning part of the organization? Select (multiple answers possible): periodic self-evaluation; education; learning from other funds; other, namely; the governing board does not take any measures. 33. Which effects do these measures have? Type in your answer. 34. Theme 4 of the Pension Fund Code (striving for quality) defines the most important dimensions of a learning organization, such as taking care of permanent education, listening to criticism and periodic self-evaluation. How satisfied are you with the scope of these dimensions? Select: very satisfied; satisfied; neutral; dissatisfied; very dissatisfied; I don’t know. 35. How does internal supervision encourage the organization to prepare and deal with these topics? Type in your answer. 36. Which measures do you take to ensure that the internal supervision itself is a learning part of the organization? Select (multiple answers possible): periodic self-evaluation; education; learning from other funds; other, namely; the internal supervision does not take these measures; I don’t know.

If selected ‘periodic self-evaluation’: what have you learned and/or implemented after the periodic self-evaluation? Type in your answer. 37. Do you observe any obstacles for internal supervision to strengthen the learning capacity of the organization? If so, which obstacles? Select: yes, namely; no; I don’t know. 38. Which measures or practices of internal supervision do you find particularly useful in strengthening the learning capacity of the organization? Type in your answer. 39. How can the Pension Fund Code play an encouraging role for internal supervision in strengthening the learning capacity of the organization? Type in your answer.

Part 5: Personal details 40. What is your name? Type in your answer. 41. What is your email address? Type in your answer. 42. What is your phone number? Type in your answer. 43. Do you have other functions in the pension sector, besides the aforementioned one? Select: yes, no.

If selected ‘yes’: how many functions do you have in the pension sector, besides the aforementioned one? Type in your answer.

If selected ‘yes’: which functions do you have in the pension sector, besides the aforementioned one? Type in your answer. 44. What is your VTE score? The full-time equivalence score (VTE score) is a measure of the total time required for your positions within the pension sector, which is required by law in the context of the suitability assessment. Type in your answer.