Abstract

This article analyses the ‘backward’ form of import-substitution industrialisation (ISI) in countries integrated into the global economy as exporters of primary commodities, using the example of the car industry in Uzbekistan. This form of incorporation defines the way in which all manufacturing capitals, regardless of ‘nationality’, accumulate at the average rate of profit via raw material rents, as mediated by specific state policies. This has been the case of Uzbekistan’s state-owned car manufacturer UzAvtoSanoat, in joint-venture with Korean Daewoo Motor Company and American General Motors in the 1992–2016 period. Orthodox (‘neoliberal’) economists view the Uzbek car industry as inefficient due to state intervention. Heterodox (‘developmental state’) scholars hail it as an example of export-oriented industrial upgrading. Neither explain, however, why leading MNCs would invest in such an inefficient market (as per the former), given its low scale of production that is mostly purchased domestically (pace the latter). Instead, I contend that all manufacturing capitals in the country could stay profitable only via rent subsidisation, the main reason for leading MNCs to invest in it. As such, ‘backward’ manufacturing ISI in Uzbekistan epitomises a specific national form taken by the global process of capital accumulation in resource-rich countries of the Global South.

Introduction

Why would multinational corporations (MNCs) invest in manufacturing in resource-rich countries of the Global South? While orthodox (‘neoliberal’) economists focus on the inefficiency of industrial production in these economies due to state interference and the corruption it engenders, their heterodox (‘developmental state’) counterparts insist that industrial policy is still key for these countries to move up the value chain following the example of the Asian tigers and, more recently, China. Yet, neither literature addresses the important question as to why, for decades, MNCs have been investing in industry in countries of the Global South, including in car manufacturing, regardless of their limited (mostly domestic) scale of such production. In other words, despite inefficiency and the lack of industrial upgrading, import-substitution industrialisation (ISI) in these countries has continued with the active participation of leading global MNCs. This has been the case of Uzbekistan’s state-owned company UzAvtoSanoat between 1992 and 2016, which neoliberals critique as inefficient and corrupt (e.g. Olma, 2021), while developmentalists praise as a successful case of export-oriented industrialisation (e.g. Popov and Chowdhury, 2016). However, the literature appears unable to explain the reason behind Korean Daewoo Motor Company (DMC) and American General Motors (GM) entering into joint-ventures (JVs) with UzAvtoSanoat in the period under review, despite the low domestic scale (hence high costs) of automobile production in the country, which is mostly purchased domestically. Equally, the origin of domestic solvent demand for these relatively expensive cars is left unaddressed.

I argue that the answer to these questions must be found in the specific way in which manufacturing capitals, regardless of ‘nationality’, turn a profit in countries of the Global South integrated into the global economy as primary commodity exporters. This entails the appropriation of raw material rents (ground-rent) through specific state policies, including the overvaluation of the national currency and the provision of cheap inputs by State-Owned Enterprises (SOEs), which, in the case of energy, for example, at least partly subsidises domestic solvent demand by lowering the cost of living/increasing the purchasing power of the general population. As such, not only have MNCs benefitted from an overvalued exchange rate for the cheaper import of heavy equipment, parts and components to these countries, but they have also put machinery obsolete for world market production to use for the manufacturing of old models in these markets. The result has been what, with Iñigo Carrera (2016), I term ‘backward’ industrialisation, as these capitals have been ‘small’ and technologically ‘backward’ by international standards, 1 hence only able to stay in business via rent subsidisation and, as a consequence, producing relatively expensive goods mostly for the protected domestic market. ‘Backward’ ISI is neither inefficient nor developmental, however, as the literature would have it, but the specific national form mediating the global process of capital accumulation in resource-rich countries of the Global South, including Uzbekistan as a cotton and, increasingly, gold and natural gas producer.

The paper is organised as follows. The literature on late industrialisation in the global South section briefly reviews the neoliberal and developmental state literature with reference to late industrialisation in the Global South, specifically in the Asian tigers and China, and the implications this may hold for other developing countries. The 'backward' industrialisation in resource-rich countries in the International Division of Labour section introduces an alternative theoretical framework pioneered by independent scholar Iñigo Carrera and affiliated researchers, which explains the distinct ‘backward’ form of rent-subsidised industrialisation in resource-rich countries of the Global South, as mediated by specific state policies within the global process of capital accumulation. It then turns to illustrate these policies in Uzbekistan between independence in 1991 and the death of the country’s first president, Islam Karimov, in 2016. The car industry in resource-rich Uzbekistan section deploys these theoretical insights to account for the development of Uzbekistan’s car industry in JV with Korean DMC and American GM between 1992 – the year the former entered the Uzbek market – and 2016, as the epitome of this specific ‘backward’ form of industrialisation. The section draws on a range of primary sources, including key pieces of legislation, never previously analysed in English. The conclusion summarises the paper’s main points.

The literature on late industrialisation in the global South

In the wake of the boom in primary commodity prices during the 2000s and 2010s, a rich debate emerged in the literature on the developmental potential of raw material exports to spur late industrialisation in the Global South (e.g. Singh and Ovadia, 2018a; Jepson, 2020). Drawing on diverse case studies particularly from Latin America and Africa, this literature argued for the enduring importance of ‘state intervention as a policy strategy to maximise rents and to pursue structural transformation’ in resource-rich countries (Singh and Ovadia, 2018b: 1046). In this perspective, if the (re)nationalisation of natural resource extraction within State-Owned Enterprises (SOEs) in the Global South represented a developmental boon for these states, industrial policy continued to be central to the process of scaling up production in strategic industries, from the extraction of primary commodities to the production of increasingly complex capital goods (Singh and Chen, 2018). In short, states could leverage high international commodity prices in order to implement developmental policies, as neo-extractivism could become a form of new developmentalism.

As such, the current debate continues the long-standing discussion on uneven development in the Global South during the past decades, particularly in light of the rapid transformation of some countries in Asia such as South Korea and, more recently, China, into global industrial powerhouses, and the role played by industrial policy in this transformation. For neoliberals, it was the governments of these Asian countries making ‘good use of international markets’ (World Bank, 1995: 3) that explains their meteoric late rise, so export-oriented industrialisation (EOI) remains crucial for development (Pomfret, 2005). In this perspective, industrial policy is still seen as a huge ‘gamble’ with little guarantee of success (World Bank cited in Hayashi, 2017: 83), particularly as state intervention often ends up favouring specific interest groups, thus giving rise to rent-seeking and corruption (Abdelrahman, 2019). This continues to be the case despite the current proliferation of industrial policies in the developed world, especially in high-tech sectors such as the car industry, which, in this view, simply represents a legitimate reaction to the unfair competitive practices of Chinese state capitalism that are allowing it to beat ‘true’ capitalism at its own game (Alami and Dixon, 2020). The implication for other countries in the Global South is that market-distorting state interventions should be avoided as they fail to promote development and create opportunities for corruption instead.

For their part, heterodox scholars contend that industrial policy in the Asian ‘developmental’ states coordinated ISI and EOI in a complementary and interactive fashion (Wade, 1990), enabling some companies from these countries to become major players in the world economy, including in high-tech manufacturing, as the success of the Korean car industry illustrates (Jeong, 2004). Since market distortions were necessary to create competitive advantage, the implication for the Global South has been that such a model can be replicated in order to develop national manufacturing capacity and, with time, gain a foothold in the most technologically advanced export markets (Stark, 2012). As such, these researchers view China’s industrialisation as confirmation of the ongoing need for developing countries to distort the market in order to engineer a change in their industrial production structure, despite the fact that, bar China, emulating the success of the Asian trailblazers has been elusive for most other countries of the Global South (Wade, 2014). As a consequence, these scholars tend to associate ‘any circumstance’ of ‘state involvement and some aspect of development’ with the potential presence of a developmental state (Fine, 2013: 22), as in the case of neo-extractivism as new developmentalism presented above.

However, it is an incontrovertible empirical fact that, at different points in time in the past decades, several resource-rich countries of the Global South have used a series of specific policy interventions to develop car industries in the form of domestically-oriented ISI with the participation of leading MNCs, while continuing to be integrated into the global economy as raw material exporters. This has been the case of Brazil and Argentina in Latin America (Fitzsimons and Guevara, 2016; Grinberg, 2011), Egypt in North Africa (Black et al., 2020), and Uzbekistan in Central Asia, the case study of this paper. Neither the neoliberal nor the developmental state literature can offer a satisfactory explanation as to why global MNCs would invest in such inefficient markets (as per the former), given the low scale of production that is mostly purchased domestically rather than exported (pace the latter).

Instead, the literature on Uzbekistan largely follows the orthodox-heterodox binary. On the one hand, neoliberal scholars focus on the inefficiency of state-owned automotive holding company UzAvtoSanoat, as confirmed by the low scale/high cost of production despite decades of subsidies, which fed a system of rent-seeking and corruption (Olma, 2021; Zhukov, 2005). Uzbekistan fares poorly when compared to Korea, specifically because ISI ‘is not a viable strategy for promoting long-run growth’; EOI is (Pomfret, 2005: 233). In contrast, along with the government of Uzbekistan (GoU), a minority of researchers hailed the development of ‘a competitive export-oriented auto industry from the ground up’ (Popov and Chowdhury, 2016: 5), including in terms of added value and employment, given the myriad small and medium enterprises (SMEs) producing parts and components in the growing automotive cluster (Center for Economic Research, 2013). In this view, the Uzbek car industry stands as a testimony to the success of industrial policy, as the country achieved what no other post-Soviet state did in the first decades of independence (Popov, 2013). However, neither literature can account for why Korean DMC and American GM would invest in the Uzbek market between 1992 and 2016, the period under review, despite the low scale/high cost (hence inefficiency, per the former) of car production by world market norms, which is mostly purchased domestically rather than exported (pace the latter). Equally, the question of how domestic demand remained solvent for these relatively expensive cars is left unaddressed.

The next section introduces an alternative theoretical framework first expounded by Iñigo Carrera and affiliated scholars, which, I argue, holds the key to answering these questions.

‘Backward’ industrialisation in resource-rich countries in the international division of labour

Despite their differences, orthodox and heterodox scholars operate on the methodological assumption that, in essence, capital accumulation (‘development’) is a nation-state-based process. In light of this methodological nationalism (Pradella, 2014), the world market is framed as the context of development, in which discreet ‘national processes of capital accumulation develop with different degrees of … autonomy’ (Grinberg, 2016: 216). The process of capital accumulation, however, is global in content and national in form only (Burnham, 1994; Bonefeld, 2014). As such, states are not autonomous entities whose policies independently determine the way in which capital accumulates within their borders. Rather, state policies mediate the constantly expanding process of global capital accumulation in line with the specific productive characteristics of their national working class, or in relation to the relatively favourable conditions for the production of raw materials in their territories (Iñigo Carrera, 2013), which constitute the basis for their participation in the international division of labour (IDL). Since labour productivity is the most powerful engine of capital accumulation and, in turn, the system of machinery in large-scale industry represents the most potent lever to increase labour productivity, productivity-enhancing technological changes revolutionise the division of labour in society and the world market (Marx, 1867/1976).

With the computerisation and robotisation of large-scale industrial production in the past decades, particularly since the microelectronic revolution of the mid-1970s, an increasing number of skills previously learnt through long on-the-job training became objectified as attributes of the computerised machinery on the robotised assembly line. As a consequence, not only could relatively simplified and, with time, progressively complex tasks be performed by relatively lower skilled (hence lower paid) labourers on the basis of longer workdays, in a work process ‘reduced in the extreme to the mechanical repetition of a manual task’ as appendages to, or operators of, the new self-calibrating machinery (Iñigo Carrera, 2013: 112). This also allowed for the relocation of specific large-scale industrial processes to some Asian countries, whose working classes combined relative cheapness with ‘the disciplined subordination to centrally and hierarchically organised collective (i.e. large-scale) work-processes and the habituation to labour-intensive activities under harsh conditions’, typical of wet-rice cultivating societies, making them particularly suited to meeting the changing material requirements of large-scale industrial capital operating on the world market (Grinberg, 2013: 182).

Therefore, these Asian countries have mediated these dynamics with specific policies that guaranteed the reproduction of a relatively cheap and highly disciplined working class as the key ‘factor endowment’ for their participation in the IDL (Iñigo Carrera, 2013). In South Korea, for instance, state repression of labour unions as well as labour market reforms to control wage growth, limit welfare and guarantee ease of hiring and firing, along with the emphasis on workers’ discipline and collaborative habits in school curricula, have been crucial to reproduce a relatively cheap and pliant labour force for large-scale industrial production for the world market since the 1960s, whether during the ‘developmental state’ or the ‘neoliberal’ phase following the 1997 Asian financial crisis (Grinberg 2011; Pirie 2012). 2 As a consequence, next to the classical IDL (CIDL) in which Global South countries largely served as producers of raw materials for export to the industrialised Global North, a new international division of labour (NIDL) emerged, as parts of Asia underwent a meteoric process of late industrialisation to become the ‘world’s factory’ (Starosta, 2016).

This global reorganisation of industrial production enabled capital to cut overall wage costs via the exploitation of these relatively cheap and highly disciplined Asian working classes, hence to increase the scale of accumulation and production most evident in the rise of MNCs and transnational corporations (TNCs), along with their global production networks and free-trade and industrial zones. By 2015, sales by MNCs/TNCs ‘amounted to about half of global GDP’, leading the rise in trade and investment of the past decades (World Bank, 2017: 62). The automotive industry is a case in point. As one of the most technologically dynamic large-scale industries, automotive manufacturing came to be dominated by ten MNCs/TNCs with total equity running in the tens of billions of USD (Pirie, 2013) and responsible for 40–45% of annual deployment of industrial robots between 2010 and 2015 (United Nations Conference on Trade and Development, 2017: 48). As such, these ‘normal’ industrial capitals accumulate at the average rate of profit, establishing the costs of production and prices of commodities under ‘normal’ competitive conditions (Iñigo Carrera, 2016).

Contrary to the Asian tigers and China, however, most countries of the Global South continue to be incorporated into the IDL on the basis of the CIDL, that is, as exporters of raw materials due to the relatively favourable natural conditions for this form of production in their territories, which has turned them into sources of appropriation of ground-rent. Instead of ‘normal’ conditions, the international prices of primary commodities are regulated by marginal conditions due to the use of land in the process of production. In other words, raw material prices need to incorporate a ground (i.e. land) rent including for the landlords of the worst (‘marginal’) lands that need to be brought into production in line with global solvent demand. As such, as long as ground-rent-bearing raw materials are sold on the world market for consumption abroad, their sale represents an inflow of value – ground-rent – into the countries exporting them (Grinberg, 2011, 2013).

In this perspective, as the main landowner in many countries of the Global South, the (landlord) state mediated the continuous reproduction of the accumulation process with specific policy interventions – such as, for example, the purchase of primary commodities on the domestic market at fixed prices for resale at international prices in the world market – that allowed it to syphon off this extraordinary wealth (ground-rent) in order to in/directly subsidise all manufacturing capitals operating therein, regardless of ‘nationality’. Crucially, this includes MNC/TNC-affiliates operating independently or in JV with domestic companies, as ground-rent subsidisation enabled these ‘normal’ capitals to profitably invest ‘fragments of specific restricted scale’ for domestic production in resource-rich countries (Iñigo Carrera, 2016: 42), revealing the reason for their entering these markets that has eluded both orthodox and heterodox scholars.

This specific form of integration into the IDL has defined the long-term process of capital accumulation in resource-rich countries, as, in order to appropriate ground-rent, all industrial manufacturing capitals needed to sell their final products on the protected domestic market or, at best, in equally protected regional markets including via free-trade agreements (FTAs). As a result, these capitals have been ‘small’ and technologically ‘backward’ by ‘normal’ world market norms, given their limited (largely domestic) scale of production that precludes the economies of scale necessary for the introduction of cutting-edge technology, mobilising instead relatively expensive labour that manufactures relatively costly final goods such as cars. This is the essence of ‘backward’ import-substitution industrialisation (ISI) in resource-rich countries incorporated into the IDL as raw material exporters, whose scale of production has followed the magnitude of ground-rent available in these national economies, in line with the fluctuations of the international prices of their resource endowments according to global solvent demand (Iñigo Carrera, 2013, 2016).

Moreover, this explains why MNC/TNC-affiliates operating in these markets clamoured for the protection of the national state as their domestic counterparts, ‘arguing their case as incipient industrial capitals in a struggle to consolidate themselves in the face of foreign competition’ (Iñigo Carrera, 2016: 42). As such, they have benefitted from the same barrage of ground-rent-subsidised benefits mediated by specific state policies as all other manufacturing capitals operating in resource-rich countries. At different times, these policies included the overvaluation of the national currency, which indirectly subsidises the import of industrial machinery, parts and components; the provision of credit at low and even negative interest rates to enterprises by state banks; the selling of inputs, utilities and means of consumption (e.g. food) at subsidised rates, especially by State-Owned Enterprises (SOEs), which subsidises production and, in the case of energy and food, also consumption by lowering the cost of living/increasing the purchasing power of the general population, at least partly accounting for domestic solvent demand; the calibrated protection of the domestic market via import tariffs and quotas on finished industrial goods (e.g. cars); and tax exemptions. Specifically, MNC/TNC-affiliates could take advantage of exchange rate overvaluation to gain higher profits upon repatriation and, crucially, to import machinery obsolete for world market production in order to use it for ‘backward’ domestic production instead (Grinberg, 2015, 2016).

Such policies have been at the heart of ‘backward’ ISI in resource-rich states. This, however, is neither the result of inefficient market distortions favouring rent-seeking (neoliberal literature), nor a necessary step towards Korea-style export-led industrial upgrading (developmental state scholars), but the specific national form taken by the process of global capital accumulation in countries integrated into the IDL as raw material exporters, hence as sources of appropriation of ground-rent (Iñigo Carrera, 2013, 2016). These policies have been a feature of ‘backward’ ISI in resource-rich countries in, for example, Latin America during the past decades, including in the car industry with the participation of MNC/TNC-affiliates (e.g. Fitzsimons and Guevara, 2016). The same has been the case in the ‘backward’ car industry of independent Uzbekistan, whose evolution is analysed in the next section. Before that, though, I turn to the combination of policies through which the Uzbek state mediated the global process of capital accumulation on its national territory.

Uzbekistan as a resource-rich country in the IDL: Ground-rent subsidisation for 'Backward’ ISI

With its hot and dry climate and abundant water resources, Central Asia has historically presented relatively favourable conditions for cotton production, which boomed after the introduction of American seed varieties by private entrepreneurs under Tsarist Russia’s colonial rule in the 19th century, and then massively expanded during Soviet times, particularly with the mass allocation of land to cotton and the building of a truly monumental canal infrastructure to irrigate it (Penati, 2013; Spoor, 2005; Tarr and Trushin, 2004). As a result, most of the cotton grown in the Soviet Union came from Central Asia, with half of it being produced in the Uzbek Soviet Socialist Republic alone in exchange for food and finished goods, including textiles and clothing manufactured in the Union’s European republics. Moreover, the Soviet authorities exported cotton and other raw materials to international markets for hard currency, in order to buy industrial equipment from the developed capitalist economies (Central Intelligence Agency (CIA), 1989; Pomfret, 2002). After the collapse of the Soviet Union in 1991, independent Uzbekistan diverted cotton production to international markets to accrue hard currency, given that, while depleted, 3 the relatively favourable natural conditions for the crop’s production remained the country’s main ‘factor endowment’ for its participation in the IDL.

Equally, despite the decrease in unionisation and the deterioration in living standards that followed the end of the Soviet era, the Uzbek working class – as was generally the case across the newly independent former Soviet republics – possessed radically different productive characteristics than that of the newly industrialising countries of Asia. Given the relatively higher level of unionisation compared to both developed and developing countries, the now-former-Soviet working class was actually relatively expensive and undisciplined, due to high wage and especially non-wage (e.g. welfare entitlements) costs and lax labour discipline, which made it unsuitable for world market production. This was particularly true at a time when China was fast becoming a virtually unlimited source of relatively cheap and highly disciplined workers in the 1990s (CIA, 1989; Starosta, 2016; World Bank, 1995). Therefore, while China experienced a meteoric process of industrialisation, Uzbekistan turned instead into a source of appropriation of ground-rent for all manufacturing capitals operating on its territory, regardless of ‘nationality’. As in other resource-rich countries in the Global South, specific state policies mediated this process to guarantee the reproduction of capital accumulation in Uzbekistan via rent subsidisation, explaining the country’s ‘backward’ form of ISI, along with the ‘strong correlation’ between international commodity prices and growth therein since independence (Asian Development Bank Institute, 2014: 88).

As such, the Uzbek (landlord) state bought raw materials at fixed lower prices in the domestic market in order to resell them at international prices in the world market, pocketing the difference, that is, ground-rent. In the crucial cotton sector, the Agricultural Fund set the procurement price for raw cotton at an ‘artificially low’ level (Muradov and Ilkhamov, 2014: 12), while the state hoarded most of the annual cotton production for sale on the international market via three ‘government-controlled trading companies’ (Bendini, 2013: 23). Likewise, the GoU established a cut-off price at which it would purchase other ‘strategic’ raw materials such as gold and copper from SOEs on the domestic market for resale on the world market in hard currency (Connolly, 1997). Moreover, the Central Bank of Uzbekistan (CBU) operated a system of multiple exchange rates and obligatory hard currency surrender requirements, with the overvalued ‘official’ rate being used to purchase all hard currency earnings from primary commodity sales, particularly cotton and gold, a further appropriation of ground-rent on top of the cut-off or procurement price (World Bank, 2013).

These resources went to subsidise priority sectors of the economy, including the car and other manufacturing industries, via credit at preferential and even negative interest rates (International Monetary Fund, 1998). The CBU’s ‘most prominent quasi-fiscal activity [has been] the granting of preferential credits’, including through commercial banks, to SOEs and priority enterprises in JV with foreign MNCs/TNCs (World Bank, 1994: 35), that is, ground-rent subsidisation for ‘backward’ ISI. Equally, the overvaluation of the national currency allowed firms to import capital goods purchased at lower prices on the international market as inputs for industrial development, as has been the case in the car industry (next section). Although machinery, equipment and technology faced ‘very low tariffs’ and individual enterprises were often ‘granted tariff [and excise tax] exemptions’ (IMF, 1998: 119), the domestic market remained protected against the import of finished goods such as cars and electronics (Bendini, 2013).

Starting in the late 1990s, international prices for raw materials began rising in order to encapsulate the growing magnitude of ground-rent necessary to expand production in the worst (‘marginal’) lands and satisfy growing global solvent demand for energy and raw materials, originating in particular from a fast-industrialising China (Jepson, 2020). Riding on this commodity supercycle, the ‘development of the hydrocarbons and gold sectors pick[ed] up speed’ in Uzbekistan (Economist Intelligence Unit, 2005: 6), with gold exports booming along with international prices from 157 million USD in 2010 (or approximately 2% of total exports) to 1.77 billion USD in 2016 (or 22% of the total) (Atlas of Economic Complexity data, 2016). Likewise, significant joint investments between Uzbekneftegaz (UNG) – the country’s oil and gas SOE – and foreign companies and development banks, particularly from Russia and Asia, flowed to the energy industry, growing from 190 million USD in 2000 to 16.3 billion USD in 2016 (Pirani, 2012; UNG, 2018).

The boom in international commodity prices translated into the rise in the mass of ground-rent inflowing into Uzbekistan that went to subsidise ‘backward’ ISI. Next to the continuation in the supply of subsidised utilities by SOEs, particularly gas and ‘gas-fired’ electricity (Pirani, 2012: 58), the GoU redoubled efforts to increase the number and volume of cheap inputs for manufacturing enterprises, particularly via extensive localisation programmes, that is, the subsidisation of ISI to manufacture more parts and components on the basis of domestically-available raw material inputs (e.g. PP-2298, 2015). 4 For example, chemical SOE UzKhimProm converted natural gas into ‘chemical intermediates used in the plastics and textiles industries’ (Asian Development Bank, 2012), as well as in the manufacturing of plastic parts and components for the car industry, such as bumper sets and dashboards, among others (UzAvtoSanoat Website a, n.d.). Equally, copper production at the Almalyk and Navoi Mining and Metallurgical Companies, the country’s main mining SOEs, guaranteed the cheap raw material inputs for the domestic manufacturing of industrially produced wires, including for use in the car industry (UzAvtoSanoat Website b, n.d.).

Given the centrality of ground-rent for the process of capital accumulation in resource-rich Uzbekistan, the volume of manufacturing in the country steeply fluctuated upward during the commodity supercycle. Increasing investments in localisation programmes went hand in hand with the establishment of three Free Economic Zones (FEZs) between 2008 and 2013, which extended subsidies, preferences and exemptions to foreign investors willing to relocate to the country, particularly in JV with domestic enterprises, such as three to seven year tax holidays depending on the level of initial investment (United Nations Development Programme, 2009). The creation of SMEs also received a boost during this period due to subsidised utilities and inputs, substantial tax breaks and reductions, and bank loans ‘at heavily subsidised interest rates’ including for the purchase of equipment from abroad (OECD, 2013: 57). As a consequence, the number of SMEs and their weight in total employment grew exponentially, with manufacturing SMEs accounting for more than 20% of this growth including in the SME cluster supplying the car industry (Tadjibaeva, 2019; UzAuto, 2018).

Finally, subsidised utilities and the GoU’s policy of subsidised grains provision meant that ground-rent-bearing natural gas and wheat, along with derived products such as flour and bread, circulated at lower-than-international prices on the domestic Uzbek market, including due to the imposition of taxes on the export of foodstuff (Connolly, 1997; Mirkasimov and Parpiev, 2017). Such subsidies contributed to increasing the purchasing power of the working class, at least partly explaining domestic solvent demand for relatively expensive domestically manufactured goods. As such, higher prices for domestically produced electronics and cars represent yet another form of ground-rent subsidisation for ‘small’ and technologically ‘backward’ manufacturing capitals in the Uzbek market. 5 As the largest manufacturing industry in terms of production capacity and people employed, the car industry provides a useful case study to analyse the ‘backward’ form of ISI in Uzbekistan. As such, not only can the general conclusions drawn from it be applied to other manufacturing sectors in the country, such as electronics, but it also epitomises ‘backward’ industrialisation in resource-rich countries of the Global South as specific national forms mediating the process of global capital accumulation. It is to this that I now turn.

A case study in 'Backward' industrialisation within the IDL: The car industry in resource-rich Uzbekistan, 1992–2016

The car industry in independent Uzbekistan has been linked to two major MNCs in JV with state holding company UzAvtoSanoat, namely Korean DMC, until the Daewoo Group went bankrupt in 2000, and subsequently American GM. The authorised capital for the JVs that DMC (UzDaewooAvto) and GM (GM Uzbekistan) formed with UzAvtoSanoat were 200 and 266.7 million USD, respectively (PKM-509, 1992; PP-800, 2008). Although significant in the context of Uzbekistan, this initial capital was clearly ‘small’ by the industry’s huge, and growing, world market norms. Instead, Uzbekistan’s integration into the IDL as a cotton exporter defined the specific ‘backward’ form of industrialisation within its territory, in line with other resource-rich countries in the Global South. As a result, ground-rent subsidisation has been the only way in which ‘small’ car manufacturing capitals could accumulate at the average rate of profit since independence, that is, make a profit and stay in business. This applies to all manufacturing capitals in the country – regardless of ‘nationality’ (Korean, American, Uzbek) – which obtained subsidies, protection and exemptions via specific policies put in place by the national state. Pace the literature, such policies are neither the result of the GoU’s ‘deeply engrained protectionist habits’ (O’Casey, 2018), nor are they temporary measures to build domestic capacity before a turn to competitive export-orientation (CER, 2013). Rather, they are the specific national forms mediating the essential unity of global capital accumulation in resource-rich Uzbekistan.

Specifically, UzDaewooAvto and GM Uzbekistan, along with their foreign partners DMC and GM, respectively, were granted long tax holidays from the beginning of production. UzDaewooAvto and DMC were exempted from all taxes, including on profit and VAT, for a period of 5 years (PKM-509, 1992). UzDaewooAvto could even retain the 22.5% excise tax on automobile sales on the Uzbek market ‘to increase production, expand the range and increase the competitiveness of manufactured consumer goods’ (PP-244, 2005: Appendix 12.1). GM Uzbekistan and GM also secured blank exemption from all taxes for a period of 10 years (PP-800, 2008), which was then extended to another JV between GM and UzAvtoSanoat for the production of car engines, namely GM Powertrain Uzbekistan (PP-1020, 2008). Many such subsidies and exemptions applied to SMEs in the automotive cluster, too, often in JVs with Korean capital (PP-1020, 2008), whose number reached 160 in the frame of the localisation push to increase the local content of manufactured cars (UzAuto, 2018), particularly during the commodity supercycle. For instance, between 2008 and 2010 SMEs localised the production of more than 260 new types of parts and components (CER, 2013). Finally, all enterprises were given subsidised provision of utilities such as gas and electricity.

Equally, the overvaluation of the domestic currency subsidised the import of capital goods as inputs for the development of the car industry. Access to hard currency at the overvalued official exchange rate allowed UzDaewooAvto and GM Uzbekistan to import machinery and equipment at subsidised prices, while commercial banks – particularly Asaka Bank – extended credits at preferential rates for the import of machinery, parts and components (PKM-509, 1992; PKM-118, 1996), which, in turn, were exempted from import tariffs and excise taxes (PKM-509, 1992; PP-800, 2008). Moreover, Daewoo Group and GM negotiated multiple ad-hoc privileges with the Cabinet of Ministers, including monopoly power within the protected Uzbek domestic market (UNCTAD, 1999). This explains why one investor has generally dominated a market segment in the automotive industry: Daewoo first and then GM monopolised the car and minivan sector; ISUZU (Japan) controlled the bus and special truck market; and MAN (Germany) dominated the heavy-duty trucks’ (Ruziev, 2021). Thus, otherwise ‘small’ manufacturing capitals by international standards could operate at a profit via ground-rent subsidisation. So, for instance, profit margins for two UzDaewooAvto produced models, the Tico and the Nexia, stood at 13.3% in 1997 (Quelch and Park, 1998). Equally, the average profitability rate of the 14 main enterprises in UzAvtoSanoat structure went from −15.2% in 2000, the year DMC went bankrupt, to 7.3% in 2010 and 2.4% in 2012. In these latter two years, GM Uzbekistan earned a profit of 6.5% and 0.9%, respectively (CER, 2013).

Moreover, the Uzbek market offered these MNCs the opportunity to redeploy and valorise fixed capital and technology that had become obsolete by international standards, and whose import for their local JVs could be subsidised via exchange rate overvaluation and tariff exemptions. Although Daewoo went on an 18-billion USD spending-and-acquisition spree in the 1990s (Brzezinski, 1997), including the opening of a ‘brand new’ passenger car plant in Korea (Tiberghien, 2007: 160), it was ‘able to reduce its own cash contribution to total overseas projects by around 15 per cent by contributing in kind: for example, by contributing machines manufactured by or dismantled from Daewoo’s subsidiaries in Korea’ (Jeong, 2004: 148, emphasis added). As a result, whereas in Korea Daewoo launched six new proprietary cars between 1996 and 2000 (Jeong, 2004: 153), at the same time UzDaewooAvto started production of old Daewoo models in Uzbekistan like the Tico and the Damas, as well as the rebranded Nexia that had been introduced in 1986 in Korea under the LeMan brand (CER, 2013; Jeong, 2004).

The available evidence suggests that the same dynamics have been at play with GM, as the import of ‘backward’ technology by international standards was subsidised to manufacture car models for the Uzbek and Commonwealth of Independent States (CIS) markets, which were either being discontinued or upgraded after years of sales in international markets. For example, in September 2007, UzDaewooAvto (soon to become GM Uzbekistan) and GMDAT (the GM-majority-owned successor to DMC after Daewoo’s 2000 bankruptcy) signed a contract for a total investment of 47.69 million USD for ‘the supply and delivery of machinery and equipment to organise the full production cycle of the Lacetti model’ (PKM-219, 2007: Art. 1). Codenamed J200 like the platform 6 on which it was produced, the Lacetti had been sold in Korea and international markets between 2002 and 2009 under different brand names, while GMDAT had promoted the J200 platform around the world half a decade prior to selling it to Uzbekistan (Wardsauto, 2003). Delivery to and installation at the Asaka plant 7 of this by-then obsolete machinery was completed between 2007 and 2009, with manufacturing beginning in two phases in 2008–2009 (PP-741, 2007), in parallel to the introduction on international markets of the new generation Lacetti J300. Likewise, in 2014, GM Uzbekistan imported machinery and equipment for 104.2 million USD to begin the full production cycle of the T250 model under the brand Nexia and Ravon Nexia R3 for the domestic and Russian export market, respectively, in 2016 (PKM-260, 2014; Azizov, 2016). These models would be assembled on the T250 platform, which had been developed in the mid-2000s (Autoevolution, 2020), that is, more than a decade before being recycled for production in the Uzbek market.

As a result, according to official data, ‘[t]he current range of car models are outdated [by an] average of 10–11 years’ (PP-4087, 2019). Put differently, in Uzbekistan ‘small’ car manufacturing capitals by international standards have used obsolete technology to produce relatively expensive cars (more on this below). Since the only way for these ‘backward’ capitals to operate at a profit has been via ground-rent subsidisation, car manufacturing has been dependent on the evolution of the magnitude of ground-rent available in the Uzbek economy in line with the changing prices of Uzbekistan’s primary commodities. Equally, as state policies mediated ground-rent subsidisation, car manufacturing has been limited largely to the confines of the protected domestic market and, at best, to other CIS markets with which Uzbekistan signed an FTA, particularly Russia and Kazakhstan. In turn, this limited scale of production has translated into increasing costs and a growing quality gap in comparison with the industry’s international standards (PP-4087, 2019), where economies of scale reduce production costs and competition drives investments in R&D and cutting-edge technology, such as industrial robots.

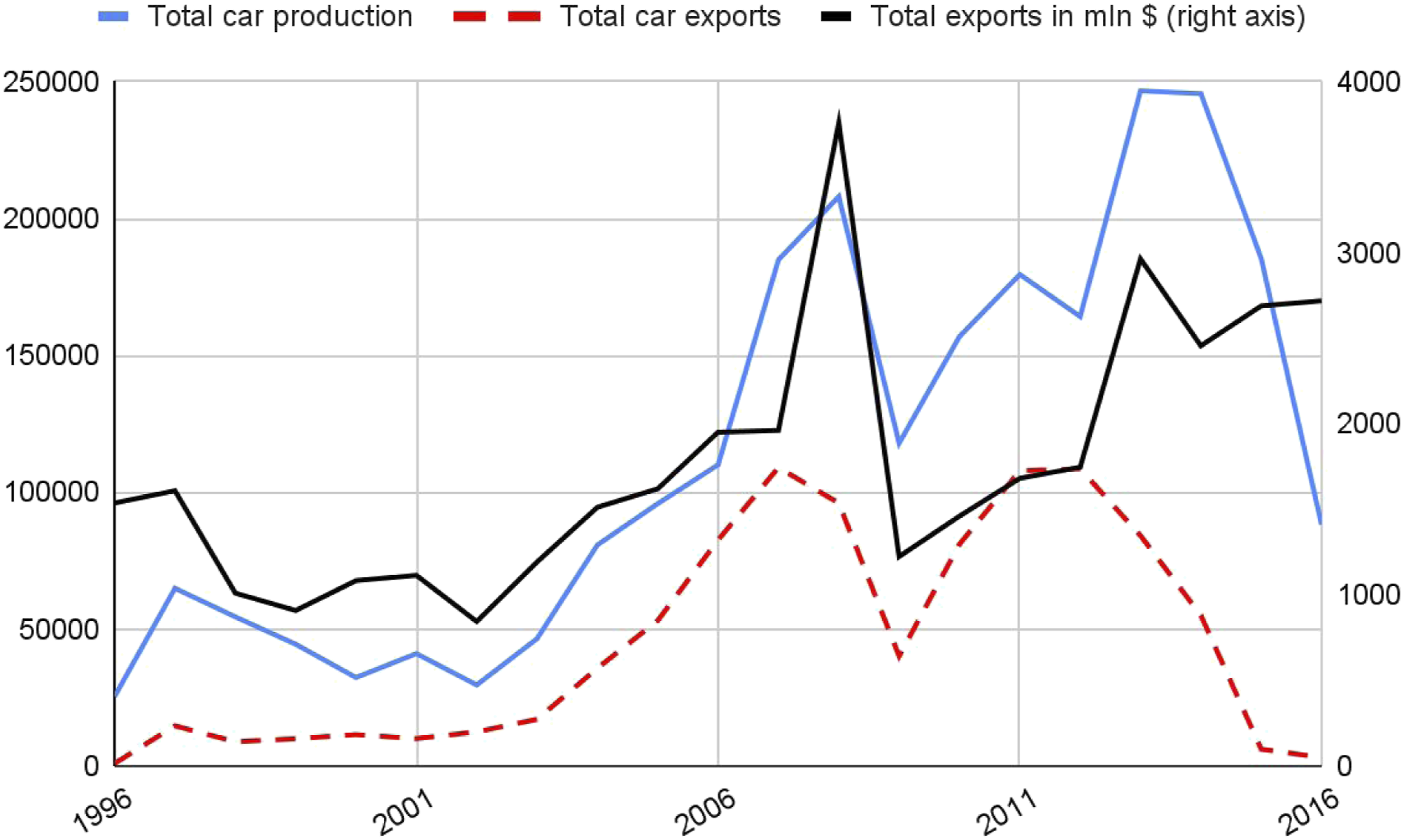

Thus, the performance of the Uzbek car industry has directly mirrored the volume of ground-rent available in Uzbekistan’s domestic market to subsidise its production, as the empirical data unequivocally show (Figure 1). Between 1996 – the year in which car manufacturing started at the Asaka plant – and 2016, car manufacturing closely fluctuated upwards and downwards in line with the parallel oscillations in revenue accrued from the country’s raw material exports, whose international prices reflected the amount of ground-rent carried by Uzbekistan’s main primary commodities – cotton and, increasingly, gold and natural gas – available on the domestic market. During this 22-year period, only in 2014–16 did production perceptibly drop despite increasing export revenues (Figure 1), as the ongoing economic crisis in Russia and Kazakhstan not only dampened demand for Uzbek cars in these key export markets, but also more than halved remittances from Uzbek migrant workers in Russia compared to 2014, undercutting solvent demand for durable goods at home, too (World Bank Migration and Remittances data, 2018).

8

Total car production/exports vis-à-vis total cotton, gold and natural gas exports in mln USD (1996–2016).

Likewise, the Uzbek car industry has manufactured relatively expensive vehicles that are uncompetitive in the international market (PP-4087, 2019). First, the industry specialises in the assembly of several old lower-end models, whose aggregate production at the Asaka plant between 1996 and 2016 never reached full capacity at 250,000 vehicles, let alone the industry’s standard of between 100,000 and 250,000 units per model, thus translating into relatively higher prices in world market terms (Fitzsimons and Guevara, 2016; PP-4087, 2019; Olma, 2021). Moreover, whereas the industry’s ‘normal’ labour productivity averages around 60 vehicles per worker (Fitzsimons and Guevara, 2016), the available data suggest that the average figure for Uzbekistan between 2006 and 2016 is about a third of that (21.4 vehicles/worker). 9 The same applies to engines built by GM Powertrain Uzbekistan at the company’s Tashkent factory, whose manufacturing capacity of 360,000 units/year is significantly below the industry’s economies of scale that run in the millions of units (Grinberg, 2011; PP-1020, 2008). Second, while the Uzbek car industry has increased its capacity over the years introducing stamping, welding and painting technology, as well as the local production of some parts and components especially during times of high raw material prices, it has no independent R&D facilities and continues to rely on GM for design engineering, along with the import of most parts and components (CER, 2013). Instead, the gap in technological development between the global automotive industry and Uzbekistan’s domestic car industry has been constantly increasing, with the country sitting at the very bottom of world rankings for robot density in manufacturing (United Nations Conference on Trade and Development, 2017: 49).

In this context, the steep increase in car production and exports in the 2004–2014 period (Figure 1) was not the result of ‘deep qualitative changes’ (CER, 2013: 36) that created a successful export-oriented industry (Popov and Chowdhury, 2016), as the developmentalists would have it. Rather, manufacturing in the industry during this decade continued in the same ‘backward’ form, growing in line with the general upward trend in ground-rent available on the Uzbek domestic market due to the Chinese-demand-led commodity supercycle. In other words, rising exports were not a sign of the increasing competitiveness of Uzbek cars in international markets. First, these exports were overwhelmingly concentrated in Russia and, to a lesser extent, Kazakhstan, two CIS markets with which Uzbekistan enjoys low entry barriers due to bilateral and CIS-wide FTAs (Schroeder et al., 2018). Second, exports were boosted through a specific policy to lower prices for exported cars (CER, 2013) and, more importantly, due to the overvaluation of the Russian and Kazakh currency, the rouble and the tenge, respectively.

The empirical data are unequivocal as to the crucial importance of rouble and tenge overvaluation vis-à-vis the Uzbek currency (the soum) for Uzbek exports to achieve a temporary, albeit easily reversible, ‘comparative advantage’. As long as the rouble and tenge were more overvalued than the soum, despite a significant dip in 2009, exports remained buoyant through the global financial crisis and even after Russia’s introduction of a recycling duty on imported cars following accession to the WTO in 2012 (bne IntelliNews, 2014). However, once the Russian economy went into recession in 2014–16 due to the dual shocks of lower oil prices and Western sanctions over the war in Ukraine (IMF, 2017), with Kazakhstan following suit in 2015 as a result of its close economic ties with Russia (Gordeyeva and Solovyov, 2015), Uzbek car exports to these key markets almost halved in 2014 and subsequently ground to a halt (Figure 1). Simply put, recession and the ensuing collapse in the rouble and tenge exchange rate vis-à-vis the Uzbek soum cancelled out the most important ‘comparative advantage’ that Uzbek car exports enjoyed in these markets. As such, despite the temporary growth in export, the ‘value added of the manufacturing sector remains generally low, and it is likely that the nominal rise in the external surplus is also being driven by high commodity prices (as well as increases in the volume of gas exports)’ (EIU, 2007: 12).

Ground-rent, remittances and domestic solvent demand

In summary, the development of ‘backward’ car manufacturing in Uzbekistan in JV with leading MNCs closely followed the fluctuation in the magnitude of ground-rent available on the domestic market to subsidise the production of relatively expensive vehicles. As such, one outstanding issue concerns the origin of solvent demand for Uzbek cars, especially given their carrying higher prices (i.e. being ‘relatively expensive’) than the industry’s international prices. This is a question that both neoliberal and developmental state scholars writing about the Uzbek car industry leave unaddressed. Only a fraction of such demand stemmed from the country’s export markets, as only in the 2005–07 and 2010–12 period did sales to Russia and Kazakhstan surpass 50% of total production. Instead, most solvent demand for Uzbekistan’s car output was domestic, originating from ground-rent and migrant workers’ remittances (World Bank, 2013).

Following land reforms that privatised access to land, effectively turning the majority of the rural population into landless peasants, millions of people started emigrating from Uzbekistan to find seasonal work in the country’s energy-rich northern neighbours, Russia and Kazakhstan, as the latter experienced an oil-fuelled construction boom in concomitance with the commodity price supercycle. Since the mid-2000s, the billions of USD in yearly remittances sent by migrant workers, especially from Russia, have represented a key influx of hard currency into Uzbekistan next to revenues from raw material exports, helping to sustain domestic demand for the country’s ‘backward’ manufacturers (World Bank, 2013). The GoU’s decision in 2007 to allow cars to be purchased also in hard currency on the domestic market confirms the importance of this money flows from migrant workers for domestic demand in general, and this industry in particular (Reuters Staff, 2017).

Likewise, domestic demand has remained solvent due to subsidies in the form of ground-rent-bearing commodities – natural gas and wheat – circulating at lower-than-international prices in the Uzbek market. First, as explained, SOEs provided cheap gas and gas-produced electricity for ‘backward’ ISI. Despite problems especially in rural areas during the winter season, subsidised utilities were also supplied to the general population. Second, the state purchased wheat at a fixed price from farmers, and then processed and distributed it and derived products such as flour and bread at fixed prices via ‘state-owned mills, their branches, and bakeries’ (Mirkasimov and Parpiev, 2017: 76). Both represent crucial forms of ground-rent subsidisation for consumption. Together, remittances and (ground-rent) subsidies have significantly enhanced the overall purchasing power of the country’s working class. Specifically, whereas the average GDP per capita in current USD in Uzbekistan hovered around 2500 USD in 2016, for example, the same figure in purchasing power parity (PPP) in current international USD was almost thrice as much, namely about 6500 USD (World Bank data, 2016). Put differently, the value of the general population’s income as expressed in PPP indicates a higher capacity for consumption for the working class than otherwise expressed in its USD exchange rate equivalent. As a consequence, since domestic demand can at least be partially explained by ground-rent subsidisation, higher-than-international prices for Uzbek cars and other industrial commodities are yet another form of ground-rent subsidisation of ‘backward’ manufacturing capitals in the Uzbek market, which enables them to be profitable and stay in business.

In industry, huge investments in the rent-subsidised import of machinery, equipment and technology actually translated into relatively high wages for industrial workers. Although obsolete by international standards as in the case of the car industry, in the context of Uzbekistan these imports allowed for significant labour productivity growth in manufacturing, particularly on the back of high commodity prices since 2004 (Ajwad et al., 2014). Labour productivity growth has been strong in the machinery building industry, one of whose main branches in the country is car manufacturing, bridging the productivity gap between Uzbekistan and upper-middle-income countries (Trushin, 2018). Still, industrial wages in the former have risen at a faster rate than productivity (Ajwad et al., 2014), so between 2007 and 2016 wage growth in inflation-adjusted terms outpaced productivity growth in the machinery building industry in every single year but 2012–13 (Trushin, 2018). Overall, ‘in terms of wages in the manufacturing sector, in 2013 wages were 57% higher in Uzbekistan than [even] in its lower-middle income peers’ (Trushin, 2018: 14). This confirms one of the key postulates of the theory expounded here, namely that manufacturing capitals in this Central Asian republic cannot profitably produce for world market export on the basis of a relatively cheap labour force, as industrial workers in Uzbekistan are actually relatively expensive by world market norms. 10 Instead, these ‘backward’ industrial capitals can only accumulate via ground-rent subsidisation, thus mobilising a relatively expensive labour force engaged in low-end technological work, such as assembly, via obsolete equipment and technology, resulting in the production of relatively expensive goods mostly consumed in the domestic market, of which Uzbek cars are a paradigmatic case in point.

Conclusion

This paper analysed the ‘backward’ form of ISI in countries integrated into the global economy as raw material exporters, using as a case study the development of the car industry in Uzbekistan in JV with Korean DMC and American GM between 1992 and 2016. Following Iñigo Carrera and affiliated scholars, I explained late industrialisation in parts of the Global South since the 1960s within the changing material requirements of global industrial capital as a result of the automatisation of production in large-scale industry. On the one hand, some countries in Asia such as South Korea and, more recently, China, mediated the reproduction of a relatively cheap and highly disciplined labour force specifically suited to serving as operators of, or appendages to, the computerised machinery on the robotised assembly line, as the main ‘factor endowment’ for their participation in the IDL. This accounts for the rise of a NIDL with these countries’ meteoric industrialisation and transformation into the ‘world’s factory’ during the past decades.

On the other hand, most countries of the Global South continued to be integrated into the IDL as exporters of primary commodities, hence as sources of appropriation of ground-rent. This defined the way in which manufacturing capitals within their territories could only operate profitably via ground-rent subsidisation, as mediated by a combination of specific state policies. As a consequence, all these capitals – regardless of ‘nationality’ – have been ‘small’ and technologically ‘backward’ in world market terms, manufacturing relatively expensive goods largely for the domestic market. The case of Uzbekistan’s car industry epitomises this ‘backward’ form of industrialisation, as the internationally ‘small' and technologically 'backward' capital of UzDaewooAvto and GM Uzbekistan in JV with DMC and GM, respectively, received a barrage of ground-rent-subsidised benefits to manufacture relatively expensive cars for the protected Uzbek market. Consequently, production fluctuated along with the international prices of the country’s raw materials, that is, with the magnitude of ground-rent available on the Uzbek market to subsidise ‘backward’ ISI.

As such, the paper provides a corrective to the contention found in the neoliberal literature that this industry failed to develop due to inefficiency and corruption, as well as to the claim by developmental state scholars that a successful export-oriented car industry was created in Uzbekistan. Instead, the theoretical framework deployed in the article enables it to show how this ‘backward’ process of ISI in the car industry is but a specific national form taken by the global process of capital accumulation in resource-rich Uzbekistan, in line with similar dynamics in other primary-commodity-exporting countries in the Global South. In this way, the paper answers the question as to why MNCs would invest in such inefficient markets (per the orthodox scholars) given the low scale of production in manufacturing industries, whose goods are mostly purchased domestically (pace the heterodox scholars), as ground-rent subsidisation enabled all such ‘backward’ capitals to turn a profit, while justifying, at least partly, domestic solvent demand for their relatively expensive manufactured goods such as cars.

Footnotes

Acknowledgements

The author would like to thank Jon Las Heras and Greig Charnock for insightful comments on different drafts of this article, as well as two reviewers for their comments and encouragement during the peer-review process. All the usual provisos apply.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.