Abstract

Global production networks (GPN) research has given limited attention to lead firms’ competitive strategies in emerging project-based industries (PBIs). Informed by the industry life cycle approach, the authors develop a process-sensitive approach that unpacks the black-boxed notion of lead firms’ competitive capabilities development processes to address this gap. The approach is operationalized in the analysis of the evolutionary trajectories of Ørsted (Denmark) and Equinor (Norway) in the emerging offshore wind power industry. Analytically, the authors differentiate between lead firms’ pre-entry, entry, and post-entry scope-related and scale-related competitive capabilities development processes. They demonstrate how these processes are shaped by industry characteristics and co-evolve with broader industry developments and extra-firm dynamics. Through this novel perspective, the paper extends conventional wisdom on the role GPNs as facilitators of knowledge transfer and of local and regional capability formation and development. The authors argue that GPNs can also facilitate both knowledge transfer to and competitive capability formation by (lead) firms.

Keywords

Introduction

In the contemporary globalized economy, an important organizational innovation has emerged in that the production of many goods and services is increasingly fragmented and organized on a global scale (Ernst, 2002). Within a rapidly expanding strand of the economic geography literature, these fragmented organizational arrangements are conceptualized as global production networks (GPNs) (Coe et al., 2004; Yeung and Coe, 2015). In GPNs, the firms that coordinate and set the parameters for other firms in the network to comply with are referred to as “lead firms.” These firms constitute a significant analytical entry point in GPN research (Coe and Yeung, 2015). However, how firms attain and subsequently maintain their dominant position has received scant attention. Current insights into the emergence of lead firms are primarily based on research on mature manufacturing industries (Coe and Yeung, 2015; Yeung, 2016). By contrast, there is a dearth of research on lead firms’ evolutionary trajectories in emerging project-based industries (PBIs).

Emerging PBIs are comprised of entrepreneurial start-ups (de novo) but often also established firms that diversify from other industries (de alio). In general, these industries are characterized by high risk and uncertainty levels, capital intensity, technical and organizational complexity, and turbulence until some degree of stability is achieved (Davies and Brady, 2000; Forbes and Kirsch, 2011). In contrast to manufacturing industries, PBIs are predominantly characterized by one-off approaches in construction projects, “unique product” production, and fragmented processes segments (Vrijhoef and Koskela, 2005). In other words, contrary to mature manufacturing industries, emerging PBIs present entirely different sets of competitive drivers that are likely to warrant different strategic responses by lead firms in their value creation, enhancement, and capture processes.

In this paper, we focus on how two diversifying energy firms—Ørsted

1

in Denmark, and Equinor

2

in Norway—have each attained a lead firm position in the offshore wind power (OWP) industry. Similar to other renewable energy sectors, OWP emerged in the last two decades, in the context of increasing urgency to ramp up climate-friendly energy production. Diversification of firms from other sectors has been crucial for scaling up and industrializing OWP, making it pertinent to understand better how the competitive strategies and evolutionary trajectories of diversifying lead firms have both shaped and been shaped by sectoral development. We address this gap in knowledge by posing the following research question: How have the two Scandinavian energy companies each achieved a lead firm position in the OWP industry?

To answer this question, we develop a novel process-sensitive approach by bringing together the global production network (GPN) framework and the evolutionary industry life cycle (ILC) approach, thereby responding to the call for cross-fertilization of GPN and evolutionary perspectives (see e.g., Afewerki, 2020; Blazek and Steen, 2021; MacKinnon, 2012; Rodríguez-Pose, 2021; Yeung, 2021). On this basis, we conceptualize the lead firms’ evolutionary trajectory in the life cycle of a particular industry as a dynamic competitive capability development and enhancement process through which they attain their dominant position. We do so by unpacking the black-boxed notion of competitive capabilities, focusing on diversifying lead firms’ entry and post-entry industry leadership strategies in an emerging PBI. Based on Chandler’s organizational capabilities framework (Chandler, 1990), we differentiate analytically between lead firms’ scope-related and scale-related competitive capabilities, arguing that production network dynamics in emerging PBIs shape and are shaped by lead firms’ competitive capabilities development imperatives and strategies. We conceptualize scope-related capabilities as outcomes of the strategies that firms employ in entering (diversifying) into and positioning in new industries, while scale-related capabilities mainly concern firms’ post-entry competitive (market and/or industry leadership) strategies. Put simply, scope-related capabilities allow diversifying lead firms to develop a new line of business, while scale-related capabilities allow for that line of business to grow. In unpacking the lead firms’ post-entry industry leadership strategies, we specifically engage with the GPN framework’s notion of cost-capability optimization (Coe and Yeung, 2015). Informed by the literature on PBIs (Davies and Brady, 2000), we also shed light on how the lead firms’ competitive capability development strategies are shaped by the specific industry’s characteristics.

Empirically, the paper makes important contributions to GPN research through the analysis of the entry and leadership strategies of the two Scandinavian energy companies into the OWP industry. OWP has shown a remarkable development from a novel concept in the early 1990s to a multinational industry that is expected to expand significantly in the coming decades. While there have been several economic geography studies of the OWP sector from a GPN perspective (see e.g., Afewerki et al., 2019; Dawley et al., 2019; Karlsen, 2018; MacKinnon et al., 2019, 2021), they have tended to focus on territorial development outcomes rather than the relationship between firm-level strategies and broader production network dynamics.

Informed by our process-sensitive approach, we find that the two firms differ distinctly in their evolutionary trajectories, reflecting differences in their pre-entry capabilities and their entry and post-entry strategies regarding capability development in-house and in conjunction with suppliers and other external actors. Hence, we extend conventional wisdom regarding the role of GPNs as facilitators of knowledge transfer and of local capability formation and development (Coe and Yeung, 2015; Ernst, 2002; Ernst and Kim, 2002) in two main ways. First, we argue that GPNs could also facilitate knowledge transfer to (lead) firms, and competitive capability formation by such firms. Second, we extend current insights into the role of industry characteristics in GPN dynamics. Specifically, we show that as PBIs mature, lead firms’ strategies tend to shift from project-by-project approaches toward project-independent approaches, based on capturing economies of repetition and choosing appropriate network configuration (contracting) strategies.

The paper is structured as follows. The next section presents the conceptual foundations and our process-sensitive approach. This is followed by a brief introduction to the OWP industry, which serves to contextualize our subsequent analysis of the evolutionary trajectories of Ørsted and Equinor in this emerging PBI. The paper ends with a concluding discussion.

Global production networks, emerging industries and lead firms’ competitive capabilities development strategies

In recent decades, the global production networks (GPN) perspective has emerged as an influential approach for understanding globally coordinated economic organizations and activities and their territorial development outcomes (Coe et al., 2004; Coe and Yeung, 2015). A GPN is defined as an organizational arrangement comprising interconnected economic and non-economic actors involved in the production of goods or services across multiple geographic locations for worldwide markets (Coe and Yeung, 2015). In GPNs, the “lead firm” coordinates and sets the parameters for other firms in the network to comply with, often drawing its strength from “its control over critical resources and capabilities that facilitate innovation, and from its capacity to coordinate transactions and knowledge exchange between the different network nodes” (Ernst and Kim, 2002: 422). According to recent (re)conceptualizations of GPN, the involvement of lead firms’ in global production networks is induced by key capitalist dynamic drivers that explain why GPNs occur in the first place (see Yeung and Coe, 2015). These causal drivers—cost-capability ratio optimization, market development, and financial discipline—are what matter for lead firms in GPNs, prompting different types of strategies, including intra-firm coordination, inter-firm partnerships and/or control, as well as extra-firm bargaining, in different regional and national economies. Due to their key role in production networks, lead firms are important units of analysis in GPN research.

However, the overarching assumption is that GPNs serve as facilitators of knowledge transfer and local industrial capability formation (and/or upgrading) and development through a strategic coupling process (Coe and Yeung, 2015; Ernst and Kim, 2002). Indeed, GPNs have created distinct opportunities for international knowledge diffusions, providing new prospects for local and regional development (Coe et al., 2004; Ernst, 2002; Ernst and Kim, 2002; Yeung, 2021). Nevertheless, the direction of causality in the link (coupling dynamics) between lead firms in GPNs and local economies may not necessarily be one-way traffic, in that the result is either the transformation of local economies or industrial upgrading through knowledge transfer from lead firms, or in worst case lock-in. As argued by Rodríguez-Pose (2021), networks facilitate knowledge transfer and thereby contribute to fostering innovations (and local and regional development). However, “Questions need to be asked about […] who participates in networks, what are their characteristics, motivations and goals, and who can reap the potential benefits of that new information and knowledge and transform them into innovation […] understanding the channels of interaction between those generating and transmitting the knowledge and those absorbing it is of paramount importance (ibid., 2021: 1012).

We argue that the unidirectional view in the extant literature on the implications (role) of GPNs partly reflects the GPN framework’s limited focus on the lead firms’ evolutionary trajectories and hence its lack of sufficient conceptual underpinnings that depict these firms’ competitive capability development processes. To date, temporal perspectives on lead firm strategies in GPNs have focused on the strategic coupling, decoupling, and recoupling between places and lead firms (see e.g., Horner, 2014; MacKinnon, 2012), as well as on the network-level strategic reorientation process through which they achieve a dominant position (see Yeung, 2016). In other words, the focus is on how firms improve their position (i.e., upgrading), notably from their network position as an original equipment manufacturer (OEM) or an original design manufacturer (ODM) to a globally recognized lead firm engaged in original brand manufacturing (OBM) in an existing production network with distinct lead firms (Yeung, 2016).

In the GPN literature, there is a lack of insight into the temporal evolution of lead firm strategies in relation to the underlying competitive dynamics along the evolutionary trajectories of emerging industries. More specifically, how firms attain emerging industry leadership positions and what this entails in terms of integrating and managing both firm-specific internal organizational practices and external knowledge and other important linkages in order to develop competitive capabilities is underdeveloped. To address this gap, we complement the GPN framework with insights from the evolutionary ILC approach.

Industry life cycle and lead firms’ competitive capability development processes

Based on the “industry life cycle” (ILC) approach, new industries emerge from technological opportunities, opening windows for new firms’ entry and the introduction of various products and/or technological innovations (for original life cycle conceptualizations, see, e.g., Clark, 1985; Klepper, 1997; Vernon, 1966). These opportunities often arise due to a gap or discontinuity in product or service offerings (Helfat and Lieberman, 2002), which in turn entails a change in the competence requirements or production process (Vernon, 1966), or because of targeted support by non-firm actors, primarily the national state (Mowery and Nelson, 1999).

Following Klepper (1997), the evolutionary trajectory of an industry life cycle can be divided into three temporal stages. In the initial stage, market volume is low, uncertainty is high, and product designs tend to be crude. Many firms enter and there is intense competition based on product innovation. In the second stage, output growth is high, dominant designs emerge, product innovation declines, and the production process becomes more refined. Firm entry slows and a shakeout of less competitive firms occurs. The emergence of a de facto dominant design (product standards and standardization) marks the shift from emergence to a mature stage. Competition then occurs on price rather than on design, while R&D and innovation shift from focusing on product and/or technology toward process (Utterback, 1994). Consequently, market shares are reallocated to the most capable firms, while others exit the industry (Anderson and Tushman, 1990; Klepper, 1997). In the third stage, the market begins to mature and output growth slows, entry declines yet further, market shares stabilize, innovations are less significant, and management, marketing, and manufacturing techniques become more refined.

An interesting aspect of the ILC approach within the context of this paper is the emphasis on coevolutionary processes of technological change and market (industry) structure, and more importantly the defining characteristics (and/or strategies) of the successful firms that shape these processes. In this regard, the focus has been on entry timing, pre-entry experience, and innovativeness. Accordingly, firms that succeed in enhancing their capabilities and “produce new or improved products and use new or improved processes gain ‘first-mover’ competitive advantages” (Chandler, 1990: 34–35). First-mover advantage is associated with cumulative learning dynamics, meaning economies of scope and scale in production, and R&D cost spreading (Chandler, 1990; Davies and Brady, 2000; Klepper, 1996).

Furthermore, diversifying entrants with experience from related industries tend to do well in emerging industries compared with entrepreneurial ventures (Helfat and Lieberman, 2002; Klepper, 1996, 2002). Successful firms possess resources and distinctive core competencies, including capital, technology, specialized skills, and routines acquired from experience in similar activities that can be leveraged into other markets and industries (Boschma and Wenting, 2007; Mäkitie, 2020). This notion is conceptualized in the evolutionary economic geography literature (partly building on Klepper’s heritage theory (Klepper, 2002) as industrial relatedness (Boschma, 2017). In addition to the effect of specialized capabilities that can be reutilized in a different sector, more generalized pre-entry resources and capabilities are likely to affect the market choices of diversifying entrants. For example, firms with greater financial liquidity tend to undertake diversified entry farther removed from their main businesses (Helfat and Lieberman, 2002).

However, firms take account of not only leverageable internal resources but also gaps between their pre-entry resources and those required for entry and industry leadership, resulting in a need for capability development and adaptation, including through various network development and configuration strategies. Accordingly, building on Chandler’s organizational capabilities framework (Chandler, 1990), we differentiate conceptually between lead firms’ scope-related and scale-related competitive capabilities development strategies. Hence, our overarching assumption is that upon entry into new industries, diversifying firms strive to redeploy both specialized and generalized pre-entry resources and capabilities in their efforts to obtain economies of scope by offering complementary products or services at a relatively lower cost (Klepper, 1996). In the context of emerging industries, the development of scope-related competitive capabilities is contingent upon learning or the acquisition of new knowledge by firms. This can take place either internally or externally through inter-firm relations. In the OWP industry, for instance, the development of corporate ventures to fund in-house R&D has been an important strategy to develop scope-related capabilities, as has inter-firm collaboration. Also, conducive policy environments and support from extra-firm actors embedded at various scales (local, regional, national, and international) are important in this regard (Hansen and Lema, 2019). Thus, involvement in GPNs can play an important role in facilitating learning and the development of scope-related competitive capabilities by diversifying lead firms. In emerging PBIs such as OWP, scope-related capabilities also affect firms' ability to identify and capitalize on different market opportunities requiring specific approaches and technologies.

Post-entry, lead firms may accumulate additional resources and capabilities tailored to the new industry’s products and markets that form the basis for exploiting economies of scale and future market entries (Chandler, 1990; Helfat and Lieberman, 2002). Key to the realization of economies of scale for OWP lead firms includes accessing and securing productive assets (i.e., good wind resources at suitable locations), which reflects the resource imperative (Bridge, 2008) of energy producing companies. In PBIs, scale-related capabilities also concern the management of productive assets (e.g., exploit synergies across multiple projects to lower costs), process innovation and standardization, and securing the necessary financial resources to develop new projects.

Emerging industries represent an important context within which intense competition takes place between firms for dominance (Forbes and Kirsch, 2011). In the evolutionary (ILC) model, industry leadership is linked to post-entry product and process innovations by firms and can be explained by the increasing returns operating through R&D processes (Klepper, 1997). Accordingly, firms that are able to develop scale-related capabilities and manage to reduce costs tend to do well in the market. The firms with the lowest costs are often those with pre-entry experience and those that enter early (i.e., large diversifiers). Drawing on the GPN (2.0) framework (Coe and Yeung, 2015), lead firms’ development of scale-related capabilities is directly linked to their ability to optimize continuously their cost-capability ratio through their competitive and/or production network configuration strategies. These strategies encompass intra-firm coordination, inter-firm control and/or partnerships, and extra-firm bargaining. 3

The post-entry leadership strategies that firms employ to optimize their cost-capability ratios are naturally also influenced by the evolving strategies and capabilities of competing lead firms and suppliers, industry characteristics (e.g., standardized mass production versus one-off construction projects), and institutional, political, and economic framework conditions. For example, to remain competitive within the rapidly maturing OWP industry, lead firms constantly need to optimize their global production and sourcing arrangements to achieve economies of scale. This has occurred in response to increasing cost pressures in the industry due to, for instance, decreasing governmental support programs and shifts toward more competitive tendering (MacKinnon et al., 2021). In turn, this has resulted in the OWP industry becoming dominated by a relatively limited number of lead firms.

However, given that lead firms’ industrial organization strategies are shaped by key industry-specific characteristics, as argued also in the GPN literature (see Afewerki et al., 2019; Bridge, 2008; Bridge and Bradshaw, 2017; Gibson and Warren, 2016; Irarrázaval and Bustos-Gallardo, 2018), they should not be assumed to be uniform. In other words, contrary to the mature manufacturing industries, emerging PBIs such as those within renewable energy present rather different sets of competitive pressures that are likely to warrant different strategic responses by lead firms. In the next section, we provide a brief introduction to production networks in PBIs. While several industries may be characterized as project-based, this paper focuses on PBIs that deliver large-scale and capital-intensive projects, such as in the energy and construction sectors (Davies and Brady, 2000).

Global production networks in emerging project-based industries

Production networks in PBIs are typically organized around engineer-to-order (ETO) products. This distinguishes PBIs from the assemble-to-order (ATO), make-to-order (MTO), and make-to-stock (MTS) production organizations that are common in the manufacturing sectors, such as the automotive sector (Vrijhoef and Koskela, 2005). Davies and Brady (2000) outline differences between PBIs and manufacturing industries, and those differences are helpful for highlighting the implications for production network dynamics and lead firm positioning strategies. First, because production activities in PBIs are temporally and spatially fragmented, production networks in these industries are often loosely linked and aimed at the delivery of a highly customized and capital-intensive mix of products and services that are either one or a few of a kind. Accordingly, production activities are often organized on a project-by-project basis, albeit with supplier relationships often transferred across projects (Alderman, 2005). In contrast to manufacturing industries, systems integration and project management are core activities of lead firms (Hobday, 1998). Thus, the realization of scope advantages by PBI lead firms is likely to be contingent upon their efficient utilization of resources (in-house as well as external, e.g., with strategic partners), which in turn stems from the development of organizational capabilities that ensure access to markets and the successful completion of projects (Chandler, 1990).

Second, the sequence of functional activities in project-based production is the reverse of that in manufacturing industries, in which product development is undertaken first, followed by production and marketing. In PBIs, products (i.e., projects) are developed after the order is secured, often following extensive tendering processes. Production and project development processes are complex, time-bound, and have strong emphasis on front-end activities. Furthermore, they are organized in stages, such as pre-construction, construction, and operation, which often take place in different localities involving varying supplier constellations (Steen and Underthun, 2011). Therefore, depending on their pre-entry experiences, lead firms in PBIs need to develop relevant organizational capabilities for project management. They also need to develop technological (product) and/or operational capabilities either internally or externally, through varying network configuration (contracting) strategies.

Moreover, lead firms in PBIs based on harnessing and/or extracting natural resources, such as renewable or fossil energy, mining, or forestry, are confronted with strong resource imperatives (Bridge, 2008). Production activities in PBIs are territorially embedded and often depend on important geophysical or biophysical factors (Irarrázaval and Bustos-Gallardo, 2018). By implication, lead firms’ extra-firm bargaining strategies are highly important in sectors with strong state involvement in terms of regulation, planning, and support (see, e.g., Bridge, 2008; Bridge and Bradshaw, 2017; MacKinnon et al., 2019). However, in the development of post-entry industry leadership capabilities, optimizing the firms’ cost-capability ratio is crucial, regardless of the industry type. In PBIs, a capability challenge is learning across projects. However, firms may take advantage of “economies of repetition,” which in the context of PBIs refers to the “organizational capabilities, routines and processes put in place to deliver an increasing number of similar and repeatable projects more efficiently and effectively” (Davies and Brady, 2000: p. 941). In OWP, this is most obviously related to scale and the sheer volume of projects executed in a cost-efficient manner. Similar to manufacturing industries, the realization of scale advantages in PBIs is likely to induce lead firms into process innovations and more project-independent forms of organization. Finally, economies of repetition are not solely developed by lead firms but also by specialized suppliers that deliver key components and services, thus pointing to the relevance of GPN notions of intra-firm coordination and inter-firm partnership and control.

Analytical framework

In this paper, our comparative analysis of the competitive capabilities development processes of the two Scandinavian energy companies, Ørsted (the world’s largest OWP developer) and Equinor (also a major OWP developer, and a pioneer in floating OWP), aims to illustrate the importance of extra-firm dynamic drivers, firm-specific strategies, and industry-level characteristics in shaping contrasting evolutionary trajectories of lead firms in emerging PBIs. Based on the discussion in the preceding section, we argue that large diversifying firms’ evolutionary trajectories in emerging PBIs can be understood as a dynamic firm-level process of competitive capability development through which firms enter and strive to establish themselves as leaders through various GPN configuration strategies.

Accordingly, informed by the GPN framework and the literature on industry evolution, our process-sensitive empirical analysis sheds light on two key dimensions. The first dimension is Ørsted’s and Equinor’s entry process into OWP through the development of scope-related competitive capabilities. We focus on how this development is shaped by firm-specific capabilities, entry timing, and extra-firm drivers, and how these factors in turn influence intra-firm and inter-firm coordination and partnership and control strategies. For example, diversifying lead firms may undertake joint ventures (i.e., inter-firm partnerships) when they lack critical resources needed in a new market. Also, entry by M&A (i.e., inter-firm control) may work best when the resources of the target firm are complementary to the resources of the acquiring firm and there is a need for better control and coordination of production activities. Additionally, joint ventures and acquisitions provide a vehicle for the diversifying firm to gain access to (and control) tacit organizational knowledge, including market knowledge. Alternatively, established firms may opt for firm-specific (i.e., intra-firm coordination strategies) internal growth by developing in-house capabilities, for example through R&D and dedicated corporate ventures (Coe and Yeung, 2015; Helfat and Lieberman, 2002). Our analysis further accounts for the role of extra-firm dynamics in the process, as lead firms’ entry into new industries may be induced by extra-firm drivers such as regulatory and policy changes, as well as government support (Hansen and Lema, 2019; Poulsen and Lema, 2017).

The second key dimension that we focus upon in the analysis is the companies’ post-entry industry leadership strategies, which are their scale-related competitive capabilities development processes. As discussed above, lead firms’ development of scale-related competitive capabilities is contingent upon their ability to reduce costs and enhance firm-specific capabilities continuously (Coe and Yeung, 2015). Accordingly, we unpack both Ørsted’s and Equinor’s cost-capability optimization strategies in the OWP industry. As these strategies are further influenced by broader industry dynamics, we further account for how the lead firms’ strategies are shaped by the emergent and project-based nature of the OWP industry, highlighting, for instance, the importance of generating economies of repetition that allow for cost reductions across projects. Hence, our analysis sheds light on the role of project-based industrial organization in shaping firms’ cost-capability optimization strategies, as well as the changing nature (and/or temporality) of those strategies in the life cycle of the industry in relation to extra-firm dynamics such as changing business, and regulatory or policy environments (Teece, 2007).

Methodology

Our predominantly qualitative research design is informed by our research on the OWP sector since 2010 (e.g., Steen and Hansen, 2014, 2018; Afewerki et al., 2019; MacKinnon et al., 2019, 2021). As part of a broader research project (2016–2019), primary data were generated from 45 semi-structured interviews with representatives of different firms and non-firm actors (including two interviews with Equinor, and several interviews with consultancy firms and other actors with a broad overview of the OWP market) in the Northern European OWP sector from 2016 to 2019. The interviews covered firm strategies, state policies, production network dynamics, and regional development outcomes. For the purposes of the study presented in this paper, we followed three steps. First, we extracted all relevant information about the two companies gained from the interviews. Considering their status as lead firms, that material provided for relatively rich descriptions of their evolutionary trajectories. Second, we compiled secondary data, including presentations (on the companies’ strategies) by representatives of Equinor and Ørsted at various events, such as industry conferences, workshops that we participated in since 2010, and others from which material was available. Additionally, secondary data were gathered from media, company reports, an industry market database 4 , websites, and industry and consultancy reports. Third, we conducted six interviews with representatives (project managers, middle-level managers, and one head of R&D) of the two companies, and four interviews with industry experts (working in OWP consultancy, industry associations, and market intelligence). As our aim was to understand the evolutionary trajectories of the two energy companies in the OWP industry, the interview themes mainly focused on strategies and activities related to capability development, market access, and supplier relationships.

Unpacking the rise of Ørsted and Equinor as lead firms in the emerging OWP industry: An introduction to the industry

OWP first emerged mainly as a market diversification from the onshore wind industry around 1990 and has since evolved into a distinct sector with specialized supply chains and institutions that differ from other energy sectors (Poulsen and Lema, 2017; Steen and Hansen, 2018; MacKinnon et al., 2019). The evolution of the OWP sector can be divided into three phases (Dedecca et al., 2016). These phases were underpinned by technological developments, the emergence of specialized supply chain structures, presence and concentration of lead firms, and changing forms of policy support.

Following Dedecca et al. (2016), the initial innovation phase (ca. 1990–2001) was characterized by experimentation and small-scale projects (∼10 MW). Lead firms were mainly utilities with experience in onshore power production, such as Ørsted. Projects were typically developed in large EPCI (Engineering, Procurement, Construction, and Installation) or turn-key arrangements by contractors with experience from other onshore and offshore construction work. Specialized suppliers were lacking, and many projects saw both technical failures and large budget overruns. The epicenter of that development was Denmark.

The second market adaptation phase (ca. 2002–2008) saw the first commercial projects (∼70 MW) and the involvement of project developers (lead firms) from offshore oil and gas (O&G) and many large utilities from the onshore power sector, often via M&A or joint ventures. Specialized and dedicated suppliers emerged, and there was consolidation in the supply chain. Although there was continued experimentation with key components, bespoke technology for bottom-fixed OWP 5 was developed along the entire supply chain. Markets developed primarily in the North Sea and Baltic Sea (Denmark, United Kingdom, Germany, Netherlands, and Belgium), with state support in the form of feed-in tariffs or renewable energy obligations.

In the third phase (since ca. 2009), the sector has increasingly matured, as signaled by the move to dominant designs and large commercial wind farm projects (> 300 MW). The lead firms are mainly large utilities or integrated energy companies, while smaller developers have become much rarer. The supplier base is characterized by strong competition in most segments and is dominated by specialized first-tier suppliers and multi-industry firms with bespoke solutions for manufacturing and service provision (Steen and Hansen, 2014). In this way, OWP has become largely decoupled from its onshore counterpart, although it has structural couplings both to that industry and to other onshore power sectors and the O&G industry via, for example, multi-industry suppliers and diversifying energy producers. State support in the form of, for example, feed-in tariffs and contracts for difference (CfDs) has been crucial for market development, and in recent years has shifted toward more competitive bidding and tendering procedures (MacKinnon et al., 2021).

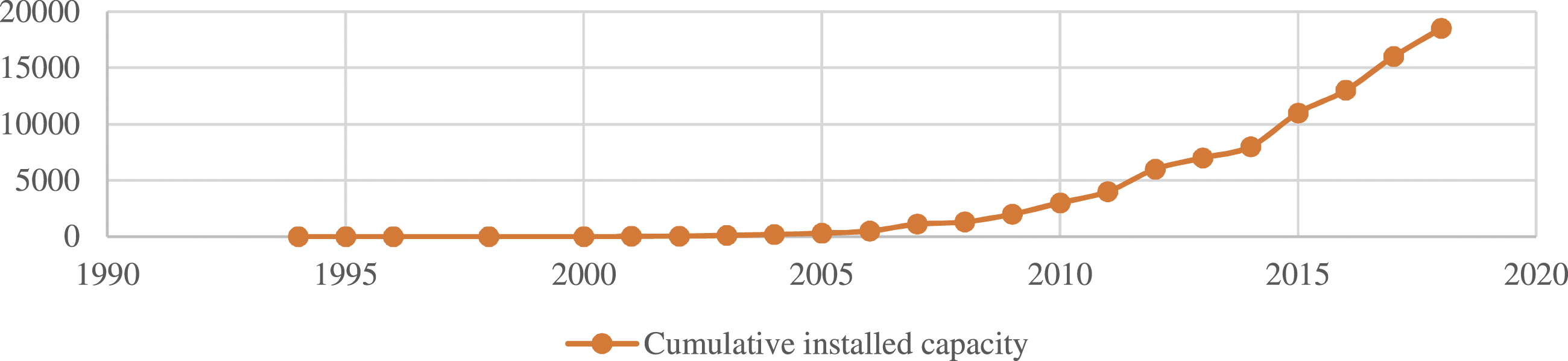

As of 2021, OWP in Northern Europe has established lead firms and relatively mature supply chains. Sectoral growth can be attributed to industry-wide technological progress, including advancements in installation and deployment technologies and methods, and the introduction of specialized and larger turbines. The development of the OWP sector between 1990 and 2018, in terms of installed power production capacity, is shown in Figure 1. Cumulative and annual offshore wind installations in Europe 1990–2018. Source: Wind Europe (2019).

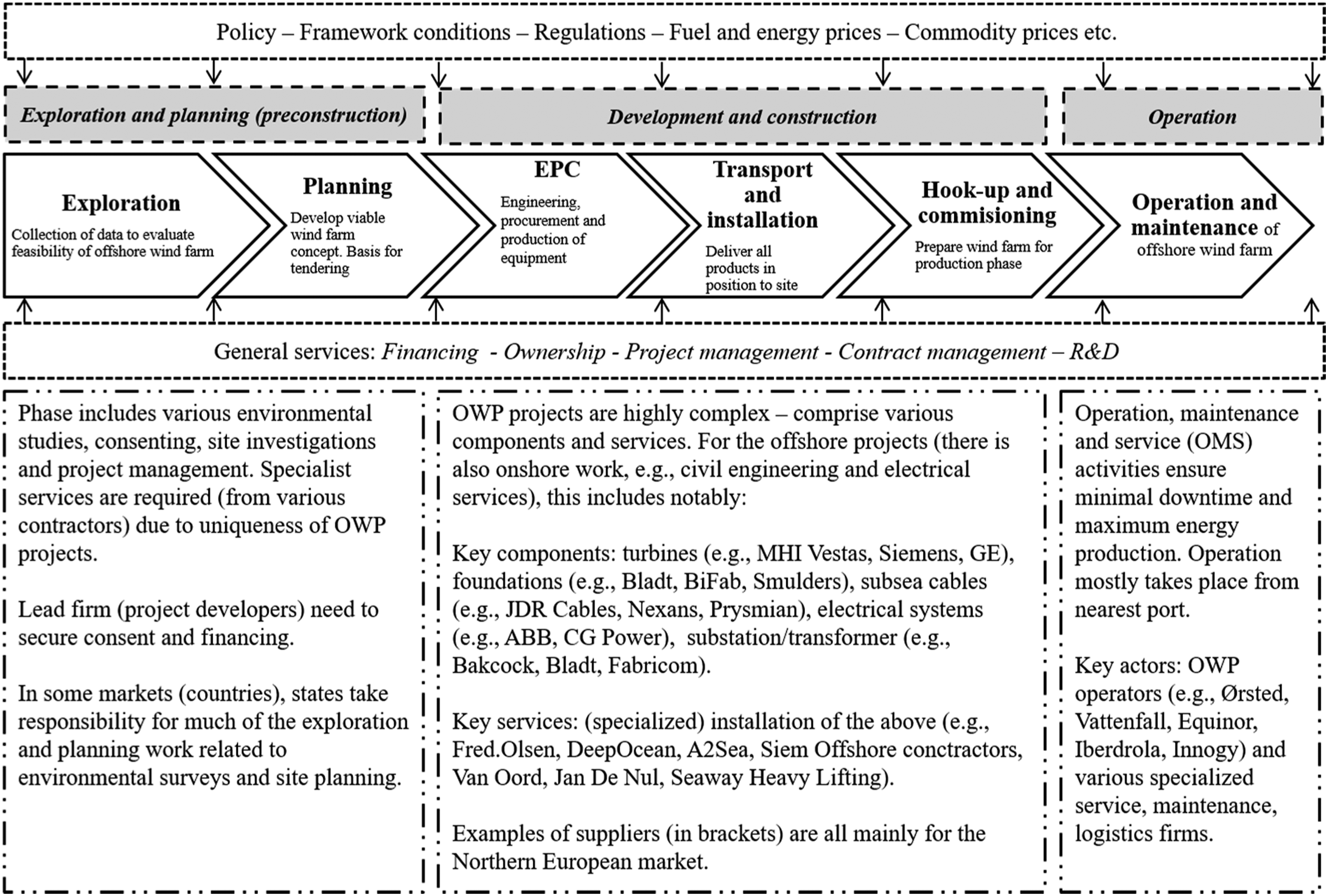

The OWP production network is structured around stage-based projects, whereby value creation activities are broadly divided into pre-construction (exploration and planning and front-end activities), construction, and operation and maintenance phases (Figure 2). These stages involve varying supplier constellations, depending on stage-specific needs and lead firms’ varying production network configuration strategies. Whereas standardization is central to the manufacturing industry, OWP is to a greater extent marked by customized specialization for “one-off” projects (Karlsen, 2018), reflecting its PBI features. OWP farm project development model. Own elaboration based on Steen and Hansen (2014).

The OWP market is national in nature, based upon the generation and distribution of electricity from wind farms to consumers through national grid systems. OWP developments require lengthy planning and consenting processes that are often shaped by the developmental aspirations of host states (Afewerki et al., 2019; MacKinnon et al., 2019). Thus, lead firms’ choice of wind farm locations and associated technology (e.g., foundation substructures, grid technology, and installation processes—all predominantly provided by specialized suppliers), associated infrastructural requirements, and the overall value creation and capture processes are determined by two key factors: (1) key geophysical factors (e.g., wind resources, water depth, distance to shore, and seabed conditions, including availability of suitable infrastructure) and biophysical factors such as marine life; (2) extra-firm bargaining strategies and country-specific energy market regulatory conditions, policy frameworks, and state subsidy schemes.

As depicted in Figure 2, a typical OWP (project) production network involves a range of firms, such as equipment manufacturers, component suppliers, logistics firms, consultancies, maintenance services providers, operators, project developers, and investors (Lema et al., 2011).The geophysical factors and subsequent demands of product scale and manufacturing volumes in such a PBI means that physical and relational proximity (Alderman, 2005) between lead firms and their suppliers is important. Thus, there is often strong locational bias in production network configurations, whereby construction bases and assembly facilities (ports) are often close to project sites. As a typical PBI organized around engineer-to-order products (ETO), OWP lead firms (developers) require most components to be ready prior to project construction in order to reduce risks in this stage (OREC, 2020).

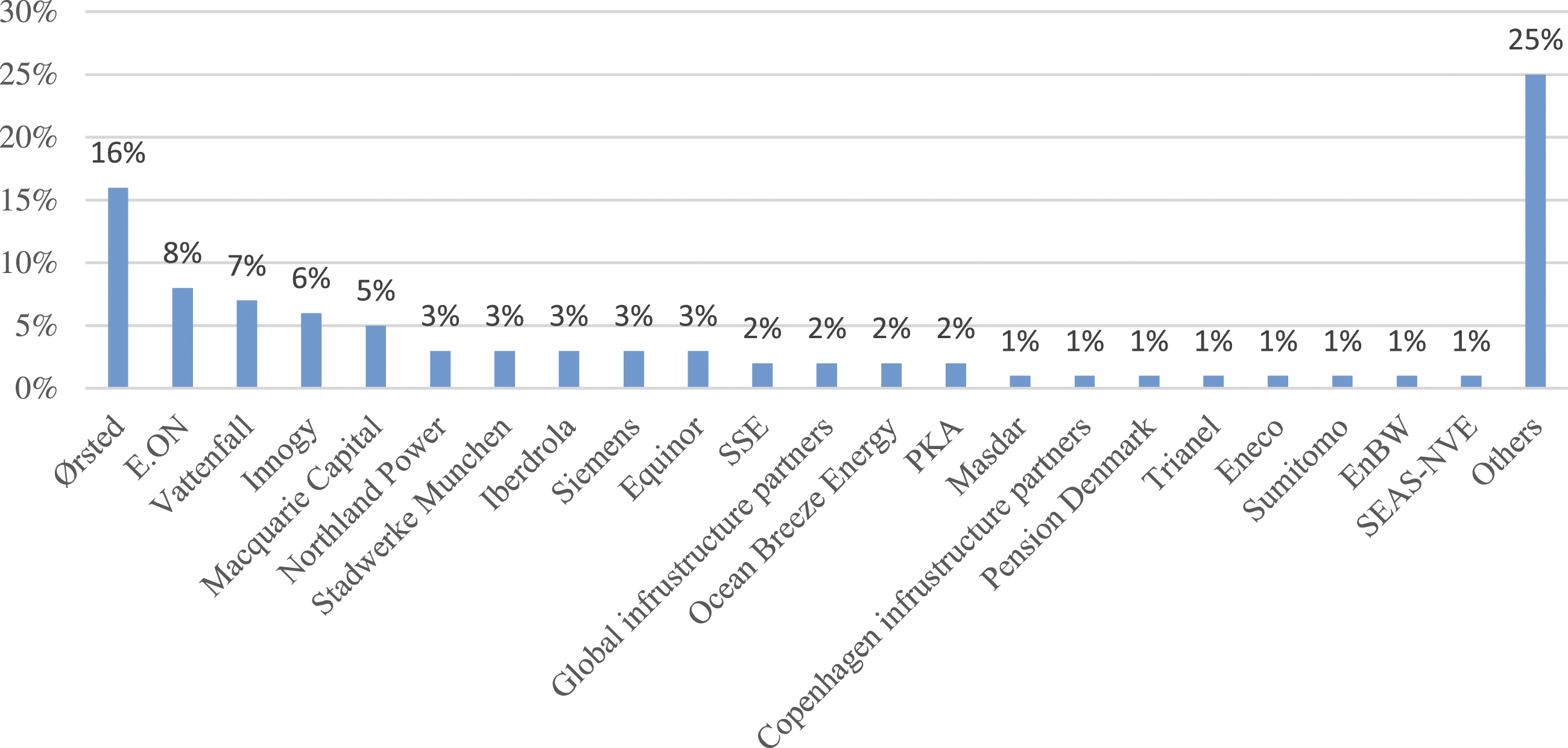

With regard to lead firms, the industry is dominated by large diversifying energy utilities (e.g., Ørsted, Vattenfall, SSE, and RWE), and petroleum companies (e.g., Equinor) (Figure 3). These utilities are important in the global green transformation due to their control of value chains related to electricity generation, distribution, and retail (Poulsen and Lema, 2017). Ørsted is a first mover and by far the largest developer and owner of OWP in Europe, with 16% of total installed capacity in 2019, whereas Equinor, a relatively late entrant to the industry, occupied 10th position with 3% of total installed capacity (Wind Europe, 2019). OW developers’ share of total cumulative installed capacity in 2019 (MW). Source: Wind Europe.

The role of extra-firm dynamics in the two diversifying energy firms’ development of scope-related capabilities in the emerging OWP industry

Ørsted’s rise to lead firm position in OWP can partly be attributed to extra-firm dynamic drivers and specifically to Denmark’s pioneer position in the development of the sector, and long-term commitment to that sector, based on its stronghold in onshore wind power. Ørsted was an integral part of the Danish Government’s policies of developing OWP-related technological capabilities (Poulsen and Lema, 2017). The Danish OWP aspiration was shaped by the country’s energy security issues (in response to the 1970s oil crisis) and rising environmental concerns in the 1980s (Danish Energy Agency, 2017), as well as prospects of “considerable economic gains, such as the opportunities for exporting wind energy components and job creation” (interview, 2017). To strengthen the competitiveness of its industry, the Danish state assisted in developing a large home market by ensuring a feed-in tariff system and grid access, and by supporting technology exports (Algers and Kattel, 2021).

Ørsted’s initial involvement can be traced back to 1985, when the two Danish power companies, ELSAM (Ørsted’s predecessor) and SEAS, received an executive order from the Danish Minister of Environment and Energy to build experimental OWP farms. This resulted in the commissioning of the world’s first OWP demonstration projects: Vindeby, 1991 (ELSAM) and Tunø Knob, 1996 (SEAS). State support triggered years of R&D and innovations in wind energy technology, with Ørsted at the forefront of those developments. The extra-firm dynamic drivers, including investments in the development of technology and the expansion of the domestic wind market, alongside the development of suppliers with the necessary capabilities and regulatory regime, coupled with the firm-specific competitive capabilities development strategies are all important factors that contributed to the rapid rise of the company as an OWP leader. As of 2021, Ørsted had over 11 GW of installed OWP capacity. Having globalized its business, 90% of its earnings come from outside Denmark (Ørsted, 2021).

In comparison with Ørsted, Equinor is relatively a late entrant into the OWP sector. Due to Norway’s high degree of energy security as a consequence of the country’s ample hydropower resources, as well as the presence of its highly profitable petroleum sector, there has been a lack of political will for domestic OWP market development (Steen and Hansen, 2018). Hence, unlike Ørsted, the role of extra-firm drivers and specifically that of the national OWP development imperatives had marginal influence on the company’s entry into the sector. The role of the state was mainly limited to subsidizing Equinor’s R&D activities related to the development of floating OWP technology. Although limited, the support contributed to Equinor’s capability development and attainment of pioneer position in the floating OWP segment in 2008 and 2009.

Reflecting the broader economic, historical, and national context within which industry emergence occurs, the two companies’ entry process into the OWP demonstrates the role of extra-firm dynamic drivers and specifically that of the state in facilitating and shaping firms’ diversification strategies and the development of firm-specific scope-related competitive capabilities.

Firm-specific scope-related capabilities development strategies

As discussed in the preceding section, Ørsted’s development of OWP-related capabilities was largely shaped by the Danish policy of nurturing domestic wind power capabilities. Ørsted’s serious diversification process into OWP began in 2002 when it became a lead investor in a venture foundation named New Energy Solutions (NES). As an important part of intra-firm coordination strategies, Ørsted set several targets, which included decarbonization of its business, OWP cost reduction, and coal phase-out: “in the increasingly climate-conscious landscape, our decision was based on the analysis that we had to develop a sustainable business model to stay relevant and competitive” (interview, 2018). This coincided with climate change increasingly becoming a political priority globally.

The NES corporate venture played a vital role for Ørsted to gain access to innovations, technological development, and capabilities in the OWP sector, reflecting how intra-firm coordination can help diversifying lead-firms develop scope-related capabilities. This capability development was further enabled through inter-firm partnership and control strategies. Accordingly, in 2007, Ørsted, together with Novo Nordisk, a leading Danish healthcare firm, launched a new business model known as a climate partnership. The partnership made the large 2008 Horns Rev II (OWP) project financially feasible, as Novo Nordisk committed to buying renewable energy certificates until 2020 (Afewerki, 2019). Since 2007, Ørsted has entered into over 100 similar partnerships with various Danish organizations, allowing it to develop comparative advantages in the wind power business area. In a joint venture with Siemens, Ørsted acquired turbine installation company A2SEA in order to control this critical part of the supply chain directly. Due to its pioneer position in the sector and signifying its early entry predominantly via internal growth (Helfat and Lieberman, 2002), Ørsted was able to attain first-mover advantages associated with cumulative learning. Through the intra-firm coordination strategy, Ørsted began its development of both scope-related and scale-related capabilities.

The restructuring processes in the global energy systems in the past decade have induced Equinor to embark on the restructuring of its business. This primarily signifies the company’s market-based shift from O&G to a broad “energy company” (interview, 2017).

Unlike Ørsted, Equinor followed a “hybrid strategy” (Helfat and Lieberman, 2002) of combining both internal growth (i.e., intra-firm coordination and relational capabilities, namely, inter-firm, acquisition (inter-firm control)) and joint venture (inter-firm partnership) driven entry into the OWP industry. First, as a latecomer to the OWP sector, Equinor has been working to position itself through investments in technology developments and specifically floating OWP to attain a first mover advantage (through technology differentiation) in a new market segment. Indeed, the company commenced its involvement in OWP through an investment in the floating Hywind concept that was originally developed after 2000 by Norsk Hydro. Second, in the conventional (bottom-fixed) OWP segment, Equinor entered through the acquisition of a 50% stake in Sheringham Shoal, a full-scale commercial UK wind farm that was commissioned in 2012. This was followed by acquisition of stakes in two additional wind farms, namely Dudgeon (UK) in 2012, and Arkona (Germany) in 2016.

Reflecting partly the role of late-entrant advantages and partly generic pre-entry resources (notably availability of financial capital) (Klepper and Simons 2000), inter-firm control (M&As), and forging strategic (inter-firm) partnerships was an important part of Equinor’s new market entry strategy: “Equinor grew as a result of partnerships […] we search for a partner that can take us forward. [In the Arkona project] EON had typically more experience than us in operating wind parks and we saw the potential in learning from them” (Rummelhof, 2016). However, industrial relatedness, meaning the company’s pre-entry experiences (Boschma and Wenting, 2007; Klepper, 2002) in subsea, offshore marine operations, and in managing large and complex project, as well as network of suppliers meant that “Offshore wind was at the heart of [Equinor’s] competence, [and] a natural progression from O&G” (Rummelhof,2016). Equinor’s Hywind concept, for instance, relies on an established technology from offshore O&G operations—the spar buoy, modified to fit the floating OWP context (interview, 2017).

Overall, the two companies’ firm-level development of scope-related capabilities was very much contingent upon their entry timing and the availability of specialized (related) and/or generic pre-entry resources. These, in turn, determined the type of strategy the firms pursued in terms of internal growth (i.e., intra-firm coordination) versus growth via M&As and joint ventures (i.e., inter-firm control and partnership), or a combination of the two.

Diversifying energy firms’ post-entry development of scale-related competitive capabilities

Ørsted’s scale-related competitive capability development process started in 2009, when the company made an official commitment to source 85% of its energy production from renewables by 2040. More specifically, as a first step, in response to the growing pipelines of OWP projects in the North Sea, Ørsted developed a new business model, which entailed following a project-independent industrialization approach to its OWP business as opposed to the project-by-project approach it had employed pre-2009. This in turn signified the growing maturity of the sector, with the emergence of dominant technology and park designs, and a shift in focus toward process innovation (Utterback, 1994). The project-by-project approach entailed planning and executing projects individually, and consequently bottlenecks in markets often caused operational challenges and higher costs.

Through its intra-firm coordination process, Ørsted started planning, contracting, and executing projects in parallel, and took the entire production network into consideration: “Our experiences from successive offshore wind projects were key in building a competitive advantage for us and bringing down the cost of energy for that technology” (interview, 2018). This ability to capitalize on economies of repetition (Davies and Brady, 2000) played an instrumental role in strengthening Ørsted’s leadership position. Furthermore, Ørsted pioneered a unique partnership model known as the farm-down and/or asset rotation approach, which signified the role of financial discipline in shaping lead firm GPN strategies (Coe and Yeung, 2015). The model entails Ørsted typically divesting 50% of its operational OWP farms to industrial and institutional partners, and reinvesting capital in subsequent projects, thus enabling scaling up production capacity and reducing financial risk.

Equinor went through a sustainability reset process between 2013 and 2014. The process resulted in a transition to low carbon economy program, which ultimately led to the creation of a division of New Energy Solutions (NES) in 2016, on a par with the company’s traditional O&G business divisions. The division, which signified an intra-firm coordination strategy, was mandated to explore new technological and business model opportunities in the renewable energy sector. Prior to the sustainability reset, Equinor’s approach to renewables was primarily to look for profitable markets where it could reutilize its O&G-related technological capabilities. However, with enhanced OWP-related capabilities, the company realized that the OWP sector presented an attractive market. By the end of 2019, Equinor had invested roughly US$ 3 billion in renewable energy. Equinor has established itself as a leader in floating OWP and aims to have 4–6 GW OWP capacity by 2026 (Algers and Kattel, 2021).

Cost-capability optimization strategies

Within this emerging industry, cost is an important competitive parameter both vis-à-vis other OWP developers and other power generation technologies (MacKinnon et al., 2021). Around the years 2009and 2010, as a relatively new technology, OWP was still expensive compared with other power generation technologies. Thus, its commercial viability was uncertain. Consequently, and particularly following the global (and mainly eurozone) economic crisis in 2012, the capital-intensive OWP sector saw a massive shakeout. Ørsted found itself at a critical juncture, “where we believed that if we managed to take the next step in providing scale to the industry, we could reduce cost significantly. But at the same time, governments increasingly wanted to see cost reduction before continuing to invest in the industry through subsidies […] That was the catch-22” (Ørsted, 2021: p. 7). Thus, deciding to forge ahead in the sector and to maintain the governmental support needed to bring down costs, Ørsted (in turn reflecting its first mover position) set a highly ambitious (top-down) target to reduce the levelized cost of electricity (LCOE) from offshore wind to EUR 100/MWh by 2020. 6 This was quickly picked up by the whole industry and particularly helped governments, especially in the United Kingdom but also in Denmark and Germany, to maintain ambitious OWP build-out targets in a time of financial austerity. In particular, this resulted in long-term price support regimes, as well as a transitioning toward a market-based approach in leasing processes. This approach, signifying the OWP PBI’s territorial embeddedness and state power, entails the state undertaking much of the planning and consenting activities before launching competitive tenders, thus leaving developers to bid based on greater certainty and security (MacKinnon et al., 2019). In turn, the market-oriented regulatory regime enhanced the competitive pressure among developers and as such has been important for cost reductions.

Another significant factor for reduced OWP costs has been enhanced capabilities and increased specialization within the supply chain in general and of key suppliers (e.g. turbine and foundation manufacturers, installation vessels providers, port operators) in particular (Ørsted, 2019). More specifically, leveraging the increased demand-driven (market-driven) supplier specializations and capabilities, this has induced developers to innovate and/or adopt innovative solutions to achieve lower overall costs and efficiency (BVG Associates, 2019). In other words, the diversifying energy firms’ industry leadership has become contingent upon cost-capability ratio optimization (Coe and Yeung, 2015) through both intra-firm and inter-firm processes.

For Ørsted, optimizing its cost-capability ratio was vital for developing scale-related capabilities both in-house and jointly with suppliers, and for optimal utilization of its wind power capacity. The intra-firm process of an “industrialization” approach discussed above was a key instrument in cost reductions through fast feedback and learning processes across the entire organization (Afewerki, 2019).

More specifically, and signifying the growing maturity of the sector, Ørsted achieved economies of scale through process innovations and standardization (Utterback, 1994). Notably, this entailed combining adjacent projects through a process known as “asset clustering,” enabling synergies, leading to lower logistics costs, fewer technician hours, fewer facilities needed, and lower inventory levels: “We have a very robust pipeline and have started planning on the basis of our whole portfolio of offshore wind developments” (Lindberg, 2016). The firm has also started employing larger and more efficient turbines, which has resulted in increased power generation capacity, while reducing the need for space, resources, and time needed for OWP installations. In sum, Ørsted has managed a ca. 66% cost reduction in OWP since 2012 (Ørsted, 2021). Learning by repetition (Davies and Brady, 2000) has been crucial in enabling the cost reduction, as have been relational capabilities (i.e. inter-firm collaboration and partnering strategies). Ørsted’s choice of suppliers in the 23 OWP projects that were fully commissioned, with Ørsted as lead firm in the UK, German and Danish markets until 2017 is indicative of how the firm has been working with the supply chain as part of generating economies of repetition and optimizing its cost-capability ratio. 7 In the projects (and irrespective of market), Bladt (turbine foundation manufacturer) was contracted 12 times, A2SEA (installation services) 16 times, and Siemens (turbine manufacturer) 14 times. In total, 9 of the 23 projects involved all three aforementioned suppliers.

As a latecomer to the OWP sector, Equinor lacks Ørsted’s volume of OWP projects. Consequently, the company strategy has been geared toward technology R&D as means to strengthen its competitive position. Leveraging its strong financial position and internal technological capabilities, it employs a range of approaches in the development of new technologies (interview, 2017). Given its almost 50 years of offshore (O&G) experience (i.e., industrial relatedness) (Boschma and Wenting, 2007), particularly around subsea resource development using floating structures, Equinor has demonstrated unique advantages in the floating OWP segment, with its Hywind foundation being based on spar buoy technology from the O&G sector.

Furthermore, to expand its capabilities and hence to achieve its technological ambitions Equinor has further relied on inter-firm partnerships and control strategies (Coe and Yeung, 2015). Similar to Ørsted, key strategies related to optimizing its cost-capability ratio include adopting larger and more efficient turbines, and standardized foundation designs and electrical systems. In both cases, these strategies (and process innovations) signify the convergence of the OWP (PBI) with the manufacturing industry.

Dynamic production network configuration strategies

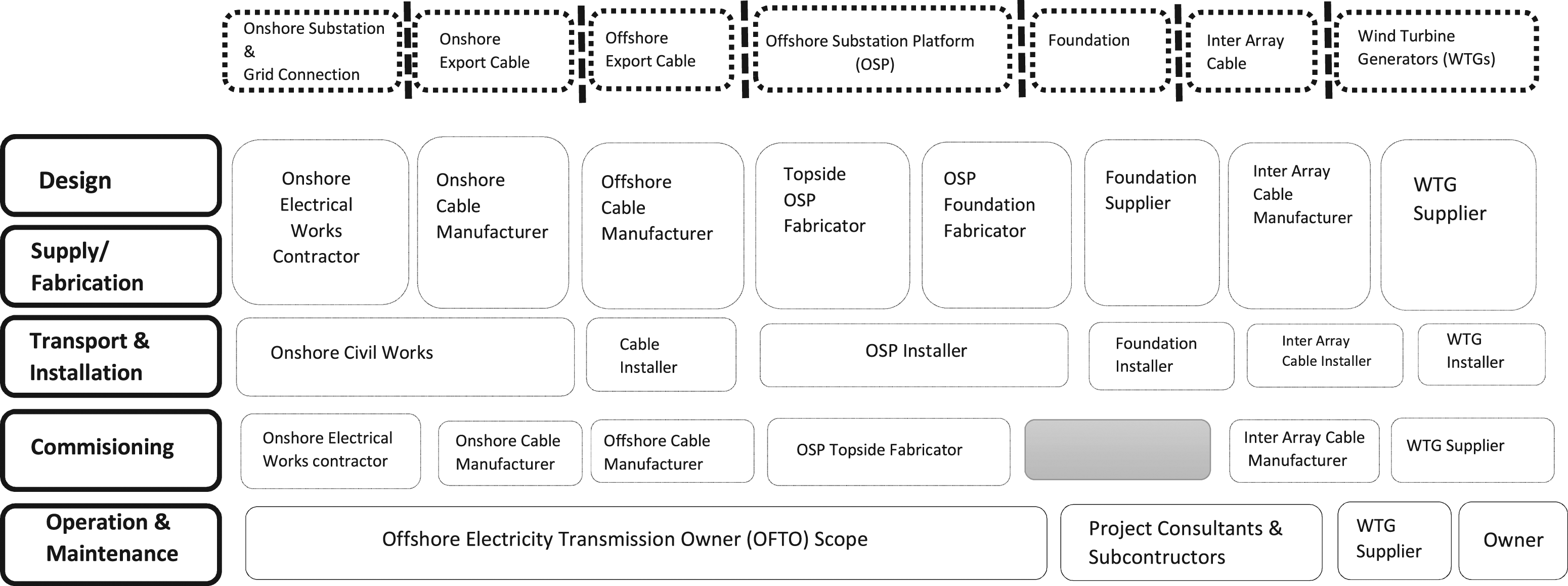

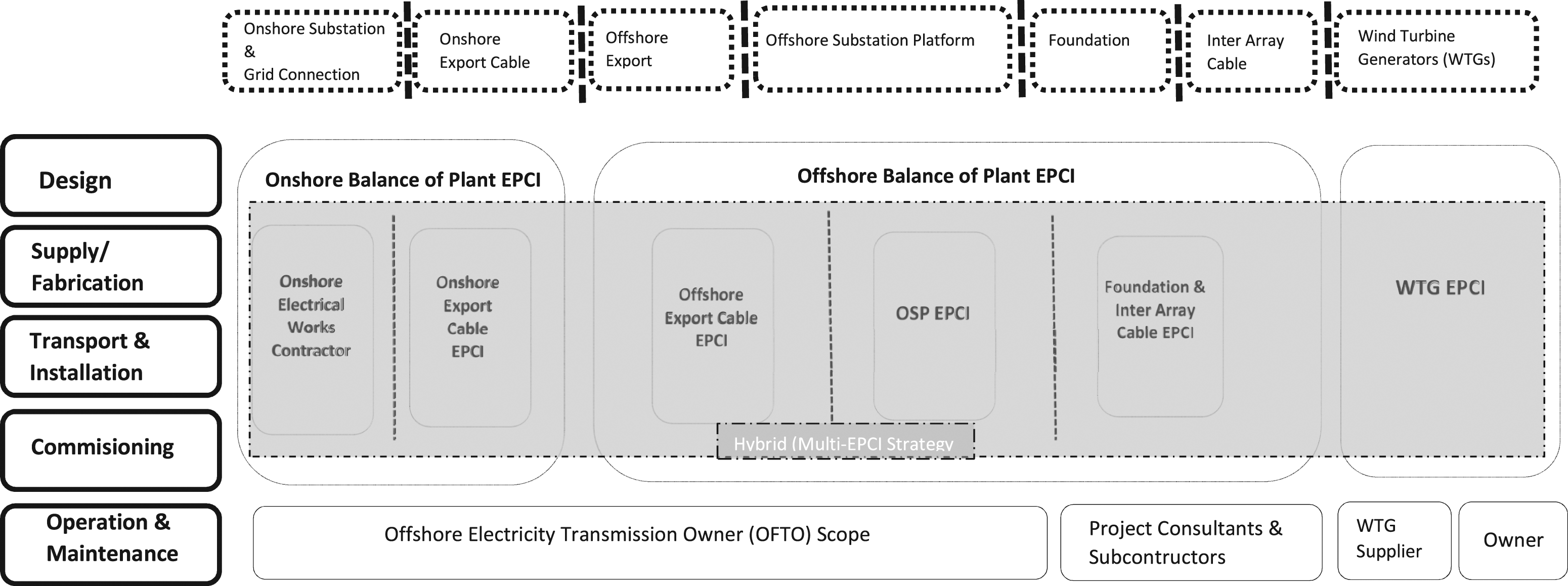

As discussed in the preceding sections, the OWP value creation activities are broadly divided into pre-construction, construction, and operation and maintenance phases. These stages involve varying supplier constellations, depending on stage-specific needs and lead firms’ varying production network configuration strategies (see Figure 2). In the emerging OWP sector, lead firms follow different contracting strategies, reflecting key characteristics of this PBI in terms of its stage-based organization of production activities, capital-intensity (and associated risks), and cost-reduction imperatives: (1) a multi-contracting strategy, which entails awarding multiple main contracts covering the key elements (stages) of the wind farm project (Figure 4), and (2) an EPCI strategy, which involves contracting two or three main packages to relatively larger experienced subcontractors (Figure 5). The EPCI strategy is often used by independent developers and less experienced utilities with comparatively less OPW-related technological and operational capabilities but often better financial capabilities (Poulsen and Lema, 2017). Illustration of the OWP multi-contracting strategy. Adapted from Thema (2020). Illustration of OWP EPCI & Hybrid (multi-EPCI) contracting strategy. Source: Thema (2020) and authors' own elaboration.

Network configuration strategies are contingent upon lead firms’ in-house capabilities. As the OWP industry has matured and stabilized, ways of procuring and managing the wide range of high-value contracts required in delivering projects have also changed, reflecting how contracting strategies are contingent upon both the in-house capability and financial strength of project developers and supply chain actors, as well as on the method of financing projects. Accordingly, in response to the cost reduction imperatives (in the life cycle of the industry) and to avoid high risk burdens on a main subcontractor, the most experienced OWP lead firms such as Ørsted have transitioned away from EPCI toward a multi-contracting approach (OREC, 2020). As is common in (mature) PBIs, lead firms invest in the technical and/or management skills internally, as they prefer to take the higher financial risk rather than pay EPCI contractors to take it (THEMA, 2020). Accordingly, and subsequent to the shift to process innovations and standardization in the third phase of OWP life cycle, Ørsted transitioned its sourcing strategy from a single supply base to multiple competitive global suppliers and procurement for multiple projects through a multi-contracting approach. As discussed, and as illustrated in Figure 4, this involved reflecting the stage-based development process, breaking down the construction work and the supply chain into as many individual packages as possible to enable Ørsted to direct control and management, which in turn was crucial for reducing uncertainty and cutting costs by enabling competitive sourcing: “Ørsted views contract management as one of its competitive advantages, as it has enabled it to drive down project costs [through competition] by dealing with the supply chain directly” (interview, 2018). More specifically, signifying a combination of the inter-firm control and partnership strategy (Coe and Yeung, 2015), the company developed to rely on a market-based competitive sourcing strategy for standard supplies, mainly in the construction phase, due to its enhanced in-house engineering, design, and contract management capabilities, which in turn showed the growing maturity of the OWP GPN and the subsequent focus on process innovation and standardization or modularization. In the case of Ørsted, this entailed strengthening the close relationships with strategic partners, including long-term framework agreements with wind turbine OEMs such as Siemens Gamesa (and other key suppliers) in the manufacturing network. This in turn ensured attractive terms for the OEMs, especially with regard to stable demand, and access to manufacturing capacity and further optimization of its cost-capability ratio for Ørsted: “[W]e are very close to all major OEMs for offshore wind turbines and therefore have a deep insight into their development pipelines” (Leopold, 2017).

Due to the strong territorial embeddedness of OWP developments (i.e., the geophysical demands of product scale and manufacturing volumes, including the need for construction sites and assembly port facilities), significant portions of the supply chain tend to be located close to the lead firm and/or the OEMs. As a result, OWP production network configurations involve intense extra-firm bargaining activities to ensure enhanced value capture in the countries that host OWP projects. Hence, Ørsted was involved in Local Enterprise Partnership programs in the UK to accommodate the 50% local content expectations (Afewerki et al., 2019).

Equinor’s aspirations to position itself in the industry through the development of floating OWP have also influenced its project sourcing strategies. For example, in the Hywind project, it applied a multi-contracting approach, thus reflecting its strong in-house capabilities in floating offshore technology. This in turn facilitated close interaction and monitoring of all project activities: “For us, close interactions with suppliers such as Siemens were vital, as these close interactions are helpful in coming up with the optimal solutions, CAPEX [capital expenditure] minimization, increasing effectiveness, and market effect maximization” (interview, 2017). However, the limited number of suppliers that could meet the special requirements associated with floating solutions when developing the pilot project Hywind Scotland meant that it was difficult to rely on international competition. More specifically, Equinor needed to make efforts to reconfigure and balance its innovation network in the face of a 50% local content expectation by the Scottish Government. However, there were no manufacturing plants in Scotland for the wind turbine generators (WGTs) or for (floating) spar foundations (interview, 2017).

By contrast, Equinor has mainly relied on an EPCI or hybrid strategy for its bottom-fixed OWP project, something it shares with other late entrants such as SSE and Iberdrola, as this allows the lead firm (see Figure 5) to manage a small number of large experienced contractors at a reduced risk but higher costs (OREC, 2020). Hence, the financial imperative (Coe and Yeung, 2015) is also an important driver of this approach, as late entrant OWP lead firms tend to use this approach especially when seeking to minimize own risk to secure project finance (OREC, 2020). However, with the increasing maturity of the sector, it is evident that the OWP lead firms’ sourcing strategies have changed, reflecting developments in their in-house capabilities (and hence cost structure), as well as suppliers’ development of OWP-related specialized capabilities. For example, in the Hywind Tampen project in domestic waters, Equinor followed a hybrid strategy of combining a multi-contracting and EPCI strategies (Figure 5), contrary to the multi-contracting strategy employed in Hywind Scotland. The hybrid contracting strategy can be partly explained by the existence of competitive local suppliers, both in terms of cost and capability, as well as assembly ports possessing specialized infrastructures (interview, 2020). However, overall, an increase in the firms’ in-house capabilities (and cost reduction imperatives) and the availability of specialized suppliers often results in the utilization of a competitive multi-contracting approach.

Concluding discussion

In this paper, we have demonstrated lead firms’ evolutionary trajectory in an emerging project-based industry (PBI), using the case of the two Scandinavian companies, Ørsted and Equinor, in the offshore wind power (OWP) industry. Informed by the GPN framework and the literature on industry life cycles (e.g., Klepper, 1997; Boschma and Wenting, 2007), our process-sensitive approach has unpacked the black-boxed notion of competitive capabilities development strategies. In this way, we have demonstrated how GPNs can shape the evolutionary trajectories of lead firms by facilitating knowledge transfer and the enhancement of competitive capabilities of these firms. So far, GPNs have mainly been understood as facilitators of knowledge transfer and local capability formation (Coe and Yeung, 2015; Ernst 2002; Kim and Ernst, 2002). By reversing the direction of causality, this paper has demonstrated how the opposite can also hold true. More specifically, by analytically differentiating between lead firms’ scope-related and scale-related competitive capabilities development strategies, our analysis has revealed how lead firms continuously configure and reconfigure their production networks. Central to this process is the integration and management of both firm-specific internal organizational practices and external linkages (relational capital) to develop competitive capabilities in order to enter and position themselves as leaders in an emerging industry.

In both cases (Ørsted and Equinor), our analysis has particularly revealed how M&As, joint ventures, and state policy played an instrumental role in their entry and scope-related competitive capabilities development activities. Furthermore, cost-capability optimization through inter-firm partnership and control, intra-firm coordination strategies, and extra-firm bargaining was crucial for the post-entry development of scale-related competitive capabilities. The empirical analysis further demonstrated how lead firms’ industrial network configuration strategies were shaped by key industry characteristics, which in the case of a PBI such as OWP particularly relates to the ability to generate economies of repetition, secure financing, and access to productive assets, as well as by choosing appropriate contracting strategies.

More specifically, beyond the significant role played by the broader economic, historical, and institutional conditions (i.e., extra-firm dynamic drivers in the initial involvement of specifically Ørsted), the paper has shed light on the two lead firms’ contrasting entry strategies into OWP. As a first mover, Ørsted primarily followed an internal growth (i.e., intra-firm coordination) strategy. By contrast, as a relatively late entrant, albeit with substantial financial resources and related capabilities, Equinor followed hybrid intra-firm coordination, as well as M&A and joint venture-based (i.e., inter-firm control and partnership) strategies. The firms’ pre-entry generic and specialized capabilities, as well as the availability of financial capital (Klepper and Simons, 2000), were crucial for the specific ways in which the firms chose to enter the emerging sector. Accordingly, and signifying the capital-intensity of PBIs such as the OWP industry, the analysis has revealed that pre-entry resources may allow latecomer diversifying firms to enter and subsequently position themselves as leaders in an emerging industry by using different strategies. The analysis has further revealed how diversifying energy firms’ post-entry industry leadership is contingent upon their ability to optimize their cost-capability ratio continuously (Coe and Yeung, 2015). However, this needs to be seen in relation to broader GPN dynamics of enhanced capabilities and capacities in the supply chain.

Based on our analysis, we identify two important contributions to the GPN literature in terms of understanding how firms attain lead firm position in emerging PBIs. First, the paper extends the GPN understanding of the emergence of production networks as an evolutionary (temporal) capability development and perpetual enhancement process by lead firms, suppliers, and extra-firm actors. As an emerging industry, OWP represents an important context within which intense dynamic processes have taken place by firms to develop their competitive capabilities, and to establish and maintain their position. Thus, from the diversifying lead energy firms’ perspective, the OWP production networks can be understood as an outcome of firms’ strategic scope-related and scale-related capability development processes. This includes a range of activities and choices with regard to learning and knowledge development, contracting strategies, business model development, partnerships, extra-firm bargaining, and securing finance. A good example of the latter is Ørsted’s climate partnerships at the beginning of its dedicated OWP journey and its farm-down financing model.

Second, the paper extends current understandings of how lead firm strategies (particularly related to their cost-capability ratio) are shaped by key industry characteristics. In the emerging OWP industry, and signifying its project-based nature, capital-intensity, and stage-based organization, lead firms follow either multi-contracting or EPCI contracting (project-sourcing) strategies. Hybrids of these ideal types of contracting strategies are also used. The key point to emphasize is that choice of contracting strategy largely reflects lead firms’ in-house capabilities, yet it is also significantly shaped by the presence of capable suppliers and sub-suppliers (MacKinnon et al., 2019). Our analysis has specifically revealed that lead firms’ GPN strategies change in response to shifting competitive dynamics and pressures in the industry life cycle. In OWP, underpinned by the firms’ enhanced in-house capabilities in conjunction with the move toward dominant designs and a more mature supply chain, the continued growth of the sector has prompted the two lead firms studied in this paper to transition from the EPCI strategy to a multi-contracting approach. This transition signifies a shift from an inter-firm partnership strategy (Coe and Yeung, 2015) to a combination of intra-firm coordination (i.e., in-housing), inter-firm control (i.e., out-sourcing of standardized products and services), and partnership (with key components and/or module manufacturers) strategies (Coe and Yeung, 2015). Accordingly, as the OWP sector has matured, the studied lead firms have shifted from a project-by-project approach toward project-independent, standardization, and/or process innovations to realize economies of repetition, and scale advantages, and hence industry leadership. As such, OWP has converged with manufacturing sectors in important ways, signifying a change in sectoral characteristics that in turn implies that the dynamics between lead firms and suppliers have transformed. Therefore, we conclude that lead firms’ production network configuration strategies should be viewed in a temporal manner.

An important implication of this paper for the broader GPN literature is that within the context of emerging industries, GPNs can play an enabling role in lead firms’ capability formation and enhancement processes. In light of the increasing urgency to change to renewable energy sources, this capability formation and enhancement, and more specifically the development of scale-related competitive capabilities by OWP lead firms (and their suppliers), could play a crucial role in accelerating the green transition process that ultimately will necessitate massive upscaling of novel energy production technologies at a global level.

While we are cautious to generalize these findings to other industries and contexts, the insights emanating from this paper with regard to how firms develop competitive capabilities and attain leadership position in capital-intensive PBIs should have broader relevance. However, more research is needed in other contexts to verify this proposition. We also believe that this enhanced understanding of lead firms in the context of emerging PBIs has relevance beyond the academic community, not least because various new industries are currently “in the making” around different renewable energy technologies and other “cleantechs” around the world. Thus, the resulting production networks and their implications for value creation and capture is a significant area of future research. While it is beyond the scope of this paper to account in detail for the influence of lead firm capability and network configuration strategies and practices on territorial development outcomes, we see this as an important future research endeavor. Future research should also account for different types of upgrading strategies (Blazek, 2016; Hansen et al., 2016) and the influence on product and process characteristics on network configurations and power relationships in different new industries.

Footnotes

Acknowledgments

The authors would like to thank Asbjørn Karlsen, for helpful comments on earlier versions of the paper. We also thank the editors and the two anonymous reviewers for their careful reviews and valuable feedback.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research was supported by research grants 255400 (InNOWiC–Internationalization of Norwegian Offshore Wind Capabilities) and 296205 (FME NTRANS–Norwegian Centre for Energy Transition Strategies) from the Research Council of Norway.