Abstract

Advanced producer services have long been theorized as pivotal in organizing the global economy. Finance takes centre stage in the advanced producer services complex as orchestrator of global flows, particularly in underwriting investment and evaluating corporate performance. The ascent of financialized globalization raises the suspicion that key advanced producer services act as rent-extracting ‘obligatory passage points’ in the orchestration of global financial flows. Competition within the financial sector is contentious given the sustained profits by globally connected banks operating in concentrated markets. Investment banks and other advanced producer services play key roles in underwriting of securities, raising questions whether underwriting is a competitive process. This paper interrogates the microeconomic foundations for the role of investment banks in investment chains to shed light on their rent extraction practices. Using a sample of 2940 initial public offerings for the USA, Canada, and Europe in the 1998–2017 period, we examine the structure of fees charged by investment banks for underwriting of equity securities. Our results are consistent with the proposition that investment banks with more market power and stronger network ties with institutional investors utilize their dominant position in the marketplace to extract rents from both issuers and institutional investors. Taken together, at times of spatial and sectoral consolidation, these results show compelling evidence for the status of investment banks and by extension the wider advanced producer services complex as obligatory passage points under financialized globalization.

Keywords

Introduction

Initial public offerings (IPOs), when companies list on a stock exchange and offer their shares to the public, help companies raise funds, scale-up and often turn founders and large investors into millionaires or even billionaires. Not all of them, however, are successful. Take for instance the biggest US technology sector IPO since Facebook in 2012 when Uber – the San Francisco headquartered ride-hailing company – went public on 10 May 2019. $8bn was raised from investors, but at the end of the first trading day, the share price was 8% lower than the IPO price of $45 per share, making it one of the worst first-day performances for a large IPO in history. By contrast, most IPOs realize a positive return on the first trading day, a phenomenon termed IPO underpricing (Liu and Ritter, 2011). While some blamed adverse market conditions, US–China trade tensions and Uber’s creative accounting, it was clear that the company and its advisors misread the market. Still, despite the disenchanting launch, Uber paid $106 m in fees to a syndicate of investment banks (IBs) that underwrote the IPO, led by Morgan Stanley, and most likely millions to accountancy (PwC) and law firms (Cooley LLP and Covington & Burling LLP) involved (Shen, 2019). 1

What justifies such high underwriting and other servicing fees despite abysmal performance? Is the ability of IBs to charge high fees a sign that these fees represent more than the service of making a company publicly tradable? If fees are charged irrespective of the IPO’s ‘success’, does this indicate that IBs are able to extract rents from counterparties in the process? And what does it tell us about structural dominance of certain intermediaries in financial and cognate services procured by what has been dubbed the advanced producer services (APS) complex? Previous research indicates that competition in APS markets in general and investment banking in particular might be limited (Christophers, 2018; Crotty, 2008). Following the 2007–2009 North Atlantic Financial Crisis, the scholarly consensus among critical observers is that global IBs have grown too-big-to-fail and are instrumental in producing recurrent crises (Tooze, 2018). Although investment banking activities have shrunk and shifted geographically since the crisis, US banks continue to dominate despite the rising importance of Asian capital markets (Wójcik et al., 2018b), as do Anglo-American accountancy and law firms (Faulconbridge, 2019).

Bassens and Van Meeteren (2015) propose to theorize the APS complex as an obligatory passage point under conditions of financialized globalization. Key in this notion is that the strategic positioning within financial networks (Van Meeteren and Bassens, 2016) enables the APS complex as a fraction of capital to extract class-monopoly rents (Harvey, 1974) from the wider economy. The APS complex, in general and tangibly in its local manifestations in financial centres, is comprised of strong formal and informal interdependencies within and between APS sectors, with finance acting as the crucial intermediary (Bassens et al., 2020). However, the relation between these interdependencies and rent extraction remains unexplored. Given IB’s current level of concentration, consolidation and their crucial intermediary function in financialized globalization, it seems IBs are well placed to drive rent extraction by the APS complex.

This paper examines whether the rent extraction characteristic of the APS complex can be pinned down within the practices of IBs. As IBs are rather inaccessible to researchers, we seek robust evidence of rent extraction by analysing observable outcomes of IB activity. We analyse gross spread and IPO underpricing as potential rent extraction channels. Gross spread is a direct fee charged for IPO underwriting services in a form of a percentage discount on issuer’s IPO share price, when shares are sold by the issuer to an IB prior to an IPO (Abrahamson et al., 2011). IPO underpricing is the difference between the end of the first trading day market value of issuer’s equity securities sold in an IPO and the issue price of such securities, effectively money left on the table and an indirect cost from the issuer’s perspective (Liu and Ritter, 2011). The focus on IPOs is all but happenstance, since they have been identified as instrumental in shifting risks and rewards among issuers, investors, intermediaries, workers and the state (Lazonick and Mazzucato, 2013). Following such readings of the risk-reward-nexus, one may even doubt the primary purpose of IPOs is to attract capital or rather an instrument to extract value for shareholders in the wider economy and society (Mazzucato, 2018). We deploy econometric methods to test a set of hypotheses originating in political-economic theory on a sample of 2940 IPOs in USA, Canada and Europe in the 1998–2017 period from the Dealogic Equity Capital Market (ECM) database. We estimate a series of linear regressions to determine whether market power and network ties of underwriters with institutional investors are statistically significantly related to gross spread and IPO underpricing, beyond what can be explained by IPO characteristics and market environment. Statistically robust evidence of such relationships can be interpreted as evidence consistent with the existence of IB rents.

Our findings show that IPO underpricing is the main channel for rent extraction. Underpricing provides more quantitative potential than gross spread, but it is also statistically more robustly linked to the characteristics of IBs that we associate with the status of APS as an obligatory passage point. These characteristics relate to oligopolistic market competition supported by the market power and network ties of IBs with institutional investors. Our results are consistent with the proposition that IBs with a more dominant positioning in an oligopolistic marketplace can extract higher rents from issuers and investors. Crucially, IBs rely on other actors within the APS complex to both deliver IPOs and to extract rents. Accounting and law firms are indispensable in co-producing IPOs, while IBs need institutional investors in order to place IPO securities. As we show, IBs in fact rely on cooperation with institutional investors to extract rents, thus corroborating the importance of interdependencies within the APS complex. Had it not been for the cooperative mechanism of rent extraction and rent sharing among IBs and institutional investors, value that is currently captured by the APS complex would have been either retained by issuers’ pre-IPO shareholders or passed onto individual investors following an IPO. Similar interdependencies and rent sharing may also exist among IBs, accounting and law firms. Consequently, in order to understand the rent extraction by IBs, we need to consider their role within the APS complex and their interactions with other key APS actors.

We proceed as follows. We first explain the structural importance of the APS complex under financialization and the role of IBs therein, followed by formulating hypotheses related to the specific mechanisms linking IB characteristics and fee structures in IPO underwriting. The subsequent section describes our data and the methodological operationalization of rent extraction. We then present findings from the econometric analysis, while the discussion section relates our results to the existing literature on investment banking, APS complexes and rent extraction. We conclude with the implications of this study for scholars in financial geography and political economy more widely.

The APS complex and the extraction of class monopoly rents

Our central proposition is that a distinct class of APS intermediaries form a complex that is in the position to extract rents from the wider economy. While the terminology of a ‘complex’ has traditionally been used to denote ‘industry complexes’ around a central ‘propulsive firm’, traditionally the oil refinery or steel mill, on which the other actors in the complex are structurally dependent (Kramer, 1991), it is in the world and global cities literature (Bosman and De Smidt, 1993; Sassen1991 [2001]) that the different APS sectors were first theorized as a complex. These ‘complexes are characterized by sets of identifiable and stable relations among firms which are in part manifested by their spatial behaviour’ (Gordon and McCann, 2000: 518). A complex is not reducible to its constituents, as no actor within the system has ‘all of the necessary information about technology, labour specialization, product innovation and markets’ (Gordon and McCann, 2000: 519). That is, financiers, lawyers, accountants, consultants, together perform an economic function that is more than the sum of its parts, like bringing an IPO into being (Pan et al., 2020). In a recent article, Bassens et al. (2020) confirm the existence of the APS complex through an analysis of its internal relations and note that it is particularly the ‘para-financial’ complex centred around finance, law and accountancy that exhibits the characteristics of an intertwined cluster. Wójcik (2020) also confirms that finance has increasingly been the ‘propulsive actor’ that determines the direction and strategy of the APS complex as a whole.

Key to our argument is that the club-like nature of the APS complex enables its members to reap class monopoly rents (Harvey, 1974). Such a perspective hails back to political economic readings of world and global cities that centre on the historical or contemporary power of metropolitan fractions of capital (Arrighi, 2010 [1994]; Braudel, 1984; Krätke, 2014; Parnreiter, 2019). On an abstract level, the structural power of the APS complex originates in its ability to connect production space with financial space at a time of overaccumulation (Bassens and Van Meeteren, 2015). Connecting financial space with production space is not by definition rent-seeking behaviour. The organizational service work of the APS complex in bringing new ventures into being through capital pooling that would not exist otherwise can be regarded as ‘productive’ (Walker, 1985). However, this changes under conditions of overaccumulation or ‘the wall of money’ (Fernandez and Aalbers, 2016), which implies that there is more capital in the world than can realize itself, and thus, there is a financial incentive for gatekeepers to leverage their power to give certain capital fractions preferential treatment in accessing profitable capital circuits (Bassens and Van Meeteren, 2015). It is hypothesized that the capacity of the APS complex to arbitrate access to investment opportunities with the best risk-return profile is a source of ‘class monopoly rents’ where ‘the rate of return to a class of providers of a […] resource […] is set by the outcome of conflict with a class of consumers of that resource’ (Harvey, 1974: 239). This resource central to the APS-complex’s power is a bundle of intangible assets – ‘nonfinancial assets that lack a physical substance, are nonrival in consumption and are at least partially appropriable’ (Durand and Milberg, 2020: 404). It is only in the collaborative work of the APS complex, their combined legal, organizational know-how and social networks, that this bundle of intangible assets emerges and makes class-monopoly rents possible. Such rents manifest themselves as the APS complex extracts a fee from the use of their collective intangible assets, regardless of whether that knowledge ultimately results in profit for the consumer of that knowledge. In the words of Christophers (2019: 315): ‘The specific problem of rent is not that it is unearned. It is that the rentier enjoys monopoly power in both the control and marketization of [the rentier’s] asset’.

The concept of class monopoly rent provides a degree of theoretical closure, yet it also puts the actual practices by the APS complex into a black box, effectively theorizing the complex as a dominant (transnational) class fraction (Jessop, 1982), difficult to disentangle empirically. The fact that APS collectively control an intellectual monopoly (Rikap, 2020) that is able to distribute risks and rewards of capital does not mean they act as a concerted monopolist. We hence need to open the black box at the micro-economic level to unpack the internal hierarchy within the complex (Van Meeteren and Bassens, 2016) and to identify which firms are in a power-position that allows rents to be appropriated.

This logic brings us to the IBs, which occupy the core of the APS complex (Wójcik, 2012, 2018). Investment banking covers a diversity of services including mergers and acquisitions, IPOs, bond issuance and brokerage (Wójcik et al., 2018a). Some of the work of IBs is infrastructurally important for the global financial system, yet there is also an incentive to drive up their fee-based income to the detriment of their clients (Folkman et al., 2007). Gatekeeping and gauging the access to any service or platform can be conceptualized as a rent source, and access to IB services and networks is no exception (Sadowski, 2020). If there is one actor in the APS complex that can control the spigot of surplus value obtained by the APS complex by ‘manipulating expectations and contingent contracts’ (Foley, 2013: 264), it is the IB.

Our empirical focus is to examine the extent to which the character of IBs as obligatory passage points in key markets correlates with the direct and indirect fees for their services. High industry concentration and routine involvement of leading IBs in IPO underwriting have already been identified as an environment conducive to corespective competition to sustain high profits in seemingly competitive markets. ‘Corespective competition points to an industry regime, in which large firms compete in many ways, but avoid the kinds of competitive actions such as price wars, that significantly undercut industry profit’ (Crotty, 2008: 170). Corespective competition also suggests that IB markets are prone to network externalities where a central position in the field becomes equivalent to a club good (Van Meeteren et al., 2016: 67). The notion of club goods emphasizes that only a select number of leading underwriters are central enough to have the capability to make their sub-network of underwriters act in concerted fashion (Gemici and Lai, 2019). Empirical evidence shows that securities underwriters benefit from their network centrality and grow faster than their lesser-connected competitors (Pažitka and Wójcik, 2019). As the case of Uber introduced above shows, the substance of these club goods is not always about enabling ‘productive’ investment, even though this is certainly possible. Rather, the ‘service’ offered by IBs is granting issuers access to their concerted sub-networks of institutional investors, where the risk-reward combination is distributed in their favour, a power derived from the IBs’ ability to place and deal securities through their networks. The implication of market power and club access inequalities is that the monopolizing global networks of the most successful IBs form the basis of their competitive advantage vis-à-vis lesser connected IBs. Such power inequalities in turn play out in the uneven ability among IBs to act as crucial intermediaries in investment chains – a theme we turn to in the next section.

IBs as an obligatory passage point in investment chains

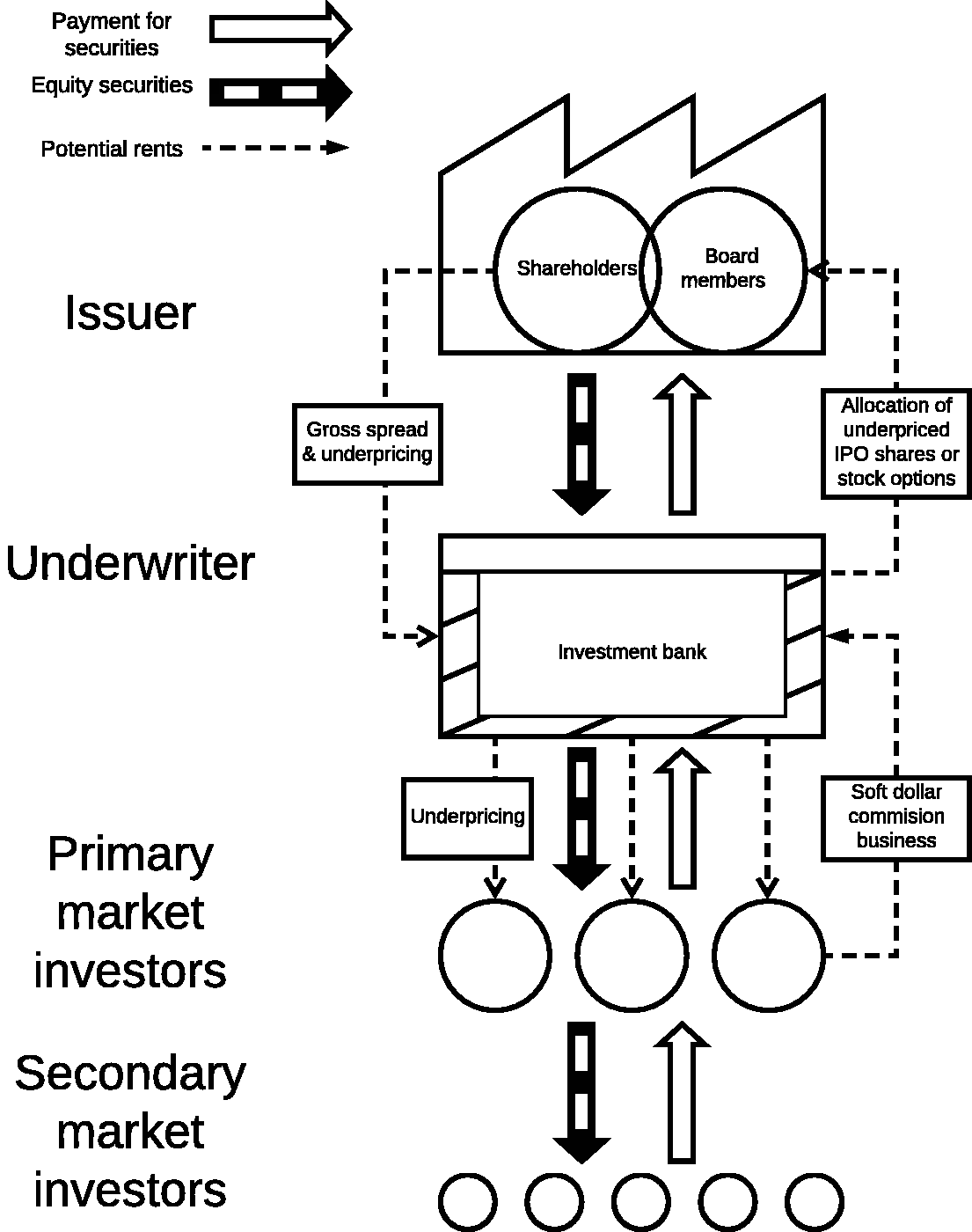

Investment chains are composed of ‘the sets of intermediaries that “sit between” savers and companies or governments, along with the links between those intermediaries’ (Arjaliès et al., 2017: 4). The investment chain concept elucidates how fees and investment returns are generated and distributed among IBs and institutional investors (Figure 1). Bookbuilding IPOs have been historically the dominant mechanism for underwriting IPOs in the US and have become common worldwide during the last 20 years (Abrahamson et al., 2011). What makes bookbuilding IPOs distinctive from other mechanisms such as open auctions is that the bookrunner (the leading underwriter of the IPO) collects expressions of interest from institutional investors during a marketing campaign, referred to as the roadshow, and the bookrunner then allocates equity securities to investors on discretionary basis. This puts IBs in a power position, as they have full discretion over the allocation of typically underpriced securities, which are a source of investment returns for institutional investors (Liu and Ritter, 2011).

Mechanisms of potential rent extraction in IPO underwriting.

We identify two mechanisms of potential rent extraction in IPOs (Figure 1). First, IBs earn fees in the form of a gross spread. This is a direct fee paid by the issuer as a percentage of the value of underwritten securities and is agreed prior to the offering, along with the price at which issuers’ securities will be sold to primary market investors. Gross spreads paid by issuers are substantial, typically 7% for US IPOs, and highly clustered, indicating potential implicit collusion among underwriters (Abrahamson et al., 2011). While the jury is still out on whether or how exactly underwriters collude to maintain gross spreads high, it appears that gross spread would at least in principle allow for rent extraction by powerful underwriters, who are able to leverage their strategic positioning in oligopolistic markets in order to extract excess fees from issuers.

Second, IPO underpricing presents a much more intricate mechanism of potential rent extraction and it allows actors other than IBs, including institutional investors and issuer’s board members, to also extract rents. Concurrently, the ability of IBs to extract rents through IPO underpricing relies on their collaboration with institutional investors and issuer’s board members. Institutional investors may extract rents from issuers’ pre-IPO shareholders by making their participation conditional on being able to buy securities in IPOs at a price that is on average below their market price in the secondary market. To do so, they however rely on IBs to price IPO securities accordingly. This persistent phenomenon has been termed IPO underpricing and allows primary market investors to realize a return on investment that oftentimes exceeds 10% during the first trading day following an IPO (Liu and Ritter, 2011). Receiving allocations of securities in IPOs, which are on average substantially underpriced, presents a very lucrative investment opportunity for institutional investors, and as a result, bookbuilding IPOs are often heavily oversubscribed. Underwriters have discretionary power over the allocation of securities in IPOs, and consequently, investors rely on their relationships with underwriters to receive allocations of securities in IPOs. This opens up the IPO underpricing channel for rent extraction by IBs.

IBs underprice IPOs for a variety of reasons, including compensating investors for risk, as well as to extract value from issuer’s pre-IPO shareholders and pass it onto institutional investors (Liu and Ritter, 2011). In doing so, IBs reduce their own gross spread revenue (Abrahamson et al., 2011). However, it has been documented that IBs are able to recoup about 50% of IPO underpricing from primary market investors in the form of trading revenue and analyst research fees (Nimalendran et al., 2007; Reuter, 2006). Recuperation is typically achieved through tacit understanding among underwriters and institutional investors that revenue generated for the underwriter through needless trading of liquid stocks prior to an IPO will be rewarded with a proportional allocation of underpriced securities. The rewards show that this fee income is a form of kickback for access to highly profitable investment opportunities and it more than offsets the underwriters’ loss of gross spread revenue, a direct consequence of IPO underpricing. Consequently, IBs can extract rents from both issuers and institutional investors by underpricing IPOs. Institutional investors are net beneficiaries of this process, which incentivizes them to participate. What ultimately allows IBs to extract rents in this manner is their discretion over the pricing of IPOs and the allocation of securities to institutional investors 2 (Liu and Ritter, 2011).

IBs may also share a fraction of the rents extracted with the issuer’s board members through allocations of IPO securities or stock options. This kickback channel has been primarily linked to securing client loyalty by underwriters (Liu and Ritter, 2010). These observations allow us to formulate the following hypotheses on the relation between gross spread, IPO underpricing and the market power of IBs.

Rent extraction has been linked to oligopolistic positioning in the market for equity underwriting services. Various proxies for market power of underwriters have been considered, including market share, industry experience and provision of leading equity analyst research (Liu and Ritter, 2011). The consideration of IBs’ network ties with institutional investors seems like a natural extension to this list of dimensions of oligopolistic market competition due to the crucial importance of underwriters as intermediaries between issuers and investors. However, IBs’ institutional investor networks have only recently been introduced in research interrogating the APS complex (Gemici and Lai, 2019) and have not yet been utilized to analyse rent extraction in IPOs. Despite the empirical difficulties of measuring ties of IBs to institutional investors directly, the network centrality of IBs in syndication networks 3 can serve as proxy for those ties.

Existing empirical evidence on the relationship between network centrality of underwriters and IPO underpricing contradicts the finance theory on information asymmetries in markets. While finance theory suggests that information asymmetries and consequently risk premia demanded by investors can be reduced by the presence of reputable and trusted intermediaries (Beatty and Ritter, 1986; Booth and Smith, 1986), network centrality of underwriters has been found to raise, rather than lower, IPO underpricing (Bajo et al., 2016; Chuluun, 2015). Existing explanations for this contradiction are still underdeveloped. For Bajo et al. (2016), more central underwriters reduce their own compensation and transfer additional value to investors to incentivize them to participate in IPOs. More intuitively, one would expect that if anything, less-connected underwriters may have to pay a premium for investors’ attention. In a related study, Chuluun (2015: 76) explains a positive partial correlation between underpricing and reciprocity in underwriters’ peer networks by suggesting that ‘[b]ook managers that maintain more reciprocal peer relationships tend to underprice more, possibly to compensate its relationship partners’. The need to compensate institutional investors more, when the lead underwriter is better connected, is not established and neither is the underwriter’s motivation to do so. We propose that the relationship between network centrality of underwriters and IPO pricing can be better explained through the mechanism of rent extraction. We hypothesize that underwriters with stronger ties with institutional investors are able to leverage their strategic positioning in investment chains to extract rents through either gross spread or IPO underpricing channel.

Research design

To construct our dataset, we start with all IPOs (34,447) underwritten between 1993 and 2017 available in Dealogic ECM database. This database has been previously used in studies of IPOs (Abrahamson et al., 2011), network connectivity of financial services firms (Pažitka and Wójcik, 2019) as well as financial centres and urban networks (Pažitka et al., 2019). Despite the shortcomings of the database regarding the availability of geographical data and its scope being limited to selected investment banking services, it provides a highly comprehensive record of IPOs and their characteristics. We then introduce restrictions to homogenize the sample, which have been used in related research (Abrahamson et al., 2011; Bajo et al., 2016; Chuluun, 2015; Liu and Ritter, 2011). We limit our sample to issuers and stock exchanges located in the USA, Canada and Europe (16,141 IPOs). We restrict ourselves to bookbuilding IPOs (10,408), given that, unlike auctions or other IPO mechanisms, they give underwriters full discretion over the allocation of shares to investors and consequently allow for rent extraction. We exclude closed-end funds, real estate investment trusts, American depository receipts, convertibles, global depositary receipts and unit trusts. We also exclude IPOs of financial companies (four-digit SIC starting with 6), deals without an offer price available in Dealogic ECM database, and IPOs that have been withdrawn. For the 1993–2017 period, these selections leave a sample of 8,388 IPOs. We use this dataset to construct our explanatory variables that rely on lagged observations, including network centrality and market share. For our econometric estimation, we use IPOs for the 1998–2017 period, for which data on gross spread or underpricing, as well on all explanatory variables, is available. This gives us 2,940 IPOs with all the necessary data available to model gross spread and 2,831 to model IPO underpricing including 2,171 US IPOs, 113 from Canada and 656 from Europe.

To operationalize our model of rent extraction (Figure 1), we use gross spread and IPO underpricing as dependent variables. Neither gross spread nor underpricing can be equated to rents, as there are numerous factors that influence gross spread and underpricing, including expenses incurred by underwriters and risk premia required by both underwriters and investors. Underwriters’ expenses in our sample range from 2.5% to 25% of gross fees, 4 hence most variation in IPO costs is due to risk premia and rent extraction. Unfortunately, neither risk premia nor rents can be isolated as easily as underwriting expenses. We can, however, disentangle the variation in gross spread and IPO underpricing by modelling gross spread and underpricing as a function of their known determinants that control for the variation related to the risks and costs associated with offerings and the market environment. We propose that the variation in the pricing of IPOs associated with market power and network ties with institutional investors is symptomatic of rent-seeking behaviour. Evidence of rents derived from individual transactions can then be also interpreted as evidence of rents at the systemic level, given that class monopoly rents are in effect an aggregate of rents earned from individual IPOs.

We employ three distinct proxies to measure the market power of underwriters. First, market share is used as a measure of positioning of IBs in what Liu and Ritter (2011) characterize as an oligopolistic market structure for underwriting services. Second, we employ an industry experience variable, operationalized as the number of IPOs in a given industry, underwritten by the IPO’s lead underwriter. Finally, we include an issuer-specific Herfindahl–Hirschman Index (HHI), utilizing Liu and Ritter’s (2011) specification. This index builds on the notion of oligopolistic competition in IPO underwriting markets and controls for the concentration within a subset of underwriters, which are identified as relevant competitors to the lead underwriter.

We operationalize our measures of network ties with institutional investors by measuring various network centrality indicators of underwriters in syndication networks, which are formed through consecutive rounds of underwriting syndicates. We utilize degree centrality, two-step reach centrality, Burt’s (2004) network constraint, Freeman’s (1979) betweenness and Bonacich (1972) eigenvector centrality, defined in Table 1. Although an indirect measure, network centrality of underwriters is closely related to network ties with institutional investors. The specification of our network centrality variables is based on the observation that underwriting syndicate members are selected purposefully to broaden the pool of institutional investors involved in an offering. Hence, we assume that underwriters that have been involved in syndicates with a wider pool of their peers will on average be able to facilitate access to a wider pool of institutional investors for issuers (Pollock et al., 2004). To isolate the effects of market power and network centrality of underwriters, we control for a wide range of IPO characteristics and market environment variables identified by previous studies (Abrahamson et al., 2011; Bajo et al., 2016; Chuluun, 2015; Liu and Ritter, 2011). Table 1 defines these variables, presents their descriptive statistics and data sources.

Definitions of variables, data sources and descriptive statistics.

aUnderwriter’s network centrality and market power variables relate to the most central/powerful underwriter by each measure, if multiple underwriters were involved in an offering.

Equation (1) represents an econometric model of gross spread as a function of network centrality (NetCen), market share of the lead underwriter over the last five years (MktShare), industry experience of the lead underwriter (IndExper), issuer-specific HHI (IssuerSpecHHI) and a vector of control variables (C). Equation (2) includes the same four variables of primary theoretical interest as well as a different set of control variables linked to underpricing in the related research (C*). Both equations are estimated using an ordinary least squares (OLS) estimator and heteroskedasticity consistent standard errors to calculate t-statistics. The correlation between market share and degree centrality is 0.76 across our sample of IBs. This reassures us that not only both explanatory factors are suitable proxies for positioning of IBs in an oligopolistic market structure but that they may also be subject to statistical conflation. To address this, we follow Bajo et al. (2016) and use the residuals from a linear regression of market share on all network centrality variables instead of the raw market share, thus effectively orthogonalizing these variables.

Results

We begin with examining the empirical distributions of gross spread and IPO underpricing to better understand their use as channels for rent extraction. The mean of these distributions reveals the fraction of deal value that is typically transferred from issuer to third parties, while the variance gives us an indication of the differences in value extraction across IPOs. Perhaps, the most striking observation here is that while the units of measurement are comparable for the two measures (both are reported as fractions of the offering size), IPO underpricing varies within a significantly wider range than gross spread. Across the entire sample, the standard deviation of underpricing is 55.44%, in contrast to 1.64% for gross spread. Additionally, average underpricing (26.30%) is also much higher than average gross spread (6.10%). This suggests that underpricing accounts for most of the variation in the value transferred from issuers to investors and IBs during IPOs. Although first trading day returns vary widely, IPOs are typically underpriced (for 74.1% of IPOs) rather than overpriced. This implies that underpricing of IPOs is intentionally engineered by underwriters, rather than a random outcome associated with trading in secondary markets.

The distributions of both market shares and network centralities indicate that a small number of the largest and most connected IBs dominate IPO underwriting markets. The five banks with the highest market share in 2017 – Morgan Stanley (6.76%), JPMorgan (6.09%), Citi (5.25%), Goldman Sachs (4.64%) and Credit Suisse (3.80%) also dominate investment banking networks and are connected to 76.5% (Morgan Stanley), 75.6% (JPMorgan), 68.0% (Citi), 72.5% (Goldman Sachs) and 75.8% (Credit Suisse) of IBs. We now proceed to review our hypotheses in the light of evidence obtained from the econometric analysis.

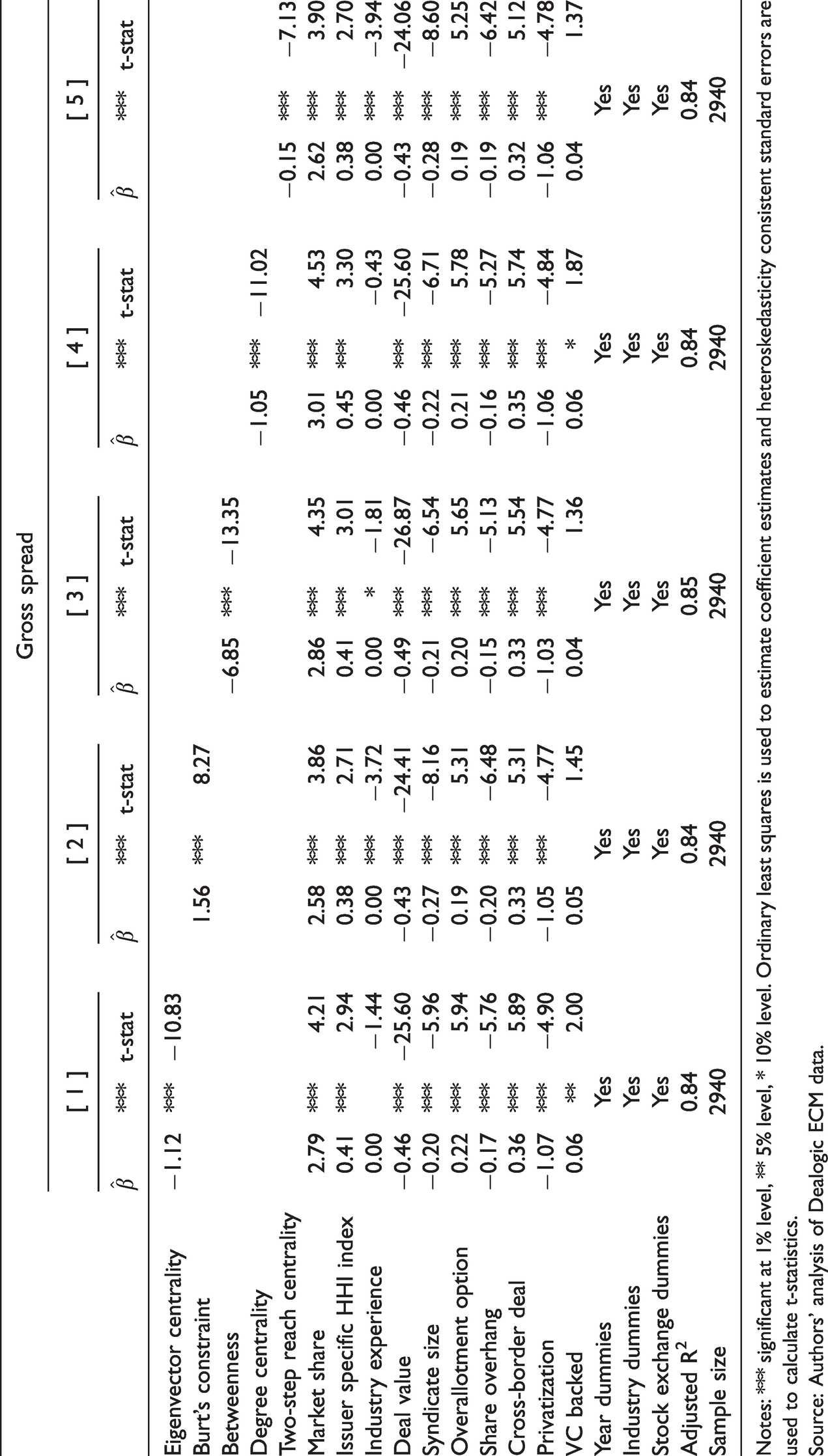

Underwriters with larger market share in the IPO underwriting market charge higher direct fees, an estimated premium of 0.11 to 0.12 percentage points for a 10% increase in underwriter’s market share (Table 2). To illustrate this premium in monetary terms, we multiply the average IPO size in our sample ($217 m) by our estimated percentage changes. This yields a premium of $239k–$260k in gross spread for an average IPO. Similarly, issuers facing a more concentrated market for underwriting services pay an estimated premium of 0.02 percentage point ($44k for an average IPO) for every 10% increase in HHI. Our estimates of the effect of industry experience have a somewhat counterintuitive negative sign, although the magnitude of the estimated coefficient suggests an effective zero effect on gross spread. Taken together, although we find some evidence of statistically significant relationships between market power of underwriters and gross spread, the economic significance of these relationships appears modest.

Gross spread channel of rent extraction.

Notes: *** significant at 1% level, ** 5% level, * 10% level. Ordinary least squares is used to estimate coefficient estimates and heteroskedasticity consistent standard errors are used to calculate t-statistics.

Source: Authors' analysis of Dealogic ECM data.

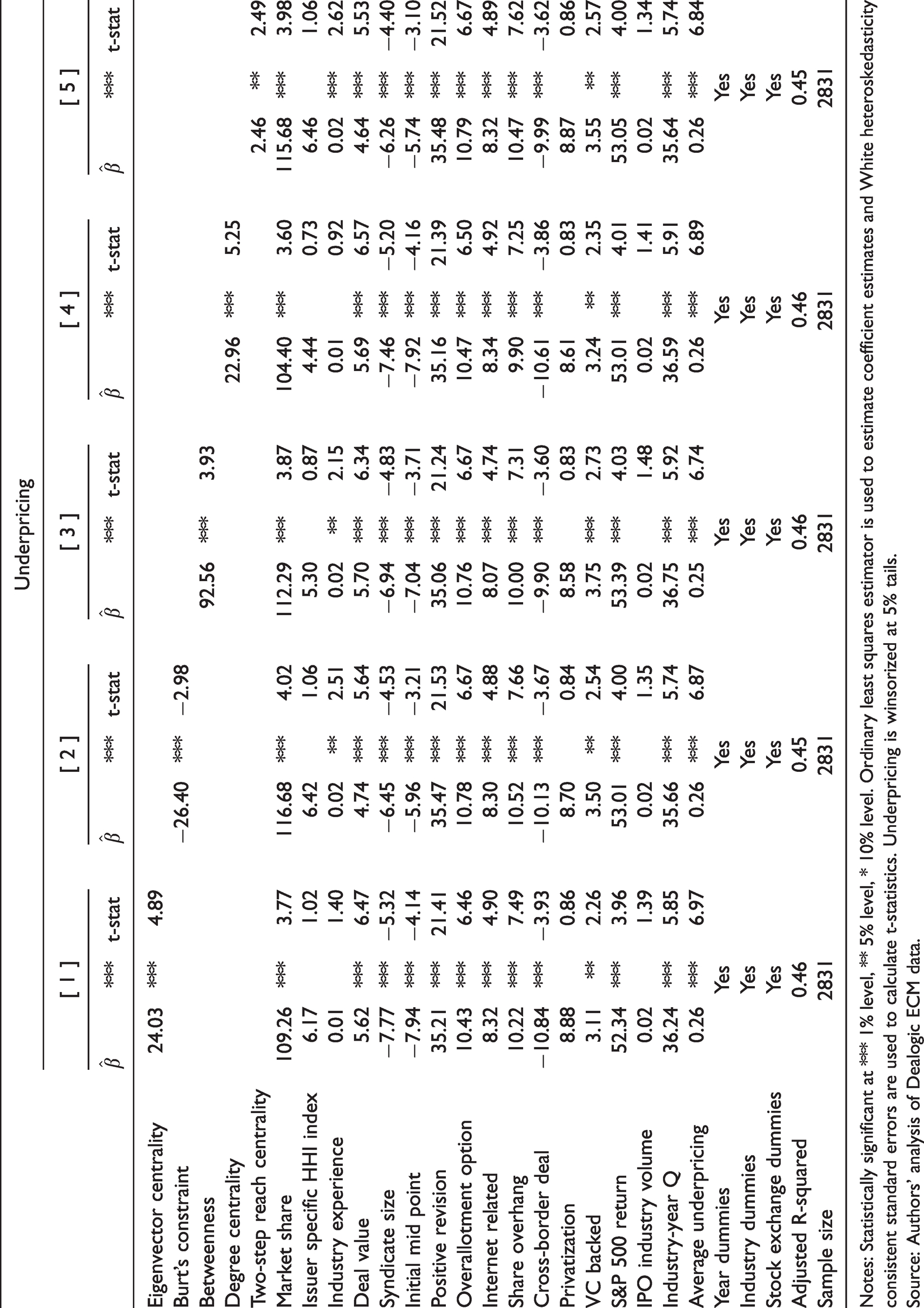

For a 10% increase in underwriter’s market share, IPO underpricing increases by 4.3 to 4.8 percentage points on average ($9.3 m–$10.4 m for an average IPO; Table 3). Coefficient estimates on the industry experience variable corroborate the above result and imply that underwriters with more industry experience underprice more, ceteris paribus, a result consistent with hypothesis H.1b. The magnitude of these estimates suggests that for additional 10 IPOs underwritten in the same Fama-French (1997) industry, 5 an IPO is expected to be underpriced by additional 0.2 percentage points ($434k for an average IPO). Our alternative specification of market power – issuer-specific HHI – also yields consistently positive estimates, although the precision of these estimates is too low to establish statistical significance.

Underpricing channel of rent extraction.

Notes: Statistically significant at *** 1% level, ** 5% level, * 10% level. Ordinary least squares estimator is used to estimate coefficient estimates and White heteroskedasticity consistent standard errors are used to calculate t-statistics. Underpricing is winsorized at 5% tails.

Source: Authors' analysis of Dealogic ECM data.

We estimate that for a 10% increase in the number of ties formed by underwriters in the three years preceding an IPO (degree centrality), they would charge on average 0.04 percentage points lower gross spread ($87k for an average IPO). This pattern is broadly repeated across our results on eigenvector centrality (0.05 percentage points decrease in gross spread per 10% increase in eigenvector centrality), two-step reach centrality (0.01) and betweenness (0.28). Our coefficient estimate on Burt’s (2004) network constraint has a positive sign, in contrast to the negative coefficient estimates on all other network centrality variables. This is not a contradiction, however, given that Burt’s (2004) network constraint decreases, as underwriters either form more ties or the redundancy of ties among their syndication partners decreases – implying that a said underwriter has improved its position as a broker connecting others. Consequently, an opposite sign is expected from a coefficient estimate on network constraint in comparison to the remainder of our network centrality variables. The coefficient estimate on network constraint implies that a 10% reduction in network constraint leads to a 0.07 percentage point decrease in gross spread ($152k for an average IPO). It therefore appears that, if anything, well-connected underwriters charge on average lower gross spread as a competitive advantage to secure new business rather than to extract rents from issuers. This contradicts our hypothesis, but to fully appreciate these results, we need to consider them in conjunction with those linking network centrality to underpricing.

The coefficient estimate on degree centrality implies that for a 10% increase in the number of unique network ties of an underwriter, underpricing increases on average by 0.95 percentage points ($2.1m for an average IPO; Table 3). The coefficient estimate on two-step reach centrality implies a much smaller economic effect of network centrality, a mere 0.10 percentage points ($217k for an average IPO) increase in underpricing for a 10% increase in two-step reach centrality. In our view, this points to the lesser importance of indirect ties. The coefficient estimate on eigenvector centrality translates into a 0.99 percentage point ($2.1m) increase in underpricing for a 10% increase in underwriter’s eigenvector centrality. Our results on Burt’s (2004) network constraint and betweenness however underline the role of the wider network structure. Burt’s (2004) network constraint is estimated to increase underpricing by 1.21 percentage points ($2.6m) for a 10% reduction in network constraint, implying lower redundancy in underwriter’s subnetworks and a larger number of direct ties. This result suggests that underwriters who benefit from being in a position of connecting many otherwise disconnected actors in their networks underprice more. This is corroborated by our results on betweenness, a simpler measure of brokerage opportunities, which suggests a 3.83 percentage point ($8.3m) increase in underpricing for a 10% increase in network centrality.

Discussion

How to interpret these statistical relationships between market power, network centrality, gross spread and IPO underpricing? Finance theory suggests that pricing of IPOs is proportional to the information asymmetries between issuers and investors, while IBs charge fees commensurate with the risks and costs that they assume (Beatty and Ritter, 1986; Booth and Smith, 1986). IBs charge a percentage fee derived from the value of the underwritten securities, termed gross spread, intended to cover the underwriters’ costs, compensate for the risks of the offering, and allow underwriters to earn profit. Gross spread is agreed in advance of the offering along with the price for which the underwriter sells securities to investors. The issuer receives the price that investors pay for securities, reduced by the value of the gross spread, which is kept by underwriters. Additionally, finance theory explains that underwriters typically aim to set the offering price below the expected market value to incentivize investors to buy securities in IPOs, compensate them for the risk of buying securities for which a market price has not yet been established, and to minimize the chance of shareholder lawsuits following the offering (Liu and Ritter, 2011). The persistent effort of underwriters to underprice IPOs below their expected market value is then again a reflection of the inherent risk in the offering. In sum, from the perspective of financial economics, both gross spread and IPO underpricing play an important role in pricing IPOs and serve as mechanisms of pricing risk associated with IPOs, as well as compensating underwriters and investors (Abrahamson et al., 2011; Bajo et al., 2016).

However, from a political-economy perspective, the observable characteristics of IPOs related to risks, costs and market environment offer only a partial explanation for the fees charged. This observation lends credence to a view that factors in a rent component into the income stream mix of IBs, or, in the terminology of Lazonick and Mazzucato (2013) that IBs are in the position to extract value for themselves and their clients. The results indeed show that IBs with higher market power and stronger network ties with institutional investors charge fees beyond what could be justified by the observable characteristics of the IPOs they underwrite.

Analysing the degree to which gross spreads and underpricing augment excess profits, we observe that the former is marginal as direct price competition between IBs is close to irrelevant. Gross spreads, which represent a cost/risk covering fee, show little variance and are highly clustered at country level. However, when we turn to IPO underpricing, the picture changes completely. The more powerful and better connected IBs on average underprice IPOs more and pocket indirect fees through kickbacks of trading revenue and equity research fees earned from institutional investors. The marginal losses on their gross spreads are compensated manifold by the extra fees gained through such kickbacks. This key finding underlines the relational character of IB networks, suggesting that much of the turnover depends on the exploitation of established relations with issuers, institutional investors and partner IBs.

What emerges from the above is the picture of a close-knit network of central IBs performing a crucial intermediary function in investment chains. In fact, within the larger population of IBs, a subset of powerful and globally connected IBs manages to systematically charge excess fees that cannot be explained by the characteristics of IPOs they underwrite. While a further dissection of the nature of these rents falls beyond the scope of this paper, we find statistically robust evidence that market concentration and industry consolidation enable IBs to extract higher fees compared to less powerful and less connected competitors. Both instances of structural power are instrumental for the business model of leading IBs and both limit competition in practice to the extent that the functioning of market dynamics is stymied (Crouch, 2011), in turn enabling rent extraction through corespective behaviour (Crotty, 2008).

The outcomes are telling. Regarding industry consolidation, the top five IBs in the US have increased their asset share from 50% to over 65% over the 2001–2007 period (Crotty, 2008), while top 10 banks control 68%, 56% and 50% of assets, loans and deposits, respectively (Christophers, 2018). In the European Union, consolidation is evident with the top five largest credit institutions seeing asset shares increasing from around 42–46% in the 2005–2015 period (European Central Bank, 2017: 30). Oligopolistic market concentration, in turn, supports the too-big-to-fail status of the intermediaries concerned and their potential to extract rents from the wider economy (Christophers, 2018). This is exactly what Wójcik et al. (2018b) find: in 2015, the top 10 banks had a 50% share in IB fees across four core service categories. 6 6 A salient feature of investment banking more widely is its spatial concentration in the apex nodes of the world city network (Wójcik et al., 2018a). The top 10 world cities provide 80% of the investment banking business (Wójcik et al., 2019). The geographies of investment banking, in other words, show a continued propensity for relational proximity of a limited number of powerful and well-connected actors, on which the periphery of the financial system is dependent (Van Meeteren and Bassens, 2016, 2018).

Conclusions

While piecemeal evidence for the rent-extracting character of IBs was in place (Christophers, 2018; Crotty, 2008), large swaths of this terrain have remained uncharted. To start broaching the thorny question of rent, this paper has provided empirical evidence that rent is accruing in IBs. We have empirically investigated two main channels through which IBs could potentially extract rent, namely gross spread and IPO underpricing, and examined their modus operandi. First, underwriters might charge higher gross spread than would be justified by the characteristics and risks of IPOs they underwrite. Second, they can underprice issuers’ securities excessively and thus reduce the amount of money received by the issuer in proportion to the market value of the securities issued. Investors can also be a target of rent extraction by underwriters when the allocation of underpriced securities in IPOs becomes conditional on the fee income that institutional investors generate for the underwriter prior to the offering. Consequently, powerful underwriters can leverage their strategic position of intermediaries between issuers and investors to extract rents from both sides of the market.

Our findings are subject to several limitations. First, we restrict ourselves to rent extraction in the underwriting of bookbuilding IPOs as our empirical context. Although we indicate how IB activity is reliant on services provided by the wider APS-complex, we cannot probe the share of the class-monopoly rent appropriated by other actors, such as accounting and law firms. This is in part due to the limitations of the data on IPO pricing available to us, which we source from the Dealogic ECM database. Second, our study covers a limited geographical area – USA, Canada and Europe – and is restricted to the 1998–2017 period. Third, although our reasoning and conceptualization of rent extraction through the underpricing channel relies on the existence of revenue kickbacks from institutional investors, we refer to published studies to corroborate this mechanism (Nimalendran et al., 2007; Reuter, 2006). Finally, rent extraction in the proposed form relies on the discretion of underwriters over the allocation of IPO securities to institutional investors, a phenomenon specific to bookbuilding IPOs. These limitations, however, do not undermine the wider significance of our results, given that bookbuilding IPOs are the dominant form of going public, constituting 64.5% of all IPOs for our sample period and countries studied. With these limitations in mind, we would like future research to consider rent extraction across different contexts and sub-sectors of the APS complex as well as across a more diverse group of countries and alternative time periods. It would also be invaluable, if alternative analytical methods for studying rent extraction are developed, to support future empirical research.

Despite these caveats, and considering that IBs act as an ‘indicator species’ (Rossi et al., 2007: 630) within the APS complex as a whole, our findings substantiate the argument that the APS complex functions as an obligatory passage point enabling rent extraction from the wider economy. As such, we also find support for the augmented world city hypothesis, which claims that APS are obligatory passage points for accumulation in times of financialized globalization (Bassens and Van Meeteren, 2015). Given that IBs serve as anchoring organizations in the APS complex, it follows that capabilities to extract rents also apply to cognate APS. Either directly as remuneration of legal, accountancy and consulting firms in the underwriting process or indirectly, as dominance in underwriting will carry over into other business supported by the wider APS complex. Such an assumption chimes with what Taylor (2000) calls a propensity of APS more widely to mine monopolies of regionalization: ‘In services such as finance, accountancy and corporate law, practitioners are not just servicing “global capital,” they are creating new products based upon their unique knowledge collectivities. In other words, they do not aim to operate in a price-setting market, but rather develop multiple monopolies of quality knowledge products to reap appropriately large profits’ (Taylor, 2000: 10). Given the long path dependent trajectory in which IBs and the necessary metropolitan endowments that facilitate IBs emerge (Wójcik et al., 2018a), the micro-level practices of rent extraction hinge on place-based and networked externalities currently available to the few. As too-big-to-fail banks remain in place, such micro-practices, despite changes in the hierarchies of financial institutions and centres, are likely to reproduce the very role of world cities as obligatory passage points for financialized globalization.

Footnotes

Acknowledgements

The article reflects only the authors’ views and the ERC or any of the above funding bodies are not responsible for any use that may be made of the information it contains.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project has received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement No. 681337), the Brussels Capital Region through the Innoviris Anticipate programme (grant agreement No. BRGEOZ289), and by the Research Foundation – Flanders (FWO) (grant agreement No., G019116N). Dariusz Wójcik has also received funding for this project from the Australian Research Council's Discovery Projects funding scheme (project DP160103855). Michiel van Meeteren would like to acknowledge funding from the UK's Economic and Social Research Council (ESRC): Innovating Next Generation Services Through Collaborative Design (Project ES/S010475/1).