Abstract

The comparative capitalism literature examined how institutions vary on a national or societal level and how these differences affect multinational companies’ strategies. Yet, little attention has been devoted to cross-national or regional differences in the governance of competition, especially in the context of digitalization of markets. The article seeks to fill this gap by looking at the case of Google. It traces the process of the stark US–EU disagreement over Google’s abuse of dominant position in digital markets, which resulted in one of the largest fines in the EU history. It is argued that the variation in the response to the company’s market and nonmarket strategies are traced back to differences between Ordoliberal and Chicago School ideas, which are embedded in the ‘competition regimes’ of European and US capitalist models. The article concludes by discussing the implications of these findings for varieties of capitalism frameworks.

Introduction

A large body of comparative literature examined how institutions vary on a national level and how these affect multinational companies’ strategies (Hall and Soskice, 2001; Jackson and Deeg, 2008; McCann, 2013). This line of inquiry suggested that the multinationals’ ability to navigate institutional complexity is key to their success or failure; and their decisions on how to respond to institutional differences are very much strategic ones (Ahmadjian, 2016). Recent studies examining the institutional systems across countries found that there is little evidence of convergence in national business systems and models of capitalism (Fainshmidt et al., 2018; Hotho, 2014; Witt et al., 2018). Extant literature has focused on different institutional spheres, for instance, corporate governance, employment relations/HRM and vocational training (Aguilera et al., 2008; Edwards et al., 2016; Fortwengel et al., 2019; Lange et al., 2015). However, less attention has been accorded to the differences in the domain of competition regimes, and their interplay with company strategies.

The purpose of this article is to first identify whether there was convergence or divergence in the governance of competition in digital markets between the US and the EU, by examining the case of Google. In the context of closer coordination between Competition Authorities, the most likely outcome was that their responses to Google would converge. Yet, the outcome of the investigations led to outright divergence. We seek to explain this empirical puzzle and we consider two alternative explanations. The first explanation is centred on the underlying ideational and philosophical differences of the EU and US competition regimes. The second explanation is based on protecting different ‘material’ interests and the political objectives that might underpin a US–EU rivalry. The case study is reconstructed through the process tracing of the events and the analysis of data from primary sources and expert interviews. The article argues that the divergent outcome in the case of Google is in large part explained by the Ordoliberal and Chicago principles that underpin the EU and US competition regimes, respectively.

The rest of the article is structured as follows. ‘The US and European competition regimes: Convergence or divergence?’ section outlines the gap in the literature and develops the analytical framework of this article by reconstructing the main tenets of the US and EU ‘competition regimes’. Next, we consider two competing theses as regards their co-evolution: regulatory convergence and transatlantic divergence, and propose to examine two alternative explanations for the prospect of divergence. The ‘Research design’ section articulates the research design of the article, justifies why Google was a most-likely case for convergence, and explains the sources and methods of analysis. ‘The governance of competition in digital markets: The case of Google’ section presents the case study of Google’s strategies in digital markets, and the response of the US and EU Authorities. Our analytical framework highlights the interplay between the ideas that underpin the different competition regimes, the multinational’s market and nonmarket strategies, and how key agencies responded. The ‘Discussion and conclusion’ section discusses the plausibility of the different explanations and concludes outlining the contribution to the literature.

The US and European competition regimes: Convergence or divergence?

The competition regime: The nonmarket environment of multinationals

The governance of competition, especially in the context of digitalization of markets, is a significant future area of research for international and comparative management research. National and supranational regulation of competition exacerbates the ‘institutional complexity’ (Ahmadjian, 2016) that firms need to navigate, resulting in failures of compliance, penalties and fines, or strategic failures (e.g. blocked mergers). Earlier literature broadly assumed that in the area of competition, there was a trend of ‘regulatory convergence’ and was dubbed as the ‘Americanization’ of competition in Europe (Djelic, 2002) suggesting that complexity was rather limited. By contrast, the differences between US and the European regimes have resurfaced in recent years, especially as the EU’s regulatory hand was strengthened since the completion of the Single Market in 1992, and put many multinationals in challenging positions. Prominent examples in the past include cases such as General Electric, Microsoft and Boeing (McGuire and Smith, 2008: 125–138), and more recently we have observed investigations of Amazon, Apple and Facebook.

Although the international business literature tends to consider firm-state interactions as part of corporate political activity and nonmarket strategies (Lawton et al., 2013: see), so far it has paid little attention to the domain of ‘competition regimes’. A ‘market strategy’ is traditionally defined as ‘a set of market actions, such as pricing, quality improvements, or product differentiation’, whereas, nonmarket strategies are focused on ‘building coalitions, lobbying legislators or regulators, making campaign contributions, and providing information to affect institutions that might defend or create revenues’ (Doh et al., 2012: 23). Since the interactions between multinationals and Competition Authorities fall within the broad domain of nonmarket strategies, our article further explores the interplay between nonmarket strategies and the regulatory environment set out in competition law.

Existing variations in antitrust regulations have the potential to increase uncertainty and complexity. Yet, we know surprisingly little about ‘competition regimes’ as institutional constraints in different capitalist models and the responses of business to the demands of competition policy (Rollings and Warlouzet, 2020). The latter question becomes even more pertinent in light of the unprecedented wave of technological change that enables the development of new ‘disruptive’ business models and facilitates the construction of new ‘digital’ markets.

The competition regime: An institutional sphere of capitalism

Hall and Soskice (2001: 32) highlighted how the competition regime is an important part of any capitalist model as one of the main components of their ‘diamond model’. This was mainly discussed as part of the inter-firm relations institutional sphere. Yet, their approach did not elaborate further on the ideational differences between competition regimes, and remained fixated on specific outcomes, such as the collaboration in pre-competitive activities (training, innovation/R&D) within coordinated market economies (CMEs), contrasted with the arm’s length relationships in liberal market economies (LMEs).

The comparative capitalism literature has progressed substantially since Hall and Soskice’s contribution (see reviews by Jackson and Deeg, 2008; Morgan and Kristensen, 2014; Wood and Allen, 2020; Kornelakis, 2018). More recent work has expanded the ‘universe of cases’ looking at a wider set of countries and business systems, beyond the standard Organisation for Economic Co-operation and Development (OECD) member-states (Fainshmidt et al., 2018; Hotho, 2014; Witt et al., 2018). However, these approaches were focused on updating the taxonomy of countries, without problematizing the interplay of institutions with multinationals’ strategies. Finally, a stream of studies examined cases of multinationals’ strategies and their interplay with regulatory institutions within the comparative capitalism framework (Benassi et al., 2016; Grimshaw and Miozzo, 2006; Lange et al., 2015; Leaver and Montalban, 2010; Kornelakis, 2015). However, their focus was on other institutional domains (e.g. employment relations), and work examining explicitly ‘competition regimes’ remained underdeveloped.

This is an important gap, since the competition regime provides the regulatory context on which both market (e.g. product market strategy) and nonmarket strategies (e.g. lobbying regulators, compliance) need to be developed (Doh et al., 2012). The competition regime defines the market strategy and constrains the positioning of the firm in relation to competitors. It influences the ‘business model’ of a firm, which in turn enables – or constrains – different ranges of options for interaction and integration of ‘exchanging partners’ including interactions with the state and government agencies (Lange et al., 2015). The key government agencies that are relevant in our investigation are the US and EU Competition Authorities. Their role is central to the well-functioning of markets, since competition was described as ‘the most important organizing principle in the capitalist world’ (Wigger and Nölke, 2007: 488). However, competition regulation relies on particular economic and legal assumptions or ‘philosophies’ (Doh et al., 2012). The next sections articulate the archetypes of the US and the EU competition regimes.

The origins of the US competition regime: From Harvard School to Chicago School

The US competition regime, set up by the 1890 Sherman Antitrust Act, initially sought to respond to public disquiet over the anticompetitive activities of large firms in the oil, steel and finance industry (McGuire and Smith, 2008). Initially, the regime was largely influenced by the Harvard School, which suggested that highly concentrated markets foreshadowed poor economic performance (Jones and Sufrin, 2016). The focus on the number and size of firms in the market led to the development of the famous ‘SCP paradigm’ in industrial organization (Kovacic and Shapiro, 2000: 52) predicting that market structure dictates firms’ conduct which then impacts economic performance. The Harvard School’s principles translated into an interventionist antitrust policy targeting trade barriers and monopolization (Cini and McGowan, 2009) through rules of per se illegality (Montalban et al., 2011). The US approach to competition at the time was thus influenced by a mix of political, social and economic goals aimed at limiting corporate power, promoting the values of individualism, fairness and free-enterprise (Cini and McGowan, 2009).

However, since the early 1970s, proponents of the Chicago School harshly criticized this approach and proposed that structure can be affected by performance or conduct as monopolies may result from superior efficiency or anticompetitive behaviour may attract new entrants (Kovacic and Shapiro, 2000). The Chicago School proponents suggested that since market participants are rational and markets self-correcting, government intervention through competition policy should be minimal (Jones and Sufrin, 2016). They further argued that the exclusive goal of antitrust laws should be the pursuit of economic efficiency to maximize consumer welfare rather than the protection of small competitors (Schweitzer, 2007). This faith in market mechanisms induces a fear of ‘type-1-errors’ (over-enforcement), which can reduce consumer welfare by prohibiting efficient behaviour.

The Chicago School also placed great importance to sophisticated economic analysis in the application of competition law (Cini and McGowan, 2009) and notably the neoclassical price theory (Wigger and Nölke, 2007) in assessing the effects of a conduct on consumer welfare. As a result, these principles influenced US competition authorities and completely transformed antitrust interpretation by the 1980s, tolerating monopoly power much more than in previous decades.

The origins of the EU competition regime: The Freiburg School and Germanic Ordoliberalism

There is a broad consensus among scholars that the EU competition regime is essentially based on the Germanic Ordoliberal principles (Bartalevich, 2016; Nölke, 2011; Siems and Schnyder, 2014; Talbot, 2016; Wigger and Nölke, 2007). For instance, Nölke (2011: 14) emphasizes that ‘the overall influence of German ordoliberal scholars […] continued to have a remarkable stronghold in EU competition policy for several decades’. The 1957 Treaty of Rome granted central importance to competition policy as it was strongly believed that rules were needed to ensure that trade barriers removed between member-states (for the purpose of market integration) would not be replaced by private barriers erected by anticompetitive business conduct (Aydin and Thomas, 2012).

Ordoliberalism evolved from the ideas of the Freiburg School of Economics (Bonefeld, 2012; Gerber, 1994). At the soul of Ordoliberalism is the idea of ‘Ordnungspolitik’ (Gerber, 1994: 45; McCann, 2013: 154) according to which the legal system shall be configured so as to create and maintain the ‘political and economic order’. In the case of competition, it suggested that the conditions of complete competition should be maintained by the legal system to allow the economic system to function most effectively (Gerber, 1994). Indeed, Ordoliberalism fundamentally did not rely on the self-regulation of markets, but rather considered them as prone to failures (Wigger and Nölke, 2007). Ordoliberalism thus advocated for regulatory intervention to avoid monopolized and cartelized markets (Monti, 2007). In effect, competition was regarded as the exercise of individual economic liberties legally sheltered from undue economic power (Jones and Sufrin, 2016). The emphasis on economic freedom implies the protection of competition as a valuable institution in itself.

Interestingly, historical research suggests that the German and US competition regimes were more similar in the past, before diverging again. The US has helped substantially in the writing of competition rules in Germany in the post-war period of reconstruction (Djelic, 2002; Sorge, 2005: 132–133). However, at the time, the US Harvard School approach was much more compatible with the Ordoliberal paradigm. In turn, the distinctiveness between the Germanic Ordoliberal and US Chicago School regime became clearer over time.

Germanic Ordoliberalism ideas did not only increasingly ban cartels and syndicates, but also aimed for a de-concentration of the industry. By contrast, for the US Chicago School, ‘big business’ was frequently accepted as a legitimate form of economic organization, in line with suggestions that private monopoly power was merely a transitory phenomenon, which will ultimately be eroded by market forces (Siems and Schnyder, 2014). As van Horn (2009: 229) suggests for the Chicago School ‘victories that allowed a large corporation to dominate the market would invariably be pyrrhic victories […] portrayed as basically short-lived price discrimination, ephemeral to the operation of the market’.

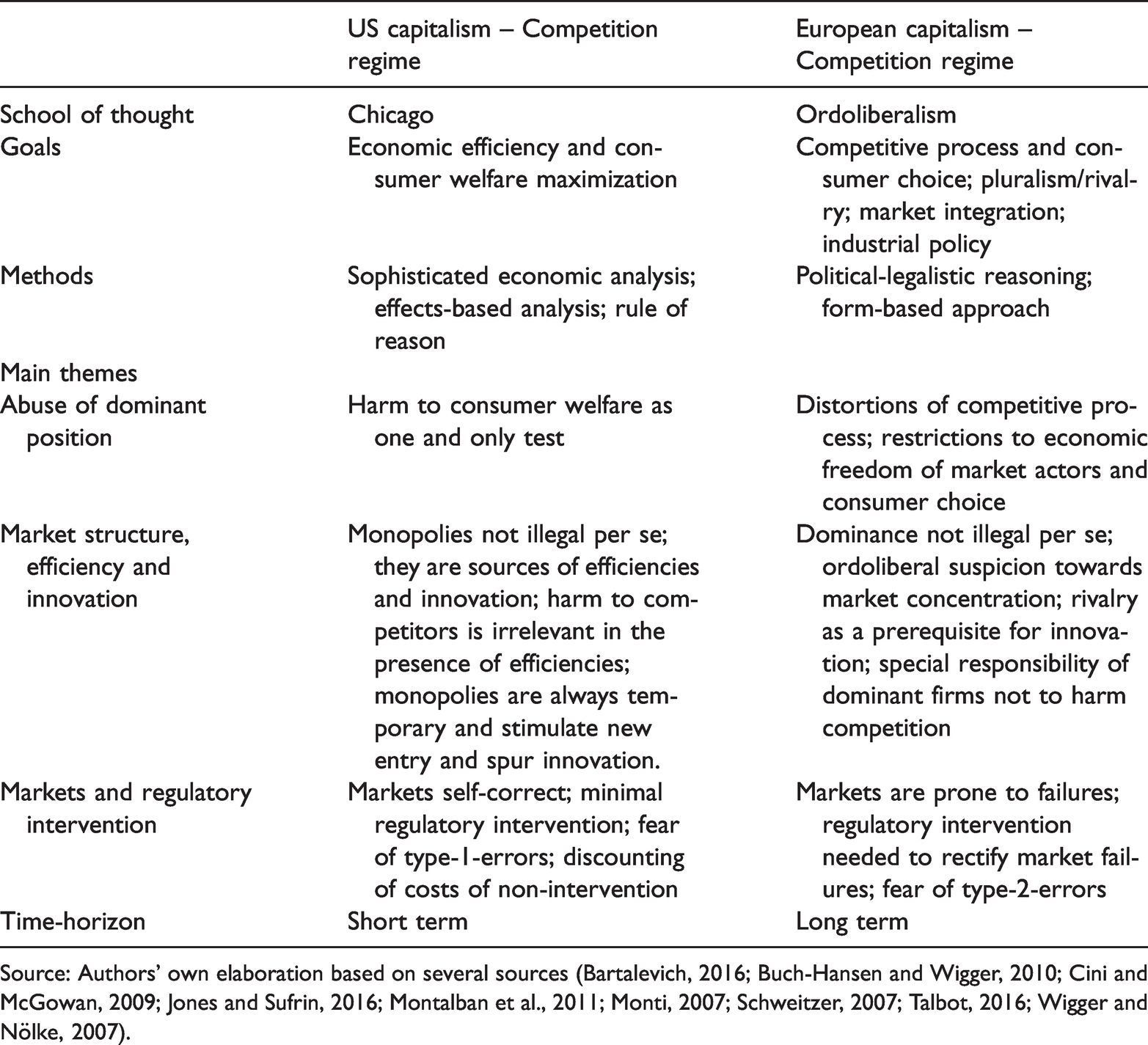

For Ordoliberalism, the goal of the law is to protect the process of competition, where the focus is not on outcome but on structure and conduct (Jones and Sufrin, 2016). Economic efficiency and consumer welfare are therefore only by-products of policy enforcement (Montalban et al., 2011; Talbot, 2016) deriving from economic freedom and the ideal composition of the market by many equal players (Montalban et al., 2011; Monti, 2007). Under an Ordoliberal approach, competition constitutes an end in itself, not a means to achieve economic efficiency (Monti, 2007), and competitors are not protected for their own sake but for the proper functioning of the competitive process. Overall, the lack of trust in the market mechanism and the practical need to protect competition in the Single Market, translated in active intervention (Monti, 2007; Talbot, 2016; Wigger and Nölke, 2007), thus, favouring over-enforcement to under-enforcement i.e. ‘type-2-error’. The loss of potential efficiencies therefore prevails over risking harming the competitive structure ‘forever’ and losing the long-term source of competition (Monti, 2007). Table 1 summarizes the main differences between the US and EU competition regimes.

Summary of US and European competition regimes.

Source: Authors’ own elaboration based on several sources (Bartalevich, 2016; Buch-Hansen and Wigger, 2010; Cini and McGowan, 2009; Jones and Sufrin, 2016; Montalban et al., 2011; Monti, 2007; Schweitzer, 2007; Talbot, 2016; Wigger and Nölke, 2007).

Regulatory convergence or transatlantic divergence?

One plausible hypothesis on the evolution of the US and the EU competition regimes can be termed as the regulatory convergence thesis. According to this perspective, competition has been a central policy area where convergence with the EU can be observed. According to some scholars, this regulatory convergence is manifested through the EU competition regime steadily becoming more similar to the Chicago neoliberal paradigm (Bartalevich, 2016; Buch-Hansen and Wigger, 2010; Wigger and Nölke, 2007). Historically, this can be traced to the process of ‘soft convergence’, when US experts collaborated with Europeans in the drafting of abuse of market power clauses in the European Coal and Steel Community (Djelic, 2002). The process has been facilitated in the context of international organizations such as the OECD, with their antitrust recommendations to its member-states. This perspective has been strengthened as a result of the General Electric-Honeywell case of regulatory conflict (Morgan and McGuire, 2004) which led to what scholars identified as a ‘paradigmatic transformation’ (Aydin and Thomas, 2012), whereby the traditional EU approach made way to ‘modern’ economic thinking in line with Chicago School principles (Buch-Hansen and Wigger, 2010).

A competing hypothesis on the evolution of the US and EU competition regimes can be summarized as the ‘transatlantic divergence’ thesis. The latter suggests that there are persisting differences between the US and the EU approaches to competition. We propose two main explanations for transatlantic divergence. The first one is centred on ideas. Doh et al. (2012: 27) suggested that the discrepancies are rooted in the ‘different underlying philosophy’ and ‘fundamentally different approaches to enforcing completion rules’ between the EU and the US. These differences have ‘stood the test of time’ in antitrust law (McGuire and Smith, 2008: 132). McGuire and Smith concluded that ‘full substantive convergence between the partners seems unlikely given the different policy trajectories followed by Europe and America’ (2008: 138).

An alternative explanation to the transatlantic divergence is centred on ‘interests’. It points to the possibility that the divergent outcomes are the result of an underlying rivalry between the US and Europe. In other words, the regulators’ decisions implicitly or explicitly protect their home companies’ interests. This is consistent with the argument of ‘regulatory capture’ (Morgan and McGuire, 2004). The EU may be blocking US companies’ strategies to serve its interests in favour of its own ‘national champions’ and vice-versa the US might be more aggressive towards European companies. These arguments will be examined against the case of Google. The next section articulates the research design of the article.

Research design

We apply a most-likely case study research design (George and Bennett, 2005) to examine analytically the diverging EU–US responses to Google’s market and nonmarket strategies. The dynamics of ‘a most-likely case’ suggest that certain conditions pre-dispose the case towards a particular outcome. First, the literature suggests that the European Commission (EC) has embraced the tools, methods and principles of the Chicago economic analysis that the Federal Trade Commission (FTC) has been applying since the 1980s (Bartalevich, 2016; Buch-Hansen and Wigger, 2010; Wigger and Nölke, 2007). Since both EU and US Authorities are using the same methods of analysis, they are most likely to reach the same decisions. Second, there are precedents of prominent US-technology firms, which had trouble with the US and EU Competition Authorities. For instance, Microsoft encountered antitrust charges in the ‘browser wars’ (with Netscape) and the Windows media player as a case of ‘bundling’ (see Daskalova, 2015). This suggests that there must be a ‘learning process’, and US technology firms should be able to appreciate differences in competition regimes. Additionally, large multinationals like Google have both the interest and the ‘resources’ to adjust their nonmarket strategies accordingly; for instance, hiring legal firms with substantial expertise to understand what needs to be done to comply with requirements of different competition regimes. Again Google appears as the most likely case to navigate the institutional complexity and reach favourable outcomes in both sides of the Atlantic. Nevertheless, the outcome of the investigations in the two sides of the Atlantic was diametrically opposed. This casts doubt to the conjectures suggesting there has been regulatory convergence. We then attempt to explain the divergence by considering two alternative explanations based on ideas and interests.

The research setting concerns two digital markets, primarily the market for price comparison websites (PCW), and the market for general search engine (GSE) services. This setting is chosen because it reflects the context of construction of new markets through digitalization; a ‘new economy’ sectoral context (McGuire and Smith, 2008: 124) that provides opportunities for entry through disruptive business models. The new business models based on instant scalability create new digital market channels, and therefore, little is known about how regulators approach these new markets. This industry is globalized, and companies from different countries are ‘born global’ and face similar entry barriers because of Google’s dominance. Furthermore, Google’s case is selected because it triggered a formal investigation by Competition Authorities on both sides of the Atlantic and is therefore conducive to a comparative analysis of their responses. Our case selection follows methodological literature which suggests that the most relevant cases are those representing ‘extreme situations’ or ‘polar types’ (Eisenhardt, 1989; Yin, 2014). The case attracted considerable media attention and earned Margrethe Vestager, the EU Commissioner for Competition, the nickname of ‘Europe’s antitrust cop’ (White and Bergen, 2017). It also portrays a stark contrast between the European 7-year investigation resulting in a decision imposing the biggest fine to that date for an abuse of dominance, and the American 19-months investigation resulting in a ‘no-case’ decision.

The data collection was based on multiple sources for triangulation purposes. We relied on three groups of sources: (1) the Google Shopping final decisions published by the EC and the FTC; as well as 42 official documents, positions, and press releases from the European Parliament, the EC, and the FTC; (2) 35 media/newspaper articles from reputable sources (e.g. Bloomberg, Economist) to enhance the validity of the data; (3) Google’s and its competitors’ perspectives in the investigation, through an online search of 17 blog articles; and (4) 5 semi-structured expert interviews to enhance the validity and credibility of our inferences and interpretation. The number of interviews is justified because further interviews were not possible, since potential interviewees were or are still involved in litigation, and are bound by non-disclosure agreements and therefore the access to them is completely blocked. Nevertheless, our interviewees are ‘expert informants’ holding deep knowledge of this or other similar competition cases who thus gave us a holistic overview of the key issues at stake. The interviews’ duration was on average 1 h. The interviews took place in the period between June and July 2018. The interview instrument was a semi-structured questionnaire with key themes and open questions. All the interviews were transcribed verbatim.

Our data analysis follows loosely Hall’s (2006: 28) ‘systematic process analysis’ model with the aim to build a narrative that traces the process of strategic interactions between the key actors including details about ‘the sequence of those events, the specific actions taken by various types of actors, public and private statements by those actors about why they took those actions’. To utilize this approach, we content-analysed the data comprising the primary policy documents, interview transcripts, blogs and newspaper articles, which were read and re-read so as to establish patterns and finding traces of evidence in relation to the key themes that emerged from the literature. There were several iterations back and forth between the literature and our data to fine-tune the common themes that emerged from the first iteration. Our analysis was thus organized thematically; the themes emerged from the theoretical review to feed into the interview transcripts. After the collection of the data, and the content analysis, the themes were revised and finalized into the following four items: abuse of dominant position; market structure, efficiency and innovation; markets and regulatory intervention; and time-horizon.

The governance of competition in digital markets: The case of Google

Google’s strategy in digital markets

Google is an American multinational technology company founded in 1998 and specialized in Internet-related services and products. Following a corporate restructuring in October 2015, Alphabet Inc. became the parent company of Google, and also the holding company for several former subsidiaries. Google’s main business offering is a general web search engine (‘GSE’). Using a ‘scoring approach’ based on the quality and quantity of links to a webpage, its so-called PageRank algorithm identifies the most relevant order of search results for a specific query. PageRank propelled Google at the forefront of the market for GSEs and has continuously been improved to allow Google keep its leading position. Today, several algorithms are run simultaneously of which, ‘Panda’, introduced in 2011, lowers the rankings of ‘low-quality websites’, typically those lacking original content e.g. content copied from other websites and/or primarily ad-oriented (FTC, 2012).

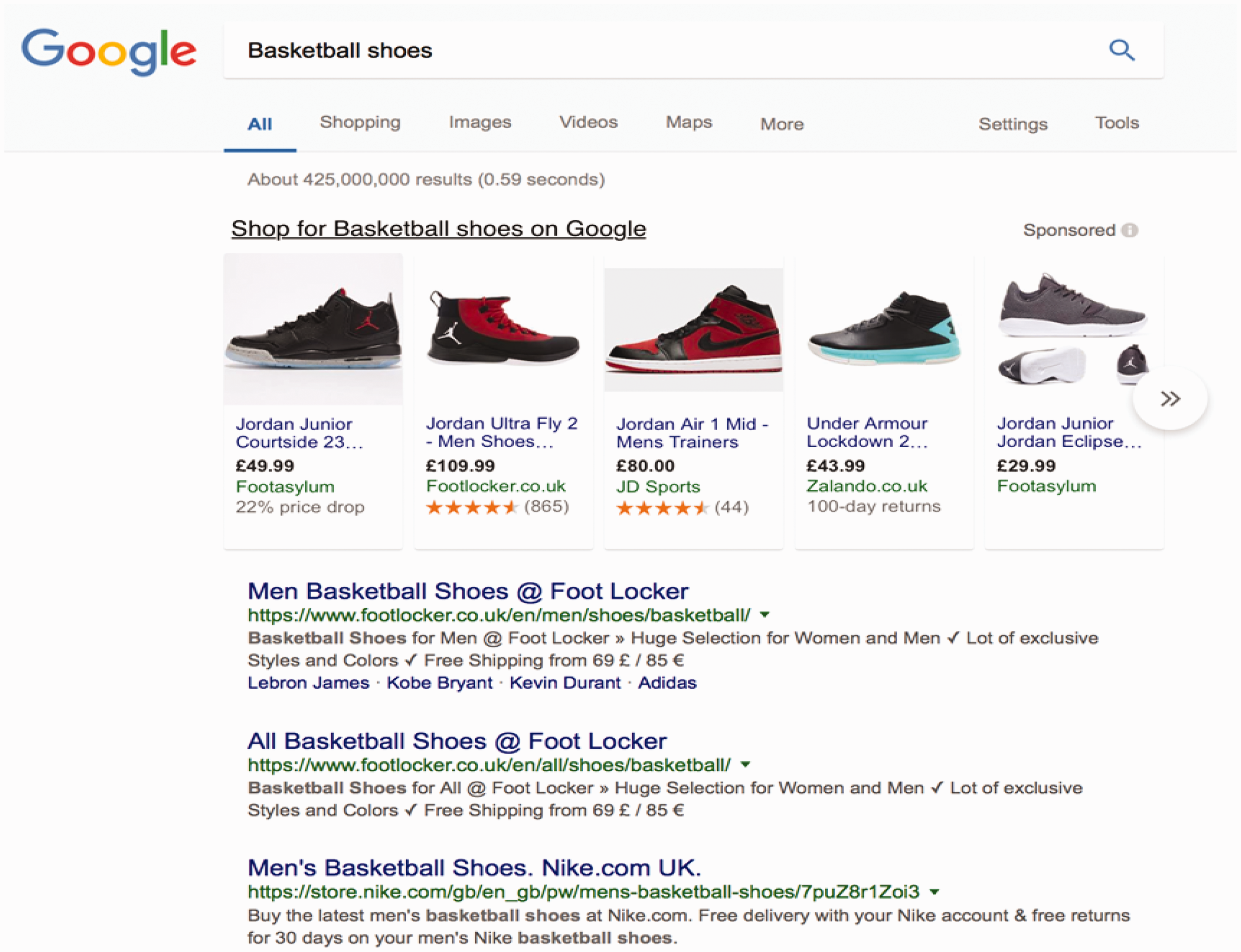

Alongside its GSE, Google developed a number of ‘vertical’ search services, whose distinctive feature is to provide results restricted to a particular category of online content such as images, news and videos. The initial release of one of the vertical search services named ‘Froogle’ was launched in 2002. It was later renamed into ‘Google Product Search’ and most recently ‘Google Shopping’. Its standalone website provided price comparison services with links to merchants’ webpages. Google Shopping operates through a pay-per-click model. In 2007 and as part of a strategy of improvement of its services, Google launched ‘Universal Search’, a new display format whereby its results page henceforth featured boxes containing Google’s specialized results above or next to generic blue links (Sullivan, 2007). The identification by the algorithms of a vertical query suffices for Google’s specialized content within that category to appear in the ‘Universal Search Box’, no matter its ranking among the results. For example, searching for ‘Basketball shoes’ leads to the results shown in Figure 1.

Google’s Shopping Box before the investigation.

Results retrieved from Google Shopping – i.e. links to merchants’ websites – appear in a richly formatted box (‘Shopping Box’) above other blue links irrespective of their PageRank. Every time a user clicks on a link in the box, the merchant pays Google a fee. The link at the top of the box (‘Shop for Basketball shoes on Google’) redirects users to Google Shopping’s standalone website. The rationale behind Google’s introduction of Universal Search was to enhance users’ experience by providing them with direct responses to their queries and minimizing their effort through reducing the number of clicks needed to find what they are looking for.

The US competition authorities’ response to Google

In June 2011, the FTC received a complaint filed by a number of vertical search engines (‘VSE’) of which several are US-based, such as Amazon, eBay, Nextag, Expedia, TripAdvisor and Yelp; and EU-based, such as Foundem (FTC, 2012). The complainants argued that Google’s search practices were problematic in two ways. First, the introduction of Universal Search unfairly promoted Google’s own vertical services through prominent display and pushing links of competing VSEs further down the results page (FTC, 2013a). Secondly, Google allegedly manipulated its algorithms in a way that ‘demoted’ rival VSEs in PageRank, thus, resulting in reduced traffic and revenue loss.

Pursuant to Section ‘The US and European competition regimes: Convergence or divergence?’, the FTC launched an investigation to find out whether Google had ‘changed its search results primarily to exclude actual or potential competitors and inhibit the competitive process; or to improve the quality of its search product and the overall user experience’ (FTC, 2013a: 2). The investigation lasted 19 months and involved interviews with industry players, hearings of Google officials and the analysis of nine million pages of documents provided by the defendant, consumer organizations, competitors and other stakeholders. The FTC’s economist team further analyzed the effects of Google’s search engine optimization on web traffic and click-rates.

In January 2013, the FTC released a statement in which it announced its decision to close the case on the premise that it had not found enough evidence demonstrating the anticompetitive nature of Google’s conduct (FTC, 2013b). Concerning the first issue – promotion of Google’s own specialized services – the FTC claimed that although competing VSEs indeed appeared further down the page (sometimes ‘below the fold’), evidence suggested that consumers greatly benefitted from Universal Search. The practice was deemed efficient and consumer welfare-enhancing. Regarding the second allegation – demotion of competitors – the FTC recognized that changes to Google’s algorithms had led to lower rankings for some VSEs, causing a loss in traffic. However, the authority considered that this was counterbalanced by the fact that the demotion resulted in greater diversity of websites appearing on the first page, with merchants’ and other links being ‘pushed up’. Furthermore, it was concluded that Google introduced design modifications with the aim of enhancing the quality of its services ‘by providing directly relevant information to consumers’ (FTC, 2013a: 3) rather than to harm competition on purpose by excluding competitors. The FTC regarded the latter as ‘incidental’ to the improvement of Google’s services and noted: While some of Google’s rivals may have lost sales due to an improvement in Google’s product, these types of adverse effects on particular competitors from vigorous rivalry are a common by-product of ‘competition on the merits’ and the competitive process that the law encourages. (FTC, 2013a: 2)

Google’s (failed) nonmarket strategy

In 2009, the Commission received a complaint by Foundem, the UK-based ‘PCW’, charging Google of exploiting the power of its GSE to systematically self-promote its own vertical services ‘while simultaneously demoting or excluding those of its competitors’ (Raff and Raff, 2011: 4). Universal Search was severely incriminated for that matter. Subsequently, around 20 VSEs lodged complaints against Google. Among the complainants were US-based competitors such as Microsoft (Ciao!), Nextag, Expedia, TripAdvisor, and Yelp; and EU-based competitors such as Twenga. The Commission opened an investigation in November 2010 to explore whether Google had, in violation of Article 102, abused its dominant position in the GSE market (EC, 2010). Under Regulation 1/2003, the defendant can suggest ‘commitments’ to address the Commission’s competition concerns. The latter then decides whether or not to make them legally binding and close the case.

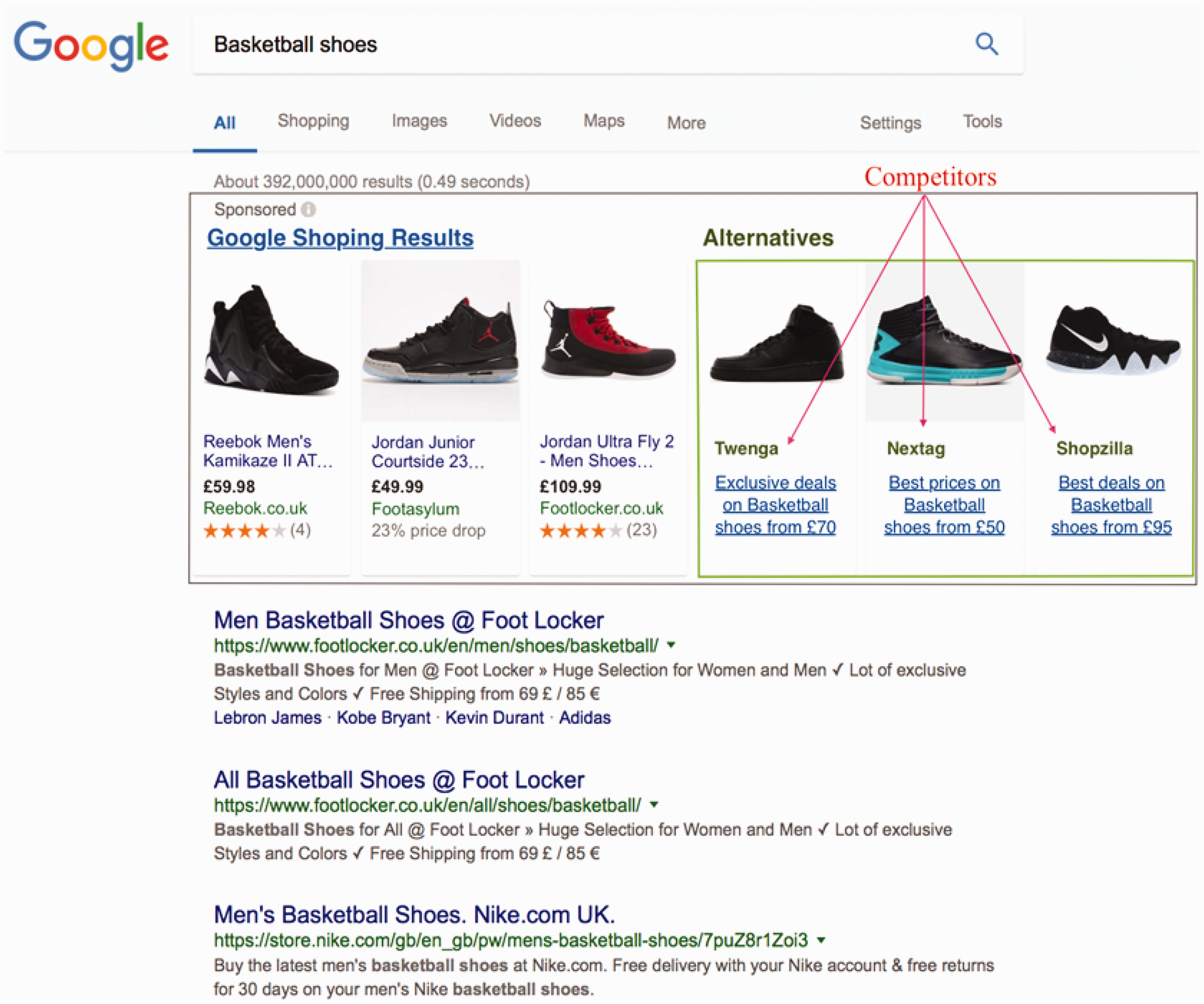

Google’s nonmarket strategy appeared to be entirely out of touch with the regulatory context provided by the EU competition regime, as they failed to address the concerns raised. The first two sets of commitments proposed by Google were rejected as they inadequately addressed the issue that relevant competing VSEs were ‘more difficult for the user to find’ (EC, 2014). The third set of commitments proposed to present results of three rivals in a comparable way and alongside Google’s own results within the Universal Search Box. Results for our ‘Basketball shoes’ query would then look as shown in Figure 2.

How Google’s Shopping Box would look like after Google’s commitments.

The commitments procedure entails a market-test of proposals and the collection of observations from third parties and complainants. Google’s proposals were eventually rejected on the grounds that ‘the feedback received […] showed that they were not effective to [fully] address’ the Commission’s concerns (EC, 2017a). The case then shifted from encompassing Google’s entire range of vertical services to one focused exclusively on its product search service (Google Shopping).

The EU competition authorities’ response to Google

The Google Shopping investigation started in July 2016 and relied on extensive evidence including internal documents and responses to requests of information from Google, complainants and third parties, 5.2 TB of search results (1.7 billion queries), surveys, experiments of user behaviour and click-rates, financial and traffic data (EC, 2017b). In June 2017, the Commission released its 216-pages-long decision imposing a fine of €2.42 billion on Google for abusing its dominant position as a GSE by systematically giving illegal advantage to its own PCW in its general search results (EC, 2017c). The Commission maintained that Google infringed Article 102 through leveraging its power in a market in which it was dominant, the market for general search services, to enhance its position in a market in which it was not (shopping comparison search).

To demonstrate the abuse, the Commission first defined the relevant digital markets. Interestingly, the Commission – contrary to the FTC – adopted a narrow definition of the market for PCWs. It argued that online marketplaces like Amazon and eBay, which also allow users to compare prices, do not operate on the same market as Google Shopping since they provide the possibility to purchase products directly. Secondly, it provided evidence for the dominance. Finally, it demonstrated the anticompetitive nature of the conduct.

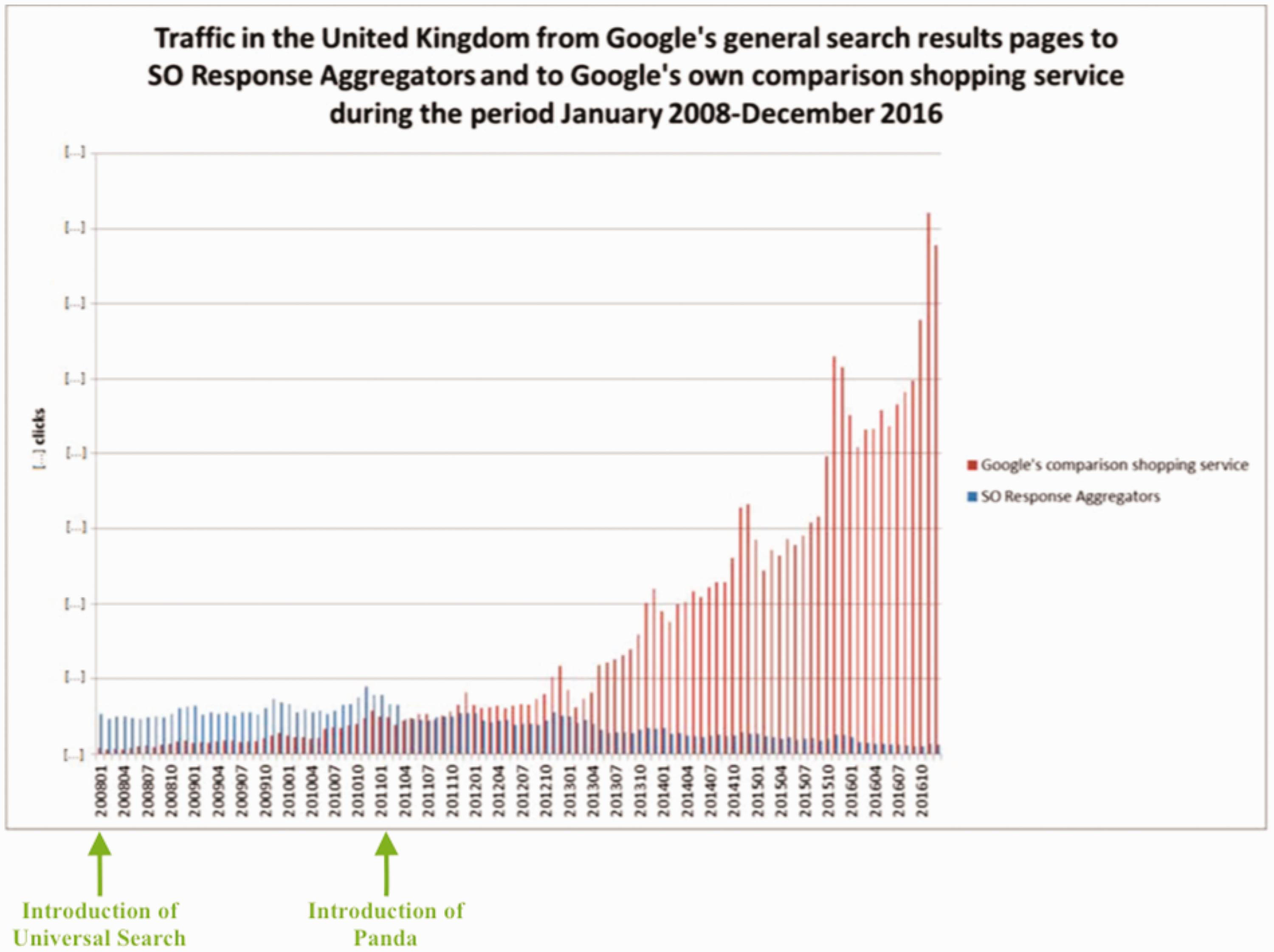

The Commission showed how Google promoted Google Shopping in its general search results by prominently positioning and displaying in rich format the Shopping Box while simultaneously applying the Panda algorithm to reduce the rankings of competing PCWs. The Commission insisted on the fact that the Shopping Box layout was never accessible to competitors while Google Shopping was never submitted to Panda. Just as in the US, two issues were at stake: self-promotion and demotion of competitors. As concerns evidence, the Commission used a Visibility Index developed by ‘Sistrix’, a search engine optimization consultancy, to prove that the introduction of Panda in 2011 considerably reduced the visibility of Google Shopping’s competitors on Google’s general search results page. It showed that competitors appeared, on average, on the fourth page of results, where traffic is substantially lower. Further, eye-tracking studies served as a basis to prove that the addition of media and information (e.g. large pictures, prices, offers) to search results – as was done with the Shopping Box – attracted significantly more traffic than a mere blue link (click-rate increased by 2.2–3.7 times). Moreover, the systematic positioning of the Shopping Box at the top of the page, above or next to generic results, further increased click-rates. It concluded – through the analysis of user behaviour and click-rate experiments – that Google’s strategy simultaneously increased traffic to Google Shopping and decreased traffic to competing PCWs, in all 13 countries where Universal Search was introduced. For instance, in the United Kingdom between 2008 and 2016, the conduct led to the changes in the patterns of click-rates between Google Shopping and its competitors as shown in Figure 3.

Traffic in the United Kingdom from Google Shopping (red) and competitors (blue).

Statements by rivals were also used to demonstrate the importance of traffic to the ability to compete. According to the Commission, without traffic, competing PCWs are not only unable to attract new merchants on their websites but more importantly cannot generate revenue. The outcome is a vicious circle: lack of revenue impedes improvements and innovation, thus reducing both the attractiveness of merchants and their traffic, restricting revenue, and so on. In parallel, it was shown that competing PCWs derive a large proportion of their traffic from Google’s general search results and that such traffic cannot be effectively replaced either by direct traffic to their websites or by other sources such as AdWords, mobile applications, social networks or other GSEs.

Next, the Commission demonstrated the ‘potential anticompetitive effects’. First, it demonstrated the foreclosure of competitors that may force them to eventually exit the market for PCWs. This would allow Google to impose higher fees on merchants, which could in turn translate into higher prices for consumers on merchants’ websites. The foreclosure is also likely to lead to less innovation for consumers as competitors may be discouraged to invest in improving their services assuming that, because of Google’s conduct, they would not be able to attract traffic. In parallel, Google may be less likely to innovate as it expects less competition from rivals and increased traffic.

Second, it demonstrated the decreased ability of consumers to access the most relevant results as they are likely to believe the results in the Shopping Box are the most relevant while these could well be results from rivals appearing in subsequent pages. The Commission added: ‘The Conduct therefore risks undermining the competitive structure of the national markets for comparison shopping services’ (EC, 2017a: 181). The Commission also noted that it is not required to prove that rivals have actually ceased to provide their services, but only that this is likely to happen. Likewise, it was sufficient to demonstrate that Google’s conduct is capable of decreasing traffic to rivals and increasing traffic to Google Shopping, not that it actually did.

In the market for GSEs, the Commission claimed that the favourable positioning and display of its own PCW gave Google a financial advantage over its rivals and therefore made it more difficult for them to compete. Further, the decision clarified why Google’s efficiency defence was rejected. It is reaffirmed that while the Shopping Box in itself may have been beneficial for consumers, it is the fact that competitors did not have access to it that was considered anticompetitive. Likewise, while the demotion of low-quality websites by Panda could have been regarded as efficiency enhancing, it is the fact that Google Shopping was not submitted to it that was deemed illegal.

Comparative analysis of the EU and the US responses to Google

Abuse of dominant position

The US and EU competition authorities had different views regarding what accounts for consumer welfare. The FTC emphasized the quality-enhancing aspects of the Universal Search Box and remained fixed on consumer welfare as defined by price, quality, output and innovation. In contrast, the Commission systematically stressed the harm to consumer choice stemming from the decreased visibility and potential exit of competitors. The Commission’s decision has many references to Google’s conduct ‘interfering with’ or ‘undermining’ the competitive structure of the market for PCWs (by excluding or threatening to exclude competitors) and the weakening of the level of competition. It stated that: …users should [instead] have the opportunity to benefit from whatever degree of competition is possible on the market. (EC, 2017c: 76)

Market structure, efficiency and innovation

The importance of pluralism and consumer choice is also illustrated by the rejection of Google’s efficiency defence on the grounds that consumer benefits derived from the Shopping Box were outweighed by the fact that competitors were denied access to it. Despite modernization and the more-economics approach, the Commission thus still favours market access over efficiency, as one interviewee said: They forgot economics. (Interview, Competition Expert B, 15/06/2018) It’s about “let’s protect weaker parties, let’s have freedom of competition” so it’s not an economic framework that they set out. […] There’s no economic, it’s just factual evidence. (Interview, Competition Expert C, 19/06/2018) would work more [in the US] than in the EU. (Interview, Competition Expert K, 04/07/2018) The real reason is that the commission isn’t taking efficiencies seriously or thinking about them in a sensible way. (Interview, Competition Expert B, 15/06/2018) From a US [perspective], if you’re a consumer welfare believer you might tolerate a situation where you have one search engine so long as [it] works to give you the best quality you can ever hope for. But if you are European then you would say ‘no, I don’t tolerate monopoly, I want choice. Even if choice is inefficient. Because choice is part of the way which we believe markets should function. (Interview, Competition Expert C, 19/06/2018) the Commission doesn’t seem to have investigated [the efficiency]. (Interview, Competition Expert B, 15/06/2018) …good for consumers, good for competition and good for innovation. (Leibowitz, 2013: 6) The Commission’s view is that innovation is more likely to happen the more rivals you have. […] The US Court once said that monopoly is good because it stimulates rivals. A monopoly is like a magnet for competition. So you have different views on what incentivizes innovation. (Interview, Competition Expert C, 19/06/2018)

Markets and regulatory intervention

As mentioned earlier, the European competition regime reflects a fear of type-2-errors, whereby the cherished competitive structure risks being damaged forever if antitrust authorities do not intervene. As one interviewee indicated: The Americans are relatively relaxed about unilateral conduct. Fifty years ago they were very strict and then you have this whole economic efficiency thing that started. And they’ve gone to another extreme now. What I’d say is that in the States there’s a much greater belief in markets than in Europe. I think that there’s a belief that over time markets will correct themselves. So you don’t want the power of the states being brought to bare, and telling people what to do and what not to do. […] They don’t like false positive, they don’t like finding people guilty when they’re not guilty. […] There isn’t much appetite for investigating unilateral behaviour. (Interview, Competition Expert A, 14/06/2018)

This disagreement over the best cure to concentrated markets reflected deep-rooted origins of the US and Rhenish capitalist models: the markets themselves in the US, and the enabling State in Europe. It’s not about the principles being different it’s about the taste for intervention being very very different. The Americans fundamentally don’t believe in intervention and the Europeans fundamentally do. (Interview, Competition Expert B, 15/06/2018) Cases have shown that the US is less concerned with big companies having potentially anticompetitive conduct […]. In Europe we have a perception that […] we should be more cautious of potential conducts of dominant nature. (Interview, Competition Expert K, 04/07/2018) …to reach a critical mass of users that would allow them to compete. (EC, 2017c: 195)

Time horizons: Short-termism vs long-term perspectives

Although the literature reported a shift to a short-term perspective (Aydin and Thomas, 2012), the Commission’s arguments outlined in the case of Google, still depict long-term concerns. First, the ‘more-economics’ approach in the EU competition regime is still highly intertwined with the long-term Internal Market project and the promotion of the four freedoms. The EC decision stated that: …any restriction on Google's rights and freedoms corresponds to the objective of the Union to establish an internal market, which […] includes a system ensuring that free competition is not distorted to the detriment of the public interest, individual undertakings and consumers. (EC, 2017c: 199) The Conduct affects the competitive structure of the internal market by eliminating or threatening to eliminate competitors operating within the territory of the Union. It therefore affects trade between member-states. (2017a: 201)

Discussion and conclusion

The comparative analysis of the Google case provided us with several interesting insights. First, considering the alternative explanation that the diverging responses were driven by protection of material interests and promoting national champions, we did not find any evidence to support this. Google’s competitors who filed complaints were predominantly US multinational technology firms. There was no clear bias in favour of European firms and no evidence of ‘regulatory capture’. Instead, these decisions benefited the interests of US competitors to a larger extent than EU competitors, especially, since the US is by default the dominant incubator of Silicon Valley-type start-up firms.

Secondly, the same pattern appears to be applicable even in cases of decisions where no US multinational is involved. The recent Alstom–Siemens merger case corroborates our argument further. The EC blocked the merger between those two EU-based multinationals, which would have created a European champion in the rail transport sector (White and Sachgau, 2019). The rationale was that the merger would ultimately limit rivalry and competition in the markets for high-speed trains and signalling systems, and seriously threaten innovation and low prices for consumers. A similar pattern is further supported by retrospective consideration of past examples. The planned merger between GE/Honeywell in the aerospace industry was blocked by the EC for similar reasons (Morgan and McGuire, 2004). Finally, the abuse of dominant position by Microsoft due to its Windows operating system, in the media player and web-browser markets through ‘tying’ (Daskalova, 2015), further enhances the plausibility of this pattern, since Netscape or other media player vendors were not European.

The analysis of this case helps us to set out the ‘boundary conditions’ of our argument. This transatlantic divergence between the US and EU competition regime is likely to resurface when the contestability of the market is threatened – irrespective of the home country of the multinational or other material interests. This contestability is even more likely to be threatened in niche technological sectors with few players. Such highly dynamic markets tend to be composed by few dominant firms owing their market power either to technological innovations (software, Internet) or high sunk costs (aerospace) or a combination of both (high speed trains). The lack of contestability is likely to fuel the European fears of insufficient competitive intensity and lack of choice for consumers.

Additionally, the divergence in competition regimes is likely when there is scope for interpretation on the boundaries of the market. This is especially the case with newly constructed digital platform markets, which are nested into each other. As recent legal analyses of the case indicate, problems of ‘vertical foreclosure’ arise when a firm that owns a dominant platform (Google Search) competes on a downstream market (comparison shopping services) with other firms that need to have access to the dominant platform to provide their services (Geradin and Katsifis, 2019: 89). One could argue that Google’s GSE is also very idiosyncratic as it can be seen as a ‘quasi-public good’; it is a free service accessible by millions. Although there is merit in this argument, what might appear as a free service is in fact paid by in non-conventional ways. Google has found other ways to receive payments, by monetizing the value of our data, and also by offering advertising space including complex pay-per-click models that we mentioned earlier.

The article unpacked the axiomatic differences between Ordoliberal and Chicago School principles, which underpin the EU and US competition regimes, respectively. This speaks against arguments that suggest there has been regulatory convergence between the US and EU competition regimes (Bartalevich, 2016; Buch-Hansen and Wigger, 2010; Wigger and Nölke, 2007). In Europe, the Ordoliberal structuralist ideas of pluralism, economic freedom and public intervention as a means of protecting the competitive process hinder the full adoption of a Chicago-style economic outcome-oriented framework that relies on markets as regulators of competition and guarantors of consumer welfare. This concurs with the argument that full substantive convergence between Europe and the US seems unlikely (McGuire and Smith, 2008: 138). That said, our findings have some limitations, as we rely on a single case study; and therefore, there are – by design – constraints to its generalizability. Although this pattern seems to be confirmed by the EU stance on other Big-tech multinationals such as Amazon, Facebook and Apple (The Economist, 2019), there is scope for future research to look into other cases and explore further the deep-seated differences in the competition regimes in the US, Europe or other regions.

Finally, the article fleshed out the ‘competition regime’ as a distinct institutional sphere that reinforces the divergence between models of capitalism. The EU competition regime is by and large designed on the basis of German capitalism model. In the US there is greater reliance on the market mechanism as a mode of coordination and greater short-termism in time horizons, whereas in Europe there is more reliance on non-market forms of coordination (including regulatory intervention when needed) and long-term perspectives. These fundamental aspects of capitalist models were clearly echoed in the responses of the US and European competition regimes to Google’s strategy. In the US, the FTC considered Google’s conduct as beneficial for consumers in the short term; intervention was avoided so as not to stifle innovation; and there was reliance on market mechanisms to eventually rectify any concentration. By contrast, the EC considered Google’s strategy as harmful for consumers through reduced choice, and also non-market intervention was required to avoid concentration and reduced competition and innovation in the long term. Overall, this perspective opens up a new avenue of future comparative research examining the interplay between the ‘competition regime’ and company strategies at the national or supranational level, as an additional layer of institutional variety and complexity.

Footnotes

Declaration of conflicting interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: The views and opinions expressed in this article are those of the authors and do not reflect the views of KPMG Luxembourg or any of the KPMG network of independent member firms affiliated with KPMG International.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.