Abstract

The ‘financialization of everyday life’ is a concept widely recognized by academics as an increasingly fundamental way of understanding the impact of neoliberal ideologies and financial processes on individual identities, subjectivities and relationships with financial services. This article contributes to debates on the consumption of sub-prime credit and calls for a sophisticated analysis of this aspect of financialization to take into account the variegated use of financial services and use of credit by people on low and moderate incomes. Drawing on qualitative analysis of the ‘lived experience’ of financialization, based on rigorous in-depth interviews with 44 low/middle income borrowers in the United Kingdom the article concludes that: individuals are at risk of financial insecurity due to increasing variegation of credit markets, and; that the binaries of ‘super inclusion’/’relic’ financial ecologies fail to reflect the complexity and variegation of credit use in contemporary society as a result of financialization.

Keywords

Introduction

The consumption of personal credit has received increased attention in recent years across the social sciences, particularly in relation to the ways in which it shapes markets and subjectivity (Burton, 2008; Burton et al., 2004; Langley, 2008a, 2008b, 2014; Leyshon et al., 2004, 2006; Soederberg, 2013). Debates have explored how credit is used for lifestyle consumption and as a means of ‘getting by’ (Burton, 2008; Soederberg, 2013). More recently, research has examined the implications of not being able to repay credit commitments and the debt recovery process (Deville, 2015). However, the consumption of credit by those on low and moderate incomes is often ignored by academics (Burton, 2008). Drawing on the concept of financial ecologies (Leyshon et al., 2004) this article adds to this debate by exploring the relationships between the sub-prime consumer credit market and individuals at the financial ‘fringe’. The financial ecologies approach suggests that the financial system (re)produces smaller: ‘distinctive ecologies of financial knowledge, practices and subjectivities [which] emerge in different places’ with unequal consequences for the consumer. (French et al., 2011: 812)

One of the early outcomes of financialization was thought to be the creation deeper and wider forms of financial exclusion depending on the extent to which individuals were able to access (mainstream) financial products and services (French et al., 2011). Sub-prime credit may be defined as high-cost for those with poor credit histories (Burton, 2008) and has been further categorized into levels of risk to create personal credit products for these markets (Burton, 2008; Dymski, 2005, 2006; Soederberg, 2013). Dymski (2006: 309) suggests that financial stratification as a result of deregulation, technological innovations and securitization for example, ‘has been a key driver of processes that create financial exclusion’. However, with the notable exception of Leyshon et al. (2004, 2006) only very few empirical studies have investigated the consumption of the sub-prime credit market, and this article addresses this gap. The consumption of credit is explored by drawing on 44 in-depth interviews with low/moderate income borrowers in the UK to provide a qualitative analysis of the ‘lived experience’ of financialization at the fringes. In so doing, the article shows how their experience of credit is much more variegated than is often assumed. This has important implications both for the understanding of the ‘financialization of everyday life’, financial subjectivity and financial ecologies.

The argument of the article is developed over six parts. The next part of the article provides some background on the use of consumer credit by those on a low to moderate income before outlining the conceptual framework. The third part outlines the research methodology. The fourth and fifth parts draw on the data to present a new taxonomy of how credit is supplied and consumed and refer to case studies that explain why consumers choose different modes of credit. The sixth part summarizes the key findings in the discussion. The final part concludes the article.

Drivers of lending and borrowing: Context and background

The liberalization of financial markets in the 1980s enabled the growth of consumer credit (Langley, 2008a, 2008b). This facilitated access to personal credit from mainstream sources such as credit cards, overdrafts and loans for those on middle and higher incomes with good credit scores to consume goods and services to maintain or enhance their lifestyle particularly if incomes were squeezed (Crouch, 2009). In 2008–2009, two-thirds of people in the UK had at least one form of unsecured credit (Rowlingson and McKay, 2014). This is due to both increased supply and demand for consumer credit.

For low-to-moderate income households, access to unsecured credit is important to meet every day needs and manage fluctuating incomes. However, for those with a poor credit history and insecure incomes, Soederberg (2013: 493) suggests that: to augment their incomes, a significant number of underemployed and unemployed … have come to rely heavily on expensive forms of debt, including payday loans, pawnshops.

Financialization has created a two tier credit system: prime and sub-prime credit. For those in the sub-prime category, without mainstream access to credit, there is a variety of high-cost alternatives ranging from short-term payday loans to longer-term home collected credit. There are also, potentially, lower cost loans available from credit unions and community development finance institutions (CDFIs), but these are options often restricted by their membership and by their responsible lending policies so are not available to everyone. In this way, Stenning et al. (2010: 142) point to the broader context to: … remind us that for all the inclusion of poor households into the circuits of international finance capital, their position often continues to be marginal and weak, and the development of fuller forms of financial citizenship based upon market mechanisms has to be questioned.

Indeed, analysis by Beddows and McAteer (2014: 7) confirms that the sub-prime market is changing rapidly and the value of payday lending (‘traditional payday loans and short-term cash advances’) increased from £0.33 billion in 2006 to £3.709 billion in 2012. It is therefore likely that (sub)prime markets will continue to be stratified to diversify the ecologies of finance and strengthen financial subjectification. This raises broader issues about the nature of financialization as a new stage of capitalism (Van der Zwan, 2014).

Conceptual approach: From financial exclusion/inclusion to financial ecologies and variegation

The financialization of everyday life is thought to be creating a new type of financial subject who is expected to be ‘a self-disciplined borrower as a consumer who is at once both responsible and entrepreneurial’ (Coppock, 2013; Langley, 2008a: 186). In practice, however, there are many challenges, particularly facing people on low and moderate incomes in relation to the access and use of mainstream and alternative sources of credit.

Financial exclusion was first termed by Leyshon and Thrift (1995) to denote one of those challenges: geographical exclusion as a response to bank branch closures and changing financial markets. The term financial exclusion has since evolved to become a broader spectrum than simply a lack of physical access to financial products and services (Kempson and Collard, 2012; Leyshon and Thrift, 1995) with financial exclusion potentially disrupting the notion of a rational financial subject. For example, the Organization for Economic Co-operation and Development (OECD) definition of financial inclusion brings together access to affordable, appropriate products and services, with the addition of financial capability (OECD, 2014). The concept of financial exclusion has therefore evolved from people having physical access to banking services to the idea of people having access to ‘appropriate and affordable’ financial services. This suggests that, for some people, it may be better to have no access to financial services if they are inappropriate. Self-exclusion may therefore be an appropriate option at a particular point in time for some people. However, Leyshon and Thrift (2007: 111) suggest that while: there are people who, no doubt for good reason, want to opt out of the formal financial system, the fact is that many more people want to be included in it but simply do not have the assets to declare a hand.

The concept of financial ex/inclusion has been helpful in increasing understanding of the financialization of everyday life. Academics such as French et al. (2011) and Kear (2013) have moved beyond a simple binary (inclusion versus exclusion) to developing notions of ‘financial citizenship’ and ‘financial ecologies’ to explore the uneven ways in which financialization plays out in practice over space. Leyshon et al.’s (2004: 625–626) article on the ‘ecology of retail financial services’ outlined how mainstream financial services have ‘super-included’ financially stable households with high, secure incomes on the one hand and ‘bypassed’ lower income households that are inhabited by ‘relic’ financial ecologies on the other. These lower-income households, often ignored by or excluded from mainstream finance, may turn to alternative lenders such as doorstep lenders, rent to own, pawn shops, and payday lenders. The concepts of ‘super-included’ and ‘relic’ financial ecologies are helpful in understanding how the financial system has created ‘uneven connectivity and material outcomes’ (Lai, 2016: 28). The financial ecologies approach helps clarify understandings of the complex relationship between financialization and financial subjects, and in particular how these are (re)shaped through the consumption of credit, which is the focus of the article.

However, while this approach is extremely helpful, consumer credit markets, particularly those considered to be ‘relic’, require further exploration to understand the changing supply and demand of credit products at the financial fringes. For example, while Leyshon et al. (2004) explored moneylenders as part of their article on financial ecologies there have been dramatic changes to the ‘sub-prime’ credit landscape since their article was published, not least with the growth of payday lending, enabled by technological advances and innovation in credit scoring. There are now a large number of products entering the market to respond to consumer demand, which serve to normalize particular ‘sub-prime’ products such as payday loans (Aitken, 2010). This article extends this wide variety of ‘sub-prime’ products, from moneylenders to pawn brokers to include payday lenders.

In the same vein, Langley (2008a: 13) has also pointed out that: everyday borrowing is indeed discriminatory, hierarchical, and marginalising, but these inequalities increasingly cannot be addressed through the binary of exclusion/inclusion.

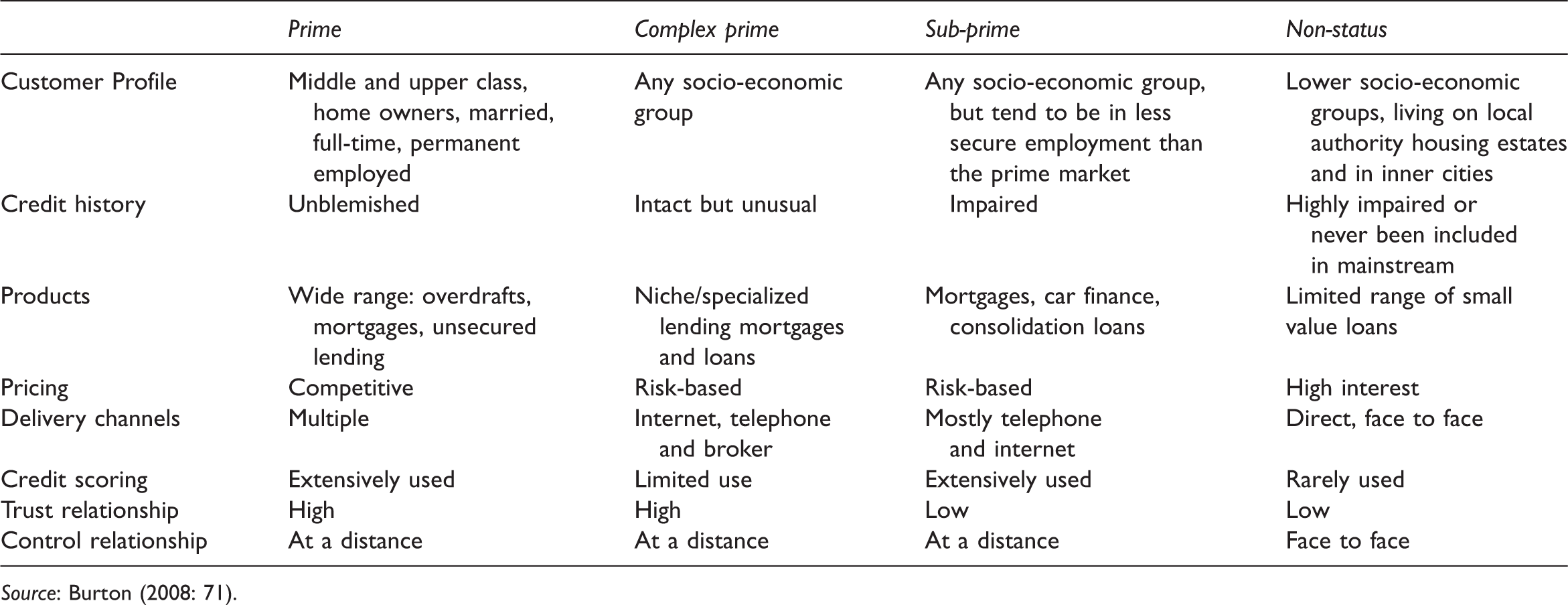

Segmentation of the personal-sector credit market.

Source: Burton (2008: 71).

Methodology

The aim of the research was to explore the variegated financialization of everyday life through an investigation into the consumption of unsecured credit for individuals on a low-to-moderate income in the UK. While the research recognizes that secured mortgage lending can also involve the mainstream/sub-prime distinction, this raises many different issues and would need to be the focus of another article. A general conceptual framework is posited posited, drawing on the literature on financialization, financial in/exclusion and financial ecologies. The qualitative research took the form of forty-four semi-structured in-depth interviews to explore people’s experiences in a grounded way. This included interviewees who had borrowed from a range of alternative lenders in the previous year – including payday lending both online and in shops, doorstep lending, pawn broking and credit union lending. The study focused on people on a low and moderate income who had accessed alternative forms of credit in the last twelve months and therefore those with no access to any of these forms of credit were excluded.

Fieldwork took place between March and June 2014 in the West Midlands and Oxfordshire regions of the UK. Participants were recruited using a specialist company who identified people in shopping centres and high streets using a screening questionnaire that the authors had designed. A broad mix of participants was interviewed in terms of age, gender, employment and family type. Each interview lasted between 45 minutes and two hours at a place of the respondent’s choice (the majority in their home and some in a café). Where possible, the authors of the article conducted the interviews in pairs to ensure research quality and safety.

The research received full ethical approval from the University of Birmingham. Informed consent was gained by explaining, at the beginning of each interview the nature of the research, how the data would be used and this was also explained in the research information sheet which was given to each participant. To thank and compensate the participants for their time (and encourage participation), they were given £30 cash. This payment was initially queried by the university ethics reviewers and while the debate about paying respondents was appreciated (Thompson, 1999), it was deemed important to recognize the time and help given by the interviewees. In addition, an information sheet with details of organizations providing free, confidential and independent advice on money issues was provided. The interviews were carried out by the authors who are fully trained and experienced in conducting interviews on potentially sensitive issues. Pseudonyms have been used and other measures to ensure participant confidentiality.

Each interview was digitally recorded and transcribed in full. The data was analysed using thematic ‘framework’ analysis (Ritchie et al., 2013) aided by Nvivo computer software. Although key themes were identified from the literature and broad theoretical framework (financial ecologies and variegation) the analysis was open to new themes emerging from the data. The next part of this article presents the new typology and also illustrates the key groups identified through selected case studies.

The spectrum of consumer credit consumption

In this section the consumption of credit is situated within the concept of financial ecologies to explore the variegation of sub-prime credit and understand the implications of financialization on everyday lending and borrowing.

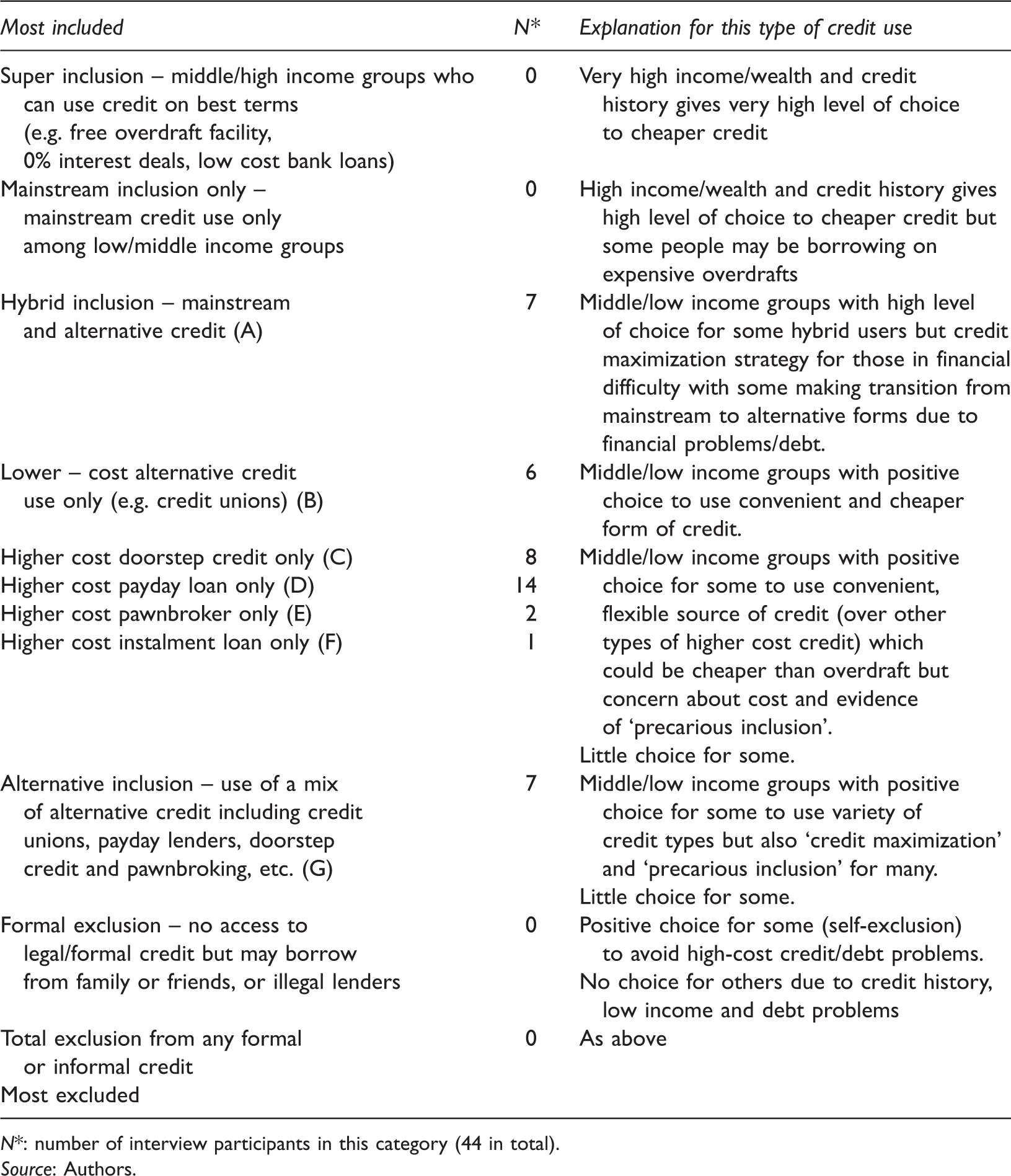

Typology of credit consumption.

N*: number of interview participants in this category (44 in total).

Source: Authors.

Table 2 also recognizes (drawing on the literature review) that some people use no formal credit at all. This may be because they have large assets and therefore never need to borrow or, at the other end of the spectrum, because they are on low incomes and choose not to borrow or are excluded from borrowing. Nevertheless, some in this group may borrow informally from family and friends. The final group in the table recognizes the fact that some people may have no access to any form of credit. These groups did not form part of our empirical research but are included in the table for the sake of completeness.

Following on from Burton’s (2008) work on the segmentation of personal credit markets, Table 2 illustrates a new typology of variegated credit use based on interview analysis. A significant proportion of borrowers (38 out of 44) did not use mainstream credit at all, either because they were excluded or self-excluded and could be considered to be either ‘complex prime’, ‘sub-prime’ or ‘non-status’ (rather than ‘prime’ or part of the ‘super included’ financial ecology) (Burton, 2008; Leyshon et al., 2004).

Explaining modes of credit use

This section explores the consumption of consumer credit by those on low to moderate incomes. The rationale for choosing particular forms of credit is explored to determine why some people are in one group rather than another. Moreover, we situate the concept of ‘relic’ financial ecologies within the context of contemporary sub-prime lending.

Overall the research suggests that people’s use of credit was largely based on knowledge and advice from family or friends which supports this aspect of the ‘relic’ financial ecology (Leyshon et al., 2004). However, it was also found that a combination of individual circumstance, credit history, attitude and previous experience, rather than whether they were simply employed or unemployed, their customer profile (for example homeowners or in permanent, full-time employment) or their level of income were also important in their choice of credit.

Groups A–G indicated signs of ‘relic’ financial ecologies in the sense that they may have poor credit histories and considered risky to lend to (Langley, 2008b; Leyshon et al., 2004). For example, some of these people were on a very low incomes/not in stable jobs/had gaps of unemployment which may explain mainstream financial exclusion. However, some were employed full-time in permanent jobs and at the margins of mainstream finance, as John explains: I’ve got a bit of a bad credit. I did try with my bank, … as recently I’ve had good credit [but] they still look at your history status beyond that. I did look at that option, even getting an overdraft, but they just declined me. I felt as if I was pushed into a bit of a corner. I did say, ‘What else can I do?’ (John, 20s, employed, tenant, one child)

To summarize, the research found that the factors that determined the particular mode of borrowing was that home credit borrowers tended to prefer cash, face-to-face transactions, flexibility of loan repayments and that there were no hidden costs. Payday loan borrowers were optimistic that they could repay their loan quickly (Bertrand and Morse, 2009). Borrowers that used credit unions were predominantly single women with children. This may be because some credit unions used child benefit for proof of loan repayment. The research also found that borrowers that used credit unions were self-employed, worked part-time or unemployed due to caring responsibilities. Credit union borrowers also tended to be debt averse. Word of mouth was key to finding out about credit unions and how they operated. Borrowers that used a combination of sub-prime sources (for example home credit, payday, credit unions) tended to be single females under the age of 30 with children, suggesting they were at greatest need of access to credit. Drawing on the case studies, the remainder of this section goes on to draw on case studies from each of the groups A to G, in order to illustrate the complexity of the issues and the difficulties of making simple judgements about financial inclusion/exclusion, even with a more refined spectrum approach.

Group A: Hybrid inclusion-Mainstream and alternative credit

Group A included six people who, in the past twelve months, had used both mainstream and alternative forms of credit. It was found that this group of people all had children, which is a key lifecycle stage when incomes are low and expenses high and it is known that lone parents are at greater risk of becoming over-indebted (Bryan et al., 2010). It raises the question as to why those with access to mainstream credit also borrow from alternative lenders because it is often assumed that mainstream credit is a better/cheaper form of credit. The case studies suggest a range of reasons. For example, some people made a choice between different forms of credit depending on need at different times. In some cases, people found that mainstream bank overdrafts were more expensive than other forms of credit and so they made a positive choice to use alternative lending in such cases: ‘How much is the bank charge…’ It’s like £6 a day. I’m trying to work out is it cheaper to get a [payday loan]… or is it cheaper to have the [overdraft] bank loans? (Amy, 20s, child, unemployed)

Finally, this group includes those who were making a transition from mainstream to sub-prime, normally as a result of changes in circumstances (for example, a change in employment or income). For example, Nigel (30s, employed, homeowner, children) stated: It was just because I was going to have a shortfall of that amount of money at that time which I couldn’t get my hands on, so the easiest way of doing it was through them because they’re quite easy to get the money off – so are a lot of other companies, to be honest. That’s just one of the ones that are, but the APR’s horrendous, so you wouldn’t have it over a long term because you’d never pay it back.

There were a number of other cases in the sample, however, of people who had borrowed from mainstream sources in the past, but had then turned to alternative sources as they struggled with their commitments. Thus the fact that people had ‘hybrid inclusion’ was often a sign of financial distress rather than greater choice. For example, Angela’s (40s, with a child, employed, mortgage) experience of access to credit led to major debt problems. Angela had recently used a pawnbroker to borrow £110 to pay some bills as she was on a debt management plan (to repay over £25,000 from credit cards and bank loans) and believed she couldn’t borrow from any other source (apart from family or friends). Angela is an example of someone making a transition from mainstream (super-included) to sub-prime (relic) due to becoming over-indebted. This transition highlights the dynamics of credit use, an issue not previously explored sufficiently by the financial ecologies literature.

Group B – Low-cost alternative credit use only (credit unions)

Another six people in the sample had only used credit unions for borrowing. Credit unions are most certainly a cheaper form of borrowing than other alternative lenders such as payday and doorstep credit, but they are not necessarily seen as ‘mainstream’ (Fuller and Jonas, 2002). However, some credit unions may be cheaper than banks for those categorized as having complex-prime, sub-prime or non-status credit. Chris, for example, was self-employed and his income fluctuated. He reported that he: Looked at the bank … but the credit union was cheaper, … I know you don’t get a decision instantly, it takes a few days, but it was just convenient, yeah. I mean, I went with them because I was recommended by a friend a few years ago. It’s just cheaper and easier. Plus … I didn’t want a loan against my bank, in case I ever needed anything from [them] in the future, and I didn’t want them saying, ‘Well, you’ve got a loan with us, we can’t do this, we can’t do that. ‘… offer individuals and households an opportunity to mediate and/or actively subvert the wider processes and impacts of financialisation and neoliberal subjectification in their everyday lives.’ (Coppock, 2013: 482)

Group C – High cost doorstep credit only

Eight people in the sample only used doorstep/home collected credit. In line with previous research (Rowlingson, 1994), doorstep credit was seen as convenient, transparent and flexible, which places them firmly in the relic financial ecology (Leyshon et al., 2006). People got to know their agents and preferred to use this form of credit to payday lending and overdrafts. However, there were signs with doorstep lending (as with other kinds of lending) that people were being encouraged to borrow more than they otherwise would. This led to a form of what we have termed ‘precarious inclusion’ whereby people had access to credit but that this could lead to debt problems. For example, Sasha was a single mother of three, including a child with disabilities, in her thirties and not working. Sasha became stuck in a doorstep credit cycle of ‘precarious-inclusion’ due to the ease with which she was able to obtain a loan. For example, she stated: Once I’d paid [the first loan], then do you want another loan, and it’s like well, I could buy this for the kids, I could buy that. It’s like easy money, you have to pay it back but it’s easy money when they’re offering it you and you’ve got like two kids and single parent. I’ve been with them years and had no problems. Sometimes you stick to what you know. I don’t do any of these pay day loans or anything like that.

Group D – High cost payday credit only

Fourteen people in the sample had only used payday lending in the last 12 months. Similar to doorstep credit (though in different ways) they saw this form of credit as easy to obtain. Payday lending was preferred by this group due to the perception that this enabled them ‘to maintain dignity, privacy, responsibility and independence’ (Rowlingson et al., 2016: 9). For Wayne (thirties, employed, tenant, with children), the loan acted as a safety net in times of need: I’d do it again, because it’s an easy option. It’s just touch of a button, kind of thing, and like I say, all depending on circumstances that I need it for, if it’s something I can wait for then no, I won’t need it, but if it’s something desperate that I need, then yes, why not, because I’ve always said if you can afford to pay it back then it shouldn’t be a problem. sensitive to the highly complex, fragile, precarious and shifting life world for many consumers for credit and have been innovative in both responding to, and attempting to extend, this market. (Burton et al., 2004: 23)

Groups E and F

These groups only had three borrowers and were drawn to: pawnbroking as a way of accessing cash quickly; and instalment loans as an easier way to repay loans compared with payday loans.

Group G – Alternative inclusion – Use of a mix of alternative credit

Some people decided to only use one form of alternative credit. This appeared to suit their needs and they may have taken out more than one loan with one or more companies. Other people, however, decided to use a mix of alternative lenders and this was the case for seven people in the sample. For some, this was a positive choice to use different lenders to meet different needs, but for others it was a form of ‘credit maximization’ which suggested financial difficulties and/or a state of financial transition.

For example, Jessica (forties, employed part-time, tenant, with children) worked 12 hours a week on minimum wage (although on long-term sick leave) used payday loans each month to bridge the financial gap between her income and outgoings. Jessica also took out a £500 loan from the local credit union once a year to pay for Christmas presents and also pawned jewellery for small amounts of money. She used these forms of credit due to bankruptcy in the past due to catalogue, doorstep credit and credit card debts: I’ve got into debt previously where I had to go bankrupt and everything but that’s all water under the bridge now, that was a few years ago now, so… I just go for the pay day loans or the Credit Union… I intend to live by my means, but it doesn’t always work out like that, you know, you always need something else. [If] I can’t make ends meet or whatever and then I go in, they’re normally pretty good because I’ve been with them now for about a year, two years, so I’ve built up a relationship with the staff and that, you know, they know who I am when I go in.

Discussion

This article has explored the diverse credit use of those who use alternative, ‘non-mainstream’ forms of unsecured credit. This article has highlighted the ways in which the geographies of credit consumption at the ‘fringes’ are being (continually) redrawn as a result of how alternative credit products and regulation are in some ways becoming normalized (Aitken, 2006, 2010). In so doing, the research has highlighted how the concept of financial ecologies has evolved as individuals have become increasingly financially variegated within the financial system (at different times and in different ways). They may transition between the two spaces and cannot therefore be simply defined as prime or sub-prime.

Four key points are made. First, that there are no simple binaries between prime/sub-prime forms of unsecured credit and between the ‘super-included’ and ‘relic’ financial ecologies (Kear, 2013; Langley, 2008a; Leyshon et al., 2004). Prime, mainstream credit varies from types of lending which can be extremely favourable (for example, free overdraft facilities and low interest bank loans which meet the needs of those on middle and high incomes) to types of lending which can be extremely expensive (including charges and interest on some overdraft facilities both pre-arranged overdrafts and those that are not arranged).

Alternative forms of credit also vary substantially from credit unions which are much lower cost than payday lending or doorstep lending but are nevertheless not part of mainstream financial services. Doorstep lending can be characterized as a ‘relic’ form of lending with its emphasis on cash and personal interaction, but payday lending is one of the most innovative and ‘modern’ forms, relying on mainstream mechanisms such as credit scoring models and online platforms (Burton et al., 2004; Leyshon et al., 2004). Financial ecologies are diversifying further alongside the variegation of credit and the boundaries between the ecologies are becoming increasingly blurred.

Second, just as forms of credit do not fit into simple boxes, patterns of credit use are also complex. As the research suggests, some people use a mixture of mainstream’ and alternative sources of credit (Group A) (Coppock, 2013). This could be interpreted as a positive development as people choose from different sources to meet their needs. However, this raises the question as to why people choose alternative forms of credit over mainstream sources that are generally assumed to be cheaper. The data shows that some people with financial difficulties are merely accessing as much credit as possible from whichever source they can (‘credit maximization’), often because they are desperate. Some people are moving from the mainstream to alternative providers as they lose access to mainstream sources, while others are exercising very ‘constrained’ choice by electing to use payday loans rather than a more expensive overdraft. The research therefore highlights the complexities of the situations people find themselves in and once again the inadequacy of prime/sub-prime binaries.

The third point relates to the issue of consumer ‘choice’. The exercise of constrained choice in this market was a recurring feature of the research, highlighting problems with the suitability and affordability of loans for many people, particularly those on a low or moderate income. However, the interviewees often relied on family and friends for information about different credit sources which suggests that financial ecologies remain significant in this respect (Leyshon et al., 2004). Given the nature of products currently available to people, self-exclusion may be the best option and it is one which many of the respondents were trying to practice. However, with the pressures on family budgets, the need to borrow money was often very high as was the encouragement to do so.

Fourth, a key theme running through many of the interviews and was what we have termed the problem of ‘precarious-inclusion’. It is argued that some people are at risk of financial insecurity and over-indebtedness due to increasing variegation of credit markets, the greater reliance on credit to meet every day needs and the tendency for different types of lenders to encourage greater levels of borrowing than some people actually wanted.

Conclusion

This article has used the concept of financial ecologies (Leyshon et al., 2004) to explore the variegation of consumer credit consumption of individuals on a low-to-moderate income. It draws on understandings of the ‘financialization of everyday life’, which shape financial subjects, markets and in the process, and which have begun to redefine the concept of financial ecologies (Leyshon et al., 2004). Drawing on rich empirical research with 44 borrowers, the research has shown how the binaries of ‘super inclusion’/’relic’ financial ecologies fail to reflect the complexity and variegation of credit use.

Following on from Burton (2008), it is suggested, in place of the prime/sub-prime binaries, there is a spectrum of inclusion (Table 2). In general, those higher in the spectrum are wealthier and have access to more appropriate and affordable forms of credit than those lower down. However, this is not always or necessarily the case. Some of those with ‘hybrid’ access to mainstream and alternative forms of credit are in very difficult financial situations which may, indeed, be worsening (hence the transition from prime to sub-prime status). Even those that use neither formal nor informal credit may be managing on their incomes and savings and therefore have no need to borrow. The spectrum is therefore useful but needs to be applied critically, through an understanding of the complex role of credit in people’s lives.

This understanding, through in-depth qualitative research, leads to a number of policy implications about the need for more appropriate financial products and services both within the mainstream and the alternative financial sector. The United Kingdom witnessed major reforms to the regulation of high-cost short-term credit in 2014/2015, including a price cap on payday lending (FCA, 2015), but the mainstream sector has so far remained relatively unreformed despite a CMA report which criticized the lack of competition in the sector and lack of transparency, including overdraft charges (CMA, 2015b). This research is also a reminder, however, that the root cause of difficulties in use of credit is linked to low and insecure incomes (both in and out of work) and this links, in turn, to broader concerns, about the nature of financialization and the particular form of capitalism currently prevalent in the UK (Van der Zwan, 2014). While some people face an impossible task to make ends meet, a focus on financial inclusion in the narrow sense of access to appropriate mainstream and alternative financial products will do little to tackle these more fundamental issues. Given the complexities that have been discussed in relation to the financial variegation within consumer credit markets, further research with individuals considered to be at the financial margins to define new financial ecologies would be welcomed.

Footnotes

Acknowledgements

An earlier version of the paper was presented at the Global Conference on Economic Geography in Oxford, 2015 and we would like to thank Karen Lai and Shaun French for organising the session on the ‘Financialisation of everyday life’. We would also like thank Gary Dymski, Carlos Ferreira, Jane Hardy and two anonymous referees for their helpful and constructive feedback on the paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Arts and Humanities Research Council [grant number AH/J001252/2].