Abstract

We analyse wage developments in Germany during the inflation shock years of 2021–2023 from three perspectives: cost of living, supply-side cost pressure, and relational. With an export-led growth model, Germany is dependent on a favourable real effective exchange rate. Because of its above-average exposure to the energy crisis and low unemployment, Germany was particularly vulnerable to strong wage demands, putting at risk its cost competitiveness. In response to the inflation crisis, moderate collective bargaining outcomes have resulted from widespread use of one-off payments, longer duration of collective agreements, and ‘zero-month’ clauses, which have delayed wage increases. As in all other eurozone countries, employees have suffered real wage losses, but nominal wage increases at the lower end of the labour market fared better than average. Major competitiveness shifts have occurred in the eurozone, particularly to the detriment of Eastern European countries and the Baltics, but not Germany.

Introduction: three perspectives on wages

Germany is highly industrialised by the standards of other developed economies. It is export-oriented, sensitive to shifts in real exchange rates and inflation averse (Baccaro and Höpner, 2022). During 2021–2023, at a time when the unemployment rate was extremely low 1 and labour shortages were felt across many occupations, Germany was disproportionately affected by the imported cost shock induced by Russia’s attack on Ukraine. A combination of price increases and tight labour markets usually gives reason to expect pronounced wage increases. For Germany, this would have implied a break with wage moderation and cost-suppressing dynamics observed since the introduction of the euro. Analysing wage developments since the energy shock is the subject of our contribution.

Our starting point is the conflict of goals that wage negotiators face in wage-setting processes. Wages have several functions in capitalist economies, resulting in different imperatives for wage negotiators, especially (but not exclusively) from the trade unions’ point of view. In normal times, these imperatives are by and large aligned. In the context of an imported cost shock, however, the situation is different. Conflicts between goals increase and collective bargaining partners can no longer meet conflicting requirements simultaneously. In the following, we will distinguish between three such imperatives.

Employees aim to protect their share of value added and must cover their costs of living from their wages. This implies that nominal wage increases, the first imperative, should not fall behind inflation. In the context of sudden price shocks, such stabilisation of real wages also counteracts the contraction of private demand and is therefore macroeconomically important. Real wage stabilisation is particularly difficult to achieve under such conditions, however. First, wage negotiations in collective bargaining take place at different intervals, in Germany typically every two years (a fact to which we will return in some detail). Wage-setters’ response to higher prices only occurs with a delay. Second and more importantly, real wages are fundamentally an endogenous variable: the future rate of inflation is not yet known when a collective agreement is concluded nor is it completely independent of nominal wage increases.

This latter characteristic points to wage-setters’ second imperative. Wages are not only the most important consumption component, but also a cost factor that shapes firms’ pricing (Bobeica et al., 2019; Deutsche Bundesbank, 2019; Di Carlo et al., 2024). Taking this into account, economic theory speaks of a ‘golden rule of wage-setting’, which indicates that, to prevent inflation spillovers and cross-country divergence in wage and price inflation, unit labour costs (total wage costs including social security contributions, adjusted for productivity gains) in a monetary union should rise approximately in line with the central bank’s target inflation (Collignon, 2013; Watt and Koll, 2021). From the trade unions’ perspective, this requirement becomes problematic in the context of sudden price shocks: as the cost of living increases, they are asked to accept real wage losses. Thus, union members are likely to reject the union’s position. Such a rule, therefore, fails to provide a good benchmark in an inflationary scenario like the 2021–2023 one. Nevertheless, higher wages add potentially inflationary cost pressures to the supply side. In our view, the decisive question is therefore not whether wage agreements try to catch up with higher living costs, thereby exerting inflation-prolonging impulses on the economy’s supply side. 2 Rather, the question is how pronounced these impulses are and whether they run the risk of perpetuating themselves into a multi-year wage-price spiral.

The third imperative adds yet another consideration. The group of countries we are interested in here belong to a common currency area in which nominal exchange rate adjustments are no longer possible. In such a constellation, inflation rates need to be synchronised, at least in the medium term, in order not to distort real effective exchange rates (REERs). Given the importance of wages as firms’ input costs, unit labour cost increases should be synchronised in the medium term, too. If different unit labour cost dynamics become entrenched in a monetary union, cross-country variation contributes to fuel current account imbalances, which can destabilise the common currency.

From this relational perspective, Germany is more than just one country among others. First, among other things, the German growth model has taken advantage of a favourable real effective exchange rate (Baccaro and Höpner, 2022). Secondly, as the largest and strongest exporting economy in the eurozone and the EU, Germany has a signalling function for others. If a small country such as the Netherlands practises competitive disinflation, other countries can largely ignore it. If Germany pursues such a policy, Europe as a whole is affected. 3 Other European countries face the choice of either following the German path to disinflation or accepting losses in price competitiveness and thus current account deficits.

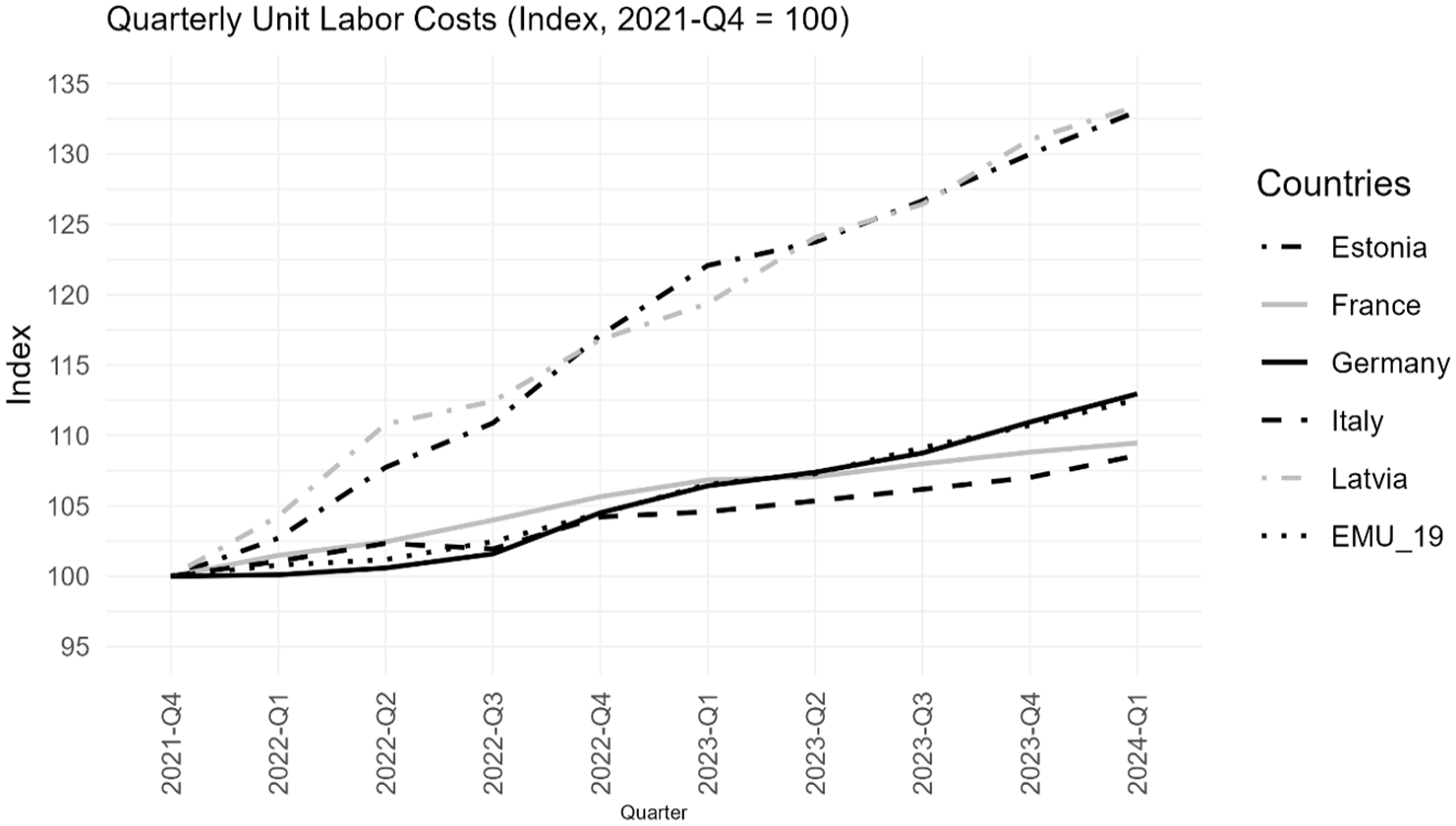

In this article, we analyse Germany’s wage developments during the inflation shock from each of these three angles. From a cost-of-living perspective, there were real wage losses in Germany, as in almost all other inflation-ridden countries (Table 1). But efforts to counteract real wage losses were more effective at the low end of the income distribution than the rest. With regard to the second and third perspectives, outcomes are different from what one might have expected. The shock led to extremely heterogeneous nominal wage increases in the eurozone and to corresponding shifts in REERs (Figure 2). Given its exposure to the shock and its good labour market conditions, one would have expected to find Germany among the countries with high wage pressure and with a corresponding deterioration of cost competitiveness. But this was not the case. Germany was able to defend its favourable competitive position with moderate to low increases in unit labour costs (Figure 1). We interpret these developments as an unexpected resilience of the German export-led growth model.

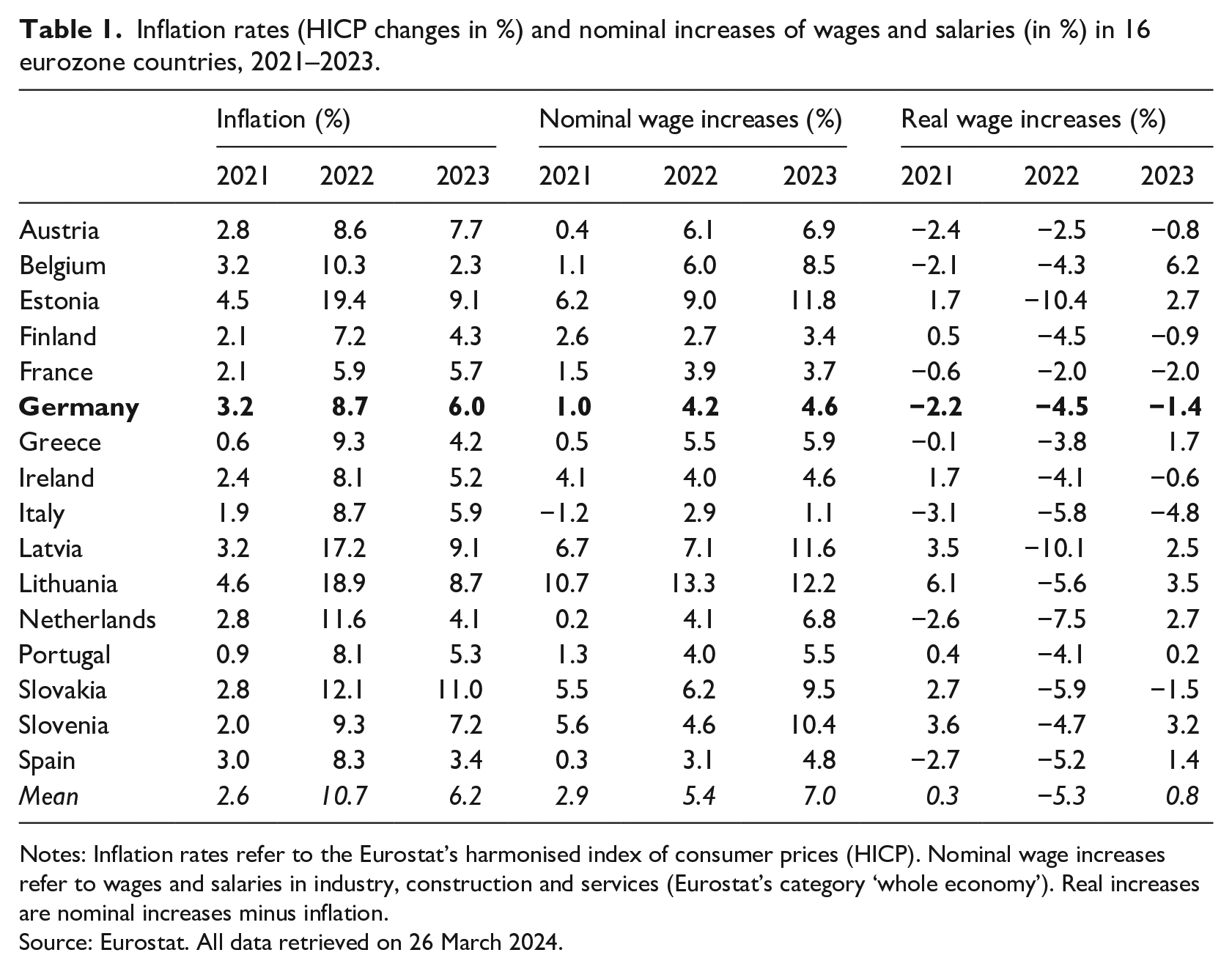

Inflation rates (HICP changes in %) and nominal increases of wages and salaries (in %) in 16 eurozone countries, 2021–2023.

Notes: Inflation rates refer to the Eurostat’s harmonised index of consumer prices (HICP). Nominal wage increases refer to wages and salaries in industry, construction and services (Eurostat’s category ‘whole economy’). Real increases are nominal increases minus inflation.

Source: Eurostat. All data retrieved on 26 March 2024.

Quarterly unit labour costs (employment based). Germany in comparative perspective.

The analysis proceeds in three steps. We first present key features of the German economy as an export-led growth model to highlight the vulnerability of German business in the face of high and growing price inflation. Two empirical sections follow. First, we focus on wage setting in Germany from a comparative perspective within the eurozone. Second, we look at the specific parameters of wage setting in the context of the German government’s fiscal responses. The last section concludes.

The German political economy and the extent of the shock

Recent political economy research describes Germany as an export-oriented economy (Baccaro et al., 2022; Hassel and Palier, 2021). The industrial export sector was traditionally important, but since the launch of the European Monetary Union Germany has developed into an export-led growth model. Germany’s economy draws a high proportion of its growth contributions from export demand, which is unusual for a large country with a large domestic market. 4 This corresponds to a relatively large industrial sector, modest tertiarisation by international standards, and persistent current account surpluses. A variety of institutions and practices on both the supply and the demand side shape these results. Crucially in our context, wage-setting institutions and practices are part of this: Germany has a particular aptitude for wage moderation both in the private (Höpner and Lutter, 2018) and the public sector (Di Carlo, 2023) and thus for defending a REER that is favourable for its large export sector.

Over the past two to three decades, German labour relations have changed considerably (Baccaro and Howell, 2017; Hassel, 1999, 2014; Palier and Thelen, 2010; Streeck, 2009). The core labour force in the industrial export sector continues to be protected by the traditional institutions of the ‘German model’: sectoral collective agreements and co-determination. During several phases of a partly disorganised decentralisation process, however, the importance of the firm level in wage setting has increased in the industrial sector. In contrast, the number of precarious jobs not protected by collective bargaining is still high by international comparison, adding to the labour market’s dualism (Hassel, 2014; Hassel and Palier, 2021). Germany also continues to enjoy a comparatively high degree of industrial peace, together with Japan, Switzerland, Austria, Sweden and the Netherlands. Beyond this, however, it is change, not stability that dominates.

In the Handwerk (skilled trades) and private services sectors, co-determination and collective agreement coverage have fallen sharply. While many European countries counteracted the erosion of collective agreements by means of statutory bargaining extensions (Günther, 2021), collective bargaining coverage in Germany has recently fallen to around only 50 per cent of all employees (Hassel, 2022). Unionisation levels have also fallen sharply to around 16 per cent. In terms of trade union structures, the model of non-competing trade unions organised sectorally remains dominant. Although there are profession-based trade unions in various occupations, such as doctors, railway workers and air transport, Germany has so far been spared a wave of ‘yellow unions’ as in Denmark. Dualisation, however, proceeds not only across different sectors, but also within the industrial sector, where growing lower-paid and less well protected peripheral jobs have spread to the core workforce.

Germany’s economic model was heavily exposed to the shock waves of 2021–2023. This is because the concentration on the production of industrial export products makes it energy-intensive (and emissions-strong), even though energy consumption per capita is not exceptional compared with other EU countries (BP, 2022). When the crisis set in, Germany’s energy mix was not an outlier. Compared with other European countries Germany showed an above-average share of renewables, as well as below-average shares of coal and nuclear energy. Germany’s special feature was an extremely high proportion (59 per cent) of natural gas imported from Russia at the onset of the Ukraine war, a proportion that had increased over time contrary to the international trend. 5 The termination of Russian gas imports as a consequence of Russia’s invasion of Ukraine meant that a large number of new supply contracts had to be concluded under less favourable conditions, resulting in the need to find new suppliers at correspondingly higher costs. 6

German wage increases in the context of the eurozone

Inflation and wage increases in the eurozone

For the purpose of our analysis, we compare data on inflation and wage increases in Germany with other eurozone (EMU) countries. We consider all euro members in 2021, 7 excluding Luxembourg, Malta and Cyprus, three very small countries. Table 1 displays inflation rates for the three years 2021 to 2023, together with nominal and real wage increases.

The price increases that began in the middle of 2021 had already pushed inflation rates in most eurozone countries above the ECB’s target inflation by the end of the year: in 12 out of the 16 countries, the inflation rate was above 2 per cent, with Germany at 3.2 per cent representing an above-average inflation hike. This is a rather unusual position for Germany, historically an inflation-averse country. On average, the data on nominal wage increases for 2021 suggest that inflation did not impact wages. If we assume an average annual medium-term productivity increase of 0.5–1 per cent (Lopez-Garcia and Szörfi, 2021), average wage increases of 2.9 per cent were roughly in line with the imperatives of the inflation-neutral golden rule of wage setting. This is mainly because of the time lag with which wage policy can react to price developments. However, the average hides significant cross-country variation. Wage increases amounted to less than 1 per cent in Austria, Greece, Italy, the Netherlands and Spain, while increases of more than 5 per cent were recorded in all Eastern European EMU members. When discounting for price inflation, across the sample there was a meagre gain in real wages of just 0.3 per cent. Germany, where real wage losses amounted to 2.2 per cent, stands out as a case in which real wage losses were remarkable.

For the years 2022 and 2023, the table shows inflation numbers that Europe had not seen in decades. In 2022, due to Russia’s attack on Ukraine and the cascade of sanctions and counter-measures, average inflation for the countries in the sample skyrocketed to 10.7 per cent, but fell to 6.2 per cent in 2023. These inflation rates, however, not only reflected exposure to the shock, but were also shaped by country-specific policy interventions. France was able to achieve the lowest inflation rate of 5.9 per cent in 2022 and 5.7 per cent in 2023 through the regulation of wholesale energy prices (Plane and Vermersch, 2022), while Eastern European countries all ended up with the highest inflation rates in the sample. Germany’s inflation of 8.7 per cent was 2 percentage points below the average in 2022. But note that the sample’s average is strongly increased by the presence of the high-inflation Eastern European countries. When Eastern Europe is excluded from the sample, Germany (as well as Italy) stood at the upper end of the scale, which highlights their above-average vulnerability to energy shock. In this group of countries, only Belgium and Greece had higher inflation rates. In 2023, Germany’s inflation was quite close to the average.

Nominal wage increases in 2022 in all countries, including Germany, lagged behind price increases, leading to high real wage losses of 5.3 per cent on average, and of 4.5 per cent for German workers. From a cost-of-living perspective these are very bad outcomes. The year 2022 was the third in a row in which German real wages fell, given that real wages had already declined in 2020, too (Destatis, 2023a). The German Statistical Office’s real wage index indicates that German real wages in 2022 stood at similar levels to 2015. In 2023, nominal wage increases exceeded inflation rates on average – but not in Germany where workers suffered from yet another (fourth) year of real wage losses.

From a cost-pressure perspective, nominal wage developments were clearly above the ECB’s inflation target in all countries in 2022, and in almost all countries (except for Italy) in 2023. We do not assume that the entirety of the inflation rates shown in the table were caused by wages. Nevertheless, higher labour costs induced by higher nominal wages may contribute to inflation in the long run. The most striking outcome with regard to the 2022 and 2023 numbers, however, is not the average above the target but the wide discrepancy across countries. 8 Figure 1 uses sample countries to illustrate that the differences between nominal wage increases shown in Table 1 translated into equally large differences between unit labour cost developments. This is because the small differences between productivity developments are hardly significant compared with the much larger differences between nominal wage increases. Unit labour cost developments were, from a cost-pressure perspective, particularly alarming in the Baltic countries.

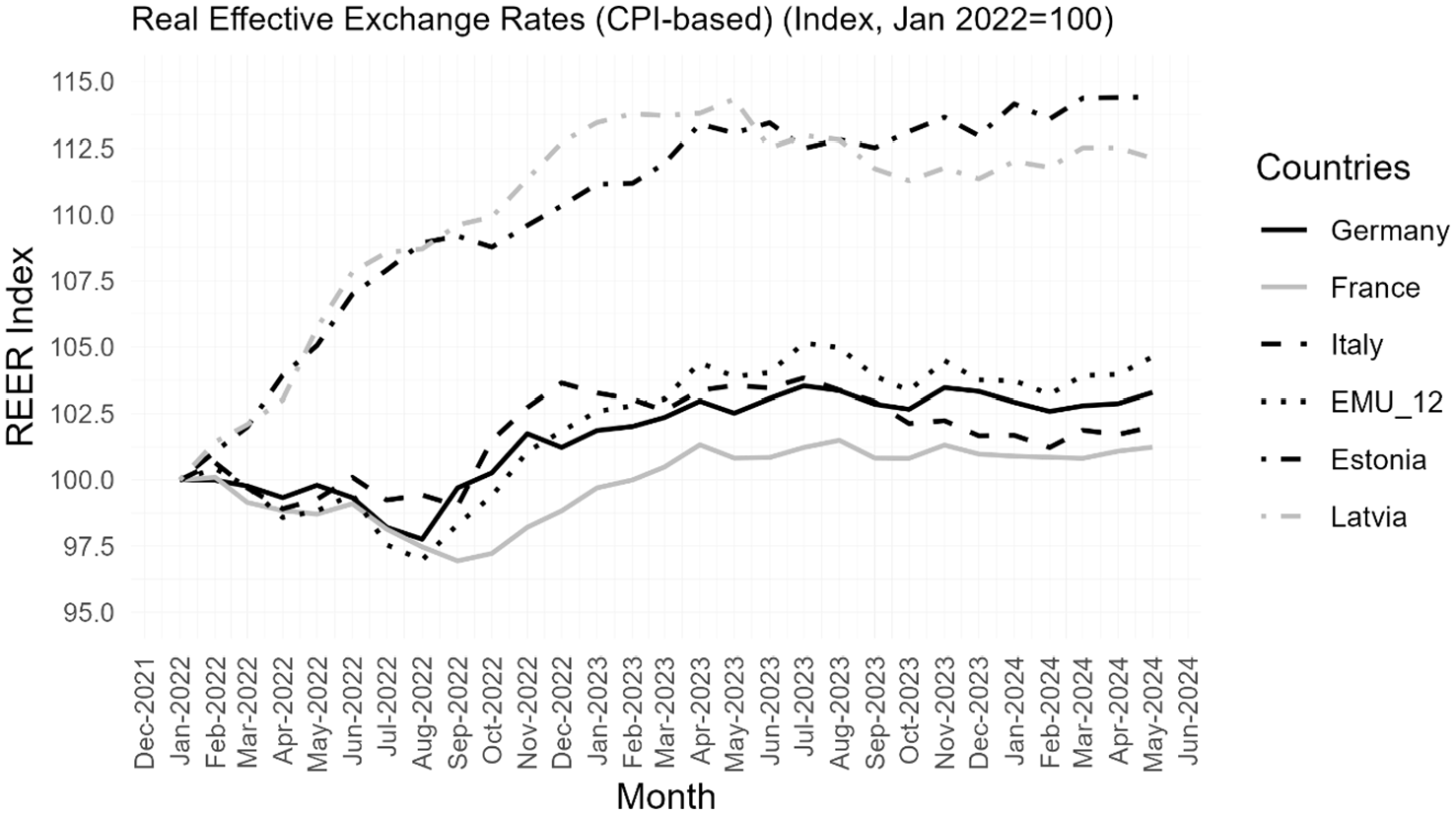

This is relevant especially with regard to our relational perspective. In a common currency, inflation differentials are equal to movements in the real exchange rate, as discussed above. The Bundesbank (Deutsche Bundesbank, 2023: 20) notes that no single year since the introduction of the euro has shaken up intra-European REERs as much as 2022 (Figure 2).

Germany’s real effective exchange rate, based on the consumer price index. Germany in comparative perspective.

Germany’s position with regard to both inflation and wages does not appear exceptional. But it implies that, from a relational perspective, Germany successfully defended its favourable cost-side competitiveness (see also Deutsche Bundesbank, 2023). This holds true not only with regard to Germany’s intra-EMU position, but also with regard to its price competitiveness against the rest of the world thanks to the euro’s weakness since the start of the inflationary period. Against the US dollar, by far the most important currency in international trade, the euro went down from US$1.20 in January 2021 to only US$0.97 in October 2022. The euro had partly recovered by the end of our period of analysis (to US$1.08 in December 2023), but it clearly remained below its long-term average.

Why the German case represents wage moderation

We have argued that wage developments can be viewed from at least three different angles. Each perspective provides different information on whether wage developments qualify as being moderate, neutral or expansionary. From a cost-of-living perspective, all countries analysed here were cases of wage restraint in 2022, and seven of them in 2023. From a cost-pressure perspective, all wage developments were more expansionary than what is generally compatible with the ECB’s treaty-based inflation target in 2022 and 2023 (except for Italy in 2023). From a relational perspective, however, Germany’s position is one of wage moderation within the EMU. In what follows, we make clear why we interpret the German case, irrespective of the contradictory results from the three angles, as a case of wage moderation.

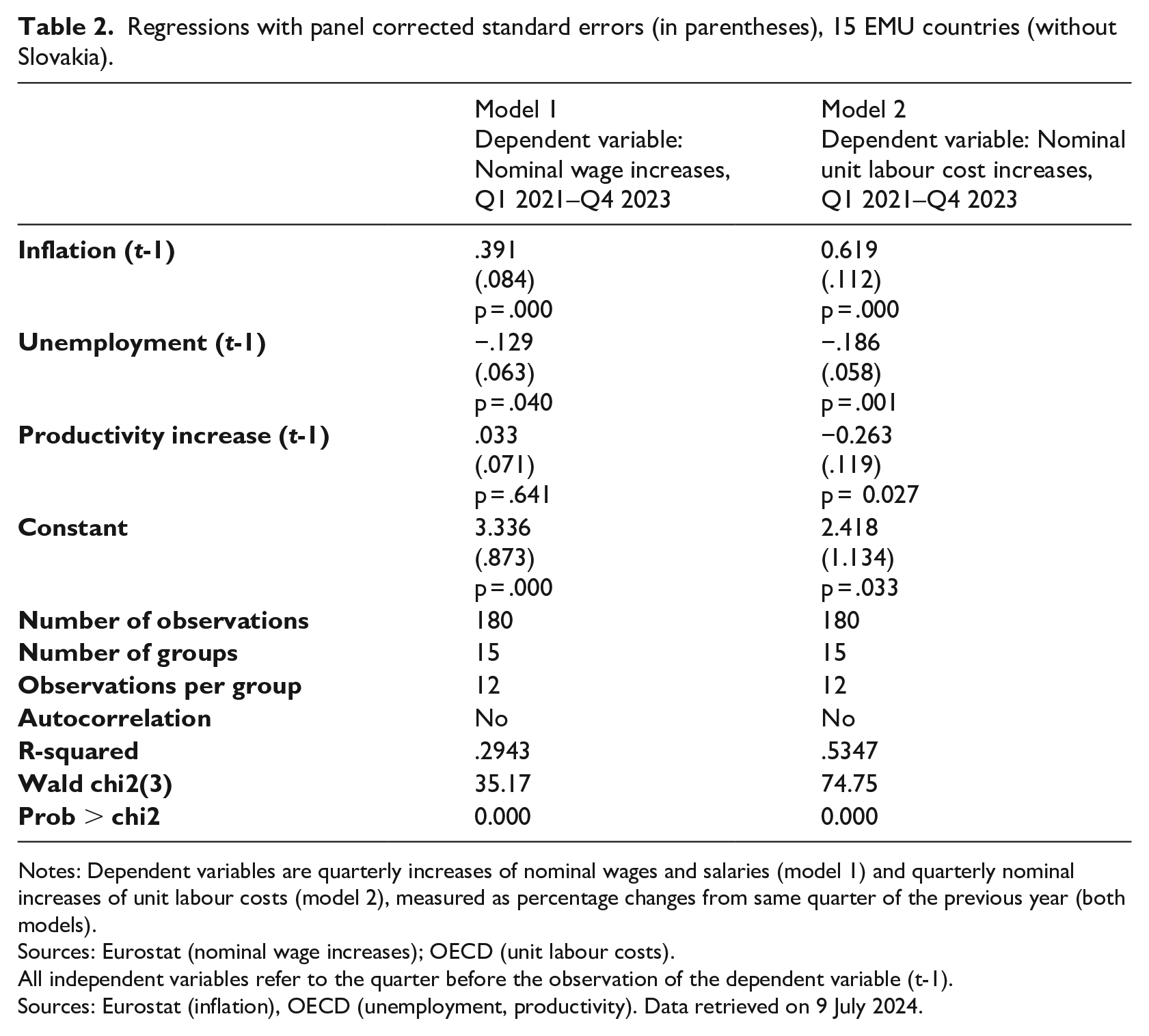

Our interest here lies in knowing how Germany’s nominal wages and nominal unit labour costs have developed relative to what would be expected based on the country’s macroeconomic conditions. To this end, we estimate regressions with panel corrected standard errors (PCSEs) and quarterly nominal increases in wages and unit labour costs (that is, labour costs including social security contributions, adjusted for productivity increases) as dependent variables. These are measured as percentage changes from the same quarter of the previous year. Inflation (t–1, that is, in the previous quarter), unemployment (t–1) and productivity increases (t–1) are the independent variables. As with the dependent variable, all independent variables are measured as changes since the same quarter of the previous year. Slovakia had to be excluded because values for productivity and unit labour costs were missing. The quarters covered are 1/2021 until 4/2023.

The expectation is that inflation will push nominal wage growth and that unemployment will hold it down. The same logic applies to the growth of unit labour costs. In addition, productivity growth should push nominal wage growth. Unit labour costs, by contrast, are already adjusted for productivity growth, so an additional positive influence is not to be expected. Rather, high productivity growth may make unit labour cost restraint easier because in that case real wages can nevertheless rise (or decline less).

All signs of the regression coefficients shown in Table 2 point in the expected directions. The results for inflation are particularly striking. They seem to suggest that wage developments were linked to inflation: the higher the inflation, the higher the wage increases. The coefficients in Table 2 imply that in the period and countries under consideration, 1 percentage point of inflation in the previous quarter translated into 0.4 percentage points higher wage increases and 0.6 percentage points higher increases in unit labour costs. 9 Wage developments linked to price increases contribute to counteracting the cost-of-living crisis and to limiting demand contractions, but can become problematic in a monetary union if, in the medium term, cross-country inflation levels become entrenched at different levels. We will return to this in the conclusion.

Regressions with panel corrected standard errors (in parentheses), 15 EMU countries (without Slovakia).

Notes: Dependent variables are quarterly increases of nominal wages and salaries (model 1) and quarterly nominal increases of unit labour costs (model 2), measured as percentage changes from same quarter of the previous year (both models).

Sources: Eurostat (nominal wage increases); OECD (unit labour costs).

All independent variables refer to the quarter before the observation of the dependent variable (t-1).

Sources: Eurostat (inflation), OECD (unemployment, productivity). Data retrieved on 9 July 2024.

In the eurozone, formal wage indexation is the exception. Such regulations exist in Belgium (Di Carlo, 2021) and in the very small countries of Luxembourg, Malta and Cyprus, which are not included in our sample (European Commission, 2022a: 54). The link between inflation and wage increases shown in Table 2 is therefore less about formal rules than about trade unions taking inflation into account in their wage demands (and in the negotiation outcomes they are prepared to accept). Hybrid mechanisms are enshrined in wage-setting practices and institutions, however, which lie between indexation rules and their absence. For example, indexation clauses can be included in sectoral collective agreements, or minimum wages can be linked to inflation (De Spiegelaere, 2023). Eurofound’s (2023) survey of European social partners indicates that wage indexation is not considered a sensible solution by Germany’s social partners, on either side.

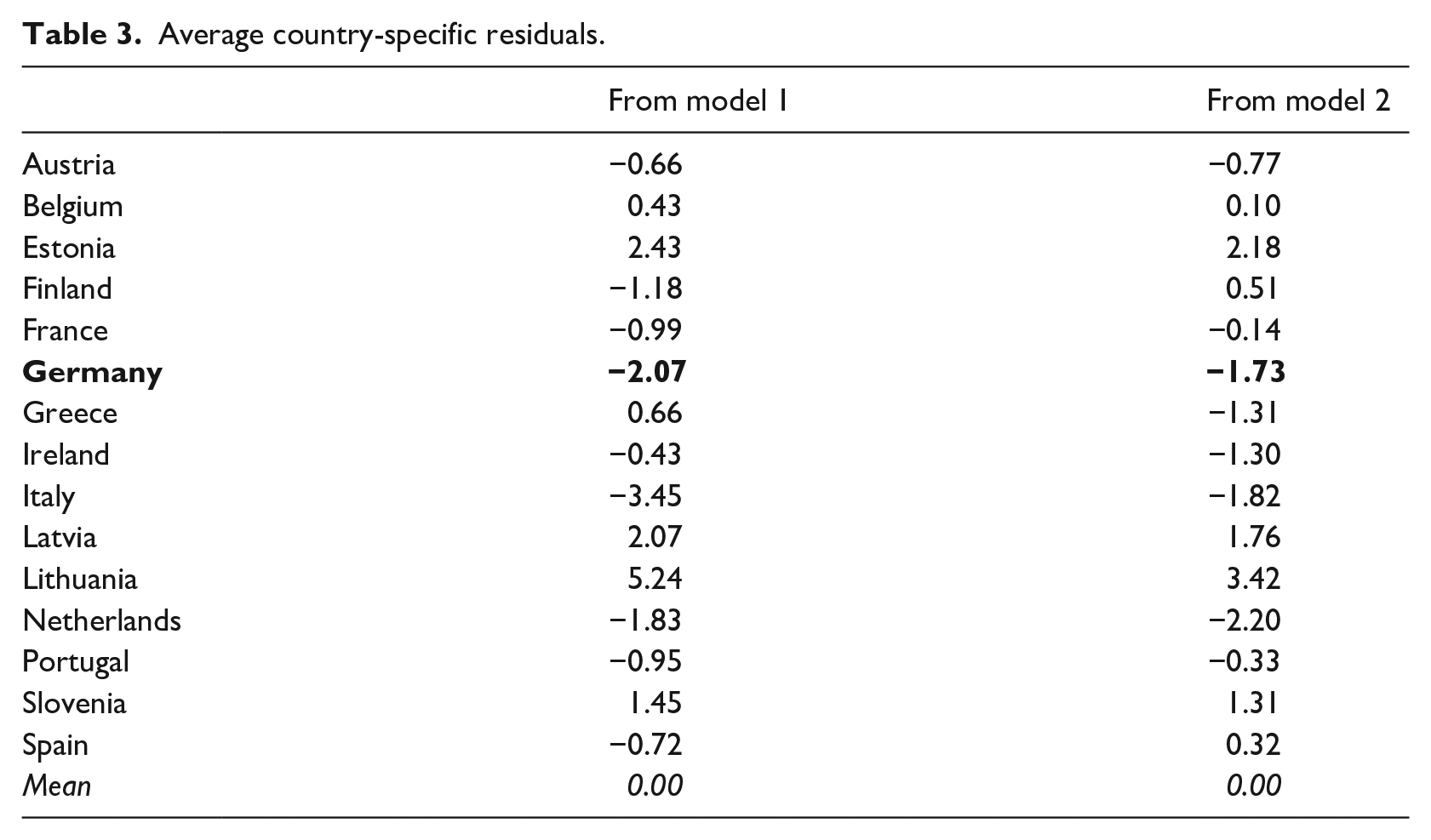

In addition, we are interested in the country-specific residuals of the regression models. They indicate how strongly and in what direction the actual measured country values deviate from the estimated values (Table 3). Germany has negative residuals in both models: the second-largest negative residuals in model 1 (wage increases) and the third-largest negative residuals in model 2 (unit labour costs). This indicates that, during the observed period, Germany experienced nominal increases in wages and unit labour costs that were lower than those one would have expected based on its macroeconomic conditions. This justifies our assessment that Germany played out its capacity for wage moderation. Germany is not an extreme case here, however, but one among several. Italy, Ireland and the Netherlands stand out as further cases of wage restraint in this perspective, in line with the results from Table 1.

Average country-specific residuals.

Wage bargaining in the context of export-led corporatism and fiscal responses to the crisis

Wage bargaining in the context of corporatist responses

In this section we zoom in on German wage-setting dynamics during the period 2021–2023 and discuss how wage moderation was achieved. First of all, it is important to note that wage bargaining in those years took place in the context of cross-class efforts to defend the competitiveness of the large German industrial sector (Di Carlo et al., in press). Germany’s adjustment strategy for the energy crisis has been negotiated and devised through various peak-level meetings in the Federal Chancellery during 2022 to which the government summoned academic experts, Bundesbank representatives and the social partners. The German government opted for social concertation to address the energy crisis.

While officially wage bargaining was not on the agenda of these corporatist meetings, the negotiations nevertheless had a significant impact on wage formation, as we shall see. The government mobilised €157.7bn to shield households and firms from the energy crisis between September 2021 and January 2023 (according to Bruegel data). 10 This amounts to a comparatively large fiscal package, which reflected the country’s favourable public debt refinancing conditions. With regard to fiscal measures to support private households – which in turn also enabled the social partners to accept wage restraint – we have no reason to assume that the subsidies granted were exceptionally high. Most of this help was not targeted specifically towards the poor, but this holds true across most industrialised countries (OECD, 2023: 46). 11

The German government’s economic strategy was exceptional in two respects, however. First, following the Temporary Framework on State Aid passed by the European Commission (2022b) to facilitate the provision of state aid by national governments, Germany made extensive use of its capacity to shield firms (for more details, see Di Carlo et al., 2023). More than 50 per cent of all state aid in the European Union went to German firms in 2022 and the first half of 2023. This points to an extraordinary distortion of competition in the European Single Market. In January 2023, EU Competition Commissioner Vestager published an alarming letter 12 denouncing the asymmetrical distribution of state aid directed to firms in the EU.

Second, the German fiscal response indirectly interfered with wage bargaining. To understand how, we shall turn to the chemical industry, which took the lead in both social partner representation in the corporatist rounds and in wage negotiations. Considering the great uncertainty about inflationary developments brought about by the new scenario in March 2022, the chemical sector trade union IG BCE refrained from specific wage demands. The first regional negotiations ended without results. In the second federal round in early April, IG BCE and the employers agreed on a bridging solution in response to the uncertain macroeconomic developments. The aim was to keep the terms of the previous sectoral agreement valid until October 2022 and, for the short term, concede a one-off payment of €1400 in May 2022 to sustain workers’ real incomes. This amount could also be reduced to €1000 if the firm experienced economic difficulties.

Chancellor Scholz welcomed this compromise and argued that the chemical agreement on one-off payments constituted a ‘very interesting solution’ 13 to help countering rising prices. As part of the third relief package of September 2022, the government decided, in close consultation with the social partners, to subsidise such inflation compensation premia. 14 Pay premia of up to €3000 paid by employers remained exempt from tax and social security contributions, although only until the end of 2024. The only other country in which such a measure was introduced was Austria (OECD, 2023: 47). Below we will look at how these one-off payments were used in practice.

Conflict intensity of wage bargaining

Germany is a low-strike country by international standards (Dribbusch et al., 2023; Vandaele, 2016: 297–282). Long-term trends include a shift in the arena of conflict from the industrial to the service sector and a decline in large-scale, industry-wide strikes in favour of a larger number of smaller conflicts (Müller and Schulten, 2023: 481–483). In terms of Germany’s peaceful industrial relations, the price shock was an interesting natural experiment, as the inflation rate is usually a good predictor of strike activity. 15 Against this background, a significant increase in industrial action could have been expected for the period 2021–2023.

This increase in conflict intensity occurred relatively late, in 2023. In 2021 and 2022, the number of strikes was low, with 9.1 and 6.5 working days lost per 1000 employees, respectively. 16 In line with the trend of previous decades, industrial relations in the chemical sector were particularly peaceful. The employer Institute of the German Economy (IW) publishes biannual reports in which, among other things, the intensity of conflict in collective bargaining is analysed and measured. The advantage of these data is that they also record the level of conflict besides strike activity, such as the duration of the collective bargaining process. The data confirm the low level of conflict. By the end of 2022, collective bargaining was recognised as ‘largely harmonious’ and the results of the wage rounds were acknowledged as ‘extremely consistent with stability’ (Lesch and Eckle, 2023a: 4, our translations; compare also Lesch and Winter, 2022 and Lesch, 2022). 17

The level of conflict and the number of strikes increased significantly during 2023 (Lesch and Eckle, 2023b, 2024; Schulten, 2024). Labour disputes were concentrated in the domestic services sector. Wage disputes were particularly conflictual in the wholesale and retail sectors, as well as at Deutsche Bahn and in the federal and local public sector. 18 In the course of the conflicts, the service trade union ver.di saw a significant increase in membership. 19 In a broader historical context, however, the increase in the level of conflict was rather moderate. At the time of writing, only estimates of the number of strikes in 2023 are available. These indicate that there were fewer strikes this year than in 2015, the last year with pronounced wage disputes (Dribbusch et al., 2024: 5). Also, in 2023 most strikes were warning strikes and not enforcement strikes (Erzwingungsstreiks). 20 This result also supports the finding that Germany came through the inflation shock years in a comparatively cooperative manner.

Long duration of agreements, one-off payments and zero-months

The duration of collective agreements is not regulated by law in Germany, but determined solely by the signatory parties. Until the early 2000s, German agreements had a one-year term, but over the past two decades Germany has joined the group of eurozone countries in which two-year durations are normal, as in Belgium and Finland (OECD, 2023: 58). 21 In contrast, annual negotiations remain typical for Austria, Estonia, France, Ireland, the Netherlands, Portugal, Slovakia and Slovenia. Longer durations are predominant in Greece and Italy (on these cases, see Tassinari et al., 2024; Theodoropoulou et al., 2024).

The 41 most important collective agreements concluded in 2021–2023 listed online by the trade union’s Institute of Economic and Social Research (WSI) can be used to analyse the duration in more detail. 22 The average duration of these collective agreements was 23.8 months (median: 24 months). The longest duration was 35 months for two wage agreements in public and private banking. Collective agreements in the domestic sector had a slightly longer average duration (25.9 months) than collective agreements in the export sector (22.8 months). The domestic sector is also characterised by great variation in the duration of agreements compared with the export sector. Longer collective bargaining agreements are favoured by employers because they provide firms with certainty about the future cost of labour and therefore greater economic stability and planning capacity. 23

The long duration of agreements also allowed for the use of one-off payments in a particularly creative way. One-off payments are not new, but were used extensively in the inflation shock years. Both sides benefit from relief from taxes and social security contributions, which also reduces unit labour costs because such contributions are part of labour costs. They have no particular wage-suppressing effect in the first round. But they do have the effect of contributing to future wage moderation. The long-term effect comes about because the next percentage wage increases in this case are based on the wages as laid down in collective agreements excluding the one-off payments. This effect accumulates over the years. 24 Of course, the collective bargaining partners on both sides are aware of this effect and could circumvent it with higher percentage increases in the next round if they wanted to. However, one of the effects of one-off payments is that they might make future wage restraint easier to communicate.

One-off payments were chosen extensively by the collective bargaining parties. This is in contrast to Austria, where the government offered them a similar subsidy (OECD, 2023: 47). Austrian trade unions made little use of this because they recognised one-off payments as unfavourable for employees (Zuckerstätter et al., 2022: 13). Depending on the sector, German collective bargaining parties handled the instrument quite differently. The €3000 were almost always used in full. Very often, they were not granted in addition to the wage increases affecting the pay scale, but as a substitute for them. In these cases, the one-off payments were paid out first in one or more stages, followed by the percentage wage increases, a strategy that works only if terms are long. In these cases, the percentage wage increases were preceded by zero-months without increases affecting the wage table. The number of these zero-months varied greatly. As far as one can observe from the available data, the highest number of zero-months was in the collective agreement for federal and municipal public employees, which was concluded on 24 April 2023: It envisaged 14 zero-months before the first percentage wage increase would become effective. 25

Communicating wage settlements

The combined effect of long contractual durations, one-off payments and zero-months facilitated the public presentation of moderate agreements. Two-year agreements have become standard in Germany, while wage demands continue to be formulated on an annual basis (Schulten, 2023: 5). This discrepancy creates confusion. If one compares the demand and the result, it looks as if the trade unions have largely prevailed – which of course is not the case if the term of the collective agreement is twice as long as the period to which the original demand related. If we add one-off payments and zero-months to the picture, confusion over the actual rate of wage developments increases even more. Even the best experts found it very difficult to present the complex wage settlements at annualised rates during the analysed period. This gave the public the impression of generous wage agreements, which failed to recognise the true extent of wage moderation.

To illustrate this, the metal and engineering industry agreement 26 agreed on 17–18 November 2022 was among the most important in our observation period. IG Metall’s wage demand was 8 per cent, as always in relation to one year. ‘Wage increase of more than eight per cent – and a one-off payment of €3000’ was the headline in a political magazine (our translation). 27 In fact, the agreement related to two years, not one; the ‘more than eight per cent’ was the result of 5.2 per cent in the first year and only 3.3 per cent (!) in the second year; and the first increase to take effect on the pay scale was preceded by eight zero-months. In short, the actual content of the agreement and the way it was presented by the media had little to do with each other.

Trade unions and employers’ organisations did not correct such misreporting because the social partners on both sides lacked the incentive to characterise the agreements accurately. Trade unions aimed to signal that they had done everything to compensate for past real wage losses, while for the employers such corrections would have paved the way for employee demands for higher increases in the future, or instigated wage drift. Thus, if the aim was to decouple talk and action, the combination of long-term contracts, one-off payments and zero-months was ideal.

Progress in the protection of low-wage earners

Apart from the rather ambivalent aspects, one feature of the German wage development under analysis here is clearly encouraging: wage increases for low-wage earners were higher than the rest, which caused a significant shrinking of Germany’s low-wage sector (defined as the number of employees earning below two-thirds of the median wage), from 19 per cent in 2022 to 16 per cent in 2023 (Destatis, 2024). This should be seen in its historical context. In the first decade of the new millennium, the growth of the low-wage sector was seen as a successful policy to combat unemployment. The sector grew from 19 per cent of total employment in 2000 to 24 per cent in 2007 and was therefore clearly oversized by European standards. The size of the sector remained more or less constant until 2017, before trending downwards and then falling significantly from the end of 2022 onwards (Grabka, 2024: 67). This implies that the rise of the low-wage sector that started in the 2000s has finally been corrected.

This can be due to either intra-sectoral or inter-sectoral developments. Both kinds of development occurred. Within sectors, the extensive use of one-off payments benefited people on lower incomes. As they were paid as the same lump sum for all employees, they led to higher percentage increases in low-wage groups. 28 The same effect was achieved by minimum payments in some collective agreements, complementing percentage wage increases. This applied, for example, to the particularly important collective agreement for federal and municipal public employees, which was concluded in April 2023. In this agreement, the percentage wage increases after five zero-months amounted to 5.5 per cent, but at least €340. Similar deals occurred at Deutsche Post AG (collective agreement dated of March 2023) and in the textile and clothing industry (collective agreement of April 2023).

Moreover, in inter-sectoral terms, wages in the low-productivity service sectors, such as hospitality, were able to catch up with the high-productivity sectors. The same holds true for the agricultural sector. 29 The OECD (2023: 36–38) compared country-specific wage trends in the years 2019–2022 in sectors with low, medium and high wage levels. In 16 of the 32 countries analysed, wage growth was highest in the low-wage sectors. 30 This includes Germany, where the study shows real wage gains for employees in low-wage sectors. 31 According to Herzog-Stein and Stein (2023: 12), the catch-up effect for the low-wage sectors was more pronounced in Germany than the eurozone average.

But note that this catching up was caused not by stronger trade unions in the low-productivity private service sectors, or by higher collective agreement coverage in these sectors (for example, by increased use of statutory bargaining extensions – see Günther and Höpner, 2023). Rather, two other developments were the cause. First, in the areas that are increasingly unprotected by collective agreements in Germany, wage development is determined by market conditions rather than agreements between the collective bargaining partners, and these have improved for low-wage earners due to increasing labour shortages in Germany. Second, on 1 October 2022 the largest increase in the minimum wage to date (to €12) 32 came into force in Germany. 33 Around 5.8 million employees benefited from this (Destatis, 2023b), particularly in hospitality, as well as in the hairdressing, building cleaning, security and bakery trades (Schulten, 2023: 15–17).

Conclusion

The results illustrate that wage setting should be seen as an integral part of the German export-oriented economy. In the wake of the inflation crisis of 2021–2023, German policy shifted to social concertation led by the chemical, metal and engineering sectors (Di Carlo et al., in press). The aim was to defend the cost competitiveness of German export companies. In the course of this adjustment, the state intervened indirectly in wage setting by exempting one-off payments from taxes and social security contributions.

German wage bargaining contributed to holding the country’s competitive REER approximately constant. Given the good labour market situation, higher wage increases could have been expected. It was only late in our observation period, in 2023, that the level of conflict in wage negotiations increased decisively. The true extent of wage restraint was not transparent for the public because of the combination of long collective agreement terms, zero-months and one-off payments. Above-average wage increases have instead been achieved at the lower end of the labour market. This was largely, but not solely because of the increase in the minimum wage to €12 in October 2022 and lump-sum wage increases. As a result, the rapid growth of the low-wage sector during the first decade after the turn of the millennium was – finally – corrected.

In this article, we have compared German developments with those in the rest of the eurozone. With regard to the common currency, the strong correlation between inflation and nominal wage increases is particularly noteworthy, despite the absence of formal wage indexation rules: the higher inflation was, the higher the nominal wage increases. With regard to the stabilisation of real wages, this is surely good. But this also means that additional cost pressure was imposed on firms precisely where inflation was already high. The energy price shock of 2022 and 2023 subsided more quickly than expected. 34 If price shocks last longer, the close correlation between price and wage developments in a currency area – in which nominal exchange rate corrections are no longer possible – is problematic. This is how the euro crisis emerged towards the end of the first decade of the new millennium (Scharpf, 2021). Eurozone members remain caught in a difficult monetary structure with limited capacity to respond to asymmetric shocks.

Footnotes

Acknowledgements

We thank Janis Jurgeleit and Konstantinos Papanikolaou for their superb research assistance.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

1

In mid-2022, Germany’s harmonised unemployment rate (Eurostat harmonisation) was only 3.0 per cent. This was the second lowest unemployment rate in the eurozone, after Malta.

2

If nominal wage increases exceed target inflation, they can nevertheless still have an inflation-reducing effect on the demand side: if real wage stabilisation does not succeed, demand will fall and, other things being equal, so will inflation.

3

The same logic applies to fiscal policy: Fiscal restraint in a small country is of little relevance to the other eurozone members. But if Europe’s largest economy exercises fiscal austerity, this has an impact on Europe as a whole.

4

Between 1996 and 2018, an average of 69 per cent of German growth contributions came from export demand (see the data in Baccaro and Höpner, 2022: 241).

5

6

Even if world market prices had not risen sharply in the period under review, the switch to the much more expensive liquified natural gas would have led to sharp cost increases.

7

Croatia joined the euro on 1 January 2023.

8

This also illustrates the complete absence of anything that could legitimately be described as transnational European wage coordination, in stark contrast to the myths cultivated by European trade unions (compare Höpner and Seeliger, 2021).

9

This effect applies in terms of both country and time variance: wage and unit labour cost increases were higher when and where inflation was high.

11

14

The German term is Inflationsausgleichsprämie.

15

In the German data for the years 1991 to 2019, we find a strong correlation between the inflation rate and the number of strike days per 1000 employees (Pearson’s r=.72).

17

18

See Di Carlo (2020, 2023) and Keller (2011) on collective bargaining in the German public sector. For more details on industrial relations in the German public sector, see ![]() .

.

19

Data source: German Statistical Office (https://de.statista.com/infografik/31808/anzahl-der-mitglieder-in-den-gewerkschaften-des-deutschen-gewerkschaftsbunds/#:~:text=Die%20H%C3%A4lfte%20der%20im%20Deutschen,vergleich%20zum%20Vorjahr%20einen%20Mitgliederzuwachs, accessed 29 February 2024). On the membership increase in 2023, see ![]() : 9).

: 9).

20

A ballot among trade union members was held at Deutsche Post for an indefinite enforcement strike, but the conflict was resolved before the strike could begin. The only enforcement strikes we are aware of in the 2021–2023 period were conducted by profession-based trade union Cockpit and dealt with wages for pilots at Deutsche Lufthansa and Eurowings (see Lesch and Eckle, 2024: 18).

22

Data source: Wirtschafts- und Sozialwissenschaftliches Institut (https://www.boeckler.de/pdf/p_ta_forderungen_abschluesse_2021.pdf; https://www.wsi.de/data/p_ta_forderungen_abschluesse_2022.pdf; ![]() ) (accessed 29 February 2024).

) (accessed 29 February 2024).

23

Long durations of agreements in the context of sudden inflation shocks take the form of risky bets on future inflation. If inflation rises during longer collective agreements, wage deals turn out to be more moderate than intended. However, the opposite result can occur as well if inflation falls sooner and/or more than expected. Towards the end of 2023, many were surprised by the rapid easing of the inflation shock. Under such conditions, even moderate agreements can result in an unexpected real plus for employees.

25

Another strategy was not to grant one-off payments in one to three steps, but to spread them out over many months. This was the case, for example, with the collective agreement for Deutsche Post (agreed in March 2023) and the public sector collective agreement in the Länder (December 2023).

26

With around 3.9 million employees.

28

In this way, the public subsidies for one-off payments had a progressive (that is, compressing) effect on the income distribution. But note that the subsidy in isolation was, paradoxically, regressive (!): the higher someone’s income, the larger the tax burden that would otherwise have been paid on the one-off payments.

29

In general, wage increases in the domestic sector tended to be higher than in industry, which mirrors the respective conflict intensities. But there are exceptions to that rule. Above all, wage developments lagged behind in the conflict-ridden wholesale and retail sector. Wage increases were also modest in construction. For detailed data see Table 4 in ![]() : 28).

: 28).

30

The low-wage sectors performed worst in only four countries: Belgium, Estonia, the Netherlands and Sweden.

31

However, it remains open whether this result would remain the same if the household-specific inflation rates of low-income earners were considered. Because food and energy account for a higher proportion of the total expenditure of low-income households (Watt, 2022: 5–7), they had to cope with higher price increases than others.

32

For country comparisons of the minimum wage increase during the inflation period, see European Commission (2022a: 68) and ![]() : 49–54).

: 49–54).

33

However, in exchange, the German minimum wage increase of 2023 was among the smallest in the EU (see the data in Lübker and Schulten, 2024: 14).

34

The shock did not trigger substantial wage-price spirals, at least in the western European Member States of the eurozone. Even in Belgium, a country with formal wage indexation, inflation fell rapidly despite substantial wage increases in 2022 and 2023 (compare ![]() ), meaning that no further second-round effects are expected for subsequent wage rounds. In our opinion, it should not be concluded from this that there is no risk of wage-price spirals in the eurozone. Longer-lasting price shocks would presumably bring about different results.

), meaning that no further second-round effects are expected for subsequent wage rounds. In our opinion, it should not be concluded from this that there is no risk of wage-price spirals in the eurozone. Longer-lasting price shocks would presumably bring about different results.