Abstract

This article compares the policy and collective bargaining responses in the three Scandinavian countries to the cost-of-living crisis that began in 2021. The countries are known for their coordinated and consensual response to exogenous shocks. However, Scandinavian variants of neoliberal reforms, the 2009 Financial Crisis and, more recently, the COVID-19 pandemic have challenged the model. The comparative analysis finds three things. First, Norway and Sweden opted for rather generous measures compared with Denmark, and their measures were generally universal in nature, whereas the Danish measures were more targeted on specific groups. Second, with no statutory minimum wage, all three countries relied on collective bargaining to shore up wage incomes. Third, the different responses in the three countries pertain to different political and economic problem loads. We also find signs of convergence as wage solidarity seems to be experiencing a revitalisation in all three countries. This could have lasting effects on bargaining systems.

Introduction

This article compares the policy and collective bargaining responses to the cost-of-living crisis in the three Scandinavian countries Denmark, Norway and Sweden. The three countries are known for their coordinated and consensual responses to exogenous shocks. Indeed, the so-called ‘Nordic model’ was established in times of crisis (Andersen et al., 2014; Katzenstein, 1987; Martin and Swank, 2012). Institutionally, the basic tenets of the model are a generous and universal welfare state, together with coordinated collective bargaining between highly organised social partners. These institutional tenets seek to strike a balance between various policy goals. First, between the competitiveness of exporting companies and real wage increases of workers. Second, between flexible and dynamic markets and income equality. Third, between fiscal soundness and generous welfare states that ensure social security. While Scandinavian variants of neoliberal reforms, the 2009 Financial Crisis and recently the COVID-19 pandemic have challenged the model and shifted the balance between policy goals over time, most scholars’ overall assessment is that the basic tenets of the model have survived (Alsos and Nergaard, 2021; Andersen et al., 2014; ILO, 2022).

How did the countries respond to the 2021 crisis in terms of public policy and collective bargaining and what might explain the differences? In answering these questions, we pay particular attention to the following issues. First, what were the political and economic problem loads in the three countries and how did governments and social partners interpret the cost-of-living crisis, including the risk of wage-price spirals? Second, were policy responses universal or targeted and how generous were they? Third, how was the challenge of shoring up incomes handled and were particular groups favoured over others?

The comparative analysis finds three things. First, the public policy responses differed in generosity and type. Norway and Sweden opted for rather generous measures compared with Denmark, and their measures were generally universal in nature, whereas the Danish measures were more targeted on specific groups. Second, in the absence of a statutory minimum wage, all three countries relied on collective bargaining to shore up real wages, which were hit hard in 2021–2022. In all countries, unions focused particularly on helping low-wage workers, which signalled a revitalisation of wage solidarity, not least in Denmark, where the low-wage strategy has been weak for many years. In Norway, the strengthened low-wage focus led to strikes in the private sector, the first in many years in a mid-way settlement. Importantly, we find revitalisation of wage solidarity in collective bargaining across all three countries. Third, we explain the differences, however subtle, in responses in terms of different political and economic problem loads in the three countries. Denmark was the least affected by the crisis. Looking forward, it remains open whether the revitalisation of wage solidarity was specific to the crisis or constitutes a strategic convergence for unions in Scandinavian industrial relations that may usher in bargaining centralisation in the future.

Literature: the politics of inflation in Scandinavia

The Scandinavian countries are known for large government sectors, generous social protection, high tax rates, an emphasis on active labour market policy, a high degree of unionisation, and highly coordinated wage bargaining (Calmfors et al., 2007). Although the three countries’ industrial mixes differ – Norway being a major oil producer – all rely on exports for economic growth. However, they have managed to balance the need for export competitiveness with high wages and a large public sector (Høgedahl et al., 2024). Key to this success is heavy investment in productivity enhancement through human capital investment, as well as production for niche markets (Baccaro and Pontusson, 2016). Some have referred to the ‘Nordic Miracle’ of full employment, competitive companies, real wage increases and high social protection (Calmfors et al., 2007). Another key ingredient in the Nordic Miracle is the countries’ capacity to deliver coordinated responses to economic crises (Andersen et al., 2014; Katzenstein, 1987). The high level of coordination is typically explained with reference to consensual politics across the political parties. In addition, both employer associations and trade unions are encompassing and thus able to pursue societal rather than special interests (Andersen et al., 2014; Calmfors and Driffil, 1988; Olson, 1982).

The current model originates from the institutional transformations in the 1980 and 1990s, which occurred in response to bouts of stagflation (stagnation and inflation) and – especially in Denmark – industrial unrest following the OPEC crises of the 1970s. Governments in the 1970s and 1980s used currency devaluation to increase competitiveness, but this beggar-thy-neighbour strategy only fuelled more inflation and did not improve competitiveness. Employers, especially in exporting sectors, argued that centralised bargaining had run its course because wage drift at lower levels undermined wage moderation. This interpretation was shared by many unions representing workers in exporting companies, wary of losing competitiveness while not enjoying any real wage increases as a result of inflation (Due et al., 1994; Pontusson and Swenson, 2000).

Realising the failure of competitive devaluations and second-round wage inflation, the 1980s and 1990s brought a stronger focus on fiscal balance and tightening of monetary policies to bring down inflation to the 2 per cent target. In line with this goal, social partners pledged to moderate nominal wages and successfully reformed and revitalised coordinated wage bargaining from centralised bargaining to industry-level bargaining around the pattern set in manufacturing. These new strategies were carved out in social pacts – as seen in EMU countries – which appeared in Denmark in the Fælleserklæring of 1987 and in Norway in the Solidaritets Alternative in 1992, but was absent in Sweden (Dølvik and Martin, 2000). Instead, social partners in Swedish manufacturing agreed ‘Industriavtalet’ in 1997 to cement their key bargaining role. But it was not until 2000 when the new Mediation Agency was established that the state undergirded the new bargaining system (Elvander, 2002). The systems, contested at first, moderated nominal wage demands by trade unions and now focused on real wages and export competitiveness, as exports constitute an increasing share of economic growth.

All countries retained their own currencies, but only Denmark follows a fixed exchange rate policy, pegging the Danish krone to the euro to ensure exchange rate stability and to control imported inflation. In contrast, Norway and Sweden adhere to a floating exchange rate, enabling them to absorb external shocks and maintain competitive export markets through devaluations, but also putting them more at risk of importing inflation.

In the absence of a statutory minimum wage, it falls on the social partners (especially unions) to maintain high bargaining coverage and decent minimum wages in collective agreements. Unions in all countries have historically favoured compression of the wage structure by ensuring that wage increases are more or less uniform. In recent decades, however, decentralisation of wage bargaining to workplace level has allowed for more wage differentiation and with it larger wage discrepancies (OECD, 2024). In Sweden and Norway, unions have consequently devised ‘low-wage strategies’ that focus on allotting higher (percentage) wage increases for low-wage workers to ensure they do not fall too far behind. More research is needed to show the success of these strategies, which were largely absent in Denmark until 2023 (Ibsen and Thelen, 2017).

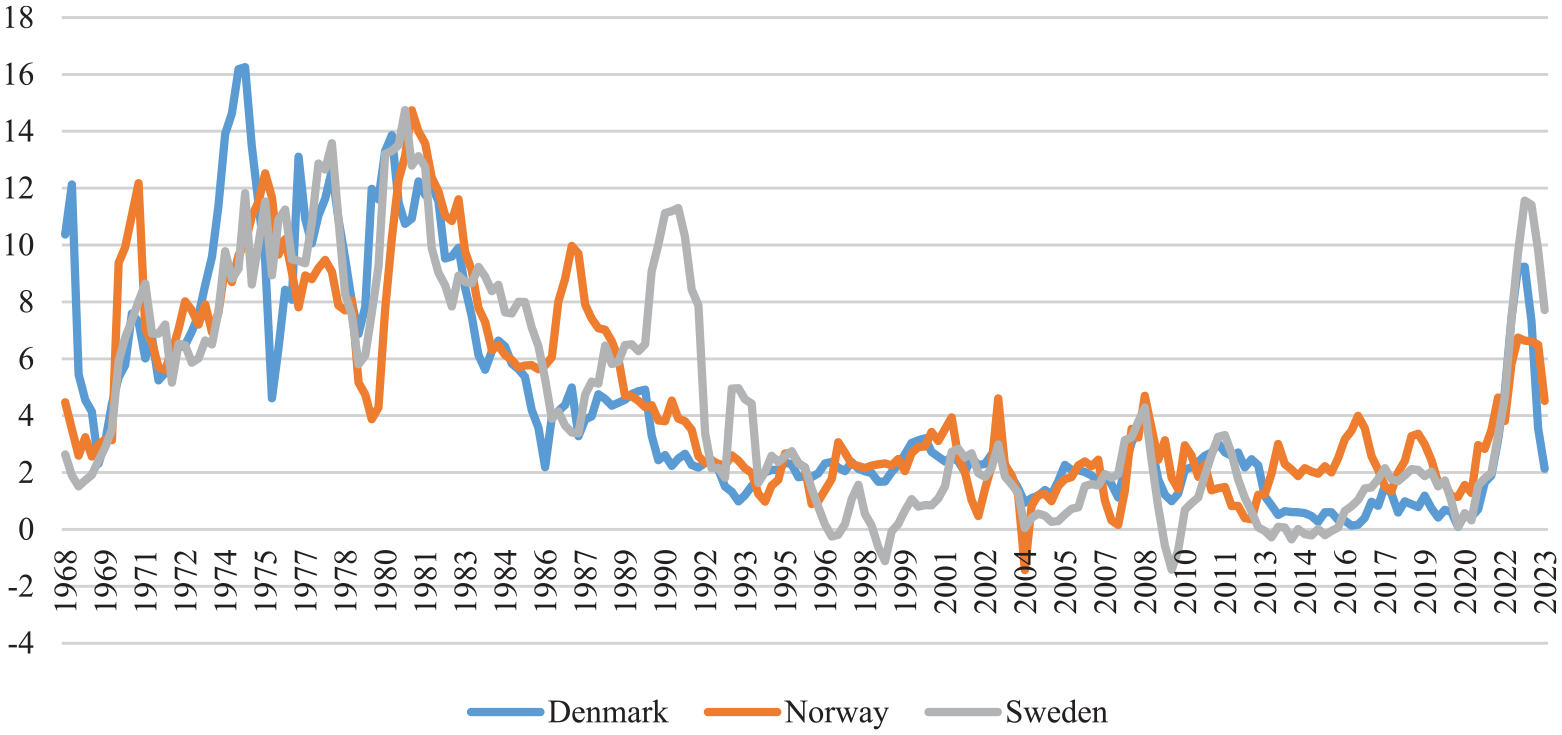

Looking at inflation developments (see Figure 1), the new regime has worked well for the average Scandinavian worker. From 2000, average annual real wages rose consistently in the three countries until 2022, except in 2016 in Norway (OECD, 2024). Evidently, occupational differences exist, but the general interpretation among unions, employer associations, economists and politicians is that the current wage-bargaining regime works and produces the appropriate balance between wage moderation, real wage increases and wage equality (Alsos et al., 2019; Andersen et al., 2014; Bender, 2024). Recently, concerns over the incidence of low wages have ignited calls for targeted wage increases in all countries, but most strongly in Sweden and most weakly in Denmark (Ibsen and Thelen, 2017). Concomitantly, gender wage inequality linked to wages in female-dominated welfare service occupations, such as nursing and child care, has spurred the unions of these workers to call for higher wage increases (Hansen and Mailand, 2024; Wagner and Teigen, 2022). However, these calls may conflict with the tight coordination around the manufacturing pattern, based on percentage rather than nominal increases. Finally, leading into the 2021 cost-of-living crisis, cracks appeared in the models due to the rise of atypical work and the incidence of low-paid migrant workers, as well as, in Sweden, persistently high unemployment.

Inflation (CPI) total, annual growth rate (%), Denmark, Norway and Sweden, Q1 1968 to Q3 2023.

Another development across the Scandinavian countries has been the gradual transformation of the welfare state towards tighter access to benefits, more targeting and lower benefits. Many reforms have been aimed at activating the unemployed and making long-term unemployment less economically attractive. However, in-work benefits to motivate employment – as seen in other countries – are not common in Scandinavia (Pedersen and Picot, 2023). While reforms have gone far (Korpi et al., 1998), they have not dismantled the Nordic welfare states, which are still more redistributive and universalist than those of other countries (Jacques and Noël, 2021). The COVID-19 pandemic represented something of a deviation from universalism as some relief policies targeted groups of citizens and businesses particularly affected by lockdowns. Moreover, there is some evidence of so-called ‘targeting within universalism’, where specific vulnerable groups get extra help (Jacques and Noël, 2021). However, there are also cases of ‘welfare chauvinism’, under which eligibility and benefit levels are tightened for particular migrant groups. As such, the cost-of-living crisis could elicit targeted responses to particularly vulnerable groups or businesses.

In sum, the current Nordic model is in many ways a response to previous periods of inflation in the 1970s to 1990s. Three main points can serve as a historical reference point for analysis of the 2021 inflation crisis:

– The 1970s–1990s inflation crises were perceived as causing wage-price inflation spirals, which had to be managed by monetary and fiscal tightening, as well as wage moderation.

– The responses were institutional in the sense that they entailed transformation of both collective bargaining and public policies.

– Collective bargaining on wages was decentralised to a pattern-bargaining system based on agreements in the export manufacturing sector and leaving room for company-level bargaining.

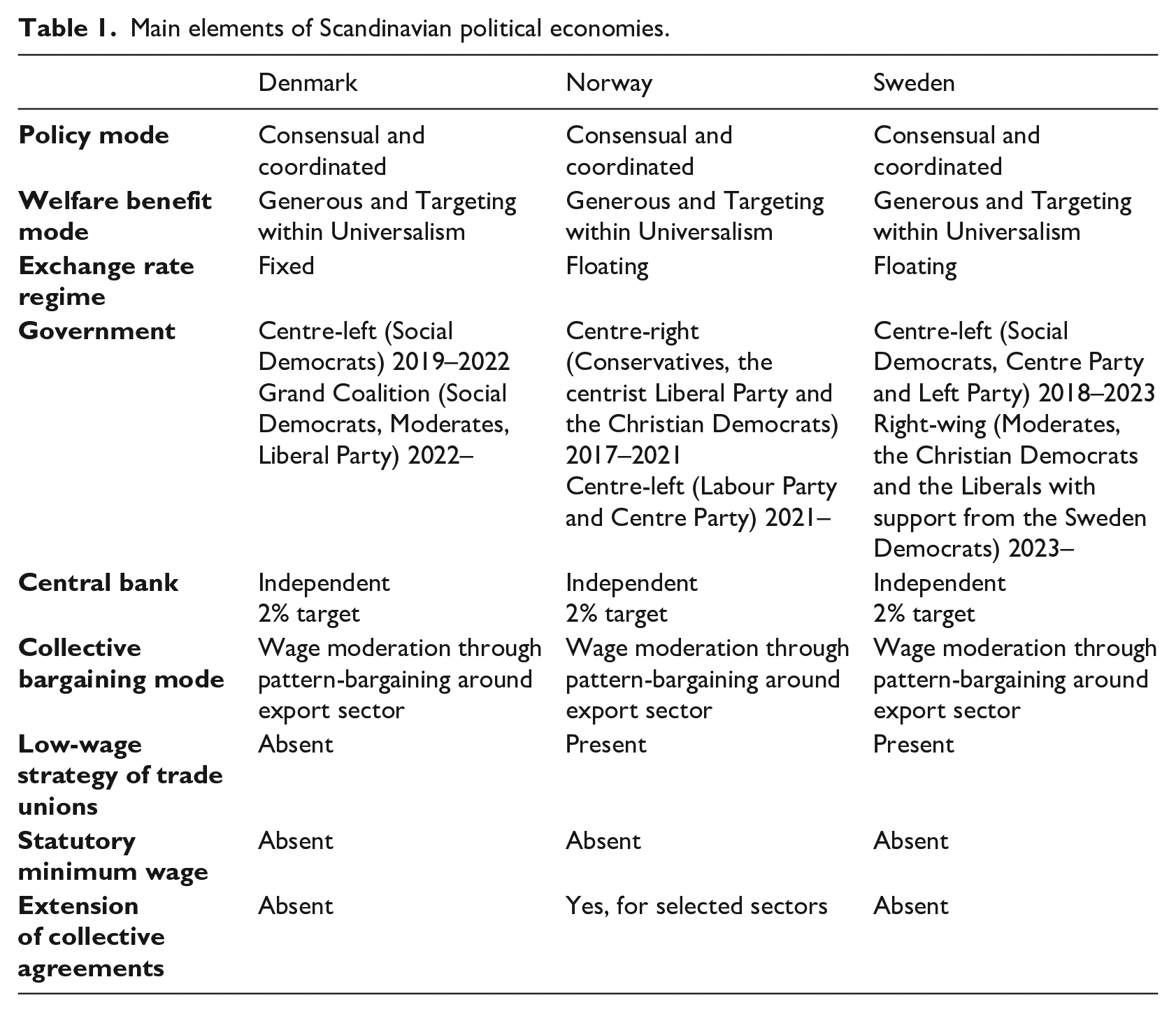

This new bargaining system allowed for more wage differentiation but did not create a massive ‘institutional void’, in which low-wage workers had no wage regulation. Similarly, welfare state reforms moved Scandinavian countries in a neoliberal direction but did not dismantle income protection. The current policy and collective bargaining regimes in Denmark, Norway and Sweden going into the cost-of-living crisis are summarised in Table 1. The three countries share most basic features, except for the exchange rate regime and the union low-wage strategy. Nonetheless, as we shall see, the countries had different problem loads and interpretations of the crisis, which resulted in different crisis responses.

Main elements of Scandinavian political economies.

Methodology

To address these topics we conducted three case studies of the public policy and collective bargaining responses in the three countries. We focus on public policies that specifically refer to the cost-of-living crisis spurred by inflation, starting in 2021. We follow the categories of income support worked out by the OECD (Hemmerlé et al., 2023: 13–14), distinguishing between energy support, income support (energy-related) and non-energy-related income support. These may be tax measures, direct transfers or price caps to help households (or businesses) through high inflation. Moreover, they may be targeted on particular groups, such as low-income households, or be universal. We use the OECD Energy Support Measure Tracker (Hemmerlé et al., 2023) for overall comparative data, but complement them with national government policy documents, policy papers, reports, press briefs, economic forecasts and news media articles, as well as secondary sources. Policy papers and press briefs from policy-makers are particularly important for the analysis of how actors interpreted the cost-of-living crisis.

For collective bargaining, we focus on the 2022–2023 bargaining rounds, depending on the expiry of agreements in each country. We focus on wage regulation in collective agreements, both overall wage increases and differences across groups. Moreover, we include measures that have a direct pecuniary value for workers to shore up incomes during high inflation, for example, the possibility of converting pension contributions into wages. While other working conditions, such as working time, also affect incomes and have played a prominent role in bargaining, we focus less on them to maintain a focus on wage regulation. We use social partner and mediation office documents, including policy papers, reports, press briefs, economic forecasts and news media articles, as well as secondary sources. Policy papers and press briefs from social partners were important for the analysis of bargaining processes and outcomes, including how the actors perceived the crisis going into bargaining and how they assessed the bargaining outcomes afterwards. Finally, to situate the Scandinavian countries in the European context we used data on macroeconomic performance from OECD/Eurostat in combination with data from the national statistical offices. When relevant, we compare the Scandinavian countries to Germany, a key reference point for all three countries (Andersen et al., 2014).

The cost-of-living crisis in Scandinavia

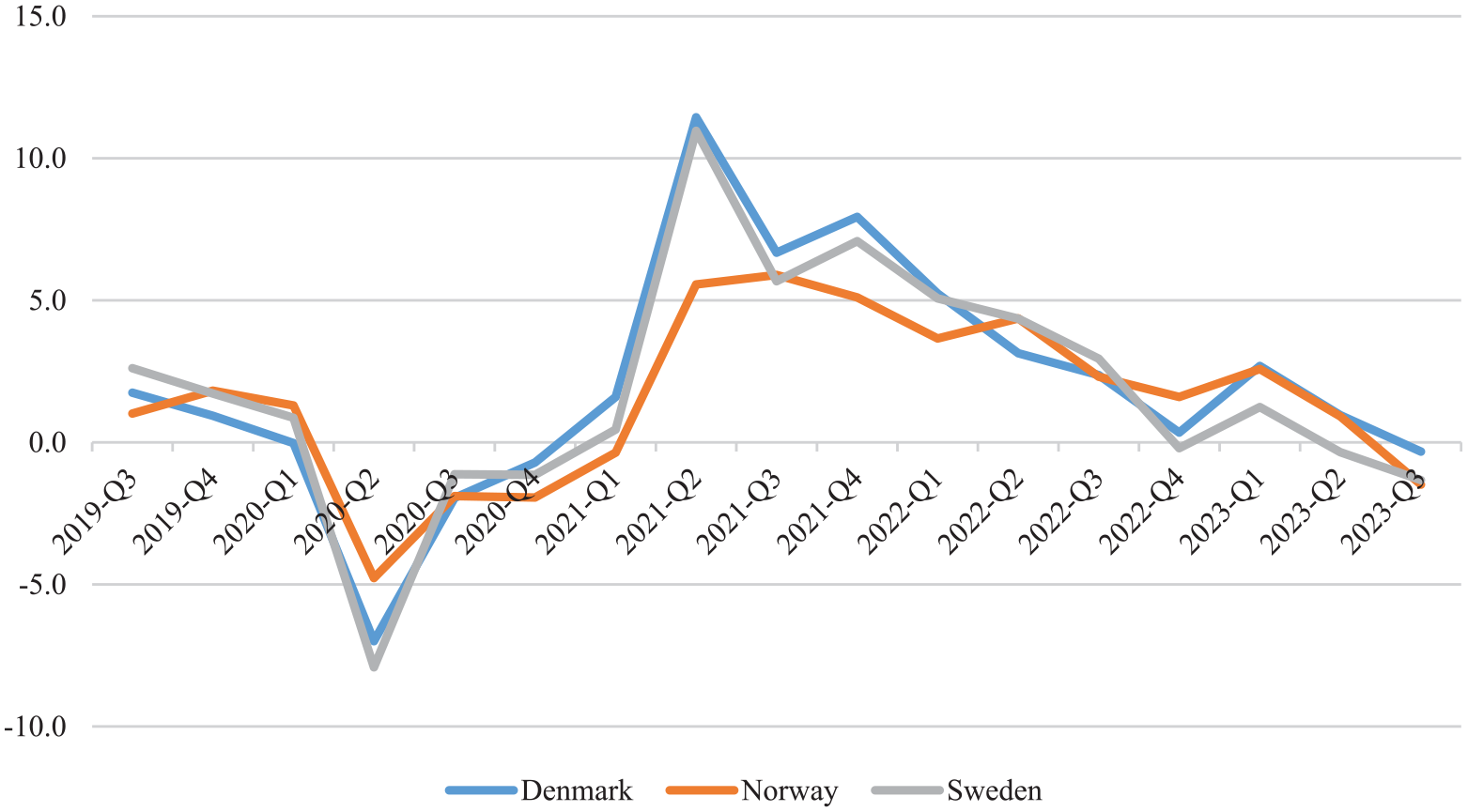

The Scandinavian economies fared comparatively well during the COVID-19 pandemic, in a European perspective. Swedish GDP growth was 2.0 per cent in 2019 and turned into a loss of 2.2 per cent in 2020, a larger drop than in Norway (−1.2), about the same as Denmark (−2.4). All countries were in recession in the third quarter of 2023 (year-on-year), as seen in Figure 2.

GDP growth by quarter in Denmark, Norway and Sweden (year-on-year), 2019-Q3 to 2023-Q3.

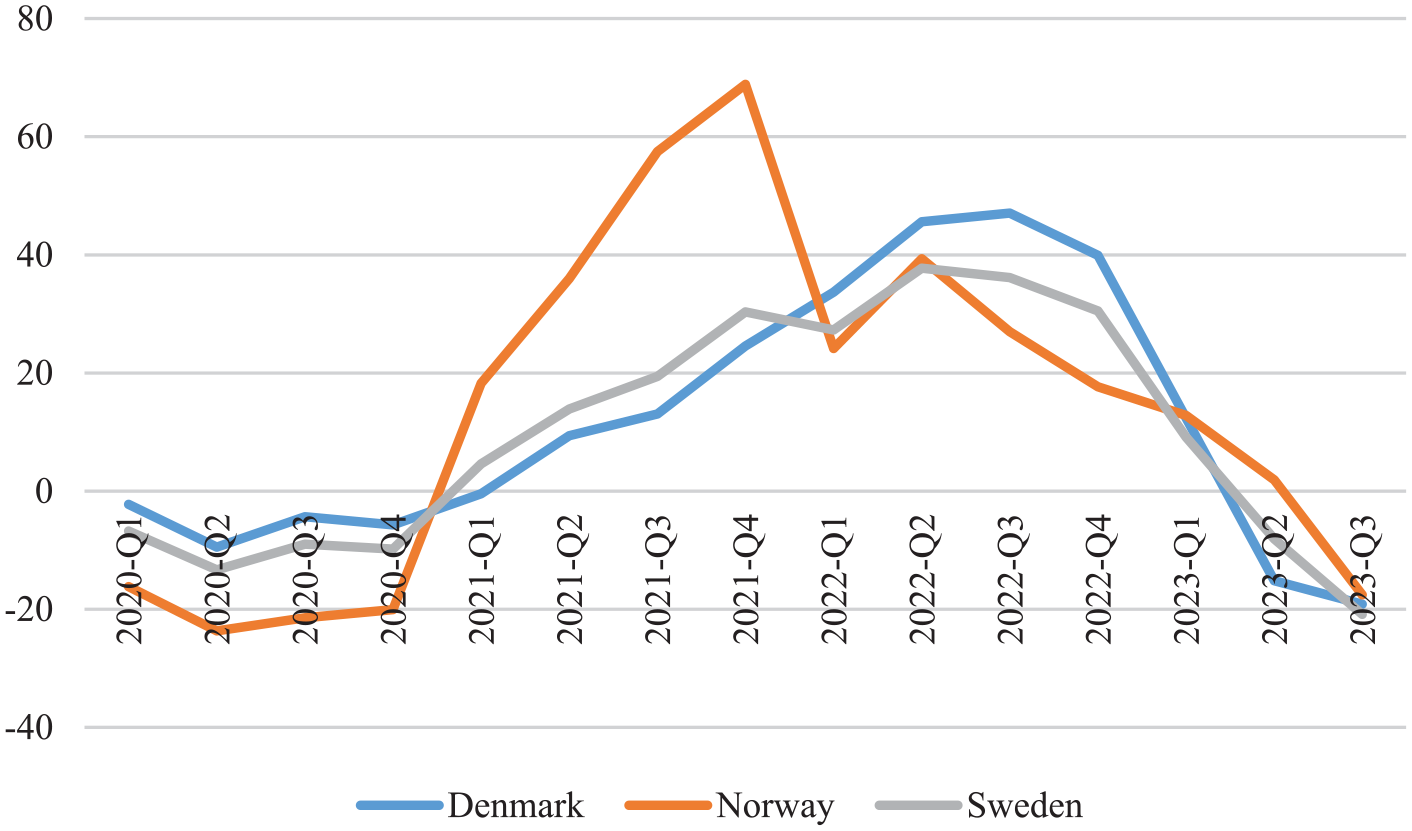

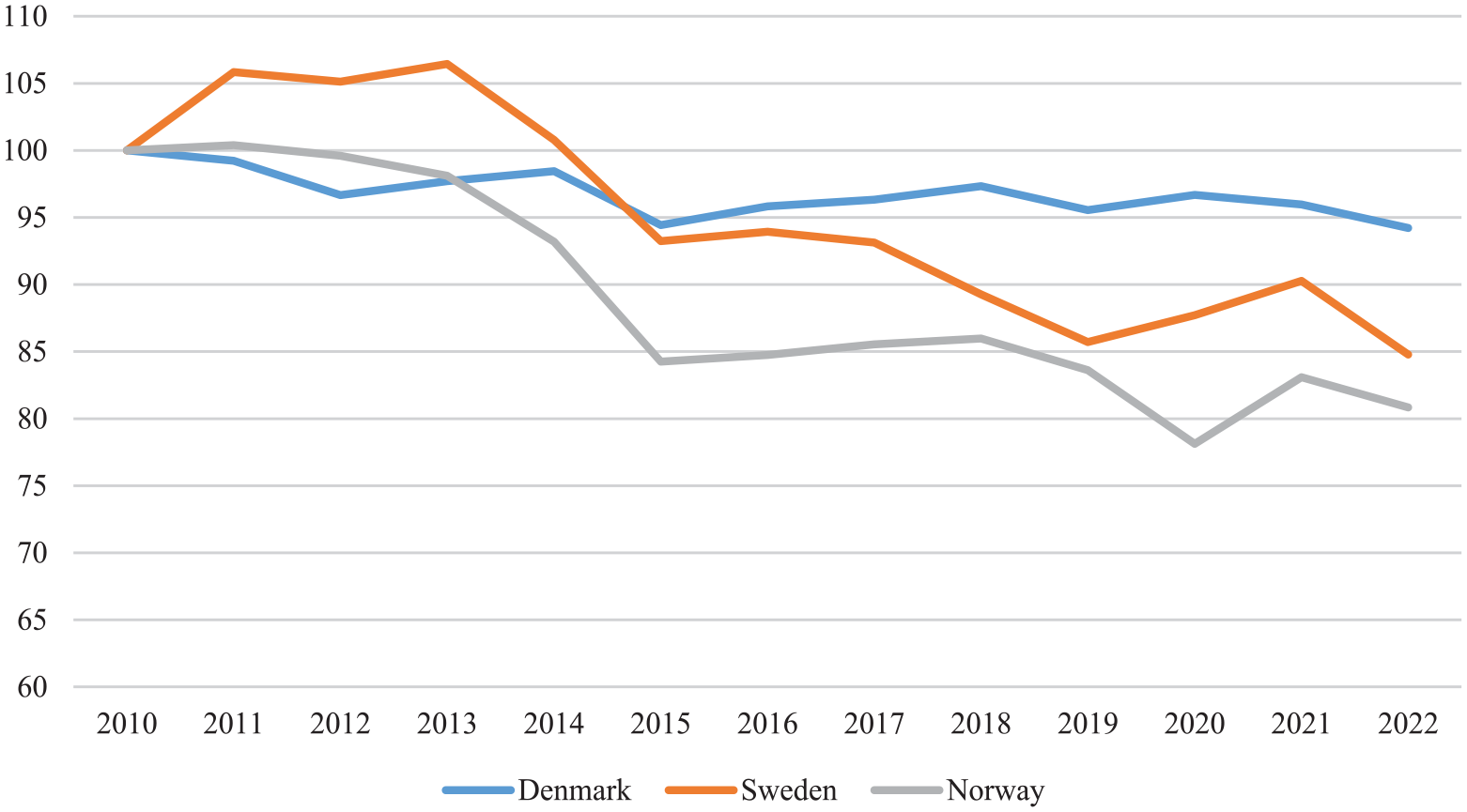

While the three Scandinavian countries share many economic, political and institutional traits, they differ widely in their energy consumption. Denmark is more dependent on fossil fuel sources than Norway and Sweden. Norway is a major exporter of oil and gas, whereas Sweden has nuclear power. Both countries have significant hydro power production and are net exporters of electricity. Notwithstanding these differences, all three countries experienced massive spikes in energy prices (see Figure 3) due to the European integration of energy prices. Thus, while energy companies – not least the large Norwegian energy exporting companies – enjoyed soaring profits, consumers in all three countries suffered. For consumers in energy-exporting Norway and Sweden, this price hike on (hydropower) electricity was especially hard to swallow and led some to question the rationale of being price-takers in the energy market. This political problem load, related to energy price inflation in Sweden and Norway, was further compounded by a weakening of the countries’ currencies (see Figure 4).

Inflation (CPI) energy, annual growth rate (%), Q1 2020 to Q3 2023.

Real effective exchange rate index in Scandinavia (2010=100).

In addition to high energy prices and bottlenecks in international supply chains, the weak Norwegian currency contributed to importing inflation. The authorities had used significant funds during the pandemic to support businesses and households’ economy. Therefore, the government argued that it was now time to normalise fiscal policy measures (Meld.St.2 (2021–2022), 2022). Both the Ministry of Finance and the Central Bank foresaw a gradual return to the inflation target aided by reduced use of petroleum revenues, a moderate increase in interest rates, and an expected strengthening of the Norwegian currency. In spring 2021, there were signals that the bank would raise interest rates during the autumn of 2021, although moderately (Norges Bank, 2021). Furthermore, the Central Bank expected that a strengthened exchange rate and prospects of moderate wage settlements would help bring inflation down.

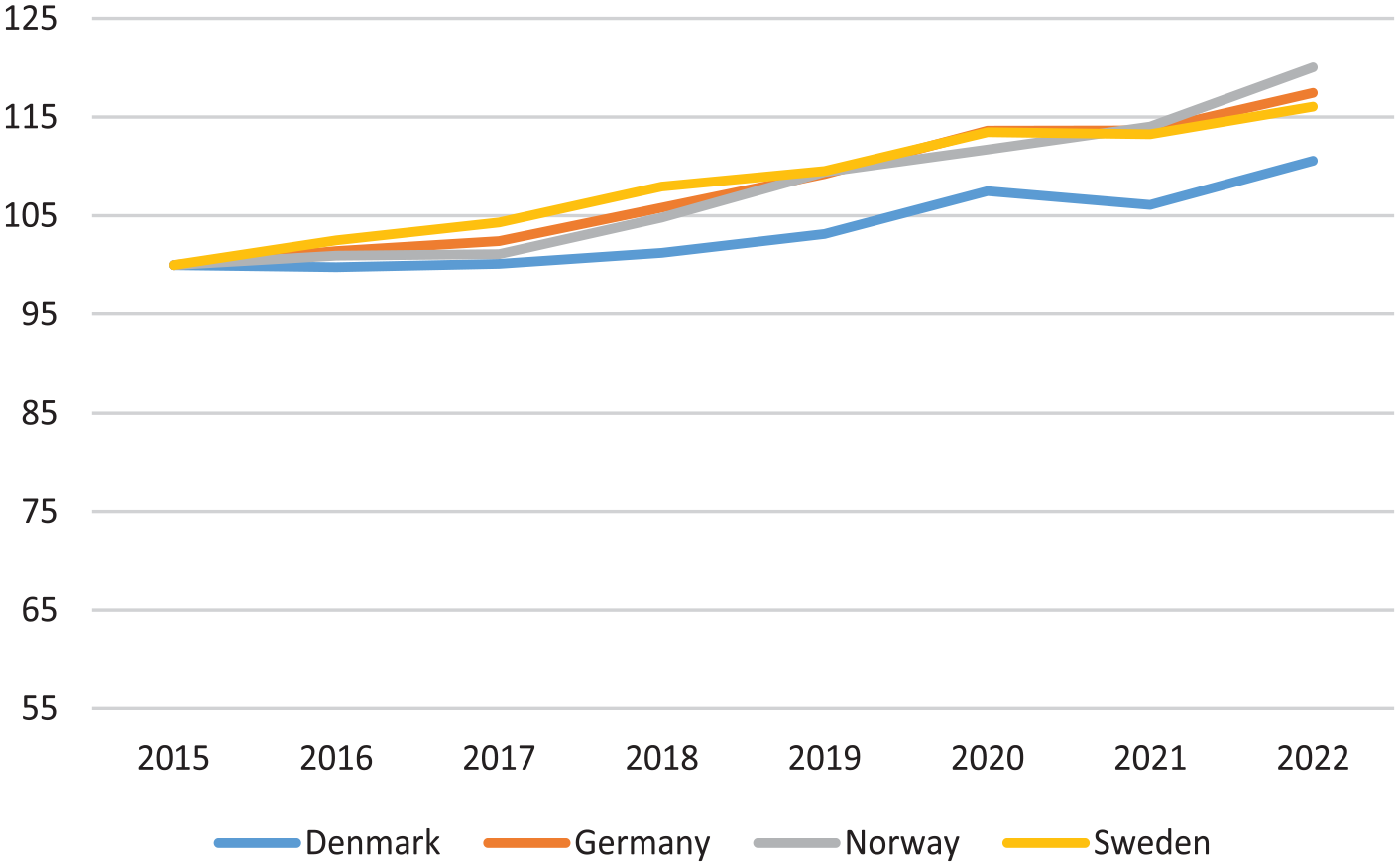

However, inflation became more entrenched than expected, not least because of internal inflation and wage growth, as seen in the unit labour cost developments in Figure 5. Compared with the 1970s, the Central Bank governor emphasised the role of the Central Bank, the framework for fiscal policy, and coordinated wage formation in which the parties focus on low unemployment and the financial health of businesses (Norges Bank, 2023). Employment picked up fairly quickly after the initial period of the pandemic. The employment rate in March/April 2022 was the highest since 2010, and unemployment remained at 3.2–3.3 per cent throughout 2022 (Statistics Norway, 2023). In autumn 2022, both Statistics Norway and the Central Bank expected that economic growth would slow down and decrease in 2023, and unemployment would rise slightly.

Unit labour costs (yearly per person employed) in Scandinavian countries, 2015–2022 (2015=100).

In Sweden, the National Institute of Economic Research (NIER) saw two main problems on the Swedish macroeconomic horizon: on the one hand, growing international supply chain and logistical problems, on the other hand lingering high levels of unemployment in Sweden, above 8 per cent even in good years. However, after the start of the Russian war in Ukraine, the NIER’s (2022) projections turned decidedly pessimistic, not least due to rising inflation. The skyrocketing inflation, falling asset prices and anticipation of further interest rate hikes made Swedish households pessimistic and a recession was expected for 2023.

Sweden, like Denmark, had a general election in September 2022. This led to the replacement of the Social Democratic government by a coalition government consisting of the Moderates, the Christian Democrats and the Liberals, with support from the Sweden Democrats. By 2023, across the political aisle, politicians were united in their view of the inflation crisis as a global crisis of supply chains and energy prices.

Denmark with its fixed exchange rate system, strong fiscal situation and comparatively modest increases in unit labour costs since 2015 seemed less challenged than Norway and Sweden. Contributing to a more resilient macroeconomy – especially in relation to Sweden – was the very strong labour market. Employment levels continued to increase during 2022 and remained high in 2023. So, while households took a hit to real incomes, the government, Central Bank and experts were less worried about the health of the Danish economy. Rather, the government argued for cautiously using the healthy economy to solve problems as they appeared rather than changing the overall macroeconomic strategy. To be sure, interest rates were raised in Denmark to tame inflation, but the problem load for government was lower there than in other countries and policies were, accordingly, less comprehensive.

The modest approach was transferred to the new Grand Coalition government of 2022, composed of the Social Democrats, the Liberal Party (Venstre) and the new party the Moderates (Moderaterne). Specifically built on a ‘pragmatic’ approach to politics, the new government argued that the polycrises of the war in Ukraine, inflation and climate change required across-the-aisle policies. However, rather than fighting inflation or shoring up household incomes, the government has focused mostly on labour market reforms that increase labour supply, for example in welfare occupations in the public sector (for more on this see below).

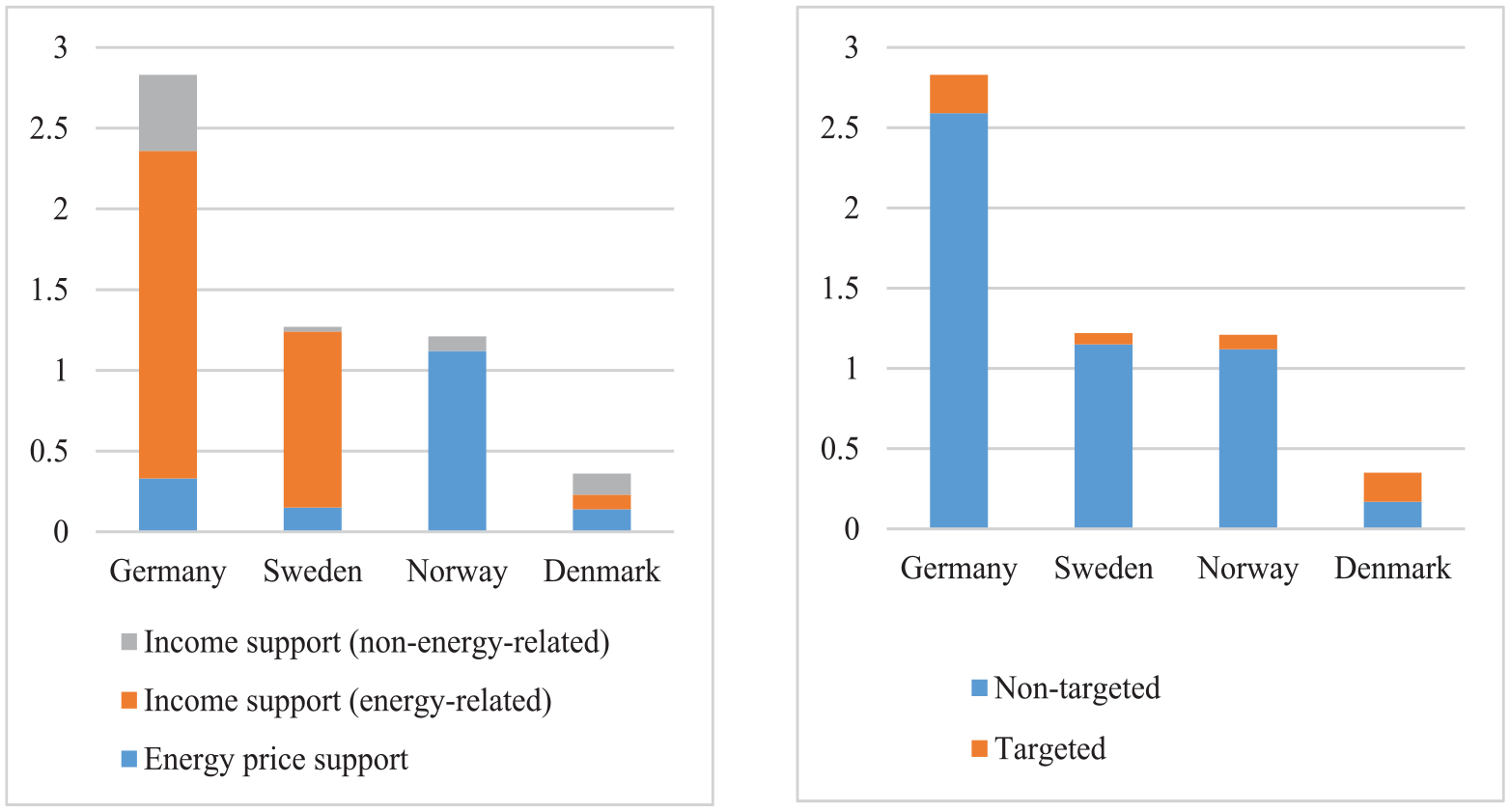

Looking at the different public policy responses of the three countries in Figure 6, we also see differences. The two figures show public support measures, broken down in two ways. First, by type, in other words, whether measures were aimed at energy price support (lowering the price of energy) or income support (energy-related or non-energy-related). Second, by target, that is, whether support measures were targeted at specific groups or not targeted. While none of the countries matches the size of the German response, Norway and Sweden spent significantly more than Denmark on supporting households and companies.

Support measures (as % of GDP) in Germany, Sweden, Norway and Denmark (by type and target).

The countries also differed significantly regarding the targets of support, as seen in Figure 6. Sweden and Norway, like Germany, allocated non-targeted, universal support to a much greater extent than Denmark, with an almost 50/50 split between targeted and non-targeted measures. Thus, not only did Norway and Sweden spend more, but they did so in a more universalist manner. Denmark deviated in this regard from the typical universalist welfare state tradition. Below, we go into the processes that resulted in these different approaches and show how collective bargaining contributed to the cost-of-living crisis responses.

Norway: universal and generous public policy – generous but contested collective bargaining

The increase in electricity prices in 2021 led to strong pressure for economic support schemes. Towards the end of 2021, the new Labour-led government proposed general electricity support for households and certain other groups. Shortly afterwards, in January 2022, the scheme was improved and from 1 September 2022 the state covered 90 per cent of electricity prices exceeding NOK 0.70 (€0.06) per kWh, but with a ceiling for the monthly consumption covered by the scheme (Regjeringen, n.d). For 2022, electricity support to households amounted to NOK 32.6bn (approximately €2.72bn) (Regjeringen, 2023). Other energy measures were also introduced, including a reduction in the electric power tax (a tax on electricity produced in Norway) and increased support for energy efficiency measures. In autumn 2022, a support scheme for businesses was also introduced. This was not aimed at the most energy-intensive businesses, however, as they generally have long-term fixed-price agreements for electricity and were therefore less affected by the increase in energy prices.

Norwegian consumers were especially displeased that EU regulation of the energy market meant that energy-exporting countries had to be price-takers, instead of being able to set prices favourably for consumers on the Norwegian market. Significant pressure was thus put on the government, also from the trade unions, to put forward a model for electricity support. The design of the scheme was settled primarily between the government and parliament, and thus was not part of a formal or informal tripartite agreement between the social partners and the authorities. However, LO (the Norwegian Confederation of Trade Unions) indicated in its wage settlement policy statement ahead of the 2023 wage negotiations that the improvement of the support scheme from 55 to 90 per cent came after a proposal from LO (LO Norway, 2023).

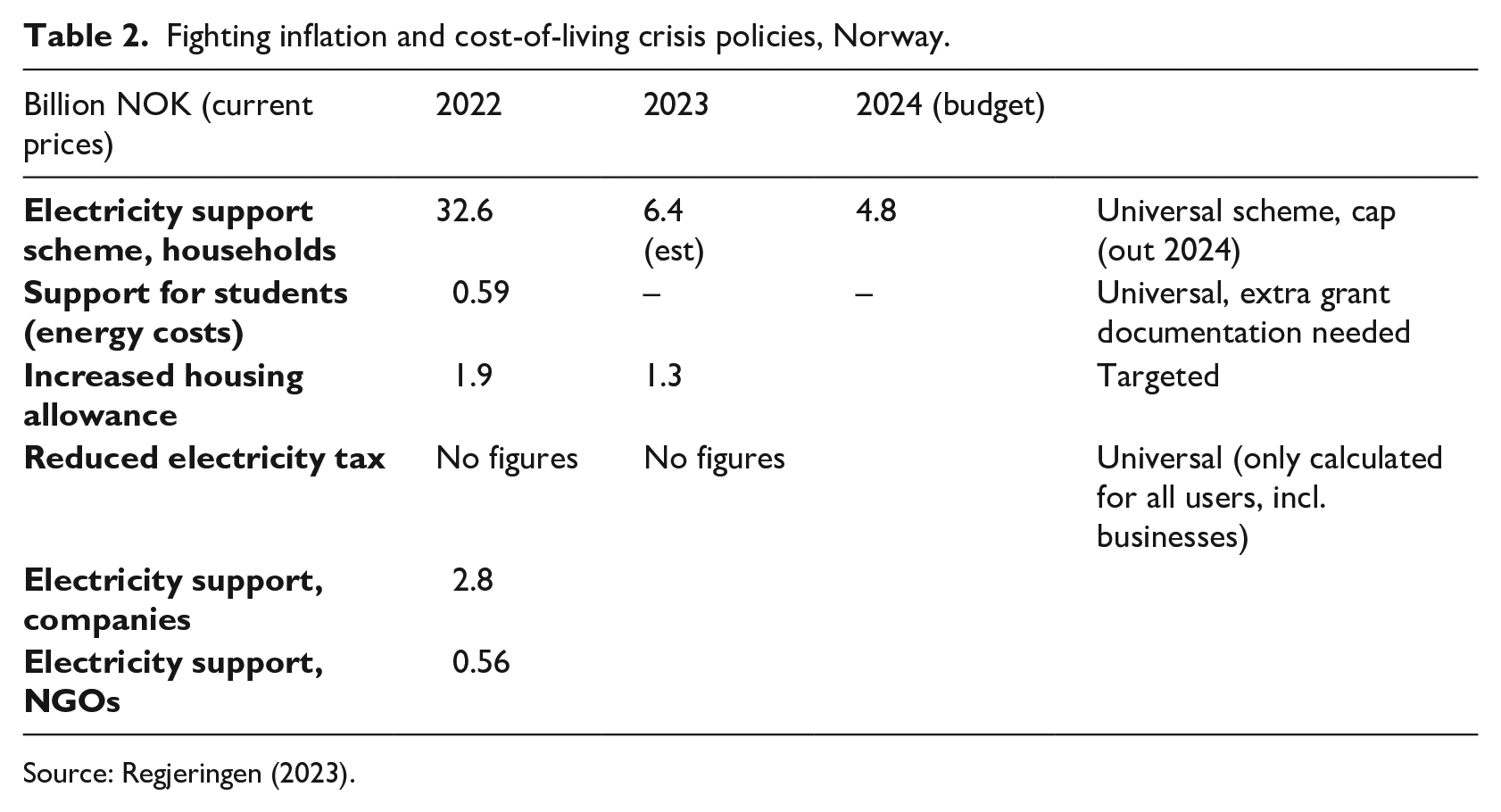

As inflation increased, other targeted measures were introduced, including increased housing allowance, higher minimum rates for social assistance, and reduced child-care fees. Nevertheless, electricity support remains the main support measure for households related to high inflation (Table 2).

Fighting inflation and cost-of-living crisis policies, Norway.

Source: Regjeringen (2023).

Repeated interest rate hikes by the Central Bank of Norway have been the main means of bringing down inflation. Between September 2021 and December 2023, the interest rate was increased 13 times, from 0 to 4.5 per cent. LO has repeatedly criticised the Central Bank for focusing only on reducing inflation and being less concerned about rising unemployment. LO argued that the Norwegian wage formation model, with responsible parties and strong coordination, helps to avoid wage-price spirals even in a situation of high inflation. This is, according to LO, especially true when inflation largely comes from abroad (LO Norway, 2024). Others by contrast have criticised the Central Bank for taking too long to raise interest rates, thereby contributing to keeping up inflation (for example, Holvik and Thorsrud, 2024).

There have also been deliberations and discussions about fiscal policy measures. The use of oil revenues has been higher than the fiscal rule prescribes under normal economic circumstances. At the same time, it has been necessary to balance this against the need to ensure that the high inflation and energy prices do not have too large distributional consequences. Additionally, significant expenses have arisen related to the high number of refugees from Ukraine, requiring fiscal prioritisation.

Turning to collective bargaining, wages in Norway are renegotiated every year in industry-level or cross-sectoral negotiations. Prior to the annual wage settlement, the Norwegian Technical Calculation Committee for Wage Settlements (TBU), with representatives of the social partners, various ministries and Statistics Norway, makes an assessment of the economic situation, as well as predictions on the development of the consumer prices index. In March 2022, the TBU stressed that uncertainties for 2022 were extraordinary and especially linked to the war in Ukraine and its effects on energy prices, food prices, the exchange rate of the Norwegian krone and the bottlenecks in the production of goods and services that currently characterise the international economy (NOU, 2022: 4).

The outcome of the 2022 wage settlement highlighted the strength of the coordinating elements of the wage-setting model. The ‘norm’ set by the front-running manufacturing industry at an annual wage increase of 3.7 per cent (higher than the CPI estimate of 3.3), was adopted across other bargaining areas, even though inflation had increased above this level before other bargaining areas were concluded. By year-end, it was apparent that the 2022 wage increases ended up being far below CPI at 5.8 per cent, whereas wages increased by 4.1 per cent, the highest increase being among white-collar workers in the private sector.

Prior to the 2023 settlement the Norwegian Central Bank assessed the Norwegian economy to be robust, marked by low unemployment and a rise in labour force participation, with several sectors experiencing labour shortages. As inflation remained high at the beginning of 2023, high wage increases were expected. There is no tradition among private sector unions of seeking compensation for real wage losses in previous years. LO’s position ahead of the 2023 mid-term settlement was therefore based on the economic situation in 2023. At the same time, in response to the previous year’s fall in real wages they aimed not only to safeguard real wages, but also to enhance workers’ purchasing power. As the internationally exposed manufacturing industry enjoyed high profits due to the weak Norwegian currency, LO further stressed the importance of ensuring the employees’ share of value creation (LO Norway, 2023). Conversely, the Confederation of Norwegian Enterprise (NHO, 2023a), concerned by the high inflation, advocated for a settlement that avoided fuelling inflation further and thereby the potential risk of wage spirals.

For the first time LO and NHO failed to reach a mid-term agreement, and consequently more than 23,000 members went on strike. Four days later the parties agreed on an annual wage increase of 5.2 per cent, 0.3 percentage points above the estimated CPI (NOU, 2023: 60). The failure to reach an agreement did not concern the size of the annual wage increase, but its distribution profile. LO aimed to secure real wage increases for low-income earners who were particularly suffering because a larger share of their income was going on food and energy, the price of which had increased the most. The settlement ensured a minimum hourly wage increase of NOK 7.50 (€0.6), with higher increases for those on lower wages. By going on strike to safeguard the purchasing power of low-wage earners, LO demonstrated their commitment to prioritising a low-wage strategy during periods of high inflation. As the economic framework of the settlement remained the same, less money was allocated to firm-level bargaining.

Following the agreement, NHO (2023b) expressed concerns about the financial burden on companies, highlighting the implications for financially struggling businesses. For the employers, the 2023 settlement illustrates the difficulty, if not impossibility, of reaching an agreement below CPI projections in a strong labour market. In such situations, moderate wage increases would indicate higher profits for the owners. However, the difficulties for NHO were related mainly to the distribution of the wage increases, which entailed high general increments to all workers, and in particular, the effects on member companies in private services and low-wage manufacturing (mainly in domestic industries). Employers were thus less worried that the settlement would reduce the competitiveness of the exposed manufacturing industry, and more by the costs to the private service sector.

Sweden: universal and generous policies – modest but solidaristic collective bargaining

The new Swedish centre-right government in 2022 launched a two-tiered strategy to deal with the cost-of-living crisis. First, pandemic-related increases in welfare spending, going back to the preceding Social Democratic government, were continued or enhanced. The raised replacement rates of unemployment insurance were kept in place to help the unemployed deal with growing inflation. The government also indexed the replacement rates for low-income pensioners and students to the consumer price index to help these relatively poor groups.

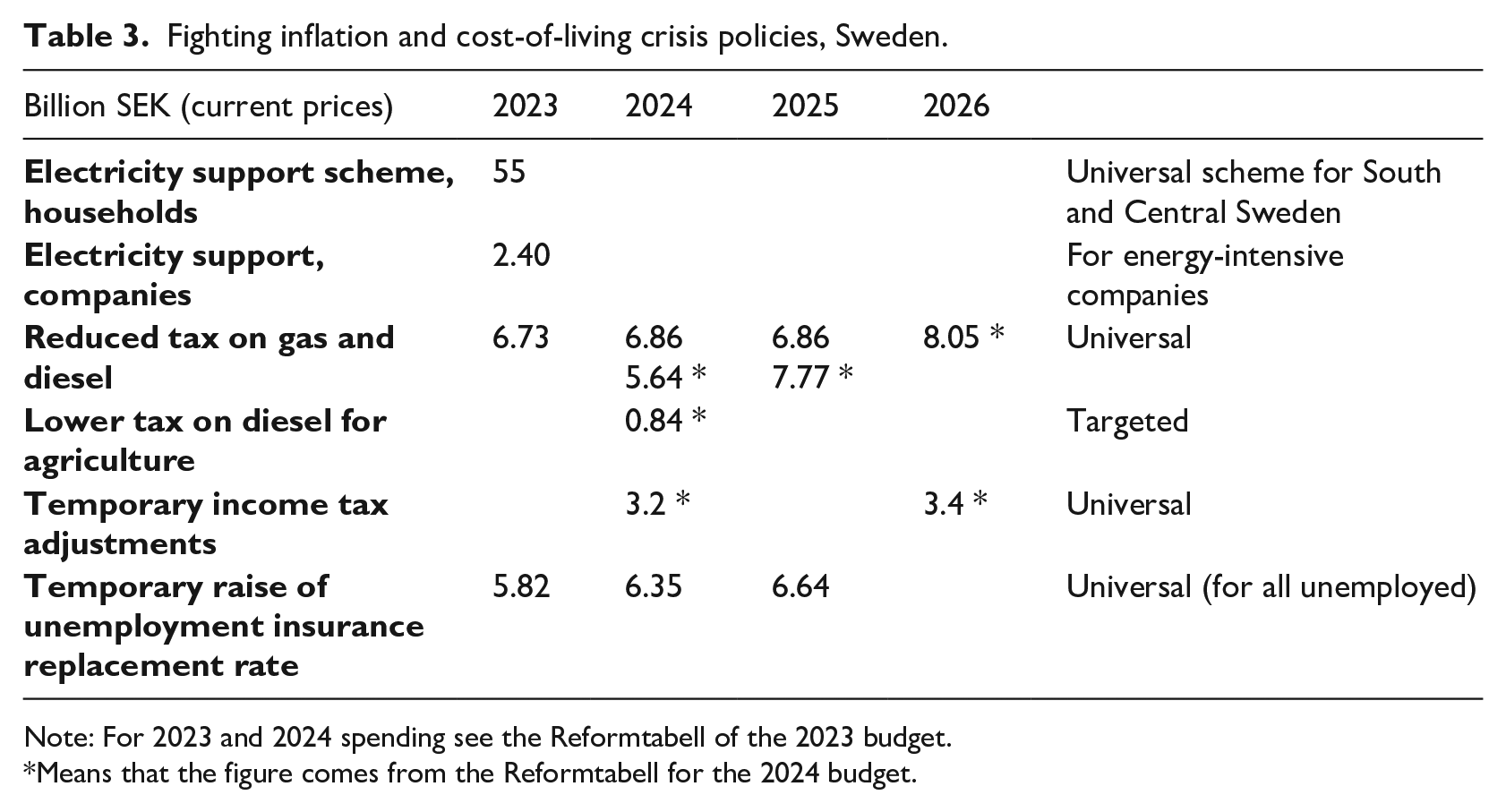

Second, the government helped households with their energy costs (see Table 3). All parties across the political spectrum were in consensus that something had to be done, but the precise design of support programmes became, alongside the ongoing crime wave, the most contentious issue in Swedish politics in 2022. The eventual outcome was that all households in South and Central Sweden – energy prices are less steep in the north due to the abundance of hydropower – would receive one-off compensation payments in 2023. The expense was enormous: SEK 56bn, by far the largest expenditure in the 2022–2023 economic policy mix, and it was criticised by the OECD and the EU for being too expansive (Dagens Nyheter, 2023; Tidningen Näringslivet, 2023). It was funded by windfall taxes on the profits of the state-owned enterprise Svenska Kraftnät, which owns the Swedish electricity grid, profits enhanced by the high electricity prices.

Fighting inflation and cost-of-living crisis policies, Sweden.

Note: For 2023 and 2024 spending see the Reformtabell of the 2023 budget.

Means that the figure comes from the Reformtabell for the 2024 budget.

More conventional was the support given to households with gasoline and diesel prices. To lower consumer prices, taxes on both ordinary gasoline and agricultural diesel were cut, and the previous government’s demands regarding the inclusion of climate-friendly materials in the fuel mix were cut down to the EU’s minimum level.

The 2024 budget, presented in September 2023, continued in the same way, the government’s first priority being the fight against inflation (Sveriges Regering, 2023). The budget contained a directed rise in pensions for those born in 1957, a group previously caught between two pension systems, and continued lowering taxes on gasoline and diesel. The finance minister described the budget for 2023 as ‘mildly restrictive’ (Sveriges Radio, 2023), while the centre-left criticised it for not fully compensating the public sector for growing costs.

As in Norway, central bank interest policy was a crucial part of the policy mix for reducing inflation. The interest rate was 0 per cent in early 2022, but at the end of the year it had reached 2.5 per cent and at the end of 2023 4 per cent. Swedish households have high debt ratios and commonly take out mortgages with adjustable interest rates, responsive to the central bank’s interest rate (Sveriges Riksbank, 2023: 8–9). This means that the Swedish economy is quite sensitive to interest rates and in 2023 the economists of the main union confederation, LO, were critical of the Swedish economic policy mix, which they believed was too restrictive, especially given the interest rate policy. The LO and the employer-side economists described the government’s fiscal policy as ‘passive’ (Dagens Nyheter, 2024; LO, 2023). They argued that the inflationary pressures came from the supply side and the international economy – energy prices, supply-side constraints – and thus could not be contained by restrictive monetary and fiscal policy. Political parties from the Social Democrats to the Conservatives, however, showed a greater aversion to inflation and greater fears that economic stimulus policies or lower interest rates would indeed exacerbate inflationary pressures; the austerity-oriented nature of Swedish politics is familiar from recent research (Bengtsson and Ryner, 2017; Mudge, 2018: 322–330). The most important heterodox policy proposal on the cost-of-living crisis was the Left Party’s suggestion to impose ‘Sweden prices’ on electricity, limiting the effects on Swedish domestic electricity prices (Sweden being a net exporter due to nuclear and hydropower) of EU demand. These attempts were, however, on the margins of Swedish politics.

Turning to collective bargaining in recent years, the spring 2020 bargaining round prolonged agreements for seven months because of the pandemic, and the new agreements were reached only in October. The 29-month agreements built on an average 5.4 per cent wage growth, with no compensation for the seven months of standstill (Medlingsinstitutet, 2021: 31–32). The year 2020 was a low inflation year – in the spring of 2020 Sweden had just exited deflation – and given the unforeseen inflation of 2021–2023, this led to a real wage fall. Thus the 2023 bargaining round, which led to new agreements in March 2023, was held under difficult circumstances, and the rhetoric was more heated than in 2020 (see Svenskt Näringsliv, 2022). The major outcome in the 2023 bargaining round was new agreements for 7.4 per cent wage growth over two years, 4.1 per cent for March 2023 to March 2024 and 3.3 per cent for March 2024 to March 2025 (Medlingsinstitutet, 2024). The Finance Ministry prognosis in the autumn of 2023 was 6.0 per cent consumer price inflation in 2023 and 2.7 per cent in 2024 (Sveriges Regering, 2023). This would entail a real wage loss of about 2 per cent in 2023 and an increase of about half a per cent in 2024, moderate levels of wage growth. However, we must also consider that the LO unions continued their low-wage strategy, a two-tier approach awarding more than the typical 7.4 per cent to the low-paid. This strategy with a ‘second mark’ has been used intermittently since the inception of the Industrial Agreement system in the late 1990s (Bender, 2024: 151–158).

The LO economists’ own analysis of the 2023 agreement was that it was a good deal, with a robust emphasis on pay growth for the low-paid, but that they never intended to compensate fully for price increases. The LO economists stated, and this is very much a centrepiece of the mainstream of the Swedish economic policy debate of the past 25 years: ‘Sweden has bad experiences of the price and wage spiral which appeared in the late 1970s and which was broken only with the economic crisis of the 1990s. [. . .] Despite high nominal wage increases, there were no real wage increases. This was in the end harmful for the entire economy. The lesson is that a price and wage spiral can be difficult to break’ (LO, 2023: 29). Overall, the social partners, the politicians and the central bank all seem quite content with the results of the 2023 bargaining round.

Denmark: targeted and modest public policy – generous and solidaristic collective bargaining

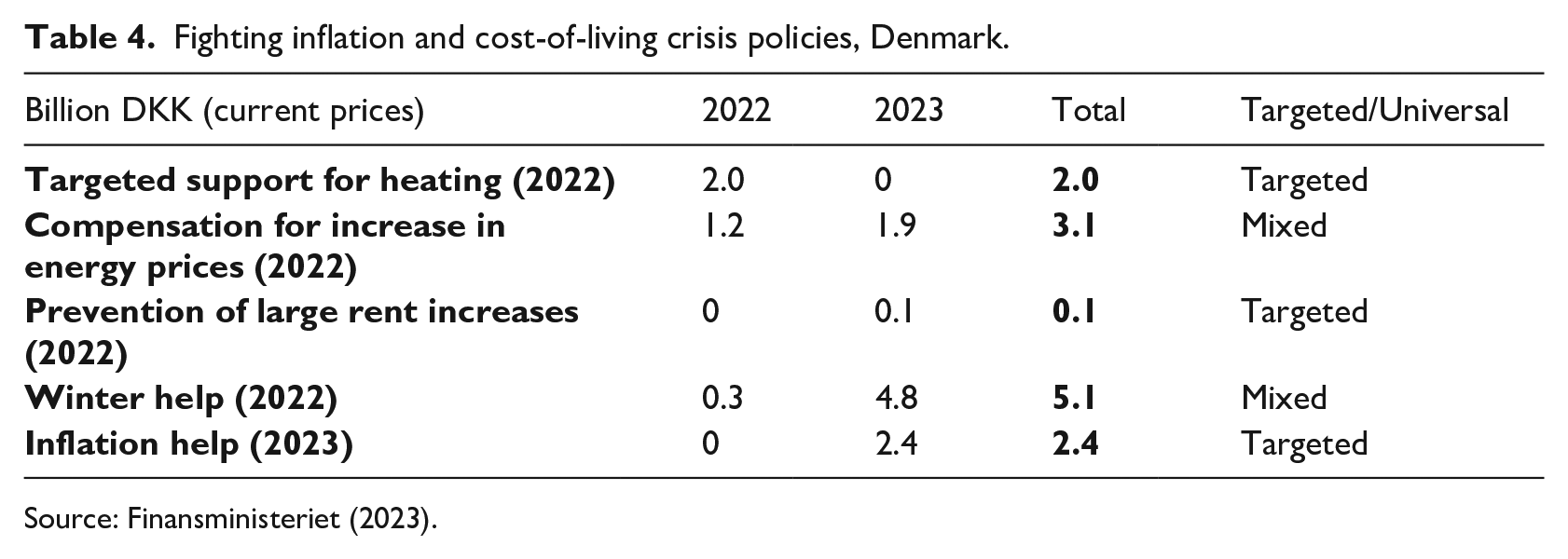

As seen in Table 4, the Danish policy response to rising energy prices and inflation was modest and fairly targeted, going against the general expectation of generous and universal income support. In line with the expectation of broad and consensual policy-making, however, all measures gained broad partisan support in parliament and passed with little contestation. The government did not convene the social partners for tripartite talks, perhaps surprisingly given the frequent use of tripartite agreements during COVID-19. The government took the view that the inflation crisis did not call for a nationally coordinated response to inflation, as there was never a strong fear of a wage-price inflation spiral, despite the low unemployment. Collective bargaining parties have a history of wage moderation since 1987 (see above), and the Ministry of Finance and Danmarks Nationalbank trusted in real interest rate hikes to dampen inflation. Likewise, the study by the IMF (Alvarez et al., 2022) on the low risk of wage-price inflation spirals contributed to a modest risk assessment.

Fighting inflation and cost-of-living crisis policies, Denmark.

Source: Finansministeriet (2023).

The modest and targeted policy measures did not contribute to excess demand in the economy, which had already been tamed by increasing interest rates, as seen in the other countries. The understanding of the crisis was that certain groups would suffer disproportionately – the elderly, homeowners with gas heating or renters – from increasing prices, but the general population would manage. In addition, the interpretation of the cost-of-living crisis was premised on responding to the needs arising in times of high volatility. Thus, rather than pumping money into society the government would generally identify groups with special challenges and help with targeted measures. This approach requires policy-making to be responsive and quick, something which the single-party Social Democratic government already tried during COVID-19.

For working people, inflation significantly hollowed out real wages during 2021 and 2022, thus putting pressure on trade unions in particular to obtain generous wage increases in the 2023 bargaining round. Because the government had not passed any significant universal packages to mitigate the real-income losses, it was up to the collective bargaining system to restore real incomes through wage increases.

There has been no major conflict in Danish private sector collective bargaining since 1998. However, the 2023 round had all the elements needed to produce one (see Andersen et al., 2023). First, the spike in price inflation hollowed out the purchasing power of workers, who – due to the endemic shortage of labour – were in a favourable employment situation. Moreover, the trade unions viewed the Danish economy as strong, not least because of its strong export performance. This combination drove up wage demands to restore real wages to the pre-inflation level. Employers, while acknowledging that wage increases would be higher than usual, cautioned that major uncertainties in the world economy called for some moderation. They wanted to avoid a repetition of the 2007 bargaining round, when high wage increases were locked in for three years, just when the financial crisis and recession hit. The different interpretations of the economy could hamper negotiations. Second, social partners in manufacturing – the key bargaining sector – were in heated discussions about their wage systems because of hourly wage increases that did not keep up with productivity increases. Trade unions complained that local wage bargaining did not work as intended because managers refused to increase wages in line with productivity increases. Employers argued that a few ‘super-star’ companies, especially in pharmaceuticals, could explain the drop in the labour share but that the average employer negotiated reasonable wage increases in line with productivity.

Despite these diverging views, the bargaining parties in manufacturing settled on a two-year agreement and the other bargaining areas followed suit as usual. The agreements contained a strong focus on low-wage workers and a return to wage solidarity in Denmark (see Ibsen and Thelen, 2017). Surprisingly, the skilled metalworkers’ union, Dansk Metal, argued for low-wage workers. This focus came about because of closer coordination between the manufacturing union and the commercial workers’ union, HK HANDEL. Likewise, 3F, the general workers’ union organising many low-wage workers – for example, in cleaning, and hotels and restaurants – coordinated internally to focus bargaining demands on low-wage workers. Not only were these workers hit hardest by inflation, but they were also the least likely to obtain increases from local bargaining. Therefore, centralised wage increases were preferred over other non-wage issues and over local wage bargaining (Andersen et al., 2023).

The centralisation strategy posed a challenge for minimum wage systems in Denmark, accounting for 80 per cent of the private sector, in which wages are negotiated at company level. Both parties, especially the unions, were reluctant because of the temporary character of this solution and quickly dismissed the introduction of one-off lump-sum payments, as seen in Germany. Instead, bargaining parties solved this challenge in three ways (CO-industri, 2023). First, the parties agreed to a 2 per cent increase in the employer contribution to pensions, shifting their contribution from 8 to 10 per cent of the wage sum. Workers reduced their contributions from 4 to 2 per cent, thus giving them a 2 per cent increase in take-home wages. Second, the agreement contained a 2 percentage point increase – from 7 to 9 per cent – in the employer contribution to the so-called ‘free-choice account’. This personal account can be used for extra paid time-off, extra pension contributions, or simply as extra wages. Combining the two meant that all workers had a guaranteed wage increase of 4 per cent over the two years of the agreement. Finally, the parties agreed to a higher than usual increase in the minimum wage of 6.9 per cent. This was done explicitly to cater for the many low-wage workers who typically get very little or nothing from local wage bargaining. Usually, manufacturing unions prefer to leave more scope for firm-level bargaining, but the 2023 agreement favoured increases in the minimum wage. As such, a low-wage worker working on the minimum wage was guaranteed a 10.9 per cent wage increase over two years (Andersen et al., 2023).

While the lack of industrial conflict and the low-wage profile of the agreements were major successes for the social partners, critics pointed out that the real wages of a majority of workers still hinged upon local wage bargaining. Were the agreements enough to bolster local wage bargaining and restore real wages during the two-year agreement? At the time of writing (Q1 2024), the 3.8 per cent loss in real wages between 2021 and 2022 has still not been recuperated. Annual real wages in the private sector increased by 2.7 per cent in the third quarter of 2023, however (FH, 2023). If inflation continues as projected, losses in real wages would be restored to pre-inflation levels by the end of the agreement. Importantly, this is true for low-wage workers in services, as well as for high-wage workers (DA, 2024). Although service sector workers trail construction and manufacturing, they are projected to recuperate their 2021 and 2022 real wage losses before 2025 (DA, 2024).

On an endnote, the 2024 renewal of public sector agreements took place against the backdrop of a hitherto unprecedented tripartite agreement that allocated wage increases to particular workers in the public sector: nurses, child-care workers, prison guards and midwives. These exceptional increases were not due to inflation but to recruitment and retention efforts, as well as long-lasting debates on wage gaps between these predominantly female workers and comparable groups of workers in the private sector (Hansen and Mailand, 2024). The combined effect of these extraordinary wage increases means that specific groups of, for example, health and social care workers can expect a 17 per cent wage increase over two years. These discussions were also important in Norway and Sweden, but did not result in above-pattern increases as seen in Denmark.

Comparative discussion of findings

The public policies and collective bargaining responses to the 2021 inflation and cost-of-living crisis in Norway, Sweden and Denmark relied, as expected, on consensual policy-making and on the social partners’ strong collective bargaining capacities. This does not mean that public policy was coordinated deliberately with collective bargaining and vice-versa. The principle of voluntarist collective bargaining (Andersen et al., 2014) was respected, and there was ‘normal’ lobbying of policy-makers by trade unions and employers’ associations during the crisis. Compared with the inflation crises of the 1970s–1990s, the responses were focused on cost-of-living support measures, whereas the risk of wage-price inflation was perceived to be modest. Unlike previous crises, the current responses have not been institutional and a major overhaul of the Nordic Models is unlikely.

While these general findings apply in all three countries, we identified some differences in the public policy responses to rapidly rising inflation in the three countries. Norway and Sweden gave priority to universal and relatively generous public policies to alleviate the impact of rising energy prices on households, while Denmark spent less on these schemes overall and they were more targeted towards specific low-income groups. What probably explains the different levels of the schemes is that Norway and Sweden are net exporters of electricity, making the electricity price surge politically explosive in these countries compared with Denmark. Concerning targeting, Denmark deviated from the expected policy mode of universal support, but this might be the unsurprising outcome of a relatively strong Danish economy despite the inflation surge.

A weak Norwegian currency and high energy prices contributed to the steeper increase in inflation, which boosted public and political demands for extraordinary and universal support schemes. A specific Swedish problem was the continuing high level of unemployment, approximately twice as high as in Norway and Denmark. The Danish fixed exchange rate system contributed to a resilient macroeconomy and Danish employment levels continued to increase throughout both 2022 and 2023 for the first time ever, surpassing 3 million workers in jobs. Accordingly, the public as well as political pressure to introduce more generous support schemes was less intense in Denmark.

None of the countries use in-work benefits or have a national minimum wage that governments can increase to bolster household purchasing power. While there is no explicit coordination between governments and social partners, wage setting is understood to be the main mechanism for improving real incomes for most households. Therefore, the renewal of agreements in 2023 in all three countries became the main tool for tackling inflation and these negotiations became more difficult than usual and in the Norwegian case even ended in industrial action.

Prior to negotiations the unions in all three countries focused on the need to raise wages significantly. However, the rhetoric and to some degree strategies differed somewhat across the Scandinavian unions. Despite no tradition among Norwegian unions for seeking compensation for real wage losses in previous years, the LO’s position this time leaned towards not only securing real wages, but also enhancing workers’ purchasing power, given a relatively strong labour market and good economic results for companies. In Denmark, the private sector unions strongly emphasised that the aim was both real wage increases in coming years but also to catch up for real wage losses in previous years. Union criticism of employers not offering sufficient wage increases in company-level wage bargaining even before the inflation crisis fuelled this union approach. Furthermore, contrary to Norwegian tradition, it has been a recurring theme that unions claimed the employers ‘owed money’ for slack wage trends in previous years. A somewhat different position was taken by Swedish unions in arguing for a certain amount of wage moderation, reflecting fears of a price and wage spiral. The relatively high level of unemployment in Sweden might also have dampened the Swedish unions’ approach compared with Denmark and Norway, as well as their more recent memory of price and wage spirals in the late 1990s.

Turning to wage outcomes in the bargaining round two observations are especially worth making. First, there was a strong element of wage solidarity in all three countries. While the Swedish and Norwegian trade union wage policy for many years has included ‘above-the-pattern’ increases for low-wage workers, Danish unions have not given the same priority to low-wage earners. The 2023 bargaining rounds saw a convergence around wage solidarity. In Norway the so-called mid-term negotiations between the two confederations, LO and NHO, broke down on the question of distributing higher wage increases to the lowest paid. After a four-day strike employers accepted prioritising the lowest paid, but the economic framework for the agreement remained unchanged, meaning that other groups of workers had to moderate wage expectations in the firm-level negotiations. In Denmark the renewed focus on low-wage workers was, surprisingly, led by the skilled metalworkers union, which has a key position in the manufacturing bargaining cartel, CO-industri, in negotiating the pattern-setting industrial agreement with the employer side. Accordingly, the metalworkers union played an important role in paving the way for extraordinary wage increases for the lowest paid. Put differently, the inflation crisis made it an obvious policy choice to give extra to the low paid and it turned out to be difficult for the employers to reject this demand from a highly coordinated group of unions.

Second, due to the rapid increase in inflation, the nominal wage increases were higher than seen for many years. It is hard to compare figures across the three countries, for a number of reasons. In Denmark and Norway the final wage increases in the private sector are negotiated largely at company level, so national-level agreements will at best only give indications of future wage levels. Local-level wage bargaining also plays a prominent role in Sweden, but there are fallback options for many workers if local bargaining parties do not settle. Local-level negotiations will have distributional effects, meaning that some groups of workers will receive higher wage increases than others. Ultimately, unions are concerned about real wages and because the level of inflation differs across the Scandinavian countries, real wage developments might differ as well. Remembering these reservations, we can nevertheless see a pattern of wage increases of 4–5 per cent in 2023 in the three countries.

Perspectives

The inflation and cost-of-living crisis tested the resilience of the Scandinavian political economies, known for their ability to respond in coordinated and egalitarian ways. Because of the different levels of political importance of energy prices and different macroeconomic problem loads in the three countries, governments in Norway and Sweden provided more relief to households and businesses than the one in Denmark and in a more universal manner. Clearly, the Danish economy was in a better state when the crisis hit and was careful not to further fuel inflation by propping up aggregate demand. The approaches of Denmark and, to a lesser extent, Norway and Sweden also show the willingness of Scandinavian governments to target support measures to particular groups when needed – the so-called ‘targeting within universalism’ approach. Of course, if targeting grows in terms of measures and fiscal size, it may crowd out the classic universalist welfare state of the Scandinavian countries over time.

With no national statutory minimum wage in any of the countries, it was mainly up to social partners to compensate for real income losses through collective bargaining. Previous inflation crises of the 1970s and 1980s (and the 1990s in Sweden), led to wage-price spirals, industrial conflict and eventually massive institutional overhaul of macroeconomic policies and wage-bargaining coordination to ensure fiscal balance and wage moderation. Such institutional responses did not materialise in the current inflation crisis, and the systems have been remarkably stable.

Nonetheless, the inflation crisis severely reduced the real wages of Scandinavian workers and made trade unions bolder in their demands. Only in Sweden did the memory of the wage-price spirals of the 1990s dampen wage demands, whereas Norwegian and Danish trade unions fought to restore real wages, especially for low-wage workers – even leading to industrial action in Norway. Thus in all three countries, unions focused on wage solidarity. The question, however, remains whether wage solidarity is back for good among the unions. For decades, Swedish and Norwegian LO unions have practised a low-wage policy, which seeks to afford a nominal amount (at a higher percentage increase) for low-wage workers, much to the chagrin of employers’ associations – and on occasion manufacturing unions (Alsos and Nergaard, 2021; Bender, 2024). For Denmark, this is new. The Scandinavian countries all base bargaining coordination on manufacturing setting the pattern for other bargaining areas. The pattern is a labour cost percentage increase and – as such – it locks in the wage structure.

In recent decades, however, local wage drift due to company-level bargaining has favoured skilled workers above the pattern set in national bargaining, meaning that low-wage workers lag further behind. Hence Swedish and Norwegian unions’ strategy of giving a nominal amount to low-wage workers. In Denmark, unions centralised wage increases in 2023 and also threatened employers that local bargaining must take place for all workers – if not, wage setting has to be centralised again. These solidaristic bargaining dynamics and re-centralisation efforts (in Denmark) show that trade unions are willing and able to challenge the institutional status quo if wage developments lag behind the general economy. Hypothetically, the revitalisation of wage solidarity may spur calls for re-centralisations of wage setting, which would signify an institutional departure from existing industrial relations reform trajectories. However, this depends on how wages keep up with inflation and productivity in the years to come. If wage developments do not recover satisfactorily in coming years, re-centralisation may very well be the preferred strategy of many union leaders eager to show their value to the rank-and-file.

Footnotes

Funding

Erik Bengtsson’s work on the article was supported by the Riksbankens Jubileumsfond [grant number M19-0231]. The other authors received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.